Embed Size (px)

Citation preview

Chicago Tax Club

Chicago Tax Club ~ April ConferenceMcDonald Corporation Hamburger University

Whistleblower and Class Action Lawsuits in Sales Tax:Damned if You Do, Damned if You Don’t

Panel:

David C. Blum, Levenfeld PearlsteinTed Bots, Baker & McKenzieDavid Hughes, Horwood Marcus & Berk

Moderator:Larry Ewing, CDH

April 13th, 2015

Chicago Tax Club

• Qui Tam Actions/State False Claims Acts

• Class Action Exposure for Over-Collection

• Efforts to Legislatively Confine Vendor Exposures

• The ABA Model Act

• MTC Uniformity Project

• Consumer Fraud Damages for Over-Collecting

Overview

Chicago Tax Club

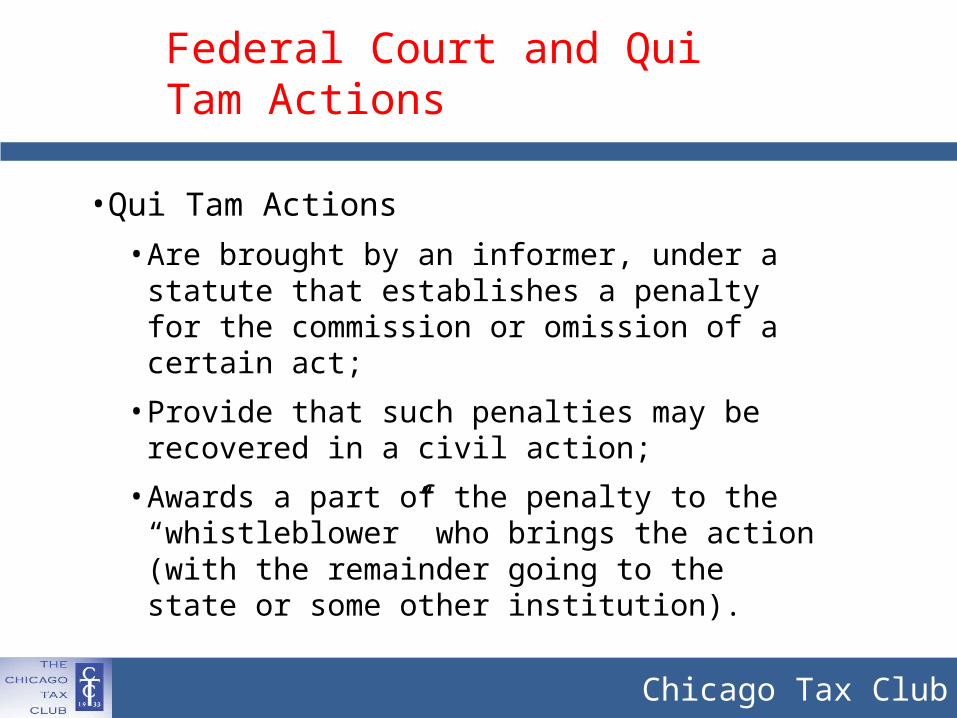

• Qui Tam Actions

• Are brought by an informer, under a statute that establishes a penalty for the commission or omission of a certain act;

• Provide that such penalties may be recovered in a civil action;

• Awards a part of the penalty to the “whistleblower” who brings the action (with the remainder going to the state or some other institution).

Federal Court and Qui Tam Actions

Chicago Tax Club

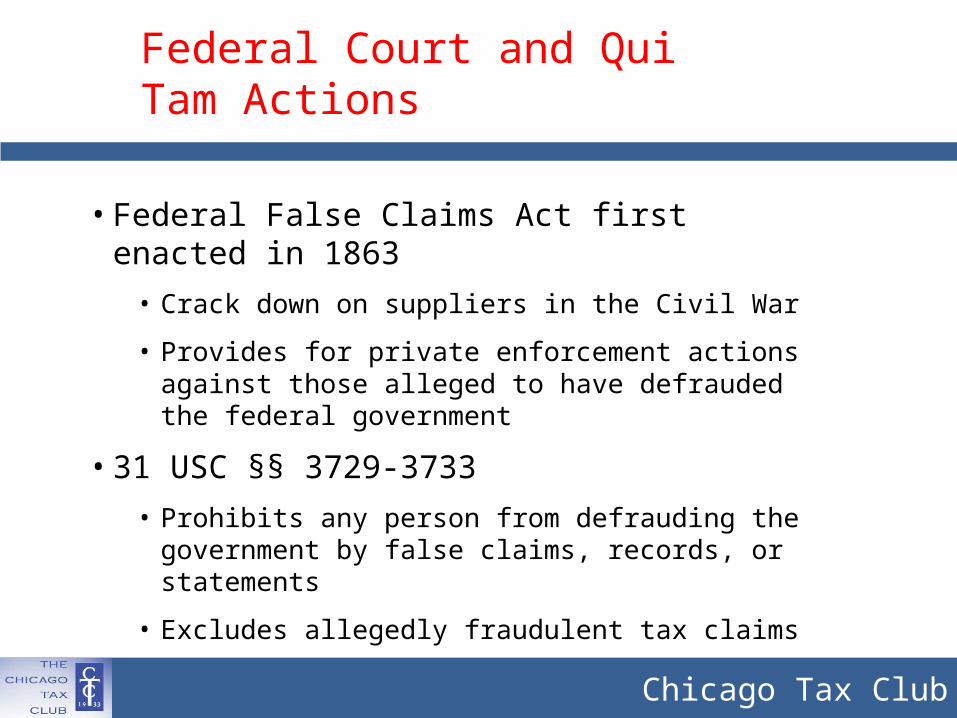

• Federal False Claims Act first enacted in 1863

• Crack down on suppliers in the Civil War

• Provides for private enforcement actions against those alleged to have defrauded the federal government

• 31 USC §§ 3729-3733

• Prohibits any person from defrauding the government by false claims, records, or statements

• Excludes allegedly fraudulent tax claims

Federal Court and Qui Tam Actions

Chicago Tax Club

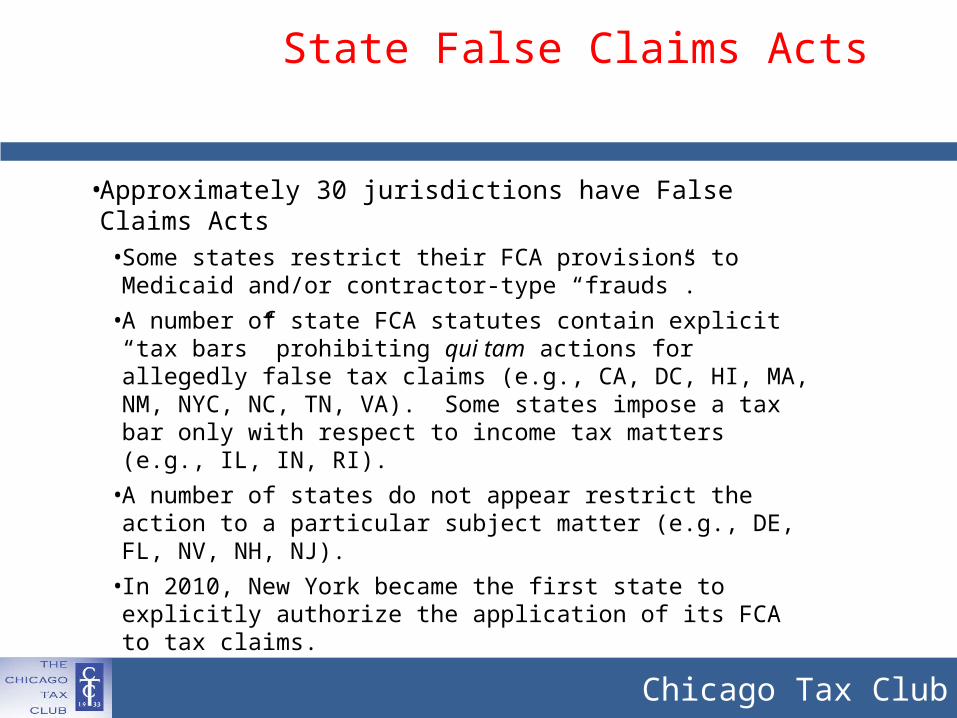

• Approximately 30 jurisdictions have False Claims Acts

• Some states restrict their FCA provisions to Medicaid and/or contractor-type “frauds”.

• A number of state FCA statutes contain explicit “tax bars” prohibiting qui tam actions for allegedly false tax claims (e.g., CA, DC, HI, MA, NM, NYC, NC, TN, VA). Some states impose a tax bar only with respect to income tax matters (e.g., IL, IN, RI).

• A number of states do not appear restrict the action to a particular subject matter (e.g., DE, FL, NV, NH, NJ).

• In 2010, New York became the first state to explicitly authorize the application of its FCA to tax claims.

State False Claims Acts

Chicago Tax Club

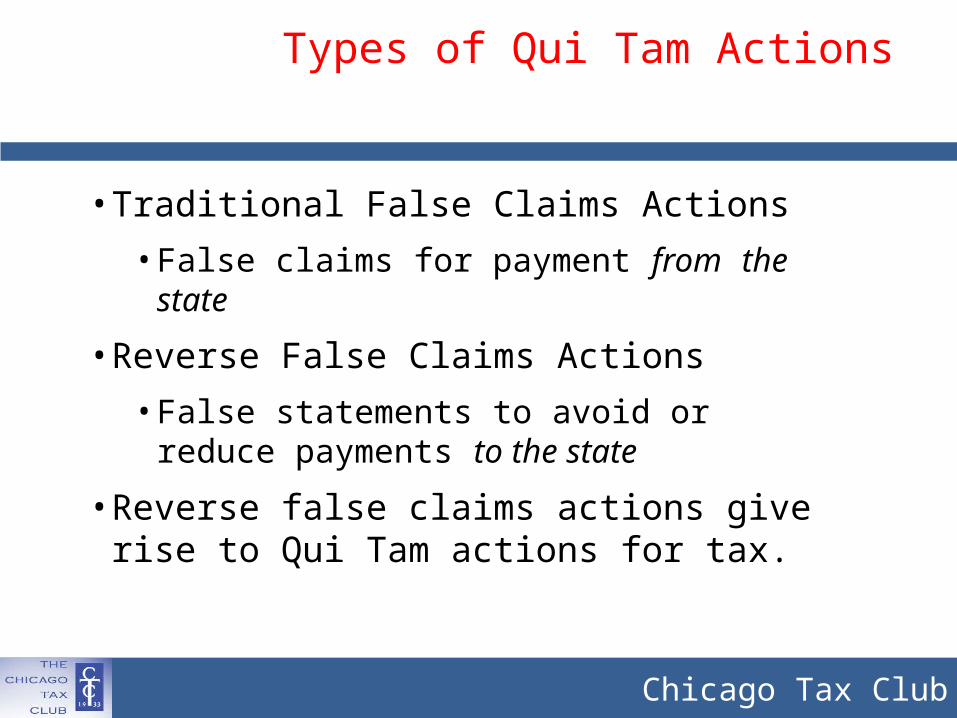

• Traditional False Claims Actions

• False claims for payment from the state

• Reverse False Claims Actions

• False statements to avoid or reduce payments to the state

• Reverse false claims actions give rise to Qui Tam actions for tax.

Types of Qui Tam Actions

Chicago Tax Club

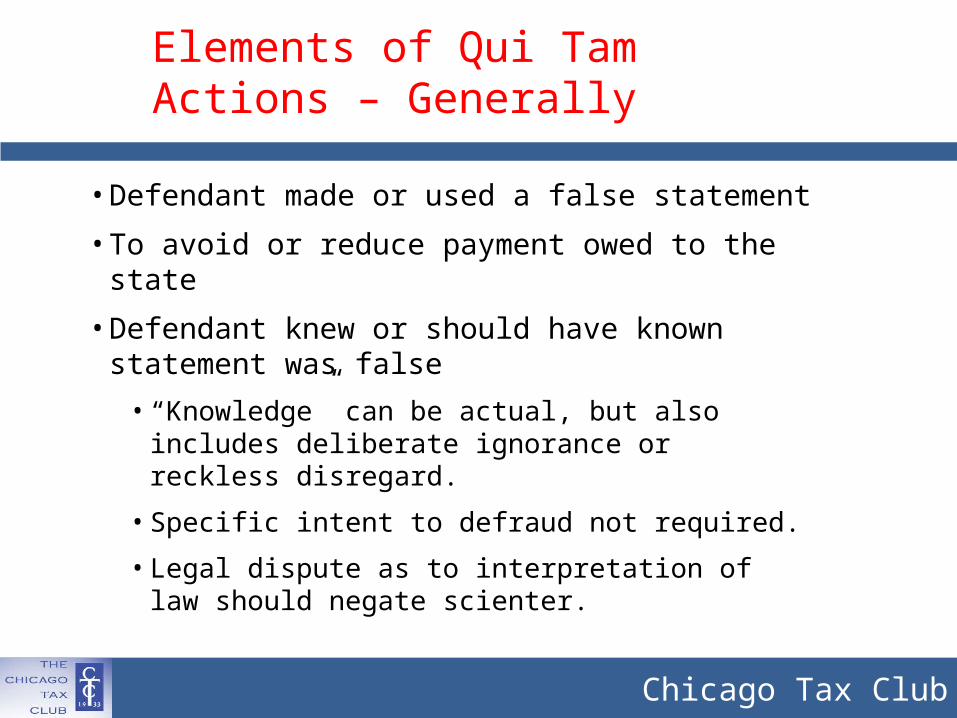

• Defendant made or used a false statement

• To avoid or reduce payment owed to the state

• Defendant knew or should have known statement was false

• “Knowledge” can be actual, but also includes deliberate ignorance or reckless disregard.

• Specific intent to defraud not required.

• Legal dispute as to interpretation of law should negate scienter.

Elements of Qui Tam Actions – Generally

Chicago Tax Club

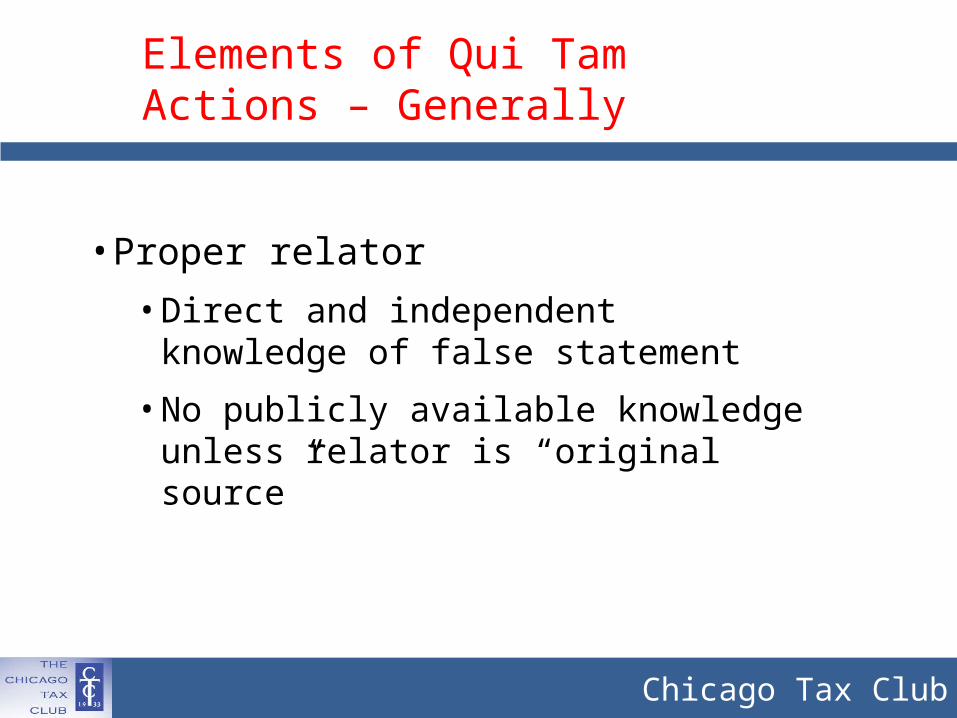

• Proper relator

• Direct and independent knowledge of false statement

• No publicly available knowledge unless relator is “original source”

Elements of Qui Tam Actions – Generally

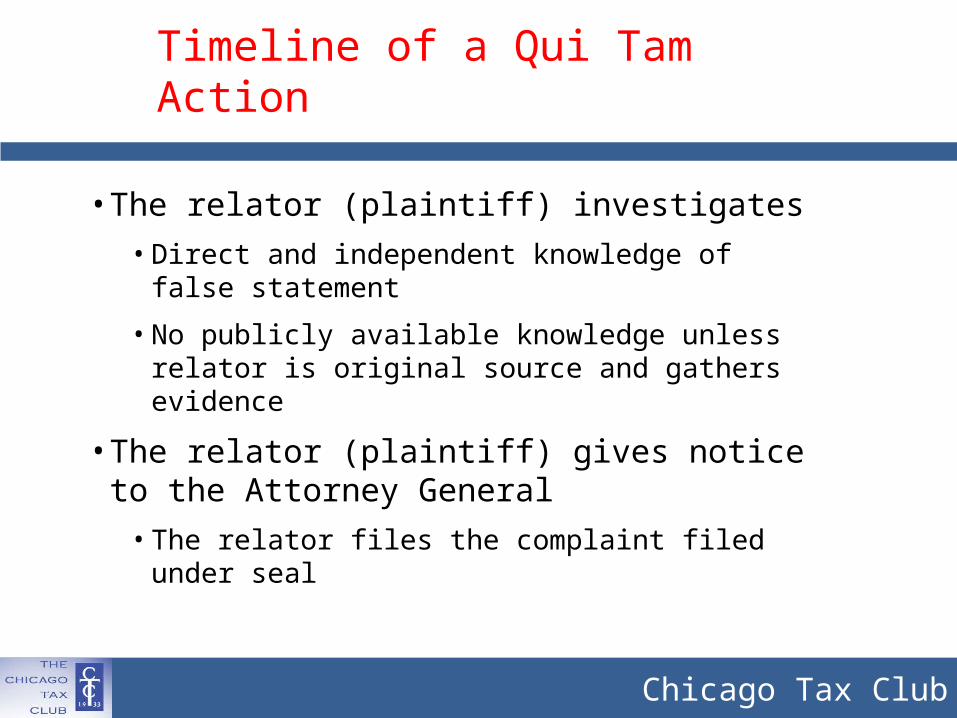

Chicago Tax Club

• The relator (plaintiff) investigates• Direct and independent knowledge of false

statement

• No publicly available knowledge unless relator is original source and gathers evidence

• The relator (plaintiff) gives notice to the Attorney General

• The relator files the complaint filed under seal

Timeline of a Qui Tam Action

Chicago Tax Club

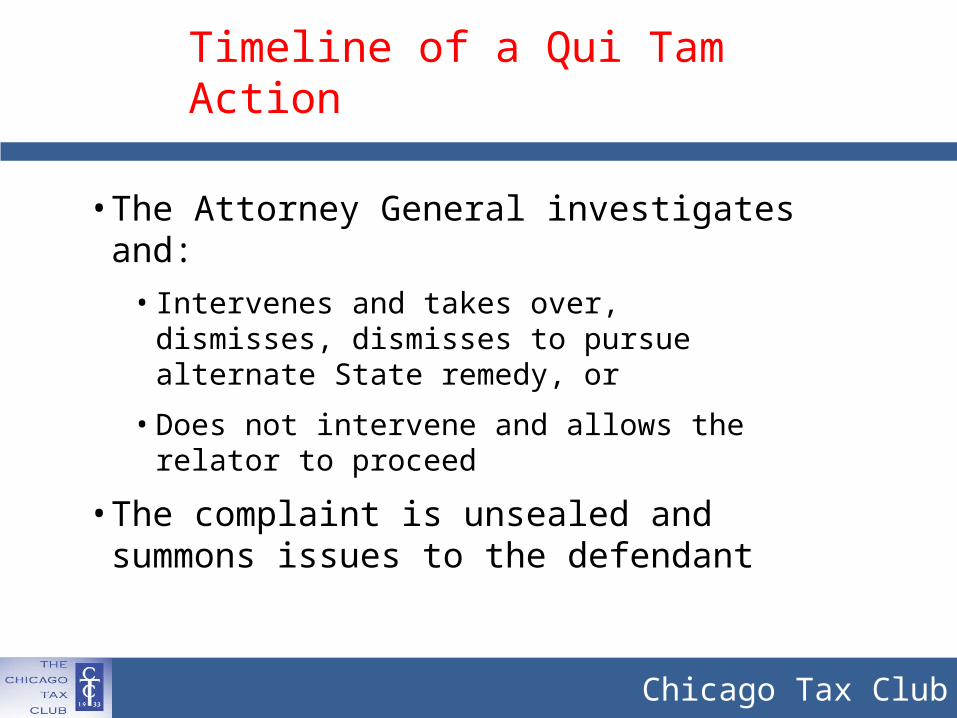

• The Attorney General investigates and:

• Intervenes and takes over, dismisses, dismisses to pursue alternate State remedy, or

• Does not intervene and allows the relator to proceed

• The complaint is unsealed and summons issues to the defendant

Timeline of a Qui Tam Action

Chicago Tax Club

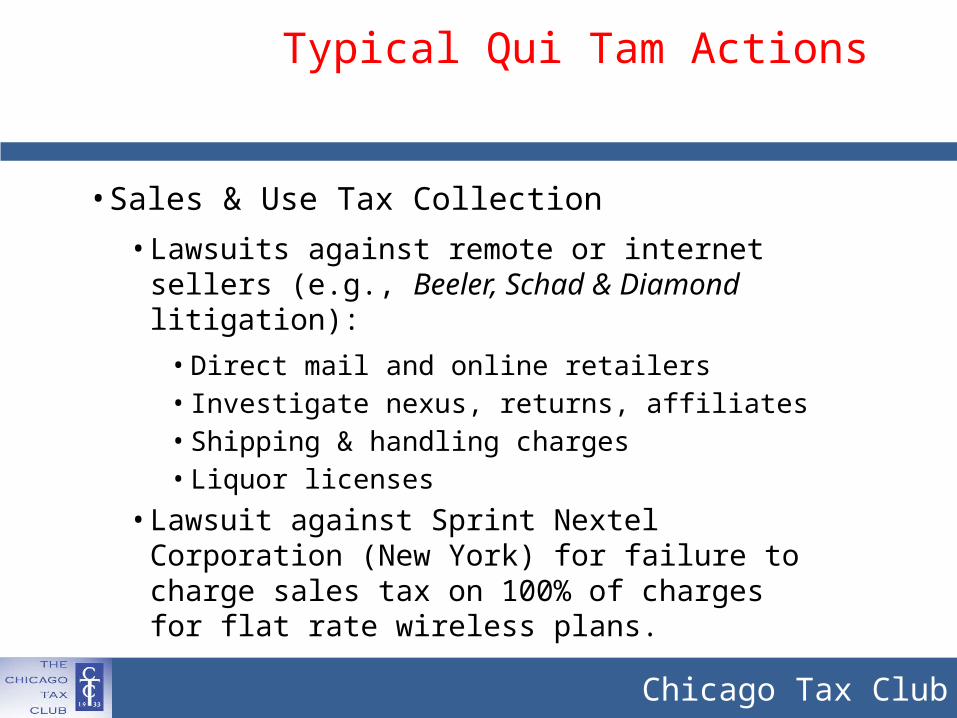

• Sales & Use Tax Collection

• Lawsuits against remote or internet sellers (e.g., Beeler, Schad & Diamond litigation):

• Direct mail and online retailers• Investigate nexus, returns, affiliates• Shipping & handling charges• Liquor licenses

• Lawsuit against Sprint Nextel Corporation (New York) for failure to charge sales tax on 100% of charges for flat rate wireless plans.

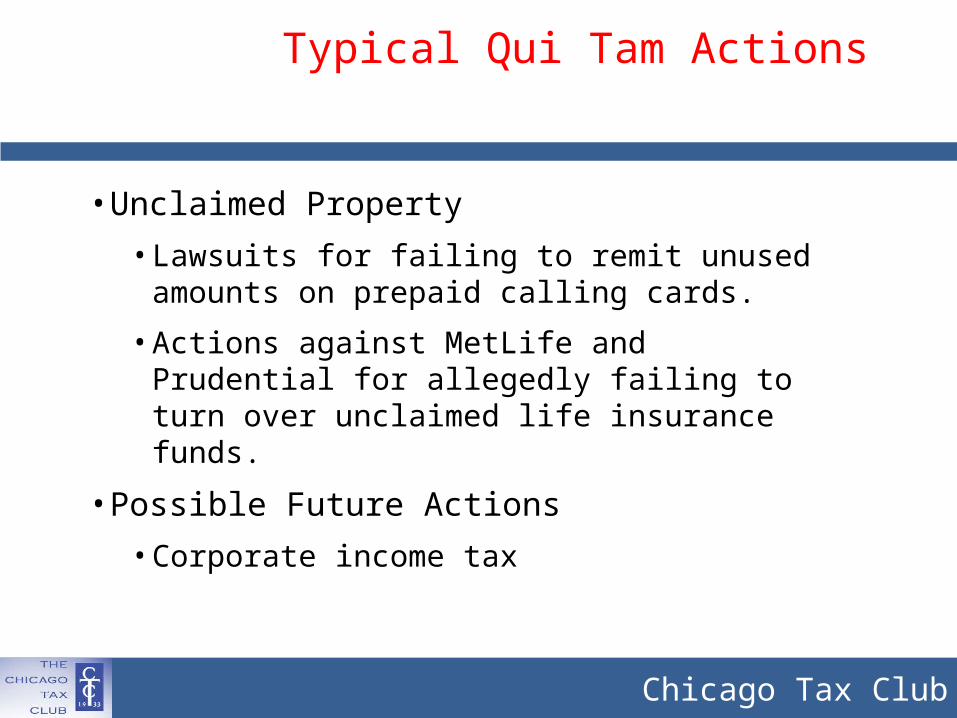

Typical Qui Tam Actions

Chicago Tax Club

• Unclaimed Property

• Lawsuits for failing to remit unused amounts on prepaid calling cards.

• Actions against MetLife and Prudential for allegedly failing to turn over unclaimed life insurance funds.

• Possible Future Actions

• Corporate income tax

Typical Qui Tam Actions

Chicago Tax Club

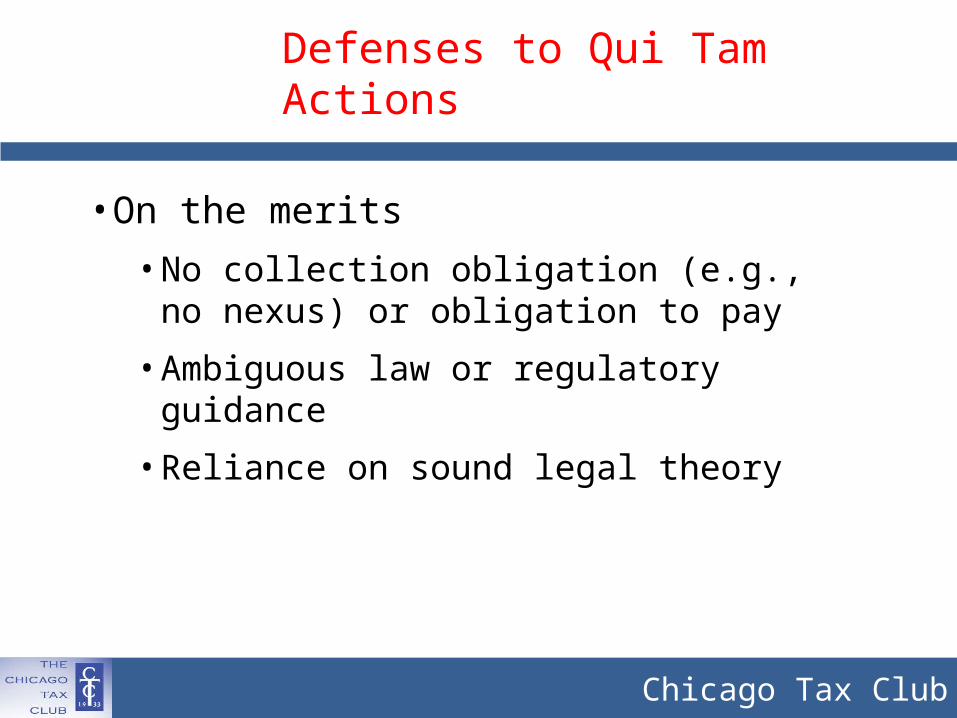

• On the merits

• No collection obligation (e.g., no nexus) or obligation to pay

• Ambiguous law or regulatory guidance

• Reliance on sound legal theory

Defenses to Qui Tam Actions

Chicago Tax Club

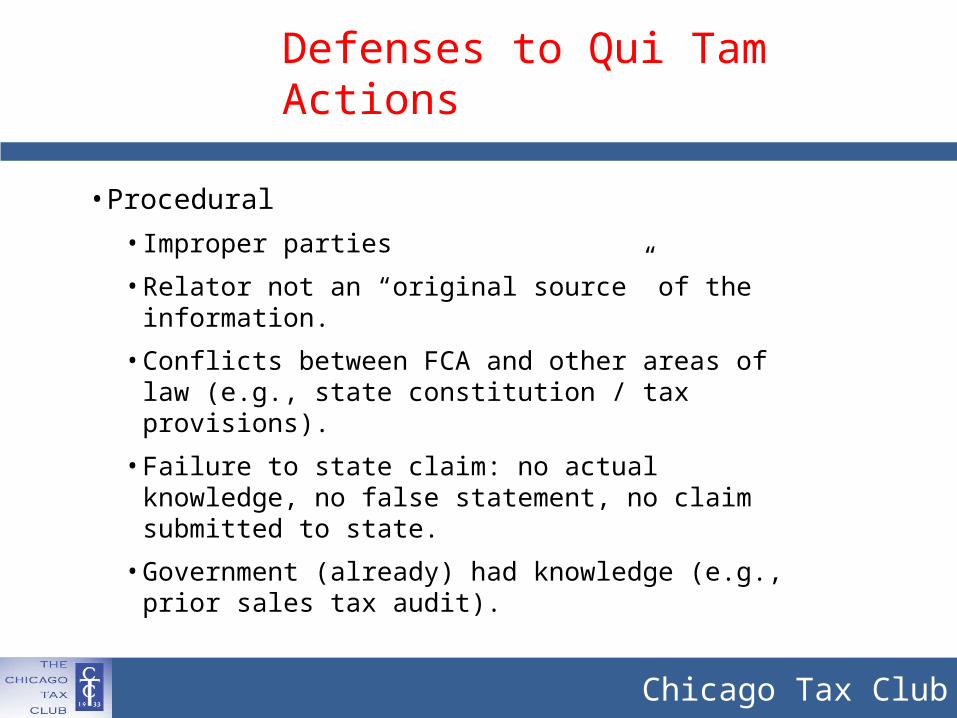

• Procedural

• Improper parties

• Relator not an “original source” of the information.

• Conflicts between FCA and other areas of law (e.g., state constitution / tax provisions).

• Failure to state claim: no actual knowledge, no false statement, no claim submitted to state.

• Government (already) had knowledge (e.g., prior sales tax audit).

Defenses to Qui Tam Actions

Chicago Tax Club

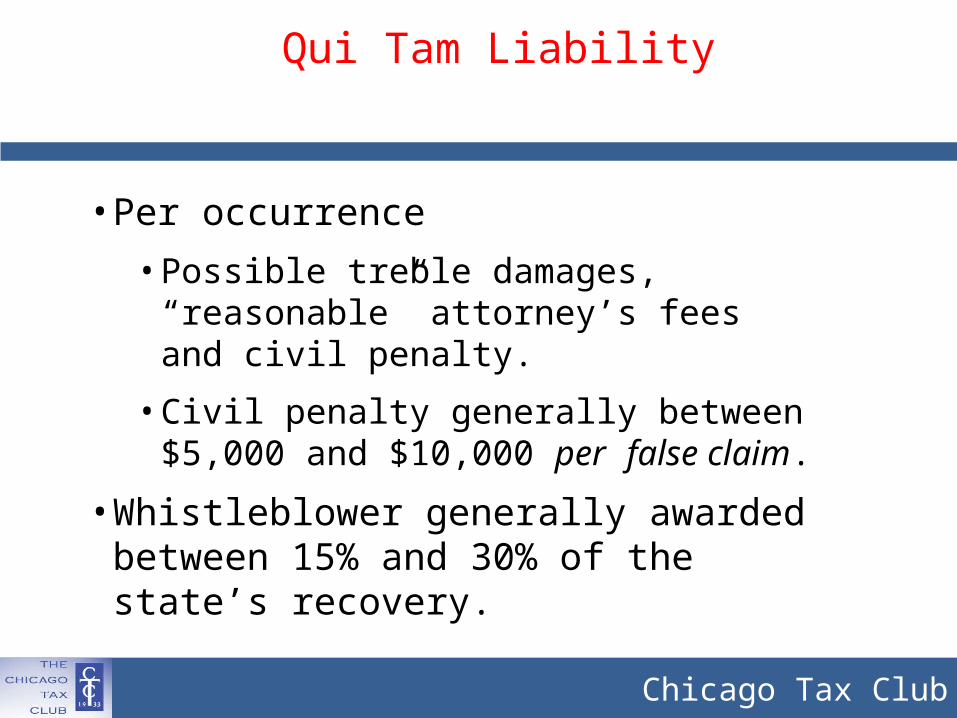

• Per occurrence

• Possible treble damages, “reasonable” attorney’s fees and civil penalty.

• Civil penalty generally between $5,000 and $10,000 per false claim.

• Whistleblower generally awarded between 15% and 30% of the state’s recovery.

Qui Tam Liability

Chicago Tax Club

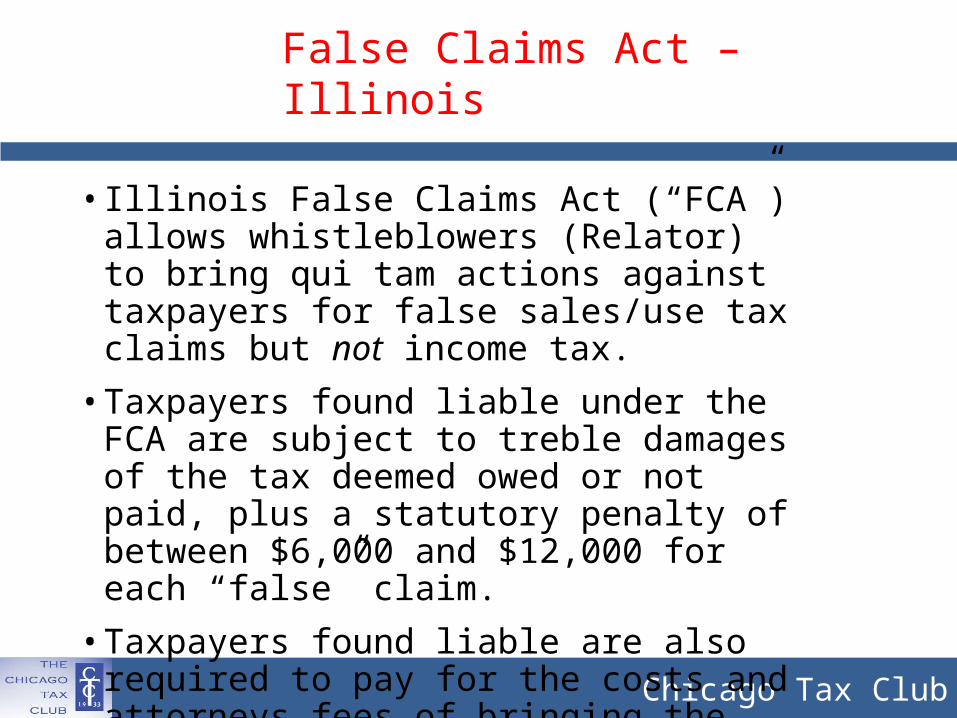

• Illinois False Claims Act (“FCA”) allows whistleblowers (Relator) to bring qui tam actions against taxpayers for false sales/use tax claims but not income tax.

• Taxpayers found liable under the FCA are subject to treble damages of the tax deemed owed or not paid, plus a statutory penalty of between $6,000 and $12,000 for each “false” claim.

• Taxpayers found liable are also required to pay for the costs and attorneys fees of bringing the action.

False Claims Act – Illinois

Chicago Tax Club

• Whistleblower Rewards

• Up to 30 percent of the recovered proceeds.

• A whistleblower who planned or initiated the false claim may even recover an award provided that the person is not convicted of a crime for the false act.

False Claims Act – Illinois

Chicago Tax Club

• Whistleblower Protections• A strengthened immunity provision and added

protections from retaliation encourage current and former employees, contractors, or agents to become whistleblowers.

• Employees, contractors, and agents are protected from retaliation for transmitting any information for the purpose of investigating, filing, or potentially filing an action under the FCA, even if the transmission “violate[s] a contract, employment term, or duty owed to the employer or contractor.”

False Claims Act – Illinois

Chicago Tax Club

• Elements Needed to Establish Liability

• Must show that the taxpayer “knowingly”:- Presented or caused to be presented, a

false or fraudulent claim for payment or approval;

- Made, used, or caused to be made or used, a false record or statement material to a false or fraudulent claim;

- Made, used, or caused to be made or used, a false record or statement material to an obligation to pay or transmit money or property to the state or a local government.

False Claims Act – Illinois

Chicago Tax Club

• “Knowingly”

• Means something more than actual knowledge.

• Also includes acting in deliberate ignorance or reckless disregard of the truth or falsity of information.

False Claims Act – Illinois

Chicago Tax Club

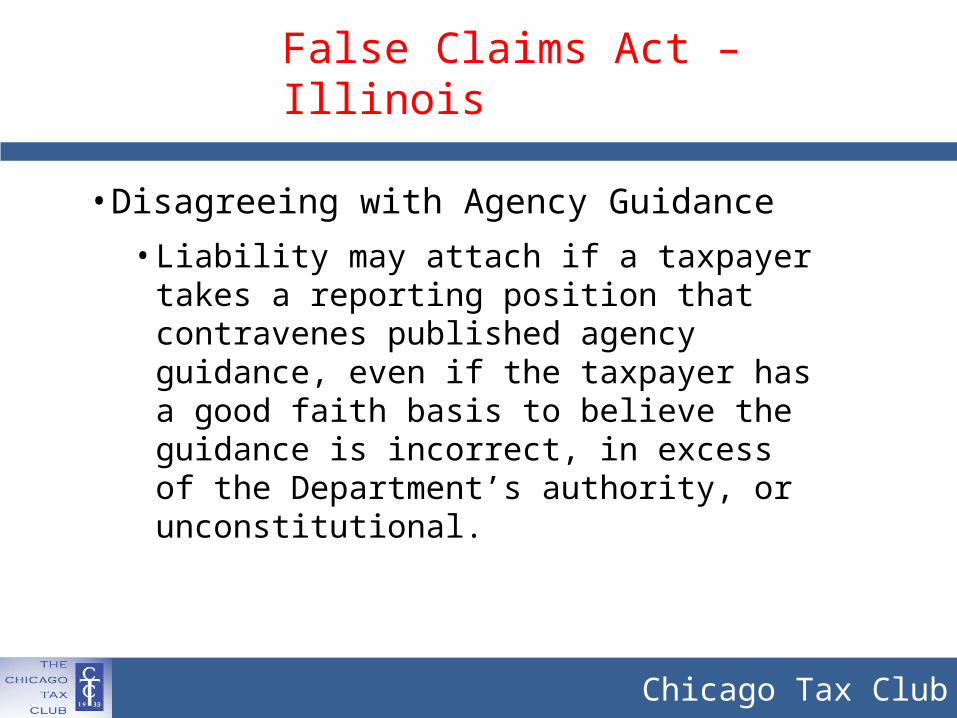

• Disagreeing with Agency Guidance

• Liability may attach if a taxpayer takes a reporting position that contravenes published agency guidance, even if the taxpayer has a good faith basis to believe the guidance is incorrect, in excess of the Department’s authority, or unconstitutional.

False Claims Act – Illinois

Chicago Tax Club

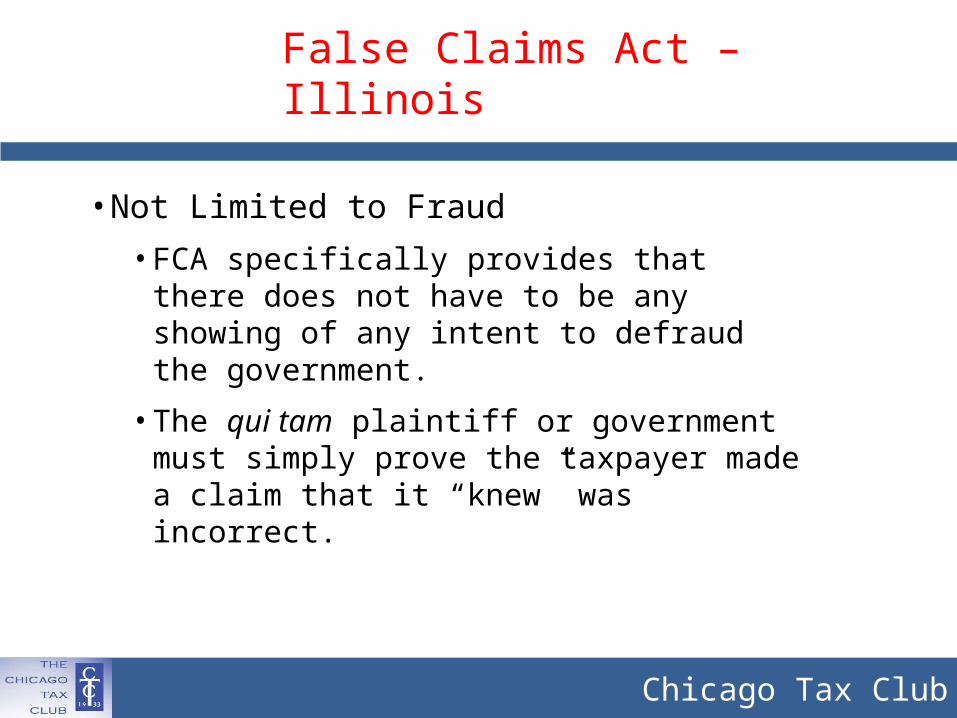

• Not Limited to Fraud

• FCA specifically provides that there does not have to be any showing of any intent to defraud the government.

• The qui tam plaintiff or government must simply prove the taxpayer made a claim that it “knew” was incorrect.

False Claims Act – Illinois

Chicago Tax Club

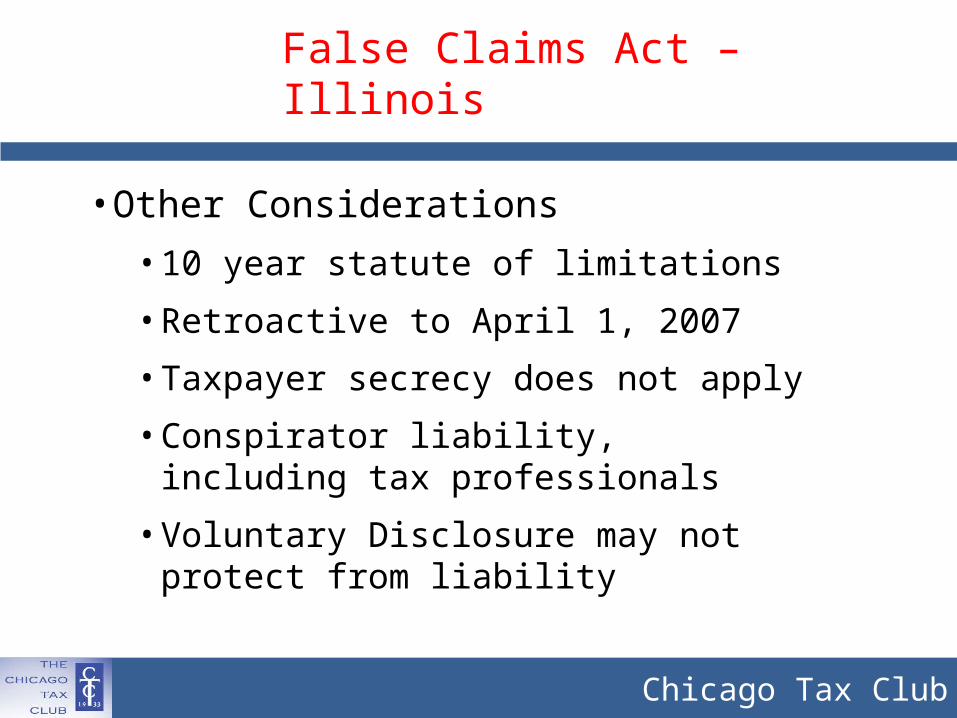

• Other Considerations

• 10 year statute of limitations

• Retroactive to April 1, 2007

• Taxpayer secrecy does not apply

• Conspirator liability, including tax professionals

• Voluntary Disclosure may not protect from liability

False Claims Act – Illinois

Chicago Tax Club

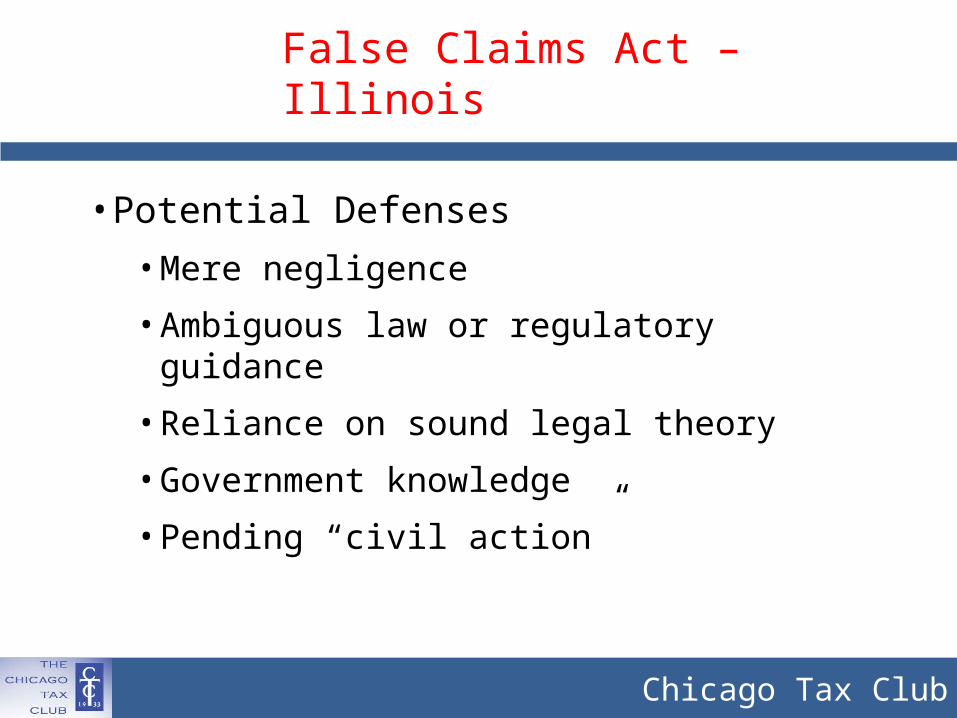

• Potential Defenses

• Mere negligence

• Ambiguous law or regulatory guidance

• Reliance on sound legal theory

• Government knowledge

• Pending “civil action”

False Claims Act – Illinois

Chicago Tax Club

• Potential Defenses

• Public disclosure

• Who’s an appropriate whistleblower?

• Voluntary disclosure?

• State and Federal Constitutional violations

False Claims Act – Illinois

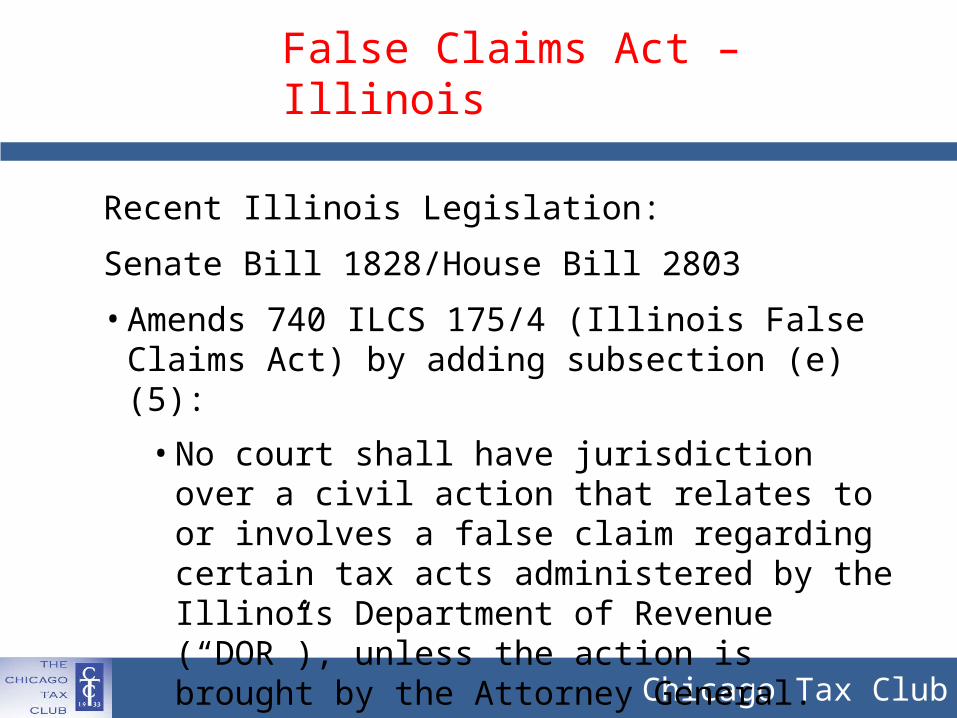

Chicago Tax Club

Recent Illinois Legislation:

Senate Bill 1828/House Bill 2803

• Amends 740 ILCS 175/4 (Illinois False Claims Act) by adding subsection (e)(5):

• No court shall have jurisdiction over a civil action that relates to or involves a false claim regarding certain tax acts administered by the Illinois Department of Revenue (“DOR”), unless the action is brought by the Attorney General.

False Claims Act – Illinois

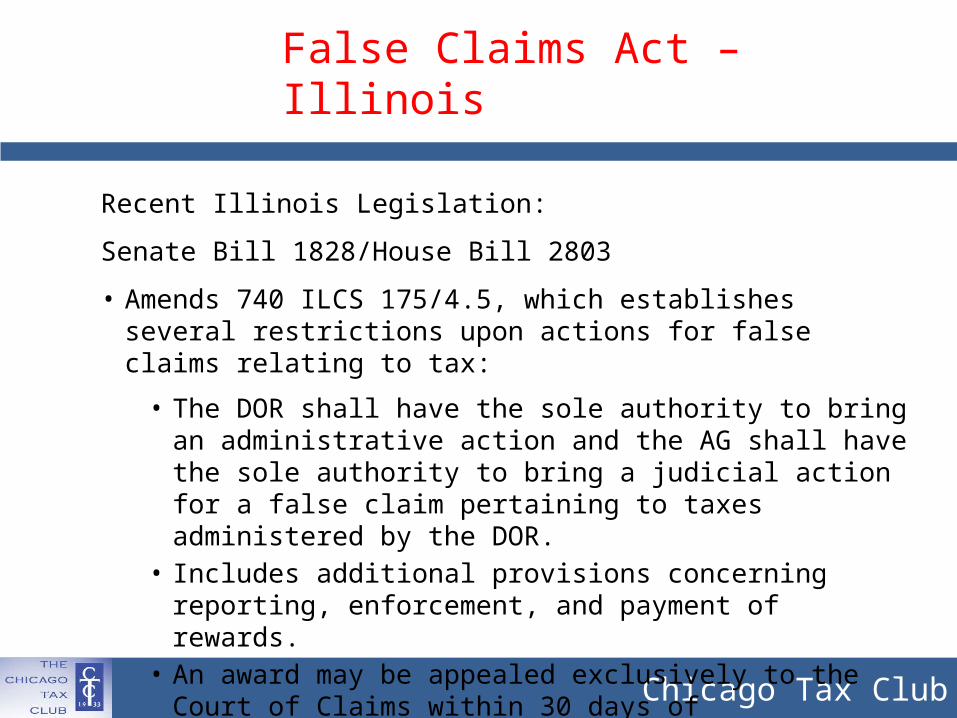

Chicago Tax Club

Recent Illinois Legislation:

Senate Bill 1828/House Bill 2803

• Amends 740 ILCS 175/4.5, which establishes several restrictions upon actions for false claims relating to tax:

• The DOR shall have the sole authority to bring an administrative action and the AG shall have the sole authority to bring a judicial action for a false claim pertaining to taxes administered by the DOR.

• Includes additional provisions concerning reporting, enforcement, and payment of rewards.

• An award may be appealed exclusively to the Court of Claims within 30 days of determination.

False Claims Act – Illinois

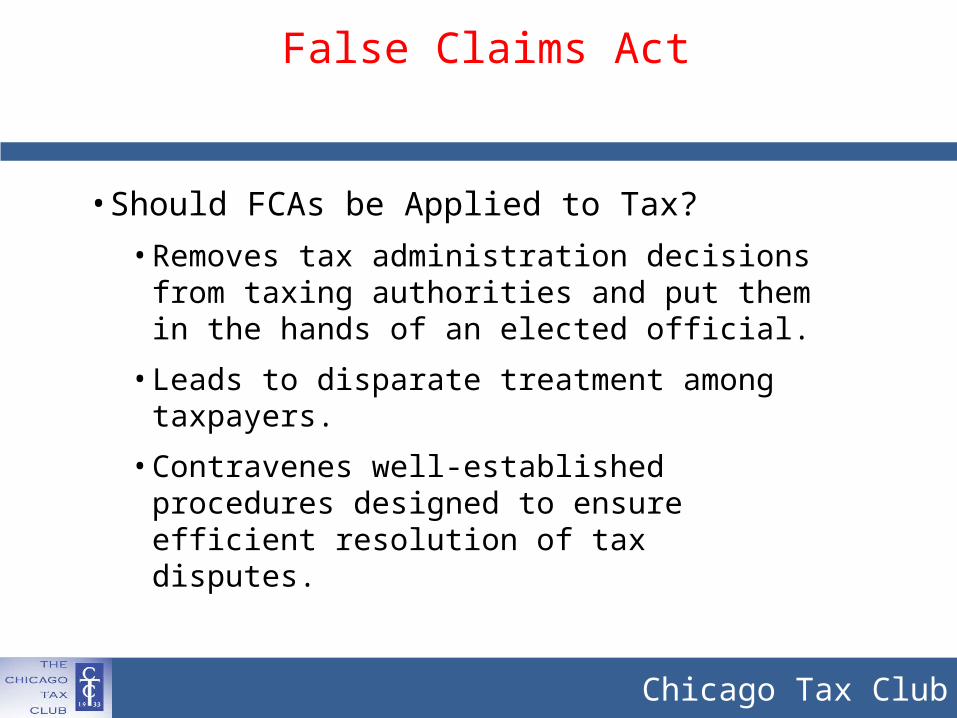

Chicago Tax Club

• Should FCAs be Applied to Tax?

• Removes tax administration decisions from taxing authorities and put them in the hands of an elected official.

• Leads to disparate treatment among taxpayers.

• Contravenes well-established procedures designed to ensure efficient resolution of tax disputes.

False Claims Act

Chicago Tax Club

• Should FCAs be Applied to Tax? (cont.)

• Upends protections for taxpayer rights, including historical right to privacy in tax matters.

• May discourage use of voluntary disclosure programs.

• Incentivizes collection of transaction taxes, which may expose taxpayers to class-action consumer fraud lawsuits.

False Claims Act

Chicago Tax Club

• Customer liability actions against vendors:

• Applications of coupons

• Jurisdiction rate assignments

• Sourcing conventions

• Product/Service taxability

• Examples

• Chang Wong v. Whole Foods No. 1:15 - CV-00898 (2014) (tax on in-store coupons)

• Schojan v. Papa Johns No. 14-CA-003491 (2014) and Tucker v. Papa Johns No. 3:14-CV-00618 (2014) (tax on delivery charges)

• Long v. Dell, C.A. No. 03-2636 (2012) (tax on service contracts and shipping charges)

• In re AT&T Mobility Wireless Data Servs. Sales Tax Litig., 789 F. Supp. 2d 935 (N.D. Ill. 2011) (internet access)

Class Action Law Suits

Chicago Tax Club

• Vendors often can defend against the actions because they used due diligence and remitted funds to the jurisdiction -- but not without costs.

• State governments can also face class action lawsuits

Class Action Law Suits

Chicago Tax Club

Kean v. Walmart

• Kean bought a trampoline on walmart.com for $23.33 plus $7.97 shipping and $2.74 sales tax (Sept. 2006).

• Alleged sales tax should have only been imposed on trampoline and not shipping and handling.

• One month later (October 2006), filed a multistate class action in Cook County Circuit Court alleging:

• consumer fraud and deceptive business practices;

• unjust enrichment; and

• Injunctive relief – creation of a “class protest fund”

• Nov 2006 filed a TRO and preliminary injunctive relief

Chicago Tax Club

Kean v. Walmart

• From Walmart’s perspective, they collected and remitted the tax, which is now held by the state.

• So if money is owed to plaintiffs, the state should refund it….

• IDOR then intervene as party defendants and among other things, filed a motion to dismiss plaintiffs’ case.

• Nov 2009, Illinois Supreme Court ruled that Walmart correctly charged and collected sales tax on shipping charges -- no refund.

Take away:

One customer, with no sales tax experience or inside knowledge, dragged Walmart through the courts for years, incurring sizable legal bills and no good way out. Plaintiff deprived taxpayer and the state of the efficient administration of an essential gov’t function.

Chicago Tax Club34

Recent Illinois Cases

• Wong v. Target (Illinois Federal Court) – Coupon Case

• Bought an item for $10, used a $1 coupon, alleged he was overcharged sales tax by applying tax on $10, not $9.

• Causes of Action: Consumer Fraud (unfair and deceptive acts and practices), Common Law Fraud, and “Money Had and Received” (i.e., unjust enrichment)

• Damages Sought: (1) Compensatory damages ($0.02 in his case); (2) Punitive damages of “at least equal to 1% of annual revenue of each of defendant’s Illinois stores during each year the violations occurred;” (3) attorney’s fees, and (4) such other relief court deems

• Wong v. Whole Foods (Illinois Federal Court)

• largely identical to the Target case

Chicago Tax Club35

Recent Cases

• Papa John’s International (Illinois & Florida)

• “Illegally” collected sales tax on delivery fees

• Consumer fraud, deceptive trade practices, etc

• Florida case recently settled; Illinois still pending

• BJ’s Wholesale Club (Florida & Pennsylvania)

• “illegally” overcharged and kept sales tax on items purchased through discounts, coupons and other price reductions offers (e.g., rebate coupon “dealer discount”)

• “prospective class consists of many thousands, If not tens of thousands, of BJ’s members who were improperly charged under the guise of BJ’s collection of sales tax”

Chicago Tax Club36

Recent Cases

• Walmart & Sam’s Club

• Pennsylvania

• Named plaintiff bought two cans of shaving gel with a “buy one get one free” coupon. Total purchase $2.97.

• Alleges Walmart overcharges sales tax in PA stores and Internet sales and has “misappropriates millions of dollars…”

• Ohio

• Retailer shortchanged customers who returned items to different stores by applying lower sales tax rates

• Breach of contract – violates terms of sale by refunding less than the original purchase price

• Walmart seeks to remove to State Tax Commission from federal court since they are exclusive arbiter of state tax refund claims.

Chicago Tax Club

• Class actions can be brought against the government jurisdiction –

• Arizona Department of Revenue v. Bernard J. Dougherty, 29 P.3d 862: class action lawsuits against the State were permitted in Tax Court.

• Granados v. County of Los Angeles, CA Court of Appeal, Second District, No. B200812 (March 28, 2012): a taxpayer can file a class action claim for refund of CA local telephone users taxes paid. Before filing the claim the plaintiff must first file a claim that contains the information required by the Government.

Tax Collection Liability Litigation

Chicago Tax Club

• Customer Remedy Procedures – § 325

• First course of remedy

• Reasonable business practice to use state provided data.

• Taxability Matrix – § 328

• Definitions and sourcing rules -- §§ 314, 315 & Library of Definitions

• Database requirements – § 307

• Local rate and boundary changes – § 302

Streamlined Agreement Provisions

Chicago Tax Club

• Prepared by the Government Submissions and Legislative Whitepapers Subcommittee with the State and Local Tax Committee

• Paper balanced conflicting interests of sellers, purchasers and state and local governments.

• Subcommittee drafted a model that would not violate SSUTA but would provide an exclusive remedy for a purchaser to obtain a refund of over-collected tax.

American Bar Association Model Act

Chicago Tax Club

• The paper outlines 15 Governing principles. Some highlights include:

• Principle 6 – Sellers are, in collecting tax from purchasers and paying it over to the taxing jurisdiction, acting merely as agents for the taxing jurisdiction. Accordingly, sellers should not be subject to claims arising from or in any way related to an overpayment by purchasers or liability to such purchasers or anyone else other than a taxing jurisdiction revenue department, regardless of the nature of the claim or cause of action asserted, unless the party asserting the liability demonstrates that in collecting the tax the seller acted with willful intent to defraud the purchaser.

American Bar Association Model Act

Chicago Tax Club

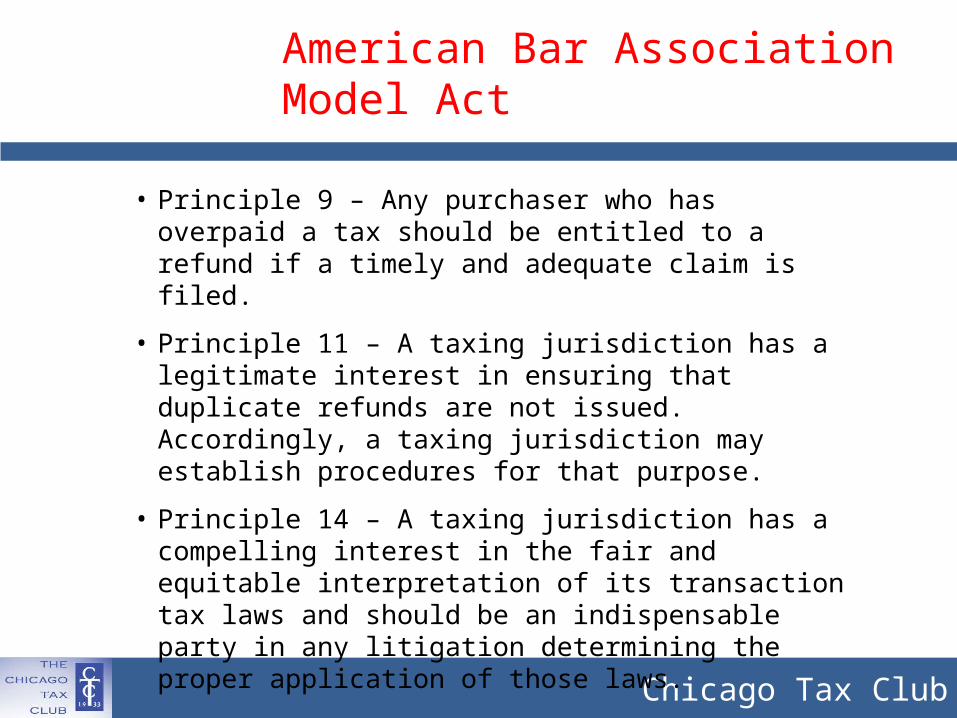

• Principle 9 – Any purchaser who has overpaid a tax should be entitled to a refund if a timely and adequate claim is filed.

• Principle 11 – A taxing jurisdiction has a legitimate interest in ensuring that duplicate refunds are not issued. Accordingly, a taxing jurisdiction may establish procedures for that purpose.

• Principle 14 – A taxing jurisdiction has a compelling interest in the fair and equitable interpretation of its transaction tax laws and should be an indispensable party in any litigation determining the proper application of those laws.

American Bar Association Model Act

Chicago Tax Club

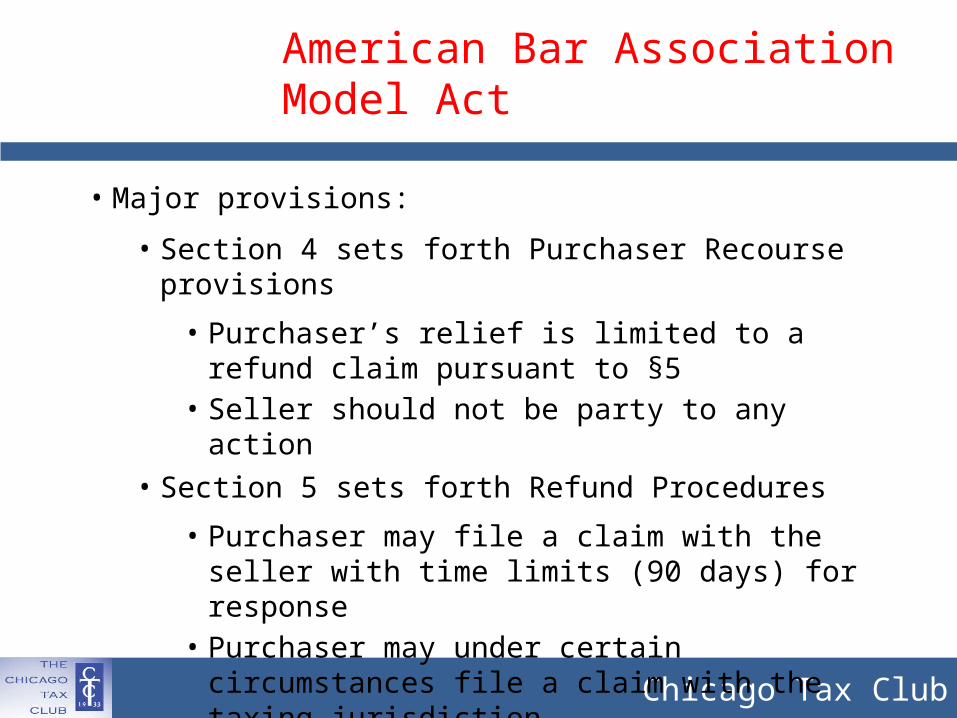

• Major provisions:

• Section 4 sets forth Purchaser Recourse provisions

• Purchaser’s relief is limited to a refund claim pursuant to §5

• Seller should not be party to any action• Section 5 sets forth Refund Procedures

• Purchaser may file a claim with the seller with time limits (90 days) for response

• Purchaser may under certain circumstances file a claim with the taxing jurisdiction

American Bar Association Model Act

Chicago Tax Club

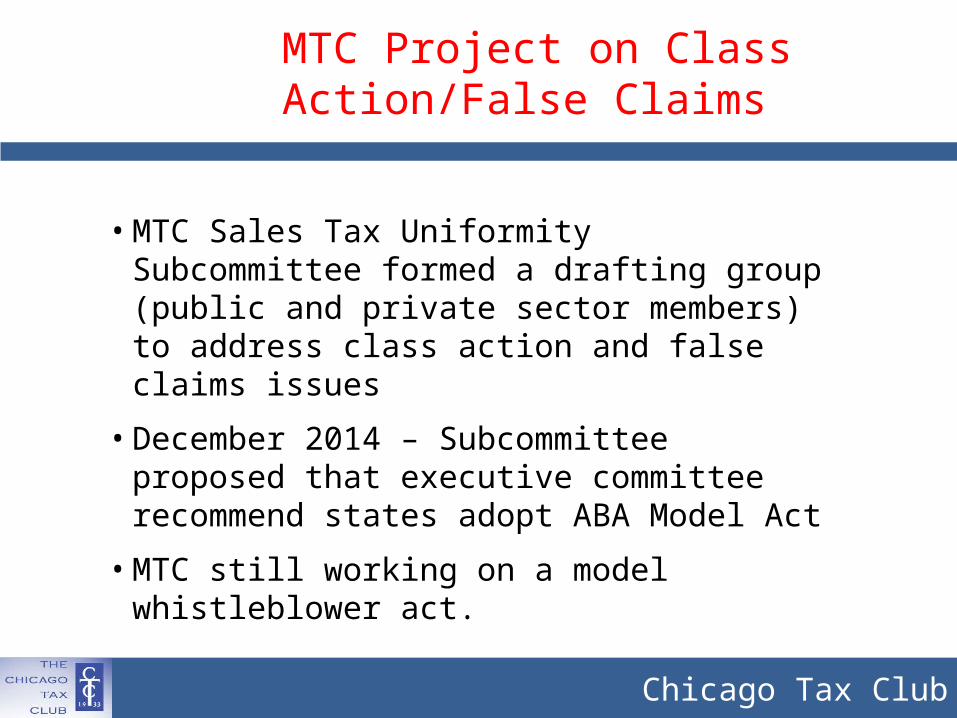

• MTC Sales Tax Uniformity Subcommittee formed a drafting group (public and private sector members) to address class action and false claims issues

• December 2014 – Subcommittee proposed that executive committee recommend states adopt ABA Model Act

• MTC still working on a model whistleblower act.

MTC Project on Class Action/False Claims

Chicago Tax Club

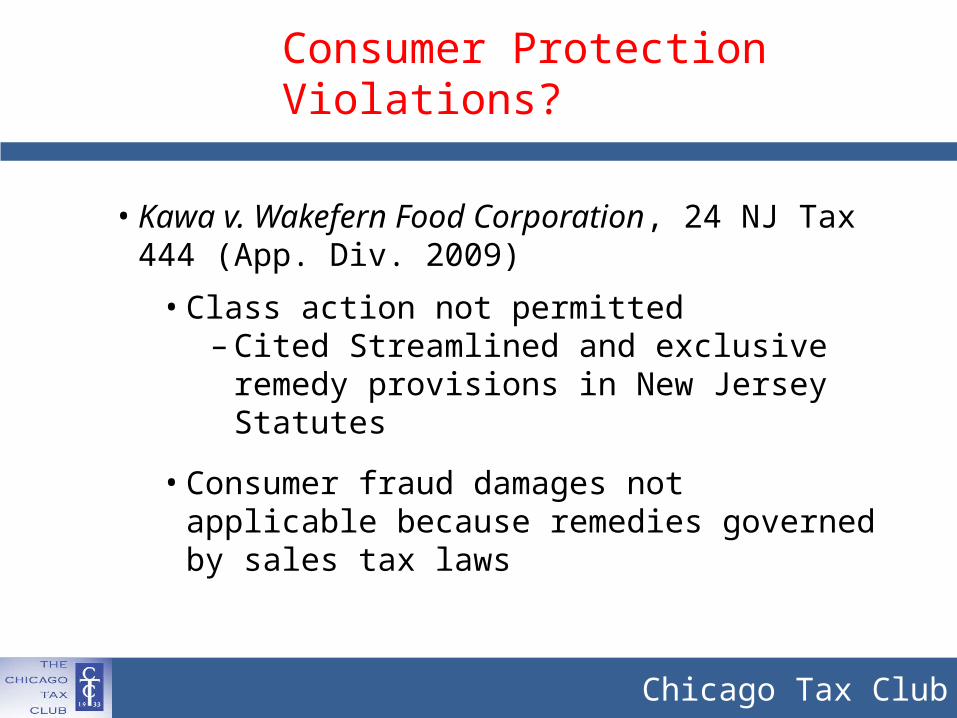

• Kawa v. Wakefern Food Corporation, 24 NJ Tax 444 (App. Div. 2009)

• Class action not permitted – Cited Streamlined and exclusive

remedy provisions in New Jersey Statutes

• Consumer fraud damages not applicable because remedies governed by sales tax laws

Consumer Protection Violations?

Chicago Tax Club

• Nava v. Sears, Roebuck and Co., Illinois Appellate Court, First District, No. 1-12-2063 (July 29, 2013)

• Tax on coupon discounts for converter boxes erroneously collected

• Customer brought suit under consumer protection act

• Also sought certification of a class action• Trial court dismissed the case, but Appellate

Court reinstated and remanded the consumer protection act claims

• Found that Sears was not statutorily authorized to collect this tax

Consumer Protection Violations?

Chicago Tax Club

• Loeffler v. Target Corporation, Slip Opinions No. 5173972 (May 1, 2014)

• May a consumer in a sales tax transaction sue a retailer under the consumer protection laws for allegedly improperly collecting sales tax reimbursement on a transaction the plaintiff contends is not subject to sales tax? Target collected sales tax reimbursement from consumers who purchased a cup of coffee “to go.”

• Held that the refund scheme created by California tax code provides the exclusive remedy for a dispute over the applicability of the state tax laws to retail transactions.

Consumer Protection Violations?

Chicago Tax Club

• Yabsley v. Cingular Wireless LLC , 176 Cal.App.4th 1156

• Did Cingular violate the CA False Advertising Law when it advertised it would collect sales tax reimbursement on sales of cellular phones?

• Under Regulation1585, the retailer must pay sales tax (and may collect sales tax reimbursement) on the full unbundled price of the phone when it sells a cell phone bundled with a service contract

• Court of Appeals agreed with the trial court that regulations provide the same safe harbor for suits under the UCL that statutes do. The class action was thus dismissed.

False Advertising Violations?

Chicago Tax Club

Questions?

David HughesHorwood MarcusChicago, Illinois(312) 267-2193

David C. BlumLevenfeld Pearlstein

Chicago, Illinois(312) 476-7557

Ted BotsBaker & McKenzie

Chicago, Illinois(312) 861-8845