Embed Size (px)

Citation preview

Transfer of Right To UsePrepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Introduction -

Taxation of 'transfer of right to use any goods' was introduced in 1982 by insertion of sub-clause 29A(d) in Article 366 under the Constitution of India for defining 'tax on the sale or purchase of goods' [i.e. a 'deemed sale']. In 2008, the taxable service category of supply of tangible goods for use ('SOTGU service') was introduced under section 65(105)(zzzzj) of the Finance Act, 1994 to bring under the ambit of service tax transactions involving supply of tangible goods (eg. machinery, equipment and other appliances etc.) for use, where the legal right of 'possession' and 'effective control' was not transferred to the hirer.

Introduction

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

The legal right to use something or occupy.. Transfer of right to use GOODS as deemed sale:Transfer of right to use goods is one of the elements of "deemed sale" under the

enlarged meaning and scope of Article 366 (29A)(d) of our constitution post the 46th Amendment.

Article 366(29A)(d) : Tax on the sale or purchase of goods includes a tax on the transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration;

Definition

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Transfer of right to use goods as Service:As per section 65(105)(zzzzj) taxable service means “any service provided or to be

provided to any person, by any other person in relation to supply of tangible goods including machinery, equipment and appliances for use, without transferring right of possession and effective control of such machinery, equipment and appliances".

service in relation to tangible goods is taxable as a separate service. This is known as Service of Intangible Goods.

Definition

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

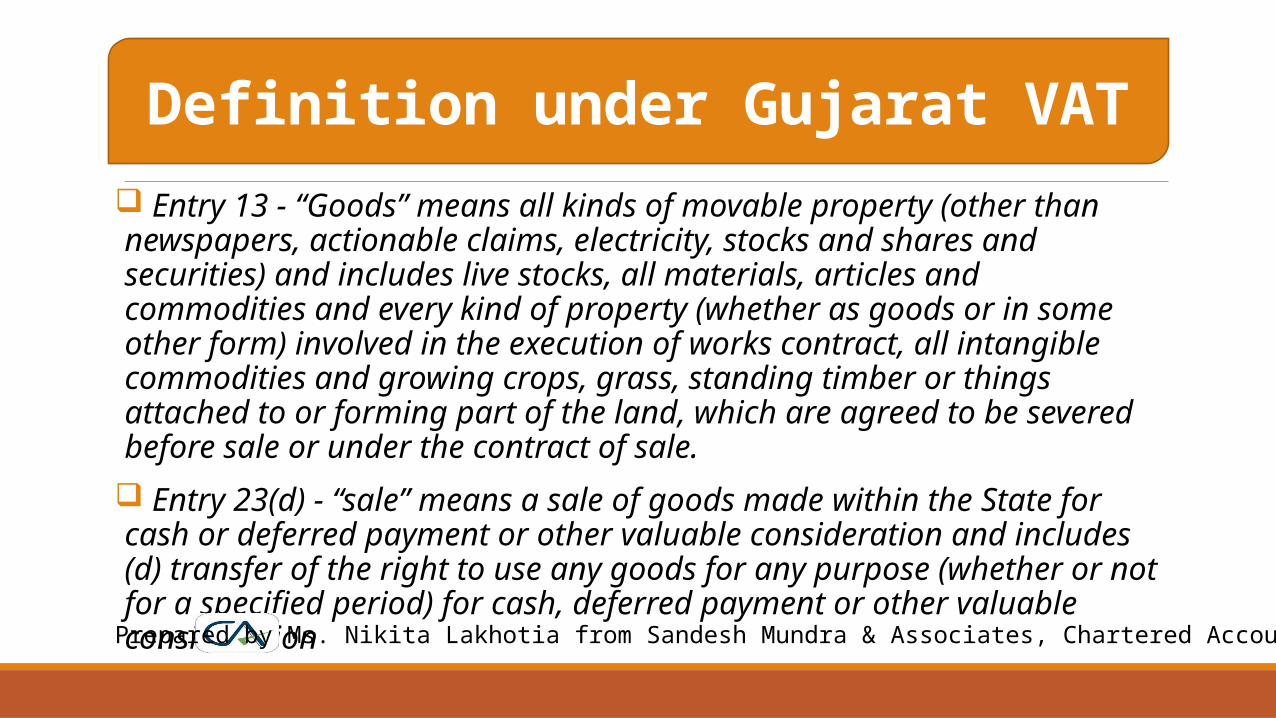

Entry 13 - “Goods” means all kinds of movable property (other than newspapers, actionable claims, electricity, stocks and shares and securities) and includes live stocks, all materials, articles and commodities and every kind of property (whether as goods or in some other form) involved in the execution of works contract, all intangible commodities and growing crops, grass, standing timber or things attached to or forming part of the land, which are agreed to be severed before sale or under the contract of sale. Entry 23(d) - “sale” means a sale of goods made within the State for cash or deferred payment or other valuable consideration and includes (d) transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration

Definition under Gujarat VAT

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

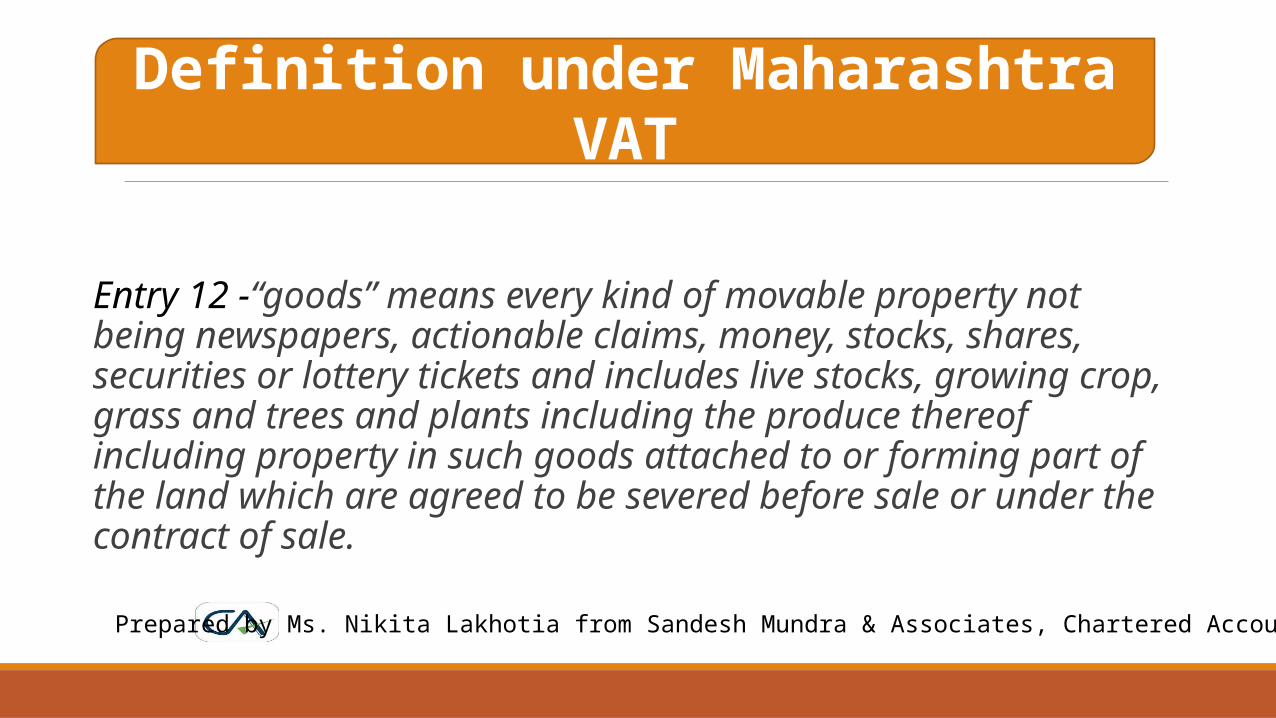

Entry 12 -“goods” means every kind of movable property not being newspapers, actionable claims, money, stocks, shares, securities or lottery tickets and includes live stocks, growing crop, grass and trees and plants including the produce thereof including property in such goods attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale.

Definition under Maharashtra VAT

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

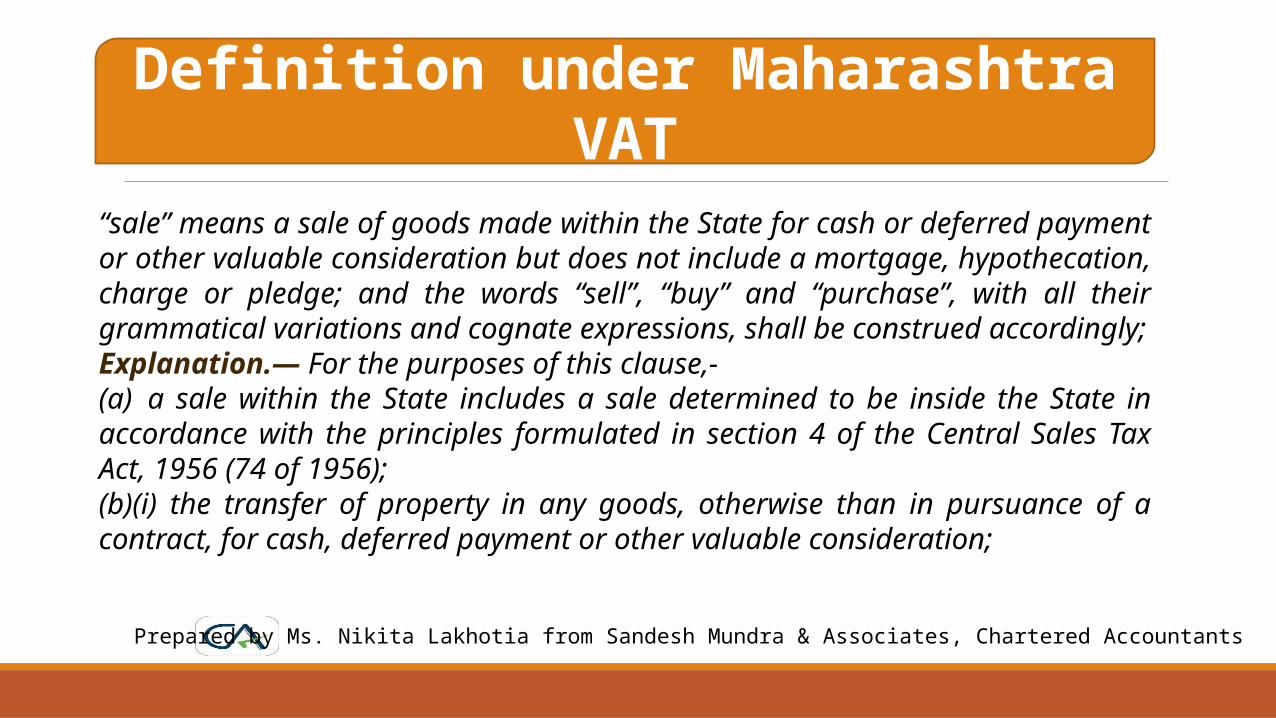

“sale” means a sale of goods made within the State for cash or deferred payment or other valuable consideration but does not include a mortgage, hypothecation, charge or pledge; and the words “sell”, “buy” and “purchase”, with all their grammatical variations and cognate expressions, shall be construed accordingly;Explanation.— For the purposes of this clause,-(a) a sale within the State includes a sale determined to be inside the State in accordance with the principles formulated in section 4 of the Central Sales Tax Act, 1956 (74 of 1956);(b)(i) the transfer of property in any goods, otherwise than in pursuance of a contract, for cash, deferred payment or other valuable consideration;

Definition under Maharashtra VAT

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

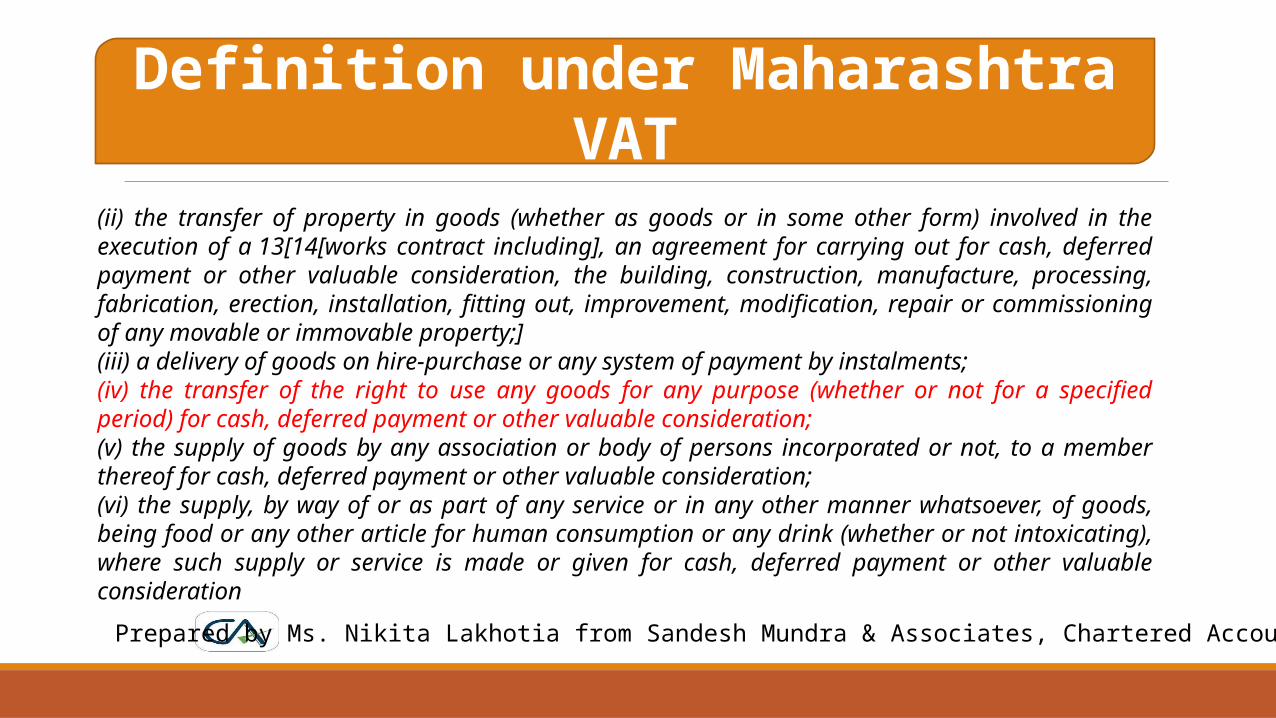

(ii) the transfer of property in goods (whether as goods or in some other form) involved in the execution of a 13[14[works contract including], an agreement for carrying out for cash, deferred payment or other valuable consideration, the building, construction, manufacture, processing, fabrication, erection, installation, fitting out, improvement, modification, repair or commissioning of any movable or immovable property;](iii) a delivery of goods on hire-purchase or any system of payment by instalments;(iv) the transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration;(v) the supply of goods by any association or body of persons incorporated or not, to a member thereof for cash, deferred payment or other valuable consideration;(vi) the supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (whether or not intoxicating), where such supply or service is made or given for cash, deferred payment or other valuable consideration

Definition under Maharashtra VAT

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

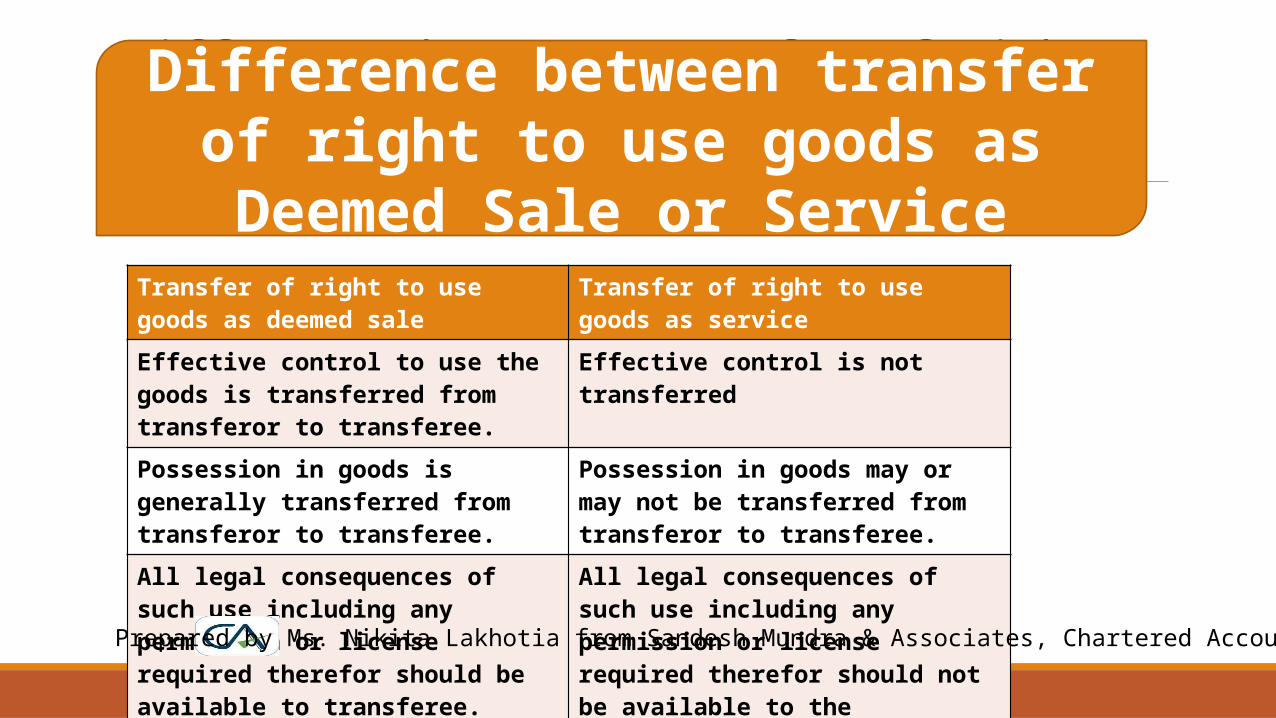

Difference between transfer of right to use goods as deemed sale and as service

Transfer of right to use goods as deemed sale

Transfer of right to use goods as service

Effective control to use the goods is transferred from transferor to transferee.

Effective control is not transferred

Possession in goods is generally transferred from transferor to transferee.

Possession in goods may or may not be transferred from transferor to transferee.

All legal consequences of such use including any permission or license required therefor should be available to transferee.

All legal consequences of such use including any permission or license required therefor should not be available to the transferor.

Difference between transfer of right to use goods as Deemed Sale or Service

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Case Laws on Transfer of Right To Use Intangible Goods

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

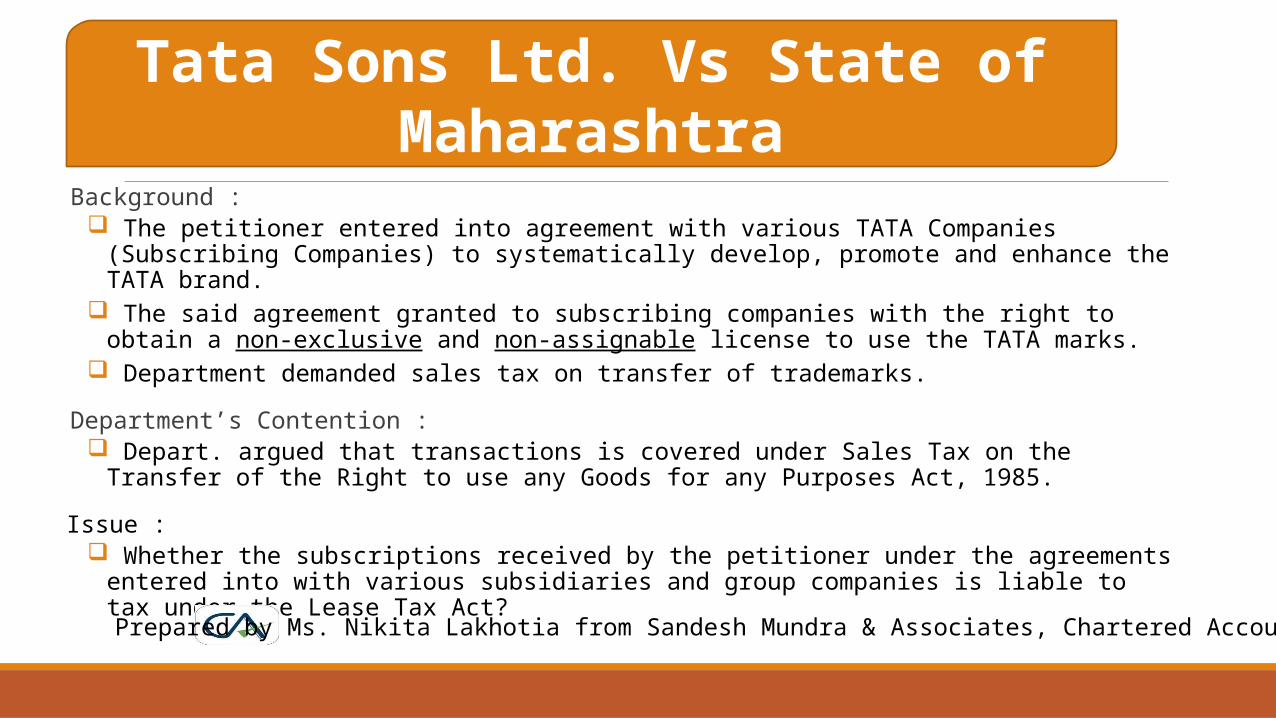

Tata Sons Ltd. Vs State of MaharashtraBackground : The petitioner entered into agreement with various TATA Companies (Subscribing Companies) to

systematically develop, promote and enhance the TATA brand. The said agreement granted to subscribing companies with the right to obtain a non-exclusive and non-

assignable license to use the TATA marks. Department demanded sales tax on transfer of trademarks.

Department’s Contention : Depart. argued that transactions is covered under Sales Tax on the Transfer of the Right to use any Goods for

any Purposes Act, 1985.

Issue : Whether the subscriptions received by the petitioner under the agreements entered into with various

subsidiaries and group companies is liable to tax under the Lease Tax Act?

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

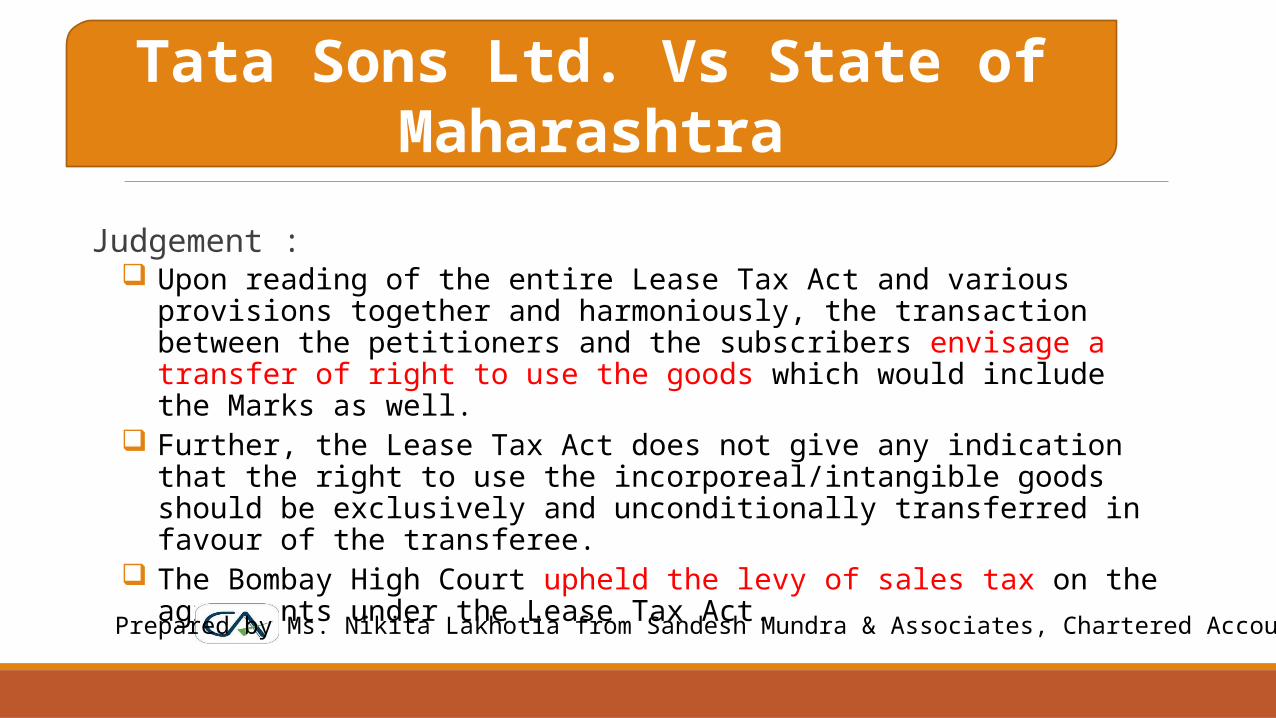

Judgement : Upon reading of the entire Lease Tax Act and various provisions together and

harmoniously, the transaction between the petitioners and the subscribers envisage a transfer of right to use the goods which would include the Marks as well.

Further, the Lease Tax Act does not give any indication that the right to use the incorporeal/intangible goods should be exclusively and unconditionally transferred in favour of the transferee.

The Bombay High Court upheld the levy of sales tax on the agreements under the Lease Tax Act.

Tata Sons Ltd. Vs State of Maharashtra

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

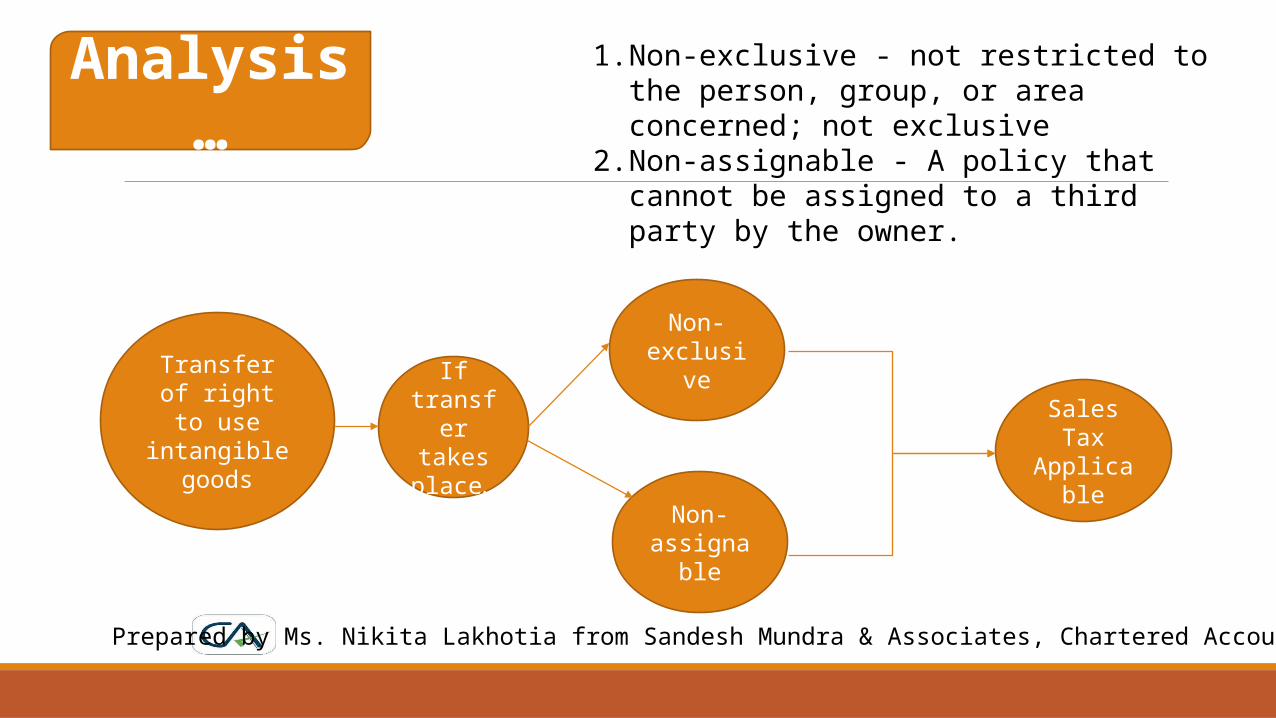

Analysis…

Transfer of right to use intangible

goods

If transfer

takes place…

Non-exclusive

Non-assignable

1. Non-exclusive - not restricted to the person, group, or area concerned; not exclusive

2. Non-assignable - A policy that cannot be assigned to a third party by the owner.

Sales Tax Applicable

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

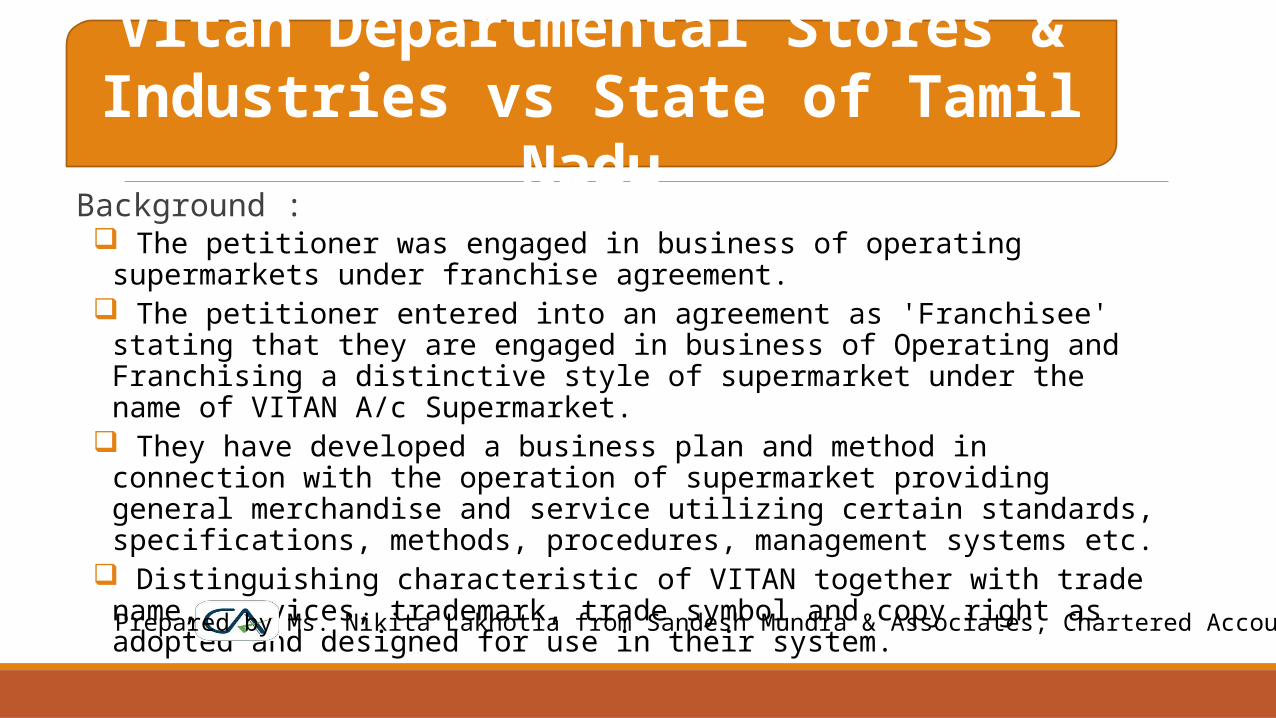

Background : The petitioner was engaged in business of operating supermarkets under franchise

agreement. The petitioner entered into an agreement as 'Franchisee' stating that they are engaged

in business of Operating and Franchising a distinctive style of supermarket under the name of VITAN A/c Supermarket.

They have developed a business plan and method in connection with the operation of supermarket providing general merchandise and service utilizing certain standards, specifications, methods, procedures, management systems etc.

Distinguishing characteristic of VITAN together with trade name, services, trademark, trade symbol and copy right as adopted and designed for use in their system.

Vitan Departmental Stores & Industries vs State of Tamil Nadu

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

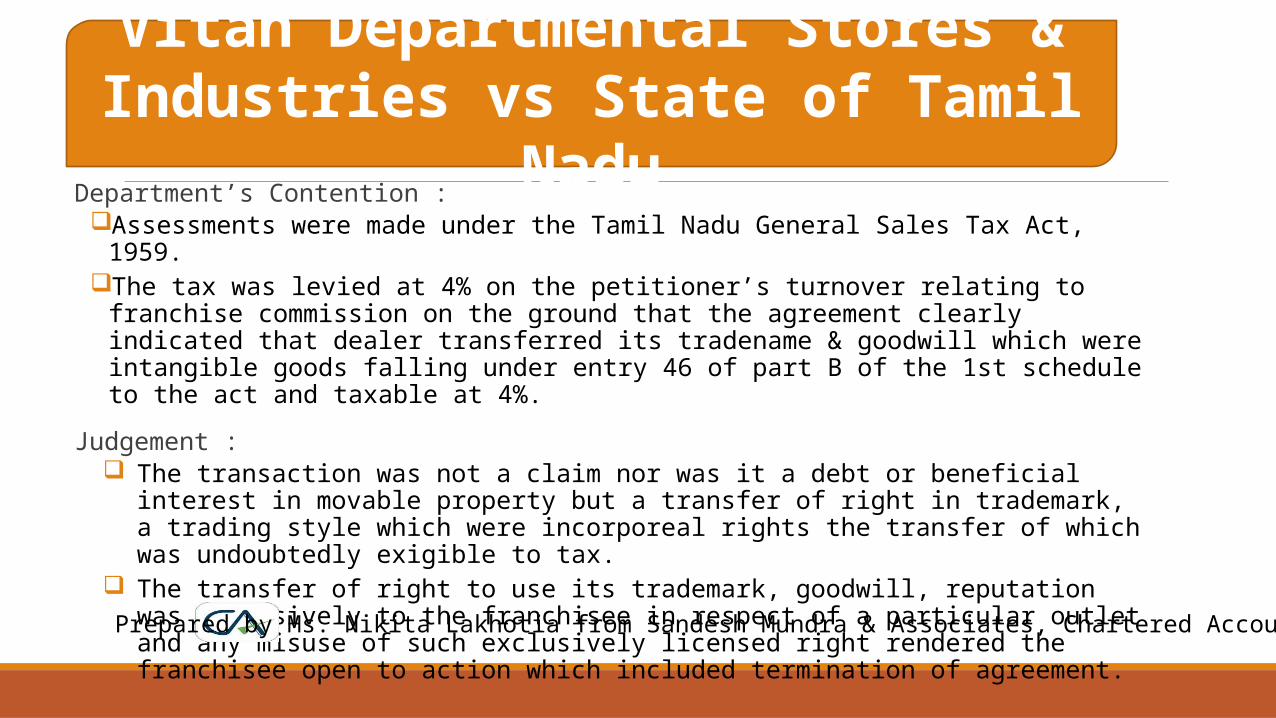

Department’s Contention :Assessments were made under the Tamil Nadu General Sales Tax Act, 1959.The tax was levied at 4% on the petitioner’s turnover relating to franchise commission on the

ground that the agreement clearly indicated that dealer transferred its tradename & goodwill which were intangible goods falling under entry 46 of part B of the 1st schedule to the act and taxable at 4%.

Judgement : The transaction was not a claim nor was it a debt or beneficial interest in movable property

but a transfer of right in trademark, a trading style which were incorporeal rights the transfer of which was undoubtedly exigible to tax.

The transfer of right to use its trademark, goodwill, reputation was exclusively to the franchisee in respect of a particular outlet and any misuse of such exclusively licensed right rendered the franchisee open to action which included termination of agreement.

Vitan Departmental Stores & Industries vs State of Tamil Nadu

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

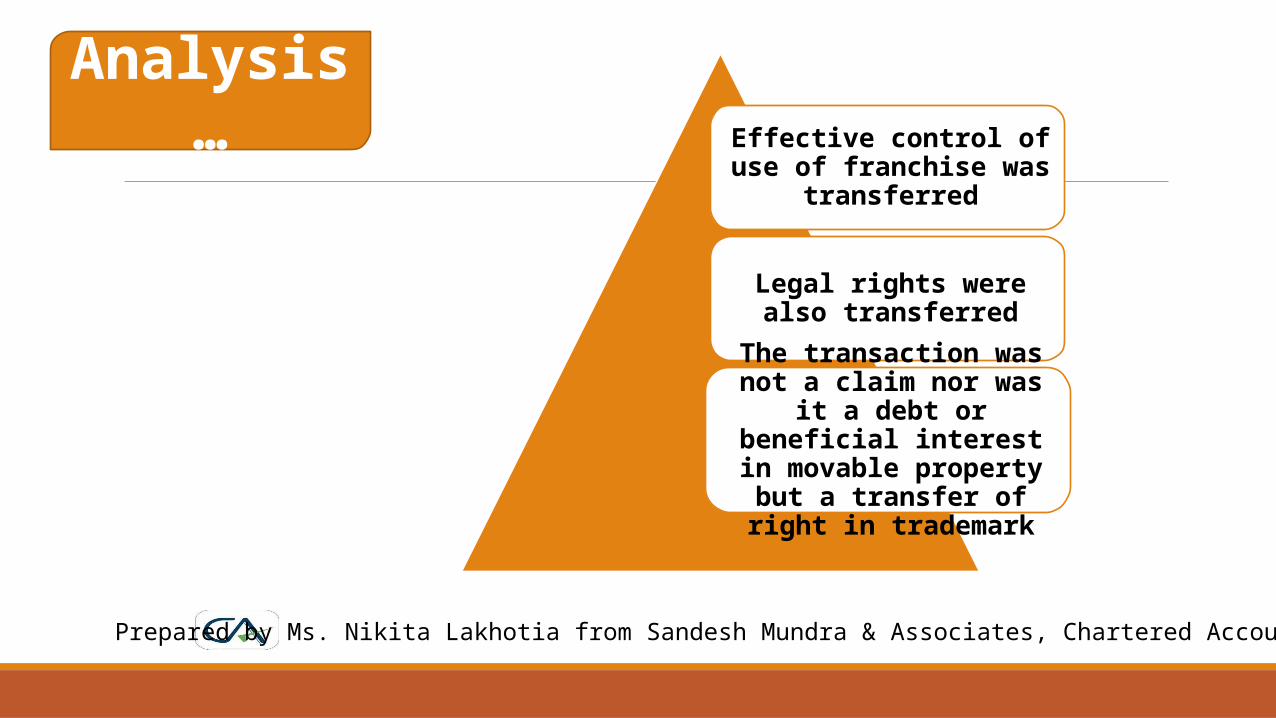

Analysis…Effective control of use of franchise was transferred

Legal rights were also transferred

The transaction was not a claim nor was it a debt or

beneficial interest in movable property but a transfer of

right in trademark

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Background :The petitioner-dealer owned telecommunication sites, infrastructure and

equipment in various licensed circles in India and provided passive infrastructure and related operations and maintenance services to telecommunication operators on a shared basis.

For providing the services, the dealer entered into identical master services agreements with telecom operators. Under the agreement the dealer offered to share its passive infrastructure and equipment with the sharing operator. The telecom service providers were charged by the dealer for the “site access availability”,

Indus Towers Ltd. Vs. Deputy Commissioner of Commercial Taxes, Enforcement 1, Bangalore and Others

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Judgment :The master services agreement was an agreement to share equipment and such sharing was by way of

permission and not by way of transfer.The intention of the parties was not to transfer at any point of time, any right, title or interest in the

infrastructure to the mobile operator under the terms of the contract. The entire infrastructure was in the physical control and possession of the dealer at all times and there was

neither physical transfer of such goods nor transfer of right to use such equipment or apparatus. Merely because access provided to the mobile operator, could not be transferred by the dealer during the

period of contract to a third party that would not amount to the dealer losing control over the infrastructure.The legal possession thereof continues to be in the owner of the property but the licensee is permitted to

make use of the premises for the particular period. But for the permission its occupation would be unlawful, and does not create in its favour any estate or interest in the property.

Indus Towers Ltd. Vs. Deputy Commissioner of Commercial Taxes, Enforcement 1, Bangalore and Others

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Analysis…Legal rights were not

transferred

Only a permission to use equipments was given

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Background : Provide direct-to-home (DTH) service to the customers in the State of Tripura. Provide STB(s) and other accessories (remote, adapter, smart card etc.) to customer to

decode signals and watch programs on TV

Department’s Contention : The contention of the petitioners is that the equipment in the nature of STB which is used by

the customers is not sold to the customers but remains the property of the service provider and the service provider retains the control of the equipment.

The contention of the State is that the transaction entered into by the petitioners virtually amount to sale of the STBs and in any event the petitioners have transferred the right to use the STBs to the customers and, therefore, such a contract is liable to be taxed

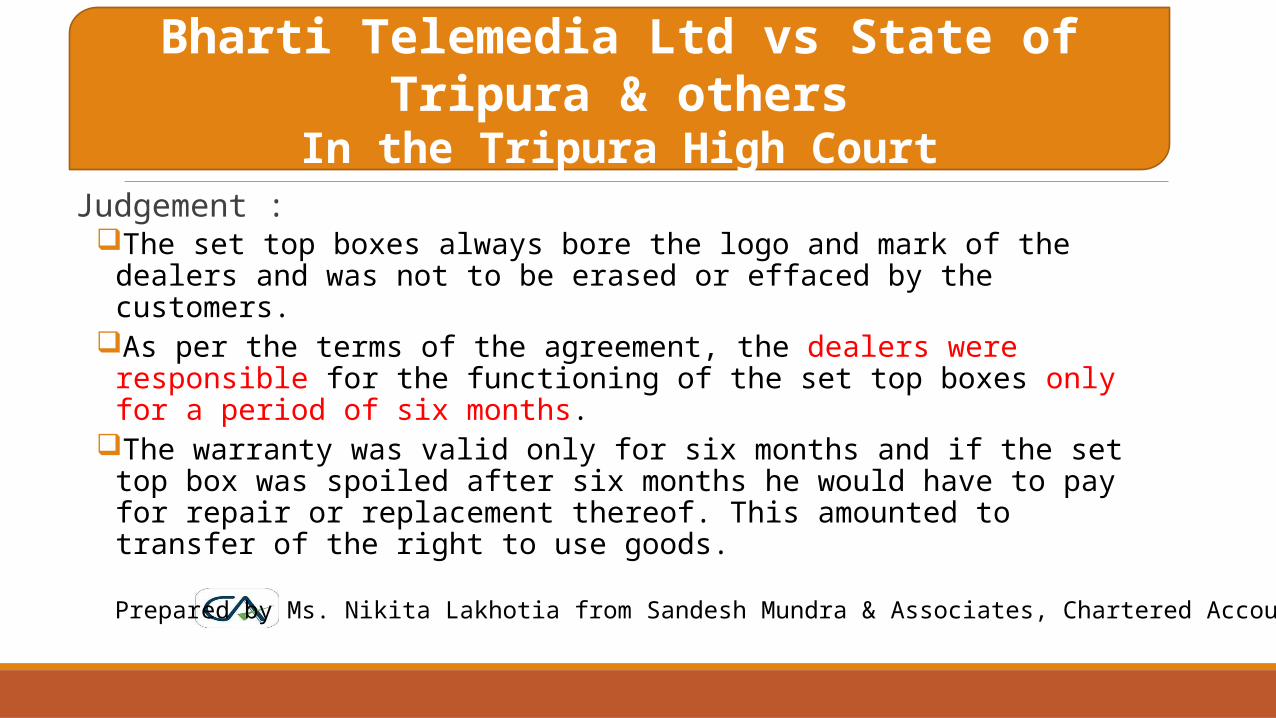

Bharti Telemedia Ltd vs State of Tripura & othersIn the Tripura High Court

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Judgement :The set top boxes always bore the logo and mark of the dealers and was not to be

erased or effaced by the customers.As per the terms of the agreement, the dealers were responsible for the functioning

of the set top boxes only for a period of six months.The warranty was valid only for six months and if the set top box was spoiled after

six months he would have to pay for repair or replacement thereof. This amounted to transfer of the right to use goods.

Bharti Telemedia Ltd vs State of Tripura & othersIn the Tripura High Court

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

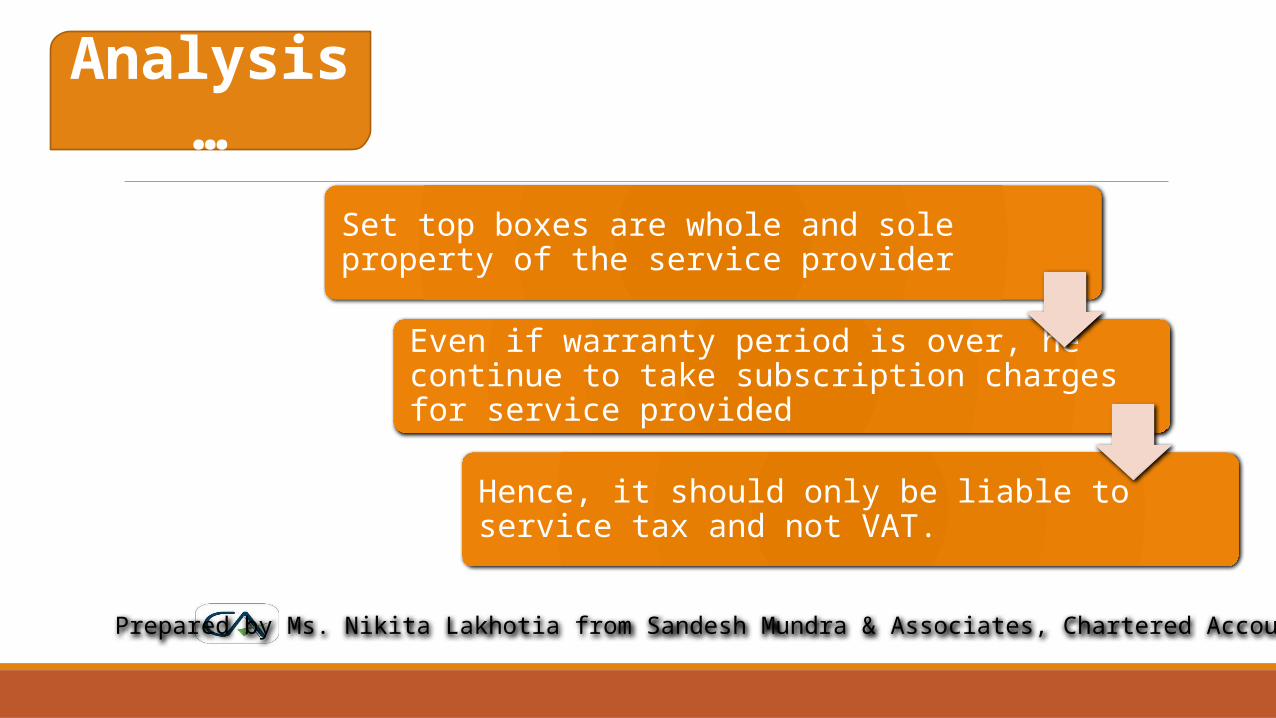

Analysis…

Set top boxes are whole and sole property of the service provider

Even if warranty period is over, he continue to take subscription charges for service provided

Hence, it should only be liable to service tax and not VAT.

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Case Laws on Transfer of Right To Use Goods

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

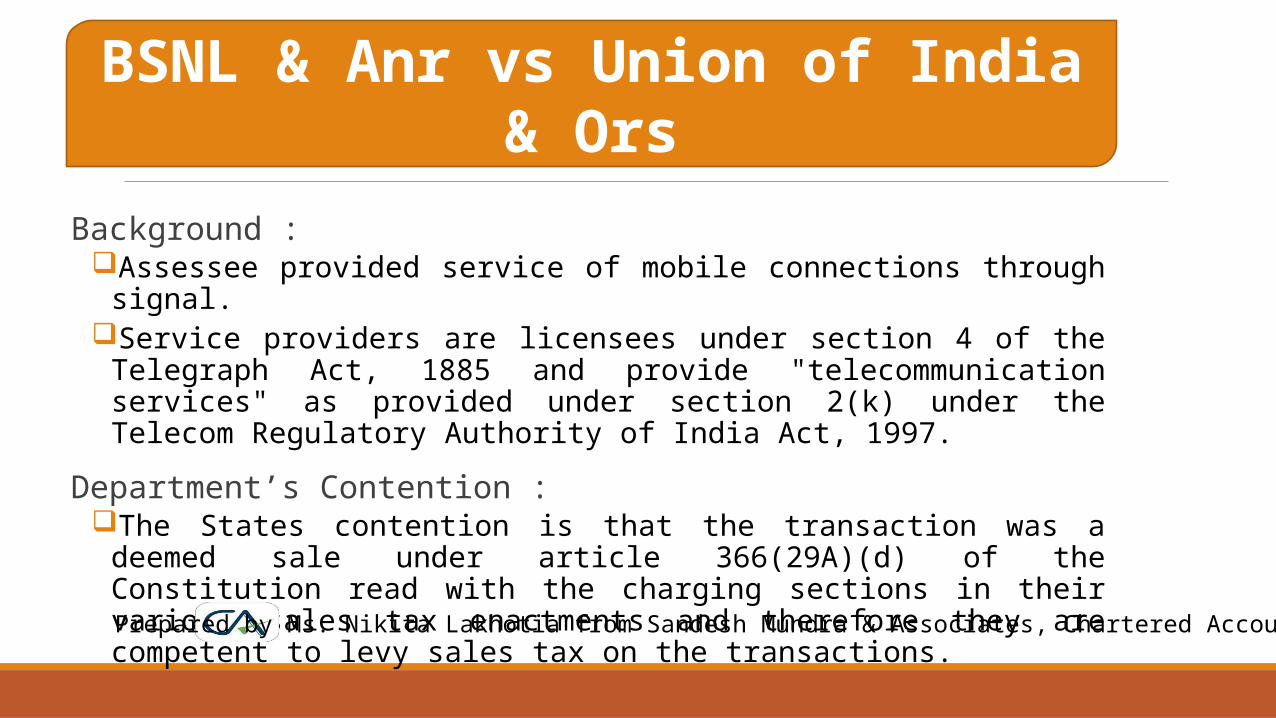

Background :Assessee provided service of mobile connections through signal.Service providers are licensees under section 4 of the Telegraph Act, 1885 and

provide "telecommunication services" as provided under section 2(k) under the Telecom Regulatory Authority of India Act, 1997.

Department’s Contention :The States contention is that the transaction was a deemed sale under article

366(29A)(d) of the Constitution read with the charging sections in their various sales tax enactments and therefore they are competent to levy sales tax on the transactions.

BSNL & Anr vs Union of India & Ors

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

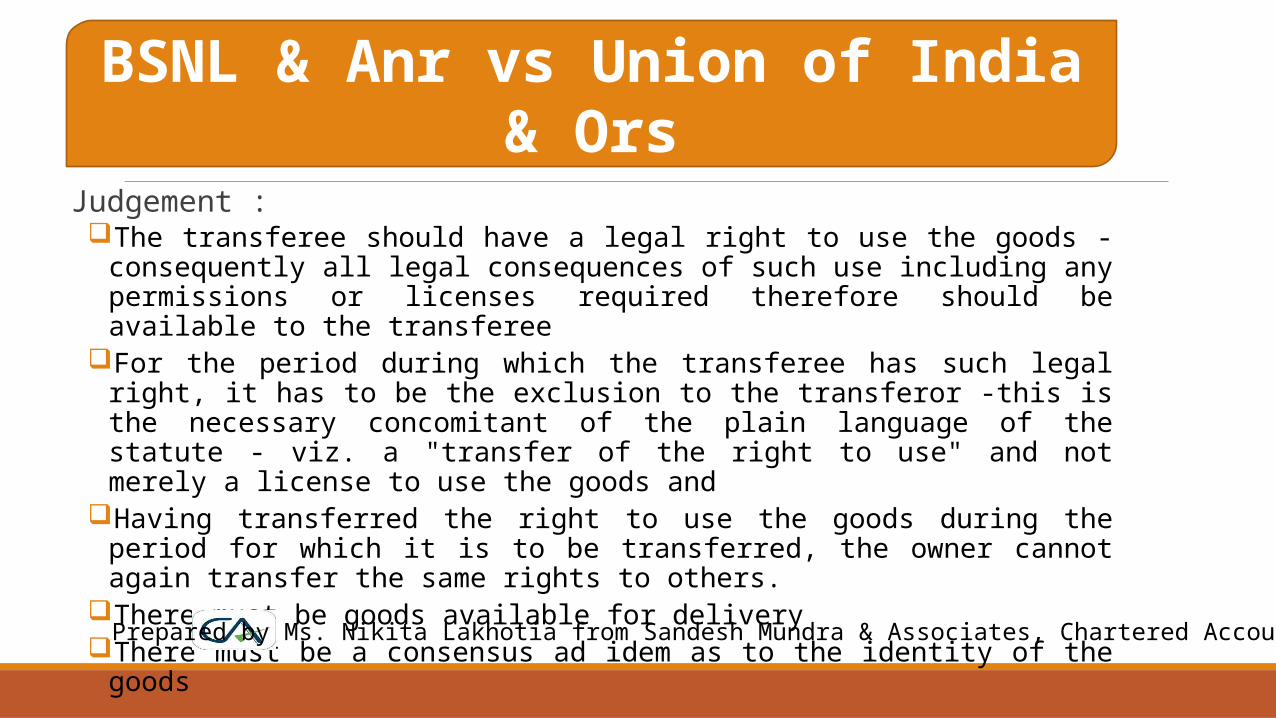

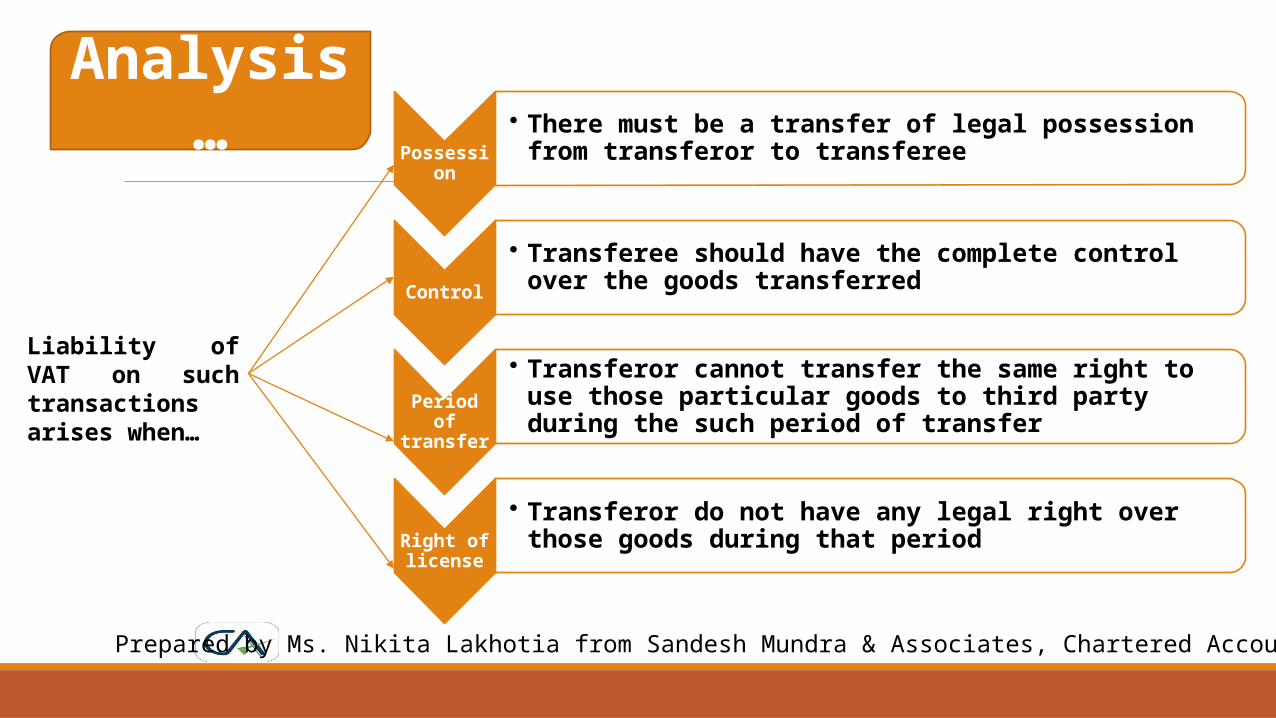

Judgement :The transferee should have a legal right to use the goods - consequently all legal

consequences of such use including any permissions or licenses required therefore should be available to the transferee

For the period during which the transferee has such legal right, it has to be the exclusion to the transferor -this is the necessary concomitant of the plain language of the statute - viz. a "transfer of the right to use" and not merely a license to use the goods and

Having transferred the right to use the goods during the period for which it is to be transferred, the owner cannot again transfer the same rights to others.

There must be goods available for deliveryThere must be a consensus ad idem as to the identity of the goods

BSNL & Anr vs Union of India & Ors

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Analysis…Possession

• There must be a transfer of legal possession from transferor to transferee

Control

• Transferee should have the complete control over the goods transferred

Period of transfer

• Transferor cannot transfer the same right to use those particular goods to third party during the such period of transfer

Right of license

• Transferor do not have any legal right over those goods during that period

Liability of VAT on such transactions arises when…

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

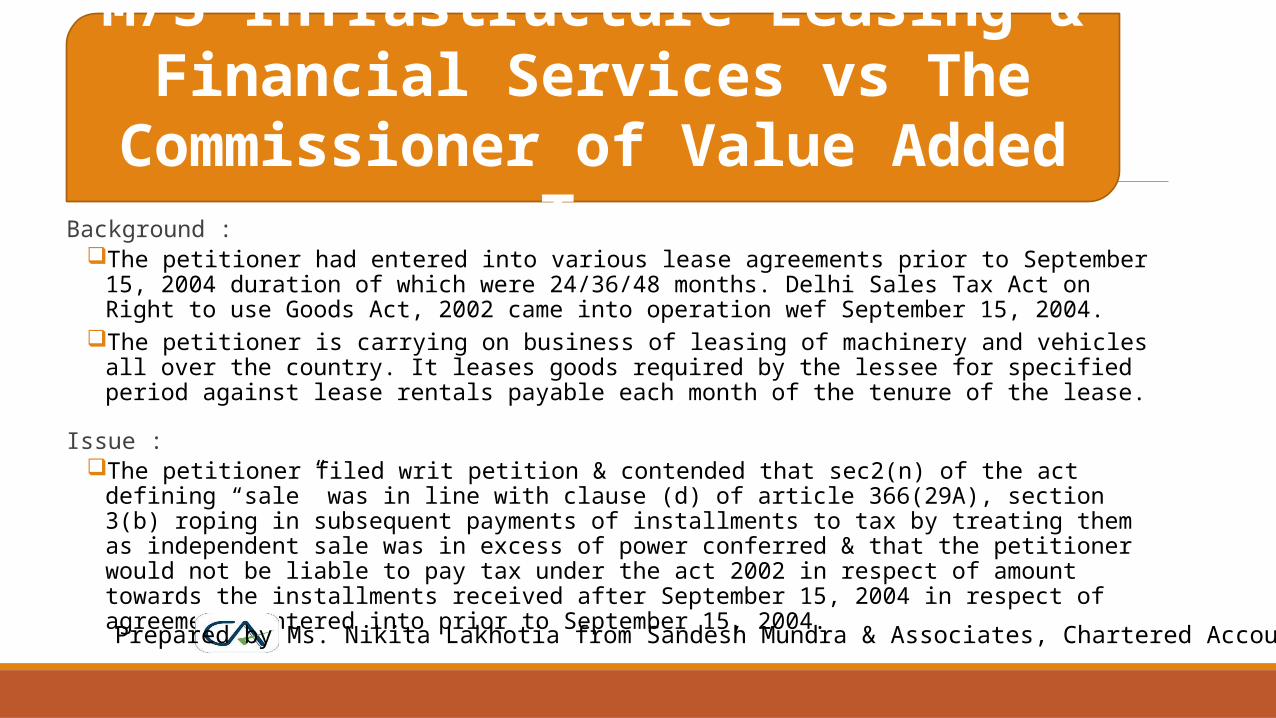

Background :The petitioner had entered into various lease agreements prior to September 15, 2004 duration of which

were 24/36/48 months. Delhi Sales Tax Act on Right to use Goods Act, 2002 came into operation wef September 15, 2004.

The petitioner is carrying on business of leasing of machinery and vehicles all over the country. It leases goods required by the lessee for specified period against lease rentals payable each month of the tenure of the lease.

Issue :The petitioner filed writ petition & contended that sec2(n) of the act defining “sale” was in line with clause

(d) of article 366(29A), section 3(b) roping in subsequent payments of installments to tax by treating them as independent sale was in excess of power conferred & that the petitioner would not be liable to pay tax under the act 2002 in respect of amount towards the installments received after September 15, 2004 in respect of agreements entered into prior to September 15, 2004.

M/S Infrastructure Leasing & Financial Services vs The Commissioner of Value

Added Tax

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

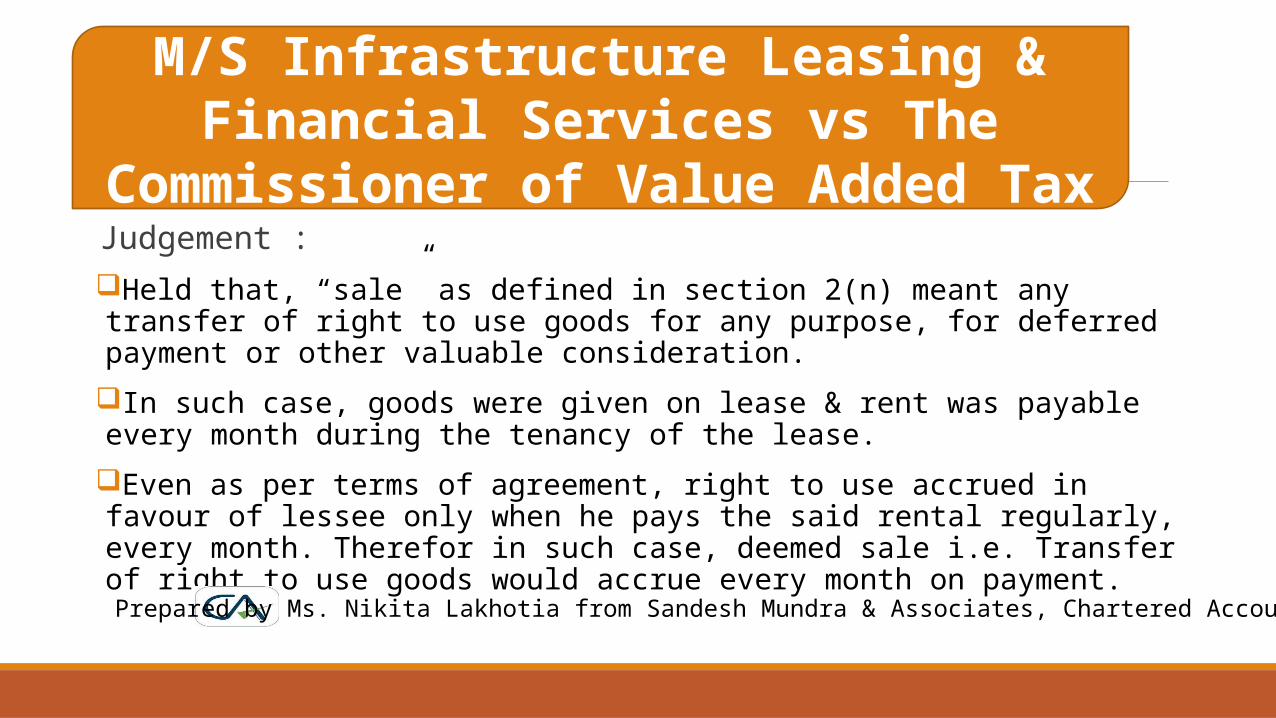

Judgement :Held that, “sale” as defined in section 2(n) meant any transfer of right to use goods for any purpose, for deferred payment or other valuable consideration.In such case, goods were given on lease & rent was payable every month during the tenancy of the lease.Even as per terms of agreement, right to use accrued in favour of lessee only when he pays the said rental regularly, every month. Therefor in such case, deemed sale i.e. Transfer of right to use goods would accrue every month on payment.

M/S Infrastructure Leasing & Financial Services vs The Commissioner of Value Added

Tax

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

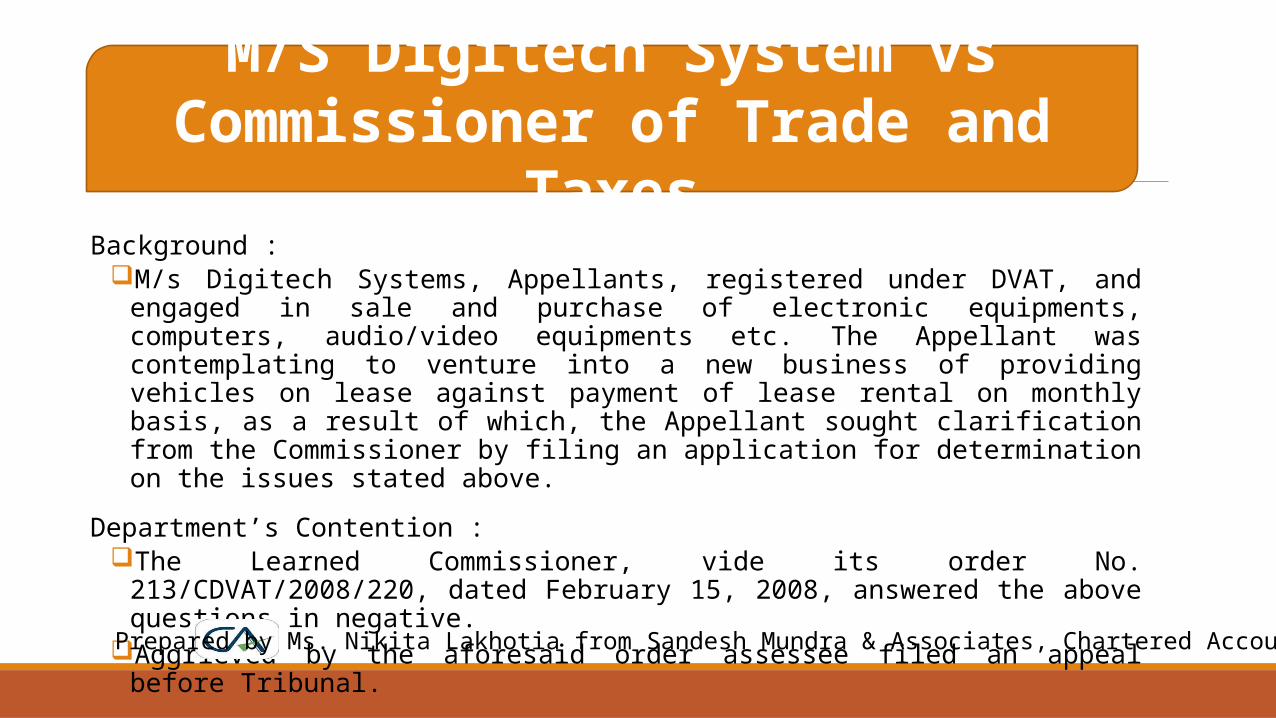

Background :M/s Digitech Systems, Appellants, registered under DVAT, and engaged in sale and purchase

of electronic equipments, computers, audio/video equipments etc. The Appellant was contemplating to venture into a new business of providing vehicles on lease against payment of lease rental on monthly basis, as a result of which, the Appellant sought clarification from the Commissioner by filing an application for determination on the issues stated above.

Department’s Contention :The Learned Commissioner, vide its order No. 213/CDVAT/2008/220, dated February 15,

2008, answered the above questions in negative.Aggrieved by the aforesaid order assessee filed an appeal before Tribunal.

M/S Digitech System vs Commissioner of Trade and Taxes

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Judgment :

◦ Right to use goods has been transferred in the leasing contract even when no ownership of goods passed.

◦ Tax to be levied with deferred payments.

M/S Digitech System vs Commissioner of Trade and Taxes

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

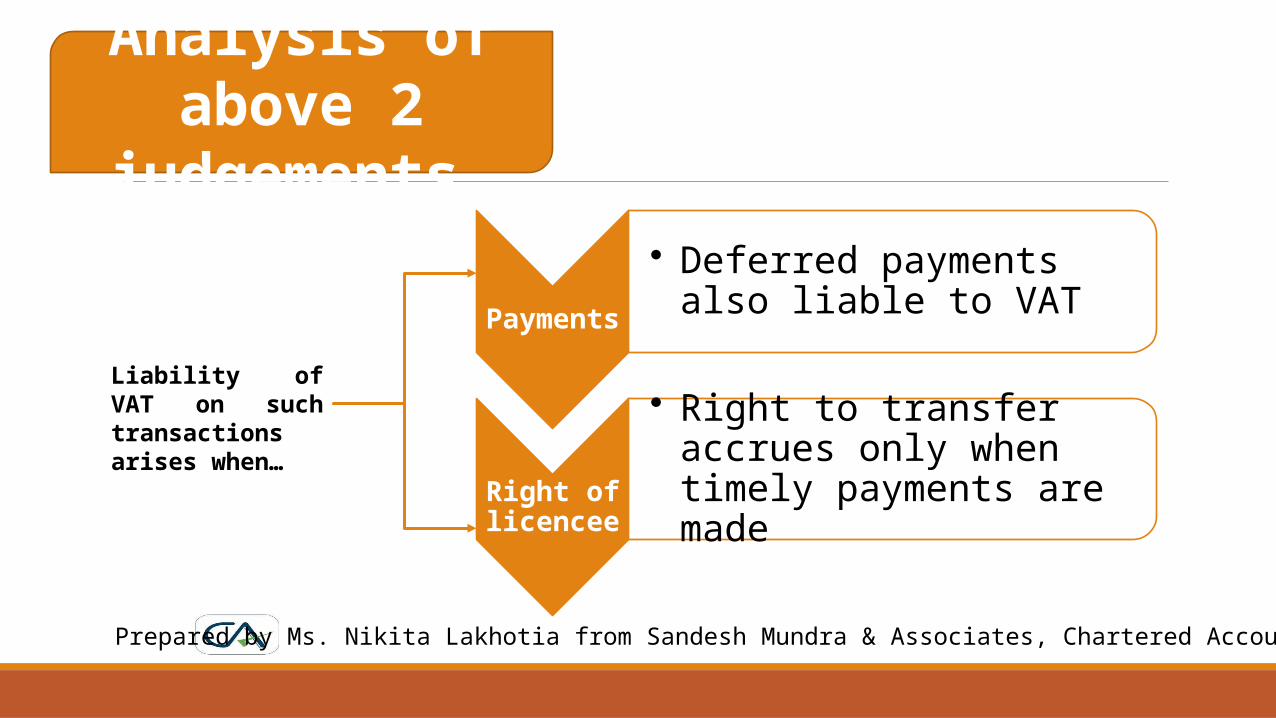

Analysis of above 2 judgements…

Payments

• Deferred payments also liable to VAT

Right of licencee

• Right to transfer accrues only when timely payments are made

Liability of VAT on such transactions arises when…

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

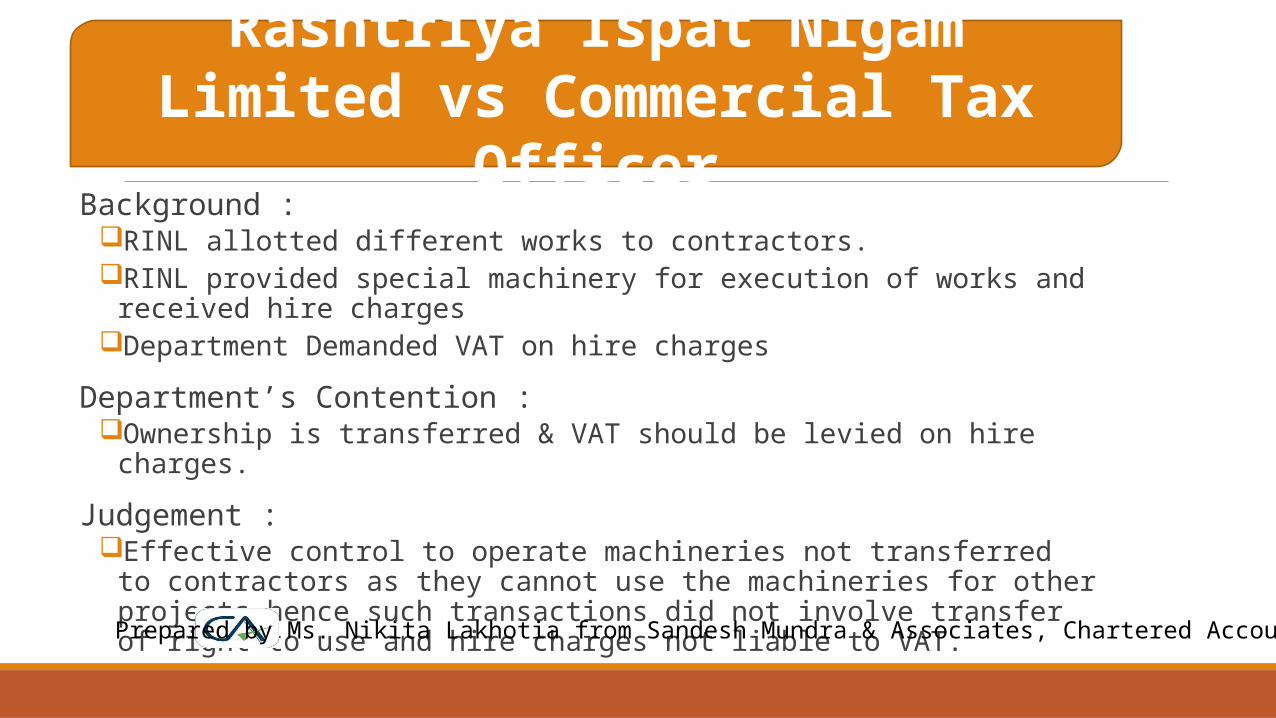

Background :RINL allotted different works to contractors.RINL provided special machinery for execution of works and received hire chargesDepartment Demanded VAT on hire charges

Department’s Contention : Ownership is transferred & VAT should be levied on hire charges.

Judgement :Effective control to operate machineries not transferred to contractors as they

cannot use the machineries for other projects hence such transactions did not involve transfer of right to use and hire charges not liable to VAT.

Rashtriya Ispat Nigam Limited vs Commercial Tax Officer

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Analysis…

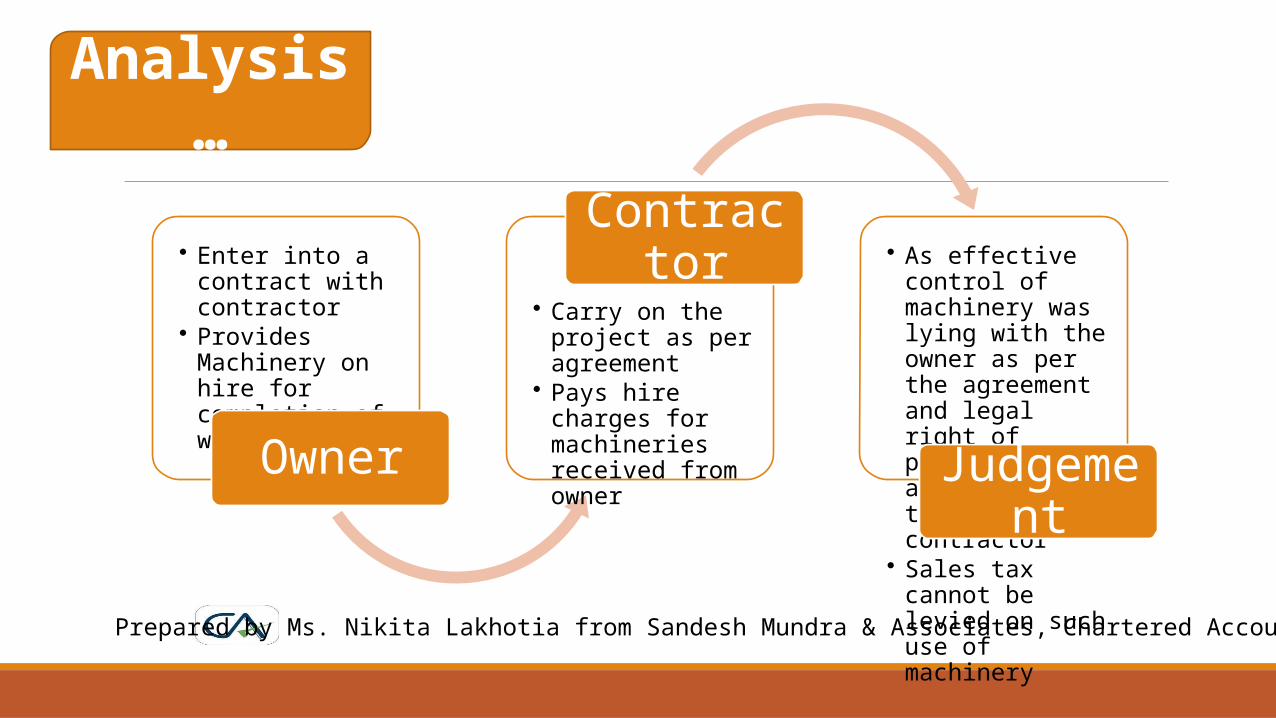

• Enter into a contract with contractor

• Provides Machinery on hire for completion of work

Owner

• Carry on the project as per agreement

• Pays hire charges for machineries received from owner

Contractor • As effective control of machinery was lying with the owner as per the agreement and legal right of possession was also not transferred to contractor

• Sales tax cannot be levied on such use of machinery

Judgement

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Background :The petitioners hiring their fleet of transit mixers to M/s Grasim Industries Ltd., Secunderabad, a unit of M/s.

Birla Ready Mix Concrete.The case of the petitioners is that Grasim manufactures Ready Mix Concrete (RMC), according to the

specifications depending on the site requirements of a customer, at its batching plants.

Facts :These contracts are for providing transportation service for shipping RMC by hiring specially designed transit

mixers.Effective control over running and using of these vehicles, as well as the disciplinary control over the drivers,

always remained with the petitioners.The clause for providing dedicated fleet of vehicles with Grasim's logo "birla concrete" being painted. To

assure the product quality to end-user, it was agreed to paint the brand name on the vehicles.

G S Lamba & Sons vs State of Andhra Pradesh(In the Andhra Pradesh High Court)

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Points for consideration :Whether the petitioners' contract is for transfer of the right to use transit mixers to M/s.

Grasim Industries Limited for transporting the RMC?Whether the State Sales Tax Appellate Tribunal has committed any error warranting

interference under section 22(1) of the Andhra Pradesh General Sales Tax Act, 1957?

Judgement :Though the phrase “offer services to take care of transporting solution needs” was used in

contract, the real purpose was to enable Grasims to have the right to use the transit mixers.The ready mix concrete had to be delivered by these drivers in transit mixers only at the

time and places as instructed by the officials of Grasim.The entire use in the property in goods was to be exclusively utilized for a period of 42

months by Grasim.Therefore, the only conclusion was that the dealers had transferred the right to use goods

to Grasim.

G S Lamba & Sons vs State of Andhra Pradesh(In the Andhra Pradesh High Court)

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Effective control transferred to transferee – liable to sales tax

All the work to be executed at the will of transferee

Analysis…

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

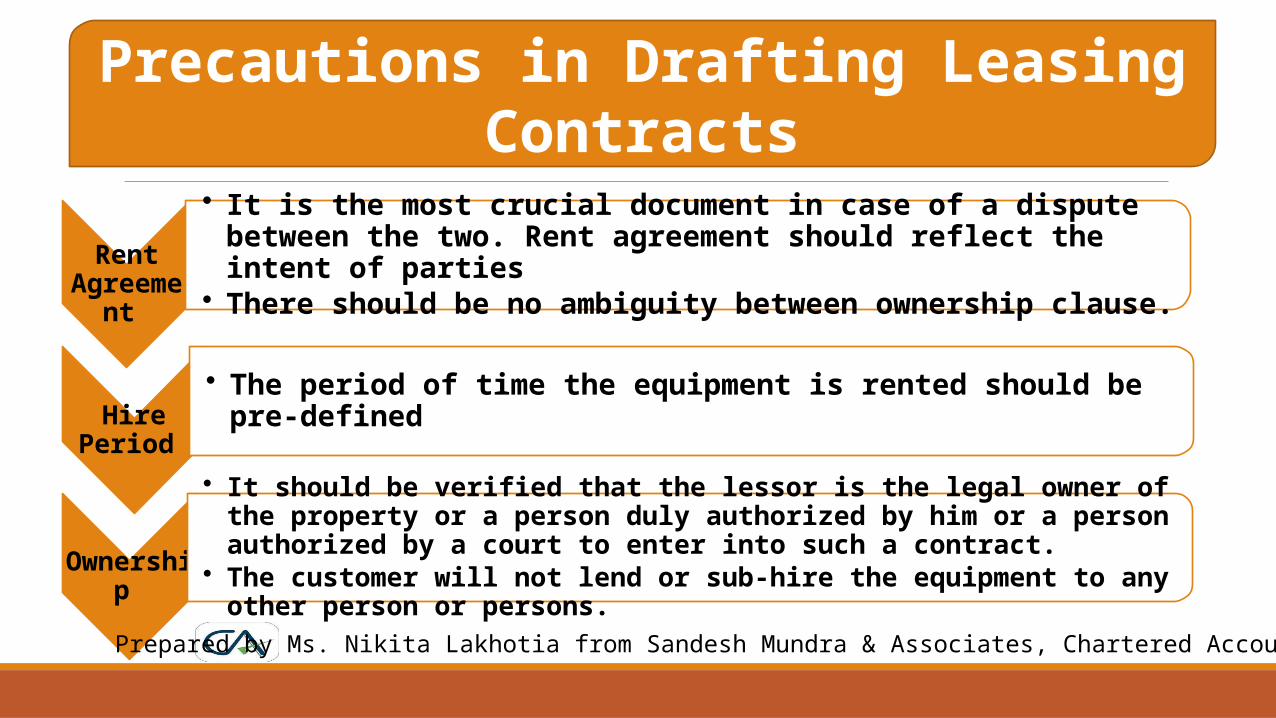

Rent Agreement

• It is the most crucial document in case of a dispute between the two. Rent agreement should reflect the intent of parties

• There should be no ambiguity between ownership clause.

Hire Period • The period of time the equipment is rented should be pre-defined

Ownership

• It should be verified that the lessor is the legal owner of the property or a person duly authorized by him or a person authorized by a court to enter into such a contract.

• The customer will not lend or sub-hire the equipment to any other person or persons.

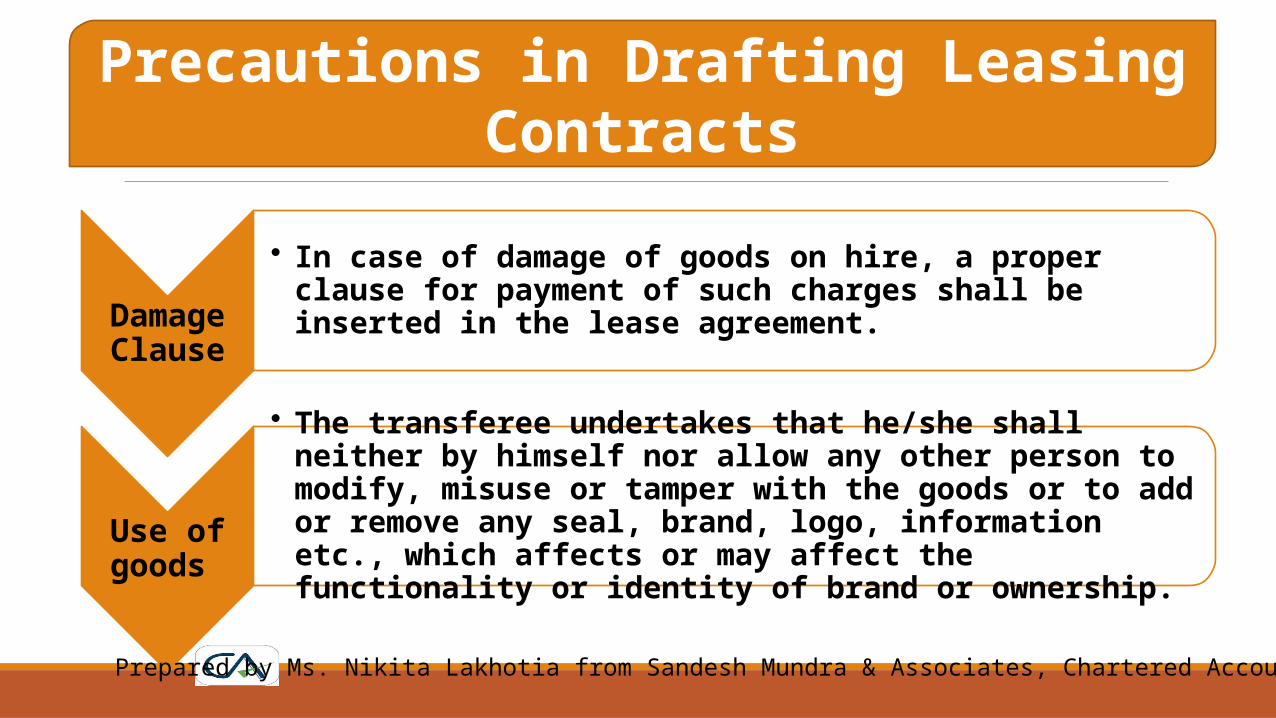

Precautions in Drafting Leasing Contracts

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

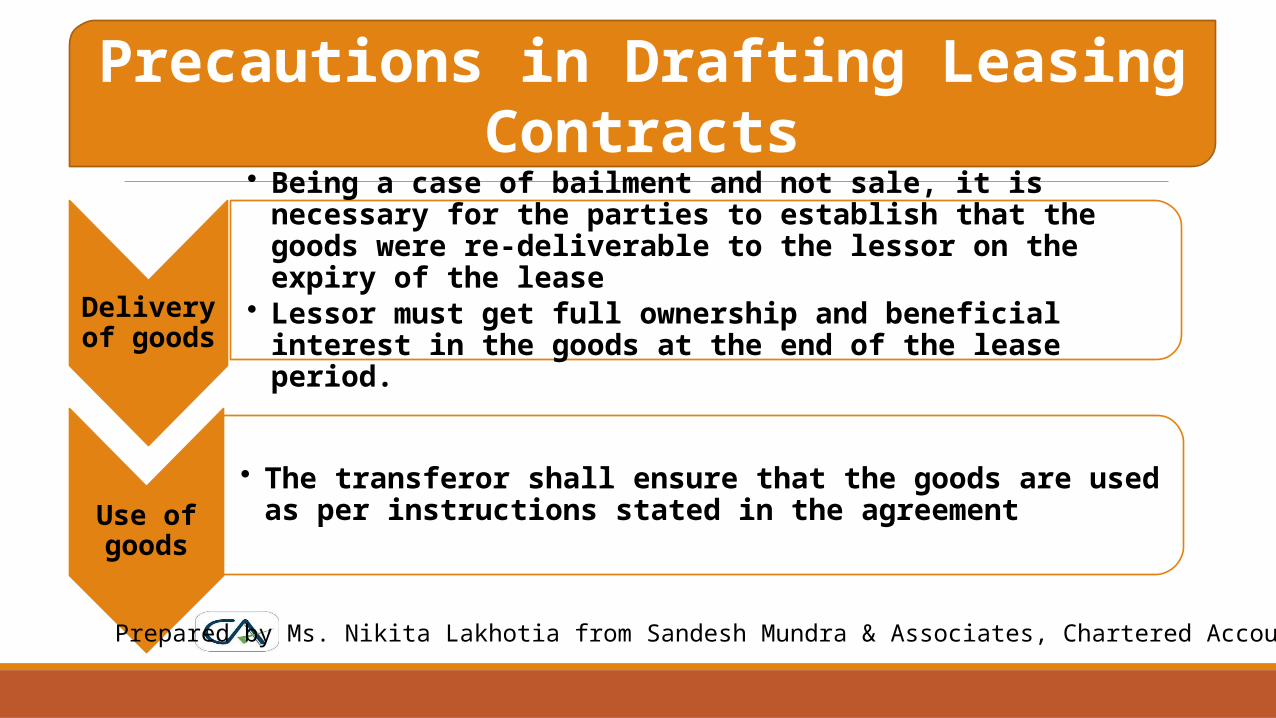

Delivery of goods

• Being a case of bailment and not sale, it is necessary for the parties to establish that the goods were re-deliverable to the lessor on the expiry of the lease

• Lessor must get full ownership and beneficial interest in the goods at the end of the lease period.

Use of goods

• The transferor shall ensure that the goods are used as per instructions stated in the agreement

Precautions in Drafting Leasing Contracts

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Precautions in Drafting Leasing Contracts

Damage Clause

• In case of damage of goods on hire, a proper clause for payment of such charges shall be inserted in the lease agreement.

Use of goods

• The transferee undertakes that he/she shall neither by himself nor allow any other person to modify, misuse or tamper with the goods or to add or remove any seal, brand, logo, information etc., which affects or may affect the functionality or identity of brand or ownership.

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

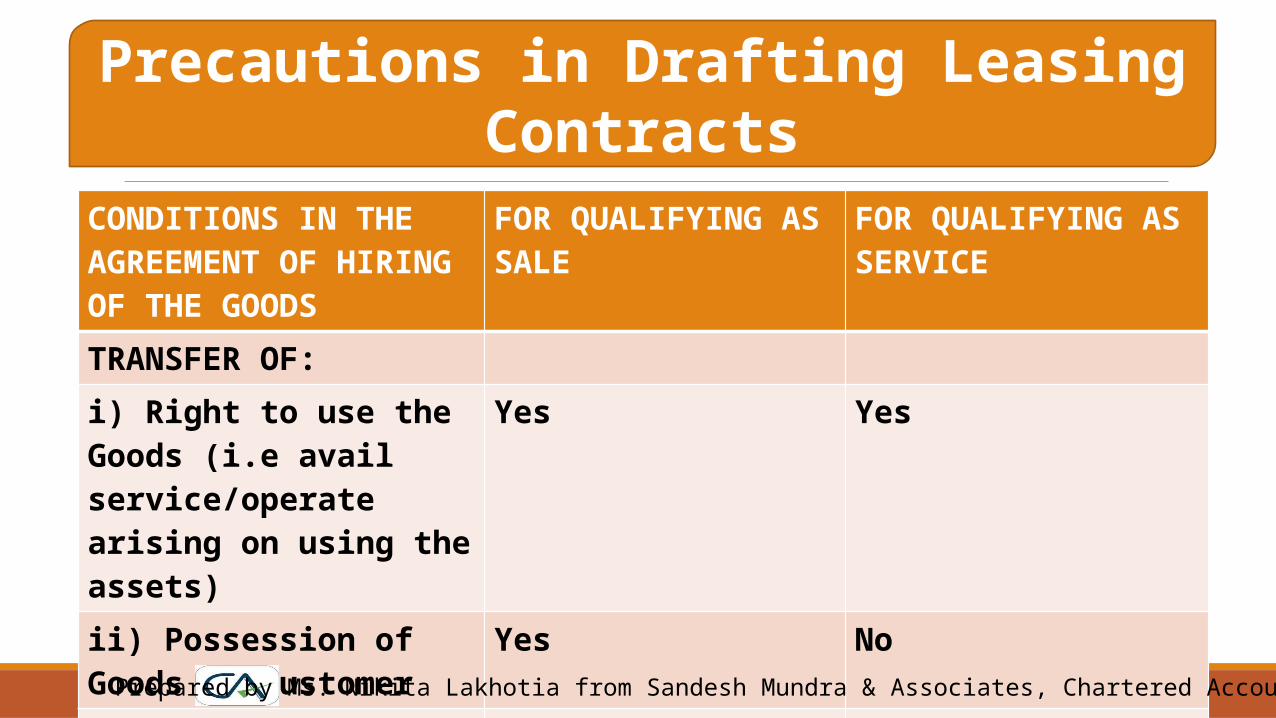

CONDITIONS IN THE AGREEMENT OF HIRING OF THE GOODS

FOR QUALIFYING AS SALE FOR QUALIFYING AS SERVICE

TRANSFER OF:i) Right to use the Goods (i.e avail service/operate arising on using the assets)

Yes Yes

ii) Possession of Goods to customer

Yes No

iii)Effective Control over Goods

Yes No

Precautions in Drafting Leasing Contracts

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

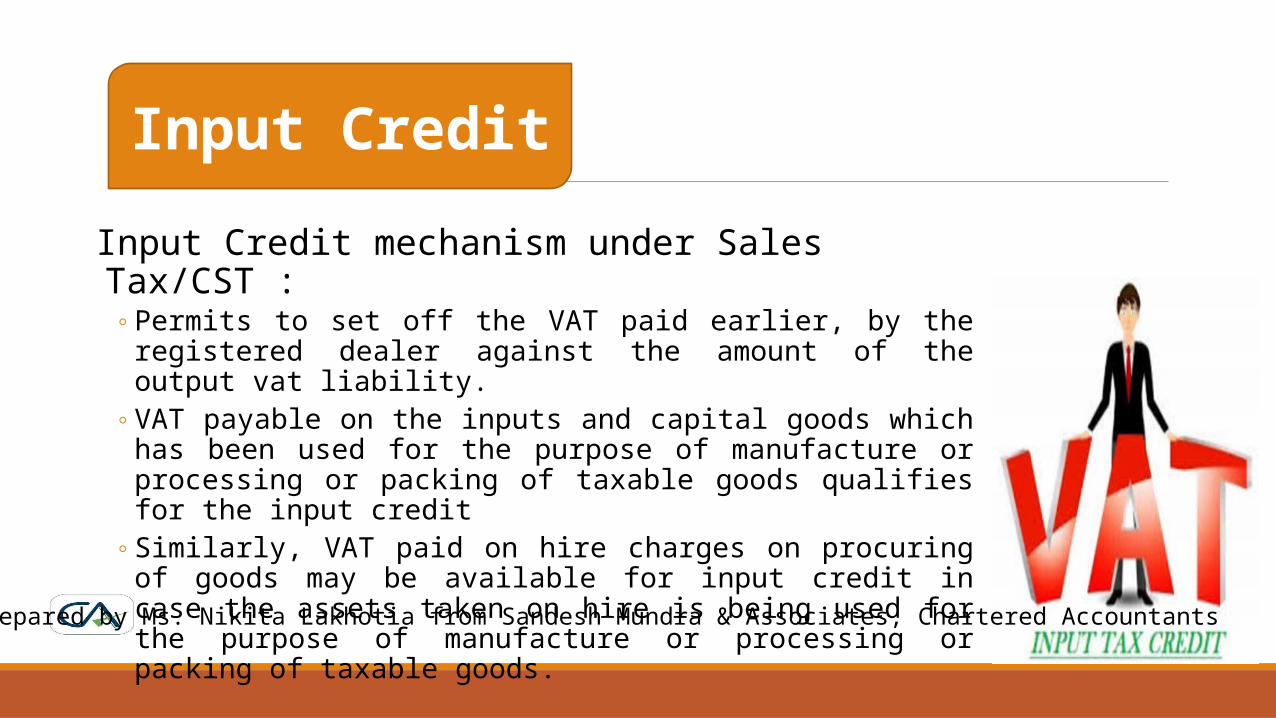

Input Credit mechanism under Sales Tax/CST :◦ Permits to set off the VAT paid earlier, by the registered dealer against

the amount of the output vat liability.◦ VAT payable on the inputs and capital goods which has been used for

the purpose of manufacture or processing or packing of taxable goods qualifies for the input credit

◦ Similarly, VAT paid on hire charges on procuring of goods may be available for input credit in case the assets taken on hire is being used for the purpose of manufacture or processing or packing of taxable goods.

Input Credit

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

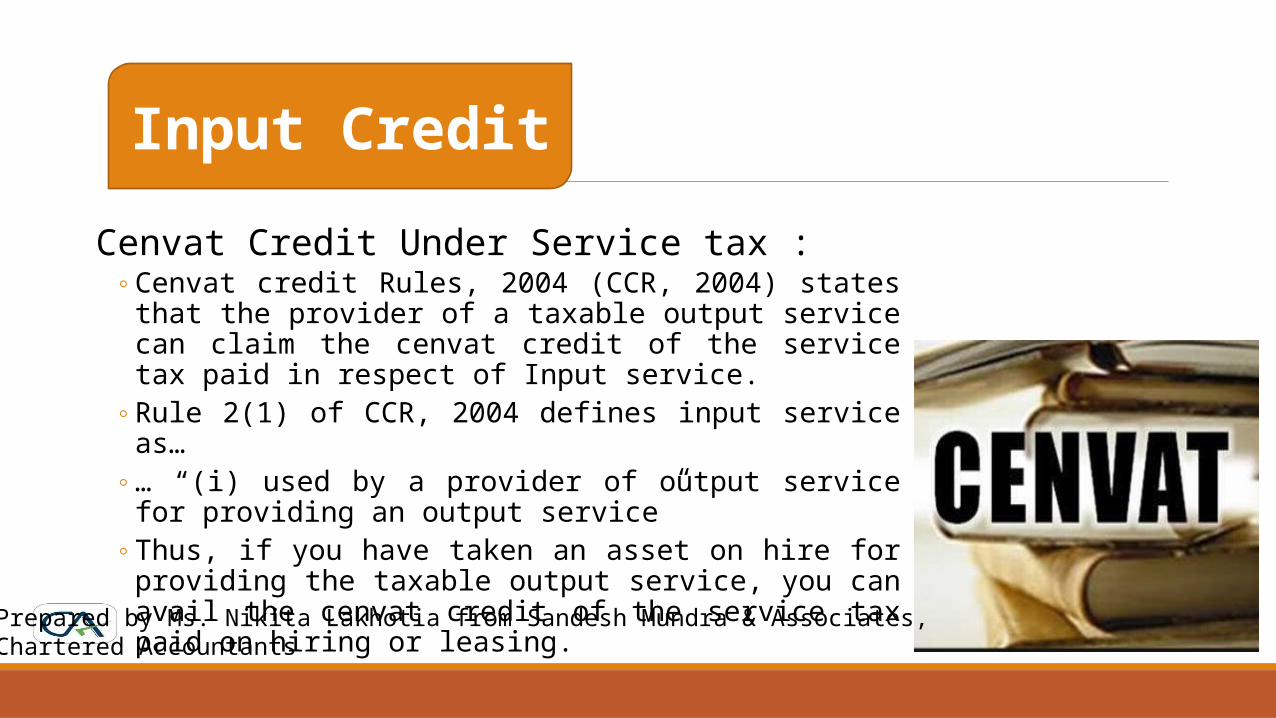

Cenvat Credit Under Service tax :◦ Cenvat credit Rules, 2004 (CCR, 2004) states that the provider of

a taxable output service can claim the cenvat credit of the service tax paid in respect of Input service.

◦ Rule 2(1) of CCR, 2004 defines input service as…◦ … “(i) used by a provider of output service for providing an

output service”◦ Thus, if you have taken an asset on hire for providing the taxable

output service, you can avail the cenvat credit of the service tax paid on hiring or leasing.

Input Credit

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Illustration 1 :◦ Company ‘A’ has 5 Road Rollers available for Hiring out.◦ Case 1 : The hiring contracts have been framed where the Road rollers

were placed at the site of the Customer, all the licenses and road permits available for operating are passed on for the exclusive use of the Customer. The Operators of those road rollers were to be paid by the Company A, but they were to operate as per the time schedule and instruction of the Customer.

◦ Case 2 : The Company a has a set of customers, who place their request for making the road rollers available to them. Company A, according to the requirement of the customers,

Illustrations

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

frame the time schedule for these road rollers, and pass on the instructions to operators to carry out operation accordingly at the customer’s site.

Solution – Case 1:◦ In case 1, the road rollers were hired out with transfer of effective control

and possession along with its right to use. Thus will qualify as deemed sale and taxable in the net of VAT.

Solution – Case 2:◦ In case 2, there has been no transfer of effective control to the customers

and hence the same will qualify as declared Service u/s 66E and service tax will be applicable on it.

Illustrations

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Illustration 2 :◦ Case 1 : VAT as Output Tax Liability

◦ Conditions :1) An asset has been taken on hire and put to use for processing

or manufacturing of taxable goods.2) The organization has an output tax liability under VAT.

◦ Solution :◦ Under this scenario, an organization can avail the input credit on

the Vat amount paid where the same has qualified as local deemed sale against the output vat liability.

Illustrations

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Whereas, if service tax has been paid than the same will not be available as Cenvat credit and the tax paid will be an additional expense on the hire charges, increasing the effective cost. In case of Central sale, the same can be advantageous against the option of service tax payable, provided C form has been permitted by Sales tax authorities of the relevant state.

Case 2 : Service tax as Output Tax Liability◦ Condition :

1) An asset has been taken on hire and put to use for rendering a taxable service2) The organization has an output service tax liability.

Solution :◦ organization can avail the Cenvat credit on the Service tax amount paid.

Illustrations

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

In GST model law, goods are defined as – “goods’’ means every kind of movable property other than actionable claim and money but includes securities, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under the contract of supply;

“services’’ is defined as “mean anything other than goods;”

Contract for transfer of right to use goods cannot be termed as contract for supply and cannot be treated as goods hence transfer of right to use goods will be treated as “Service”

Impact under GST

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants

Thank you

Prepared by Ms. Nikita Lakhotia from Sandesh Mundra & Associates, Chartered Accountants