Embed Size (px)

Citation preview

Singapore: An Increasingly Attractive

Offshore Tax Haven

Presented By:

Savi Arora

PGDM 2013-2015

Singapore

Jurisdiction Status – Independent Sovereign State

Population –

Official Language(s) – Mandarin; English; Malay; Tamil

Legal System – Anglo Saxon

Geograpgy

Singapore

Singapore’s aim is to become a major financial hub in the Asia-Pacific region, and judging by its recent performance in the wake of the global recession it appears to be achieving this goal.

Singapore achieved economic growth of 14.5% for 2010

Excellent telecommunications and good transport links

The Port of Singapore

Singapore

Singapore ranked fifth on 2013 Financial Secrecy Index.

Singapore is arguably the world’s fastest-growing centre for private wealth management.

A WeathInsight report in April 2013 expects it to overtake Switzerland by 2020 as the world’s largest offshore wealth centre.

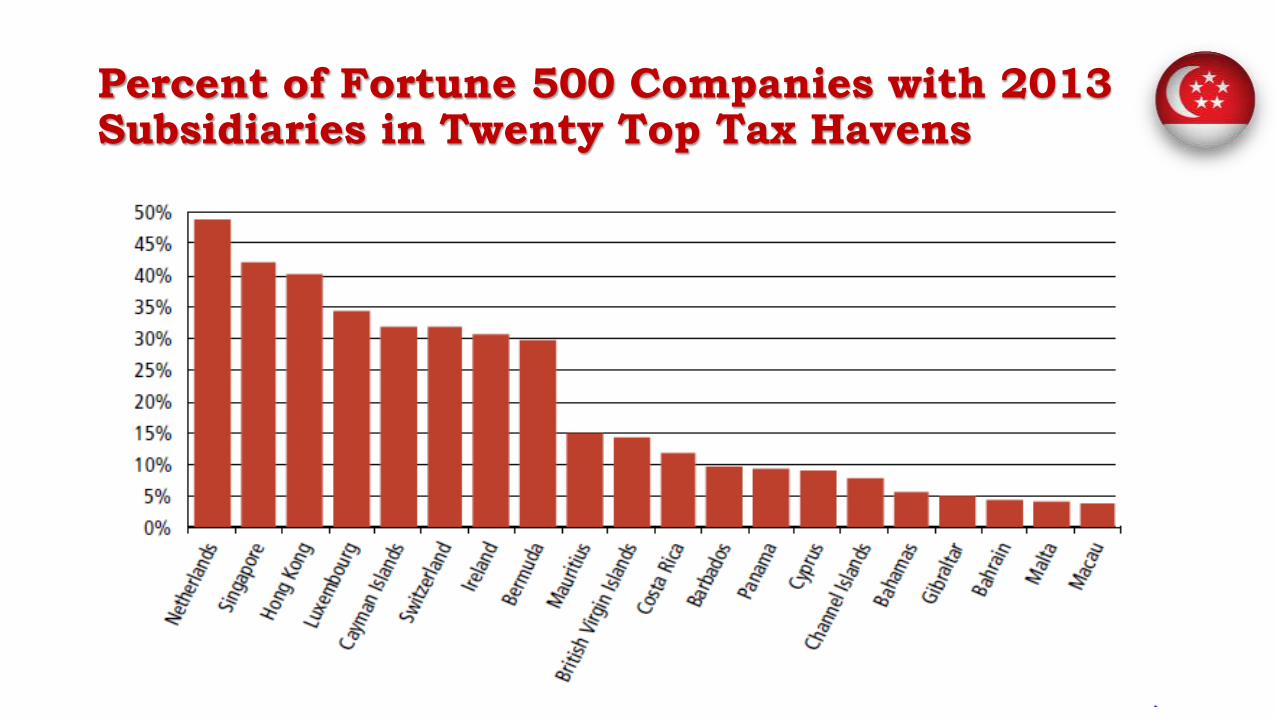

Percent of Fortune 500 Companies with 2013 Subsidiaries in Twenty Top Tax Havens

Offshore Legal and Tax Regimes

Forms Of Operation

Foreign business entities can use the following forms:

Limited liability company

Branch, subsidiary or representative office

Partnership (whether general, limited or limited liability)

Holding company

Bank

Investment fund

Offshore insurance company

Shipping company

Tax Treatment Of Operations Of Foreign Business EntitiesDomestic Corporate Taxation for the general principles of Singapore corporate taxation, which also generally apply to foreign business entities.

Note that branches located in Singapore do not qualify for tax and other incentives available to Singapore businesses.

International and regional headquarters located in Singapore can benefit from reduced corporate income tax rates of 10% and 15% respectively, compared to the standard tax rate of 17% .

Qualifying foreign investment funds that are managed by a Singapore-based fund manager are tax exempt on gains, dividends, profits and interest from designated investments such as stocks, shares and bonds.

Exchange Control

There are no foreign exchange controls in Singapore. Payments, capital transfers and remittances can be made in any currency and to any country without prior approval.

Trust LawLaw of Offshore

Trust Law

Trust law in Singapore is governed by the Trust Companies Act of 2005, which was revised in 2006.

Singapore reformed its trust laws in 2004, and since then has increased the number of trust licences issued from around 15 (before the reform) to 40 (as of March 2010).

The Singapore Trustees Association represents trust companies in Singapore, also promotes Singapore as a location for trustee services and trust administration abroad.

Banking LawLaw of Offshore

Banking Law

Banking secrecy is key to Singapore’s success as a financial centre.

Tax Information Exchange Agreements (TIEAs)

Information regarding a customer’s bank account can only be disclosed under a court order.

Any disclosure that fails to meet Singapore’s banking secrecy rules can result in a SGD78,000 fine or three years’ imprisonment.

Banking Law

A foreign offshore bank must maintain eligible assets of not less than SGD5m in Singapore at all times.

Foreign wholesale banks operating in Singapore are required at all times to maintain in Singapore the higher of an asset maintenance ratio of not less than 0.15 or eligible assets of SGD5m.

Banking law in Singapore has also allowed for the fast development of Islamic finance in the jurisdiction

Singapore has set up a financial intelligence unit to combat money laundering and the financing of terrorism.

Domestic Corporate Taxation

Scope Of Corporation Tax

A company is resident in Singapore if its central management and control of the business is exercised there.

Singapore-resident companies are generally taxed on their worldwide income;

Non-resident companies are taxed on their Singapore-source income only, which can prove attractive to international holding and trading companies.

Non-resident companies do not benefit from double tax treaties signed by the Singapore government.

Corporation Tax Rates

The corporate income tax rate is 17% (decreased from 18% prior to 2010).

There is a partial tax exemption on normal chargeable income of up to SGD300,000, as follows:

75% on the first SGD 10,000 of income; then

50% on the next SGD 290,000,

which gives a total exemption of SGD 152,500.

Corporation Tax Rates

New start-up companies benefit from full tax exemption on the first SGD 100,000 of normal chargeable income for the first three consecutive years of assessment,

plus a further 50% exemption (from tax year 2008) on the next SGD 200,000 of normal chargeable income.

Therefore, a new start-up company can qualify for a total exemption of up to SGD 200,000 in each of the first three years of business

Corporation Tax Rates

International and regional headquarters can benefit from reduced corporate income tax rates of 10% and 15% respectively.

There are also reduced corporate income tax rates and exemptions available to companies involved in shipping and maritime activities.

Branch Or Subsidiary

A Subsidiary must be registered as a private company limited by shares, with the parent company as the majority or sole shareholder.

This means the Subsidiary operates as a legal entity in its own right.

Subsidiary can benefit from the same tax exemptions and incentives as exist for other local businesses.

Branch, on the other hand, the parent is liable for the debts and obligations of the Branch, and the Branch cannot qualify for local tax exemptions and incentives.

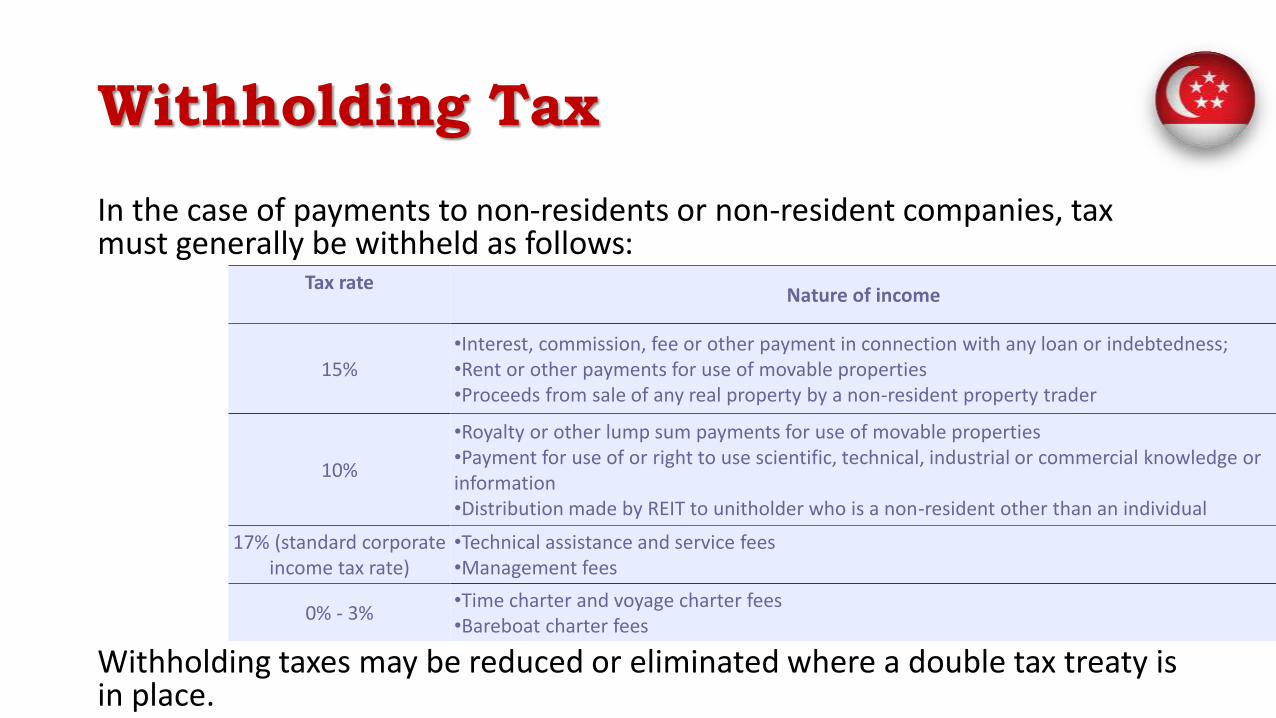

Tax rateNature of income

15%•Interest, commission, fee or other payment in connection with any loan or indebtedness;•Rent or other payments for use of movable properties•Proceeds from sale of any real property by a non-resident property trader

10%

•Royalty or other lump sum payments for use of movable properties•Payment for use of or right to use scientific, technical, industrial or commercial knowledge or information•Distribution made by REIT to unitholder who is a non-resident other than an individual

17% (standard corporate income tax rate)

•Technical assistance and service fees•Management fees

0% - 3%•Time charter and voyage charter fees•Bareboat charter fees

Withholding Tax

In the case of payments to non-residents or non-resident companies, tax must generally be withheld as follows:

Withholding taxes may be reduced or eliminated where a double tax treaty is in place.

Goods And Services Tax

Companies must register for goods and services tax (GST) if their turnover for the previous 12 months exceeds SGD 1m.

Voluntary registration is permitted.

The standard rate of GST is 7%, and applies to most sales of goods and services made in Singapore.

Exports and related international services are zero-rated. Financial services and the sale or lease of residential properties are exempt from GST.

Personal Taxation

Residence And Liability For Taxation

A person is tax resident in Singapore if he or she spends at least 183 days in a year or straddling two years in Singapore.

A foreign person who has become a Singapore Permanent Resident and has established his or her home in Singapore is resident for tax purposes.

All individuals pay tax on income earned or received in Singapore.

Personal Income Tax Rates

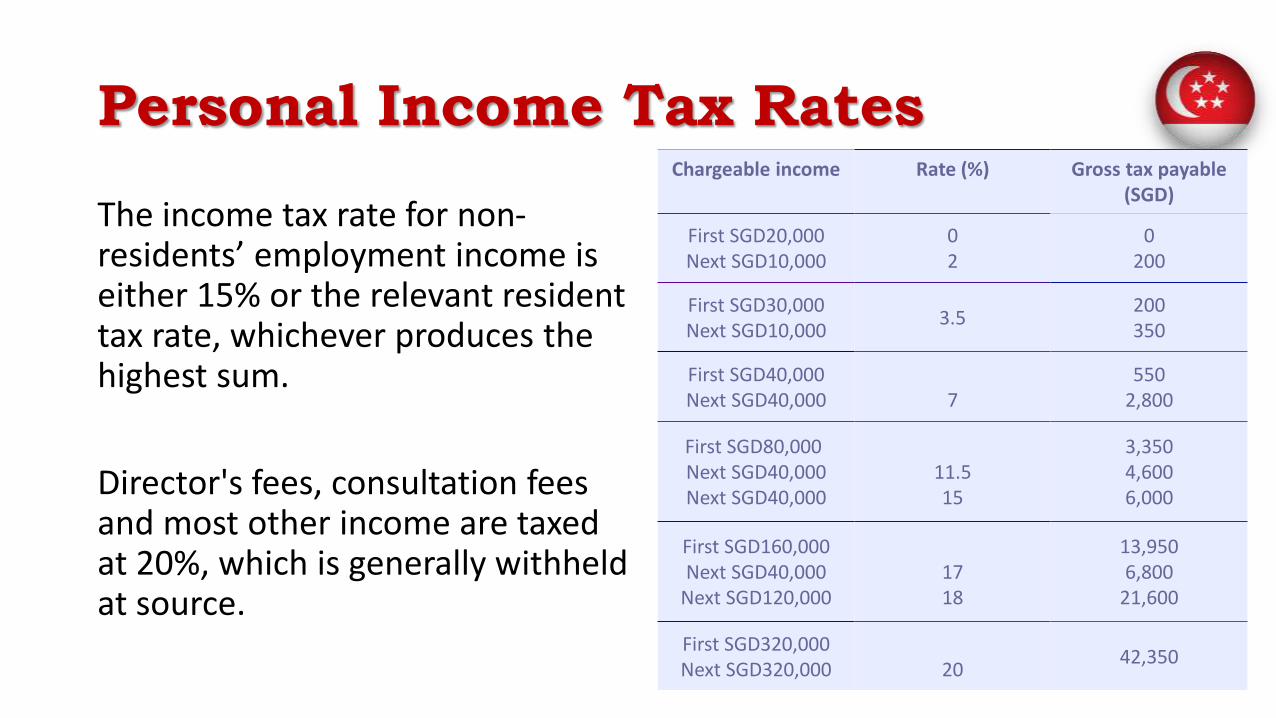

The income tax rate for non-residents’ employment income is either 15% or the relevant resident tax rate, whichever produces the highest sum.

Director's fees, consultation fees and most other income are taxed at 20%, which is generally withheld at source.

Chargeable income Rate (%) Gross tax payable (SGD)

First SGD20,000Next SGD10,000

02

0200

First SGD30,000Next SGD10,000

3.5200350

First SGD40,000Next SGD40,000 7

5502,800

First SGD80,000Next SGD40,000Next SGD40,000

11.515

3,3504,6006,000

First SGD160,000Next SGD40,000

Next SGD120,0001718

13,9506,800

21,600

First SGD320,000Next SGD320,000 20

42,350

Capital Gains Tax

Generally, capital gains realised from the sale of property in Singapore, or derived from buying and selling shares or other financial instruments, are not subject to tax.

If, however, such sale of property or buying and selling of shares and other financial instruments are regarded as a trade, the gain may be regarded as taxable income.

Estate Duty And Estate/Trust Income

There is no estate duty in Singapore.

However, assets that continue to produce income during the period one day after death until the end of the administration period are deemed to be either estate or trust income;

such income is therefore subject to income tax until the assets are sold or transferred.

Stamp Duty

Stamp duty is payable on certain executed documents relating to properties and shares, or interest in properties and shares.

Such documents include a lease, sale, purchase, gift or mortgage of property.

Liability arises once the document is executed, even if the transaction itself has been aborted.

The amount of duty payable varies according to the transaction.

For example, in the case of a mortgage, the duty is SGD4 for every SGD1,000 or part thereof, subject to a maximum duty payable of SGD500.

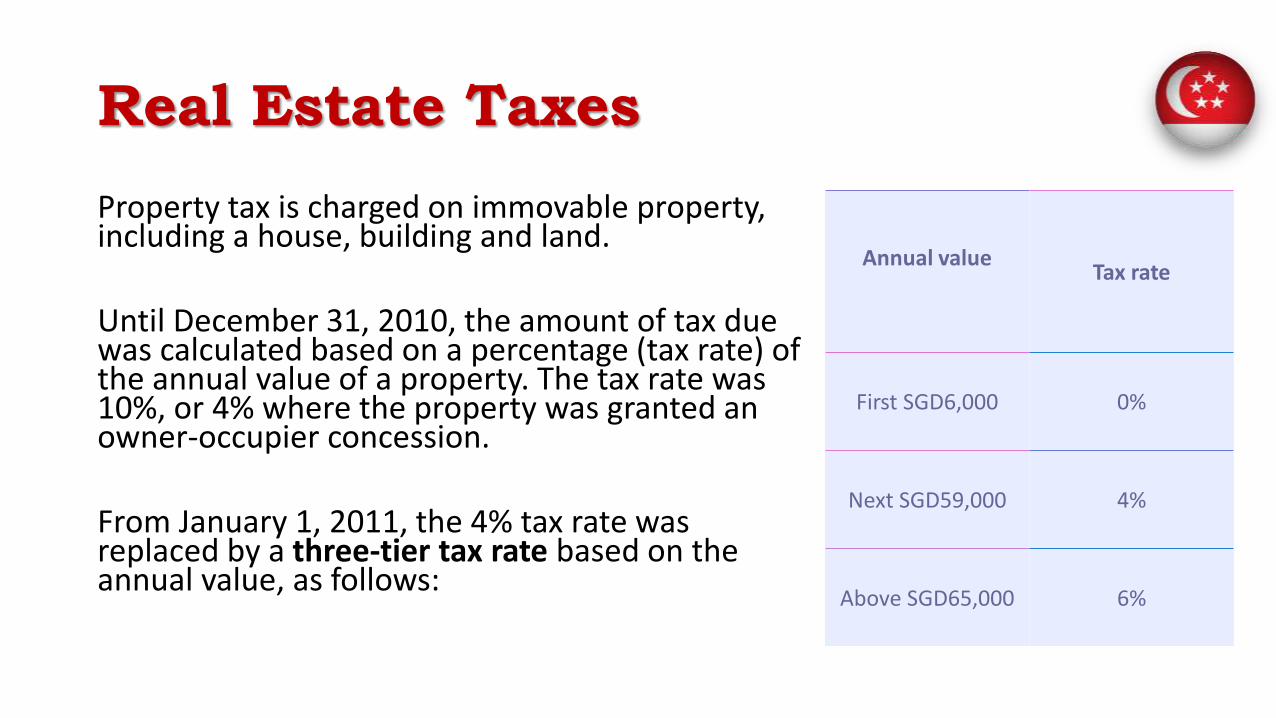

Real Estate Taxes

Property tax is charged on immovable property, including a house, building and land.

Until December 31, 2010, the amount of tax due was calculated based on a percentage (tax rate) of the annual value of a property. The tax rate was 10%, or 4% where the property was granted an owner-occupier concession.

From January 1, 2011, the 4% tax rate was replaced by a three-tier tax rate based on the annual value, as follows:

Annual valueTax rate

First SGD6,000 0%

Next SGD59,000 4%

Above SGD65,000 6%

Double Tax Treaties

Introduction

A double tax treaty allows that tax paid can be offset in one of two countries against tax payable in the other, thus avoiding double taxation.

Singapore is a signatory to double tax treaties with many countries throughout the world.

Some forms of income are exempt from tax or qualify for reduced rates. These include royalties, dividends and capital gains.

Latest Singapore Treaty Updates

Treaty Update: Singapore – Various 21 January, 2015Singapore signed DTAs with France and Uruguay on January 16, 2015, and January 15, 2015, respectively.

Treaty Update: Singapore - United Arab Emirates 04 November, 2014Singapore signed a protocol amending its DTA with the United Arab Emirates on October 31, 2014.

Treaty Update: Singapore – Various 17 September, 2014DTA protocols signed by Singapore with the Czech Republic and Kazakhstan entered into force on September 12, 2014.

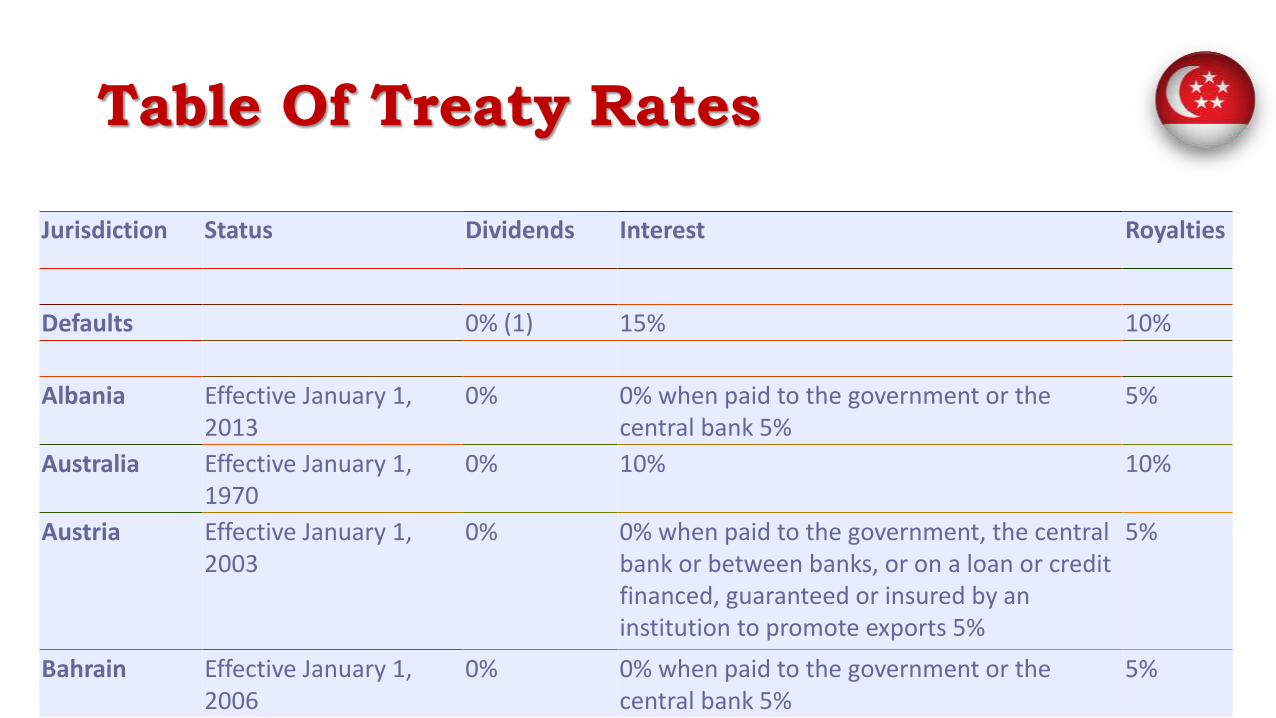

Table Of Treaty Rates

Jurisdiction Status Dividends Interest Royalties

Defaults 0% (1) 15% 10%

Albania Effective January 1, 2013

0% 0% when paid to the government or the central bank 5%

5%

Australia Effective January 1, 1970

0% 10% 10%

Austria Effective January 1, 2003

0% 0% when paid to the government, the central bank or between banks, or on a loan or credit financed, guaranteed or insured by an institution to promote exports 5%

5%

Bahrain Effective January 1, 2006

0% 0% when paid to the government or the central bank 5%

5%

Other International Agreements

Singapore has entered into a number of tax information exchange agreements, and has met the OECD's "white list" requirements.

The jurisdiction has also entered into international free trade agreements with Australia, Brunei, Chile, the European Free Trade Association, India, Japan, Jordan, New Zealand, Peru, South Korea and the USA.

Wealth Management

The Wealth Management Industry

Singapore is reputed to have the highest density of millionaires in the world.

A comparison with Switzerland is particularly apt.

Assets under management in Singapore are thought to total about US$1 trillion, as against US$3 trillion in Switzerland, but the gap is closing fast.

Shorex wealth management forum

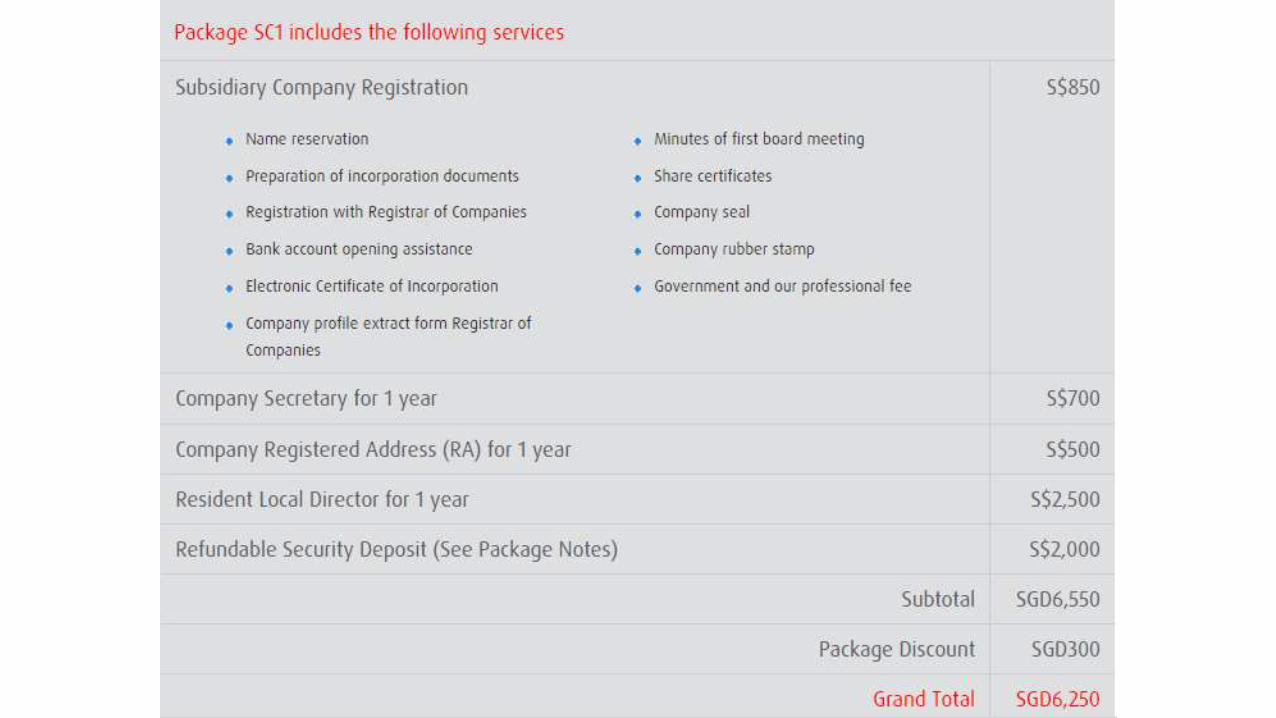

Incorporation Packages

http://www.guidemesingapore.com/