Embed Size (px)

Citation preview

Conversion Of Companies & Compliance by LLP

V.K.Tulsyan & Co.15/06/2015 1C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan 2

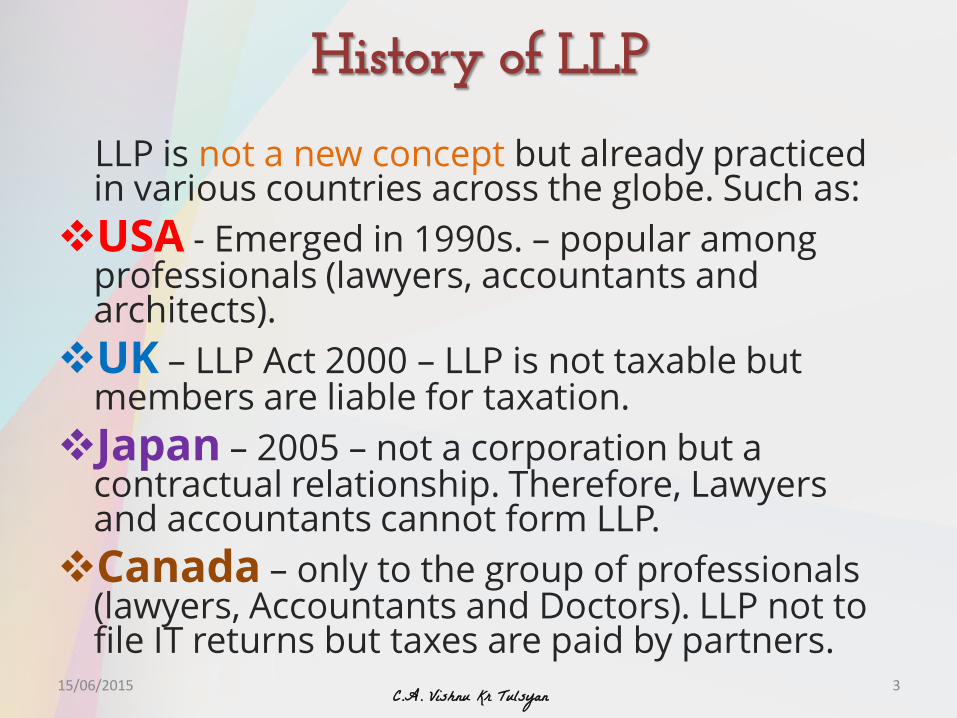

History of LLP

LLP is not a new concept but already practiced in various countries across the globe. Such as:

USA - Emerged in 1990s. – popular among professionals (lawyers, accountants and architects).

UK – LLP Act 2000 – LLP is not taxable but members are liable for taxation.

Japan – 2005 – not a corporation but a contractual relationship. Therefore, Lawyers and accountants cannot form LLP.

Canada – only to the group of professionals (lawyers, Accountants and Doctors). LLP not to file IT returns but taxes are paid by partners.

15/06/2015 3C.A. Vishnu Kr Tulsyan

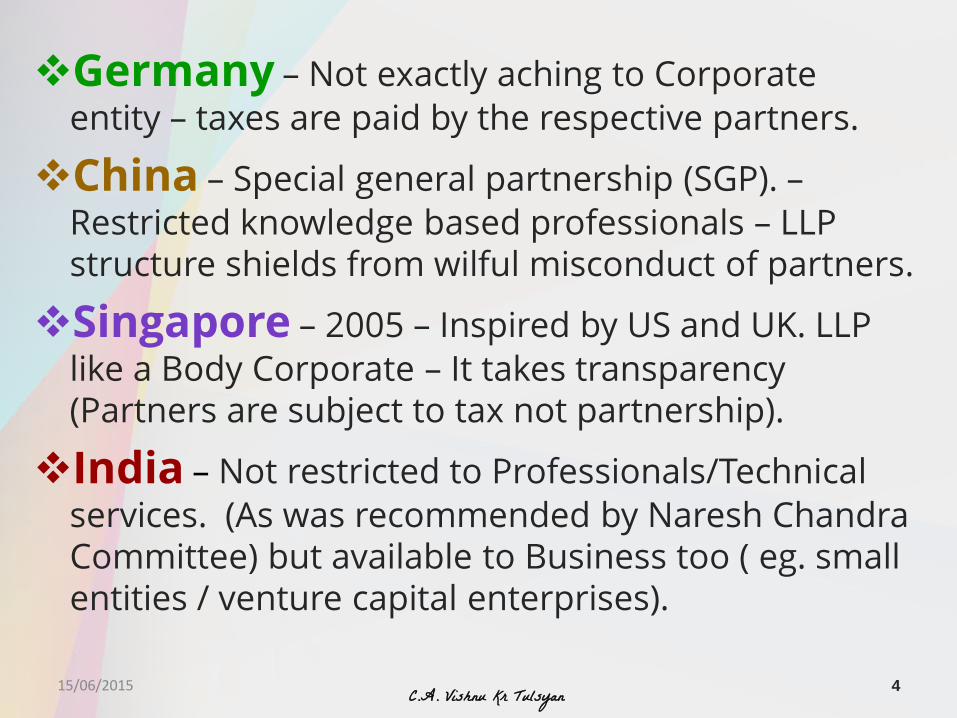

Germany – Not exactly aching to Corporate

entity – taxes are paid by the respective partners.

China – Special general partnership (SGP). –

Restricted knowledge based professionals – LLP structure shields from wilful misconduct of partners.

Singapore – 2005 – Inspired by US and UK. LLP

like a Body Corporate – It takes transparency (Partners are subject to tax not partnership).

India – Not restricted to Professionals/Technical

services. (As was recommended by Naresh Chandra Committee) but available to Business too ( eg. small entities / venture capital enterprises).

15/06/2015 4C.A. Vishnu Kr Tulsyan

What Is Limited Liability Partnership??

LLP is Relatively a new arrival that has taken thecentre stage. An LLP is a Corporate businessvehicle that combines the flexibility of aPartnership with the advantages of SeparateLegal entity. It has rightly been called theHYBRID of a Company and Partnership Firm.

15/06/2015 5C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan V.K.Tulsyan & Co.

Features

Of

LLP

Essential Features Of LLPSl.

No.LLP is……

1.BodyCorporate

A Body Corporate formed and incorporatedunder the Limited Liability Act, 2008 andregistered with the Registrar of Companies.

2.SeparateLegal Entity

A Separate Legal entity from its partners, it cansue and be sued and hold property in its ownname.

3.PersonalLiability

A Partner is not personally liable for an obligationof the LLP or misconduct of other partners. LLPliable for its full assets visais partners for theiragreed contribution.

15/06/2015 7C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan

4.Agent-PrincipalRelationship

Every partner is the agent of the LLP, but not ofother Partners.

5.PerpetualSuccession

Any change in partners does not affect theexistence rights or liabilities of the LLP.

6.Taxation Treated at par with traditional Partnerships

under the Income Tax Act, 1961.

7.Business View Point only

“Carrying on a Lawful Business with the view toProfit.” Hence, Non-profit objectives (Section 25or Section 8) of the Companies Act 1956/2013cannot form LLP.

8

Difference between LLP & Company

C.A. Vishnu Kr Tulsyan15/06/2015 9

Difference between LLP & Company

Sr. No. Limited Liability Partnership Private Limited Company

1. Governed by LLP Act,2008 Governed by Companies Act 1956 & 2013.

2.Liability of the partner limited to theextent of his capital contributed oragreed to be contributed as per LLPagreement.

Liability of shareholders is limited to theextent amount due on shares subscribed.

3. Minimum 2 partners, maximum unlimited.

Minimum 2 shareholders, maximum 200.

4.LLP agreement is the maindocument defining the activities ofLLP & provides the procedure to befollowed by LLP.

Memorandum of Association is the maindocument defining the activities of thecompany & it is compulsory for acompany to have its own articles ofassociation.

5.Managed by the partners,agreement give the power to run thebusiness to one or more partners.

Managed by the Board of Directors.

15/06/2015 10C.A. Vishnu Kr Tulsyan

Sr. No. Limited Liability Partnership Private Limited Company

6.Designated partners are liable for compliance of the LLP requirementsi.e. filing returns, Annual Accounts etc.

Secretary / Managing director / executive director / Directors / Manager is liable for compliance of Company Law requirements. ( KMP)

7.Minimum 2 Designated partners andno directors.

Minimum 2 Directors.

8.Transfer allowed . Transferee does notbecome partner automatically.

The AOA has to provide restrictions fortransfer of shares.

9.LLP can be converted into LimitedCompany by following Company Lawprocedure. In that event LLP would bewound up.

Unlisted Companies and Private LimitedCompanies can be converted into LLP.

10.Common Seal is optional. Common Seal is Compulsory.

( recent amendment has made it optional )

11.Change of registered office from onestate to another possible with very lesslegal formalities to be followed.

Change of registered office from one stateto another possible with lot of legalformalities to be followed.( Sec 17 in 1956 / Sec 13 in CA 2013)

15/06/2015 11C.A. Vishnu Kr Tulsyan

Formation of LLP

LLP

Conversion

From Existing Companies

From Existing Firms

New Formation

15/06/2015 12C.A. Vishnu Kr Tulsyan

Why Conversion Needed ?

A Registered Limited Company in India (Private or Public) has a lot of

1. Complex formalities.

2. Additional overheads for managing affairs including

mandatory Board Meeting, maintenance of

Statutory records, etc.

3. Penalty and prosecution provisions

15/06/2015 13C.A. Vishnu Kr Tulsyan

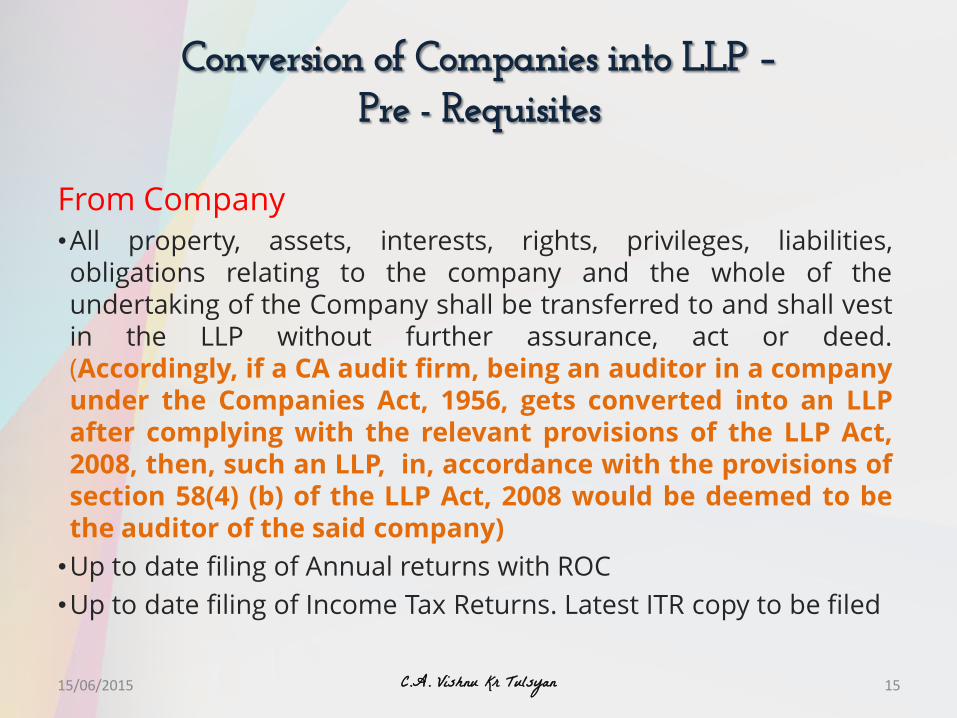

Conversion of Companies into LLP –

Pre - Requisites / Conditions

15/06/2015 C.A. Vishnu Kr Tulsyan

From Company•All property, assets, interests, rights, privileges, liabilities,obligations relating to the company and the whole of theundertaking of the Company shall be transferred to and shall vestin the LLP without further assurance, act or deed.(Accordingly, if a CA audit firm, being an auditor in a companyunder the Companies Act, 1956, gets converted into an LLPafter complying with the relevant provisions of the LLP Act,2008, then, such an LLP, in, accordance with the provisions ofsection 58(4) (b) of the LLP Act, 2008 would be deemed to bethe auditor of the said company)

•Up to date filing of Annual returns with ROC

•Up to date filing of Income Tax Returns. Latest ITR copy to be filed

15/06/2015

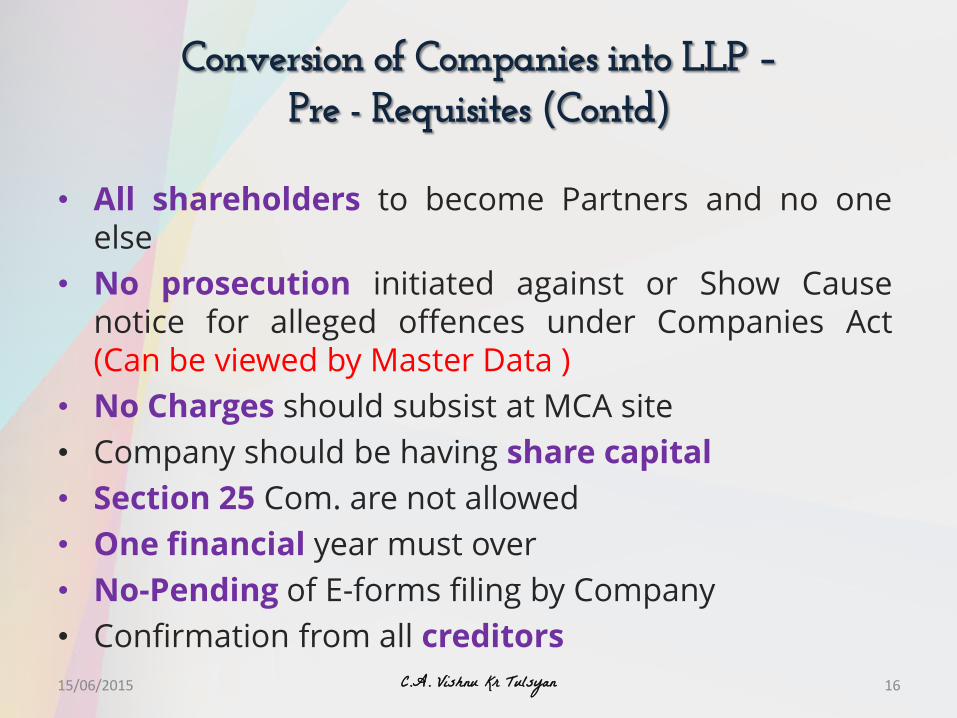

Conversion of Companies into LLP –Pre - Requisites

15C.A. Vishnu Kr Tulsyan

• All shareholders to become Partners and no oneelse

• No prosecution initiated against or Show Causenotice for alleged offences under Companies Act(Can be viewed by Master Data )

• No Charges should subsist at MCA site

• Company should be having share capital

• Section 25 Com. are not allowed

• One financial year must over

• No-Pending of E-forms filing by Company

• Confirmation from all creditors

15/06/2015

Conversion of Companies into LLP –Pre - Requisites (Contd)

16C.A. Vishnu Kr Tulsyan

Conversion of Companies into LLP –Pre - Requisites (Contd)

Things to be ensured before or at time of filing of form 18(i) Individual Consent/statement (as per Part-B of form 18) from shareholders.

(Mandatory)

(ii) Disinterested Shareholders, if any, to be provided exit option, (share acquisition/

transfer) otherwise no conversion.

(iii)Approval from any other body/ authority ( under any LAW ).

(iv) Rejection of earlier application for conversion, if any – SRN of old F18 and

reasons.

(v) Details of conviction, ruling, order, judgment of any Court- subsisting if any.

(vi) Consent of all the secured creditors with list, if any. xi) Clearance from any body/

authority, if any,

(vii) Statement of Assets and Liabilities of the company duly certified as true and

correct by the auditor & 2 Directors.

(viii) Any other information can be provided as an optional attachment.

15/06/2015 17C.A. Vishnu Kr Tulsyan

From Director• DIN -residential status must (For DP)• DIN –PAN integration (For DP)• PAN/ passport (partners)• PAN containing abbreviation are not

allowed (PAN must be in full)

15/06/2015

Conversion of Companies into LLP –Pre - Requisites / Conditions

18C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan V.K.Tulsyan & Co.

Conversion of Companies into LLP

Procedure

From Company• Board Resolution for conversion into LLP• Approved DIN (Designated Identification Number) is a pre-

requisite for incorporation process.• Filing of form 1 –Application for Name availability (Approval)

Documents required for incorporation of an LLP• Drafting of a LLP Agreement vetted by Promoters• Application for conversion shall be made in e-Form 18• Form 2 (Statement by Promoter)• Form 3 (Information regarding the LLP Agreement)• Form 14 (Conversion intimation to ROC)• Subscription sheet signed by the promoters• LLP Agreement should be duly stamped• Proof of Address of Registered Office

15/06/2015

Conversion of Companies into LLP -Procedure

20C.A. Vishnu Kr Tulsyan

Conversion of Companies into LLP Procedure

Filing Form 3• Within 30 days of date of registration of the LLP• With signed LLP agreement containing Changes (on Stamp

Paper)

Filing of form 14• Within 15 days of the date of registration of the LLP with

ROC• Attachment- LLP Conversion Certificate (result of F-18)• Digitally signed by one of the directors in the company

before conversion

15/06/2015 21C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan V.K.Tulsyan & Co.

Merits and

DemeritsConversion of

Companies into LLP

Conversion of Companies into LLPMerits (Overall)

Exemption from Dividend taxation and DDT

Exemption from benefit and perquisite taxation

Lower rate of taxation

Deemed Speculation loss not applicable

Restriction u/s. 79 for c/f of loss inapplicable

MAT u/s. 115JB not applicable to LLP

S. 46 as applicable to Liquidation not to apply

Wealth tax not applicable on LLP

Assigning realistic values

15/06/2015 23C.A. Vishnu Kr Tulsyan

No Limit on number of shareholders/partnersMinimal Compliance Level & Cost effective

model Automatic transferNo Stamp Duty (but it’s a grey area)No Capital Gain Tax STCG also exempt Continuation of Brand Value Carry Forward and Set off Losses and

Unabsorbed Depreciation Exemption for partners u/s. 10(2A)

15/06/2015

Conversion of Companies into LLPMerits (Contd-)

24C.A. Vishnu Kr Tulsyan

MAT credit not available

Restriction on interest and remuneration

Applicability of s. 78 for c/f losses

Applicability of s. 45(4) on distribution of capital assets

Wealth tax on partners

Period of holding for partners’ share extended

Applicability of AMT u/s. 115JC

Company specific deduction not available

Lower rate of incentives under chapter VI-A

15/06/2015

Conversion of Companies into LLPDe-Merits

25C.A. Vishnu Kr Tulsyan

Stringent compliance for exemptionExposure to withdrawal u/s. 47(4A)Lapse of some unabsorbed allowancesUnabsorbed losses under non business headsClaim for deduction by successor - s. 801B(12)No specific exemption u/s 47 for amalgamation, demergerNo specific exemption provision for exemption on reconversion

15/06/2015

Conversion of Companies into LLPDe-Merits

26C.A. Vishnu Kr Tulsyan

Conversion of Company into LLP

Post Conversion Issues

Obtain

Fresh IT PAN/ TAN.

New Bank Account.

All other applicable Licenses like Service Tax, VAT, Excise, Customs, IEC etc.

Maintain

Formerly known as “…………Private Limited”converted and registered as LLP on 31-03-2013vide LLPIN:……. with limited liability- for 12 months.

15/06/2015 27C.A. Vishnu Kr Tulsyan

Conversion of Company into LLP Taxation Advantages

Post Conversion Effect ( In case of Company Conversion)Criteria as per IT• Carry forward loss & Accumulated Depreciation next 8 yrs• Tax Saving as per illustration (Surcharge)• Unlimited no. of partners• Last 3 years average turnover of Company should be less than

60 lakhs. (eligibility)• No consideration to partners for conversion• All assets of company to be assets of LLP• All shareholders to be partners of LLP• Accumulated profits on date of Conversion are not allowed for

distribution for next 3 years from date of conversion. (Post)• 50% of shareholders of Company should continue to hold for

next 5 years .(Post)• The shareholder of the company shall not receive any

consideration directly or indirectly except profit sharing in LLP

15/06/2015 28C.A. Vishnu Kr Tulsyan

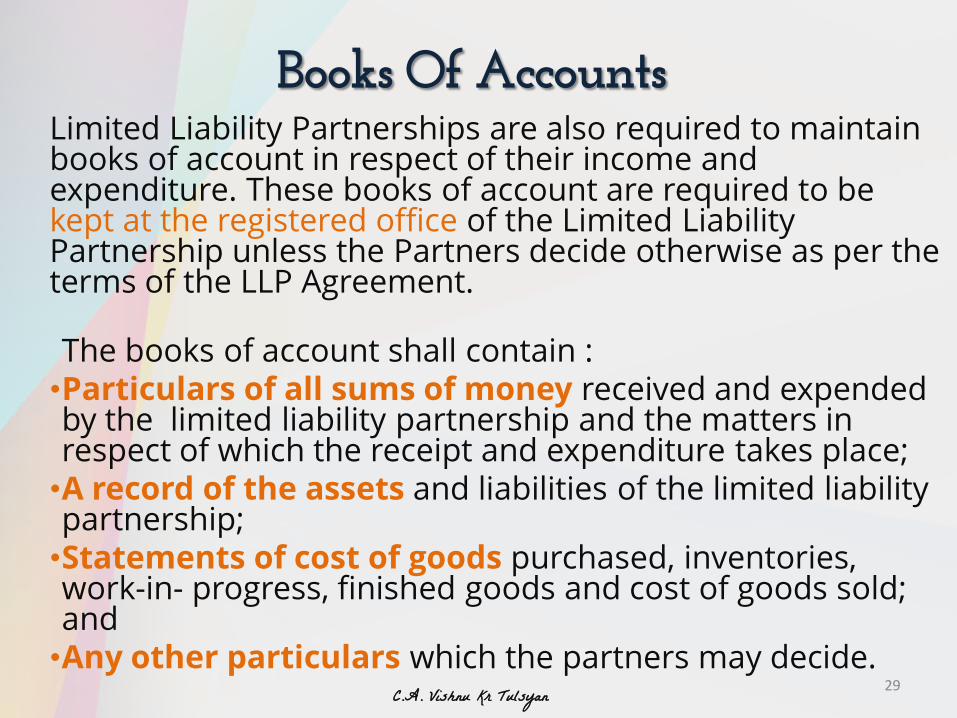

Books Of AccountsLimited Liability Partnerships are also required to maintain books of account in respect of their income and expenditure. These books of account are required to be kept at the registered office of the Limited Liability Partnership unless the Partners decide otherwise as per the terms of the LLP Agreement.

The books of account shall contain :•Particulars of all sums of money received and expended by the limited liability partnership and the matters in respect of which the receipt and expenditure takes place;

•A record of the assets and liabilities of the limited liability partnership;

•Statements of cost of goods purchased, inventories, work-in- progress, finished goods and cost of goods sold; and

•Any other particulars which the partners may decide.29C.A. Vishnu Kr Tulsyan

Methods of AccountingLimited Liability Partnerships are required to maintain their Books ofAccount on cash basis or accrual basis and according to the doubleentry system of accounting. Currently the accounting standards arenot applicable to LLP.

Financial StatementsLLP is required to prepare the following statement annually:

•A Balance Sheet – to give a true and fair view of the State of affairs of the LLP as at the end of financial year.

•An Income and Expenditure Account – to give a true and fair view of the Income and Expenditure of the LLP for a particular Financial Year.

•Statement of Solvency: It is in form of declaration by the LLP, that it will be able to pay its debts in full as they become due in the normal course of business.

15/06/2015 30C.A. Vishnu Kr Tulsyan

Statutory Audit Of LLP

•Limited Liability Partnership whose contribution exceed Rs. 25 Lakhs or the Limited Liability Partnership whose turnover exceed Rs. 40 lakhs are required to annually get their accounts audited by any Chartered Accountant in practice.

•The LLP, which are not required to get their accounts audited, are required to In furnish a statement in the Statement of Account and Solvency by the partners to the effect that the partners acknowledge their responsibilities for complying with the requirements of the Act and the Rules with respect to preparation of books of account

•The Designated Partners responsible for the compliances of LLP will appoint the auditor also. However if the designated partner fails to appoint the auditor then the partners may appoint the auditor.

15/06/2015 31C.A. Vishnu Kr Tulsyan

Tax Audit Of LLP

Where the total sales, turnover or gross receiptsof the business exceed Rs. 100 lakhs (Rs. 25lakhs in case of profession) in any financial yearof the company, than a the accounts shall beaudited by chartered accountant and tax auditreport based on the same, is required to besubmitted to the tax authorities’ along with theReturn of Income of the business.

15/06/2015 32C.A. Vishnu Kr Tulsyan

Appointment of Auditors By DPs15/06/2015 C.A. Vishnu Kr Tulsyan

Appointment of Auditors By DPs

LLPs have to appoint Auditor for each financial year unless itis exempt from audit. It can appoint more than one auditorsfor the purpose.

The Designated Partners may appoint an Auditor:

a)At any time for the first financial year. However, theappointment has to be made before the end of the firstfinancial year

b)Within 30 days before the end of Financial year

c)To fill a casual vacancy in the office of Auditor

d)To fill up the vacancy caused by removal of an Auditor

If the designated partners have not appointed the auditor asstated above, then the partners may appoint the Auditor.

Only Chartered Accountants can be appointed as Auditor.15/06/2015 34C.A. Vishnu Kr Tulsyan

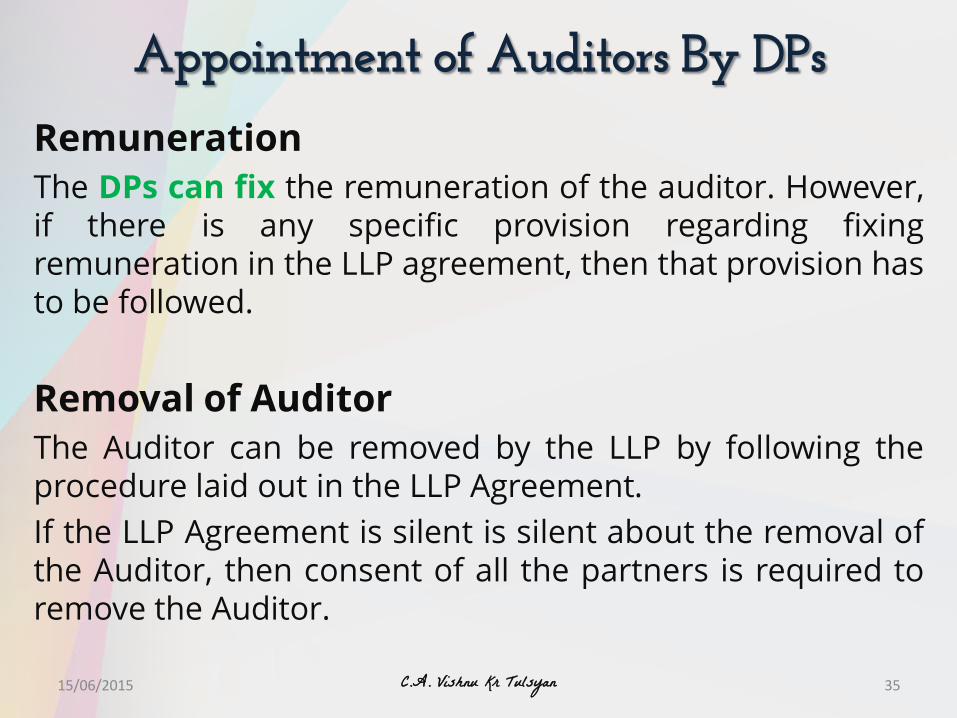

Remuneration

The DPs can fix the remuneration of the auditor. However,if there is any specific provision regarding fixingremuneration in the LLP agreement, then that provision hasto be followed.

Removal of Auditor

The Auditor can be removed by the LLP by following theprocedure laid out in the LLP Agreement.

If the LLP Agreement is silent is silent about the removal ofthe Auditor, then consent of all the partners is required toremove the Auditor.

15/06/2015

Appointment of Auditors By DPs

35C.A. Vishnu Kr Tulsyan

PENALTIES

Any LLP which fails to comply with theabove stated requirements for appointmentof Auditors shall be punishable with fineONLY of

1. Rs. 25,000 but not exceeding Rs. 5,00,000.

2. Every DP be punishable with fine - not beless than Rs. 10,000 but exceeding Rs.1,00,000.

15/06/2015 36C.A. Vishnu Kr Tulsyan

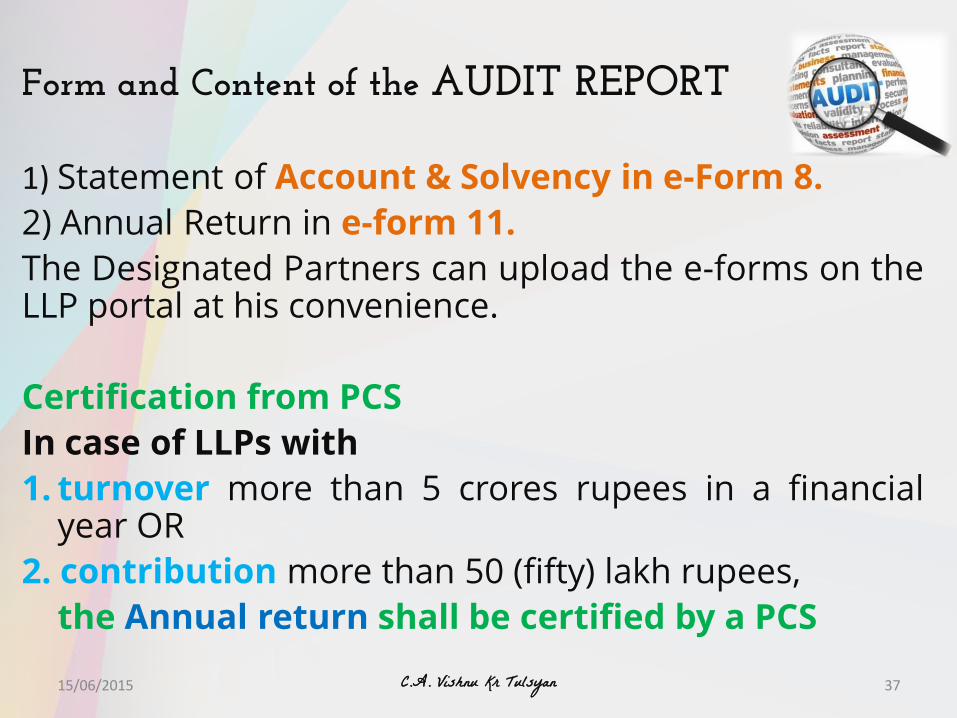

Form and Content of the AUDIT REPORT

1) Statement of Account & Solvency in e-Form 8.

2) Annual Return in e-form 11.

The Designated Partners can upload the e-forms on theLLP portal at his convenience.

Certification from PCS

In case of LLPs with

1. turnover more than 5 crores rupees in a financialyear OR

2. contribution more than 50 (fifty) lakh rupees,

the Annual return shall be certified by a PCS

15/06/2015 37C.A. Vishnu Kr Tulsyan

Filing Annual Accounts, Annual Return & Income Tax Returns

Filing Annual Accounts

All LLPs - FORM 8 to be filed with the registrar of LLPs on orbefore 30th October every year.

Filing Annual Return

Every LLP - Annual Return in FORM 11 to the Registrar within60 days from the closure of financial year i.e. the AnnualReturns has to be filed on or before 30th May every year.

Filing Income Tax Returns

1. In case where Audit is required - 30th September everyyear,

2.Wherein business which do not fall under the Auditrequirements criteria will have to file Income Tax Returnson or before 31st July every year.

38C.A. Vishnu Kr Tulsyan

Penalty for NON - FILING

If there is delay in filing form No. 8 and11of LLP - Rs. 100 per day till it iscomplied. You cannot close or wind upyour LLP without filing Annual Accounts.

So, if it is not filed on time, your LLP turnsinto unlimited statutory liability till the dayit is complied.

15/06/2015 39C.A. Vishnu Kr Tulsyan

15/06/2015 C.A. Vishnu Kr Tulsyan

Closing of LLPAny LLP can close down its business by adopting any of the following two ways:•Declaring the LLP as Defunct•Winding up of LLP

Declaring the LLP as Defunct:In case the LLP wants to close down its business or where it is notcarrying on any business operations for the period of one year ormore, it can make an application to the Registrar for declaring the LLPas defunct and removing the name of the LLP from its register ofLLP’s.E-Form 24 is required to be filed for striking off the name of LLP.Similarly, Registrar also has the power to strike off any defunct LLPafter satisfying himself of the need to strike off and has reasonablecause. However, in this case, registrar has to send a notice to the LLPof his intention and request to send their representation within onemonth from the date of the notice. The Registrar shall publish suchnotice or content of the application made by the LLP on its website fora period of one month for the information of the general public. Incase no reply is received within the mentioned period, registrar maystrike off the name of LLP.

15/06/2015 41C.A. Vishnu Kr Tulsyan

Winding Up & Dissolution of LLP

The winding up of a limited liability partnership may be eithervoluntary or by the Tribunal and limited liability partnership, sowound up may be dissolved.

1. Voluntary Winding up

2. Compulsory winding upA limited liability partnership may be compulsorily wound up by the Tribunal:

If the limited liability partnership decides that limited liability partnership be wound up by the Tribunal;

If, for a period of more than six months, the number of partners of the limited liability partnership is reduced below two;

If the limited liability partnership is unable to pay its debts; If the limited liability partnership has acted against the interests of the

sovereignty and integrity of India, the security of the State or public order; If the limited liability partnership has made a default in filing with the

Registrar the Statement of Account and Solvency or annual return for any five consecutive financial years; or

If the Tribunal is of the opinion that it is just and equitable that the limited liability partnership be wound up.

15/06/2015 42C.A. Vishnu Kr Tulsyan

FORMS

Form 1 Form 2 Form 3 Form 4 Form 8

Form 11 Form 14 Form 17 Form 18 Form 24

C.A. Vishnu Kr Tulsyan 4315/06/2015

Thank You!

CS Vishnu Kr Tulysan+91 98310 54180 / [email protected]

www.vktulsyan.com/

CA Vishnu Kr Tulsyan is practicing Chartered Accountant & Company Secretary with over 15 years of exhaustive experience in the filed of Finance, Accounts, Corporate Compliance & Advisory, Regulatory Changes Implementation.

44C.A. Vishnu Kr Tulsyan