Embed Size (px)

Citation preview

THE INDIAN PARTNERSHIP ACT ,1932

PARTNERSHIP ACT & COMPANY LAWGROUP 3

THE INDIAN PARTNERSHIP ACT ,1932 The Indian Partnership Act was enacted in

1932.

The Act came into force on 1st October,1932.

Act extend to the whole of India except the state of Jammu Kashmir.

Before the passing of this act, the law relating to the partnership was contained in chapter XI of the Indian Contract Act, 1872 .

Chapter XI of the Act was not exhaustive, hence the partnership act was enacted in 1932.

The Indian Partnership Act is mainly based on the English Law.

Many of the general principles of the contract in the Indian Contract Act, continue to be applicable in Partnership transactions such as fee consent, legality of object etc.

DEFINITION OF PARTNERSHIP ACT

Section 4 para 1 of the Indian Partnership Act 1932, defines partnership as:“Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all”.

ESSENTIAL ELEMENTS OF A PARTNERSHIP

There must be a contract. Between two or more persons. Who agree to carry on business. With the object of sharing profits. The business must be carried on by all or

any of them acting for all.

PARTNERS

Persons entered into partnership individually. Two essential conditions to be fulfilled by a

person to become a partner are:(1)There must be an agreement to share the

profits of the business,(2) the business must be carried on by all or any of

the partners acting for all.

FIRM

Collectively a firm.

A collective name for the members composing a firm.

A firm cannot be a partner in another firm.

Under Law of Partnership, a firm has no legal existence apart from its partners.

FIRM NAME

The name under which the business is carried.

A firm name may be personal or impersonal, singular or plural, imaginary or real, and need not contain the name of any existing partner.

JOINT HINDU FAMILY BUSINESS Comes into existence as per the Hindu

Inheritance Act of India.

This form of business found only in India.

All members of the Hindu Undivided Family(HUF) own the business jointly.

The affairs of the business are managed by head of the family called “Karta”. All other members are called “coparceners”.

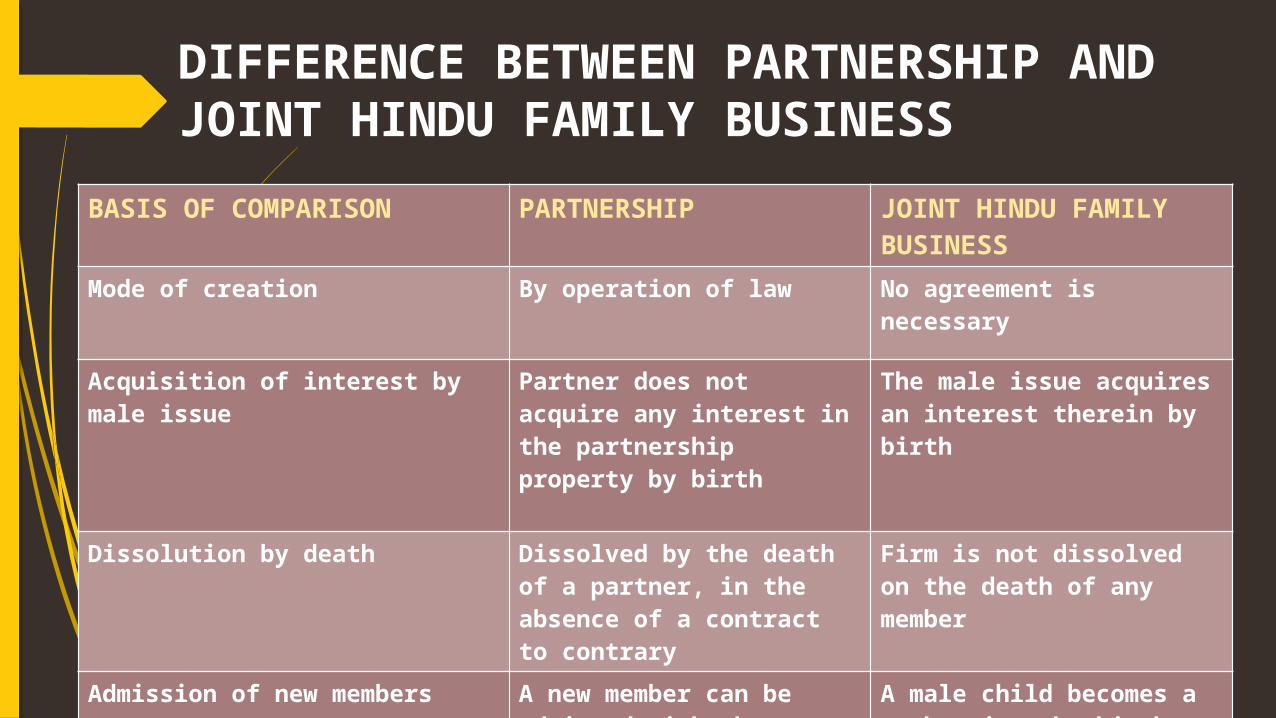

DIFFERENCE BETWEEN PARTNERSHIP AND JOINT HINDU FAMILY BUSINESS

BASIS OF COMPARISON PARTNERSHIP JOINT HINDU FAMILY BUSINESS

Mode of creation By operation of law No agreement is necessary

Acquisition of interest by male issue

Partner does not acquire any interest in the partnership property by birth

The male issue acquires an interest therein by birth

Dissolution by death Dissolved by the death of a partner, in the absence of a contract to contrary

Firm is not dissolved on the death of any member

Admission of new members A new member can be admitted with the consent of other parties

A male child becomes a member just by birth

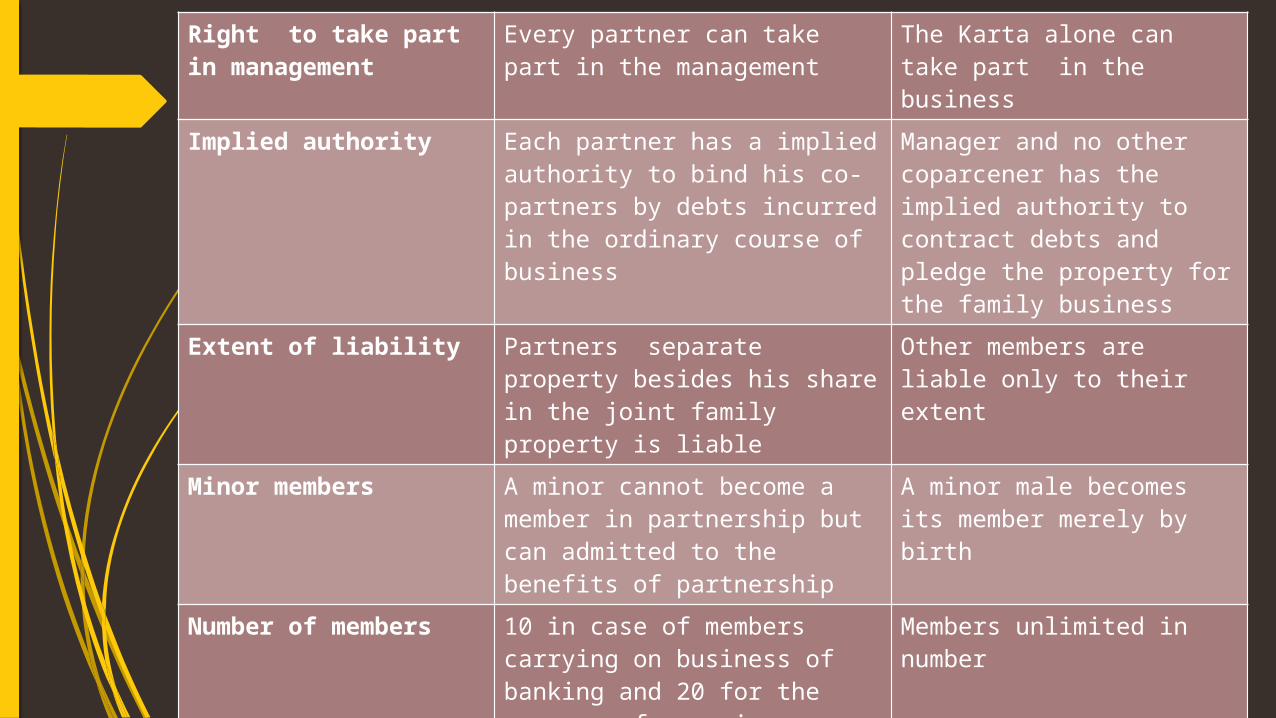

Right to take part in management

Every partner can take part in the management

The Karta alone can take part in the business

Implied authority Each partner has a implied authority to bind his co-partners by debts incurred in the ordinary course of business

Manager and no other coparcener has the implied authority to contract debts and pledge the property for the family business

Extent of liability Partners separate property besides his share in the joint family property is liable

Other members are liable only to their extent

Minor members A minor cannot become a member in partnership but can admitted to the benefits of partnership

A minor male becomes its member merely by birth

Number of members 10 in case of members carrying on business of banking and 20 for the purpose of carrying on any other business

Members unlimited in number

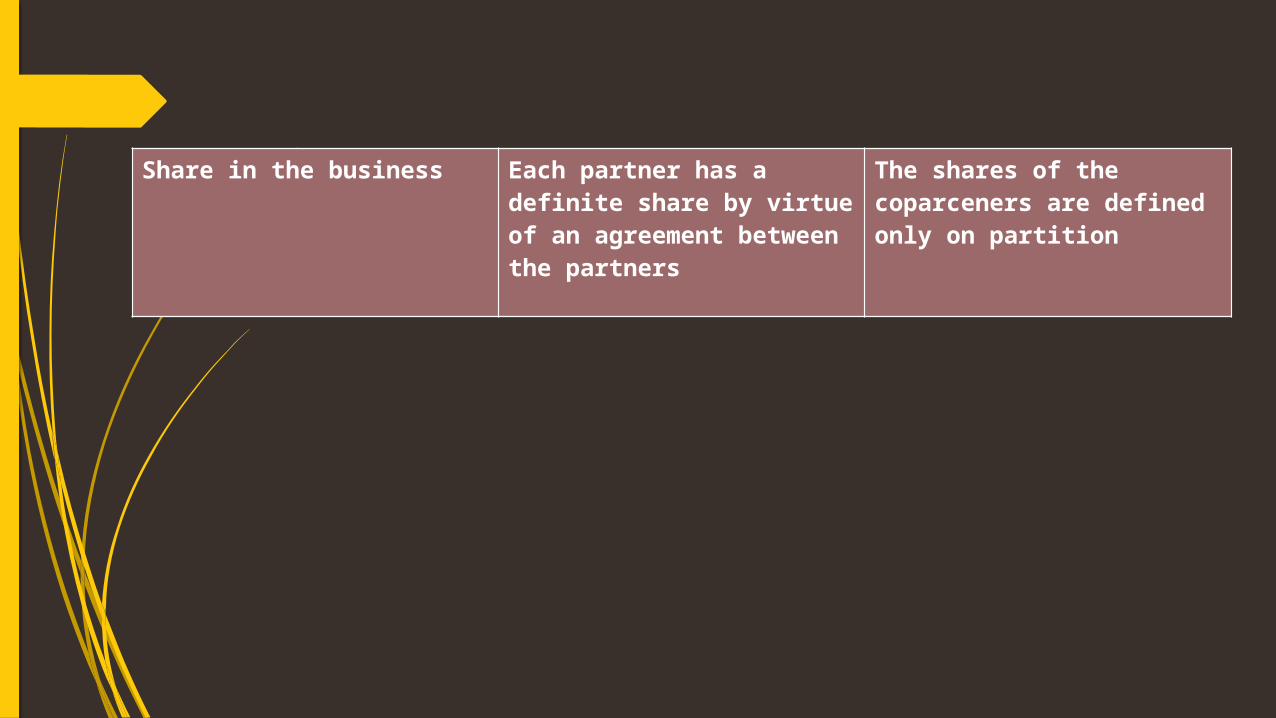

Share in the business Each partner has a definite share by virtue of an agreement between the partners

The shares of the coparceners are defined only on partition

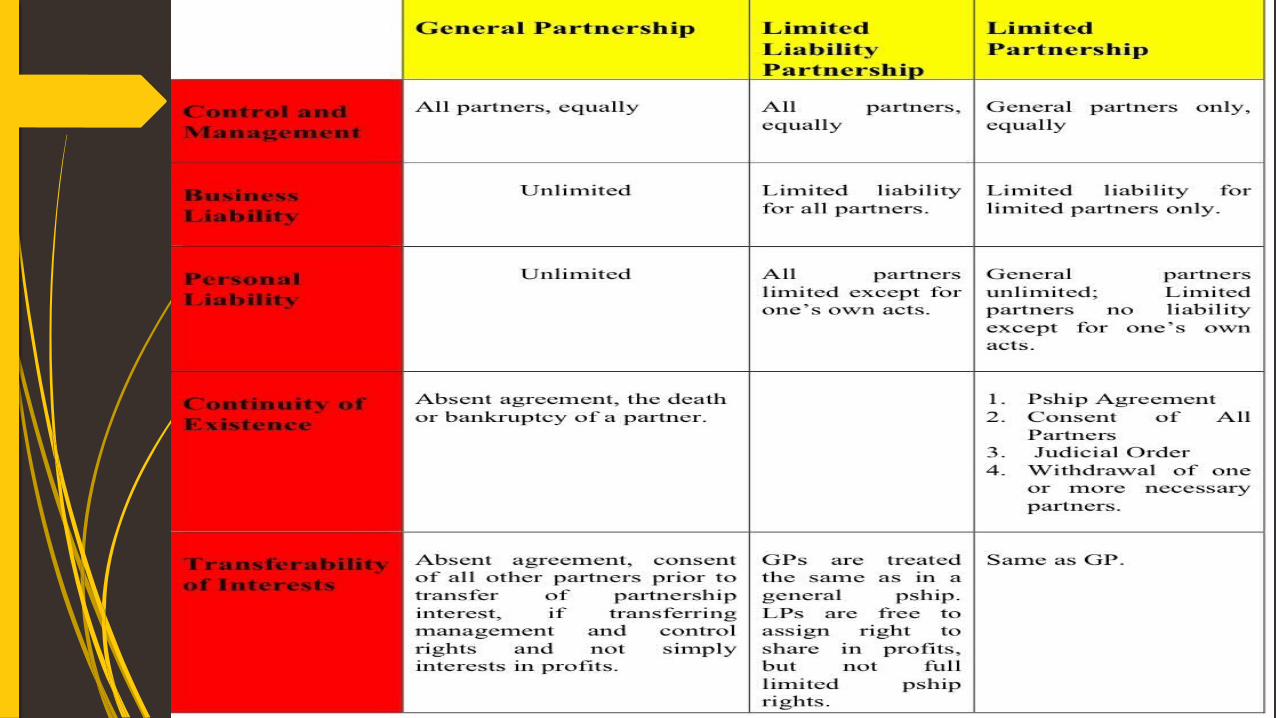

Types of Partnership

General Partnership Limited Partnership Limited Liability Partnership

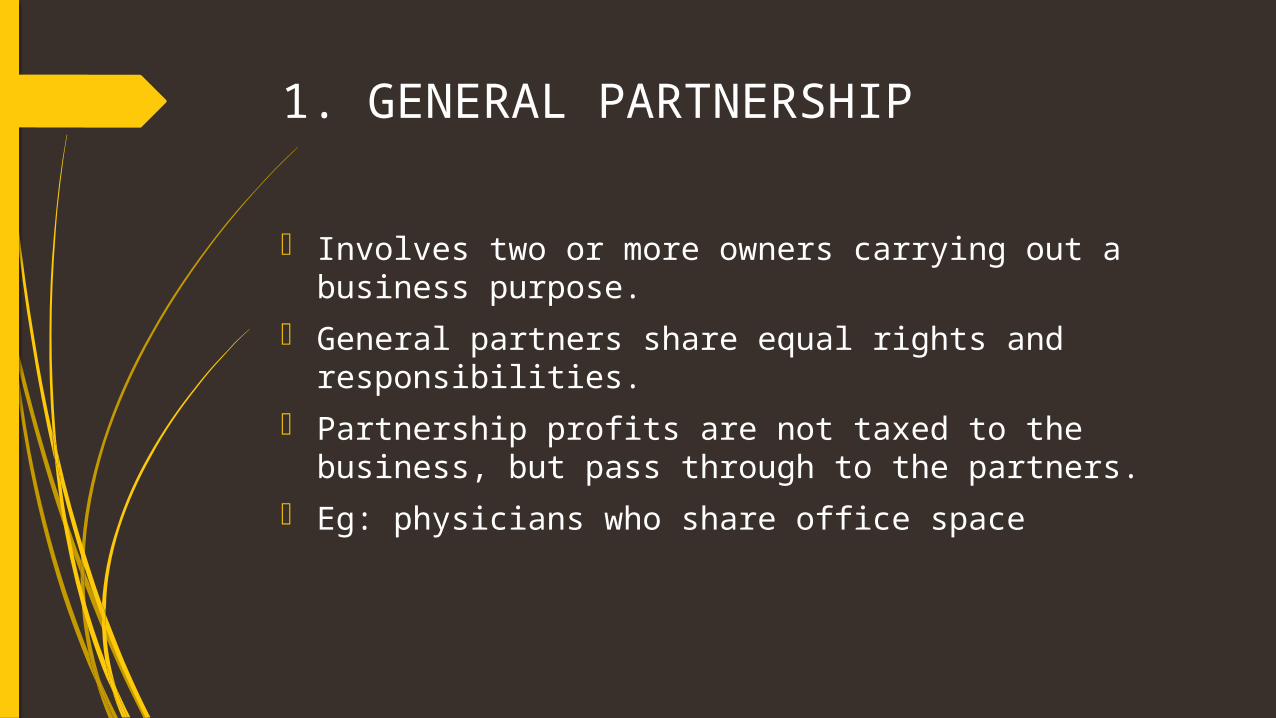

1. GENERAL PARTNERSHIP

Involves two or more owners carrying out a business purpose.

General partners share equal rights and responsibilities.

Partnership profits are not taxed to the business, but pass through to the partners.

Eg: physicians who share office space

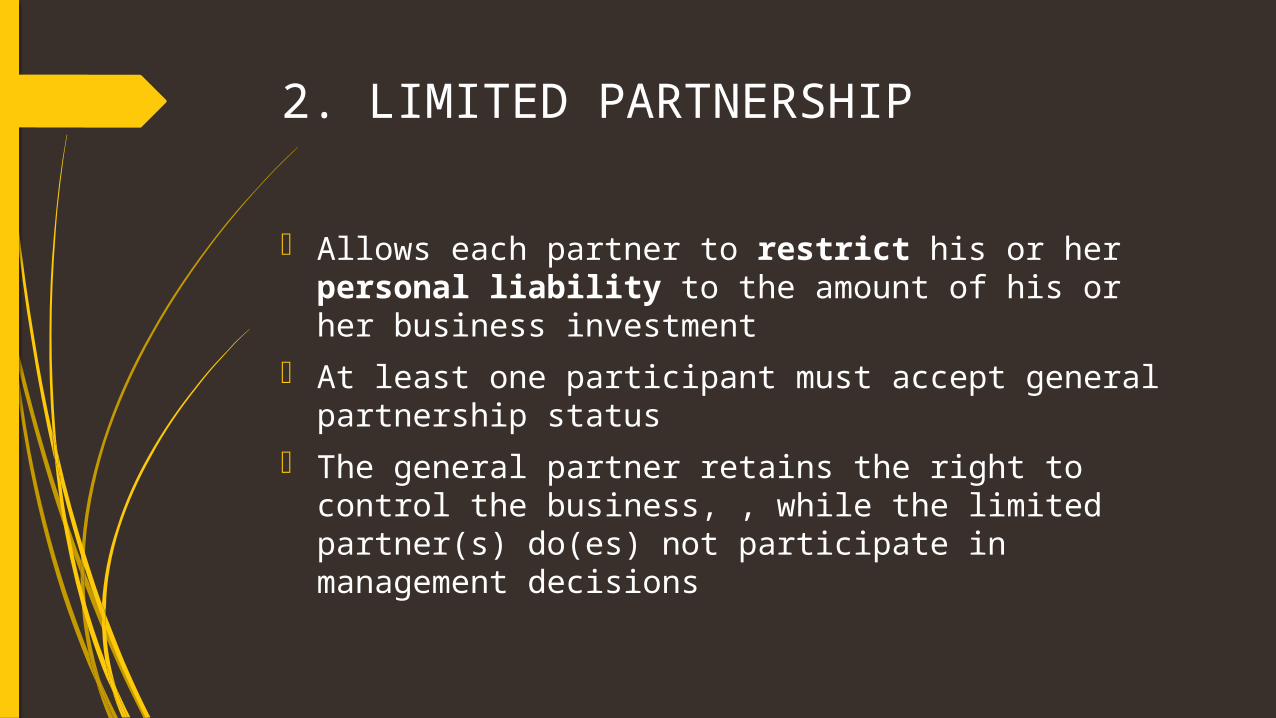

2. LIMITED PARTNERSHIP

Allows each partner to restrict his or her personal liability to the amount of his or her business investment

At least one participant must accept general partnership status

The general partner retains the right to control the business, , while the limited partner(s) do(es) not participate in management decisions

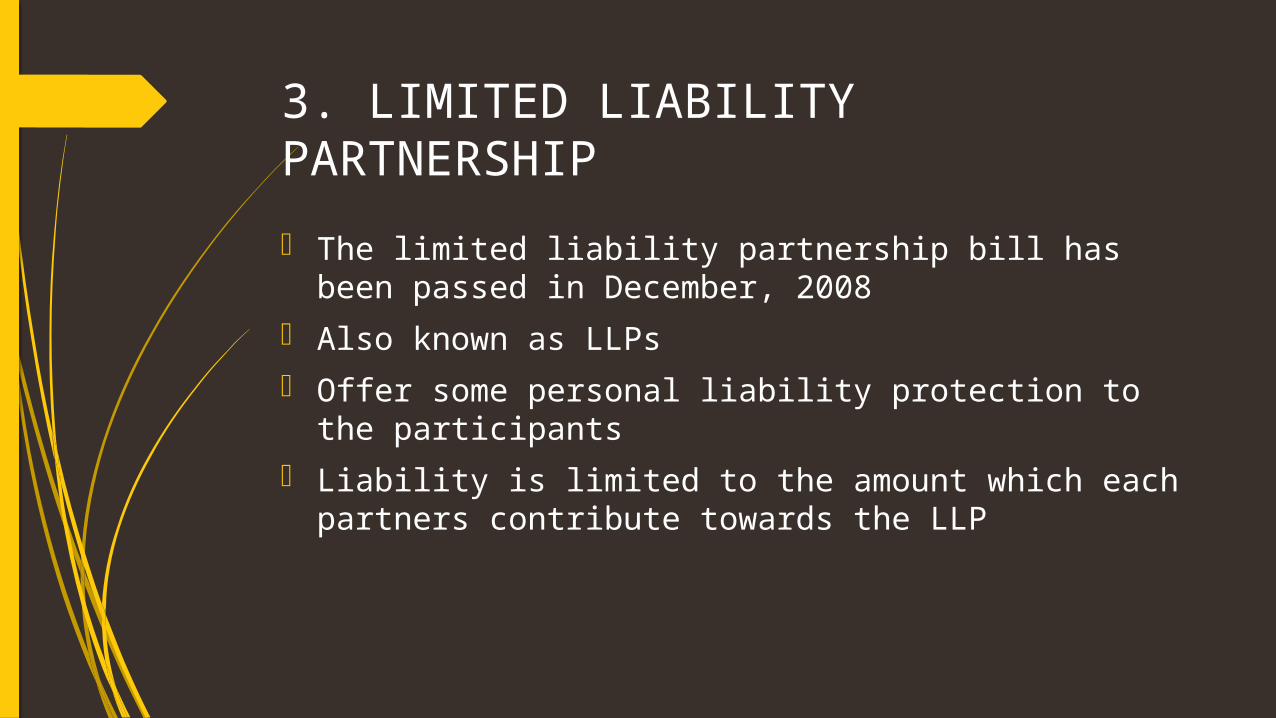

3. LIMITED LIABILITY PARTNERSHIP

The limited liability partnership bill has been passed in December, 2008

Also known as LLPs Offer some personal liability protection to the

participants Liability is limited to the amount which each partners

contribute towards the LLP

Registration of Partnership Firms

The registration of the firm may be affected at any time by filing an application in the form of a statement, giving the necessary information, with the registrar of the firms of the area.

The application of the registration of a firm shall be accompanied by the prescribed fee

The statement shall be signed by all the partners or by their agents specially authorized in this behalf [Sec. 58(1)]

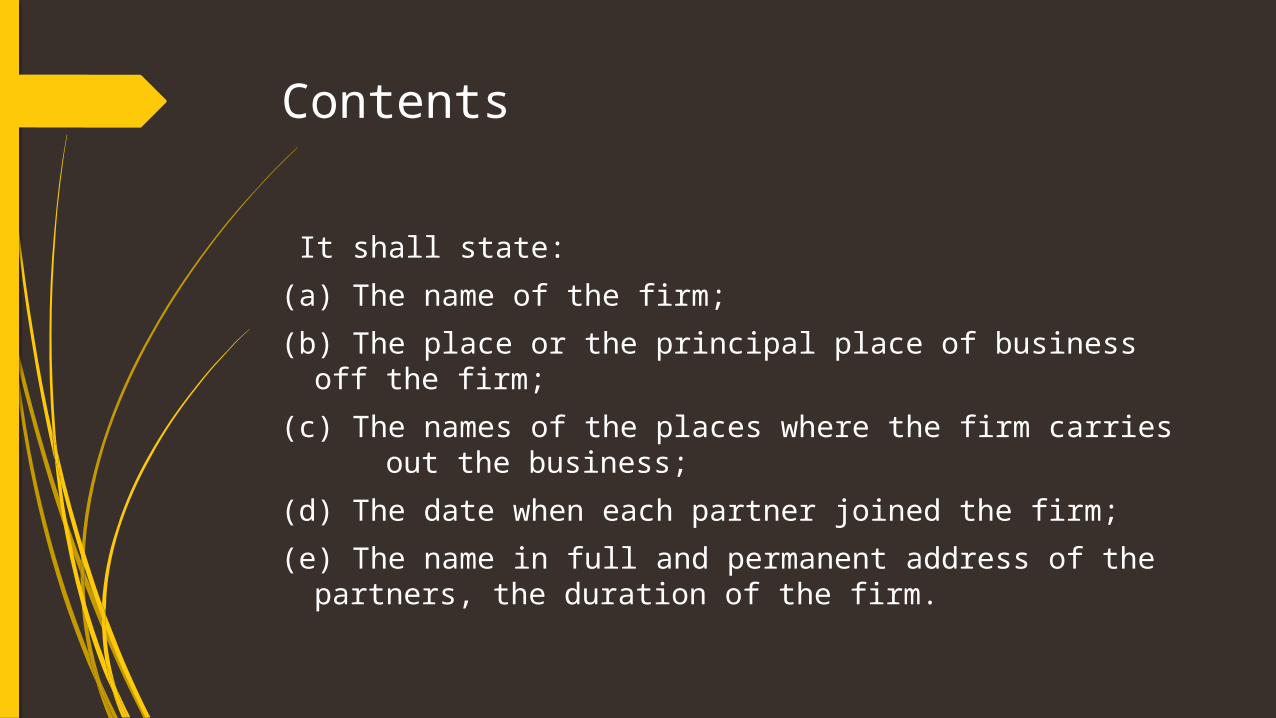

Contents

It shall state:(a) The name of the firm;(b) The place or the principal place of business off the firm;(c) The names of the places where the firm carries out

the business;(d) The date when each partner joined the firm;(e) The name in full and permanent address of the

partners, the duration of the firm.

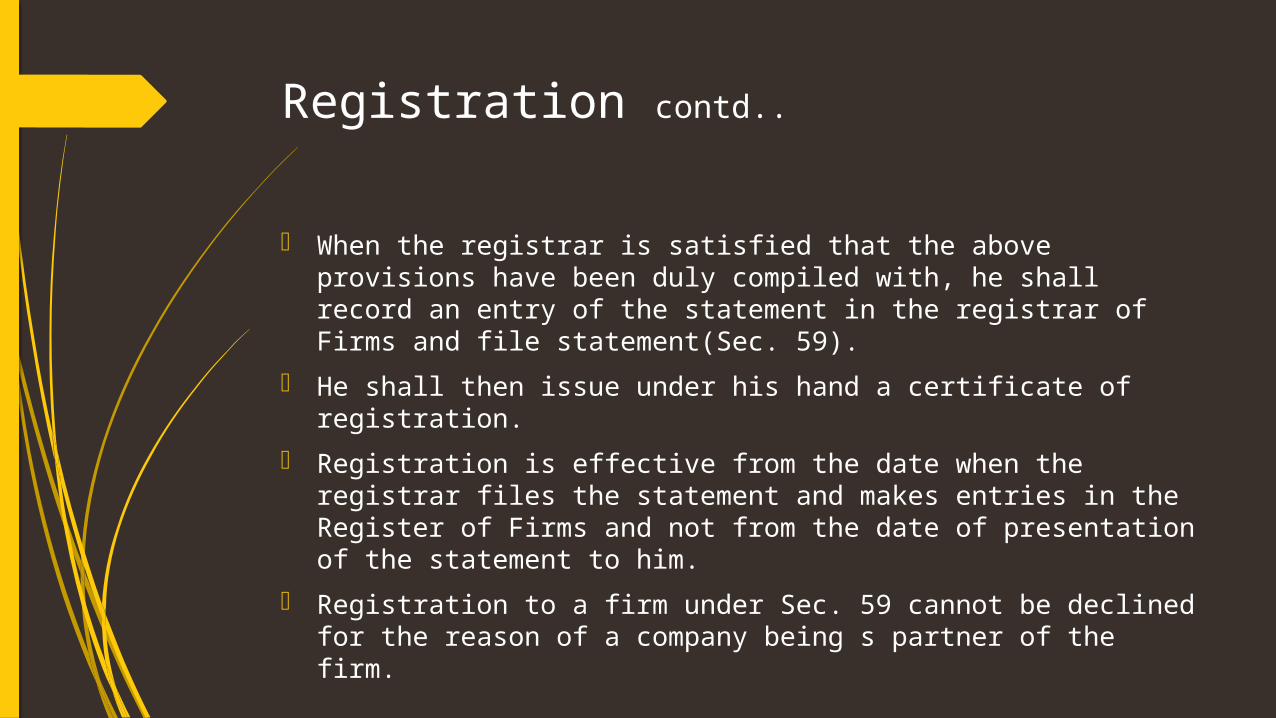

Registration contd..

When the registrar is satisfied that the above provisions have been duly compiled with, he shall record an entry of the statement in the registrar of Firms and file statement(Sec. 59).

He shall then issue under his hand a certificate of registration. Registration is effective from the date when the registrar files the

statement and makes entries in the Register of Firms and not from the date of presentation of the statement to him.

Registration to a firm under Sec. 59 cannot be declined for the reason of a company being s partner of the firm.

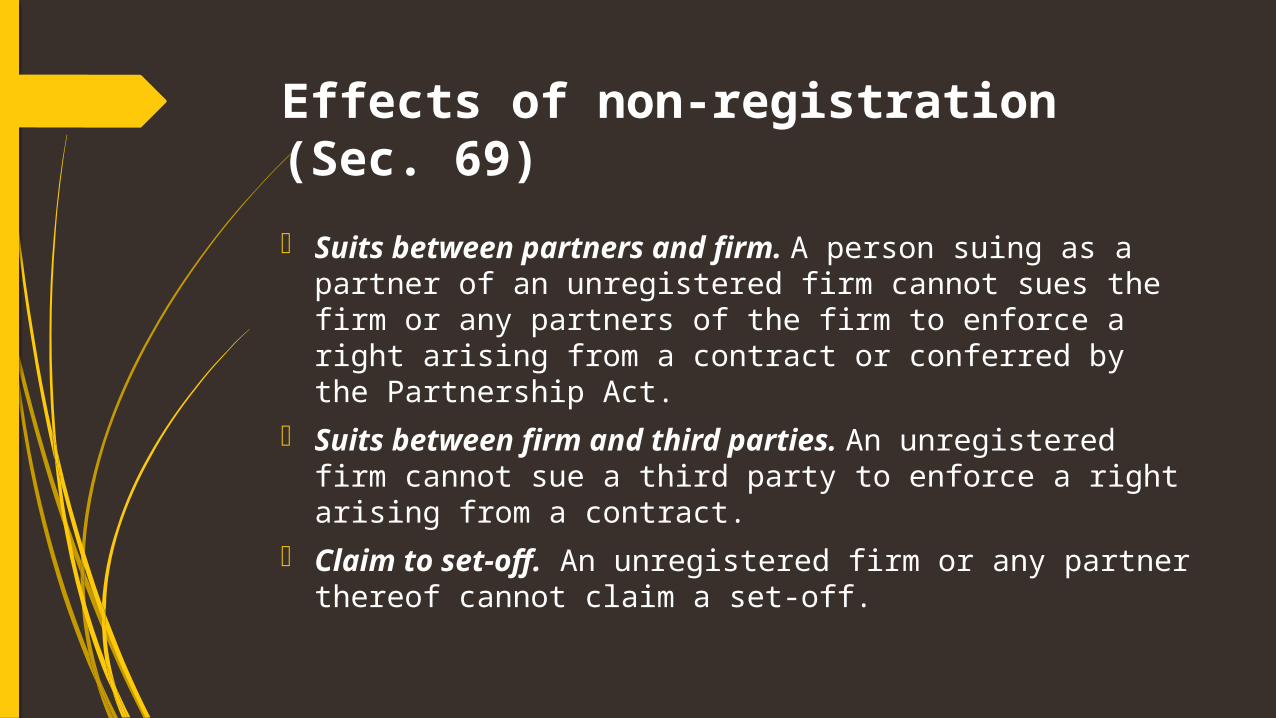

Effects of non-registration (Sec. 69) Suits between partners and firm. A person suing as

a partner of an unregistered firm cannot sues the firm or any partners of the firm to enforce a right arising from a contract or conferred by the Partnership Act.

Suits between firm and third parties. An unregistered firm cannot sue a third party to enforce a right arising from a contract.

Claim to set-off. An unregistered firm or any partner thereof cannot claim a set-off.

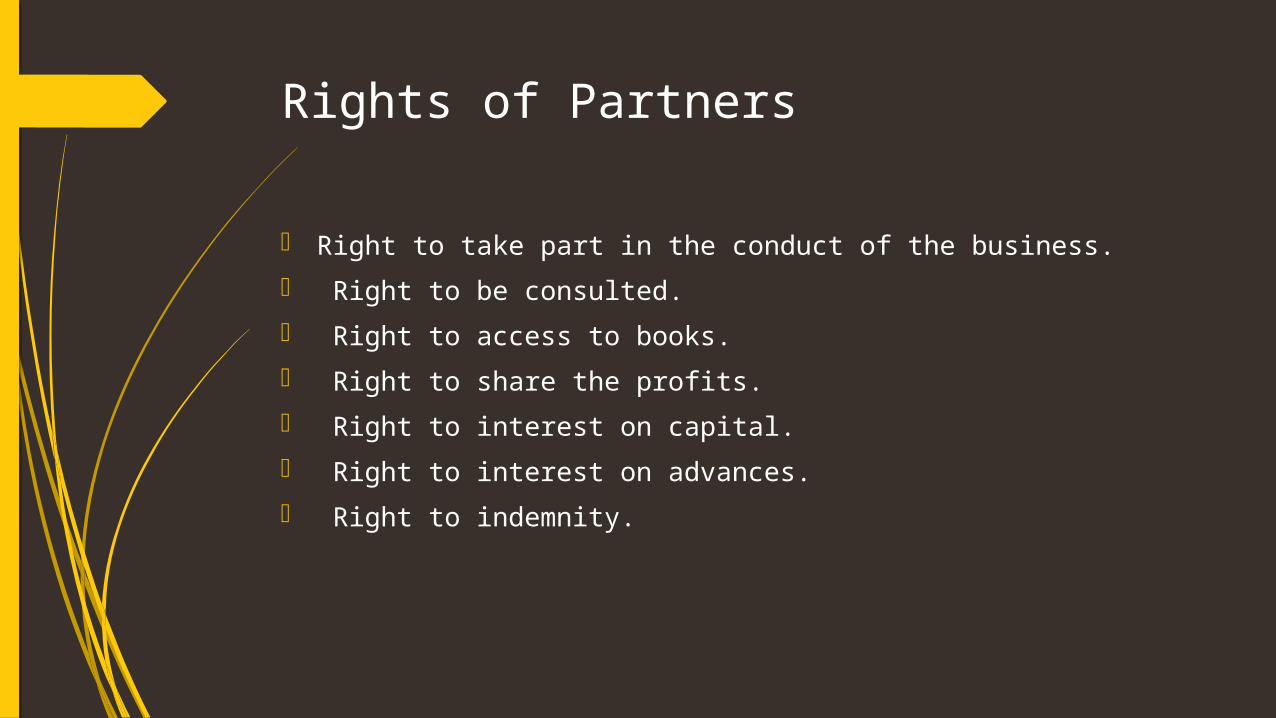

Rights of Partners

Right to take part in the conduct of the business. Right to be consulted. Right to access to books. Right to share the profits. Right to interest on capital. Right to interest on advances. Right to indemnity.

LIABILITY OF PARTNERS TO THIRD PARTIES Liability of a partner for acts of the firm. Liability of the firm for wrongful acts of a partner. Liability of the firm for misapplication by partners.

Liability of a partner for acts of the firm(sec. 25)

Every partner is liable, jointly with all the other partners and also severally, for all acts of the firm done while he is a partner.

As between the partners themselves, the partner paying for more than his share of the liability may claim contribution from the others according to the terms of the partnership agreement

Liability of the firm for wrongful acts of a partner(Sec. 26) Where, by the wrongful act or omission of a partner

acting in the ordinary course of the business of a firm, or with the authority of his partners, loss or injury is caused to any third party, or any penalty is incurred, the firm is liable therefore to the same extend as the partner.

The wrongful act may be tort, fraud, or negligence.

Liability of the firm for misapplication by partners (Sec. 27).Where(a) A partner acting within his apparent authority receives money or property from a third party and misapplies it.(b) A firm in the course of its business receives money or property from a third party, and the same is misapplied by any of the partners while it is in the custody of the firm, the firm is liable to make good the loss.

Liability of an incoming partner

A new partner becomes liable for the debts and acts of the firm only from the date he is admitted as a partner.He cannot be held liable for the acts of the old firm. A new partner may, however, agree to be liable for the debts existing prior to his admission but such agreeing will not give to a prior creditor the right to sue him because of absence of ‘privity of contract.’

Dissolution of the Firm

Section. 39 provides that the dissolution of partnership between all the partners of a firm is called ‘dissolution of the firm.’

Modes of dissolutionA firm may be dissolved in any one of the following ways:

By Agreement. By Notice On the happening of certain contingencies Compulsory Dissolution Dissolution by the Court

Contd..

By Agreement: A firm may be dissolved with the consent of all the partners or in accordance with a contract between the partners. Partnership is created by a contract, it can also be terminated by a contract.

By notice: Where the partnership is at will, the firm may be dissolved by any partner giving the notice in writing to all the other partners of his intention to dissolve the firm. A notice of dissolution once given cannot be withdrawn without the consent of all the other partners.

Contd..

3. On the happening of certain contingencies: Subject to a contract between the partners, a firm may be dissolved if:

a.) If constituted for a fixed term, by the expiry of that term. b.) If constituted to carry out one or more adventures or

undertakings, by the completion thereof. c.) By the death of the partner. d.) By the adjudication of partner as an insolvent.

Contd..

4. Compulsory Dissolution: A firm may be compulsorily dissolved if:

(a) When all the partners, or all the partners but one, are

adjudged insolvent. (b) When some event has happened which makes it unlawful

for the business of the firm to be carried on.

contd..

5. Dissolution by the Court: Dissolution by the court is necessitated when there is a difference of opinion between the partners regarding the matter of dissolution in cases of:

(a) Insanity (b) Permanent Incapacity (c) Misconduct (d) Persistent breach of agreement (e) Transfer of interest (f) Just and Equitable

COMPANY ACT

Company A company in the normal sense means an association of persons united for the common object. Accordingly the term is used to represent associations formed to carry on some business for profit or to promote art, science, education or some charitable purpose.

Definition According to section 3 (1) (i) of the companies Act, a company means, “A company formed and registered under this Act or an existing company.” An existing company means, “A company formed and registered under any of the previous companies laws.

Characteristics of a company1. Incorporated association

A company comes into existence on incorporation or registration under the companies act. A joint stock company may be incorporated under the act either as private or a public company. If not registered as a company or under any other law, becomes an illegal association.2. Separate legal entity

The main feature of a company is its independent corporate existence. A company formed and registered under the companies act is a distinct legal entity. Its personality is separate and distinct from personality of those who compose it.3. Limited liability

It is the reason why many people invest their money in limited companies. Here the liability of the members is limited to such amount as the members may undertake to contribute to the assets of the company , in the event of its wounding up.

Contd..4. Separate property

A company is a legal person and therefore it is capable of enjoying, owning and disposing of property in its own name. the shareholders don’t have any proprietary rights over the property of the company.5. Perpetual succession:

A company never dies. It is not in any manner affected by insolvency or death of any of its members. It continues to exist even if all its members are dead. A company is created by a process of law and can be put an end to only by a process of law.6. Common seal:

As a company is an artificial person it cannot sign its name on a contract. So it functions with the help of a seal. Common seal is used as a substitute for its signature. Every company must have a seal with its name engraved on it.7. Transferability of shares:

The shares of a company are freely transferable and can be sold or purchased in the share market.

Merits of company

Large resources benefits of large scale operations Professional management Research and development Corporate personality Limited liability Perpetual succession Transferability of shares Separate property

Limitations• Difficult to form• Control by a Group• Excessive Government Control• Delay in Decision Making• Incorporation and wind up formalities and expense• Heavy fines, penalties and even imprisonment in case of non-

compliance of laws• Too much disclosure in form of annual returns, intimation to stock

exchanges etc.• Demutualization (separation of ownership and management)• Greater tax burden as company has to pay tax on flat rates• Greater social responsibility

Companies legal entity

A company is an artificial person different for its members and directors. In the eyes of law it has a separate corporate personality. It has its own corporate name. It works under that name. In normal circumstances company cannot be considered as agent or trustee of its members. Therefore members and directors of a company cannot be held liable for any act of that company.

This concept is known as Corporate Veil. Means only company can be held liable for an act done in the name of the company.

Contd..But, as per company laws, a company can be created for lawful purpose only. If a company is created for dishonest use fraudulent purpose unlawful purpose evading taxes any other purpose which is against the public interestthan law can identify the persons who are behind it and are responsible for any fraud/unlawful act. Company cannot work or think on its own. Its directors and members are its mind and body. Therefore, company can’t do anything wrong own its own. Thus, for any wrong act in the name of company, members/directors can be held liable.

This concept is called “Lifting of Corporate Veil”.

45

In the following circumstances different courts found it necessary to lift the corporate veil and punish the actual persons who did wrong or unlawful acts under the name of company:

Protection of Revenue The Court may

ignore the Separate Legal Entity status of a Company, where it is used for tax invasion or circumventing tax obligation.

46Determination of enemy character of the Company Company being an artificial

person cannot be enemy or friend. But during war, it may become necessary to lift the corporate veil and see the persons behind it to determine whether they are friends or enemy. This is due to the reason that though a company enjoys Separate Legal Entity but its affairs are run by individuals.

47Prevention of fraud

Where a Company is used for committing frauds or improper conduct, Court may lift the corporate veil and look at the realities of the situation.

Avoidance of Welfare Legislation

Where a Company tries to avoid its legal obligations, the corporate veil shall be lifted to look at the real picture.

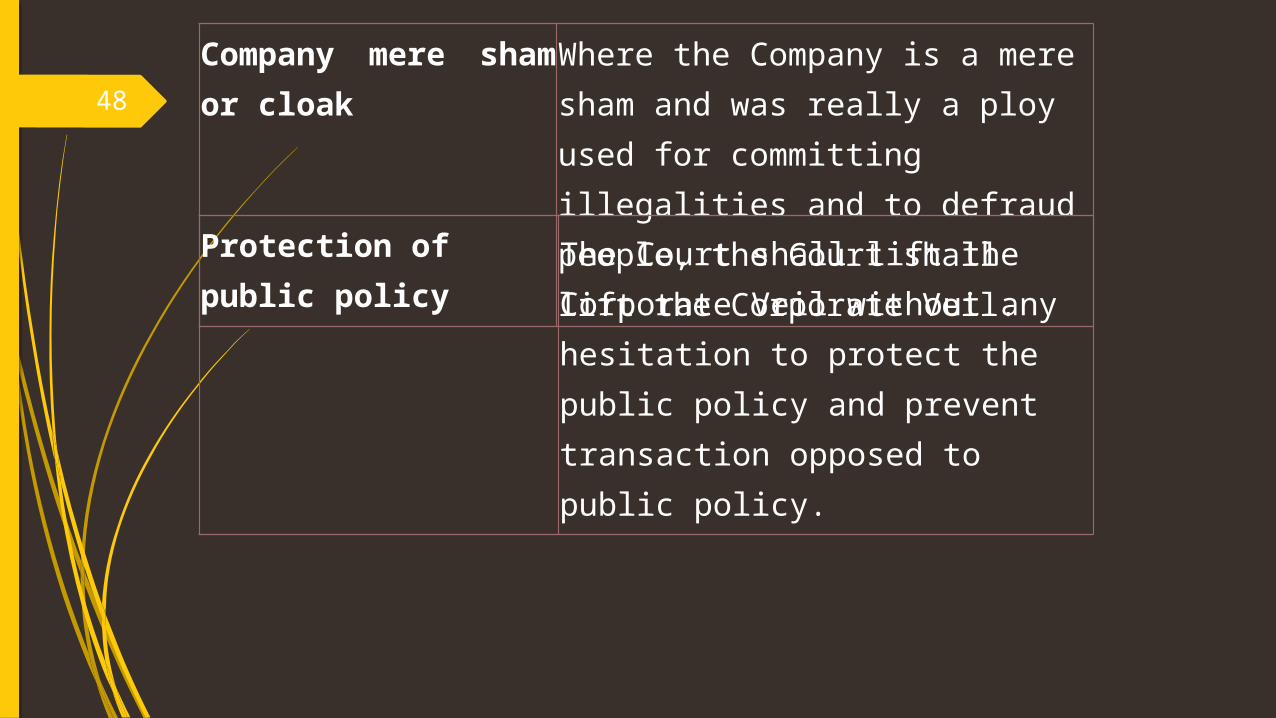

48Company mere sham or cloak

Where the Company is a mere sham and was really a ploy used for committing illegalities and to defraud people, the Court shall lift the Corporate Veil. Protection of public

policy The Court shall lift the Corporate Veil without any hesitation to protect the public policy and prevent transaction opposed to public policy.

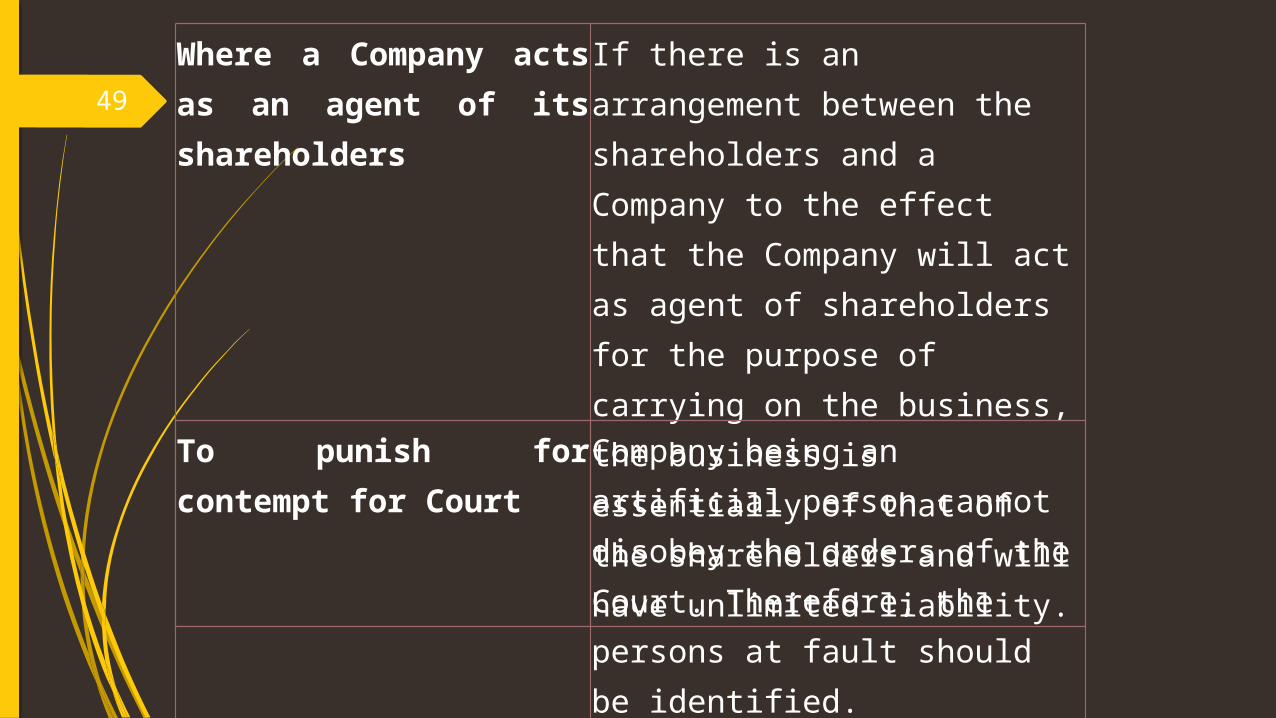

49Where a Company acts as an agent of its shareholders

If there is an arrangement between the shareholders and a Company to the effect that the Company will act as agent of shareholders for the purpose of carrying on the business, the business is essentially of that of the shareholders and will have unlimited liability.To punish for

contempt for CourtCompany being an artificial person cannot disobey the orders of the Court. Therefore, the persons at fault should be identified.

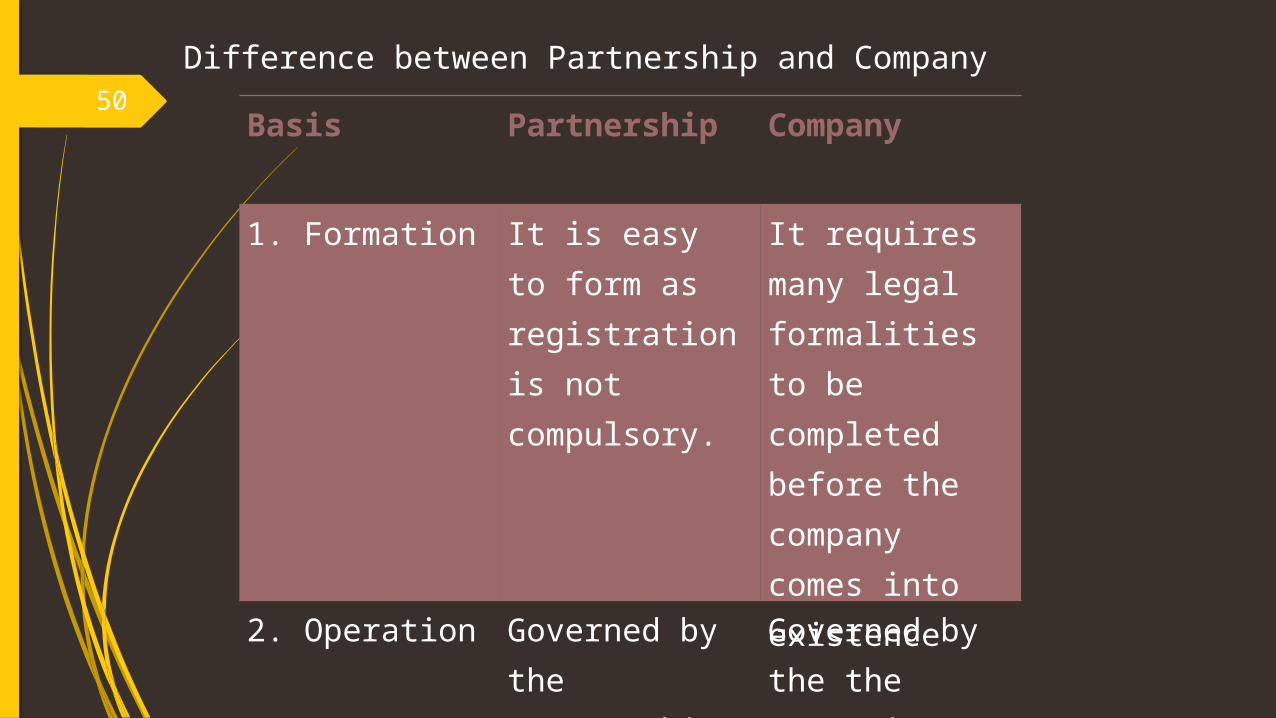

50Difference between Partnership and Company

Basis Partnership Company

1. Formation It is easy to form as registration is not compulsory.

It requires many legal formalities to be completed before the company comes into existence

2. Operation Governed by the Partnership Act, 1932.

Governed by the the Companies,. Act, 1956.

51

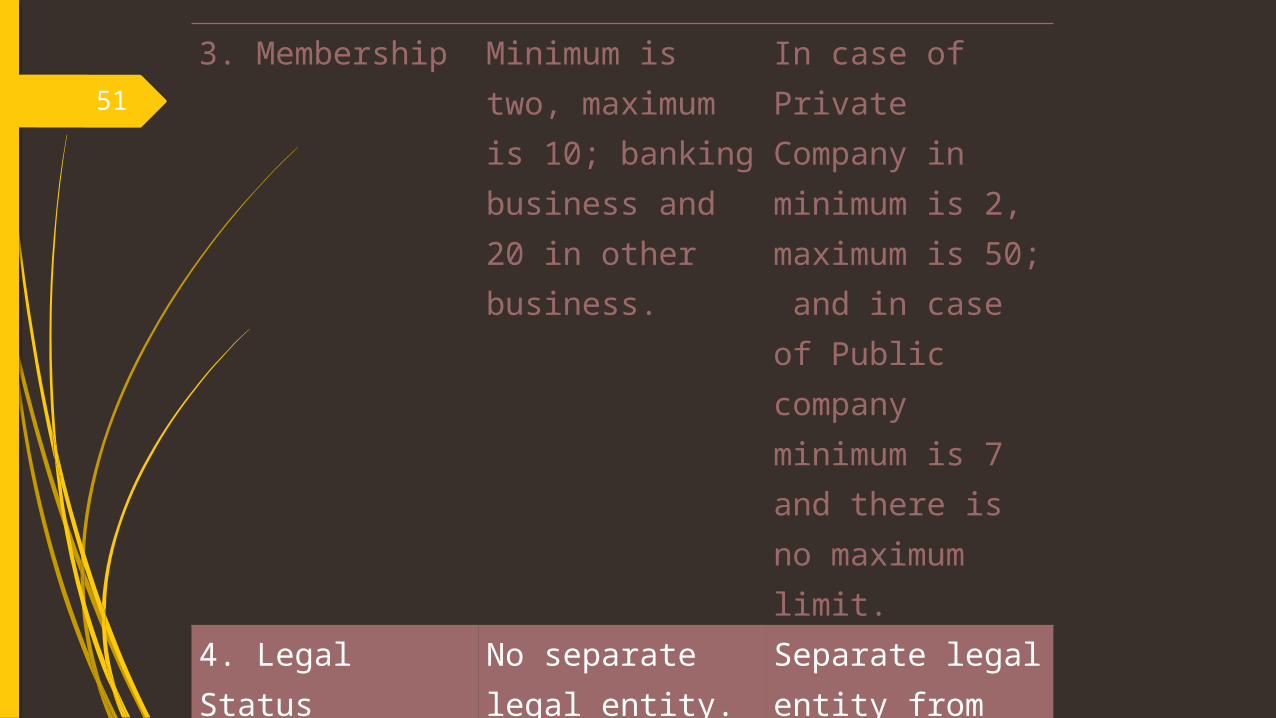

3. Membership Minimum is two, maximum is 10; banking business and 20 in other business.

In case of Private Company in minimum is 2, maximum is 50; and in case of Public company minimum is 7 and there is no maximum limit.

4. Legal Status No separate legal entity.

Separate legal entity from that of its members.

5. Liability Joint and several to unlimited extent.

Limited to the face value held.

52

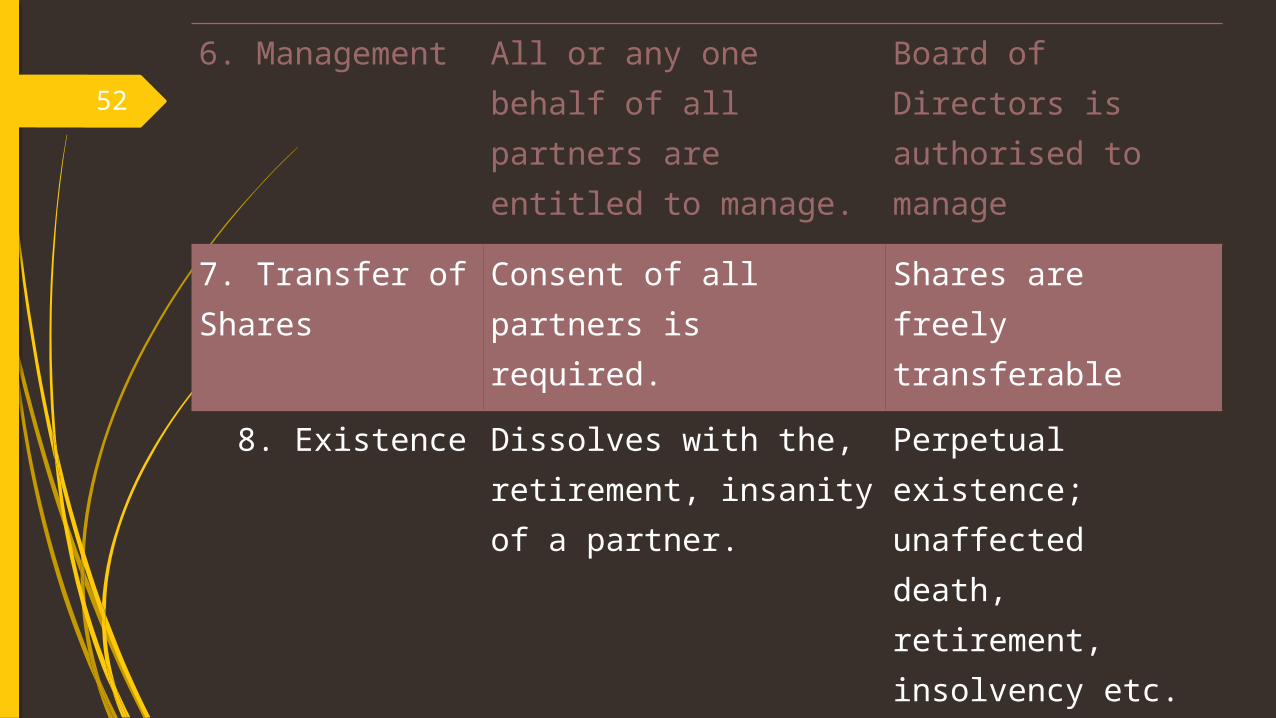

6. Management All or any one behalf of all partners are entitled to manage.

Board of Directors is authorised to manage

7. Transfer of Shares Consent of all partners is required.

Shares are freely transferable

8. Existence

Dissolves with the, retirement, insanity of a partner.

Perpetual existence; unaffected death, retirement, insolvency etc. of the shareholders.

9. Finance Relatively limited scope for raising finance.

Vast and unlimited scope for raising finance.

53

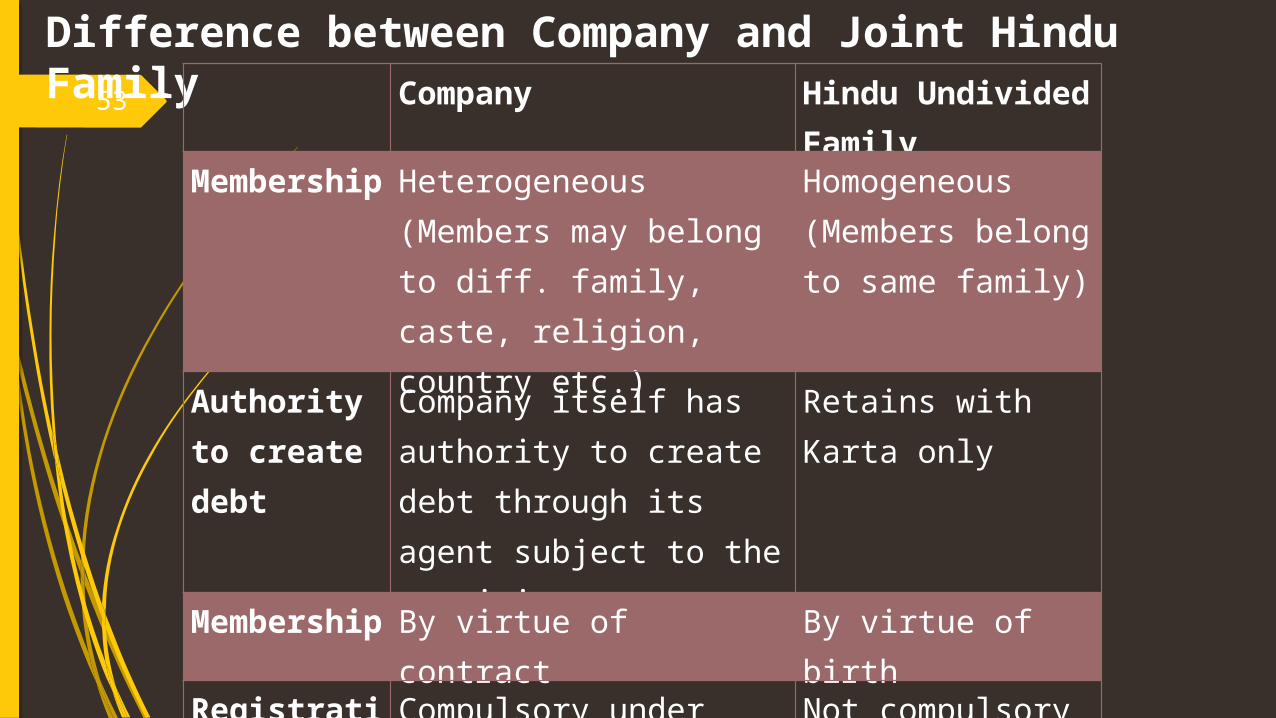

Difference between Company and Joint Hindu Family Company Hindu Undivided

FamilyMembership Heterogeneous (Members

may belong to diff. family, caste, religion, country etc.)

Homogeneous (Members belong to same family)

Authority to create debt

Company itself has authority to create debt through its agent subject to the provisions.

Retains with Karta only

Membership By virtue of contract By virtue of birth

Registration Compulsory under Company Laws

Not compulsory under any law

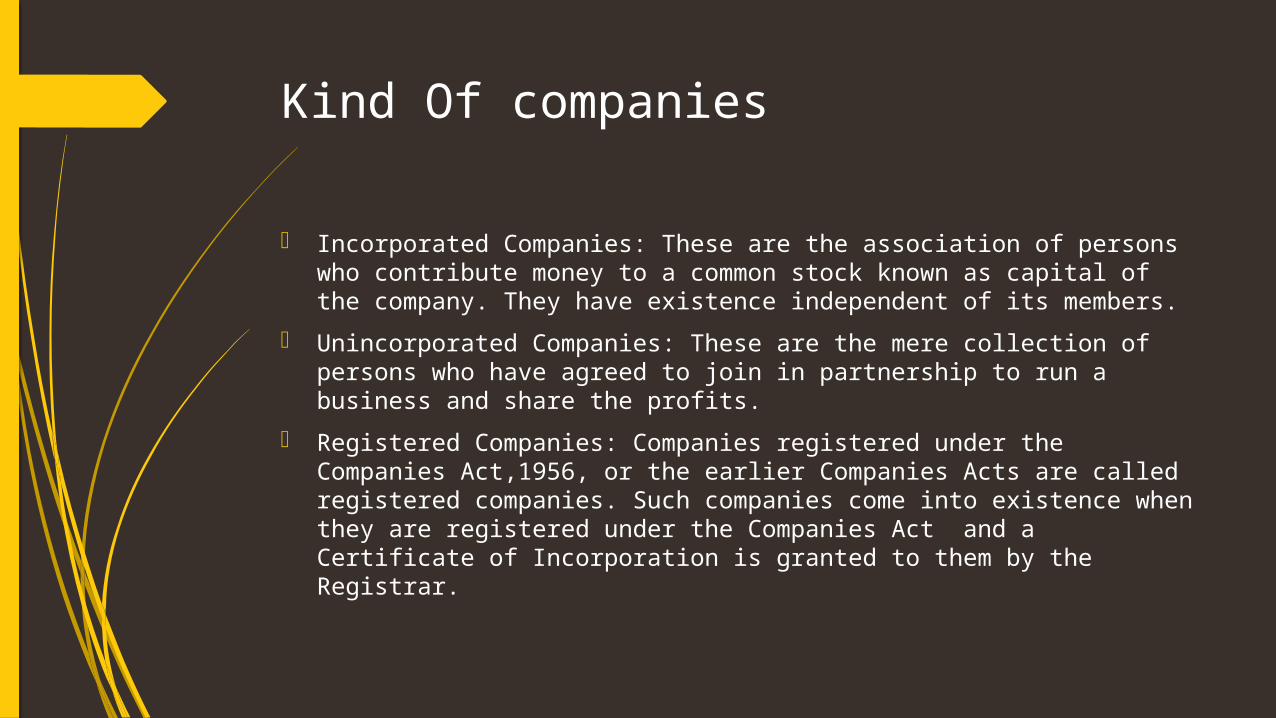

Kind Of companies

Incorporated Companies: These are the association of persons who contribute money to a common stock known as capital of the company. They have existence independent of its members.

Unincorporated Companies: These are the mere collection of persons who have agreed to join in partnership to run a business and share the profits.

Registered Companies: Companies registered under the Companies Act,1956, or the earlier Companies Acts are called registered companies. Such companies come into existence when they are registered under the Companies Act and a Certificate of Incorporation is granted to them by the Registrar.

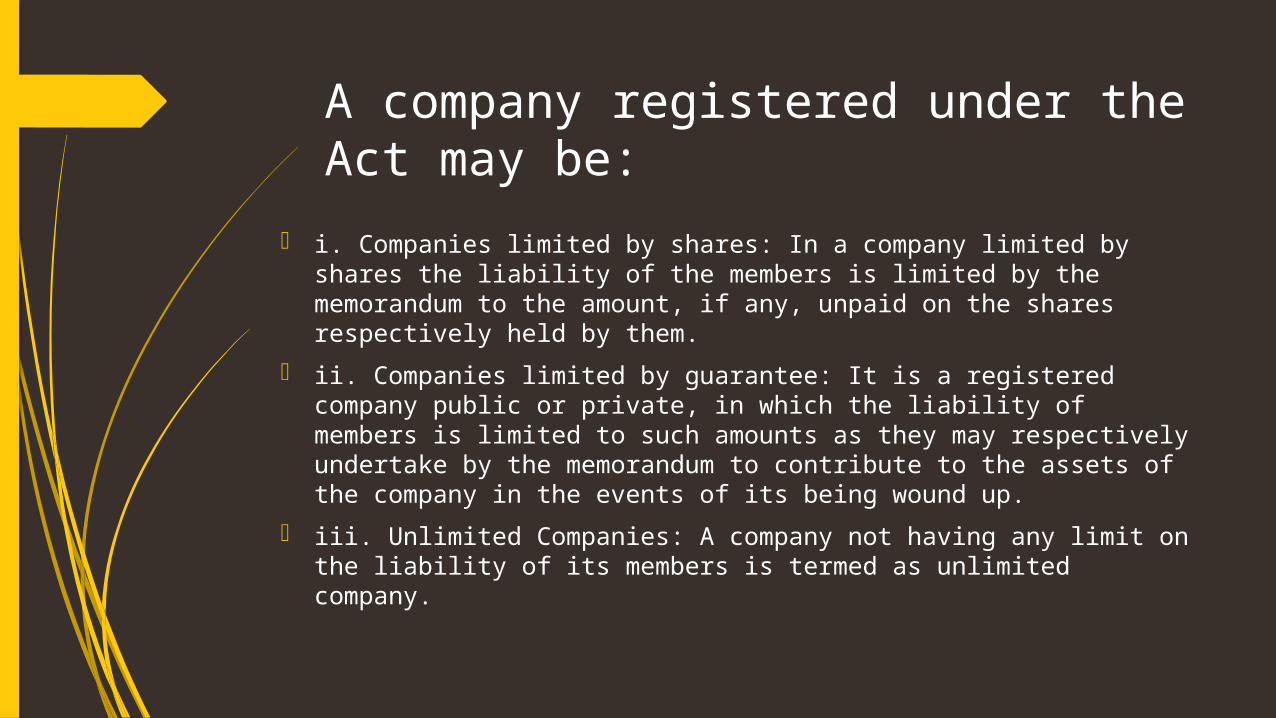

A company registered under the Act may be:

i. Companies limited by shares: In a company limited by shares the liability of the members is limited by the memorandum to the amount, if any, unpaid on the shares respectively held by them.

ii. Companies limited by guarantee: It is a registered company public or private, in which the liability of members is limited to such amounts as they may respectively undertake by the memorandum to contribute to the assets of the company in the events of its being wound up.

iii. Unlimited Companies: A company not having any limit on the liability of its members is termed as unlimited company.

Contd..

Private company: According to Section 3(1)(iii) of the Companies (Amendment)Act,2000, a private company means a company which:

(a) has a minimum paid up capital of one lakh rupees or such higher amount as may be prescribed by the Government;

(b) has a minimum of 2 and maximum of members excluding employees;

(c) restricts the right of members to transfer its shares , if any;

(d) prohibits any invitation to the general public to subscribe for its shares or debentures;

(e) does not invite the public to subscribe to its deposits. E.g.:- Ambika Industries Pvt. Ltd., Paras Pharmaceutical Pvt. Ltd.

etc.

Contd..

Public Company: According to Section 3(1)(iv) of the Companies (Amendment)Act,2000, a public company means a company which:

(a) is not a private company; and (b) has a minimum paid up capital of five lakh rupees or such

higher amount as may be prescribed by the Government.

E.g.:-Reliance Industries Ltd., Tata Iron & Steel Co. Ltd., D.C.M. Ltd., etc.

Besides all these companies there are few more kinds of Companies:

Government Companies: It is a company of which 51% or more equity share capital is held by the Government. Rest of the shares can be held by private individuals or businessmen.

Foreign Companies: It is incorporated outside India but has a place of business in India. Some of the popular MNCs operating in India are Coca Cola(USA), Pepsi Cola(USA), Sony(Japan),etc.

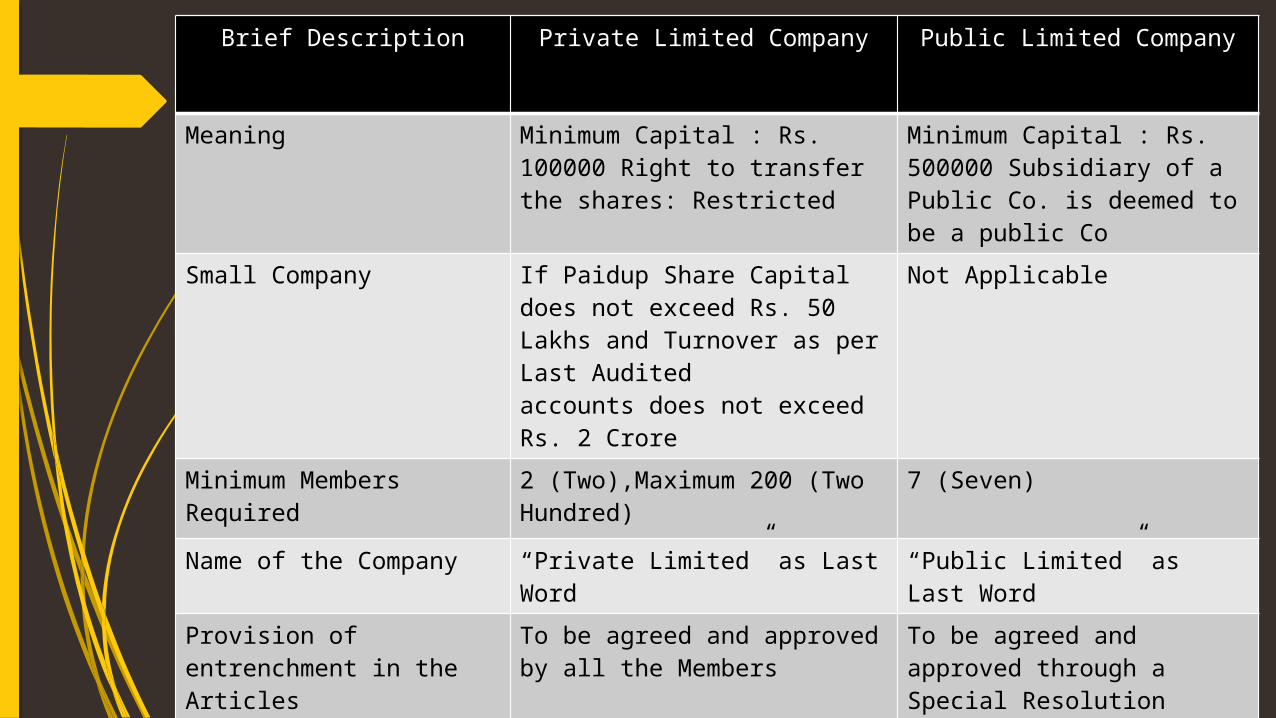

Brief Description Private Limited Company Public Limited Company

Meaning Minimum Capital : Rs. 100000 Right to transfer the shares: Restricted

Minimum Capital : Rs. 500000 Subsidiary of a Public Co. is deemed to be a public Co

Small Company If Paidup Share Capital does not exceed Rs. 50 Lakhs and Turnover as per Last Auditedaccounts does not exceed Rs. 2 Crore

Not Applicable

Minimum Members Required

2 (Two),Maximum 200 (Two Hundred)

7 (Seven)

Name of the Company “Private Limited” as Last Word “Public Limited” as Last Word

Provision of entrenchment in the Articles

To be agreed and approved by all the Members

To be agreed and approved through a Special Resolution

Issue of Securities By way of Right Issue or Bonus Issue Through Private Placement

To Public through Prospectus (“Public Offer”)By way of Right Issue or Bonus Issue Through Private Placement

Brief Description Private Limited Company Public Limited Company

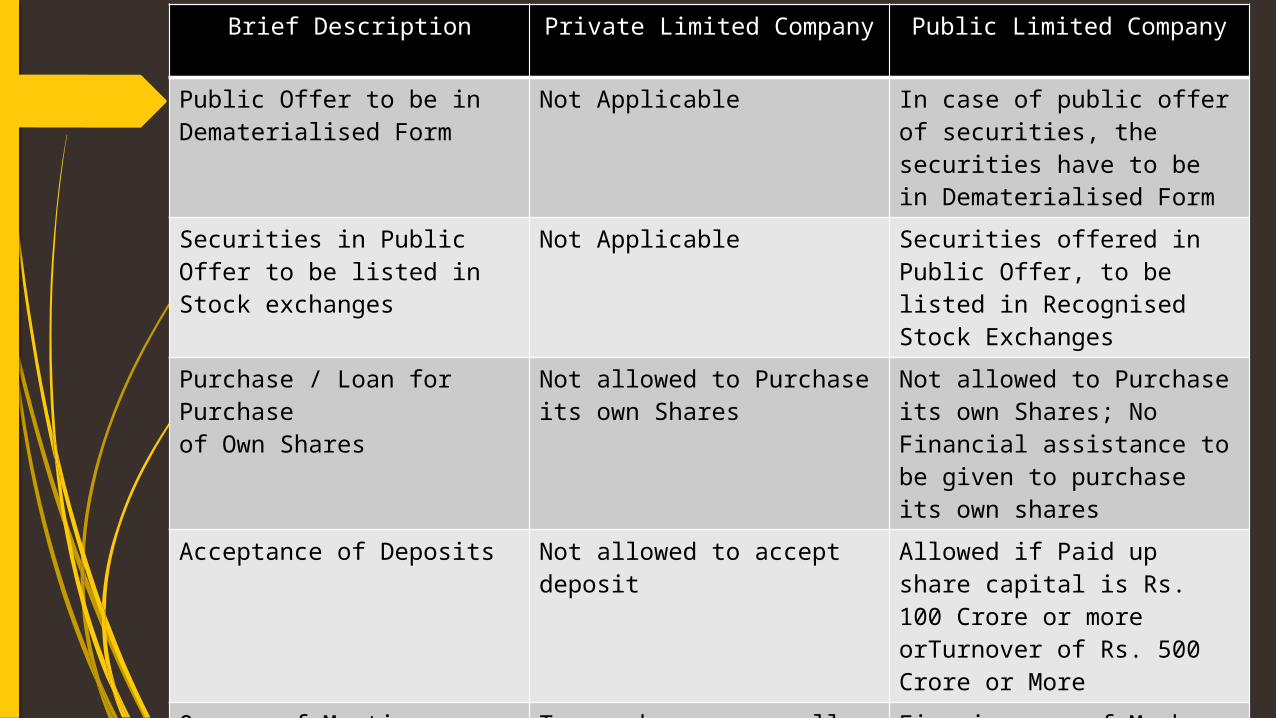

Public Offer to be in Dematerialised Form

Not Applicable In case of public offer of securities, the securities have to be in Dematerialised Form

Securities in Public Offer to be listed in Stock exchanges

Not Applicable Securities offered in Public Offer, to be listed in Recognised Stock Exchanges

Purchase / Loan for Purchaseof Own Shares

Not allowed to Purchase its own Shares

Not allowed to Purchase its own Shares; No Financial assistance to be given to purchase its own shares

Acceptance of Deposits Not allowed to accept deposit

Allowed if Paid up share capital is Rs. 100 Crore or more orTurnover of Rs. 500 Crore or More

Quorum of Meetings Two members personally present

Five in case of Members upto 1000;Fifteen in case of Members more than 1000, upto 5000;Thirty in case of Members exceed 5000.

Brief Description Private Limited Company Public Limited Company

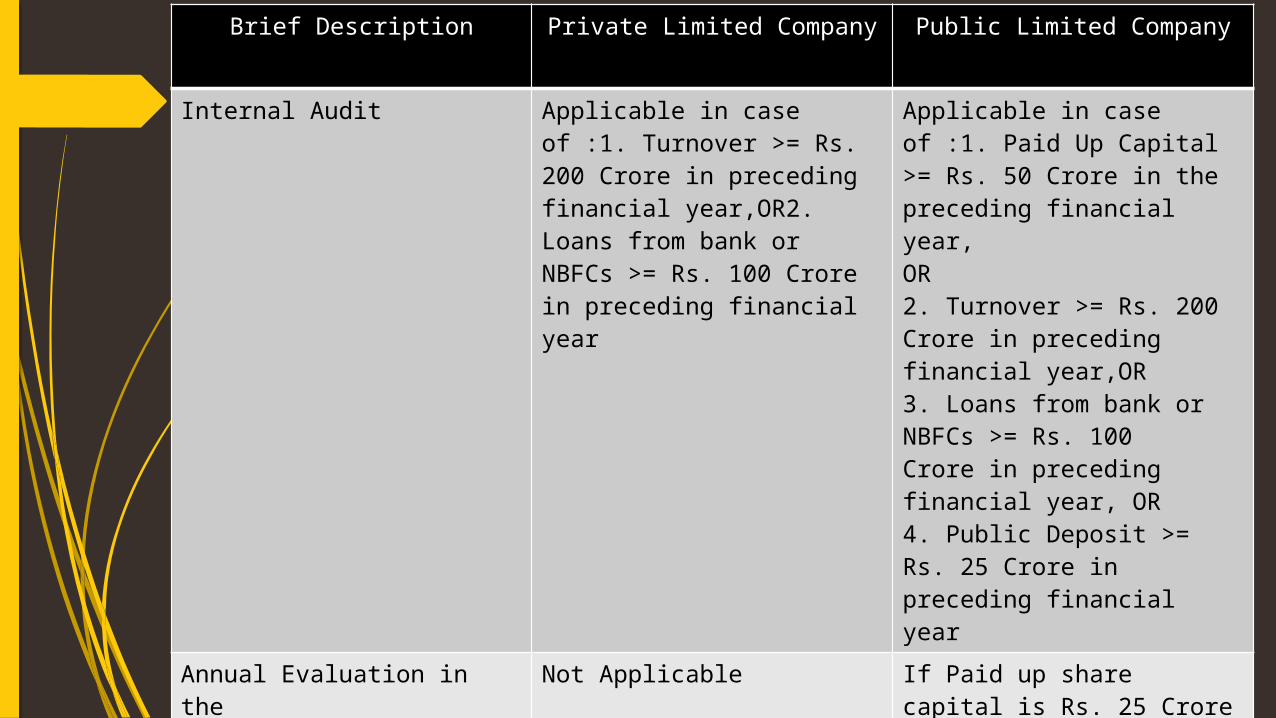

Internal Audit Applicable in case of :1. Turnover >= Rs. 200 Crore in preceding financial year,OR2. Loans from bank or NBFCs >= Rs. 100 Crore in preceding financial year

Applicable in case of :1. Paid Up Capital >= Rs. 50 Crore in the preceding financial year,OR2. Turnover >= Rs. 200 Crore in preceding financial year,OR 3. Loans from bank or NBFCs >= Rs. 100Crore in preceding financial year, OR4. Public Deposit >= Rs. 25 Crore in preceding financial year

Annual Evaluation in theBoard’s Report

Not Applicable If Paid up share capital is Rs. 25 Crore or more, the details of annual evaluation in the Board’s Report

Rotation of Auditor Applicable in case of Paid up Capital is Rs. 20Crore or more

Applicable in case of Paid up Capital is Rs. 10 Crore or more

Brief Description Private Limited Company Public Limited Company

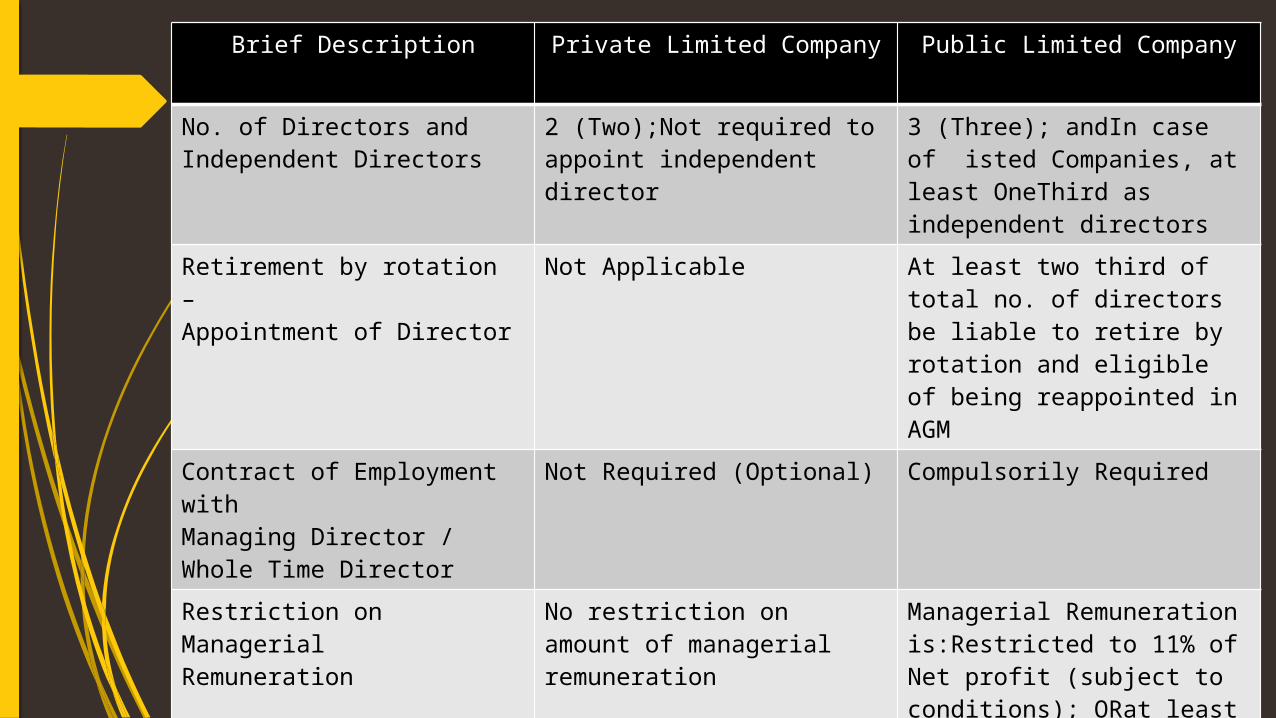

No. of Directors and Independent Directors

2 (Two);Not required to appoint independent director

3 (Three); andIn case of isted Companies, at least OneThird as independent directors

Retirement by rotation –Appointment of Director

Not Applicable At least two third of total no. of directors be liable to retire by rotation and eligible of being reappointed in AGM

Contract of Employment withManaging Director / Whole Time Director

Not Required (Optional) Compulsorily Required

Restriction on ManagerialRemuneration

No restriction on amount of managerial remuneration

Managerial Remuneration is:Restricted to 11% of Net profit (subject to conditions); ORat least Rs. 30 lakh p.a. depending upon paid upCapital

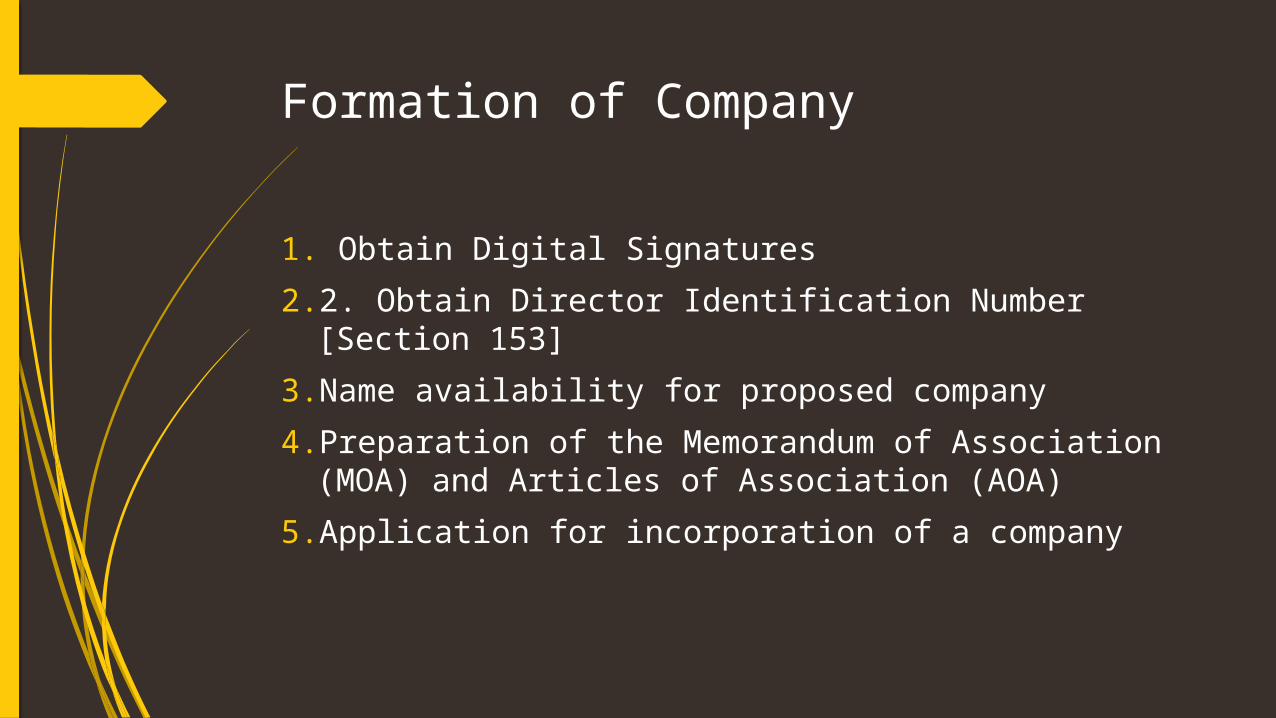

Formation of Company

1. Obtain Digital Signatures2. 2. Obtain Director Identification Number [Section 153]3. Name availability for proposed company4. Preparation of the Memorandum of Association (MOA)

and Articles of Association (AOA)5. Application for incorporation of a company

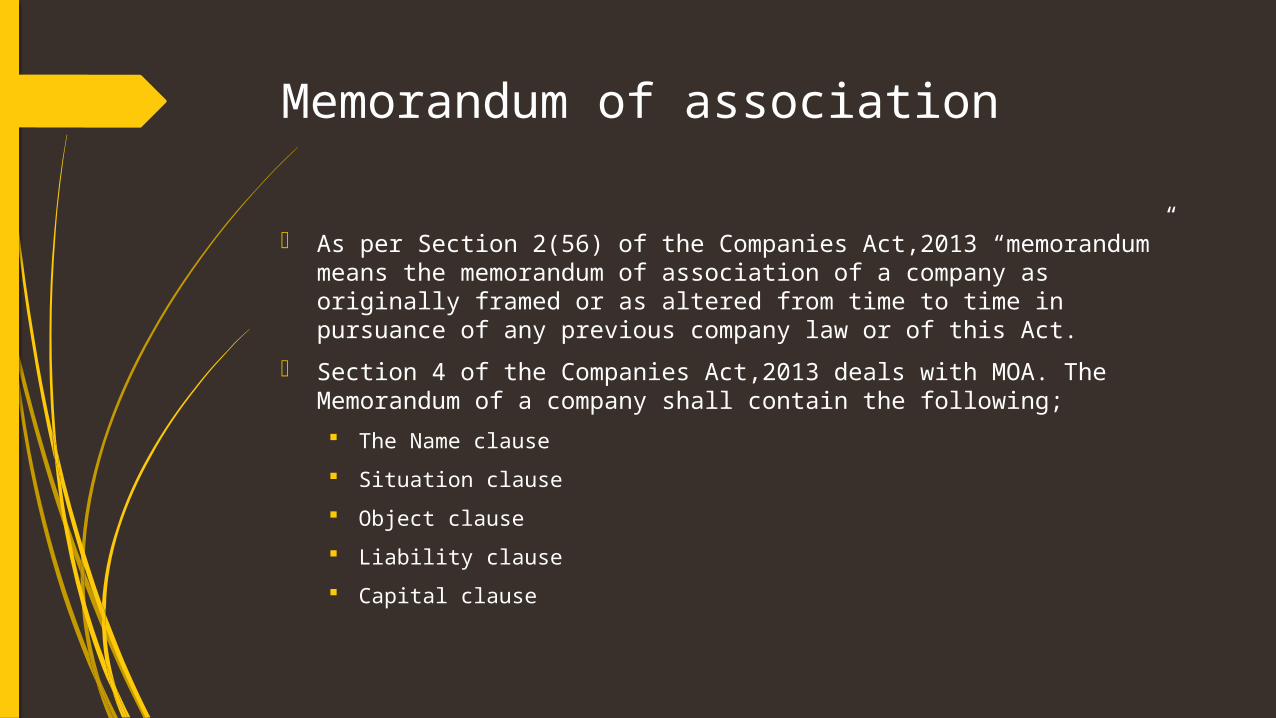

Memorandum of association

As per Section 2(56) of the Companies Act,2013 “memorandum” means the memorandum of association of a company as originally framed or as altered from time to time in pursuance of any previous company law or of this Act.

Section 4 of the Companies Act,2013 deals with MOA. The Memorandum of a company shall contain the following; The Name clause Situation clause Object clause Liability clause Capital clause

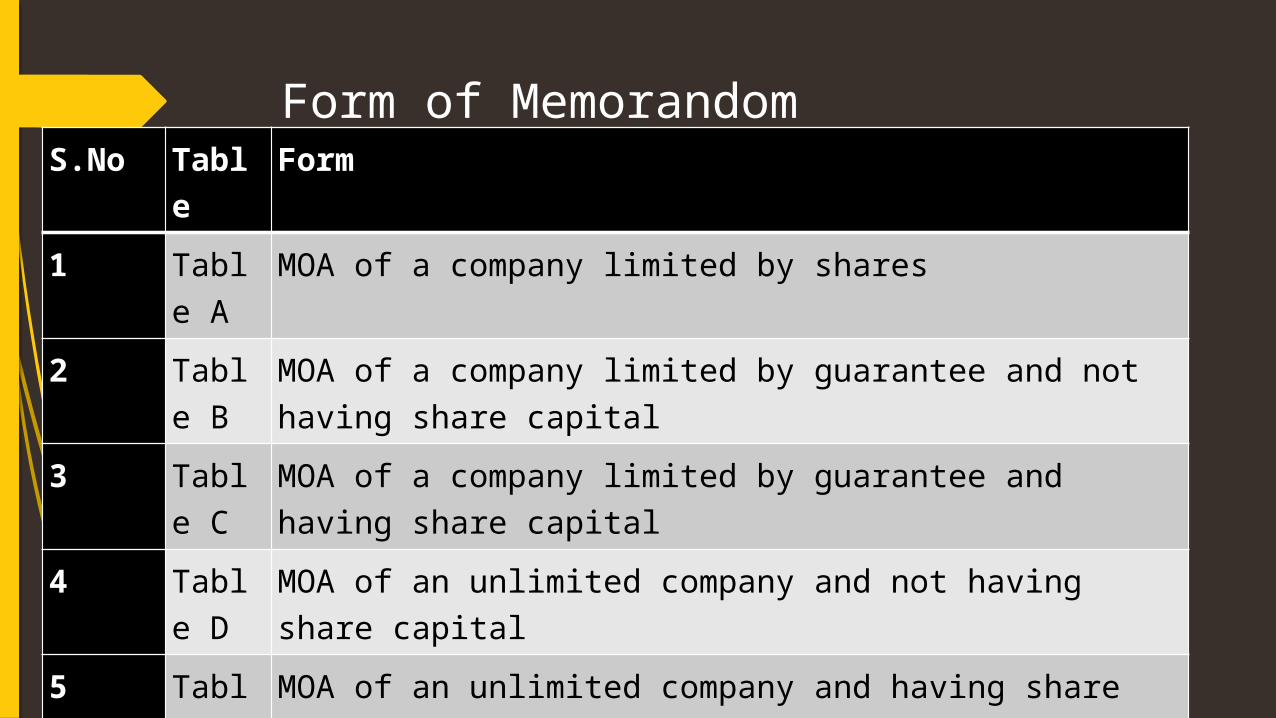

Form of MemorandomS.No Tabl

eForm

1 Table A

MOA of a company limited by shares

2 Table B

MOA of a company limited by guarantee and not having share capital

3 Table C

MOA of a company limited by guarantee and having share capital

4 Table D

MOA of an unlimited company and not having share capital

5 Table E

MOA of an unlimited company and having share capital

Articles of association

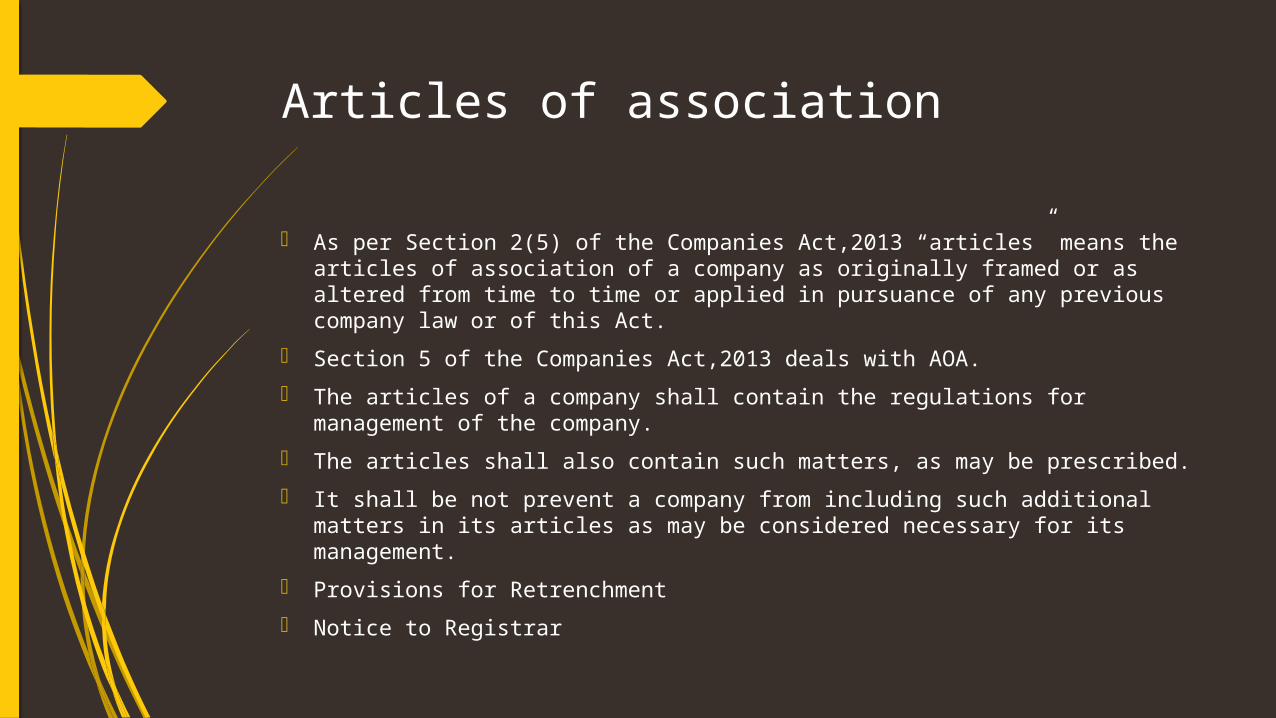

As per Section 2(5) of the Companies Act,2013 “articles” means the articles of association of a company as originally framed or as altered from time to time or applied in pursuance of any previous company law or of this Act.

Section 5 of the Companies Act,2013 deals with AOA. The articles of a company shall contain the regulations for management

of the company. The articles shall also contain such matters, as may be prescribed. It shall be not prevent a company from including such additional matters

in its articles as may be considered necessary for its management. Provisions for Retrenchment Notice to Registrar

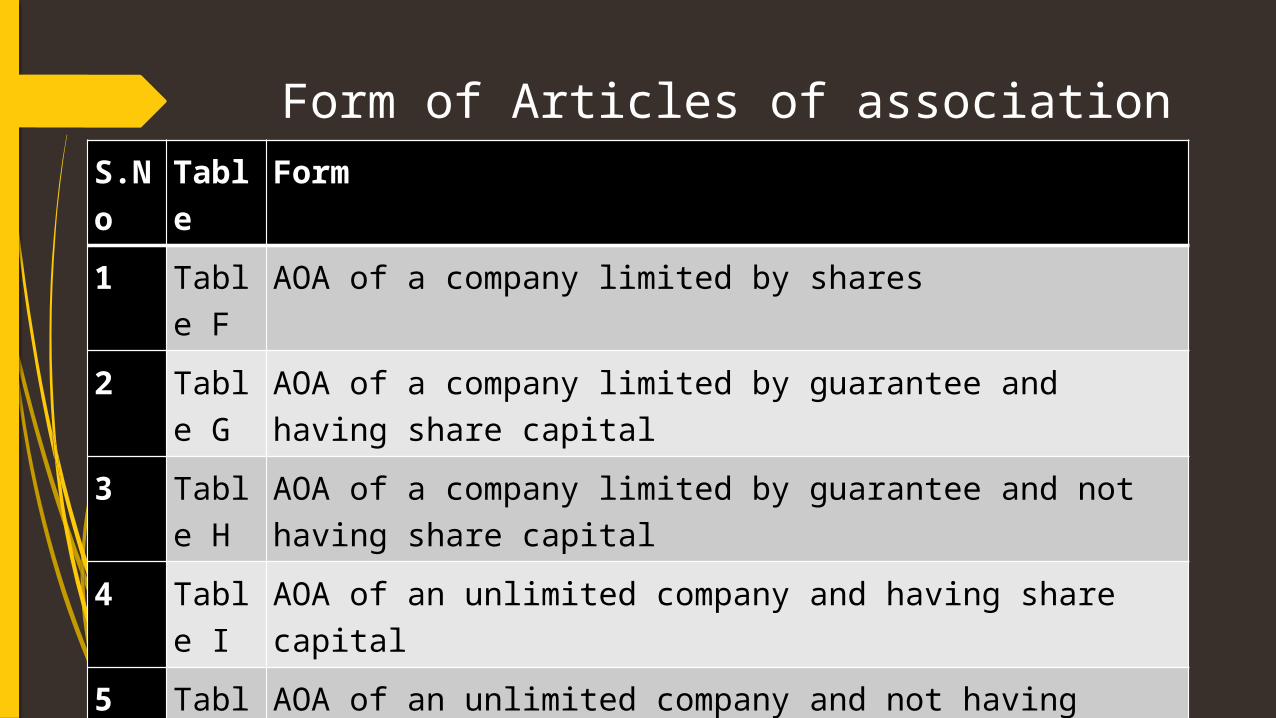

Form of Articles of associationS.No

Table

Form

1 Table F

AOA of a company limited by shares

2 Table G

AOA of a company limited by guarantee and having share capital

3 Table H

AOA of a company limited by guarantee and not having share capital

4 Table I

AOA of an unlimited company and having share capital

5 Table J

AOA of an unlimited company and not having share capital

Prospectus

Clause (70) of Section 2 of this Bill define “prospectus” means any document described or issued as a prospectus and includes a red herring prospectus referred to in section 32 or shelf prospectus referred to in section 31 or any notice, circular, advertisement or other document inviting offers from the public for the subscription or purchase of any securities of a body corporate.

Section 26 deals with matters to be stated in prospectus.

MATTERS TO BE STATED IN PROSPECTUS (SECTION 26): A prospectus may be issued by or behalf of a public company either with

reference to its formation or subsequently, or by or on behalf of any person who is or has been engaged or interested in the formation of a public company.

Information in Prospectus: Every prospectus shall state following information:- i. names and addresses of the registered office of the company,

company secretary, Chief Financial Officer, auditors, legal advisers, bankers, trustees, if any, underwriters and such other persons as may be prescribed;

ii. dates of the opening and closing of the issue, and declaration about the issue of allotment letters and refunds within the prescribed time;

iii. a statement by the Board of Directors about the separate bank account where all monies received out of the issue are to be transferred and disclosure of details of all monies including utilised and unutilised monies out of the previous issue in the prescribed manner;

iv. details about underwriting of the issue; v. consent of the directors, auditors, bankers to the issue, expert’s

opinion, if any, and of such other persons, as may be prescribed; vi. the authority for the issue and the details of the resolution passed

there for;

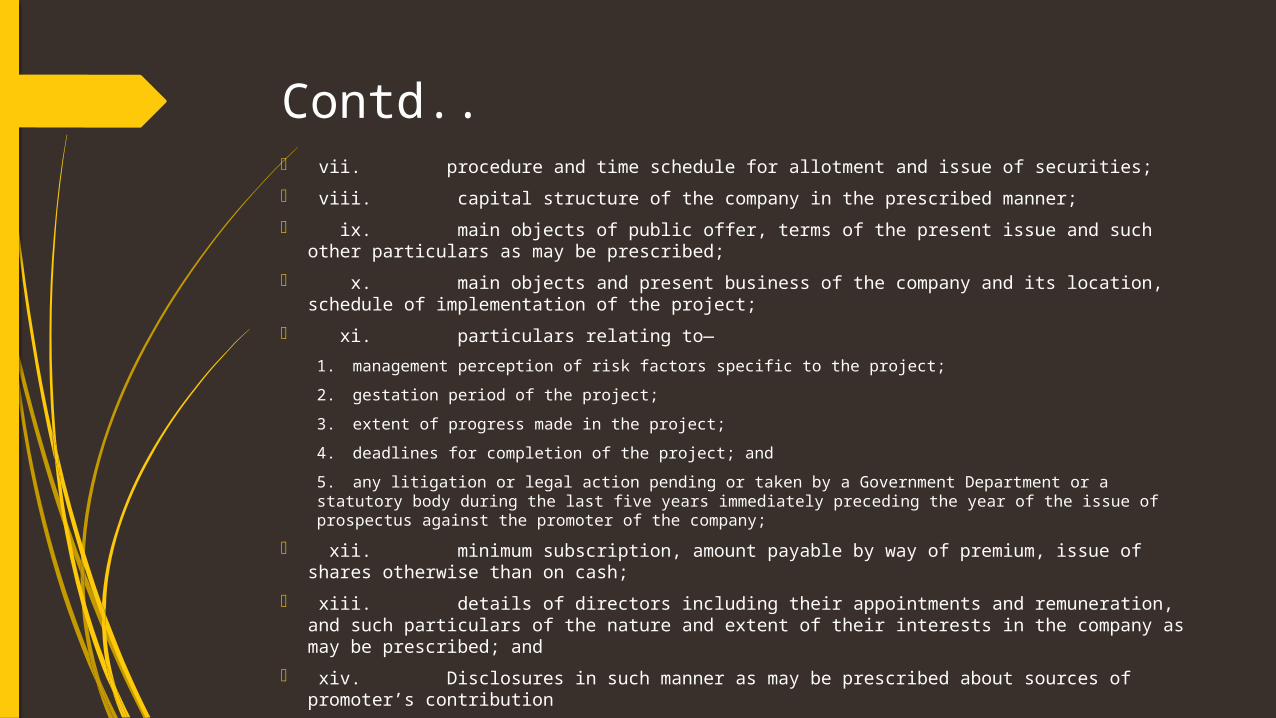

Contd.. vii. procedure and time schedule for allotment and issue of securities; viii. capital structure of the company in the prescribed manner; ix. main objects of public offer, terms of the present issue and such other particulars as

may be prescribed; x. main objects and present business of the company and its location, schedule of

implementation of the project; xi. particulars relating to—

1. management perception of risk factors specific to the project;2. gestation period of the project;3. extent of progress made in the project;4. deadlines for completion of the project; and5. any litigation or legal action pending or taken by a Government Department or a statutory body during the last five years immediately preceding the year of the issue of prospectus against the promoter of the company;

xii. minimum subscription, amount payable by way of premium, issue of shares otherwise than on cash;

xiii. details of directors including their appointments and remuneration, and such particulars of the nature and extent of their interests in the company as may be prescribed; and

xiv. Disclosures in such manner as may be prescribed about sources of promoter’s contribution

Reports with prospectus i. Reports by the auditors of the company with respect to its profits

and losses and assets and liabilities and such other matters as may be prescribed;

ii. Reports relating to profits and losses for each of the five financial years immediately preceding the financial year of the issue of prospectus including such reports of its subsidiaries and in such manner as may be prescribed. Where company has not completed five financial years than such report for all financial years is required.

iii. Reports made in the prescribed manner by the auditors upon the profits and losses of the business of the company for each of the five financial years immediately preceding issue and assets and liabilities of its business on the last date to which the accounts of the business were made up, being a date not more than one hundred and eighty days before the issue of the prospectus. Where company has not completed five financial years than such report for all financial years is required.

iv. Reports about the business or transaction to which the proceeds of the securities are to be applied directly or indirectly.

Declaration of Compliance:

Every prospectus shall make a declaration about the compliance of the provisions of this Act and a statement to the effect that nothing in the prospectus is contrary to the provisions of this Act, the Securities Contracts (Regulation) Act, 1956 and the Securities and Exchange Board of India Act, 1992 and the rules and regulations made there under.

Other matters in Prospectus:

Clause (d) of Sub – section (1) of section 26 give unlimited power to central government to list other matters and set out other reports to be included in a prospectus

Delivery of Prospectus with Registrar:

A copy of prospectus shall be delivered to the Registrar for registration signed by every person who is named as a director or proposed director of the company or by his duly authorised attorney on or before the date of its publication and only then it shall be issued by or on behalf of a company or in relation to an intended company.

Statement of an Expert: A statement made by an expert shall be included only if expert is or was

engaged or interested in the formation or promotion or management of the company and has given his written consent to the issue of the prospectus.

Such consent of expert must not be withdrawn by his before the delivery of prospectus to the Registrar for registration and a statement to that effect shall be included in the prospectus.

Every prospectus issued shall state that a copy has been delivered to the Registrar and specify attached documents.

The registrar shall not register a prospectus all requirements has been complied with and the prospectus is accompanied by the consent in writing of all the person named in the prospectus.

Prospectus shall not be valid if it is issued more than ninety days after the date on which a copy thereof delivered to the Registrar.

Caution:

If a prospectus is issued in contravention of the provisions of section 26, the company shall be punishable with fine which shall not be less than fifty thousand rupees but which may extend to three lakh rupees and every person who is knowingly a party to the issue of such prospectus shall be punishable with imprisonment for a term which may extend to three years or with fine which shall not be less than fifty thousand rupees but which may extend to three lakh rupees, or with both

VARIATION IN TERMS OF CONTRACT OR OBJECTS IN PROSPECTUS (SECTION 27): A company may vary the terms of a contract refered in the prospectus

or object for which the prospectus was issued, only under approval or authority given by way of special resolution.

Requirement in Deemed Prospectus (Section 25): Section 26 as applied by Section 25 shall have effect as if —1. it required a prospectus to state in addition to the matters required by section 26 to be stated in a prospectus— i. the net amount of the consideration received or to be received by the company in respect of the securities to which the offer relates; and ii. the time and place at which the contract where under the said securities have been or are to be allotted may be inspected;2. the persons making the offer were persons named in a prospectus as directors of a company.

STATEMENT IN LIEU OF PROSPECTUS

Similar to actual prospectus but without the invitation to the public for subscribing to the shares of the company

Prepared when a company issues shares by private placement. Prepared for the purpose of record, and it is filed with the Registrar of

Companies before allotment of share. The prospectus contains a summary of the past, present and prospects

of the company The prospectus expressly invites the public to buy shares issued by the

company It is the basis of share issue. The contents of prospectus are considered

legal evidence in the event of dispute between share holder and the company.

A misleading clause in the prospectus will be taken seriously by the courts.

Contents of the Prospectus

1. Name of company and location of the registered office of the company2. Main objects of the company3. The number and classes of the shares to be issued4. Names and addresses of the directors, managing director their qualification shares.5. Provisions regarding the remuneration of directors6. The minimum subscription to be raised by share issue7. The amounts payable on application, allotment for each class of shares9. Rights, privileges and restrictions each class of shareholders10. Underwriters to the issue11. Merchant bankers to the issue12. Registrars to the issue

The supreme executive authority controlling the management and affairs of a company vests in the team of directors of the company, collectively known as its Board of Directors.

.Section 2 (10) of the Companies Act, 2013 defined that “Board of Directors” or “Board”, in relation to a company, means the collective body of the directors of the company.

Companies Act, 2013 has brought in the concept of Key Managerial Personnel

MANAGEMENT OF COMPANIES

DIRECTORS OF COMPANY

An appointed or elected member of the board of directors of a company. He has the responsibility for determining and implementing the

company’s policy. Directors derive their powers emanating from board resolutions. Unlike shareholders, directors cannot participate through proxy. Unlike employees, cannot absolve themselves of their responsibility for

the delegated duties

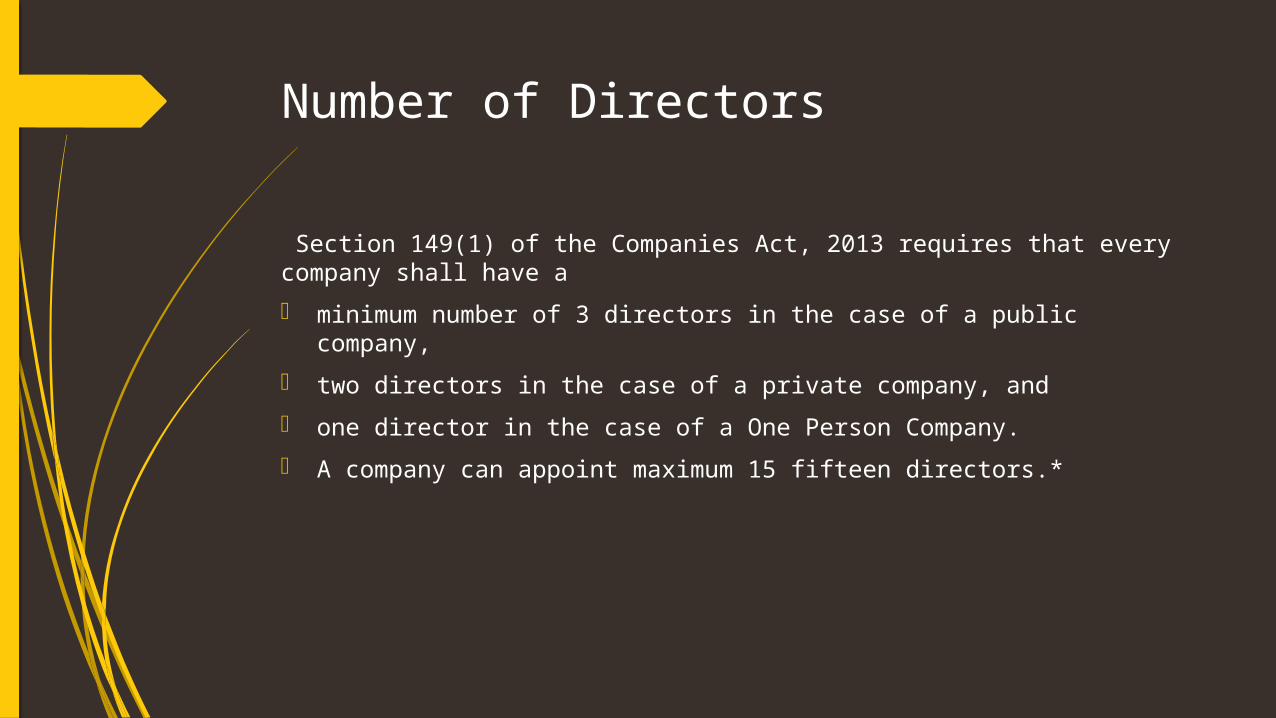

Number of Directors

Section 149(1) of the Companies Act, 2013 requires that every company shall have a minimum number of 3 directors in the case of a public company, two directors in the case of a private company, and one director in the case of a One Person Company. A company can appoint maximum 15 fifteen directors.*

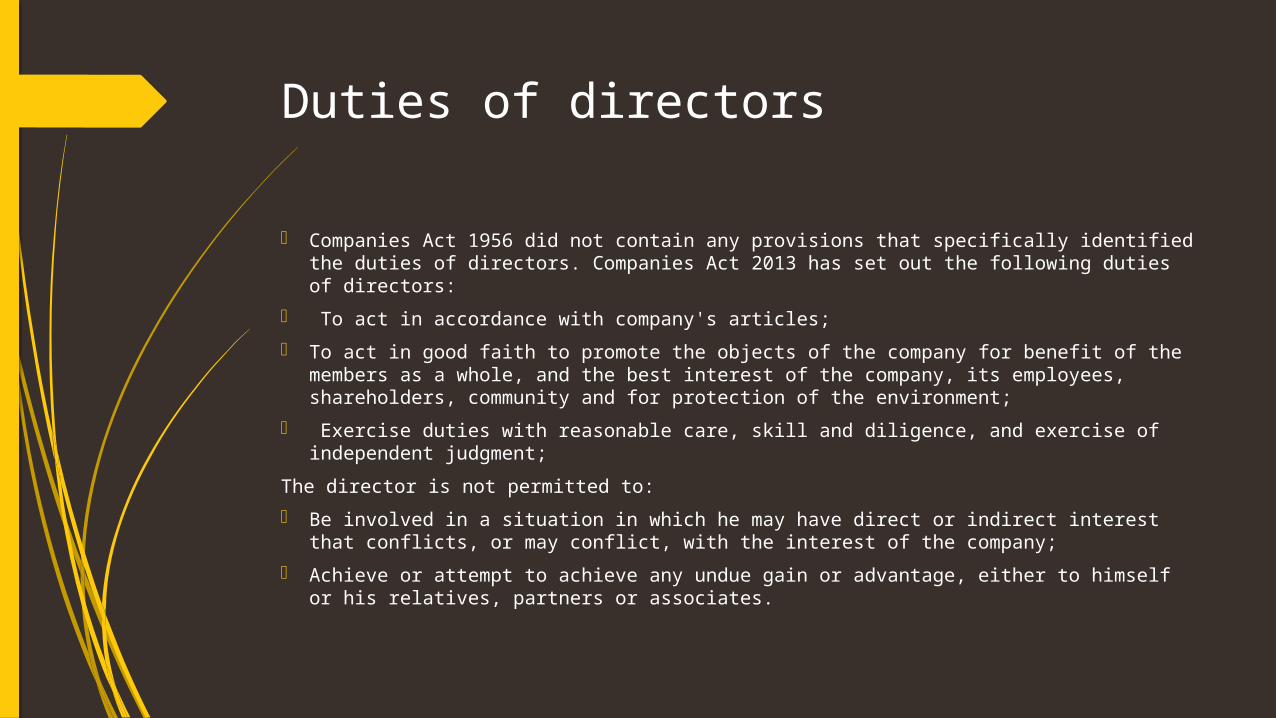

Duties of directors

Companies Act 1956 did not contain any provisions that specifically identified the duties of directors. Companies Act 2013 has set out the following duties of directors:

To act in accordance with company's articles; To act in good faith to promote the objects of the company for benefit of the members

as a whole, and the best interest of the company, its employees, shareholders, community and for protection of the environment;

Exercise duties with reasonable care, skill and diligence, and exercise of independent judgment;

The director is not permitted to: Be involved in a situation in which he may have direct or indirect interest that

conflicts, or may conflict, with the interest of the company; Achieve or attempt to achieve any undue gain or advantage, either to himself or his

relatives, partners or associates.

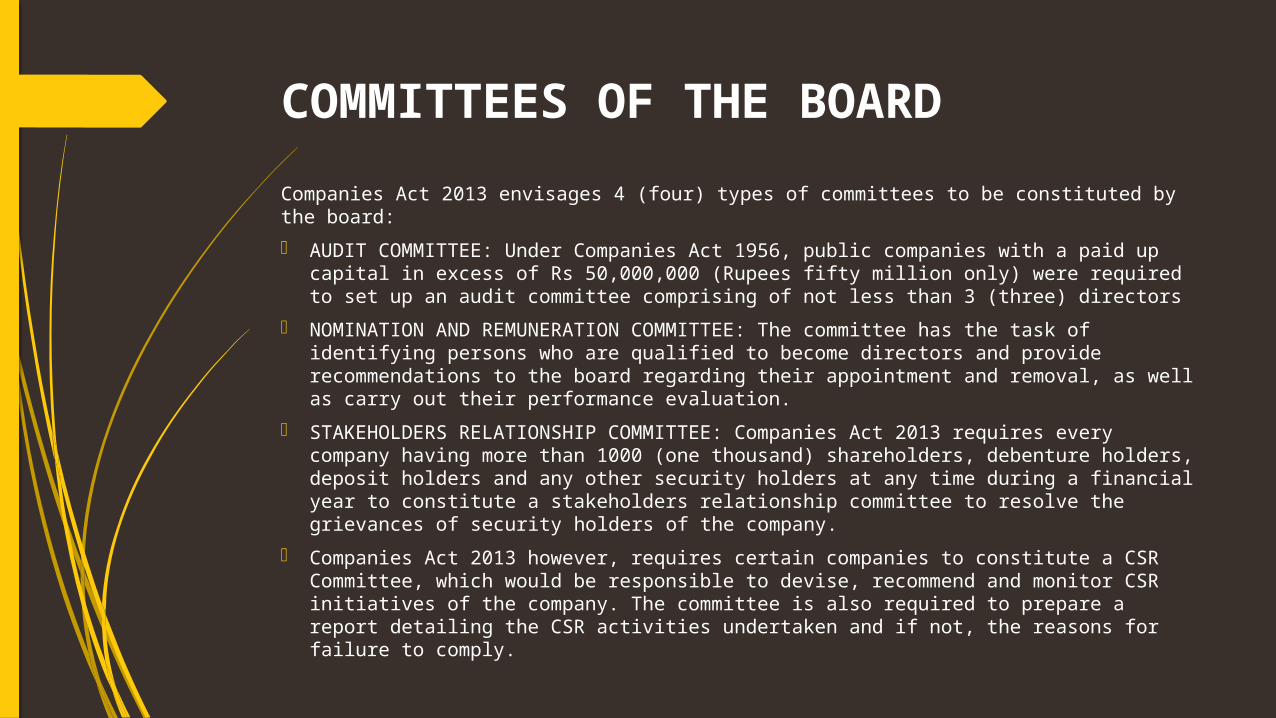

COMMITTEES OF THE BOARDCompanies Act 2013 envisages 4 (four) types of committees to be constituted by the board: AUDIT COMMITTEE: Under Companies Act 1956, public companies with a paid up

capital in excess of Rs 50,000,000 (Rupees fifty million only) were required to set up an audit committee comprising of not less than 3 (three) directors

NOMINATION AND REMUNERATION COMMITTEE: The committee has the task of identifying persons who are qualified to become directors and provide recommendations to the board regarding their appointment and removal, as well as carry out their performance evaluation.

STAKEHOLDERS RELATIONSHIP COMMITTEE: Companies Act 2013 requires every company having more than 1000 (one thousand) shareholders, debenture holders, deposit holders and any other security holders at any time during a financial year to constitute a stakeholders relationship committee to resolve the grievances of security holders of the company.

Companies Act 2013 however, requires certain companies to constitute a CSR Committee, which would be responsible to devise, recommend and monitor CSR initiatives of the company. The committee is also required to prepare a report detailing the CSR activities undertaken and if not, the reasons for failure to comply.

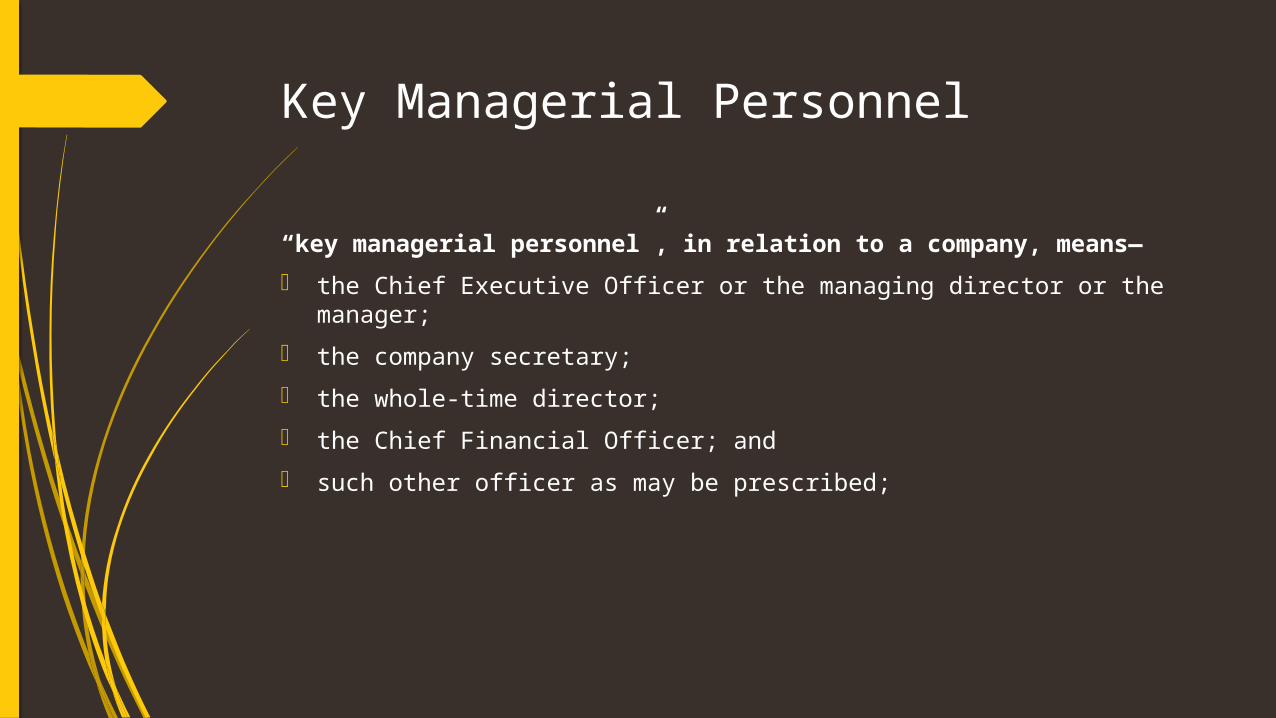

Key Managerial Personnel

“key managerial personnel”, in relation to a company, means— the Chief Executive Officer or the managing director or the manager; the company secretary; the whole-time director; the Chief Financial Officer; and such other officer as may be prescribed;

BOARD MEETINGS AND PROCESSES

First board meeting of a company to be held within 30 (thirty) days of incorporation

Notice of minimum 7 (seven) days must be given for each board meeting

Companies Act 2013 has permitted directors to participate in board meetings through video conferencing or other audio visual means which are capable of recording and recognising the participation of directors.

Meeting

Members MeetingAnnual General

MeetingExtra Ordinary

General Meeting Class Meeting

ANNUAL GENERAL MEETING (AGM) (Sec. 96)1. Annual general meeting should be held once every year.2. First annual general meeting of the company should be held within 9

months from the closing of the first financial year. Hence it shall not be necessary for the company to hold any annual general meeting in the year of its incorporation.

3. Subsequent annual general meeting of the company should be held within 6 months from the closing of the financial year.

4. The gap between two annual general meetings should not exceed 15 months.

EXTRA ORDINARY GENERAL MEETING

By Board [Section 100 (1)]The Board may, whenever it deems fit, call an extraordinary general meeting of

the company. (II) By Board on requisition [Section 100 (2)]

The Board must call an extraordinary general meeting on receipt of the requisition (III) By requisitionists [Section 100(4)]

If the Board does not within 21 days from the date of receipt of a valid requisition in regard to any matter, proceed to call a meeting for the consideration of that matter on a day not later than 45 days from the date of receipt of such requisition (IV) By Tribunal [Section 98 (not yet enforced)]

Section 98 provides that if for any reason it is impracticable to call a meeting of a company or to hold or conduct the meeting of the company, the Tribunal may, either suo motu or on the application of any director or member of the company who would be entitled to vote at the meeting

NOTICE OF THE MEETING

A general meeting of a company may be called by giving not less than 21 clear days’ notice either in writing or through electronic mode. Notice through electronic mode shall be given in such manner as may be prescribed.

Short noticeA general meeting may be called after giving a shorter notice also if

consent is given in writing or by electronic mode by not less than 95% of the members entitled to vote at such meeting. CONTENTS OF NOTICE

Place of meeting Day of meeting Time of meeting Agenda Proxy clause with reasonable prominence

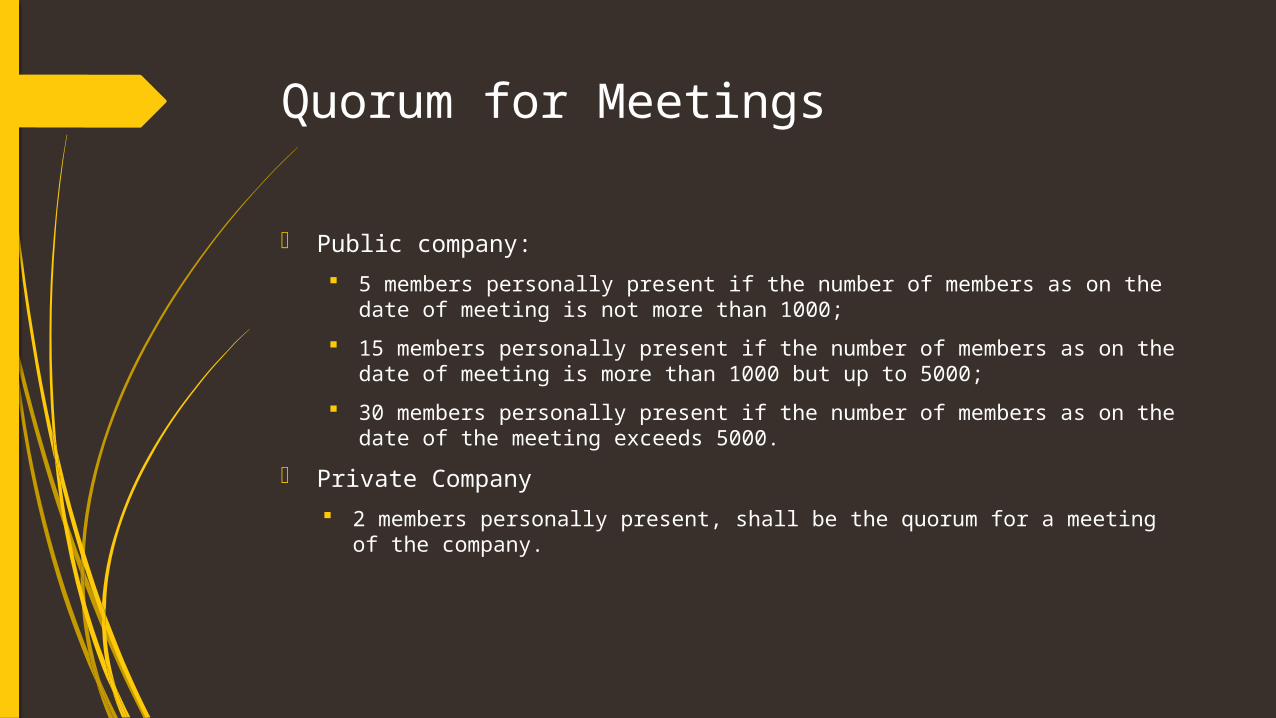

Quorum for Meetings

Public company: 5 members personally present if the number of members as on the date of

meeting is not more than 1000; 15 members personally present if the number of members as on the date of

meeting is more than 1000 but up to 5000; 30 members personally present if the number of members as on the date of

the meeting exceeds 5000. Private Company

2 members personally present, shall be the quorum for a meeting of the company.

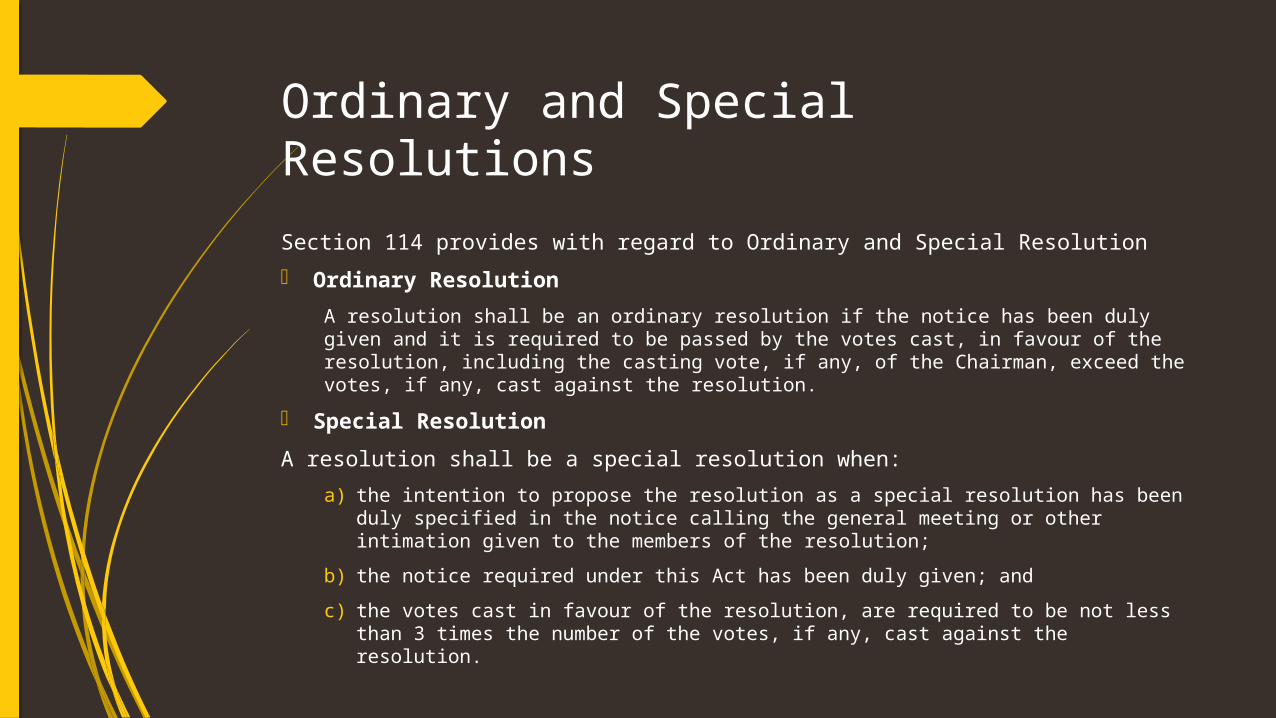

Ordinary and Special Resolutions

Section 114 provides with regard to Ordinary and Special Resolution Ordinary Resolution

A resolution shall be an ordinary resolution if the notice has been duly given and it is required to be passed by the votes cast, in favour of the resolution, including the casting vote, if any, of the Chairman, exceed the votes, if any, cast against the resolution.

Special ResolutionA resolution shall be a special resolution when:

a) the intention to propose the resolution as a special resolution has been duly specified in the notice calling the general meeting or other intimation given to the members of the resolution;

b) the notice required under this Act has been duly given; andc) the votes cast in favour of the resolution, are required to be not less than 3

times the number of the votes, if any, cast against the resolution.

Contd..

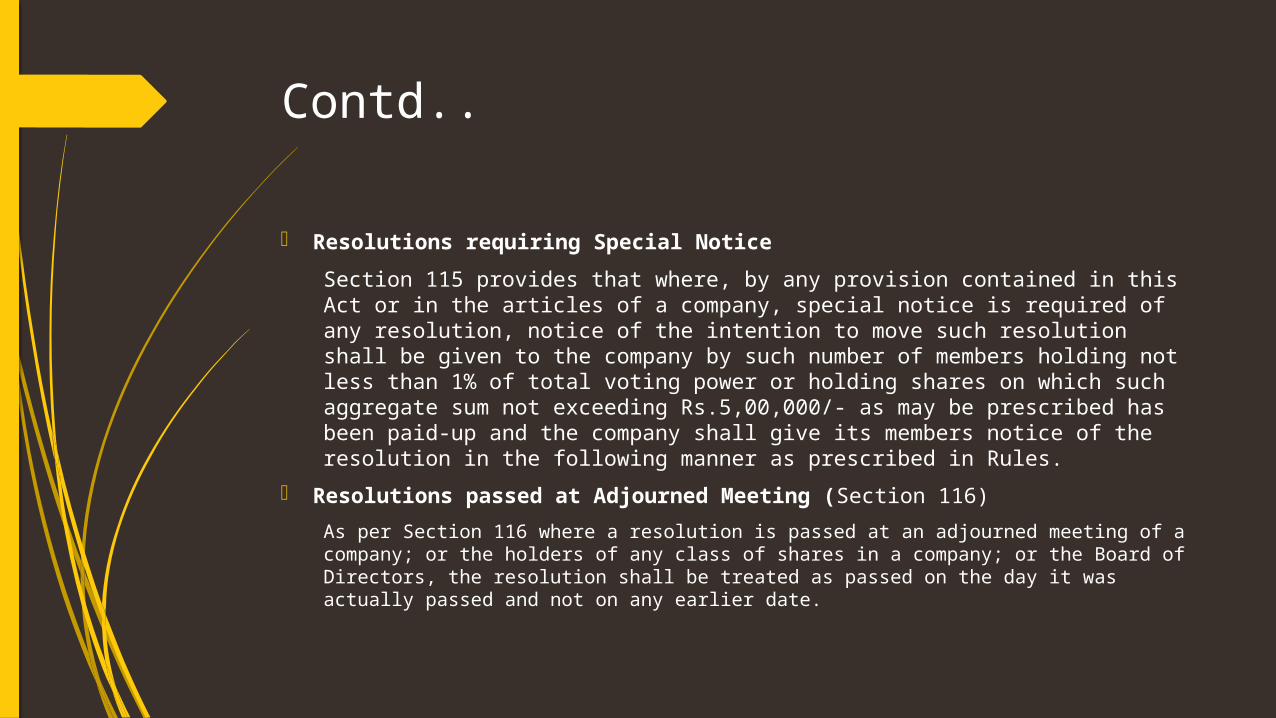

Resolutions requiring Special NoticeSection 115 provides that where, by any provision contained in this Act or in the articles of a company, special notice is required of any resolution, notice of the intention to move such resolution shall be given to the company by such number of members holding not less than 1% of total voting power or holding shares on which such aggregate sum not exceeding Rs.5,00,000/- as may be prescribed has been paid-up and the company shall give its members notice of the resolution in the following manner as prescribed in Rules.

Resolutions passed at Adjourned Meeting (Section 116)As per Section 116 where a resolution is passed at an adjourned meeting of a company; or the holders of any class of shares in a company; or the Board of Directors, the resolution shall be treated as passed on the day it was actually passed and not on any earlier date.

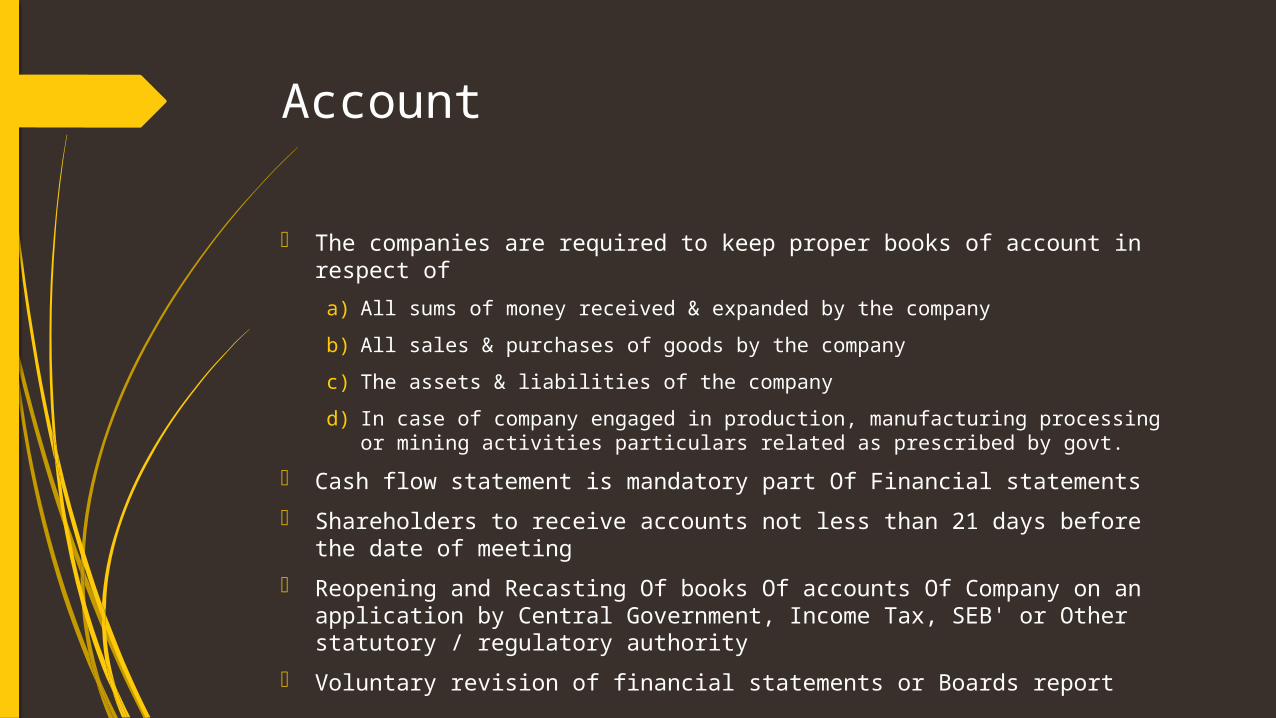

Account

The companies are required to keep proper books of account in respect ofa) All sums of money received & expanded by the companyb) All sales & purchases of goods by the companyc) The assets & liabilities of the companyd) In case of company engaged in production, manufacturing processing or

mining activities particulars related as prescribed by govt. Cash flow statement is mandatory part Of Financial statements Shareholders to receive accounts not less than 21 days before the date of

meeting Reopening and Recasting Of books Of accounts Of Company on an

application by Central Government, Income Tax, SEB' or Other statutory / regulatory authority

Voluntary revision of financial statements or Boards report

Auditors

Mandatory auditor rotation for listed and other prescribed companies every 5 years

Members Of a company may resolve to provide that in the audit firm appointed by it, the auditing partner and his team shall be rotated at such intervals as may be specified in the resolution

Auditor will be required to immediately report to the central movement upon reasonable suspicion Of any offence involving fraud

Winding Up of a Company

Winding up of a company is the process whereby its life is ended i.e. , the company dissolved and its property administered for the benefit of its creditors and members.

Modes of Winding up - According to sec. 270 of the companies Act 2013, the procedure for winding up of a company can be initiated either -i. By the tribunal or,ii. Voluntary

Winding up by a tribunal As per new Companies Act 2013, a company can be wound up by a

tribunal on the basis of following reasons:1. Unable to pay debts2. If the company has by special resolution resolved that the company

would be wound up by the tribunal.3. Acted against the interest of the integrity or morality of India,

security of the state, or has spoiled any kind of friendly relations with foreign or neighbouring countries.

4. Not filled financial statements for preceding 5 consecutive years.5. If the tribunal by any means finds that it is just & equitable that the

company should be wound up.6. Indulged in fraudulent activities or any unlawful business, or any

person or management connected with the formation of company is found guilty of fraud, or any kind of misconduct.

Filling of winding up petition

Sec. 272 provides that a petition is to be filed in the prescribed format and is to be submitted in 3 sets by any of the following persons: 1. The company2. The creditors3. Any contributories4. By the central or state govt.5. By the registrar of any person authorized by central govt. After preparing the statement it shall be certified by a practising Chartered Accountant.

Final order and its content

The tribunal after hearing the petition has the power to dismiss it or to make an interim order as it think appropriate or it can appoint the provisional liquidator of the company till the passing of winding u order.

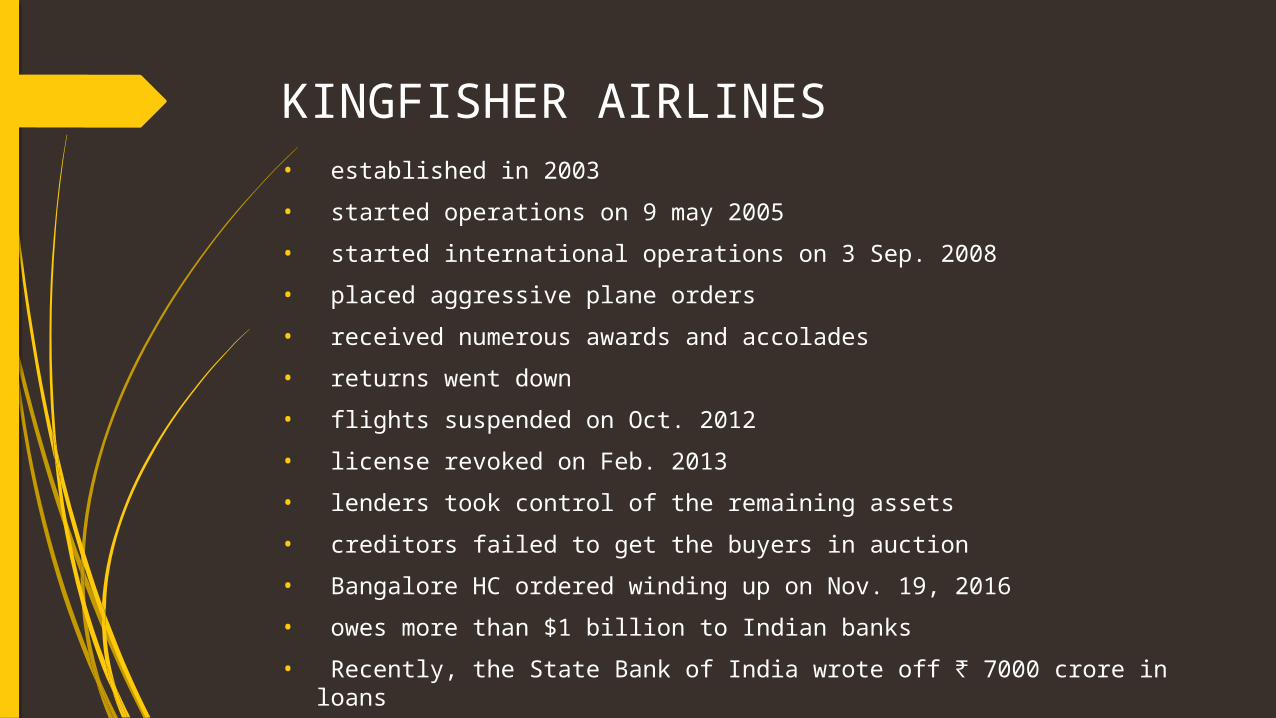

KINGFISHER AIRLINES• established in 2003• started operations on 9 may 2005• started international operations on 3 Sep. 2008• placed aggressive plane orders• received numerous awards and accolades• returns went down• flights suspended on Oct. 2012• license revoked on Feb. 2013• lenders took control of the remaining assets• creditors failed to get the buyers in auction• Bangalore HC ordered winding up on Nov. 19, 2016• owes more than $1 billion to Indian banks• Recently, the State Bank of India wrote off ₹ 7000 crore in loans

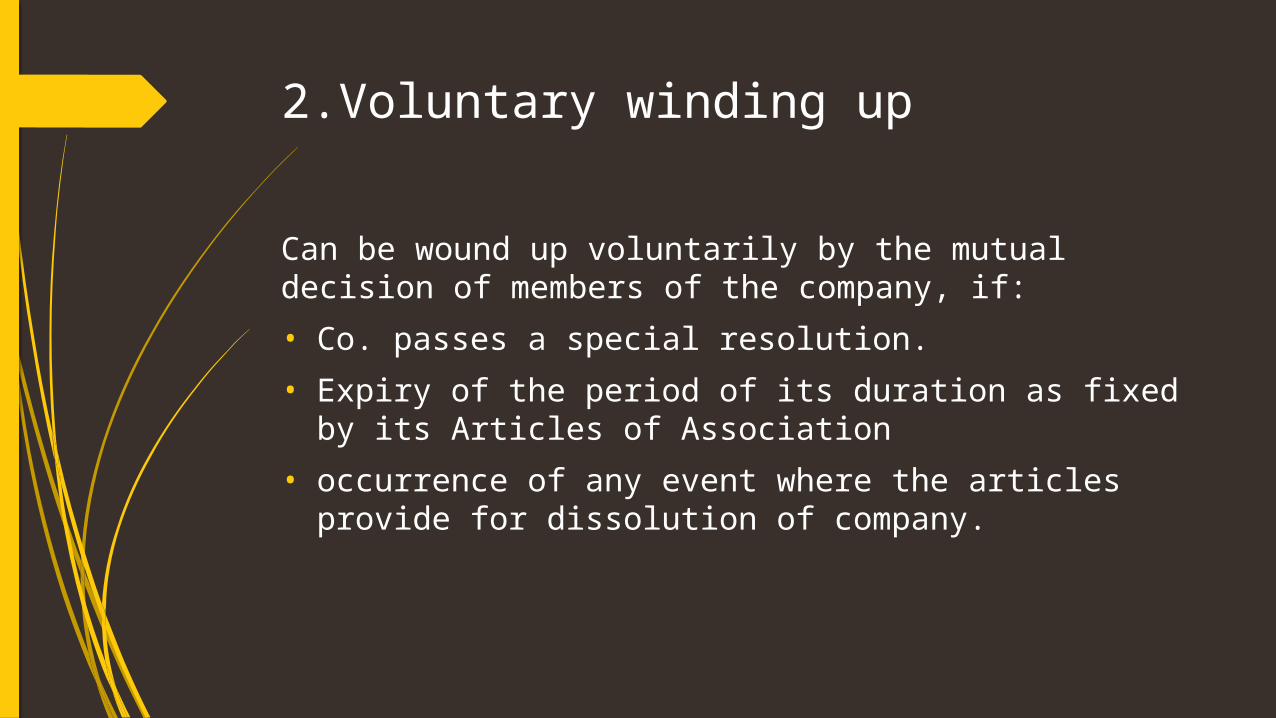

2.Voluntary winding up

Can be wound up voluntarily by the mutual decision of members of the company, if:• Co. passes a special resolution.• Expiry of the period of its duration as fixed by its

Articles of Association• occurrence of any event where the articles provide for

dissolution of company.

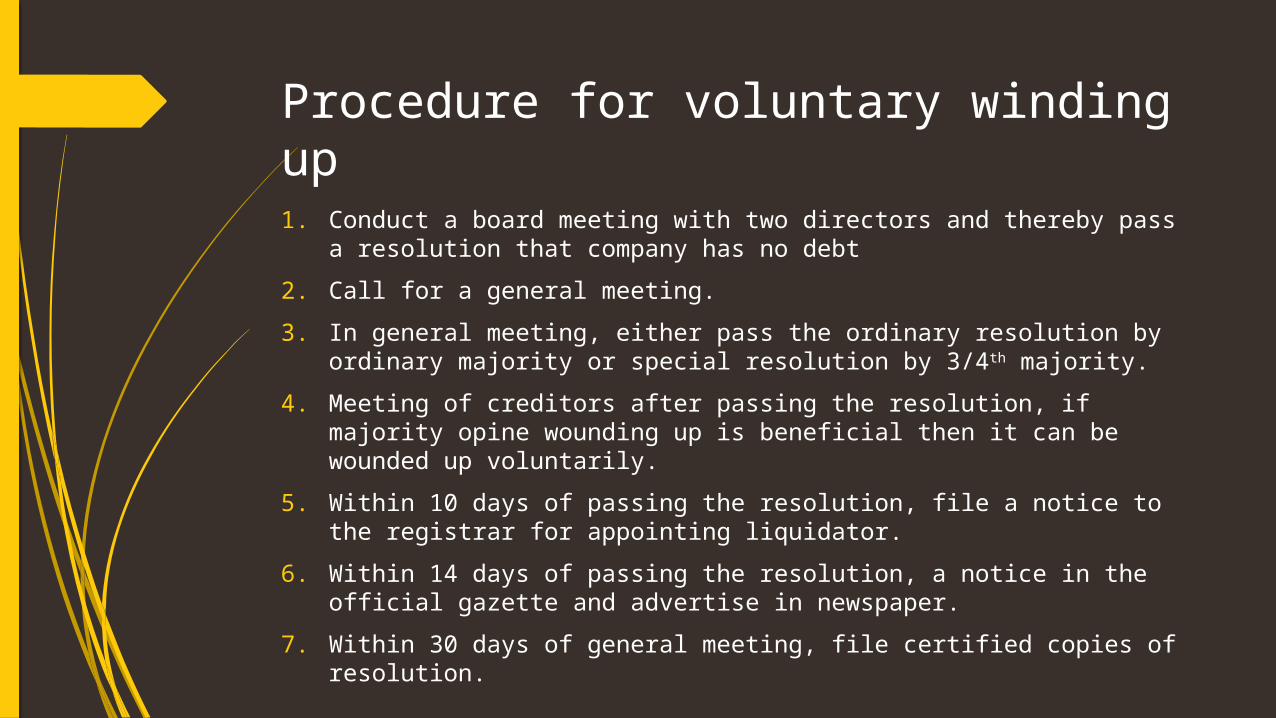

Procedure for voluntary winding up

1. Conduct a board meeting with two directors and thereby pass a resolution that company has no debt

2. Call for a general meeting.3. In general meeting, either pass the ordinary resolution by ordinary

majority or special resolution by 3/4th majority.4. Meeting of creditors after passing the resolution, if majority opine

wounding up is beneficial then it can be wounded up voluntarily.5. Within 10 days of passing the resolution, file a notice to the registrar

for appointing liquidator.6. Within 14 days of passing the resolution, a notice in the official gazette

and advertise in newspaper.7. Within 30 days of general meeting, file certified copies of resolution.

Contd..

8. Wind up affairs of the co. and prepare the liquidators account and get the same audited.

9. Conduct a general meeting of the company.10. Pass a special resolution for disposal of books and all necessary

documents of the co.11. Within 15 days of final general meeting, submit a copy of accounts and

file an application to the tribunal for passing order of dissolution.12. If tribunal is satisfied, he shall pass the order within 60 days of

receiving such application.13. Appointed liquidator then file a copy of order with registrar.14. The registrar then publish a notice in the official gazette declaring that

the co. is dissolved.

Types of voluntary winding up :

Types of Voluntary Winding up - Voluntary winding up may be of two types, namely,a) Members’ voluntary winding up ; b) Creditors’ voluntary winding up.

A) Members’ Voluntary Winding up - Members’ voluntary winding up is possible only in case of solvent companies. 1) DECLARATION OF SOLVENCY (S448)–

The directors must enquire whether the company will be able to able to pay all its debts within the period of 3 years.

In order to be effective, this declaration must be made within 5 weeks immediately preceding the date of passing of the winding up resolution by the members;

delivered to the Registrar for filing ; and must be accompanied by a copy of the report of the auditors of the company on

the accounts and balance sheet.

Appointment and remuneration of liquidators: (S492) the company in general meeting must:a) appoint one or more liquidatorsb) fix the remuneration

Any remuneration so fixed cannot be increased in any circumstances whatever, whether with or without the sanction of the court. No liquidator shall charge of his office unless his remuneration is fixed.

Board’s power to cease: (S491)on the appointment of the liquidators all the powers of the directors cease but their powers may continue if the general body or the liquidator sanctions it.

Notice of the appointment of the liquidator to be given to the registrar(S493):within 10 days of his appointment .otherwise Rs.1000 fine per day.

Power of liquidator to accept shares, etc., as consideration of sales of property of the company(S497):

Duty of liquidator to call creditors meeting in case of insolvency S495 : if the liquidator finds that the company will not be able to pay its debts he should tell it to the creditors with all records.

Duty of liquidator to call general meeting at the end of each year(S496): In case the winding takes more then one year the liquidator must call a general meeting and tell the acts and winding operations done by him.

Final meeting and dissolution(S497): the liquidator must(a)make up an account of the winding up showing how the company has been disposed of (b)call the general meeting of the company for laying the account before it as well as explanations.

B) Creditors Voluntary Winding Up :- Creditors’ voluntary winding up - Where the Board of directors does not file a declaration as to solvency of the company, the voluntary winding up is called ‘ the Creditors voluntary winding up.

- if the members and creditors nominate two different persons as liquidators creditors nominee shall become the liquidator of the company.

- Besides, in the case of creditors winding up if the creditors so wish a committee of inspection ‘ may be appointed to work along with the liquidator's.

Notice to registrar: A company of any resolution passed at the creditors meeting must be filed with the registrar within 10 days of the passing thereof. otherwise fine of 500 Rs per day(S501).

Appointment of liquidator: (S502) the creditors and the members at their respective first meeting may nominate a person to be liquidator but should take the board of directors into considerations.

Committee of inspection(S503): The creditors at their first or any subsequent meeting, appoint a committee of inspection of not more than 5 members.

Fixing of liquidator’s remuneration(S505): the remuneration of the liquidator is fixed by the committee of inspection.

Board’s power to cease on appointment of liquidator(S505): all the powers of the directors should go to the liquidator.

Duty of liquidator to call meeting of company and creditors at the end of each year[S508]: within 3 months from the end of the year.

Final meeting and dissolution [S509]

Voluntary winding up under supervision of the court :

A voluntary winding up may be effected under supervision of the Court where an application to that effect is made by a creditor or a contributory or the company or the liquidator and the Court makes an order that the voluntary winding up should continue subject to the supervision of the Court.

Such an order is passed by the Court where (i) the resolution for winding up was obtained by fraud, or (ii) the rules relating to the winding up order have not been observed, or(iii) the liquidator is prejudicial or is negligent in collecting the assets.

The Court is also empowered under the section 527 to make an order for compulsory winding up superseding the order of winding up under its supervision.

Contributory :

Contributory - the term ‘ contributory ‘ is defined under section 428 to mean every person liable to contribute to the assets of a company in the event of its being wound up.

The expression includes the holder of any shares which are fully paid up.

A past member shall however be not liable to contribute if he ceased to be a member for one year or more before the commencement of the winding up.

![THE PARTNERSHIP ACT, 1932 (IX OF 1932) - Punjab PARTNERSHIP ACT, 1… · TEXT THE PARTNERSHIP ACT, 1932 (IX OF 1932) [8th April 1932] An Act to define and amend the law relating to](https://img.pdfslide.us/doc/110x75/5a797b9f7f8b9ade698c0b32/the-partnership-act-1932-ix-of-1932-partnership-act-1text-the-partnership.jpg)