Embed Size (px)

Citation preview

#DeMo to #NaMoRelevant proposals and way ahead

BY JAIN SHRIMAL & CO.

JAIPUR|MUMBAI

Executive Summary

Tax Rates

Other Proposals

GST

(C) JAIN SHRIMAL & CO. 2

INDEX

Executive Summary #QUICK #GRAB

(C) JAIN SHRIMAL & CO. 3

(C) JAIN SHRIMAL & CO. 4

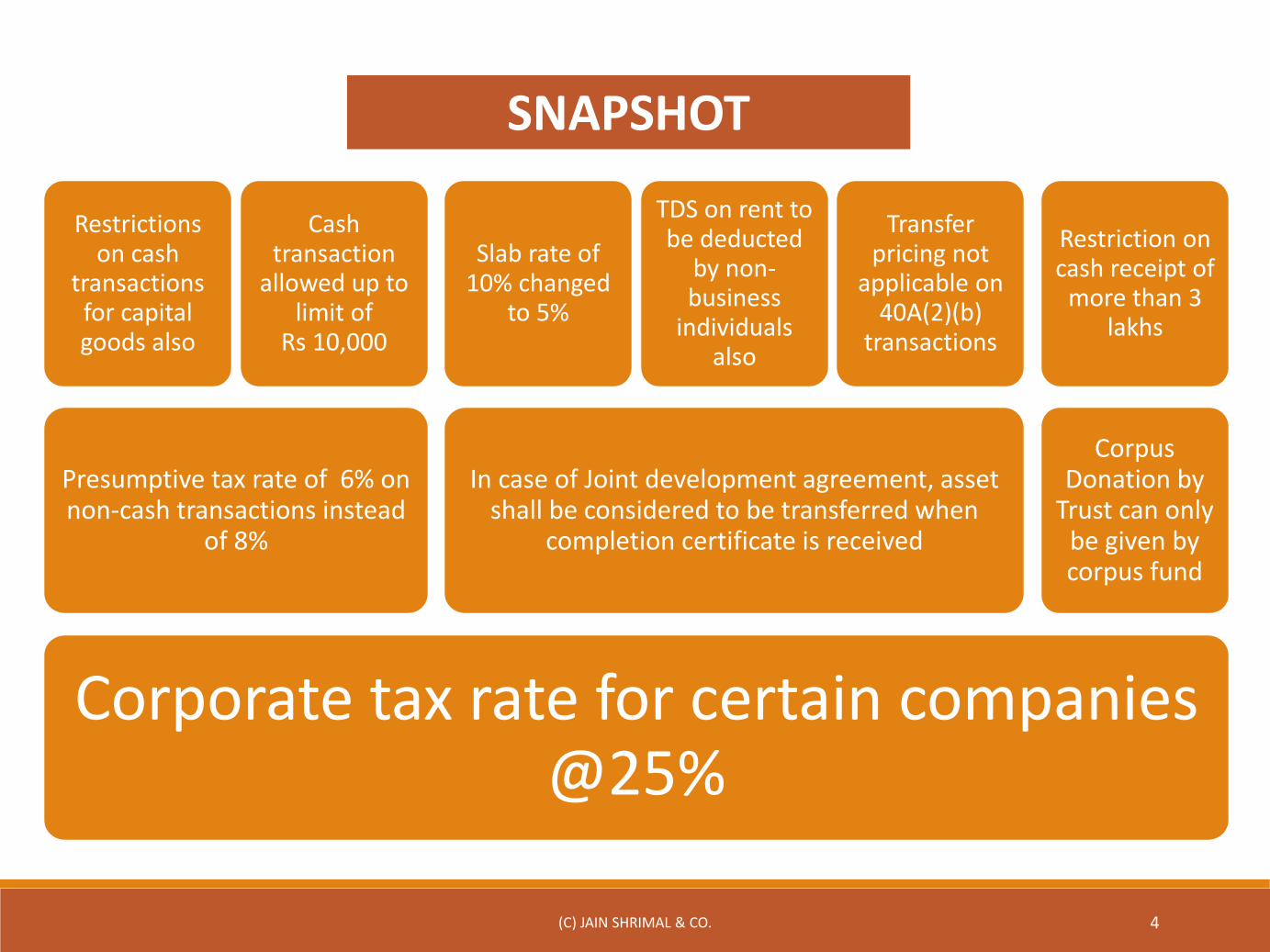

Corporate tax rate for certain companies @25%

Presumptive tax rate of 6% on non-cash transactions instead

of 8%

Restrictions on cash

transactions for capital goods also

Cash transaction

allowed up to limit of

Rs 10,000

In case of Joint development agreement, asset shall be considered to be transferred when

completion certificate is received

Slab rate of 10% changed

to 5%

TDS on rent to be deducted

by non-business

individuals also

Transfer pricing not

applicable on 40A(2)(b)

transactions

Corpus Donation by

Trust can only be given by corpus fund

Restriction on cash receipt of

more than 3 lakhs

SNAPSHOT

Tax Rates#PINCH #LESS

(C) JAIN SHRIMAL & CO. 5

(C) JAIN SHRIMAL & CO. 6

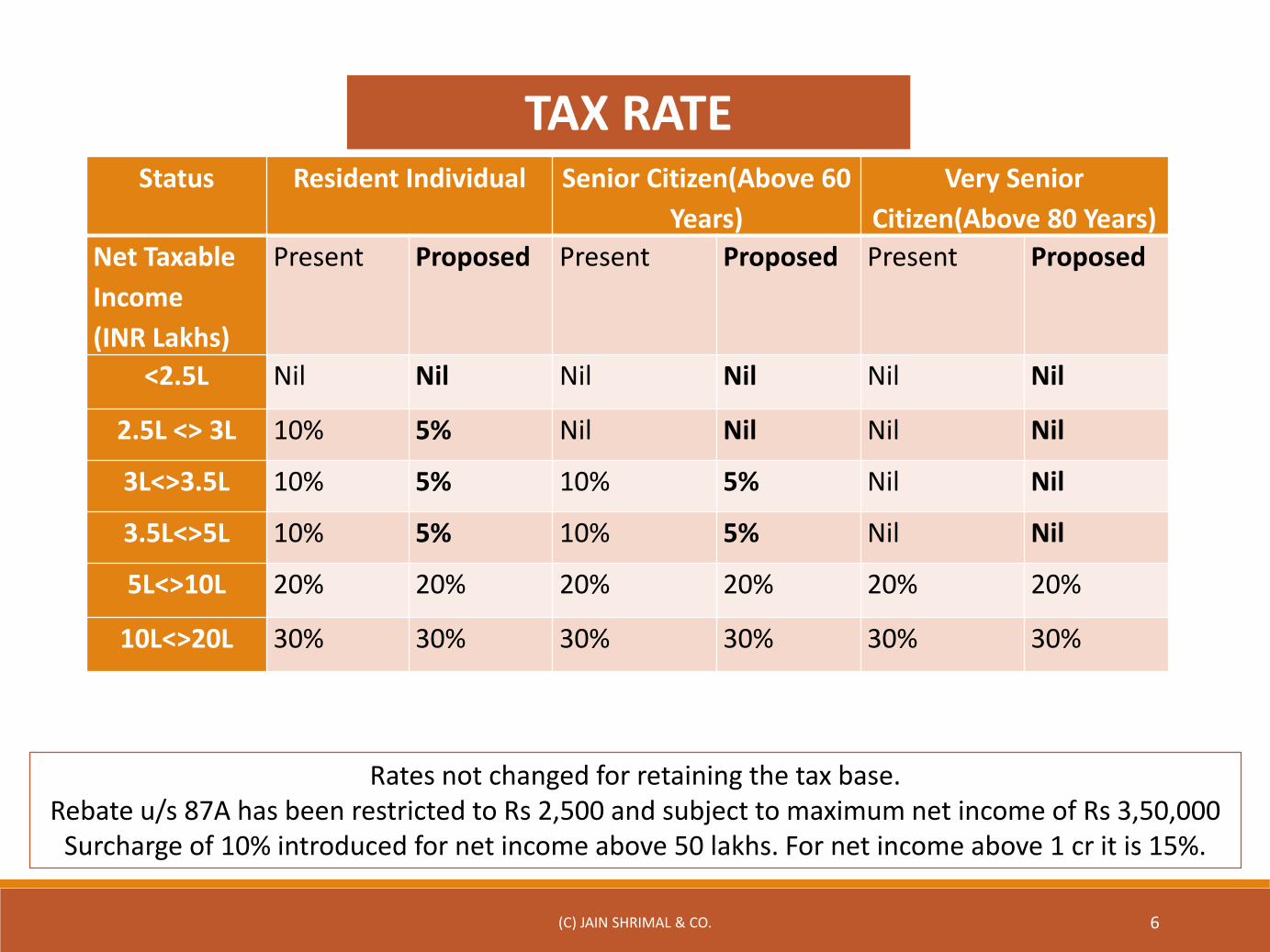

Status Resident Individual Senior Citizen(Above 60

Years)

Very Senior

Citizen(Above 80 Years)

Net Taxable

Income

(INR Lakhs)

Present Proposed Present Proposed Present Proposed

<2.5L Nil Nil Nil Nil Nil Nil

2.5L <> 3L 10% 5% Nil Nil Nil Nil

3L<>3.5L 10% 5% 10% 5% Nil Nil

3.5L<>5L 10% 5% 10% 5% Nil Nil

5L<>10L 20% 20% 20% 20% 20% 20%

10L<>20L 30% 30% 30% 30% 30% 30%

Rates not changed for retaining the tax base.Rebate u/s 87A has been restricted to Rs 2,500 and subject to maximum net income of Rs 3,50,000

Surcharge of 10% introduced for net income above 50 lakhs. For net income above 1 cr it is 15%.

TAX RATE

(C) JAIN SHRIMAL & CO. 7

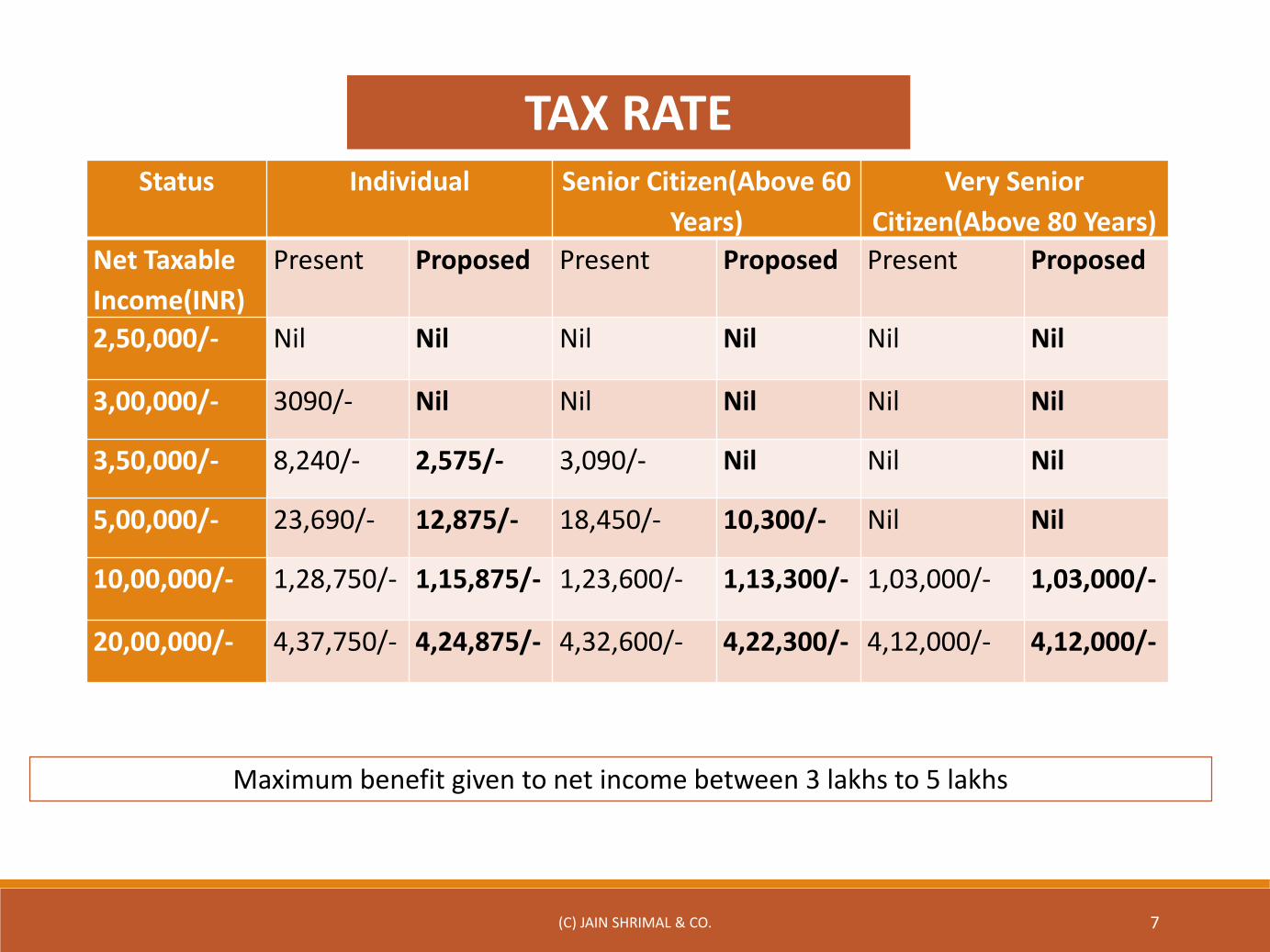

Status Individual Senior Citizen(Above 60

Years)

Very Senior

Citizen(Above 80 Years)

Net Taxable

Income(INR)

Present Proposed Present Proposed Present Proposed

2,50,000/- Nil Nil Nil Nil Nil Nil

3,00,000/- 3090/- Nil Nil Nil Nil Nil

3,50,000/- 8,240/- 2,575/- 3,090/- Nil Nil Nil

5,00,000/- 23,690/- 12,875/- 18,450/- 10,300/- Nil Nil

10,00,000/- 1,28,750/- 1,15,875/- 1,23,600/- 1,13,300/- 1,03,000/- 1,03,000/-

20,00,000/- 4,37,750/- 4,24,875/- 4,32,600/- 4,22,300/- 4,12,000/- 4,12,000/-

Maximum benefit given to net income between 3 lakhs to 5 lakhs

TAX RATE

(C) JAIN SHRIMAL & CO. 8

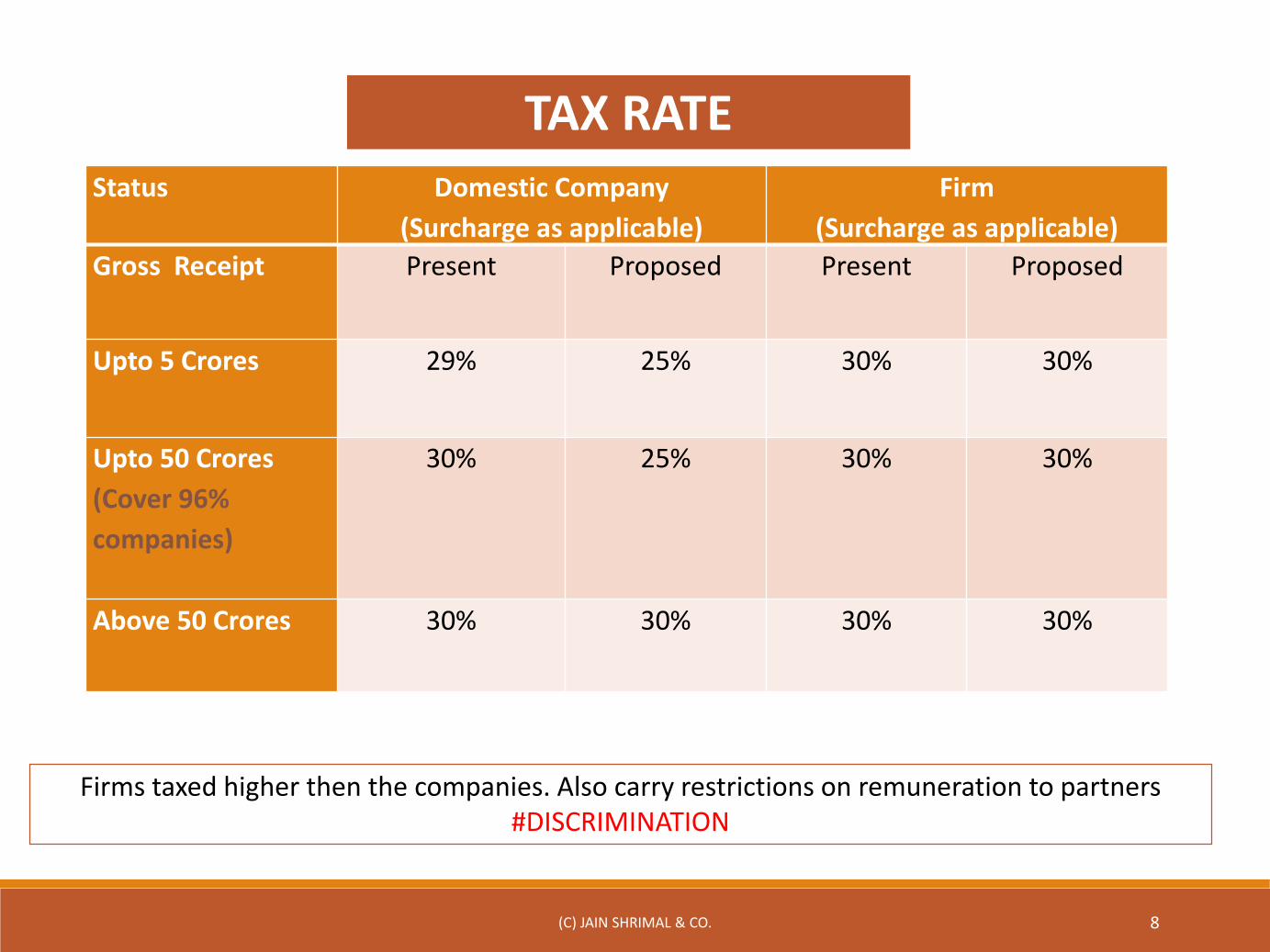

Status Domestic Company

(Surcharge as applicable)

Firm

(Surcharge as applicable)

Gross Receipt Present Proposed Present Proposed

Upto 5 Crores 29% 25% 30% 30%

Upto 50 Crores

(Cover 96%

companies)

30% 25% 30% 30%

Above 50 Crores 30% 30% 30% 30%

Firms taxed higher then the companies. Also carry restrictions on remuneration to partners #DISCRIMINATION

TAX RATE

Other Proposals #DEVIL #IN #DETAIL

(C) JAIN SHRIMAL & CO. 9

(C) JAIN SHRIMAL & CO. 10

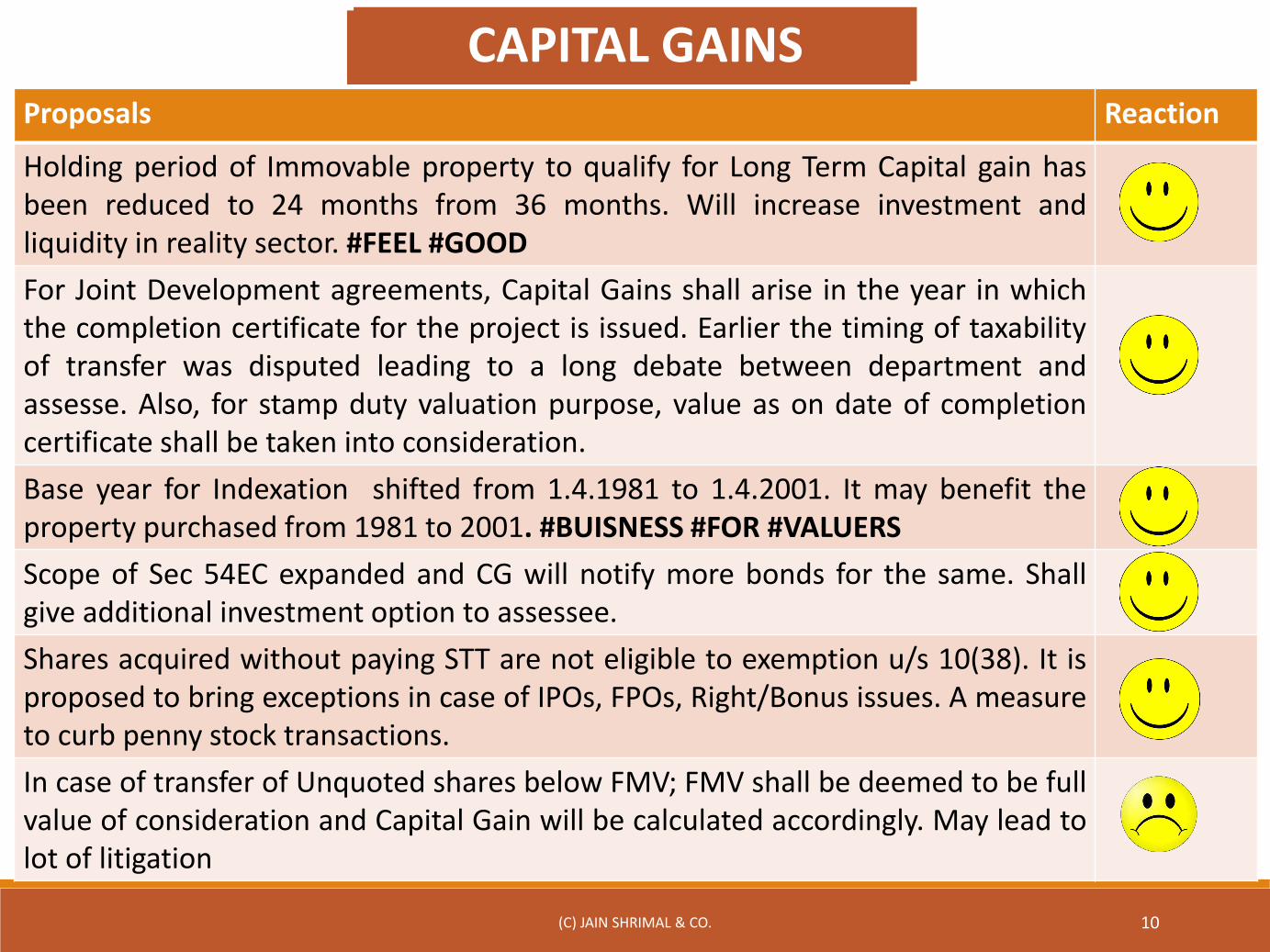

Proposals Reaction

Holding period of Immovable property to qualify for Long Term Capital gain hasbeen reduced to 24 months from 36 months. Will increase investment andliquidity in reality sector. #FEEL #GOOD

For Joint Development agreements, Capital Gains shall arise in the year in whichthe completion certificate for the project is issued. Earlier the timing of taxabilityof transfer was disputed leading to a long debate between department andassesse. Also, for stamp duty valuation purpose, value as on date of completioncertificate shall be taken into consideration.

Base year for Indexation shifted from 1.4.1981 to 1.4.2001. It may benefit theproperty purchased from 1981 to 2001. #BUISNESS #FOR #VALUERS

Scope of Sec 54EC expanded and CG will notify more bonds for the same. Shallgive additional investment option to assessee.

Shares acquired without paying STT are not eligible to exemption u/s 10(38). It isproposed to bring exceptions in case of IPOs, FPOs, Right/Bonus issues. A measureto curb penny stock transactions.

In case of transfer of Unquoted shares below FMV; FMV shall be deemed to be fullvalue of consideration and Capital Gain will be calculated accordingly. May lead tolot of litigation

CAPITAL GAINSCAPITAL GAINS

(C) JAIN SHRIMAL & CO. 11

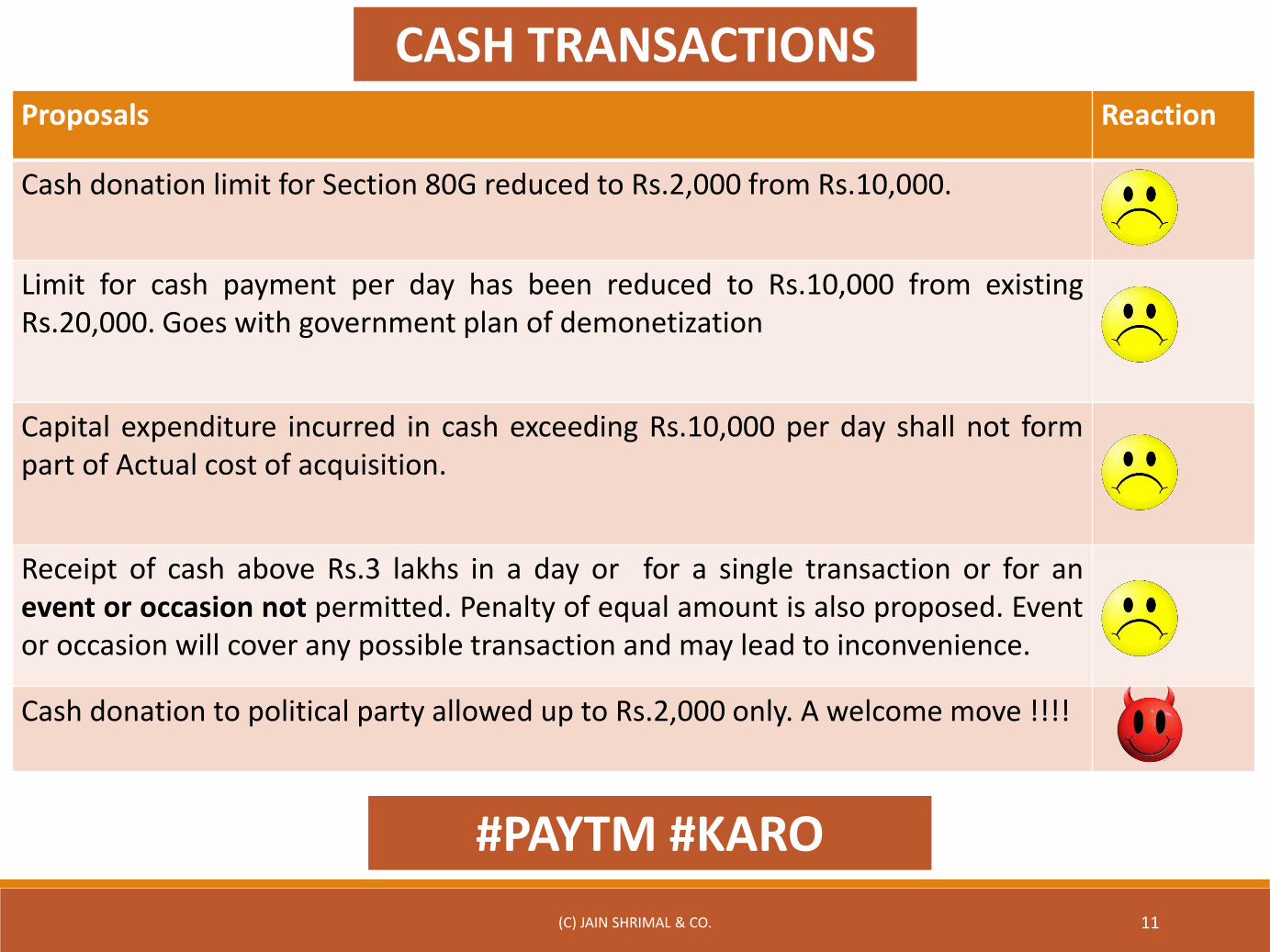

Proposals Reaction

Cash donation limit for Section 80G reduced to Rs.2,000 from Rs.10,000.

Limit for cash payment per day has been reduced to Rs.10,000 from existingRs.20,000. Goes with government plan of demonetization

Capital expenditure incurred in cash exceeding Rs.10,000 per day shall not formpart of Actual cost of acquisition.

Receipt of cash above Rs.3 lakhs in a day or for a single transaction or for anevent or occasion not permitted. Penalty of equal amount is also proposed. Eventor occasion will cover any possible transaction and may lead to inconvenience.

Cash donation to political party allowed up to Rs.2,000 only. A welcome move !!!!

CASH TRANSACTIONS

#PAYTM #KARO

(C) JAIN SHRIMAL & CO. 12

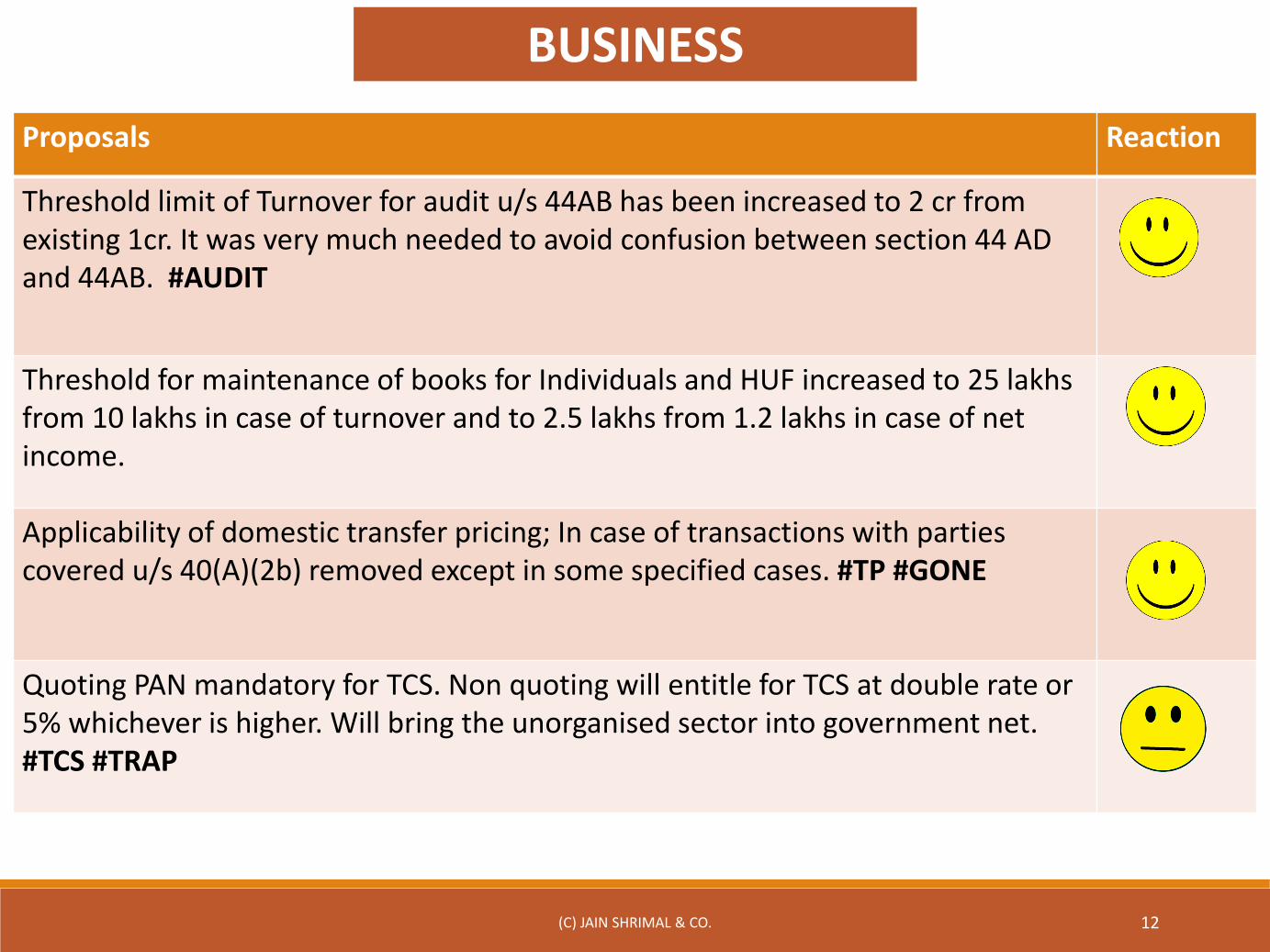

Proposals Reaction

Threshold limit of Turnover for audit u/s 44AB has been increased to 2 cr from existing 1cr. It was very much needed to avoid confusion between section 44 AD and 44AB. #AUDIT

Threshold for maintenance of books for Individuals and HUF increased to 25 lakhs from 10 lakhs in case of turnover and to 2.5 lakhs from 1.2 lakhs in case of net income.

Applicability of domestic transfer pricing; In case of transactions with parties covered u/s 40(A)(2b) removed except in some specified cases. #TP #GONE

Quoting PAN mandatory for TCS. Non quoting will entitle for TCS at double rate or 5% whichever is higher. Will bring the unorganised sector into government net. #TCS #TRAP

BUSINESS

(C) JAIN SHRIMAL & CO. 13

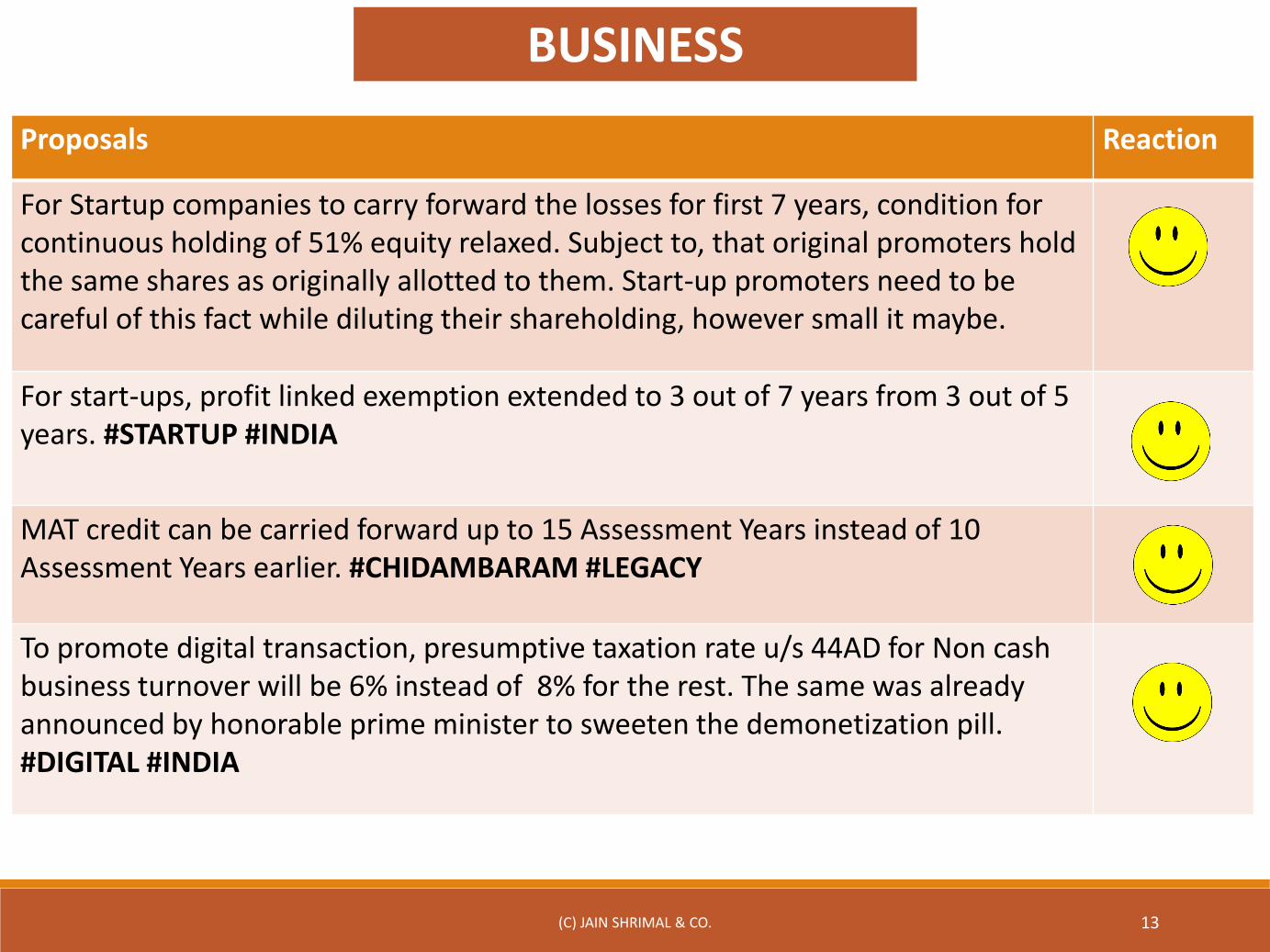

Proposals Reaction

For Startup companies to carry forward the losses for first 7 years, condition for continuous holding of 51% equity relaxed. Subject to, that original promoters hold the same shares as originally allotted to them. Start-up promoters need to be careful of this fact while diluting their shareholding, however small it maybe.

For start-ups, profit linked exemption extended to 3 out of 7 years from 3 out of 5 years. #STARTUP #INDIA

MAT credit can be carried forward up to 15 Assessment Years instead of 10 Assessment Years earlier. #CHIDAMBARAM #LEGACY

To promote digital transaction, presumptive taxation rate u/s 44AD for Non cash business turnover will be 6% instead of 8% for the rest. The same was already announced by honorable prime minister to sweeten the demonetization pill. #DIGITAL #INDIA

BUSINESS

(C) JAIN SHRIMAL & CO. 14

Proposals Reaction

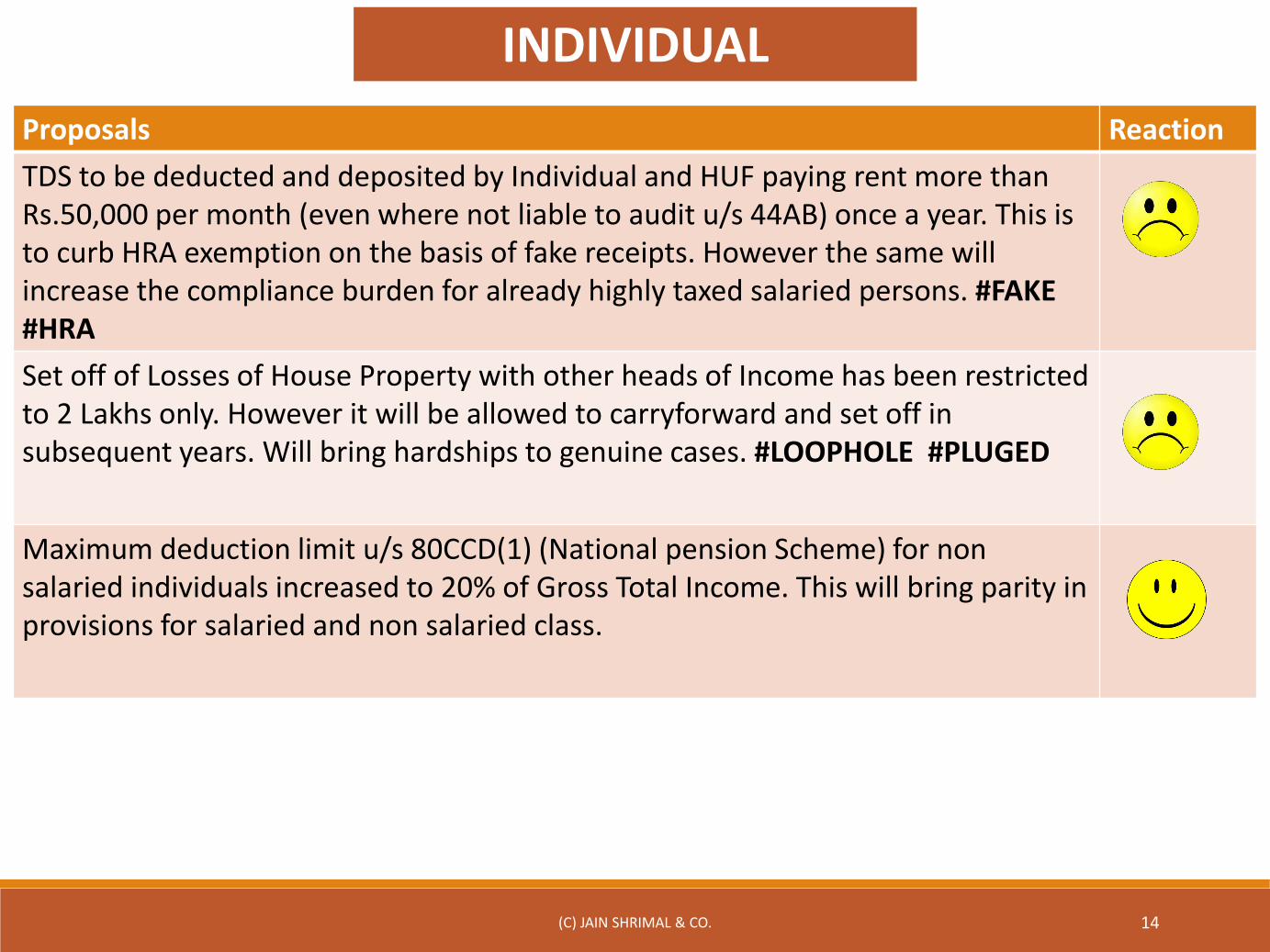

TDS to be deducted and deposited by Individual and HUF paying rent more than Rs.50,000 per month (even where not liable to audit u/s 44AB) once a year. This is to curb HRA exemption on the basis of fake receipts. However the same will increase the compliance burden for already highly taxed salaried persons. #FAKE#HRA

Set off of Losses of House Property with other heads of Income has been restricted to 2 Lakhs only. However it will be allowed to carryforward and set off in subsequent years. Will bring hardships to genuine cases. #LOOPHOLE #PLUGED

Maximum deduction limit u/s 80CCD(1) (National pension Scheme) for non salaried individuals increased to 20% of Gross Total Income. This will bring parity in provisions for salaried and non salaried class.

INDIVIDUAL

(C) JAIN SHRIMAL & CO. 15

Proposals Reaction

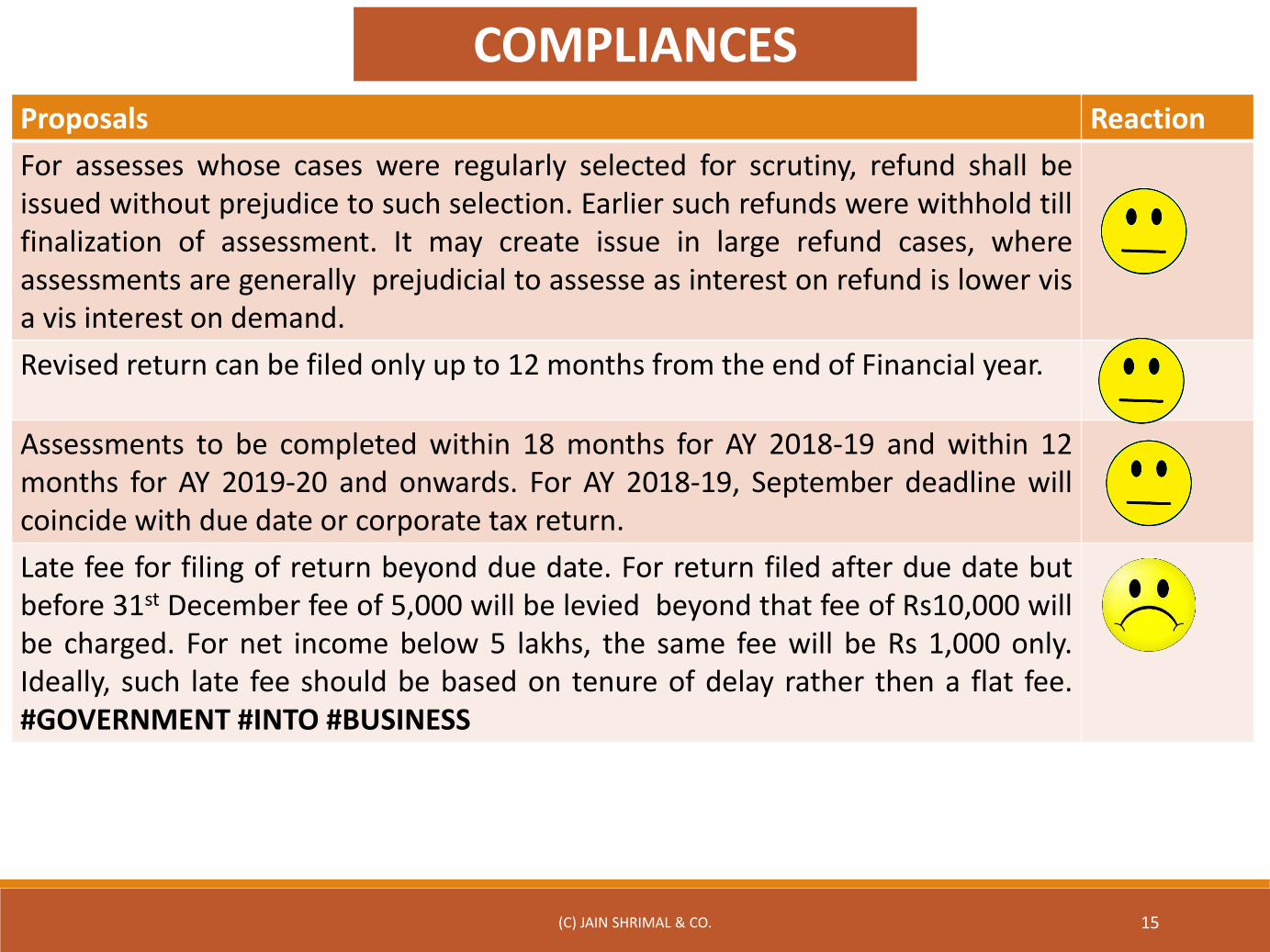

For assesses whose cases were regularly selected for scrutiny, refund shall beissued without prejudice to such selection. Earlier such refunds were withhold tillfinalization of assessment. It may create issue in large refund cases, whereassessments are generally prejudicial to assesse as interest on refund is lower visa vis interest on demand.

Revised return can be filed only up to 12 months from the end of Financial year.

Assessments to be completed within 18 months for AY 2018-19 and within 12months for AY 2019-20 and onwards. For AY 2018-19, September deadline willcoincide with due date or corporate tax return.

Late fee for filing of return beyond due date. For return filed after due date butbefore 31st December fee of 5,000 will be levied beyond that fee of Rs10,000 willbe charged. For net income below 5 lakhs, the same fee will be Rs 1,000 only.Ideally, such late fee should be based on tenure of delay rather then a flat fee.#GOVERNMENT #INTO #BUSINESS

COMPLIANCES

(C) JAIN SHRIMAL & CO. 16

Proposals Reaction

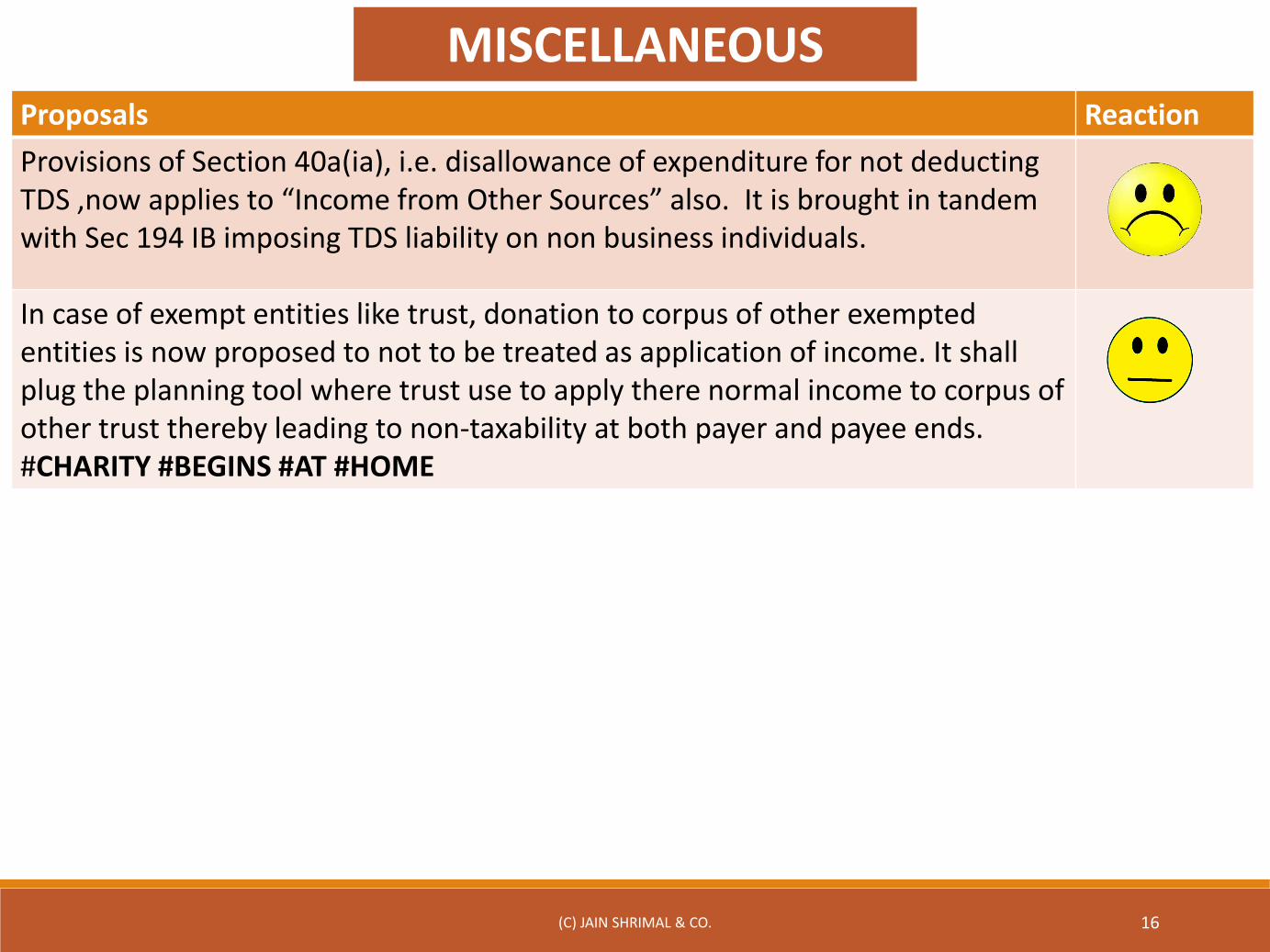

Provisions of Section 40a(ia), i.e. disallowance of expenditure for not deducting TDS ,now applies to “Income from Other Sources” also. It is brought in tandem with Sec 194 IB imposing TDS liability on non business individuals.

In case of exempt entities like trust, donation to corpus of other exempted entities is now proposed to not to be treated as application of income. It shall plug the planning tool where trust use to apply there normal income to corpus of other trust thereby leading to non-taxability at both payer and payee ends. #CHARITY #BEGINS #AT #HOME

MISCELLANEOUS

GST#CHANGE #IS #ALWAYS #CONSTANT

(C) JAIN SHRIMAL & CO. 17

(C) JAIN SHRIMAL & CO. 18

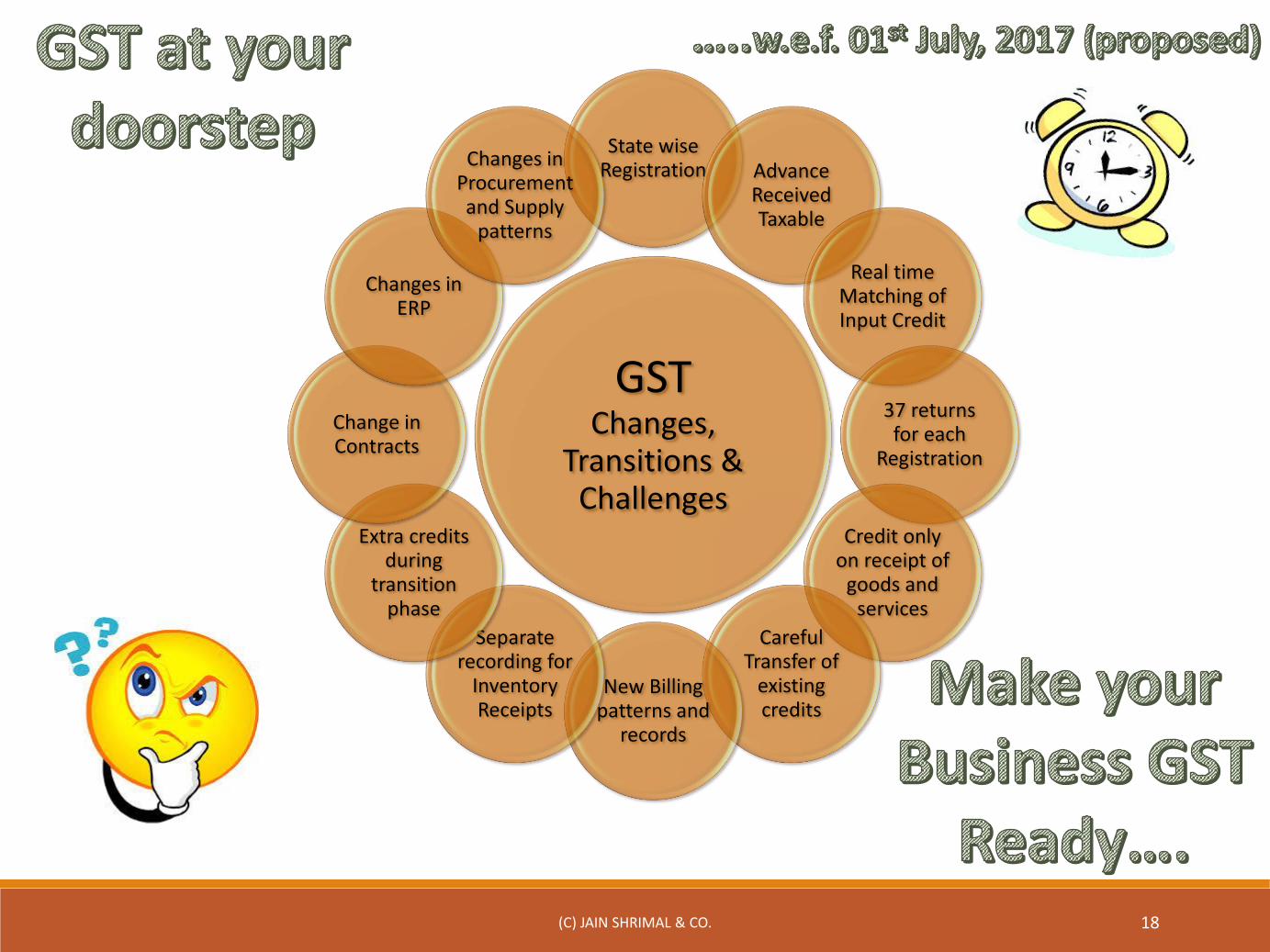

GST Changes,

Transitions & Challenges

State wise Registration Advance

Received Taxable

Real time Matching of Input Credit

37 returns for each

Registration

Credit only on receipt of

goods and services

Careful Transfer of

existing credits

New Billing patterns and

records

Separate recording for

Inventory Receipts

Extra credits during

transition phase

Change in Contracts

Changes in ERP

Changes in Procurement and Supply

patterns

Thank You

Editorial Team

CA Narendra Shrimal |CA Naman Shrimal |CA Ranjan Mehta

Shreyansh Karnawat | Palak Bansal

Thanks & Regards

CA S K Jain |CA Ashok Jain |CA Mohit Patni

CA Nikesh Sharma |CA Priyansh Gupta

CA Anshul Chittora | CA Akshay Jain |CA Krishan Singhal

(C) JAIN SHRIMAL & CO. 19

DisclaimerThe information contained on this presentation is based on Budget proposal as on 1st

February 2017 and is general in nature and does not take into account any personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from an adviser before acting on the same.