Embed Size (px)

Citation preview

`

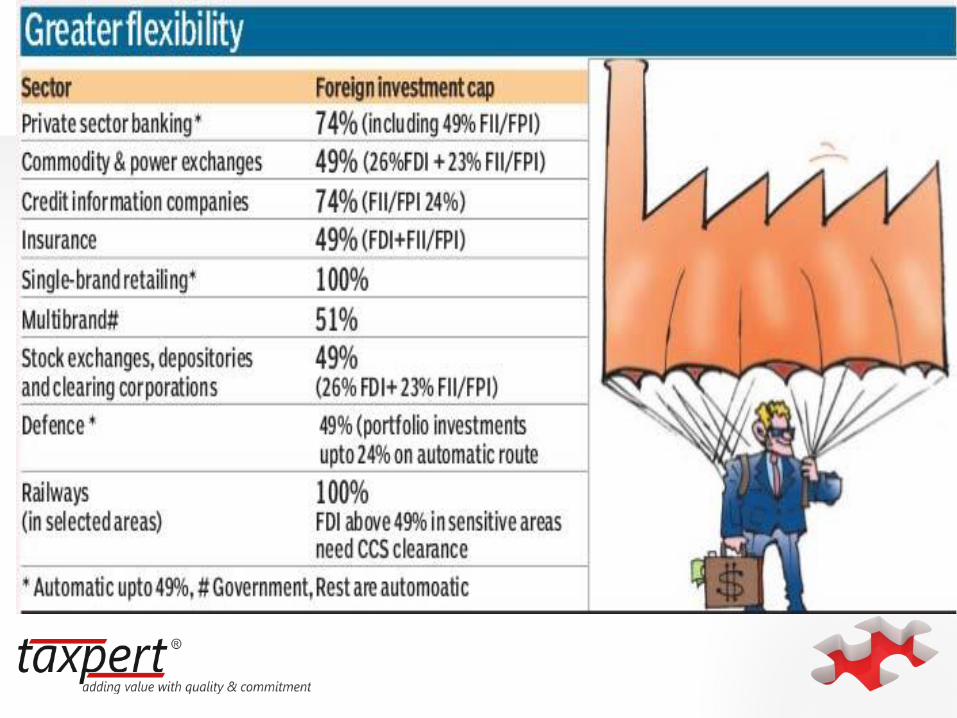

Major Changes

Capital Account Transactions

Money Laundering provisions

FDI in AIF

Merging of FDI and FII limits

`

FM Mr. Arun Jaitley said…

“Capital Account Controls is a policy, rather than a

regulatory, matter. I, therefore, propose to amend, throughthe Finance Bill, Section-6 of FEMA to clearly provide thatcontrol on capital flows as equity will be exercised by theGovernment, in consultation with the RBI”

Changes in Section 6 Changes in Section 47 Changes in Section 46

`

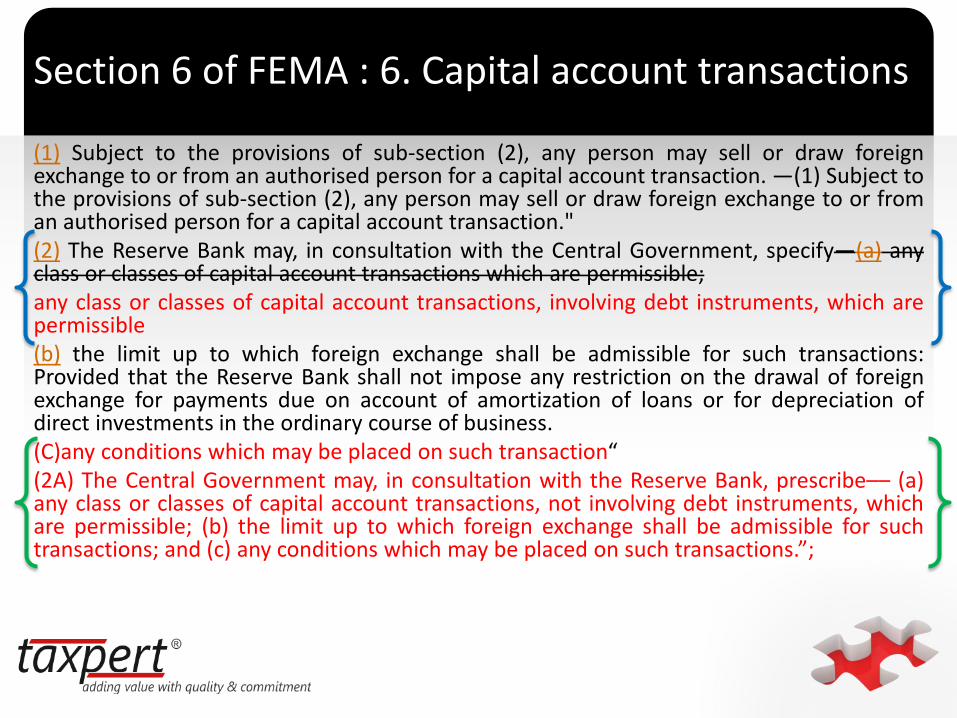

Section 6 of FEMA : 6. Capital account transactions

(1) Subject to the provisions of sub-section (2), any person may sell or draw foreignexchange to or from an authorised person for a capital account transaction. —(1) Subject tothe provisions of sub-section (2), any person may sell or draw foreign exchange to or froman authorised person for a capital account transaction."(2) The Reserve Bank may, in consultation with the Central Government, specify—(a) anyclass or classes of capital account transactions which are permissible;any class or classes of capital account transactions, involving debt instruments, which arepermissible(b) the limit up to which foreign exchange shall be admissible for such transactions:Provided that the Reserve Bank shall not impose any restriction on the drawal of foreignexchange for payments due on account of amortization of loans or for depreciation ofdirect investments in the ordinary course of business.(C)any conditions which may be placed on such transaction“(2A) The Central Government may, in consultation with the Reserve Bank, prescribe–– (a)any class or classes of capital account transactions, not involving debt instruments, whichare permissible; (b) the limit up to which foreign exchange shall be admissible for suchtransactions; and (c) any conditions which may be placed on such transactions.”;

`

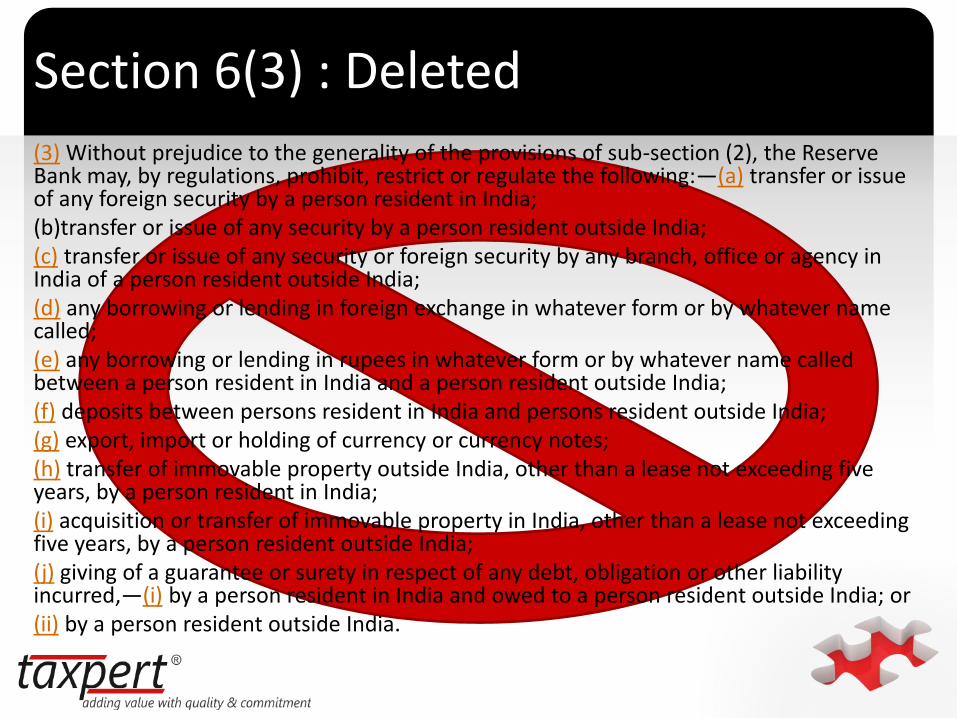

Section 6(3) : Deleted

(3) Without prejudice to the generality of the provisions of sub-section (2), the Reserve Bank may, by regulations, prohibit, restrict or regulate the following:—(a) transfer or issue of any foreign security by a person resident in India;(b)transfer or issue of any security by a person resident outside India;(c) transfer or issue of any security or foreign security by any branch, office or agency in India of a person resident outside India;(d) any borrowing or lending in foreign exchange in whatever form or by whatever name called;(e) any borrowing or lending in rupees in whatever form or by whatever name called between a person resident in India and a person resident outside India;(f) deposits between persons resident in India and persons resident outside India;(g) export, import or holding of currency or currency notes;(h) transfer of immovable property outside India, other than a lease not exceeding five years, by a person resident in India;(i) acquisition or transfer of immovable property in India, other than a lease not exceeding five years, by a person resident outside India;(j) giving of a guarantee or surety in respect of any debt, obligation or other liability incurred,—(i) by a person resident in India and owed to a person resident outside India; or(ii) by a person resident outside India.

`

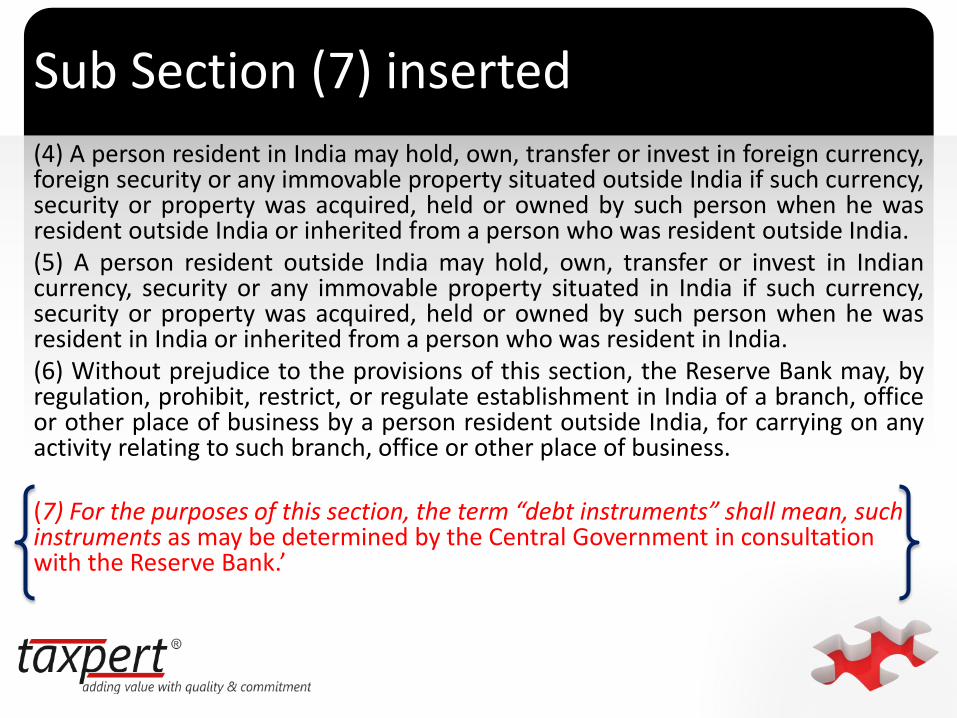

Sub Section (7) inserted

(4) A person resident in India may hold, own, transfer or invest in foreign currency,foreign security or any immovable property situated outside India if such currency,security or property was acquired, held or owned by such person when he wasresident outside India or inherited from a person who was resident outside India.(5) A person resident outside India may hold, own, transfer or invest in Indiancurrency, security or any immovable property situated in India if such currency,security or property was acquired, held or owned by such person when he wasresident in India or inherited from a person who was resident in India.(6) Without prejudice to the provisions of this section, the Reserve Bank may, byregulation, prohibit, restrict, or regulate establishment in India of a branch, officeor other place of business by a person resident outside India, for carrying on anyactivity relating to such branch, office or other place of business.

(7) For the purposes of this section, the term “debt instruments” shall mean, such instruments as may be determined by the Central Government in consultation with the Reserve Bank.’

`

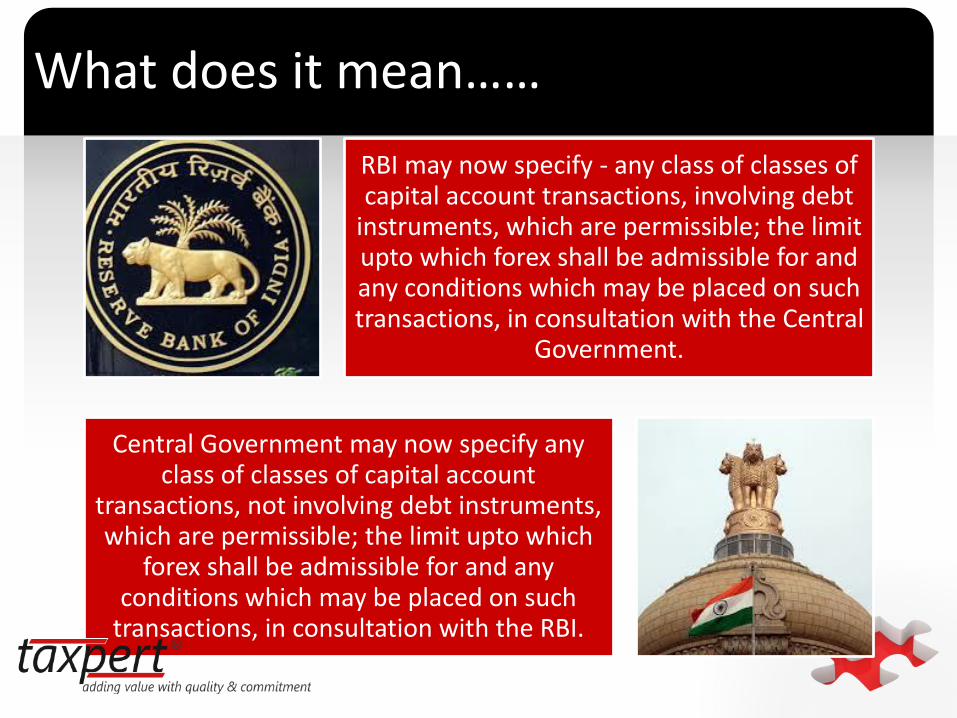

What does it mean……

RBI may now specify - any class of classes of capital account transactions, involving debt

instruments, which are permissible; the limit upto which forex shall be admissible for and any conditions which may be placed on such transactions, in consultation with the Central

Government.

Central Government may now specify any class of classes of capital account

transactions, not involving debt instruments, which are permissible; the limit upto which

forex shall be admissible for and any conditions which may be placed on such

transactions, in consultation with the RBI.

`

Section 47

Section 47 of FEMA Act, 1999 which empowered RBI to make regulations has beenamended to the extent that all regulations made by RBI till date under Section 6 and Section47 on capital account transactions, the regulation making power in respect of which nowvests with the Central Government, shall continue to be valid, until amended or rescindedby the Central Government

`

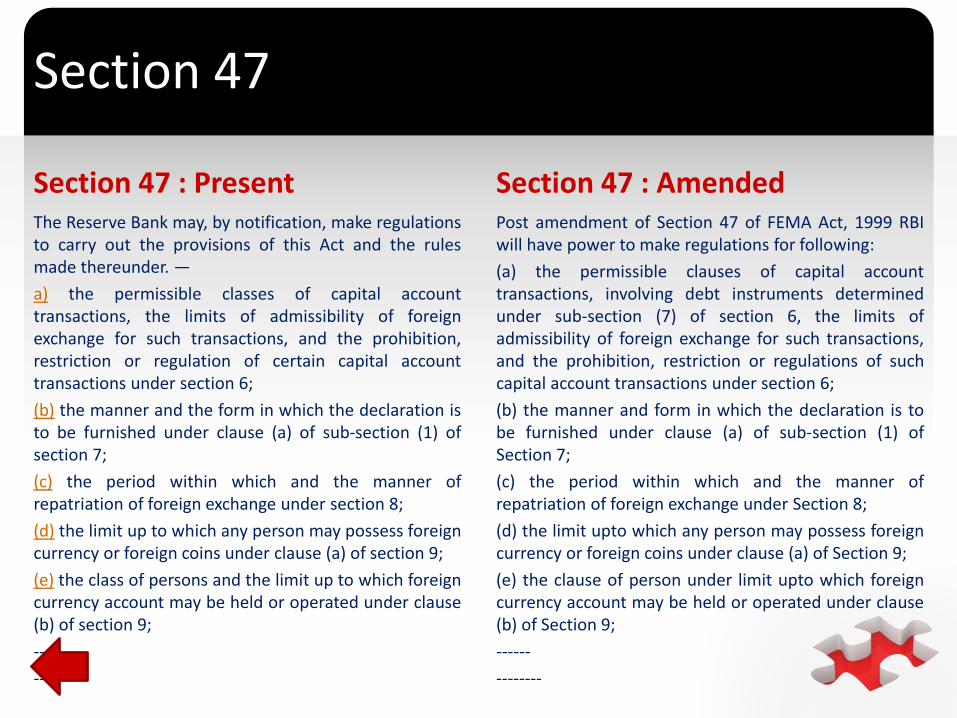

Section 47

Section 47 : PresentThe Reserve Bank may, by notification, make regulationsto carry out the provisions of this Act and the rulesmade thereunder. —

a) the permissible classes of capital accounttransactions, the limits of admissibility of foreignexchange for such transactions, and the prohibition,restriction or regulation of certain capital accounttransactions under section 6;

(b) the manner and the form in which the declaration isto be furnished under clause (a) of sub-section (1) ofsection 7;

(c) the period within which and the manner ofrepatriation of foreign exchange under section 8;

(d) the limit up to which any person may possess foreigncurrency or foreign coins under clause (a) of section 9;

(e) the class of persons and the limit up to which foreigncurrency account may be held or operated under clause(b) of section 9;

----

------

Section 47 : AmendedPost amendment of Section 47 of FEMA Act, 1999 RBIwill have power to make regulations for following:

(a) the permissible clauses of capital accounttransactions, involving debt instruments determinedunder sub-section (7) of section 6, the limits ofadmissibility of foreign exchange for such transactions,and the prohibition, restriction or regulations of suchcapital account transactions under section 6;

(b) the manner and form in which the declaration is tobe furnished under clause (a) of sub-section (1) ofSection 7;

(c) the period within which and the manner ofrepatriation of foreign exchange under Section 8;

(d) the limit upto which any person may possess foreigncurrency or foreign coins under clause (a) of Section 9;

(e) the clause of person under limit upto which foreigncurrency account may be held or operated under clause(b) of Section 9;

------

--------

`

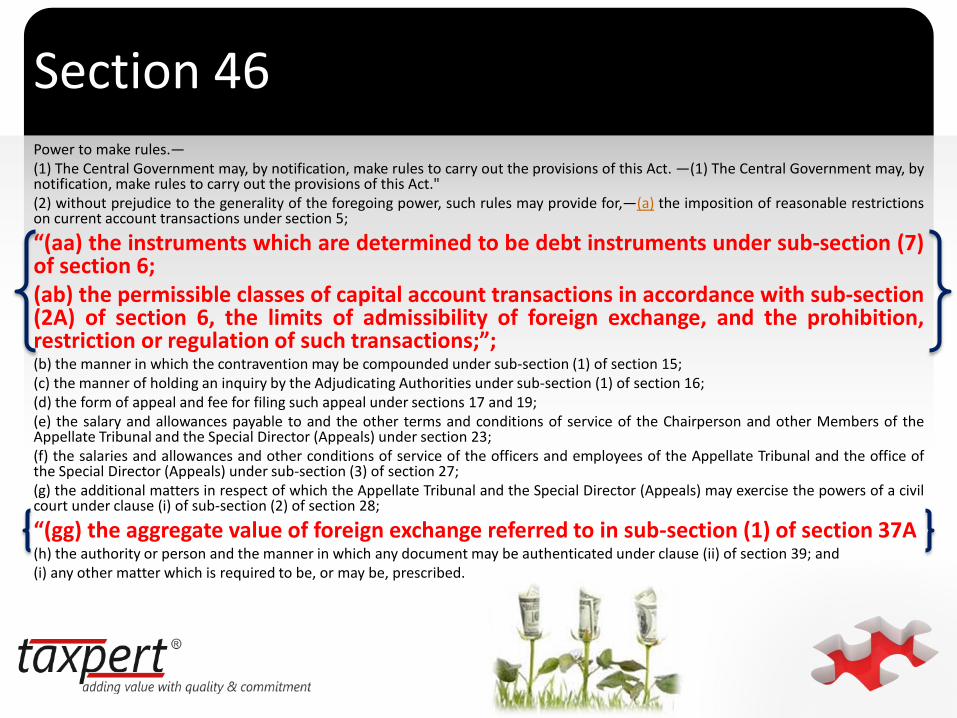

Section 46Power to make rules.—(1) The Central Government may, by notification, make rules to carry out the provisions of this Act. —(1) The Central Government may, bynotification, make rules to carry out the provisions of this Act."(2) without prejudice to the generality of the foregoing power, such rules may provide for,—(a) the imposition of reasonable restrictionson current account transactions under section 5;

“(aa) the instruments which are determined to be debt instruments under sub-section (7)of section 6;(ab) the permissible classes of capital account transactions in accordance with sub-section(2A) of section 6, the limits of admissibility of foreign exchange, and the prohibition,restriction or regulation of such transactions;”;(b) the manner in which the contravention may be compounded under sub-section (1) of section 15;(c) the manner of holding an inquiry by the Adjudicating Authorities under sub-section (1) of section 16;(d) the form of appeal and fee for filing such appeal under sections 17 and 19;(e) the salary and allowances payable to and the other terms and conditions of service of the Chairperson and other Members of theAppellate Tribunal and the Special Director (Appeals) under section 23;(f) the salaries and allowances and other conditions of service of the officers and employees of the Appellate Tribunal and the office ofthe Special Director (Appeals) under sub-section (3) of section 27;(g) the additional matters in respect of which the Appellate Tribunal and the Special Director (Appeals) may exercise the powers of a civilcourt under clause (i) of sub-section (2) of section 28;

“(gg) the aggregate value of foreign exchange referred to in sub-section (1) of section 37A(h) the authority or person and the manner in which any document may be authenticated under clause (ii) of section 39; and(i) any other matter which is required to be, or may be, prescribed.

`

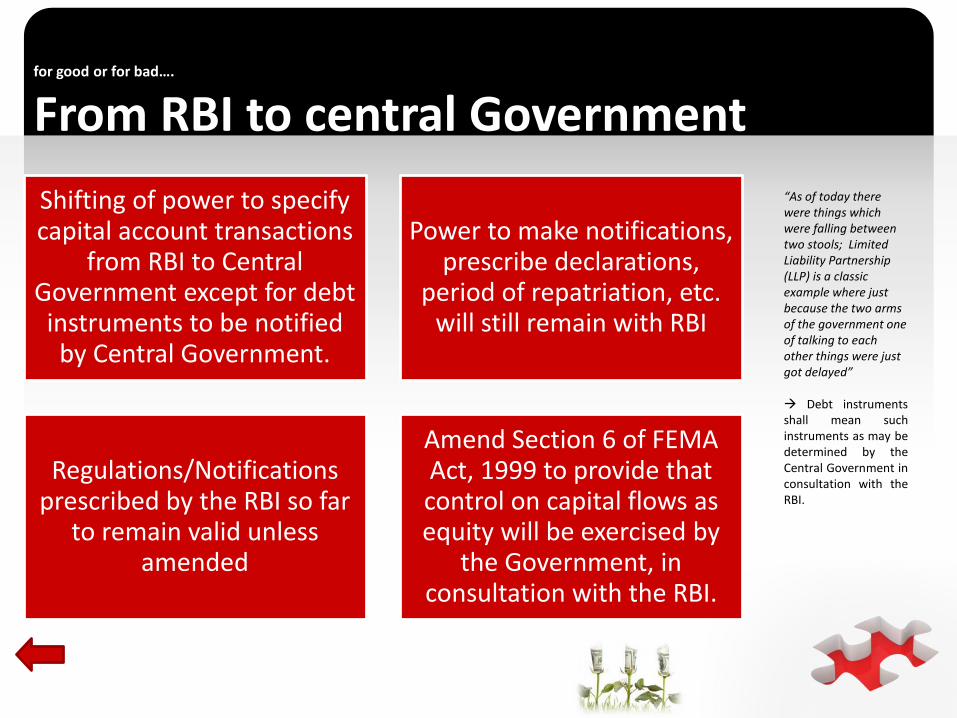

for good or for bad….

From RBI to central Government

Shifting of power to specify capital account transactions

from RBI to Central Government except for debt instruments to be notified by Central Government.

Power to make notifications, prescribe declarations,

period of repatriation, etc. will still remain with RBI

Regulations/Notifications prescribed by the RBI so far

to remain valid unless amended

Amend Section 6 of FEMA Act, 1999 to provide that control on capital flows as equity will be exercised by

the Government, in consultation with the RBI.

“As of today there were things which were falling between two stools; Limited Liability Partnership (LLP) is a classic example where just because the two arms of the government one of talking to each other things were just got delayed”

Debt instrumentsshall mean suchinstruments as may bedetermined by theCentral Government inconsultation with theRBI.

`

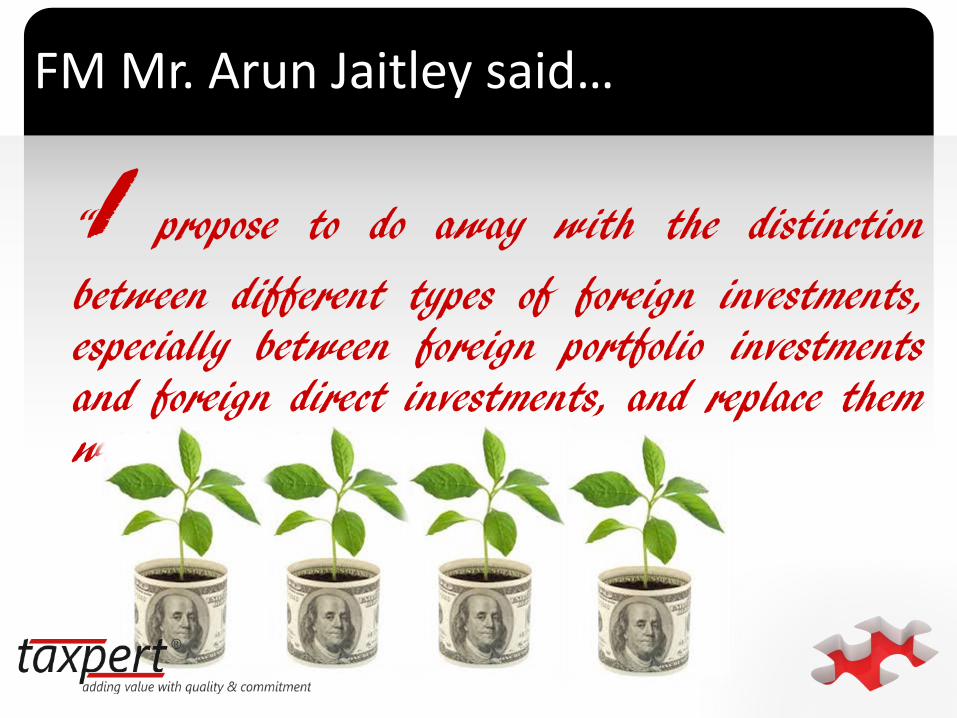

FM Mr. Arun Jaitley said…

“I propose to do away with the distinction

between different types of foreign investments,especially between foreign portfolio investmentsand foreign direct investments, and replace themwith composite caps”

`

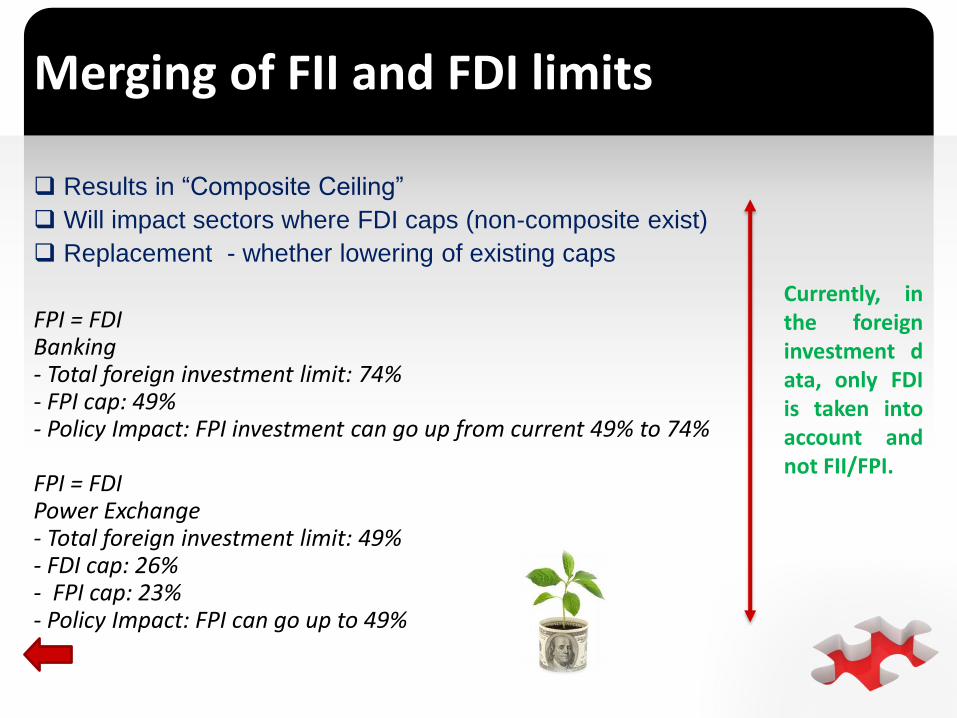

Merging of FII and FDI limits

Results in “Composite Ceiling”

Will impact sectors where FDI caps (non-composite exist)

Replacement - whether lowering of existing caps

FPI = FDIBanking- Total foreign investment limit: 74%- FPI cap: 49%- Policy Impact: FPI investment can go up from current 49% to 74%

FPI = FDIPower Exchange- Total foreign investment limit: 49%- FDI cap: 26%- FPI cap: 23%- Policy Impact: FPI can go up to 49%

Currently, inthe foreigninvestment data, only FDIis taken intoaccount andnot FII/FPI.

`

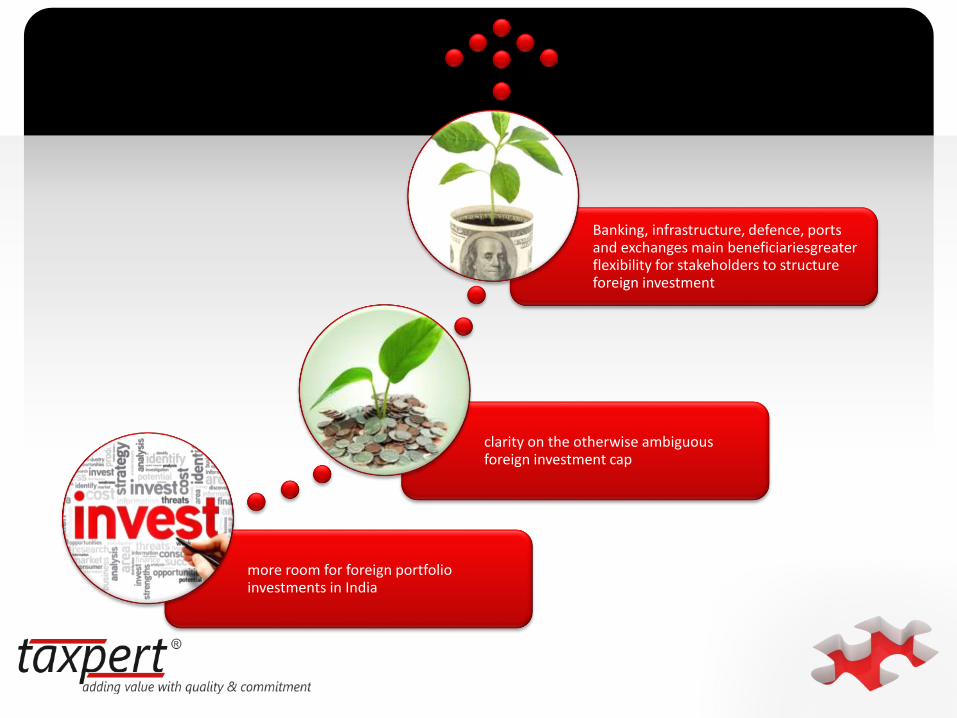

more room for foreign portfolio investments in India

clarity on the otherwise ambiguous foreign investment cap

Banking, infrastructure, defence, ports and exchanges main beneficiariesgreaterflexibility for stakeholders to structure foreign investment

`

FM Mr. Arun Jaitley said…

Alternate Investment Funds Regulations have been

notified by SEBI. Such alternate investment funds provideanother vehicle for facilitating domestic investments.Keeping in view the need to increase investments from allsources, I propose to also allow foreign investments inAlternate Investment Funds.”

`

Background

The SEBI (Alternative Investment Funds) Regulations, 2012(“AIF Regulations”) were notified on May 21, 2012.

The AIF Regulations succeeded and repealed the erstwhileSEBI (Venture Capital Funds) Regulations, 1996 (“VCFRegulations”).

Erstwhile FDI Policy, did not contemplate or provide anyimpact of the various relevant provisions on thealternative investment funds (“AIFs”) that have now beenregistered with SEBI under the AIF Regulations.

Considering the number of AIFs being registered with theSEBI and the interest shown by non-residents to invest insuch AIFs, it was imperative for the DIPP to issue animmediate clarification on this issue.

“To promotedomestic investmentsand manufacturing asspelt out in the ‘Makein India’ programme,the Government hasproposed to allowforeign directinvestments inAlternativeInvestment Funds —a privately pooledinvestment fund forreal estate, privateequity and hedgefunds.”

`

Allow foreign Investment in AIFs

Consolidated FDI Policy still talks of VCFs instead of AIFs

FIPB Policy acknowledged the need for FDI Policy to take cognizance of AIF regulations

FIPB has so far granted specific approvals to AIFs while treating such investments at par with Foreign Investment

Yet to be clarified ….. Whether all investments to fall under automatic route?

Whether downstream investments will require FIPB clearance?

Whether the first leg of investment (issue of trust units to foreign investor) would be subject to FDI rules such as pricing guidelines, etc.?

AIFs are basically funds established or incorporated in India for the purpose of pooling in capital from Indian investors.

`

FM Mr. Arun Jaitley said…

Tracking down and bringing back the wealth

which legitimately belongs to the country is our abiding commitment to the country

Changes in Section 2 Section 18 amendedSection 37A introduced

`

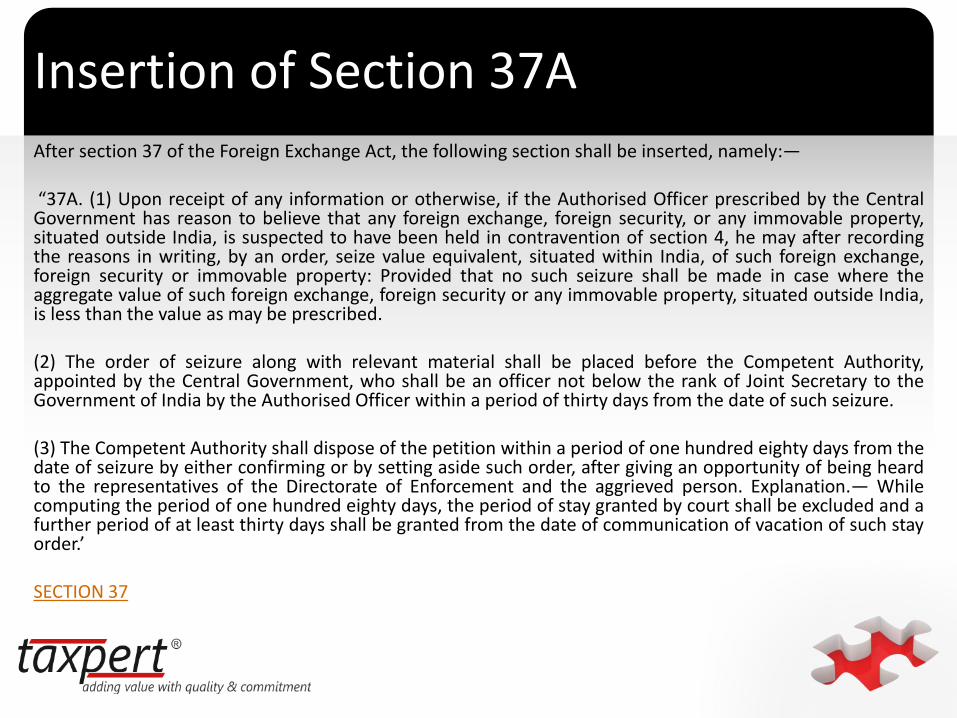

Insertion of Section 37AAfter section 37 of the Foreign Exchange Act, the following section shall be inserted, namely:—

“37A. (1) Upon receipt of any information or otherwise, if the Authorised Officer prescribed by the CentralGovernment has reason to believe that any foreign exchange, foreign security, or any immovable property,situated outside India, is suspected to have been held in contravention of section 4, he may after recordingthe reasons in writing, by an order, seize value equivalent, situated within India, of such foreign exchange,foreign security or immovable property: Provided that no such seizure shall be made in case where theaggregate value of such foreign exchange, foreign security or any immovable property, situated outside India,is less than the value as may be prescribed.

(2) The order of seizure along with relevant material shall be placed before the Competent Authority,appointed by the Central Government, who shall be an officer not below the rank of Joint Secretary to theGovernment of India by the Authorised Officer within a period of thirty days from the date of such seizure.

(3) The Competent Authority shall dispose of the petition within a period of one hundred eighty days from thedate of seizure by either confirming or by setting aside such order, after giving an opportunity of being heardto the representatives of the Directorate of Enforcement and the aggrieved person. Explanation.— Whilecomputing the period of one hundred eighty days, the period of stay granted by court shall be excluded and afurther period of at least thirty days shall be granted from the date of communication of vacation of such stayorder.’

SECTION 37

`

Authorised Officer and Competent AuthoritySection 2 is amended to include :

‘(cc) ‘‘Authorised Officer’’ means an officer of theDirectorate of Enforcement authorised by the CentralGovernment under section 37A

(gg) “Competent Authority’’ means the Authorityappointed by the Central Government under sub-section(2) of section 37A

`

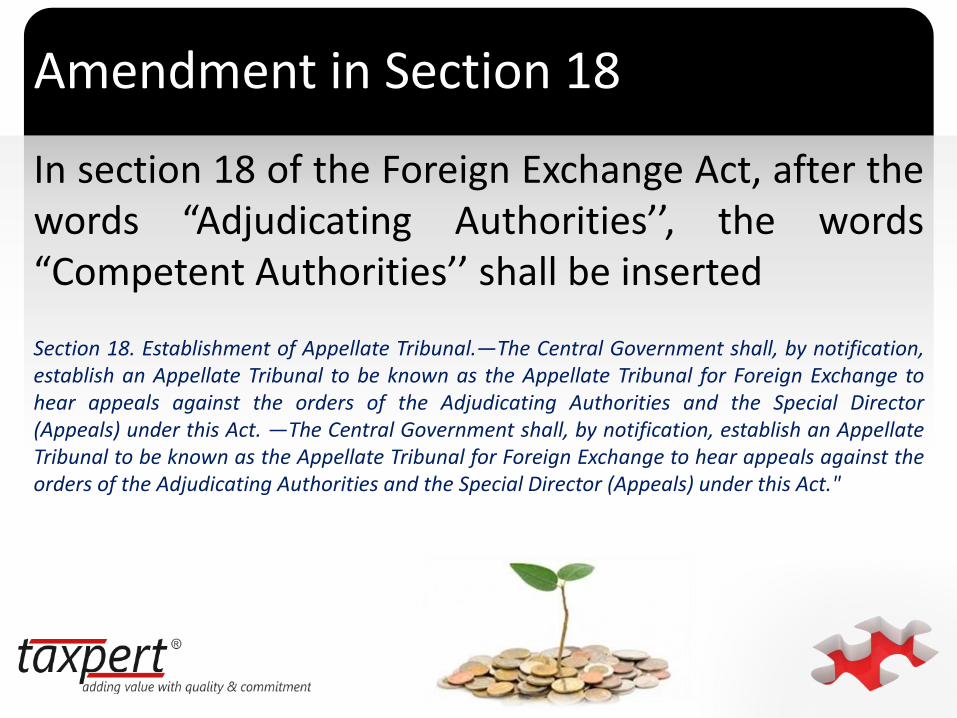

Amendment in Section 18

In section 18 of the Foreign Exchange Act, after thewords “Adjudicating Authorities’’, the words“Competent Authorities’’ shall be inserted

Section 18. Establishment of Appellate Tribunal.—The Central Government shall, by notification,establish an Appellate Tribunal to be known as the Appellate Tribunal for Foreign Exchange tohear appeals against the orders of the Adjudicating Authorities and the Special Director(Appeals) under this Act. —The Central Government shall, by notification, establish an AppellateTribunal to be known as the Appellate Tribunal for Foreign Exchange to hear appeals against theorders of the Adjudicating Authorities and the Special Director (Appeals) under this Act."

`

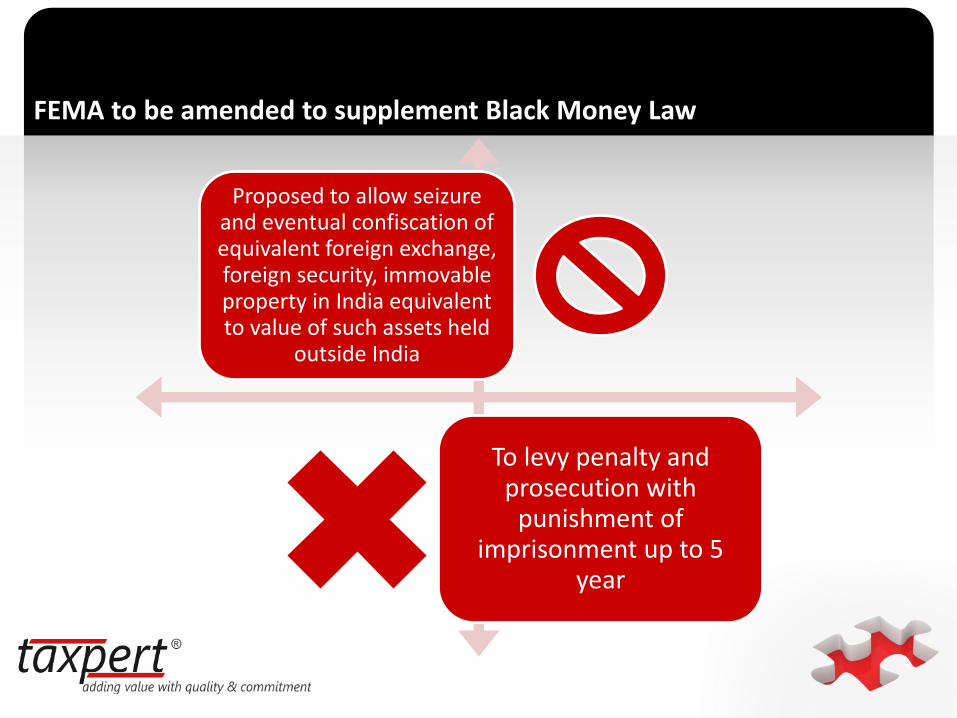

FEMA to be amended to supplement Black Money Law

Proposed to allow seizure and eventual confiscation of equivalent foreign exchange, foreign security, immovable property in India equivalent to value of such assets held

outside India

To levy penalty and prosecution with

punishment of imprisonment up to 5

year

`

Taxpert Professionals Private Limited

Tel: +91 9769134554 || 022 25138323

E-mail us: [email protected]

Visit us at: www.taxpertpro.com

![FOREIGN INTELLIGENCE SURVEILLANCE ACT OF …...Foreign Intelligence Surveillance Act of 1978 Amendments Act of 2008. July 10, 2008 [H.R. 6304] kgrant on POHRRP4G1 with PUBLIC LAWS](https://img.pdfslide.us/doc/110x75/5ec5dc6fd03eef7a965b9db7/foreign-intelligence-surveillance-act-of-foreign-intelligence-surveillance-act.jpg)