Embed Size (px)

Citation preview

Presented By:

Tool Kit for Crisis Management and Risk Assessment

October 29, 2016

Presented By:

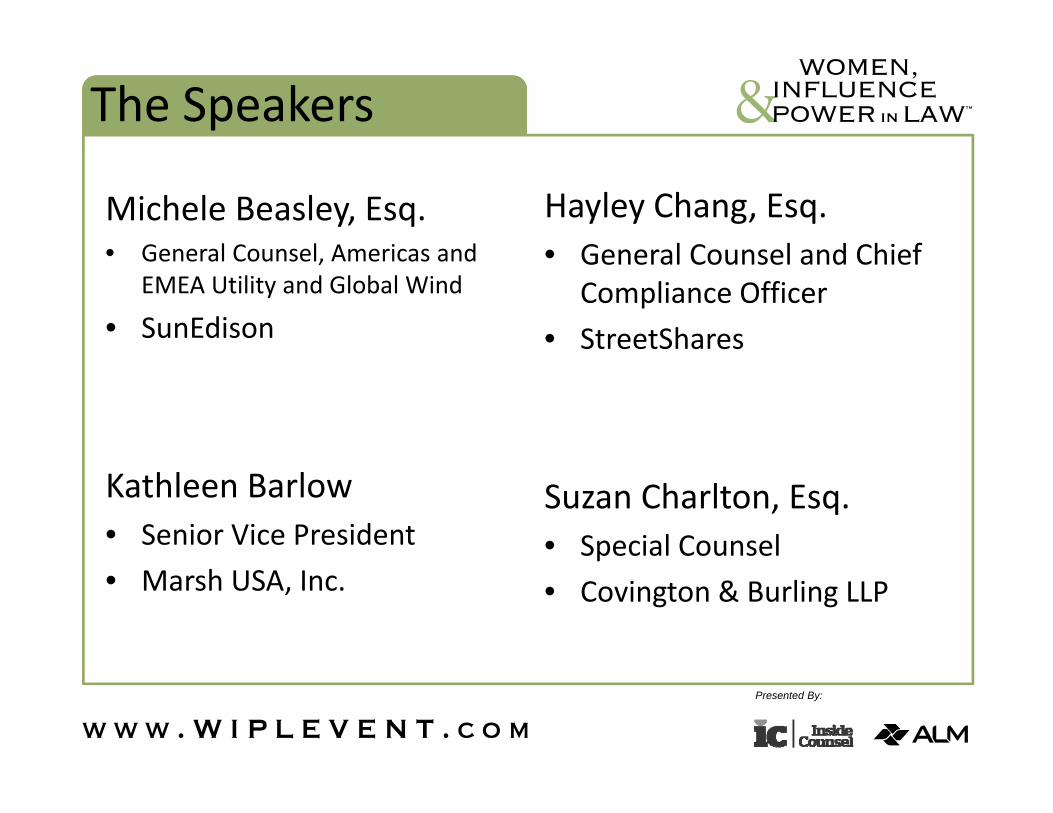

The Speakers

Michele Beasley, Esq.• General Counsel, Americas and

EMEA Utility and Global Wind

• SunEdison

Kathleen Barlow• Senior Vice President• Marsh USA, Inc.

Hayley Chang, Esq.• General Counsel and Chief

Compliance Officer• StreetShares

Suzan Charlton, Esq.• Special Counsel• Covington & Burling LLP

Presented By:

Agenda• Tool Kit:

– Managing change in the regulated world• Keeping up with industry, regulations, and crisis response

• Developing a risk profile

– Practical advice and illustrations• risks to property and life/safety• cyber security• government investigations

– Leveraging your insurance broker

Presented By:

MANAGING CHANGEIN THE REGULATED WORLD

Presented By:

OverviewI. Current regulatory landscape

II.Constant change

III.Compliance lawyer’s tool kit

Outline

Presented By:

I. REGULATORY LANDSCAPE

Presented By:

Federal Regulations

• U.S. executive branch agencies issue a few thousand rules per year

• CFR = 175,000 pages– With regs by 438 federal agencies– … or more?

Presented By:

Presented By:

State Regulations

• 50 states + DC• And local regulators• Sometimes, they work together

– Ex: NASAA and securities notice filings• Other times, they’re wildly inconsistent

– Ex: commercial lending laws

• Even conflicting

Presented By:

State bureaucracies

Presented By:

Global Compliance Issues• International regulatory framework

– Global capital flow– 24/7, worldwide operations– Labor mobility– Instant, real time communication– Patchwork of myriad and conflicting regulations

• simultaneous compliance with differing regimes by a unitary work force

• drive to remove silos may inadvertently increase regulatory risk

Presented By:

II. CHANGE IS THE ONLY CONSTANT

Presented By:

ALTERNATIVE FINANCE OVER THE PAST DECADE

2005 2007 2009 2011 2013 2015 2006 2008 2010 2012 2014

JOBS Act

R.506(c)

Reg A+

Treasury RFI

Goldman Sachs Report

IPO

Example: Financial Services

Presented By:

• Rules change– Trying to keep up with new industries– Crisis response– Regulatory reform

• Risks change– Cyber – Emerging markets– Political risks

Change

Presented By:

Change• Business must constantly transform to keep up

– Always “on” • 24/7 operations• Instantaneous, real‐time communication

– Always moving• Labor mobility• Advances in technology• Changes in U.S. and international regulatory framework• Corporate mergers, acquisitions, restructuring, etc.

– Everywhere• Competition

Presented By:

III. COMPLIANCE LAWYER’S TOOLBOX

Presented By:

A. TRACKING TRENDS

Presented By:

• Keep apprised of current legal developments‐ Industry publications‐ Set up news alerts

• Spot coming trends‐ Stay close to your business‐ Listen to the non‐legal team

Presented By:

B. RISK PROFILE DEVELOPMENT

Presented By:

What is a Risk Profile?

• Evaluation of 1. willingness to take/assume risks2. threats to your organization

Greater risk greater required return

• Risks must be accurately assessed in order to be adequately priced

Presented By:

Managing Risk• 3 ways to manage risk

1. Assume• No insurance; high SIR’s• “Cost of doing business”

2. Reduce/Avoid• Quality control• Safety

3. Transfer• Third Party Contractual Assumption of Risk• Indemnities• Insurance

Presented By:

Developing a Risk Profile

• Risk assessment• Risk tolerances

‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐

• Threat assessment• Countermeasures

Presented By:

C. SYSTEMS ARE YOUR FRIEND

Presented By:

Usefulness of Systems• Use the “least necessary” approach to compliance system development

• USE TOOLS! – Automate!

• Provides for consistency• Reduces human error• Creates a record• Humans are bad at consistency over more than a handful of people

– Insert analytic and logic into tools so users are focused on just the facts (e.g., derivatives, suitability and Know Your Customer programs)

• Make an audit trail and USE IT

Presented By:

Necessity of Systems

If it isn’t documented…. it didn’t happen

Presented By:

PRACTICAL ADVICE: RISK AND CRISIS MANAGEMENT SCENARIOS

Presented By:

Practical Advice: Risks

• Human Life/Safety• Property and liability risks• Developing markets• Cyber security• Government investigations

MEB1

Slide 27

MEB1 not sure this slide adds anything new??Michele E. Beasley, 10/21/2015

Presented By:

Human Life/Safety Risks• Threats?

• Inherently dangerous business activities• Travel (security, medical and kidnap/extortion risks)• Inadequate procedures/training/reporting

• Risk assumption/transfer– Hard to insure for– How much to self‐insure?

Presented By:

Property/Liability Risks• Threats?

• Business interruption• Tort liability• Product recalls

• Risk assumption/transfer• Supplier indemnities• How much to self‐insure?

• Other insurance considerations• AI coverage• D&O coverage

Presented By:

Developing Markets

• Risks the company is willing to take:– How do you know what you don’t yet know?

• Security Assessments (internal/external); Anti‐corruption analysis and safeguards

• International regulatory settings—figuring out the rules of the road for new roads

• Insurance considerations: – beyond property and casualty – currency, inflation, expropriation, political risk, others

Presented By:

31

Cyber Security

Risks/Threats:

• Management awareness lags behind threats– Little understanding of impact of cyber events– Inadequate security programs & incident response planning

–No data on impact: cyber business interruption & loss exposures

– Lack of governance structure, defined roles & responsibilities

Presented By:

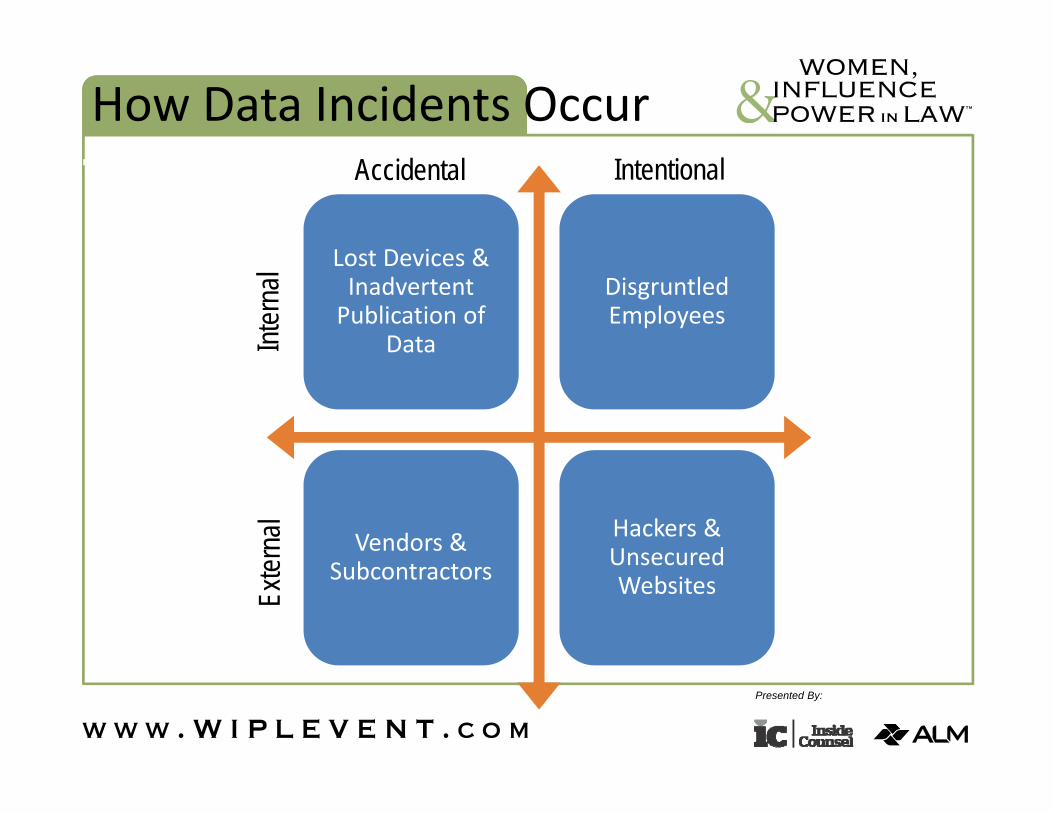

How Data Incidents Occur

Lost Devices & Inadvertent Publication of

Data

Disgruntled Employees

Vendors & Subcontractors

Hackers & Unsecured Websites

Inter

nal

Exter

nal

Accidental Intentional

Presented By:

33

Presented By:

Cyber Risk Assessment• Internal and external vulnerabilities, weaknesses in existing framework

• Relevant threats, including threats from third‐party entities

• Impact/harm– What do regulations require? – What do shareholders and customers require?

• Likelihood that harm will occur• Ability to transfer risk through insurance

Presented By:

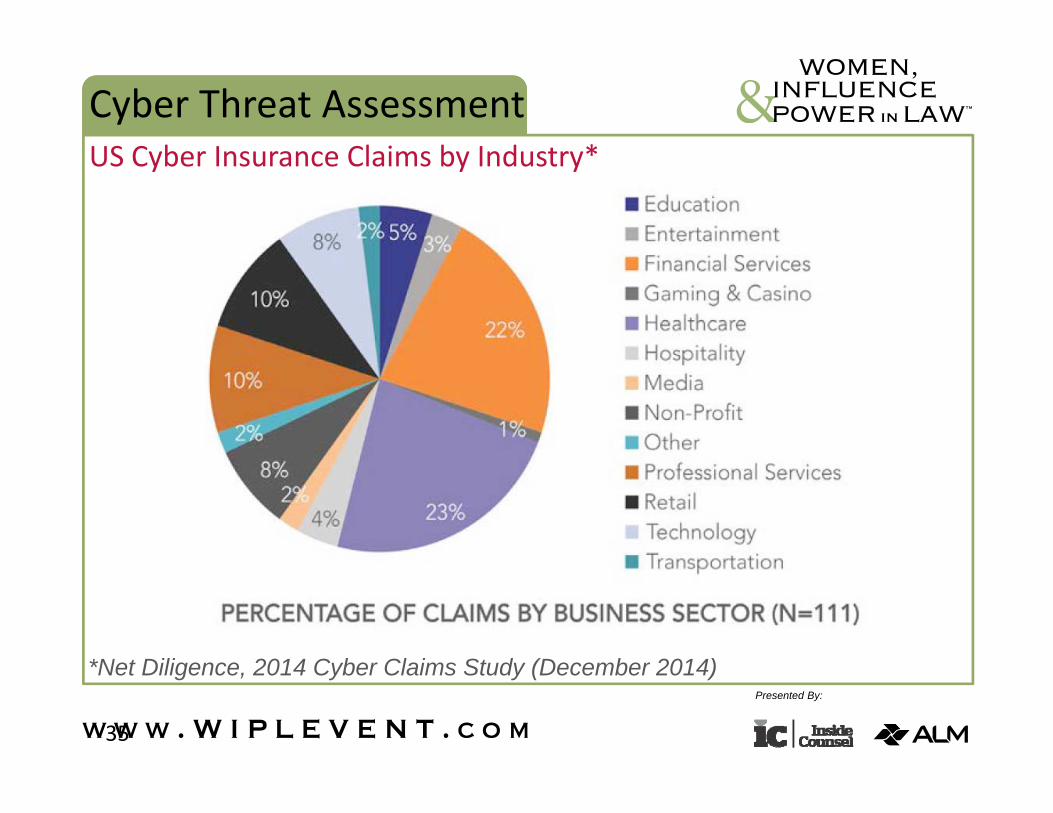

35

*Net Diligence, 2014 Cyber Claims Study (December 2014)

Cyber Threat AssessmentUS Cyber Insurance Claims by Industry*

Presented By:

Government Investigations

• Types of investigations– environmental– Anti‐corruption– whistleblowers/qui tam– other compliance issues

• FCA cases (FY 2014):– 700+ whistleblower suits– >$5 billion to U.S. DOJ in qui tam litigations

Presented By:

Government Investigations

• Is an investigation a crisis? – Routine compliance or allegations of wrongdoing?

• Do you have insurance for it? – Understand what your policies actually cover– Timing: notice of “claim” or “circumstances”

• Best practices– Flag government inquiries early

• Train employees to report

– Preserve coverage by noticing “circumstances”

Presented By:

LEVERAGING YOUR INSURANCE BROKER’S SERVICES

Presented By:

I. Insurance as part of a Risk Management Assessment

II. Using your insurance “advisor” effectively

Presented By:

Key Business Objectives

• Insurance as part of Risk Management Assessment

• Financial protection against – Direct loss (caused by harm to own business)– Liability loss (caused by harm to others)– Financial and reputational protection to key company management personnel

– Damage to company reputation and relationships– Business continuity

40

Presented By:

Insurance Risk Assessment• Insurable risks

– What is at risk? Is everything covered?

– Who is at risk? Is everyone covered? • Affiliates, subs, indemnified companies, merged companies?

• Sufficient amount of coverage?• Legal issues arising from policy language?• How do the insurance policies in the portfolio

interact? Are there gaps? • Are there non-insurance mechanisms to avoid

and spread risk?

41

Presented By:

GC’s and Risk/Insurance• Changing Role of the Legal Department in Risk Management and Insurance – More focus on risk management– GC involvement in financial and professional lines

• D&O— importance to board and “C Suite”• Cyber liability – data breach, compromise of employee information, evolving daily

• E&O/Professional liability — outside of “cyber” or integral to?

– Company risk management philosophy• Teamwork? or not (power play)?• Legal, Finance, Risk Management, HR, Facilities, etc.

42

Presented By:

43

• Who is ultimately responsible for ensuring that the company’s most significant risks are addressed?

GC’s and Risk/Insurance

Presented By:

Why My Department?• Why Should You and Legal Department Be Involvedin Risk Management and Insurance Issues?– Managing rising litigation costs– Evaluate need for new insurance if available

• FCPA violations• Wage and Hour violations• Cyber Liability

– Because your CEO will expect you to be prepared to jump into crisis and risk – be proactive

– Professional development• Carve out a role in legal department that is yours and impacts all other departments

44

Presented By:

Using Your BrokerBeyond renewals….• What the broker knows:

– Risk; impacts and likelihood– Insurance markets; new insurance coverages

• Who the broker knows:– Brokers may have relationships with insurers, which can facilitate future claims handling

• What (else) the broker can do:– Keep positive relationship between policyholder and insurer; affect claim assessment and resolution

– Who is your “claims advocate” at the broker?

45

Presented By:

Using Your Broker

• Caveat: – No Attorney‐Client relationship with Broker – No privileged conversations

46

Presented By:

“And for what we don’t cover, there’s insurance insurance.”

Presented By:

Key Take‐Aways

Two things everyone in the room can do to advance their organization’s risk management efforts: 1. Today, after this

seminar2. Next week