Embed Size (px)

Citation preview

1

Conference Call / WebcastRESULTS ANNOUCEMENT3rd Quarter 2008(Brazilian Corporate Law)

Almir Guilherme BarbassaCFO and Investor Relations OfficerNovember, 12th 2008

2

Disclaimer

The presentation may contain forecasts about future events. Such forecasts merely reflect the expectations of the Company's management. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forecasts. These predictions evidently involve risks and uncertainties, whether foreseen or not by the Company. Therefore, the future results of operations may differ from current expectations, and readers must not base their expectations exclusively on the information presented herein. The Company is not obliged to update the presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as oil and gas resources, that the SEC’s guidelines strictly prohibit us from including in filings with the SEC.

CAUTIONARY STATEMENT FOR US INVESTORS

3

NATIONAL OIL AND NATURAL GAS PRODUCTION – 3Q08 VS 2Q08

271 321 330

1,8541,797 1,883

3Q07 2Q08 3Q08Oil and LNG Natural Gas

Thou

s. b

pd

2,1752,213

2%

Oil and Gas Average National Production

2,068

• 2% Increase in oil production due to productiongrowth in platforms P-52 and P-54 .

105.295.262.2P-54

149.1

Production3Q08

P-52

Platforms

155.7107.9

Current ProductionOct, 2008Production 2Q08

7%

Thou

sand

bpd

1,887 1,885

1,898

July August September

4

P-51 P-53 FPSO Cidade de Niterói

JAN/09

NOV/08

JAN/09

FIRST OIL

Marlim Leste

Marlim Leste

Marlim Sul

FIELD

100 th. bpd3.5 million m3/d

180 th. bpd6 million m3/d

180 th. bpd6 million m3/d

CAPACITY

Arrival to thelocation andbegining theancoring

Wells connection

Move to location

NEXT STEPS

Coming to BrazilFPSO Cidade de Niterói

On LocationP-53

Soon leaving theshipyard

P-51

STATUSPLATFORMS

STATUS OF NEW PRODUCTION SYSTEMS

5

UPDATE ON SANTOS BASIN PRE SALT

BM-S-17

BM-S-50

BM-S-52(Corcovado)

BM-S-42

Wells Drilled

BM-S-21 (Caramba)

BM-S-8 (Bem-te-Vi)

BM-S-10 (Parati)

BM-S-11(Tupi)

(Guará)

BM-S-24(Jupiter)

(Yara)

BM-S-22

BM-S-9 (Carioca)

Updates:

• Completed the MinimalExploratory Program;

• Preparation for theextended well test ofTupi. The test and thepilot system are onschedule;

• Presently evaluatingwhere to developadditional well tests andpilot systems, in thecluster.

6

LIFTING COST IN BRAZIL

14.45 14.66 15.22 15.16 16.34 17.61

20.58 23.26 25.76 28.0434.80 36.79

0

10

20

30

40

50

60

70

80

2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

Lifting Cost (R$) Gov Take (R$)

7.33 7.65 8.60 8.66 9.88 10.21

10.62 12.48 14.56 16.1621.20 20.06

115

96.9

121

88.774.968.8

0

10

20

30

40

50

60

70

80

2Q07 3Q07 4Q07 1Q08 2Q08 3Q080

20

40

60

80

100

120

140

Lifting Cost (US$) Gov. Take (US$) Brent

US$/barrel R$/barrel

Increase in lifting cost without government take:

• Higher expenses with maintenance and intervention ;

• Higher expenses with personnel;

Increase in government take:

• Increase of the production in Roncador field which began to pay higher special participation tax;

• Increase in referential oil price from R$ 160,59 in 2Q08 to R$ 162,30 in 3Q08.

7

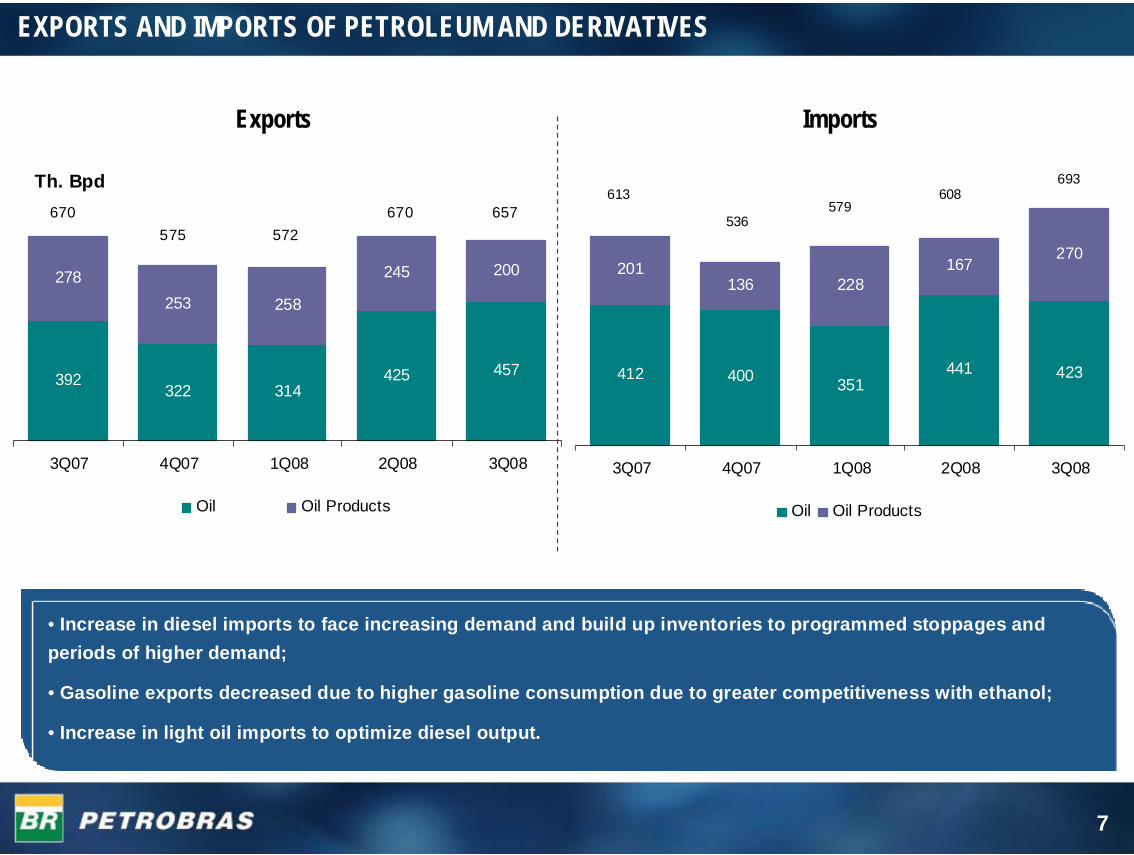

EXPORTS AND IMPORTS OF PETROLEUM AND DERIVATIVES

• Increase in diesel imports to face increasing demand and build up inventories to programmed stoppages and periods of higher demand;

• Gasoline exports decreased due to higher gasoline consumption due to greater competitiveness with ethanol;

• Increase in light oil imports to optimize diesel output.

392322 314

425 457

278253 258

245 200

3Q07 4Q07 1Q08 2Q08 3Q08

Oil Oil Products

670575 572

670 657

Th. Bpd

412 400 351441 423

201136 228

167270

3Q07 4Q07 1Q08 2Q08 3Q08

Oil Oil Products

613

536579

608693

Exports Imports

8

1,8211,790

1,846

1,7761,8061,796 1,795 1,7641,768

1,709

1,776

1,703

89909189 95 93

777978 7878 76

1,500

1,650

1,800

1,950

2Q07 3Q07 4Q07 1Q08 2Q08 3Q0830

40

50

60

70

80

90

Output of Domestic Oil Products Sales Volume of Total Oil ProductsUse of Installed Capacity - Brazil (%) Domestic Crude (%) of Total Feedstook Processed

Thous. bpd %

DOWNSTREAM OPERATIONAL PERFORMANCE

• Maintenance of the output in higher levels as a result of continued operational reliability;• Increase of oil products sales in the 3Q08 due to seasonality and economic growth;• Highlights: diesel sales growth (5% - supplied by imports), gasoline (7%) and fuel oil (8%).

9

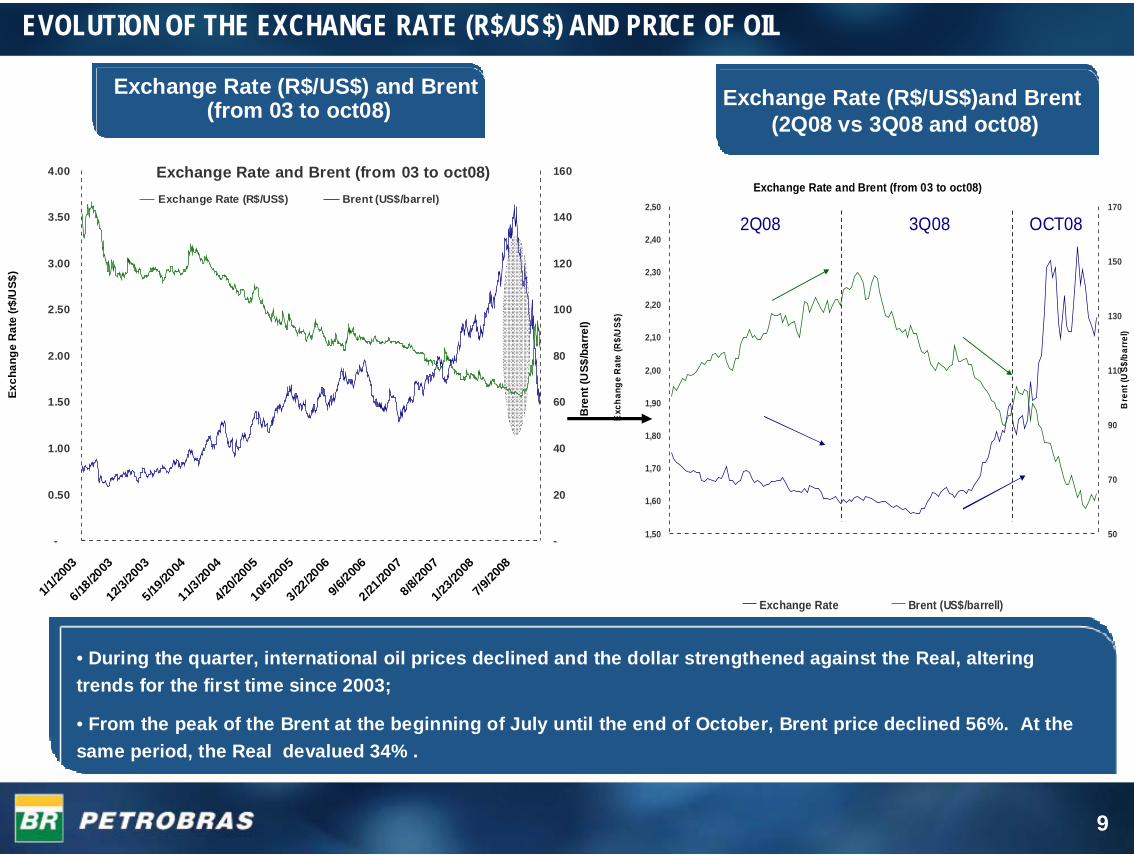

EVOLUTION OF THE EXCHANGE RATE (R$/US$) AND PRICE OF OIL

Exchange Rate (R$/US$)and Brent(2Q08 vs 3Q08 and oct08)

Exchange Rate (R$/US$) and Brent (from 03 to oct08)

• During the quarter, international oil prices declined and the dollar strengthened against the Real, altering trends for the first time since 2003;

• From the peak of the Brent at the beginning of July until the end of October, Brent price declined 56%. At the same period, the Real devalued 34% .

Exchange Rate and Brent (from 03 to oct08)

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

1/1/20

036/18

/2003

12/3/

2003

5/19/20

0411/3

/2004

4/20/2

005

10/5/20

053/22

/2006

9/6/200

62/21

/2007

8/8/20

071/2

3/200

87/9

/2008

Exch

ange

Rat

e (r$

/US$

)

-

20

40

60

80

100

120

140

160

Bre

nt (U

S$/b

arre

l)

Exchange Rate (R$/US$) Brent (US$/barrel)Exchange Rate and Brent (from 03 to oct08)

1,50

1,60

1,70

1,80

1,90

2,00

2,10

2,20

2,30

2,40

2,50

1/4/20

089/4/

2008

17/4/

2008

25/4/

2008

5/5/20

0813/5

/2008

21/5/

2008

29/5/

2008

6/6/20

0816

/6 /2008

24/6/

2008

2/7/20

0810/7

/2008

18/7/200

828

/7 /2008

5/8/20

0813

/8/20

0821/8

/2008

29/8/

2008

8/9/20

0816

/9/20

0824/9

/2008

2/10/200

810

/10/20

0820

/10/20

0828/1

0/200

8

Exc

hang

e R

ate

(R$/

US$

)

50

70

90

110

130

150

170

Bre

nt (U

S$/b

arre

l)

Exchange Rate Brent (US$/barrell)

2Q08 3Q08 OCT08

10

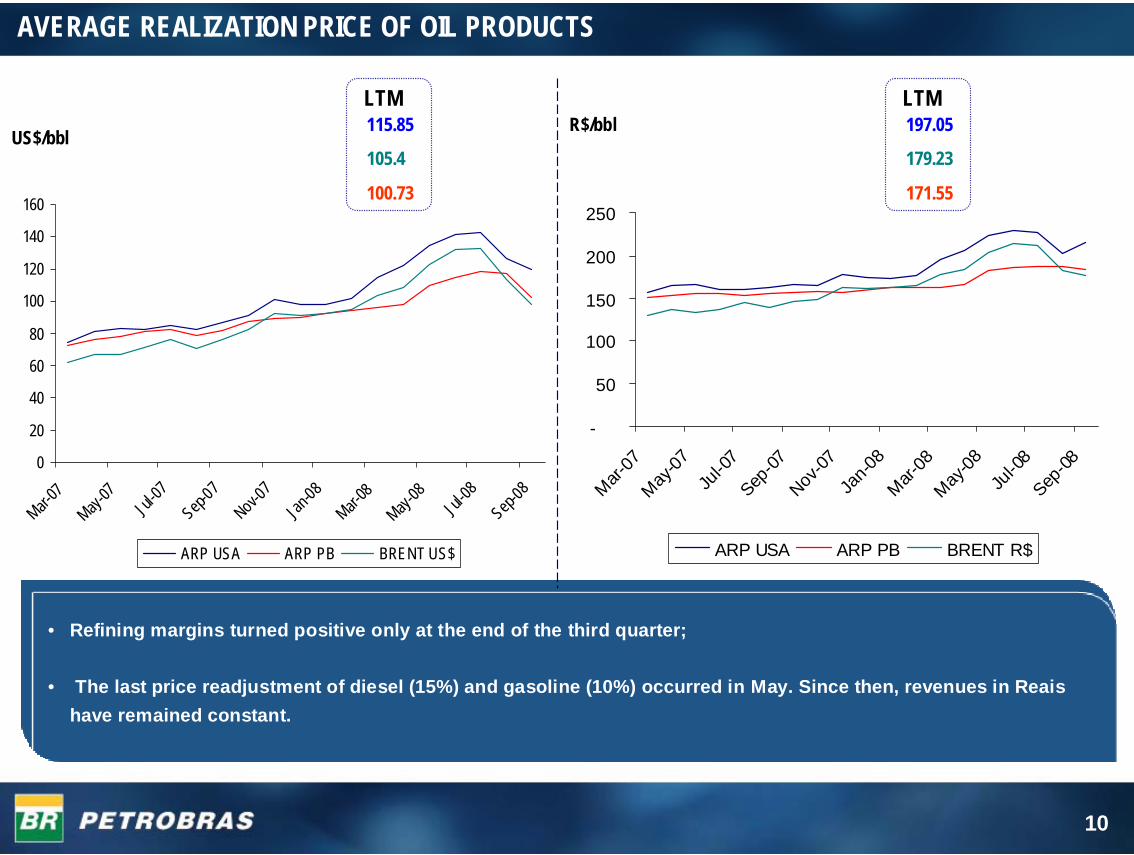

AVERAGE REALIZATION PRICE OF OIL PRODUCTS

US$/bbl

• Refining margins turned positive only at the end of the third quarter;

• The last price readjustment of diesel (15%) and gasoline (10%) occurred in May. Since then, revenues in Reaishave remained constant.

R$/bblLTM115.85

105.4

100.73

LTM197.05

179.23

171.55

0

20

40

60

80

100

120

140

160

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

ARP USA ARP PB BRENT US$

-

50

100

150

200

250

Mar-07

May-07

Jul-0

7Sep

-07Nov

-07Ja

n-08

Mar-08

May-08

Jul-0

8Sep

-08

ARP USA ARP PB BRENT R$

11

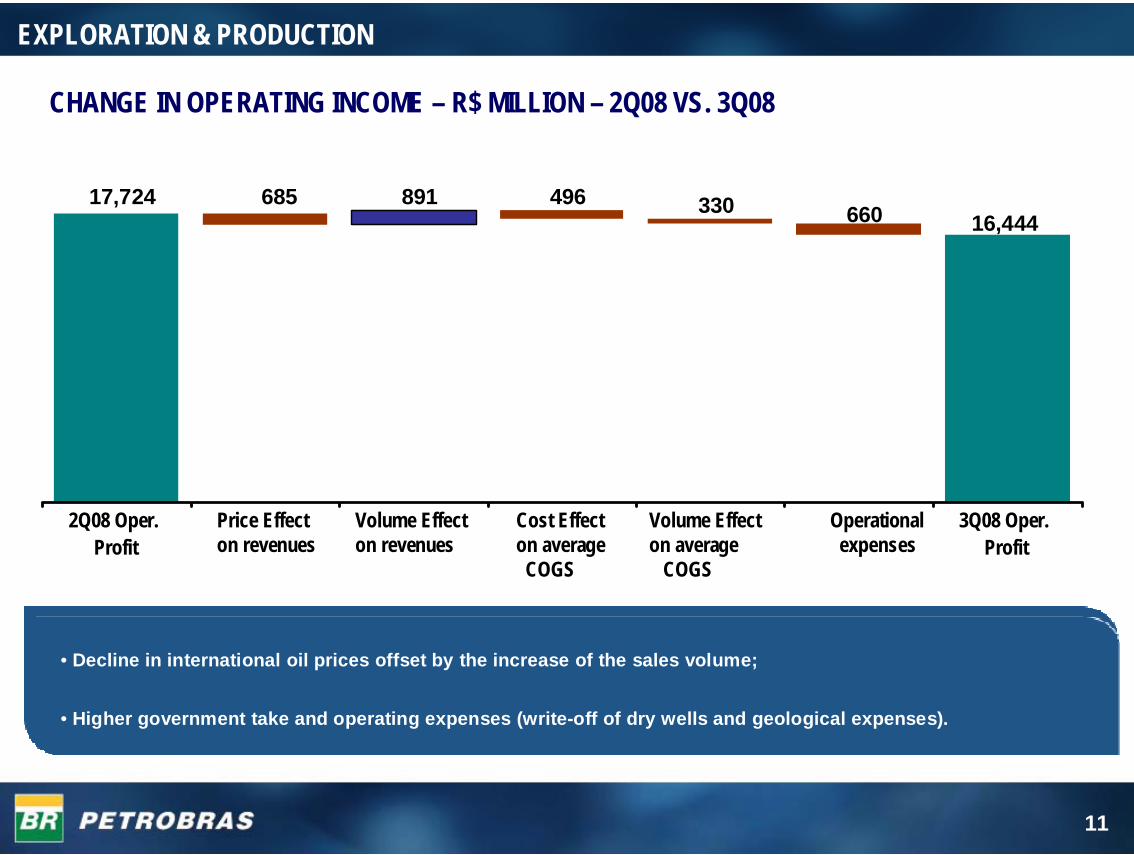

17,724 685 891 496 330 660 16,444

• Decline in international oil prices offset by the increase of the sales volume;

• Higher government take and operating expenses (write-off of dry wells and geological expenses).

EXPLORATION & PRODUCTION

2Q08 Oper.Profit

Price Effecton revenues

Volume Effecton revenues

Cost Effecton averageCOGS

Volume Effecton average

COGS

Operationalexpenses

3Q08 Oper.Profit

CHANGE IN OPERATING INCOME – R$ MILLION – 2Q08 VS. 3Q08

12

(577)

7,545

2,110 9,467

1,720

440

(2,549)

• Higher COGS due to increased oil products imports;

• Sales of inventories acquired at a higher cost in the previous quarters.

DOWNSTREAM

Volume Effecton average

COGS

OperationalExpenses

3Q08Oper. Loss

2Q08 Oper. Loss Volume Effecton Revenue

Price Effect onRevenue

Cost Effecton average COGS

CHANGE IN OPERATING INCOME – R$ MILLION – 2Q08 VS. 3Q08

13

• Lower margins due to increase of the purchase price of natural gas and electrical energy;

• Higher operating expenses from contractual fines and charges related to natural gas supply.

452

192

235 699

176

270 (266)

2Q08 Oper.Profit

Price Effecton revenues

Volume Effecton revenues

Cost Effecton averageCOGS

Volume Effecton average

COGS

Operationalexpenses

3Q08 Oper.Profit

GAS & POWER

CHANGE IN OPERATING INCOME – R$ MILLION – 2Q08 VS. 3Q08

14

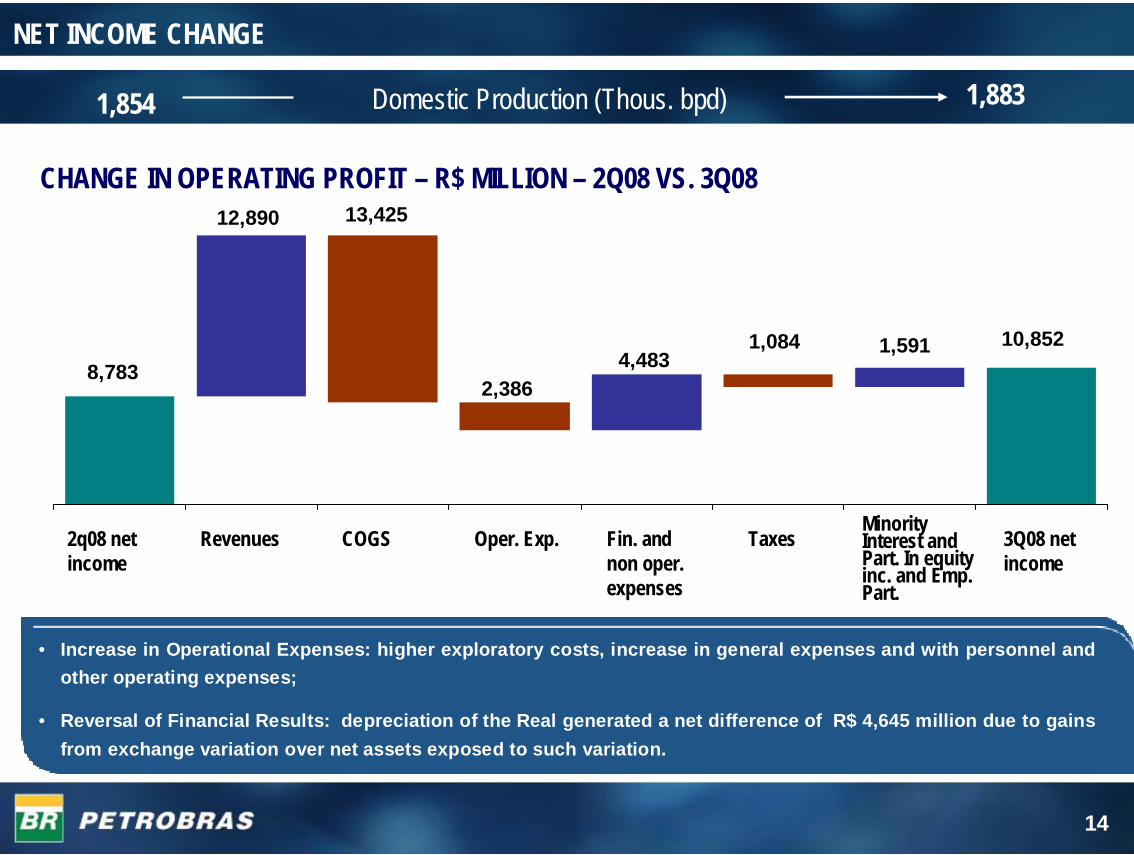

1,8831,854 Domestic Production (Thous. bpd)

• Increase in Operational Expenses: higher exploratory costs, increase in general expenses and with personnel and other operating expenses;

• Reversal of Financial Results: depreciation of the Real generated a net difference of R$ 4,645 million due to gains from exchange variation over net assets exposed to such variation.

NET INCOME CHANGE

8,783

12,890 13,425

2,3864,483

1,084 1,591 10,852

2q08 net income

Revenues Fin. andnon oper. expenses

MinorityInterest andPart. In equityinc. and Emp. Part.

Taxes 3Q08 net income

COGS Oper. Exp.

CHANGE IN OPERATING PROFIT – R$ MILLION – 2Q08 VS. 3Q08

15

ASSETS AND LIABILITIES SUBJECT TO MONETARY VALUATION

• The increase of the Net Asset exposure to exchange variation was due to the investments in International Area and E&P assets (Platforms and other oil production assets used in Brazil are owned through offshore subsidiaries) and to the decrease of the liabilities (suppliers) . • This increase of the Net Assets and the depreciation of the exchange rate (20% in the third quarter) resulted in an Net Financial Result of R$ 2,843 million in 3Q08.

(in R$ Million) 09.30.2008 06.30.2008AssetsCurrent Assets 6,884 6,692 Non-current Assets 26,498 20,227 Total Assets 33,382 26,919 LiabilitiesCurrent Liabilities (6,632) (6,332) Long-Term Liabilities (12,845) (12,601) Total Liabilities (19,477) (18,933)

Others -322 -258

Net Assets (Liabilities) in Reais 13,583 7,728

16

CASH FLOW

Jan-Sep/08 2007Net Cash Generated by Operating Activities 34,673 41,897 (-) Cash used for Capex (35,167) (45,233) E&P Investments (17,286) (20,405)

Downstream Investments (8,140) (9,647) Others (9,741) (15,181) (=)Free Cash Flow (494) (3,336)(-) Cash used in Financing Activities (1,801) (11,422)

Financing 4,386 (3,948)Dividends (6,187) (7,474)

(=) Net Cash Generated in the Period (2,295) (14,758)Cash at Beginning of Period 13,071 27,829 Cash at End of Period 10,776 13,071

R$ million

• The Cash Flow from Operating activities in 2008 is essentially in balance with our investment spending;

• Investment portfolio gives flexibility to adjust CAPEX spending.

17

DEBT PROFILE

• Petrobras maintains its relationship with numerous funding sources and has already financed all its needs for 2008;

• In 2008, including short term lines, the Company has already contracted/disbursed, approximately, US$ 9.2 billion. Of this total amount, US$1.1 billion was financed by capital markets and foreign commercial banks.

Sources 2007 2008Commercial Banks 3.6 5.3 Trade Finance 1.5 1.8 Internacional 1.0 0.6 Domestic 0.3 2.9Capital Markets 1.3 0.8Project Finance 2.3 2.9ECA - 0.2TOTAL 7.2 9.2

NEW FUNDING (US$ billion)

Sources 2007 Jun-08Commercial Banks 4.7 7.2Capital Markets 7.4 8Project Finance 4.4 4.8ECA 1.6 1.5BNDES 2.5 3.1Others 1.3 1.3TOTAL 21.9 25.9

SOURCE OF FUNDING (US$ billion) - US GAAP

18

QUESTION AND ANSWER SESSIONVisit our website: www.petrobras.com.br/ri

For more information contact:Petróleo Brasileiro S.A – PETROBRAS

Investor Relations

E-mail: [email protected]. República do Chile, 65 – 22o floor

20031-912 – Rio de Janeiro, RJ(55-21) 3224-1510 / 3224-9947

![TSKB 3Q08 IR-(14Nov08) internet.ppt [Read-Only] · 2008-11-21 · 3Q08 BRSA RESULTS INVESTOR PRESENTATION. TSKB APPENDICES. TSKB at a Glance ... (000 USD) 3Q07 3Q08 Change Adj. Net](https://img.pdfslide.us/doc/110x75/5fb9e4cfee80b63d2e0ecfb8/tskb-3q08-ir-14nov08-read-only-2008-11-21-3q08-brsa-results-investor-presentation.jpg)