Embed Size (px)

Citation preview

Principal Financial Group®

February 2017

A non-GAAP financial measure is a numerical measure of performance, financial position, or cash flows that includes adjustments from a comparable financial measure presented in accordance with U.S. GAAP. The company uses a number of non-GAAP financial measures that management believes are useful to investors because they illustrate the performance of the company’s normal, ongoing operations which is important in understanding and evaluating the company’s financial condition and results of operations. While such measures are also consistent with measures utilized by investors to evaluate performance, they are not, however, a substitute for U.S. GAAP financial measures. Therefore, on principal.com/investor, the company has provided reconciliations of the non-GAAP financial measures to the most directly comparable U.S. GAAP financial measure. The company adjusts U.S. GAAP financial measures for items not directly related to ongoing operations. However, it is possible these adjusting items have occurred in the past and could recur in future reporting periods. Management also uses non-GAAP financial measures for goal setting, as a basis for determining employee and senior management awards and compensation, and evaluating performance on a basis comparable to that used by investors and securities analysts. The company also uses a variety of other operational measures that do not have U.S. GAAP counterparts, and therefore do not fit the definition of non-GAAP financial measures. Assets under management is an example of an operational measure that is not considered a non-GAAP financial measure.

Use of Non-GAAP Financial Measures

2

Certain statements made by the company which are not historical facts may be considered forward-looking statements, including, without limitation, statements as to operating earnings, net income available to common stockholders, net cash flows, realized and unrealized gains and losses, capital and liquidity positions, sales and earnings trends, and management’s beliefs, expectations, goals and opinions. The company does not undertake to update these statements, which are based on a number of assumptions concerning future conditions that may ultimately prove to be inaccurate. Future events and their effects on the company may not be those anticipated, and actual results may differ materially from the results anticipated in these forward-looking statements. The risks, uncertainties and factors that could cause or contribute to such material differences are discussed in the company’s annual report on Form 10-K for the year ended Dec. 31, 2015 , and in the company’s quarterly report on Form 10-Q for the quarter ended Sep. 30, 2016, filed by the company with the U.S. Securities and Exchange Commission, as updated or supplemented from time to time in subsequent filings. These risks and uncertainties include, without limitation: adverse capital and credit market conditions may significantly affect the company’s ability to meet liquidity needs, access to capital and cost of capital; conditions in the global capital markets and the economy generally; volatility or declines in the equity, bond or real estate markets; changes in interest rates or credit spreads or a sustained low interest rate environment; the company’s investment portfolio is subject to several risks that may diminish the value of its invested assets and the investment returns credited to customers; the company’s valuation of investments and the determination of the amount of allowances and impairments taken on such investments may include methodologies, estimations and assumptions that are subject to differing interpretations; any impairments of or valuation allowances against the company’s deferred tax assets; the company’s actual experience could differ significantly from its pricing and reserving assumptions; the pattern of amortizing the company’s DAC and other actuarial balances on its universal life-type insurance contracts, participating life insurance policies and certain investment contracts may change; the company may not be able to protect its intellectual property and may be subject to infringement claims; the company’s ability to pay stockholder dividends and meet its obligations may be constrained by the limitations on dividends or distributions Iowa insurance laws impose on Principal Life; changes in laws, regulations or accounting standards; results of litigation and regulatory investigations; from time to time the company may become subject to tax audits, tax litigation or similar proceedings, and as a result it may owe additional taxes, interest and penalties in amounts that may be material; applicable laws and the company’s certificate of incorporation and by-laws may discourage takeovers and business combinations that some stockholders might consider in their best interests; competition from companies that may have greater financial resources, broader arrays of products, higher ratings and stronger financial performance; a downgrade in the company’s financial strength or credit ratings; changes in investor preferences; inability to attract and retain qualified employees and sales representatives and develop new distribution sources; international business risks; fluctuations in foreign currency exchange rates; the company may need to fund deficiencies in its “Closed Block” assets that support participating ordinary life insurance policies that had a dividend scale in force at the time of Principal Life’s 1998 conversion into a stock life insurance company; the company’s reinsurers could default on their obligations or increase their rates; risks arising from acquisitions of businesses; and a computer system failure or security breach could disrupt the company’s business and damage its reputation.

Forward Looking Statements

3

26%

24% 15%

16%

13% 6%

RIS - Fee

Principal GlobalInvestors

PrincipalInternational

RIS - Spread

SpecialtyBenefits

Individual Life

Operating Earnings1

$1,887.6 million As of Dec. 31, 2016

Fortune 500 company; 137 year history A Leading Financial Services Company

67%

24%

9% Principal GlobalInvestors

PrincipalInternational &Other PFGEntitiesThird Party AssetManagers

Assets Under Management2

$591.6 billion As of Dec. 31, 2016

1 Trailing Twelve Months. Pre-tax. Results exclude Corporate. 2 Assets under management by asset manager. 4

Company Overview

Fee

Spread

Risk

Segment Reporting Structure

Principal Financial Group Dan Houston CEO

Deanna Strable CFO

Retirement & Income

Solutions (RIS) Nora Everett

President

Principal Global Investors (PGI)

Jim McCaughan President

U.S. Insurance Solutions (USIS) Amy Friedrich/Greg Linde

SVP

Corporate

Management team averages 30 years of industry experience

Principal International (PI)

Luis Valdes President

RIS – Fee RIS – Spread

Specialty Benefits Life

5

Company Overview

6

Where we compete More than 70 countries around the world

As of 12/31/2016

Asset management, retirement/long-term savings, risk protection

Asset management, retirement/long-term savings

Asset management

Company Overview

*As of 12/2017

Experienced Management Team

7

Company Overview

Name Age* Title (Industry/PFG)*__

Daniel J. Houston 56 Chairman, President & Chief Executive Officer 33/33 Nora M. Everett 58 President - Retirement & Income Solutions 26/26 James P. McCaughan 64 President - Global Asset Management 43/15 Deanna D. Strable 49 Executive VP & President - U.S. Insurance Solutions 28/28 Luis E. Valdes 60 President - International Asset Management and Accumulation 29/26 Timothy M. Dunbar 60 Executive VP & Chief Investment Officer 36/31 Terrance J. Lillis 65 Executive VP & Chief Financial Officer 35/35 Gary P. Scholten 60 Executive VP & Chief Information Officer 37/37 Karen E. Shaff 63 Executive VP, General Counsel & Secretary 35/35 Elizabeth S. Brady 57 Senior VP & Chief Marketing Officer 33/4 Gregory B. Elming 57 Senior VP & Chief Risk Officer 35/35 Elizabeth L. Raymond 51 Senior VP & Chief Human Resources Officer 26/17

Sources: 1Pensions & Investments, “The Best Places to Work in Money Management among companies with our size category”, PFG recognition 12/12/2016. 2Asociacion de Administradóras de Fondos Mutuos De Chile, June 2016. 3The 5th largest manager of domestic real estate equity (net of leverage), out of 66 managers profiled. Managers ranked by U.S. institutional, tax-exempt assets managed internally, as of Jun. 30, 2016. “Real Estate Managers”, PENSIONS & INVESTMENTS, Oct 3, 2016. 4 12th largest manager of high yield securities, out of 85 managers profiled. Managers ranked by U.S. institutional, tax-exempt assets managed internally, as of Dec. 31, 2015 “Largest Money Managers”, PENSIONS & INVESTMENTS, May 30, 2016. 5March 28, 2016, U.S. Environmental Protection Agency, Principal Real Estate Investors awarded. 6 PLANSPONSOR Recordkeeping Survey, June 2016. 7AUM among multi-country pension providers. 8CONSAR, September 2016. 9Ranking in terms of AUM for PGBL and VGBL products, Fenaprevi. September 2016. 10Gadbury Group MPF Market Share Report, September 2016. 11PLANSPONSOR Defined Benefit Administration Survey, May 2015. 12PLANSPONSOR Recordkeeping Survey, June 2016. 13PLANSPONSOR NQDC Buyer’s Guide, July 2015. 14LIMRA 2015 survey: Non-medical based on fully insured employer contracts in force. 15 LIMRA 2015 survey: Individual Disability Insurance (IDI) rank based on in-force premium

Industry Leadership

Global Retirement and Long-Term Savings

Risk Protection

Global Asset Management

#1 Non-qualified deferred compensation13

#4 Non-medical coverages14 #5 Individual Disability

Insurance15

#4 provider of DC plans6

#2 Pension provider in Latin America7 #7 AFORE – Mexico8

Brasilprev #1 market share – Brazil9

#5 MPF provider – Hong Kong10

#1 provider of DB plans11

#1 provider of ESOP plans12

Best Place to Work in Money Mgmt1 #1 APV – Chile Funds2

Top 10 manager Real Estate3 12th largest manager High Yield4

ENERGY STAR Partner of the Year5

8

Company Overview

Current Ratings (As of January 2017)

Ratings related to Principal Life Insurance Company and Principal National Life Insurance Company.

9

Company Overview

Moody’s Investors Service ‘A1’, Good – fifth highest of 21 rating levels. Outlook: Stable

Fitch Ratings ‘AA-’, Very Strong – fourth highest of 19 rating levels. Outlook: Stable

Standard & Poor’s ‘A+’, Strong – fifth highest of 20 rating levels. Outlook: Stable

A.M. Best ‘A+’, Superior – second highest of 13 rating levels. Outlook: Stable

Strong business fundamentals

10 1Department of Labor & Cerulli Associates, 2015. 2For trailing 12 months. 3Defined contribution and defined benefit.

Net cash flow as a percent of beginning of year account value (2011-2015 average)

- 0.1%

+2.4%

Industry1 Principal

4Q 2012

4Q 2016 CAGR

RIS total account value $172B $231B 8%

RIS-Fee return on net revenue2 30.6% 32.7%

RIS-Spread return on net revenue2 56.8% 61.3%

Participants3 3.9M 5.1M 7%

Retirement & Income Solutions

Customer-Centric Business Model

Bundled

Unbundled

Small Case Large Case

BU

SIN

ESS

MO

DEL

TARGET MARKET

MetLife

Nationwide

John Hancock

ING/VOYA

Transamerica Great West

Mass Mutual

Fidelity T.Rowe Price

Prudential

Vanguard

Wells Fargo

11

Retirement & Income Solutions (RIS – Fee)

0

5

10

15

20

25

UNITED STATES 2nd THROUGH 10thLARGEST

MARKETS COMBINED

$ Tr

illio

ns

Defined Contribution

+ IRA

Defined Benefit

Source: Retirement Markets 2015, Retirement Research Inc., April 2015

Retirement market opportunities RETIREMENT READINESS: • New plan formation • Non-participants • Under-saved INCOME SOLUTIONS: • Yield/Income • Outcomes:

−Longevity −Market volatility −Inflation

The Top Retirement Market in the World

12

Retirement & Income Solutions (RIS – Fee)

Principal Total Retirement Suite SM Still a differentiator

All rankings sourced from PLANSPONSOR magazine as follows – Defined Benefit: DB Administration Survey 05/15; Defined Contribution and ESOP: Recordkeeping Survey 06/16; Nonqualified Deferred Compensation: PLANSPONSOR NQDC Buyer’s Guide, July 2015

Defined Benefit

#1 DB provider

(by # of clients)

Defined Contribution

#4 DC plan recordkeeper

(by # of plans)

Employee Stock Ownership Plan

#1 ESOP plan recordkeeper

(by # of plans)

Nonqualified Plans

#1 Deferred Comp provider

(by # of plans)

13

Retirement & Income Solutions (RIS – Fee)

2.9 3.0 3.4 3.6 4.2

2.5 1.8 1.8 1.9 2.3

2.6 3.1 1.9 1.9

2.6

3.3 2.7 2.2 2.5

3.3

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

2012 2013 2014 2015 2016

$ B

illio

ns1 4th Quarter

3rd Quarter2nd Quarter1st Quarter

Balanced Sales Approach

14

Retirement & Income Solutions (RIS – Fee)

11.3

12.4

9.9 9.3

10.6

1 Transfer deposits

3.7 4.1 4.3 4.8 5.0

3.5 4.2 4.3 4.6 4.9

3.3 3.6 4.1

4.3 4.6 3.4 3.8

4.1 4.2

4.5

0

2

4

6

8

10

12

14

16

18

20

2012 2013 2014 2015 2016

$ B

illio

ns2

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

• People making a deferral +40%1

• Avg deferral per member +10%1

• People receiving a match +45%1

The Power of Payroll Deduction

13.9

15.7 16.8 17.9

1 4Q11 compared to 4Q16 2 Recurring deposits

19.0

15

Retirement & Income Solutions (RIS – Fee)

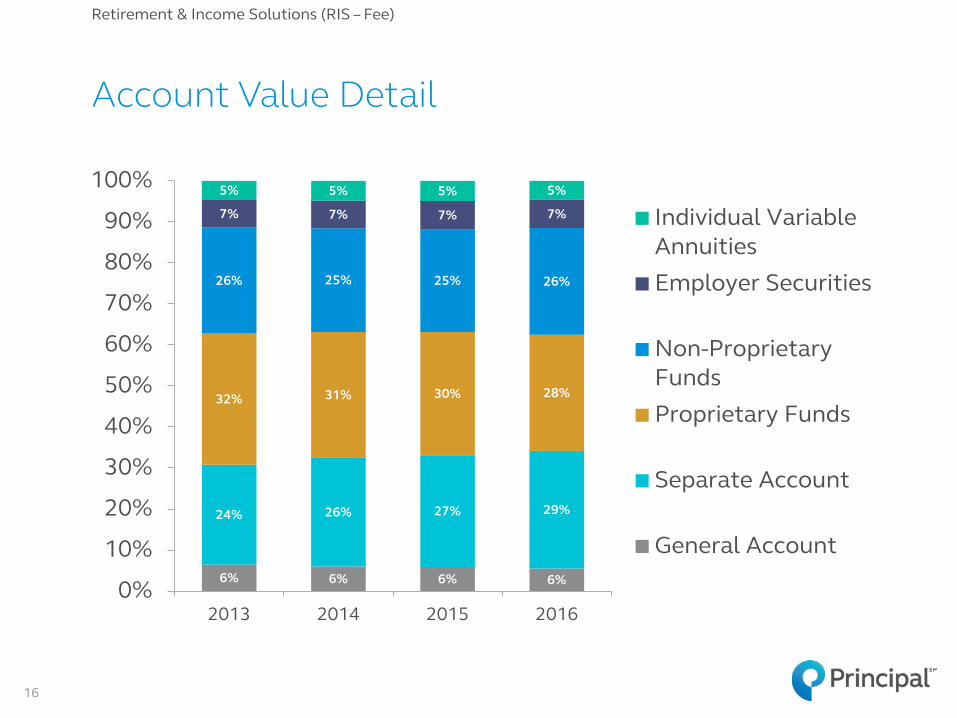

6% 6% 6% 6%

24% 26% 27% 29%

32% 31% 30% 28%

26% 25% 25% 26%

7% 7% 7% 7%

5% 5% 5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016

Individual VariableAnnuitiesEmployer Securities

Non-ProprietaryFundsProprietary Funds

Separate Account

General Account

Account Value Detail

16

Retirement & Income Solutions (RIS – Fee)

Multiple Businesses Leverage Success Revenue sourced from 401(k) platform ($Billions)

Variable Annuities, RIS – Spread, PGI, and Individual Life are all beneficiaries

17

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2016 2021E

$Bill

ions

Other PFG businessesDefined contribution

$0.6B

$0.4B

Retirement & Income Solutions (RIS – Fee)

Innovative Solutions: Solving Income Needs

MULTI-PRODUCT SOLUTION SET

• “Through Retirement” Lifecycle Funds • Mutual Funds that: ‒Generate income ‒Preserve capital ‒Protect against inflation ‒Address market volatility

• Annuities to provide: ‒Fixed returns ‒Guaranteed income ‒Protection against volatility

• Bank products • Full Service Payout ‒Defined Benefit plan terminations

ACCUMULATION RETIREMENT INCOME

OUR APPROACH: • Education • Planning assistance

(RetireSecure®)

• Full array of options • Innovative solutions

18

Retirement & Income Solutions

$59 B

$189 B

19

$143 B

Diversified Global Asset Management Organization

$391B

Fixed Income Equity Alternatives

19

of AUM1

• Broad range of investors in over 70 countries

• Offices in major money centers worldwide

• Long commitment to corporate stewardship; signatory to United Nations’ Principles for Responsible Investment (PRI)

• Principal ranked among top companies with 1,000+ employees in Pensions & Investments’ Best Places to Work in Money Management, for the last four years2

1AUM as of 12/31/2016. 2Pensions & Investments, “The Best Places to Work in Money Management among companies with our size category”, PFG recognition 12/12/2016.

Principal Global Investors

Global leadership in funds

20 20

PGI/Funds integration makes Principal a global destination for funds • $176B in AUM across U.S. and International platforms, as well as

various private funds1

• Strong performance across boutiques and strategies

• Well positioned in Active and Smart Beta ETFs

Key functions aligned globally • Distribution, governance and operations

Capabilities compelling to big intermediaries

• Focus on global consultants, global distributors, U.S. wirehouses, U.S. independent broker-dealers and RIAs2, private banks

Work closely with PI in their local markets

1As of 12/31/2016. Includes Principal Funds, PGI Trust CITs, PGI Dublin Funds, PGI Australia Funds, and various boutique-level funds. 2RIA: Registered Investment Advisor.

Principal Global Investors

Morningstar rankings Percentage of funds in the top two quartiles

Top Tier Investment Performance

88% 89% 93%

59%

90% 86%

51%

76%

86%

1-Year 3-Year 5-Year

12/31/2015 09/30/2016 12/31/2016

Principal “I” shares; if no “I” share class then “A” share class; separate accounts use “R6” rate level; Includes Principal mutual funds, separate accounts and collective investment trusts (CITs); Excludes money market, stable value and U.S. Property separate account.

4 OR 5 STARS = 36 FUNDS 3 STARS 19 FUNDS

2 STARS 3 FUNDS

1 STAR 1 FUND

of rated funds have 4 or 5 star rating

61%

21

Principal Global Investors

Wells Fargo Merrill Lynch Morgan Stanley Raymond James Principal Securities Inc

Top 5 distributors Top 5 U.S. strategies

Distribution – Principal Funds

1 AUM figures include both Retail and Retirement AUM and remove double counting for fund-of-fund assets. As of 12/31/2016.

Success through engaging distributors and advisors across channels

AUM (1) 5-Yr AUM CAGR

Target Date $25.9B 8.5%

Dynamic Outcome Strategies $14.0B 33.6%

Strategic Asset Management $13.9B 9.5%

Midcap $10.9B 44.2%

Preferred Securities $5.2B 15.5%

22

Principal Global Investors

• Strong teams, representing all boutiques

• Close partnership with product specialists in the boutiques

• Broad range of specialist investment capabilities enables us to attract top sales talent

• #30 on Institutional Investor Top 3001

Global Distribution Institutional

$110.2 $114.7

$122.0 $130.6

2013 2014 2015 2016

Principal Global Investors Institutional AUM

($ in billions)

1 Managers ranked by total assets under management. II 300 America’s Top 300 Money Manager, Institutional Investor, July 2016, data as of 12/31/2015. 23

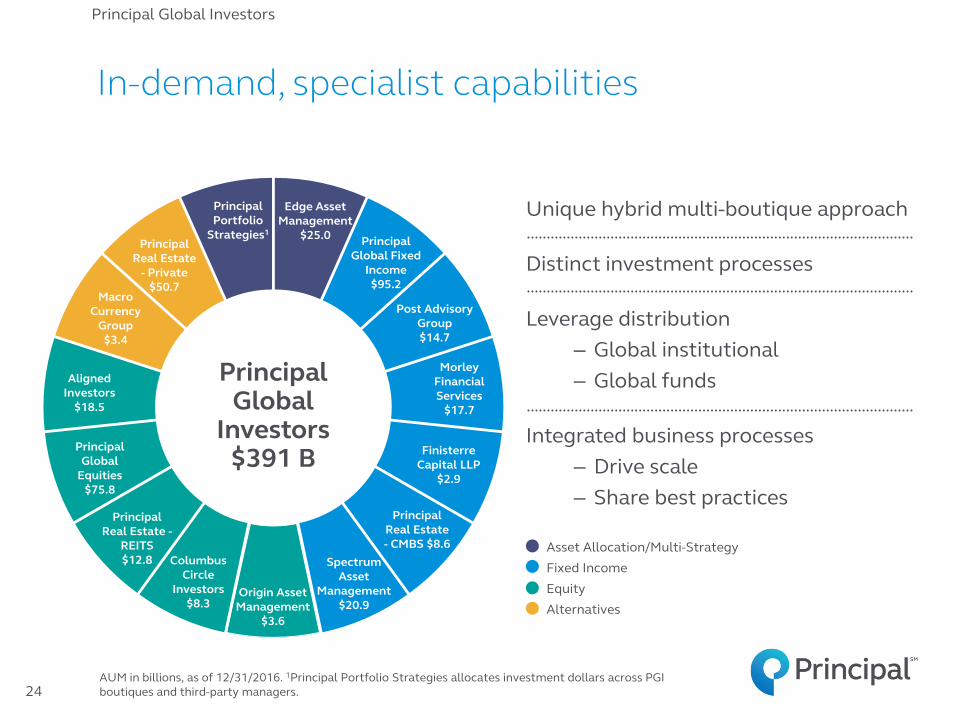

Principal Global Investors

In-demand, specialist capabilities

Principal Global

Equities $75.8

Principal Portfolio

Strategies1

Principal

Global Fixed Income $95.2

Finisterre Capital LLP

$2.9

Principal Global

Investors $391 B

Principal Real Estate

- Private $50.7

Morley Financial Services

$17.7

Edge Asset Management

$25.0

Post Advisory Group $14.7

Columbus Circle

Investors $8.3

Origin Asset Management

$3.6

Spectrum Asset

Management $20.9

Macro Currency

Group $3.4

Principal Real Estate -

REITS $12.8

Principal Real Estate - CMBS $8.6

Aligned Investors

$18.5

Unique hybrid multi-boutique approach

Distinct investment processes

Leverage distribution – Global institutional – Global funds

Integrated business processes – Drive scale – Share best practices

24

Asset Allocation/Multi-Strategy Fixed Income Equity Alternatives

AUM in billions, as of 12/31/2016. 1Principal Portfolio Strategies allocates investment dollars across PGI boutiques and third-party managers.

Principal Global Investors

• Industry leader in delivering solutions, including multi-asset solutions

• Strong and growing suite of alternatives

• Early entrant in the Active ETF space

• Hybrid, Passive and Indexed offerings on retirement platform of the Principal Financial Group

• With boutiques across asset classes, sector rotation presents opportunities

Well-Positioned for Industry Trends

Generate Income

Manage Volatility

Protect Purchasing

Power

Client Needs

25

Principal Global Investors

Our Locations We operate in emerging markets with a fast growing middle class

26

Principal International

(Year) = Principal entered country

PI Sourced AUM as of 12/31/2016

Principal Financial

Group Mexico (1993)

• Annuities, Mutual Funds, Pensions, Asset Management

• AUM of $8.7B • Wholly owned

Chile (1995) • Annuities, Mutual Funds, Asset

Management, Mandatory Pensions, Voluntary Pensions

• AUM of $41.7B • Wholly owned • Cuprum – a 98% majority owned

company AUM of $35.5B

Brazil (1999) • Annuities, Pensions,

Mutual Funds, Asset Management

• Brasilprev – a 25% owned joint venture with Banco do Brasil

AUM of $61.8B • Claritas – 100% owned

mutual fund company AUM of $1.3B

India (2000) • Asset Management,

Mutual Funds, Advisory Services

• AUM of $0.7B • 79% majority owned

company with Punjab National Bank

Malaysia (2003) • Conventional & Islamic

Asset Management, Mutual Funds, Pensions

• AUM of $12.0B • CIMB-Principal – 40%

owned joint venture with CIMB Group; 50% owned Islamic company with CIMB

China (2005) • Asset Management,

Mutual Funds • AUM of $101.3B • CCB-Principal – a 25%

owned joint venture with China Construction Bank

Hong Kong (1996) • Asset Management,

Mutual Funds, Pensions • AUM of $7.6B • AXA – Transaction closed

9/1/2015 adding AUM of $3.1B

• Wholly owned

Thailand (2010) • Asset Management, Mutual Funds • AUM of $2.9B • Wholly owned subsidiary of Malaysian JV

Indonesia (2007) • Asset Management,

Mutual Funds • AUM of $0.4B • Wholly owned

subsidiary of Malaysian JV

Singapore (2006) • Asset Management • AUM of $5.7M • Wholly owned

subsidiary of Malaysian JV

Country 2014 rank 2019E rank

2024E rank

2030E rank

U.S. #1 #1 #1 #2

China #2 #2 #2 #1

Brazil #7 #7 #6 #5

India #9 #5 #4 #3

Mexico #15 #14 #13 #13

Indonesia #16 #15 #15 #12

$64 $102

$400

2012 2020 2050

2014 2030 16 year CAGR

$34 Trillion $100 Trillion 7%

Total GDP for Six Listed Countries

6.0% CAGR

Global Asset Management Industry Projected AUM

In Trillions

4.7% CAGR

Sources: Asset Management 2020: A Brave New World, PwC, 2014; The age of asset management? Speech by Andrew G Haldane, Executive Director, Financial Stability, Bank of England, at the London Business School, London, 4 April 2014.) ; http://www.cebr.com/reports/world-economic-league-table-2015/

High Growth High Potential Markets

27

Principal International

Joint Venture Partner Partner’s Industry Ranking Partner’s Distribution Reach

Banco do Brasil Largest bank in Latin America(1)

5,430 branches (2)

65 million customers (2)

2nd largest listed bank in world(1)

14,917 branches (3)

341 million retail customers (3)

5th largest banking group in ASEAN (4)

992 branches (4)

12 million retail customers(4)

2nd largest Nationalized bank in India(5)

6,560 branches (6)

104 million retail customers (6)

SOURCE: (1) S&P Global Market Intelligence, 4/11/2016 in terms of total assets; (2) Banco do Brasil 3Q 2016 Historical Data IR site; (3) CCB 2015 Annual Report (4) CIMB Group 2015 Annual Report; (5) Indian Banks’ Association March 2016 in terms of assets; (6) PNB 2015 Annual report – customer count based on customer accounts

Leveraging Strong Marquee Partners Principal International

28

Proven Strength & Success

BRAZIL MEXICO CHILE

Brasilprev: #1 in net

deposits and total market

share

7th largest AFORE (by AUM)

#1 APV: PI Chile and

Cuprum

Principal is 2nd Largest Pension Provider in Latin America

Brazil source: Ranking in term of AUM for PGBL and VGBL products, Fenaprevi September 2016. Mexico source: CONSAR September 2016. Chile source: Asociacion de Administradóras de Fondos Mutuos De Chile September 2016. Principal is 2nd largest pension provider in Latin America by AUM among multi-country pension providers. 29

Principal International

Building a Strong Foundation

*Mandatory Provident Fund. Malaysia source: Lipper. Percentage of market share as of December 2016. Hong Kong source: Gadbury Group MPF Market Share Report as of September 2016. China source: East Money. Based on AUM as of December 2016. India source: Company data/media tracking at launch 11/12

HONG KONG

5th largest MPF provider

MALAYSIA

#2 in PRS

CHINA

#6 in Mutual Funds

INDIA

1st mover in advisory services business

30

Principal International

Focus on the SMB market Solutions for business owners, employers, and individuals

• Business Owner Executive Solutions (life & disability)

Business Owners Individuals Employers

• Group Insurance (dental, vision, disability, life)

• Multi-life Disability • Nonqualified Deferred

Compensation

• Group Voluntary Insurance (dental, vision, disability, life, critical illness)

• Individual Disability Insurance • Individual Life Insurance • Individual Dental

U.S. Insurance Solutions

31

2015 Market Share

2015 Industry

Rank Specialty Benefits • Total Group In-Force Contracts 7.5% #4

• Life 10.2% #3

• Disability 7.9% #5

• Dental 5.1% #7

• Individual Disability In-Force Premium 9.5% #5

• Individual Disability New Sales Premium 15.8% #3

Individual Life • Non-Qualified Plans1 13.9% #1

• Total Life New Sales Premium 1.5% #20

Success Reflects Expertise Serving SMB Market

Nonqualified Plans ranking from PLANSPONSOR Buyers Guide Survey, July 2015. All other rankings are from LIMRA 2015. 1Excludes governmental 457 plans. 2Based on LIMRA 2014 data

32

U.S. Insurance Solutions

BOES 28%

ER/NQ 25%

Individual 47%

Solutions for businesses, business owners and key executives

Business owners’ financial challenges • Exiting the business • Business transition • Retaining key employees • Retirement planning

Solutions for key employees • Retirement income • Survivor income • Business protection

Focus on the Business Market

2016 Sales

BOES = Business Owner/Executive Solutions ER/NQ = Employer/Non-qualified

33

U.S. Insurance Solutions: Individual Life

5.6%

10.9%

3.1% 1.6%

Group Benefits Individual DI

The Principal Industry

Balanced Portfolio and Above Industry Premium Growth

2016 Total Premium & Fees

Group Benefits

81%

• Stable loss ratios • Attractive margins • ROE of 14% +

Source: LIMRA 2012-2015

3 Year In-Force Premium Growth (2012 – 2015 CAGR)

34

U.S. Insurance Solutions: Specialty Benefits Insurance

Group Disability

27%

Dental/ Vision 47%

Group Life 26%

Group Benefits

83%

Individual Disability

17%

U.S. Distribution Overview

PRINCIPAL CONNECTION

• 70 counselors with focus on education

PRINCIPAL ADVISOR

NETWORK

• 1,200 advisors • Sell all products • Financial

Planning Focused

BANKS INSURANCE-ORIENTED

INVESTMENT-ORIENTED

• Wirehouses • Regional

Broker/Dealers • Planners

• Brokerage General Agents

• Insurance Producers

• Banks • Broker/

Dealers • Marketers

THIRD PARTY PROPRIETARY

Global Firm Relations Select 3rd party distributors with dedicated support

STRENGTHENS RELATIONSHIPS AND FUELS SALES GROWTH

All supported by DEDICATED SERVICE TEAMS providing education, training, counseling and retention

WHOLESALE CHANNELS Group

Benefits Retirement Investment Solutions Annuities NQDC

Disability Insurance

Retail Life ESOP

35

Distribution

Broad and Deep Distribution Proprietary provides foundation; 3rd party provides accelerated growth

Product Line New Sales 1st 2nd 3rd Top 3

Represent

NQ Life 38% Retail Life 58% Individual Disability Plus Group 38%

Group Benefits 10% Fixed Annuities 74% Variable Annuities KeyCorp Ins.

Agency 97%

Mutual Funds 19% FSA – New Sales Assets 30%

FSA – New Sales Case Counts 34%

Highland Capital Brokerage

Principal Advisor Network

Principal Advisor Network

Principal Advisor Network

Principal Advisor Network

Principal Advisor Network

Principal Advisor Network

Rankings and percentages as of 12/31/2016

36

Distribution

Corporate Public Bonds

28%

Corporate Private Bonds

16%

CMBS

5%

Commercial Mortgages

15% MBS

6% ABS

5%

Government, Agency, State & Political

10%

Other1

11% Cash

4%

1Other includes Equity Securities, Residential Mortgages, Real Estate, Policy Loans, Investment in Equity Method subs, Direct Finance Leases and Other Investments

Investment philosophy & strategy

Our strategy hasn’t changed:

High quality, well-diversified portfolio Liability-driven investment approach Active asset/liability management Optimized risk adjusted yields and returns Global collaboration and best practices Portfolio responsibility remains at local country

Total PFG as of 12/31/2016 GAAP carrying value

Diversified investment portfolio Total invested assets & cash

$78.6B Total invested assets & cash

37

Investments

Continual shift in mix of business leading to a higher ROE and more free cash flow

68%

12%

20%

2016

Operating Earnings After tax

Power of our Fee-Based Model

30%

40%

30%

2001

Fee Spread Risk

Fee includes Retirement & Income Solutions – Fee, Principal Global Investors, and Principal International. Spread includes Retirement & Income Solutions - Spread. Risk includes U.S. Insurance Solutions.

38

Financials

Returning Capital to Shareholders

• Less capital needed to support organic growth • Moving to higher dividend payout ratio • Diligently pursuing active acquisition opportunities • Opportunistically buying back shares

Organic Growth Dividends Available Capital

Current Targeted 2007

50%

25%

25%

34% 33%

33%

30% 40%

30%

(Acquisitions & share buybacks)

39

Financials

Grow capital • Organic growth • Mergers and

acquisitions (M&A)

Expect to deploy 65–70% of our net income over the long-term, with fluctuations in any given year

Balanced capital deployment strategy

Return capital • Common

stock dividends • Share repurchases

Optimize capital structure • Financial flexibility

40

Long-term financial outlook

Financials

Driving ROE Growth Earnings

+ 4-5% for market performance

+ 4-5% for growth from sales/NCF

+ 1-2% operational efficiency

• Organic growth • Dividend growth • Opportunistic

share repurchases

ROE =

30-60 bps average annual ROE

improvement

Equity

41

Financials

Executing on our strategy to increase our global footprint and fee-based earnings

We’ve Played Offense Since the Recession

Opportunity Year

Announced Rationale

AXA Hong Kong Pension 2014

15 year exclusive distribution with 4,440 agents

Gateway into China

2012 Complete offering in Chile

with marquee pension and savings franchise

2012 Entry into Brazil mutual

fund and asset management market

2011 Enhance global equity investment capabilities

2011 Establish leadership in

emerging markets fixed income investing

2011 Solidify position as a leader in Mexican Afore market

BrasilPrev 2010 23 year extension of

successful JV with Banco do Brasil

Emerged from financial crisis in a position of strength and flexibility

AFORE

42

Financials

Capital Deployment

Deployed $480 million

$287 $150

$50

Deployed $855 million

$375

$200

$180

$100

Long term: expect to deploy 65–70 percent of our net income with fluctuations in any given year

Deployed $1.1 billion

$441

$275

$355

43

Financials

Deployed $856 million

$465 $257

$40 $94

2013 2014 2015 2016

Common Stock Dividends Share Repurchases Strategic Acquisition Surplus Note Redemption

$ in millions

If macroeconomics change by…

Equity market return +/- 10%

Interest rates

+/- 100 bps FX: US dollar

changes +/- 2%

Then Principal’s annual pre-tax operating earnings will change by…

+/- 4-6%1 +/- < 1%2 -/+ < 1%3

And the primary businesses impacted are…

RIS – Fee RIS – Spread PI

PGI Individual Life

SBD

1 Assumes an immediate 10% change in the S&P 500 followed by 2% growth per quarter thereafter. 2 Excludes the impact of actuarial unlockings. 3 Principal is primarily impacted by changes in Latin American and Asian currencies. Inverse relationship between movement of the US dollar and impact to Operating Earnings.

What if things don’t go as expected?

44

Changes in key macroeconomic conditions have an impact on Principal’s annual pre-tax operating earnings

Long-term financial outlook

Financials

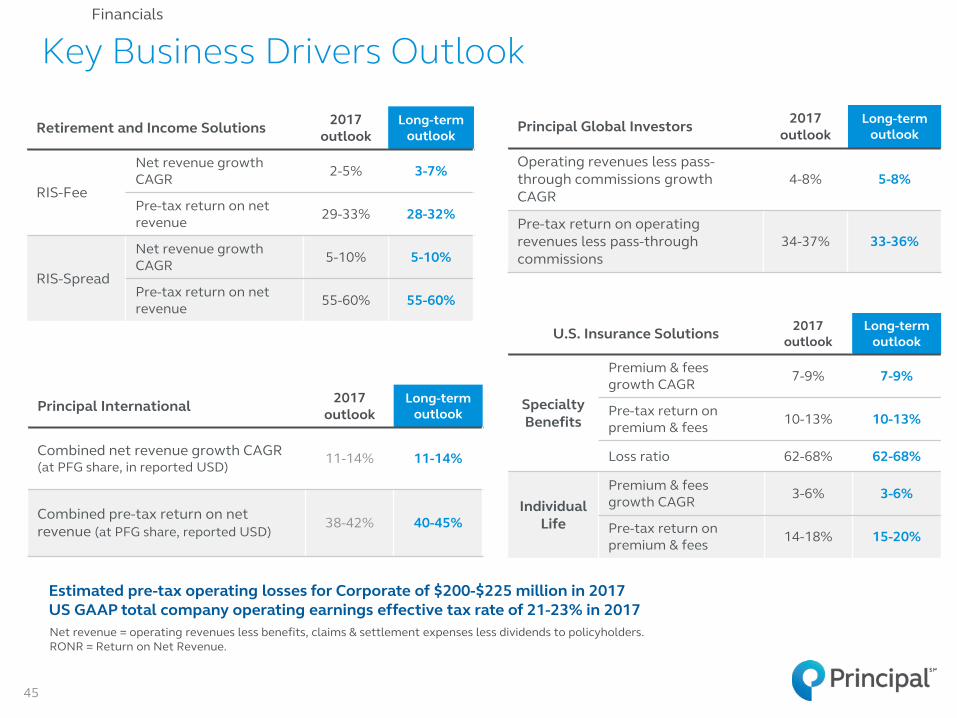

Key Business Drivers Outlook

Net revenue = operating revenues less benefits, claims & settlement expenses less dividends to policyholders. RONR = Return on Net Revenue.

Estimated pre-tax operating losses for Corporate of $200-$225 million in 2017 US GAAP total company operating earnings effective tax rate of 21-23% in 2017

45

Financials

Retirement and Income Solutions 2017 outlook

Long-term outlook

RIS-Fee

Net revenue growth CAGR 2-5% 3-7%

Pre-tax return on net revenue 29-33% 28-32%

RIS-Spread

Net revenue growth CAGR 5-10% 5-10%

Pre-tax return on net revenue 55-60% 55-60%

Principal International 2017 outlook

Long-term outlook

Combined net revenue growth CAGR (at PFG share, in reported USD) 11-14% 11-14%

Combined pre-tax return on net revenue (at PFG share, reported USD)

38-42% 40-45%

Principal Global Investors 2017 outlook

Long-term outlook

Operating revenues less pass-through commissions growth CAGR

4-8% 5-8%

Pre-tax return on operating revenues less pass-through commissions

34-37% 33-36%

U.S. Insurance Solutions 2017 outlook

Long-term outlook

Specialty Benefits

Premium & fees growth CAGR 7-9% 7-9%

Pre-tax return on premium & fees 10-13% 10-13%

Loss ratio 62-68% 62-68%

Individual Life

Premium & fees growth CAGR 3-6% 3-6%

Pre-tax return on premium & fees 14-18% 15-20%

Non-GAAP Financial Measure Reconciliations

Pre-tax operating earnings (losses):

Trailing twelve

months, 31-Dec-16

Pre-tax operating earnings, excluding Corporate $1,887.6Pre-tax operating earnings - Corporate (218.9)Pre-tax operating earnings - PFG 1,668.7

Pre-tax net realized capital gains, as adjusted 46.3Pre-tax other adjustments -86.4

Certain adjustments related to equity method investments and noncontrollinginterest (36.9)Income before income taxes $1,591.7

Financials

46