Embed Size (px)

Citation preview

1

2030 Strategic Plan and

2014-2018 Business Plan

Maria das Graças Silva Foster

CEO

2

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future events within the

meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of

the Securities Exchange Act of 1934, as amended, that are not based on historical facts

and are not assurances of future results. Such forward-looking statements merely reflect

the Company’s current views and estimates of future economic circumstances, industry

conditions, company performance and financial results. Such terms as "anticipate",

"believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with

similar or analogous expressions, are used to identify such forward-looking statements.

Readers are cautioned that these statements are only projections and may differ

materially from actual future results or events. Readers are referred to the documents

filed by the Company with the SEC, specifically the Company’s most recent Annual

Report on Form 20-F, which identify important risk factors that could cause actual results

to differ from those contained in the forward-looking statements, including, among other

things, risks relating to general economic and business conditions, including crude oil and

other commodity prices, refining margins and prevailing exchange rates, uncertainties

inherent in making estimates of our oil and gas reserves including recently discovered oil

and gas reserves, international and Brazilian political, economic and social

developments, receipt of governmental approvals and licenses and our ability to obtain

financing.

We undertake no obligation to publicly update or revise any forward-looking

statements, whether as a result of new information or future events or for any

other reason. Figures for 2014 on are estimates or targets.

All forward-looking statements are expressly qualified in their entirety by this

cautionary statement, and you should not place reliance on any forward-looking

statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas resources,

that we are not permitted to present in documents filed with the United States

Securities and Exchange Commission (SEC) under new Subpart 1200 to

Regulation S-K because such terms do not qualify as proved, probable or

possible reserves under Rule 4-10(a) of Regulation S-X.

DISCLAIMER

3

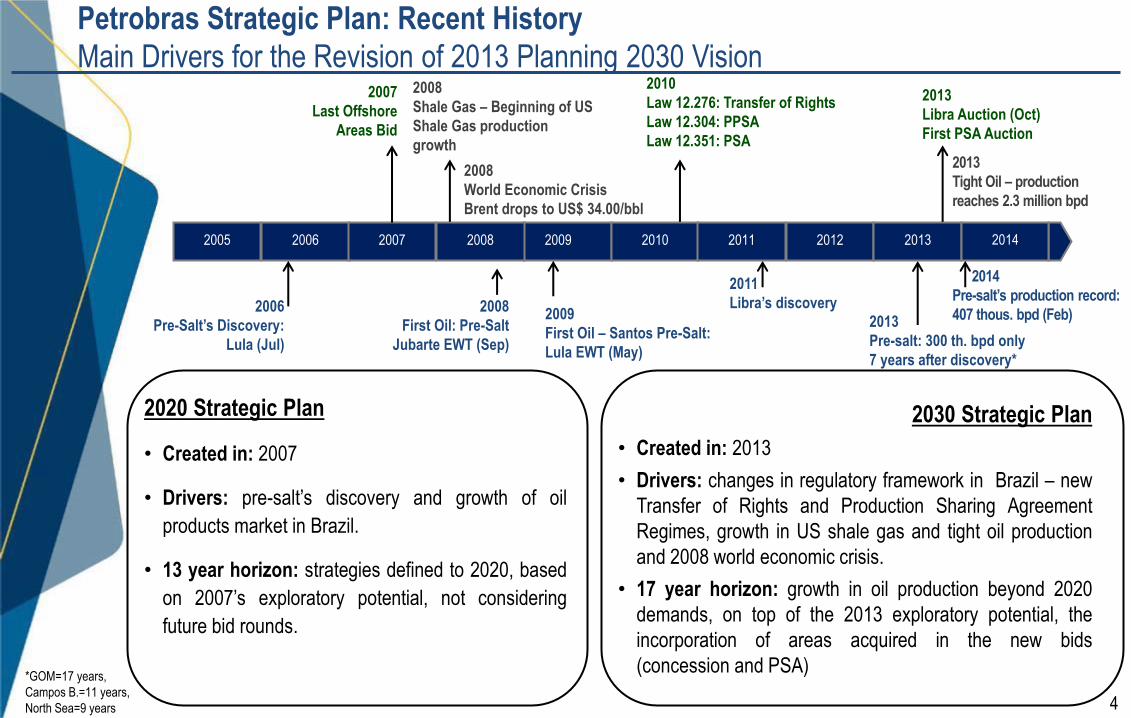

2030 Strategic Plan

4

2030 Strategic Plan

• Created in: 2013

• Drivers: changes in regulatory framework in Brazil – new

Transfer of Rights and Production Sharing Agreement

Regimes, growth in US shale gas and tight oil production

and 2008 world economic crisis.

• 17 year horizon: growth in oil production beyond 2020

demands, on top of the 2013 exploratory potential, the

incorporation of areas acquired in the new bids

(concession and PSA)

Petrobras Strategic Plan: Recent History

Main Drivers for the Revision of 2013 Planning 2030 Vision

2005 2006

2006

Pre-Salt’s Discovery:

Lula (Jul)

2008

First Oil: Pre-Salt

Jubarte EWT (Sep)

2009

First Oil – Santos Pre-Salt:

Lula EWT (May)

2014

Pre-salt’s production record:

407 thous. bpd (Feb)

2011

Libra’s discovery

2013

Pre-salt: 300 th. bpd only

7 years after discovery*

2007 2008 2009 2010 2011 2012 2013 2014

2020 Strategic Plan

• Created in: 2007

• Drivers: pre-salt’s discovery and growth of oil

products market in Brazil.

• 13 year horizon: strategies defined to 2020, based

on 2007’s exploratory potential, not considering

future bid rounds.

2013

Libra Auction (Oct)

First PSA Auction

2007

Last Offshore

Areas Bid

2010

Law 12.276: Transfer of Rights

Law 12.304: PPSA

Law 12.351: PSA

*GOM=17 years,

Campos B.=11 years,

North Sea=9 years

2008

Shale Gas – Beginning of US

Shale Gas production

growth

2008

World Economic Crisis

Brent drops to US$ 34.00/bbl

2013

Tight Oil – production

reaches 2.3 million bpd

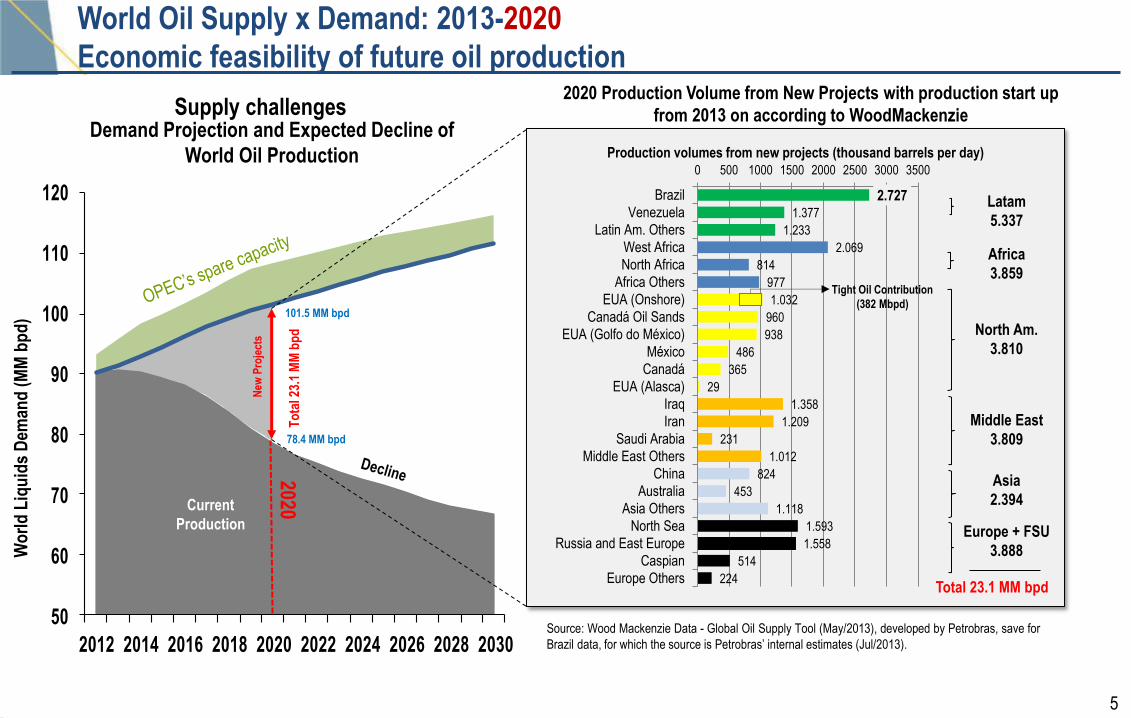

5

50

60

70

80

90

100

110

120

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Demand Projection and Expected Decline of

World Oil Production

Supply challenges

New

Pro

ject

s

Current

Production

2020

To

tal 2

3.1

MM

bp

d

101.5 MM bpd

78.4 MM bpd

Wo

rld

Liq

uid

s D

eman

d (

MM

bp

d)

World Oil Supply x Demand: 2013-2020

Economic feasibility of future oil production

224

514

1.558

1.593

1.118

453

824

1.012

231

1.209

1.358

29

365

486

938

960

1.032

977

814

2.069

1.233

1.377

2.727

0 500 1000 1500 2000 2500 3000 3500

Europe Others

Caspian

Russia and East Europe

North Sea

Asia Others

Australia

China

Middle East Others

Saudi Arabia

Iran

Iraq

EUA (Alasca)

Canadá

México

EUA (Golfo do México)

Canadá Oil Sands

EUA (Onshore)

Africa Others

North Africa

West Africa

Latin Am. Others

Venezuela

Brazil

Production volumes from new projects (thousand barrels per day)

Latam

5.337

Africa

3.859

North Am.

3.810

Middle East

3.809

Asia

2.394

Europe + FSU

3.888

Total 23.1 MM bpd

Source: Wood Mackenzie Data - Global Oil Supply Tool (May/2013), developed by Petrobras, save for

Brazil data, for which the source is Petrobras’ internal estimates (Jul/2013).

Tight Oil Contribution

(382 Mbpd)

2020 Production Volume from New Projects with production start up

from 2013 on according to WoodMackenzie

6

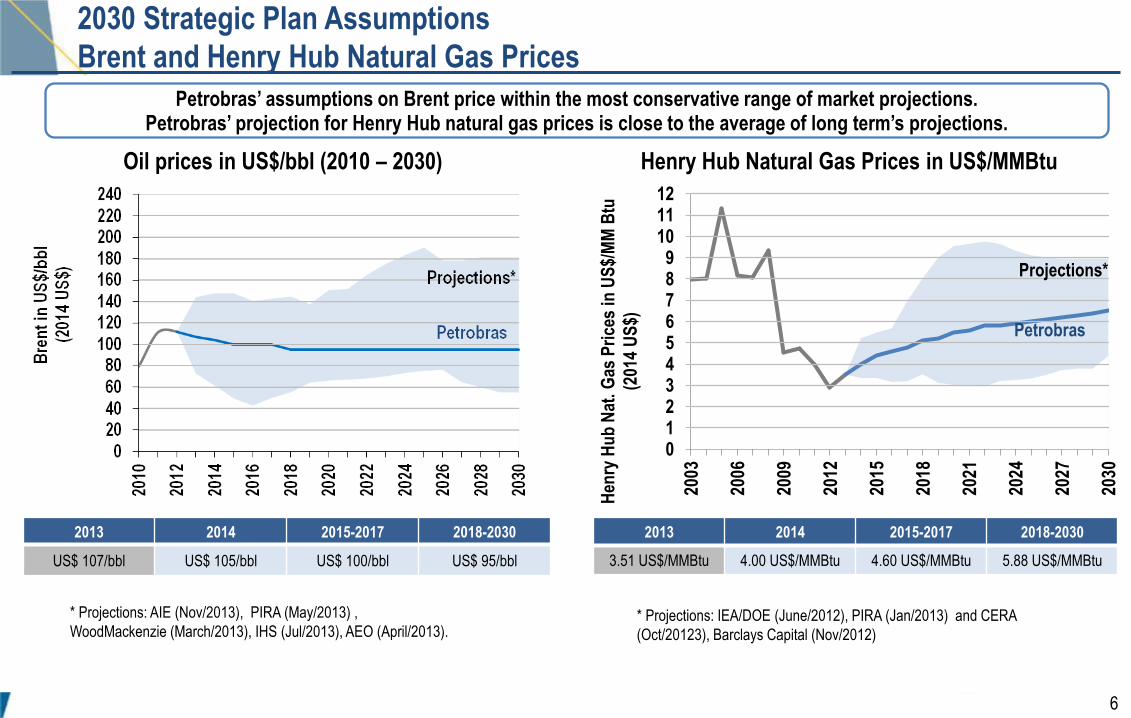

2030 Strategic Plan Assumptions

Brent and Henry Hub Natural Gas Prices

Petrobras’ assumptions on Brent price within the most conservative range of market projections. Petrobras’ projection for Henry Hub natural gas prices is close to the average of long term’s projections.

2013 2014 2015-2017 2018-2030

US$ 107/bbl US$ 105/bbl US$ 100/bbl US$ 95/bbl

Oil prices in US$/bbl (2010 – 2030)

* Projections: AIE (Nov/2013), PIRA (May/2013) ,

WoodMackenzie (March/2013), IHS (Jul/2013), AEO (April/2013).

0123456789

101112

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

Hen

ry H

ub

Nat

. G

as P

rice

s in

US

$/M

M B

tu

(201

4 U

S$)

* Projections: IEA/DOE (June/2012), PIRA (Jan/2013) and CERA

(Oct/20123), Barclays Capital (Nov/2012)

Henry Hub Natural Gas Prices in US$/MMBtu

Petrobras

2013 2014 2015-2017 2018-2030

3.51 US$/MMBtu 4.00 US$/MMBtu 4.60 US$/MMBtu 5.88 US$/MMBtu

Projections*

7

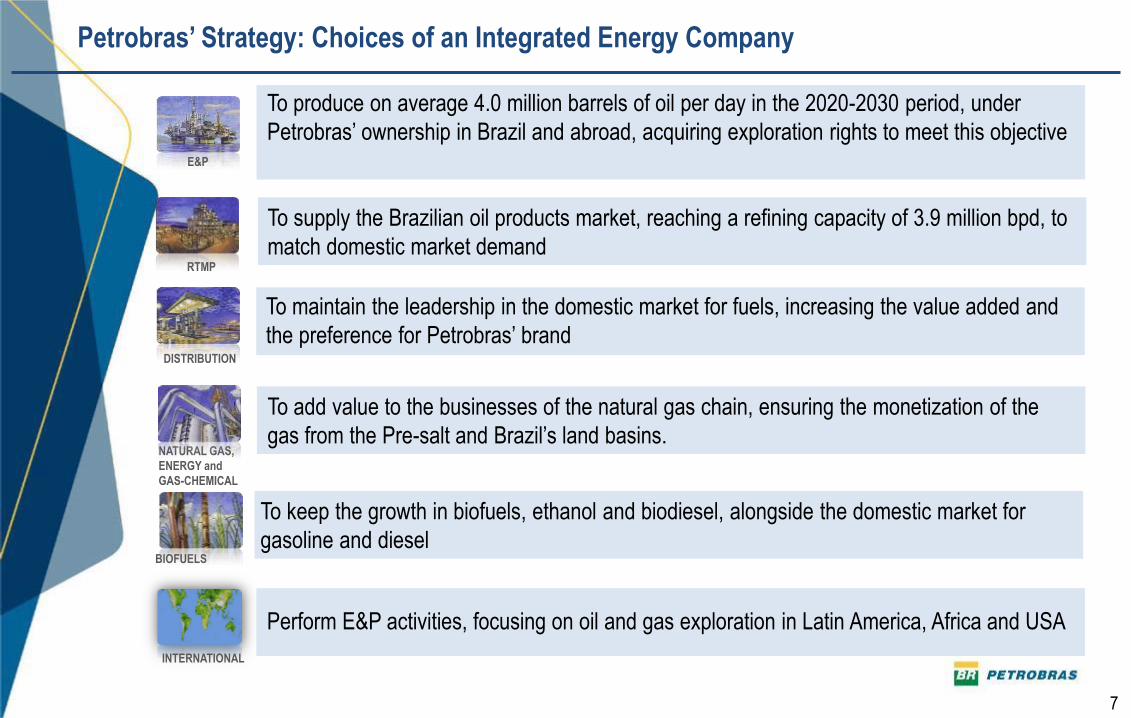

INTERNATIONAL

DISTRIBUTION

NATURAL GAS,

ENERGY and

GAS-CHEMICAL

BIOFUELS

To produce on average 4.0 million barrels of oil per day in the 2020-2030 period, under

Petrobras’ ownership in Brazil and abroad, acquiring exploration rights to meet this objective

To maintain the leadership in the domestic market for fuels, increasing the value added and

the preference for Petrobras’ brand

To add value to the businesses of the natural gas chain, ensuring the monetization of the

gas from the Pre-salt and Brazil’s land basins.

To keep the growth in biofuels, ethanol and biodiesel, alongside the domestic market for

gasoline and diesel

RTMP

To supply the Brazilian oil products market, reaching a refining capacity of 3.9 million bpd, to

match domestic market demand

Perform E&P activities, focusing on oil and gas exploration in Latin America, Africa and USA

E&P

E&P

Petrobras’ Strategy: Choices of an Integrated Energy Company

8

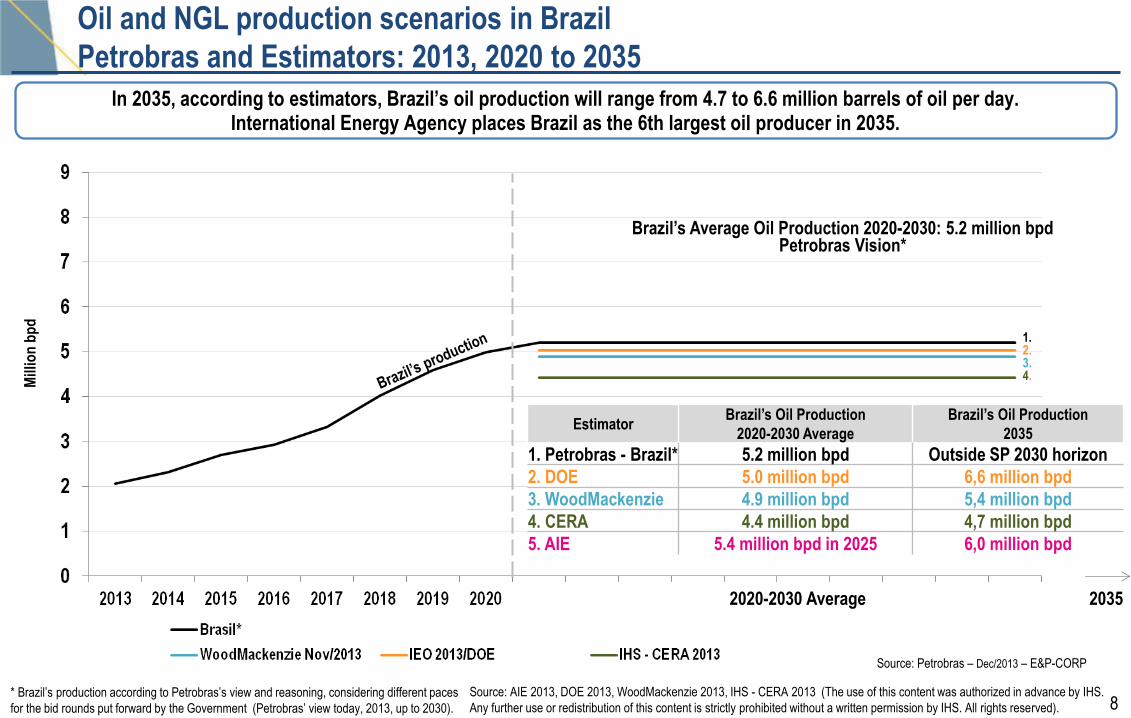

Source: Petrobras – Dec/2013 – E&P-CORP

Oil and NGL production scenarios in Brazil

Petrobras and Estimators: 2013, 2020 to 2035

2020-2030 Average

Mill

ion

bp

d

Brazil’s Average Oil Production 2020-2030: 5.2 million bpd Petrobras Vision*

In 2035, according to estimators, Brazil’s oil production will range from 4.7 to 6.6 million barrels of oil per day. International Energy Agency places Brazil as the 6th largest oil producer in 2035.

Source: AIE 2013, DOE 2013, WoodMackenzie 2013, IHS - CERA 2013 (The use of this content was authorized in advance by IHS.

Any further use or redistribution of this content is strictly prohibited without a written permission by IHS. All rights reserved).

Estimator Brazil’s Oil Production

2020-2030 Average

Brazil’s Oil Production

2035

1. Petrobras - Brazil* 5.2 million bpd Outside SP 2030 horizon

2. DOE 5.0 million bpd 6,6 million bpd

3. WoodMackenzie 4.9 million bpd 5,4 million bpd

4. CERA 4.4 million bpd 4,7 million bpd

5. AIE 5.4 million bpd in 2025 6,0 million bpd

2035

1. 2. 3. 4.

* Brazil’s production according to Petrobras’s view and reasoning, considering different paces

for the bid rounds put forward by the Government (Petrobras’ view today, 2013, up to 2030).

9

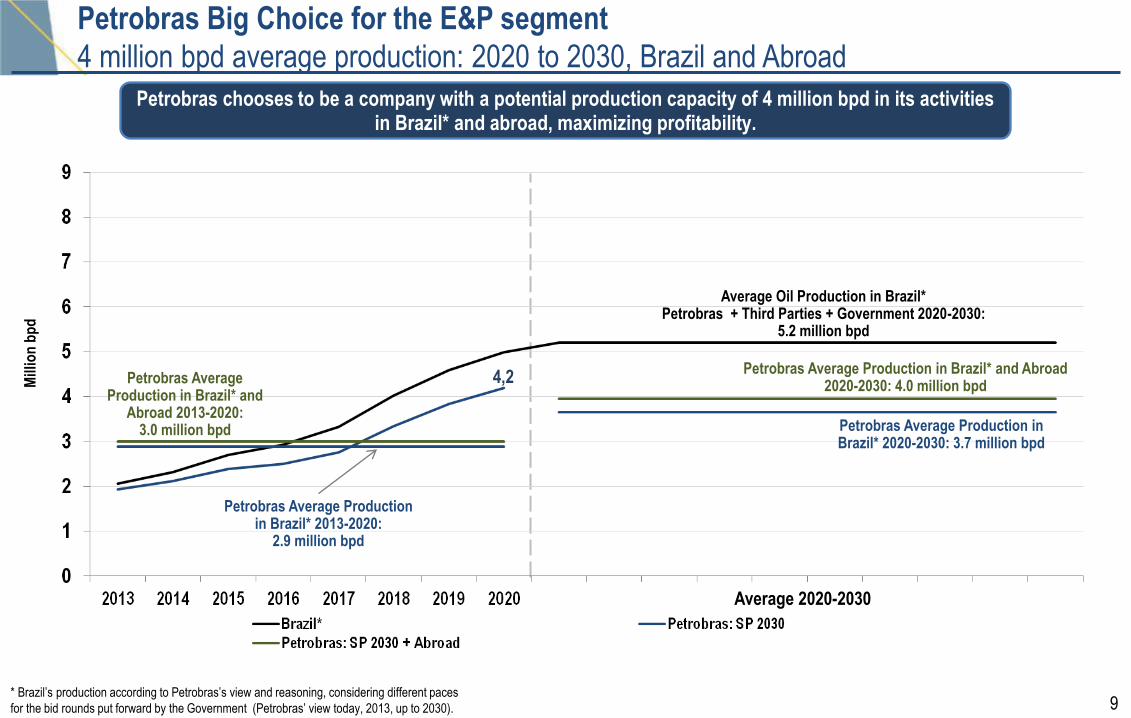

4,2

Petrobras Big Choice for the E&P segment

4 million bpd average production: 2020 to 2030, Brazil and Abroad

Petrobras chooses to be a company with a potential production capacity of 4 million bpd in its activities in Brazil* and abroad, maximizing profitability.

Petrobras Average Production in Brazil* and Abroad 2020-2030: 4.0 million bpd

Average 2020-2030

Mill

ion

bp

d

Petrobras Average Production in Brazil* 2020-2030: 3.7 million bpd

Average Oil Production in Brazil* Petrobras + Third Parties + Government 2020-2030:

5.2 million bpd

Petrobras Average Production in Brazil* and

Abroad 2013-2020: 3.0 million bpd

Petrobras Average Production in Brazil* 2013-2020:

2.9 million bpd

* Brazil’s production according to Petrobras’s view and reasoning, considering different paces

for the bid rounds put forward by the Government (Petrobras’ view today, 2013, up to 2030).

10

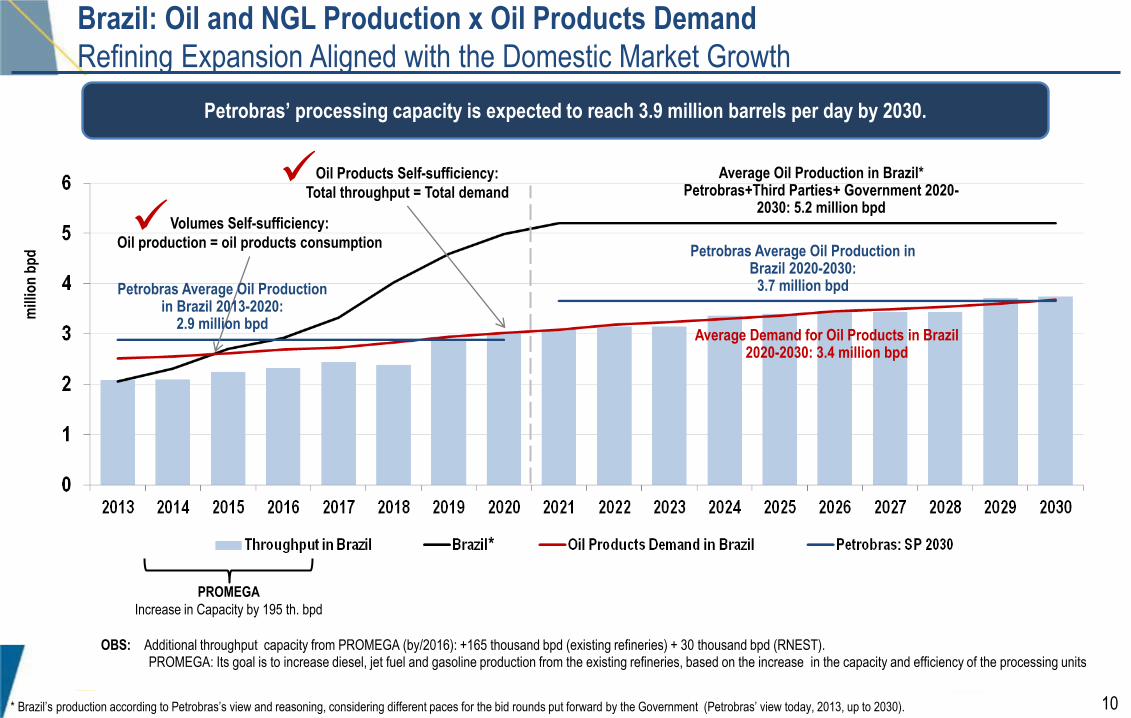

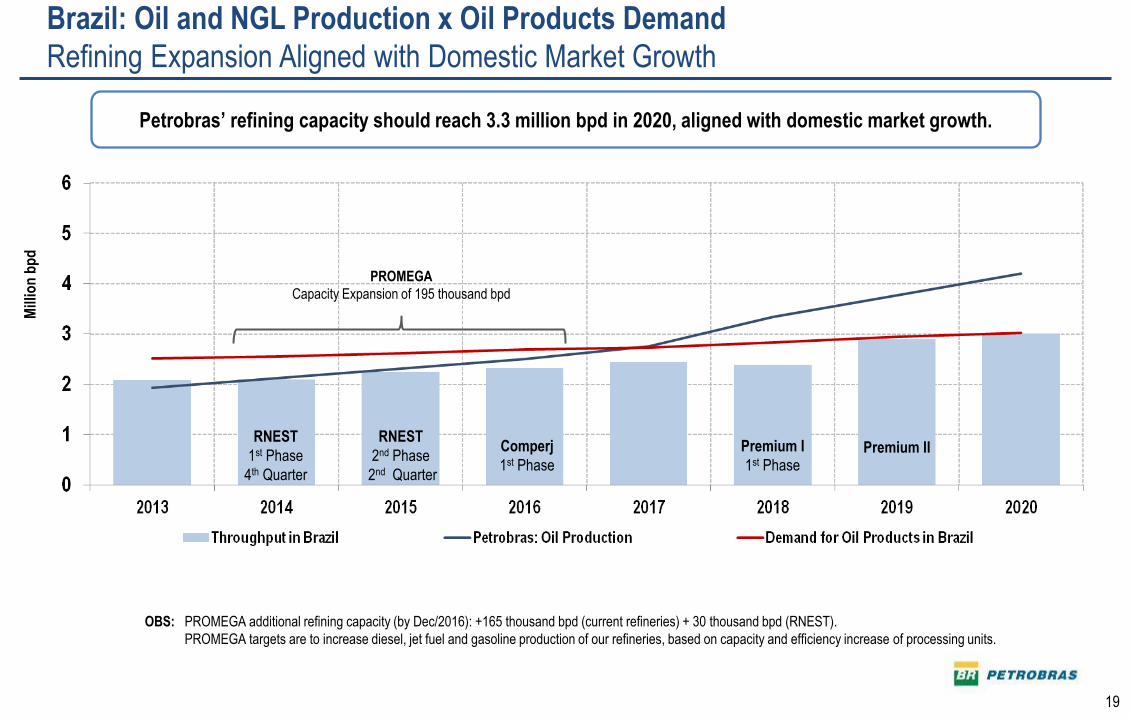

Brazil: Oil and NGL Production x Oil Products Demand

Refining Expansion Aligned with the Domestic Market Growth

OBS: Additional throughput capacity from PROMEGA (by/2016): +165 thousand bpd (existing refineries) + 30 thousand bpd (RNEST). PROMEGA: Its goal is to increase diesel, jet fuel and gasoline production from the existing refineries, based on the increase in the capacity and efficiency of the processing units

mill

ion

bp

d

PROMEGA

Increase in Capacity by 195 th. bpd

Average Oil Production in Brazil* Petrobras+Third Parties+ Government 2020-

2030: 5.2 million bpd

Average Demand for Oil Products in Brazil 2020-2030: 3.4 million bpd

Oil Products Self-sufficiency:

Total throughput = Total demand

Petrobras Average Oil Production in Brazil 2020-2030:

3.7 million bpd

Volumes Self-sufficiency:

Oil production = oil products consumption

Petrobras Average Oil Production in Brazil 2013-2020:

2.9 million bpd

Petrobras’ processing capacity is expected to reach 3.9 million barrels per day by 2030.

*

* Brazil’s production according to Petrobras’s view and reasoning, considering different paces for the bid rounds put forward by the Government (Petrobras’ view today, 2013, up to 2030).

11

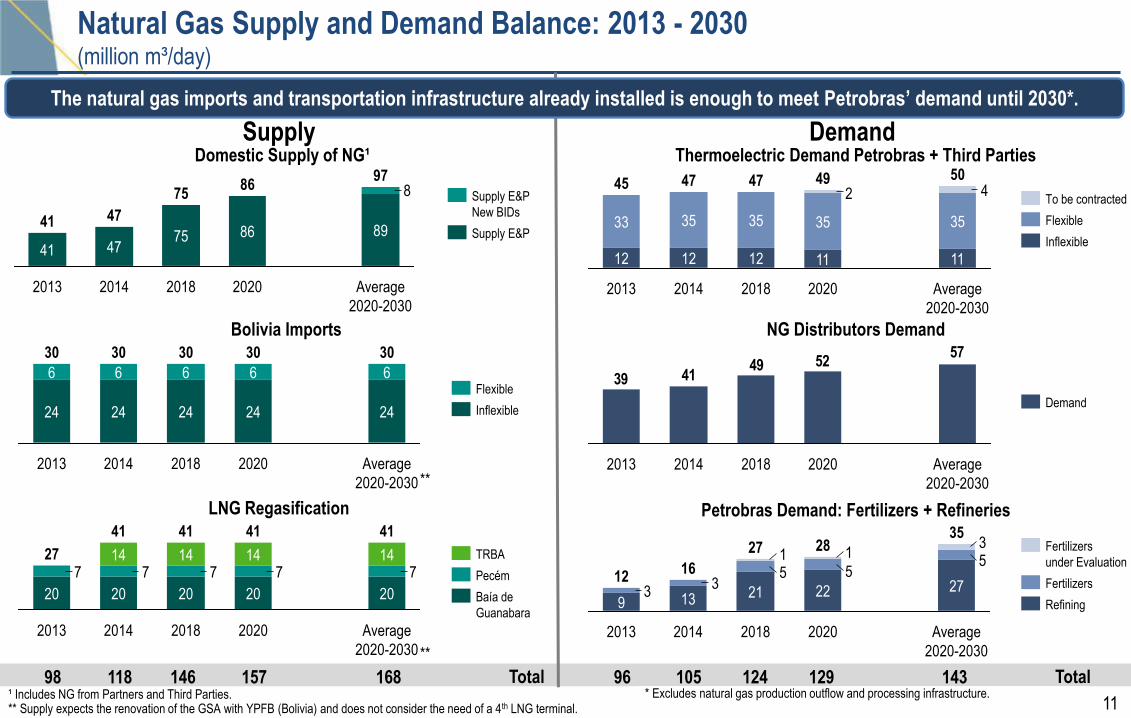

Natural Gas Supply and Demand Balance: 2013 - 2030 (million m³/day)

Supply Demand

LNG Regasification

Thermoelectric Demand Petrobras + Third Parties

42

12

35

2014

47

12

35

2013

45

12

33

Average

2020-2030

50

11

35

2020

49

11

35

2018

47

Inflexible

Flexible

To be contracted

NG Distributors Demand 57

52494139

2014 2013 Average

2020-2030

2020 2018

Demand

Petrobras Demand: Fertilizers + Refineries

555

33

31127

21

2014

16

13

2013

12

9

Average

2020-2030

35

27

2020

28

22

2018

Refining

Fertilizers

Fertilizers

under Evaluation

96 124 129 143 98 146 157 168 118 105 Total

77777

Average

2020-2030

41

20

14

2020

41

20

14

2018

41

20

14

2014

41

20

14

2013

27

20 Baía de

Guanabara

Pecém

TRBA

Bolivia Imports

2020

24

6

2013

30

24

6

Average

2020-2030

30

24

6

30

24

6

2018

30

24

6

2014

30

Inflexible

Flexible

Domestic Supply of NG¹

8

47

2013

41

41

Average

2020-2030

97

89

2020

86

86

2018

75

75

2014

47 Supply E&P

Supply E&P

New BIDs

Total ¹ Includes NG from Partners and Third Parties. ** Supply expects the renovation of the GSA with YPFB (Bolivia) and does not consider the need of a 4th LNG terminal.

**

**

The natural gas imports and transportation infrastructure already installed is enough to meet Petrobras’ demand until 2030*.

* Excludes natural gas production outflow and processing infrastructure.

12

Mission, Vision 2030 and Corporate Drivers

To be one of the five largest integrated energy

companies in the world¹ and the preferred one

by its stakeholders.

¹ Metric: one of the five largest oil producers among all companies, with or without shares in stock

exchanges. (Source for calculation: Petroleum Intelligence Weekly – PIW - Annual Report )

Integrated Growth

Corporate Drivers

Profitability Social and Environmental

Responsibility

Mission

To perform in the oil and gas industry in an

ethic, safe and profitable way, with social and

environmental responsibility, providing products

suited to the needs of its clients and contributing

to the development of Brazil and the countries

where it operates.

Vision 2030

13

2014-2018 Business

and Management Plan

14

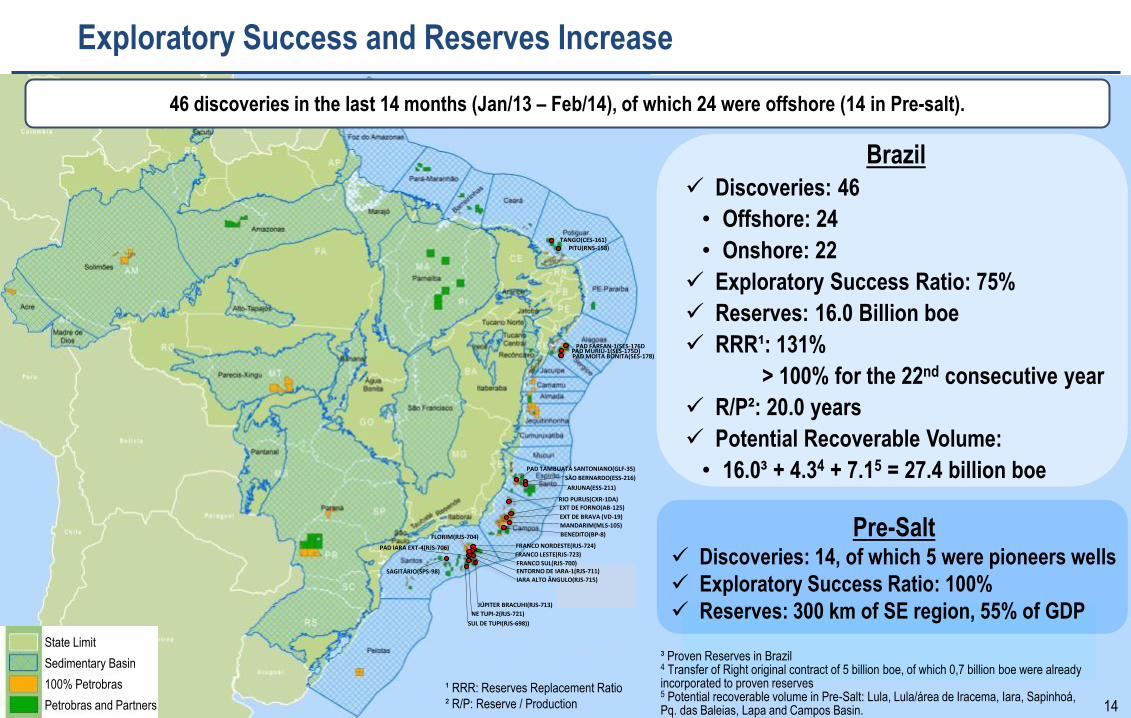

Exploratory Success and Reserves Increase

14

TANGO(CES-161) PITU(RNS-158)

PAD FARFAN-1(SES-176D PAD MURIÚ-1(SES-175D) PAD MOITA BONITA(SES-178)

SÃO BERNARDO(ESS-216)

ARJUNA(ESS-211)

RIO PURUS(CXR-1DA)

PAD TAMBUATÁ SANTONIANO(GLF-35)

EXT DE FORNO(AB-125)

EXT DE BRAVA (VD-19)

MANDARIM(MLS-105)

BENEDITO(BP-8)

FRANCO NORDESTE(RJS-724)

FRANCO LESTE(RJS-723)

FRANCO SUL(RJS-700)

FLORIM(RJS-704)

IARA ALTO ÂNGULO(RJS-715)

ENTORNO DE IARA-1(RJS-711)

PAD IARA EXT-4(RJS-706)

NE TUPI-2(RJS-721)

JÚPITER BRACUHI(RJS-713)

SUL DE TUPI(RJS-698))

SAGITÁRIO(SPS-98)

46 discoveries in the last 14 months (Jan/13 – Feb/14), of which 24 were offshore (14 in Pre-salt).

State Limit

Sedimentary Basin

100% Petrobras

Petrobras and Partners

¹ RRR: Reserves Replacement Ratio

² R/P: Reserve / Production

³ Proven Reserves in Brazil 4 Transfer of Right original contract of 5 billion boe, of which 0,7 billion boe were already incorporated to proven reserves 5 Potential recoverable volume in Pre-Salt: Lula, Lula/área de Iracema, Iara, Sapinhoá, Pq. das Baleias, Lapa and Campos Basin.

Brazil

Discoveries: 46

• Offshore: 24

• Onshore: 22

Exploratory Success Ratio: 75%

Reserves: 16.0 Billion boe

RRR¹: 131%

> 100% for the 22nd consecutive year

R/P²: 20.0 years

Potential Recoverable Volume:

• 16.0³ + 4.34 + 7.15 = 27.4 billion boe

Pre-Salt Discoveries: 14, of which 5 were pioneers wells

Exploratory Success Ratio: 100%

Reserves: 300 km of SE region, 55% of GDP

15

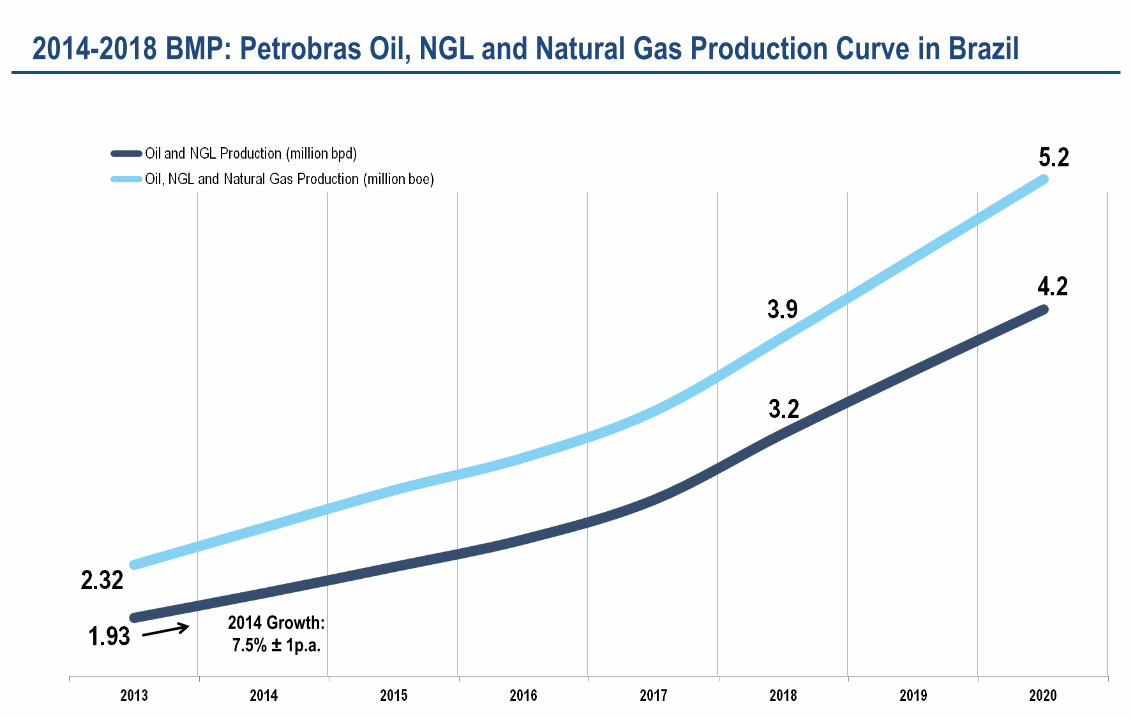

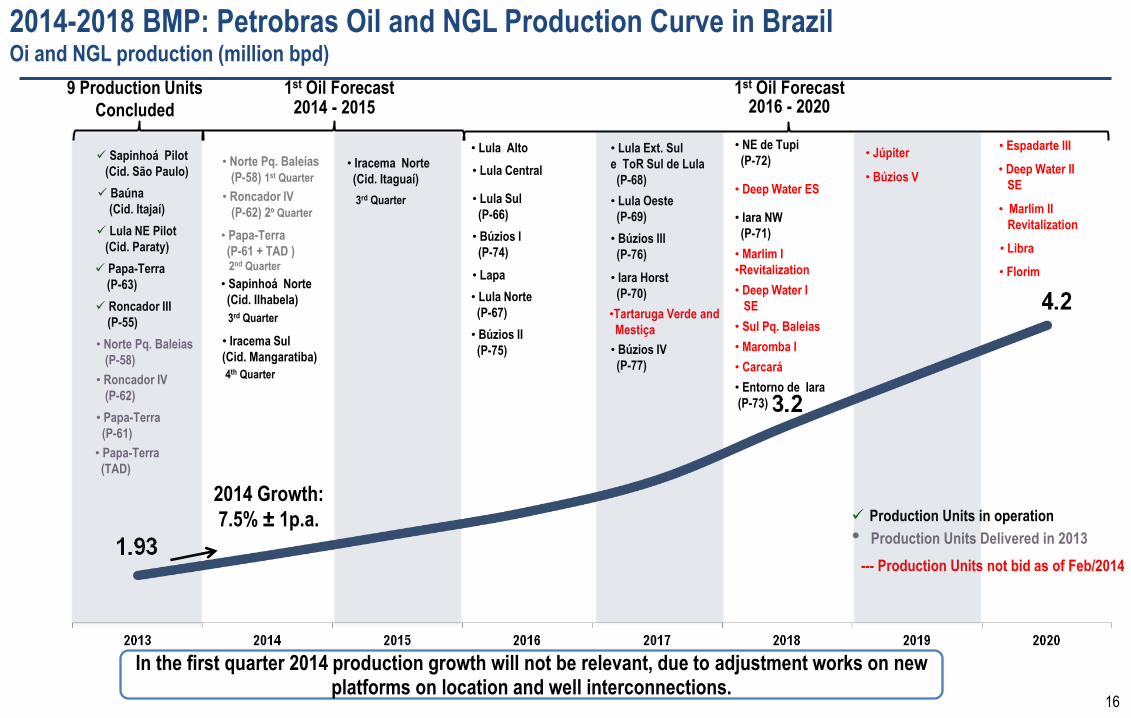

2014 Growth:

7.5% ± 1p.a.

2014-2018 BMP: Petrobras Oil, NGL and Natural Gas Production Curve in Brazil

16 16

• Norte Pq. Baleias

(P-58) 1st Quarter

Sapinhoá Pilot

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

• Iracema Sul

(Cid. Mangaratiba)

• Roncador IV

(P-62) 2º Quarter

• Sapinhoá Norte

(Cid. Ilhabela)

• Papa-Terra

(P-61 + TAD ) 2nd Quarter

• Florim

• Júpiter • Lula Alto

• Lula Central

• Lula Sul

(P-66)

• Búzios I

(P-74)

• Lapa

• Lula Norte

(P-67)

• Búzios II

(P-75)

• Lula Ext. Sul

e ToR Sul de Lula

(P-68)

• Lula Oeste

(P-69)

• Búzios III

(P-76)

•Tartaruga Verde and

Mestiça

• Maromba I

• Iara Horst

(P-70)

• Búzios IV

(P-77)

• Entorno de Iara

(P-73)

• NE de Tupi

(P-72)

• Iara NW

(P-71)

• Sul Pq. Baleias

• Deep Water ES

• Carcará

• Búzios V

• Espadarte III

Production Units in operation

• Deep Water I

SE

• Marlim I

•Revitalization

• Deep Water II

SE

• Libra

• Marlim II

Revitalization Lula NE Pilot

(Cid. Paraty)

Papa-Terra

(P-63)

Roncador III

(P-55)

--- Production Units not bid as of Feb/2014

1st Oil Forecast

3rd Quarter

4th Quarter

• Iracema Norte

(Cid. Itaguaí)

3rd Quarter

1st Oil Forecast 9 Production Units

Concluded

• Norte Pq. Baleias

(P-58)

• Roncador IV

(P-62)

• Papa-Terra

(P-61)

• Papa-Terra

(TAD)

• Production Units Delivered in 2013

2014 Growth:

7.5% ± 1p.a.

2014-2018 BMP: Petrobras Oil and NGL Production Curve in Brazil Oi and NGL production (million bpd)

2014 - 2015 2016 - 2020

In the first quarter 2014 production growth will not be relevant, due to adjustment works on new platforms on location and well interconnections.

17 17 Pro

du

ctio

n U

nit

s D

eliv

ered

, un

der

Co

nst

ruct

ion

an

d u

nd

er B

idd

ing

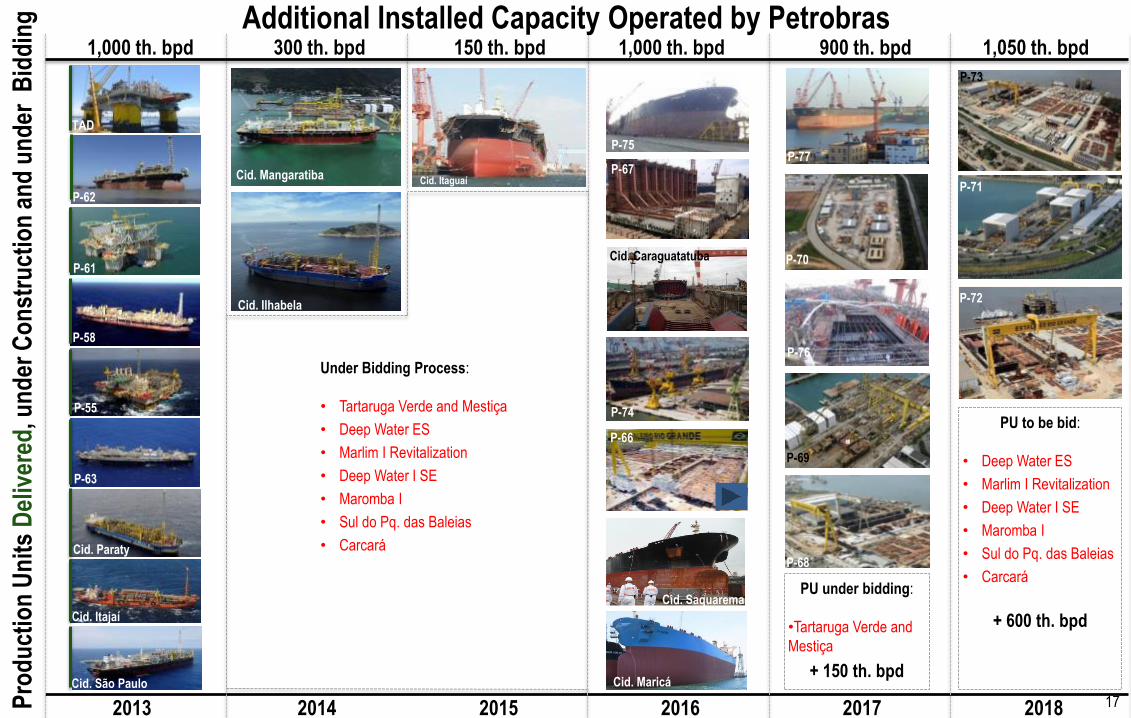

2014 2015 2016 2017 2018 2013

1,000 th. bpd 300 th. bpd

Additional Installed Capacity Operated by Petrobras 150 th. bpd 1,000 th. bpd 900 th. bpd 1,050 th. bpd

Cid. Ilhabela

Cid. Mangaratiba

P-75

P-67

P-74

P-66

P-68

P-69

P-76

P-77

P-72

P-71

P-73

P-67 Cid. Itaguaí

Cid. Maricá

Cid. Saquarema

Cid. Caraguatatuba

Cid. São Paulo

Cid. Itajaí

Cid. Paraty

P-63

P-55

P-61

P-58

P-62

TAD

PU to be bid:

• Deep Water ES

• Marlim I Revitalization

• Deep Water I SE

• Maromba I

• Sul do Pq. das Baleias

• Carcará

+ 600 th. bpd

PU under bidding:

•Tartaruga Verde and

Mestiça

+ 150 th. bpd

P-70

Under Bidding Process:

• Tartaruga Verde and Mestiça

• Deep Water ES

• Marlim I Revitalization

• Deep Water I SE

• Maromba I

• Sul do Pq. das Baleias

• Carcará

18 18

PL

SV

s u

nd

er O

per

atio

n a

nd

Co

nst

ruct

ion

2014 2016 2014

Current Fleet = 11 PLSVs + 2

19 New PLSVs to support the Oil Curve + 8 throughout 2014 + 9

P-58

2017

Sunrise 270t

Deep Constructor 125t

Skandi Vitória 300t

Skandi Niterói 270t

Kommandor 3000 135t

Normand7 340t

Seven Mar 340t

Seven Seas 430t

Seven Condor 230t

Seven Phoenix 340t

McDermott

Agile 200t

North Ocean 102 210t

Polar Onyx 275t

Coral do Atlântico 550t Estrela do Mar 550t

Lay Vessel 105 300t

Seven Waves 550t

1 PLSVs of 300t

(The Netherlands)

Sapura Diamante 550t

Sapura Topázio 550t

3 PLSVs of 550t

(The Netherlands)

2 PLSVs of 650t

(Norway)

1 PLSVs of 300t

(Suape)

1 PLSVs of 550t

(The Netherlands)

1 PLSVs of 300t

(Suape)

2 PLSVs of 550t

(The Netherlands)

PLSV: Pipe Laying Support Vessel

19 19

Brazil: Oil and NGL Production x Oil Products Demand

Refining Expansion Aligned with Domestic Market Growth

RNEST

1st Phase

4th Quarter

RNEST

2nd Phase

2nd Quarter

Comperj

1st Phase

Premium I

1st Phase Premium II

OBS: PROMEGA additional refining capacity (by Dec/2016): +165 thousand bpd (current refineries) + 30 thousand bpd (RNEST).

PROMEGA targets are to increase diesel, jet fuel and gasoline production of our refineries, based on capacity and efficiency increase of processing units.

Mill

ion

bp

d

PROMEGA

Capacity Expansion of 195 thousand bpd

Petrobras’ refining capacity should reach 3.3 million bpd in 2020, aligned with domestic market growth.

20

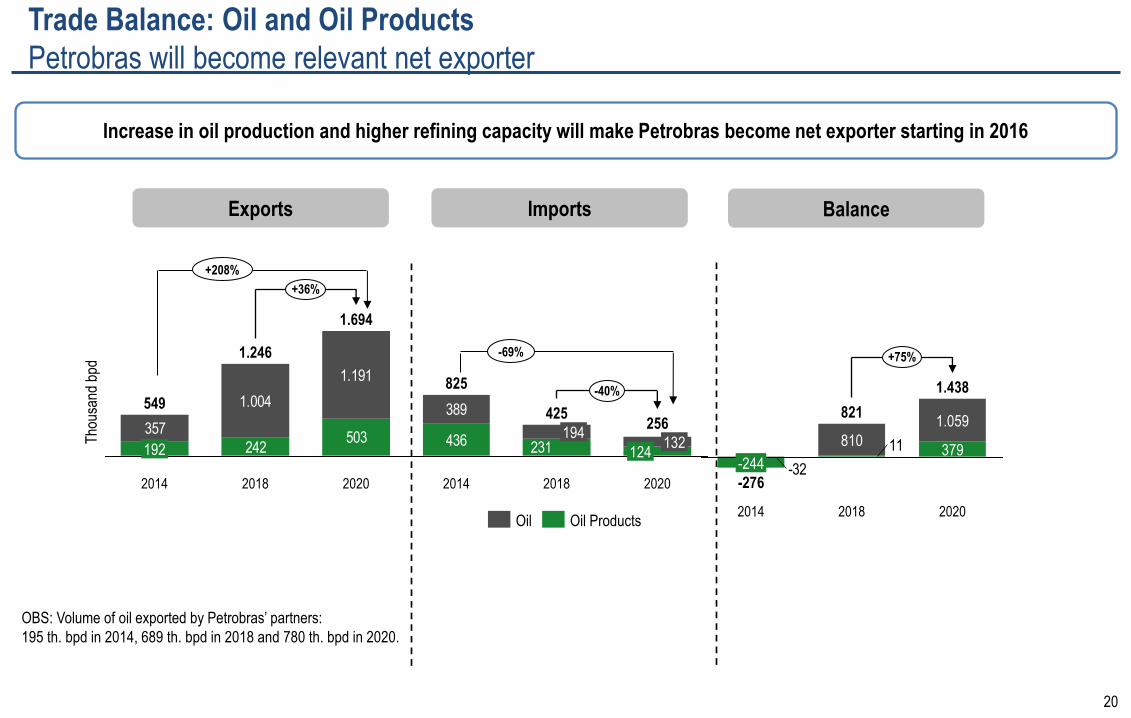

Trade Balance: Oil and Oil Products

Petrobras will become relevant net exporter

Exports Imports Balance

Tho

usan

d bp

d

242503 436

357

1.004

1.191

389

231

-40%

+36%

2020

256

124 132

2018

425

194

2014

825

2020

1.694

2018

1.246

2014

549

192

Oil Products Oil

+208%

11

-32

+75%

2020

1.438

379

1.059

2018

821

810

2014

-276

-244

-69%

Increase in oil production and higher refining capacity will make Petrobras become net exporter starting in 2016

OBS: Volume of oil exported by Petrobras’ partners:

195 th. bpd in 2014, 689 th. bpd in 2018 and 780 th. bpd in 2020.

21 21

RNEST and COMPERJ Refineries

Physical and Financial Monitoring

PNG 13-17 2016

Projetado 2016

0

10

20

30

40

50

60

70

80

90

100

110

mai

-04

nov-

04m

ai-0

5no

v-05

mai

-06

nov-

06m

ai-0

7no

v-07

mai

-08

nov-

08m

ai-0

9no

v-09

mai

-10

nov-

10m

ai-1

1no

v-11

mai

-12

nov-

12m

ai-1

3no

v-13

mai

-14

nov-

14m

ai-1

5no

v-15

mai

-16

nov-

16m

ai-1

7no

v-17

mai

-18

nov-

18m

ai-1

9no

v-19

mai

-20

nov-

20m

ai-2

1no

v-21

PNG 12-16 PNG 13-17 Realizado Projetado

Physical Monitoring – S-Curve

(%)

PNG 13-17 2014

Projetado 2014

0

10

20

30

40

50

60

70

80

90

100

110

abr-

05ou

t-05

abr-

06ou

t-06

abr-

07ou

t-07

abr-

08ou

t-08

abr-

09ou

t-09

abr-

10ou

t-10

abr-

11ou

t-11

abr-

12ou

t-12

abr-

13ou

t-13

abr-

14ou

t-14

abr-

15ou

t-15

abr-

16ou

t-16

abr-

17ou

t-17

abr-

18ou

t-18

abr-

19ou

t-19

abr-

20ou

t-20

PNG 12-16 PNG 13-17 Realizado Projetado

Physical Monitoring – S-Curve

BMP 13-17: 87%

Accomplished: 84%

PNG 13-17: US$ 13.457 MM

Projetado: US$ 13.596 MM

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

jan-

10

jul-1

0

jan-

11

jul-1

1

jan-

12

jul-1

2

jan-

13

jul-1

3

jan-

14

jul-1

4

jan-

15

jul-1

5

jan-

16

jul-1

6

jan-

17

jul-1

7

jan-

18

jul-1

8

jan-

19

jul-1

9

jan-

20

jul-2

0

jan-

21

jul-2

1

US

$ M

M

PNG 13-17 Realizado Projetado

(%)

Financial Monitoring – S-Curve

Financial Monitoring – S-Curve

BMP 13-17: 7,882 Million

Accomplished: 7,573 Million

PNG 13-17: US$ 18.515 MM

Projetado: US$ 18.579 MM

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

abr-

05ou

t-05

abr-

06ou

t-06

abr-

07ou

t-07

abr-

08ou

t-08

abr-

09ou

t-09

abr-

10ou

t-10

abr-

11ou

t-11

abr-

12ou

t-12

abr-

13ou

t-13

abr-

14ou

t-14

abr-

15ou

t-15

abr-

16ou

t-16

abr-

17ou

t-17

abr-

18ou

t-18

abr-

19ou

t-19

abr-

20ou

t-20

US

$ M

M

PNG 13-17 Realizado Projetado

IMPLEMENTION MILESTONES

1 - Start-up - ETA (Mar/2014)

2 - Start-up - ETDI (Sep/2014)

3 - Start-up UDA 11 (Oct/2014)

4 - Start-up UCR 21 (Nov/2014)

5 - Start-up HDT Diesel 31 (Nov/2014)

IMPLEMENTATION MILESTONES

1 - Start-up – ETA (Jun/2015)

2 - Start-up - ETDI (Jun/2015)

3 - Start-up - UDAV (Ago/2016)

4 - Start-up - UCR (Ago/2016)

5 - Start-up - HCC (Ago/2016)

BMP 13-17: 15,246 Million

Accomplished: 14,841 Million

BMP 13-17: 67%

Accomplished: 66%

COMPERJ Start-up: 2016

Feb/14

BMP 13-17 Accomplished Planned BMP 13-17 Accomplished Planned

BMP 12-16 BMP 13-17 Accomplished Planned BMP 13-17 Accomplished Planned

BMP 13-17

2016

Planned

2016

Planned

2014

BMP 13-17

2014 BMP 13-17

US$ 18.515 MM

Planned

US$ 13.596 MM

BMP 13-17

US$ 13.457 MM

Planned

US$ 18.579 MM

RNEST

Start-up: 4th Quarter BMP 12-16 Mar/14

22

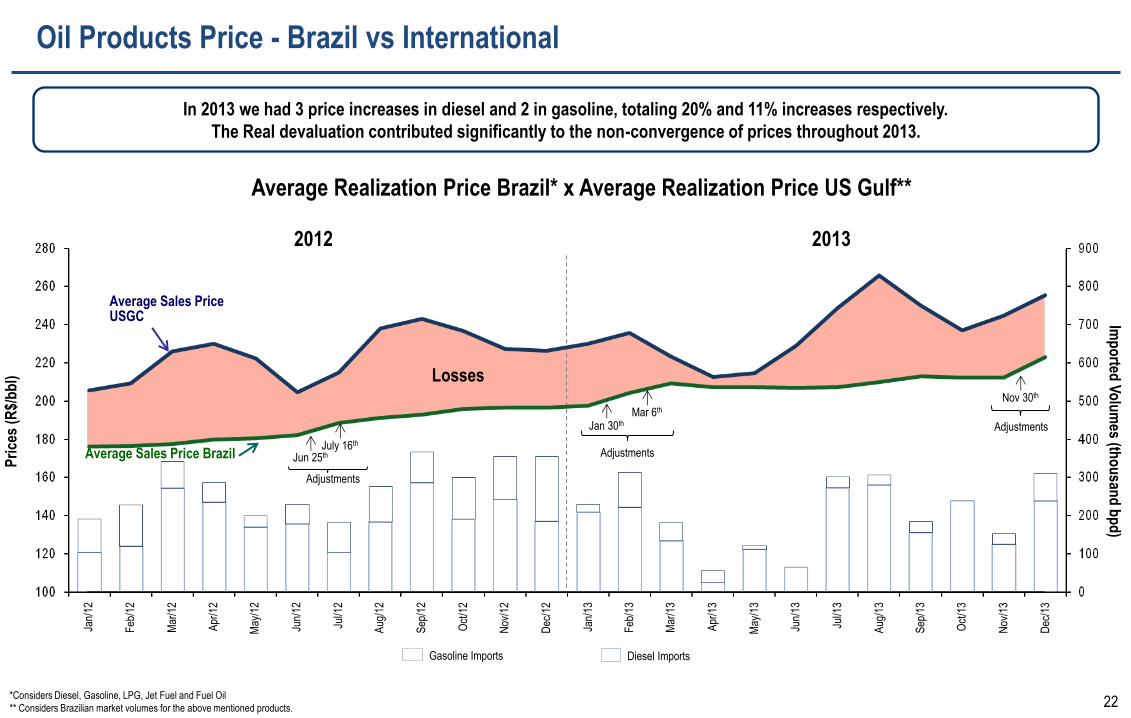

Average Realization Price Brazil* x Average Realization Price US Gulf**

*Considers Diesel, Gasoline, LPG, Jet Fuel and Fuel Oil

** Considers Brazilian market volumes for the above mentioned products.

In 2013 we had 3 price increases in diesel and 2 in gasoline, totaling 20% and 11% increases respectively.

The Real devaluation contributed significantly to the non-convergence of prices throughout 2013.

Oil Products Price - Brazil vs International

Dec

/13

Nov

/13

Oct

/13

Sep

/13

Aug

/13

Jul/1

3

Jun/

13

May

/13

Apr

/13

Mar

/13

Feb

/13

Jan/

13

Dec

/12

Nov

/12

Oct

/12

Sep

/12

Aug

/12

Jul/1

2

Jun/

12

May

/12

Apr

/12

Mar

/12

Feb

/12

Jan/

12

Pri

ces

(R$/

bb

l)

2012 2013

Average Sales Price USGC

Jun 25th

Adjustments

July 16th Average Sales Price Brazil Adjustments

Jan 30th Mar 6th

Nov 30th

Adjustments

Losses

Gasoline Imports Diesel Imports

Imp

orted

Vo

lum

es (tho

usan

d b

pd

)

23 23

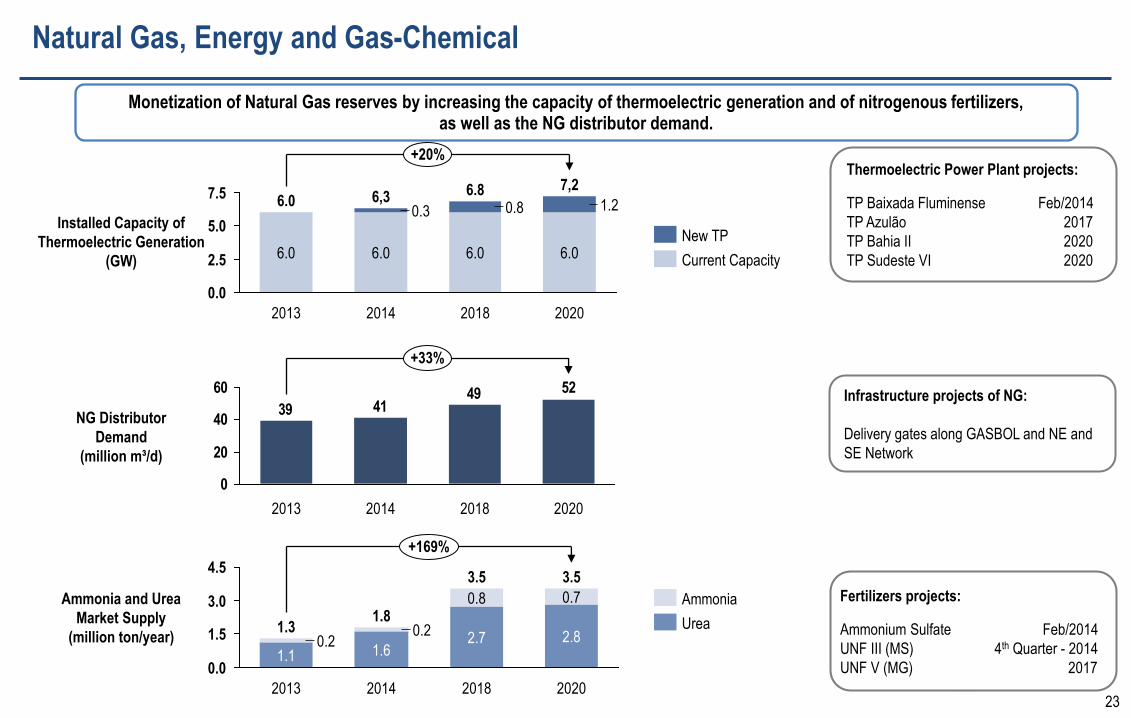

Natural Gas, Energy and Gas-Chemical

7.5

5.0

2.5

0.0

+20%

2020

7,2

6.0

1.2

2018

6.8

6.0

0.8

2014

6,3

6.0

0.3

2013

6.0

6.0

Installed Capacity of

Thermoelectric Generation

(GW) Current Capacity

New TP

52494139

0

20

40

60

+33%

2020 2018 2014 2013

NG Distributor

Demand

(million m³/d)

0.7

2018

4.5

3.0

1.5

0.0

+169%

2020

3.5

2.8

1.8

1.6

3.5

2.7

0.8

2014

0.2

2013

1.3

1.1 0.2

Ammonia and Urea

Market Supply

(million ton/year)

Ammonia

Urea

Thermoelectric Power Plant projects:

TP Baixada Fluminense Feb/2014

TP Azulão 2017

TP Bahia II 2020

TP Sudeste VI 2020

Fertilizers projects:

Ammonium Sulfate Feb/2014

UNF III (MS) 4th Quarter - 2014

UNF V (MG) 2017

Infrastructure projects of NG:

Delivery gates along GASBOL and NE and

SE Network

Monetization of Natural Gas reserves by increasing the capacity of thermoelectric generation and of nitrogenous fertilizers, as well as the NG distributor demand.

24 24

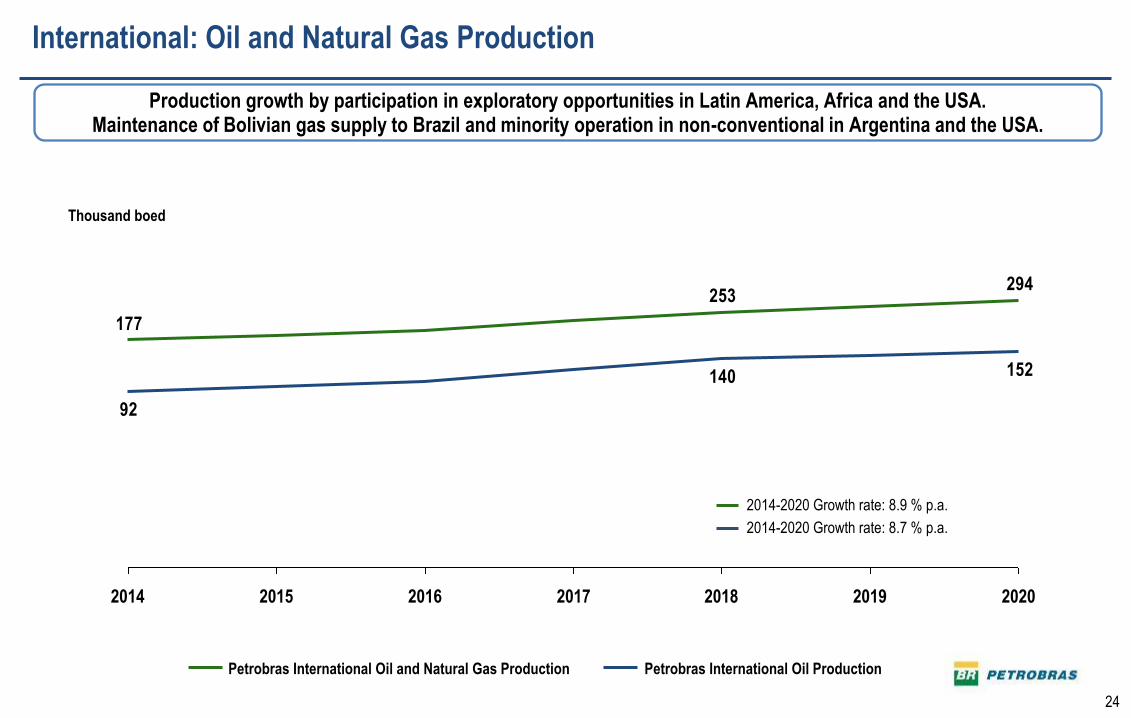

International: Oil and Natural Gas Production

Production growth by participation in exploratory opportunities in Latin America, Africa and the USA. Maintenance of Bolivian gas supply to Brazil and minority operation in non-conventional in Argentina and the USA.

294253

177

152140

92

2020 2019 2017 2018 2016 2014 2015

Petrobras International Oil and Natural Gas Production Petrobras International Oil Production

Thousand boed

2014-2020 Growth rate: 8.9 % p.a.

2014-2020 Growth rate: 8.7 % p.a.

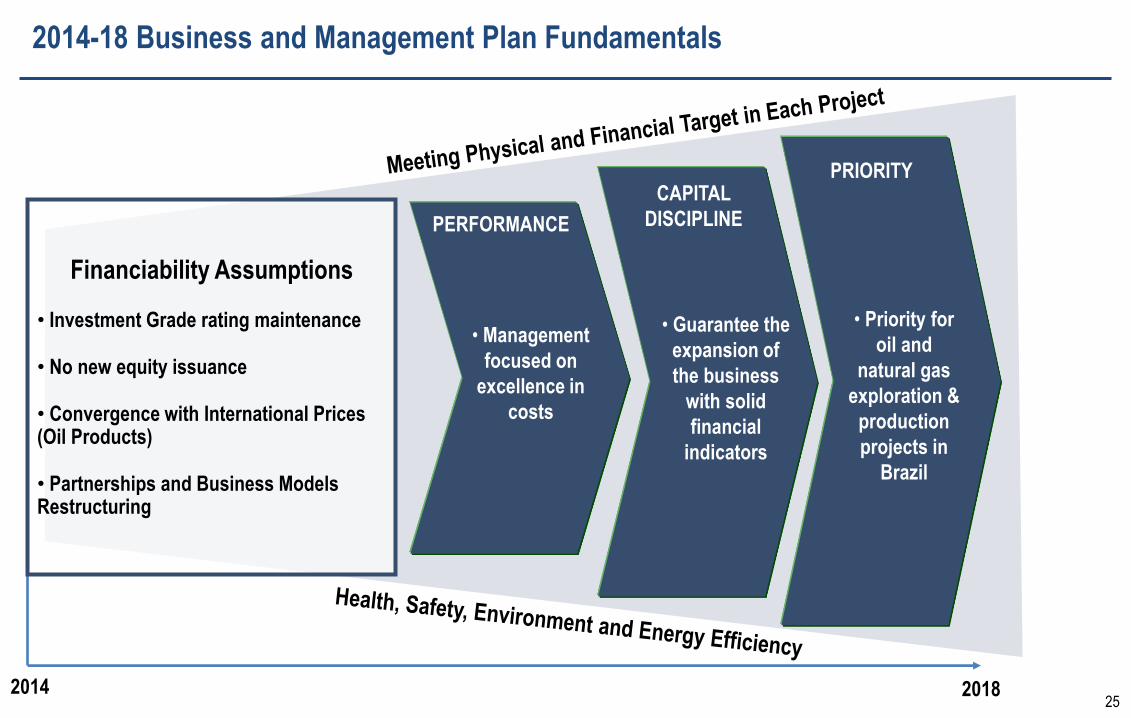

25 25

• Management

focused on

excellence in

costs

PERFORMANCE

• Guarantee the

expansion of

the business

with solid

financial

indicators

CAPITAL

DISCIPLINE

• Priority for

oil and

natural gas

exploration &

production

projects in

Brazil

PRIORITY

2014 2018

Financiability Assumptions

• Investment Grade rating maintenance

• No new equity issuance

• Convergence with International Prices (Oil Products)

• Partnerships and Business Models Restructuring

2014-18 Business and Management Plan Fundamentals

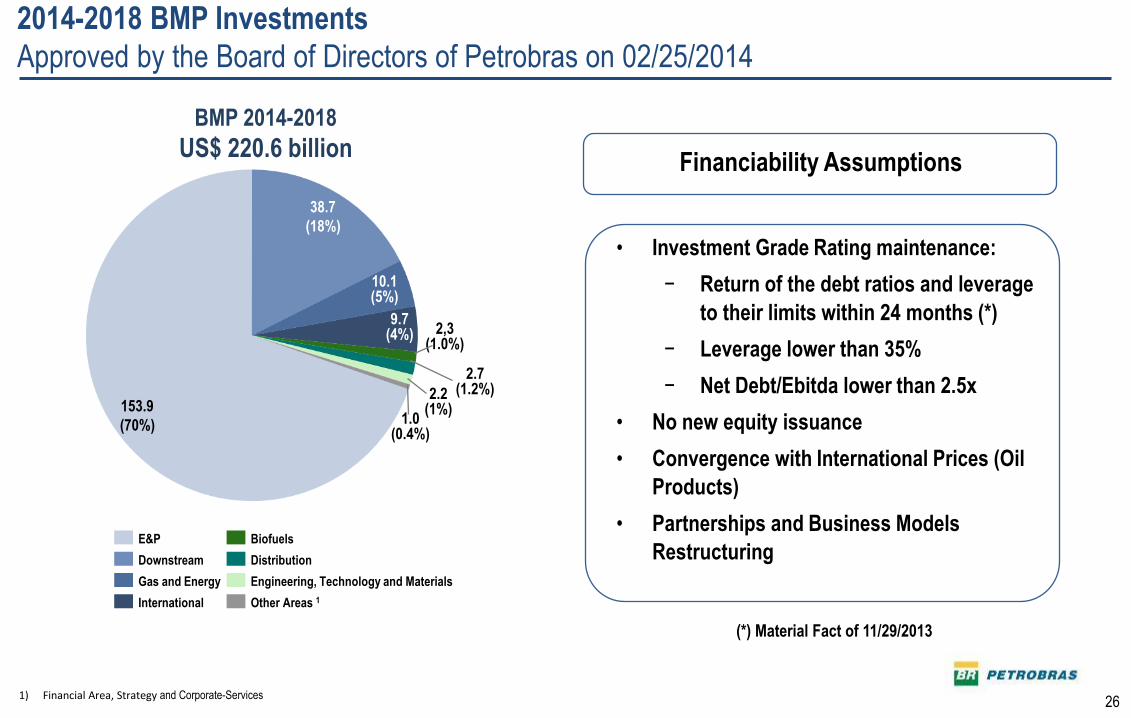

26 26

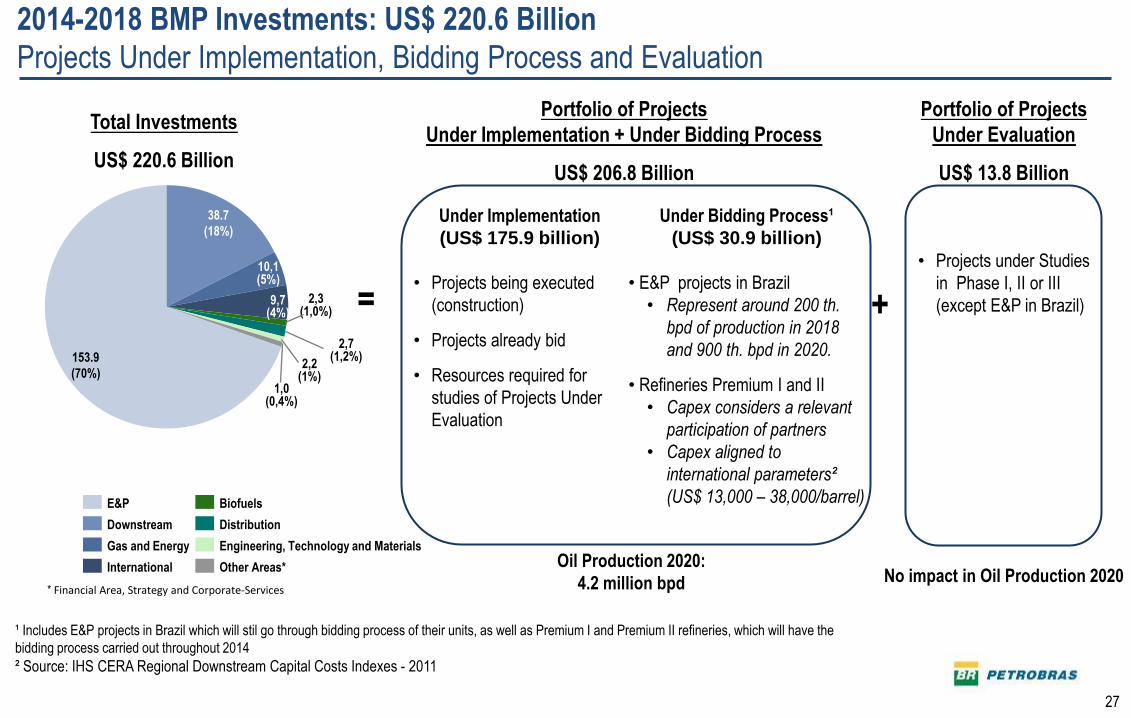

BMP 2014-2018

US$ 220.6 billion

2014-2018 BMP Investments

Approved by the Board of Directors of Petrobras on 02/25/2014

• Investment Grade Rating maintenance:

− Return of the debt ratios and leverage

to their limits within 24 months (*)

− Leverage lower than 35%

− Net Debt/Ebitda lower than 2.5x

• No new equity issuance

• Convergence with International Prices (Oil

Products)

• Partnerships and Business Models

Restructuring

Financiability Assumptions

38.7

(18%)

153.9

(70%)

Distribution

Biofuels

Downstream

Other Areas 1 International

Gas and Energy Engineering, Technology and Materials

E&P

2.2 (1%)

1.0 (0.4%)

2.7 (1.2%)

2,3 (1.0%)

9.7 (4%)

10.1 (5%)

1) Financial Area, Strategy and Corporate-Services

(*) Material Fact of 11/29/2013

27 27

2014-2018 BMP Investments: US$ 220.6 Billion

Projects Under Implementation, Bidding Process and Evaluation

Under Implementation

(US$ 175.9 billion)

• Projects being executed

(construction)

• Projects already bid

• Resources required for

studies of Projects Under

Evaluation

=

38.7

(18%)

153.9

(70%) 2,2

(1%) 1,0

(0,4%)

2,7 (1,2%)

2,3 (1,0%)

9,7 (4%)

10,1 (5%)

Total Investments

US$ 220.6 Billion

Portfolio of Projects

Under Evaluation

US$ 13.8 Billion

Under Bidding Process¹

(US$ 30.9 billion)

• E&P projects in Brazil

• Represent around 200 th.

bpd of production in 2018

and 900 th. bpd in 2020.

• Refineries Premium I and II

• Capex considers a relevant

participation of partners

• Capex aligned to

international parameters²

(US$ 13,000 – 38,000/barrel)

• Projects under Studies

in Phase I, II or III

(except E&P in Brazil)

Oil Production 2020:

4.2 million bpd No impact in Oil Production 2020

+

Portfolio of Projects

Under Implementation + Under Bidding Process

US$ 206.8 Billion

* Financial Area, Strategy and Corporate-Services

Distribution

Biofuels

Downstream

Other Areas* International

Gas and Energy Engineering, Technology and Materials

E&P

¹ Includes E&P projects in Brazil which will stil go through bidding process of their units, as well as Premium I and Premium II refineries, which will have the

bidding process carried out throughout 2014

² Source: IHS CERA Regional Downstream Capital Costs Indexes - 2011

28 28

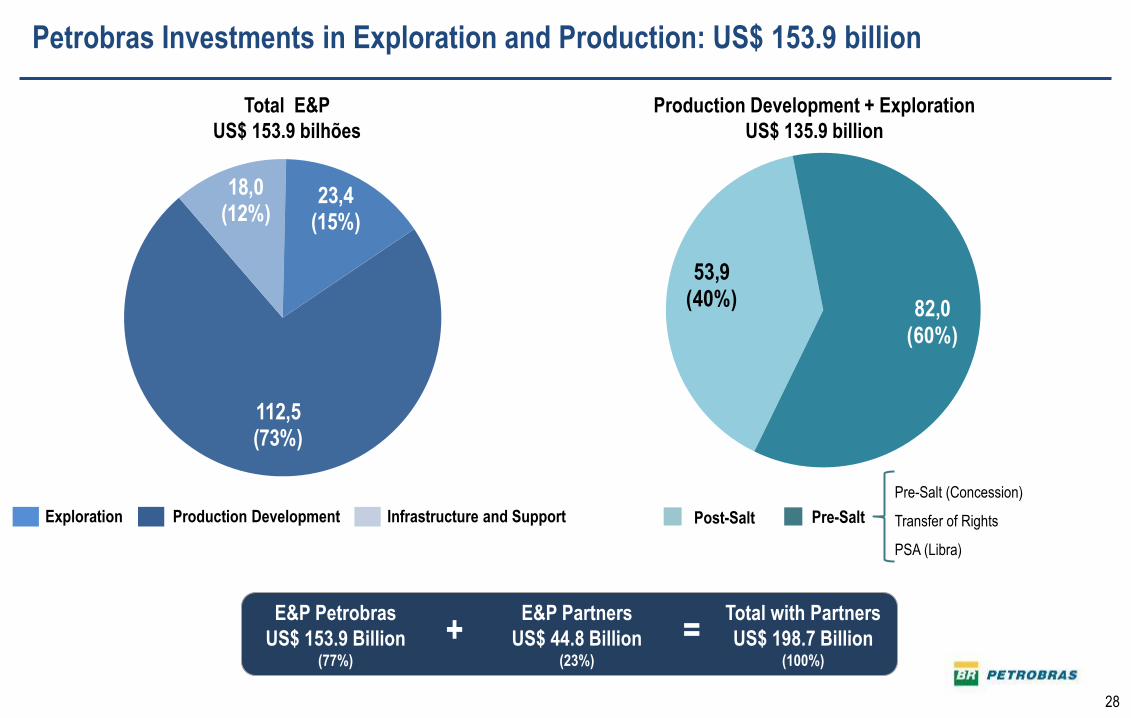

112,5(73%)

18,0(12%)

23,4(15%)

Petrobras Investments in Exploration and Production: US$ 153.9 billion

Total E&P

US$ 153.9 bilhões

Production Development Exploration Infrastructure and Support

E&P Petrobras

US$ 153.9 Billion (77%)

= + E&P Partners

US$ 44.8 Billion (23%)

Total with Partners

US$ 198.7 Billion (100%)

Pre-Salt Post-Salt

Production Development + Exploration

US$ 135.9 billion

Pre-Salt (Concession)

Transfer of Rights

PSA (Libra)

53,9(40%) 82,0

(60%)

29 29

9,092%

0,050,5%

0,66%

0,010,1% 0,05

0,5%0,1

0,7%

Projects Under Implementation

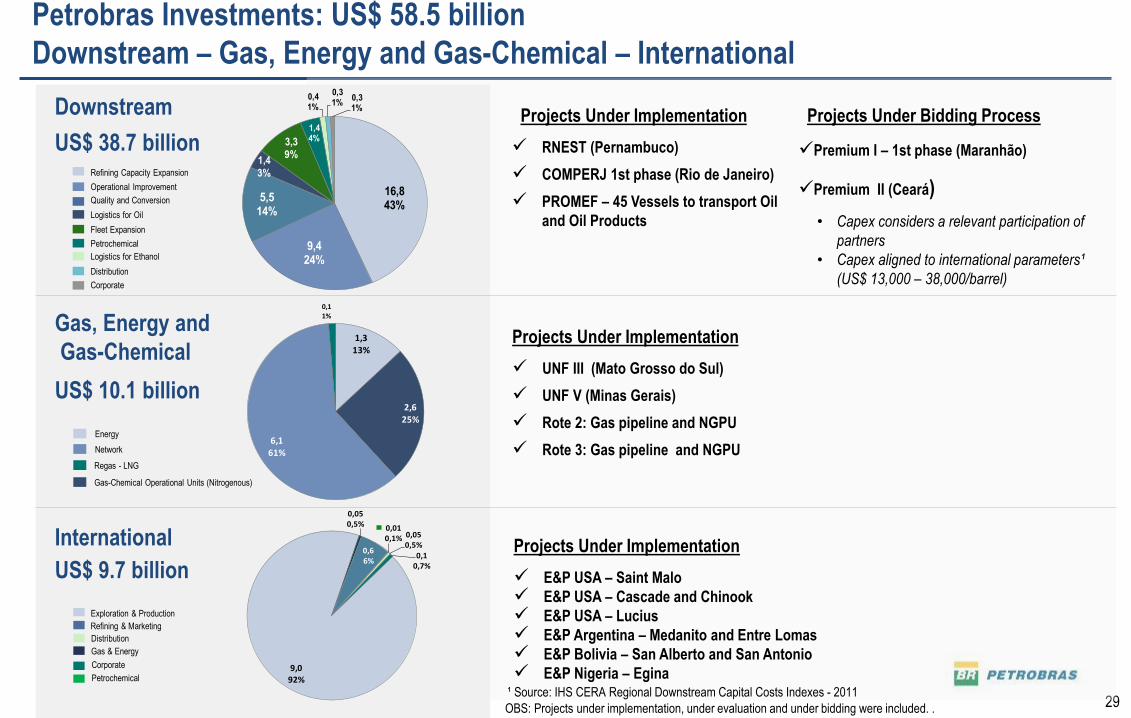

RNEST (Pernambuco)

COMPERJ 1st phase (Rio de Janeiro)

PROMEF – 45 Vessels to transport Oil

and Oil Products

Projects Under Bidding Process

Premium I – 1st phase (Maranhão)

Premium II (Ceará)

• Capex considers a relevant participation of

partners

• Capex aligned to international parameters¹

(US$ 13,000 – 38,000/barrel)

Projects Under Implementation

UNF III (Mato Grosso do Sul)

UNF V (Minas Gerais)

Rote 2: Gas pipeline and NGPU

Rote 3: Gas pipeline and NGPU

Downstream

Gas, Energy and

Gas-Chemical

International Projects Under Implementation

E&P USA – Saint Malo

E&P USA – Cascade and Chinook

E&P USA – Lucius

E&P Argentina – Medanito and Entre Lomas

E&P Bolivia – San Alberto and San Antonio

E&P Nigeria – Egina

US$ 38.7 billion

US$ 10.1 billion

US$ 9.7 billion

Petrobras Investments: US$ 58.5 billion

Downstream – Gas, Energy and Gas-Chemical – International

Logistics for Ethanol

Corporate

Petrochemical

Fleet Expansion

Logistics for Oil

Quality and Conversion

Operational Improvement

Refining Capacity Expansion

Distribution

Gas-Chemical Operational Units (Nitrogenous)

Regas - LNG

Network

Energy

Distribution

Corporate

Gas & Energy

Refining & Marketing

Exploration & Production

Petrochemical

1,313%

2,625%

6,161%

0,11%

16,843%

9,424%

5,514%

1,43%

3,39%

1,44%

0,41%

0,31%

0,31%

OBS: Projects under implementation, under evaluation and under bidding were included. .

¹ Source: IHS CERA Regional Downstream Capital Costs Indexes - 2011

30

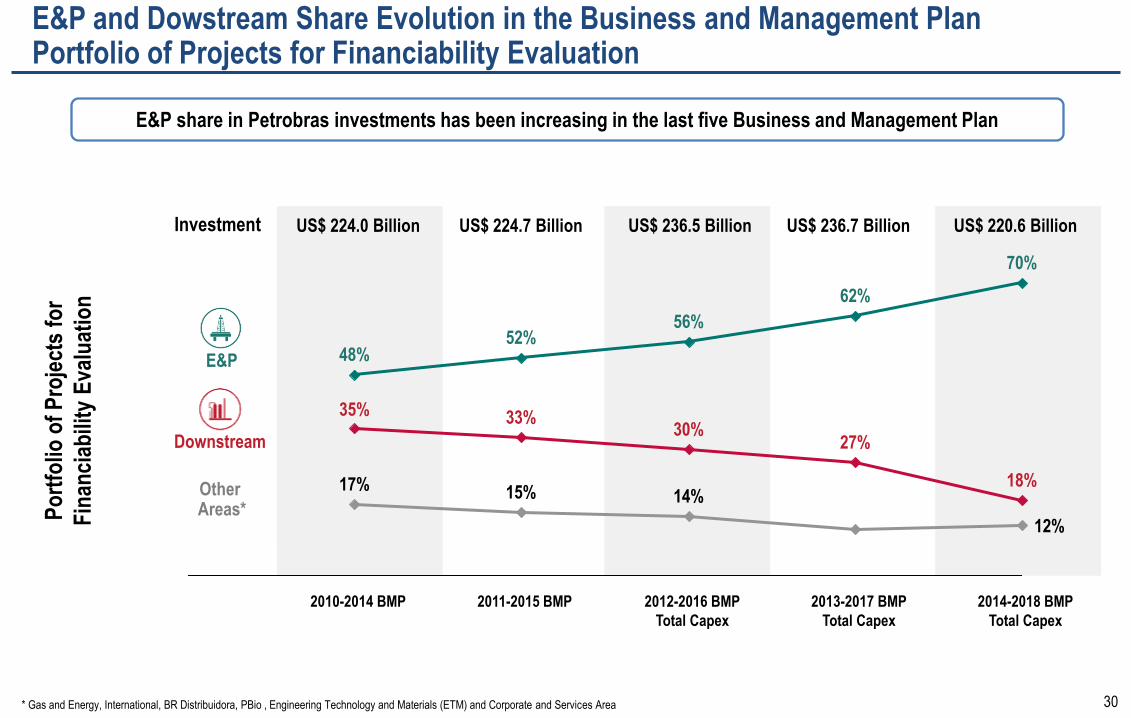

E&P and Dowstream Share Evolution in the Business and Management Plan Portfolio of Projects for Financiability Evaluation

* Gas and Energy, International, BR Distribuidora, PBio , Engineering Technology and Materials (ETM) and Corporate and Services Area

2014-2018 BMP

Total Capex

2012-2016 BMP

Total Capex

2013-2017 BMP

Total Capex

2010-2014 BMP 2011-2015 BMP

E&P

Downstream

Other Areas* P

ort

folio

of

Pro

ject

s fo

r

Fin

anci

abili

ty E

valu

atio

n

US$ 224.0 Billion Investment US$ 224.7 Billion US$ 236.5 Billion US$ 236.7 Billion US$ 220.6 Billion

E&P share in Petrobras investments has been increasing in the last five Business and Management Plan

48%

35%

17%

52%

33%

11% 15%

18%

27%

62%

14%

30%

56%

70%

12%

31 31

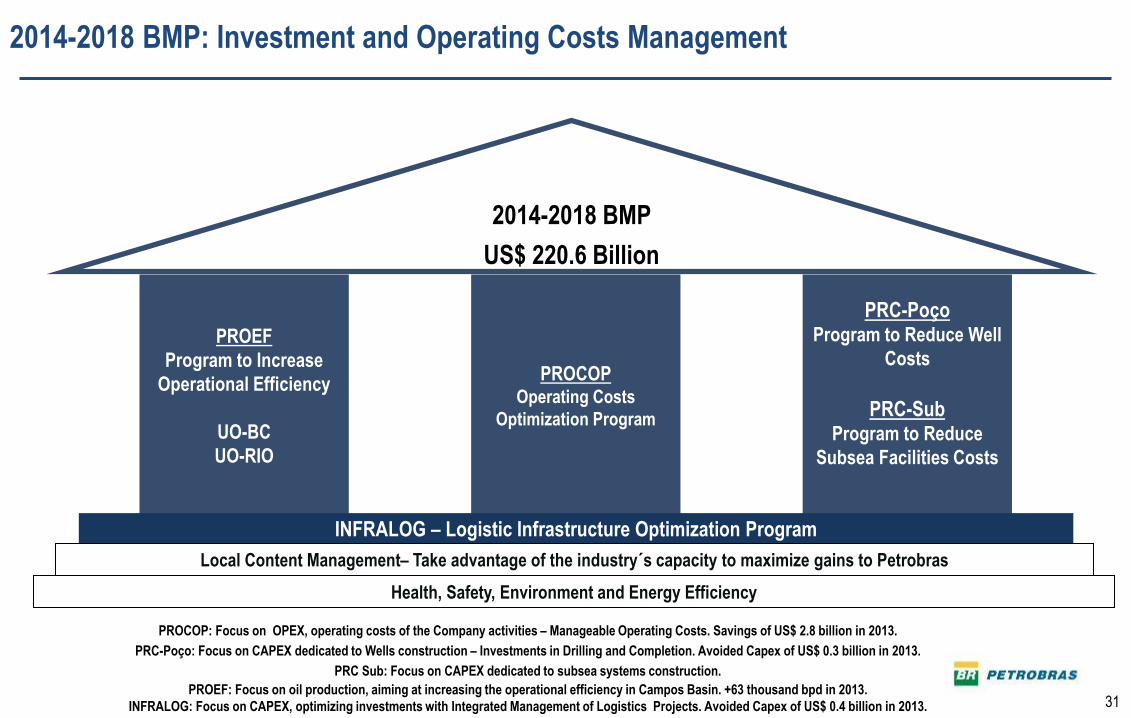

2014-2018 BMP: Investment and Operating Costs Management

2014-2018 BMP

US$ 220.6 Billion

PRC-Poço Program to Reduce Well

Costs

PRC-Sub Program to Reduce

Subsea Facilities Costs

PROEF

Program to Increase

Operational Efficiency

UO-BC

UO-RIO

PROCOP Operating Costs

Optimization Program

INFRALOG – Logistic Infrastructure Optimization Program

Local Content Management– Take advantage of the industry´s capacity to maximize gains to Petrobras

Health, Safety, Environment and Energy Efficiency

PROCOP: Focus on OPEX, operating costs of the Company activities – Manageable Operating Costs. Savings of US$ 2.8 billion in 2013.

PRC-Poço: Focus on CAPEX dedicated to Wells construction – Investments in Drilling and Completion. Avoided Capex of US$ 0.3 billion in 2013.

PRC Sub: Focus on CAPEX dedicated to subsea systems construction.

PROEF: Focus on oil production, aiming at increasing the operational efficiency in Campos Basin. +63 thousand bpd in 2013.

INFRALOG: Focus on CAPEX, optimizing investments with Integrated Management of Logistics Projects. Avoided Capex of US$ 0.4 billion in 2013.

32 32

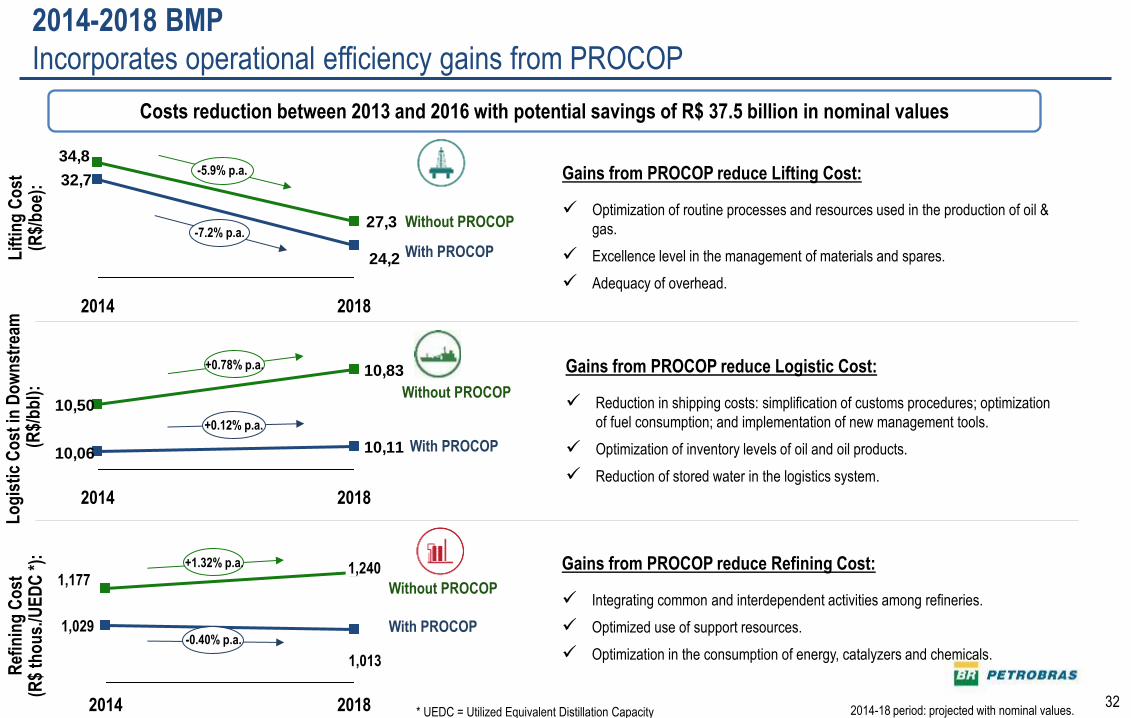

2014-2018 BMP

Incorporates operational efficiency gains from PROCOP

* UEDC = Utilized Equivalent Distillation Capacity 2014-18 period: projected with nominal values.

Lif

tin

g C

ost

(R

$/b

oe)

:

27,3

34,8

24,2

32,7

2018 2014

-7.2% p.a.

-5.9% p.a.

10,83

10,11

10,50

10,06

2018 2014

+0.12% p.a.

+0.78% p.a.

1,177

2018

1,013

1,240

2014

1,029 -0.40% p.a.

+1.32% p.a.

Costs reduction between 2013 and 2016 with potential savings of R$ 37.5 billion in nominal values

Lo

gis

tic

Co

st in

Do

wn

stre

am

(R

$/b

bl)

: R

efin

ing

Co

st

(R$

tho

us.

/UE

DC

*):

Without PROCOP

With PROCOP

Without PROCOP

With PROCOP

Without PROCOP

With PROCOP

Gains from PROCOP reduce Logistic Cost:

Reduction in shipping costs: simplification of customs procedures; optimization

of fuel consumption; and implementation of new management tools.

Optimization of inventory levels of oil and oil products.

Reduction of stored water in the logistics system.

Gains from PROCOP reduce Lifting Cost:

Optimization of routine processes and resources used in the production of oil &

gas.

Excellence level in the management of materials and spares.

Adequacy of overhead.

Gains from PROCOP reduce Refining Cost:

Integrating common and interdependent activities among refineries.

Optimized use of support resources.

Optimization in the consumption of energy, catalyzers and chemicals.

33 33

*Financial Area, Strategy and Corporate-Services

No impact in Oil

Production 2020

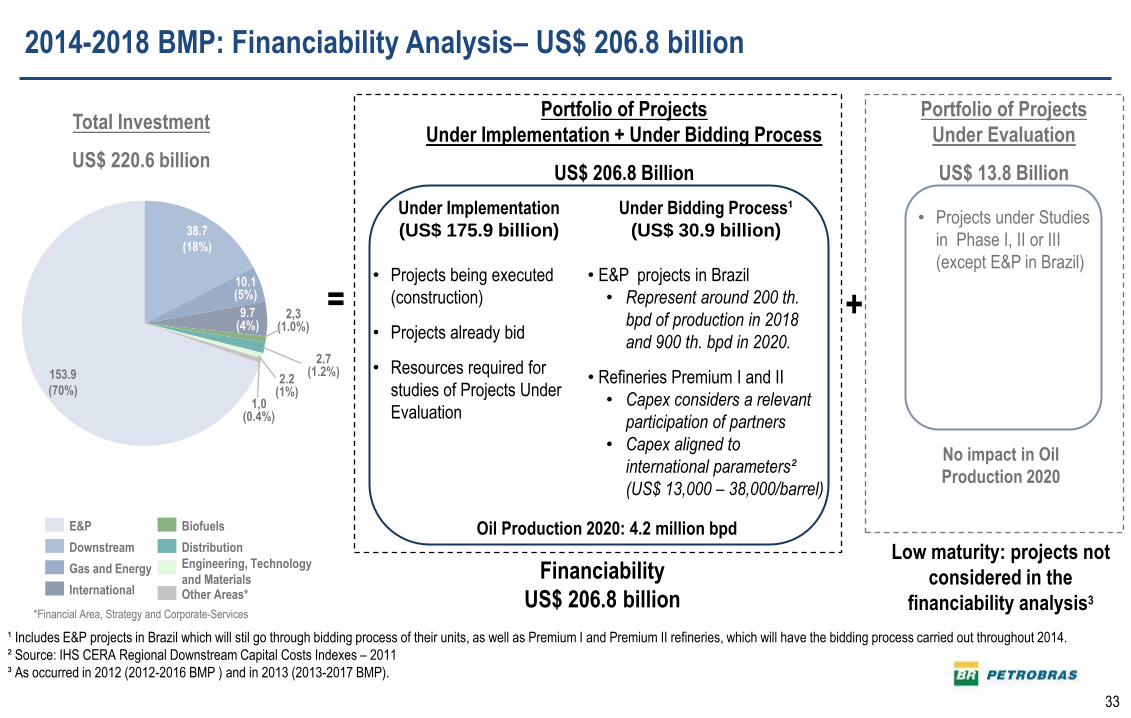

2014-2018 BMP: Financiability Analysis– US$ 206.8 billion

Total Investment

US$ 220.6 billion

• Projects under Studies

in Phase I, II or III

(except E&P in Brazil)

+

Financiability

US$ 206.8 billion

Low maturity: projects not

considered in the

financiability analysis3

38.7

(18%)

153.9

(70%) 2.2

(1%) 1,0

(0.4%)

2.7 (1.2%)

2,3 (1.0%)

9.7 (4%)

10.1 (5%)

Distribution

Biofuels

Downstream

Other Areas* International

Gas and Energy Engineering, Technology

and Materials

E&P

¹ Includes E&P projects in Brazil which will stil go through bidding process of their units, as well as Premium I and Premium II refineries, which will have the bidding process carried out throughout 2014.

² Source: IHS CERA Regional Downstream Capital Costs Indexes – 2011

³ As occurred in 2012 (2012-2016 BMP ) and in 2013 (2013-2017 BMP).

Portfolio of Projects

Under Evaluation

US$ 13.8 Billion

Portfolio of Projects

Under Implementation + Under Bidding Process

US$ 206.8 Billion

• Projects under Studies

in Phase I, II or III

(except E&P in Brazil)

Oil Production 2020: 4.2 million bpd

Under Implementation

(US$ 175.9 billion)

• Projects being executed

(construction)

• Projects already bid

• Resources required for

studies of Projects Under

Evaluation

Under Bidding Process¹

(US$ 30.9 billion)

• E&P projects in Brazil

• Represent around 200 th.

bpd of production in 2018

and 900 th. bpd in 2020.

• Refineries Premium I and II

• Capex considers a relevant

participation of partners

• Capex aligned to

international parameters²

(US$ 13,000 – 38,000/barrel)

=

34 34

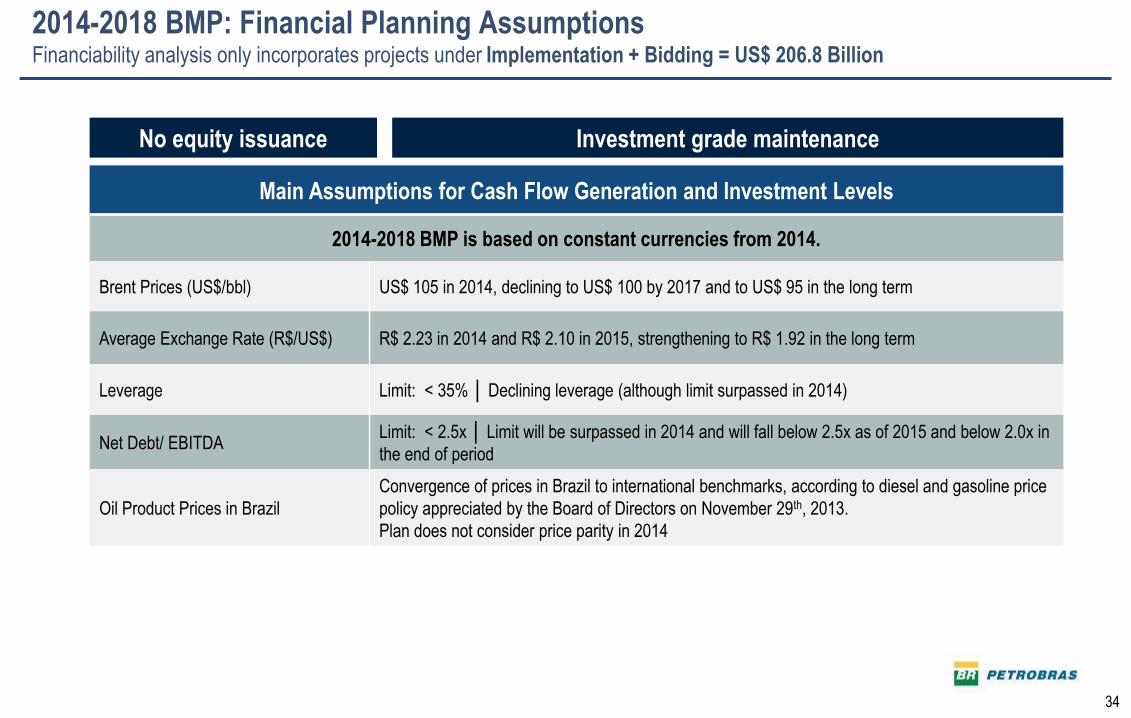

2014-2018 BMP: Financial Planning Assumptions Financiability analysis only incorporates projects under Implementation + Bidding = US$ 206.8 Billion

Main Assumptions for Cash Flow Generation and Investment Levels

2014-2018 BMP is based on constant currencies from 2014.

Brent Prices (US$/bbl) US$ 105 in 2014, declining to US$ 100 by 2017 and to US$ 95 in the long term

Average Exchange Rate (R$/US$) R$ 2.23 in 2014 and R$ 2.10 in 2015, strengthening to R$ 1.92 in the long term

Leverage Limit: < 35% │ Declining leverage (although limit surpassed in 2014)

Net Debt/ EBITDA Limit: < 2.5x │ Limit will be surpassed in 2014 and will fall below 2.5x as of 2015 and below 2.0x in

the end of period

Oil Product Prices in Brazil

Convergence of prices in Brazil to international benchmarks, according to diesel and gasoline price

policy appreciated by the Board of Directors on November 29th, 2013.

Plan does not consider price parity in 2014

No equity issuance Investment grade maintenance

35 35

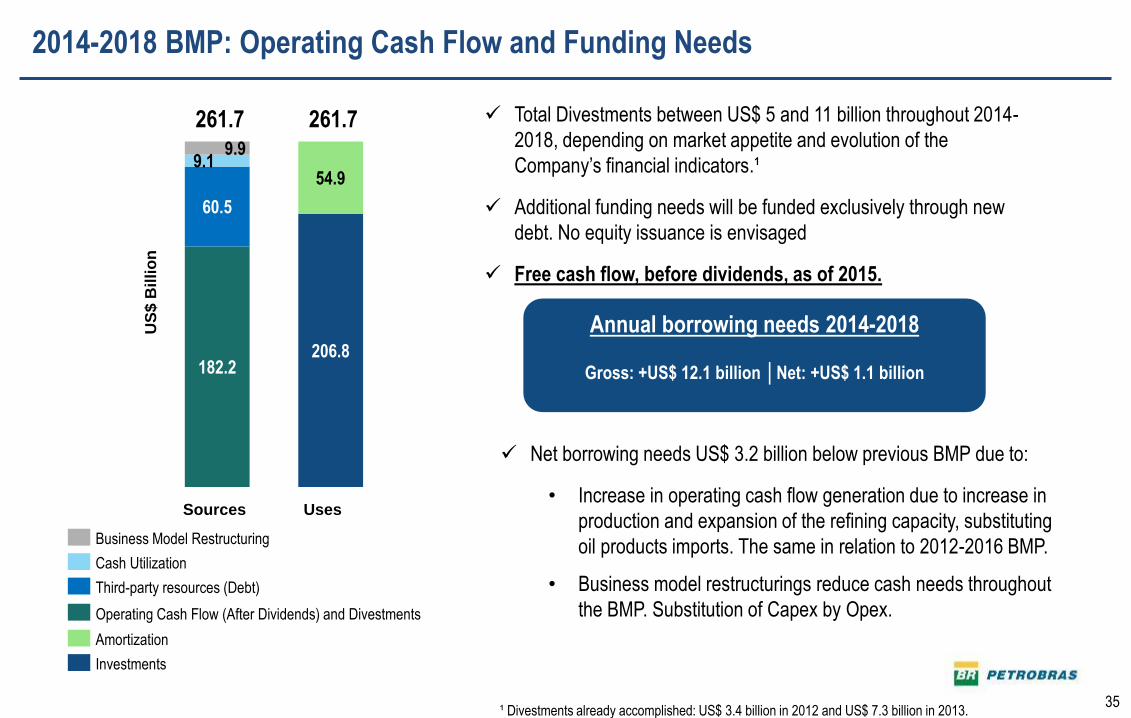

2014-2018 BMP: Operating Cash Flow and Funding Needs

61,3

165,0

Operating Cash Flow (After Dividends) and Divestments

Third-party resources (Debt)

Cash Utilization

Business Model Restructuring

207,1

39,8

Amortization

Investments

Annual borrowing needs 2014-2018

Gross: +US$ 12.1 billion │Net: +US$ 1.1 billion

Total Divestments between US$ 5 and 11 billion throughout 2014-

2018, depending on market appetite and evolution of the

Company’s financial indicators.¹

Additional funding needs will be funded exclusively through new

debt. No equity issuance is envisaged

Free cash flow, before dividends, as of 2015.

Net borrowing needs US$ 3.2 billion below previous BMP due to:

• Increase in operating cash flow generation due to increase in

production and expansion of the refining capacity, substituting

oil products imports. The same in relation to 2012-2016 BMP.

• Business model restructurings reduce cash needs throughout

the BMP. Substitution of Capex by Opex.

182.2

60.5

9.1 9.9

206.8

54.9

261.7 261.7

Fontes Usos

US

$ b

ilhão

Sources Uses

US

$ B

illi

on

¹ Divestments already accomplished: US$ 3.4 billion in 2012 and US$ 7.3 billion in 2013.

36 36

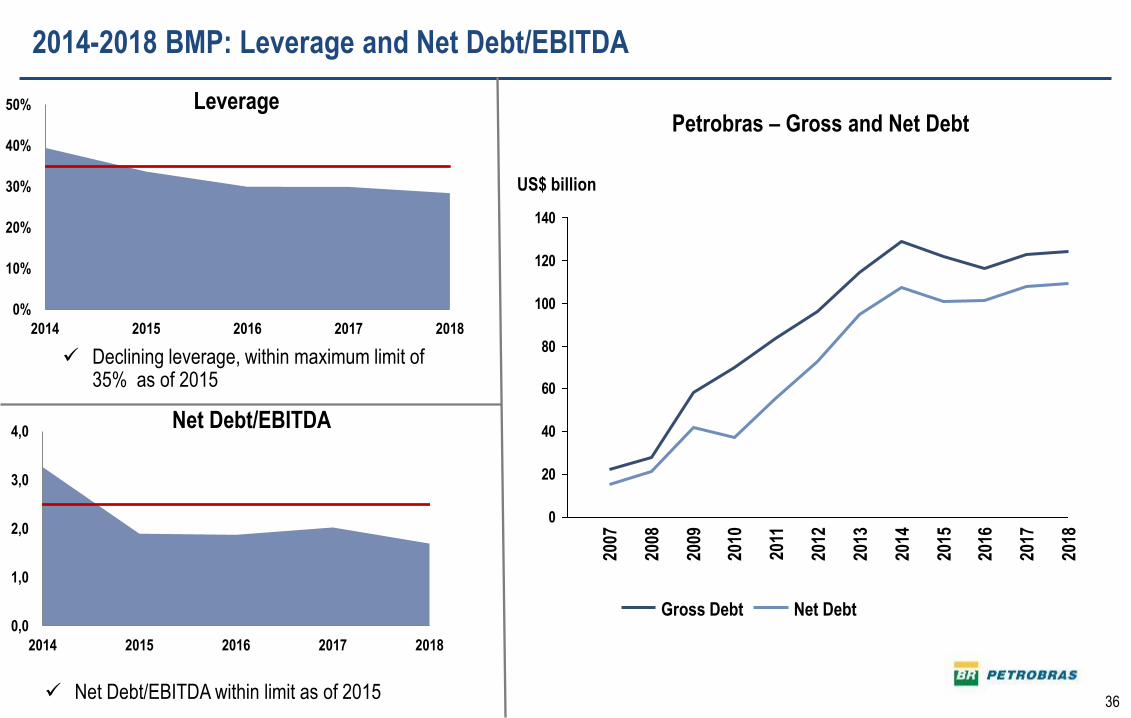

2014-2018 BMP: Leverage and Net Debt/EBITDA

Net Debt/EBITDA within limit as of 2015

Leverage

Net Debt/EBITDA

Declining leverage, within maximum limit of 35% as of 2015

0

20

40

60

80

100

120

140

2008

2009

2010

2011

2012

2018

2013

2014

2015

2016

2017

2007

Net Debt Gross Debt

US$ billion

Petrobras – Gross and Net Debt

0%

10%

20%

30%

40%

50%

2014 2015 2016 2017 2018

0,0

1,0

2,0

3,0

4,0

2014 2015 2016 2017 2018

37

FX Rate Sensitivity

38

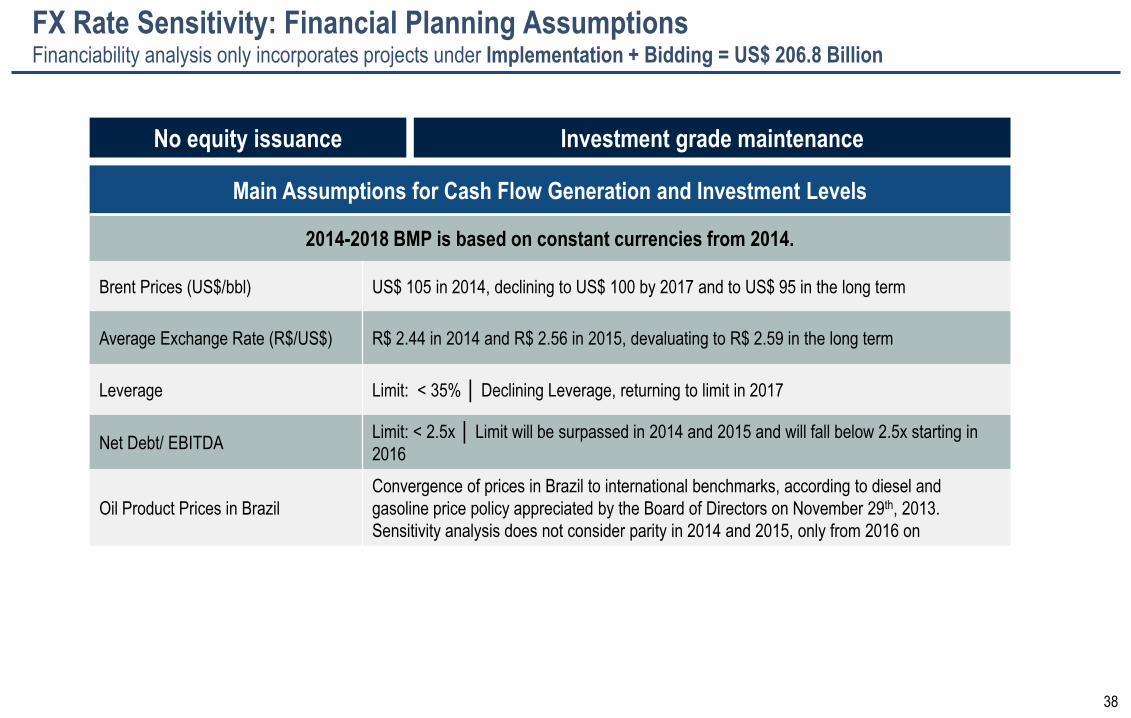

FX Rate Sensitivity: Financial Planning Assumptions Financiability analysis only incorporates projects under Implementation + Bidding = US$ 206.8 Billion

Main Assumptions for Cash Flow Generation and Investment Levels

2014-2018 BMP is based on constant currencies from 2014.

Brent Prices (US$/bbl) US$ 105 in 2014, declining to US$ 100 by 2017 and to US$ 95 in the long term

Average Exchange Rate (R$/US$) R$ 2.44 in 2014 and R$ 2.56 in 2015, devaluating to R$ 2.59 in the long term

Leverage Limit: < 35% │ Declining Leverage, returning to limit in 2017

Net Debt/ EBITDA Limit: < 2.5x │ Limit will be surpassed in 2014 and 2015 and will fall below 2.5x starting in

2016

Oil Product Prices in Brazil

Convergence of prices in Brazil to international benchmarks, according to diesel and

gasoline price policy appreciated by the Board of Directors on November 29th, 2013.

Sensitivity analysis does not consider parity in 2014 and 2015, only from 2016 on

No equity issuance Investment grade maintenance

39

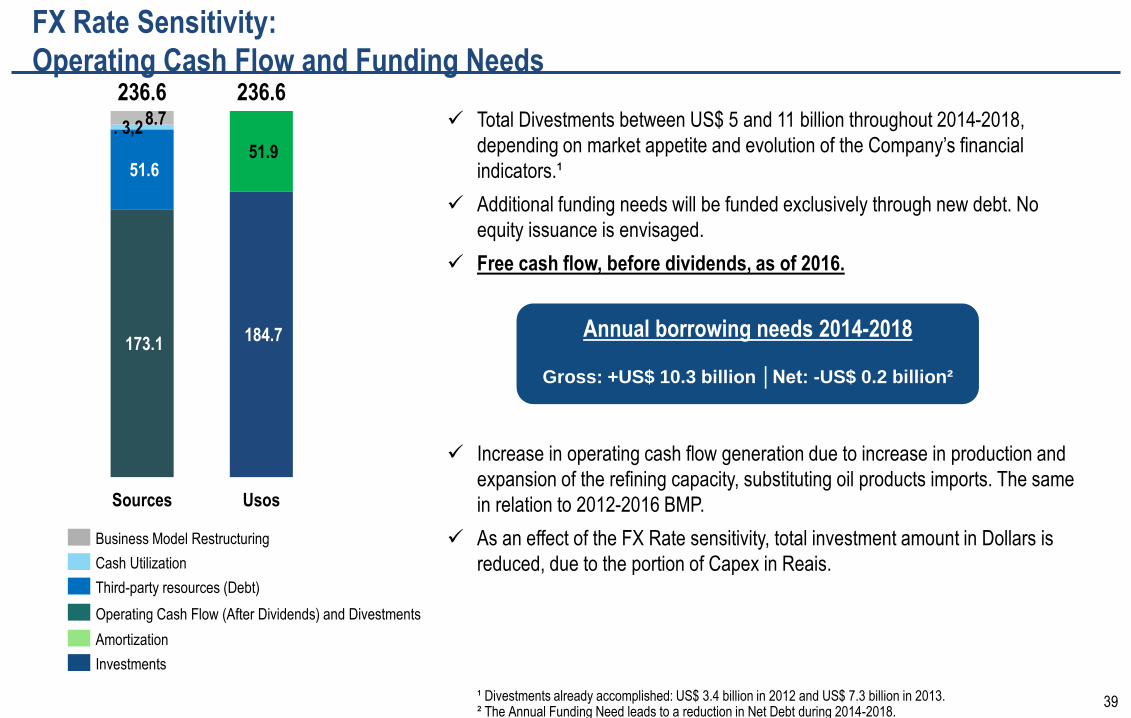

FX Rate Sensitivity:

Operating Cash Flow and Funding Needs

61,3

165,0

207,1

39,8

Annual borrowing needs 2014-2018

Gross: +US$ 10.3 billion │Net: -US$ 0.2 billion²

Total Divestments between US$ 5 and 11 billion throughout 2014-2018,

depending on market appetite and evolution of the Company’s financial

indicators.¹

Additional funding needs will be funded exclusively through new debt. No

equity issuance is envisaged.

Free cash flow, before dividends, as of 2016.

Increase in operating cash flow generation due to increase in production and

expansion of the refining capacity, substituting oil products imports. The same

in relation to 2012-2016 BMP.

As an effect of the FX Rate sensitivity, total investment amount in Dollars is

reduced, due to the portion of Capex in Reais.

173.1

51.6

. 3,2 8.7

184.7

51.9

236.6 236.6

Sources Usos

¹ Divestments already accomplished: US$ 3.4 billion in 2012 and US$ 7.3 billion in 2013. ² The Annual Funding Need leads to a reduction in Net Debt during 2014-2018.

Operating Cash Flow (After Dividends) and Divestments

Third-party resources (Debt)

Cash Utilization

Business Model Restructuring

Amortization

Investments

40

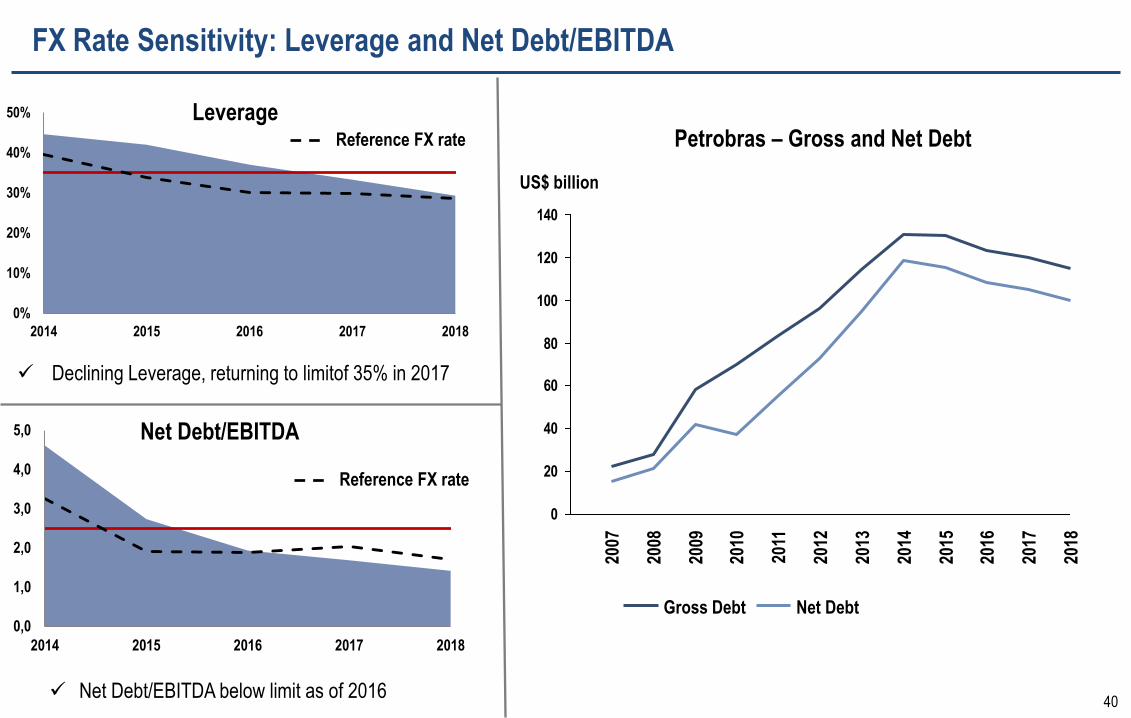

FX Rate Sensitivity: Leverage and Net Debt/EBITDA

Declining Leverage, returning to limitof 35% in 2017

Leverage

Net Debt/EBITDA

Net Debt/EBITDA below limit as of 2016

0

20

40

60

80

100

120

140

2016

2015

2008

2007

2010

2009

2018

2017

2014

2013

2012

2011

Net Debt Gross Debt

US$ billion

Petrobras – Gross and Net Debt

0%

10%

20%

30%

40%

50%

2014 2015 2016 2017 2018

0,0

1,0

2,0

3,0

4,0

5,0

2014 2015 2016 2017 2018

Reference FX rate

Reference FX rate

41

Investment Sensitivity

(Portfolio Under Implementation

= US$175.9 billion)

42

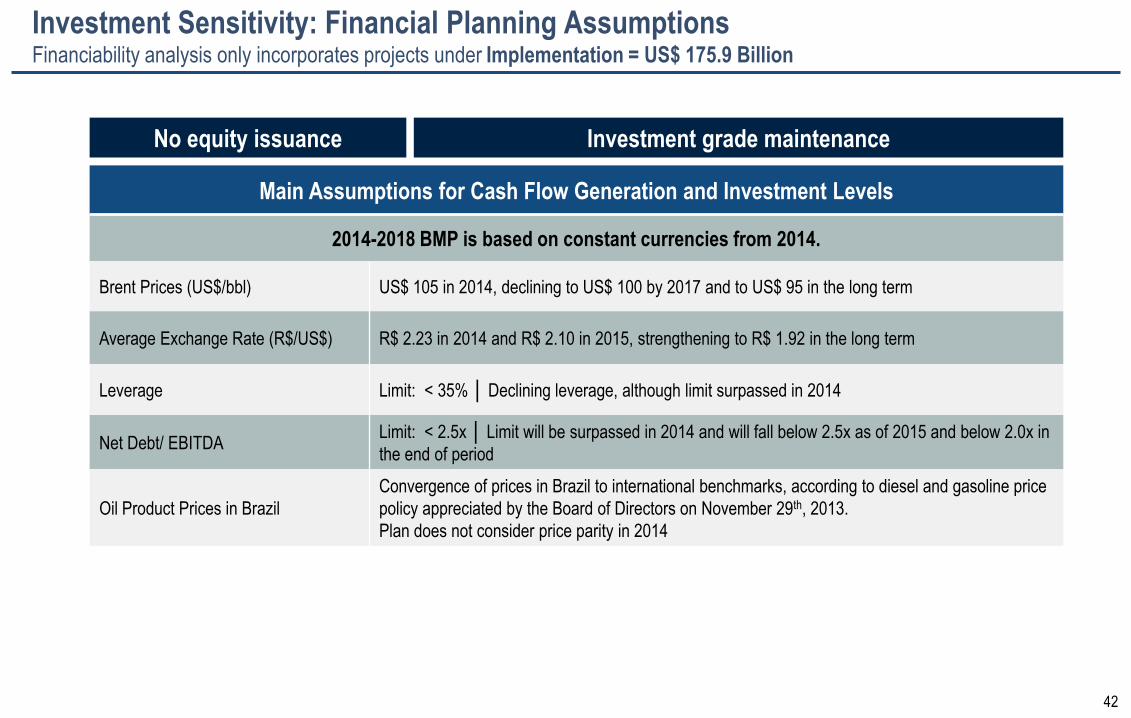

Investment Sensitivity: Financial Planning Assumptions Financiability analysis only incorporates projects under Implementation = US$ 175.9 Billion

Main Assumptions for Cash Flow Generation and Investment Levels

2014-2018 BMP is based on constant currencies from 2014.

Brent Prices (US$/bbl) US$ 105 in 2014, declining to US$ 100 by 2017 and to US$ 95 in the long term

Average Exchange Rate (R$/US$) R$ 2.23 in 2014 and R$ 2.10 in 2015, strengthening to R$ 1.92 in the long term

Leverage Limit: < 35% │ Declining leverage, although limit surpassed in 2014

Net Debt/ EBITDA Limit: < 2.5x │ Limit will be surpassed in 2014 and will fall below 2.5x as of 2015 and below 2.0x in

the end of period

Oil Product Prices in Brazil

Convergence of prices in Brazil to international benchmarks, according to diesel and gasoline price

policy appreciated by the Board of Directors on November 29th, 2013.

Plan does not consider price parity in 2014

No equity issuance Investment grade maintenance

43

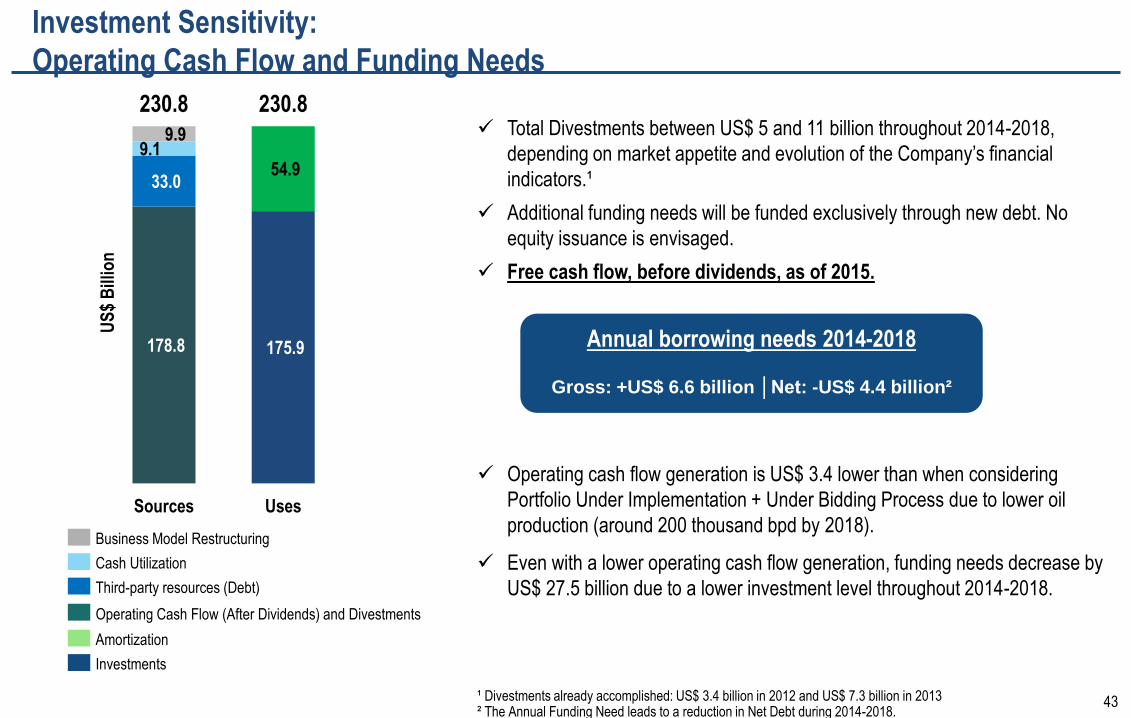

Investment Sensitivity:

Operating Cash Flow and Funding Needs

61,3

165,0

207,1

39,8 Total Divestments between US$ 5 and 11 billion throughout 2014-2018,

depending on market appetite and evolution of the Company’s financial

indicators.¹

Additional funding needs will be funded exclusively through new debt. No

equity issuance is envisaged.

Free cash flow, before dividends, as of 2015.

Operating cash flow generation is US$ 3.4 lower than when considering

Portfolio Under Implementation + Under Bidding Process due to lower oil

production (around 200 thousand bpd by 2018).

Even with a lower operating cash flow generation, funding needs decrease by

US$ 27.5 billion due to a lower investment level throughout 2014-2018.

178.8

33.0

9.1 9.9

175.9

54.9

230.8 230.8

Sources Uses

US

$ B

illio

n

¹ Divestments already accomplished: US$ 3.4 billion in 2012 and US$ 7.3 billion in 2013 ² The Annual Funding Need leads to a reduction in Net Debt during 2014-2018.

Annual borrowing needs 2014-2018

Gross: +US$ 6.6 billion │Net: -US$ 4.4 billion²

Third-party resources (Debt)

Cash Utilization

Business Model Restructuring

Amortization

Investments

Operating Cash Flow (After Dividends) and Divestments

44

Investment Sensitivity: Leverage and Net Debt/EBITDA

Leverage

Net Debt/EBITDA

0

20

40

60

80

100

120

140

2008

2007

2012

2011

2018

2016

2017

2015

2014

2013

2010

2009

Gross Debt Net Debt

US$ billion

Petrobras – Gross and Net Debt

Declining leverage, within maximum limit of 35% as of 2015

Net Debt/EBITDA within limit as of 2015

0%

10%

20%

30%

40%

50%

2014 2015 2016 2017 2018

0,0

1,0

2,0

3,0

4,0

2014 2015 2016 2017 2018

45

Investment (Portfolio Under

Implementation = US$175.9 billion)

and FX Rate Sensitivity

46

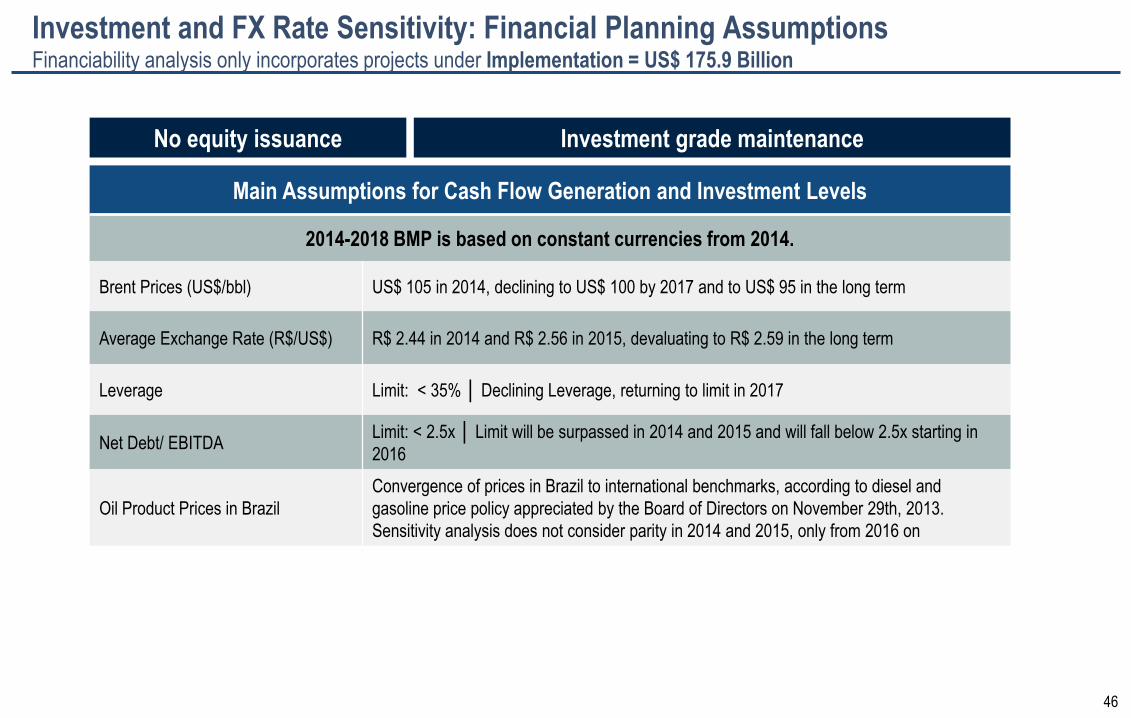

Investment and FX Rate Sensitivity: Financial Planning Assumptions Financiability analysis only incorporates projects under Implementation = US$ 175.9 Billion

Main Assumptions for Cash Flow Generation and Investment Levels

2014-2018 BMP is based on constant currencies from 2014.

Brent Prices (US$/bbl) US$ 105 in 2014, declining to US$ 100 by 2017 and to US$ 95 in the long term

Average Exchange Rate (R$/US$) R$ 2.44 in 2014 and R$ 2.56 in 2015, devaluating to R$ 2.59 in the long term

Leverage Limit: < 35% │ Declining Leverage, returning to limit in 2017

Net Debt/ EBITDA Limit: < 2.5x │ Limit will be surpassed in 2014 and 2015 and will fall below 2.5x starting in

2016

Oil Product Prices in Brazil

Convergence of prices in Brazil to international benchmarks, according to diesel and

gasoline price policy appreciated by the Board of Directors on November 29th, 2013.

Sensitivity analysis does not consider parity in 2014 and 2015, only from 2016 on

No equity issuance Investment grade maintenance

47

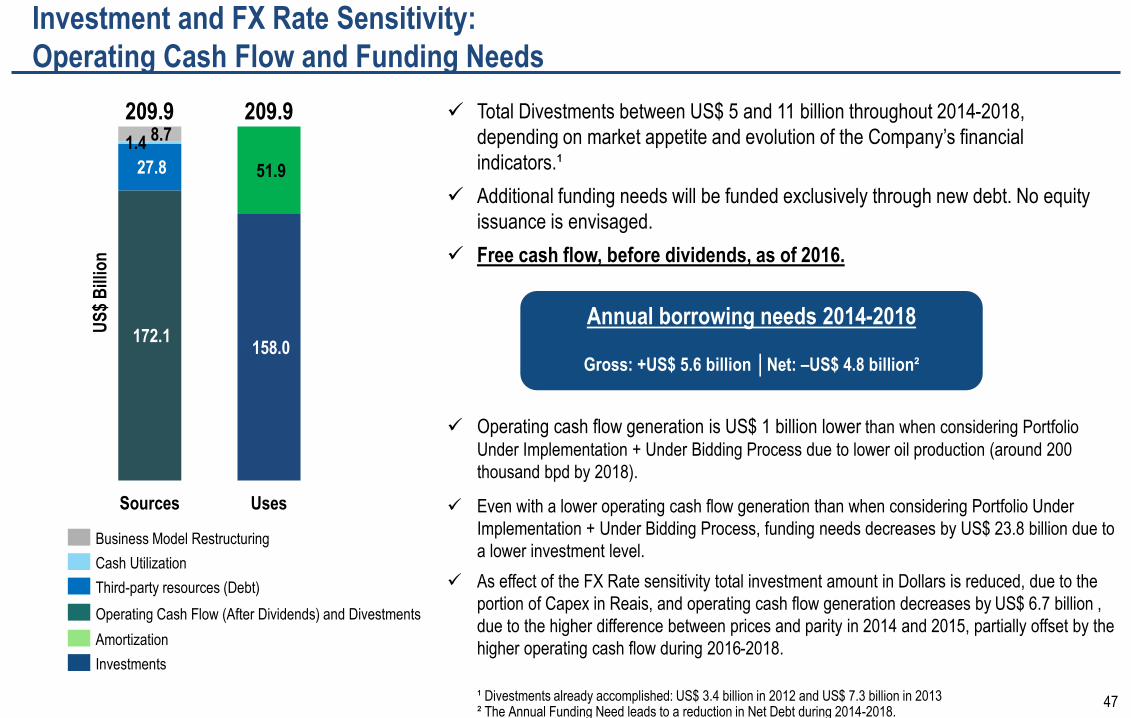

Investment and FX Rate Sensitivity:

Operating Cash Flow and Funding Needs

61,3

165,0

207,1

Total Divestments between US$ 5 and 11 billion throughout 2014-2018,

depending on market appetite and evolution of the Company’s financial

indicators.¹

Additional funding needs will be funded exclusively through new debt. No equity

issuance is envisaged.

Free cash flow, before dividends, as of 2016.

Operating cash flow generation is US$ 1 billion lower than when considering Portfolio

Under Implementation + Under Bidding Process due to lower oil production (around 200

thousand bpd by 2018).

Even with a lower operating cash flow generation than when considering Portfolio Under

Implementation + Under Bidding Process, funding needs decreases by US$ 23.8 billion due to

a lower investment level.

As effect of the FX Rate sensitivity total investment amount in Dollars is reduced, due to the

portion of Capex in Reais, and operating cash flow generation decreases by US$ 6.7 billion ,

due to the higher difference between prices and parity in 2014 and 2015, partially offset by the

higher operating cash flow during 2016-2018.

172.1

27.8

1.4 8.7

158.0

51.9

209.9 209.9

Sources Uses

US

$ B

illio

n

Annual borrowing needs 2014-2018

Gross: +US$ 5.6 billion │Net: –US$ 4.8 billion²

Operating Cash Flow (After Dividends) and Divestments

Third-party resources (Debt)

Cash Utilization

Business Model Restructuring

Amortization

Investments

¹ Divestments already accomplished: US$ 3.4 billion in 2012 and US$ 7.3 billion in 2013 ² The Annual Funding Need leads to a reduction in Net Debt during 2014-2018.

48

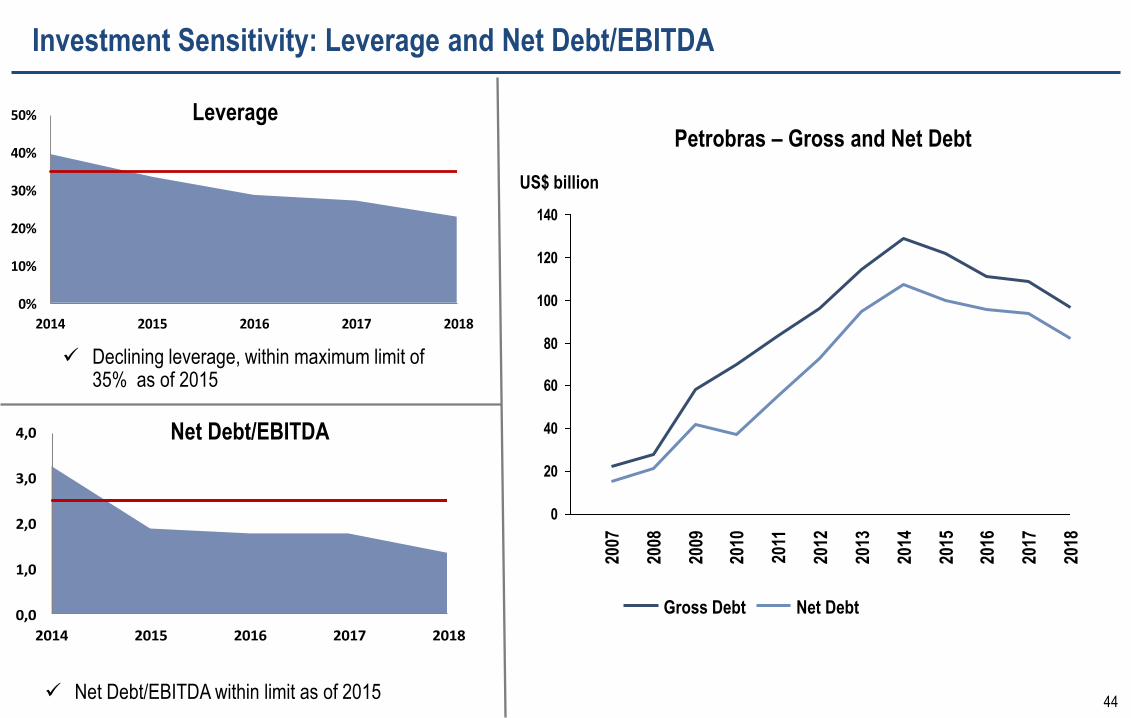

Investment and FX Rate Sensitivity: Leverage and Net Debt/EBITDA

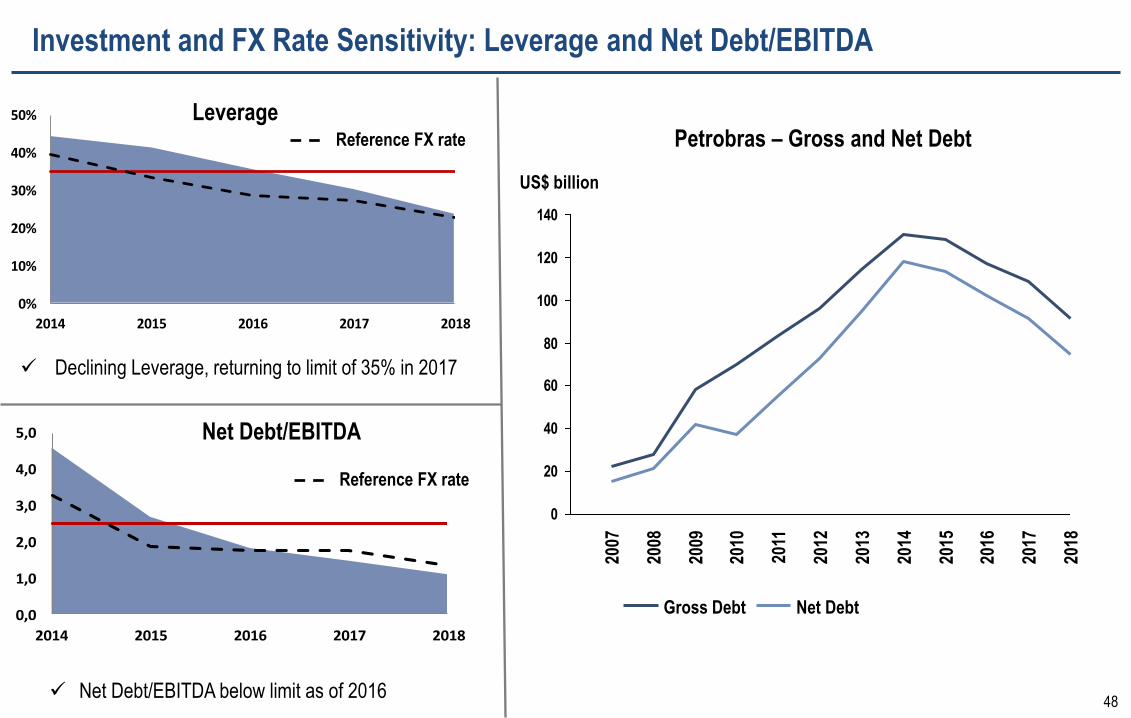

Leverage

Net Debt/EBITDA

0

20

40

60

80

100

120

140

2018

2009

2008

2007

2016

2017

2015

2014

2013

2012

2011

2010

Gross Debt Net Debt

US$ billion

Petrobras – Gross and Net Debt

Declining Leverage, returning to limit of 35% in 2017

Net Debt/EBITDA below limit as of 2016

0%

10%

20%

30%

40%

50%

2014 2015 2016 2017 2018

0,0

1,0

2,0

3,0

4,0

5,0

2014 2015 2016 2017 2018

Reference FX rate

Reference FX rate

49

2014 – 2018

Business and Management Plan

The End