Embed Size (px)

Citation preview

Press conference

26 February 2015

Annual figures 2014

Annual figures 2014Wiebe Draijer, Chairman of the Executive Board

Annual figures 2014 – analysisBert Bruggink, CFRO

Balance sheet

In billions of euros 31-Dec-14 31-Dec-13 31-Dec-14 31-Dec-13

Cash and cash Due to

equivalents 43 43 customers 326 326

Loans to customers 462 456 Debt securities in issue 189 195

Financial assets 48 57 Due to other banks 18 15

Due from other Derivative financial instruments

banks 45 41 and other trade liabilities 68 50

Derivative financial instruments 56 40 Other liabilities 41 44

Other assets 27 32 Equity 39 39

Total assets 681 669 Total liabilities 681 669

Lending

420

425

430

435

440

31-Dec-13 Private individuals TIS Food and agri 31-Dec-14

Private sector loan portfolio in billions of euros

Loan portfolio EUR 430 billion; -1%• Declines at local Rabobanks, Obvion and FGH Bank• Increases at Wholesale, Rural & Retail and DLL, partly due to currency effects

-3% -3% +6%

Funding (1)Amounts due to customers and liquidity ratios

300305310315320325330

31-Dec-13 Savings Other 31-Dec-14

Amounts due to customers, in billions of euros

-6% +5%

Amounts due to customers EUR 326 billion; 0%• Customer savings deposits EUR 143 billion; -6%• Loan-to-deposit ratio of 1.33 (1.35)• Liquidity coverage ratio; LCR 144% (126%)• Net stable funding ratio; NSFR 115% (114%)

Funding (2)Liquidity buffer at a comfortable level

In billions of euros 31-Dec-14 31-Dec-13 ChangeDomestic retail banking 209 216 -7Wholesale and international retail banking 116 109 +7Other entities 1 2 -1

Amounts due to customers 326 326 0

Wholesale funding 216 219 -3

Liquidity buffer (HQLA) 80 84 -4

Equity

In billions of eurosEquity as at 31-Dec-13 38.5

Net profit +1.8Payments on certificates, hybrid capital and other non-controlling interests -1.2

Reserve capacity +0.6Issued Rabobank Certificates +0.1Repayment of Capital Securities and Trust Preferred Securities -1.3Foreign currency translation reserves +0.5Other changes +0.5Equity as at 31-Dec-14 38.9

CapitalStrategy

10.7% 10.0% 10.8% 12.2%

2.8% 2.8% 2.8% 2.8%3.1% 2.5% 2.4%3.5%3.2% 3.5%

5.3%3.5%4.0%

0%

4%

8%

12%

16%

20%

24%

28%

31-dec-13 1-Jan-14(CRD IV)

31-Dec-14(CRD IV)

Target 2016 TLAC

In percent of RWA

CET1 excluding certificates Rabobank CertificatesAdditional tier 1 Tier 2Subordinated debt

• Target capital ratio >20%; 2014: 21.3%

• Target CET1 ratio 14%; 2014: 13.6%

Development of capital ratiosImprovement of ratios in 2014

0

4

8

12

16

20

24

2005 2006 2007 2008 2009 2010 2011 2012 2013 1-Jan-14(CRD IV)

31-Dec-14(CRD IV)

Capital ratios in percent

Common equity tier 1 ratio Tier 1 ratio Capital ratio

Financial resultsRabobank Group

In millions of euros 31-Dec-14 31-Dec-13 ChangeInterest 9,118 9,095Commission 1,879 2,001 -6%Other results 1,860 1,934 -4%Total income 12,857 13,030 -1%Operating expenses 8,055 9,760 -17%Bad debt costs 2,633 2,643Bank tax expense and resolution levy 488 197Operating profit before taxation 1,681 430Taxation -161 88Net profit from continued operations 1,842 342Net profit from discontinued operations - 1,665Net profit 1,842 2,007 -8%

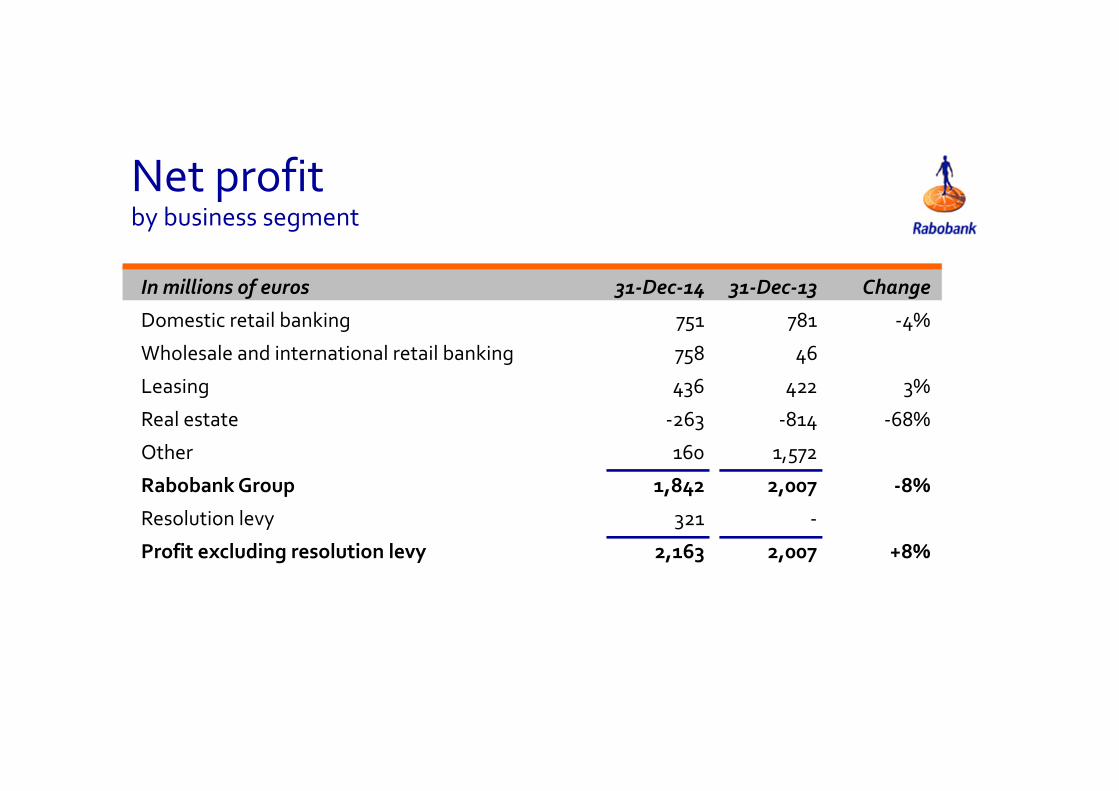

Net profit by business segment

In millions of euros 31-Dec-14 31-Dec-13 Change

Domestic retail banking 751 781 -4%

Wholesale and international retail banking 758 46

Leasing 436 422 3%

Real estate -263 -814 -68%

Other 160 1,572

Rabobank Group 1,842 2,007 -8%

Resolution levy 321 -

Profit excluding resolution levy 2,163 2,007 +8%

Operating expensesSharp fall in operating expenses (-17%)

0100020003000400050006000700080009000

10000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

In millions of euros

• Efficiency ratio up 12.2 percentage points to 62.7%• Operating expenses at domestic retail banking down EUR 353 million on 2013• Settlement for the Libor affair recognised in the operating expenses of wholesale and

international retail in 2013

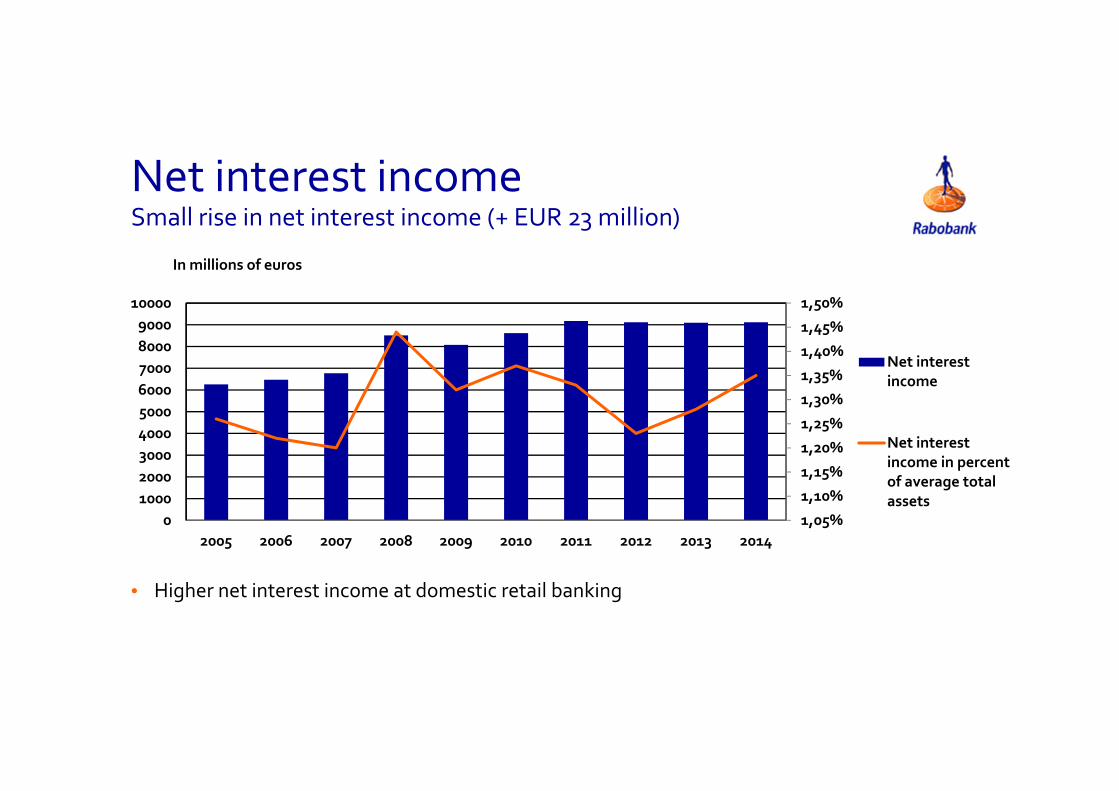

Net interest incomeSmall rise in net interest income (+ EUR 23 million)

1,05%

1,10%

1,15%

1,20%

1,25%

1,30%

1,35%

1,40%

1,45%

1,50%

0100020003000400050006000700080009000

10000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

In millions of euros

Net interestincome

Net interestincome in percentof average totalassets

• Higher net interest income at domestic retail banking

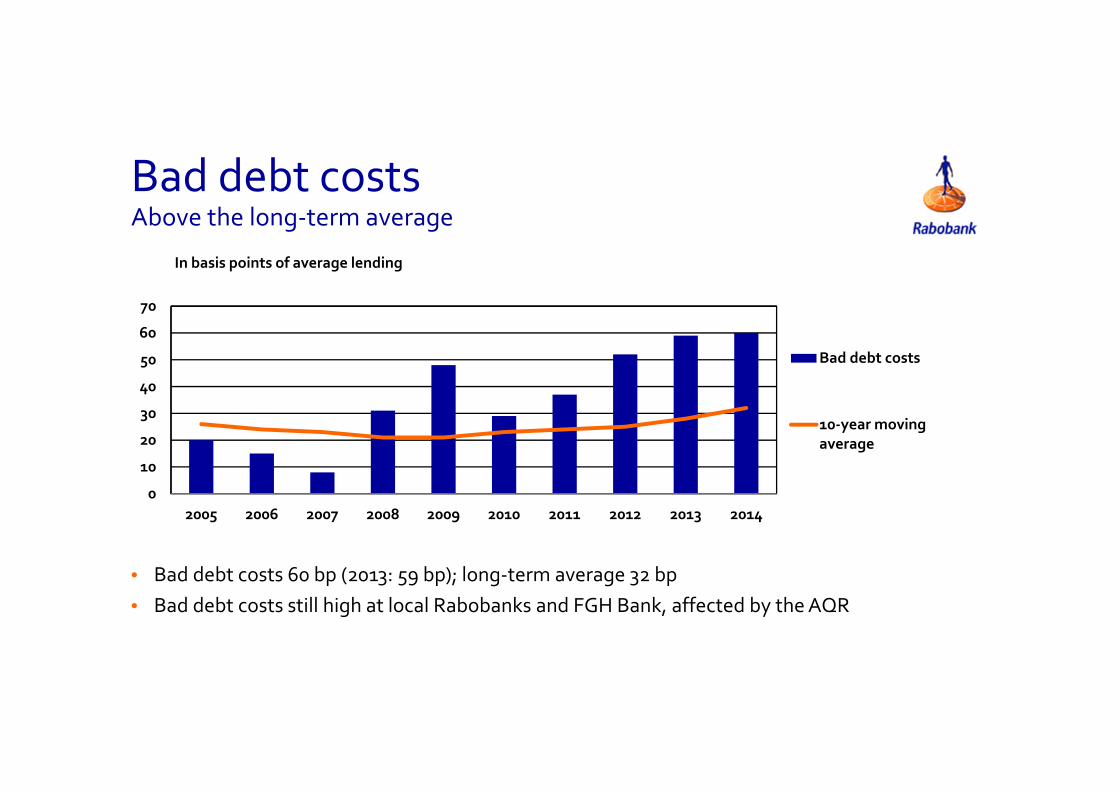

Bad debt costsAbove the long-term average

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

In basis points of average lending

Bad debt costs

10-year movingaverage

• Bad debt costs 60 bp (2013: 59 bp); long-term average 32 bp• Bad debt costs still high at local Rabobanks and FGH Bank, affected by the AQR

Residential mortgages in the Netherlands48% of lending; 5% of bad debt costs

31-Dec-14

31-Dec-13

Residential mortgages in billions of euros

31-Dec-14

31-Dec-13

Bad debt costs in millions of euros

Residential mortgages EUR 205.0 (209.1) billion• Contraction due to additional repayments• 21% (20%) portfolio financed with NHG

mortgage guarantee scheme• Loan-to-value 78% (81)%

• Bad debt costs residential mortgages EUR 112 million; -12%

• Bad debt costs at 5 (6) basis points

209.1

127

112

205.0

Commercial real estate in the NetherlandsWrite-downs versus bad debt costs

0

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014

In millions of euros

Bad debt costs Write-downs

Domestic retail bankingNet profit EUR 751 million; -4%

31-Dec-14

31-Dec-13

Net profit in millions of euros

31-Dec-14

31-Dec-13

In billions of euros

Amounts due to customers Loan portfolio

• Result of domestic retail banking impacted by EUR 274 million resolution levy

781

215.7303.1

209.1290.5

751

• Loan portfolio EUR 290.5 billion; -4%• Amounts due to customers EUR 209.1 billion;

-3%

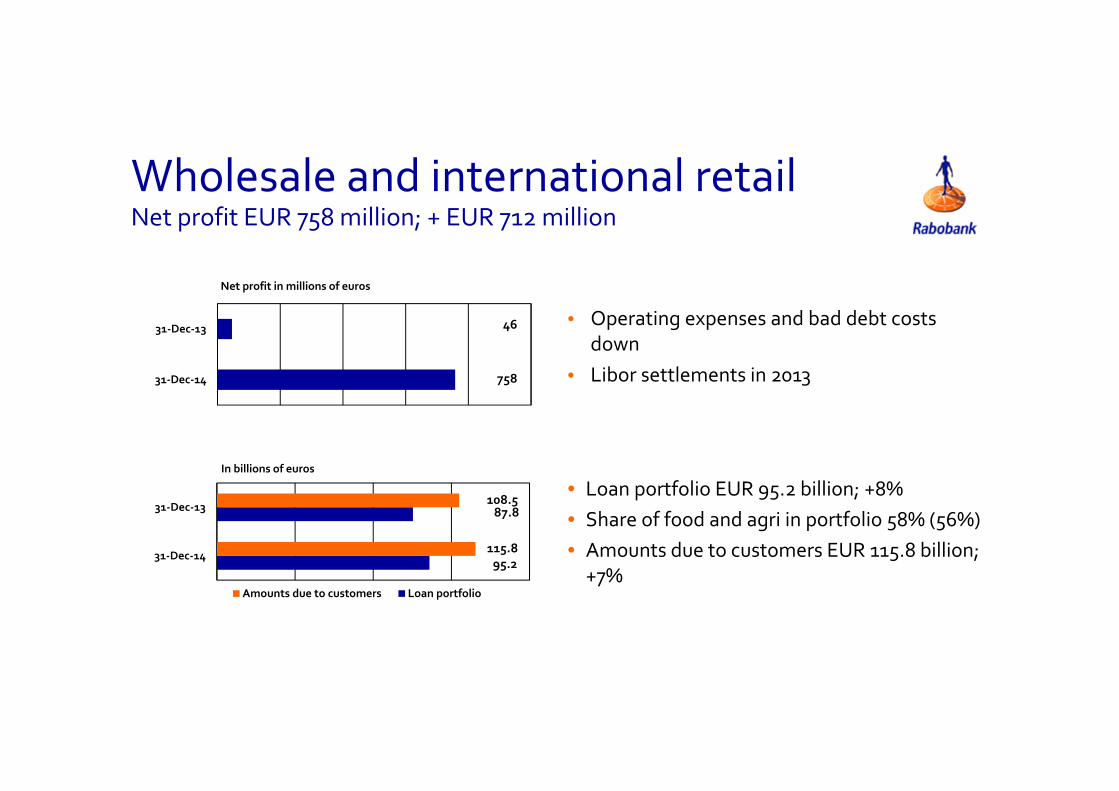

Wholesale and international retail Net profit EUR 758 million; + EUR 712 million

31-Dec-14

31-Dec-13

Net profit in millions of euros

31-Dec-14

31-Dec-13

In billions of euros

Amounts due to customers Loan portfolio

• Operating expenses and bad debt costs down

• Libor settlements in 2013

46

758

108.587.8

115.895.2

• Loan portfolio EUR 95.2 billion; +8%• Share of food and agri in portfolio 58% (56%)• Amounts due to customers EUR 115.8 billion;

+7%

LeasingNet profit EUR 436 million; +3%

31-Dec-14

31-Dec-13

Net profit in millions of euros

31-Dec-14

31-Dec-13

Lease portfolio in billions of euros

• Interest profit up• Bad debt costs down

422

436

30.2

33.0

• Lease portfolio EUR 33.0 billion; +9%• Share of food and agri in portfolio 32% (30%)

Real EstateNet loss of EUR 263 million

31-Dec-14

31-Dec-13

Net loss in millions of euros• No heavy impairments on land positions and

operations, unlike 2013 • Bad debt costs still high in 2014

-814

-263

7341

17200

8982

1780031-Dec-14

31-Dec-13

Loan portfolio in billions of euros

• Number of homes sold 7,064; +37%• Loan portfolio EUR 16.7 billion; -9%• Assets under management EUR 6.4 billion;

+8%

18.4

16.7

22

Thank you for your attention

Annual figures 2014Annual figures 2014