Embed Size (px)

Citation preview

INVESTOR PRESENTATION - MARCH 2017

A PRIVATE EXPLORATION AND DEVELOPMENT COMPANY CU – AU ASSETS IN THE HEART OF EUROPE

Open Pit at Mala

NEW CYPRUS COPPER CORPORATION

Cautionary Note Regarding Forward-Looking Information This presentation includes certain statements that may be deemed "forward-looking statements". Forward-looking information is generally identifiable by use of the words “believes,” “may,” “plans,” “will,” “anticipates,” “intends,” “budgets”, “could”, “estimates”, “expects”, “forecasts”, “projects” and similar expressions, and the negative of such expressions. Forward-looking information in this presentation includes statements about the formation, terms and future activities at the Company’s property. All statements in this presentation, other than statements of historical facts, that address permitting, exploration drilling, exploitation activities and events or developments that the company expects are forward-looking statements. N C C has made numerous assumptions, while NCC considers these assumptions to be reasonable, these assumptions are inherently subject to significant uncertainties and contingencies. Although NCC believes the expectations expressed in the forward-looking statements herein contained to based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Additionally, there are known and unknown risk factors which could cause NCC’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information contained herein. A more complete discussion of the risks and uncertainties facing NCC is disclosed in NCC's continuous disclosure filings with regulatory authorities. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continuity of mineralization, potential environmental issues and liabilities associated with exploration, development and mining activities, uncertainties related to the ability to obtain necessary permits, licenses and title and delays due to third party opposition, changes in government policies regarding mining and natural resource exploration and exploitation, continued availability of capital and financing, and general economic, market or business conditions. In addition, NCC has yet to acquire the Treasure Project and only has an option to do so. NCC may elect to not exercise the option or may not have sufficient capital to do so. Furthermore, further exploration and development of the property may not occur as expected. All forward-looking information herein is qualified in its entirety by this cautionary statement, and NCC disclaims any obligation to revise or update any such forward-looking information or to publicly announce the result of any revisions to any of the forward-looking information contained herein to reflect future results, events or developments, except as required by law. All figures are in Euros (EUR) unless otherwise indicated.

This Presentation may include information referring to the potential range of the quantity and grade of minerals (including copper and gold) the potential range of quantity and grade is conceptual in nature and relates only to the exploration targets, there has been insufficient exploration to define a mineral resource and it is uncertain if further exploration will result in the targets being delineated as a mineral resource and or mineral reserve. The reader is specifically advised that any references to ranges of minerals are not classified as mineral resources nor mineral reserves and that the data referenced herein is based on certain exploration data available to the Company but which was not necessarily obtained by the Company directly and therefore represents information from third parties. The potential tonnages and grades are conceptual in nature and are based on previous drill results that defined the approximate length, thickness, depth and grade of the portion of the estimate. There has been insufficient exploration to define a current resource and the Company cautions that there is a risk further exploration will not result in the delineation of a current resource. Any disclosures, inferences, extrapolations, references to the NCC Property being analogous to other properties, and similar references contained herein are estimates only and may not be supported by future results. Many statements are preliminary in nature and may include inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the preliminary assessment will be realized. No feasibility study (as that term is defined by NI 43-101) has been carried out.

NCC undertakes no obligation to update or advise in the event of any change, addition, or alteration to the information catered in this presentation including such forward-looking statements. This presentation does not constitute an offer of the securities described herein.

Technical Information: The scientific and technical data contained in this Presentation pertaining to the Treasure Project was reviewed by H. Andrew Daniels, P. Geol a non-independent qualified person to NCC who is responsible for ensuring that the geologic information provided in this Presentation is accurate and acts as a “qualified person” under National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”).

SAFE HARBOUR

2

3

NCC INVESTMENT CASE

Rare opportunity across an entire package of polymetallic Cu-Au (plus Ni, Zn and Ag) brownfield projects in Europe

• Large, highly prospective landholding covering abandoned mines and historic prospects in Greek Cyprus (EU) (~37.8 km²);

• Copper + Gold + Nickel (plus Zinc and Silver credits). • Targeting near-term JORC / NI43-101 Resources at brownfields sites:

• Access to recently granted Kslavassos Mining District with unmined reserves and resources still in-situ at 7 historical mines;

• Building further on recent drilling success at Mala and other prospects: – Drilling at Mala returned high-grade copper-gold-zinc-silver in volcanogenic massive sulphides; – Drilling at Pevkos discovered high-grade nickel-copper-gold. NCC is now a first mover for a potential

new nickel province; – Potential to bring Kalavassos and Mala to production within a 24-36 month timeframe;

• Excellent discovery potential for more high-grade copper-gold deposits; • Application of modern exploration methods and geology understanding in underexplored

historic mining areas. • Internal preliminary economic assessment suggest a low CAPEX and low OPEX type

scenario with high returns even in the current metal price environment.

4

NCC CORPORATE STRATEGY

Investment Proposition: Restart of historic mines in Europe

• Company strategy is to develop resources around existing historic mines that were shut down during the 1974 Turkish invasion that were never exhausted.

• These mines closed due to the war with reserves still in the ground and no modern exploration has been carried out on them in the period since.

• NCC has acquired licenses over 13 of these historical mines in Southern (Greek) Cyprus.

• Our priority target is the “Kalavassos” copper-gold project. • Second priority is the “Mala” mine where NCC can quickly define a resource based on existing drilling

and potentially on a historic “waste” dump. • Overall NCC’s exploration target (which is based on historical drilling and reserves) is

35 million tonnes. This includes: • 20Mt at >1.5% Cu + 1.5 g/t Au at Kalavassos. This is the total target across the 13 historical mines

being Platies, Mavri Sykia, Landaria, Mavridhia, Mousoulos and Petra, plus the Kalavassos mines. • 10-15Mt at >1.0% Cu and 1.0 g/t Au at the other projects. This includes the Mala mine, where NCC

expects at least 5Mt. Drilling around the old pit at Mala has delivered significant grades within wide intersections and NCC aims to deliver a JORC resource of ~1Mt at Mala over the next 12 months by evaluating an unprocessed Cu-Au mine waste dump and between the existing pit wall and already completed RC drilling.

5

NCC MANAGEMENT TEAM

MR. H. ANDREW DANIELS, P. GEO, MANAGING DIRECTOR Annual pay €47.500 cash, €47,500 deferred (post-listing or shares) Over 30-years of experience in capital markets, international mining and exploration geology including management and

supervisory experience at senior levels in open pit and underground mines, major drilling and evaluation programs. Extensive mining finance experience including 3.5 years with Deutsche Bank AG in the Global Commodities Group (culminating as

Director, Global Mining Finance). Extensive experience working with and consulting to industry leading organizations including Western Mining Corp. (Nickel

Division) (10 years), Kilborn SNC – Lavalin (2 years), Minorco Services BV / Anglo American plc. (6 years). Extensive senior management and executive experience as both Officer and Director of public companies including; Exploration

Director – Mountain Lake Resources, VP Exploration – Chariot Resources, VP Exploration – Riverside Resources, VP Geology – Century Mining, COO Morro Bay Resources, CEO Resource Intelligence Inc, and Head Global Banking – Palisades Global

DR. PIERRE RICHARD, EXECUTIVE DIRECTOR Annual pay €23.750 cash, €23,750 deferred (post-listing or shares) Over 15-years of experience in finance, law and management and has spent the last 9-years as a mining executive across

exploration, mining, minerals processing and sales of ores and concentrates. Management and control experience as General Manager of nickel exploration and development for Dutch consortium Espero

Mining & Trading UA in Albania. Project director for design, construction and commissioning of a lead-zinc flotation plant and associated mine expansion in Turkey

for Meskan Olmez Madencilik / Anatolian Resources. Management of off-take financing and sales contracts. Founding Chairman of ASX-listed company exploring Chile for Au-Cu-Ag. Establishing and implementing public company

corporate governance systems and establishing company strategy.

MR. DOMINIC J. MAJENDIE, LEGAL AND FINANCE ADVISER Paid €450 cash and €450 deferred remuneration per day of consultancy Over 25 years of experience in finance, law and marketing at an executive level in high growth technology, telecommunications,

mining and manufacturing companies in Europe, North America and the Middle East. Senior legal counsel negotiating and managing iron, complex ore and gold projects in Eastern Europe, with acquisition analysis of

mining projects in Europe, the Middle East and Asia. Has experience listing and managing public and private companies, including accelerated filers and Cypriot entities. Has started

and grown several businesses with extensive experience in start ups, business restructuring and strategic planning.

6

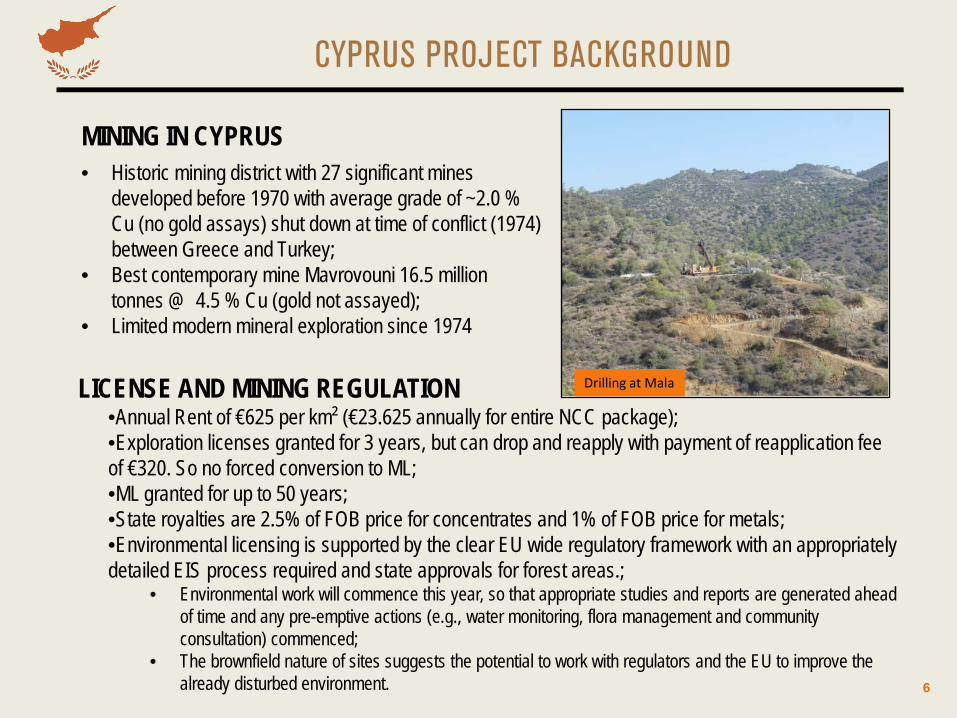

CYPRUS PROJECT BACKGROUND

LICENSE AND MINING REGULATION •Annual Rent of €625 per km² (€23.625 annually for entire NCC package); •Exploration licenses granted for 3 years, but can drop and reapply with payment of reapplication fee of €320. So no forced conversion to ML; •ML granted for up to 50 years; •State royalties are 2.5% of FOB price for concentrates and 1% of FOB price for metals; •Environmental licensing is supported by the clear EU wide regulatory framework with an appropriately detailed EIS process required and state approvals for forest areas.;

• Environmental work will commence this year, so that appropriate studies and reports are generated ahead of time and any pre-emptive actions (e.g., water monitoring, flora management and community consultation) commenced;

• The brownfield nature of sites suggests the potential to work with regulators and the EU to improve the already disturbed environment.

Drilling at Mala

MINING IN CYPRUS • Historic mining district with 27 significant mines

developed before 1970 with average grade of ~2.0 % Cu (no gold assays) shut down at time of conflict (1974) between Greece and Turkey;

• Best contemporary mine Mavrovouni 16.5 million tonnes @ 4.5 % Cu (gold not assayed);

• Limited modern mineral exploration since 1974

7

NCC TENEMENT LOCATIONS

NCC PROJECT OVERVIEW

JORC

Res

ource

PROD

UCTI

ON

MALA

KOKKINOCHOMA

MATHIATAS

MOUSOULOS MAVRIDHIA

PETRA

PLATIES

MAVRI SYKIA

LANDARIA

KOKKINOKREMMOS

VASA KOKKINA LAONA

XYLOMASHERKA

ADVANCED

KALAVASSOS Cu-Au-Ag

VRECHIA Cu-Au-Zn-Ag

KAMBIA Cu-Au

LAXIA

PEVKOS PETROMOUTTI

MAZOKAMBOS BLACK PINE Ni-Cu-Co-Au

KALAVASSOS

Key Red Text Historical Reserve Yellow Text Prospect Modern Drilling

8

Historical Drilling at Kalavassos: 456 Historic Holes

52,287 metres drilled

Partial Data in possession of NCC. Further compilation

required

Historical Drilling at Mala: 45 Historic Holes (Noranda)

1,985 metres drilled

Partial Data in possession of NCC. Further compilation

required

9

KALAVASSOS

• Two exploration licences covering all historic Kalavassos Copper mines; • 13 massive sulphide bodies discovered and mined between 1937-77; • Recorded production included 4.62 million tonnes at >1.0% Cu; • Remnant massive sulphide recorded at 2.28 million tonnes in one previous mine (no specified

grade, non-JORC);

• No gold or silver values provided for mined massive sulphide;

• Historic mining of 61,450 tonnes of oxide zone produced 16,490 oz Au (8.3 g/t), and 34,740 oz Ag (17.7 g/t);

• Review of historic data underway to upgrade mapping systems and produce geological model.

KALAVASSOS PROJECT

KALAVASSOS – REMNANT RESERVES AND RESOURCES

Mine Years of operation

Mining method

Ore mined (tonnes)

Cu % S % Residual reserves (t)

Kalavassos 1937-1956 Undergr. 1,910,000 1.0-2.5 33 UNDEFINED Mousoulos 1964-1976 Undergr. 1,660,000 1.0-2.5 40 940,000 Mavridhia 1971-1977 Open cut 400,000 1.5 30-40 200,000 Petra 1953-1957 Undergr. 226,000 1.0-2.5 25-46 300,000 Landaria 1963-1964 Undergr. 65,000 0.5 35-46 250,000 Mavri Sykia 1 1954-1962 Undergr. 269,000 1.5-2.5 30-46 UNDEFINED Mavri Sykia 2 1970-1977 Open cut 107,000 1.5-2.5 30-46 590,000 Platies 1955-1958 Glory hole 43,900 2.5-3.0 46 UNDEFINED

Mined: 4.62 Mt @ 1.0-3.0 % Cu, including 0.82 Mt @ >1.5 % Cu Residual: 2.03 Mt @ 1.0-2.5 % Cu, including 0.79 Mt @ >1.5 Cu and as yet UNDEFINED residual reserves at Kalavassos, Mavri Sykia 1 and Platies. Gold: 61,450 tonnes of gossan mined from 1937-1943 to produce 16,400 oz gold (8.3 g/t Au) and 34,746 oz silver (17.6 g/t Ag). No gold assays are available for the Cu-rich sulphide ore.

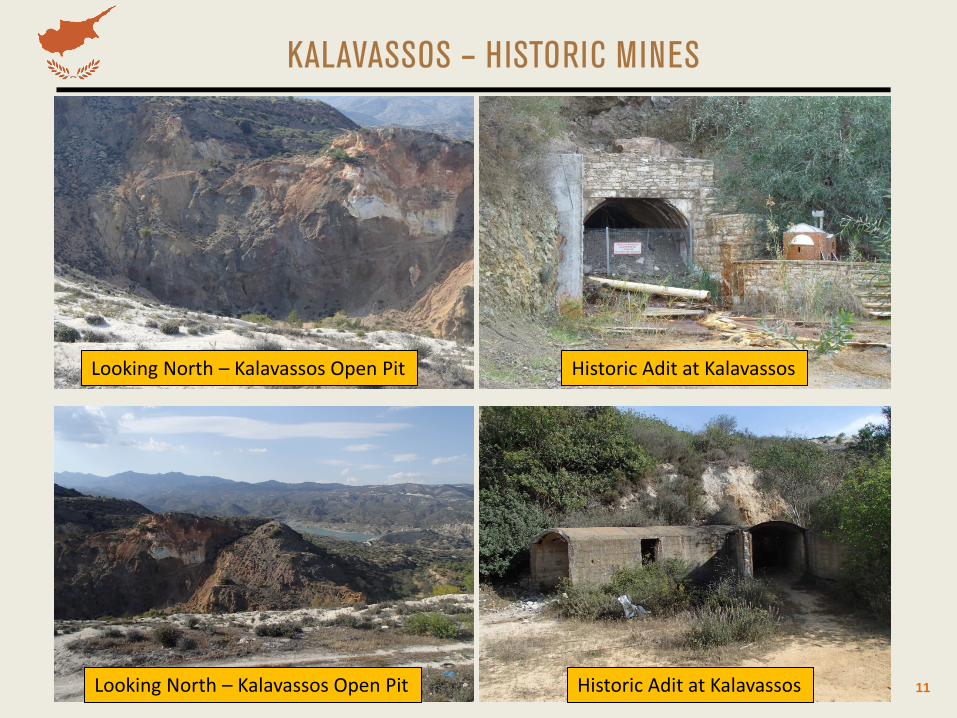

KALAVASSOS – HISTORIC MINES

Looking North – Kalavassos Open Pit Historic Adit at Kalavassos

Looking North – Kalavassos Open Pit Historic Adit at Kalavassos 11

KALAVASSOS – MINES AND INFRASTRUCTURE

Historic Crusher Station and Rail Load Out Looking North – Kalavassos Open Pit

Vasiliko Port Facilities near Kalavassos Vasiliko Port Facilities near Kalavassos 12

13

MALA - VRECHIA

• Licence covering Mala mine and surrounding gossans; • 45 historical holes drilled by Noranda in 1976; • Targeting high-grade Cu-Au-Zn in volcanic-hosted massive sulphide units;

• Modern (2014) drilling confirmed high-grade Au with Cu-Zn;

• Open along strike with many gossans adjacent;

• Nearby gossans and prospective geology indicates large sulphide system with scope for expansion.

MALA PROJECT

14

MALA - VRECHIA

MALA DRILLING 2014 • 13 RC holes completed for 1,092

m; • “BLACK SMOKER” zones returns

high-grade Au-Cu-Zn-Ag; • Thick intervals of moderate grade

also intersected; • Relatively flat-lying, near surface; • Mineralisation open along strike in

various directions;

HIGH-GRADE “BLACK SMOKER” ZONES • 6m at 3.70 g/t Au, 0.41% Cu, 4.10% Zn, 11.3 g/t Ag from 46 m (MALRC007) • 5 m at 2.15 g/t Au, 0.23% Cu, 1.80% Zn, 5.1 g/t Ag from 37 m (MALRC004) • 4 m at 1.46 g/t Au, 0.43% Cu, 2.13% Zn, 9.2 g/t Ag from 54 m (MALRC003) • 3 m at 0.76 g/t Au, 1.30% Cu, 1.48% Zn, 2.3 g/t Ag from 37 m (MALRC002) • 2 m at 2.16 g/t Au, 0.37% Cu, 1.92% Zn, 17.8 g/t Ag from 21 m (MALRC011)

15

MALA - VRECHIA

MALA DRILLING 2014 VERY HIGH-GRADE “BLACK SMOKER” ZONE

• 1 metre at 15.5 g/t Au, 0.65% Cu, 12.3% Zn, 42 g/t Ag from 48 m (MALRC007)

BROAD MODERATE GRADE ZONES

• 25 metres at 1.23 g/t Au, 0.34% Cu, 1.16% Zn, 4.2 g/t Ag from 46 m (MALRC007)

• 39 metres at 0.59 g/t Au, 0.39% Cu, 0.30% Zn, 1.3 g/t Ag from 33 m (MALRC004)

• “BLACK SMOKER” zone open to north and northeast;

• Sulphide-altered volcanics open in all directions;

• Gossan outcrops cover >600 x 1000 metres indicating large prospective mineralising system.

16

MALA - VRECHIA

MALA - PATHWAY TO RESOURCE INSITU – OPEN PITTABLE

• Two sections drilled north of pit sufficient to outline potential inferred resources;

WASTE DUMP

• Rough volume estimate suggests up to 500,000 tonnes of material south of the Mala open pit in waste dump;

• Material was removed in late 1980’s when Mala was developed solely for the high grade pyrite that capped the Cu-Au mineralisation;

• Opportunity to cost effectively drill the waste dump to test Cu-Au potential;

• Potential to obtain EU assistance to “clean up” the Mala waste dump and rehabilitate;

• Test work on dense media and gravity separation may allow upgrading of already mined and crushed material.

Waste Dump Location South

Photo taken from middle of dump pickup for scale

17

KAMBIA

• Two licences covering historic mines and potential extensions;

• Production of pyrite and copper with historic gold and silver production recorded. Name Operation Cu (%) S (%) Tonnes Produced Operation Period Mathiatas Surface 0.2 30-35 2,100,000 1965-1984 Kapedes (Kokkinochoma) Surface UNKNOWN 30-35 54,666 1955-1958

KAMBIA PROJECT

18

BLACK PINE (PEVKOS AND LAXIA)

• First mover for these Ni - Cu Sulphide deposits in a potential new nickel sulphide province;

• Four known prospects identified;

• Limited modern exploration;

• Ni-Cu sulphide deposits are globally significant.

BLACK PINE – PEVKOS PROJECT • Magmatic Ni-Cu sulphides possibly overprinted with Cu-Au VMS mineralisation;

• High-grade Ni-Cu sulphides found near contact between ultramafic complex and dolerite intrusions;

• Drilling at Pevkos and Laxia in 2014 confirmed this mineralisation and presence of a significant Co-Au component;

19

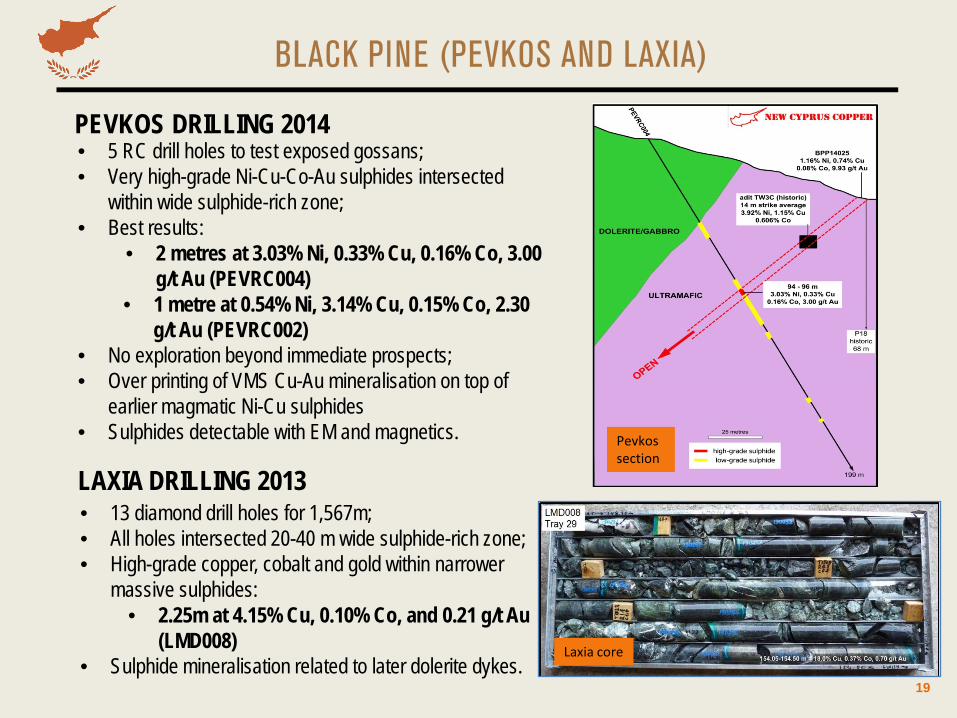

BLACK PINE (PEVKOS AND LAXIA)

• 5 RC drill holes to test exposed gossans; • Very high-grade Ni-Cu-Co-Au sulphides intersected

within wide sulphide-rich zone; • Best results:

• 2 metres at 3.03% Ni, 0.33% Cu, 0.16% Co, 3.00 g/t Au (PEVRC004)

• 1 metre at 0.54% Ni, 3.14% Cu, 0.15% Co, 2.30 g/t Au (PEVRC002)

• No exploration beyond immediate prospects; • Over printing of VMS Cu-Au mineralisation on top of

earlier magmatic Ni-Cu sulphides • Sulphides detectable with EM and magnetics.

PEVKOS DRILLING 2014

• 13 diamond drill holes for 1,567m; • All holes intersected 20-40 m wide sulphide-rich zone; • High-grade copper, cobalt and gold within narrower

massive sulphides: • 2.25m at 4.15% Cu, 0.10% Co, and 0.21 g/t Au

(LMD008) • Sulphide mineralisation related to later dolerite dykes.

LAXIA DRILLING 2013

Laxia core

Pevkos section

COMPARISON OF NCC PROJECTS AND HISTORICAL MINES

20

Source: EMED Mining 2015

21

NCC PROJECT RIGHTS

PROJECT RIGHTS • NCC has a majority 70% holding of the shares of Treasure Development Ltd (TDL) which has 100%

ownership of all licenses. Minority 30% shareholder is ASX-listed company BMG Limited; • NCC will move to 90% shareholding on completion of a 2-year exploration plan (content to be put

forward by NCC, but planned to contain a small resource definition target of ~1Mt); • NCC will gain final 10% of TDL through payment of AUD2m to BMG either as:

• a one-off lump-sum within 12 months of moving to 90%, or • a 1% NSR (NSR ends when total of AUD2m has been paid).

Mala Waste Dump – Showing Thickness Massive Sulphide Mineralisation - Mala

22

THE EUROPEAN COPPER MARKET • Good local demand: Europe a negative copper

balance – with 18% of global smelting, 19% of fabrication, but only 10% of mining (ICSG, 2014).

• Positive logistics: Nearby producers include Atlantic Copper in Spain (284,000t Cu cathode), Aurubis Bulgaria (230,000tpa Cu cathode) – each needing around 1.2Mt Cu concentrate per annum (source: the companies, 2015 figures)*.

• Good value capture: Typical Cu concentrate pricing (source: trading house offer received in Sept. 2016)

• Cu 95% payable (with min deduction 1%), • Au 90% payable (min deduction 1 g/t) • less T/C $110/t and R/C $0.11/lb payable copper

COPPER FLOTATION • Technology over 100 years old and implemented all

over the world (no technical risk) • Low capex $13m for 300,000tpa plant (source:

regional supplier quote) which will deliver high metal payables

EUROPEAN COPPER PRODUCTION ECONOMICS

* See: http://bulgaria.aurubis.com/our-business/raw-materials/, http://bulgaria.aurubis.com/about-us/ and http://www.atlantic-copper.es/en/production-process/the-metallurgical-complex

23

› Update Cu-Au-Zn targets at Mala › Integrate Kalavassos archival material into database and develop

drill plan for Kalavassos › Drill targets across all projects › DEFINE JORC / 43-101 - COMPLIANT RESOURCE AT MALA

NEAR TERM (0 – 12 months)

MEDIUM TERM (12 - 24 months)

STRENGTHS

› Further drilling to upgrade resources › DEFINE JORC / 43-101 - COMPLIANT RESOURCE AT KALAVASSOS › Metallurgical testwork and marketing studies including export options › Pre-Feasibility Studies › Review contractor and off-take agreements

LONGER TERM (24 - 48 months)

› Establish full mining operation with expansion capability › Build 300,000tpa Cu-Au flotation plant (capex ~$13m) near Kalavassos › Further resource exploration to support plant expansion/upgrades › Ship concentrate to access export market

› High-grade sulphide targets and large technical database › Strong gold, nickel and cobalt credits indicated › Anticipated low cost, highly profitable operations › Well-established infrastructure within close proximity › Experienced mining personnel in surrounding regions › Experienced and cost effective management

NCC CORPORATE TIMELINE

24

NCC CAPITAL STRUCTURE AND STAGED BUDGET

CAPITAL STRUCTURE • New Cyprus Copper Corporation (NCC) 100% privately held and Cyprus registered; • 10M shares issued (20M authourised) – 50% each to two principal owners; • Initial SEED funding raised via Convertible Notes:

• 77,000 Euros raised at 0.075 euro cents • Note coupon of 8% pa maturing March 31, 2018 • No forced conversion and currently non dilutive

• NCC owns 70% of Treasure Development Ltd. (TDL) the local operating Company purchased in the acquisition arrangement. TDL holds Cyprus licenses and employs local staff.

STAGED BUDGET • Total Budget over 2 year = €3M Euros • Immediate Term – €350,000 Euros:

• Timeframe 6 months; • Compile extensive database that was part of acquisition and build proper GIS database; • Drill Mala waste dump to evaluate Cu-Au potential; • Estimate 43-101 / JORC Resource at Mala – waste dump and insitu; • Detailed Kalvassos geology and targetting; • Pevkos mineralogy research; • Baseline environmental data collection; • Project rents, field vehicle, NCC management and general G and A..

NCC CAPITAL STRUCTURE AND STAGED BUDGET (2)

IMMEDIATE TERM USE OF FUNDS – LINE ITEMS • Total Budget over 2 year = €3M Euros • Immediate Term – €350,000 Euros (6 months estimated)

1. Data Compilation – Kalavassos and Mala (Consultant): €25,000 2. Mala waste dump drilling (inc assays and QAQC): €50,000 3. Mala Resource estimation (Consultant): €30,000 4. Kalvassos detailed geology and drill targeting (Consultant): €40,000 5. Mala dense media and garvity separation test work. €20,000 6. Baseline environmental data collection (Consultant): €35,000 7. Permitting Study – assess mining, environmental and social (Consultant): €20,000 8. Pevkos Mineralogy (University of Western Ontario): €5,000 9. Field vehicle upgrade: €20,000 10. Project rents and fees: €15,000 11. TDL operating expenses: €15,000 12. Broker and finance advisory fees €25,000 13. NCC Management and corporate fees (accounting, legal, management): €60,000 Total Immediate Term (6 month) Budget and Use of Proceeds: €350,000

Cost Effective, High Value Project Exploration and Development Work 25

26

NCC CAPITAL STRUCTURE AND STAGED BUDGET (3)

STAGED BUDGET • Total Budget over 2 year = €3M Euros (continued) • Medium Term – €1,000,000 Euros (estimated)

• Timeframe 7 – 13 months; • Airborne VTEM survey over all TDL Licenses; • Drill KALAVASSOS to confirm historic resource indications; • Environmental data collection; • Project rents, geological and environmental consultant and general G and A.

• Long Term – €1,650,000 Euros (estimated) • Timeframe 14 – 24 months; • Continue drilling at Kalavassos and additional drilling at Mala; • Land acquisition – as defined in the airborne survey if warranted; • Further metallurgical testwork on Mala and Kalavassos; • Environmental Impact Assessment (EIA); • Scoping / Prefeasibility Study at Kalavassos and/or Mala; • Project rents, geological, environmental, metallurgical and mining consultant and general G and

A.

RESULT AT END OF 24 MONTHS – PLANT CONSTRUCTION AND PRODUCTION DECISION PLUS OWNERSHIP INCREASE TO 90%

27

NCC INVESTMENT CASE SUMMARY

› Multiple high-grade Cu+Ni+Au (+Zn+Co+Ag) prospects › Historic copper mining province in Cyprus › Application of modern exploration › Low capex cash generating development economics › Potential to upgrade Cu-Au tailings for processing

HIGH QUALITY PROJECT PORTFOLIO

NEAR TERM VALUE CATALYSTS

PATHWAY TO DEVELOPMENT

› Build on recent drilling success (Pevkos, Mala) › Access to Kalavassos mining area › Extensive technical database › Multiple high-potential targets › Short term JORC / 43-101 Resource Potential at Mala

› Targeting high quality resource base › Low cost operation potential › Robust nearby infrastructure › Politically stable jurisdiction with low “country” risk

MARCH 2017

CONTACT: H. ANDREW DANIELS, P. GEO – MANAGING DIRECTOR DR. PIERRE RICHARD – EXECUTIVE DIRECTOR EMAILS: [email protected] [email protected] PHONE: +1 902 792 0877 +44 777 546 4567

Confidential

NEW CYPRUS COPPER CORPORATION