Embed Size (px)

Citation preview

Barry Allan 416.860.7612 [email protected]

Ryan Hanley 416.860.8337

June 27, 2014

KLONDEX MINES LTD. – BUY

On A Dark Desert Highway, High Grade In The Air EVENT– KDX Hosts Site Visit To Midas And Fire Creek

Klondex hosted a site visit the week of June 23rd, highlighting the recently acquired Midas mine and mill, as well as the growth at Fire Creek. Although we did not come back with much new information, we did get an increased sense of confidence in both assets.

IMPACT – Positive. Midas Working Well, Further Exploration Potential At Fire Creek

Midas in good form: The 1,200tpd Midas mill (Figure 1), which was acquired at the beginning of the year from Newmont for $83mm, appears to have been well taken care of with only ~50% of the capacity currently being utilized (~400tpd from the Midas mine with the balance from Fire Creek). Although throughput is expected to increase in late 2015 and 2016 once Fire Creek is permitted for full production, we still anticipate that there will be ~200tpd of extra room which will likely be used for toll milling.

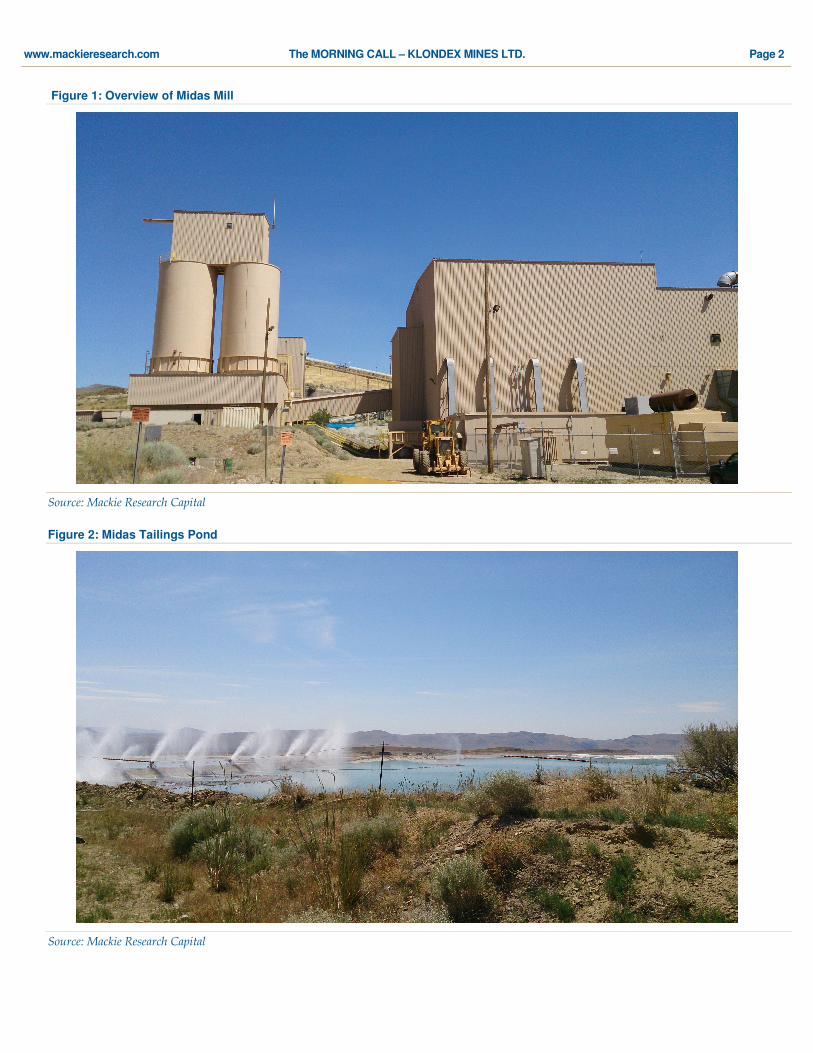

As for the Midas mine, grades continue to reconcile positively (+30% Au & +65% Ag), with the implementation of new mining methods having reduced dilution by 50% (down to 100%–150% vs. 250% previously). Items which remain of concern include the continued risks associated with the implementation of new mining methods. We also continue to focus on the amount of water in the tailings pond (Figure 2) and remaining tailings capacity. Although there is still under three years of capacity at the current mining rate, the concern remains around a decision as to how to proceed with tailings expansion (BLM land vs. private land) and the associated permitting requirements and timelines.

Fire Creek exploration continues: Approximately 100 miles to the south at Fire Creek, bulk sample grades continue to average ~1oz/t (expected average of ~29g/t over 2014), while development begins to approach the recently discovered Karen vein which was not included in the last resource or recent PEA. Further upside is expected to not only come from the Karen vein, on which more data is to be provided over 2H/14, but also as a result of processing halo material (mineralization around the veins) which varies in grade from 5 to 10g/t, but that was excluded in the PEA (calculated as dilution with 0 grade).

ACTION – Maintain BUY. An Emerging High-Grade Producer

Our NAV remains largely unchanged, declining slightly to $3.12 from $3.25. KDX continues to trade at ~0.6x on a P/NAV basis vs. junior peers which average over 0.9x. Upcoming catalysts include updated resource estimates in Q4/14, as well as continued exploration results (ongoing) and full permitting for Fire Creek (expected mid-2015).

Corporate Profile

Klondex Mines Ltd. is headquartered in Elko, Nevada. The company is listed on the TSX under the KDX and on the OTC under the ticker KLNDF. Klondex is currently exploring the 100%-owned Fire Creek deposit in a well-known area of Nevada.

Upcoming Events

Updated Resource Estimate (Q4/14) Fire Creek Permitting (mid-2015)

This report has been created by analysts who are employed by Mackie Research Capital Corporation, a Canadian Investment Dealer. For further disclosures, please see last page of this report.

KDX - TSX $1.97

TARGET: $3.25

PROJ. RETURN: 65%

VALUATION: 1.0x NAVPS

Share Data

Basic Shares O/S (mm) 111.3

Fully Diluted 137.8

Market Cap ($mm) 219.3

NAVPS $3.08

Dividend $0.00

Yield 0.0%

Next Reporting Date September-2014

$1.00

$1.50

$2.00

Jul-13 Oct-13 Feb-14 Jun-14

Q1/14A Q2/14E Q3/14E Q4/14E 2014E Q1/15E Q2/15E Q3/15E Q4/15E 2015E 2016E

Production 000 oz Au Eq 16.1 30.5 28.4 26.9 101.9 28.1 28.1 26.9 32.9 116.0 155.0

Cash Costs US$/oz $906 $386 $415 $439 $537 $435 $435 $427 $421 $424 $723

EPS $/sh ($0.02) $0.15 $0.12 $0.11 $0.36 $0.12 $0.12 $0.14 $0.17 $0.31 $0.85

P/EPS Multiple n/a n/a n/a n/a 5.5x n/a n/a n/a n/a 6.4x 2.3x

CFPS $/sh ($0.03) $0.17 $0.14 $0.13 $0.41 $0.14 $0.14 $0.18 $0.22 $0.40 $1.13

P/CFPS Multiple n/a n/a n/a n/a 4.8x n/a n/a n/a n/a 4.9x 1.7x

www.mackieresearch.com The MORNING CALL – KLONDEX MINES LTD. Page 2

Figure 1: Overview of Midas Mill

Source: Mackie Research Capital

Figure 2: Midas Tailings Pond

Source: Mackie Research Capital

www.mackieresearch.com The MORNING CALL – KLONDEX MINES LTD. Page 3

RISKS TO TARGET

Key risks are typical of mineral exploration companies. These include exploration and operational success, the ability to raise capital, favourable metal prices, and permitting/regulatory risk.

RELEVANT DISCLOSURES APPLICABLE TO: KLONDEX MINES LTD.

1. Within the last 3 years, Mackie Research Capital Corporation has managed or co-managed an offering of securities by the subject issuer.

2. Within the last 3 years, Mackie Research Capital Corporation has received compensation for investment banking and related services from the subject issuer.

3. In June 2011 Ryan Hanley visited the Fire Creek mine in Nevada. Transportation and accommodation was paid for by Klondex Mines Ltd.

4. In June 2014 Ryan Hanley visited the Midas mine in Nevada. Partial accommodation was paid for by Klondex Mines Ltd.

ANALYST CERTIFICATION

Each analyst of Mackie Research Capital Corporation whose name appears in this report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no part of the research analyst’s compensation was or will be directly or indirectly related to the specific conclusions or recommendations expressed in this research report.

In fo rmat ion about Mackie Research Cap i ta l Corpora t ion ’s Rat ing System, the d ist r ibu t ion o f our research to c l ien ts and the percentage o f recommendat ions wh ich are in each o f our ra t ing categor ies is ava i lab le on our web si te a t www.mackieresearch .com.

The in fo rmat ion conta ined in th is report has been drawn f rom sources be l ieved to be re l iab le bu t i ts accuracy or comple teness is no t guaranteed, nor in p rovid ing i t does Mackie Research Capi ta l Corpora t ion assume any responsib i l i ty o r l iab i l i ty . Mackie Research Cap i ta l Corpora t ion , i ts d i rectors, o f f icers and o ther employees may, f rom t ime to t ime, have posi t ions in the secur i t ies ment ioned here in . Contents o f th is report cannot be reproduced in who le or in par t w i thout the express permission of Mackie Research Cap i ta l Corpora t ion . US Inst i tu t iona l C l ien ts - Mackie Research USA Inc. , a who l ly owned subsid ia ry o f Mackie Research Cap i ta l Corpora t ion , accepts responsib i l i ty fo r the contents o f th is report sub ject to the te rms and l imi ta t ions se t ou t above. US f i rms or inst i tu t ions rece iv ing th is report shou ld e f fect t ransact ions in securi t ies d iscussed in the report th rough Mackie Research USA Inc. , a Broker-Dea ler reg iste red wi th the F inancia l Industry Regu latory Author i ty (F INRA).

Member-Canad ian Investor Pro tect ion Fund / membre-fonds canad ien de pro tect ion des épargnants

Toronto 416.860.7600 - Montreal 514.399.1500 - Vancouver 604.662.1800 - Calgary 403.218.6375 - Regina 306.566.7550 - St. Albert 780.460.6460