Embed Size (px)

Citation preview

Annual Accounts Press Conference Wuppertal, 26 June 2014

1.Business model

2. Portfolio development and M&A

3. Financial year 2013/2014

4. Financial year 2014/2015

5. The GESCO share

Overview

2

GESCO – an industrial group shaped by SMEs with market and technology leaders

Tool manufacturing/mechanical engineering and plastics technology segments

Currently 17 operating subsidiaries under the GESCO AG umbrella

We think and act sustainably and in an entrepreneurial manner.

We are active in established industries with innovative technologies.

We provide technology “Made in Germany” to the world’s markets.

GESCO consists of flexible, independently operating and managed units that benefit from belonging to a strong group.

1. The business model

3

1. The business model

The GESCO AG investment philosophy Acquisition and development of industrial SMEs Long-term orientation, no intent to exit Majority takeover, usually 100 % Usually as part of succession planning New managers hold a share of up to 20 % in their companies

(“entrepreneurial companies”)

4

2. Portfolio development

MAE strengthens position in US by acquiring local competitor

MAE: international market leader for automatic straightening machines and wheel presses

Eitel is the US market leader for straightening machines Founded in 1973 Sales: around € 10 million Around 50 employees Export ratio: around 20 %

(Canada, Mexico, South America) Transition of expertise in both

directions Eitel expands range of products

and services, addresses new target groups

Positive synergy effects in the medium term

5

2. Portfolio development

Setter takes over smaller competitor Papersticks UK

Papersticks produces paper sticks for

sweets and hygiene articles, focus on UK and South Africa

Sales volume: around € 1 million p.a.

Acquisition of key assets in April 2014

Production to take place in future in Germany using more modern Setter machines

Niche shakeout

6

Current M&A situation Fewer offers, possibly because …many industrial companies recorded declines in

incoming orders, sales and earnings in 2013 not an ideal basis for approaching investors

…business owners wonder what to do with the money in a zero-interest environment

Increasing competition, e.g. from family offices

Two projects currently about to enter into due diligence A direct acquisition by GESCO AG A strategic enhancement of a subsidiary abroad

2. M&A

7

3. Financial year 2013/2014

Financial year 2013/2014:

Not an easy year

Massive strategic investments US acquisition at MAE

8

3. Financial year 2013/2014

German GDP in 2013: +0.4 %

VDMA reports drop (-1.7 %), GKV growth (+3 %)

GESCO Group: Sales unchanged organically, growing inorganically Order intake fell organically, compensated for by inorganic development

Why did margins fall?

Earnings quality generally poorer Processes less efficient due to customers placing orders at short

notice and hesitantly Some pronounced weaknesses in countries/sectors (China weak;

massive reluctance to invest, esp. at major automotive suppliers; semiconductors and photovoltaics weak)

On top: technical problems with two large orders, due diligence costs higher than expected

9

3. Financial year 2013/2014

Massive strategic investments A total of € 28 million in property, plant and equipment

as well as intangible assets (planned: € 30 million)

Focus: companies with concrete growth potential Dörrenberg Edelstahl GmbH (including new plant in Dieringhausen for the

expansion of capacities and the product spectrum) MAE Maschinen- und Apparatebau Götzen GmbH (new assembly hall) AstroPlast Kunststofftechnik GmbH & Co. KG

(property in Meschede, logistics and production building)

10

3. Financial year 2013/2014

Keep in mind:

GESCO AG and GESCO Group financial year = 1 April to 31 March

Subsidiaries’ financial year = calendar year

Financial statement 2013/2014 encompasses calendar year 2013 in operating terms

11

3. 2013/2014: GESCO Group key figures

2012/2013

2013/2014

Change

Incoming orders €‘million 439.4 435.6 -0.9 %

Group sales €‘million 440.4 453.3 2.9 %

Group EBITDA €‘million 51.8 48.7 -5.9 %

Group EBIT €‘million 37.3 32.0 -14.3 % Earnings before tax €‘million 33.8 29.0 -14.2 % Income taxes €‘million -11.1 -9.3 -16.5 % Earnings after tax €‘million 22.7 19.8 -13.1 % Group net income for the year (after minority interest)

€‘million 20.9 18.1 -13.4 %

Earnings per share acc. to IFRS

€ 6.30 5.45 -13.4 %

Cash flow €‘million 36.2 36.6 1.2 % Employees No. 2,292 2.360 3.0 %

12

50

100

150

200

250

300

350

400

31.03.2013 31.03.2014 31.03.2014 31.03.2013

Current liabilities

Non-current liabilities

Equity capital

Liquid assets

Receivables and other assets

Inventories

Non-current assets

Assets Equity and liabilities

In € million

3. 2013/2014 Group balance sheet structure

126

67

37

128

119

81

39

177

89

114

167

83

108

380 380

141

358 358

Equity ratio: 46.5 %

€ 28 million in investments Goodwill: € 12.4 million = 7 % of equity capital

Adequate liquid assets Net liabilities to banks to EBIDTA: 1.2 13

4. Financial year 2014/2015

Financial year 2014/2015:

The economic climate is better. Sales should rise, but earnings will not increase yet because of impact from two key factors

14

4. Financial year 2014/2015

Starting position and expectations

Economic forecasts point to recovery (GDP: +1.9 %, VDMA: production + 3 %, GKV: sales +4 % to 5 %)

Positive signals at GESCO Group since the start of the year Demand from China has recovered

Stop on investments at major automotive suppliers no longer as strict

Situation at the companies particularly affected in 2013/2014 is improving.

Special steel business at Dörrenberg Edelstahl GmbH at an appealing level good sign for the German capital goods industry

Sales at GESCO Group set to rise

Two issues weighing down earnings performance

15

4. Financial year 2014/2015

Issue 1: Protomaster GmbH

Manufactures metal forming tools Produces body parts and assemblies for small and medium-scale

series using these tools Niche position, few comparable suppliers Dramatic rise in call-off orders for several ongoing (major) orders;

labour shortage and organisational deficits Concrete support by GESCO Group, investments in future development

Issue 2: MAE Maschinen- und Apparatebau Götzen GmbH

International market leader for automatic straightening machines and wheel presses

Growth driven strongly by innovation; sales more than doubled between 2006 and 2013; extensive construction and expansion projects with new administration and production building

Burdens on several fronts due to strong operating growth, construction activities, technical challenges, Eitel acquisition and organisational development, labour bottlenecks

Active support by GESCO AG

16

4. Financial year 2014/2015

Impact of the Ukraine/Russia crisis

Currency devaluation in Russia, Ukraine, Kazakhstan leading to slump in business by German agricultural machinery manufacturers Frank Walz- und Schmiedetechnik GmbH in OEM business, directly impacted

An escalation of the situation would have a significant impact on German industry – which would also have an impact on GESCO Group

This crisis is not yet reflected in the VDMA and GKV forecasts

17

4. Financial year 2014/2015

Q1: incoming orders high and satisfactory, operations still rather weak

Includes operations at subsidiaries between January and March 2014

Incoming orders at around € 126 million (Q1 previous year: € 110.4 million): +14 %

Sales at around € 109 million (Q1 previous year: € 108.9 million)

Resulting in a book-to-bill ratio of > 1

Earnings weighed down significantly by the two “issues” in particular

Order backlog at the end of Q1: around € 205 million

18

4. Financial year 2014/2015

Sales and incoming orders by quarter (in €'000)

─ Incoming orders ─ Sales 19

20.000

40.000

60.000

80.000

100.000

120.000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2009 2010 2011 2012 2013 2014

4. Financial year 2014/2015

Additional strategic investments A total of €30 million in property, plant and equipment planned

Major growth investments:

Frank Walz- und Schmiedetechnik GmbH: new hall and forged-parts production line for new product group

Werkzeugbau Laichingen-Gruppe: construction of new hall, new press Protomaster GmbH: capacity expansion, expansion of manufacturing

technology

Most of these growth investments won’t be completed before the end of 2014.

20

4. Financial year 2014/2015

2013/2014 Actual figures

2014/2015e

Target

Change

Group sales € million 453.3 470 to 480 +3.7 % to +5.9 %

Group net income for the year after minority interest

€ million 18.1 17.5 to 18.5 -3.3 % to +2.2 %

Earnings per share acc. to IFRS

€ 5.45 5.26 to 5.56 -3.3 % to +2.2 %

Target figures

21

Conclusion: 2014/2015 to bring a certain recovery to business

The two “issues” are weighing down earnings

Appropriate countermeasures have been taken

Keep in mind: the political risks are substantial

(Ukraine/Russia, eurozone, Iraq…)

4. Financial year 2014/2015

22

5. The GESCO share

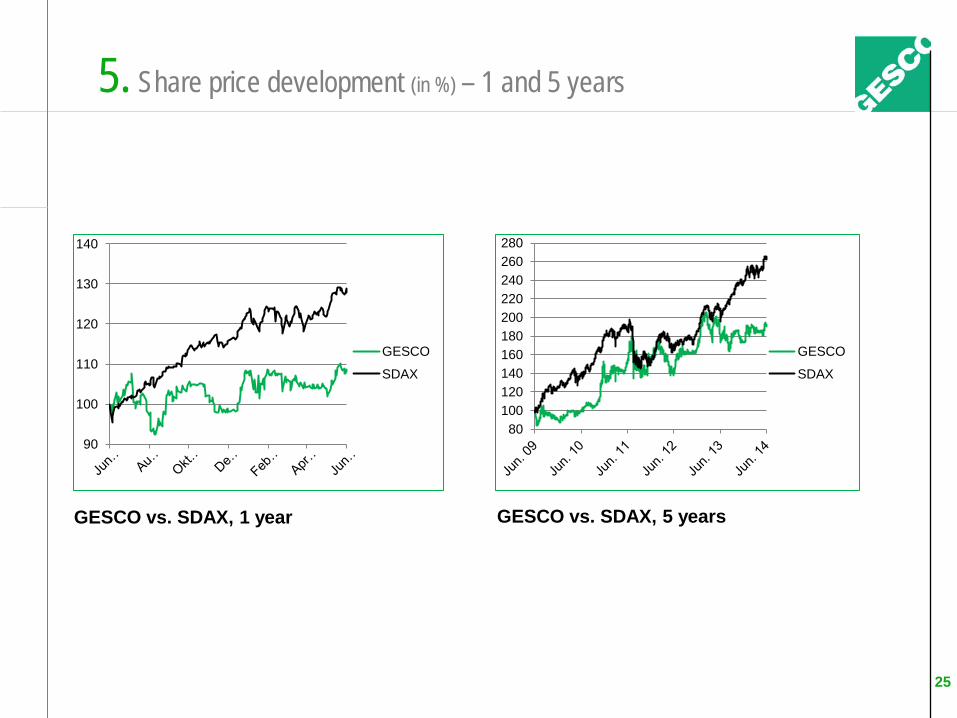

The GESCO share: an underperformer after two years of outperformance

Price performance in financial year 2013/2014:

+0.8 % (SDAX +25.8 %)

Price development in calendar year 2013: +0.4 % (SDAX +27.2 %)

Dividend proposal: € 2.20 per share (previous year: € 2.50) – equivalent to long-term distribution ratio of around 40 % of EPS

23

5. The GESCO share

Freefloat: 86.4 %

Stefan Heimöller, entrepreneur, private investor: 13.6 %

Stefan Heimöller 13.6 %

Private investors ~ 46.4 %

Institutional investors ~ 40 %

Mr Heimöller was elected by the Annual General Meeting on 25 July 2013 to the Supervisory Board as Mr Back’s successor

24

5. Share price development (in %) – 1 and 5 years

GESCO vs. SDAX, 1 year GESCO vs. SDAX, 5 years

90

100

110

120

130

140

GESCO

SDAX

80 100 120 140 160 180 200 220 240 260 280

GESCO

SDAX

25

5. Share price development (in %) – 10 years

GESCO vs. SDAX, 10 years

0

100

200

300

400

500

GESCO

SDAX

26

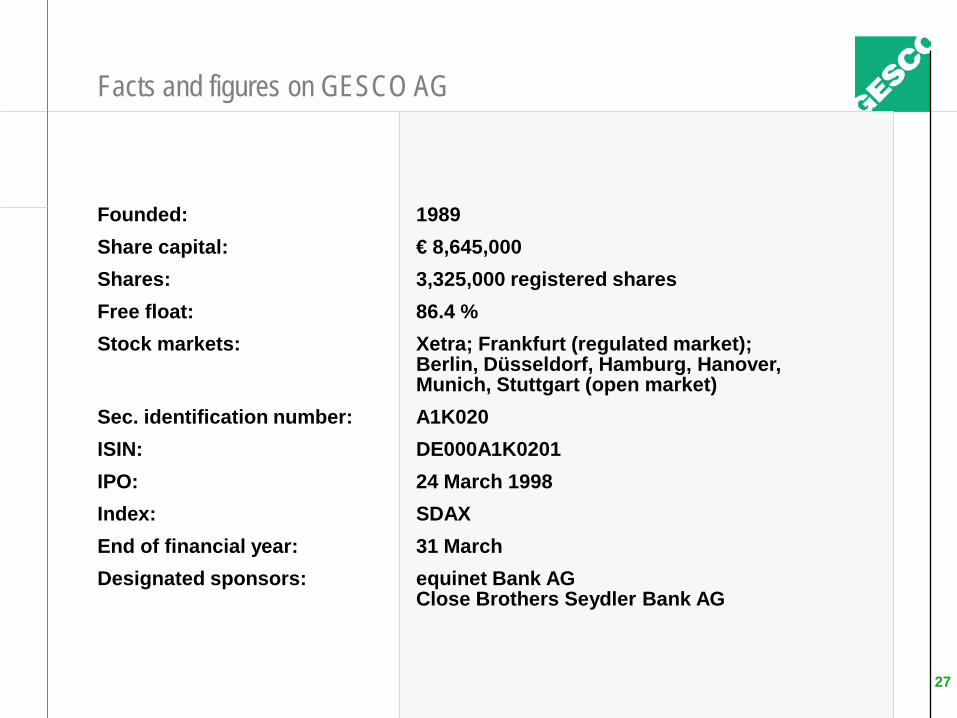

Founded: 1989 Share capital: € 8,645,000 Shares: 3,325,000 registered shares Free float: 86.4 % Stock markets: Xetra; Frankfurt (regulated market); Berlin, Düsseldorf, Hamburg, Hanover, Munich, Stuttgart (open market) Sec. identification number: A1K020 ISIN: DE000A1K0201 IPO: 24 March 1998 Index: SDAX End of financial year: 31 March Designated sponsors: equinet Bank AG Close Brothers Seydler Bank AG

Facts and figures on GESCO AG

27

Financial calendar and investor relations contact

Financial calendar

26 June 2014 Annual Accounts Press Conference and Analysts’ Meeting

15 August 2014 Q1 figures (01.04 to 30.06.2014)

28 August 2014 Annual General Meeting

November 2014 Q2 figures (01.04 to 30.09.2014)

February 2015 Q3 figures (01.04 to 31.12.2014)

25 June 2015 Annual Accounts Press Conference and Analysts’ Meeting

Investor Relations

GESCO AG Phone: +49 202 24820-18 Investor Relations Fax: +49 202 24820-49 Oliver Vollbrecht E-mail: [email protected] Johannisberg 7 Internet: www.gesco.de 42103 Wuppertal

Germany

28

![Database Peraturan [JDIH BPK RI]](https://img.pdfslide.us/doc/110x75/6157dc760b0486657b547613/database-peraturan-jdih-bpk-ri.jpg)