Embed Size (px)

Citation preview

Copperbelt Energy Corporation Plc

Annual earnings presentationfor the year ended 31 December 2014

www.cecinvestor.com

Contents

Page

Sub Saharan power potential 7

The Nigerian opportunity 11

Zambian mining sector growth 12

Group structure 13

Regulatory events 14

Financial results 17

Focus on AEDC 26

Pipeline 32

Outlook 34

www.cecinvestor.com 1

Your presenters

www.cecinvestor.com 2

Owen SilavweManaging Director

Owen was appointed Managing Director for CEC Plc inAugust 2014, having served as Managing Director –Operations (in charge of the Operations Division of thebusiness) since 2013. Prior to his current role, he servedas the Chief Operations Officer for the Company fromMarch 2012. Owen has previously held the position ofCommercial Director responsible for organic businessdevelopment and other commercial aspects of theCompany’s Operations division. Having served invarious positions within CEC, including System PlanningEngineer, Projects Engineer, Projects Manager andBusiness Development Manager, Owen rose throughthe ranks to his current position. He has been one of themain contributors to reforming contractor procurementprocesses in CEC as well as financing andimplementation structures of organic business growth

projects. Owen holds a Bachelor of ElectricalEngineering degree from the University of Zambia anda Master of Science in Power Engineering fromChalmers University in Sweden.

Your presenters

www.cecinvestor.com 3

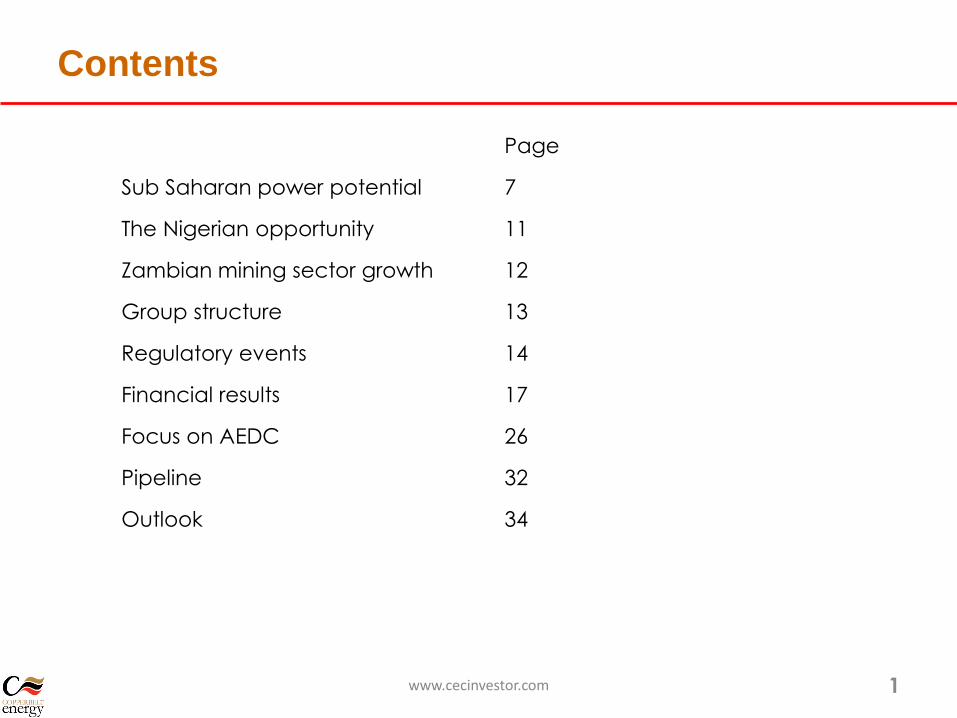

Mutale MukukaChief Financial Officer

Mutale was appointed Group Chief Financial Officer inAugust, 2014. Prior to this appointment, he was the first CFOfor subsidiary CEC Africa and had also served as CEC Africa’s

Regional Head - West Africa, based in Abuja, Nigeria. He ledthe business development and financing transactions foracquisition of equity interest in Abuja Electricity DistributionCompany and North South Power. Other senior positions heheld within the Group include that of Director - CorporateFinance for CEC Plc, Manager Corporate Finance and

Business Planning Head. As CFO, he is responsible for drivingfinancial strategy, financial operations and control as well asoverseeing statutory reporting across several jurisdictions.Mutale has over 14 years of experience covering a numberof industries in project development, corporate finance, taxplanning, project structuring, financial reporting and control.He started his career in audit, and joined CEC Plc in 2003,having previously worked for the Zambia Revenue Authority.He is a qualified UK Chartered Management Accountantand a Fellow of the Zambia Institute of CharteredAccountants.

Statements in this presentation (including all other media) that are not historical facts or

information may be forward-looking statements.

These forward-looking statements are based on information available at the time the

statements are made and/or management's belief as of that time with respect to

future events and involve risks and uncertainties that could cause actual results and

outcomes to be materially different. Important factors that could cause such

differences include, but are not limited to the loss of key customers, the disruption to

operations, economic conditions, political conditions, regulatory issues and reduction in

demand.

Forward looking statements

4

How to access information on CEC

We’re connecting with investors

http://cecinvestor.com/investorconnect-2/

5

How to access pan African power sector news

Pan-African power sector news is published through our Twitter

– follow us!

https://twitter.com/cecinvestor

6

CEC

Sub-Saharan power sector potential

www.cecinvestor.com 7

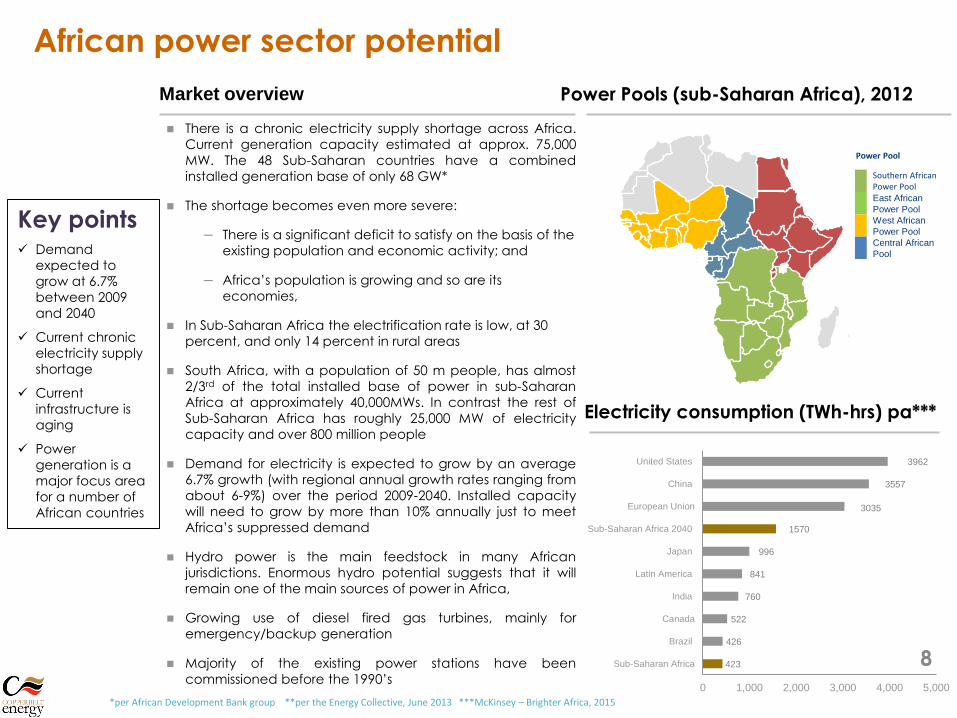

Market overview

There is a chronic electricity supply shortage across Africa.

Current generation capacity estimated at approx. 75,000

MW. The 48 Sub-Saharan countries have a combined

installed generation base of only 68 GW*

The shortage becomes even more severe:

– There is a significant deficit to satisfy on the basis of the

existing population and economic activity; and

– Africa’s population is growing and so are its

economies,

In Sub-Saharan Africa the electrification rate is low, at 30

percent, and only 14 percent in rural areas

South Africa, with a population of 50 m people, has almost

2/3rd of the total installed base of power in sub-Saharan

Africa at approximately 40,000MWs. In contrast the rest of

Sub-Saharan Africa has roughly 25,000 MW of electricity

capacity and over 800 million people

Demand for electricity is expected to grow by an average

6.7% growth (with regional annual growth rates ranging from

about 6-9%) over the period 2009-2040. Installed capacity

will need to grow by more than 10% annually just to meet

Africa’s suppressed demand

Hydro power is the main feedstock in many African

jurisdictions. Enormous hydro potential suggests that it will

remain one of the main sources of power in Africa,

Growing use of diesel fired gas turbines, mainly for

emergency/backup generation

Majority of the existing power stations have been

commissioned before the 1990’s

Power Pools (sub-Saharan Africa), 2012

Power Pool

Southern African Power Pool

East African

Power Pool

West African

Power Pool

Central African

Pool

Key points Demand

expected to

grow at 6.7%

between 2009

and 2040

Current chronic

electricity supply

shortage

Current

infrastructure is

aging

Power

generation is a

major focus area

for a number of

African countries

Electricity consumption (TWh-hrs) pa***

*per African Development Bank group **per the Energy Collective, June 2013 ***McKinsey – Brighter Africa, 2015

423

426

522

760

841

996

1570

3035

3557

3962

0 1,000 2,000 3,000 4,000 5,000

Sub-Saharan Africa

Brazil

Canada

India

Latin America

Japan

Sub-Saharan Africa 2040

European Union

China

United States

African power sector potential

8

Selected sub-Saharan countries and energy highlights

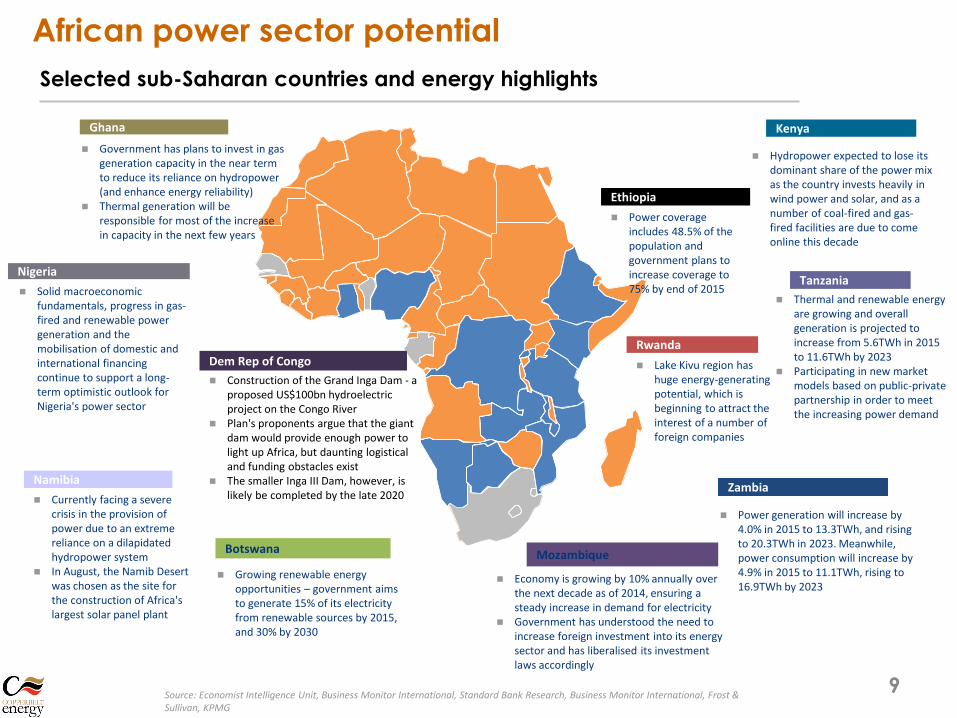

Ethiopia

Power coverage includes 48.5% of the population and government plans to increase coverage to 75% by end of 2015

Ghana

Government has plans to invest in gas generation capacity in the near term to reduce its reliance on hydropower (and enhance energy reliability)

Thermal generation will be responsible for most of the increase in capacity in the next few years

Nigeria

Solid macroeconomic fundamentals, progress in gas-fired and renewable power generation and the mobilisation of domestic and international financing continue to support a long-term optimistic outlook for Nigeria's power sector

Namibia

Currently facing a severe crisis in the provision of power due to an extreme reliance on a dilapidated hydropower system

In August, the Namib Desert was chosen as the site for the construction of Africa's largest solar panel plant

Botswana Mozambique

Economy is growing by 10% annually over the next decade as of 2014, ensuring a steady increase in demand for electricity

Government has understood the need to increase foreign investment into its energy sector and has liberalised its investment laws accordingly

Zambia

Power generation will increase by 4.0% in 2015 to 13.3TWh, and rising to 20.3TWh in 2023. Meanwhile, power consumption will increase by 4.9% in 2015 to 11.1TWh, rising to 16.9TWh by 2023

Tanzania

Thermal and renewable energy are growing and overall generation is projected to increase from 5.6TWh in 2015 to 11.6TWh by 2023

Participating in new market models based on public-private partnership in order to meet the increasing power demand

Kenya

Hydropower expected to lose its dominant share of the power mix as the country invests heavily in wind power and solar, and as a number of coal-fired and gas-fired facilities are due to come online this decade

Growing renewable energy opportunities – government aims to generate 15% of its electricity from renewable sources by 2015, and 30% by 2030

Rwanda

Lake Kivu region has huge energy-generating potential, which is beginning to attract the interest of a number of foreign companies

Source: Economist Intelligence Unit, Business Monitor International, Standard Bank Research, Business Monitor International, Frost & Sullivan, KPMG

Dem Rep of Congo

Construction of the Grand Inga Dam - a proposed US$100bn hydroelectric project on the Congo River

Plan's proponents argue that the giant dam would provide enough power to light up Africa, but daunting logistical and funding obstacles exist

The smaller Inga III Dam, however, is likely be completed by the late 2020

African power sector potential

9

5

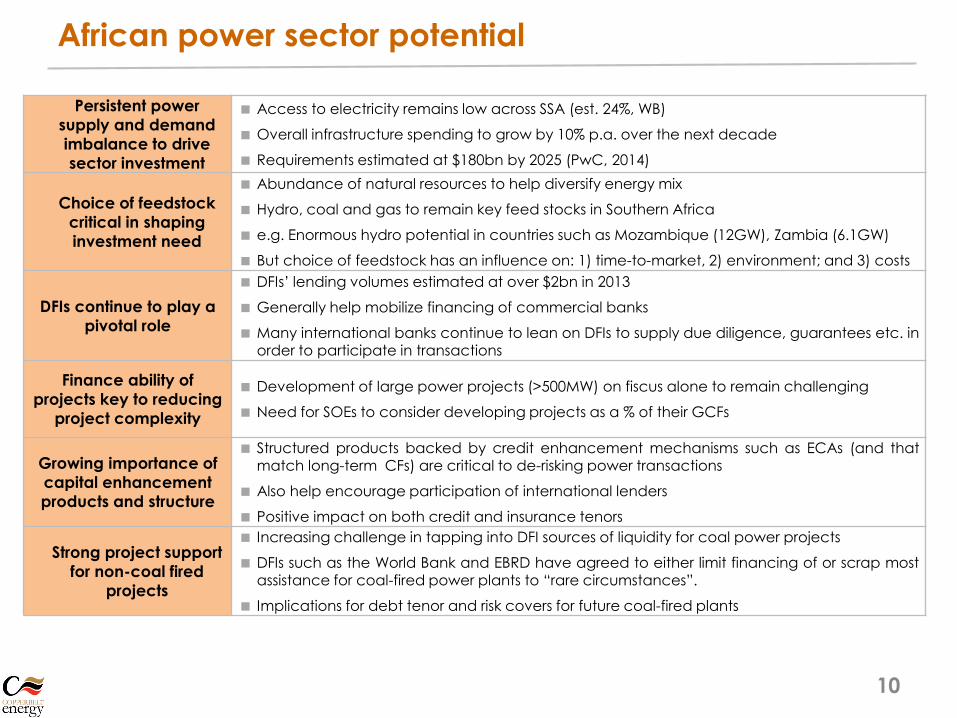

Persistent power

supply and demand

imbalance to drive

sector investment

Access to electricity remains low across SSA (est. 24%, WB)

Overall infrastructure spending to grow by 10% p.a. over the next decade

Requirements estimated at $180bn by 2025 (PwC, 2014)

Choice of feedstock

critical in shaping

investment need

Abundance of natural resources to help diversify energy mix

Hydro, coal and gas to remain key feed stocks in Southern Africa

e.g. Enormous hydro potential in countries such as Mozambique (12GW), Zambia (6.1GW)

But choice of feedstock has an influence on: 1) time-to-market, 2) environment; and 3) costs

DFIs continue to play a

pivotal role

DFIs’ lending volumes estimated at over $2bn in 2013

Generally help mobilize financing of commercial banks

Many international banks continue to lean on DFIs to supply due diligence, guarantees etc. inorder to participate in transactions

Finance ability of

projects key to reducing

project complexity

Development of large power projects (>500MW) on fiscus alone to remain challenging

Need for SOEs to consider developing projects as a % of their GCFs

Growing importance of

capital enhancement

products and structure

Structured products backed by credit enhancement mechanisms such as ECAs (and thatmatch long-term CFs) are critical to de-risking power transactions

Also help encourage participation of international lenders

Positive impact on both credit and insurance tenors

Strong project support

for non-coal fired

projects

Increasing challenge in tapping into DFI sources of liquidity for coal power projects

DFIs such as the World Bank and EBRD have agreed to either limit financing of or scrap mostassistance for coal-fired power plants to “rare circumstances”.

Implications for debt tenor and risk covers for future coal-fired plants

African power sector potential

10

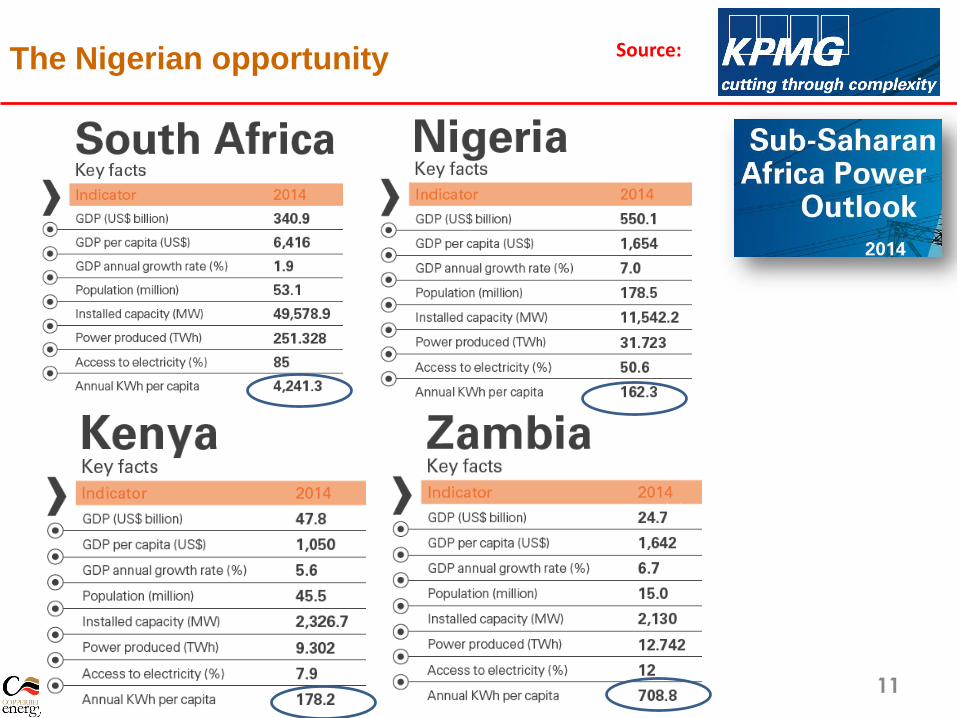

The Nigerian opportunity

11

Source:

Zambian mining sector growth

12

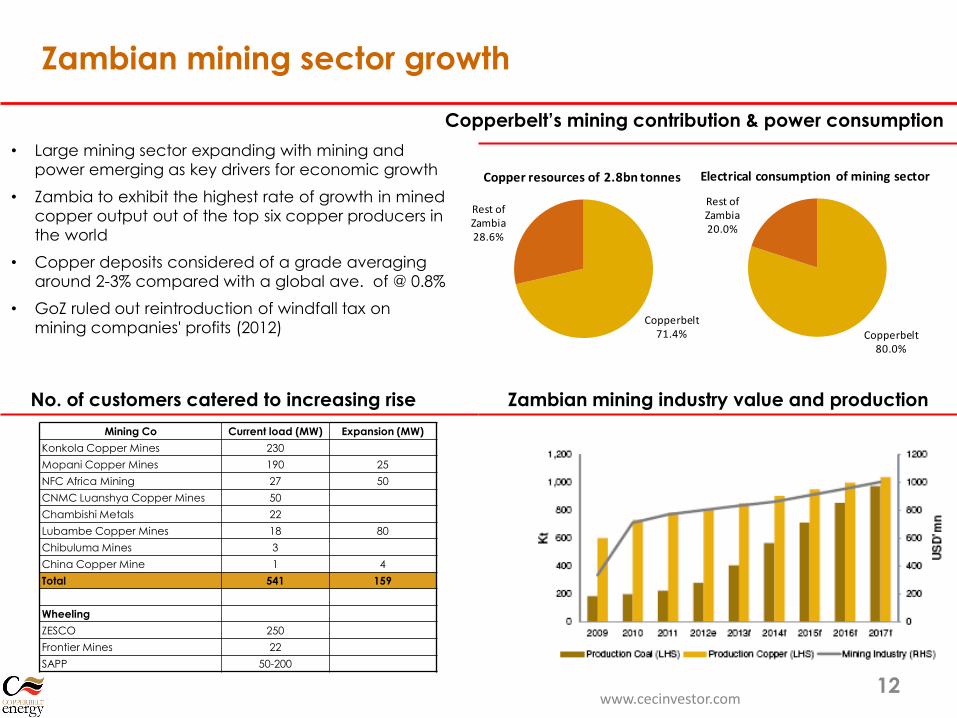

Copperbelt’s mining contribution & power consumption

Zambian mining industry value and production

• Large mining sector expanding with mining and

power emerging as key drivers for economic growth

• Zambia to exhibit the highest rate of growth in mined

copper output out of the top six copper producers in

the world

• Copper deposits considered of a grade averaging

around 2-3% compared with a global ave. of @ 0.8%

• GoZ ruled out reintroduction of windfall tax on

mining companies' profits (2012)

No. of customers catered to increasing rise

Mining Co Current load (MW) Expansion (MW)

Konkola Copper Mines 230

Mopani Copper Mines 190 25

NFC Africa Mining 27 50

CNMC Luanshya Copper Mines 50

Chambishi Metals 22

Lubambe Copper Mines 18 80

Chibuluma Mines 3

China Copper Mine 1 4

Total 541 159

Wheeling

ZESCO 250

Frontier Mines 22

SAPP 50-200

Copperbelt71.4%

Rest of Zambia28.6%

Copper resources of 2.8bn tonnes

Copperbelt80.0%

Rest of Zambia20.0%

Electrical consumption of mining sector

www.cecinvestor.com

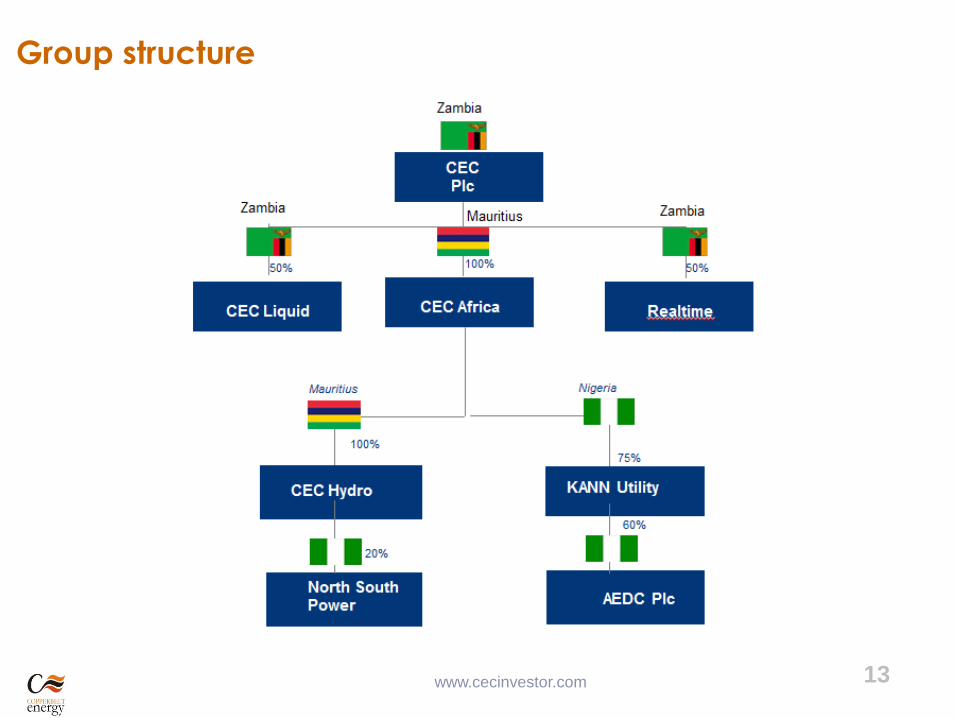

13Group structure

www.cecinvestor.com 13

CEC

Regulatory regime & events

www.cecinvestor.com 14

Regulatory events

Revocation of Statutory Instrument 33 of 2012

• Summary: Zambia’s Finance Ministry revoked Statutory Instruments Number 33 of 2012 (SI 33)

and 55 (SI 55) of 2013 in Mar/14• Provision: Power Supply Agreements and the Bulk Supply Agreement to be denominated in

U$ against ZMW• Effect: Match borrowings to revenue in terms of currency, as U$ adopted as function

currency• Benefit: Low FX risk as revenue and borrowings are denominated in U$

Revised Multi-Year Tariff Order

• Summary: NERC published the revised Multi-Year Tariff Order (MYTO v2.1) in Jan/15• Provision: Increase in tariffs

– Commercial and Industrial customers: Tariffs increase of 27% effective Feb/15

– Domestic customers: Tariffs increase of 59% effective Jul/15

• Benefit: Top-line and bottom-line benefit to AEDC

Commencement of the Transitional Electricity Market (TEM)

• Summary: Interim Rules recognize that electricity tariffs in Nigeria are not yet cost-reflective; TEM to render all commercial contracts as enforceable

• Provision: AEDC currently obligated to pay 65% of the Market Operators bills• Effect: Residual 35% accrued on a monthly basis reflected as losses to be negated after TEM is

enforcedwww.cecinvestor.com 15

Nigerian tariff regime

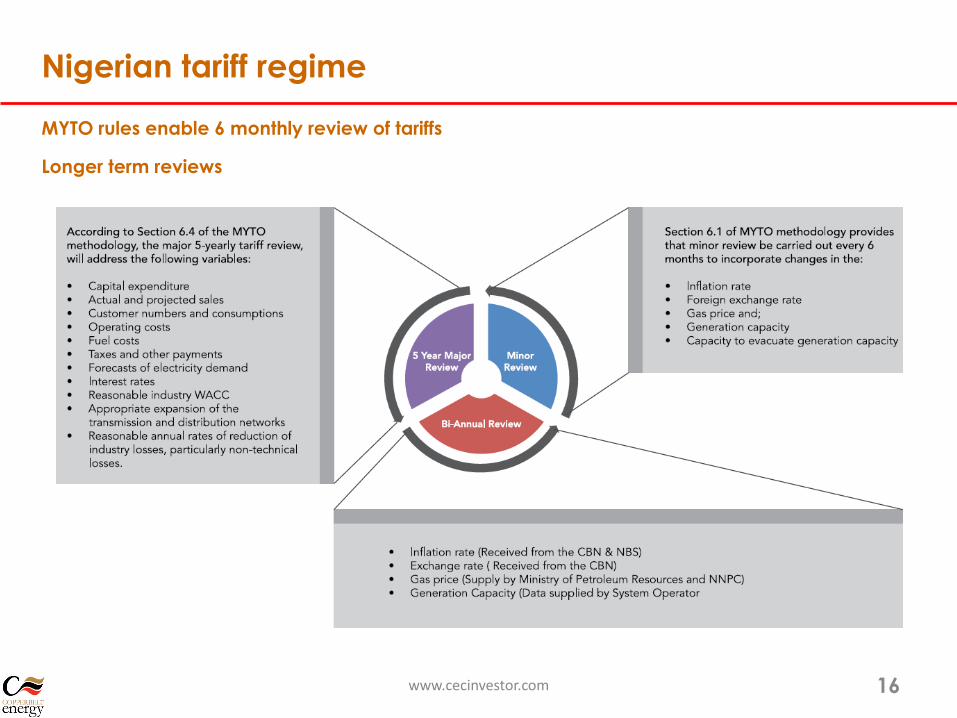

MYTO rules enable 6 monthly review of tariffs

Longer term reviews

www.cecinvestor.com 16

CEC

Financial results

www.cecinvestor.com 17

0%

20%

40%

60%

80%

100%

120%

20

09

20

10

20

11

20

12

20

13

(15)

(10)

(5)

0

5

10

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

EPS Uc

(240)

(160)

(80)

0

80

160

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Continuing ops earnings U$m

0

200

400

600

800

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Revenue U$m

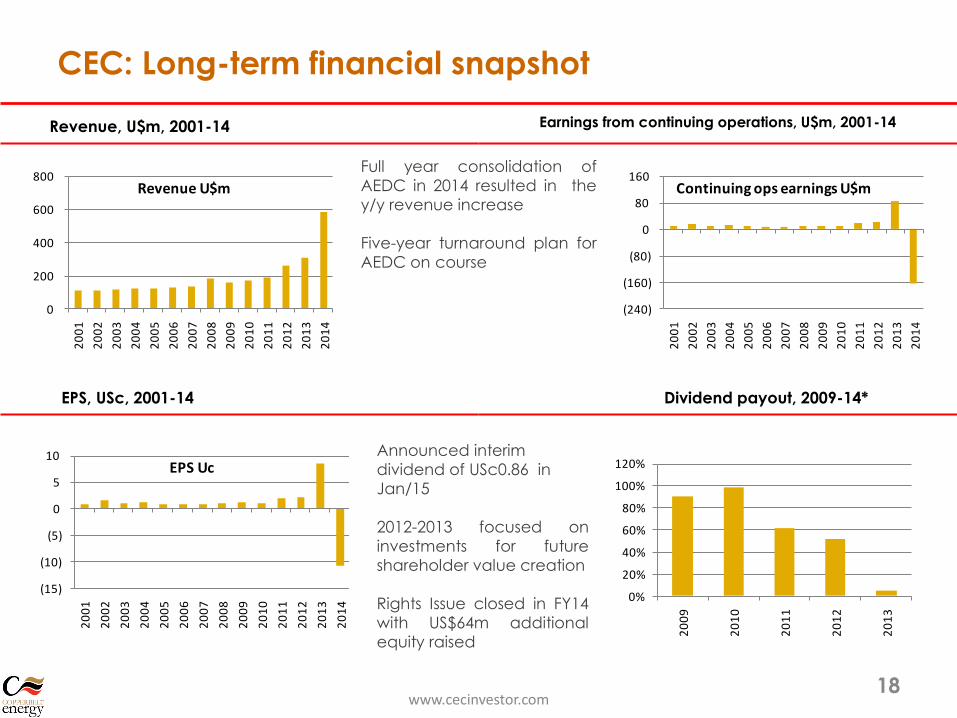

Earnings from continuing operations, U$m, 2001-14

Dividend payout, 2009-14*

Revenue, U$m, 2001-14

EPS, USc, 2001-14

CEC: Long-term financial snapshot

www.cecinvestor.com18

Full year consolidation of

AEDC in 2014 resulted in the

y/y revenue increase

Five-year turnaround plan for

AEDC on course

Announced interim

dividend of USc0.86 in

Jan/15

2012-2013 focused on

investments for future

shareholder value creation

Rights Issue closed in FY14

with US$64m additional

equity raised

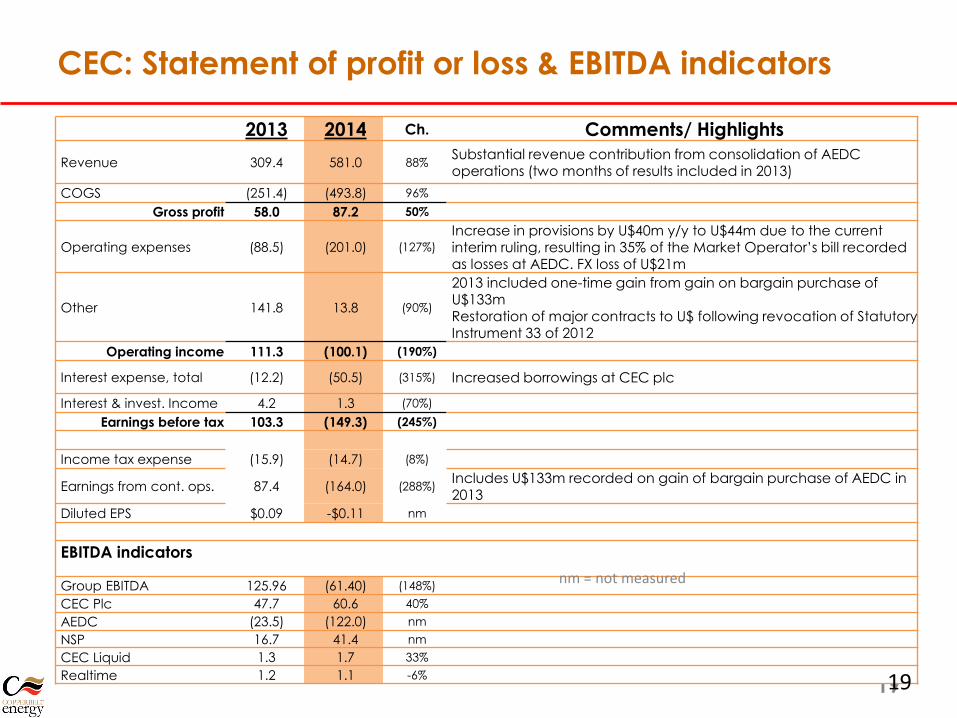

CEC: Statement of profit or loss & EBITDA indicators

19

2013 2014 Ch. Comments/ Highlights

Revenue 309.4 581.0 88%Substantial revenue contribution from consolidation of AEDC operations (two months of results included in 2013)

COGS (251.4) (493.8) 96%

Gross profit 58.0 87.2 50%

Operating expenses (88.5) (201.0) (127%)

Increase in provisions by U$40m y/y to U$44m due to the current interim ruling, resulting in 35% of the Market Operator’s bill recorded as losses at AEDC. FX loss of U$21m

Other 141.8 13.8 (90%)

2013 included one-time gain from gain on bargain purchase of U$133mRestoration of major contracts to U$ following revocation of Statutory Instrument 33 of 2012

Operating income 111.3 (100.1) (190%)

Interest expense, total (12.2) (50.5) (315%) Increased borrowings at CEC plc

Interest & invest. Income 4.2 1.3 (70%)

Earnings before tax 103.3 (149.3) (245%)

Income tax expense (15.9) (14.7) (8%)

Earnings from cont. ops. 87.4 (164.0) (288%)Includes U$133m recorded on gain of bargain purchase of AEDC in 2013

Diluted EPS $0.09 -$0.11 nm

EBITDA indicators

Group EBITDA 125.96 (61.40) (148%)

CEC Plc 47.7 60.6 40%

AEDC (23.5) (122.0) nm

NSP 16.7 41.4 nm

CEC Liquid 1.3 1.7 33%

Realtime 1.2 1.1 -6%

nm = not measured

19

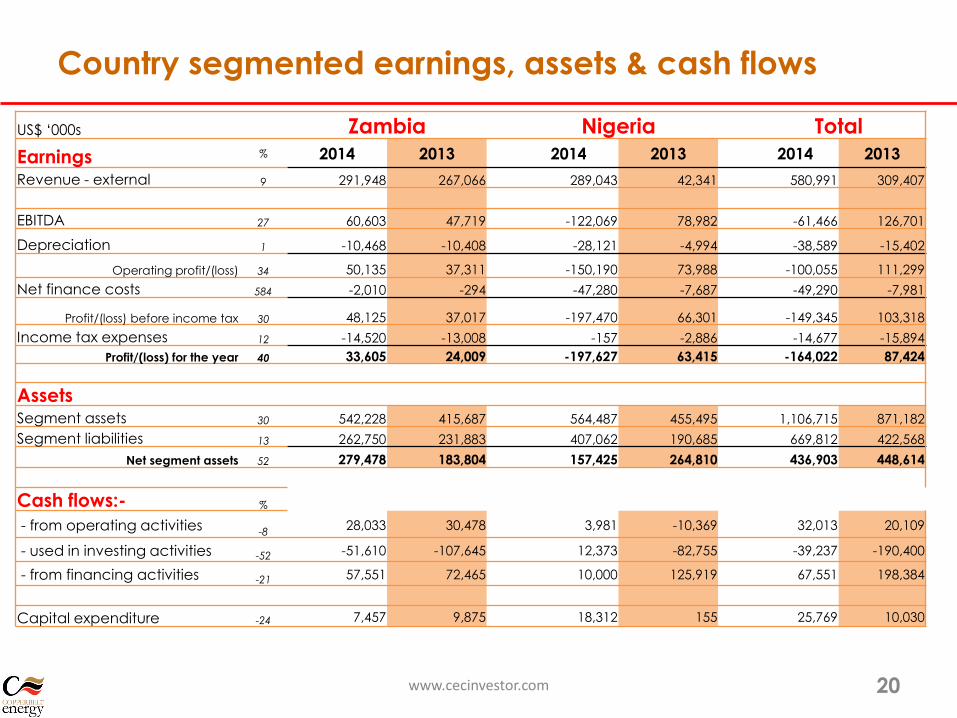

Country segmented earnings, assets & cash flows

20

US$ ‘000s Zambia Nigeria Total

Earnings % 2014 2013 2014 2013 2014 2013

Revenue - external 9 291,948 267,066 289,043 42,341 580,991 309,407

EBITDA 27 60,603 47,719 -122,069 78,982 -61,466 126,701

Depreciation 1 -10,468 -10,408 -28,121 -4,994 -38,589 -15,402

Operating profit/(loss) 34 50,135 37,311 -150,190 73,988 -100,055 111,299

Net finance costs 584 -2,010 -294 -47,280 -7,687 -49,290 -7,981

Profit/(loss) before income tax 30 48,125 37,017 -197,470 66,301 -149,345 103,318

Income tax expenses 12 -14,520 -13,008 -157 -2,886 -14,677 -15,894

Profit/(loss) for the year 40 33,605 24,009 -197,627 63,415 -164,022 87,424

AssetsSegment assets 30 542,228 415,687 564,487 455,495 1,106,715 871,182

Segment liabilities 13 262,750 231,883 407,062 190,685 669,812 422,568

Net segment assets 52 279,478 183,804 157,425 264,810 436,903 448,614

Cash flows:- %

- from operating activities -828,033 30,478 3,981 -10,369 32,013 20,109

- used in investing activities -52 -51,610 -107,645 12,373 -82,755 -39,237 -190,400

- from financing activities -21 57,551 72,465 10,000 125,919 67,551 198,384

Capital expenditure -24 7,457 9,875 18,312 155 25,769 10,030

www.cecinvestor.com

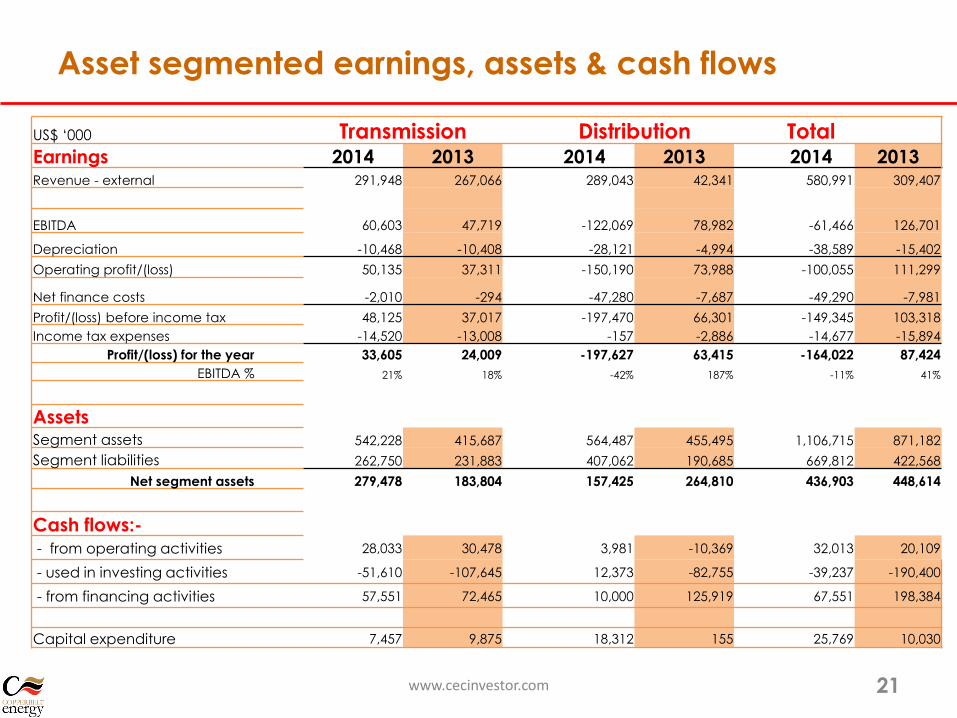

Asset segmented earnings, assets & cash flows

21

US$ ‘000 Transmission Distribution TotalEarnings 2014 2013 2014 2013 2014 2013Revenue - external 291,948 267,066 289,043 42,341 580,991 309,407

EBITDA 60,603 47,719 -122,069 78,982 -61,466 126,701

Depreciation -10,468 -10,408 -28,121 -4,994 -38,589 -15,402

Operating profit/(loss) 50,135 37,311 -150,190 73,988 -100,055 111,299

Net finance costs -2,010 -294 -47,280 -7,687 -49,290 -7,981

Profit/(loss) before income tax 48,125 37,017 -197,470 66,301 -149,345 103,318

Income tax expenses -14,520 -13,008 -157 -2,886 -14,677 -15,894

Profit/(loss) for the year 33,605 24,009 -197,627 63,415 -164,022 87,424

EBITDA % 21% 18% -42% 187% -11% 41%

AssetsSegment assets 542,228 415,687 564,487 455,495 1,106,715 871,182

Segment liabilities 262,750 231,883 407,062 190,685 669,812 422,568

Net segment assets 279,478 183,804 157,425 264,810 436,903 448,614

Cash flows:-- from operating activities 28,033 30,478 3,981 -10,369 32,013 20,109

- used in investing activities -51,610 -107,645 12,373 -82,755 -39,237 -190,400

- from financing activities 57,551 72,465 10,000 125,919 67,551 198,384

Capital expenditure 7,457 9,875 18,312 155 25,769 10,030

www.cecinvestor.com

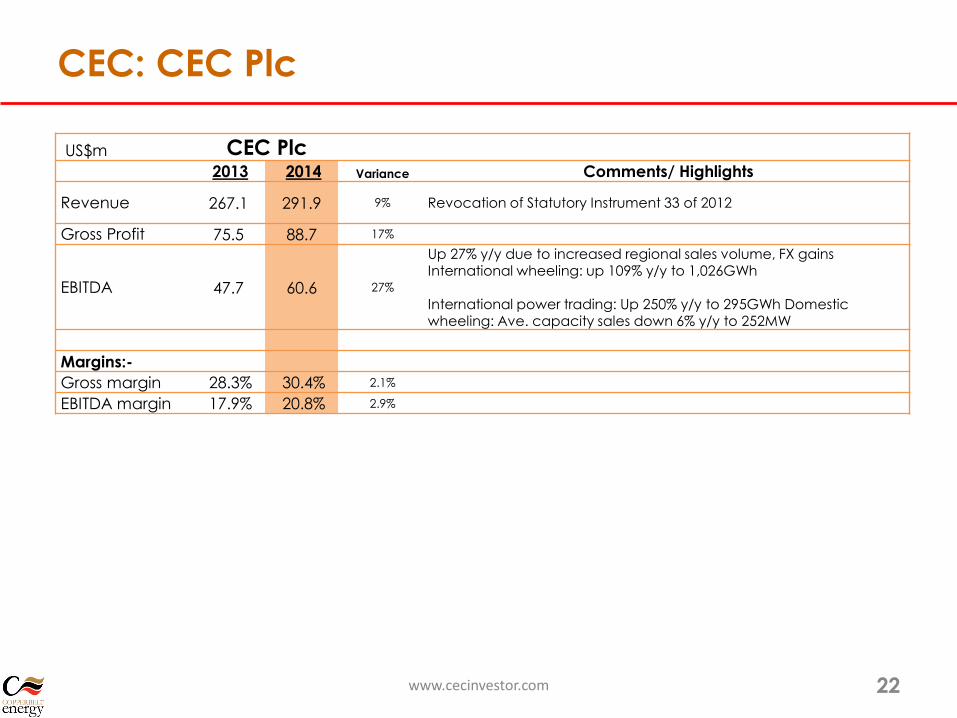

CEC: CEC Plc

US$m CEC Plc2013 2014 Variance Comments/ Highlights

Revenue 267.1 291.9 9% Revocation of Statutory Instrument 33 of 2012

Gross Profit 75.5 88.7 17%

EBITDA 47.7 60.6 27%

Up 27% y/y due to increased regional sales volume, FX gains International wheeling: up 109% y/y to 1,026GWh

International power trading: Up 250% y/y to 295GWh Domestic wheeling: Ave. capacity sales down 6% y/y to 252MW

Margins:-

Gross margin 28.3% 30.4% 2.1%

EBITDA margin 17.9% 20.8% 2.9%

www.cecinvestor.com 22

CEC: Telecommunications

CEC LiquidUS$m 2013 2014 Variance Comments/ Highlights

Revenue 10.6 13.3 26% Fiber footprint: Up 14% y/y in 2014 to 2,494kms

Gross profit 5.2 7.3 41%

EBITDA 1.3 1.7 33%

Margins:-

Gross margin 49.0% 54.7% 5.7%

EBITDA margin 12.1% 12.8% 0.6%

RealtimeUS$m 2013 2014 Variance Comments/ Highlights

Revenue 7.2 7.0 -2.6% Internet Bandwidth: Increased to 340MB/s, increase of 91% y/y

Gross Profit 3.7 3.5 -4.4%

EBITDA 1.2 1.1 -6.2%

Margins:-

Gross margin 51.0% 50.0% -1.0%

EBITDA margin 16.1% 15.4% -0.6%

www.cecinvestor.com 23

0.20x 0.16x

0.54x 0.57x0.72x 0.63x

1.93x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

2011 2012 2013 2014

Debt/ Equity Debt/ EBITDA

15

40

10

26

14

(13)

10 6

(20)

0

20

40

60

2011 2012 2013 2014

Capex Free Cash Flow

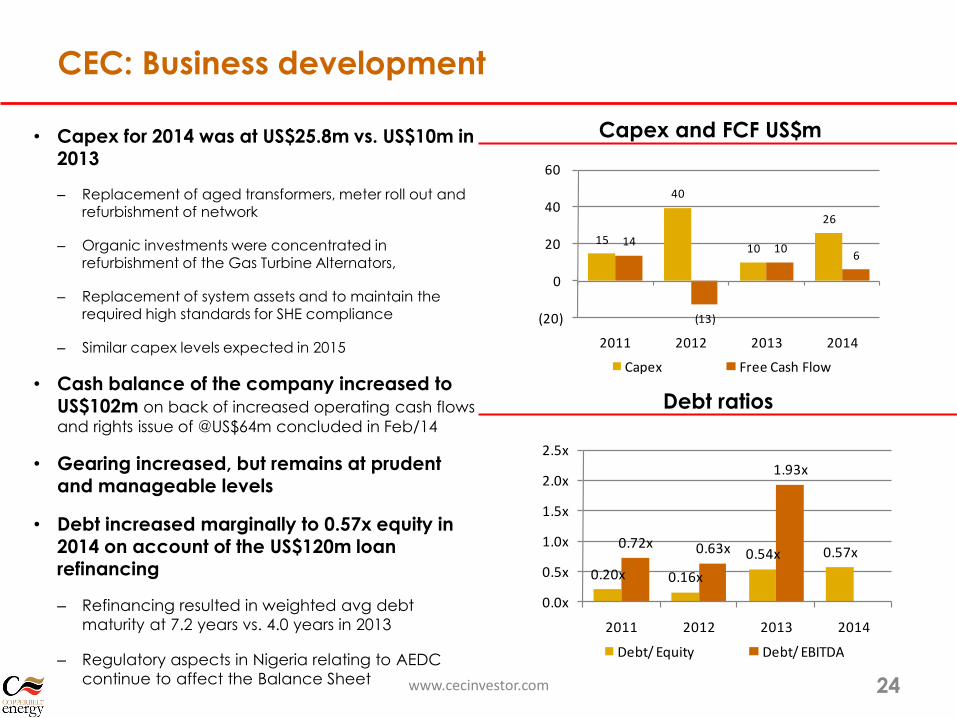

CEC: Business development

24

Capex and FCF US$m

Debt ratios

www.cecinvestor.com

• Capex for 2014 was at US$25.8m vs. US$10m in 2013

– Replacement of aged transformers, meter roll out and refurbishment of network

– Organic investments were concentrated in refurbishment of the Gas Turbine Alternators,

– Replacement of system assets and to maintain the required high standards for SHE compliance

– Similar capex levels expected in 2015

• Cash balance of the company increased to US$102m on back of increased operating cash flows

and rights issue of @US$64m concluded in Feb/14

• Gearing increased, but remains at prudent and manageable levels

• Debt increased marginally to 0.57x equity in 2014 on account of the US$120m loan refinancing

– Refinancing resulted in weighted avg debt

maturity at 7.2 years vs. 4.0 years in 2013

– Regulatory aspects in Nigeria relating to AEDC

continue to affect the Balance Sheet

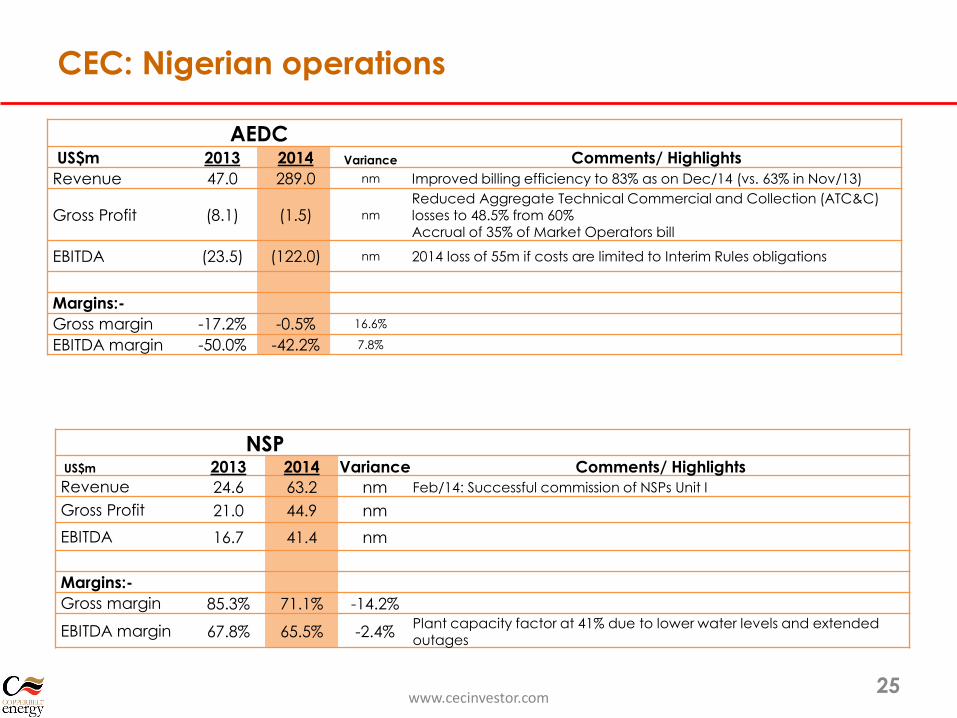

CEC: Nigerian operations

AEDCUS$m 2013 2014 Variance Comments/ Highlights

Revenue 47.0 289.0 nm Improved billing efficiency to 83% as on Dec/14 (vs. 63% in Nov/13)

Gross Profit (8.1) (1.5) nm

Reduced Aggregate Technical Commercial and Collection (ATC&C) losses to 48.5% from 60%Accrual of 35% of Market Operators bill

EBITDA (23.5) (122.0) nm 2014 loss of 55m if costs are limited to Interim Rules obligations

Margins:-

Gross margin -17.2% -0.5% 16.6%

EBITDA margin -50.0% -42.2% 7.8%

NSPUS$m 2013 2014 Variance Comments/ Highlights

Revenue 24.6 63.2 nm Feb/14: Successful commission of NSPs Unit I

Gross Profit 21.0 44.9 nm

EBITDA 16.7 41.4 nm

Margins:-

Gross margin 85.3% 71.1% -14.2%

EBITDA margin 67.8% 65.5% -2.4%Plant capacity factor at 41% due to lower water levels and extended outages

www.cecinvestor.com25

Focus on AEDC

www.cecinvestor.com 26

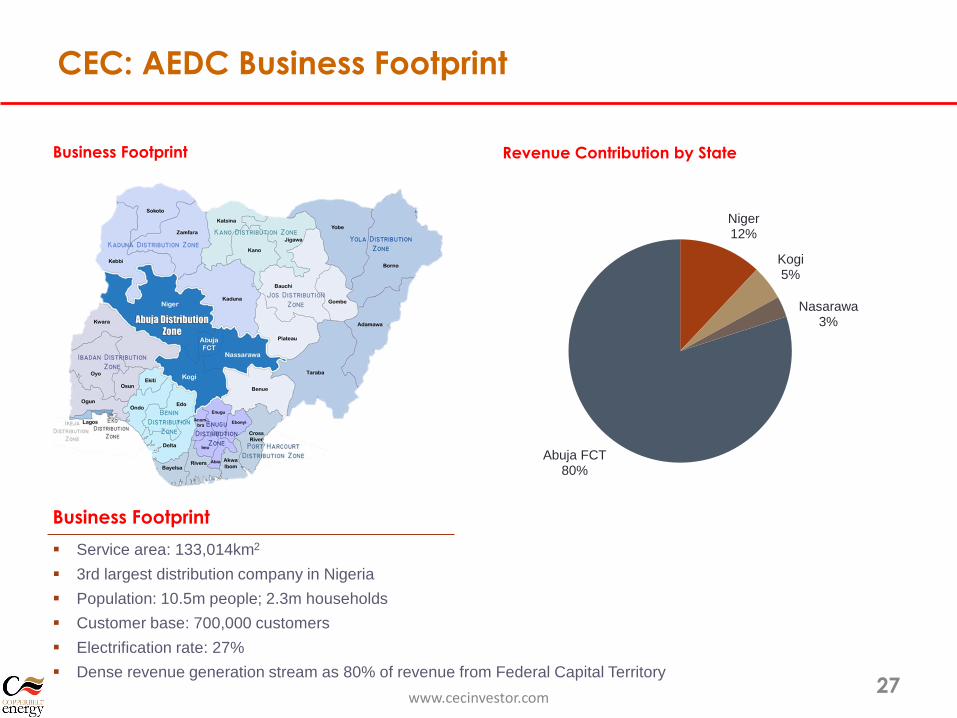

CEC: AEDC Business Footprint

www.cecinvestor.com27

Revenue Contribution by StateBusiness Footprint

Service area: 133,014km2

3rd largest distribution company in Nigeria

Population: 10.5m people; 2.3m households

Customer base: 700,000 customers

Electrification rate: 27%

Dense revenue generation stream as 80% of revenue from Federal Capital Territory

Business Footprint

Niger12%

Kogi5%

Nasarawa3%

Abuja FCT80%

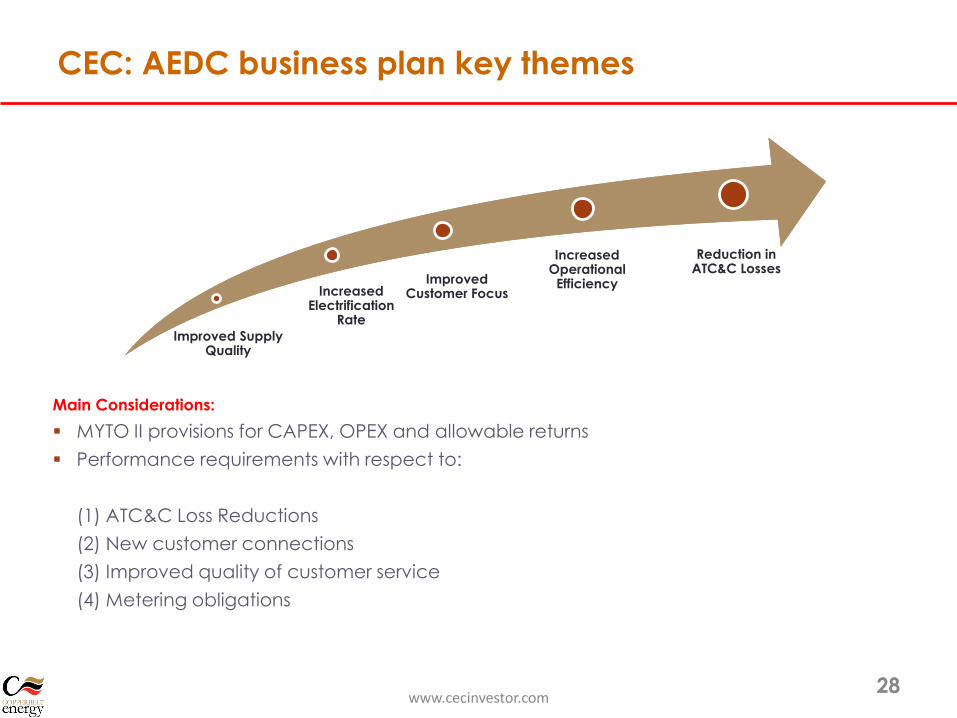

CEC: AEDC business plan key themes

www.cecinvestor.com28

Improved Supply Quality

Increased Electrification

Rate

Improved Customer Focus

Increased Operational

Efficiency

Reduction in ATC&C Losses

Main Considerations:

MYTO II provisions for CAPEX, OPEX and allowable returns

Performance requirements with respect to:

(1) ATC&C Loss Reductions

(2) New customer connections

(3) Improved quality of customer service

(4) Metering obligations

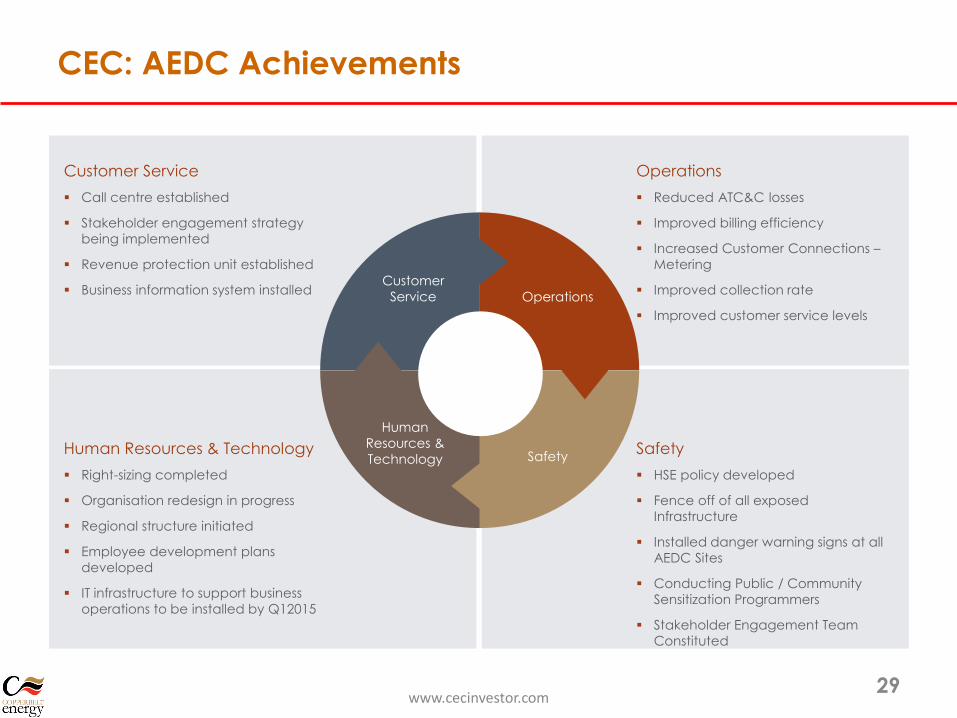

CEC: AEDC Achievements

www.cecinvestor.com29

Operations

Reduced ATC&C losses

Improved billing efficiency

Increased Customer Connections –

Metering

Improved collection rate

Improved customer service levels

Human

Resources &

Technology

Operations

Safety

Customer

Service

Safety

HSE policy developed

Fence off of all exposed

Infrastructure

Installed danger warning signs at all

AEDC Sites

Conducting Public / Community

Sensitization Programmers

Stakeholder Engagement Team

Constituted

Customer Service

Call centre established

Stakeholder engagement strategy

being implemented

Revenue protection unit established

Business information system installed

Human Resources & Technology

Right-sizing completed

Organisation redesign in progress

Regional structure initiated

Employee development plans

developed

IT infrastructure to support business

operations to be installed by Q12015

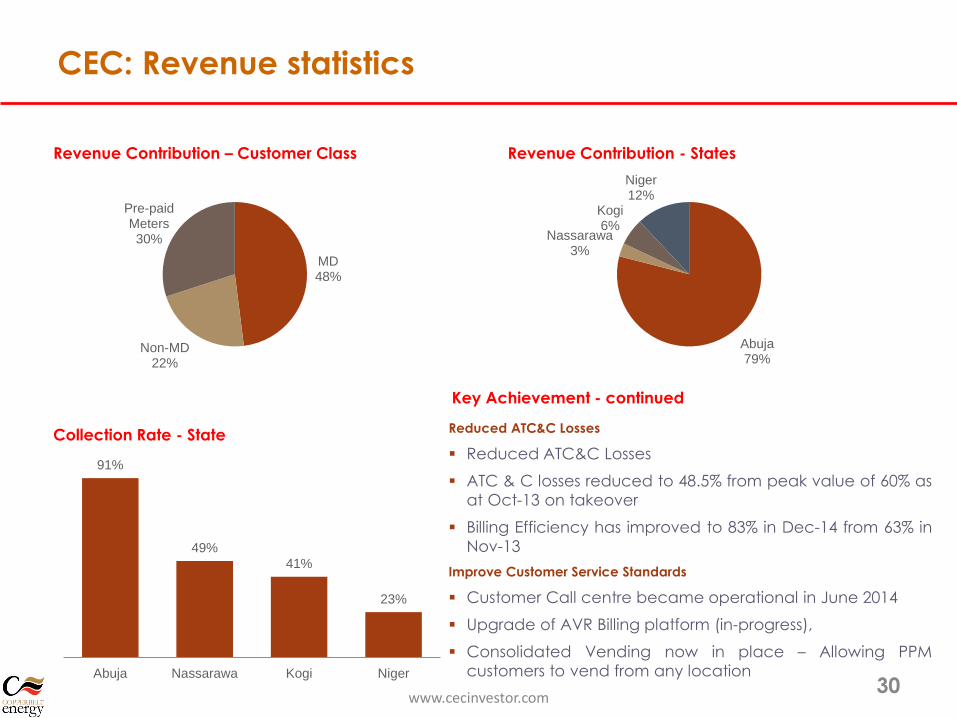

CEC: Revenue statistics

www.cecinvestor.com30

Revenue Contribution - StatesRevenue Contribution – Customer Class

Key Achievement - continued

Collection Rate - StateReduced ATC&C Losses

Reduced ATC&C Losses

ATC & C losses reduced to 48.5% from peak value of 60% as

at Oct-13 on takeover

Billing Efficiency has improved to 83% in Dec-14 from 63% in

Nov-13

Improve Customer Service Standards

Customer Call centre became operational in June 2014

Upgrade of AVR Billing platform (in-progress),

Consolidated Vending now in place – Allowing PPM

customers to vend from any location

MD48%

Non-MD22%

Pre-paid Meters30%

Abuja79%

Nassarawa3%

Kogi6%

Niger12%

91%

49%

41%

23%

Abuja Nassarawa Kogi Niger

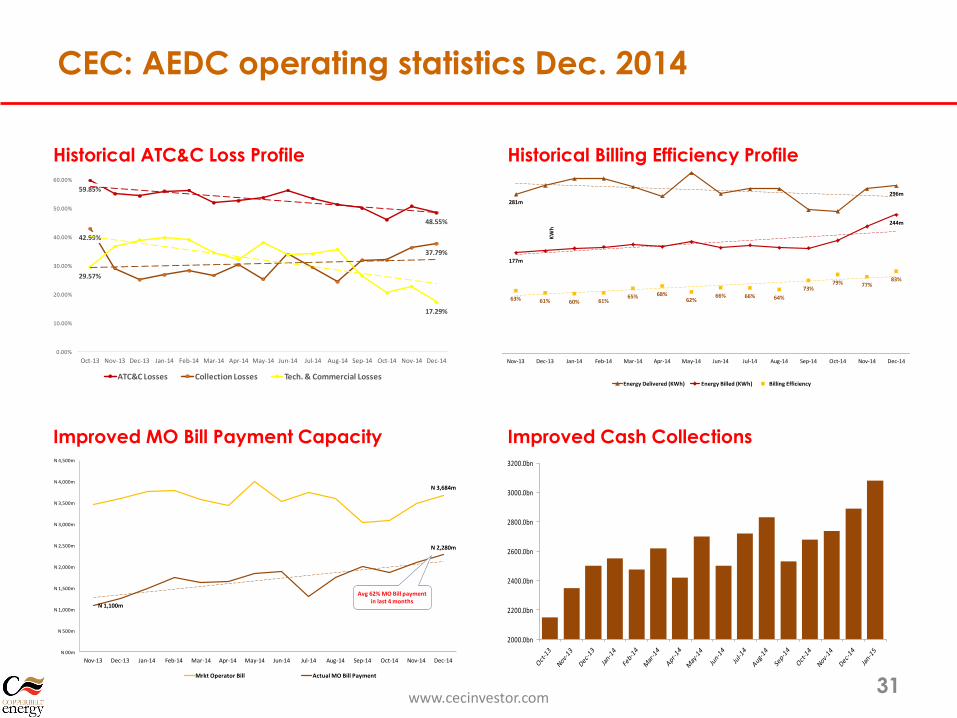

CEC: AEDC operating statistics Dec. 2014

www.cecinvestor.com31

281m

296m

177m

244m

63% 61% 60% 61%65% 68%

62%66% 66% 64%

73%79% 77%

83%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

200.0%

00m

50m

100m

150m

200m

250m

300m

350m

Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

KW

h

Energy Delivered (KWh) Energy Billed (KWh) Billing Efficiency

59.85%

48.55%

42.99%

37.79%

29.57%

17.29%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

ATC&C Losses Collection Losses Tech. & Commercial Losses

N 3,684m

N 1,100m

N 2,280m

N 00m

N 500m

N 1,000m

N 1,500m

N 2,000m

N 2,500m

N 3,000m

N 3,500m

N 4,000m

N 4,500m

Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Mrkt Operator Bill Actual MO Bill Payment

Avg 62% MO Bill payment in last 4 months

2000.0bn

2200.0bn

2400.0bn

2600.0bn

2800.0bn

3000.0bn

3200.0bn

Historical Billing Efficiency ProfileHistorical ATC&C Loss Profile

Improved Cash CollectionsImproved MO Bill Payment Capacity

Pipeline

www.cecinvestor.com 32

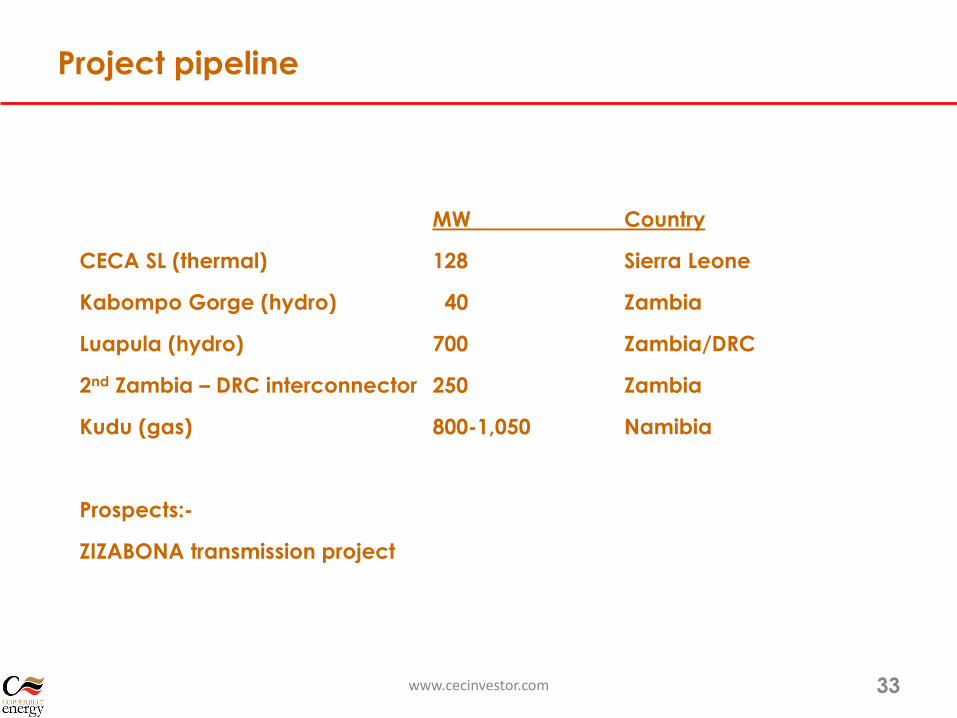

Project pipeline

www.cecinvestor.com 33

MW Country

CECA SL (thermal) 128 Sierra Leone

Kabompo Gorge (hydro) 40 Zambia

Luapula (hydro) 700 Zambia/DRC

2nd Zambia – DRC interconnector 250 Zambia

Kudu (gas) 800-1,050 Namibia

Prospects:-

ZIZABONA transmission project

Outlook

www.cecinvestor.com 34

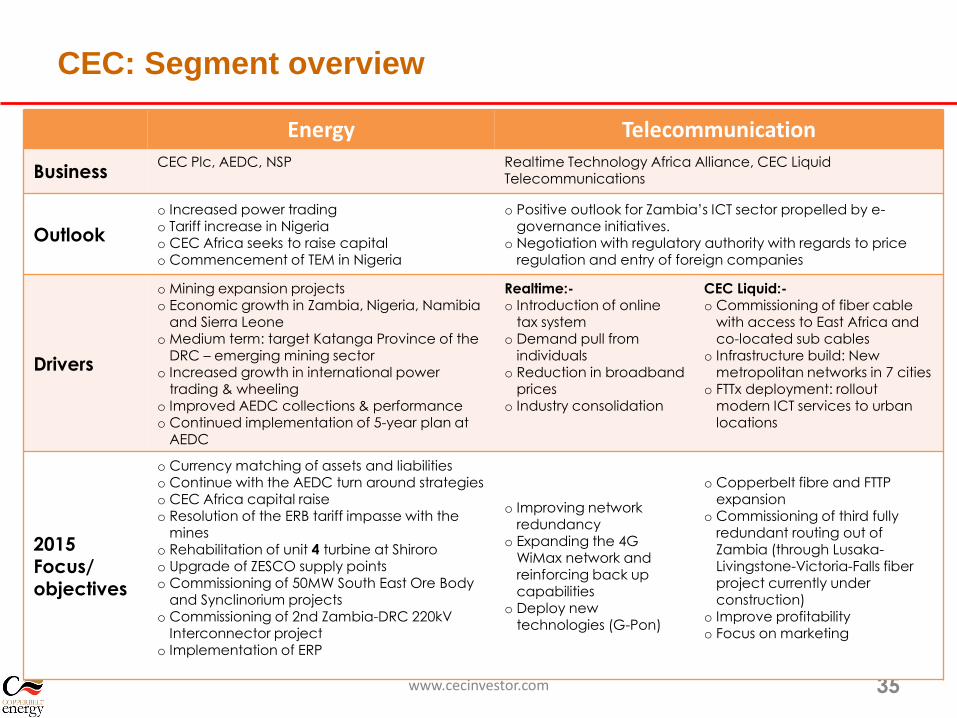

CEC: Segment overview

www.cecinvestor.com 35

Energy Telecommunication

BusinessCEC Plc, AEDC, NSP Realtime Technology Africa Alliance, CEC Liquid

Telecommunications

Outlook

o Increased power tradingo Tariff increase in Nigeriao CEC Africa seeks to raise capitalo Commencement of TEM in Nigeria

o Positive outlook for Zambia’s ICT sector propelled by e-governance initiatives.

o Negotiation with regulatory authority with regards to price regulation and entry of foreign companies

Drivers

o Mining expansion projectso Economic growth in Zambia, Nigeria, Namibia

and Sierra Leoneo Medium term: target Katanga Province of the

DRC – emerging mining sectoro Increased growth in international power

trading & wheelingo Improved AEDC collections & performanceo Continued implementation of 5-year plan at

AEDC

Realtime:-o Introduction of online

tax systemo Demand pull from

individualso Reduction in broadband

priceso Industry consolidation

CEC Liquid:-o Commissioning of fiber cable

with access to East Africa and co-located sub cables

o Infrastructure build: New metropolitan networks in 7 cities

o FTTx deployment: rollout modern ICT services to urban locations

2015 Focus/ objectives

o Currency matching of assets and liabilities o Continue with the AEDC turn around strategieso CEC Africa capital raiseo Resolution of the ERB tariff impasse with the

mineso Rehabilitation of unit 4 turbine at Shiroroo Upgrade of ZESCO supply pointso Commissioning of 50MW South East Ore Body

and Synclinorium projectso Commissioning of 2nd Zambia-DRC 220kV

Interconnector projecto Implementation of ERP

o Improving network redundancy

o Expanding the 4G WiMax network and reinforcing back up capabilities

o Deploy new technologies (G-Pon)

o Copperbelt fibre and FTTP expansion

o Commissioning of third fully redundant routing out of Zambia (through Lusaka-Livingstone-Victoria-Falls fiber project currently under construction)

o Improve profitabilityo Focus on marketing

Q&A

www.cecinvestor.com 36