Embed Size (px)

Citation preview

Wilson HTM Equities Research – The Citadel Group Limited

Issued by Wilson HTM Ltd (Wilson HTM) ABN 68 010 529 665 - Australian Financial Services Licence No 238375, a participant of ASX Group and should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report and an explanation of recommendations can be found at the end of this document.

11 March 2016

THE CITADEL GROUP LIMITED (CGL)

Latent value in a trusted IT services provider

We initiate coverage on Citadel Group Ltd (CGL) with a Buy

recommendation and $5.77 share price target. CGL provides a range of

trusted technology, health and education solutions to high quality

government, health and education sector clients. The share price is

underpinned by annuity-like managed service technology revenues of

average 4.6 year duration. In the short-term, we expect management’s

quality pedigree (ex-senior military and Government professionals) will

help secure new contracts wins and drive cross-sell. In the medium-term,

we expect: (i) CGL will become a pure play technology stock by

repositioning (or exiting) its education business; (ii) value-adding

acquisitions which leverage CGL’s balance sheet flexibility and strong

acquisition skill set; and (iii) high growth from CGL’s leading position in

electronic pathology information management.

Trusted IT services provider

Management and Board’s experience and networks provide a competitive

advantage for access into high quality Government, Defence, Health and

Education clients.

Premium education provider

CGL is a premium provider in the vocational education and training (VET) sector,

with high quality clients and student results distinguishing it from its competition.

Annuity-like cash flows

Long-dated contracts and a history of strong customer renewal provide high

transparency into the Technology segment revenues, with ~70% of Tech

Segment revenues locked in each year under contract.

Strong balance sheet provides acquisition flexibility

CGL has net cash of ~$42m, providing acquisition flexibility. We expect bolt-on

acquisitions which provide cross-selling opportunities into new verticals or with

adjacent products.

Risks and catalysts

Education segment risks (i) loss of licence, fines or suspensions; (ii) loss of VET

FEE HELP accreditations; (iii) reduced volume through VET funding changes.

Technology segment risks: (i) loss of key management; (ii) technology

obsolescence; (iii) acquisitions; (iv) competition.

Catalysts: (i) acquisitions; (ii) new contracts.

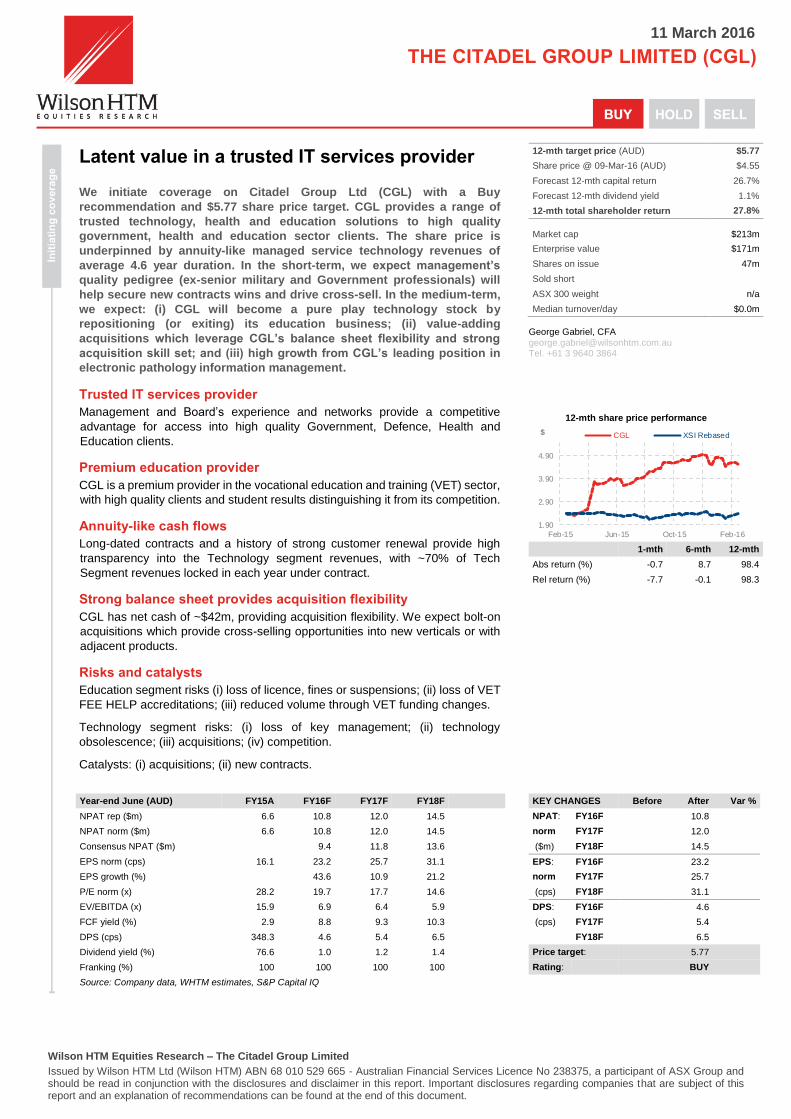

12-mth target price (AUD) $5.77

Share price @ 09-Mar-16 (AUD) $4.55

Forecast 12-mth capital return 26.7%

Forecast 12-mth dividend yield 1.1%

12-mth total shareholder return 27.8%

Market cap $213m

Enterprise value $171m

Shares on issue 47m

Sold short

ASX 300 weight n/a

Median turnover/day $0.0m

George Gabriel, CFA [email protected] Tel. +61 3 9640 3864

12-mth share price performance

1-mth 6-mth 12-mth

Abs return (%) -0.7 8.7 98.4

Rel return (%) -7.7 -0.1 98.3

Year-end June (AUD) FY15A FY16F FY17F FY18F

NPAT rep ($m) 6.6 10.8 12.0 14.5

NPAT norm ($m) 6.6 10.8 12.0 14.5

Consensus NPAT ($m) 9.4 11.8 13.6

EPS norm (cps) 16.1 23.2 25.7 31.1

EPS growth (%) 43.6 10.9 21.2

P/E norm (x) 28.2 19.7 17.7 14.6

EV/EBITDA (x) 15.9 6.9 6.4 5.9

FCF yield (%) 2.9 8.8 9.3 10.3

DPS (cps) 348.3 4.6 5.4 6.5

Dividend yield (%) 76.6 1.0 1.2 1.4

Franking (%) 100 100 100 100

Source: Company data, WHTM estimates, S&P Capital IQ

KEY CHANGES Before After Var %

NPAT: FY16F 10.8

norm FY17F 12.0

($m) FY18F 14.5

EPS: FY16F 23.2

norm FY17F 25.7

(cps) FY18F 31.1

DPS: FY16F 4.6

(cps) FY17F 5.4

FY18F 6.5

Price target: 5.77

Rating: BUY

1.90

2.90

3.90

4.90

Feb-15 Jun-15 Oct-15 Feb-16

$ CGL XSI Rebased

Init

iati

ng

co

vera

ge

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 2

PRICE TARGET

Valuation

Discounted Cash Flow 5.77

Sum of the parts valuation 7.43

Average 6.60

Share price target 5.77

INTERIMS ($m)

Half-year (AUD) Dec 14 Jun 15 Dec 15 Jun 16

1HA 2HA 1HE 2HE

Sales revenue 29.4 42.9 46.8 47.4

EBITDA 10.3 0.5 12.6 12.2

EBIT 10.3 -0.7 10.5 10.1

Net profit 9.9 -3.4 5.5 5.3

Norm EPS 24.4 -8.3 11.9 11.3

EBIT/sales (%) 35.0 -1.7 22.4 21.3

Dividend (c) 346.0 2.4 2.2 2.4

Franking (%) 100.0 100.0 100.0 100.0

FINANCIAL STABILITY

Year-end June (AUD) FY15A FY16F FY17F

Net debt -33.9 -45.0 -54.9

Net debt/equity (%) <0 <0 <0

Net debt/EV (%) <0 <0 <0

Current ratio (x) 3.0 2.7 2.8

Interest cover (x) 18.8 5.6 6.1

Adj cash int cover (x) 17.9 7.7 8.2

Debt/cash flow (x) 0.2 0.2 0.2

Net debt (cash)/share ($)

NTA/share ($) 1.4 1.4 1.5

Book value/share ($) 1.4 1.4 1.5

Payout ratio (%) >500 20 21

Adj payout ratio (%) 67 27 27

EPS RECONCILIATION ($m)

FY15A FY16F

Rep Norm Rep Norm

Sales revenue 72 72 94 94

EBIT 9.6 9.6 20.5 20.5

Net profit 6.6 6.6 10.8 10.8

Notional earn 0.0 0.0 0.0 0.0

Pref/conv div 0.0 0.0 0.0 0.0

Profit for EPS 6.6 6.6 10.8 10.8

Diluted shrs (m) 41 41 47 47

Diluted EPS (c) 16.1 16.1 23.2 23.2

RETURNS

FY15A FY16F FY17F FY18F

ROE (%) 12.8 18.0 18.1 19.7

ROIC (%) 42.3 69.7 95.0 132.2

Incremental ROE 23.0 48.0 18.5 34.8

Incremental ROIC 58.1 160.0 -32.2 -60.5

KEY ASSUMPTIONS

Year-end June (AUD) FY15A FY16F FY17F FY18F

Revenue Growth (%) 29.1 6.7 7.1

NPAT Growth (%) nm 64.9 10.9 21.2

EPS Growth (%) nm 43.6 10.9 21.2

EBITDA / Sales (%) 14.9 26.3 26.6 27.0

EBIT / Sales (%) 13.2 21.8 22.5 23.6

Tax Rate (%) 27.6 35.8 36.0 32.4

ROA (%) 7.6 16.5 17.1 18.1

ROE (%) 11.5 17.1 17.2 18.7

PROFIT AND LOSS ($m)

Year-end June (AUD) FY15A FY16F FY17F FY18F

Sales revenue 72.3 94.2 99.8 106.9

EBITDA 10.8 24.7 26.5 28.9

Depn & amort 1.2 4.2 4.1 3.7

EBIT 9.6 20.5 22.4 25.2

Net interest expense 0.5 3.7 3.7 3.7

Tax 2.5 6.0 6.7 7.0

Minorities/pref divs 0.0 0.0 0.0 0.0

Equity accounted NPAT 0.0 0.0 0.0 0.0

Net profit (pre-sig items) 6.6 10.8 12.0 14.5

Abns/exts/signif 0.0 0.0 0.0 0.0

Reported net profit 6.6 10.8 12.0 14.5

CASH FLOW ($m)

Year-end June (AUD) FY15A FY16F FY17F FY18F

EBITDA 10.8 24.7 26.5 28.9

Interest & tax -0.5 -3.7 -3.7 -3.7

Working cap/other -3.4 -1.4 -3.1 -3.3

Operating cash flow 6.9 19.7 19.8 21.9

Maintenance capex -0.8 -0.9 0.0 0.0

Free cash flow 6.1 18.7 19.8 21.9

Dividends paid -4.1 -5.1 -5.4 -6.5

Growth capex -0.1 -0.4 -0.8 -0.8

Invest/disposals -9.1 0.0 0.0 0.0

Other inv flows -0.8 2.6 0.0 0.0

Cash flow pre-financing -8.0 15.8 13.6 14.6

Funded by equity 22.0 0.0 2.1 2.5

Funded by debt -0.1 -1.8 -5.7 -6.0

Funded by cash -14.0 -14.0 -9.9 -11.1

BALANCE SHEET SUMMARY ($m)

Year-end June (AUD) FY15A FY16F FY17F FY18F

Cash 37.2 49.0 59.0 70.0

Current receivables 21.3 10.6 10.6 10.6

Current inventories 1.8 0.0 0.0 0.0

Net PPE 2.6 3.8 3.8 3.8

Investments 0.0 0.0 0.0 0.0

Intangibles/capitalised 59.9 56.6 53.3 50.4

Other 3.8 4.2 4.2 4.2

Total assets 126.7 124.2 130.8 139.0

Current payables 21.9 15.2 15.2 15.2

Total debt 3.3 4.1 4.1 4.1

Other liabilities 44.5 41.8 41.8 41.8

Total liabilities 69.7 61.0 61.0 61.0

Minorities/convertibles 0.0 0.0 0.0 0.0

Shareholder equity 57.0 63.1 69.7 77.7

Total funds employed 60.3 67.2 73.8 81.8

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 3

Table of contents

1. Investment view

1.2 Recommendation and price target ................................................................. 4

1.3 Investment considerations .............................................................................. 5

1.4 Key catalysts ................................................................................................... 6

1.5 Key risks .......................................................................................................... 6

2. Valuation

2.1 Price target ...................................................................................................... 9

2.2 Comparable companies analysis .................................................................... 9

2.3 Sum of the parts (SOTP) valuation .............................................................. 13

2.4 DCF valuation ............................................................................................... 14

2.5 Earnings guidance ........................................................................................ 15

3. Business overview

3.1 Business model ........................................................................................... 16

3.2 Business history ............................................................................................ 18

3.3 Revenue model ............................................................................................ 18

3.4 Revenue mix ................................................................................................. 19

3.5 Customer mix ................................................................................................ 20

4. Board and management

4.1 Board ............................................................................................................ 21

4.2 Management ................................................................................................ 23

5. Risks and catalysts

5.1 Regulatory risk ............................................................................................. 24

5.2 Contract risk ................................................................................................. 25

5.3 Loss of key management personnel ............................................................. 26

5.4 Technology risk ............................................................................................. 26

5.5 Acquisition risk ............................................................................................. 26

5.6 Competition .................................................................................................. 26

5.7 Catalysts ........................................................................................................ 26

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 4

1. Investment summary

1.1. Recommendation and price target

We initiate coverage with a Buy recommendation and $5.77 share price target.

1.2. Business overview

CGL provides Technology and Education services to clients in the public and private sectors.

It is a premium service provider, both in terms of:

The product suite, which comprises white collar education services and complex IT and

technology solutions; and

Client base, which includes the highest levels of Government, Health and Defence

Departments.

Technology (Managed Services)

CGL’s Technology segment is comprised of 3 brands: Frontier Group Australia Pty Ltd

(“Frontier”), Jakeman Business Solutions Pty Ltd (JBC) and ServicePoint Australia Pty Ltd

(ServicePoint). This segment generates revenue by providing services typically under long-

term contracts. It provides services predominantly under long-term contracts in complex and

sensitive environments, such as secure communications, enterprise content management and

e-health solutions.

Clients are the highest level of Government (Department of Prime Minister & Cabinet;

Department of Defence; Department of Foreign Affairs & Trade; Customs; Attorney General)

and Government agencies (Australian Federal Police; Therapeutic Goods Administration;

Australian Government Solicitor). Health sector clients include medicare; NSW, QLD and SA

Government Health Departments. Corporate clients include Lockheed Martin Australia,

Spotless and a leading Australian telecommunications company.

Health

PJA Solutions is a business founded in 1984 and acquired by CGL in May 2015. PJA is a

leading provider of technology managed services in the pathology sector in Vic, NSW and Qld

and is responsible for >30% of all data transactions associated with public laboratory testing.

PJA was acquired to supplement CGL’s existing capabilities in the health sector. CGL had pre-

existing contracts with NSW Health and New Royal Adelaide Hospital. PJA has been

rebranded “Citadel Health” and fully integrated into CGL’s pre-existing health segment

offerings. We expect this segment will both organically and through strategic bolt-on

acquisitions of adjacent products.

Note that for the purposes of our sum-of-the-parts valuation in this note, we have separately

valued PJA on a stand-alone basis, given the discrete financial disclosures regarding PJA

which were provided at the time of the acquisition.

Education

CGL’s education business Australian Business Academy (ABA) is a Registered Training Organisation (RTO) and an accredited VET FEE-HELP and Commonwealth Register of Institutions and Courses for Overseas Students (CRICOS) provider. CGL’s business is a high quality operator, distinguished from many of the troubled RTOs through client quality (white collar students) and results.

ABA generates revenue by charging students a fixed price for courses delivered over a 12-18

month period. CGL receives no Government subsidies for the education services it delivers,

but students can receive loans under the Federal Government VET FEE-HELP scheme.

CGL’s education business is distinguished from many of the troubled RTOs through client quality and results.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 5

1.3. Investment considerations

Well-positioned IT services provider

CGL has a track record of delivering complex projects in sensitive environments, which is

reflected in its high-level Government and Corporate client base. The Canberra headquarters

and ex-military pedigree of many of its senior management and Board strengthens CGL’s ties

to Government.

CGL’s core competency is in managing knowledge in Defence, Government and Health

markets. It is now seeking to leverage its credentials into the university/education markets.

CGL’s core competency is in managing knowledge in Defence, Government and Health markets.

Trusted adviser to a high quality customer base

CGL is seen as a trusted adviser to a high quality customer base, including:

Defence & Secure Agencies (Department of Defence; DFAT; Attorney-General;

Immigration).

Government (Australian Federal Police; Australian Government Solicitor; Department of

Prime Minister & Cabinet; Therapeutic Goods Administration).

Health sector (medicare; NSW, QLD and SA Government Health).

CGL’s high quality customer base in the Technology segment provides an inherent structural

incentive to maintain the highest possible standards in the RTO business.

CGL is seen as a trusted service provider to a high quality customer base.

Premium education provider

We believe CGL will (and should) exit the education segment in the medium-term, to become

a pure play technology stock with exposure to the fast growth healthtec segment, underpinned

by annuity-like revenues of the Technology (Managed Services) Segment.

CGL’s education business is distinguished from many of the troubled RTOs through:

Client quality. ABA delivers Diploma and Advanced Diploma to students in a range of

driven white collar industry sectors - including finance, business and IT.

Results. In 2013, 100% of graduating students who applied for university courses were

accepted and 98% of students who completed an internship as part of their course gained

employment within 12 weeks of graduation.

Structural incentive to maintain high standards in its Education business, given CGL’s

close ties with government customers in CGL’s technology segment.

We expect CGL will exit Education in the medium-term to become a pure play technology stock.

Annuity revenue streams

CGL’s Technology segment delivers recurring revenues through existing contracts with major

Government organisations and corporates. These contracts tend to be of multi-year duration

at the time of award. Key points CGL describes are:

>80% FY16 tech revenues locked in.

Approx. 70% of tech revenues each year are locked in under managed services contracts.

All current contracts ongoing until at least the end of 2017, with a strong history of renewal.

Average contract duration of 4.6 years. CGL reports continued growth in its average

contract length.

No contracts maturing until the end of CY 2017.

CGL’s Technology segment delivers recurring revenues through existing contracts with major Government organisations and corporates.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 6

Strong balance sheet provides acquisition flexibility

CGL’s strong balance sheet and cash generation supports future acquisitions. CGL had cash

of $37.22m as at June 2015 (up from $19.26 in FY14), with debt of ~$1.4m. AS at 30 Sep 15,

CGL reported $40.7m cash.

CGL’s strong balance sheet and cash generation supports future acquisitions.

Acquisition opportunities

CGL has a strong acquisition track record, successfully executing the PJA acquisition in May

2015. We believe the PJA acquisition was well structured to both mitigate downside risk and

incentivise ongoing vendor performance. The private equity skill set of the CGL founders and

the investment banking pedigree of the Chairman will serve CGL well as it considers a range

of adjacent acquisition opportunities. We expect that CGL could acquire IT services business

in its target segments of defence, government, health and education or acquire RTOs which

meet its quality standards.

CGL has a strong acquisition track record and skill set, which supports potential for further accretive acquisitions.

Leveraged to growth in health technology

PJA positions CGL for strong growth in the e-health segment. PJA’s strong market (>30% of

all data transactions associated with public laboratory testing) positions CGL well for cross-

selling and accretive acquisitions of adjacent products. Over 30k clinicians per month use the

system. CGL expects the acquisition to be >40% earnings accretive in FY16F and to provide

significant technology cross sell opportunities. We expect CGL’s health segment will be a

primary driver of shareholder value in future. .

We believe CGL’s health business will be a primary driver of shareholder value.

High quality management and Board

The leadership team’s ties to Government and military clearly provide a competitive advantage:

A former Chief of Army (Peter Leahy)

Chairman of Macquarie Bank (Ken McCann)

Former MD of an ASX-listed technology consulting practice, SMS Management &

Technology (SMX), Mr Darren Stanley

Former Army intelligence officer, with high level corporate governance skills and co-

founder of Citadel with his own private consultancy and other entrepreneurial ventures

(Miles Jakeman)

Seasoned private equity executive (Mark McConnell)

PhD Information Technology (Dr Matthew Smith)

CGL’s leadership team is a key competitive advantage.

Growth strategies

CGL has a range of organic growth options in both education and technology segments. We

expect that the core focus in the next 12 months will be the technology segment.

Growth strategies in technology include:

Cross-selling additional services to existing clients.

Extending its offering in health and education.

Acquisitions.

Though less of an immediate priority, growth strategies in the education segment include:

Opening further campuses.

Extending the organisation’s scope of nationally accredited courses.

Marketing additional courses via online delivery platforms.

Acquisitions.

CGL has a range of organic growth options in both education and technology segments.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 7

Dividend policy

CGL targets a payout ratio of 40-50% of pro-forma NPAT, which the Board expects will be fully

franked.

Sum of the parts (SOTP) valuation

As a cross-check against our DCF valuation, we have undertaken a SOTP valuation. We

valued CGL’s Education and Technology segments with reference to comparable listed

companies in Education and Technology segments.

Our SOTP valuation of $7.43 per CGL share concludes that there is latent value in CGL. We

do not expect CGL’s latent value to be realised until it becomes a pure-play technology stock,

with increased visibility on the growth of its technology businesses, particularly PJA solutions.

Recent contract wins

Our revenue growth forecasts are supported by recent contract wins. On 15 December 2015,

CGL announced:

A new 5 year (3 x 1 x 1) contract with Monash University worth $8-10m annually in base

services, plus additional project work that Monash may award through a supplementary

supplier panel process.

New technology contracts within its Defence portfolio generating anticipated revenues of

$8m throughout the remaining FY16, with additional projects likely to follow in FY17.

1.4 Key catalysts

New contracts or expanding existing ones

CGL remains well placed to win new contracts with the Government and Corporate sectors.

Acquisitions

We believe CGL is well placed to continue with accretive acquisitions, given its strong cash

balance, private equity experience and recent positive track record with the PJA acquisition.

PJA visibility

We believe CGL should provide increased disclosure into the key value drivers and operational

metrics of the PJA acquisition to enable investors to potentially value PJA in line with high

growth, software as a service (SaaS) listed business models. CGL has integrated PJA without

issue, and to date it remains on track to generate $9.5m EBITDA, in line with CGL guidance at

the time of the acquisition in May 2015.

1.5 Key risks

Regulatory risk

Regulatory change may impact ABA, which holds 3 licences: (i) RTO registration; (ii) VET FEE-

HELP scheme provider status and (iii) CRICOS Provider Registration.

~95% of BA revenues are derived from the VET-FEE HELP scheme. Changes in this scheme

could reduce the number of students able to fund VET courses.

RTOs are subject to regular audits. CGL is a high quality operator, distinguished from its peer

group with the quality of its customer base and reputation. This is evidenced by CGL’s RTO

registration being recently extended for a 10 year period.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 8

Competition

CGL competes with other VET providers (RTOs and TAFE institutions) and also tertiary

education providers.

CGL also competes with a wide range of managed services IT solutions providers.

Contract renewal

The loss of any key contract would adversely impact revenue and earnings.

CGL has a number of key contracts such as Department of Defence, Hansen Yuncken

Leighton Contractors, and Spotless. These customer relationships have historically been

strong, providing recurring revenue and earnings.

Acquisition risk

CGL intends to acquire selective adjacent businesses in either its technology and/or education

segments. Acquisitions are inherently uncertain regarding price and earnings impact.

Technology risk

There is a risk that CGL’s technology may become obsolete and so adversely impact customer

Service Level Agreements and CGL’s ongoing ability to service these customers.

Key personnel and management risk

The loss of key senior management may adversely impact contract renewals given the strong

relationships between management and several Government agencies.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 9

2. Valuation and price target

2.1 Price target

Our price target is $5.77 per share, which is in line with our DCF valuation.

Our price target is $5.77 per share.

Key assumptions are:

6% revenue growth in FY17F and FY18F, followed by 4% perpetuity revenue growth

assumption.

EBITDA margins declining from ~43% in 1H16 to ~40% in perpetuity, driven by a

challenging outlook for the education segment. This could prove to be an overly

conservative assumption if the technology segment continues to scale.

11% discount rate.

2.2 Earnings outlook

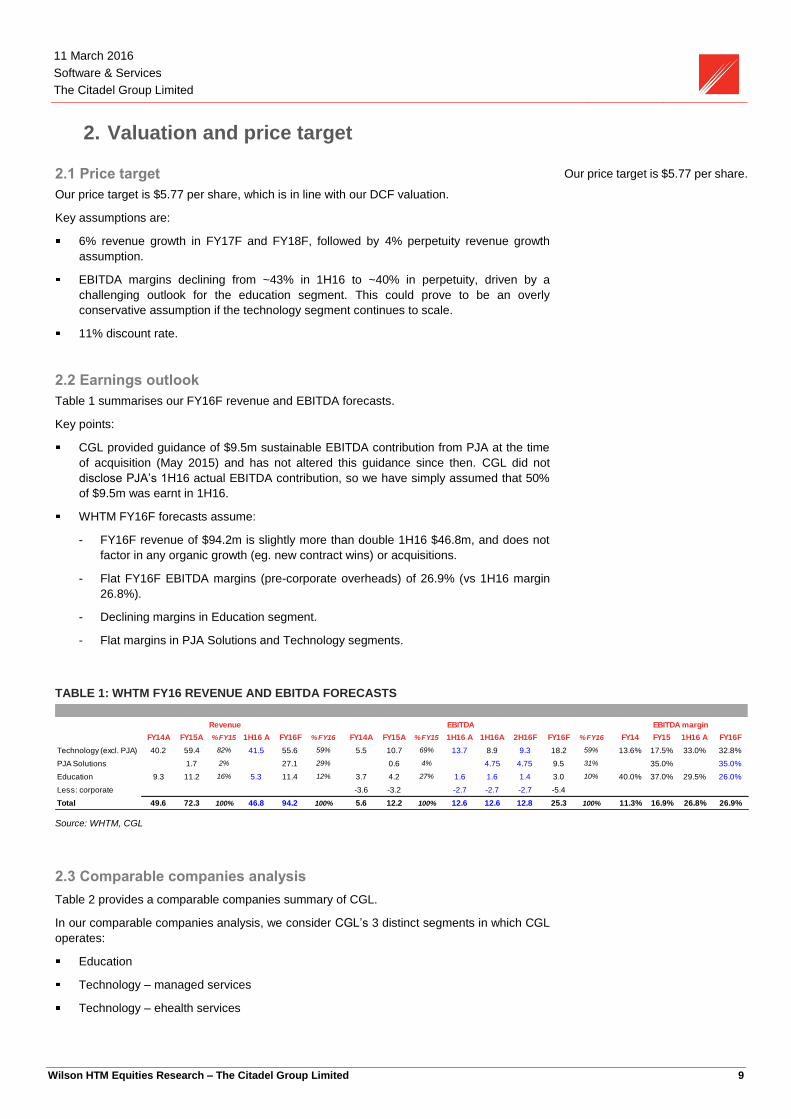

Table 1 summarises our FY16F revenue and EBITDA forecasts.

Key points:

CGL provided guidance of $9.5m sustainable EBITDA contribution from PJA at the time

of acquisition (May 2015) and has not altered this guidance since then. CGL did not

disclose PJA’s 1H16 actual EBITDA contribution, so we have simply assumed that 50%

of $9.5m was earnt in 1H16.

WHTM FY16F forecasts assume:

- FY16F revenue of $94.2m is slightly more than double 1H16 $46.8m, and does not

factor in any organic growth (eg. new contract wins) or acquisitions.

- Flat FY16F EBITDA margins (pre-corporate overheads) of 26.9% (vs 1H16 margin

26.8%).

- Declining margins in Education segment.

- Flat margins in PJA Solutions and Technology segments.

TABLE 1: WHTM FY16 REVENUE AND EBITDA FORECASTS

Source: WHTM, CGL

2.3 Comparable companies analysis

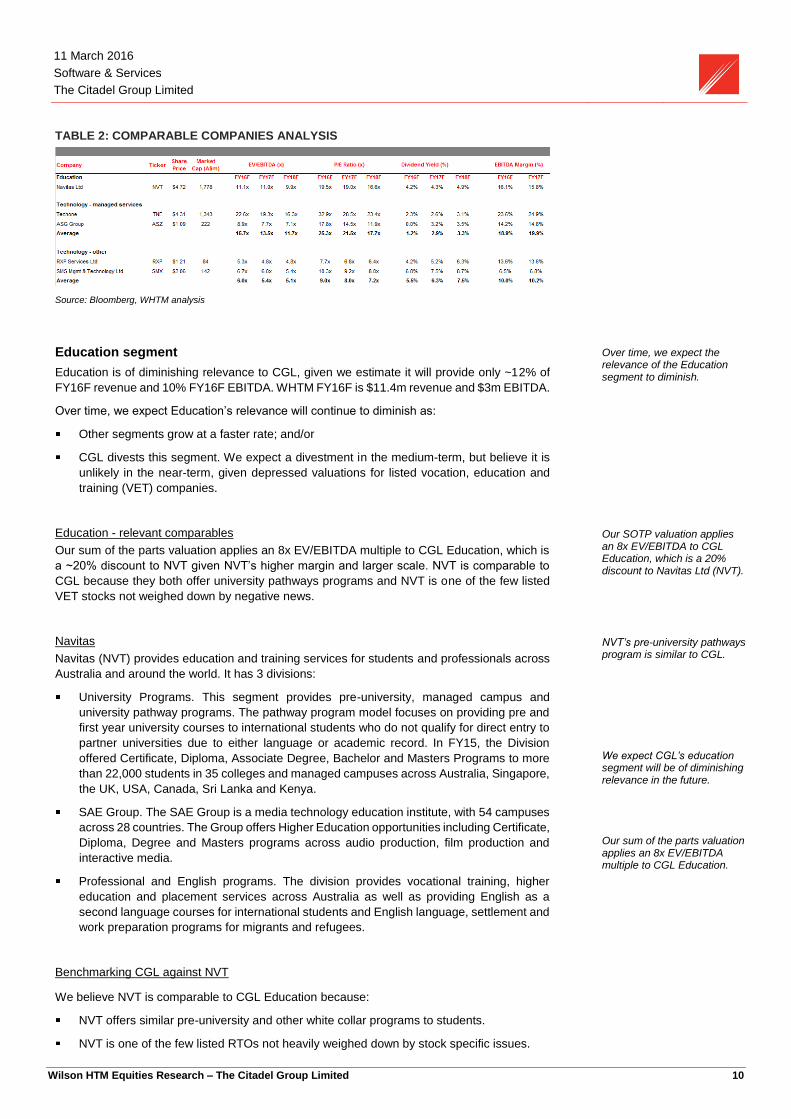

Table 2 provides a comparable companies summary of CGL.

In our comparable companies analysis, we consider CGL’s 3 distinct segments in which CGL

operates:

Education

Technology – managed services

Technology – ehealth services

FY14A FY15A % FY15 1H16 A FY16F % FY16 FY14A FY15A % FY15 1H16 A 1H16A 2H16F FY16F % FY16 FY14 FY15 1H16 A FY16F

Technology (excl. PJA) 40.2 59.4 82% 41.5 55.6 59% 5.5 10.7 69% 13.7 8.9 9.3 18.2 59% 13.6% 17.5% 33.0% 32.8%

PJA Solutions 1.7 2% 27.1 29% 0.6 4% 4.75 4.75 9.5 31% 35.0% 35.0%

Education 9.3 11.2 16% 5.3 11.4 12% 3.7 4.2 27% 1.6 1.6 1.4 3.0 10% 40.0% 37.0% 29.5% 26.0%

Less: corporate -3.6 -3.2 -2.7 -2.7 -2.7 -5.4

Total 49.6 72.3 100% 46.8 94.2 100% 5.6 12.2 100% 12.6 12.6 12.8 25.3 100% 11.3% 16.9% 26.8% 26.9%

Revenue EBITDA EBITDA margin

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 10

TABLE 2: COMPARABLE COMPANIES ANALYSIS

Source: Bloomberg, WHTM analysis

Education segment

Education is of diminishing relevance to CGL, given we estimate it will provide only ~12% of

FY16F revenue and 10% FY16F EBITDA. WHTM FY16F is $11.4m revenue and $3m EBITDA.

Over time, we expect Education’s relevance will continue to diminish as:

Other segments grow at a faster rate; and/or

CGL divests this segment. We expect a divestment in the medium-term, but believe it is

unlikely in the near-term, given depressed valuations for listed vocation, education and

training (VET) companies.

Over time, we expect the relevance of the Education segment to diminish.

Education - relevant comparables

Our sum of the parts valuation applies an 8x EV/EBITDA multiple to CGL Education, which is

a ~20% discount to NVT given NVT’s higher margin and larger scale. NVT is comparable to

CGL because they both offer university pathways programs and NVT is one of the few listed

VET stocks not weighed down by negative news.

Our SOTP valuation applies an 8x EV/EBITDA to CGL Education, which is a 20% discount to Navitas Ltd (NVT).

Navitas

Navitas (NVT) provides education and training services for students and professionals across

Australia and around the world. It has 3 divisions:

University Programs. This segment provides pre-university, managed campus and

university pathway programs. The pathway program model focuses on providing pre and

first year university courses to international students who do not qualify for direct entry to

partner universities due to either language or academic record. In FY15, the Division

offered Certificate, Diploma, Associate Degree, Bachelor and Masters Programs to more

than 22,000 students in 35 colleges and managed campuses across Australia, Singapore,

the UK, USA, Canada, Sri Lanka and Kenya.

SAE Group. The SAE Group is a media technology education institute, with 54 campuses

across 28 countries. The Group offers Higher Education opportunities including Certificate,

Diploma, Degree and Masters programs across audio production, film production and

interactive media.

Professional and English programs. The division provides vocational training, higher

education and placement services across Australia as well as providing English as a

second language courses for international students and English language, settlement and

work preparation programs for migrants and refugees.

NVT’s pre-university pathways program is similar to CGL.

We expect CGL’s education segment will be of diminishing relevance in the future.

Our sum of the parts valuation applies an 8x EV/EBITDA multiple to CGL Education.

Benchmarking CGL against NVT

We believe NVT is comparable to CGL Education because:

NVT offers similar pre-university and other white collar programs to students.

NVT is one of the few listed RTOs not heavily weighed down by stock specific issues.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 11

Relevant considerations for benchmarking purposes are:

NVT is much larger business than CGL Education, with NVT annual revenues of ~A$1

billion, compared to WHTM FY16F CGL Education revenue of ~$11m.

CGL Education has a higher WHTM FY16F EBITDA margin of 26%, vs Bloomberg

consensus NVT FY16F of 16.1%. Many of NVT’s university contracts are lower margin

than CGL’s Education business.

NVT’s share price has fallen from a high of $5.12 recently to a low ~$4.50 recently, given:

- Full-year FY16F guidance is flat vs FY15.

- Macquarie University contract is rolling off and NVT is trying to find offsetting revenue.

NVT is comparable to CGL in that they both offer university pathways programs. NVT is a much larger business but CGL has higher margins.

Education – irrelevant comparables

We conclude that most listed education companies are not comparable to CGL for various

reasons.

Simonds Group Ltd (SIO) is not a pure play, with a mix of building construction and

vocational education.

Redhill Group (RDH) is too small to be comparable ($24m market capitalisation) and we

have no view on earnings outlook given RDH is not covered by research analysts and the

company has not issued guidance.

Vocation Ltd (VET) went into voluntary administration on 30 November 2015 after a series

of operational irregularities resulted in voluntary administration.

Australian Careers Network Ltd-(ACO) was suspended from ASX trading after being

accused of misconduct.

Ashley Services Group Limited (ASH) was materially adversely affected by the

government termination of funding the $5,500 “Tools for your Trade” incentive program on

1 July 2014. The share price has since collapsed, and ASH has been accused of

misleading investors.

Intueri Education Group Ltd (IQE) received a notice of serious fraud office enquiry,

triggering a share price collapse.

Most listed education companies are not comparable to CGL for various reasons.

Technology (Managed Services) segment

CGL’s Technology segment (ex PJA acquisition) mostly comprises long-term, contracted

revenues.

WHTM FY16F CGL Technology (Managed Services) revenue is $55.6m and FY16F EBITDA

is $18.2m. Revenues are underpinned by long-term contracts, with ~70% revenues locked in

under managed services contracts with an average duration of 4.6 years and no contracts

maturing until the end of CY 2017.

Our sum of the parts valuation applies a 12x EV/EBITDA multiple to CGL Tech (Managed

Services) FY17F EBITDA, which is 11% below the ~13.5x average of TNE 19.3x and ASZ

7.7x.

Technology One (TNE)

We believe CGL is comparable to Technology One Ltd (TNE) because the contribution from

annuity-like technology services to total revenue is similar. Of TNE’s $218m FY15 revenues,

approx. $99m is annuity-like revenue (~45%) comprising Annual Licence Fees of $95.3m and

Cloud Service Fees of $4.1m. This is similar to CGL’s ratio of ~43% of total Group FY16F

revenues being annuity like tech/managed services.

TNE is an enterprise software provider which provides an end-to-end services from the

development of software to implementation and customer support. Its software has been

developed specifically for a number of industry sectors including government, financial

Approx. 70% of tech revenues are locked in under managed services contracts, with all current contracts ongoing until at least the end of 2017, with a strong history of renewal.

CGL is comparable to Technology One Ltd (TNE) because the contribution from annuity-like technology services to total revenue is similar, with ~43% vs ~45% respectively of total Group FY16F revenues being annuity like tech/managed services.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 12

services, health & community services, education and utilities. Products include financials, HR

& payroll, supply chain and business intelligence. TNE has 14 offices throughout Australia, NZ,

Asia, the South Pacific and the UK.

Benchmarking CGL against TNE

Relevant considerations for benchmarking purposes are:

TNE is a much larger business than CGL, with Bloomberg consensus FY16F revenues of

~$239m, compared to our CGL FY16F total revenue of ~$100m.

TNE’s market capitalisation is ~$1.4bn, compared to CGL ~$220m.

TNE operates on a global scale.

CGL Technology (Managed Services) has a lower WHTM FY16F EBITDA margin of

~18%, vs Bloomberg consensus TNE FY16F of 23.6%.

ASG Group (ASZ)

We believe ASZ is comparable to CGL. ASZ provides IT management, consulting services,

and business intelligence to sectors such as mining, transport and manufacturing, government,

education, communications and technology, healthcare, corporate and utilities. ASZ is a

certified partner with vendors, such as HP, Oracle, Microsoft, SAP and Redhat. ASZ

businesses are located in Australia. Services provided include (i) managed services; (ii)

business solutions; (iii) SAP solutions; (iv) IT service management and (v) enterprise analytics.

We believe ASZ is comparable to CGL Technology (Managed Services) because both offer IT

managed services and ASZ also has Government clients (eg. Australian Transport Safety

Bureau; Department of Primary & Environment Industries and Australian Maritime Safety

Authority).

ASZ is comparable to CGL Technology (Managed Services) because both provide IT managed services to Government clients.

Benchmarking CGL against ASZ

Relevant considerations for benchmarking purposes are:

Absolute EBITDA is similar. ASZ Bloomberg FY16F EBITDA $25.9m compares to CGL

FY16F $21.7m.

CGL is higher margin, with FY16F EBITDA margin of 18% in Technology (Managed

Services) vs Bloomberg consensus for ASZ 13.6%.

ASZ has ~98% of FY15 revenue locked in for FY16. CGL has ~70% of total tech revenues

locked in for FY16F.

ASZ has average contract length of 4 years vs GCL 4.6 years.

ASZ has provided FY16F EBITDA guidance of $25.9m, which implies it is trading on ~8x

FY16F EV/EBITDA at ~$200m market capitalisation.

Technology - eHealth (PJA Solutions)

For the purposes of our SOTP valuation, we have considered PJA Solutions as a stand-alone

business. We have valued PJA at 12x EV/EBITDA, which is a ~20% discount to Orion Health

Group Ltd due to lack of earnings visibility. We believe CGL needs to disclose key operating

metrics and value drivers of PJA so that investors are better able to value the business segment

on a stand-alone basis.

Orion Health Group Ltd (OHE)

OHE provides Smarter Hospitals software which enables hospitals to automate key processes,

connecting all clinical information into a single viewer within a hospital. OHE also provide

software to Governments and Health Provider networks to enable care coordination, analytics

and patient engagements.

We have valued PJA at 12x EV/EBITDA, which is a ~20% discount to Orion Health Group Ltd.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 13

We believe OHE is comparable to PJA because they both offer ehealth solutions to

Governments and the health care sector.

Benchmarking CGL against TNE

Relevant considerations for benchmarking purposes are:

Adjusted FY16F EV/EBITDA of 15x. (We have adjusted OHE EBITDA by adding back

research and development expenditure and annualising 1H16 EBITDA).

~41% of OHE revenue is recurring. It is not clear what percentage of PJA revenue is

recurring, but we would estimate that it is at least in line with ~70% of CGL Managed

Services.

2.4 Sum of the parts (SOTP) valuation

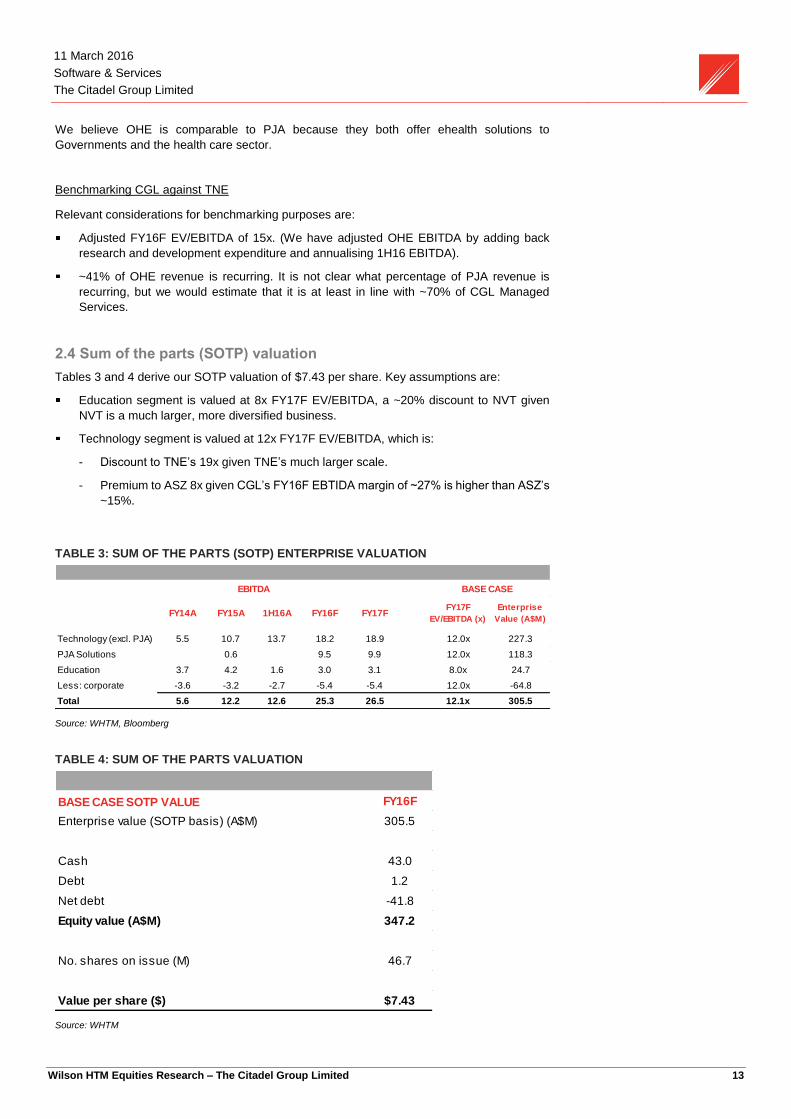

Tables 3 and 4 derive our SOTP valuation of $7.43 per share. Key assumptions are:

Education segment is valued at 8x FY17F EV/EBITDA, a ~20% discount to NVT given

NVT is a much larger, more diversified business.

Technology segment is valued at 12x FY17F EV/EBITDA, which is:

- Discount to TNE’s 19x given TNE’s much larger scale.

- Premium to ASZ 8x given CGL’s FY16F EBTIDA margin of ~27% is higher than ASZ’s

~15%.

TABLE 3: SUM OF THE PARTS (SOTP) ENTERPRISE VALUATION

Source: WHTM, Bloomberg

TABLE 4: SUM OF THE PARTS VALUATION

Source: WHTM

FY14A FY15A 1H16A FY16F FY17FFY17F

EV/EBITDA (x)

Enterprise

Value (A$M)

Technology (excl. PJA) 5.5 10.7 13.7 18.2 18.9 12.0x 227.3

PJA Solutions 0.6 9.5 9.9 12.0x 118.3

Education 3.7 4.2 1.6 3.0 3.1 8.0x 24.7

Less: corporate -3.6 -3.2 -2.7 -5.4 -5.4 12.0x -64.8

Total 5.6 12.2 12.6 25.3 26.5 12.1x 305.5

EBITDA BASE CASE

BASE CASE SOTP VALUE FY16F

Enterprise value (SOTP basis) (A$M) 305.5

Cash 43.0

Debt 1.2

Net debt -41.8

Equity value (A$M) 347.2

No. shares on issue (M) 46.7

Value per share ($) $7.43

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 14

2.5 Discounted cash flow valuation

Our DCF valuation is $5.77 per share.

Key assumptions are:

FY16F revenue of A$100m, which grows to $121m in FY19 and then grows at 3%

annualised.

Annual cost growth of 3%.

WACC of 11%.

Perpetuity growth rate of 3%.

2.6 Earnings guidance

CGL has not issued any specific earnings or revenue guidance. Key commentary is summarised below.

1H16 results commentary (15 Feb 2016)

Outlook commentary

“the group intends to continue to pursue organic and acquisitive opportunities as part of

its growth strategy during the next 12 months (principally within its technology and health

businesses)”

“management highlights the risk associated with headwinds in the education sector and

possible further regulatory changes over the next 12 months”

Outlook is for both organic and acquisition growth; regulatory risks in education sector remain. No quantitative outlook guidance provided.

Operational updates:

Hired Darren Stanley, former Managing Director of ASX-listed SMS Management &

Technology (SMX). Completed the integration of PJA Solutions into CGL.

Renewed large contract with Defence.

No tech contracts are up for renewal until late 2017.

Achieved substantial completion with new Royal Adelaide Hospital contract (removing any

exposure to liquidated damages).

No tech contracts are up for renewal until late 2017.

2015 AGM commentary (11 Nov 2015)

AGM commentary

Within the Technology segment:

The contract with Charles Sturt University (CSU) to provide a new collaboration network

supporting up to 25,000 students, faculty, and staff communicating face-to-face in real

time was successfully completed. This is the world’s largest deployment of concurrent

videoconferencing connections.

Within the Education segment:

The Group successfully expanded its education operations to two new sites in Penrith

NSW and Ashfield NSW, with the two new campuses each with approximately a 150-

students per annum capacity;

Obtaining approval to offer Bachelor-level qualifications remains an important strategic

objective for Citadel

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 15

Key contracts

On 15 December 2015, CGL announced:

A new 5 year (3 x 1 x 1) contract with Monash University worth $8-10m annually in base

services, plus additional project work that Monash may award through a supplementary

supplier panel process.

New technology contracts within its Defence portfolio generating anticipated revenues of

$8m throughout the remaining FY16, with additional projects likely to follow in FY17.

Continued growth in its average contract length.

>80% FY16 tech revenues locked in.

CGL reports continued growth in its average contract length.

>80% FY16 tech revenues locked in.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 16

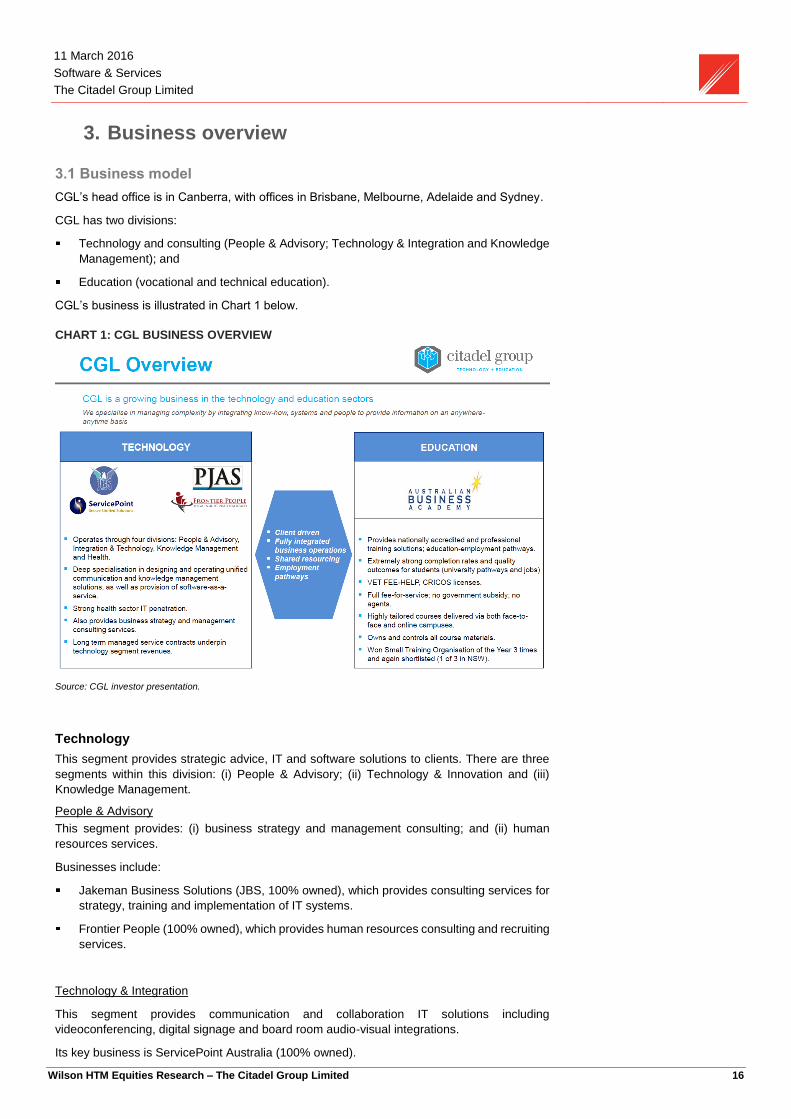

3. Business overview

3.1 Business model

CGL’s head office is in Canberra, with offices in Brisbane, Melbourne, Adelaide and Sydney.

CGL has two divisions:

Technology and consulting (People & Advisory; Technology & Integration and Knowledge

Management); and

Education (vocational and technical education).

CGL’s business is illustrated in Chart 1 below.

CHART 1: CGL BUSINESS OVERVIEW

Source: CGL investor presentation.

Technology

This segment provides strategic advice, IT and software solutions to clients. There are three

segments within this division: (i) People & Advisory; (ii) Technology & Innovation and (iii)

Knowledge Management.

People & Advisory

This segment provides: (i) business strategy and management consulting; and (ii) human

resources services.

Businesses include:

Jakeman Business Solutions (JBS, 100% owned), which provides consulting services for

strategy, training and implementation of IT systems.

Frontier People (100% owned), which provides human resources consulting and recruiting

services.

Technology & Integration

This segment provides communication and collaboration IT solutions including

videoconferencing, digital signage and board room audio-visual integrations.

Its key business is ServicePoint Australia (100% owned).

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 17

Knowledge Management

This segment provides design, implementation and support of knowledge technology solutions

such as systems engineering, audit and security controls, and collaboration and presentation

toolsets.

Businesses include:

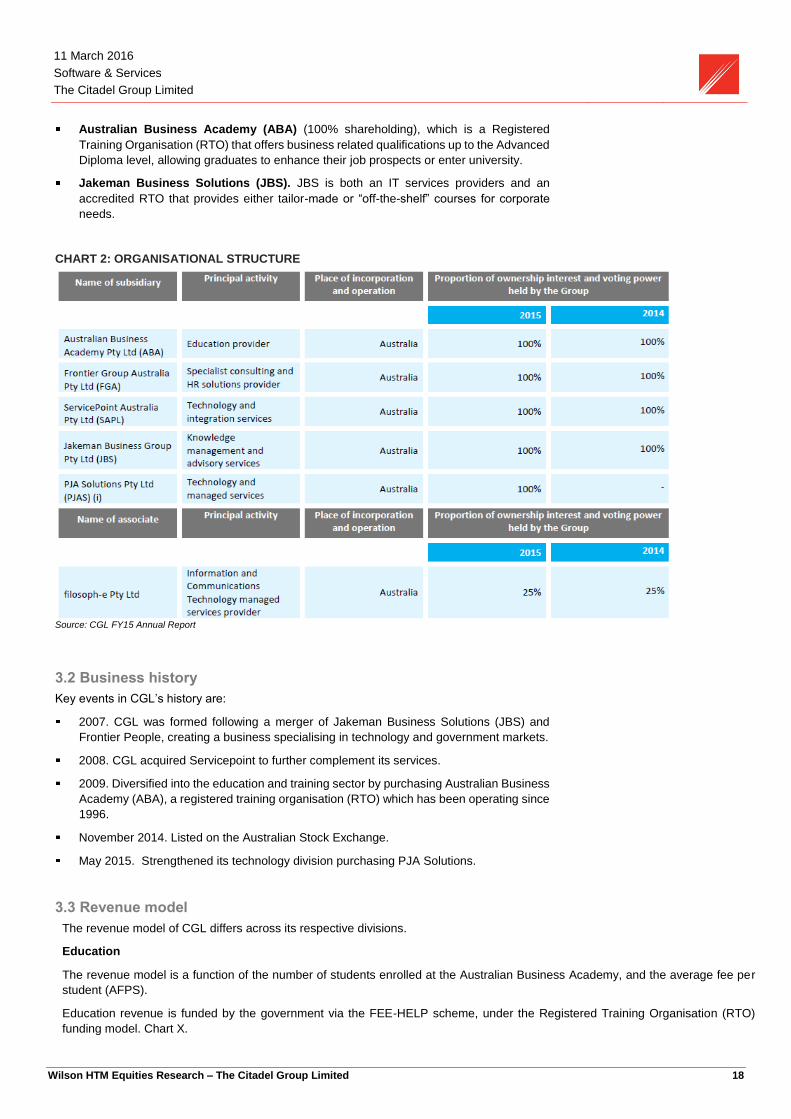

filosoph-e (25% shareholding), which implements and maintains Electronic Content

Management (ECM) systems. Value-added services include development of workflows,

bulk information uploading and digitisation. This business is equity accounted within CGL’s

financial statements.

SME Gateway (through Jakeman Business Solutions). This is a not-for-profit company

that assists small-to-medium enterprises to win new business in professional services.

PJA Solutions (100% shareholding) provides software solutions, products and managed

services for use across Australian hospitals. For example, it manages the pathology

information of Australians treated in a public hospital and the management of client

workflows. PJA also provides technical advisory for its solutions.

Health – PJA Solutions (PJA)

PJA is a high quality business which positions CGL for strong growth in the e-health segment.

Business overview

PJA was founded in 1984 and is a leading provider of technology managed services in the

pathology sector (Vic, NSW and Qld). PJA’s Auslab system is used to manage pathology

information for more than 30% of Australians who have had treatment in a public hospital. More

than 30,000 clinicians per month use the system. The system allows paperless electronic

ordering of diagnostic tests and has functions for reviewing and approving result reports and

preparing clinical and discharge summaries for patients.

Transaction overview

In May 2015, CGL acquired PJA Solutions for up to $60m ($45m to expand its position in the

e-health sector.

Citadel (CGG) will make an initial payment of $20m, followed by two additional payments

totalling up to $25m over the next 30 months. It will make a third additional payment of $15m,

subject to the achievement of financial growth objectives, after FY2017.

The initial payment was funded from existing cash reserves and issue of new shares worth

$5m, priced at $2.30 each. Financial close was ~ une 2015.

Citadel expects the acquisition to be earnings accretive immediately. It expects the PJA deal

to add $9.5m, or more than 80 per cent, to its EBITDA (earnings before interest tax depreciation

and amortisation) on a full-year basis.

PJA has >30% share, with more than 30k clinicians per mth using the system.

Education

This segment provides:

Nationally accredited training courses at diploma level and above to assist school leavers

to gain university entry.

Tailor made professional development courses for corporations.

The segment accesses government student FEE-HELP loans and delivers online education.

Training courses include business and management, human resources, IT, graphic design and

tourism. They are delivered both online and face-to-face.

Businesses include:

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 18

Australian Business Academy (ABA) (100% shareholding), which is a Registered

Training Organisation (RTO) that offers business related qualifications up to the Advanced

Diploma level, allowing graduates to enhance their job prospects or enter university.

Jakeman Business Solutions (JBS). JBS is both an IT services providers and an

accredited RTO that provides either tailor-made or “off-the-shelf” courses for corporate

needs.

CHART 2: ORGANISATIONAL STRUCTURE

Source: CGL FY15 Annual Report

3.2 Business history

Key events in CGL’s history are:

2007. CGL was formed following a merger of Jakeman Business Solutions (JBS) and

Frontier People, creating a business specialising in technology and government markets.

2008. CGL acquired Servicepoint to further complement its services.

2009. Diversified into the education and training sector by purchasing Australian Business

Academy (ABA), a registered training organisation (RTO) which has been operating since

1996.

November 2014. Listed on the Australian Stock Exchange.

May 2015. Strengthened its technology division purchasing PJA Solutions.

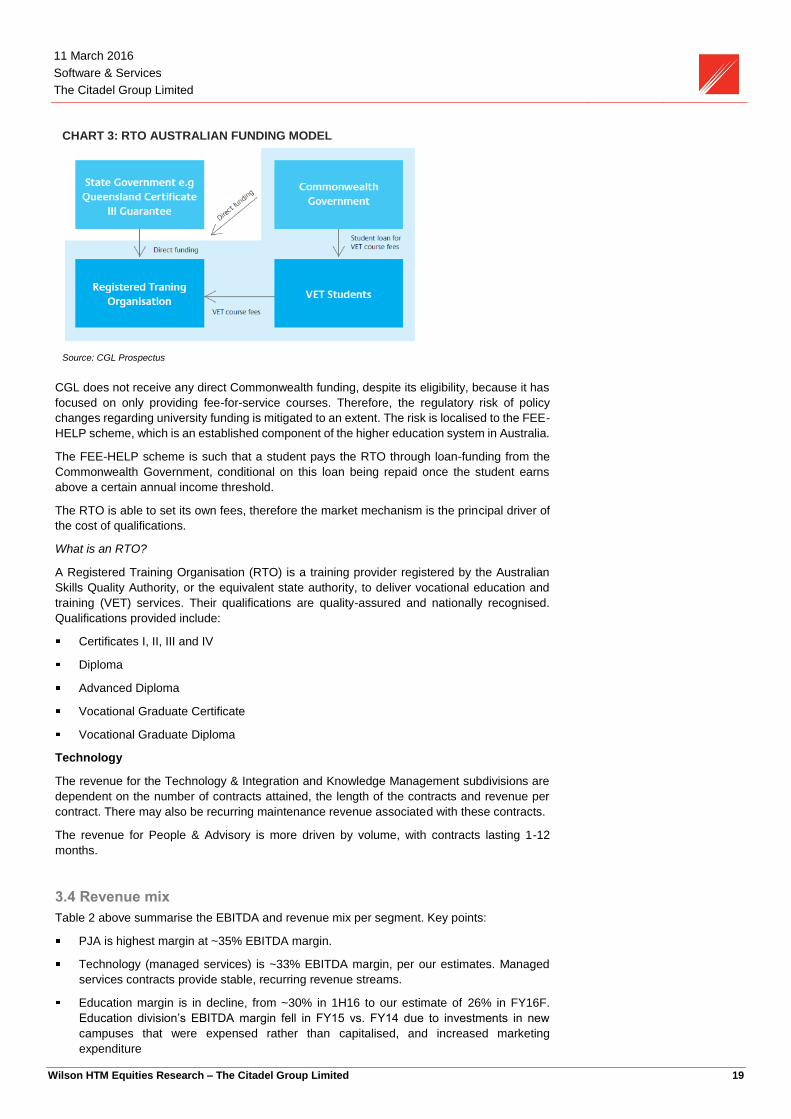

3.3 Revenue model

The revenue model of CGL differs across its respective divisions.

Education

The revenue model is a function of the number of students enrolled at the Australian Business Academy, and the average fee per

student (AFPS).

Education revenue is funded by the government via the FEE-HELP scheme, under the Registered Training Organisation (RTO)

funding model. Chart X.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 19

CHART 3: RTO AUSTRALIAN FUNDING MODEL

Source: CGL Prospectus

CGL does not receive any direct Commonwealth funding, despite its eligibility, because it has

focused on only providing fee-for-service courses. Therefore, the regulatory risk of policy

changes regarding university funding is mitigated to an extent. The risk is localised to the FEE-

HELP scheme, which is an established component of the higher education system in Australia.

The FEE-HELP scheme is such that a student pays the RTO through loan-funding from the

Commonwealth Government, conditional on this loan being repaid once the student earns

above a certain annual income threshold.

The RTO is able to set its own fees, therefore the market mechanism is the principal driver of

the cost of qualifications.

What is an RTO?

A Registered Training Organisation (RTO) is a training provider registered by the Australian

Skills Quality Authority, or the equivalent state authority, to deliver vocational education and

training (VET) services. Their qualifications are quality-assured and nationally recognised.

Qualifications provided include:

Certificates I, II, III and IV

Diploma

Advanced Diploma

Vocational Graduate Certificate

Vocational Graduate Diploma

Technology

The revenue for the Technology & Integration and Knowledge Management subdivisions are

dependent on the number of contracts attained, the length of the contracts and revenue per

contract. There may also be recurring maintenance revenue associated with these contracts.

The revenue for People & Advisory is more driven by volume, with contracts lasting 1-12

months.

3.4 Revenue mix

Table 2 above summarise the EBITDA and revenue mix per segment. Key points:

PJA is highest margin at ~35% EBITDA margin.

Technology (managed services) is ~33% EBITDA margin, per our estimates. Managed

services contracts provide stable, recurring revenue streams.

Education margin is in decline, from ~30% in 1H16 to our estimate of 26% in FY16F.

Education division’s EBITDA margin fell in FY15 vs. FY14 due to investments in new

campuses that were expensed rather than capitalised, and increased marketing

expenditure

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 20

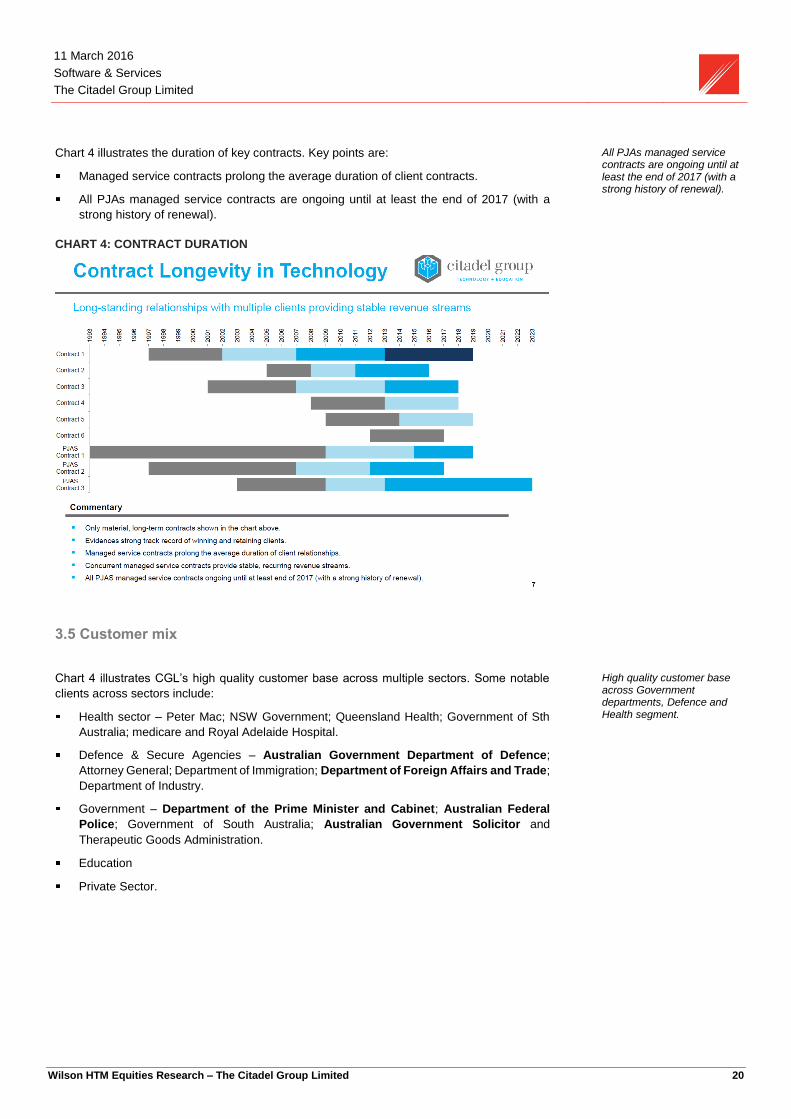

Chart 4 illustrates the duration of key contracts. Key points are:

Managed service contracts prolong the average duration of client contracts.

All PJAs managed service contracts are ongoing until at least the end of 2017 (with a

strong history of renewal).

All PJAs managed service contracts are ongoing until at least the end of 2017 (with a strong history of renewal).

CHART 4: CONTRACT DURATION

3.5 Customer mix

Chart 4 illustrates CGL’s high quality customer base across multiple sectors. Some notable

clients across sectors include:

Health sector – Peter Mac; NSW Government; Queensland Health; Government of Sth

Australia; medicare and Royal Adelaide Hospital.

Defence & Secure Agencies – Australian Government Department of Defence;

Attorney General; Department of Immigration; Department of Foreign Affairs and Trade;

Department of Industry.

Government – Department of the Prime Minister and Cabinet; Australian Federal

Police; Government of South Australia; Australian Government Solicitor and

Therapeutic Goods Administration.

Education

Private Sector.

High quality customer base across Government departments, Defence and Health segment.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 21

CHART 4: SELECTED CUSTOMER BASE

4. Board and management

We believe CGL has a strong Board, with appropriate seniority and experience to engage

with the Government, education and health care sectors at the appropriate levels.

We believe the management team is appropriately diverse, with a good skills mix that can

service CGL’s various customer segments.

4.1 Board of Directors

Mr H Kevin McCann AM

Kevin in the Non-Executive Chairman of Citadel. He is also the Chairman of Macquarie

Group Limited and a Director of Evans & Partners Ltd. Kevin is also a former Chairman of

ASX listed companies including Origin Energy Limited, an integrated energy company, and

Healthscope Limited.

He has a Bachelor of Arts and Law (Honours) from Sydney University and a Master of Law

from Harvard University. He practiced as a commercial lawyer and as a partner of Allens Arthur

Robinson from 1970 to 2004 and was Chairman of Partners from 1995 to 2004.

He is a Fellow of the Senate of the University of Sydney; Co-Vice Chair of the New Colombo

Plan Reference Group and a member the Australian Treasury Advisory Council (ATAC)

established by the Australian Treasury.

Dr Miles Jakeman

Miles is the Managing Director of Citadel. He has been Citadel’s Managing Director since

the Company’s inception. Miles is a visiting Fellow at the Australian National University, a

member of the Australian Institute of Company Directors and the ACT's Capital Angels. He is

also a member of the not-for-profit Kokoda Foundation, and Midnight Basketball Australia.

Miles has a Bachelor of Science (Hons), a Graduate Diploma in Asian Studies, a Doctorate of

Philosophy (PhD) in Asian Studies and a PhD in Business Leadership. He has also completed

the AICD Advanced Diploma Mastering the Boardroom and the AICD Diploma of International

Company Directors, plus holds an Advanced Diploma Project Management.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 22

For over 27 years, he has advised senior business leaders and government officials, including

representing countries in Ministerial forums. His key skills cover sales, marketing and business

development, business strategy, program management, security risk management and staff

development. Miles has significant overseas working experience with multinational companies.

Mr Mark McConnell

Mark is an Executive Director of Citadel. He has been a director of Citadel since its formation

in 2007. Mark is the Chairman or Director of several private companies, and recently joined the

board of the GWS Giants Foundation. Since 2007, he has been the Managing Director of

New Territories Investments, a private equity fund that has assisted the growth

strategies of multiple technology businesses in Australia, including Citadel.

Mark has a Bachelor of Science, a Graduate Diploma of Employment Relations, a Graduate

Diploma of Logistics Management, and a Masters of Business Administration. He is also a

Fellow of the Australian Institute of Company Directors (FAICD). Mark was awarded the ACT

Young Entrepreneur of the Year in 2003 and 2006.

After serving as an officer in the Royal Australian Air Force for 8 years, Mark moved into the

corporate world and has spent the last 17 years in a range of executive roles in the fields of

aviation, technology and investment finance. His skills cover areas of business strategy,

investor relations, capital raising and innovation. Mark has founded several private companies

and has been recognized with a number of entrepreneurial awards.

Ms Deena Shiff

Deena is a Non-Executive Director of the Citadel Group. She is currently the Deputy

Chairman at Export Finance & Insurance Corporation (EFIC), an NED at Ipscape which is a

venture capital-backed software business Chair of the Sydney Writers' Festival.

Deena holds a Bachelor of Science (Economics) from the London School of Economics and

Political Science and a Masters of Arts (Law) from the University of Cambridge. She is also a

Fellow of the Australian Institute of Company Directors.

She has extensive executive experience in the communications industry. She worked as a

Group Managing Director at Telstra Corporation Ltd between 2005 and 2013, during which

time she led the Wholesale Division, established Telstra’s Business Division dedicated to small

to medium enterprises and established Telstra’s corporate venture capital arm. Deena was

also a partner of Mallesons Stephen Jaques, in-house corporate counsel at Telstra and has

served as a senior executive and advisor on legal and social policy reforms for the Australian

Government.

Lieutenant General Peter Leahy AC(Retired)

Peter is a Non-Executive Director of the Citadel Group. He is a Director of Codan Limited

and Electro Optic Systems Holdings Limited. He is a member of the SA State Government’s

Defence South Australia Advisory Board. Not-for-profit positions include charities such as

Chairman of both Soldier On and the Red Shield Appeal Committee for the Australian Capital

Territory and as a Trustee of the Prince’s Charities Australia.

Peter holds a Master of Military Arts and Science from the US Army Command and General

Staff College, where he also served as an instructor and is a graduate of the Australian Institute

of Company Directors. He was awarded the Companion of the Order of Australia in 2007 for

eminent service to the Australian Defence Force in command of the Australian Army and

strategic staff appointments.

Peter retired from the Army in July 2008 after a 37 year career. He concluded his career in the

Army with the rank of Lieutenant General after a six year appointment as the Chief of Army.

After leaving the Army, he became a Professor of the University of Canberra and the foundation

Director of the National Security Institute where he teaches and continues to write on defence

and security matters.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 23

4.2 Management

We believe the recent hire of Darren Stanley has helped broaden the Citadel management

team and added to succession planning options.

Mr Darren Stanley

Deena is Chief Operating Officer and Deputy CEO of the Citadel Group.

Darren holds a Bachelor of Science (UNSW) and MBA (Deakin) and has also completed a

Harvard Business School program on Leading Professional Services Companies.

Darren was previously Managing Director of the ASX listed company SMS Management &

Technology Ltd (SMX), where he worked for ~12 years.

We believe the recent hire of Darren Stanley has helped broaden the Citadel management team and added to succession planning options.

Mr Robert (Andrew) Burns - Chief Financial Officer

Andrew has been the CFO and Citadel Company Secretary since January 2008.

Andrew is a Chartered Accountant, graduate of the AICD, as well as a Six Sigma Master

Black Belt and an alumni member of Australian Graduate School of

Management’s MBA Program.

Andrew has strong technical competencies in financial management, accounting, and process

improvement techniques. Prior to joining Citadel, Andrew spent 10 years with General Electric

in various senior leadership roles including Finance Manager of GE Healthcare ANZ and Six

Sigma Quality Leader for GE Healthcare Financial Services globally

Mr Michael McRoberts – Deputy Chief Financial Officer

Michael is the Group’s Deputy CFO and has been with the Group since 2012.

Michael holds a Bachelor of Commerce (Accounting), an MBA, and is completing a Bachelor

of Economics.

Prior to joining Citadel, Michael was a senior executive with the Department of Human Services

(DHS) with a strong track record in finance. Prior to DHS, Michael worked as a Systems

Accountant with AusAID and also completed a secondment to Ernst & Young in assurance and

advisory business services.

Mr Stephen Lynch – Capability Leader, Health Practice

Stephen joined Citadel in 2015 as Capability Leader – Health Practice of PJA Solutions.

Stephen has been with PJA Solutions since 2010 and has over 28 years’ experience in the

health sector in Australia and internationally.

Stephen was previously COO of Global Health Ltd (GLH), where he was active in e-Health

reforms and involved in projects for secure message delivery to GPs and other primary care

providers. Stephen also worked at Digital Equipment Corporation (DEC) as the Business

Development Manager for the health sector and remained in that role through their merger with

Compaq Computer Corporation (now Hewlett Packard). During this period Stephen established

DEC as the leading infrastructure supplier for health in Victoria and directed major projects into

Alfred Health, Austin Health, Melbourne Health Shared Services, Peter MacCallum and

Eastern Health.

Before this, Stephen also held General Manager and international executive sales positions

within IBA Healthcare which involved developing the sales strategy and managing the

operational delivery of projects and executive sales in domestic and international markets.

During his time at IBA Stephen directed major software implementation projects at St Vincent’s

and Royal Children’s Hospitals in Melbourne as well as several international projects.

Mr Andrew Pike - General Manager, Education & Training

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 24

Andrew joined Citadel in 2014 as General Manager of Australian Business Academy

following several years in executive and regional leadership roles. He has worked in both the

private and public sector including leading organisations such as Jacobs, Ernst & Young,

Nous Group and Westpac.

Andrew holds a Master of Business Administration, a Bachelor of Science (Psychology), and

a Graduate Diploma of Commercial Law.

Andrew’s previous roles involved responsibility for growing revenues and developing strong

teams. He has strong commercial skills supported by extensive experience in sales, client

service, project delivery and people management.

Mr Mike Ricketts – General Manager, Technology and Integration Division

Mike is responsible for the creation and management of the company footprint in Melbourne

and the expansion of operations in South Australia.

Mike has a Bachelor of Arts (Hons) and is based in Melbourne.

He has extensive experience working with medium and large businesses across a range of

industries with a particular emphasis on sales, operational leadership and change

management. His most recent experience in the technology space has seen him lead large

scale, complex deployments into the education and government sectors.

Prior to joining Citadel, Mike was the National Sales Manager/COO at Electroboard where he

was responsible for the Australian and New Zealand branch network (11 locations). He

managed key corporate accounts such as KPMG, Asciano, Woodside, Mars and Emerson.

Dr Matthew Smith - Program and Continuous Improvement Manager, PJA Solutions

Matthew has a long history as a senior associate with Citadel before becoming the General

Manager, Knowledge Management in 2014.

He has a PhD in Information Technology from the University of New South Wales. He

also holds a Masters of Information Science and a Bachelor of Science in Computer Science

& Economics.

Matthew brings with him a wealth of experience in leadership and program management.His

last role was as the General Manager of ABA, where he oversaw the substantial growth of

the business. Prior to this, Matthew ran the Defence enterprise content management account

for JBS.

5. Risks and catalysts

5.1 Regulatory risk

There is regulatory risk within CGL’s education business Australian Business Academy (ABA).

The ABA is reliant on government accreditation as a:

Regulated Training Organisation (RTO),

CRICOS (Commonwealth Register of Institutions and Courses for Overseas Students)

provider and

VET (vocational education and training) FEE-HELP provider.

ASQA

RTO providers face the risk of loss of licence, fines or suspension.

The VET sector is highly regulated with entry and on-going compliance requirements.

The Australian Skills Authority (ASQA) is responsible for RTO registration, course accreditation

and compliance with registration standards and conditions in all States apart from WA and

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 25

Victoria. WA’s regulator is the Training Accreditation Council (TAC) and Victoria has the

Victorian Registration and Qualifications Authority (VRQA).

RTO compliance includes:

Annual audit for training and assessment standards.

Adequate data management and reporting systems and insurances.

State Government funding imposes a further level of compliance with training and assessment

standards. Breaches can result in fines, suspension or de-registration.

In response to the adverse publicity of some unethical operators, Greens Senator Lee

Rhiannon has called a Senate inquiry which will be conducted by the Education and

Employment References Committee.

ASQA now monitors key data from RTOs including the following:

financial performance,

student outcomes,

employer surveys

enrolment numbers and

completion rates.

ASQA has extended ABA’s registration to 2nd June 2020 without requirement for an external

audit.

Government Funding

Loss of VET FEE-HELP accreditation can result in lost Government revenue.

CGL sources nearly 100% of its education revenue through the VET FEE-HELP system,

therefore the loss of VET FEE-HELP accreditation may result in students being unable to afford

ABA education.

VET-FEE HELP is essentially a loan from the Government to a student who is studying a VET

qualification, generally provided to students studying Diploma level or higher. An eligible

student must be an Australian citizen or permanent humanitarian visa holder who is a resident

in Australia for the duration of study

The student pays for the course directly to the education provider and is solely responsible for

servicing and repayment of the debt once an income threshold. The current VET FEE-HELP

limit is $97,728 for most students and the income threshold for compulsory repayment is

$54,126 for the 2015-16 income year.

This differs from government-subsidised courses where the State or Commonwealth

Government (or both) will fund the course fees, resulting in no net payment from the student.

The amount the student repays each year is calculated as a percentage of their repayment

income. The repayment percentage increases as income increases, but is capped at 8 per cent

of income. The ATO will calculate compulsory repayments for the year and includes it on the

student’s income tax notice of assessment.

Citadel’s ABA has specifically operated on a fee-for-service model to mitigate the funding risk

associated with government-subsidised courses. Of the 5,000 RTO’s nation-wide, only 235

have VET FEE-HELP accreditation.

Out of ABA’s 1,339 students in FY14, 96% of students paid for their fees using the VET FEE-

HELP scheme.

5.2 Contract risk

CGL’s Technology division is heavily reliant on the ability to win and renew key contracts.

Approx. 70% of tech revenues are locked in under managed services contracts, with all current

contracts ongoing until at least the end of 2017, with a strong history of renewal.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 26

Loss of key contracts presents a material downside risk to CGL, though this risk appears

mitigated by the above considerations.

5.3 Loss of key management personnel

Key management play an integral role in securing contracts, in what is a relationship-oriented

business (eg Department of Defence). Retired Lieutenant General Peter Leahy and former

RAAF officer Mark McConnell serve on CGL’s board and would provide a key conduit between

CGL and the government. Losing either of these two board members, or other key

management personnel would place some of CGL’s lucrative contracts at risk

We believe this risk has been mitigated somewhat by the recent hire of Darren Stanley, COO

and Deputy CEO. He was former MD of SMS Management and Technology (SMX).

5.4 Technology risk

Given 85% of revenues are derived from the Technology division, CGL faces technology risk.

This risk comes in the form of CGL’s technology offering becoming obsolete and superseded

by the offerings of its competitors. As a result, CGL must continually invest in its technology to

ensure that it remains competitive and relevant.

5.5 Acquisition risk

CGL’s stated aim is to pursue acquisitions using a mix of both debt and equity funding. While

we do not view CGL’s acquisitive nature negatively, risks do arise from acquisition selection

and integration. This becomes especially pertinent when debt financing is an option, however

this is mitigated by the current net cash position and strong cash generative nature of the

business model.

CGL must ensure that its acquisitions are carefully selected and integrated into its group of

companies, and that shareholders are not unnecessarily diluted or placed at risk through

leverage

5.6 Competition

CGL has a number of listed competitors in the Education and Technology spaces.

We believe that most listed ASX companies are not competitors to CGL in the education

segment, given they either operate in different segments or they have internal company

specific operating issues. Listed VET education competitors include Ashley Services

(ASX:ASH), Australian Careers Network (ASX:ACO, currently suspended from trading), Intueri

Education Group (ASX:IQE) and Redhill Education (ASX:RDH). We believe Navitas is most

likely to be a competitor to CGl.

Technology competitors include service integrators (eg. Accenture, KPMG Advisory), product

providers (eg. Microsoft, IBM), IT consultants (eg. Objective) and other consultants (eg. SMS

Management & Technology, UXC Ltd).

Healthtec competitors include companies like Orion Health Ltd (OHE).

5.7 Catalysts

Acquisitions

CGL stated at its FY15 results that it intends to target additional acquisitions, using both debt

and equity financing. This follows the highly accretive PJA Solutions acquisition in June 2015,

which is expected to add over $9.5m to FY16 EBITDA (82% of FY15 EBITDA).

Further acquisitions to bolster CGL’s presence in the IT consultancy space would likely be well

received by the market, should they deliver EPS accretion and strategic fit. CGL has

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 27

considerable headroom in its balance sheet to leverage, which should not negatively impact

solvency due to the highly cash generative nature of the business.

Winning/renewing contracts

CGL’s Technology division is highly dependent on winning/renewing contracts in order to

sustain and grow revenue and earnings in the long term.

The average length of contracts is 4.6 years, after which the revenue stream either ends or is

only legacy maintenance revenue. Therefore, it is crucial to the long-term success of CGL that

it is able to continue to win/renew contracts

Increased visibility

We believe CGL’s ehealth segment could be valued more highly if additional disclosure of key

value drivers was provided. There is the risk that PJA’s upside gets lost in the conglomerate

structure of CGL. We believe CGL should provide more insightful disclosure of key value

drivers on a regular and consistent basis.

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 28

The Citadel Group Limited (CGL)

BUSINESS DESCRIPTION

The Citadel Group Limited (CGL) is a trusted provider of education and technology solutions to a high quality customer base including government,

Defence and Health Departments.

INVESTMENT THESIS

We initiate coverage on Citadel Group Ltd (CGL) with a Buy recommendation and $5.77 share price target. CGL provides a range of trusted

technology and education solutions to high quality government, health and education sector clients. The share price is underpinned by annuity-like

managed service technology revenues of average 4.6 year duration. In the short-term, we expect management’s quality pedigree (ex-senior military

and Government professionals) will help secure new contracts wins and drive cross-sell. In the medium-term, we expect: (i) CGL will become a pure

play technology stock by exiting its education business; (ii) value-adding acquisitions which leverage CGL’s balance sheet flexibility and strong

acquisition skill set; and (iii) high growth from CGL’s leading position in electronic pathology information management.

REVENUE DRIVERS BALANCE SHEET

Education segment – number of students and revenue per

student.

Technology – Managed services contracts with an average ~4.6

year duration.

Strong balance sheet with net cash of $42m.

MARGIN DRIVERS BOARD

Cross-sales across the customer base and business units.

New contracts.

Kevin McCann, Chairman

Dr Miles Jakeman, MD

Mark McConnell, Executive Director

Deana Shiff

Lt General Peter Leahy (former Chief of Army)

KEY ISSUES/CATALYSTS MANAGEMENT

New contracts

Divestment of education business

Increased visibility into PJA Solutions driving a re-rating

Darrren Stanley, COO and Deputy CEO (former MD of ASx-listed

SMS)

Robert Burns, CFO

RISK TO VIEW CONTACT DETAILS

Contract losses

Regulatory change in education segment

www.citadelgroup.com.au

Citadel House, High Technology Park, Level 1, 11-13 Faulgin St,

ACT

11 March 2016

Software & Services

The Citadel Group Limited

Wilson HTM Equities Research – The Citadel Group Limited 29

Disclosures and disclaimers

Recommendation structure and other definitions

Definitions at http://www.wilsonhtm.com.au/Disclosures

Disclaimer

While Wilson HTM Ltd believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy

and persons relying on this information do so at their own risk. To the extent permitted by law Wilson HTM Ltd disclaims all liability to any person

relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage) however