Embed Size (px)

Citation preview

Barclays Global Consumer Staples Conference September 9, 2015

2

This presentation contains “forward-looking statements” within the meaning of U.S. federal securities laws. Forward-looking statements are not historical facts, and are based upon management’s current expectations, beliefs, projections and targets, many of which, by their nature, are inherently uncertain. Such expectations, beliefs, projections and targets are expressed in good faith. However, there can be no assurance that management’s expectations, beliefs, projections and targets will be achieved and actual results may differ materially from what is expressed in or indicated by the forward- looking statements. Forward-looking statements are subject to significant business, economic, regulatory and competitive risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the forward-looking statements, including risks detailed in Pinnacle Foods Inc.’s (“Pinnacle Foods,” “Pinnacle” or the “Company”) filings with the U.S. Securities and Exchange Commission (the “SEC”). Nothing in this presentation should be regarded as a representation by any person that these forward-looking statements will be achieved.

Forward-looking statements speak only as of the date the statements are made. The Company assumes no obligation to update forward-looking statements to reflect actual results, subsequent events or circumstances or other changes affecting forward-looking information except to the extent required by applicable securities laws.

This presentation includes certain financial measures, including Adjusted Gross Profit and Unleveraged Free Cash Flow, which differ from results using U.S. Generally Accepted Accounting Principles (GAAP). Non-GAAP financial measures typically exclude certain charges, which are not expected to occur routinely in future periods. The Company uses non-GAAP financial measures internally to focus management on performance excluding these special charges to gauge our business operating performance. Management believes this information is helpful to investors in understanding trends in the business. The most directly comparable GAAP financial measures and reconciliations to non-GAAP financial measures are set forth in the slides in this presentation and included in the Company’s filings with the SEC.

Forward-Looking Statements & Non-GAAP Financial Measures

3

Agenda Overview

Executing Our Strategy

Financial Update

Outlook

4

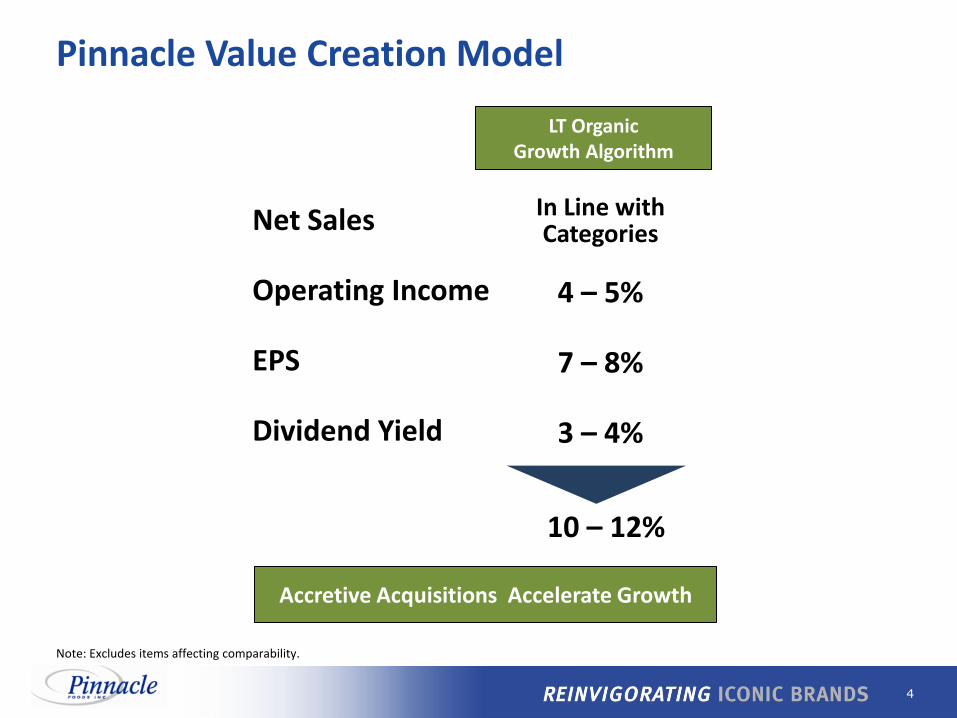

Pinnacle Value Creation Model

Net Sales

Operating Income

EPS

Dividend Yield

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

LT Organic Growth Algorithm

Accretive Acquisitions Accelerate Growth

Note: Excludes items affecting comparability.

5

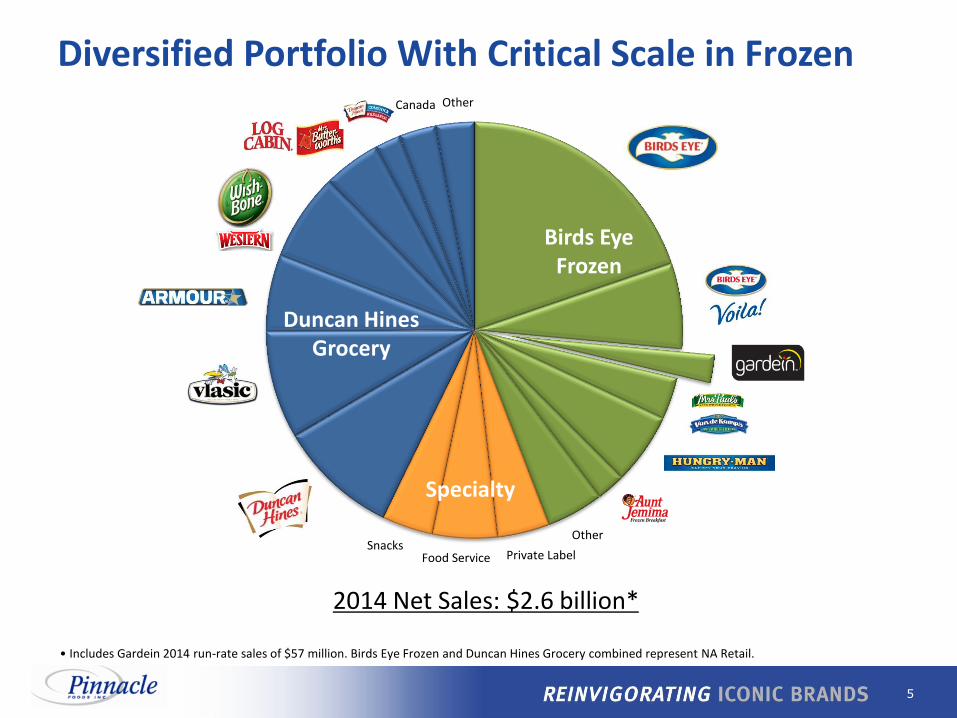

Birds Eye Frozen

Specialty

Duncan Hines Grocery

Other

2014 Net Sales: $2.6 billion*

Diversified Portfolio With Critical Scale in Frozen

• Includes Gardein 2014 run-rate sales of $57 million. Birds Eye Frozen and Duncan Hines Grocery combined represent NA Retail.

Canada

Snacks Food Service Private Label

Other

6

70% 77% 73%

80%

Net Sales

2014 2015 2014 2015

30% 23% 27%

20%

2014 2015 2014 2015

Invest in marketing to drive growth and share expansion

Focus on breakthrough innovation

Gross Profit Net Sales Gross Profit

Maintain stable sales/market position and cash flow

Focus on brand renovation

Leadership Brands Foundation Brands

(% of NA Retail) (% of NA Retail)

1st Half: 1st Half:

Portfolio Management Strategy

7

Net Sales

Operating Income

EPS

Dividend Yield

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

LT Organic Growth Algorithm

10%

39%

3%

Outpaced Categories

42%

2013 Actual

Accretive Acquisitions Accelerate Growth Beyond Algorithm

Note: Excludes items affecting comparability. See reconciliation to GAAP financial measures in Appendix.

17%

14%

2014 Actual

Outpaced Categories

3%

13%

Attractive Value Creation Results

8

Agenda Overview

Executing Our Strategy

Financial Update

Outlook

9

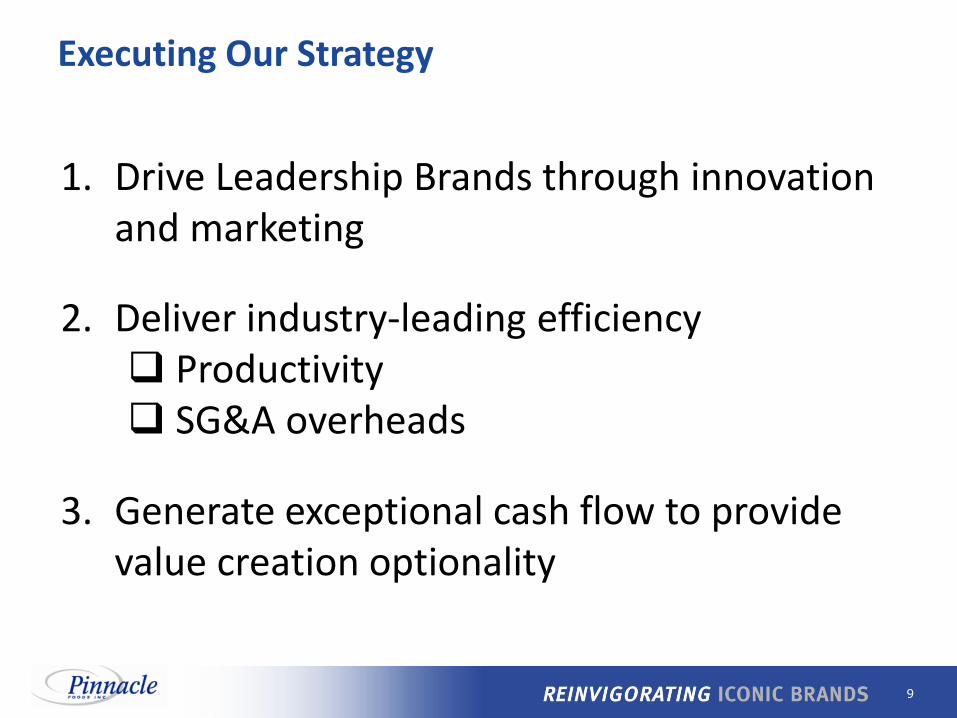

3. Generate exceptional cash flow to provide value creation optionality

1. Drive Leadership Brands through innovation and marketing

2. Deliver industry-leading efficiency Productivity SG&A overheads

Executing Our Strategy

10

Leadership Brands

Category

Pinnacle Market Position

Growing/ Holding Share

Frozen Vegetables #1

Frozen Complete Bagged Meals #1

Frozen Prepared Seafood #2

Frozen/Refrig. Meat Substitutes #4

Shelf-Stable Pickles #1

Table Syrups #1

Cake/Brownie Mixes and Frostings #2

Shelf-Stable Salad Dressings #3

Source: IRI US Multi-Outlet data, YTD ending 8/2/15; based on IRI’s Pinnacle custom definitions; market position ranks are among branded players.

Growth driven by strong performance of Leadership Brands

2012 2013 2014 2015 YTD

$ Market Share +0.1 pts. +0.3 pts. +0.2 pts. +0.5 pts.

(Change vs. PY)

Pinnacle Foods Composite Market Share

11

Innovation

Q2 Introductions

Flavor Full

Protein Blends

Q3 Introductions

Disney-themed sides

Voila! premium offerings

Marketing

New campaign supporting base business and new platforms

Television

Digital

Social

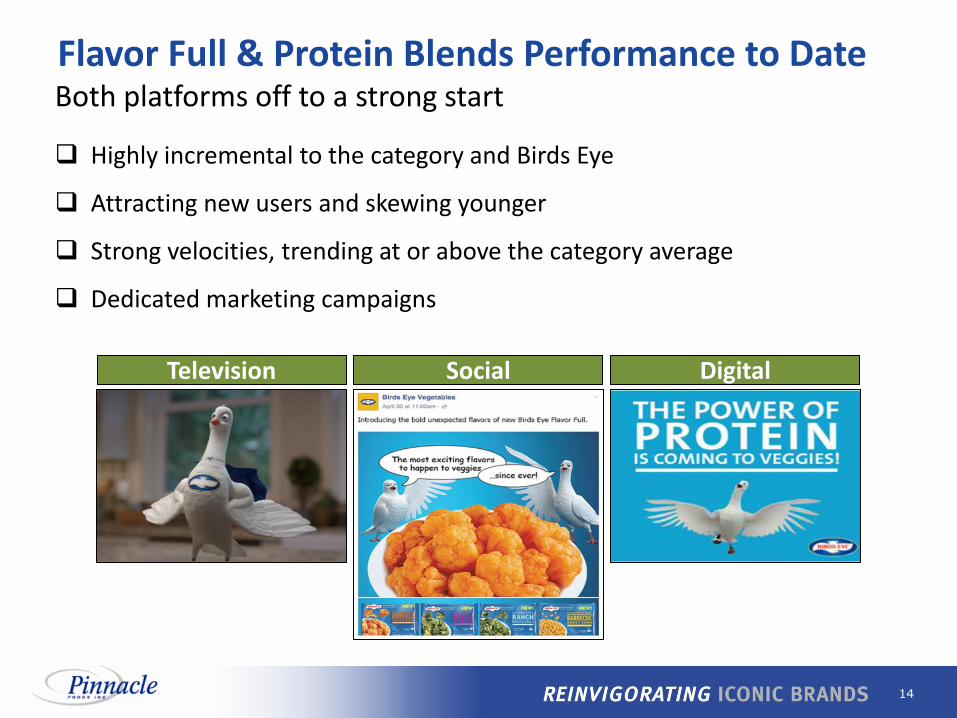

Birds Eye - $1 Billion Health & Wellness Brand Driving growth through innovation and marketing

12

Birds Eye Flavor Full Pairing of popular vegetables with on-trend flavors creates a perfect combination of taste and nutrition

13

Birds Eye Protein Blends Delivering plant-based protein benefit through the power of nutrient-rich vegetables, beans and whole grains

14

Both platforms off to a strong start

Highly incremental to the category and Birds Eye

Attracting new users and skewing younger

Strong velocities, trending at or above the category average

Dedicated marketing campaigns

Flavor Full & Protein Blends Performance to Date

Digital Television Social

15

Marketing Vegetables to Kids Birds Eye pioneered marketing vegetables to kids and continues to expand its reach

16

Birds Eye Disney-themed Sides Great-tasting, nutritious offering featuring key Disney characters

17

Regular Size

Family Size

15.7% 17.2% 21.1%

23.7%

28.0%

33.9%

39.8%

2009 2010 2011 2012 2013 2014 2015YTD

$ Market Share

Source: IRI US Multi-Outlet data; based on IRI’s Pinnacle custom definitions.

More than doubled share and grew consumption 88% since acquisition

2015 YTD consumption +16%

Adding capacity in Q4 2015

Birds Eye Voila! Vegetable-rich complete meals at a great value

18

New beef, pork and shrimp varieties in unique recipes

Priced at a 20% premium to chicken-based offerings

Birds Eye Voila! Innovation Expansion of Birds Eye Voila! with new premium price tier

19

Birds Eye Advertising New campaign supporting new platforms and base business, including dedicated advertising for Voila! for the first time

20

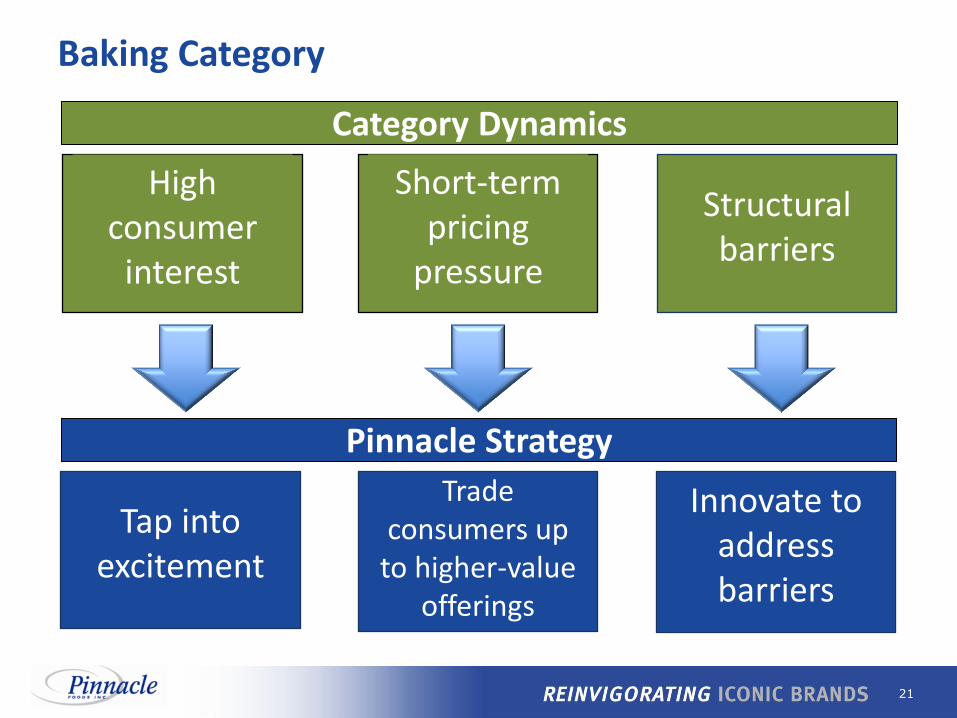

Baking Category

21

High consumer

interest

Structural barriers

Short-term pricing

pressure

Category Dynamics

Tap into excitement

Innovate to address barriers

Trade consumers up

to higher-value offerings

Pinnacle Strategy

Baking Category

22

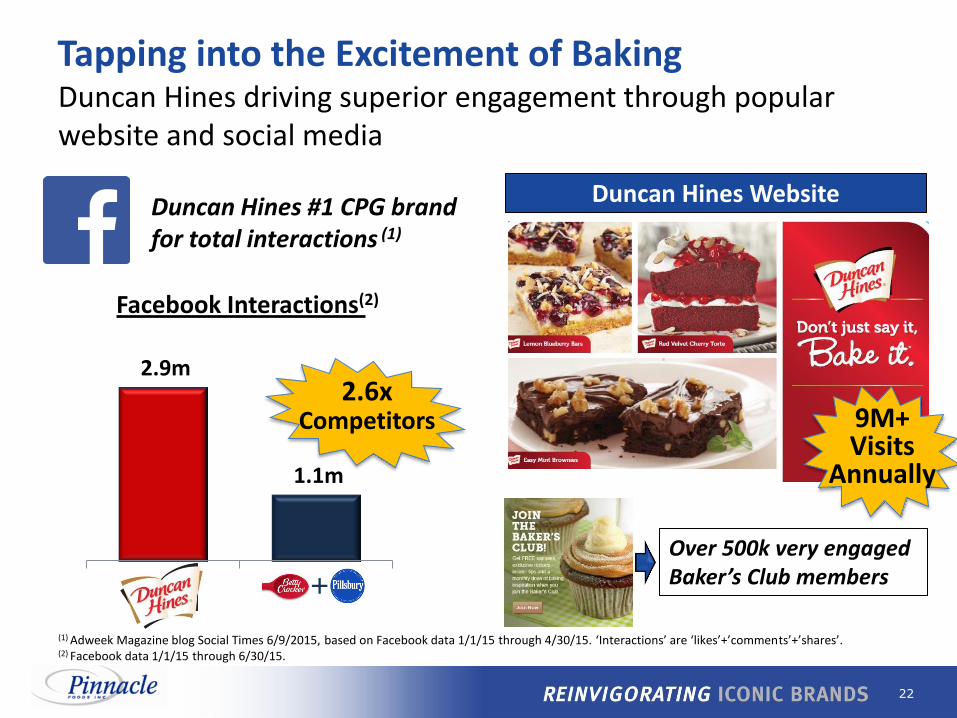

Tapping into the Excitement of Baking Duncan Hines driving superior engagement through popular website and social media

Duncan Hines Website

(1) Adweek Magazine blog Social Times 6/9/2015, based on Facebook data 1/1/15 through 4/30/15. ‘Interactions’ are ‘likes’+’comments’+’shares’. (2) Facebook data 1/1/15 through 6/30/15.

9M+ Visits

Annually

2.6x Competitors

Duncan Hines #1 CPG brand for total interactions (1)

2.9m

1.1m

+

Facebook Interactions(2)

Over 500k very engaged Baker’s Club members

23

Price Tier/ Benefit

Decadent Classic Signature

Tiered pricing and benefits strategy driving profitable market share growth…

Trading Consumers Up to Higher-Value Offerings

Source: IRI US Multi-Outlet data, YTD ending 8/2/15; based on IRI’s Pinnacle custom definitions. Price and share changes versus year ago.

Premium/ Extreme Indulgence

Entry Level/ Everyday Baking

Mid-Tier/ Special Recipes

$ Share ∆ 2014

+0.7 pts. 2015 YTD

-0.1 pts. 2014

+0.4 pts. 2015 YTD

+0.4 pts. 2014

+0.6 pts. 2015 YTD

+0.0 pts.

…with significant net price growth versus category in 2014 and 2015 YTD

24

Ideal for serving 2 to 4 people

Kit includes mix, frosting and 6-inch disposable pan

New premium baking kits positioned for smaller households

Innovating to Address Structural Barriers

25

Significant Consumer Excitement for Perfect Size

goobereena August 14 2015, 3:52 PM finally a cake mix for a single to 2 person household!!!

“Thank you for having a great new product called Perfect Size. There are only 2 of us and this is the

right amount of cake to bake for us…”

“…I bought it as it is the perfect size product for people who live alone and love cake. No more having to eat something for a week…”

“It's just me and my husband and every time I make a cake we end up throwing half of it away. These are, well, perfect!! What's not to love!”

Ioma August 1 2015, 7:19 PM Moist, flavorful, and just the right size. No waste. judy gambill August 7 2015, 2:48 PM

Thank you Duncan Hines!!! Finally someone thinks about 2 people families like mine now that we are retired...

“Thank you, thank you, thank you. I was making the other cakes and throwing them away after 2

days. Too much cake. Thank you so much!”

26

A Disciplined Approach to M&A

North America focus

Existing or adjacent categories

Market leadership or line of sight to leadership

Synergy-rich transactions

Speed of integration

27

Category remains highly competitive, with share below expectations

Profitability on track with acquisition model

In-house manufacturing start-up complete

Robust new product pipeline ready for launch in early 2016

Wish-Bone Update

28

Rapidly growing innovator of plant-based proteins

Broad portfolio of 25+ retail SKUs

Popular flavors and formats

Gardein Update Unique health & wellness platform

29

Results by Channel

Optimizing Vancouver plant capacity

Adding capacity at newly-acquired Hagerstown, MD site

Expansion Plans Underway

Award-winning plant-based protein offering positioned against key trends

Gardein Platform Opportunity

Traditional Natural & Organic

$ Consumption vs. PY +31% +41%

ACV Distribution +66% +87%

Avg. Items/Store +07% +06%

Source: IRI US Multi-Outlet data and SPINS US Natural data; consumption 12 weeks ended 7/12/15; ACV and items/store 4 weeks ended 7/12/15.

30

2015 New Products

31

Agenda Overview

Executing Our Strategy

Financial Update

Outlook

32

($m, except EPS) $ Vs. PY

Net Sales – Consolidated Net Sales – NA Retail

$1,297 $1,126

+2.8% +2.8%

Gross Margin 26.3% flat

Operating Income (EBIT) $182 +2%

Diluted EPS $0.75 +9%

Note: Gross Margin, Operating Income (EBIT) and Diluted EPS are on an adjusted basis. See reconciliation to GAAP financial measures in Appendix.

2015 First-half Financial Results Strong EPS growth driven by solid top-line performance and benefits of lower interest expense and effective tax rate

33

4.0% 4.1% 3.7% 3-4%

7.4%

2.3% 2.7% 3-3.5%

2012 2013 2014 2015E

Productivity Inflation

% of COGS

Productivity exceeded inflation in the past two years, enabling offset to weak industry growth

2015 2nd half gross margin expected to accelerate, benefitting from favorable productivity/inflation relationship

Business model calls for productivity to offset inflation over time

Productivity and Inflation

34

Conversion

Logistics

Proteins

Grains & Oils

Packaging Vegetables

& Fruit

All Other Sugar & Cocoa

2015 Cost of Goods Sold: $1.9 billion

More Inflationary

Logistics

Proteins

Conversion

Deflationary

Grains & Oils

Sugar & Cocoa

2015 Outlook

Diversity of cost basket serves as a natural hedge

2015 Input Cost Breakdown

35

2014 37.9%

One-time items benefitting 2014 +0.8%

2014 Ongoing 38.7%

Domestic Production Activities Deduction (DPAD)

Foreign Tax Credit (FTC)

Other

2015 Guidance 36.5% - 37.0%

ETR

Utilization of NOL benefit enables ETR reduction in 2015

2015 Effective Tax Rate (ETR)

Note: ETR is on an adjusted basis. See reconciliation to GAAP financial measures in Appendix.

36

$345 $325

$452 $400+

$0

$100

$200

$300

$400

$500

$600

$700

2012 2013 2014 2015E

Unleveraged Free Cash Flow (1)

~3%

~6%

Peer Average

Pinnacle Estimate

Free Cash Flow Yield (2)

($m)

(1) See reconciliation to GAAP financial measures in Appendix. (2) 2015E based on industry analysts’ valuation analyses using prices as of 8/28/2015.

Superior Free Cash Flow Generation Another year of strong cash flow expected in 2015…

…despite impact of strong crop season driving higher inventories

37

Key Drivers of Free Cash Flow

$2m $4m $8m

$17m

2012 2013 2014 2015E

$181m

$109m $96m $90m

2012 2013 2014 2015E

Minimal cash taxes and declining interest expense have fueled industry-leading free cash flow conversion

Minimal Cash Taxes

Significant NOLs benefit through 2015; residual benefit through 2027

Acquisition-related amortization tax shield through 2029

DPAD and FTC benefits start in 2015

Declining Interest Expense

Significant deleveraging; leverage ratio expected to decline to <4x in 2015

2013 refinancing and 2014 interest rate step-down

38

2012 2013 2014 2015E

Capital Expenditures

Capital Expenditures

Prudent investment against both acquisitions and the base business further supports strong cash flow

$78m $84m

$103m

$110m-$120m

Base Acquisition-related

Base Acquisition-related

39

After servicing debt and paying dividends at approximately 50% of net earnings, cash flow deployed to highest priorities:

Capital Allocation Strategy

Acquisitions #1

Debt Reduction #2

Share Repurchase #3

40

Agenda Overview

Executing Our Strategy

Financial Update

Outlook

41

Net Sales Growth exceeds categories

Inflation 3.0% to 3.5% of COGS Nm

Productivity 3% to 4% of COGS Nm

ETR 36.5% to 37.0%

Diluted EPS $1.89 to $1.91 +9% to +10%

CAPEX $110m to $120m

Note: Diluted EPS and ETR adjusted for items affecting comparability.

Outlook

H1 weighted

H2 weighted

H2 weighted

2015 Full Year Outlook

42

Attractive Value Creation Potential

Long-Term Organic Growth Algorithm

Net Sales

Operating Income

EPS

Dividend Yield

Note: Excludes items affecting comparability.

In Line with Categories

10 – 12%

4 – 5%

7 – 8%

3 – 4%

Accretive acquisitions would accelerate growth further

Realistic organic growth targets

Sustainable productivity program

Strong FCF providing optionality

Disciplined M&A approach with demonstrated value creation

43

Appendix

44

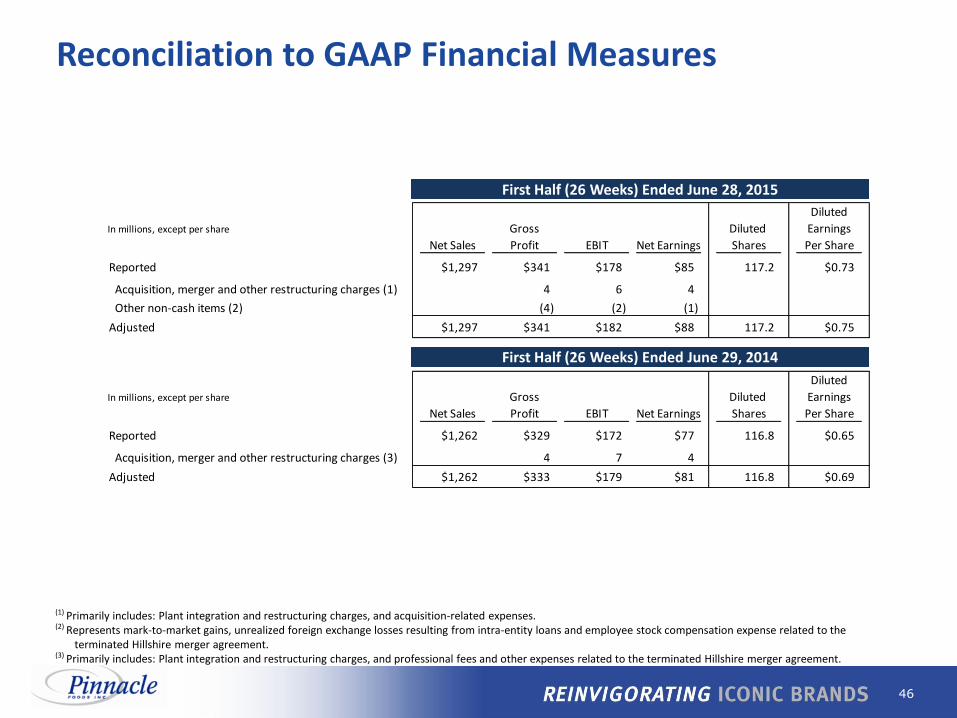

Reconciliation to GAAP Financial Measures

(1) Primarily includes: Hillshire agreement termination fee (net of costs), restructuring charges including integration costs, employee severance and non-recurring merger costs. (2) Primarily includes: Equity-based compensation expense resulting from liquidity event, fair value write-up of acquired inventories and mark-to-market gains/losses. (3) Primarily includes: Restructuring charges from plant consolidations, integration costs, non-recurring merger costs and employee severance. (4) Primarily includes: Bond redemption costs and management fee paid to sponsor. (5) Pro forma data reflects Adjusted Statement of Operations amounts assuming IPO and 2013 Refinancing occurred on the first day of Fiscal 2013.

Year (52 Weeks) Ended December 29, 2013

Diluted

In millions, except per share Gross Diluted Earnings

Net Sales Profit EBIT EBT Net Earnings Shares Per Share

Reported $2,591 $681 $512 $416 $248 116.9 $2.13

Acquisition, merger and other restructuring charges (1) 12 (130) (130) (79)

Other non-cash items (2) 18 41 41 34

Adjusted 2,591 711 423 327 203 116.9 $1.74

Diluted

In millions, except per share Gross Diluted Earnings

Net Sales Profit EBIT EBT Net Earnings Shares Per Share

Reported $2,464 $654 $293 $161 $89 108.6 $0.82

Acquisition, merger and other restructuring charges (3) 4 22 22 14

Other non-cash items (2) 6 6 6 3

Other adjustments (4) 53 76 55

Adjusted 2,464 664 374 265 161 108.6 $1.49

IPO and Refinancing (5) 26 16 8.0

Pro Forma $2,464 $664 $374 $291 $177 116.6 $1.52

Stock-based Compensation 1 8 8 6 0.05

Pro Forma Excluding Stock-based Compensation $665 $382 $299 $183 116.6 $1.57

Year (52 Weeks) Ended December 28, 2014

45

(1) Primarily includes: Accelerated depreciation from plant consolidations, restructuring charges including integration costs and employee severance. (2) Primarily includes: Bond redemption costs. (3) Pro forma data reflects Adjusted Statement of Operations amounts assuming IPO occurred on the first day of Fiscal 2012.

Diluted

In millions, except per share Diluted Earnings

Net Sales EBIT Net Earnings Shares Per Share

Reported $2,479 $284 $53 86.5 $0.61

Acquisition, merger and other restructuring charges (1) 45 28

Other adjustments (2) 21 23

Adjusted 2,479 350 104 86.5 $1.20

IPO (3) 30 30.9

Public company costs (3) (3) (2)

Pro Forma $2,479 $347 $132 117.4 $1.13

Year (53 Weeks) Ended December 30, 2012

Reconciliation to GAAP Financial Measures

46

(1) Primarily includes: Plant integration and restructuring charges, and acquisition-related expenses. (2) Represents mark-to-market gains, unrealized foreign exchange losses resulting from intra-entity loans and employee stock compensation expense related to the

terminated Hillshire merger agreement. (3) Primarily includes: Plant integration and restructuring charges, and professional fees and other expenses related to the terminated Hillshire merger agreement.

Diluted

In millions, except per share Gross Diluted Earnings

Net Sales Profit EBIT Net Earnings Shares Per Share

Reported $1,297 $341 $178 $85 117.2 $0.73

Acquisition, merger and other restructuring charges (1) 4 6 4

Other non-cash items (2) (4) (2) (1)

Adjusted $1,297 $341 $182 $88 117.2 $0.75

Diluted

In millions, except per share Gross Diluted Earnings

Net Sales Profit EBIT Net Earnings Shares Per Share

Reported $1,262 $329 $172 $77 116.8 $0.65

Acquisition, merger and other restructuring charges (3) 4 7 4

Adjusted $1,262 $333 $179 $81 116.8 $0.69

First Half (26 Weeks) Ended June 29, 2014

First Half (26 Weeks) Ended June 28, 2015

Reconciliation to GAAP Financial Measures

47

(1) Primarily includes: Restructuring charges from plant consolidations, integration costs, non-recurring merger costs and employee severance.

2012 2013 2014

Reported Cash Flows from Operating Activities $203 $262 $551

Capital expenditures (78) (84) (103)

Hillshire termination fee (net of costs and cash taxes) (150)

Acquisition, merger and other restructuring charges (1) 48 39 64

Free Cash Flow $173 $217 $362

Cash interest expense 172 108 90

Unleveraged Free Cash Flow $345 $325 $452

Reconciliation of Unleveraged Free Cash Flow to Reported Cash Flows from Operating Activities - $m

Reconciliation to GAAP Financial Measures

![Barclays Virtual Investor Conference 9-10-20.pptx [Read-Only]€¦ · Microsoft PowerPoint - Barclays Virtual Investor Conference 9-10-20.pptx [Read-Only] Author: 00081735 Created](https://img.pdfslide.us/doc/110x75/600f26791386122e333902a9/barclays-virtual-investor-conference-9-10-20pptx-read-only-microsoft-powerpoint.jpg)

![Barclays Wave v6 Final 25 Jun[1]](https://img.pdfslide.us/doc/110x75/546b0f9eb4af9f842c8b4ad5/barclays-wave-v6-final-25-jun1.jpg)

![Barclays capital radar strategy citywire stockholm final [read only]](https://img.pdfslide.us/doc/110x75/5472a2b9b4af9fa30a8b503d/barclays-capital-radar-strategy-citywire-stockholm-final-read-only.jpg)