Embed Size (px)

Citation preview

© 2014 Level 3 Communications, LLC. All Rights Reserved.

BAML Leveraged Finance Conference

December 3, 2014

© 2014 Level 3 Communications, LLC. All Rights Reserved. 2

200,000+ miles of fiber in over 60 countries

Over 13,000 employees across North America, LATAM, EMEA, Asia

Over $8 billion in annual revenue pro forma for tw telecom

~350 datacenter and colocation facilities

Level 3 is Local to Global

© 2014 Level 3 Communications, LLC. All Rights Reserved.

Fundamental Strategy

We want to be the premier provider of global communications

Enterprise is the growth engine for Level 3

Enterprise is about 70% of the combined company’s revenue

We are taking market share and we have a large opportunity to grow

To win in Enterprise we focus on Operational Excellence,

not just scale and price

Deliver a differentiated customer experience

Simplify our processes, tools, and systems

Our Wholesale business gives us scale, reach and efficiency

3

© 2014 Level 3 Communications, LLC. All Rights Reserved.

Enterprise is Level 3’s Growth Engine

2013 2014(3)(4)

Wholesale CNS Enterprise CNS

2011(1)(2)

~

~

71%

29%

(1) Level 3 standalone results

(2) FY2011 Wholesale CNS includes Europe revenue

(3) 2014 results are annualized based on the third quarter 2014 results for the combined company

(4) Combined company CNS revenue is adjusted for $60 million on an annualized basis related to intercompany eliminations 6

36%64%

$3B $5.6B $7.6B

$ in millions

59%

41%

© 2014 Level 3 Communications, LLC. All Rights Reserved.

Combination with tw telecom further strengthens the company’s position

New company size and trajectory leads to:

Increased breadth and scale of the combined company’s metro footprint, expanded

addressable market and service portfolio

Growing market opportunity as the competitive landscape shifts to favor our strengths and

our combined market share is still in the single digits

Our network, products and sales and marketing capabilities will give us complete customer

coverage from global multi-national corporations to medium-size businesses

Innovation in new products and services our customers need for their growth, efficiency and

security for the long term

Enhances credit and Free Cash Flow profile enables increase opportunity for de-leveraging,

investments and other value-enhancing opportunities

Creates a more focused, capable and powerful competitor to the incumbents and

provides choice to customers

Level 3 Going Forward

5

© 2014 Level 3 Communications, LLC. All Rights Reserved.

FINANCIALS

© 2014 Level 3 Communications, LLC. All Rights Reserved.

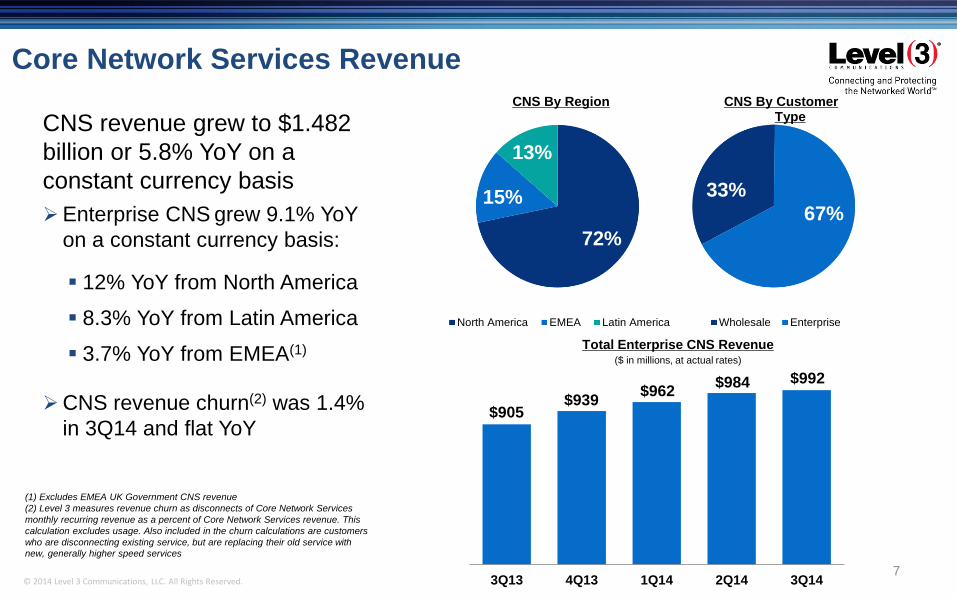

$905 $939

$962 $984 $992

3Q13 4Q13 1Q14 2Q14 3Q147

CNS By Region CNS By Customer TypeCNS revenue grew to $1.482

billion or 5.8% YoY on a

constant currency basis

Enterprise CNS grew 9.1% YoY

on a constant currency basis:

12% YoY from North America

8.3% YoY from Latin America

3.7% YoY from EMEA(1)

CNS revenue churn(2) was 1.4%

in 3Q14 and flat YoY

(1) Excludes EMEA UK Government CNS revenue

(2) Level 3 measures revenue churn as disconnects of Core Network Services

monthly recurring revenue as a percent of Core Network Services revenue. This

calculation excludes usage. Also included in the churn calculations are customers

who are disconnecting existing service, but are replacing their old service with

new, generally higher speed services

Total Enterprise CNS Revenue ($ in millions, at actual rates)

33%

67%

Wholesale Enterprise

72%

15%

13%

North America EMEA Latin America

Core Network Services Revenue

© 2014 Level 3 Communications, LLC. All Rights Reserved.

Year to date, capital expenditures

of 12.5% as a percent of total

revenue

Level 3 Adjusted EBITDA and Capital Expenditures

8

Continued double digit growth

in Adjusted EBITDA on a YoY

basis

Adjusted EBITDA(1)

($ in millions)

$404

$471

25.7%

28.9%

3Q13 3Q14

Adj EBITDA Adj EBITDA % of Total Revenue

$194 $204

3Q13 3Q14

Capital Expenditures($ in millions)

(1) Third quarter 2013 Adjusted EBITDA and resulting Adjusted EBITDA margin are adjusted to include the $11 million in bonus-related non-cash compensation expenses and to

exclude $30 million of severance charges

© 2014 Level 3 Communications, LLC. All Rights Reserved.

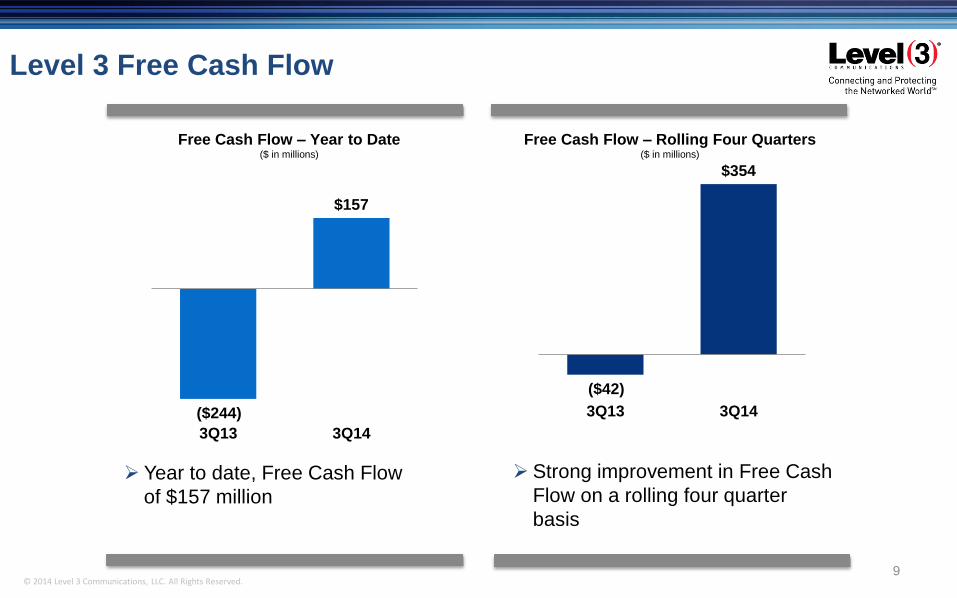

Level 3 Free Cash Flow

9

Free Cash Flow – Year to Date($ in millions)

($42)

$354

3Q13 3Q14

Free Cash Flow – Rolling Four Quarters ($ in millions)

Strong improvement in Free Cash

Flow on a rolling four quarter

basis

Year to date, Free Cash Flow

of $157 million

($244)

$157

3Q13 3Q14

© 2014 Level 3 Communications, LLC. All Rights Reserved.

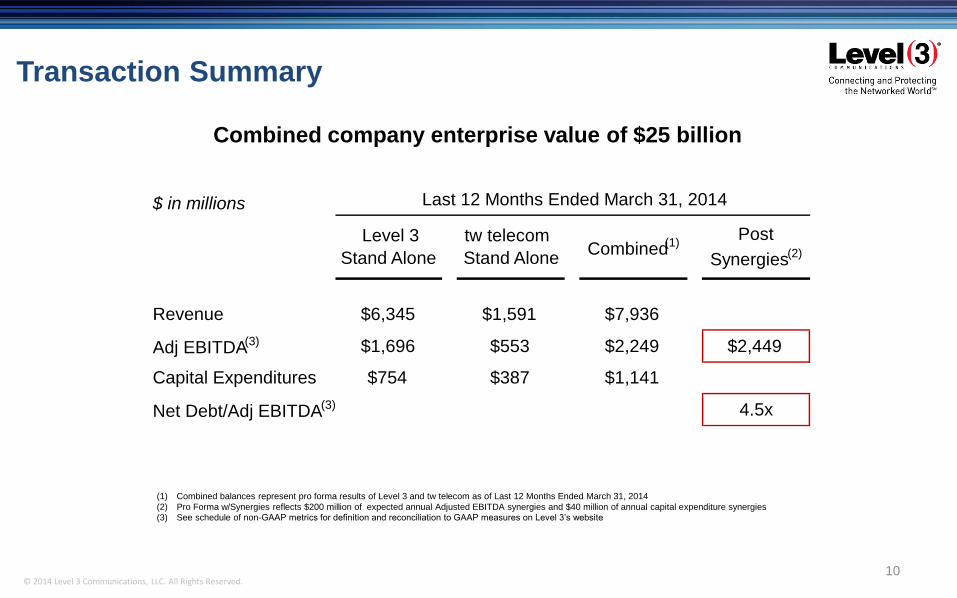

$ in millions

Revenue $6,345 $1,591 $7,936

Adj EBITDA(3) $1,696 $553 $2,249 $2,449

Capital Expenditures $754 $387 $1,141

Net Debt/Adj EBITDA(3) 4.5x

Last 12 Months Ended March 31, 2014

Level 3

Stand Alone

tw telecom

Stand AloneCombined(1)

Post

Synergies(2)

(1) Combined balances represent pro forma results of Level 3 and tw telecom as of Last 12 Months Ended March 31, 2014

(2) Pro Forma w/Synergies reflects $200 million of expected annual Adjusted EBITDA synergies and $40 million of annual capital expenditure synergies

(3) See schedule of non-GAAP metrics for definition and reconciliation to GAAP measures on Level 3’s website

Combined company enterprise value of $25 billion

Transaction Summary

10

© 2014 Level 3 Communications, LLC. All Rights Reserved. 11

Synergies Create Value

$240 million expected total run-rate

synergies

• $200 million of expected annualized run-rate Adjusted EBITDA savings

• Expect to achieve 70% of annualized Adjusted EBITDA savings within 18 months of closing

• $40 million of expected capital expenditure synergies

Expect integration costs of $170 million with: • 60% from operating expenses • 40% from capital expenditures• Expect to incur the majority of integration

expenses by the end of 2015

NPV of Expected Synergies of $2.2 billion

Annualized Adjusted EBITDA

Savings

55%45%

NetEx OpEx

© 2014 Level 3 Communications, LLC. All Rights Reserved.

$475 $300

$2,815

$3,471

$640

$3,600

2014 2015 2016 2017 2018 2019 2020 2021 2022

Pro Forma Debt Maturity Profile

16

Raised an aggregate of $3 billion through two capital markets transactions to facilitate the

closing of the tw telecom transaction

In the fourth quarter 2014, refinanced 11.875% Senior Notes with 5.75% Senior Notes due

2022, lowering cash interest expense

2015 maturity is 7% Convertible Senior Notes that convert at $27 per share

Continue to target lower end of leverage ratio of 3x-5x

No material maturities until 2019

Note: Maturity chart excludes capital leases and other debt of approximately $225 million

Pro forma

Q4 2014

($ in Millions)

© 2014 Level 3 Communications, LLC. All Rights Reserved.

Q&A