Embed Size (px)

Citation preview

1

PETROBRASPETROBRAS

Theodore M. Helms

Investors Relations Executive Manager

January, 2010

Pre-Salt Reservoir

2

The presentation may contain forecasts about future events. Such forecasts merely reflect the expectations of the Company's management. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forecasts. These predictions evidently involve risks and uncertainties, whether foreseen or not by the Company. Therefore, the future results of operations may differ from current expectations, and readers must not base their expectations exclusively on the information presented herein. The Company is not obliged to update the presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange

Commission permits oil and gas companies,

in their filings with the SEC, to disclose only

proved reserves that a company has

demonstrated by actual production or

conclusive formation tests to be

economically and legally producible under

existing economic and operating conditions.

We use certain terms in this presentation, such as oil and gas

resources, that the SEC’s guidelines strictly prohibit us from including in

filings with the SEC.

CAUTIONARY STATEMENT FOR US INVESTORS

DISCLAIMER

3

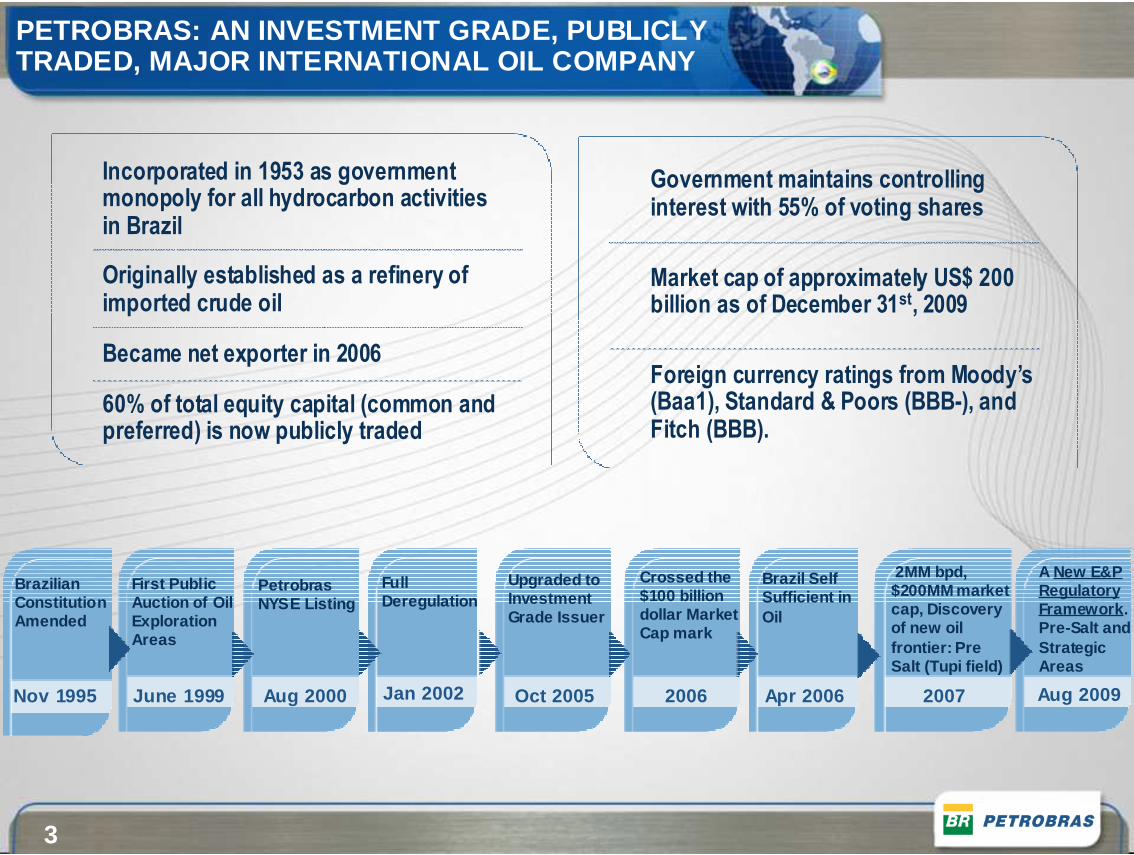

Government maintains controlling interest with 55% of voting shares

Market cap of approximately US$ 200 billion as of December 31st, 2009

Foreign currency ratings from Moody’s (Baa1), Standard & Poors (BBB-), and Fitch (BBB).

Incorporated in 1953 as government monopoly for all hydrocarbon activities in Brazil

Originally established as a refinery of imported crude oil

Became net exporter in 2006

60% of total equity capital (common and preferred) is now publicly traded

BrazilianConstitutionAmended

PetrobrasNYSE Listing

First PublicAuction of OilExplorationAreas

FullDeregulation

Brazil SelfSufficient in Oil

Upgraded toInvestmentGrade Issuer

Crossed the$100 billiondollar MarketCap mark

Nov 1995 Aug 2000June 1999 Jan 2002 Apr 2006Oct 2005 2006

2MM bpd, $200MM market cap, Discovery of new oil frontier: Pre Salt (Tupi field)

2007

A New E&PRegulatory Framework .Pre-Salt and Strategic Areas

Aug 2009

PETROBRAS: AN INVESTMENT GRADE, PUBLICLY TRADED, MAJOR INTERNATIONAL OIL COMPANY

4

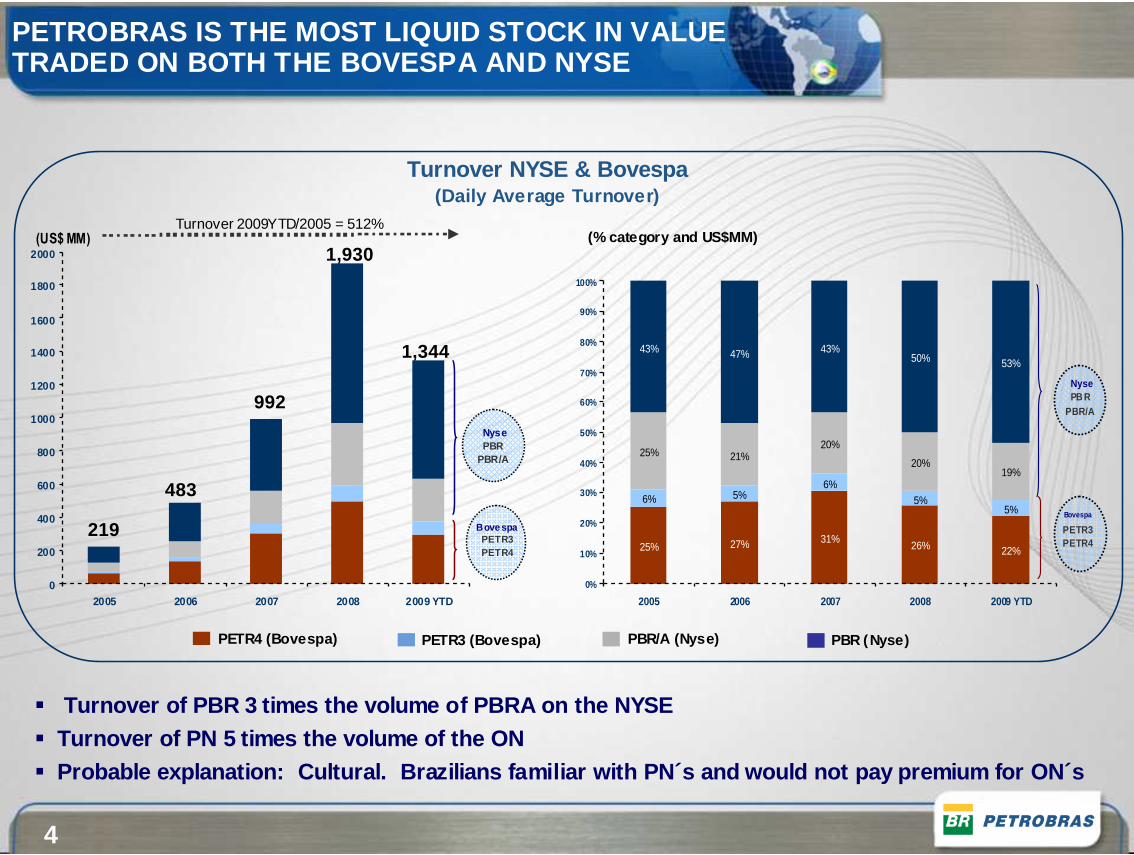

Turnover NYSE & Bovespa (Daily Average Turnover)

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2005 2006 2007 2008 2009 YTD

NysePBR

PBR/A

BovespaPETR3PETR4

(US$ MM)

25% 27% 31%26% 22%

6% 5%6%

5%5%

25% 21%20%

20%19%

43% 47% 43%50% 53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 YTD

NysePB R

PBR/A

Bovespa

PETR3PETR4

PETR4 (Bovespa) PBR/A (Nyse)PETR3 (Bovespa) PBR (Nyse)

(% category and US$MM)

1,344

1,930

992

483

219

Turnover 2009YTD/2005 = 512%

� Turnover of PBR 3 times the volume of PBRA on the N YSE� Turnover of PN 5 times the volume of the ON� Probable explanation: Cultural. Brazilians famili ar with PN´s and would not pay premium for ON´s

PETROBRAS IS THE MOST LIQUID STOCK IN VALUE TRADED ON BOTH THE BOVESPA AND NYSE

5

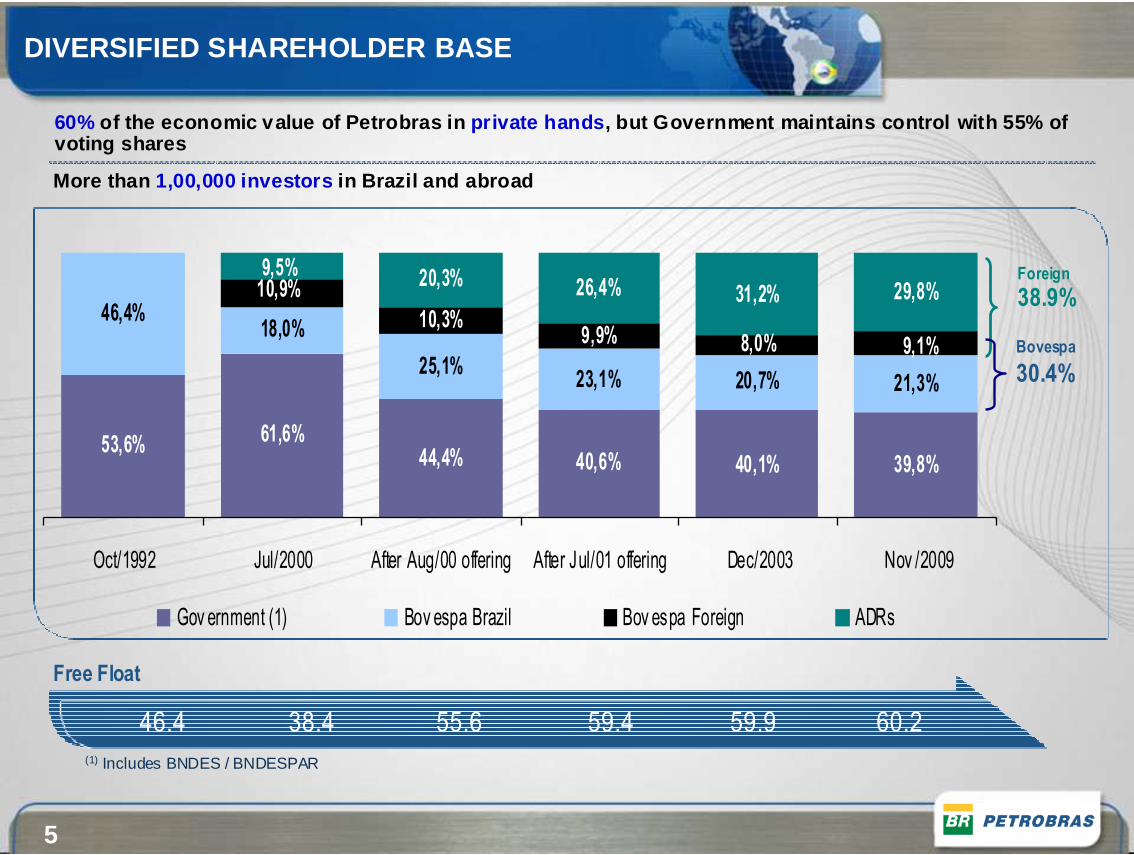

DIVERSIFIED SHAREHOLDER BASE

60% of the economic value of Petrobras in private hands , but Government maintains control with 55% of voting shares

More than 1,00,000 investors in Brazil and abroad

53,6% 61,6%44,4% 40,6% 39,8%

46,4%18,0%

25,1%23,1% 20,7% 21,3%

10,3%9,9% 8,0%

29,8%

40,1%

9,1%

10,9% 31,2%26,4%20,3%9,5%

Oct/1992 Jul/2000 After Aug/00 offering After Jul/01 offering Dec/2003 Nov /2009

Gov ernment (1) Bov espa Brazil Bov espa Foreign ADRs

Foreign

38.9%

Bovespa

30.4%

Free Float

46.4 38.4 55.6 59.4 59.9 60.2(1) Includes BNDES / BNDESPAR

6

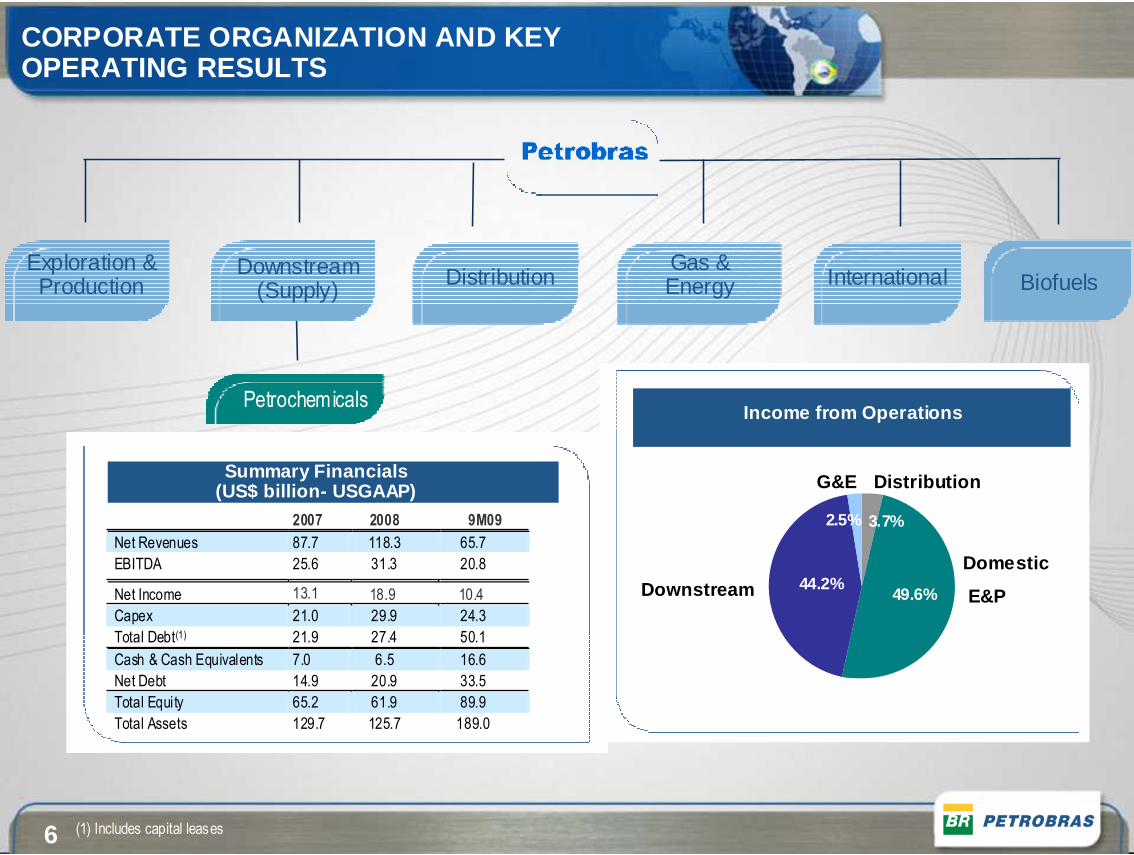

2007 2008 9M09

Net Revenues 87.7 118.3 65.7

EBITDA 25.6 31.3 20.8

Net Income 13.1 18.9 10.4

Capex 21.0 29.9 24.3

Total Debt(1) 21.9 27.4 50.1

Cash & Cash Equivalents 7.0 6.5 16.6

Net Debt 14.9 20.9 33.5

Total Equity 65.2 61.9 89.9

Total Assets 129.7 125.7 189.0

Exploration & Production

Downstream(Supply)

Gas & EnergyDistribution

Petrochemicals

International

Summary Financials (US$ billion- USGAAP)

(1) Includes capital leases

Biofuels

2.5% 3.7%

49.6%44.2%

Income from Operations

CORPORATE ORGANIZATION AND KEY OPERATING RESULTS

Domestic

E&PDownstream

G&E Distribution

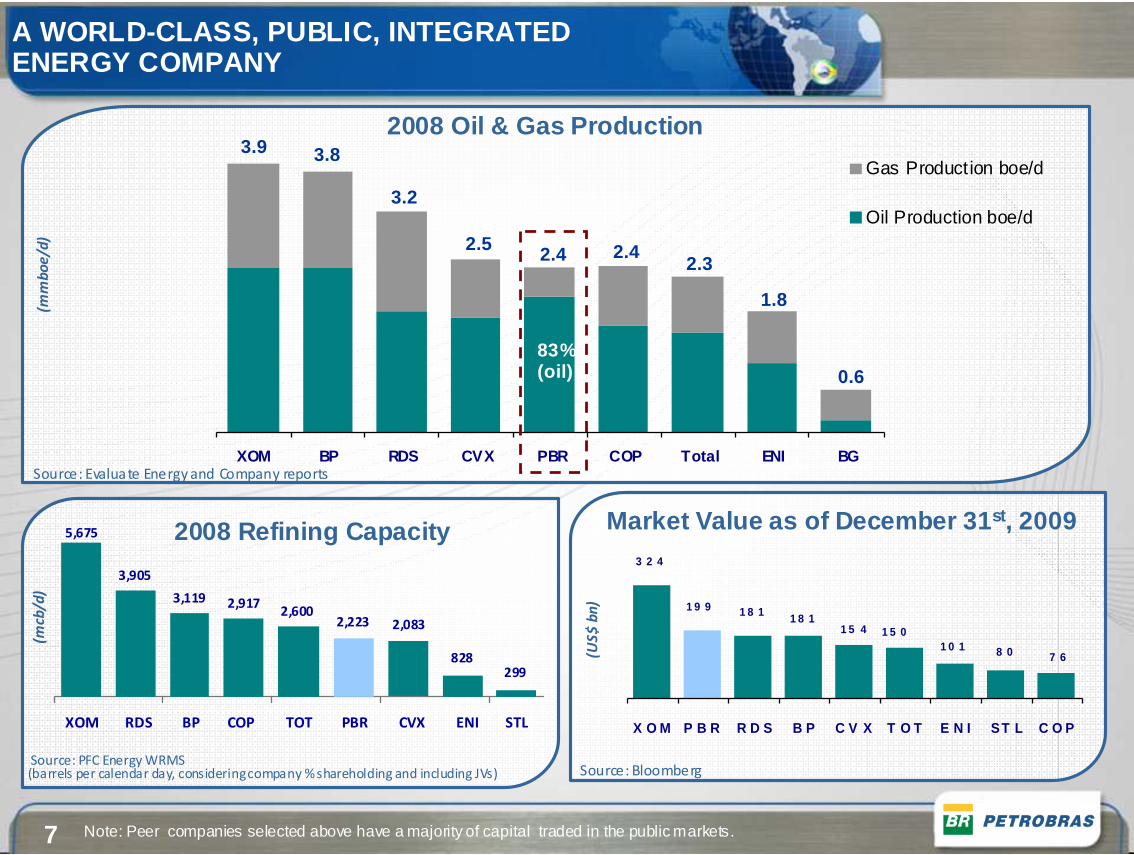

7

2008 Oil & Gas Production

2008 Refining Capacity

A WORLD-CLASS, PUBLIC, INTEGRATED ENERGY COMPANY

Note: Peer companies selected above have a majority of capital traded in the public markets.

Source: Evaluate Energy and Company reports

Source: PFC Energy WRMS (barrels per calendar day, considering company % shareholding and including JVs)

(mm

bo

e/d

)(m

cb/d

)

299828

2,223 2,083

5,675

2,6002,9173,119

3,905

XOM RDS BP COP TOT PBR CVX ENI STL

Market Value as of December 31 st, 20093 2 4

1 9 9 1 8 1

7 68 01 0 11 5 01 5 4

1 8 1

X O M P B R R D S B P C V X T O T E N I ST L C O P

(US

$ b

n)

Source: Bloomberg

XOM BP RDS CVX PBR COP Total ENI BG

Gas Production boe/d

Oil Production boe/d

3.9 3.8

3.2

2.5 2.4 2.42.3

1.8

0.683%(oil)

8

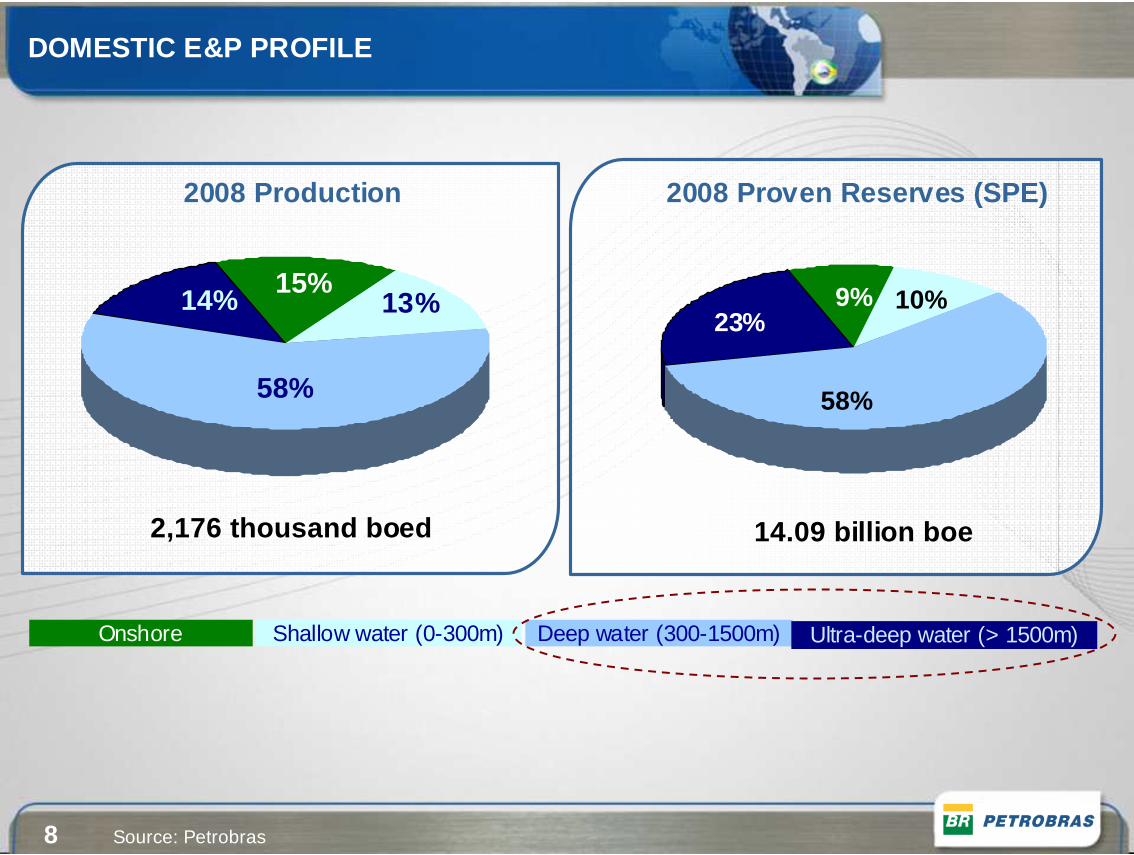

DOMESTIC E&P PROFILE

2008 Proven Reserves (SPE)

9% 10%

58%

23%

14.09 billion boe

Shallow water (0-300m)Onshore Deep water (300-1500m) Ultra-deep water (> 1500m)

Source: Petrobras

15%13%

58%

14%

2008 Production

2,176 thousand boed

9

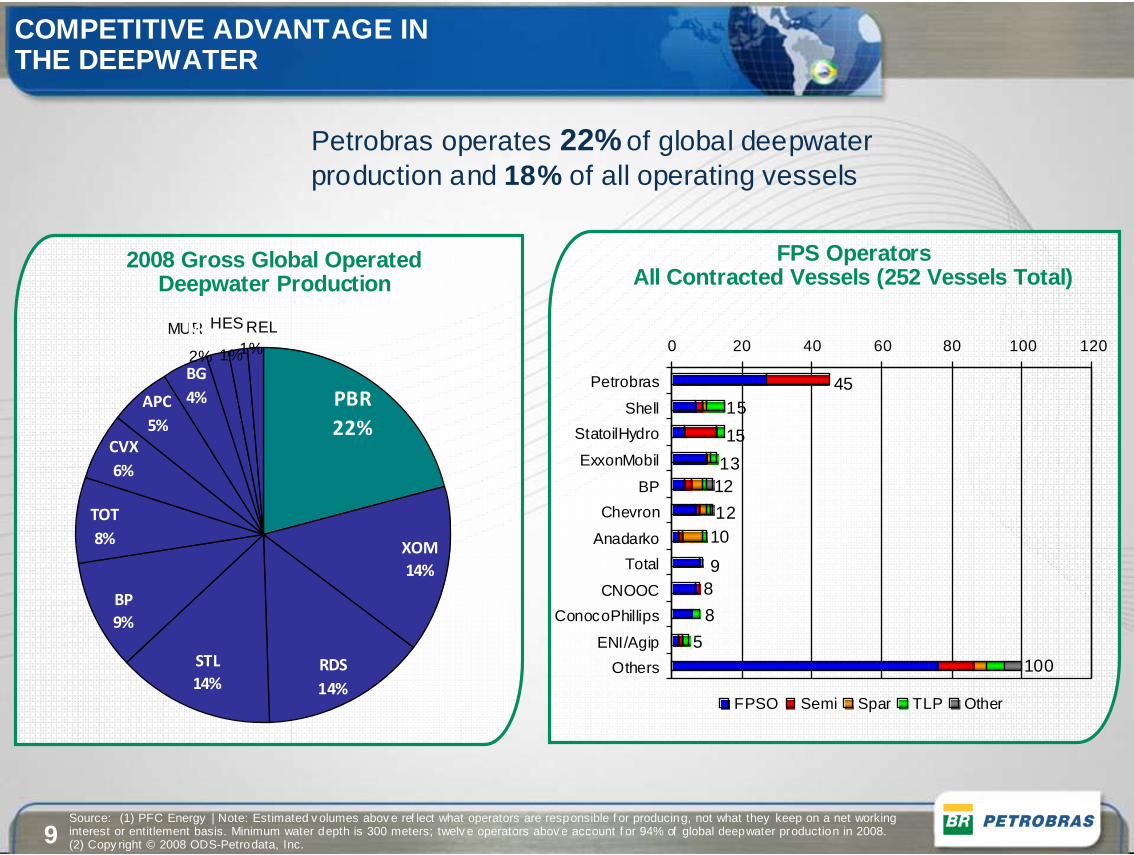

COMPETITIVE ADVANTAGE IN THE DEEPWATER

XOM

APC6%

MUR

Petrobras operates 22% of global deepwater production and 18% of all operating vessels

Source: (1) PFC Energy | Note: Estimated v olumes abov e ref lect what operators are responsible f or producing, not what they keep on a net working interest or entitlement basis. Minimum water depth is 300 meters; twelv e operators abov e account f or 94% of global deepwater production in 2008. (2) Copy right © 2008 ODS-Petrodata, Inc.

2008 Gross Global Operated Deepwater Production

PBR

22%

XOM

14%

RDS

14%

STL

14%

BP

9%

TOT

8%

CVX

6%

APC

5%

BG

4%

MUR

2%

REL

1%

HES

1%

2%

HES

1%1%REL

8

45

5

8

1012

13

15

15

100

9

12

0 20 40 60 80 100 120

Petrobras

Shell

StatoilHydro

ExxonMobil

BP

Chevron

Anadarko

Total

CNOOC

ConocoPhillips

ENI/Agip

Others

FPSO Semi Spar TLP Other

FPS OperatorsAll Contracted Vessels (252 Vessels Total)

10

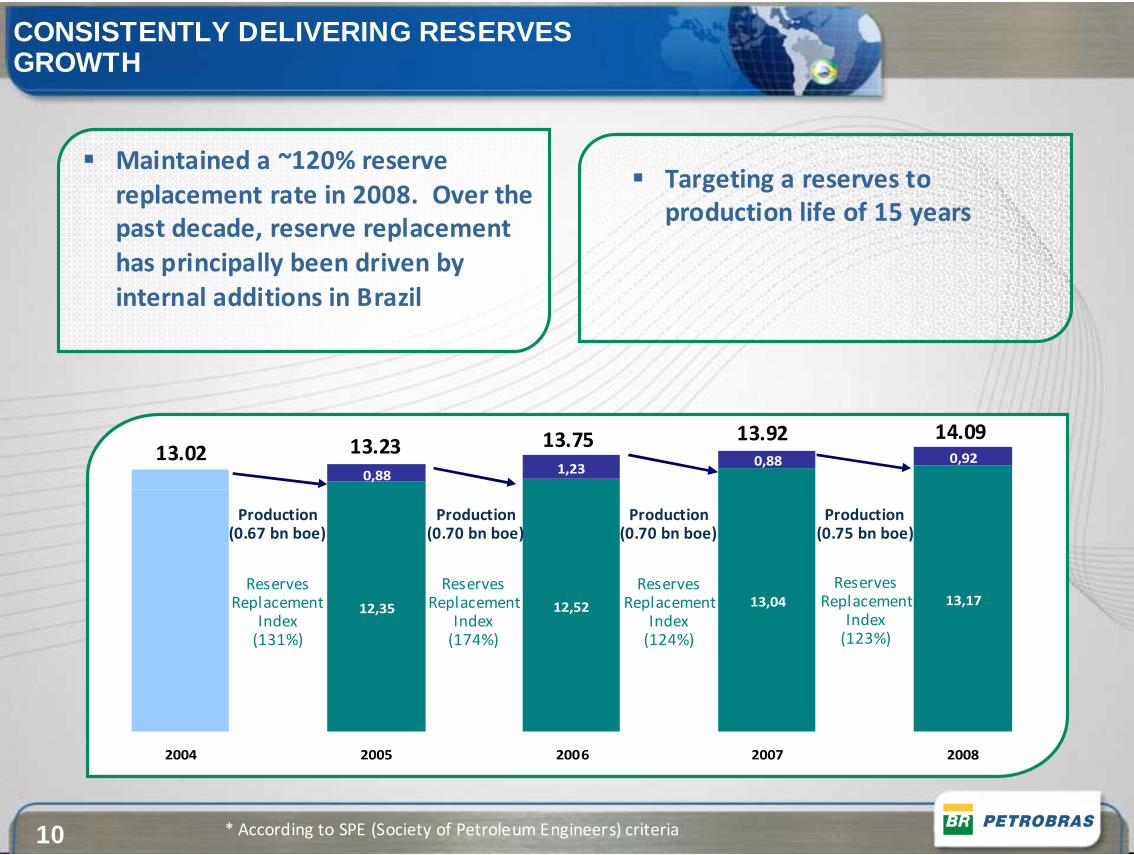

CONSISTENTLY DELIVERING RESERVES GROWTH

� Maintained a ~120% reserve

replacement rate in 2008. Over the

past decade, reserve replacement

has principally been driven by

internal additions in Brazil

� Targeting a reserves to

production life of 15 years

13,0412,3513,1712,52

0,880,88

0,921,23

2004 2005 2006 2007 2008

Production(0.70 bn boe)

13.02 13.23 13.75

Production(0.67 bn boe)

Reserves Replacement

Index(174%)

Reserves Replacement

Index(131%)

Production(0.75 bn boe)

Reserves Replacement

Index(123%)

Production(0.70 bn boe)

Reserves Replacement

Index(124%)

13.92 14.09

* According to SPE (Society of Petroleum Engineers) criteria

11

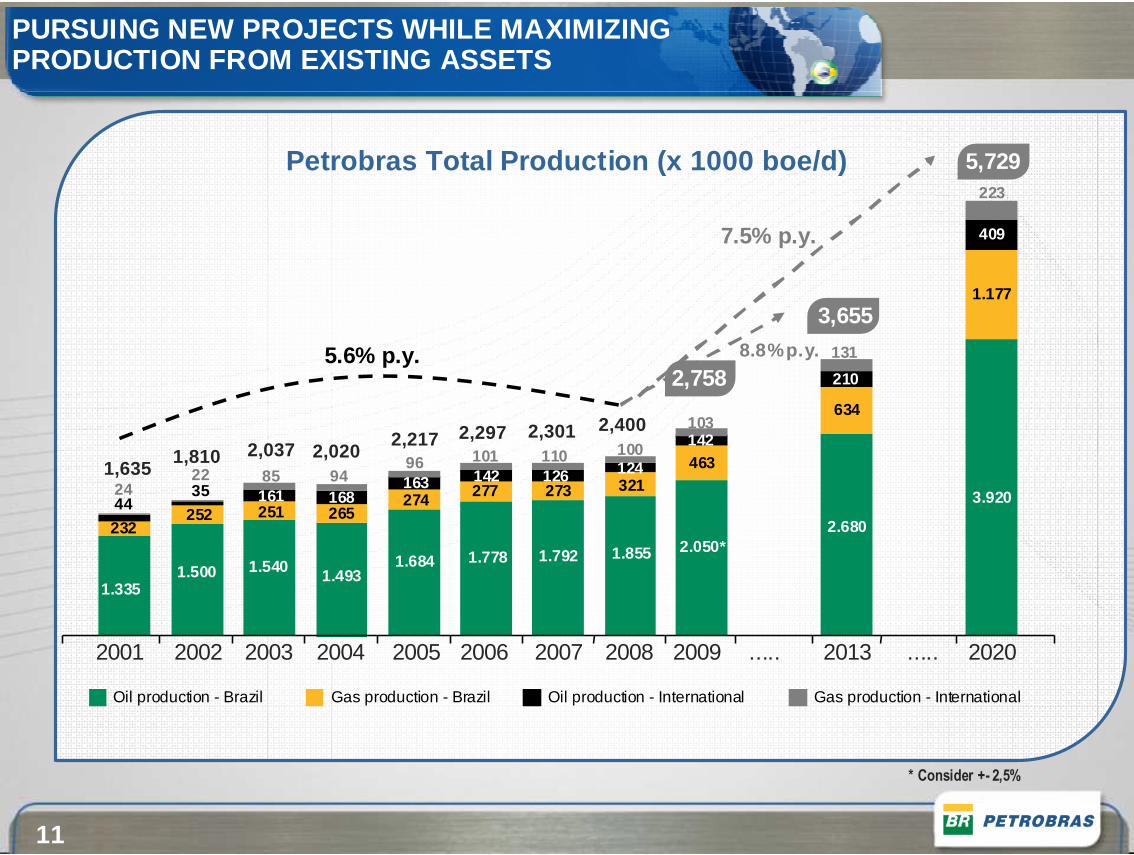

Petrobras Total Production (x 1000 boe/d)

1.335

232

4424

1.500

252

3522

1.540

25116185

1.493

26516894

1.684

27416396

1.778

277142101

1.792

273126110

1.855

321124100

2.050*

463142103

2.680

634

210

131

3.920

1.177

409

223

2001 2002 2003 2004 2005 2006 2007 2008 2009 ..... 2013 2020.....

* Consider +- 2,5%

8.8% p.y.

2,4002,3012,2972,2172,0202,0371,810

1,635

5.6% p.y.

7.5% p.y.

2,758

3,655

5,729

Oil production - Brazil Gas production - Brazil Oil production - International Gas production - International

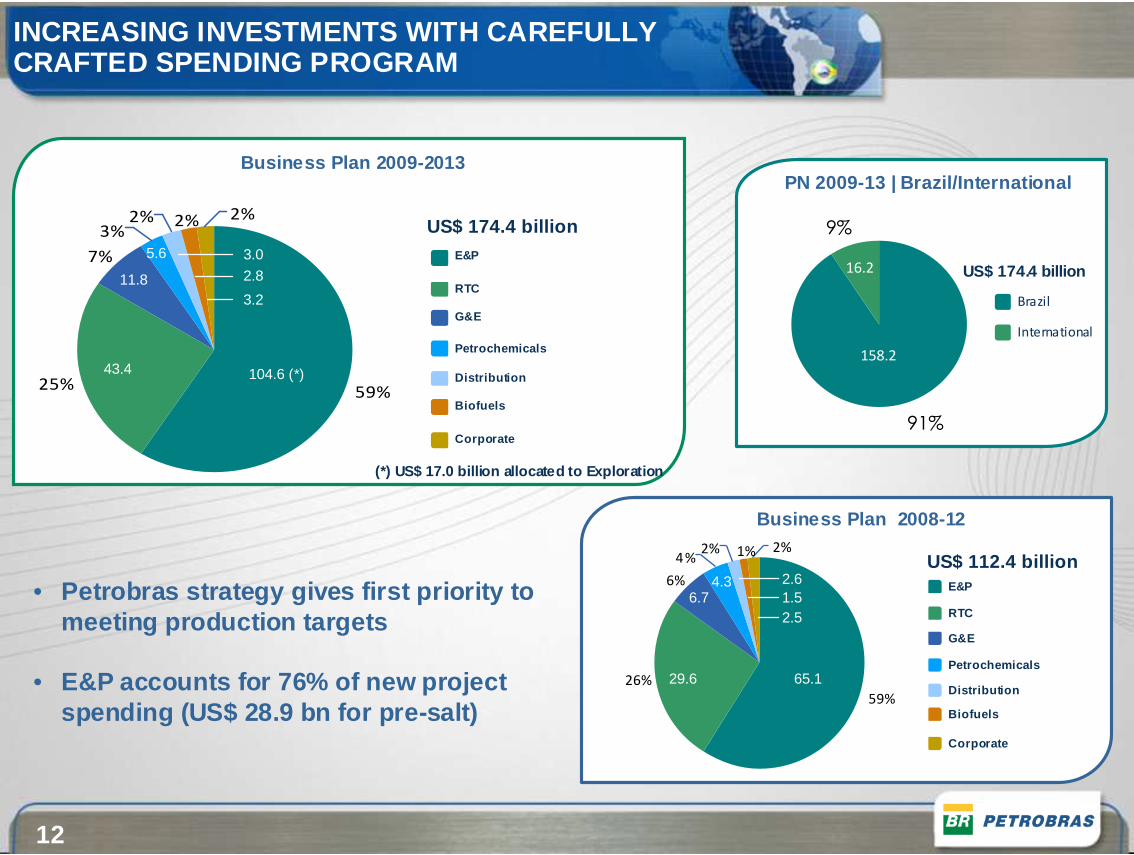

PURSUING NEW PROJECTS WHILE MAXIMIZING PRODUCTION FROM EXISTING ASSETS

12

Business Plan 2008-12

26%

1%2%

6%

4%2%

59%

E&P

RTC

G&E

Petrochemicals

Biofuels

Distribution

Corporate

US$ 112.4 billion

65.129.6

6.74.3 2.6

1.52.5

Business Plan 2009-2013

25%

2%2%

7%

3%2%

59%

E&P

RTC

G&E

Petrochemicals

Biofuels

Distribution

Corporate

US$ 174.4 billion

104.6 (*)43.4

11.8

5.6 3.0

2.8

3.2

(*) US$ 17.0 billion allocated to Exploration

INCREASING INVESTMENTS WITH CAREFULLY CRAFTED SPENDING PROGRAM

PN 2009-13 | Brazil/International

91%

9%

158.2

16.2

Brazil

International

US$ 174.4 billion

• Petrobras strategy gives first priority to meeting production targets

• E&P accounts for 76% of new project spending (US$ 28.9 bn for pre-salt)

13

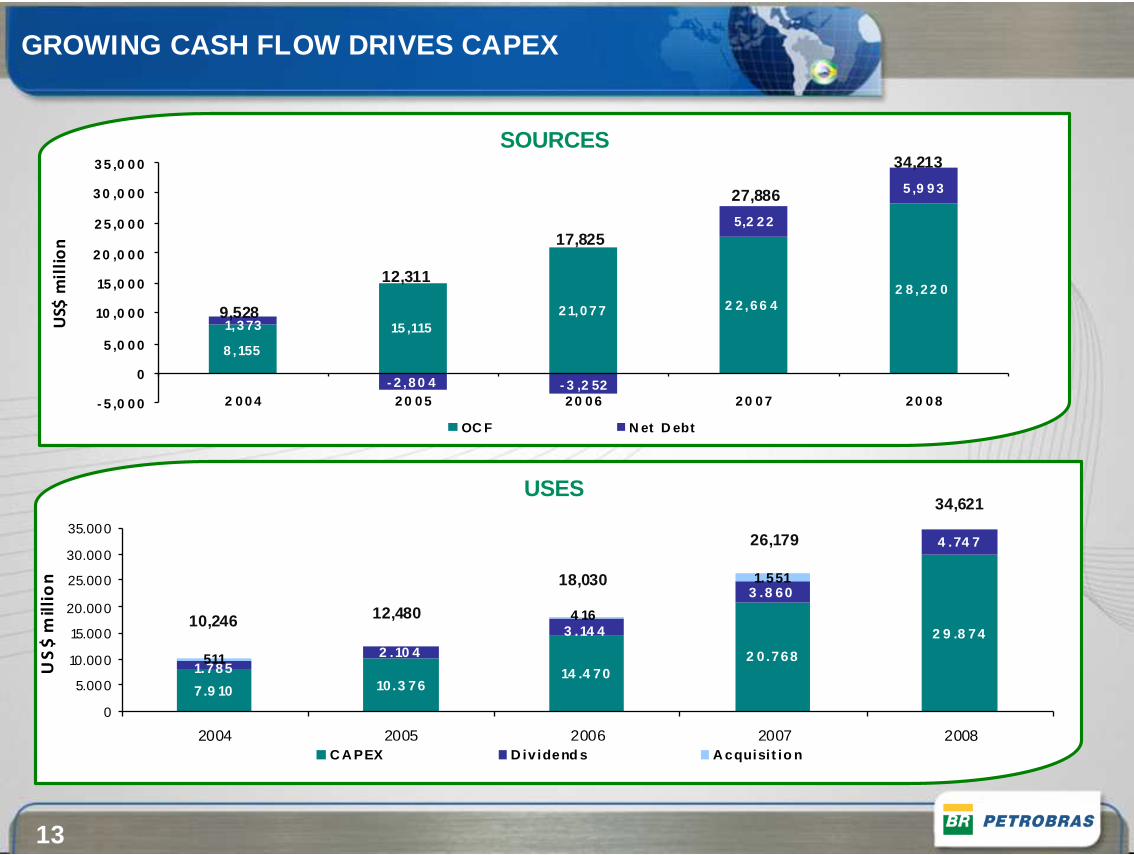

SOURCES

8 ,155

15 ,1152 1,0 7 7 2 2 ,6 6 4

2 8 ,2 2 0

5 ,9 9 3

5,2 2 2

- 3 ,2 52- 2 ,8 0 4

1,3 73

- 5 ,0 0 0

0

5 ,0 0 0

10 ,0 0 0

15 ,0 0 0

2 0 ,0 0 0

2 5 ,0 0 0

3 0 ,0 0 0

3 5 ,0 0 0

2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8

US$

mil

lio

n

OC F N et D ebt

USES

GROWING CASH FLOW DRIVES CAPEX

7.9 10 10.3 7614 .4 70

2 0.768

2 9 .8 742 .10 4

3 .8 60

4 .74 7

1.551

3 .14 4

1.785

4 16

511

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2004 2005 2006 2007 2008

US

$ m

illi

on

C A PEX D iv idend s A cquisi t io n

9,528

12,311

17,825

27,886

34,213

10,246

18,030

26,179

34,621

12,480

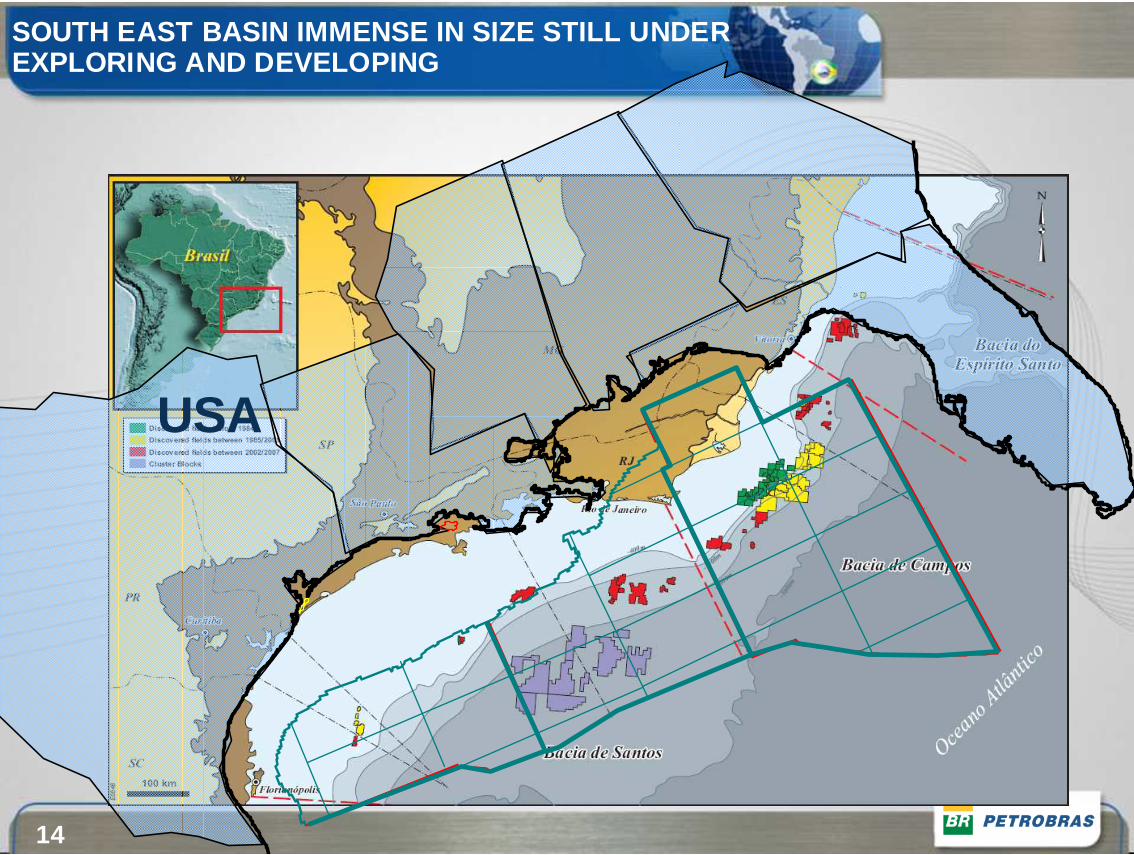

14 t

USA

SOUTH EAST BASIN IMMENSE IN SIZE STILL UNDER EXPLORING AND DEVELOPING

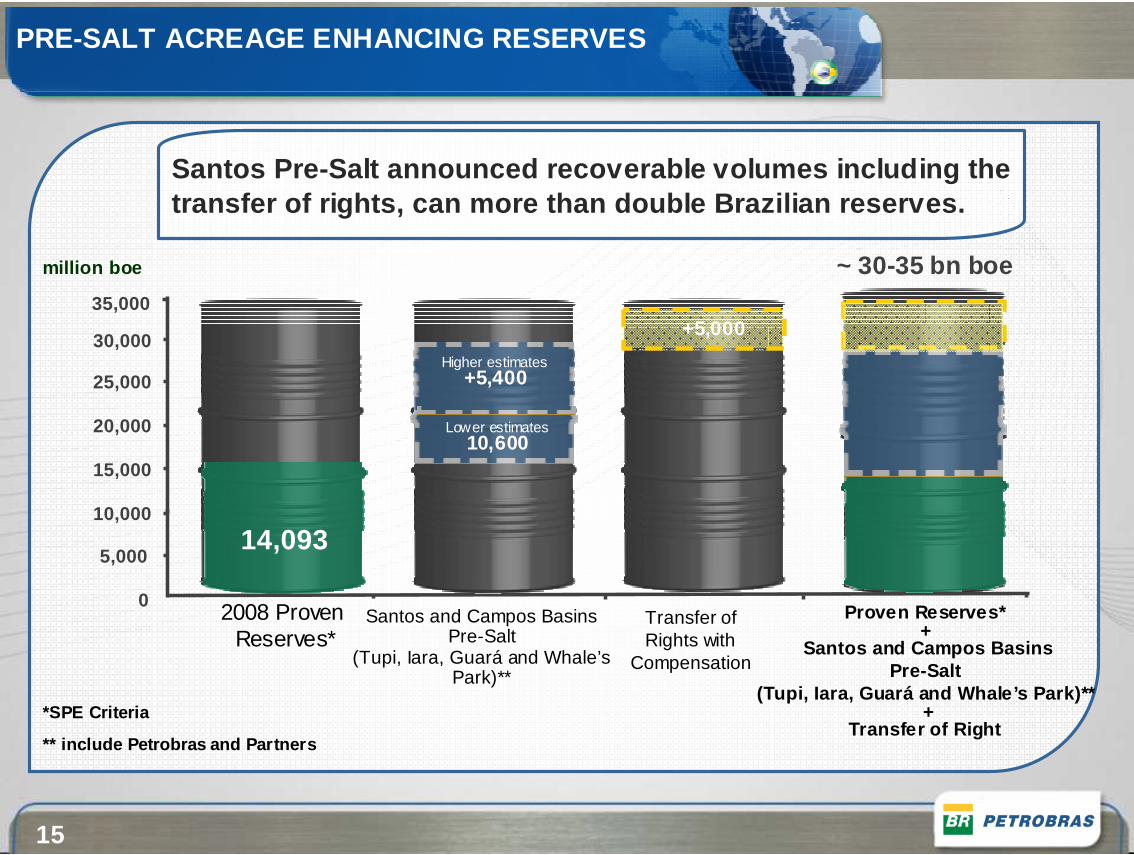

15

20,000

25,000

30,000

Santos and Campos BasinsPre-Salt

(Tupi, Iara, Guará and Whale’sPark)**

million boe ~ 30-35 bn boe

Proven Reserves* +

Santos and Campos BasinsPre-Salt

(Tupi, Iara, Guará and Whale’s Park)**+

Transfer of Right

5,000

10,000

15,000

2008 ProvenReserves*

14,093

0

PRE-SALT ACREAGE ENHANCING RESERVES

*SPE Criteria

** include Petrobras and Partners

Santos Pre-Salt announced recoverable volumes inclu ding the transfer of rights, can more than double Brazilian reserves.

Transfer ofRights with

Compensation

35,000

Higher estimates+5,400

Lower estimates10,600

+5,000

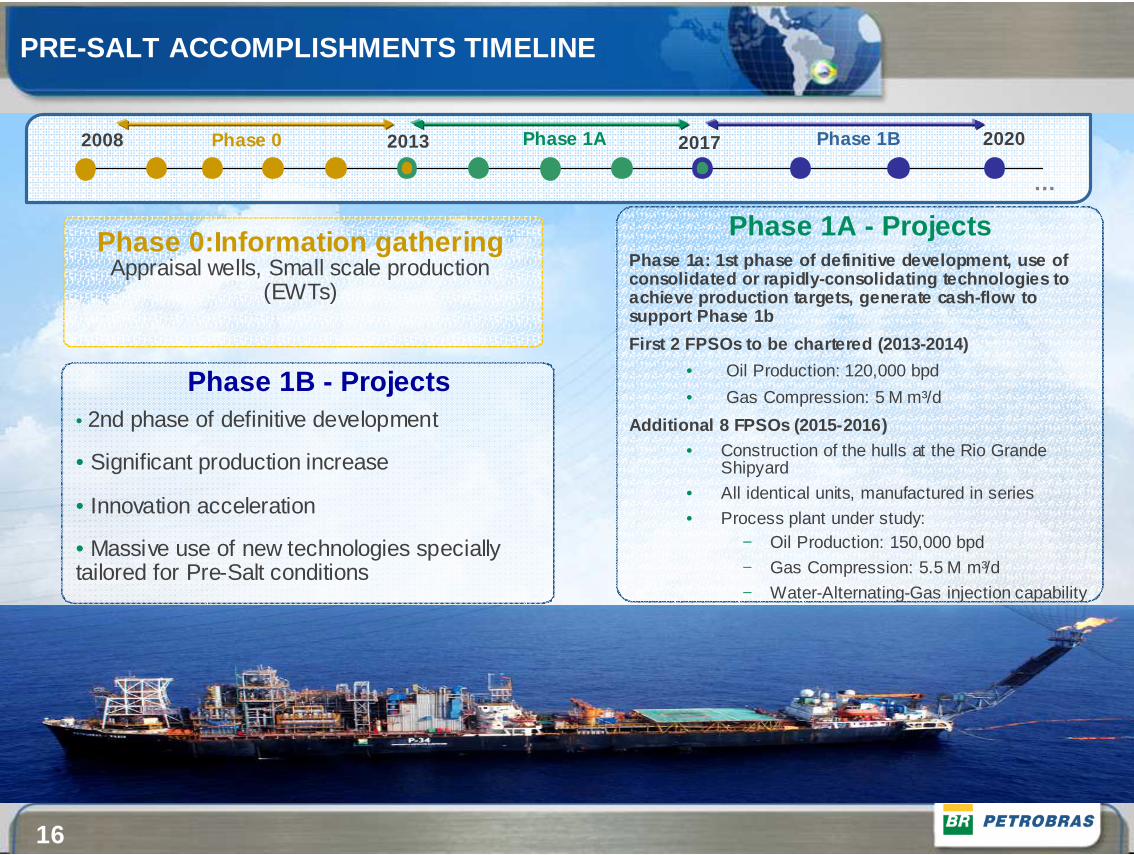

16

2017 2020Phase 1A Phase 1B

…

2013

Phase 1a: 1st phase of definitive development, use of consolidated or rapidly-consolidating technologies to achieve production targets, generate cash-flow to support Phase 1b

First 2 FPSOs to be chartered (2013-2014)

• Oil Production: 120,000 bpd

• Gas Compression: 5 M m³/d

Additional 8 FPSOs (2015-2016)• Construction of the hulls at the Rio Grande

Shipyard

• All identical units, manufactured in series

• Process plant under study:− Oil Production: 150,000 bpd

− Gas Compression: 5.5 M m³/d

− Water-Alternating-Gas injection capability

Phase 1A - Projects

Phase 1B - Projects• 2nd phase of definitive development

• Significant production increase

• Innovation acceleration

• Massive use of new technologies specially tailored for Pre-Salt conditions

Phase 0:Information gatheringAppraisal wells, Small scale production

(EWTs)

2008 Phase 0

PRE-SALT ACCOMPLISHMENTS TIMELINE

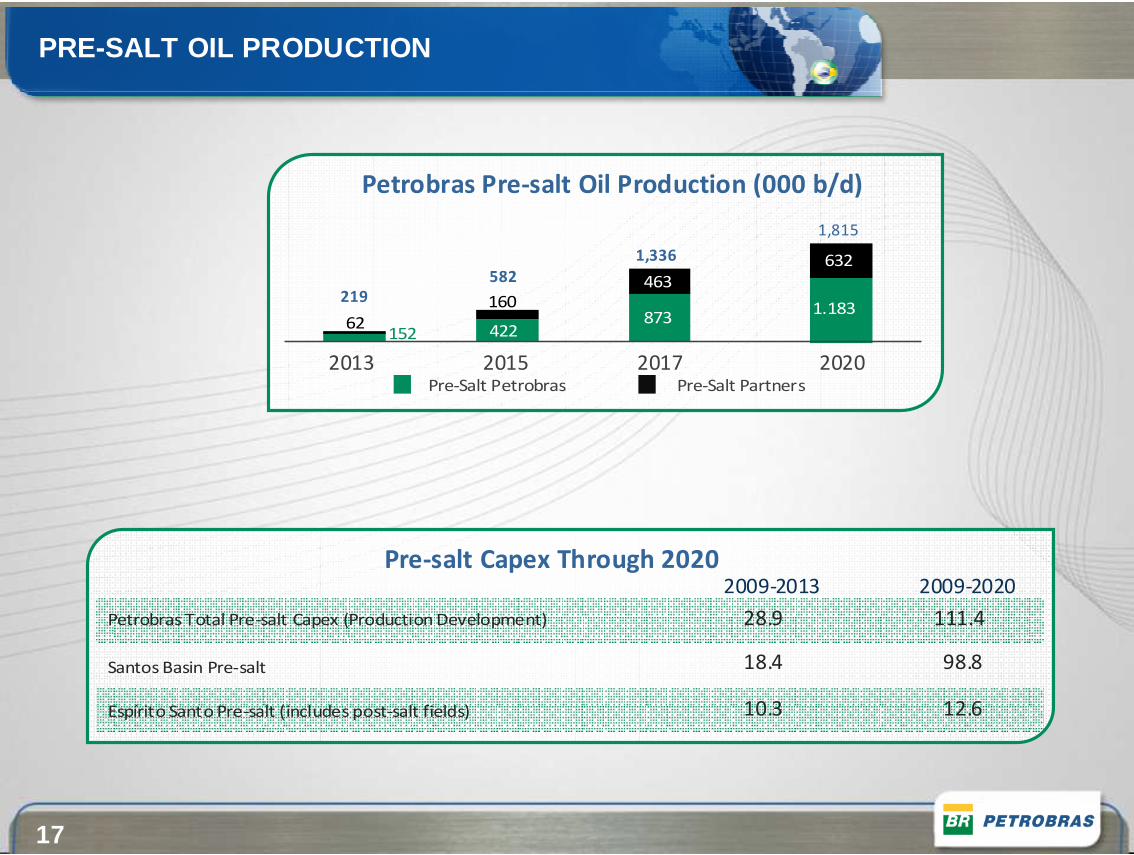

17

Petrobras Pre-salt Oil Production (000 b/d)

2013 2015 2017 2020

62152

160

422

463

873

632

1.183

Pre-Salt Petrobras Pre-Salt Partners

219

1,336

1,815

582

Pre-salt Capex Through 2020

Petrobras Total Pre-salt Capex (Production Development)

Santos Basin Pre-salt

Espírito Santo Pre-salt (includes post-salt fields)

2009-2013 2009-2020

28.9

18.4

10.3

111.4

98.8

12.6

PRE-SALT OIL PRODUCTION

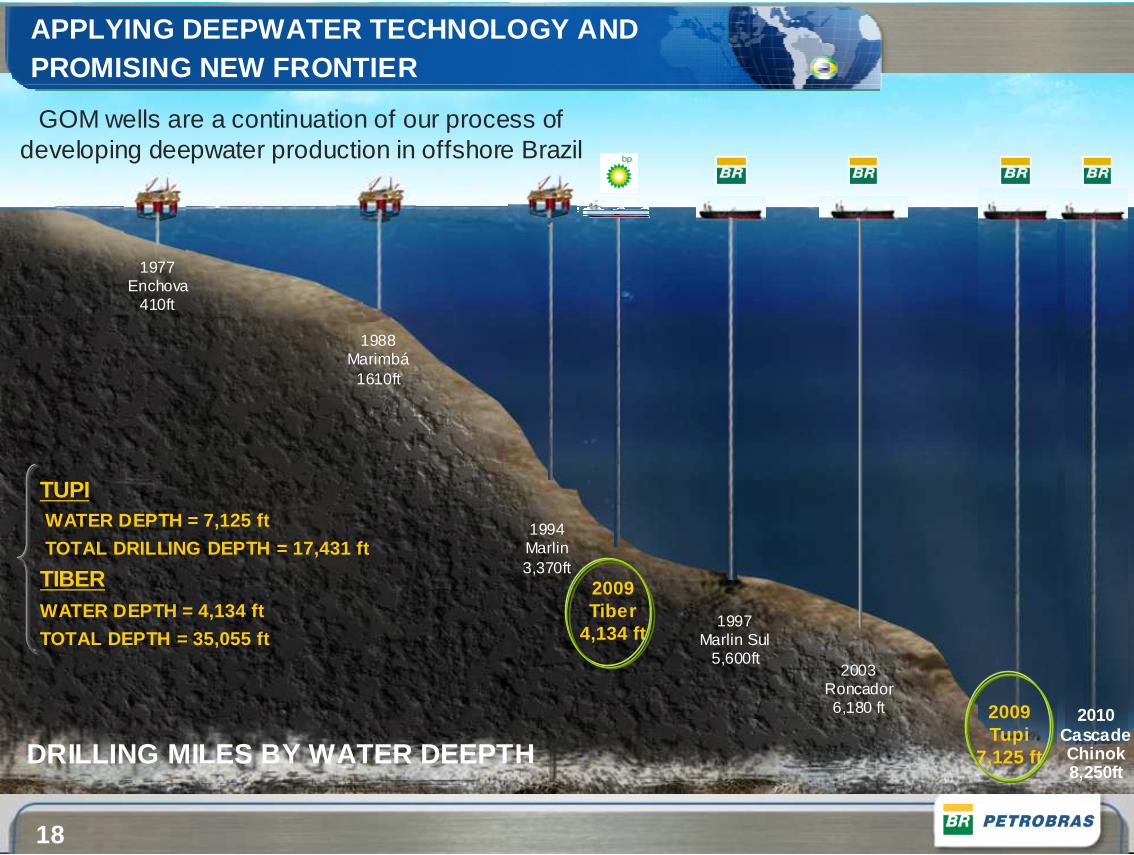

18

1977Enchova

410ft

1988Marimbá

1610ft

1994Marlin3,370ft

2009Tiber

4,134 ft1997

Marlin Sul5,600ft

2003Roncador6,180 ft

DRILLING MILES BY WATER DEEPTH

GOM wells are a continuation of our process of developing deepwater production in offshore Brazil

APPLYING DEEPWATER TECHNOLOGY AND PROMISING NEW FRONTIER

2009Tupi

7,125 ft

2010CascadeChinok8,250ft

TUPIWATER DEPTH = 7,125 ft

TOTAL DRILLING DEPTH = 17,431 ft

TIBERWATER DEPTH = 4,134 ft

TOTAL DEPTH = 35,055 ft

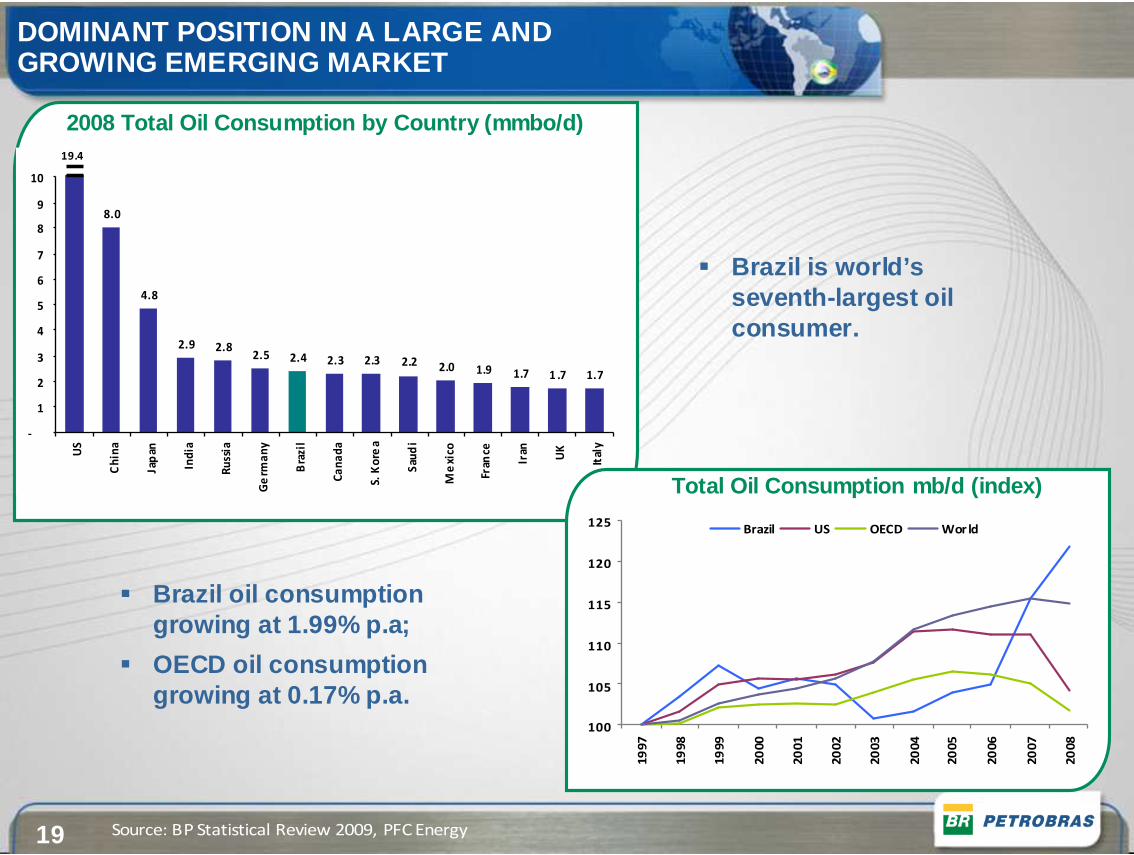

19

8.0

4.8

2.9 2.82.5 2.4 2.3 2.3 2.2 2.0 1.9 1.7 1 .7 1.7

-

1

2

3

4

5

6

7

8

9

10

US

Ch

ina

Jap

an

Ind

ia

Ru

ssia

Ge

rma

ny

Bra

zil

Ca

na

da

S. K

ore

a

Sau

di

Me

xico

Fran

ce

Iran UK

Ital

y

2008 Total Oil Consumption by Country (mmbo/d)

DOMINANT POSITION IN A LARGE AND GROWING EMERGING MARKET

Source: BP Statistical Review 2009, PFC Energy

� Brazil is world’s seventh-largest oil consumer.

� Brazil oil consumption growing at 1.99% p.a;

� OECD oil consumption growing at 0.17% p.a.

19.4

100

105

110

115

120

125

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Brazil US OECD Wor ld

Total Oil Consumption mb/d (index)

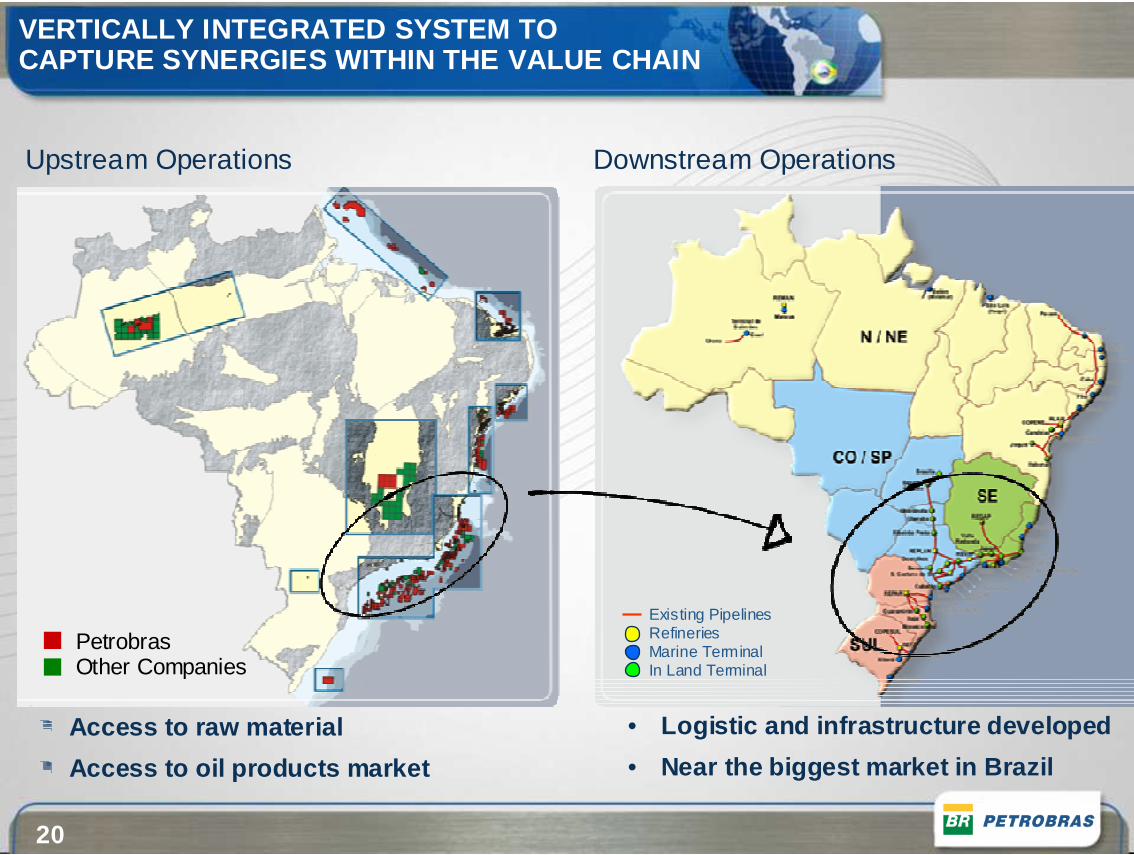

20

VERTICALLY INTEGRATED SYSTEM TO CAPTURE SYNERGIES WITHIN THE VALUE CHAIN

PetrobrasOther Companies

Upstream Operations Downstream Operations

Existing PipelinesRefineriesMarine Terminal In Land Terminal

Access to raw material

Access to oil products market

• Logistic and infrastructure developed

• Near the biggest market in Brazil

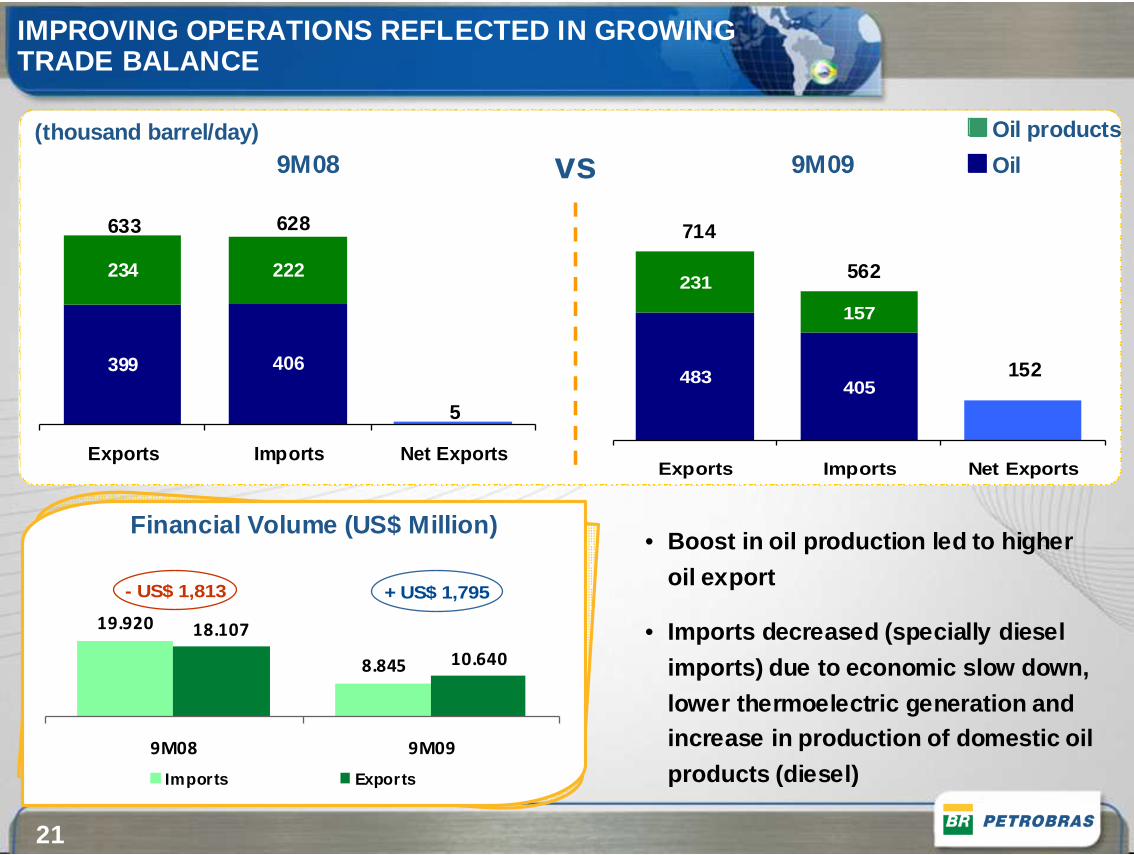

21

9M09

483405

231

157

Exports Imports Net Exports

9M08

399 406

234 222

Exports Imports Net Exports

628633

5

152

562

714

vs

19.920

8.845

18.107

10.640

9M08 9M09

Imports Exports

+ US$ 1,795- US$ 1,813

IMPROVING OPERATIONS REFLECTED IN GROWING TRADE BALANCE

Oil

Oil products(thousand barrel/day)

Financial Volume (US$ Million)• Boost in oil production led to higher

oil export

• Imports decreased (specially diesel

imports) due to economic slow down,

lower thermoelectric generation and increase in production of domestic oil

products (diesel)

22

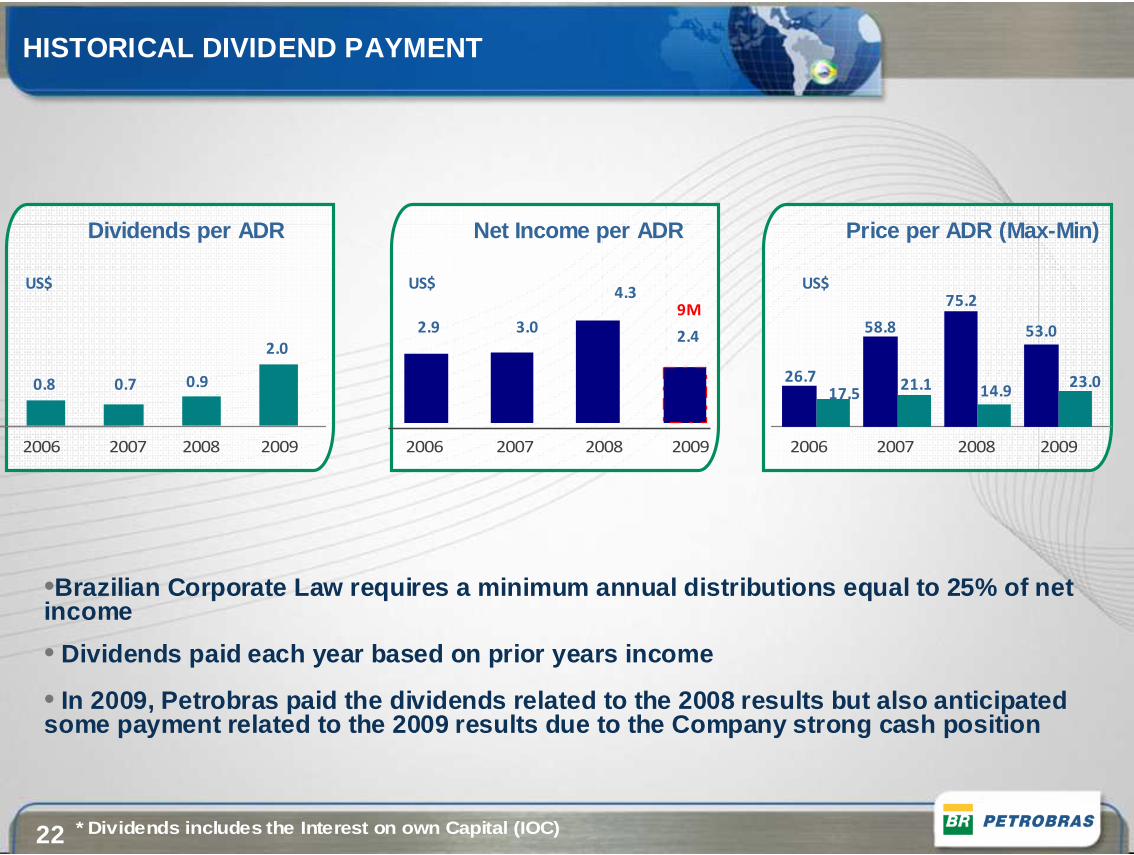

•Brazilian Corporate Law requires a minimum annual d istributions equal to 25% of net income

• Dividends paid each year based on prior years incom e

• In 2009, Petrobras paid the dividends related to th e 2008 results but also anticipated some payment related to the 2009 results due to the Company strong cash position

HISTORICAL DIVIDEND PAYMENT

* Dividends includes the Interest on own Capital (I OC)

2006

0.8

2007 2008 2009

0.7 0.9

2.0

2006 2007 2008 2009

2.9 3.0

4.3

2.4

2006 2007 2008 2009

9M

26.717.5

58.8

21.1

75.2

14.9

53.0

23.0

US$

Dividends per ADR Net Income per ADR Price per ADR (M ax-Min)

US$ US$

23

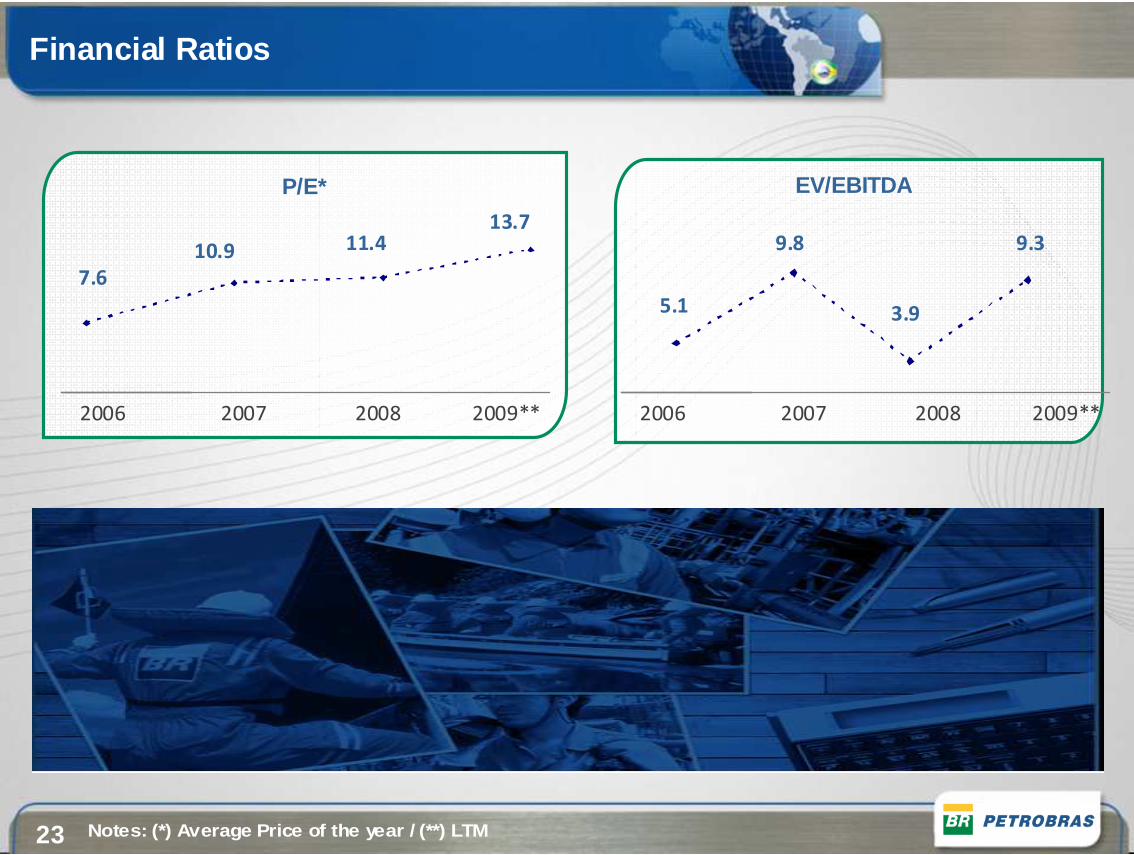

Financial Ratios

Notes: (*) Average Price of the year / (**) LTM

2006 2007 2008 2009** 2006 2007 2008 2009**

7.6

10.9 11.413.7

P/E* EV/EBITDA

5.1

9.8

3.9

9.3

24

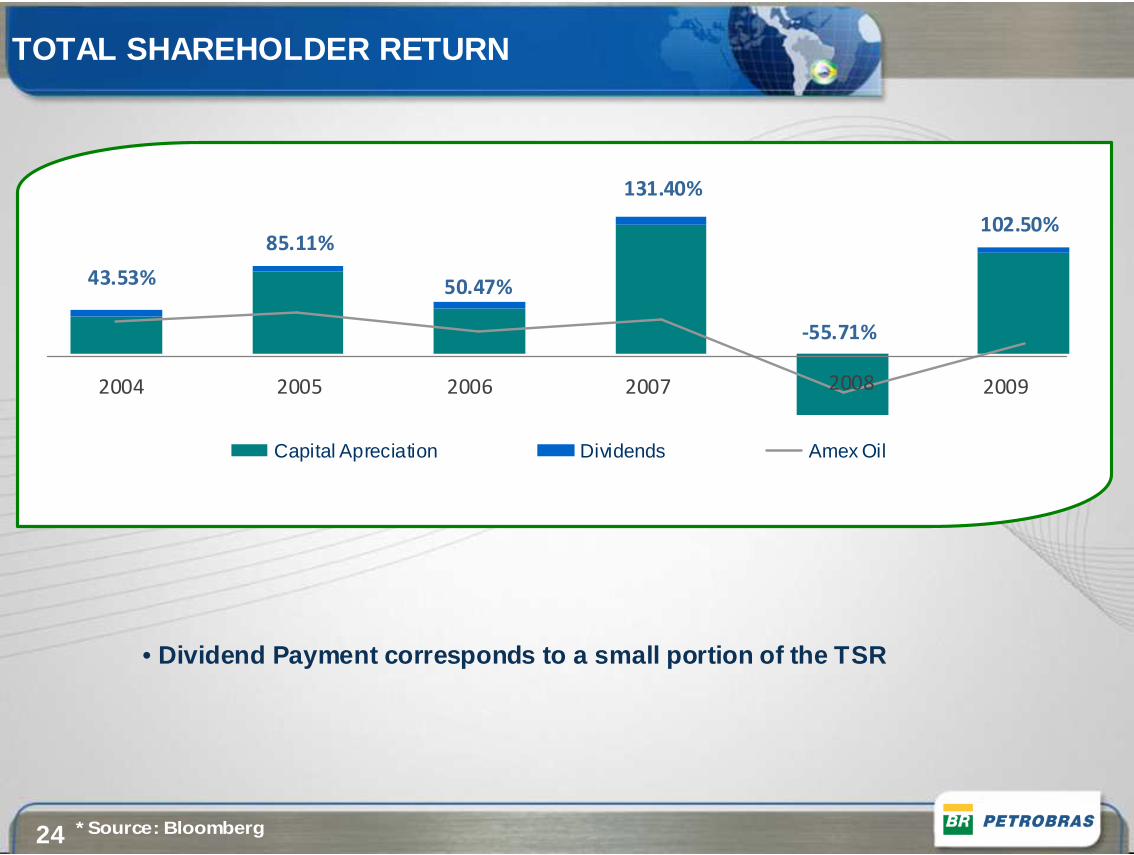

Capital Apreciation Dividends Amex Oil

TOTAL SHAREHOLDER RETURN

* Source: Bloomberg

• Dividend Payment corresponds to a small portion of the TSR

2006 2007 2008 200920052004

43.53%

85.11%

50.47%

131.40%

-55.71%

102.50%

25

For more information:Investor Relations

www.petrobras.com.br/ri+55 21 3224-1510