Embed Size (px)

Citation preview

0

Company No. 380410-P

Freight Management Holdings Bhd (Company No. 380410-P)

(Incorporated in Malaysia under the Companies Act, 1965)

Renounceable rights issue of up to 57,000,000 rights shares on the basis of 1

right share for every 3 existing FMHB shares held as at 5.00 pm on 17 MAY

2016, together with up to 19,000,000 warrants on the basis of 1 warrant for

every 3 rights shares subscribed for, at an issue price of RM0.89 per rights

share.

Principal Advisors

T- Journe Investment Berhad

Eloise Ewe Xiao Yun CEA 130015

Lim Whye Kiat CEA 130045

Najwa Anati Nazlan CEA 130057

Sim Hui Ling CEA 130081

IMPORTANT RELEVANT DATES AND TIMES: Entitlement Date : Tuesday, 17 May 2016 at 5:00 p.m. Last date and time for the sale of Provisional Allotments : Friday, 13 May 2016 at 5:00 p.m. Last date and time for the transfer of Provisional Allotments : Friday, 27 May 2016 at 4:00 p.m. Last date and time for acceptance and payment : Monday, 1 June 2016 at 5:00 p.m. Last date and time for application and payment for Excess Rights :Monday, 1 June 2016 at 5:00 p.m.

1

Company No. 380410-P

Contents

1.0 BACKGROUND OF THE COMPANY ................................................................................. 2

1.1 Company’s Overview ............................................................................................................ 2

1.2 Company’s Financial Performance ..................................................................................... 4

2.0 RATIONALE FOR THE RIGHTS ISSUE ............................................................................ 7

3.0 DETAILS OF RIGHT ISSUE WITH WARRANTS ............................................................. 8

3.1 Basis Of Determining The Issue Price ................................................................................. 8

3.2 Basis Of Determining The Exercise Price ........................................................................... 9

3.3 Details Of Warrants .............................................................................................................. 9

4.0 INVESTMENT PROJECTS .................................................................................................. 10

4.1 Acquisition Of A Cargo Vessel .......................................................................................... 10

4.2 Acquisition Of A Cargo Plane ............................................................................................ 11

5.0 RISK FACTORS ..................................................................................................................... 13

5.1 Risk Involved In The Company ......................................................................................... 13

5.2 Risks Relating To The Transportation And Logistics Industry ..................................... 13

5.3 Risks Associated To The Rights Issue With Warrants .................................................... 14

5.4 Other Risks .......................................................................................................................... 14

6.0 FINANCIAL EFFECTS ......................................................................................................... 15

6.1 Financial Effects Of The Investment Projects On The Company’s Income Statement 15

6.2 Financial Effects On The Company’s Cash Flow Statement .......................................... 15

6.2.1 Cash Flows From Investing Activities ....................................................................... 15

6.2.3 Cash Flows From Financing Activities ..................................................................... 16

6.3 Financial Effects Of The Rights Issue With Warrants On The Company’s Balance

Sheet 16

6.3.1 Issued And Paid-Up Share Capital ............................................................................ 16

6.3.2 Total Equity and Liability .......................................................................................... 17

6.3.3 Net Asset ...................................................................................................................... 17

6.3.4 Earnings Per Share (EPS) .......................................................................................... 18

7.0 VALUE OF THE COMPANY SHARE ON THE EX-DATE OF THE RIGHTS-ISSUE

LISTING .............................................................................................................................................. 18

8.0 APPLICATION OF THEORIES .......................................................................................... 20

8.1 Capital Asset Pricing Model Theory ................................................................................. 20

8.2 (Modern) Portfolio Theory (MPT) .................................................................................... 21

8.3 Trade-Off Theory of Capital Structure ............................................................................ 22

DISCLAIMER..................................................................................................................................... 23

APPENDICES ..................................................................................................................................... 24

REFERENCES .................................................................................................................................... 35

2

Company No. 380410-P

1.0 BACKGROUND OF THE COMPANY

1.1 Company’s Overview

Freight Management Holdings Bhd (FMHB) is an

investment holding company which engages in multimodal

freight services and forwarding industry. The services

provided include sea, air, rail, tug and barge, warehouse,

transport, and custom brokerage services. The operations of

the Companies are conducted in Malaysia, Australia,

Indonesia, Thailand, Vietnam, India and Singapore. The

subsidiaries of the Company include FM Multimodal

Services Sdn. Bhd., FM Worldwide Logistics (Penang) Sdn.

Bhd., Freight Management MSC Sdn. Bhd. And FM Global

Logistics (M) Sdn. Bhd.

The multimodal freight services of FMHB:

Services Activities

Sea freight

services

Provides export and import freight

services, and handle customers’ cargo

movement internationally and between

West Malaysia and Sabah/Sarawak

Air freight

services

Offers inbound and outbound services

that cater the needs of customers in

Peninsular Malaysia and Sabah/Sarawak.

Rail freight

services

Handles fully containerized land-bridge

rail services between Port Klang and

Penang in Malaysia and Bangkok in

Thailand

Tug & barge

services

Specializes in the movement of dry bulk

cargoes between South Thailand, the

West Coast of Peninsular Malaysia and

Singapore.

Warehouse

services

Provides complete warehousing solutions

to the customers with the newly built,

state-of-the-art, warehousing complex in

Port Klang.

Transport &

customs

brokerage

services

Consists of container haulage,

conventional trucking and customs

brokerage to complement the multimodal

services

Exchange: Bursa Malaysia

Sector: Industrials

Industry: Transportation & Logistics

Sub Industry: Logistics Services

BUY Share Price RM1.27

Target Price RM1.30

Share Price Performance

KLCI 1621.21

YTD KLCI chg -7.05%

Stock Information

Bloomberg Ticker FMH:MK

Market Cap (RM m) 219.840

Issued shares (m) 174.476

52-week high/low (RM) 1.57/1.25

Beta 0.333

Major Shareholders

Chong Keat Chew 25.68%

Singapore Enterprise 21.40%

Heng Lam Yang 17.30%

Source: Bloomberg

3

Company No. 380410-P

Freight Management Company is an investment holding company which provides

multimodal freight services that includes rail, tug barge, sea, air, custom brokerage,

distribution container haulage, and conventional tracking. It also provides management

service to its subsidiary and associated companies. It was founded in 1988 and the

headquarter is in Port Klang, Malaysia. Corporate in 1996 under the Act, it was known as

Freight Management (Holdings) Sdn Bhd as a private limited company. It changed the nature

of the business to public limited company in 2004.

During 1988, Chew Chong Keat, Yang Heng Lam and Gan Siew Yong, namely as a

promoter of Freight Management Holding, operate the business of providing freight services

that only with 8 staffs at that time based on Port Klang, the maritime gateway of Malaysia.

The main focus at that time is to provide freight services to Singapore. At the very beginning,

Freight Management Holding had already 2 overseas independent agents in Hong Kong and

Singapore. In the next year, Freight Management Holding has expanded their company by

incorporate Freight Management (Penang) Sdn Bhd to cover the north region of West

Malaysia.

To establish the base of the corporation, the Promoters have introduced FM Airfreight

Sdn Bhd which is now known as FM-Hellman Worlwide Logistics Sdn Bhd at Subang

International Airport as air freight services in 1990. In 1991, in order to continue expand their

business to the stage that be proud of, Freight Management Holding has continuously offer

range of freight service by incorporate Citra Multimodal Services Sdn Bhd which previously

known as Citra Timuran Sdn Bhd to cover LCL consolidation and FCL services between East

and West Malaysia.

1993 remarks another change that been made by Freight Management Group by

expanding their business in Perak, to cover the marketing and sales of freight services in that

area, named Freight Management (Ipoh) Sdn Bhd. It is located in Kinta Valley. The

promoters also initiated Group’s first CFS operations in Port Klang. The following year,

Freight Management Group has incorporated FM Worldwide Logistics (Penang) Sdn Bhd

that previously named FM Airfreight (Penang) Sdn Bhd to cover the air freight business in

that respective area to continue expand the business.

In 1996, it creates another milestone of change to the business as they have obtained

their first ISO 9002 which rectify the business growing organization whether as for

qualitatively or quantitatively. They also have continue expanding in a purpose to cater the

southern region’s need of air freight business by incorporate Freight Management (Melaka)

Sdn Bhd. In the same year, they also commenced the operations of the then Logistar Sdn Bhd

which now known as Advanced Logistar Sdn Bhd to cover all the customs barrier related and

services to further complement this range of air freight services.

In order to complete this freight service offered, Freight Management Holding

provided rail service that cover from Port Klang to Bangkok in 1999. With this achievement,

Freight Management Holding has complete the requirement to be the multimodal freight

4

Company No. 380410-P

service that can cater the freight services range from air service, maritime and also through

railway. It also introduces the first bonded warehouse with 40,000 square feet to record their

future achievement in the same year.

In present, Freight Management is leading multimodal freight service that provides

various services range from sea, rail, air, custom brokerage and distribution service. Freight

Management can also be classified as successful company as it has 127 ports worldwide and

has 107 agents that globally represent Freight Management Holding. The logistic segments

which are operated in Malaysia, Australia, Indonesia, Thailand, Vietnam, and India offers

integrated freight and logistics service while the marine segment engage as operators and

charterer of barges and tugboats that operated by a company in Singapore. While the other

segment cover operation related to provision of management services, IT related services,

investment holdings and also support services.

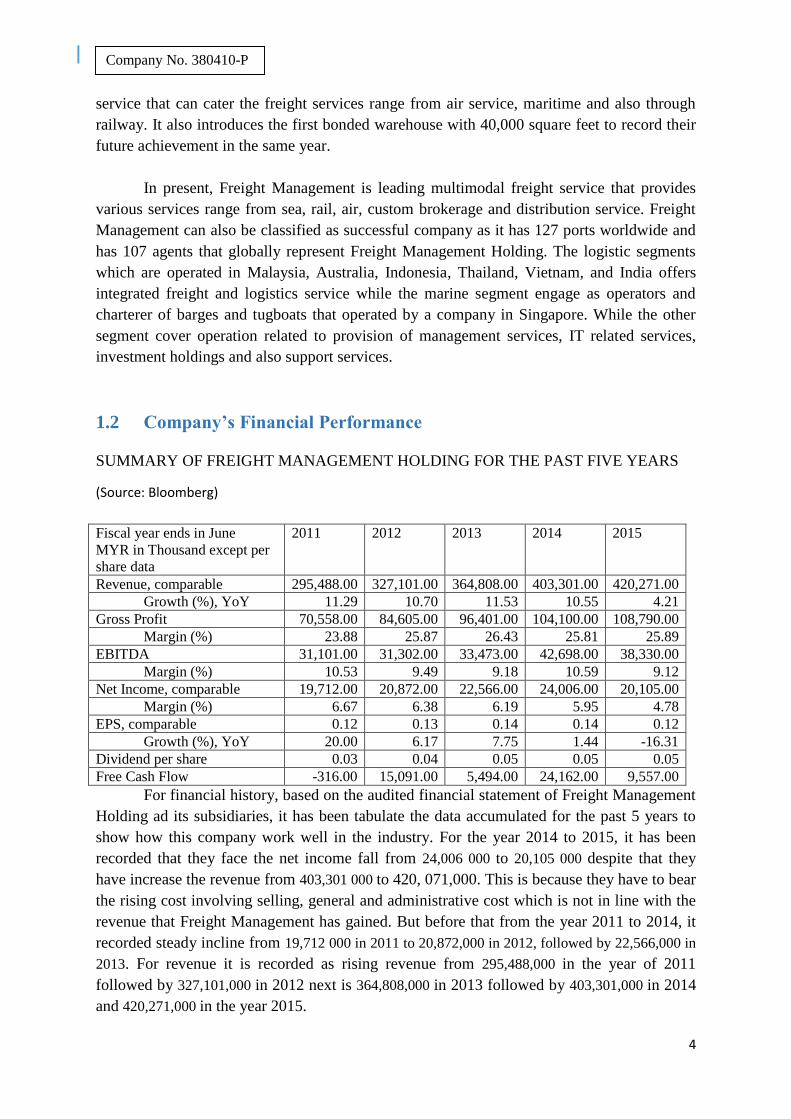

1.2 Company’s Financial Performance

SUMMARY OF FREIGHT MANAGEMENT HOLDING FOR THE PAST FIVE YEARS

(Source: Bloomberg)

For financial history, based on the audited financial statement of Freight Management

Holding ad its subsidiaries, it has been tabulate the data accumulated for the past 5 years to

show how this company work well in the industry. For the year 2014 to 2015, it has been

recorded that they face the net income fall from 24,006 000 to 20,105 000 despite that they

have increase the revenue from 403,301 000 to 420, 071,000. This is because they have to bear

the rising cost involving selling, general and administrative cost which is not in line with the

revenue that Freight Management has gained. But before that from the year 2011 to 2014, it

recorded steady incline from 19,712 000 in 2011 to 20,872,000 in 2012, followed by 22,566,000 in

2013. For revenue it is recorded as rising revenue from 295,488,000 in the year of 2011

followed by 327,101,000 in 2012 next is 364,808,000 in 2013 followed by 403,301,000 in 2014

and 420,271,000 in the year 2015.

Fiscal year ends in June

MYR in Thousand except per

share data

2011 2012 2013 2014 2015

Revenue, comparable 295,488.00 327,101.00 364,808.00 403,301.00 420,271.00

Growth (%), YoY 11.29 10.70 11.53 10.55 4.21

Gross Profit 70,558.00 84,605.00 96,401.00 104,100.00 108,790.00

Margin (%) 23.88 25.87 26.43 25.81 25.89

EBITDA 31,101.00 31,302.00 33,473.00 42,698.00 38,330.00

Margin (%) 10.53 9.49 9.18 10.59 9.12

Net Income, comparable 19,712.00 20,872.00 22,566.00 24,006.00 20,105.00

Margin (%) 6.67 6.38 6.19 5.95 4.78

EPS, comparable 0.12 0.13 0.14 0.14 0.12

Growth (%), YoY 20.00 6.17 7.75 1.44 -16.31

Dividend per share 0.03 0.04 0.05 0.05 0.05

Free Cash Flow -316.00 15,091.00 5,494.00 24,162.00 9,557.00

5

Company No. 380410-P

For the growth rate recorded, the growth in dividend per share remained constantly

while on the other hand, earning per share fell by 16.31%. But while this figures have been

compared throughout this past 5 years, it is recorded that both dividend per share and earning

per share ranked highest compare to other company in this industry. For dividend per share it

recorded a steady increase from 2011 to 2014 and record static amount from 2014 to 2015.

For earning per share, it recorded increase from 2011 to 2013 while from 2013 to 2014

recorded static growth and for 2015, there is slight drop.

MYR in Thousand 2011 2012 2013 2014 2015

Total Cash Flows from

Operations

22,465.00 31,819.00 20,374.00 41,123.00 20,645.00

Total Cash Flows from

Investing

-13,302.00 -15,150.00 -11,776.00 -20,600.00 -2,936.00

Total Cash Flows from

Financing

-3,759.00 -6,951.00 -3,568.00 -15,999.00 -21,408.00

Net Change in Cash 5,404.00 9,718.00 5,030.00 4524.00 -3,699.00

(Source: Bloomberg)

For cash flow from operations, it shows fluctuate amount which we can see from the

table above. For 2011 to 2012, it shows gradual amount from RM 22, 465, 000 to RM

31,819,000, followed by drop with 11 445 000 until it is recorded RM 20, 374,000 in 3013

and then highest amount in 2014 which is RM 41, 123, 000 followed by drop in 2015 which

records RM 20, 645,000. For net change in cash, it also shows fluctuate amount with RM 5,

404,000 in 2011, followed by RM 9,718,000 in 2012, next is drop to RM 5,030,000 followed

by drop to RM 4524,000 in 2014 and next with the negative amount of –RM 3 699 000.

Balance Sheet

MYR in Thousand 2011 2012 2013 2014 2015

Assets

Total current assets 93,296.00 107,085.00 130,845.00 136,215.00 156,758.00

Total assets 200,962.00 222,459.00 257,041.00 285,714.00 352,426.00

Liabilities

Total current liabilities 52,554.00 51,706.00 55,455.00 57,391.00 63,983.00

Total liabilities 84,397.00 95,531.00 102,412.00 128,630.00

Stockholder Equity

Total shareholders equity 120,474.00 138,062.00 161,510.00 183,302.00 223,796.00

Total liabilities and

shareholders equity 200,962.00 222,459.00 257,041.00 285,714.00 352,426.00

(Source: Bloomberg)

For the total assets, it has been recorded a steady growth from 2011 to 2015 which

range from 200,962 in 2011, followed by 222,459 ,000 in 2012 and then increased by 34

582,000 in 2013 make it 257,041,000 , 285,714,000 in 2014 and next is 352,426,000 in 2015.

Despite that, it also recorded a rapid growth in total debt from 2011 to 2015. For the first

2011 and 2012 year, it is maintained figure of the amount of total debt by 37,725,000 and

37,316,000 respectively , 43,344 ,000 in the year of 2013, followed by 47,794,000 in 2014 and

6

Company No. 380410-P

next to record the highest total debt in 2015 worth around 59,021,000. The debt to total capital

ratio of 2015 recorded a higher figure than last year with 0.91% from 20.68% to 20.87%.

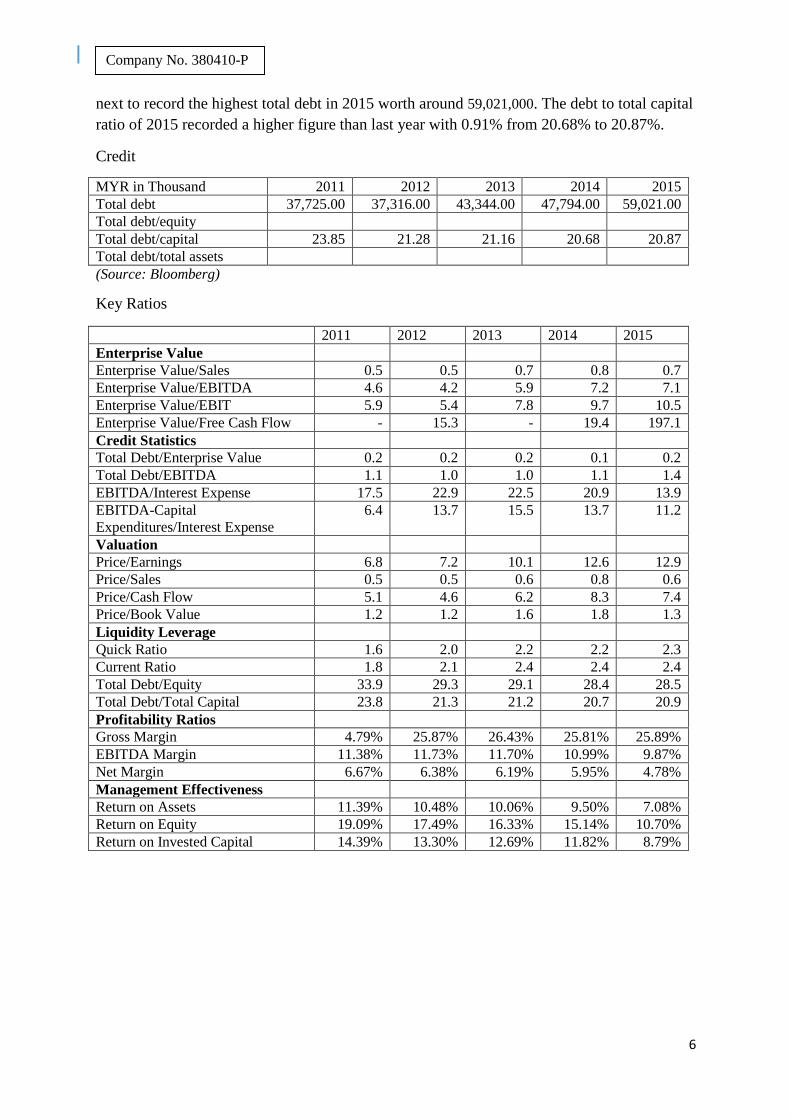

Credit

MYR in Thousand 2011 2012 2013 2014 2015

Total debt 37,725.00 37,316.00 43,344.00 47,794.00 59,021.00

Total debt/equity

Total debt/capital 23.85 21.28 21.16 20.68 20.87

Total debt/total assets

(Source: Bloomberg)

Key Ratios

2011 2012 2013 2014 2015

Enterprise Value

Enterprise Value/Sales 0.5 0.5 0.7 0.8 0.7

Enterprise Value/EBITDA 4.6 4.2 5.9 7.2 7.1

Enterprise Value/EBIT 5.9 5.4 7.8 9.7 10.5

Enterprise Value/Free Cash Flow - 15.3 - 19.4 197.1

Credit Statistics

Total Debt/Enterprise Value 0.2 0.2 0.2 0.1 0.2

Total Debt/EBITDA 1.1 1.0 1.0 1.1 1.4

EBITDA/Interest Expense 17.5 22.9 22.5 20.9 13.9

EBITDA-Capital

Expenditures/Interest Expense

6.4 13.7 15.5 13.7 11.2

Valuation

Price/Earnings 6.8 7.2 10.1 12.6 12.9

Price/Sales 0.5 0.5 0.6 0.8 0.6

Price/Cash Flow 5.1 4.6 6.2 8.3 7.4

Price/Book Value 1.2 1.2 1.6 1.8 1.3

Liquidity Leverage

Quick Ratio 1.6 2.0 2.2 2.2 2.3

Current Ratio 1.8 2.1 2.4 2.4 2.4

Total Debt/Equity 33.9 29.3 29.1 28.4 28.5

Total Debt/Total Capital 23.8 21.3 21.2 20.7 20.9

Profitability Ratios

Gross Margin 4.79% 25.87% 26.43% 25.81% 25.89%

EBITDA Margin 11.38% 11.73% 11.70% 10.99% 9.87%

Net Margin 6.67% 6.38% 6.19% 5.95% 4.78%

Management Effectiveness

Return on Assets 11.39% 10.48% 10.06% 9.50% 7.08%

Return on Equity 19.09% 17.49% 16.33% 15.14% 10.70%

Return on Invested Capital 14.39% 13.30% 12.69% 11.82% 8.79%

7

Company No. 380410-P

2.0 RATIONALE FOR THE RIGHTS ISSUE

Our Group is in the opinion that the Rights Issue with Warrants is the most appropriate

funding option amongst others, the various funding option includes issuance of private debt

securities or making bank loans. The rights issue is undertaken for the following reasons:-

i. To raise adequate funds for the investment projects (approximately RM44 million) at a

lower cost without incurring additional finance costs, as compared to other funding

option such as bank borrowings;

ii. To optimise the capital structure and further improve the gearing levels of our Group;

iii. To provide the existing shareholders an opportunity to further participate in the

company’s equity and prospects of the Group

iv. The free warrants to be issued pursuant to the rights issue with warrants allow the

entitled shareholders to increase their equity participation in our company at a pre-

determined price over the tenure of the warrants. The entitled shareholders may also

benefit from any potential capital appreciation of the warrants. In addition, our

company would be able to raise further proceeds as and when any of the warrants are

exercised.

After taking those rationales into account, Our Board is of the opinion that Right Issue with

Warrants is the best way for fund-raising to satisfy the best interest of our Company and our

Shareholders.

8

Company No. 380410-P

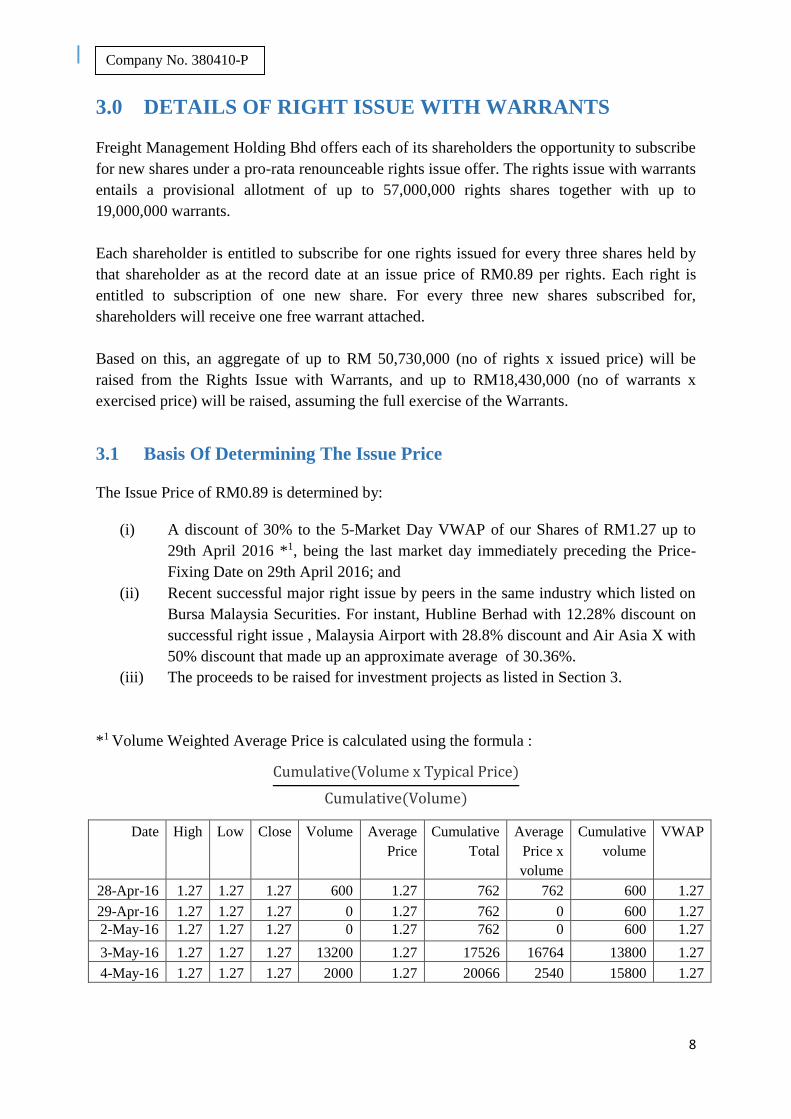

3.0 DETAILS OF RIGHT ISSUE WITH WARRANTS

Freight Management Holding Bhd offers each of its shareholders the opportunity to subscribe

for new shares under a pro-rata renounceable rights issue offer. The rights issue with warrants

entails a provisional allotment of up to 57,000,000 rights shares together with up to

19,000,000 warrants.

Each shareholder is entitled to subscribe for one rights issued for every three shares held by

that shareholder as at the record date at an issue price of RM0.89 per rights. Each right is

entitled to subscription of one new share. For every three new shares subscribed for,

shareholders will receive one free warrant attached.

Based on this, an aggregate of up to RM 50,730,000 (no of rights x issued price) will be

raised from the Rights Issue with Warrants, and up to RM18,430,000 (no of warrants x

exercised price) will be raised, assuming the full exercise of the Warrants.

3.1 Basis Of Determining The Issue Price

The Issue Price of RM0.89 is determined by:

(i) A discount of 30% to the 5-Market Day VWAP of our Shares of RM1.27 up to

29th April 2016 *1, being the last market day immediately preceding the Price-

Fixing Date on 29th April 2016; and

(ii) Recent successful major right issue by peers in the same industry which listed on

Bursa Malaysia Securities. For instant, Hubline Berhad with 12.28% discount on

successful right issue , Malaysia Airport with 28.8% discount and Air Asia X with

50% discount that made up an approximate average of 30.36%.

(iii) The proceeds to be raised for investment projects as listed in Section 3.

*1 Volume Weighted Average Price is calculated using the formula :

Cumulative(Volume x Typical Price)

Cumulative(Volume)

Date High Low Close Volume Average

Price

Cumulative

Total

Average

Price x

volume

Cumulative

volume

VWAP

28-Apr-16 1.27 1.27 1.27 600 1.27 762 762 600 1.27

29-Apr-16 1.27 1.27 1.27 0 1.27 762 0 600 1.27

2-May-16 1.27 1.27 1.27 0 1.27 762 0 600 1.27

3-May-16 1.27 1.27 1.27 13200 1.27 17526 16764 13800 1.27

4-May-16 1.27 1.27 1.27 2000 1.27 20066 2540 15800 1.27

9

Company No. 380410-P

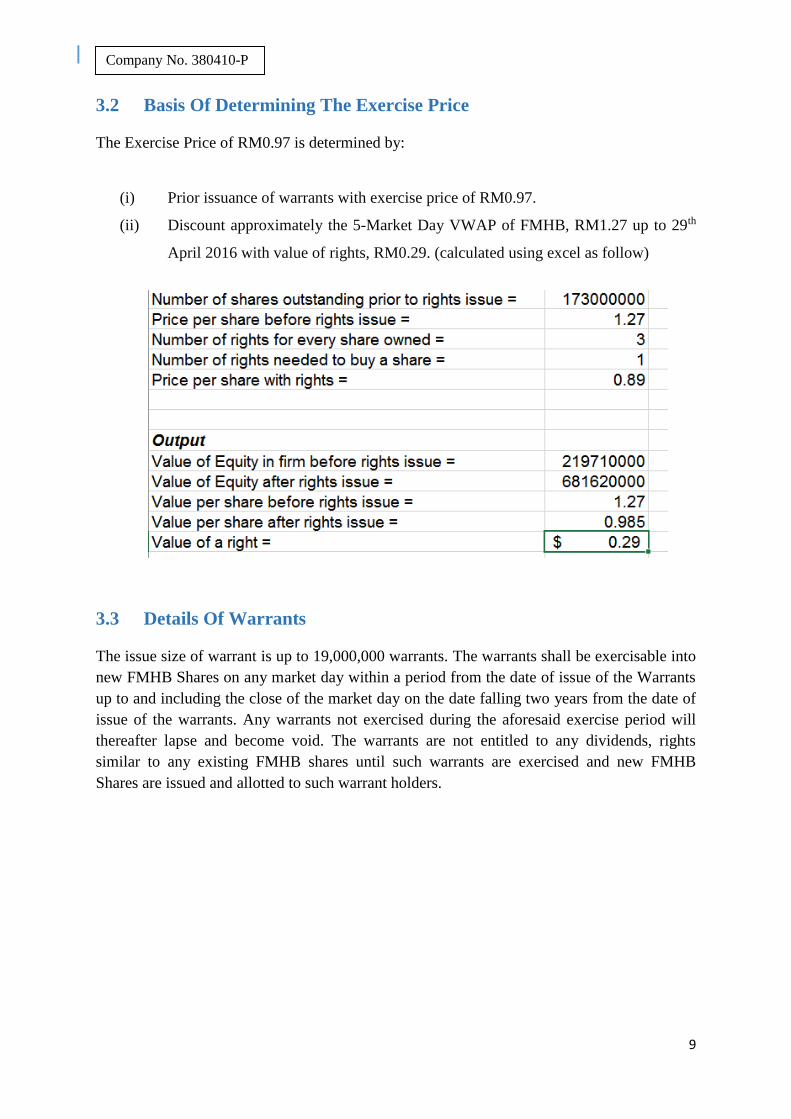

3.2 Basis Of Determining The Exercise Price

The Exercise Price of RM0.97 is determined by:

(i) Prior issuance of warrants with exercise price of RM0.97.

(ii) Discount approximately the 5-Market Day VWAP of FMHB, RM1.27 up to 29th

April 2016 with value of rights, RM0.29. (calculated using excel as follow)

3.3 Details Of Warrants

The issue size of warrant is up to 19,000,000 warrants. The warrants shall be exercisable into

new FMHB Shares on any market day within a period from the date of issue of the Warrants

up to and including the close of the market day on the date falling two years from the date of

issue of the warrants. Any warrants not exercised during the aforesaid exercise period will

thereafter lapse and become void. The warrants are not entitled to any dividends, rights

similar to any existing FMHB shares until such warrants are exercised and new FMHB

Shares are issued and allotted to such warrant holders.

10

Company No. 380410-P

4.0 INVESTMENT PROJECTS

Funds raised from this Rights Issue Offer will enable to the Group to raise immediate gross

proceeds of approximately RM 50,730,000. The proceeds are utilised to acquire these two

investment projects mentioned below. It is expected to have positive contribution in the

future earnings of Freight Management Holdings Bhd.

Details of utilisation Time frame Amount (RM)

Acquisition of a cargo vessel 3 months 28,327,600

Acquisition of a cargo plane 3 months 14,973,160

Estimated fees and expenses for right issues with warrants* 1 month 7,429,240

Total 50,730,000

* The remaining proceeds used after acquisitions are used for expenses like legal costs,

professional fees, transaction costs, underwriting fees and other related costs.

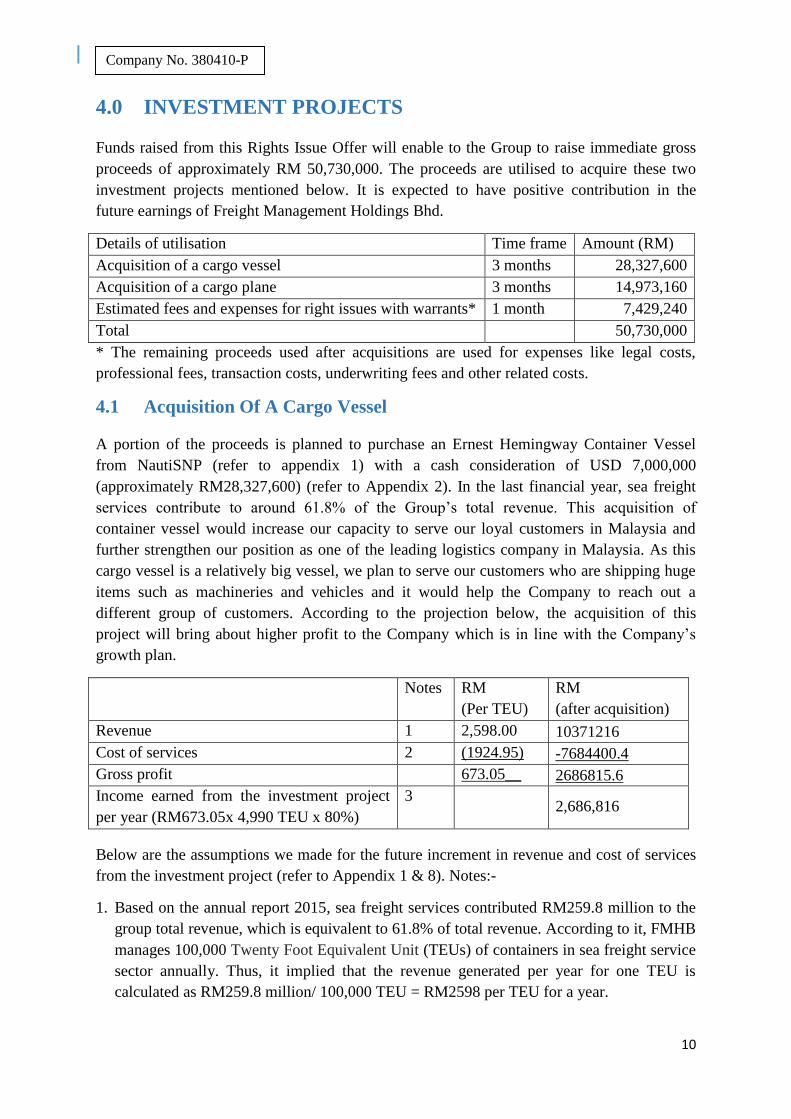

4.1 Acquisition Of A Cargo Vessel

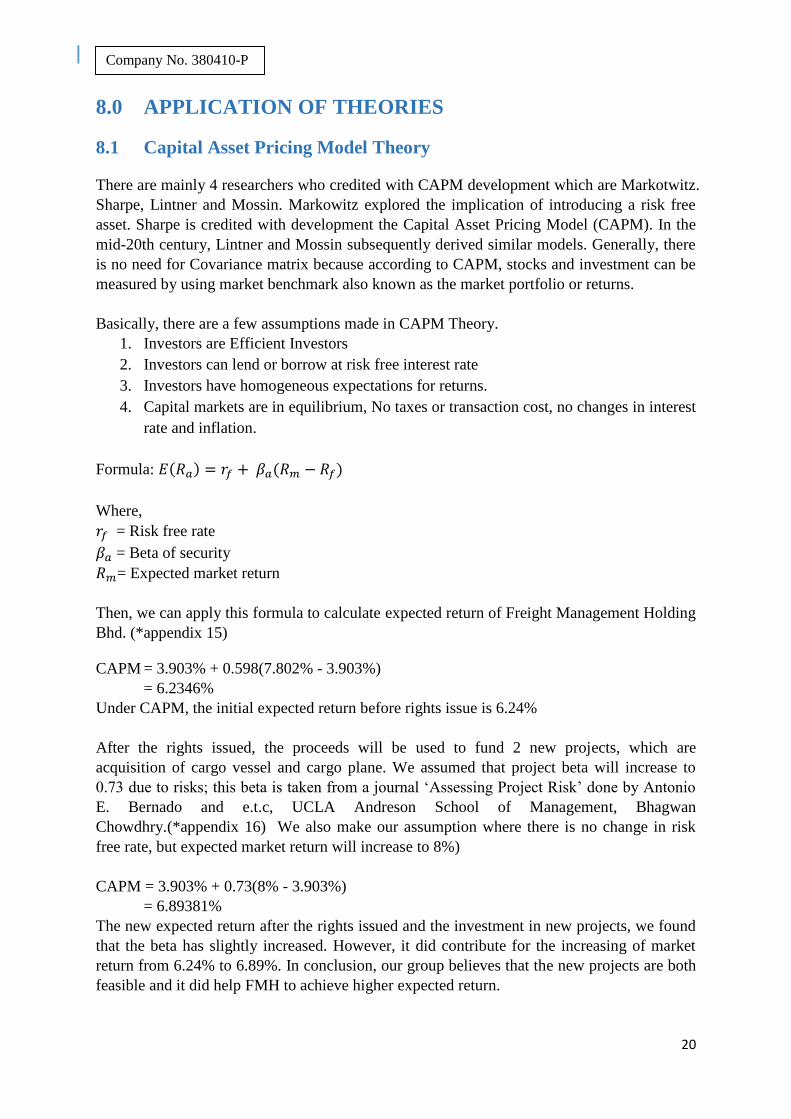

A portion of the proceeds is planned to purchase an Ernest Hemingway Container Vessel

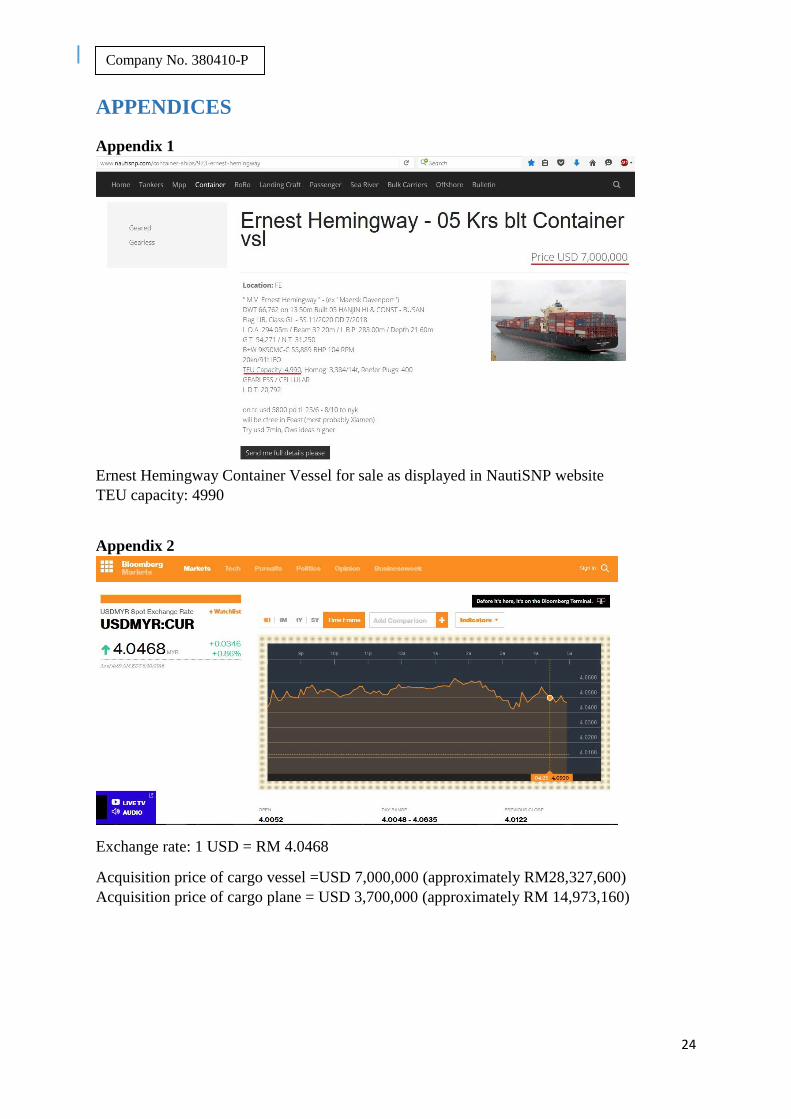

from NautiSNP (refer to appendix 1) with a cash consideration of USD 7,000,000

(approximately RM28,327,600) (refer to Appendix 2). In the last financial year, sea freight

services contribute to around 61.8% of the Group’s total revenue. This acquisition of

container vessel would increase our capacity to serve our loyal customers in Malaysia and

further strengthen our position as one of the leading logistics company in Malaysia. As this

cargo vessel is a relatively big vessel, we plan to serve our customers who are shipping huge

items such as machineries and vehicles and it would help the Company to reach out a

different group of customers. According to the projection below, the acquisition of this

project will bring about higher profit to the Company which is in line with the Company’s

growth plan.

Notes RM

(Per TEU)

RM

(after acquisition)

Revenue 1 2,598.00 10371216

Cost of services 2 (1924.95) -7684400.4

Gross profit 673.05__ 2686815.6

Income earned from the investment project

per year (RM673.05x 4,990 TEU x 80%)

3 2,686,816

Below are the assumptions we made for the future increment in revenue and cost of services

from the investment project (refer to Appendix 1 & 8). Notes:-

1. Based on the annual report 2015, sea freight services contributed RM259.8 million to the

group total revenue, which is equivalent to 61.8% of total revenue. According to it, FMHB

manages 100,000 Twenty Foot Equivalent Unit (TEUs) of containers in sea freight service

sector annually. Thus, it implied that the revenue generated per year for one TEU is

calculated as RM259.8 million/ 100,000 TEU = RM2598 per TEU for a year.

11

Company No. 380410-P

2. Based on the annual report 2015, the total cost of services for the group is RM311.481

million. Assume the proportion of cost of services is the same as revenue, thus the cost of

service for sea freight sector is RM192.495 million (RM311,481 million x 61.8%).

Therefore, the cost of services per year for one TEU is calculated as RM192.495 million/

100,000 TEU = RM1924.95 per TEU for a year.

3. The new cargo vessel has a capacity of 4,990 twenty-foot equivalent units (TEUs).

Assuming the utilisation rate is 80% of the maximum capacity, the estimated annual cash

inflow from the acquisition would be RM2,686,816 (RM673.05/TEU x 4,990 TEU x 80%)

per year.

𝑵𝒆𝒕 𝑷𝒓𝒆𝒔𝒆𝒏𝒕 𝑽𝒂𝒍𝒖𝒆 (𝑵𝑷𝑽)

= − 𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 + 𝑃𝑉 𝑜𝑓 𝐹𝑢𝑡𝑢𝑟𝑒 𝐶𝑎𝑠ℎ 𝑓𝑙𝑜𝑤𝑠

= −28,327,600 + 𝑃 [1 − (1 + 𝑟)−𝑛

𝑟]

= −28,327,600 + 2,686,816 [1 − (1 + 0.056)−30

0.056]

= 𝑅𝑀10,294,349.28

* The cargo vessel is estimated to have a useful life of 30 years with no residual value.

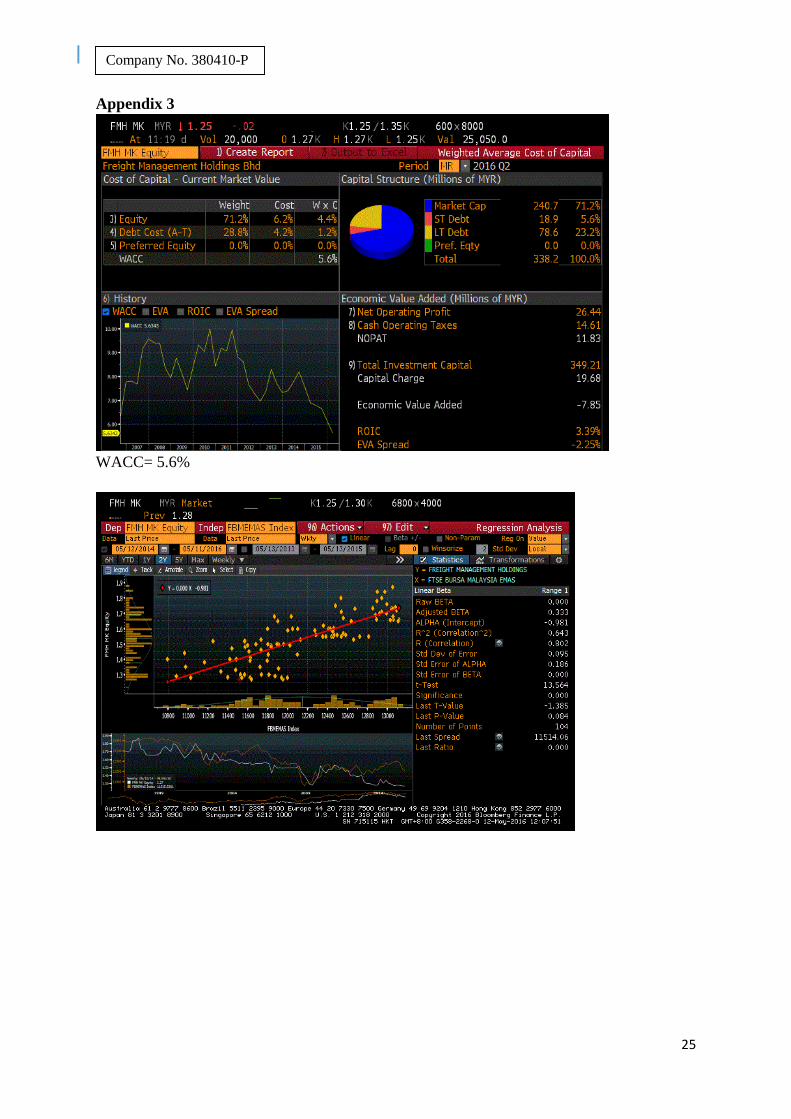

* The discount rate used is Weighted Average Cost of Capital (WACC), 5.6% ***.

*** refer to Appendix 3

4.2 Acquisition Of A Cargo Plane

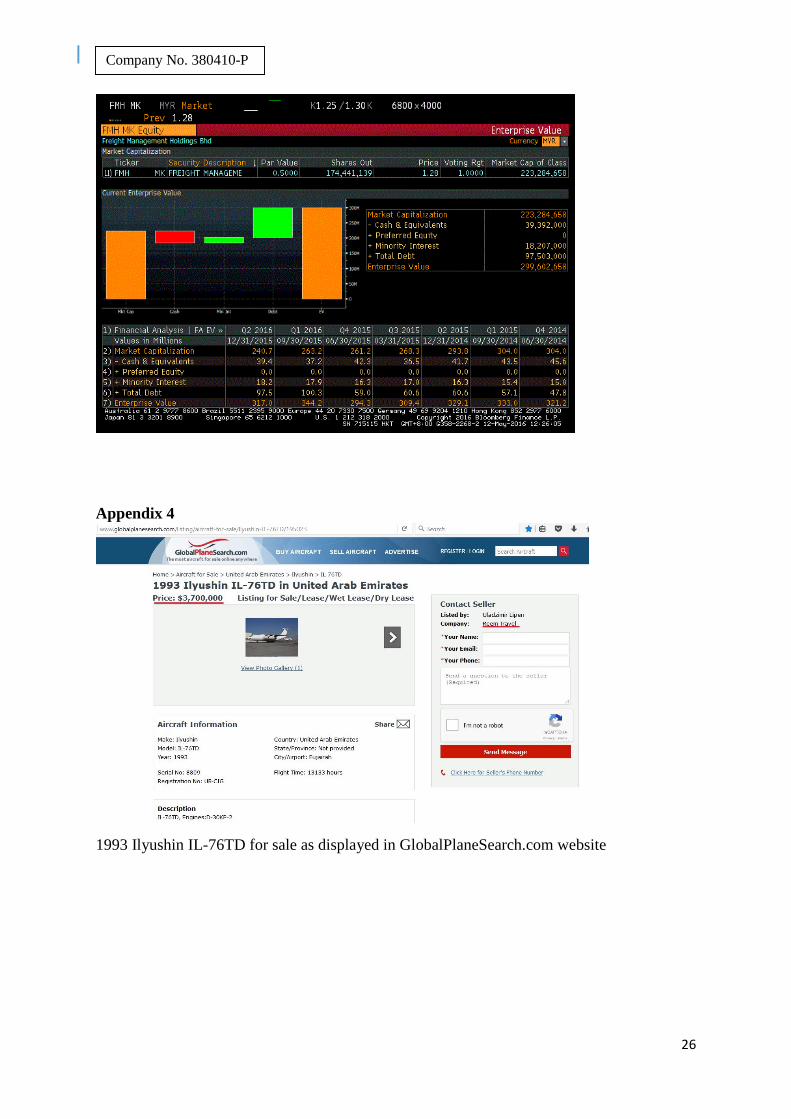

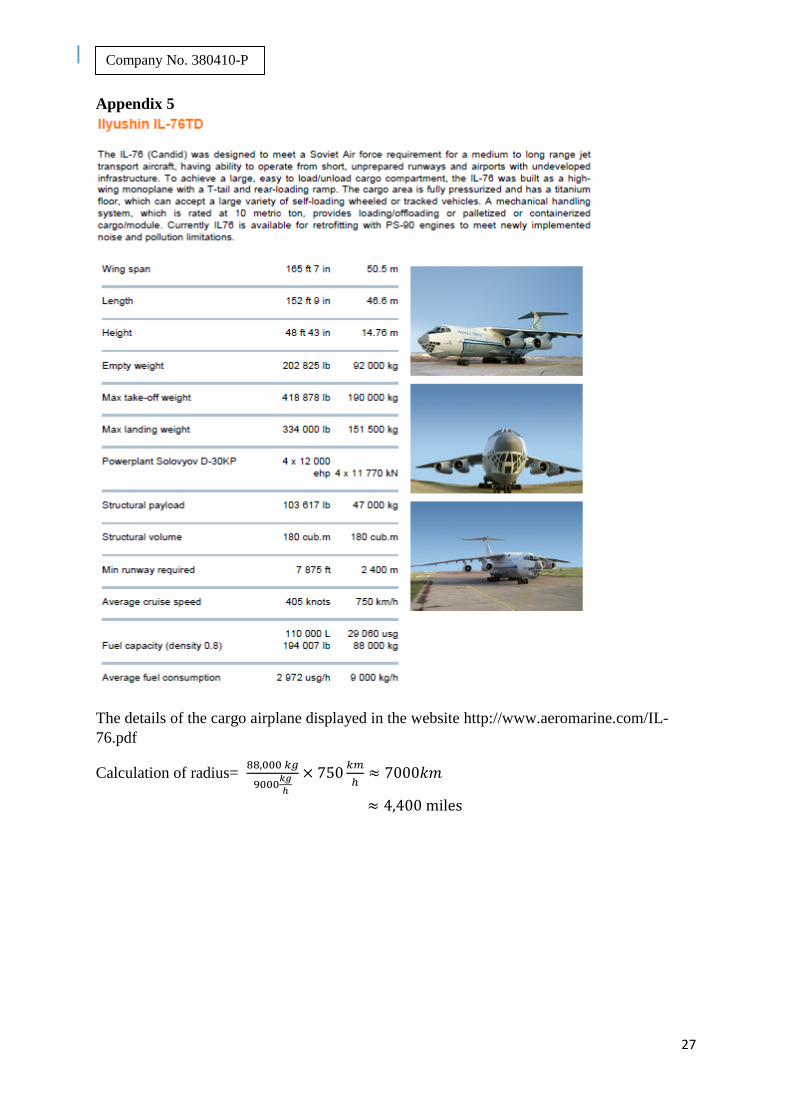

Another portion of the proceeds from the rights issues is planned to purchase a 1993 Ilyushin

IL-76TD, a cargo plane from Reem Travel (refer to Appendix 4) that is listing the plane on

GlobalPlaneSearch.com with a cash consideration of USD 3,700,000 (approximately RM

14,973,160) (refer to Appendix 2). In the previous financial year, only 9% of the total

revenue comes from air freight. The advancement in internet and booming of e-commerce

industry is creating a borderless world where a buyer can buy goods from sellers from the

other part of the world. This trend is shaping the future of global logistics and it will soon be

a profitable industry that our Company can be a part of. The acquisition of Ilyushin IL-76TD

will be one crucial step for our Company to continue our growth momentum in the global

stage.

As China is one of the largest exporters around the globe, we are assuming that we will

provide air freight services to export goods from China to different parts of the world within a

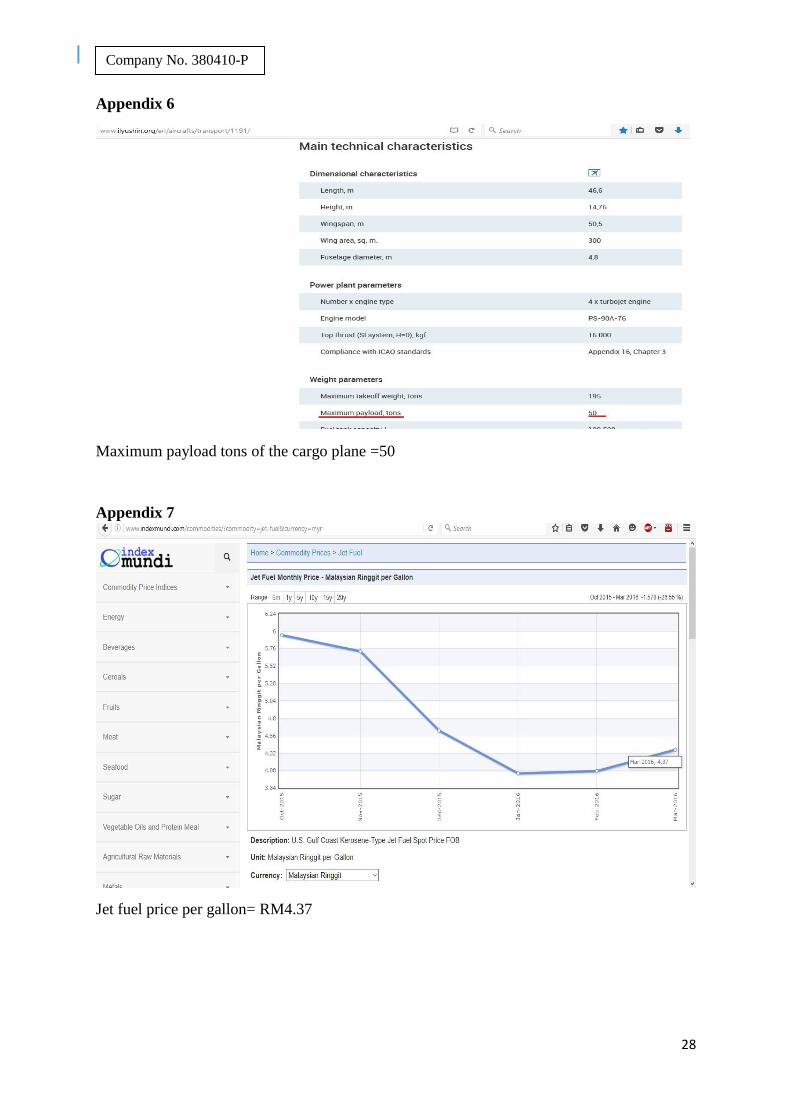

radius of 7,000km or 4,400 miles (refer to Appendix 5). The new cargo plane has a capacity

50 tonnes.

12

Company No. 380410-P

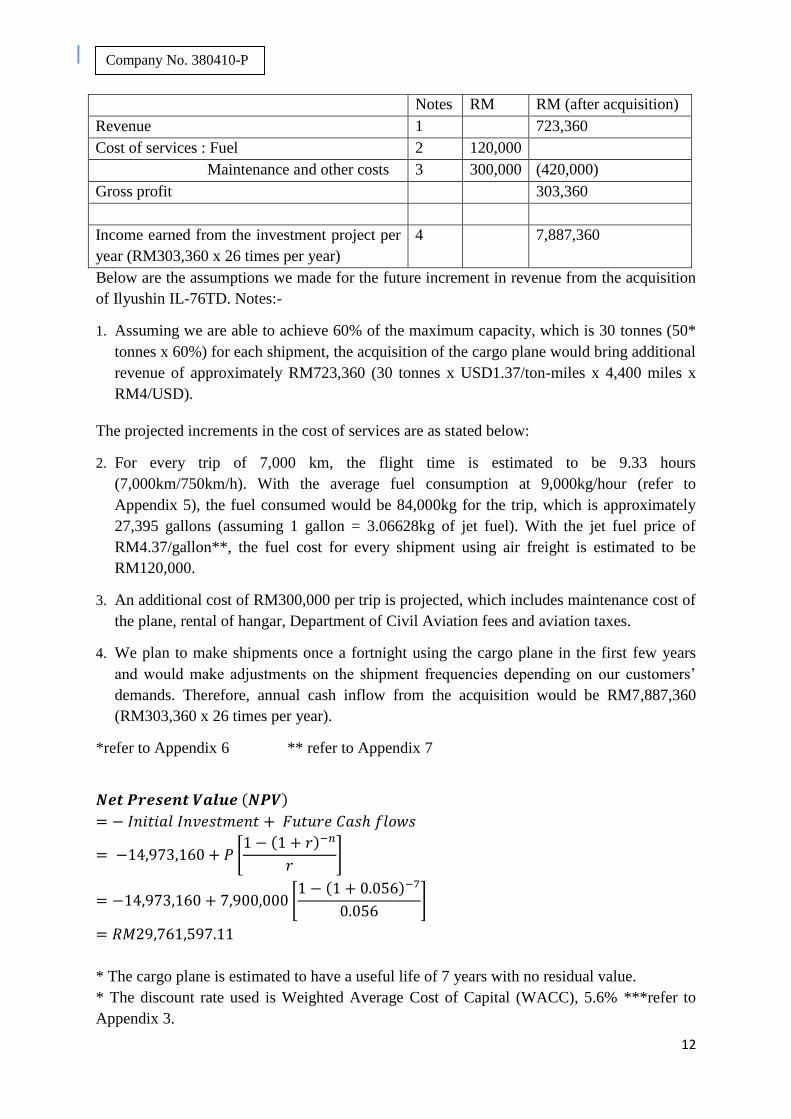

Notes RM RM (after acquisition)

Revenue 1 723,360

Cost of services : Fuel 2 120,000

Maintenance and other costs 3 300,000 (420,000)

Gross profit 303,360

Income earned from the investment project per

year (RM303,360 x 26 times per year)

4 7,887,360

Below are the assumptions we made for the future increment in revenue from the acquisition

of Ilyushin IL-76TD. Notes:-

1. Assuming we are able to achieve 60% of the maximum capacity, which is 30 tonnes (50*

tonnes x 60%) for each shipment, the acquisition of the cargo plane would bring additional

revenue of approximately RM723,360 (30 tonnes x USD1.37/ton-miles x 4,400 miles x

RM4/USD).

The projected increments in the cost of services are as stated below:

2. For every trip of 7,000 km, the flight time is estimated to be 9.33 hours

(7,000km/750km/h). With the average fuel consumption at 9,000kg/hour (refer to

Appendix 5), the fuel consumed would be 84,000kg for the trip, which is approximately

27,395 gallons (assuming 1 gallon = 3.06628kg of jet fuel). With the jet fuel price of

RM4.37/gallon**, the fuel cost for every shipment using air freight is estimated to be

RM120,000.

3. An additional cost of RM300,000 per trip is projected, which includes maintenance cost of

the plane, rental of hangar, Department of Civil Aviation fees and aviation taxes.

4. We plan to make shipments once a fortnight using the cargo plane in the first few years

and would make adjustments on the shipment frequencies depending on our customers’

demands. Therefore, annual cash inflow from the acquisition would be RM7,887,360

(RM303,360 x 26 times per year).

*refer to Appendix 6 ** refer to Appendix 7

𝑵𝒆𝒕 𝑷𝒓𝒆𝒔𝒆𝒏𝒕 𝑽𝒂𝒍𝒖𝒆 (𝑵𝑷𝑽)

= − 𝐼𝑛𝑖𝑡𝑖𝑎𝑙 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 + 𝐹𝑢𝑡𝑢𝑟𝑒 𝐶𝑎𝑠ℎ 𝑓𝑙𝑜𝑤𝑠

= −14,973,160 + 𝑃 [1 − (1 + 𝑟)−𝑛

𝑟]

= −14,973,160 + 7,900,000 [1 − (1 + 0.056)−7

0.056]

= 𝑅𝑀29,761,597.11

* The cargo plane is estimated to have a useful life of 7 years with no residual value.

* The discount rate used is Weighted Average Cost of Capital (WACC), 5.6% ***refer to

Appendix 3.

13

Company No. 380410-P

5.0 RISK FACTORS

Prior to the Rights Shares and Warrants investment and subscription, prospective subscribers

and investors should pay particular attention to the following risk factors as the large extent

of our operations are not only governed by the legal, regulatory and business environment in

Malaysia, but other countries as well. There are also some uncontrollable factors involved in

our business. In addition, consideration should be paid to the other risk factors or future risks

which are not stated below, as those risks may impose material and adverse impacts on our

future business, financial condition and/or on our Shares.

5.1 Risk Involved In The Company

Our Company is an investment holding company, which is also known as one of the leading

freight forwarders in Malaysia. The main operation of FMHB is the intermediate agent

between importers/exporters and carriers. The business and operational risks arise from the

risk inherent in the logistics industry which includes, but not restrained to fluctuations of

charter rates, increases of labour costs, unforeseen breakdown of vessels, cargo planes, trains

and trucks, threat of rivalry, rise of port tariffs, lengthy quarantines and severe weather

phenomena at land and sea. Several strategies have been implemented to limit the risks, such

as delivering good services and develop good business relationship to maintain large client

base, close supervision of the transportation lines, controlling operation costs effectively, thus

there is no assurance that those factors will not affecting our Group’s business adversely.

Financing risk will be solved through the proceeds raised from the Rights Issue with

Warrants, to fund the working capital requirements if necessary. However, no assurance can

be given that there will be availability of necessary financing for our Group. Foreign currency

risks of our Group results from the transactions that are denominated in currencies other than

functional currencies of our Group, and in respect of the overseas investments in which the

risks arise from the fluctuation in foreign exchange.

5.2 Risks Relating To The Transportation And Logistics Industry

The transportation and logistics industry is highly and indirectly dependent on the fuel prices,

which constitute a large portion in the operating costs of this industry. The fluctuation of oil

prices might have adverse impact on the operating costs, which will indirectly cause the

cancellation of routes, transportation frequencies, and eventually lead to bankruptcy of some

companies. Thus, no assurance is provided that future revenue generated from our Group will

not be affected by the fuel prices.

The overall industry in general is subjected to terrorist attacks, natural disasters, epidemics

and social and political unrest. These threats may cause notable reduction in our services

demand, trip cancellations or delays which may results in operating costs increments.

Furthermore, for those events that are out of our control, may lead to decline in our services

demand and hike in operating costs, thus influence the financial condition and company’s

performance adversely.

14

Company No. 380410-P

5.3 Risks Associated To The Rights Issue With Warrants

The fluctuation of our Shares prices and trading volume is affected by various factors, such as

the prevailing market and stock market sentiment, instability of equity markets, fluctuation of

interest rate, future prospects of industry, demand and supply factors of our Shares.

Furthermore, the prices of FMHB Shares could be adversely influenced by external factors

including the conditions of economic, political and industry. Thus, no assurance can be given

that the market price of Rights Shares will trade above the current price or theoretical ex-

rights price that will meet the specific targets of the holders of the Right Shares, after

completing the Rights Issue with Warrants.

The risks of delay or cancellation of Rights Issue with Warrants may arise during the

implementation if the events or circumstances involved significant adverse change that are

beyond our control. In addition, there are conditions where the Managing Underwriter may

terminate the Underwriting Agreement on behalf of the Joint Underwriters if termination

events stated in the agreement happened. These events may have a negative impact on the

financial condition and prospect of our Company and therefore the Managing Underwriter

would be reluctant to proceed with the Right Issue with Warrants as documented in the

agreement. Hence, no assurance can be given. No assurance would be provided that the

events above will not cause a delay or abortion of the Rights Issue with Warrants. The

Company will return all monies that were received from the applicants without interest in

events where the Rights Issue with Warrants is cancelled.

Reduction of voting interest and proportionate ownership, may occur if the entitled

shareholders do not or unable to accept the Provisional Allotments. Accordingly, there will

be reduction in their shareholdings in FMHB regarding the percentage of enlarged issued and

paid-up capital share.

5.4 Other Risks

The assets of our Group are substantially located, and the operations are mainly conducted in

Malaysia. However, to further strengthen the expansion and growth of our businesses, we

have also conducted extensive worldwide coverage with the network of 200 independent

agents covering 145 ports in more than 53 countries. Therefore, our Group’s financial

performance and results of operations are very much dependent on the prevalent economic,

political, and regulatory environment in Malaysia and also other regional and/other countries

from time to time. We constantly seek to reduce the risks by adopting prudent management

and operating the procedures effectively, yet, no assurance can be provided that such risks

will not have material impact on our Group.

15

Company No. 380410-P

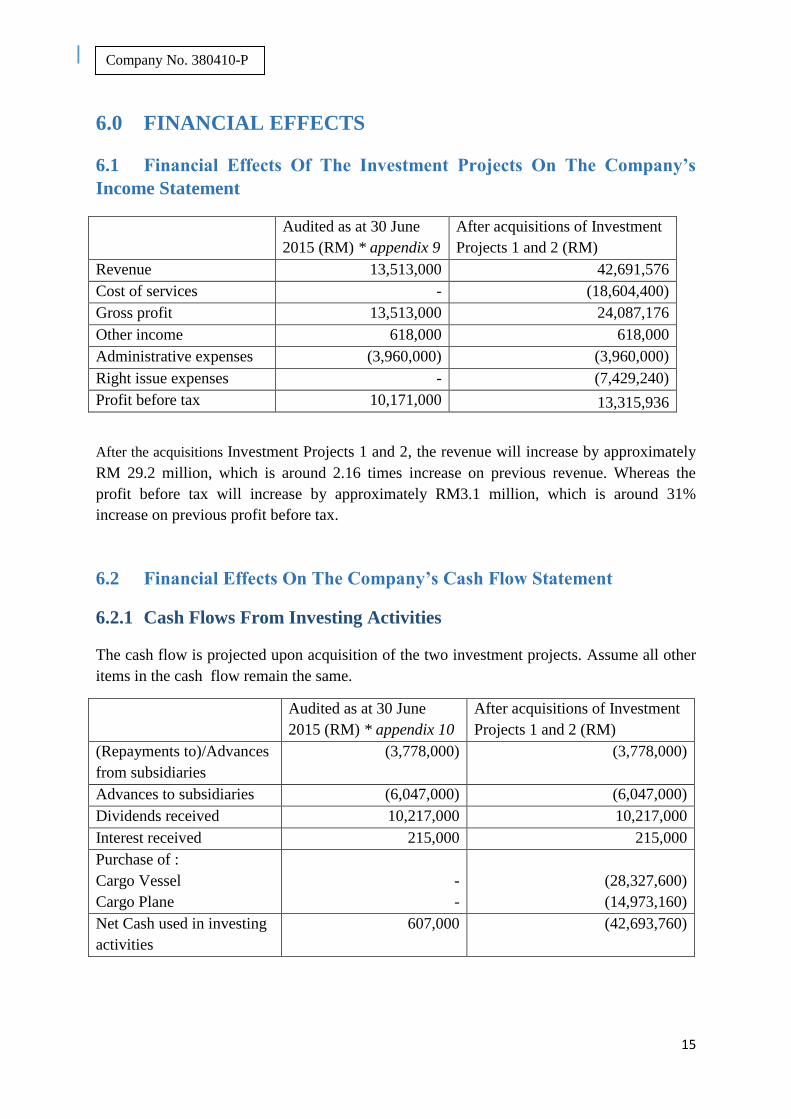

6.0 FINANCIAL EFFECTS

6.1 Financial Effects Of The Investment Projects On The Company’s

Income Statement

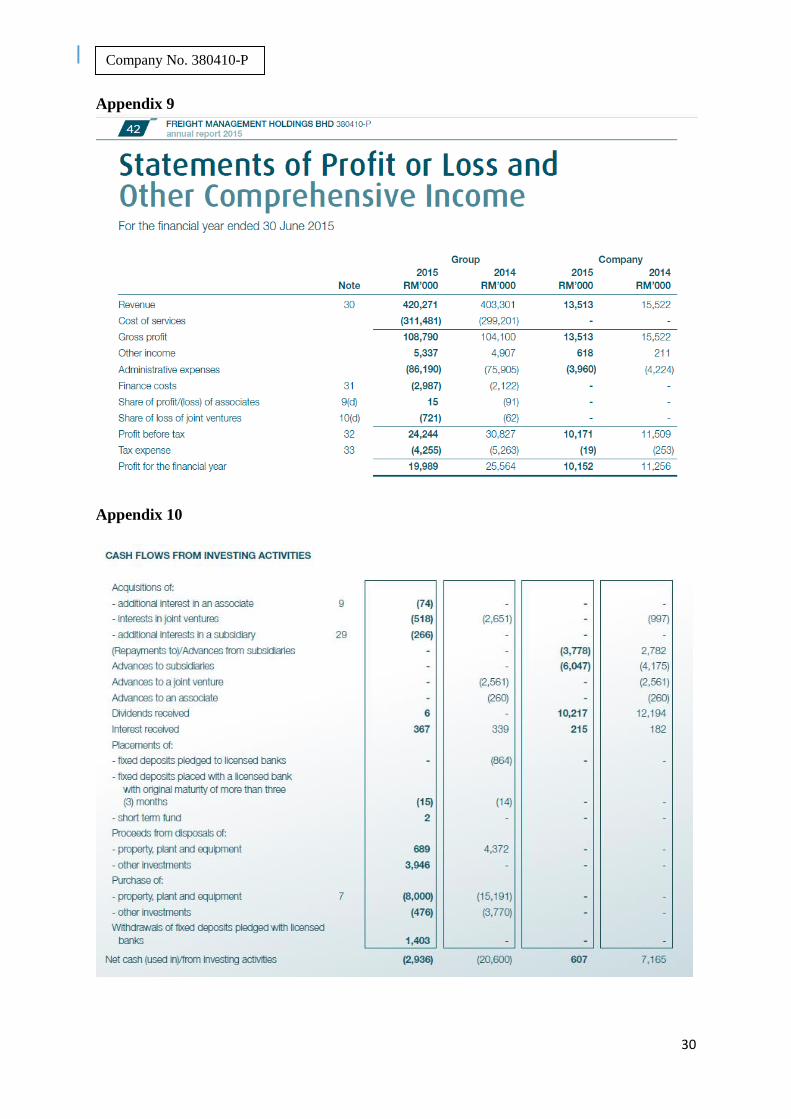

Audited as at 30 June

2015 (RM) * appendix 9

After acquisitions of Investment

Projects 1 and 2 (RM)

Revenue 13,513,000 42,691,576

Cost of services - (18,604,400)

Gross profit 13,513,000 24,087,176

Other income 618,000 618,000

Administrative expenses (3,960,000) (3,960,000)

Right issue expenses - (7,429,240)

Profit before tax 10,171,000 13,315,936

After the acquisitions Investment Projects 1 and 2, the revenue will increase by approximately

RM 29.2 million, which is around 2.16 times increase on previous revenue. Whereas the

profit before tax will increase by approximately RM3.1 million, which is around 31%

increase on previous profit before tax.

6.2 Financial Effects On The Company’s Cash Flow Statement

6.2.1 Cash Flows From Investing Activities

The cash flow is projected upon acquisition of the two investment projects. Assume all other

items in the cash flow remain the same.

Audited as at 30 June

2015 (RM) * appendix 10

After acquisitions of Investment

Projects 1 and 2 (RM)

(Repayments to)/Advances

from subsidiaries

(3,778,000) (3,778,000)

Advances to subsidiaries (6,047,000) (6,047,000)

Dividends received 10,217,000 10,217,000

Interest received 215,000 215,000

Purchase of :

Cargo Vessel

Cargo Plane

-

-

(28,327,600)

(14,973,160)

Net Cash used in investing

activities

607,000 (42,693,760)

16

Company No. 380410-P

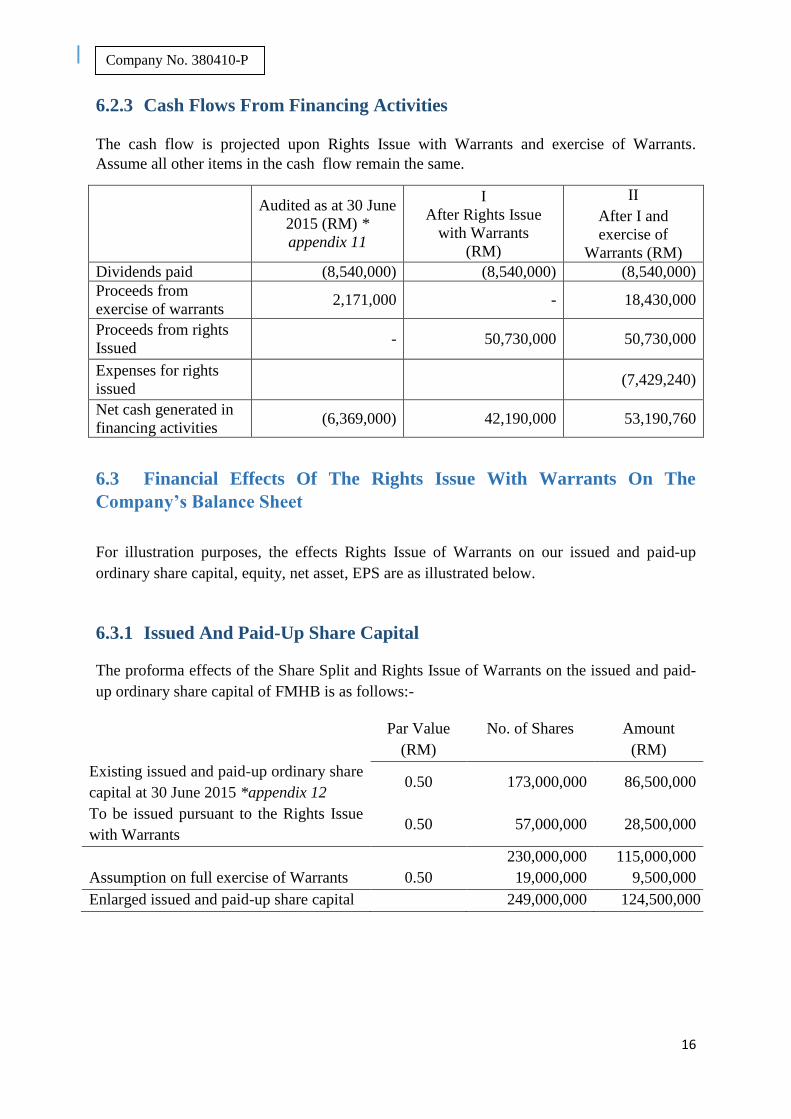

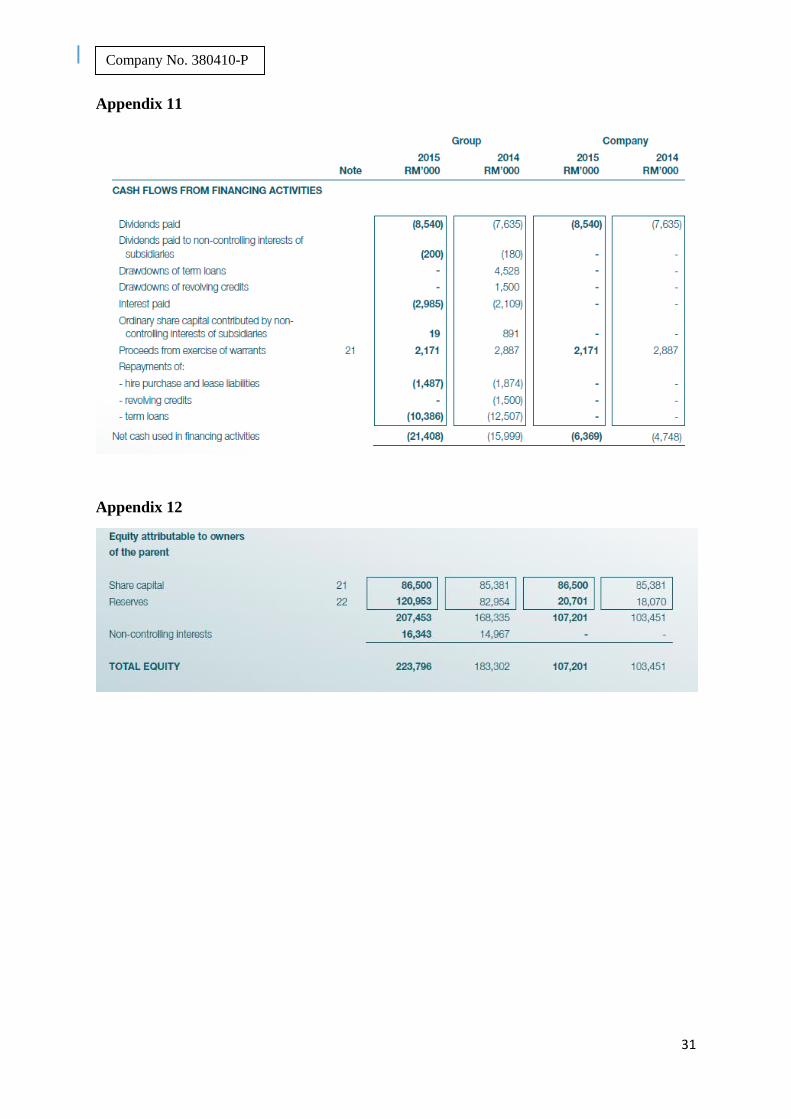

6.2.3 Cash Flows From Financing Activities

The cash flow is projected upon Rights Issue with Warrants and exercise of Warrants.

Assume all other items in the cash flow remain the same.

Audited as at 30 June

2015 (RM) *

appendix 11

I

After Rights Issue

with Warrants

(RM)

II

After I and

exercise of

Warrants (RM)

Dividends paid (8,540,000) (8,540,000) (8,540,000)

Proceeds from

exercise of warrants 2,171,000 - 18,430,000

Proceeds from rights

Issued - 50,730,000 50,730,000

Expenses for rights

issued (7,429,240)

Net cash generated in

financing activities (6,369,000) 42,190,000 53,190,760

6.3 Financial Effects Of The Rights Issue With Warrants On The

Company’s Balance Sheet

For illustration purposes, the effects Rights Issue of Warrants on our issued and paid-up

ordinary share capital, equity, net asset, EPS are as illustrated below.

6.3.1 Issued And Paid-Up Share Capital

The proforma effects of the Share Split and Rights Issue of Warrants on the issued and paid-

up ordinary share capital of FMHB is as follows:-

Par Value

(RM)

No. of Shares Amount

(RM)

Existing issued and paid-up ordinary share

capital at 30 June 2015 *appendix 12 0.50 173,000,000 86,500,000

To be issued pursuant to the Rights Issue

with Warrants 0.50 57,000,000 28,500,000

230,000,000 115,000,000

Assumption on full exercise of Warrants 0.50 19,000,000 9,500,000

Enlarged issued and paid-up share capital 249,000,000 124,500,000

17

Company No. 380410-P

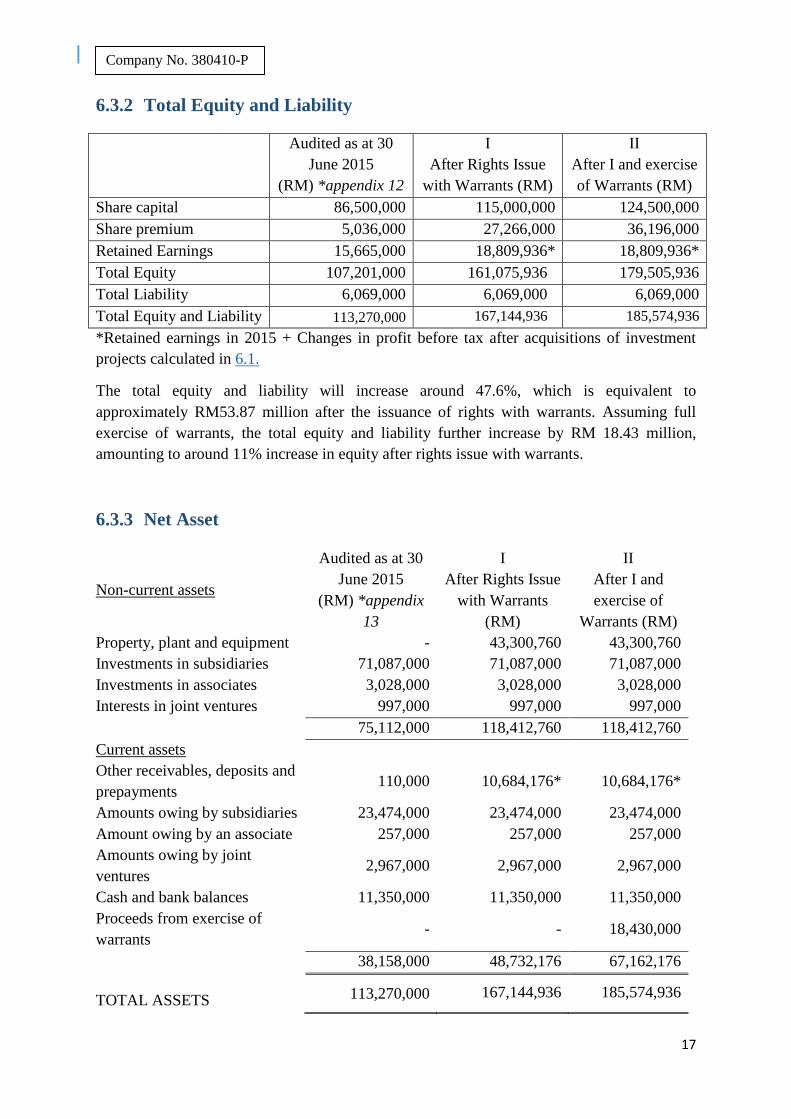

6.3.2 Total Equity and Liability

Audited as at 30

June 2015

(RM) *appendix 12

I

After Rights Issue

with Warrants (RM)

II

After I and exercise

of Warrants (RM)

Share capital 86,500,000 115,000,000 124,500,000

Share premium 5,036,000 27,266,000 36,196,000

Retained Earnings 15,665,000 18,809,936* 18,809,936*

Total Equity 107,201,000 161,075,936 179,505,936

Total Liability 6,069,000 6,069,000 6,069,000

Total Equity and Liability 113,270,000 167,144,936 185,574,936

*Retained earnings in 2015 + Changes in profit before tax after acquisitions of investment

projects calculated in 6.1.

The total equity and liability will increase around 47.6%, which is equivalent to

approximately RM53.87 million after the issuance of rights with warrants. Assuming full

exercise of warrants, the total equity and liability further increase by RM 18.43 million,

amounting to around 11% increase in equity after rights issue with warrants.

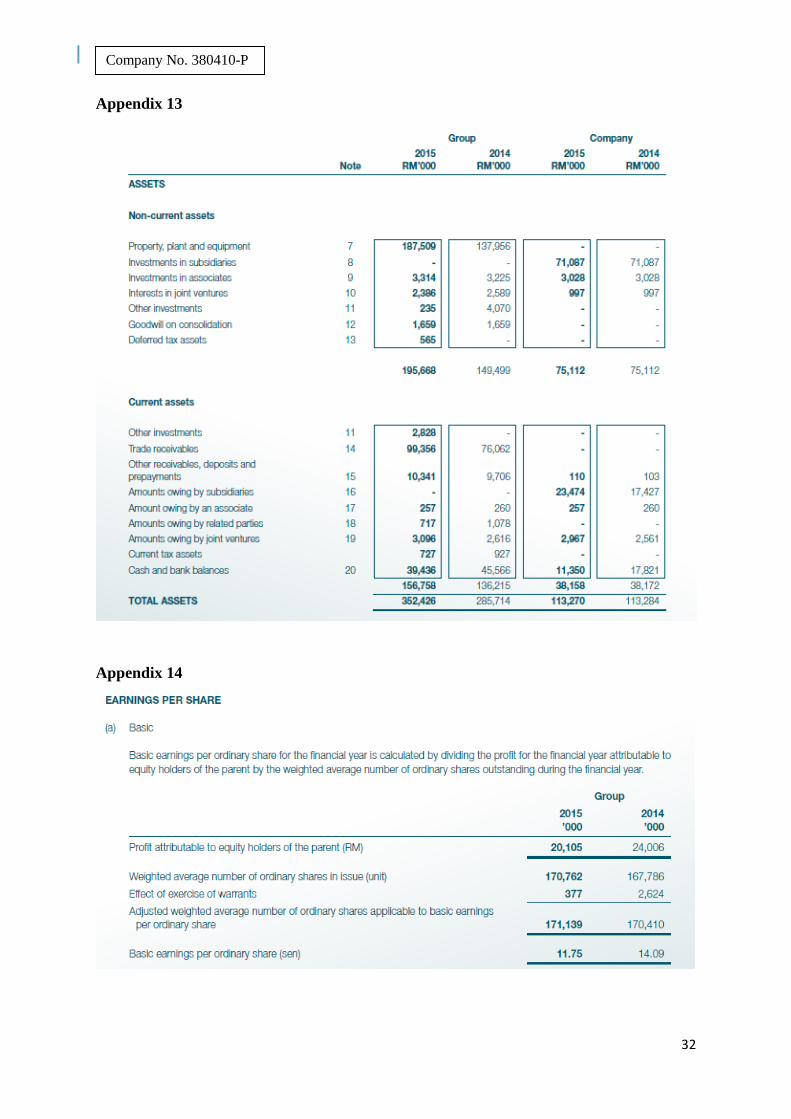

6.3.3 Net Asset

Non-current assets

Audited as at 30

June 2015

(RM) *appendix

13

I

After Rights Issue

with Warrants

(RM)

II

After I and

exercise of

Warrants (RM)

Property, plant and equipment - 43,300,760 43,300,760

Investments in subsidiaries 71,087,000 71,087,000 71,087,000

Investments in associates 3,028,000 3,028,000 3,028,000

Interests in joint ventures 997,000 997,000 997,000

75,112,000 118,412,760 118,412,760

Current assets

Other receivables, deposits and

prepayments 110,000 10,684,176* 10,684,176*

Amounts owing by subsidiaries 23,474,000 23,474,000 23,474,000

Amount owing by an associate 257,000 257,000 257,000

Amounts owing by joint

ventures 2,967,000 2,967,000 2,967,000

Cash and bank balances 11,350,000 11,350,000 11,350,000

Proceeds from exercise of

warrants - - 18,430,000

38,158,000 48,732,176 67,162,176

TOTAL ASSETS 113,270,000 167,144,936 185,574,936

18

Company No. 380410-P

* Other receivables, deposits and prepayments in 2015 + income generated from investment

projects as calculated in 6.1.

Assuming acquisition of investment projects are done once the rights are issued. The total

assets increased by RM53,874,936, which is around 47.6% after rights issue with warrants,

and further increased by RM18,430,000 after the full exercise of warrants assuming all other

items remain the same.

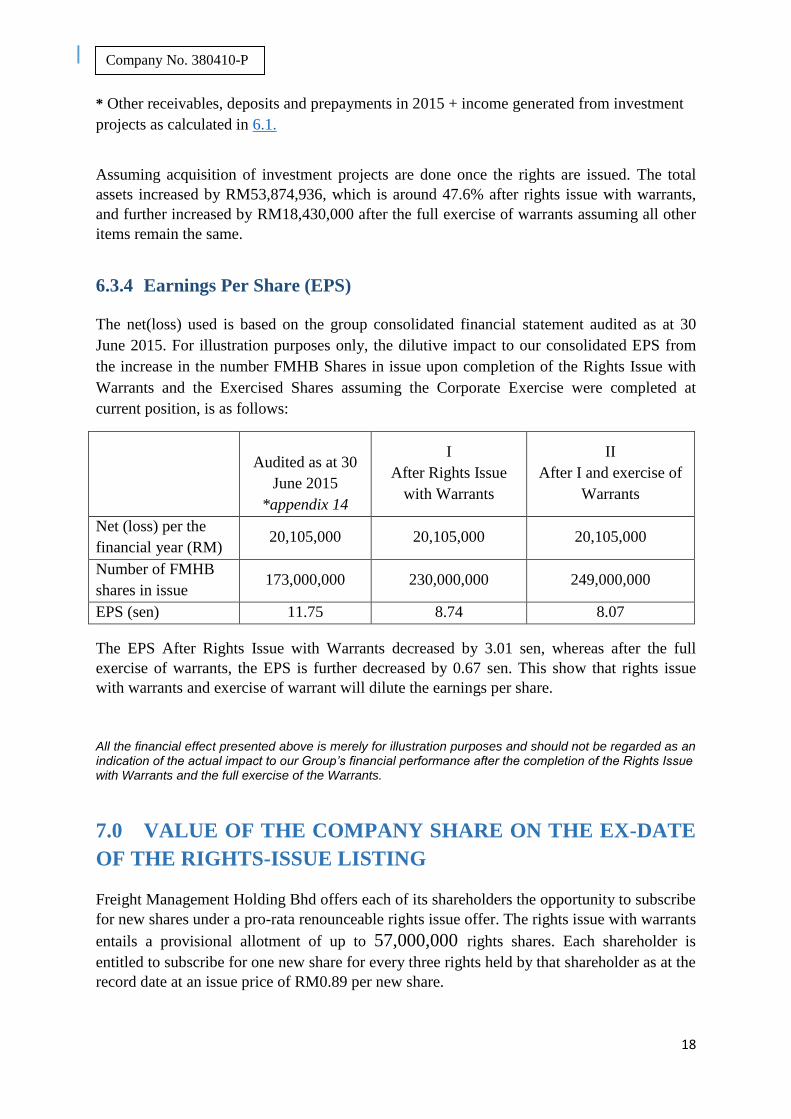

6.3.4 Earnings Per Share (EPS)

The net(loss) used is based on the group consolidated financial statement audited as at 30

June 2015. For illustration purposes only, the dilutive impact to our consolidated EPS from

the increase in the number FMHB Shares in issue upon completion of the Rights Issue with

Warrants and the Exercised Shares assuming the Corporate Exercise were completed at

current position, is as follows:

Audited as at 30

June 2015

*appendix 14

I

After Rights Issue

with Warrants

II

After I and exercise of

Warrants

Net (loss) per the

financial year (RM) 20,105,000 20,105,000 20,105,000

Number of FMHB

shares in issue 173,000,000 230,000,000 249,000,000

EPS (sen) 11.75 8.74 8.07

The EPS After Rights Issue with Warrants decreased by 3.01 sen, whereas after the full

exercise of warrants, the EPS is further decreased by 0.67 sen. This show that rights issue

with warrants and exercise of warrant will dilute the earnings per share.

All the financial effect presented above is merely for illustration purposes and should not be regarded as an indication of the actual impact to our Group’s financial performance after the completion of the Rights Issue with Warrants and the full exercise of the Warrants.

7.0 VALUE OF THE COMPANY SHARE ON THE EX-DATE

OF THE RIGHTS-ISSUE LISTING

Freight Management Holding Bhd offers each of its shareholders the opportunity to subscribe

for new shares under a pro-rata renounceable rights issue offer. The rights issue with warrants

entails a provisional allotment of up to 57,000,000 rights shares. Each shareholder is

entitled to subscribe for one new share for every three rights held by that shareholder as at the

record date at an issue price of RM0.89 per new share.

19

Company No. 380410-P

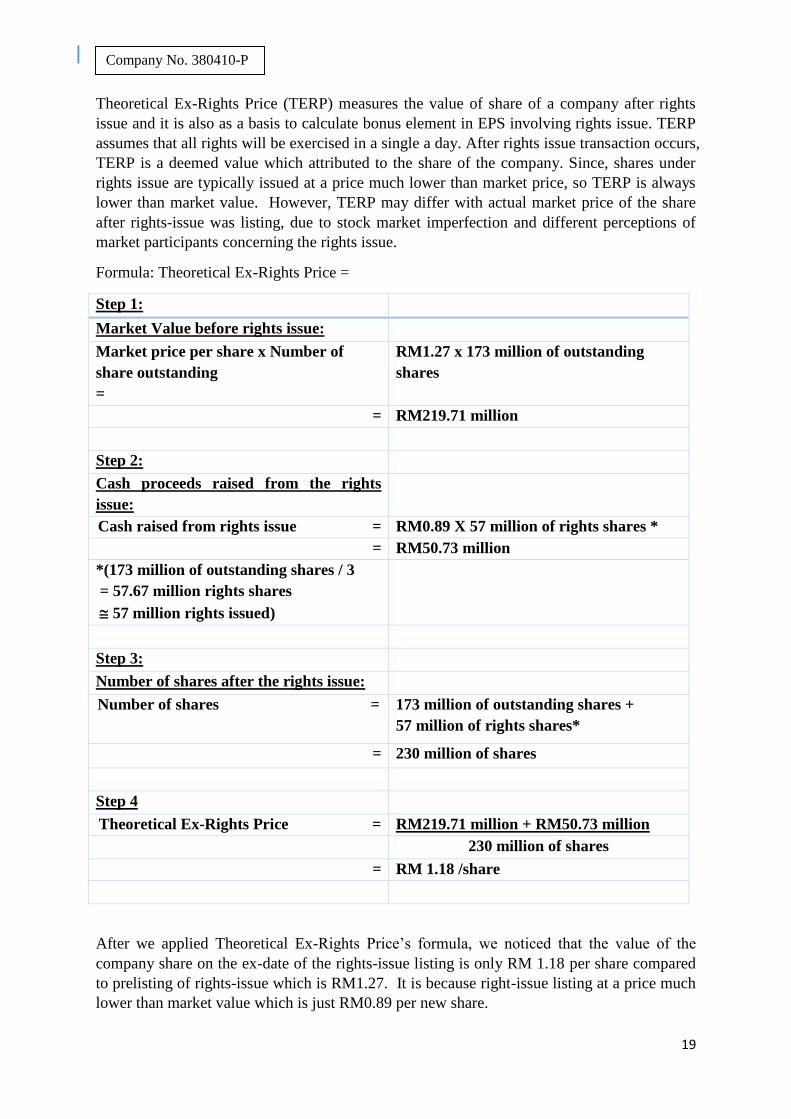

Theoretical Ex-Rights Price (TERP) measures the value of share of a company after rights

issue and it is also as a basis to calculate bonus element in EPS involving rights issue. TERP

assumes that all rights will be exercised in a single a day. After rights issue transaction occurs,

TERP is a deemed value which attributed to the share of the company. Since, shares under

rights issue are typically issued at a price much lower than market price, so TERP is always

lower than market value. However, TERP may differ with actual market price of the share

after rights-issue was listing, due to stock market imperfection and different perceptions of

market participants concerning the rights issue.

Formula: Theoretical Ex-Rights Price =

Step 1:

Market Value before rights issue:

Market price per share x Number of

share outstanding

=

RM1.27 x 173 million of outstanding

shares

= RM219.71 million

Step 2:

Cash proceeds raised from the rights

issue:

Cash raised from rights issue = RM0.89 X 57 million of rights shares *

= RM50.73 million

*(173 million of outstanding shares / 3

= 57.67 million rights shares

57 million rights issued)

Step 3:

Number of shares after the rights issue:

Number of shares = 173 million of outstanding shares +

57 million of rights shares*

= 230 million of shares

Step 4

Theoretical Ex-Rights Price = RM219.71 million + RM50.73 million

230 million of shares

= RM 1.18 /share

After we applied Theoretical Ex-Rights Price’s formula, we noticed that the value of the

company share on the ex-date of the rights-issue listing is only RM 1.18 per share compared

to prelisting of rights-issue which is RM1.27. It is because right-issue listing at a price much

lower than market value which is just RM0.89 per new share.

20

Company No. 380410-P

8.0 APPLICATION OF THEORIES

8.1 Capital Asset Pricing Model Theory

There are mainly 4 researchers who credited with CAPM development which are Markotwitz.

Sharpe, Lintner and Mossin. Markowitz explored the implication of introducing a risk free

asset. Sharpe is credited with development the Capital Asset Pricing Model (CAPM). In the

mid-20th century, Lintner and Mossin subsequently derived similar models. Generally, there

is no need for Covariance matrix because according to CAPM, stocks and investment can be

measured by using market benchmark also known as the market portfolio or returns.

Basically, there are a few assumptions made in CAPM Theory.

1. Investors are Efficient Investors

2. Investors can lend or borrow at risk free interest rate

3. Investors have homogeneous expectations for returns.

4. Capital markets are in equilibrium, No taxes or transaction cost, no changes in interest

rate and inflation.

Formula: 𝐸(𝑅𝑎) = 𝑟𝑓 + 𝛽𝑎(𝑅𝑚 − 𝑅𝑓)

Where,

𝑟𝑓 = Risk free rate

𝛽𝑎 = Beta of security

𝑅𝑚= Expected market return

Then, we can apply this formula to calculate expected return of Freight Management Holding

Bhd. (*appendix 15)

CAPM = 3.903% + 0.598(7.802% - 3.903%)

= 6.2346%

Under CAPM, the initial expected return before rights issue is 6.24%

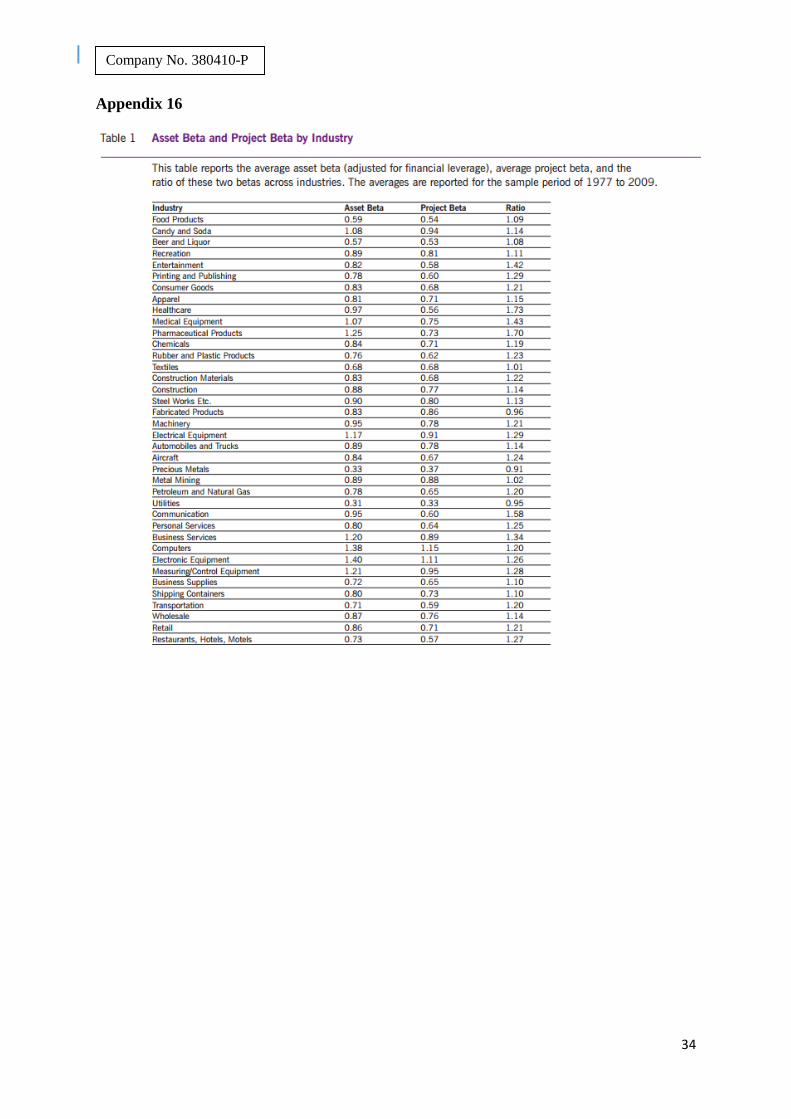

After the rights issued, the proceeds will be used to fund 2 new projects, which are

acquisition of cargo vessel and cargo plane. We assumed that project beta will increase to

0.73 due to risks; this beta is taken from a journal ‘Assessing Project Risk’ done by Antonio

E. Bernado and e.t.c, UCLA Andreson School of Management, Bhagwan

Chowdhry.(*appendix 16) We also make our assumption where there is no change in risk

free rate, but expected market return will increase to 8%)

CAPM = 3.903% + 0.73(8% - 3.903%)

= 6.89381%

The new expected return after the rights issued and the investment in new projects, we found

that the beta has slightly increased. However, it did contribute for the increasing of market

return from 6.24% to 6.89%. In conclusion, our group believes that the new projects are both

feasible and it did help FMH to achieve higher expected return.

21

Company No. 380410-P

8.2 (Modern) Portfolio Theory (MPT)

In1950s, Harry Markowitz has come out one of the most influential theories for financial and

investment. He developed Modern Portfolio Theory and published it in Journal of Finance.

Furthermore, efficient market hypothesis is the cornerstone of portfolio theory; securities

market is always competitive and efficient. Basically, the central tenet of portfolio theory is

markets are dominated by rational, risk adverse investors who seek for maximum possible

expected return. Investors are all being assumed as risk-averse under this theory. This means

that investors will choose the least risky portfolio with higher expected return.

In MPT, it stated that two components in the risk of individual stock returns which are

systematic risk and unsystematic risk. Systematic risk is called common, undiversifiable or

market risk which cannot be diversified away. For example, economic downturn, changes in

interest rate and others. Unsystematic risk is also called unique, diversifiable or firm-specific

risk. This risk can be diversified away by holding more number of stocks in your portfolio.

There are normally 2 types of news that will affect the stock price and dividend. Firm specific

news and market-wide news will cause the fluctuation of stock price and dividend. When we

combined many stocks in a large portfolio, the unsystematic risk will be diversified away due

to good news and bad news in the market that will affect different stocks. Thus, in the end

good and bad news will be relatively constant. However, systematic risk cannot be diversified

away because the stocks are simultaneously affected by the news, so it will directly affects

the entire portfolio.

Formula: E(𝑟𝑝) = 𝑤𝐷E(𝑟𝐷) + 𝑤𝐸 E(𝑟𝐸)

𝜎2𝑝 = 𝑊𝐷²𝜎𝐷² + 𝑊𝐸²𝜎𝐸² + 2𝑊𝐷𝑊𝐸𝐶𝑜𝑣(𝑟𝑑, 𝑟𝑒)

Sharpe ratio: 𝑅−𝑟𝑓

𝜎

Freight Management Holding Berhad will invest equally in both projects which are

acquisition of cargo vessel and cargo plane. According to various projects that have been

done by other companies within the same industry, we assumed the expected return of each

project will be 12% & 10% respectively. The standard deviations are 15% and 20%

accordingly. The portfolio has a correlation of 20%. Thus, now we can work out the formula.

Er = 0.50(0.25) + 0.50(0.20) = [email protected]%

σ = [0.50²0.15² + 0.50²0.20² + 2(0.5)(0.5)(0.20)(0.15)(0.20)]½ = 0.1365 @ 13.65%

Sharpe ratio = (22.5% - 3.903%) / 13.65% = 1.3624

This portfolio provides 11% of expected return and the volatility or risk is only 13.65%. Most

importantly, the Sharpe ratio is more than 1, 1.3624 is considering good. In other words, this

portfolio able to generate high return on a risk adjusted basis.

22

Company No. 380410-P

8.3 Trade-Off Theory of Capital Structure

According to this theory, it is an idea that how a company makes corporate finance decision

to choose how much debt and equity financing to maximize the value of the company. This

theory pointed that firms or companies are always financed by both debt and equity. It

normally deals with 2 concepts, agency costs and financial distress costs. Another important

objective of trade-off theory is offsetting the costs against benefits of debt. In other words,

tax shield is one of the benefits of debt. It can be used to against the financial distress costs

associated with leverage. Thus, the amount of debt that a firm should take in order to

maximize its value is depending on the benefits of leverage.

By referring to M&M theory, when the leverage is increase, it will cause the value of firm to

increase. The tax benefit of debt will actually be eroded if the cost of financial distress is too

significant, then the value of the firm will start to decrease, it will also lead to increase of the

likelihood of default. So, there is always an optimal debt level, at this level, the firm’s value

is maximized. Beyond the level aforesaid, the probability of default becomes higher and

higher, then the financial distress started to arise. The likelihood of firms cannot settle their

debt and therefore default is determined by the probability of financial distress.

Formula:

𝑉𝐿 = 𝑉𝑈 + 𝑃𝑉(Interest Tax Shield) − 𝑃𝑉(𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑎𝑙 𝐷𝑖𝑠𝑡𝑟𝑒𝑠𝑠 𝐶𝑜𝑠𝑡𝑠)

After Freight Management Holding Bhd (FMH) has decided to carry out 2 new investment

projects which are acquisition of cargo plane and cargo vessel. According to Bloomberg,

FMH debt to equity ratio is decreasing from 0.26379 to 0.2320, and has an equity cost of

capital of 6.2% and debt cost of capital of 4.2%. FMH’s corporate tax rate is 25%, and its

new market capitalization is RM250.44m, total new outstanding debt is RM59.02m. Pretax

WACC is 6.4%, FCF is expected to be RM 8m in 2016 and expected future growth rate per

year is 3.1% (*Appendix 3)

WACC = 1

1.232(6.2%) +

0.232

1.232(4.2%)(1 − 0.25) = 5.6%

𝑉𝐿 = 𝐸 + 𝐷 = RM250.44m + RM59.02m = RM309.46m

𝑉𝑢 =𝐹𝐶𝐹

𝑝𝑟𝑒𝑡𝑎𝑥 𝑊𝐴𝐶𝐶−𝑔=

𝑅𝑀8𝑚

6.4%−3.1% = RM242.42m

PV(Interest Tax Shield) = RM309.46m – RM242.42m = RM67.04m

Therefore, 𝑉𝐿𝑜𝑓 𝐹𝑀𝐻 = 𝑅𝑀242.42𝑚 + 𝑅𝑀67.04𝑚 = 𝑅𝑀309.46𝑚

We assumed that there is no any financial distress cost as Freight Management Holding Bhd

is still has enough financial means to settle their interest of out-standing debt. Also, FMH

new debt to equity ratio is only 0.2320, it also a signal to prove that their outstanding debt is

low and FMH has enough financial capability to increase their debt to get more interest tax

shield as it can maximize value of Freight Management Holding Bhd.

23

Company No. 380410-P

DISCLAIMER

The information set forth herein has been obtained or derived from sources generally

available to the public and believed by the author(s) to be reliable, but the author(s) does not

make any representation or warranty, express or implied, as to its accuracy or completeness.

The information and data contained in the report has been obtained from sources believed to

be reliable but have not been independently verified and consequently no representation is

made as to the accuracy or completeness of this report. For any direct or indirect losses that

arise from the reliance or use of the information and data in this analyst report are no liable

by anyone. There are subject to change for any information or recommendations that

contained in this report, without prior notice. This report may contain identifiable forward

looking statements and based on the information currently available and assumptions. Thus,

they are contained uncertainties and risks that could cause the difference between real results

and estimated results. This report should not be considered to be a recommendation by any

individual with regard to this company’s prospectus.

24

Company No. 380410-P

APPENDICES

Appendix 1

Ernest Hemingway Container Vessel for sale as displayed in NautiSNP website

TEU capacity: 4990

Appendix 2

Exchange rate: 1 USD = RM 4.0468

Acquisition price of cargo vessel =USD 7,000,000 (approximately RM28,327,600)

Acquisition price of cargo plane = USD 3,700,000 (approximately RM 14,973,160)

25

Company No. 380410-P

Appendix 3

WACC= 5.6%

26

Company No. 380410-P

Appendix 4

1993 Ilyushin IL-76TD for sale as displayed in GlobalPlaneSearch.com website

27

Company No. 380410-P

Appendix 5

The details of the cargo airplane displayed in the website http://www.aeromarine.com/IL-

76.pdf

Calculation of radius= 88,000 𝑘𝑔

9000𝑘𝑔

ℎ

× 750𝑘𝑚

ℎ≈ 7000𝑘𝑚

≈ 4,400 miles

28

Company No. 380410-P

Appendix 6

Maximum payload tons of the cargo plane =50

Appendix 7

Jet fuel price per gallon= RM4.37

29

Company No. 380410-P

Appendix 8

Financial highlights in annual report year 2015

30

Company No. 380410-P

Appendix 9

Appendix 10

31

Company No. 380410-P

Appendix 11

Appendix 12

32

Company No. 380410-P

Appendix 13

Appendix 14

33

Company No. 380410-P

Appendix 15

34

Company No. 380410-P

Appendix 16

35

Company No. 380410-P

REFERENCES

T. P. (n.d.). What Happens to the Share Price When New Shares Are Issued? Retrieved May

15, 2016, from http://finance.zacks.com/happens-share-price-new-shares-issued-7922.html

Online, T. S. (2015, March 19). Malaysia Airports rights issue oversubscribed. Retrieved

May 3, 2016, from http://www.thestar.com.my/business/business-news/2015/03/19/malaysia-

airports-rights-issue-oversubscribed/

Online, T. S. (2015, December 21). Hubline rights shares fully subscribed. Retrieved May 3,

2016, from http://www.thestar.com.my/business/business-news/2015/12/21/hubline-rights-

fully-subscribed/

Freight Management Holdings Bhd. (n.d.). Retrieved May 7, 2016, from

http://www.fmmalaysia.com.my/i_finance.html

Finding Right Stock. (n.d.). Retrieved May 15, 2016, from

http://www.reuters.com/finance/stocks/MAHB.KL/key-developments/article/3142467

Equities. (n.d.). Retrieved May 15, 2016, from

http://markets.ft.com/research/Markets/Tearsheets/Financials?s=FREIGHT:KLS

Bernardo, A. E., Chowdhry, B., & Goyal, A. (2012). Assessing Project Risk. Journal of

Applied Corporate Finance, 24(3), 94-100. doi:10.1111/j.1745-6622.2012.00393.x

The Capital Asset Pricing Model (CAPM). (2012). Essential Mathematics for Market Risk

Management Hubbert/Essential, 91-99. doi:10.1002/9781118467213.ch7

Definition of "Capital asset pricing model (CAPM)" - NASDAQ Financial Glossary. (n.d.).

Retrieved May 12, 2016, from http://www.nasdaq.com/investing/glossary/c/capital-asset-

pricing-model

Modern Portfolio Theory: An Overview - JMHinternational.com. (n.d.). Retrieved May 12,

2016, from

http://www.jmhinternational.com/news/news/selectednews/files/2009/03/20090312_Investop

edia_ModernPortfolioTheory-An Overview.pdf

Smith, K. V., Elton, E. J., & Gruber, M. J. (1982). Modern Portfolio Theory and Investment

Analysis. The Journal of Finance, 37(5), 1317. doi:10.2307/2327857

Modern Portfolio Theory (MPT) Definition | Investopedia. (2003). Retrieved May 13, 2016,

from http://www.investopedia.com/terms/m/modernportfoliotheory.asp

The MM Capital Structure vs. The Tradeoff Theory of Leverage - CFA Level 1 |

Investopedia. (2008). Retrieved May 13, 2016, from http://www.investopedia.com/exam-

guide/cfa-level-1/corporate-finance/mm-capital-structure-versus-tradeoff-leverage.asp

36

Company No. 380410-P

Trade-off Theory of Capital Structure. (n.d.). Retrieved May 13, 2016, from

http://finance.mapsofworld.com/corporate-finance/hybrid-financing/trade-off-theory-capital-

structure.html

Zhao, T., & Susmel, R. (n.d.). Testing the Trade-Off Theory of Capital Structure: A Kalman

Filter Approach. SSRN Electronic Journal SSRN Journal. doi:10.2139/ssrn.1303209

Miglo, A. (n.d.). The Pecking Order, Trade-Off, Signaling, and Market-Timing Theories of

Capital Structure: A Review. SSRN Electronic Journal SSRN Journal.

doi:10.2139/ssrn.1629304