Embed Size (px)

Citation preview

1

Earnings Release | Conference Call – 2Q14

August 15th, 2014

2

Agenda

Ricardo Ribeiro

Vice President

Carlos Wollenweber

CFO | IR Officer

Operational Highlights

Financial Highlights

3

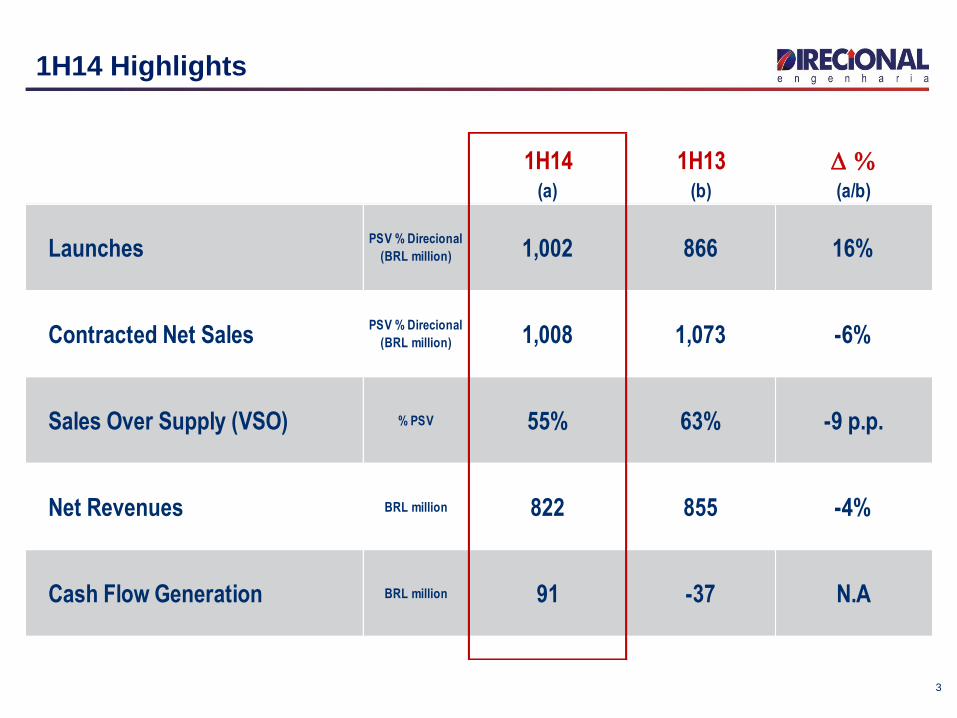

1H14 Highlights

1H14 1H13 D %(a) (b) (a/b)

LaunchesPSV % Direcional

(BRL million) 1,002 866 16%

Contracted Net SalesPSV % Direcional

(BRL million) 1,008 1,073 -6%

Sales Over Supply (VSO) % PSV 55% 63% -9 p.p.

Net Revenues BRL million 822 855 -4%

Cash Flow Generation BRL million 91 -37 N.A

4

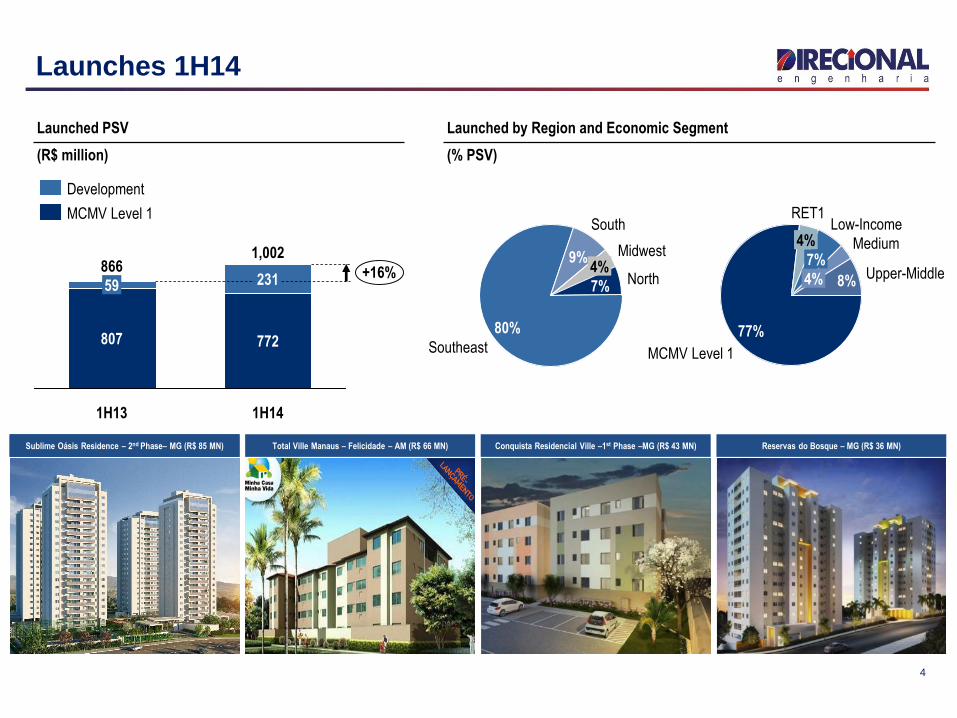

Launches 1H14

1,002

+16%

1H14

772

231

1H13

866

807

59

Launched PSV

(R$ million)

MCMV Level 1

Development

Conquista Residencial Ville –1st Phase –MG (R$ 43 MN)Total Ville Manaus – Felicidade – AM (R$ 66 MN)Sublime Oásis Residence – 2ª Etapa – MG (R$ 45,9 MM) Reservas do Bosque – MG (R$ 36 MN)

South

9%

Southeast

80%

North7%

Midwest4% Upper-Middle

8%

Medium

4%

Low-Income

7%

RET1

4%

MCMV Level 1

77%

Sublime Oásis Residence – 2nd Phase– MG (R$ 85 MN)

Launched by Region and Economic Segment

(% PSV)

5

Net Sales and Inventory – 1H14

Contracted Net Sales

(PSV - R$ million)

2Q14

13.4%

1Q14

55.3%

14.0%

4Q13

55.1%

21.1%

3Q13

46.9%

15.4%

2Q13

49.6%

21.2%

With MCMV Level 1 projectWithout MCMV Level 1 project

Sales-over-supply ratio (VSO)¹

(% Total PSV)

1 - VSO ratio = Net s ales inthe period / (Initial Inventory + Launches in the Period)

-6%

1H14

1,008

772

237

1H13

1,073

807

266

MCMV Level 1

Development

1H14

28%

2013

38%

201210%

<2012

24%

Sales by of Launching Period

(% PSV – Ex-MCMV Level 1)

6

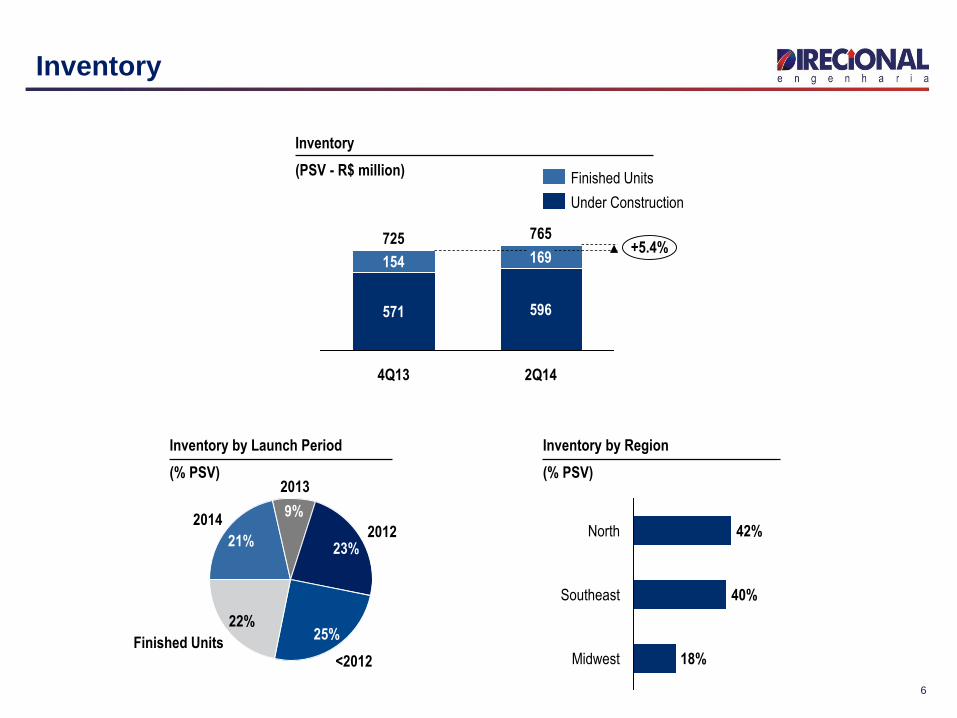

Inventory

Inventory

(PSV - R$ million)

765+5.4%

2Q14

596

169

4Q13

725

571

154

Finished Units

Under Construction

Finished Units

2013

9%2014

21%

22%

<2012

25%

201223%

Midwest 18%

Southeast 40%

North 42%

Inventory by Region

(% PSV)

Inventory by Launch Period

(% PSV)

7

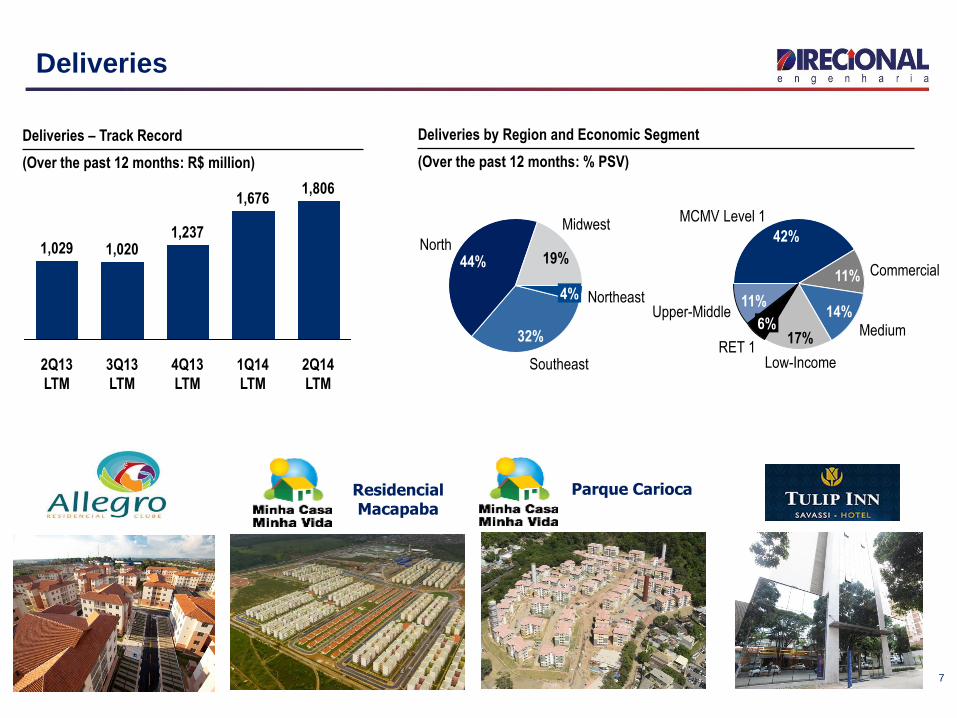

Deliveries

2Q14

LTM

1,806

1Q14

LTM

4Q13

LTM

1,676

3Q13

LTM

1,237

2Q13

LTM

1,0201,029

Deliveries – Track Record

(Over the past 12 months: R$ million)

Residencial Macapaba

Parque Carioca

Deliveries by Region and Economic Segment

(Over the past 12 months: % PSV)

Northeast4%

Midwest

19%North

44%

Southeast

32% 17%

Low-Income

14%Medium

11% Commercial

42%

MCMV Level 1

Upper-Middle11%

6%

RET 1

8

Carlos Wollenweber

CFO | IR OfficerFinancial Highlights

9

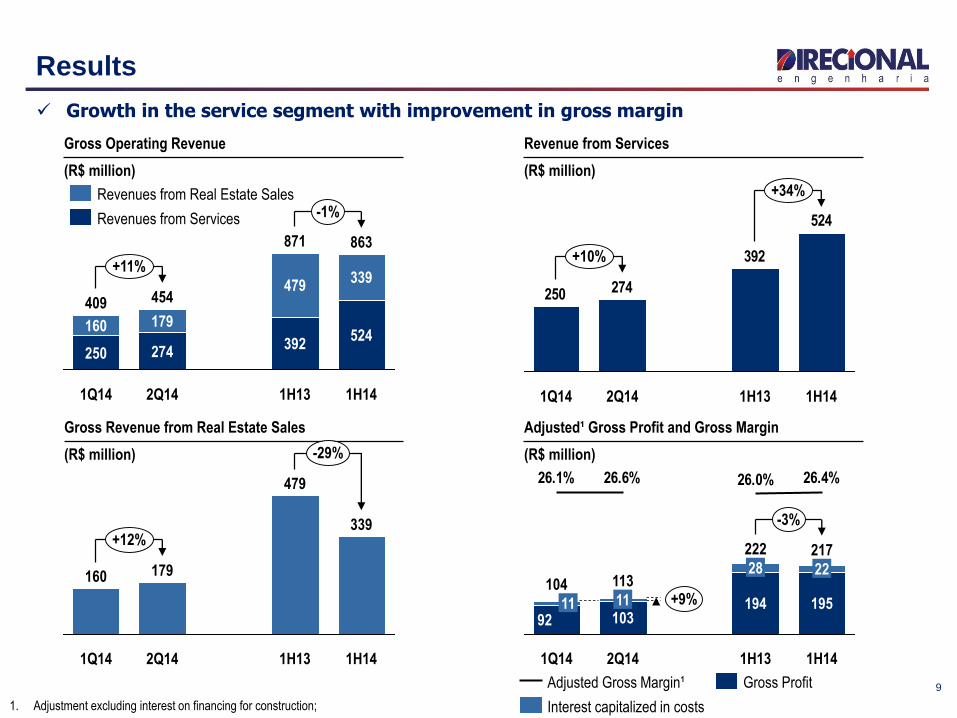

Results

1. Adjustment excluding interest on financing for construction;

+11%

-1%

1H14

863

524

339

1H13

871

392

479

2Q14

454

274

179

1Q14

409

250

160

Gross Operating Revenue

(R$ million)

Revenues from Services

Revenues from Real Estate Sales

524

392

274250

+10%

+34%

1H141H132Q141Q14

Revenue from Services

(R$ million)

+12%

-29%

1H14

339

1H13

479

2Q14

179

1Q14

160

Gross Revenue from Real Estate Sales

(R$ million)

Adjusted¹ Gross Profit and Gross Margin

(R$ million)

26.4%26.0%26.6%26.1%

-3%

+9%

1H14

217

195

22

1H13

222

194

28

2Q14

113

10311

1Q14

104

9211

Gross Profit

Interest capitalized in costs

Adjusted Gross Margin¹

Growth in the service segment with improvement in gross margin

10

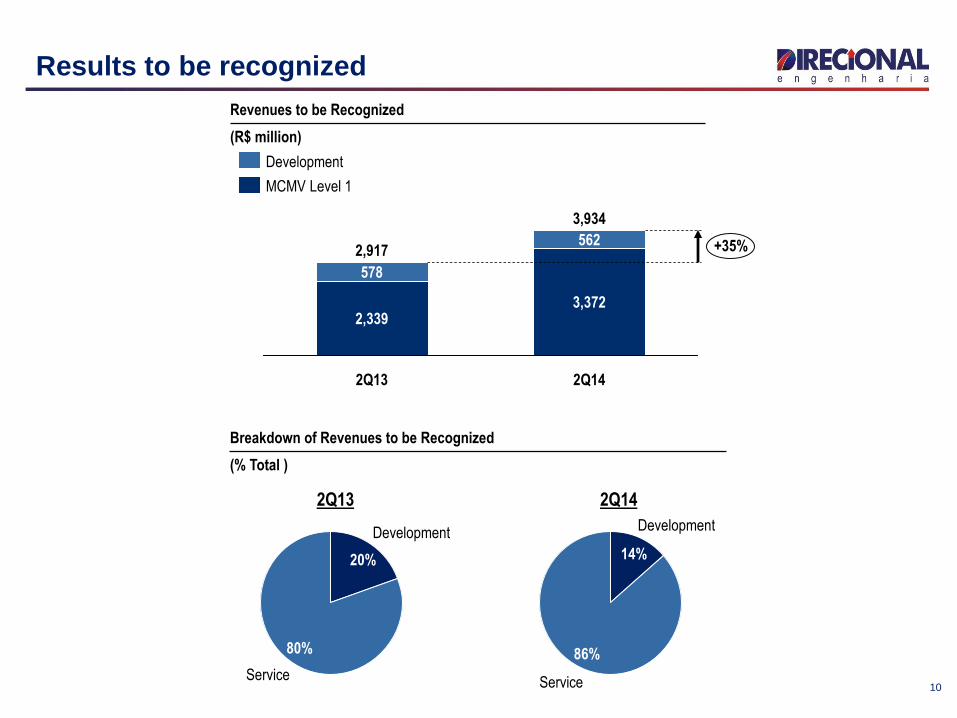

Results to be recognized

Service

86%

Development

14%

Service

80%

Development

20%

Breakdown of Revenues to be Recognized

(% Total )

2Q142Q13

3,934

+35%

2Q14

3,372

562

2Q13

2,917

2,339

578

MCMV Level 1

Development

Revenues to be Recognized

(R$ million)

11

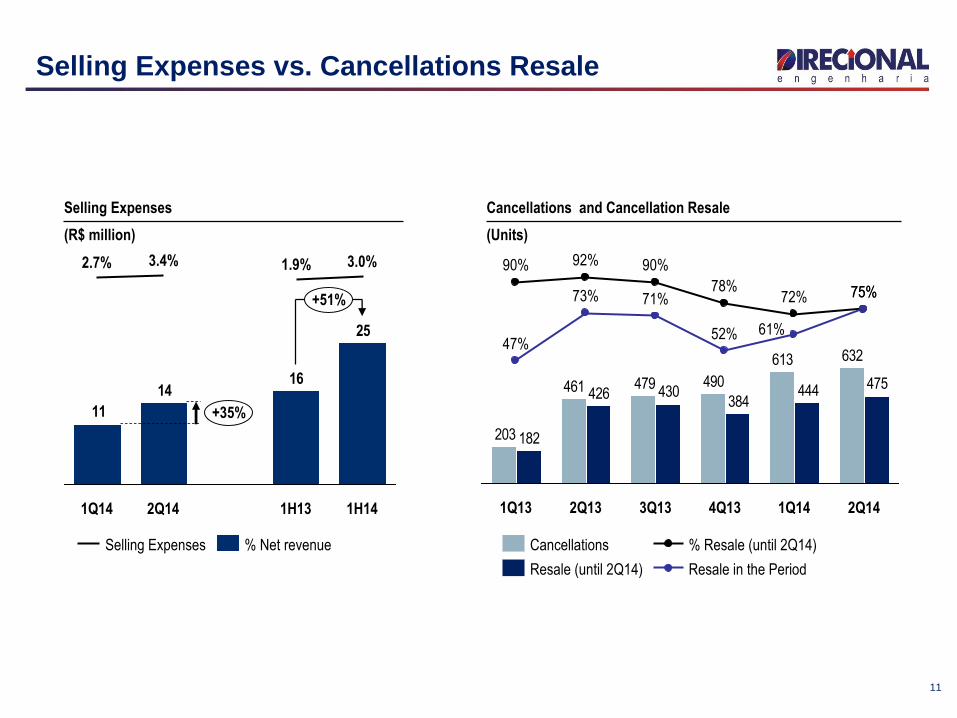

Selling Expenses vs. Cancellations Resale

Cancellations and Cancellation Resale

(Units)

632613

490479461

203

475444384

430426

182

47%

75%

52%

73% 71%

61%

72%

1Q14

75%

2Q14

90%

78%

3Q13 4Q132Q13

92%90%

1Q13

Resale (until 2Q14)

Cancellations % Resale (until 2Q14)

Resale in the Period

Selling Expenses

(R$ million)

25

1614

11

1H13 1H14

+51%

3.0%

+35%

1.9%2.7%

1Q14

3.4%

2Q14

Selling Expenses % Net revenue

12

1. Adjustment excluding interest expenses on construction financing

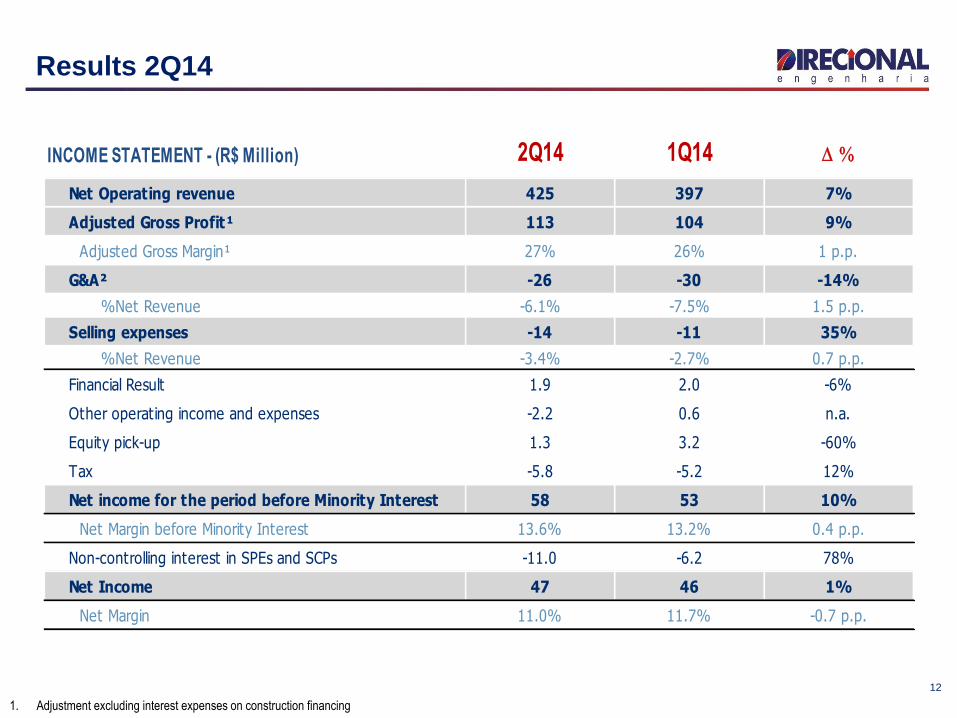

Results 2Q14

INCOME STATEMENT - (R$ Million) 2Q14 1Q14 D %

Net Operating revenue 425 397 7%

Adjusted Gross Profit¹ 113 104 9%

Adjusted Gross Margin¹ 27% 26% 1 p.p.

G&A² -26 -30 -14%

%Net Revenue -6.1% -7.5% 1.5 p.p.

Selling expenses -14 -11 35%

%Net Revenue -3.4% -2.7% 0.7 p.p.

Financial Result 1.9 2.0 -6%

Other operating income and expenses -2.2 0.6 n.a.

Equity pick-up 1.3 3.2 -60%

Tax -5.8 -5.2 12%

Net income for the period before Minority Interest 58 53 10%

Net Margin before Minority Interest 13.6% 13.2% 0.4 p.p.

Non-controlling interest in SPEs and SCPs -11.0 -6.2 78%

Net Income 47 46 1%

Net Margin 11.0% 11.7% -0.7 p.p.

13

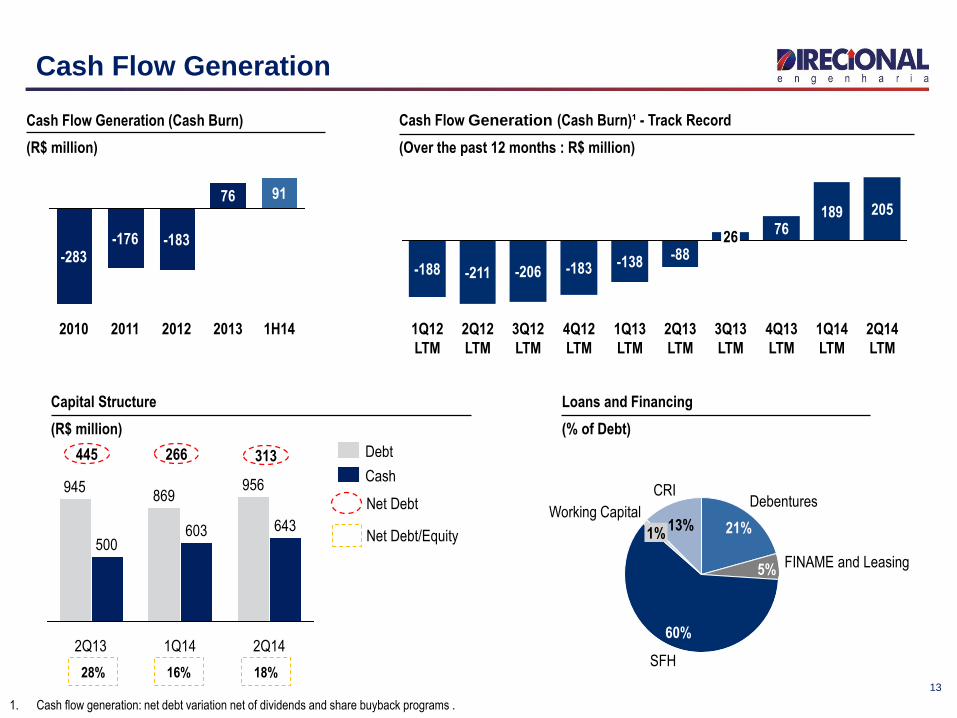

Cash Flow Generation

Cash Flow Generation (Cash Burn)

(R$ million)

Capital Structure

(R$ million)

445

Net Debt

28% 16% 18%

Net Debt/Equity

266 313

CRI

13%Working Capital

1%

SFH

60%

FINAME and Leasing5%

Debentures

21%

Loans and Financing

(% of Debt)

2013

76

2012

-183

2011

-176

2010

-283

1H14

91

2Q14

643

956

1Q14

603

869

2Q13

500

945Cash

Debt

2Q14

LTM

205

1Q14

LTM

189

4Q13

LTM

76

3Q13

LTM

26

2Q13

LTM

-88

1Q13

LTM

-138

4Q12

LTM

-183

3Q12

LTM

-206

2Q12

LTM

-211

1Q12

LTM

-188

Cash Flow Generation (Cash Burn)¹ - Track Record

(Over the past 12 months : R$ million)

1. Cash flow generation: net debt variation net of dividends and share buyback programs .

14

Disclosure and Contacts

This presentation contains certain forward-looking statements concerning the business prospects, projections of

operating and financial results and growth potential of the Company, which are based on management’s current

expectations and estimates of the future performance of the Company. Although the Company believes such

forward-looking statements are based on reasonable assumptions, it can give no assurance that its expectations

will be achieved. Expectations and estimates that are based on the future prospects of the Company are highly

dependent upon market behavior, Brazil’s political and economic situation, existing and future regulations of the

industry and international markets and, therefore, are subject to changes outside the Company’s and

management’s control. The Company undertakes no obligation to update any information contained herein or to

revise any forward-looking statement as a result of new information, future events or other information.

www.direcional.com.b/ir

(55 31) 3214-6200

(55 31) 3214-6450

Carlos Wollenweber

CFO | IR Officer

Paulo Sousa

IR Coordinator

Luiz Felipe Almeida

IR Analist