Embed Size (px)

Citation preview

The Affordable Care Act

Understanding it and enrolling in your new health care plan

RLee Insurance Solutions LLC

How does the ACA improve my health care?• Provides health insurance to those that were once considered ‘uninsurable’ with

pre-exiting health conditions.• Provides for certain protections and rights to make your coverage

fairer and easier to understand.• Provides for a health care Marketplace for an easier shopping experience.• Holds insurance companies accountable for rate increases.• Makes it illegal for health insurance companies to

arbitrarily cancel your health insurance.• Covers young adults under 26.• Provides free preventive care.• Ends lifetime and years dollar limits.• Guarantees your right to appeal

Questions? Call 1-800-318-2596, 24 hours a day, 7 days a week. (TTY: 1-855-889-4325)

What will my new policy cover?All private health insurance plans offered in the Marketplace will offer the same set of essential health benefits. These are services all plans must cover.The essential health benefits include at least the following items and services:• Ambulatory patient services (outpatient care you get without being admitted to a hospital)• Emergency services• Hospitalization (such as surgery)• Maternity and newborn care (care before and after your baby is born)• Mental health and substance use disorder services, including behavioral health treatment (this includes

counseling and psychotherapy)• Prescription drugs• Rehabilitative and habilitative services and devices (services and devices to help people with injuries,

disabilities, or chronic conditions gain or recover mental and physical skills)• Laboratory services• Preventive and wellness services and chronic disease management• Pediatric services

OK so how do I start ?First thing you need to figure out is are you applying “on exchange” or “off exchange”?• If your income is between 138% - 400% of the federal poverty level then you may

qualify for a federal subsidy, premium assistance tax credit. It was put into place to help reduce the cost of premiums, this subsidy may only be applied to “on exchange” plans. Since you can only use your subsidy with plans that are “on exchange” and you must enroll through the government web site Healthcare.gov.

• If your income is above 138% - 400% of the federal poverty level you may apply for either “on exchange” or “off exchange” plans. If you choose to enroll in a “on exchange” plan then you must go through the Healthcare.gov web site. Plans that are “off exchange” may be purchased though various web sites.

• Lastly if your income is below 138% of the poverty level you do not qualify for a subsidy and in many cases you can enroll for Medicaid through Healthcare.gov or your State web site. You may also choose to buy an “off exchange” plan since no subsidy is involved.

Just what is a subsidy?The ‘subsidy’ or Advance Premium Tax Credit (APTC) is actually an advance on next years tax return based on your ‘projected’ income for this year. You can choose to use this tax credit in any one of 3 different ways.

1. You can use the entire monthly credit to reduce your out of pocket expense for you monthly health premium.

2. You could use only a portion of your credit and pay more out of pocket for your health premiums each month, you would then get the remainder at the end of the year with a high tax return, this is a good option if you are unsure of the coming year’s income.

3. You could choose to not use your monthly tax credit at all and receive the entire amount at the end of the year on your tax return.

*Keep in mind if you misjudge your income for the year you could be a position where you would owe part of your APTC back to the government. Always report any change in income levels as soon as possible the Federally Facilitated Marketplace at 1-800-318-2596, they can adjust your monthly APTC to the appropriate amount for you.

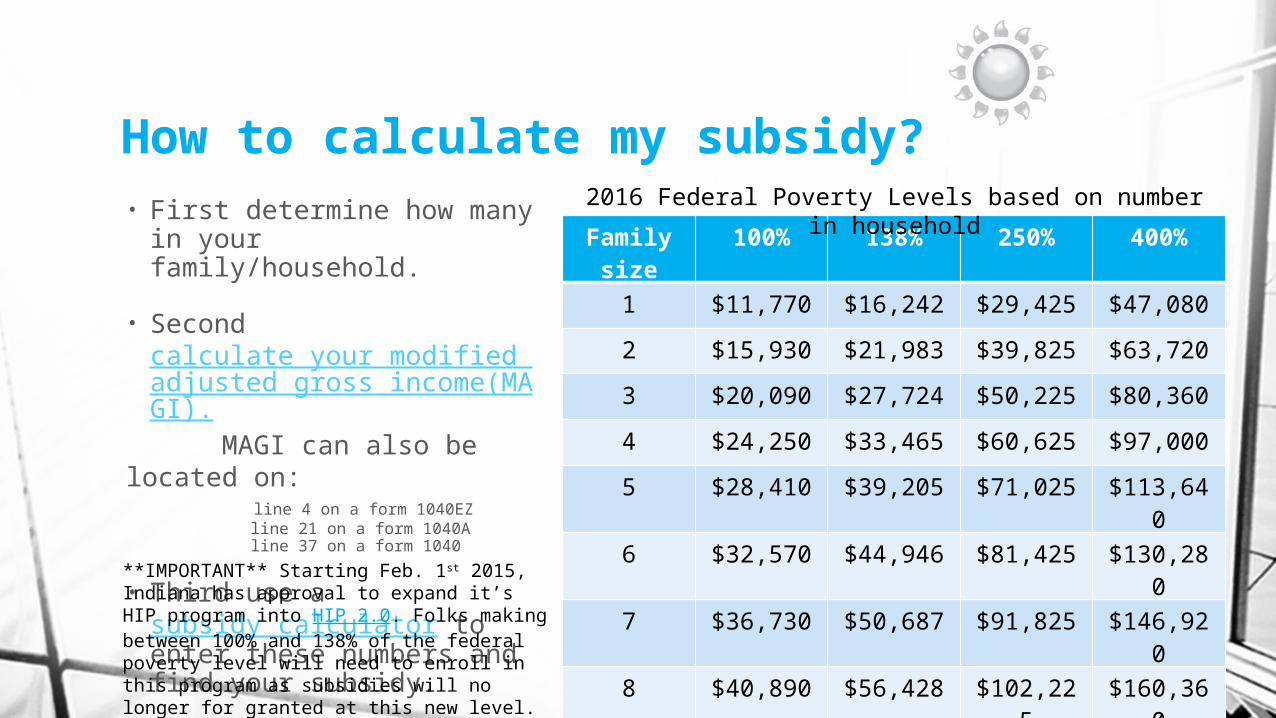

How to calculate my subsidy?• First determine how many in

your family/household.• Second

calculate your modified adjusted gross income(MAGI).

MAGI can also be located on: line 4 on a form 1040EZ line 21 on a form 1040A line 37 on a form 1040

• Third use a subsidy calculator to enter these numbers and find your subsidy.

**IMPORTANT** Starting Feb. 1st 2015, Indiana has approval to expand it’s HIP program into HIP 2.0. Folks making between 100% and 138% of the federal poverty level will need to enroll in this program as subsidies will no longer for granted at this new level.

Family size

100% 138% 250% 400%

1 $11,770 $16,242 $29,425 $47,0802 $15,930 $21,983 $39,825 $63,7203 $20,090 $27,724 $50,225 $80,3604 $24,250 $33,465 $60,625 $97,0005 $28,410 $39,205 $71,025 $113,64

06 $32,570 $44,946 $81,425 $130,28

07 $36,730 $50,687 $91,825 $146,92

08 $40,890 $56,428 $102,22

5$160,36

0

2016 Federal Poverty Levels based on number in household

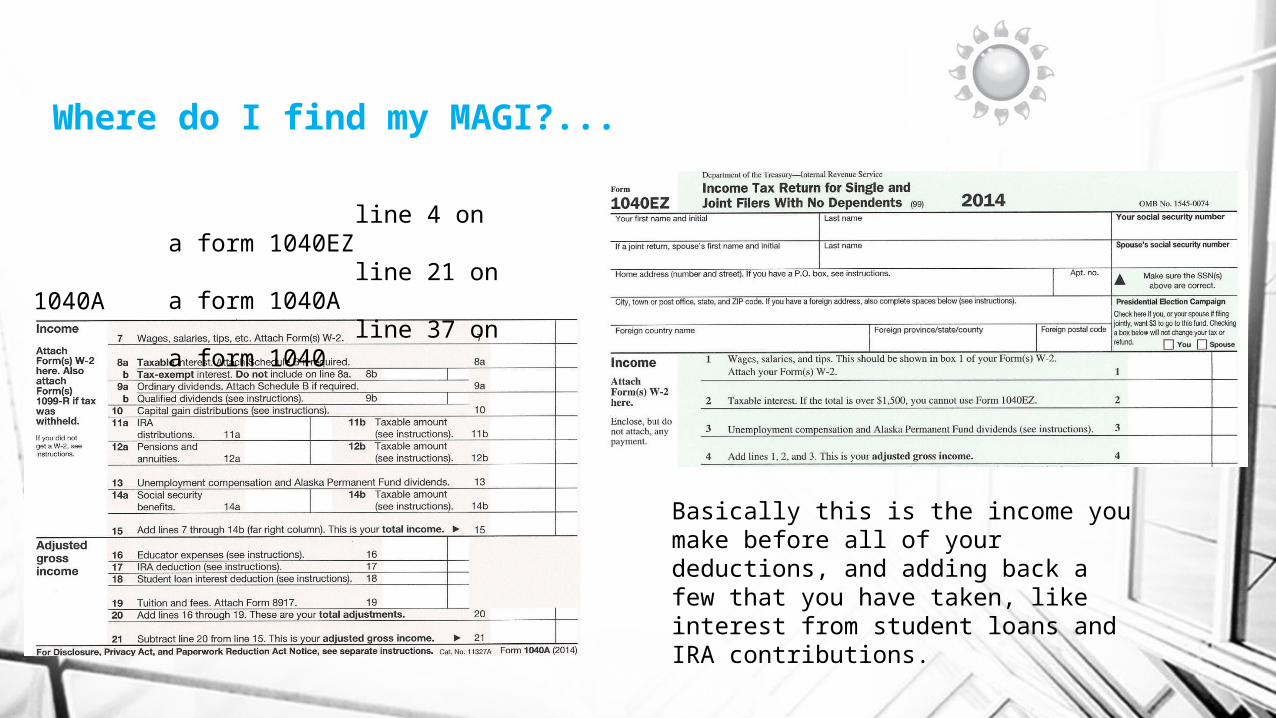

Where do I find my MAGI?...

1040A

Basically this is the income you make before all of your deductions, and adding back a few that you have taken, like interest from student loans and IRA contributions.

line 4 on a form 1040EZ line 21 on a form 1040A line 37 on a form 1040

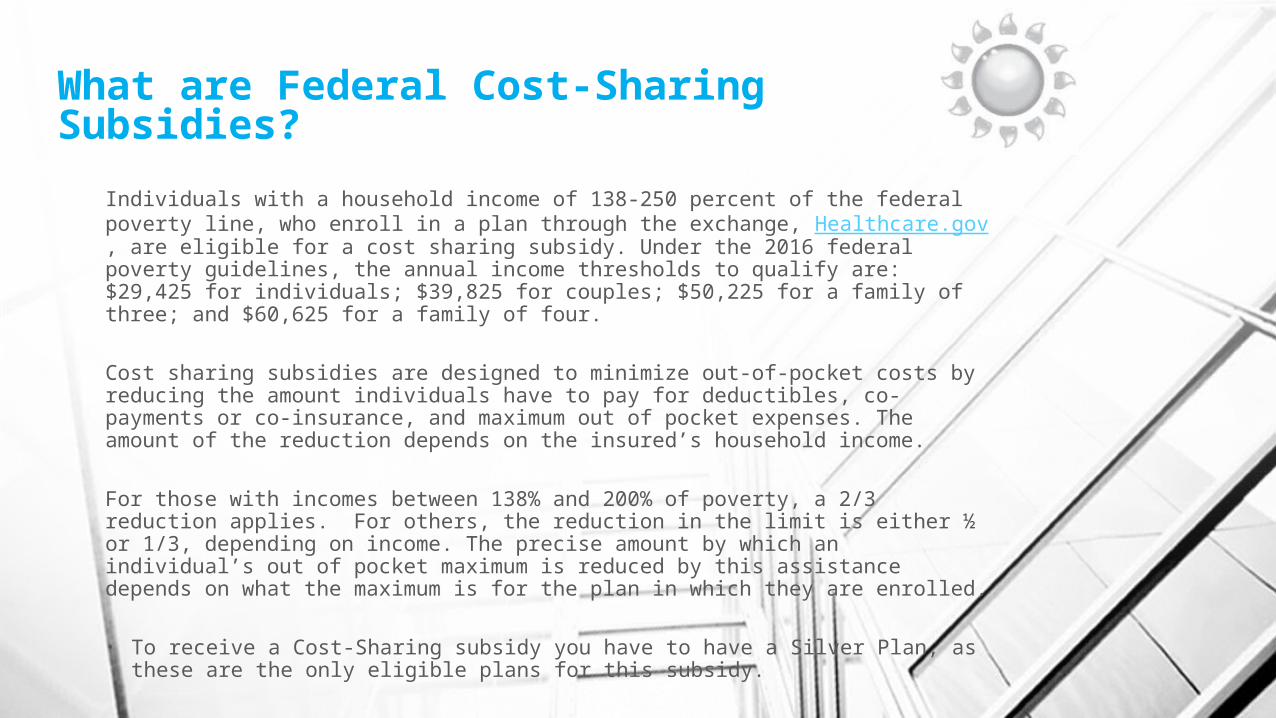

What are Federal Cost-Sharing Subsidies?

Individuals with a household income of 138-250 percent of the federal poverty line, who enroll in a plan through the exchange, Healthcare.gov, are eligible for a cost sharing subsidy. Under the 2016 federal poverty guidelines, the annual income thresholds to qualify are: $29,425 for individuals; $39,825 for couples; $50,225 for a family of three; and $60,625 for a family of four.

Cost sharing subsidies are designed to minimize out-of-pocket costs by reducing the amount individuals have to pay for deductibles, co-payments or co-insurance, and maximum out of pocket expenses. The amount of the reduction depends on the insured’s household income.

For those with incomes between 138% and 200% of poverty, a 2/3 reduction applies. For others, the reduction in the limit is either ½ or 1/3, depending on income. The precise amount by which an individual’s out of pocket maximum is reduced by this assistance depends on what the maximum is for the plan in which they are enrolled.

• To receive a Cost-Sharing subsidy you have to have a Silver Plan, as these are the only eligible plans for this subsidy.

But which plan?The new plans will be labeled with “metallic” names, bronze, silver, gold, and platinum. There is also one more plan labeled “catastrophic” but only certain folks may apply for them.

• Each plan will have a deductible, an amount you must pay before benefits are triggered.

• After you have satisfied the deductible you will have to pay a co-pay, or coinsurance, a set percentage of your bill.

• The good news each plan does have a maximum amount listed that you would have to pay. Should your health expenses exceed the maximum out of packet amount your plan will generally pay all remaining medical expenses.

The Plans…Catastrophic PlansA catastrophic plan generally requires you to pay all of your medical costs up to a certain amount, usually several thousand dollars. Costs for essential health benefits over that are generally paid by the insurance company.

These policies usually have lower premiums than a comprehensive plan, but cover you only if you need a lot of care. They basically protect you from worst-case scenarios.• Only people under 30 may apply for them.• You may apply for a hardship exemption if

over 30

*Not a subsidy eligible plan

Bronze PlansGenerally speaking, the Bronze Plan is intended to have the lowest premium of the 4 new categories of plans but charge the highest out-of-pocket costs for healthcare services. For people without group insurance from an employer or other group, the Bronze plan is the minimum health insurance plan in which they can enroll that will satisfy the Affordable Care Act’s mandate for people to purchase health insurance.• Plans often have high deductibles.• Co-pay is at the 60/40 level

The Plans…Silver PlansThe Silver Plans have lower out-of-pocket costs than the Bronze Plans but higher out- of-pocket costs than both the Gold and Platinum Plans. All Silver Plans share the same minimum health benefits but the way they charge out-of-pocket costs can differ significantly.• Subsidies in your state are based on

Silver plans in your state.• Co-pay is at the 70/30 level

Gold Plans

The Gold Plan is one of the two plan types that an insurance company must offer in order to participate in a health insurance exchange. A health insurance exchange is a state marketplace for health insurance plans meeting the ACA requirements.

One of the issues that the government intends to monitor is whether Gold and Platinum plans attract more sickly enrollees and drive up premiums.• These plans have the second lowest

out-of-pockets of the metallic plans. • Co-pay is at the 80/20 level

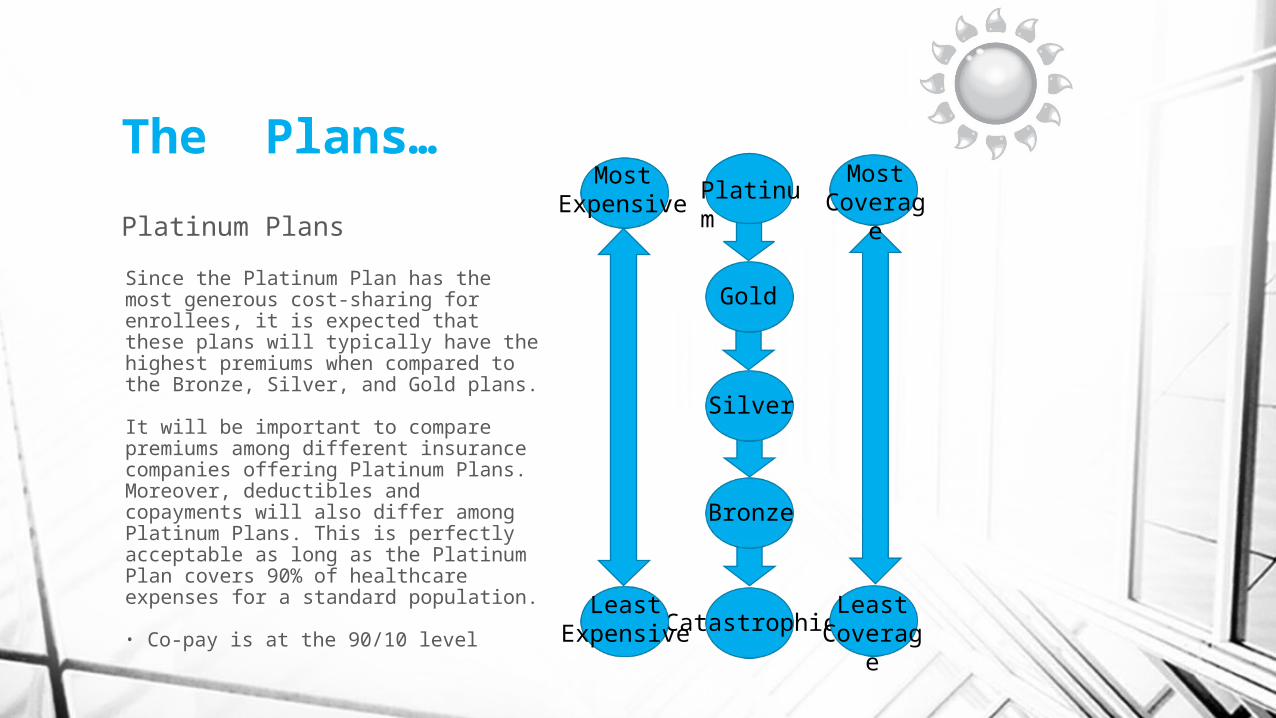

The Plans…Platinum PlansSince the Platinum Plan has the most generous cost-sharing for enrollees, it is expected that these plans will typically have the highest premiums when compared to the Bronze, Silver, and Gold plans.

It will be important to compare premiums among different insurance companies offering Platinum Plans. Moreover, deductibles and copayments will also differ among Platinum Plans. This is perfectly acceptable as long as the Platinum Plan covers 90% of healthcare expenses for a standard population. • Co-pay is at the 90/10 level

Platinum

Gold

Silver

Bronze

Catastrophic

MostExpensive

LeastExpensive

MostCoverag

e

LeastCoverag

e

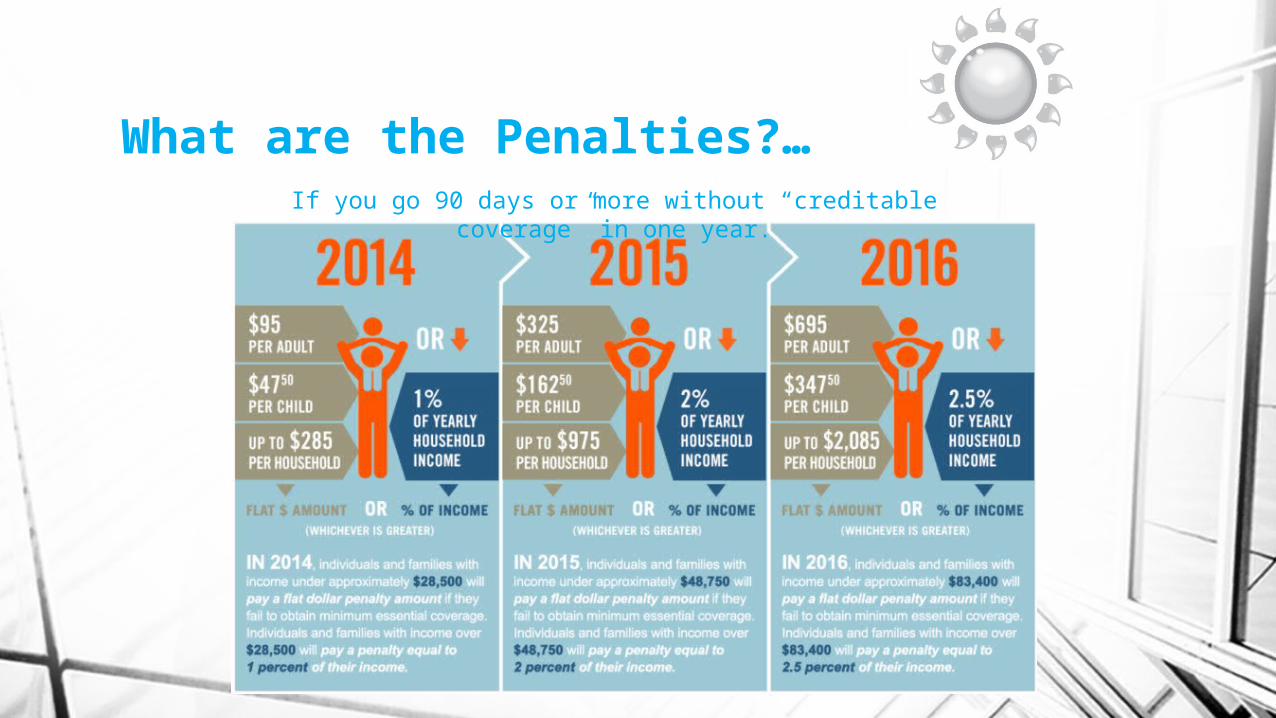

What are the Penalties?…If you go 90 days or more without “creditable coverage” in

one year.

RLee Insurance SolutionsLocated just off IN 26 in Lafayette Indiana, we are easy to find with ample parking and our facility is handicapped accessible. Click here for easy Directions

100 Executive Dr.Suite DLafayette, IN 47905

Phone: 765-746-6459Web: https://rleeinsurancesolutions.comEmail: [email protected]

Our office Location