Embed Size (px)

DESCRIPTION

Revenue Cycle Strategist “Revenue Lost And Found-Four Ways A Debt-Buying Partner Can Impact Your Bottom Line”

Citation preview

RevenueCycleStrategist

Insights and actions for successful results

www.hfma.org/rcs

Sponsored by

October 2010

In this challenging economic climate ofhigh unemployment and individualsincreasingly struggling to pay medical bills,more healthcare organizations are employ-ing a debt-selling strategy that recoverslong-lost revenue yet remains sensitive tothe financial strains of patients.

Selling all or a portion of these charged-offaccounts after a primary collections agencyhas done its best job can have an immedi-ate and significant impact on the bottomlines of healthcare organizations, generatefunding for stalled projects, and open upnew, predictable revenue streams.

“Having the option to recoup some of themonies that could potentially becomelosses improves our overall revenue cycle

management,” said Jim Moake, opera-tions CFO for IASIS Healthcare, a net-work of 15 acute care hospital facilitiesand one behavioral health hospital facil-ity with a total of 2,848 beds. “However,the most impressive part of our debt-buying service is that it is able to takeover these difficult accounts with mini-mal complaints from patients.”

The action of selling self-pay and self-pay-after-insurance receivables to adebt buyer, although not a new concept,is still a sideline consideration for manyhospitals, physicians’ groups, first-responders, and behavioral healthproviders. This is due in part to thereluctance of some healthcare financialmanagers to shift away from traditional

Selling debt can affect your healthcare organization’s bottomline in four key ways.

INSIDE THIS ISSUE

Coding Q&A 4

Taking Notice of Observation

Service Opportunities and Risks 5

2010 MAP Award Winner

Profile: Danbury Hospital 6

Strategies for Simplifying

Your Staff Training 7

Uninsured Young Adults with

Cost-Related Access or

Medical Bill Problems 8

WEB EXTRA!

Case Study: Maintain the Team in Times

of Change at www.hfma.org/rcs

NEW HFMA RESOURCE

FY11 IPPS Final Rule Fact Sheet,

www.hfma.org/Templates/InteriorMaster.

aspx?id=22769

Revenue Lost and Found: Debt Buying and Your Bottom LineBy Mikel J. Burroughs

collections methods. They remain relianton third-party agencies because they arelong-held partnerships and allow health-care organizations to maintain control ofpatient accounts. The traditional thinkinggoes: If I don’t sell the self-pay bad debtoutright, I can monitor the accounts andensure patients are not subjected tooverly aggressive collections tactics.

Such concerns are valid and not to bediscounted, but they don’t take intoaccount the protections and proceduresused by a reputable debt buyer. A truedebt-buying partner knows the impor-tance of treating patients in a profes-sional manner. In fact, the best debtbuyers readily provide references andtestimonials, adhere to Health InsurancePortability and Accountability Act(HIPAA) and Fair Debt CollectionPractices Act (FDCPA) guidelines, go topainstaking lengths to minimize patientcomplaints, and allow providers to recallqualifying accounts without penalty.

As the traditional debt-managementparadigm shifts toward newerapproaches, more healthcare financialmanagers are expected to use debt-sell-ing tools to shape the revenue cycle. Infact, the best debt buyers will augment ahealthcare organization’s collectionsprocesses and function as one memberof a three-way partnership—provider,collections agency, and debt purchaser—that maximizes the revenue cycle bykeeping everyone competitive. As anadded effect, some hospitals and groups,after incorporating a debt-selling strat-egy, see their liquidation rates improvebecause debtors see that even their olderaccounts will be pursued.

When weighing the debt-selling option,it’s helpful to consider four examples ofimpact on a healthcare organization’sbottom line.

Impact 1: One-Time Debt Sale to Test Waters

Many healthcare organizations are sittingon a growing pool of warehoused accountsreceivables (A/R)—debts that likely wentthrough an internal process, an early-outprogram, and one or more collectionsagencies within the first 120 days.

After 120 days, these accounts won’t getmuch more attention. The collectionsindustry is highly competitive and agen-cies typically are paid low rates—roughly14 to 23 cents on every dollar collected.At these rates, uncollected A/R are amuch less profitable prospect after fourmonths, and agencies are much less ableto put more resources into collecting the

debt. The result? At the 120-day mark,many agencies have only scraped the surface and recovered the easier balancesthrough calls and letters. The more diffi-cult balances remain uncollected.

By contrast, a debt buyer stands ready toimmediately pay a hospital or physiciangroup extra liquidation dollars to own thedebt. That’s because the debt buyer’score business is to analyze the value ofdebt, purchase the debt, and revive thedormant accounts through speciallytrained staff, a network of legal partners,and proprietary technology. Because adebt buyer owns the accounts, it canthrow more resources at them and workwith account holders to find solutions forrepayment and recovery of assets over alonger time horizon—as long as six years.

Moving earlier to sell debt is key forhealthcare organizations because“fresher” debt garners a higher pricefrom a debt buyer. The amount of liqui-dation dollars offered to own the accountportfolio, however, will differ dependingon how many third parties have tried tocollect the debt, as well as hospital orgroup demographics, how the businessperforms, location, type of facility, andnumber of beds.

Before the sale takes place, a debt-buyingpartner should provide a free evaluationto analyze a designated portfolio eitherbefore or after it is placed with a primaryor secondary agency. The focus is on pur-chasing accounts not currently beingworked, including archived, out-of-statute, and written-off debts. Withaccess to the basic information of a port-folio of self-pay accounts, a debt buyershould be able to make a bid in just a fewdays.

If the hospital agrees to sell, it can usu-ally be paid the full sum in just a matterof days. The hospital then has a new

2 October 2010 Revenue Cycle Strategist

Robert Fromberg Carole BolsterEditor-in-Chief Senior Editor

Amy D. LarsenProduction

Revenue Cycle Strategist is published 10 times a year bythe Healthcare Financial Management Association, TwoWestbrook Corporate Center, Suite 700, Westchester, IL60154

Presorted nonprofit postage paid in Chicago, IL 60607.©2010 Healthcare Financial Management Association.

Volume 7, Number 8

Subscriptions are $110 for HFMA members and $165 for other individuals and organizations. Subscribe online atwww.hfma.org/rcs or call 1-800-252-HFMA, ext 2.To order reprints, call 1-800-252-HFMA, ext. 387.

To submit an article, contact Carole Bolster at [email protected].

Revenue Cycle Strategist is indexed with Hospital andHealth Administration Index and the HealthSTAR database.

Material published in Revenue Cycle Strategist is providedsolely for the information and education of its readers.HFMA does not endorse the published material or warrantor guarantee its accuracy. The statements and opinions inRevenue Cycle Strategist articles and columns are thoseof the authors and not those of HFMA. References to commercial manufacturers, vendors, products, or servicesthat may appear in such articles or columns do not constitute endorsements by HFMA.

ISSN 1549-0858

Many hospitals are sitting on a growing pool of warehoused accounts receivables. After 120 days,these accounts won’t getmuch more attention.

www.hfma.org/rcs October 2010 3

source of revenue for both immediateand long-term needs.

Impact 2: Shortening the Placement Cycle

When it comes to selling debt, a one-offbusiness transaction is often how ahealthcare organization tests the watersbefore diving into a more regular part-nership. More healthcare organizations,however, are finding that partnering witha debt buyer to shorten the debt place-ment cycle can dramatically increasetheir self-pay account revenue. How?Instead of waiting for the primary agencyto work the debt for a year, a healthcareorganization can shorten the revenuecycle by selling the debt after four to sixmonths. In doing so, it will be able to geta higher price for the accounts from thedebt buyer. Otherwise, most bad debtswill sit for five or six months past the120-day mark. As they collect more dust,their value goes down.

Ideally, a healthcare organization entersinto a “forward-flow” agreement with adebt buyer. These agreements arebecoming much more common and allowthe provider group or hospital to sell itsdelinquent receivables on an ongoingbasis, often as they reach the one-to six-month threshold post “early out.”

This process creates a more predictablecash flow and alleviates the buildup ofbad debt going forward. It also reducesadministrative work, and therefore,valuable hours for providers.

Impact 3: Testing ROI of TraditionalCollections Versus Debt Selling

Some CFOs and other healthcare financialmanagers further define their debt-sellingstrategies by using a champion-challengertest to determine whether traditional col-lections or debt selling has the greatestimpact on processes and cash flow.

To do so, a healthcare organization wouldplace equal amounts of debt with its pri-mary collections agency and its debt buyerfor a set period of time—say 12 months. Itwould then compare the advantages andreturn each partner delivers over time andhow each approach affects internalprocesses and staff.

For example, the hospital pays the col-lections agency contingency fees over a12-month period, with fees varyingdepending on the hospital’s location anddemographics. The net liquidation, grossrecovery, and net dollars also are spreadover 12 months. In addition, after severalmonths, the debt may need to be placedwith a secondary agency for a higherservice fee or returned as uncollectible.

By contrast, a debt purchaser is paidnothing by the hospital. It essentiallybuys the placement on day one, and the

Checklist: How to Select a Debt Buyer

In addition to thorough analysis of how your organization might benefitfrom a debt-selling strategy, it’s important to give the selection of anydebt-buying partner careful consideration by following this checklist. Verify the debt buyer’s experience. Ask detailed questions to understand

the company’s history and level of industry experience.

Confirm that the debt buyer also services accounts. Some debt buyersonly purchase the debt and use independent collection agencies toservice it. A suggested practice is to opt for a company that will bothbuy and service the paper.

Determine the best time to introduce the debt buyer into your revenuecycle. Many facilities engage debt buyers when their accounts havereached “charged-off” status, having gone through an internal collec-tions process, an early-out process, and typically through one or morecollections agencies.

Determine the value and details of your debt. How many accounts do youhave? How old are they? Which ones should you sell to a debt buyerversus those to be collected by an agency?

Be willing to open your books and to provide comprehensive information.The more information you are able to provide to debt buyers, the more completely they can evaluate your portfolio to provide the best pricingstructure.

Ensure that your debt buyer adheres to mandates and regulations forpatient privacy. HIPAA and FDCPA, for example, are federal

regulations to protect the privacy and rights of patients. It is imperativethat your debt buyer adheres to these regulations to ensure patients’rights are preserved. Have the debt buyer sign a business associateagreement before sharing files with the firm.

Investigate secure communications options provided by your debt buyer.Options such as secure, read-only access to your billing system ensureadded protection for you and your patients and save time for your staff. Additionally, investigate the debt buyer’s systems and securityprocedures.

Evaluate how much cash flow you require, and in what time frame. The collection process for a self-pay account can take days, months, evenyears. Working with a debt buyer can significantly accelerate cash flow and help you meet your needs sooner rather than later.

Determine whether you can repurchase accounts. Positive patient rela-tionships are key to your business. For your peace of mind, ask a potential debt buyer whether you can repurchase accounts at any time and for any reason, whether there is a cap on quantity, whetherthere is a price mark- up, and whether you can exchange for other valid accounts as opposed to paying for them in cash.

Ensure that the debt buyer operates nationwide or in the regions yourequire. In addition to national regulations, many states have specificlaws regulating debt collection. Make sure your debt buyer under-stands and operates within these parameters.

hospital receives cash right away. With anadditional revenue-sharing program, thehospital may receive additional dollarsover the life of the purchased portfolio ifthe debt buyer hits certain targets in aspecified period of time.

In addition to those considerations, thehospital should weigh the impact overthe 12-month sample period of workingwith the collections agency on remit-tance detail and day-to-day operations,versus the impact of monthly self-paymoney from the debt purchaser thatrequires minimal day-to-day operations.

For many managers, the test comes downto the value of money trickling in overseveral years versus the value of moneytoday. Often, the winner is money inhand today. The debt buyer is essentially

putting more cash quicker into the hos-pital’s pocket. This makes an immediateimpact on the revenue stream and allowsthe facility to fund ongoing operations orinvest in improvements.

Impact 4: Debt Buyer as

Revenue-Sharing Partner

Sometimes, a revenue-sharing relation-ship between a healthcare organizationand a debt buyer is possible on the backend of a successful asset recovery process.Such an agreement becomes an optionwhen a debt buyer purchases debt for theright price, can successfully revive thedormant accounts, and after severalyears, can reciprocate the hospital orgroup by paying out additional revenues.Such revenue-sharing agreements are notpart of a set program but are individuallydetermined at the time the debt is priced.

Even so, the revenue-sharing agreementis a strong example of how a debt-sellingpartnership can provide benefits on several different levels. It also shows how

a debt buyer’s aim, ultimately, is to be atrue partner along with the primary collections agency in the successful management of a hospital’s or grouppractice’s revenue cycle.

One thing is certain: With falling collec-tions rates and rising medical debt, eco-nomic pressures are mounting for revenuecycle managers. In response, hospitalCFOs, directors of patient accounts, busi-ness managers, and other healthcarefinancial managers alike are exploring allavailable tools to optimize the revenuestreams and support the core mission ofdelivering high-quality patient care.

In that regard, debt selling is a powerfuloption for maintaining revenue-cyclestability and funding a healthcare orga-nization’s progress, even in these shakyeconomic times.

Mikel J. Burroughs is president, SquareTwo Financial

Healthcare Funding, Denver

4 October 2010 Revenue Cycle Strategist

Q: We recently had a claim rejected for apatient who returned to surgery to addressan infection two weeks after gall-bladdersurgery on the grounds that the secondoperation was within the 90-day globalperiod for the initial surgery. In what casesmay a second surgery within the 90-dayperiod be billed, and how should it becoded?

A: There are three circumstances under which asecond surgery within the global period may bebilled. Each should be reported with a specific

modifier to ensure that the procedure is notincluded in an ongoing global period.

Treatment of postoperative complicationsrequiring an unplanned return to the operatingroom is one, and it may apply in your case. Such aprocedure should be billed with modifier 78 toindicate it is unplanned but related to the initialsurgery.

In cases where a more extensive procedure isundertaken because an initial less extensive procedure was not successful, the second

surgery may be billed. It should be reported withmodifier 58 to indicate it is a staged or relatedprocedure.

A surgery unrelated to the initial surgery mayalso be billed within the global period of the firstsurgery. Modifier 79 should be reported with thesecond surgery to indicate that it is unrelated tothe first procedure.

Jennifer Swindle, RHIT, CCS-P, CPC, CPMA, is

director, coding and compliance, Pivot Health LLC,

Nashville, Tenn. ([email protected]).

Coding Q&A

Send your coding questions to Carole Bolster at [email protected].

By Jennifer Swindle

Debt selling is a powerfuloption for maintaining revenue-cycle stability.

www.hfma.org/rcs October 2010 5

The issues surrounding the development of astrong program include:> Ever-changing Medicare and fiscal intermedi-

ary guidance > Differing requirements among various payers> Case management staffing and training> Lack of structured physician advisory and

review processes

All of these issues make the admission decisionchallenging. Frequently, the billing for observa-tion services has been difficult because of weakdocumentation, including unclear admissionorders, a lack of negotiated observation rates formanaged care payers, and insufficient systeminfrastructure for ensuring that all Medicarerequirements are met.

The starting point for compliant patient billing isthe physician’s decision to admit the patient toobservation level of care. Case management’srole in this process is to ensure that the patient’smedical necessity supports this level of care andthat all documentation is complete. This typicallymeans using standard industry guidelines as ascreening tool. Often, the case managementevaluation of the patient, the industry guidelines,and the physician’s order may not agree. Wheresuch disagreements occur, the physician adviserand the utilization committee should be involvedto resolve the issue while the patient is in house.

As hospitals have implemented observation pro-grams, external pressures to increase the num-ber of patients placed into observation haveincreased significantly. Both governmental andother payers have implemented recovery pro-grams based on medical necessity, primarilyfocusing on short-stay inpatient cases that mayhave been appropriately handled as observation

stays. At many hospitals, these pressures haveresulted in an overcorrection and an overutiliza-tion of observation services.

Some of the related pitfalls regarding theincreased utilization of observation servicesinclude the artificial increase in the hospital’scase mix indexes (CMI) and increased length ofstay on inpatient cases. The CMI issues may fur-ther exacerbate the government’s notion that thehospitals are increasing coding, when in fact the CMI increase is simply a result ofremoving the low DRG weight cases from thecalculations. Given Medicare’s recent reductionin the payment levels related to what was histori-cally called DRG creep, this issue may have a sig-nificant impact on the hospitals’ future paymentsas well. Additionally, hospitals need to be con-cerned about the financial and public relationsimpact on the patient of billing what appears to bean inpatient service as outpatient. Finally, evi-dence supports that the readmission rate forobservation care is relatively high, raising thequestion of the impact of observation programson clinical quality.

To ensure compliant billing and avoid the obser-vation volume creep being experienced at manyhospitals, the best practices include following dis-tinct physician-driven pathways. The factors to beconsidered in physician level of care assignmentper the Centers for Medicare & MedicaidServices regulations are individualized, notdriven solely by time of encounter or diagnosiscategory.

Observation services also can offer a significant opportunity to hospitals that have yetto implement programs and begin billing for theservice appropriately. Observation revenue

typically exceeds $1,000 per case comparedwith outpatient billing without observation. Manymanaged care contracts call for observation perdiems comparable to inpatient per diems. If theinpatient care is going to be denied due to lack ofmedical necessity, hospitals should have a com-prehensive plan in place to capture the optimumobservation revenue.

As with most things, the key to implementing aneffective observation service is developing acomprehensive process that is driven by physi-cian decision making related to level of careassignment.

Joanne Vaul is executive director, CBIZ KA Consulting

Services, LLC, East Windsor, N.J., and a member of

HFMA’s New Jersey Chapter ([email protected]).

Elizabeth Gallagher is a director, CBIZ KA Consulting

Services, LLC, East Windsor, N.J., and a member of

HFMA’s New Jersey Chapter ([email protected]).

Revenue Assurance By Joanne Vaul and Elizabeth Gallagher

Recent pressures from the Medicare Recovery Audit Contractorsand various third-party payers have increased the sense ofurgency that hospital leaders feel about getting observation programs established.

Don’t Miss HFMA’s MAP Event MAP Event is your opportunity to learnstrategies that improve revenue cycle performance on specific indicators. Duringthis peer-to-peer program, winners of theMAP Award—hospitals that have demon-strated outstanding revenue cycle results—will share proven practices to push yourrevenue cycle to peak performance.Applications for the 2011 MAP Award will be available at MAP Event.

November 7-9, 2010Coronado Island Marriott Resort and SpaSan Diego, Calif.

Learn more and register now atwww.hfma.org/mapevent.

Taking Notice of Observation ServiceOpportunities and Risks

6 October 2010 Revenue Cycle Strategist

Back in 2002, staff on the billing and collectionsside of the revenue cycle at Danbury Hospitalwere spending way too much time cleaning upclaims.

“Bills were being returned because a memberwas not on file—one of the easiest problems toeliminate. There were denials because a diagno-sis wasn’t appropriate for the services provided. We were getting denials from Medicare becausewe didn’t have advance beneficiary notices.There was a tremendous amount of rework onthe back end,” recalls Mary Brannigan-Lowe,director of patient access and financial servicesfor the 371-bed teaching hospital located insouthwest Connecticut.

Brannigan-Lowe and others at the hospital at thattime had been reading about the advantages oftransferring back-end revenue cycle processesto the patient access area. But she, her CFO, theCOO, and the hospital president wanted tomove beyond admitting and preregistration andtake the revenue cycle directly into the clinicaldepartments. “That’s where the revenue cyclereally starts. If you can get the information youneed for a clean claim from the clinical depart-ment the first time out, you get paid the first timeout. So we were looking for greater accountabil-ity from our clinical departments in coding, regis-tration, verification, and eligibility,” she says.

Making the Case for CentralizationShifting accountability to the clinical depart-ments meant centralizing revenue cycle

functions in the patient financial services depart-ment. Clinical departments were reluctant at firstbecause they didn’t want to lose any staff. “Thedepartments would say, ‘They are my staff. Theyare multiskilled. They also file and answer thephone and do other things,’” she says.

Brannigan-Lowe started making the case for cen-tralization by conducting a full-scale prebillreview. She asked three FTEs to analyze everysingle bill, not just to find claims issues, but also tolook for insurance verification and eligibilityinformation. She then tracked and publicizederrors by department to show who was doing agood job and who wasn’t. “Once the clinicaldepartments realized they weren’t doing verywell and they didn’t really want to devote moreresources to deal with patient registration, verifi-cation, and eligibility, they said, ‘We’ll give youthe staff. You can consolidate ours with yours,’”she says.

Brannigan-Lowe added punctuation to the argu-ment for centralization by charging denials backto the clinical departments. “Anything that says‘denied’ is sent back to the clinical department,and the department has so many days to respondto tell us whether we should appeal the denial orwhether a diagnosis or a code needs to be cor-rected. Charging denials back to the departmentmakes a big difference because the denials hurtthe department’s financial performance,” shesays.

Fostering CollaborationStaff and administration at Danbury Hospitalhave worked hard to foster strong and collabora-tive relationships between the patient financialservices department and the clinical depart-ments. It’s all about communication and team-work,” says Brannigan-Lowe. “The clinicaldepartments are not afraid to call us if they have aquestion. I don’t hesitate to call the COO or oneof the vice presidents of operations if I have a

problem with a department. Within minutes, weare all in a room together sharing issues and con-cerns and brainstorming better processes.”

The hospital’s business operations unit, in particu-lar, helps keep channels of communication open.Unit staff routinely advise clinical departments,particularly the high-cost, high-volume areassuch as radiology and cardiology, on chargingand coding. “We also have an extremely strongcoding staff who work along with patient financialservices and the clinical departments to makesure we are not going to be dealing with a prob-lem after the fact. They also notify us of any pat-terns of problems,” she says.

Since Danbury Hospital started measuring keyperformance indicators in 2005, it has seen itsA/R greater than 90 days drop from a high of 31percent to 11 to 12 percent today. Its credit bal-ance, which was well over $1 million, now aver-ages $250,000. The return-to-provider errorrate from Medicare is less than 1 percent.

None of this would have been possible withoutsupport from executive leadership. “You can’tmake the changes we’ve made and get theresults we get today without a commitment fromthe top. Our president, COO, and CFO havebeen committed to improving our revenue cycleprocess by making our clinical departmentsaccountable and by incorporating the revenuecycle in all performance evaluations. Everyonefrom the top of the administration down to thestaff knows this is important,” Brannigan-Lowesays.

2010 MAP Award Winner Profile

Danbury Hospital

This month, 2010 MAP Award-winning Danbury Hospitaldescribes the impact of its emphasis on clean claims.

HFMA’s MAP Award is sponsored by:

www.hfma.org/mapaward

Charging denials back to thedepartment makes a big difference because the denialshurt the department’s financial performance.

Have you ever wondered how to takesome of the stress out of your day-to-dayoperations or help your patient financialservices staff work more efficiently?These tips for simplifying your stafftraining can help you reach those goals.

Prepare a Binder of Tasks and Policies

Each work station should have a binderthat lists the tasks each staff member per-forms and includes relevant policies. Thebinders help to simplify and organizetraining for new employees. The bindersshould be reviewed yearly to ensure thatthe processes are still valid and in place.

The value of using policy and proceduremanuals for staff training cannot beoverstated. Policies can be as simple ashow to check in a patient, or moredetailed, such as how to use an advancebeneficiary notice (ABN) manual.Policies are needed not only to provideoperating parameters for staff, but also tohelp you accomplish necessary taskswhen staff members are unavailable.

To prepare the binders, work with staffmembers individually to see how theyaccomplish tasks and to determine ways tostreamline the process. Write down eachtask that staff members perform, and out-line how the task is to be accomplished.

The sample policy at www.hfma.org/rcsspells out who is responsible for a taskand how the task is to be accomplished.

Policies help staff members “own” theirtasks and give them a means to accom-plish those tasks. They are greatresources to ensure consistent training.

Training

Next, host training sessions with staff,get their input regarding how to improveprocesses, and cross-train staff on howeach task is done. Training sessions helpstaff members understand what theircoworkers need to accomplish and howthey can help.

Communication is the key to success.Training staff is time-consuming, buttaking a systematic approach simplifiesthe process.

More comprehensive training isrequired for large transitions, such aselectronic medical record or ICD-10implementation. For major training, youneed to assess work flow and determinethe best methods of training. Someemployees may require more individualattention. Some might need training tobring their computer skills up to speed.And those transitioning into ICD-10coding who have limited knowledge ofanatomy or medical terminology mayneed refresher courses before receivingother training.

Another important point is that peoplehave different learning styles. Peopledepend on their senses to process infor-mation, and they tend to use one of theirsenses more than the others. The threemost common learning styles are visual,auditory, and kinesthetic.

Visual learners prefer to see how to dothings rather than talk about them. Mostpeople are visual learners.

Auditory learners can often follow direc-tions precisely after being told only once

or twice what to do. Some auditory learn-ers concentrate better when they havemusic or white noise in the background,or retain new information better whenthey talk it out.

Kinesthetic learners typically learn bestby doing. They are naturally good atphysical activities, such as sports anddance. They enjoy learning throughhands-on methods. They typically likehow-to guides and action-adventure sto-ries. They might pace while on the phoneor take breaks from studying to get upand move around. Some kinestheticlearners seem fidgety, having a hard timesitting still.

Training Will Enhance Office Operations

It’s important to provide your staff withconsistent, comprehensive training. Asyou train them, consider their individualneeds and learning styles. With propertraining, your office will operate moresmoothly and efficiently.

Rhonda Buckholtz, CPC, CPMA, CPC-I, CGSC,

COBGC, CPEDC, CENTC, is vice president of busi-

ness and member development, American Academy of

Professional Coders, Salt Lake City.

www.hfma.org/rcs October 2010 7

Leadership Tips By Rhonda Buckholtz

Strategies for Simplifying Your Staff Training

Binders containing tasks and policies and training sessions forstaff can improve patient financial services office operations.

Don’t Miss the Virtual Event of the Year!

HFMA’s Virtual Healthcare Finance

Conference is set for Dec. 1 and 2. Access

your choice of eight CPE-eligible live educa-

tion programs and 10 on-demand sessions

from industry leaders from the comfort of your

office. Free to HFMA members; nonmember

fee includes a special membership offer.

For more information and to register, visit

www.hfma.org/virtualconference.

WEB EXTRA!

See a sample policy for small balancewrite-offs at www.hfma.org/rcs.

Two Westbrook Corporate CenterSuite 700Westchester, IL 60154

PRESORTED NONPROFITU.S. POSTAGEPAIDPERMIT NO. 2862CHICAGO, IL

Sponsored by

To subscribe, call 1-800-252-HFMA,ext. 2. Or visit www.hfma.org/rcs

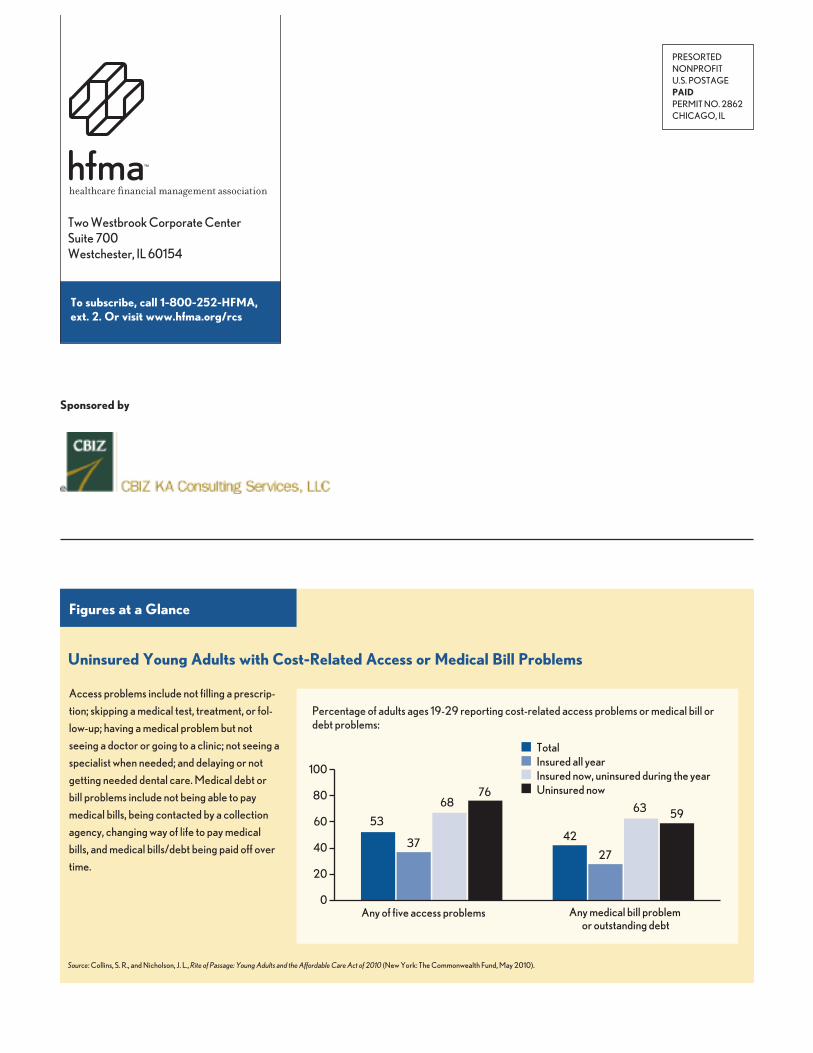

Figures at a Glance

Uninsured Young Adults with Cost-Related Access or Medical Bill Problems

Access problems include not filling a prescrip-tion; skipping a medical test, treatment, or fol-low-up; having a medical problem but notseeing a doctor or going to a clinic; not seeing aspecialist when needed; and delaying or notgetting needed dental care. Medical debt orbill problems include not being able to paymedical bills, being contacted by a collectionagency, changing way of life to pay medicalbills, and medical bills/debt being paid off overtime.

TotalInsured all yearInsured now, uninsured during the yearUninsured now

100

80

60

40

20

0Any medical bill problem

or outstanding debtAny of five access problems

53

37

6876

42

27

63 59

Source: Collins, S. R., and Nicholson, J. L., Rite of Passage: Young Adults and the Affordable Care Act of 2010 (New York: The Commonwealth Fund, May 2010).

Percentage of adults ages 19-29 reporting cost-related access problems or medical bill ordebt problems: