Embed Size (px)

Citation preview

Planned Hospital IT Investment: Budgets, Plans and Purchases in a stratified marketplace

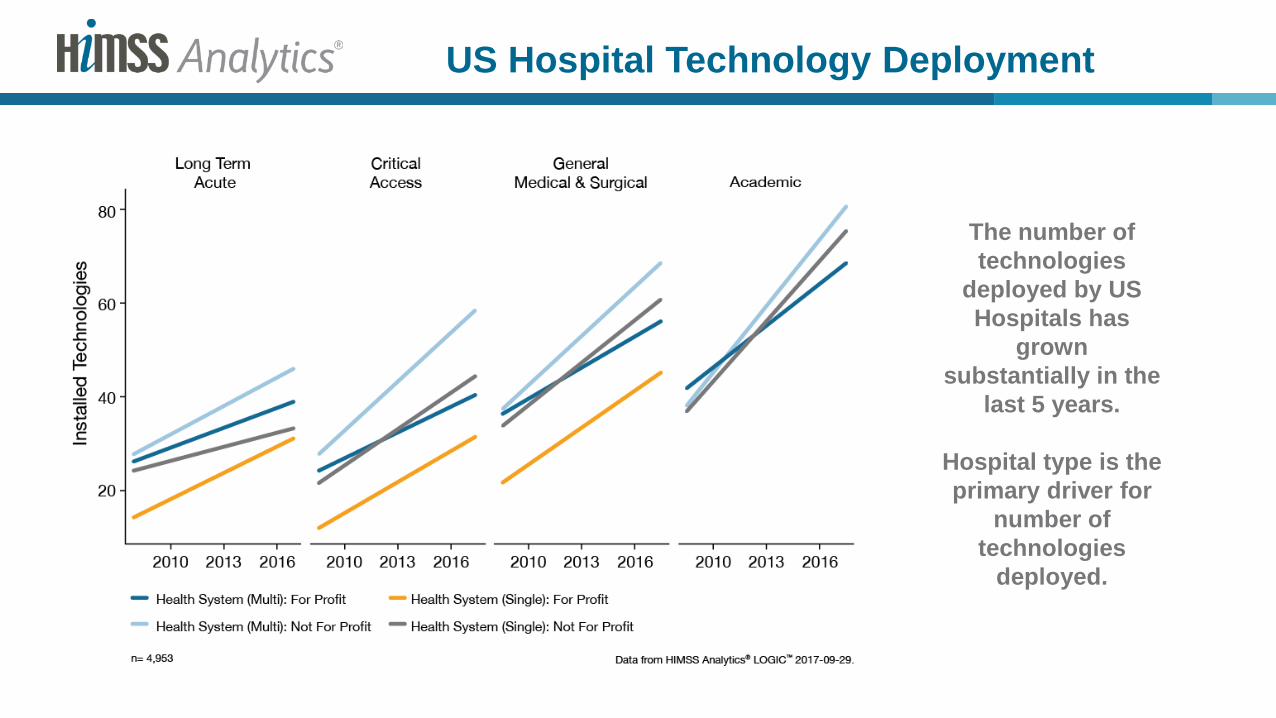

US Hospital Technology Deployment

The number of technologies

deployed by US Hospitals has

grown substantially in the

last 5 years.

Hospital type is the primary driver for

number of technologies

deployed.

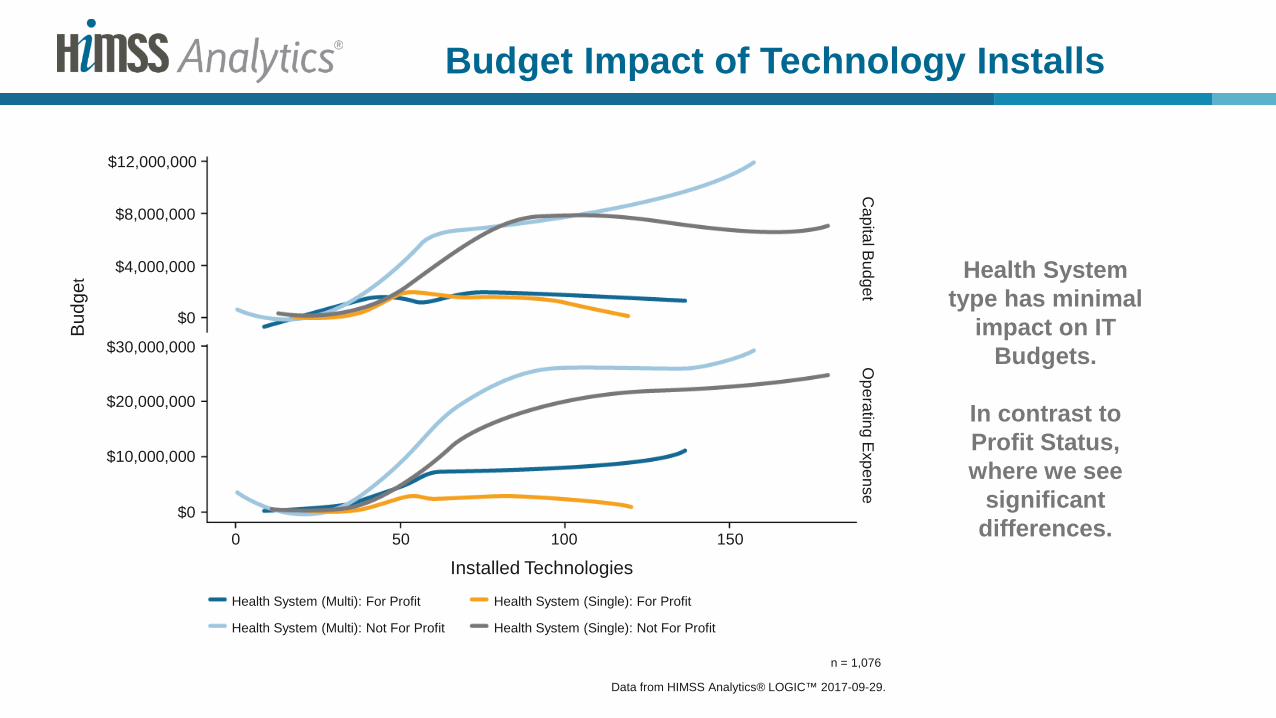

Budget Impact of Technology Installs

Health System type has minimal

impact on IT Budgets.

In contrast to Profit Status, where we see

significant differences.

$12,000,000

$8,000,000

$4,000,000

$30,000,000

$20,000,000

$10,000,000

$0

Bud

get

0

$0

Capital B

udgetO

perating Expense

Installed Technologies50 100 150

Health System (Multi): For Profit

Health System (Multi): Not For Profit

Health System (Single): For Profit

Health System (Single): Not For Profit

Data from HIMSS Analytics® LOGIC™ 2017-09-29.

n = 1,076

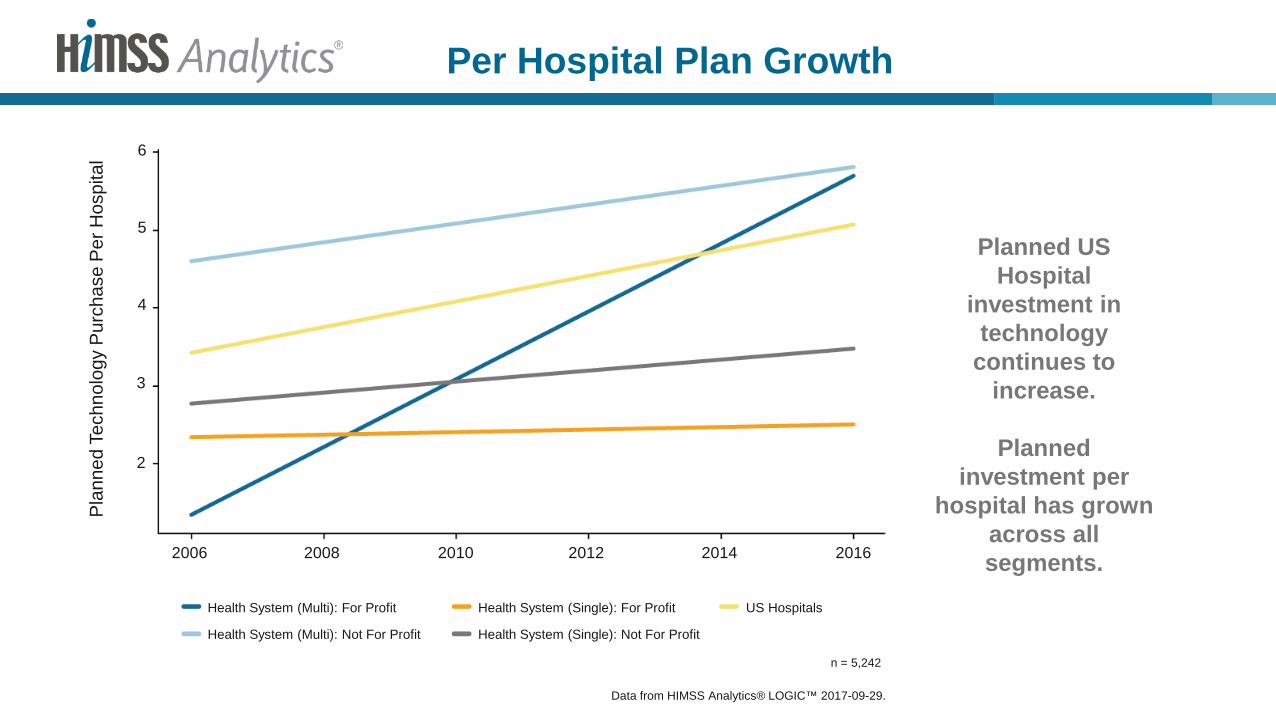

Per Hospital Plan Growth

Planned US Hospital

investment in technology

continues to increase.

Planned investment per

hospital has grown across all segments.

4

3

2

Pla

nned

Tec

hnol

ogy

Pur

chas

e P

er H

ospi

tal

2006

Health System (Multi): For Profit

Health System (Multi): Not For Profit

Health System (Single): For Profit

Health System (Single): Not For Profit

5

6

US Hospitals

Data from HIMSS Analytics® LOGIC™ 2017-09-29.

n = 5,242

2008 2010 2012 2014 2016

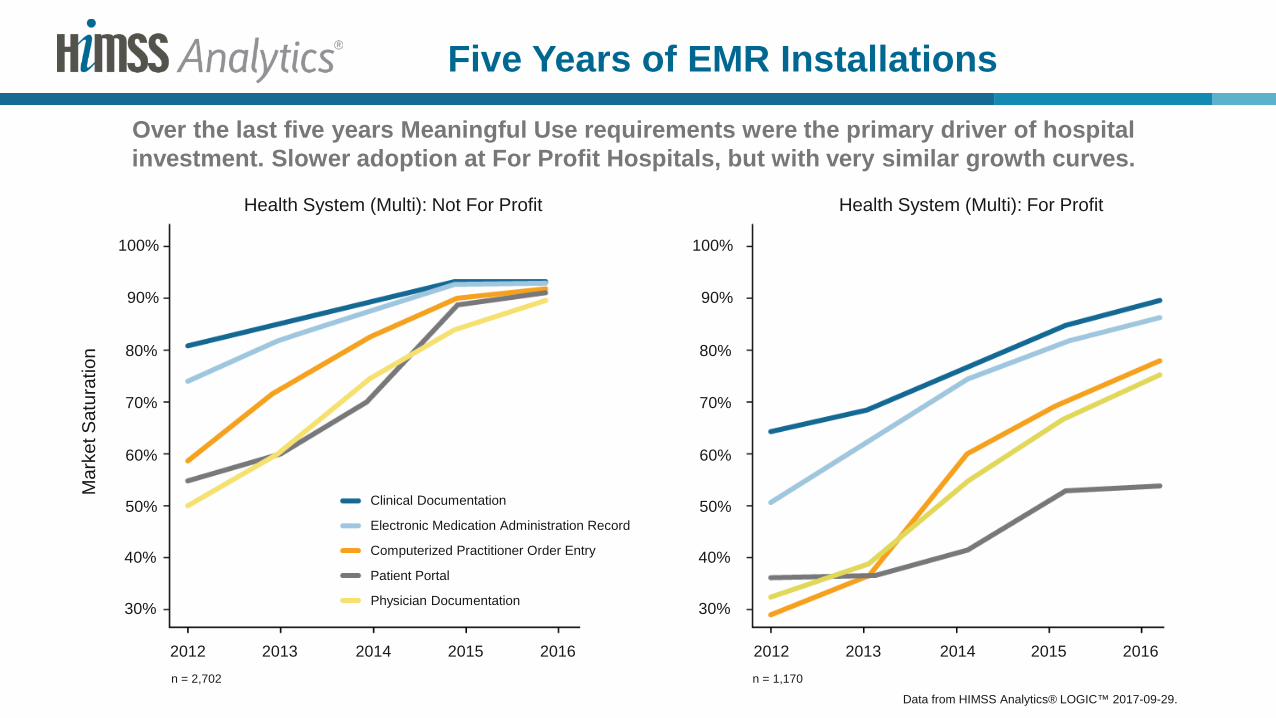

Five Years of EMR Installations

Over the last five years Meaningful Use requirements were the primary driver of hospital investment. Slower adoption at For Profit Hospitals, but with very similar growth curves.

50%

40%

30%

2012

Clinical Documentation

Electronic Medication Administration Record

Computerized Practitioner Order Entry

Patient Portal

60%

70%

Physician Documentation

Data from HIMSS Analytics® LOGIC™ 2017-09-29.

n = 1,170

2013 20152014 2016

80%

90%

100%

Mar

ket S

atur

atio

n

Health System (Multi): Not For Profit Health System (Multi): For Profit

50%

40%

30%

2012

60%

70%

2013 20152014 2016

80%

90%

100%

n = 2,702

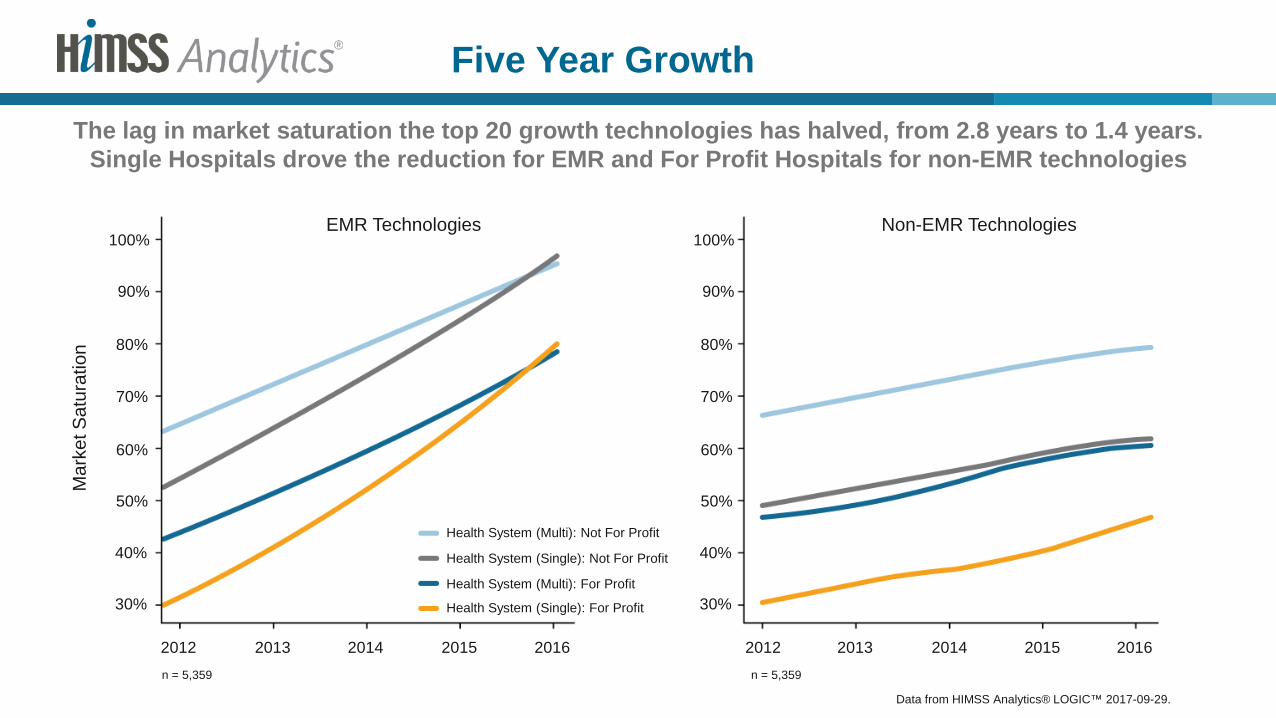

Five Year Growth

The lag in market saturation the top 20 growth technologies has halved, from 2.8 years to 1.4 years. Single Hospitals drove the reduction for EMR and For Profit Hospitals for non-EMR technologies

50%

40%

30%

2012

60%

70%

2013 20152014 2016

80%

90%

100%

Mar

ket S

atur

atio

n

n = 5,359

50%

40%

30%

2012

60%

70%

2013 20152014 2016

80%

90%

100%

n = 5,359

Data from HIMSS Analytics® LOGIC™ 2017-09-29.

EMR Technologies Non-EMR Technologies

Health System (Multi): For Profit

Health System (Multi): Not For Profit

Health System (Single): For Profit

Health System (Single): Not For Profit

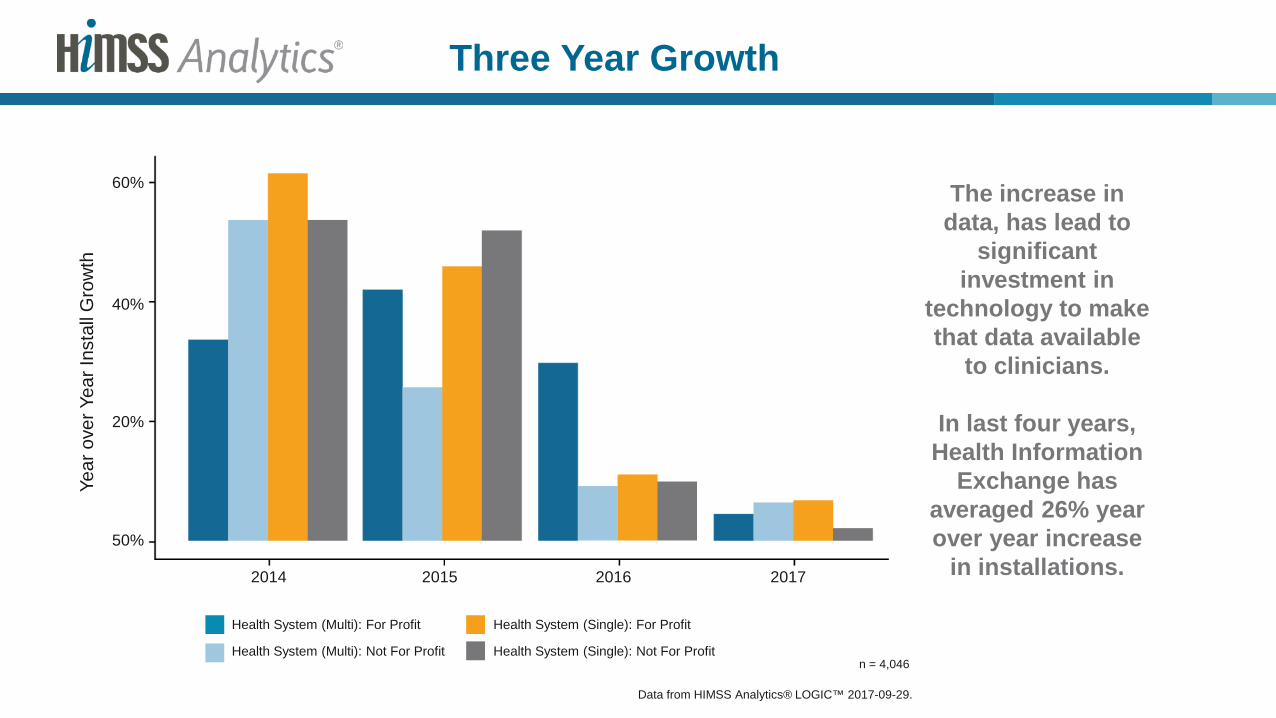

Three Year Growth

The increase in data, has lead to

significant investment in

technology to make that data available

to clinicians.

In last four years, Health Information

Exchange has averaged 26% year over year increase

in installations.

Year

ove

r Yea

r Ins

tall

Gro

wth

n = 4,046

Data from HIMSS Analytics® LOGIC™ 2017-09-29.

50%

2014

20%

40%

60%

2015 2016 2017

Health System (Multi): For Profit

Health System (Multi): Not For Profit

Health System (Single): For Profit

Health System (Single): Not For Profit

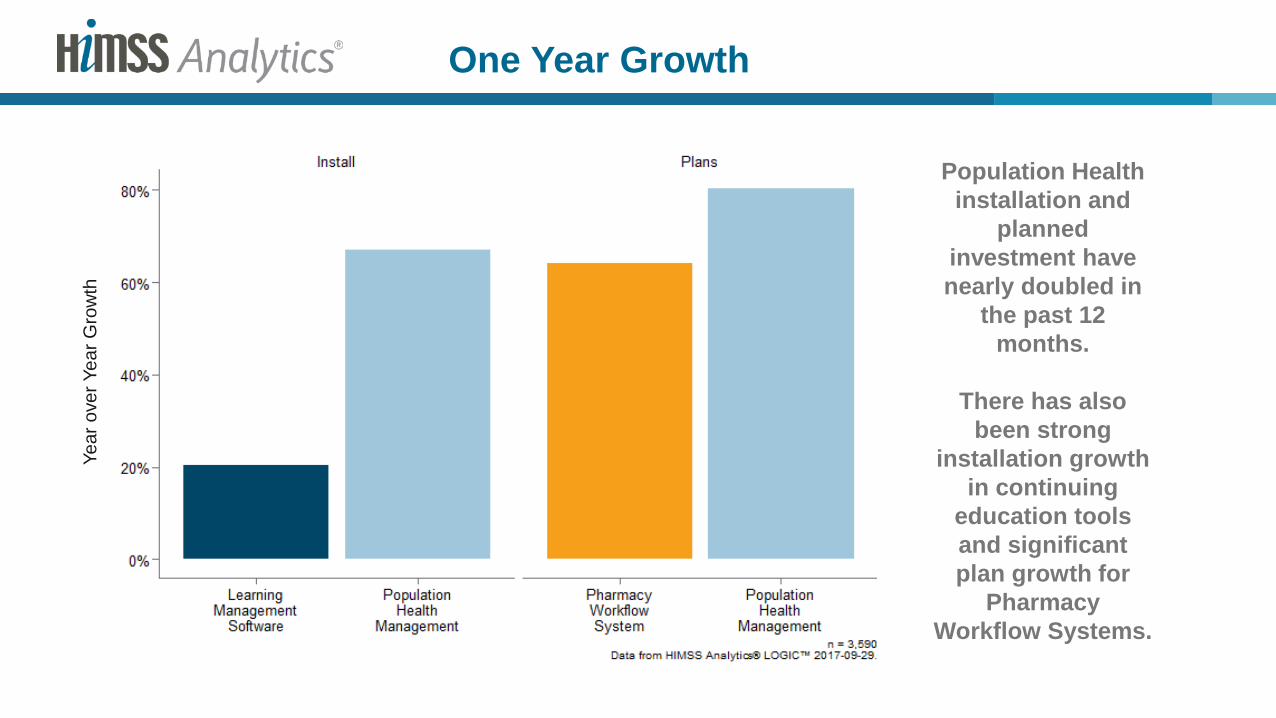

One Year Growth

Population Health installation and

planned investment have nearly doubled in

the past 12 months.

There has also been strong

installation growth in continuing

education tools and significant plan growth for

Pharmacy Workflow Systems.

Year

ove

r Yea

r Gro

wth