Embed Size (px)

Citation preview

Slide 1

Medicare, private health insurance and three elephants in the room

Paul Gross PhD

Invited address, 15th Annual Health Insurance Summit, 28 July 2016

Slide 2

This presentation

n Ten great truths (or at least bold conjectures) n Three elephants in the room n Refining PHI to bend the cost curve: 8 ways

Slide 3

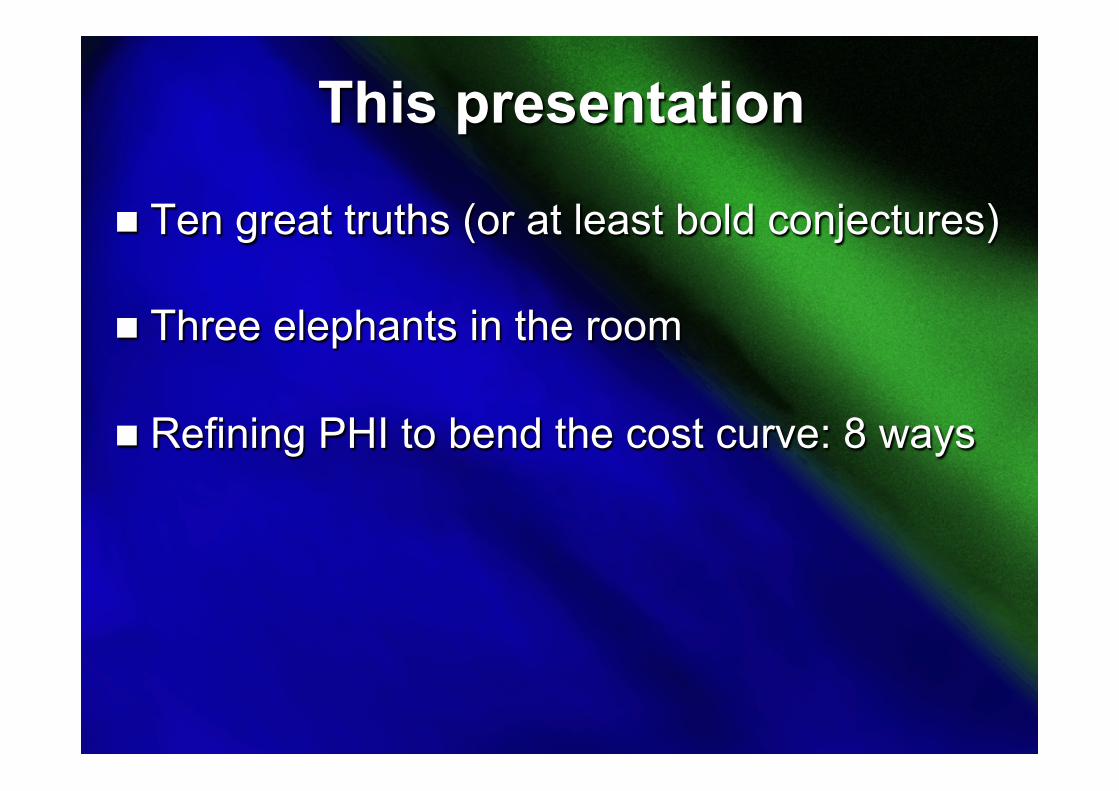

Budget cuts +

PHI irrelevance +

Increasing privatisation of care =

Higher copayments AND

Larger elephant in room: financial protection

GREAT TRUTH 1 post 2 July 2016

Slide 4

GREAT TRUTH 2: Medicare reform 2016

Simplistic solutions ≠ Medicare reform

n Raise the Medicare levy1 n Medicare Select single payer + HSA2 n Unravel the MBS freeze3

n Medical Home pilot n Listing surgical Px prices alone4

None of these avoid the iceberg of RISING COPAYMENTS

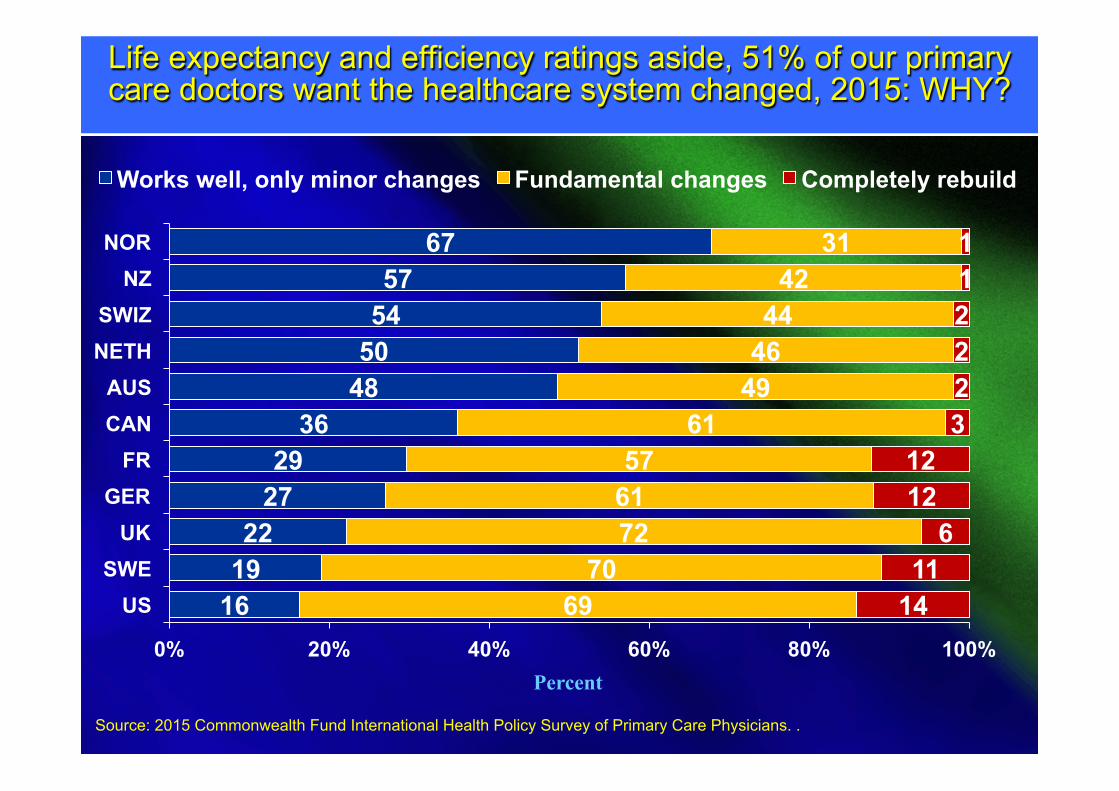

Slide 5 5 Life expectancy and efficiency ratings aside, 51% of our primary care doctors want the healthcare system changed, 2015: WHY?

16 19 22

27 29

36 48 50 54 57

67

69 70

72 61 57

61 49 46 44

42 31

14 11

6 12 12

3 2 2 2 1 1

0% 20% 40% 60% 80% 100%

US SWE

UK GER

FR CAN AUS

NETH SWIZ

NZ NOR

Works well, only minor changes Fundamental changes Completely rebuild

Percent

Source: 2015 Commonwealth Fund International Health Policy Survey of Primary Care Physicians. .

Slide 6

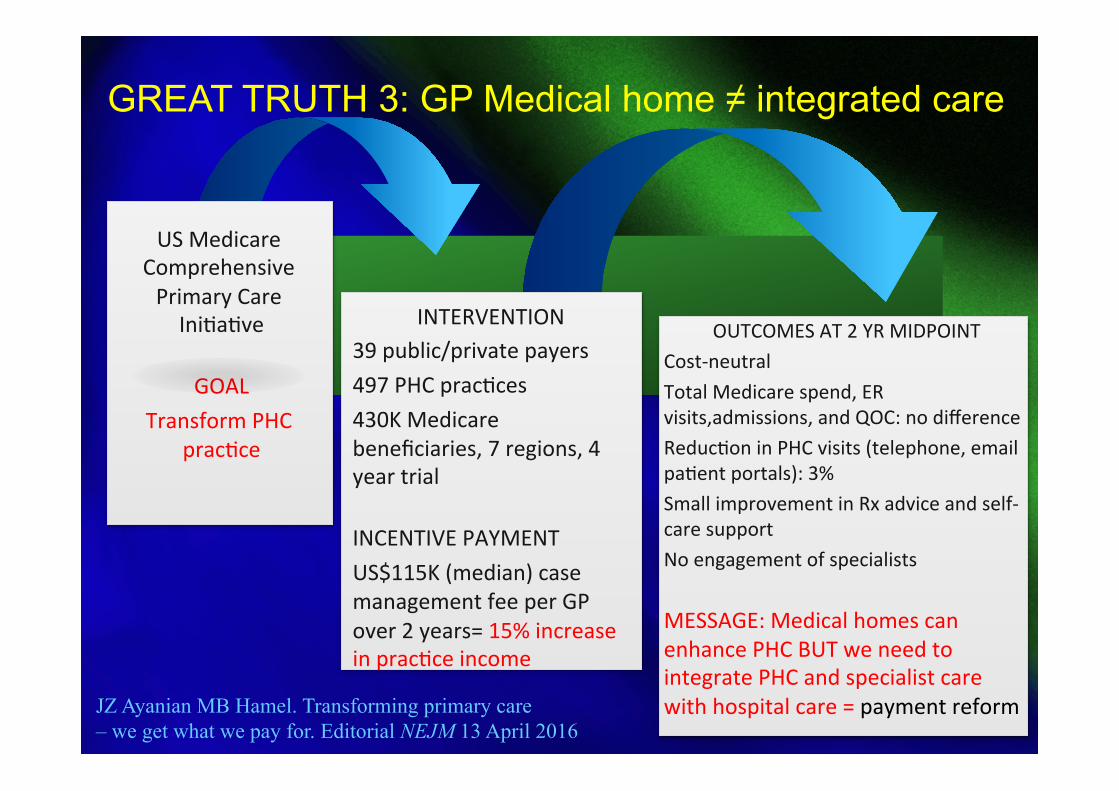

OUTCOMES AT 2 YR MIDPOINT Cost-‐neutral Total Medicare spend, ER visits,admissions, and QOC: no difference ReducEon in PHC visits (telephone, email paEent portals): 3% Small improvement in Rx advice and self-‐care support No engagement of specialists

MESSAGE: Medical homes can enhance PHC BUT we need to integrate PHC and specialist care with hospital care = payment reform

US Medicare Comprehensive Primary Care IniEaEve

GOAL Transform PHC

pracEce

INTERVENTION 39 public/private payers 497 PHC pracEces 430K Medicare beneficiaries, 7 regions, 4 year trial

INCENTIVE PAYMENT US$115K (median) case management fee per GP over 2 years= 15% increase in pracEce income

GREAT TRUTH 3: GP Medical home ≠ integrated care

JZ Ayanian MB Hamel. Transforming primary care – we get what we pay for. Editorial NEJM 13 April 2016

Slide 7

Great truth 4: Transitional care matters n Four of eleven programs in Medicare Coordinated Care

Demonstration reduced hospitalizations by 8–33 percent among enrollees who had a high risk of near-term hospitalization.

n Care coordinators in at least three of the four programs :

– supplement telephone calls to patients with frequent in-person meetings;

– occasionally meet in person with providers; – act as a communications hub for providers; – deliver evidence-based education to patients; – provide strong medication management; and – provide timely & comprehensive TC post-discharge

“The approaches would save money only if care coordination fees were modest and organizations found cost-effective ways to deliver the interventions”

Slide 8

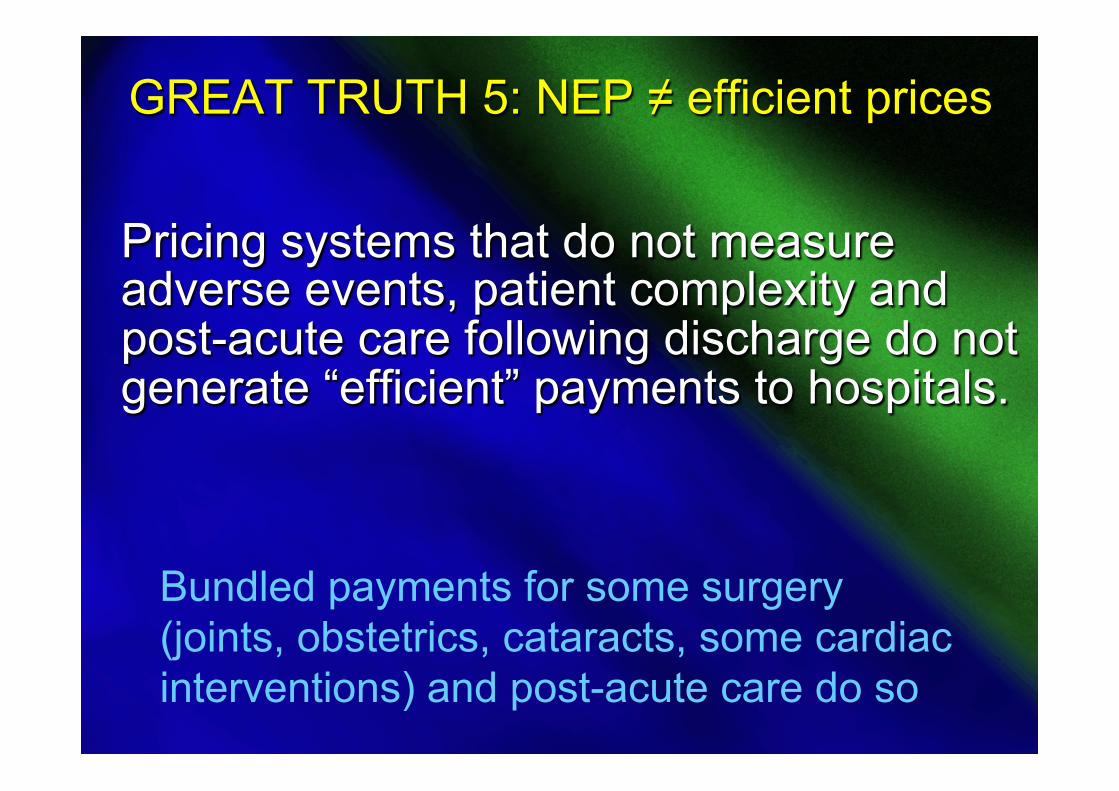

GREAT TRUTH 5: NEP ≠ efficient prices

Pricing systems that do not measure adverse events, patient complexity and post-acute care following discharge do not generate “efficient” payments to hospitals.

Bundled payments for some surgery (joints, obstetrics, cataracts, some cardiac interventions) and post-acute care do so

Slide 9

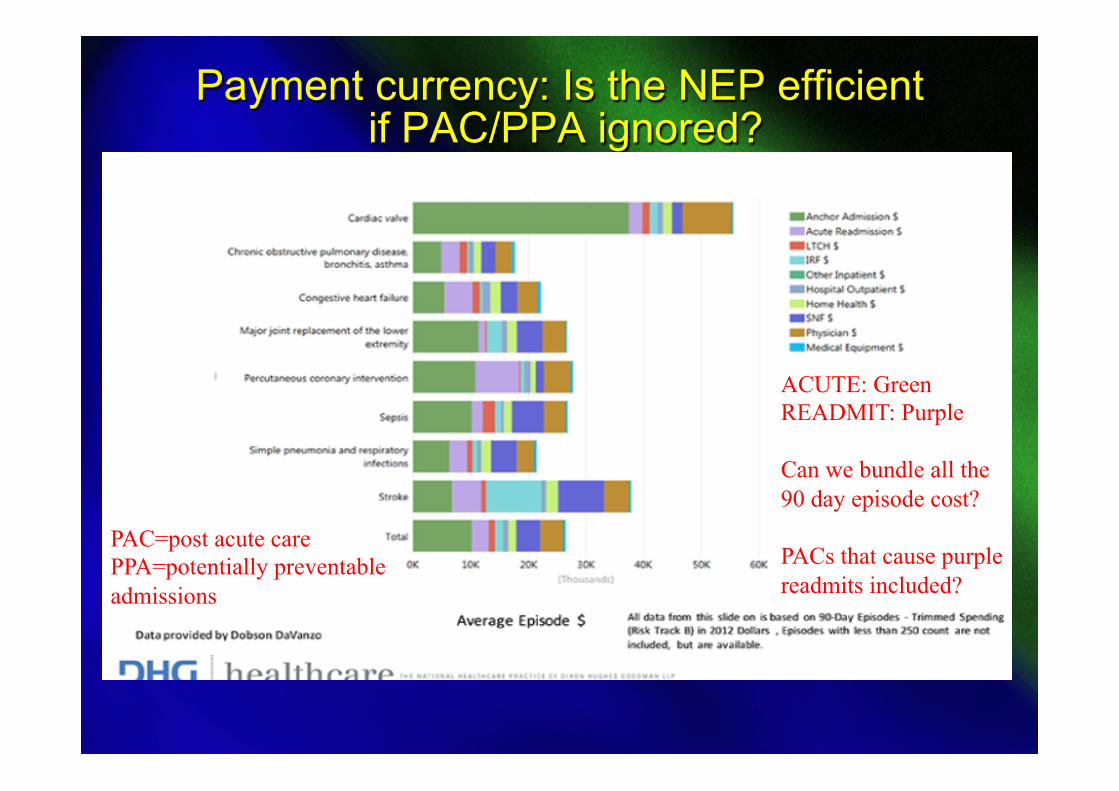

Payment currency: Is the NEP efficient if PAC/PPA ignored?

ACUTE: Green READMIT: Purple Can we bundle all the 90 day episode cost? PACs that cause purple readmits included?

PAC=post acute care PPA=potentially preventable admissions

Slide 10

GREAT TRUTH 6: Reform w/o doctors ≠ reform

It's a lot easier to get doctors and perhaps hospitals engaged in transformation when it's done at the locus of their control.

After De Brantes, 2015

Confirmed by Healthe initiative with DVA

Slide 11

Technological

Your Logo

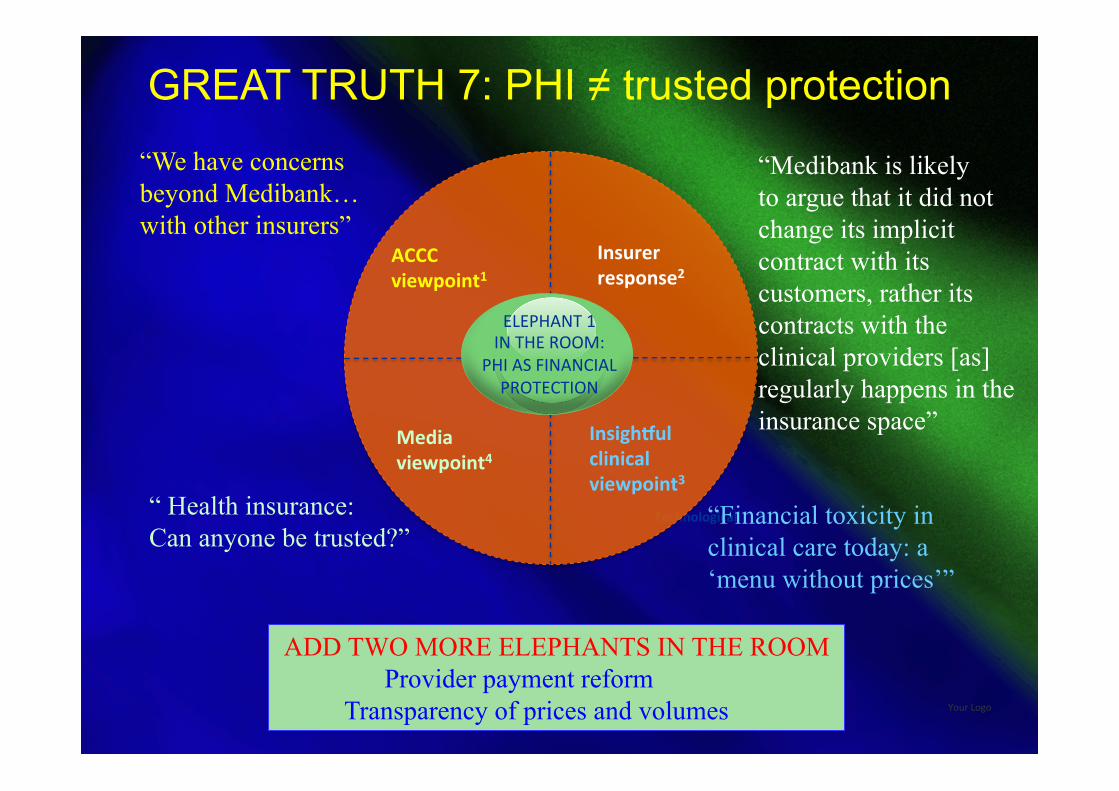

ELEPHANT 1 IN THE ROOM:

PHI AS FINANCIAL PROTECTION

ACCC viewpoint1

Media viewpoint4

Insurer response2

Insigh;ul clinical viewpoint3

“We have concerns beyond Medibank… with other insurers”

“ Health insurance: Can anyone be trusted?”

“Medibank is likely to argue that it did not change its implicit contract with its customers, rather its contracts with the clinical providers [as] regularly happens in the insurance space”

“Financial toxicity in clinical care today: a ‘menu without prices’”

ADD TWO MORE ELEPHANTS IN THE ROOM Provider payment reform Transparency of prices and volumes

GREAT TRUTH 7: PHI ≠ trusted protection

Slide 12

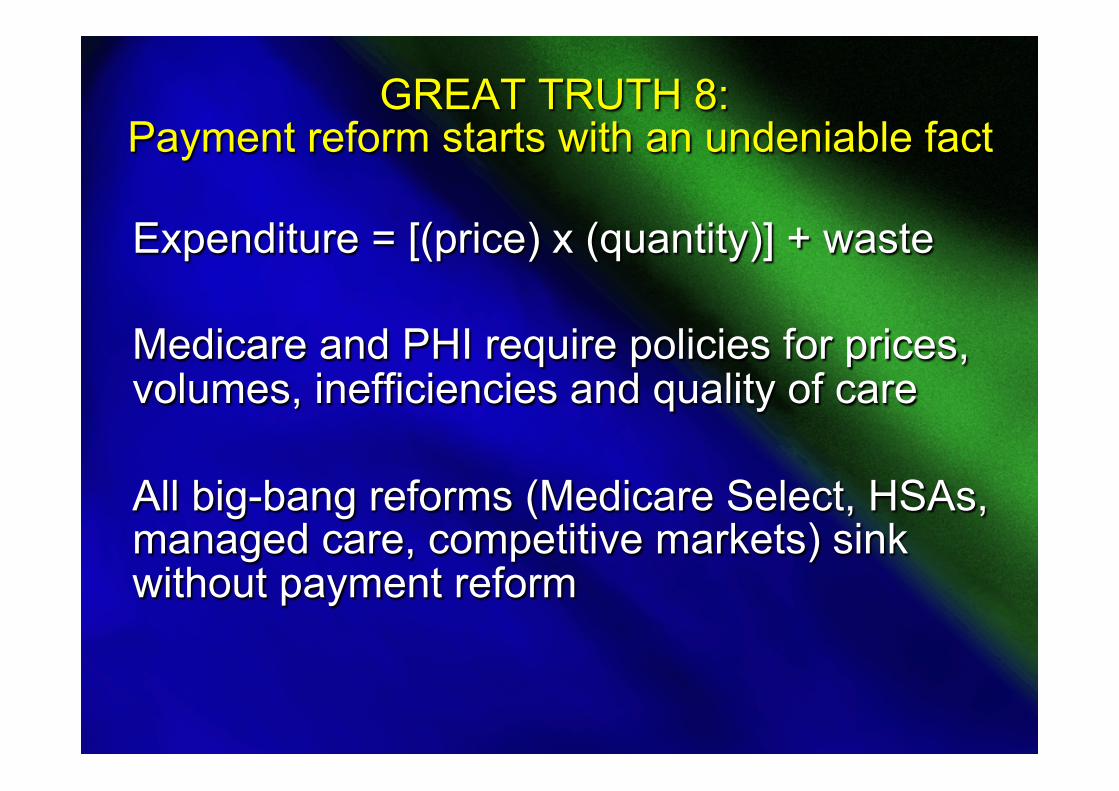

GREAT TRUTH 8: Payment reform starts with an undeniable fact

Expenditure = [(price) x (quantity)] + waste Medicare and PHI require policies for prices, volumes, inefficiencies and quality of care All big-bang reforms (Medicare Select, HSAs, managed care, competitive markets) sink without payment reform

Slide 13

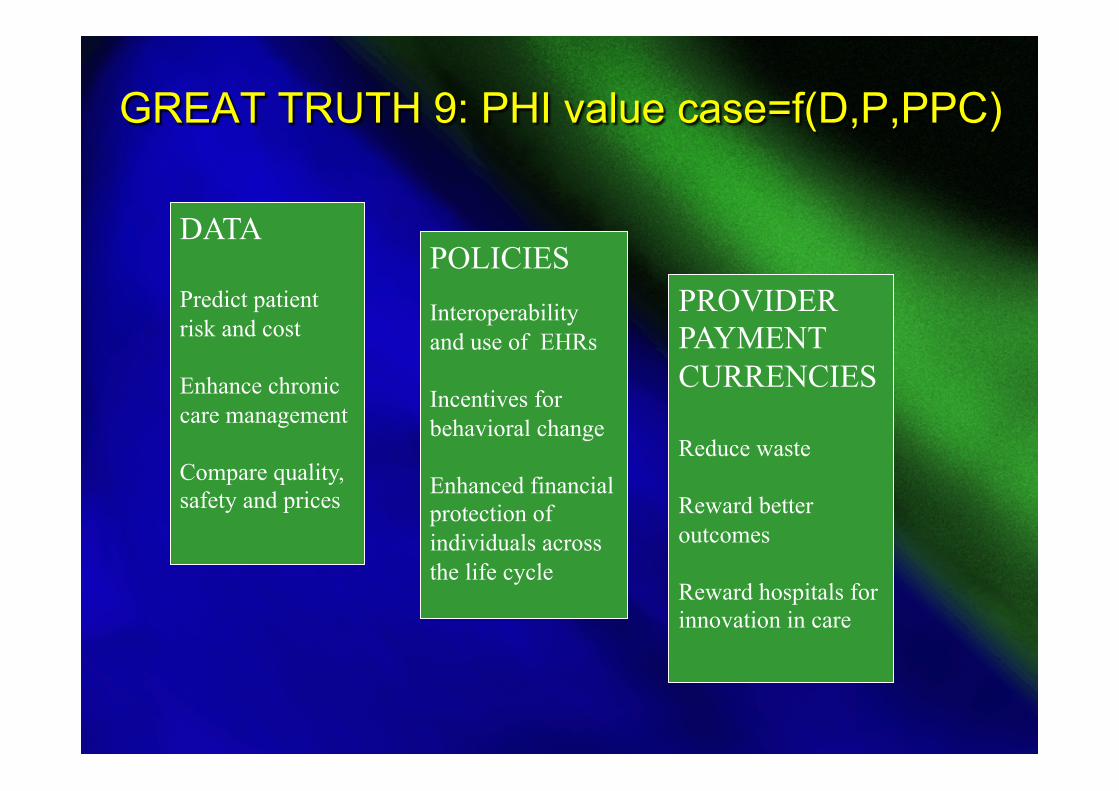

GREAT TRUTH 9: PHI value case=f(D,P,PPC)

DATA Predict patient risk and cost Enhance chronic care management Compare quality, safety and prices

POLICIES Interoperability and use of EHRs Incentives for behavioral change Enhanced financial protection of individuals across the life cycle

PROVIDER PAYMENT CURRENCIES Reduce waste Reward better outcomes Reward hospitals for innovation in care

Slide 14

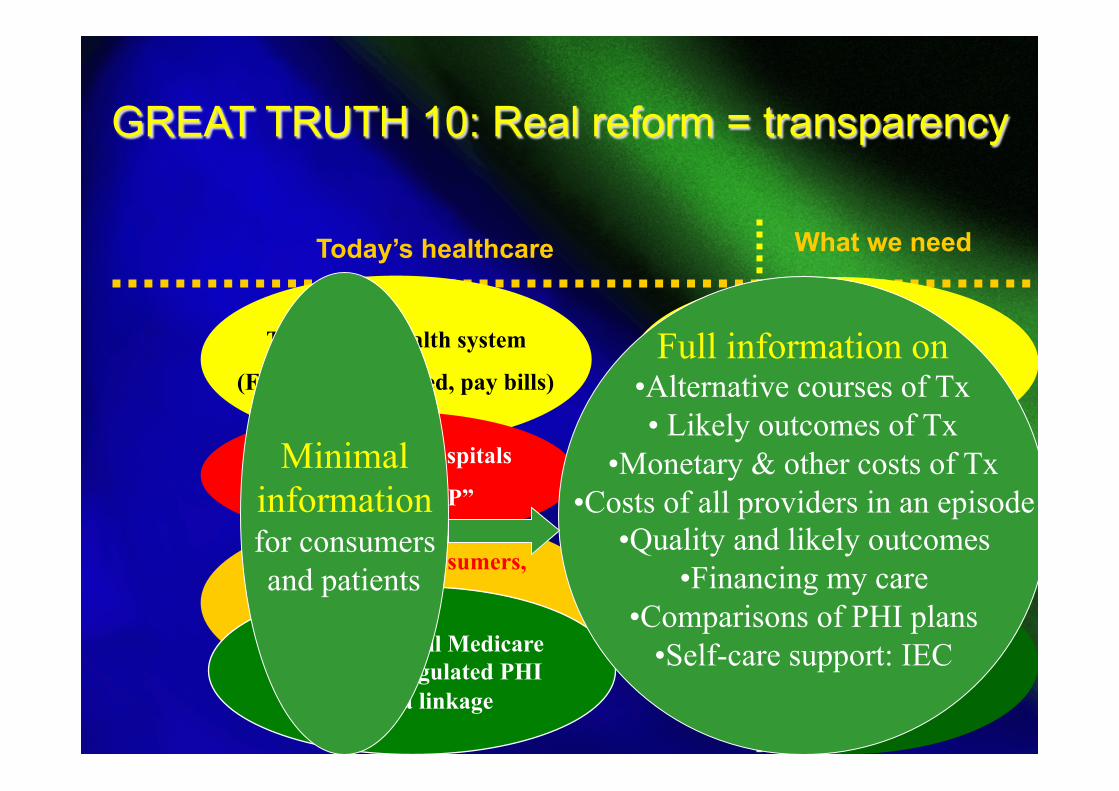

GREAT TRUTH 10: Real reform = transparency

Today’s healthcare What we need

Disease management (change behavior)

Traditional health system

(FFS, uncoordinated, pay bills)

Ill-informed consumers,

minimal self-care,

no economic incentives

Informed buyers,

Consumer-directed healthcare

Behavioral incentives

Multispecialist hospitals

Casemix, “NEP”

More single-specialty hospitals

Pay-for-value

Medicare

PHI + MSA’s, LTCI

Data linkage

One-size-fits-all Medicare Irrelevant, regulated PHI

No data linkage

Minimal information for consumers and patients

Full information on • Alternative courses of Tx • Likely outcomes of Tx

• Monetary & other costs of Tx • Costs of all providers in an episode

• Quality and likely outcomes • Financing my care

• Comparisons of PHI plans • Self-care support: IEC

Slide 15

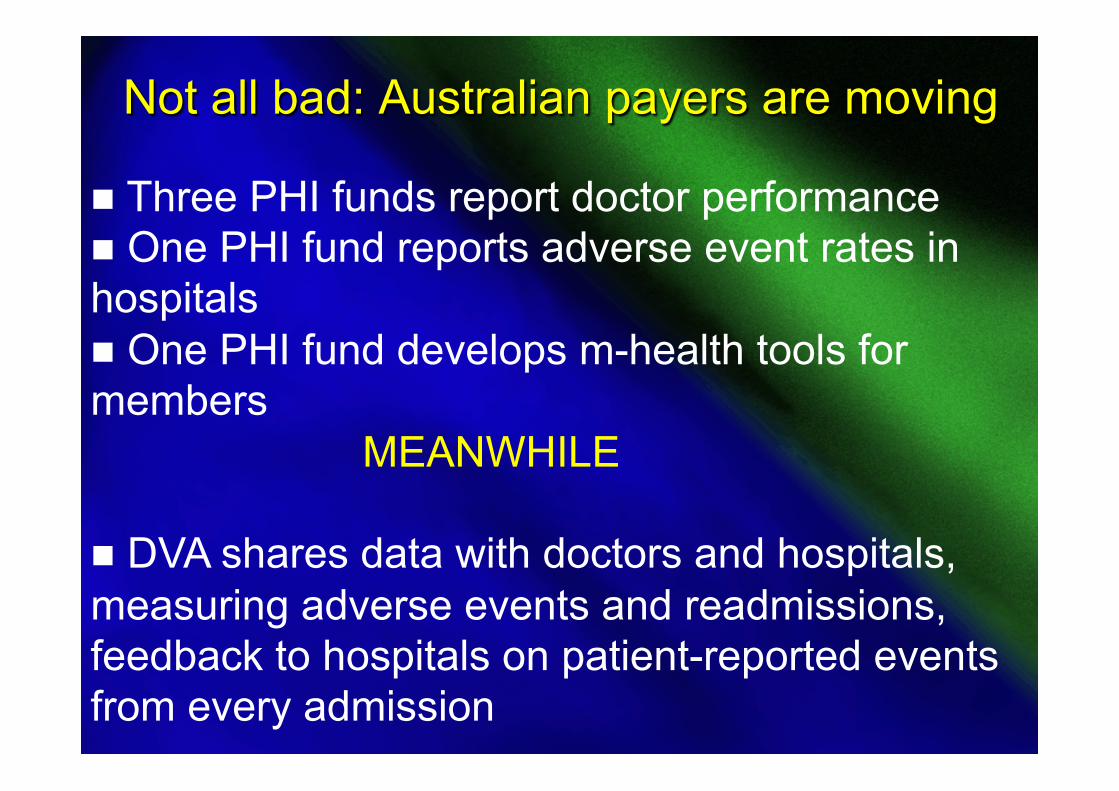

Not all bad: Australian payers are moving

n Three PHI funds report doctor performance n One PHI fund reports adverse event rates in hospitals n One PHI fund develops m-health tools for members MEANWHILE n DVA shares data with doctors and hospitals, measuring adverse events and readmissions, feedback to hospitals on patient-reported events from every admission

Slide 16

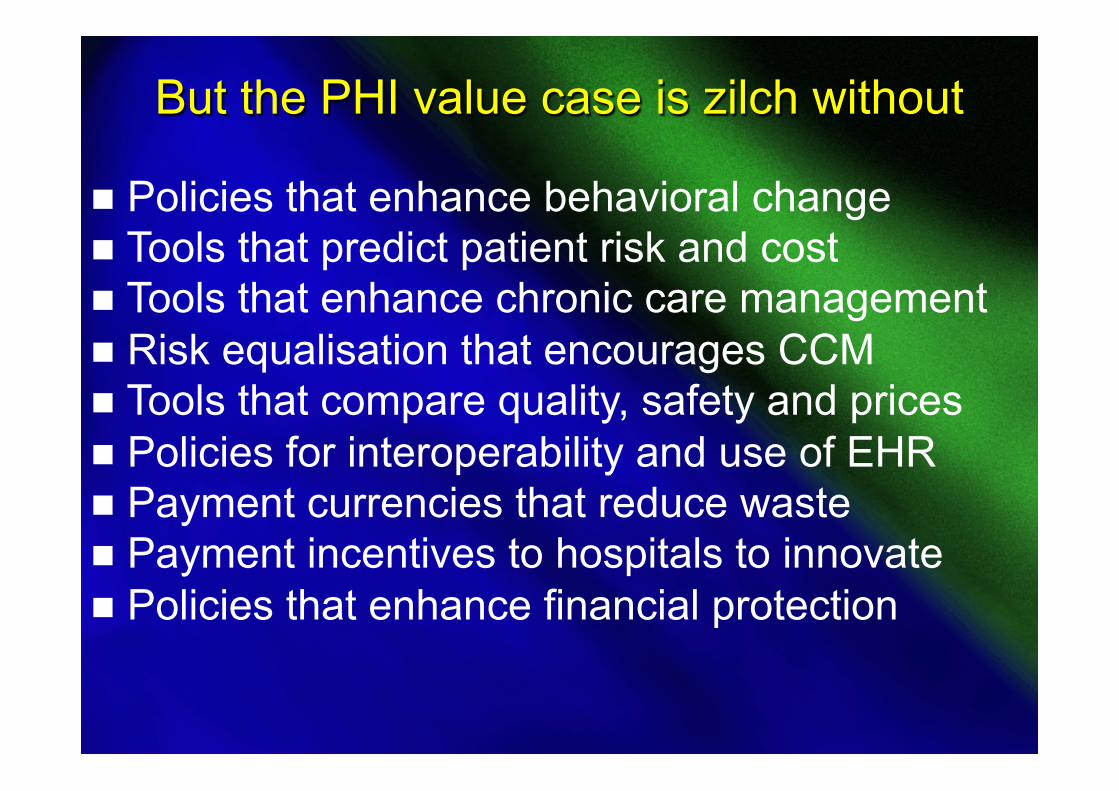

But the PHI value case is zilch without

n Policies that enhance behavioral change n Tools that predict patient risk and cost n Tools that enhance chronic care management n Risk equalisation that encourages CCM n Tools that compare quality, safety and prices n Policies for interoperability and use of EHR n Payment currencies that reduce waste n Payment incentives to hospitals to innovate n Policies that enhance financial protection

Slide 17

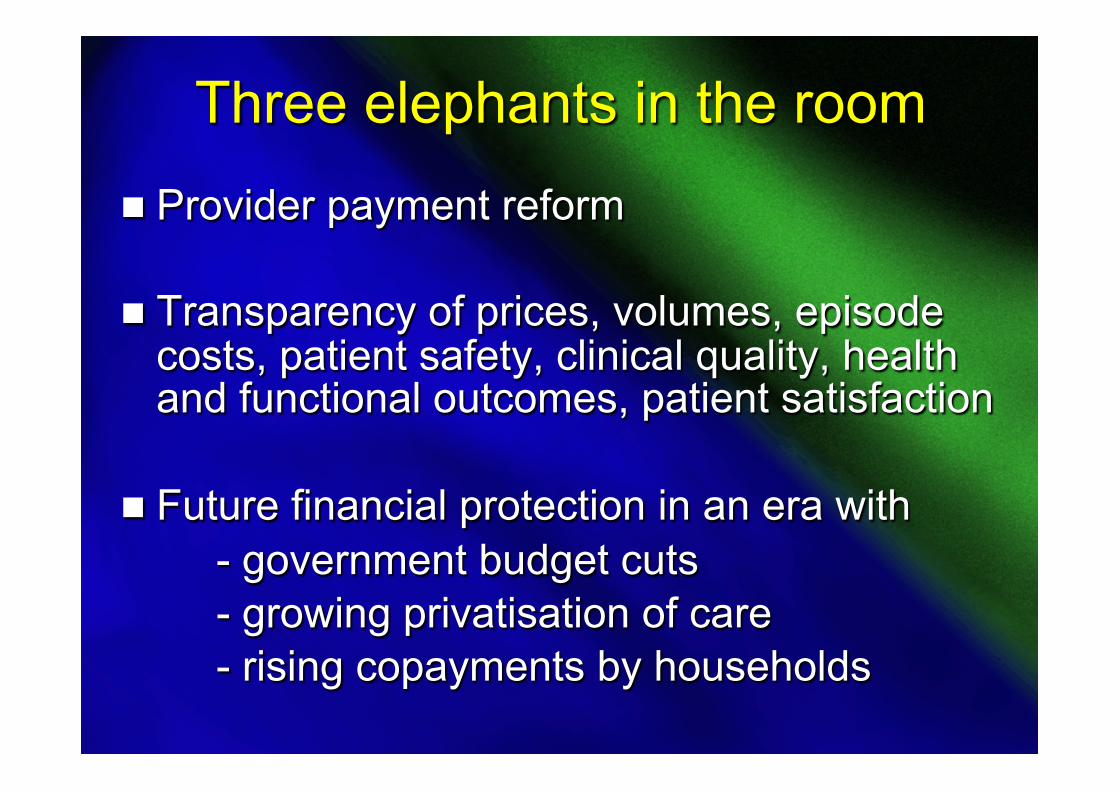

Three elephants in the room n Provider payment reform n Transparency of prices, volumes, episode

costs, patient safety, clinical quality, health and functional outcomes, patient satisfaction

n Future financial protection in an era with

- government budget cuts - growing privatisation of care - rising copayments by households

Slide 18

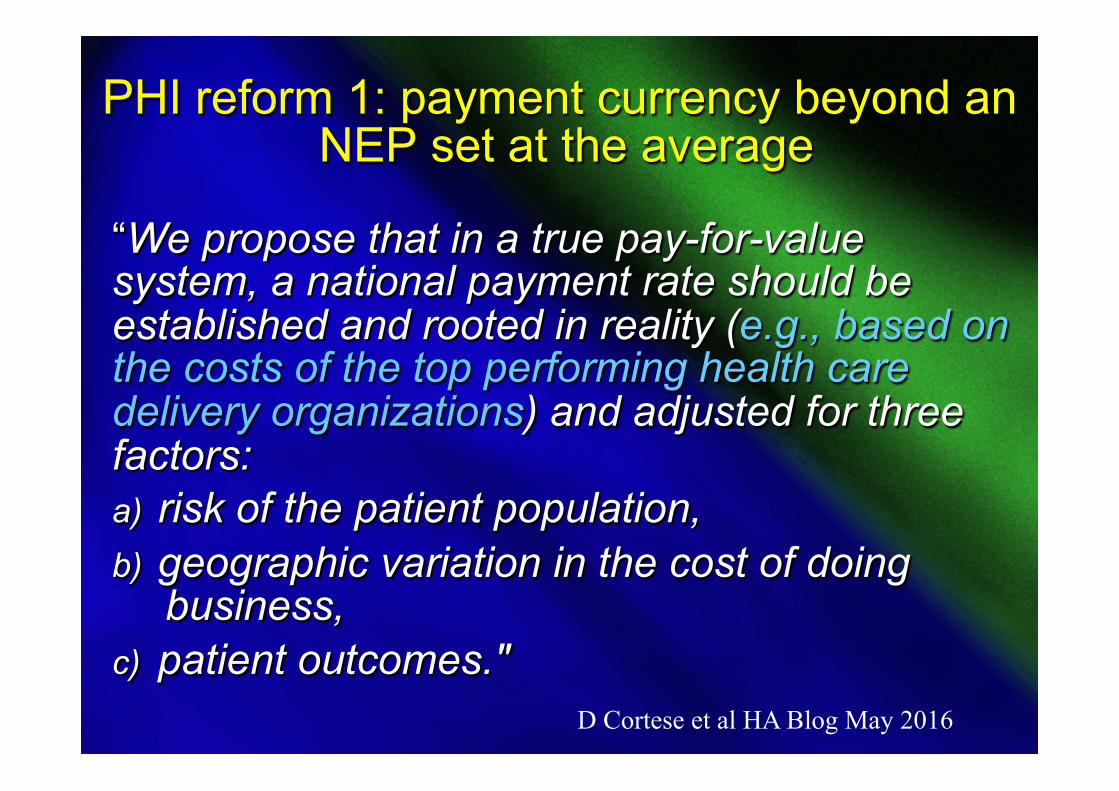

PHI reform 1: payment currency beyond an NEP set at the average

“We propose that in a true pay-for-value system, a national payment rate should be established and rooted in reality (e.g., based on the costs of the top performing health care delivery organizations) and adjusted for three factors: a) risk of the patient population, b) geographic variation in the cost of doing

business, c) patient outcomes."

D Cortese et al HA Blog May 2016

Slide 19

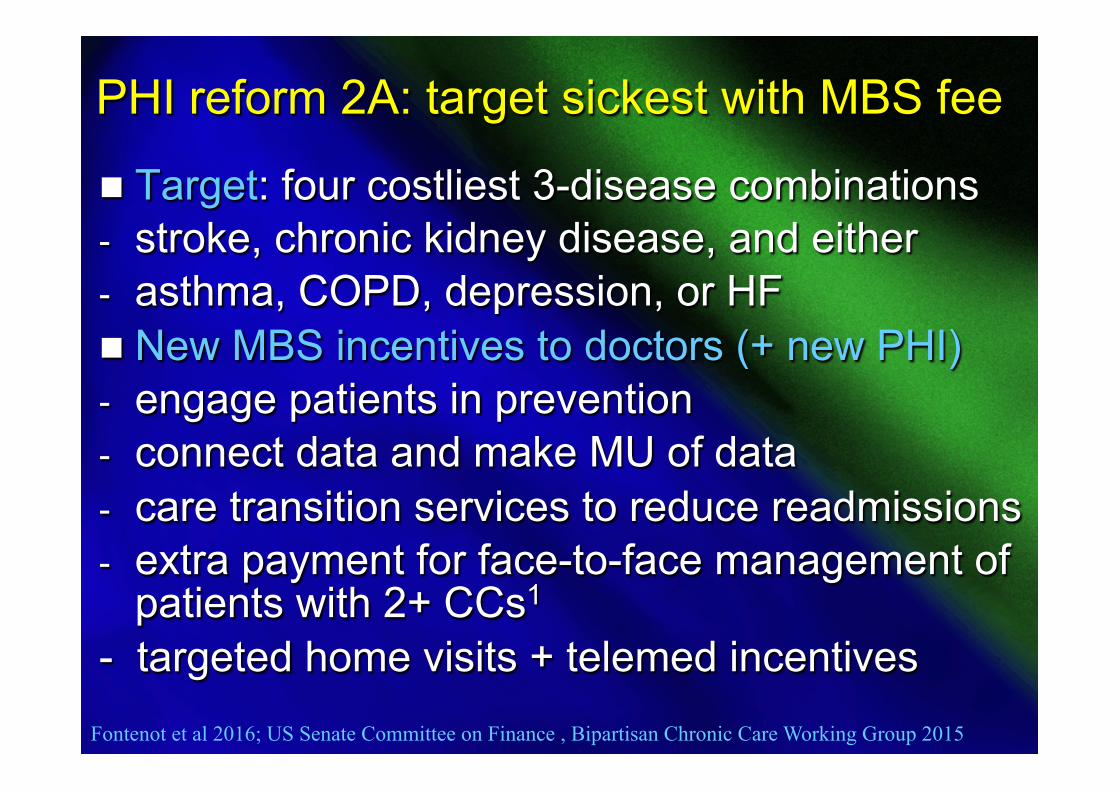

PHI reform 2A: target sickest with MBS fee

n Target: four costliest 3-disease combinations - stroke, chronic kidney disease, and either - asthma, COPD, depression, or HF n New MBS incentives to doctors (+ new PHI) - engage patients in prevention - connect data and make MU of data - care transition services to reduce readmissions - extra payment for face-to-face management of

patients with 2+ CCs1 - targeted home visits + telemed incentives

Fontenot et al 2016; US Senate Committee on Finance , Bipartisan Chronic Care Working Group 2015

Slide 20

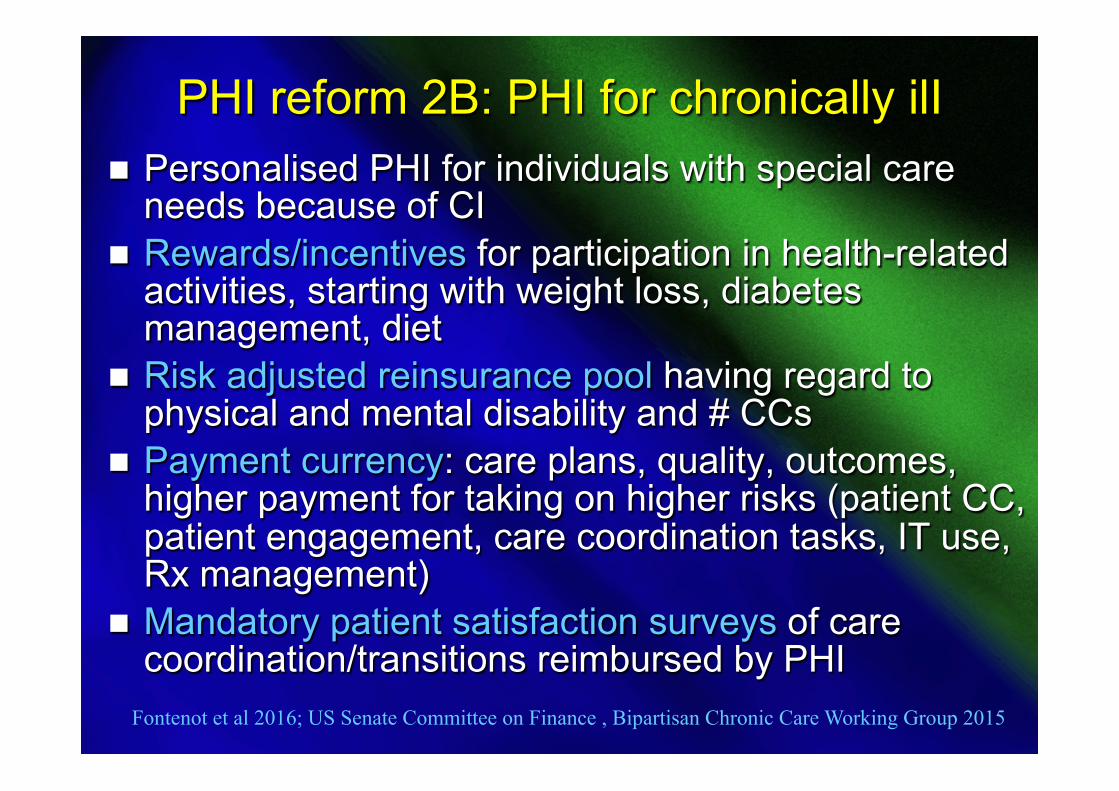

PHI reform 2B: PHI for chronically ilI n Personalised PHI for individuals with special care

needs because of CI n Rewards/incentives for participation in health-related

activities, starting with weight loss, diabetes management, diet

n Risk adjusted reinsurance pool having regard to physical and mental disability and # CCs

n Payment currency: care plans, quality, outcomes, higher payment for taking on higher risks (patient CC, patient engagement, care coordination tasks, IT use, Rx management)

n Mandatory patient satisfaction surveys of care coordination/transitions reimbursed by PHI

Fontenot et al 2016; US Senate Committee on Finance , Bipartisan Chronic Care Working Group 2015

Slide 21

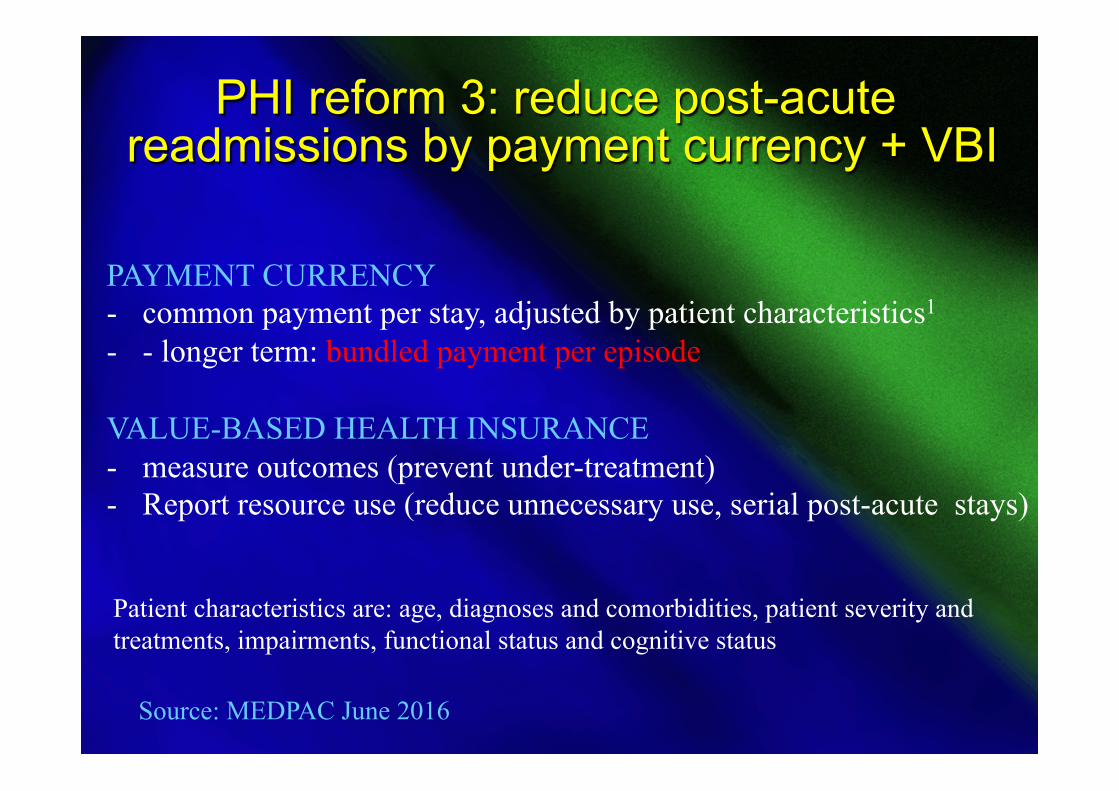

PHI reform 3: reduce post-acute readmissions by payment currency + VBI

Source: MEDPAC June 2016

PAYMENT CURRENCY - common payment per stay, adjusted by patient characteristics1 - - longer term: bundled payment per episode VALUE-BASED HEALTH INSURANCE - measure outcomes (prevent under-treatment) - Report resource use (reduce unnecessary use, serial post-acute stays)

Patient characteristics are: age, diagnoses and comorbidities, patient severity and treatments, impairments, functional status and cognitive status

Slide 22

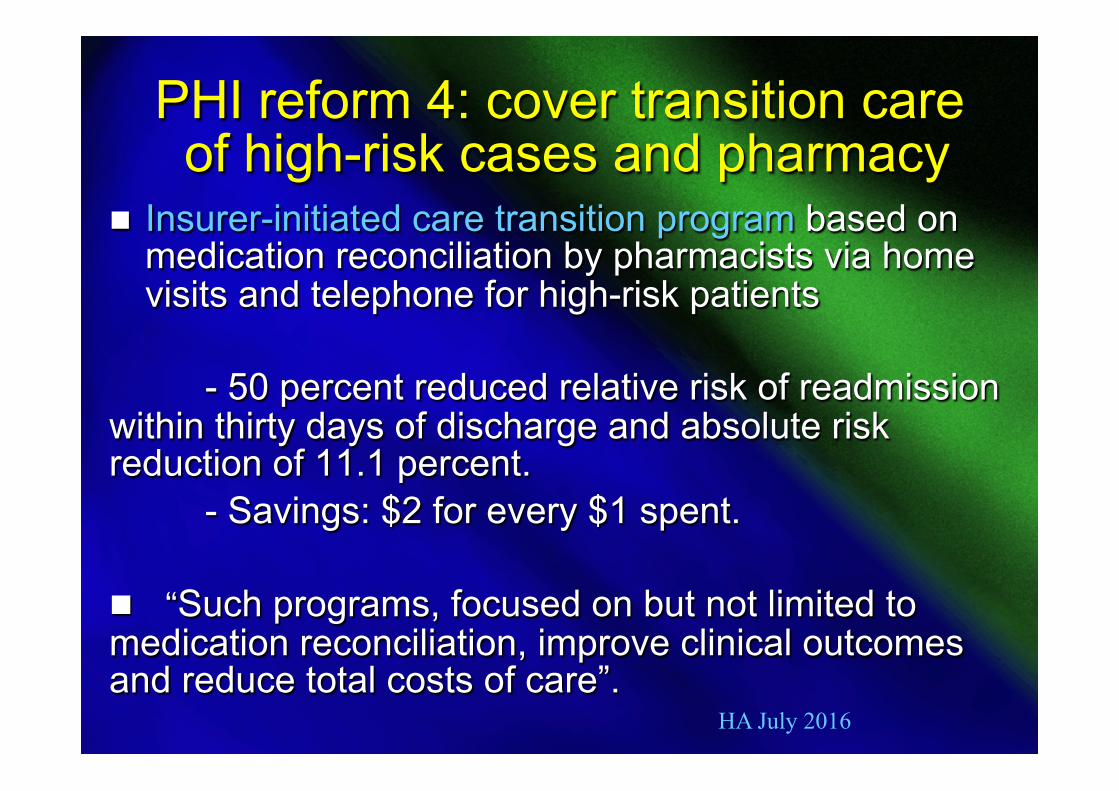

PHI reform 4: cover transition care of high-risk cases and pharmacy

n Insurer-initiated care transition program based on medication reconciliation by pharmacists via home visits and telephone for high-risk patients

- 50 percent reduced relative risk of readmission within thirty days of discharge and absolute risk reduction of 11.1 percent.

- Savings: $2 for every $1 spent. n “Such programs, focused on but not limited to medication reconciliation, improve clinical outcomes and reduce total costs of care”.

HA July 2016

Slide 23

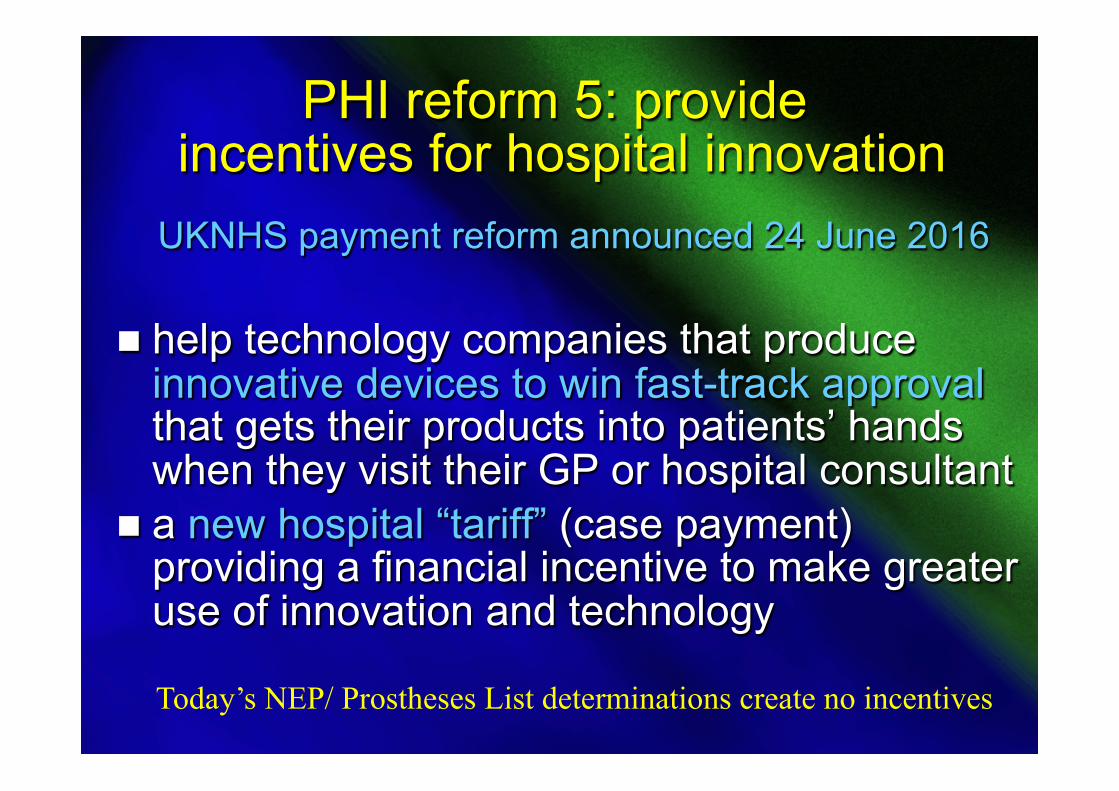

PHI reform 5: provide incentives for hospital innovation

UKNHS payment reform announced 24 June 2016 n help technology companies that produce

innovative devices to win fast-track approval that gets their products into patients’ hands when they visit their GP or hospital consultant

n a new hospital “tariff” (case payment) providing a financial incentive to make greater use of innovation and technology

Today’s NEP/ Prostheses List determinations create no incentives

Slide 24

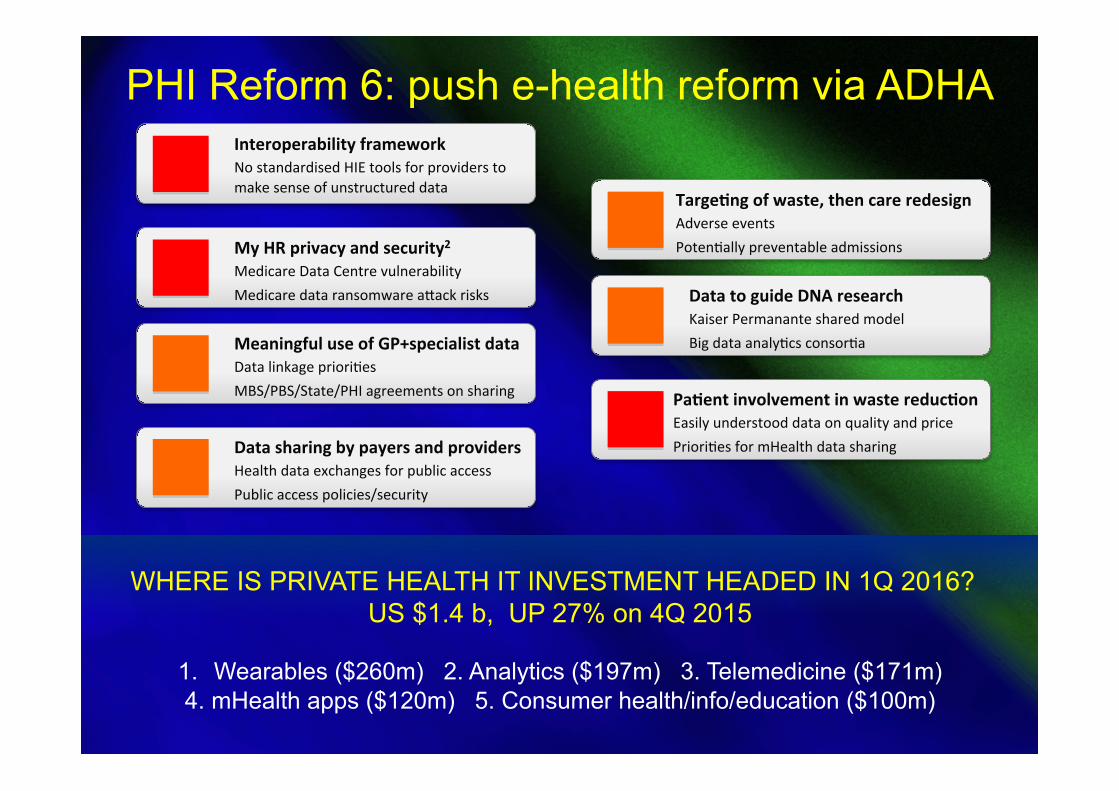

WHERE IS PRIVATE HEALTH IT INVESTMENT HEADED IN 1Q 2016? US $1.4 b, UP 27% on 4Q 2015

1. Wearables ($260m) 2. Analytics ($197m) 3. Telemedicine ($171m) 4. mHealth apps ($120m) 5. Consumer health/info/education ($100m)

Interoperability framework No standardised HIE tools for providers to make sense of unstructured data

My HR privacy and security2 Medicare Data Centre vulnerability Medicare data ransomware acack risks

Meaningful use of GP+specialist data Data linkage prioriEes MBS/PBS/State/PHI agreements on sharing

Data sharing by payers and providers Health data exchanges for public access Public access policies/security

TargeHng of waste, then care redesign Adverse events PotenEally preventable admissions

Data to guide DNA research Kaiser Permanante shared model Big data analyEcs consorEa

PaHent involvement in waste reducHon Easily understood data on quality and price PrioriEes for mHealth data sharing

PHI Reform 6: push e-health reform via ADHA

Slide 25

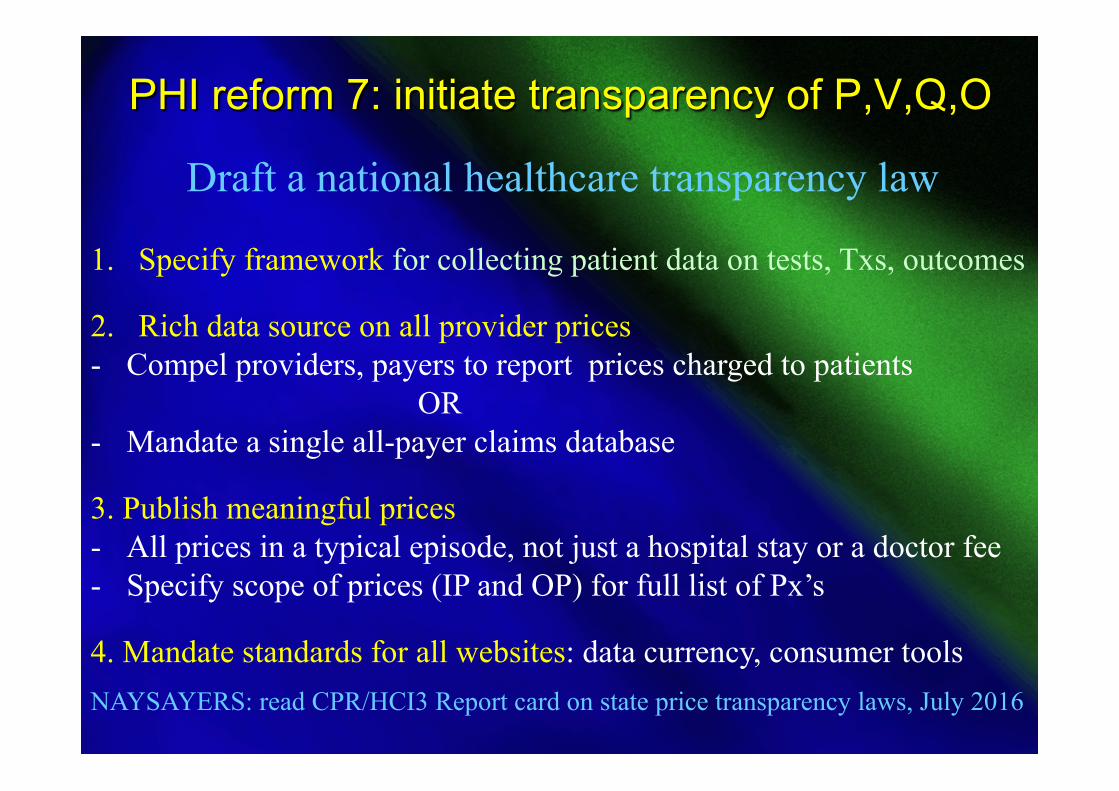

PHI reform 7: initiate transparency of P,V,Q,O

Draft a national healthcare transparency law 1. Specify framework for collecting patient data on tests, Txs, outcomes 2. Rich data source on all provider prices - Compel providers, payers to report prices charged to patients OR - Mandate a single all-payer claims database

3. Publish meaningful prices - All prices in a typical episode, not just a hospital stay or a doctor fee - Specify scope of prices (IP and OP) for full list of Px’s 4. Mandate standards for all websites: data currency, consumer tools NAYSAYERS: read CPR/HCI3 Report card on state price transparency laws, July 2016

Slide 26

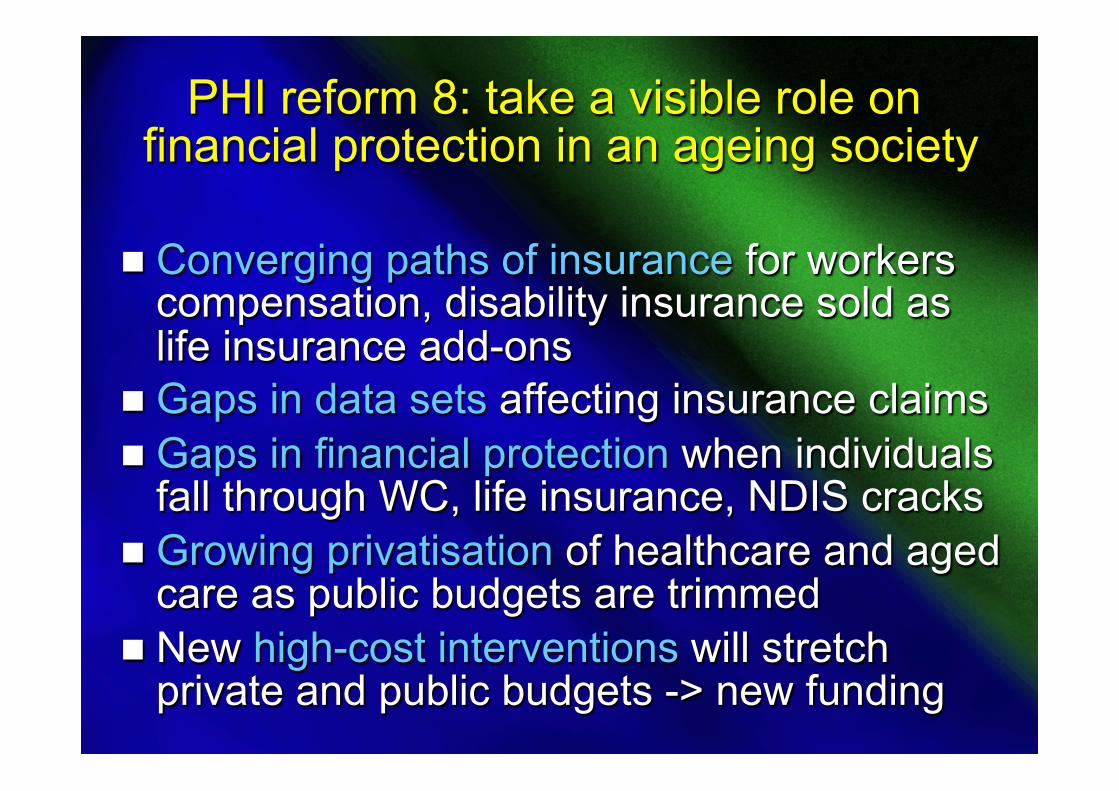

PHI reform 8: take a visible role on financial protection in an ageing society

n Converging paths of insurance for workers

compensation, disability insurance sold as life insurance add-ons

n Gaps in data sets affecting insurance claims n Gaps in financial protection when individuals

fall through WC, life insurance, NDIS cracks n Growing privatisation of healthcare and aged

care as public budgets are trimmed n New high-cost interventions will stretch

private and public budgets -> new funding

Slide 27

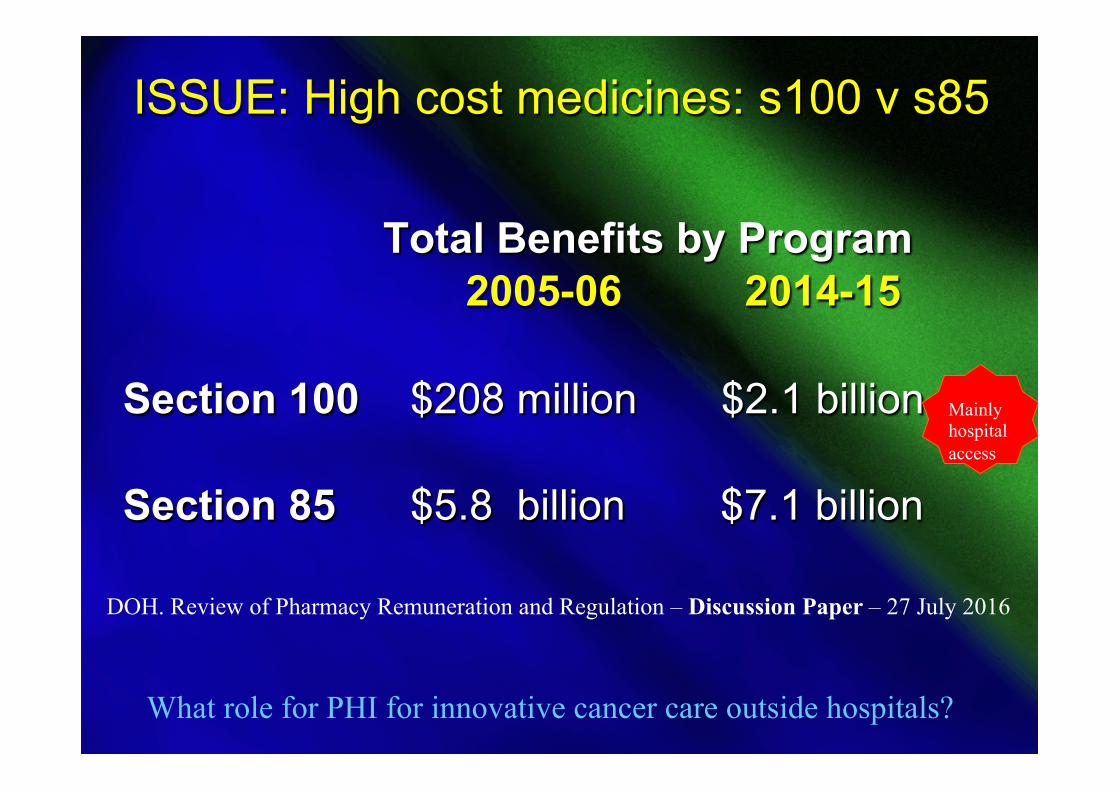

ISSUE: High cost medicines: s100 v s85

Total Benefits by Program 2005-06 2014-15 Section 100 $208 million $2.1 billion Section 85 $5.8 billion $7.1 billion

DOH. Review of Pharmacy Remuneration and Regulation – Discussion Paper – 27 July 2016

Mainly hospital access

What role for PHI for innovative cancer care outside hospitals?

Slide 28

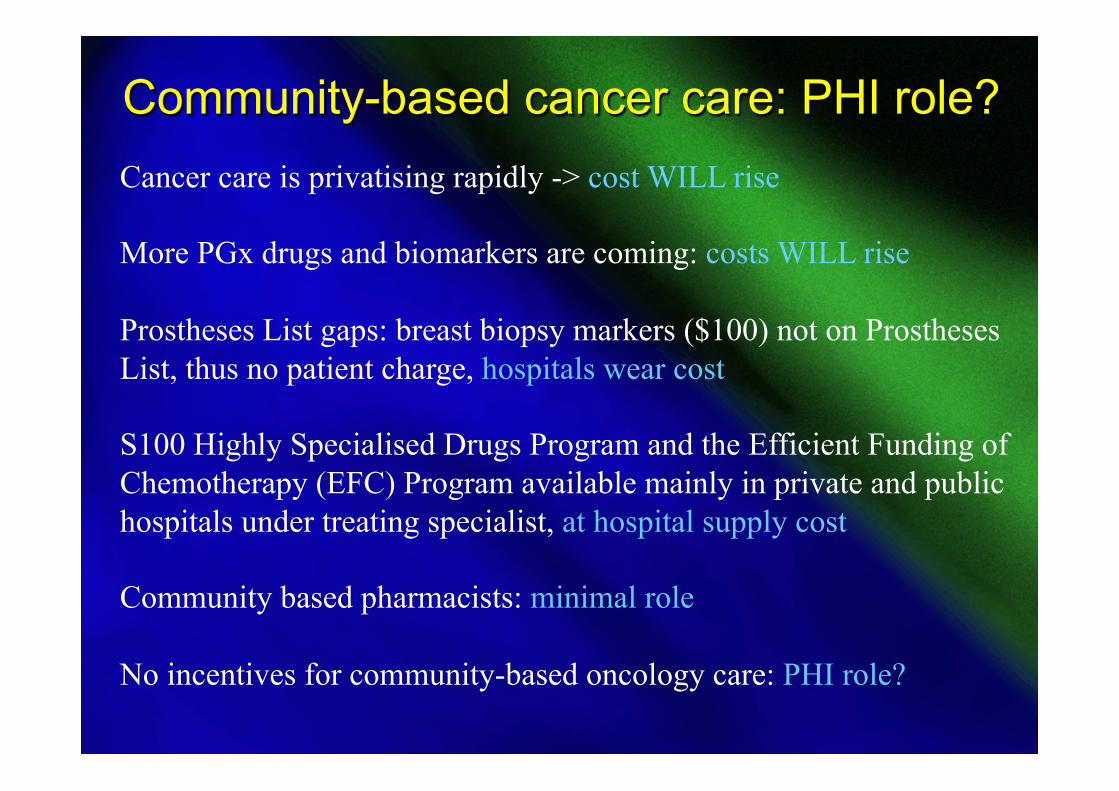

Community-based cancer care: PHI role? Cancer care is privatising rapidly -> cost WILL rise More PGx drugs and biomarkers are coming: costs WILL rise Prostheses List gaps: breast biopsy markers ($100) not on Prostheses List, thus no patient charge, hospitals wear cost S100 Highly Specialised Drugs Program and the Efficient Funding of Chemotherapy (EFC) Program available mainly in private and public hospitals under treating specialist, at hospital supply cost Community based pharmacists: minimal role No incentives for community-based oncology care: PHI role?

Slide 29

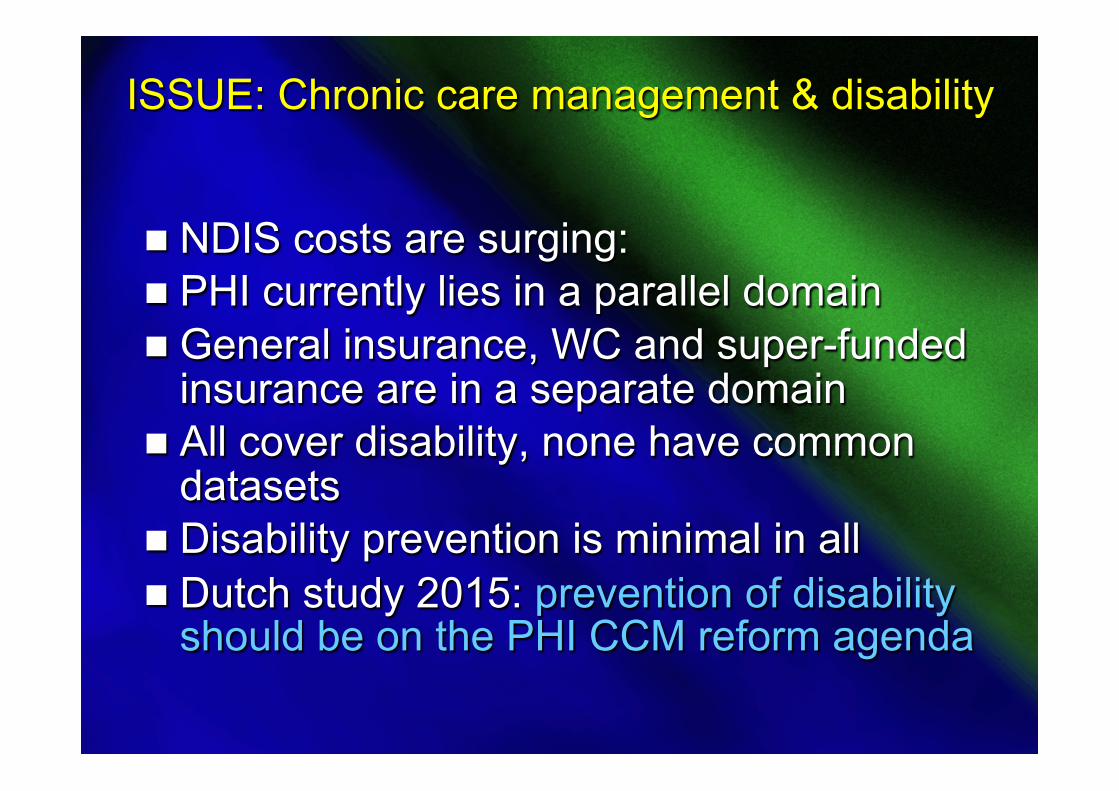

ISSUE: Chronic care management & disability

n NDIS costs are surging: n PHI currently lies in a parallel domain n General insurance, WC and super-funded

insurance are in a separate domain n All cover disability, none have common

datasets n Disability prevention is minimal in all n Dutch study 2015: prevention of disability

should be on the PHI CCM reform agenda

Slide 30

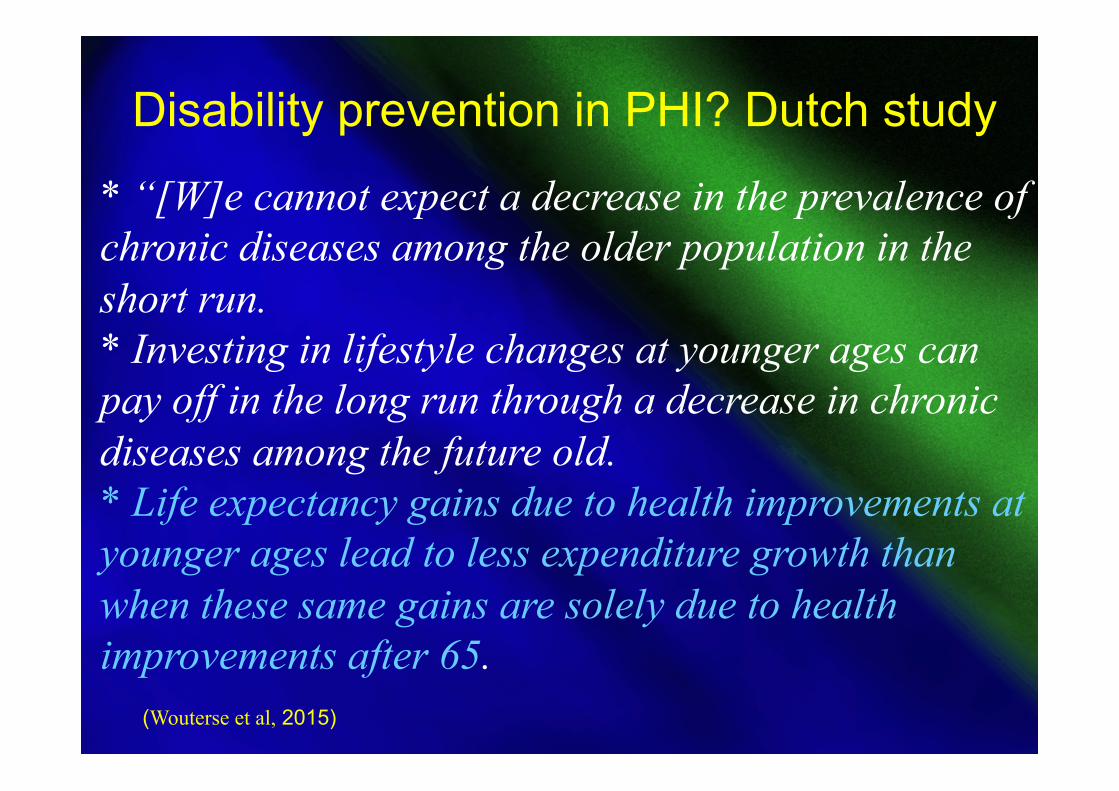

Disability prevention in PHI? Dutch study

* “[W]e cannot expect a decrease in the prevalence of chronic diseases among the older population in the short run. * Investing in lifestyle changes at younger ages can pay off in the long run through a decrease in chronic diseases among the future old. * Life expectancy gains due to health improvements at younger ages lead to less expenditure growth than when these same gains are solely due to health improvements after 65.

(Wouterse et al, 2015)

Slide 31

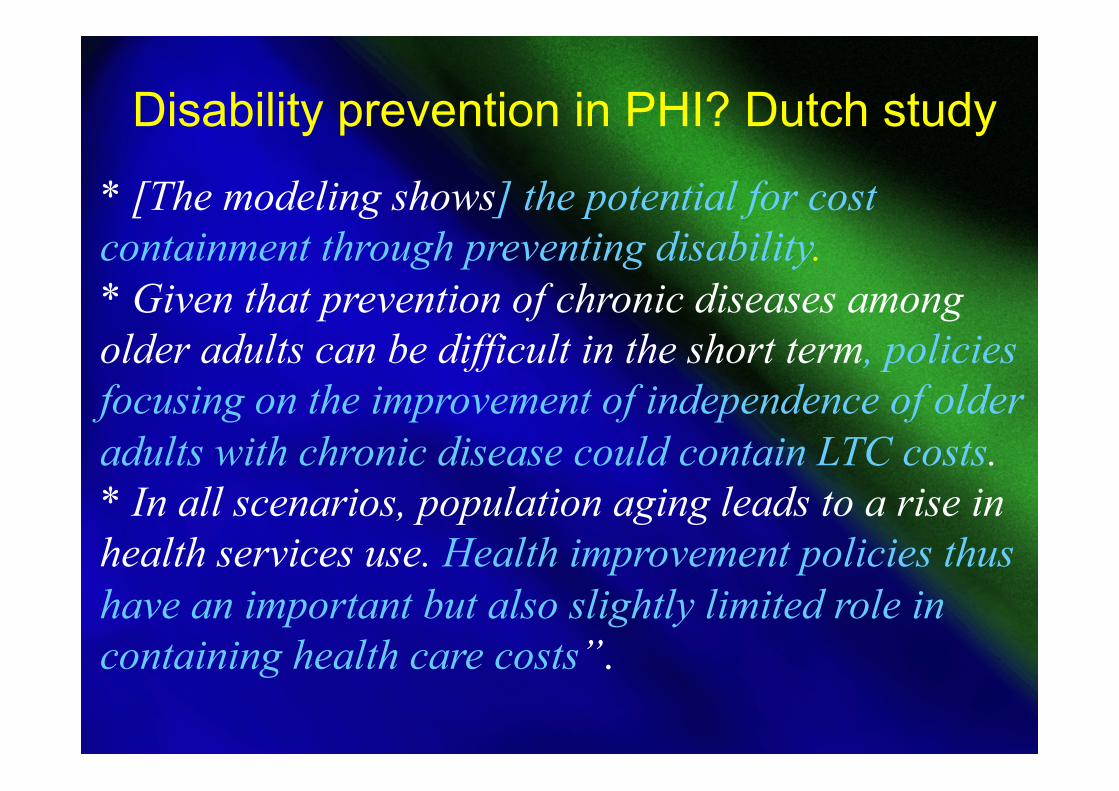

Disability prevention in PHI? Dutch study

* [The modeling shows] the potential for cost containment through preventing disability. * Given that prevention of chronic diseases among older adults can be difficult in the short term, policies focusing on the improvement of independence of older adults with chronic disease could contain LTC costs. * In all scenarios, population aging leads to a rise in health services use. Health improvement policies thus have an important but also slightly limited role in containing health care costs”.

Slide 32

“It’s clear that somebody has to do something, and it’s just pathetic that it has to be us.”

Jerry Garcia (of the Grateful Dead)

We cannot let politicians stuff up healthcare by protracted inaction and endless reviews

The “us” are in this room