Embed Size (px)

Citation preview

1

Cash Balance 201Interest Crediting Rates

Explained

Kevin DonovanCPA, EA, MSPA, FCAPinnacle Plan Design

www.pinnacle-plan.com

2

The information contained in this presentation is accurate as of August 2015

3

Agenda

Ideal Cash Balance Candidates Cash Balance Overview Cash Balance Possibilities Cash Balance Plan Contributions Interest Crediting Rates Investing Cash Balance Plan Assets Tools for Reviews Fees and Disclosures Next Steps

4

Ideal Cash Balance Candidates

Highly compensated owners Owners looking to put more $$ away Low Employee/Owner ratio Owners older than the employees (on

average) Non-cyclical industry Prime cash balance candidates include

professional groups:

DRs Lawyers

CPAs Dentists Financial

Advisors

5 Cash Balance Overview

6

Cash Balance Overview

Cash balance plans:

A defined benefit (DB) plan

Permanent in nature with required contributions by the employer

Provides employees with an account value versus periodic payments of a traditional DB plan

Significant contribution limits over and above defined contribution (DC) plan limits

7

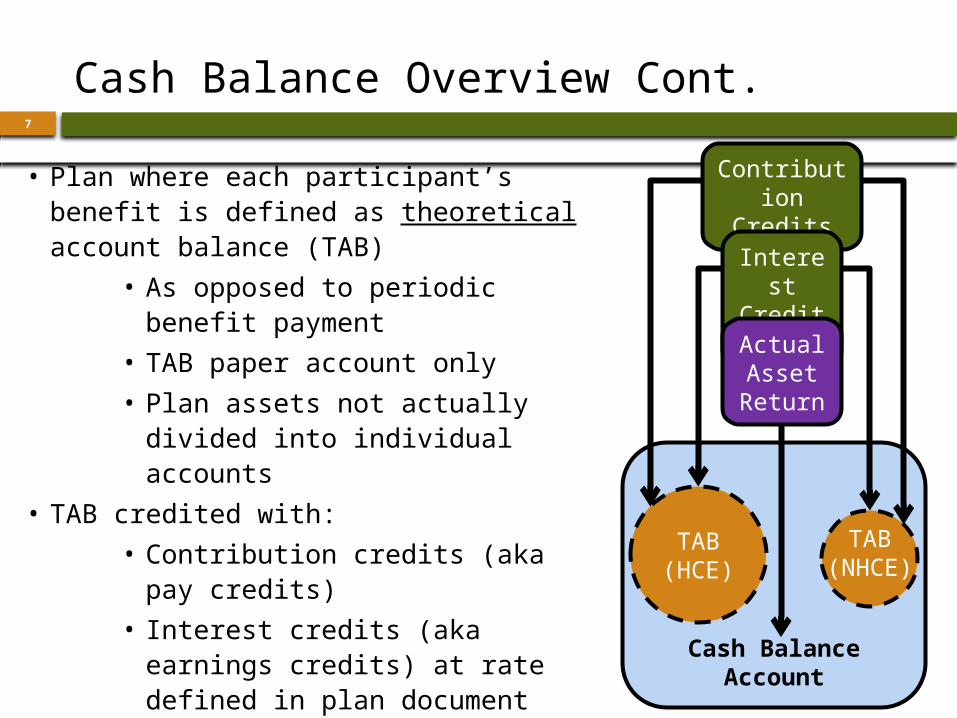

Cash Balance Overview Cont.

• Plan where each participant’s benefit is defined as theoretical account balance (TAB)

• As opposed to periodic benefit payment

• TAB paper account only

• Plan assets not actually divided into individual accounts

• TAB credited with:

• Contribution credits (aka pay credits)

• Interest credits (aka earnings credits) at rate defined in plan document

• It is a DB plan: benefit not based on actual asset return

Cash Balance Account

TAB(HCE)

Contribution Credits

Interest Credits

Actual Asset Return

TAB(NHCE)

8

PPA and Cash Balance Plans

Upon distribution, amount payable not less than cumulative pay credits Preservation of Capital Rule

Lump sum = account balance No more “whipsaw” resulting from projecting forward

at a high interest crediting rate and discounting back at a low statutory rate

Fully vested after three years

Similarly situated rule allows age discrimination to be measured based on TAB instead of life annuity

9

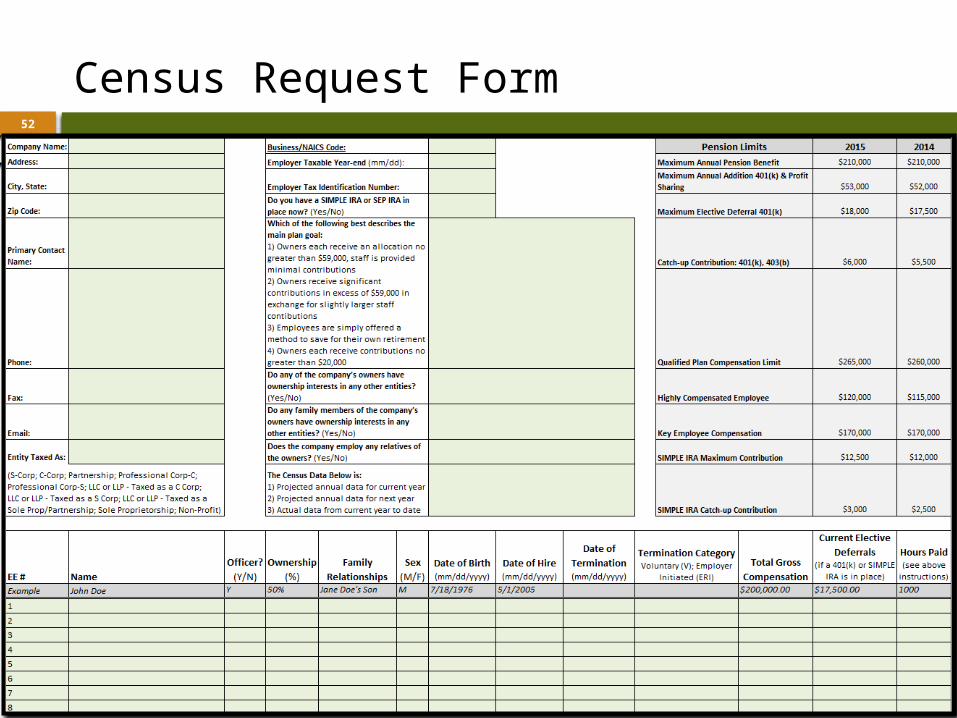

Cash Balance Plan Retirement Benefit

Maximum benefit payable to any individual lesser of 100% of average compensation

Reduced for years of service less than 10 Dollar limit ($210,000 for years ending in 2015)

Reduced for years of participation less than 10 Reduced if commenced before age 62 Increased if commenced post age 65

Payable as straight life annuity (SLA)

Adjusted if paid other than as SLA With small plans, distributions are almost always taken as

lump sums Maximum lump sum is approximately $2.6 million at age

62, assuming 10 years of plan participation

10

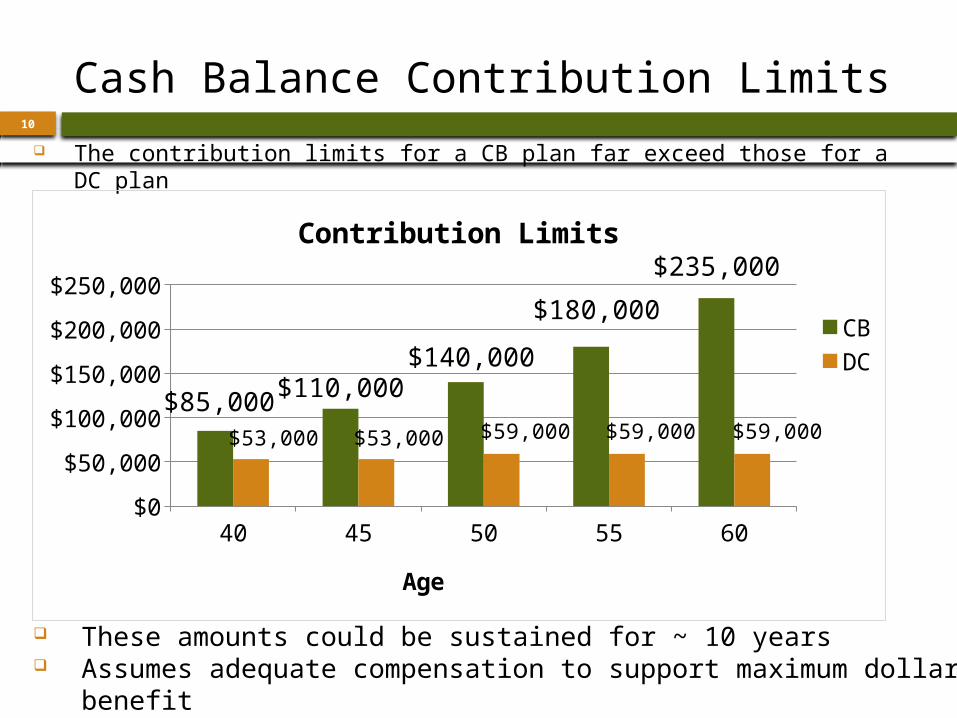

Cash Balance Contribution Limits

The contribution limits for a CB plan far exceed those for a DC plan

40 45 50 55 60$0

$50,000

$100,000

$150,000

$200,000

$250,000

$85,000$110,000

$140,000

$180,000

$235,000

$53,000 $53,000 $59,000 $59,000 $59,000

Contribution Limits

CBDC

Age

These amounts could be sustained for ~ 10 years Assumes adequate compensation to support maximum dollar

benefit

11

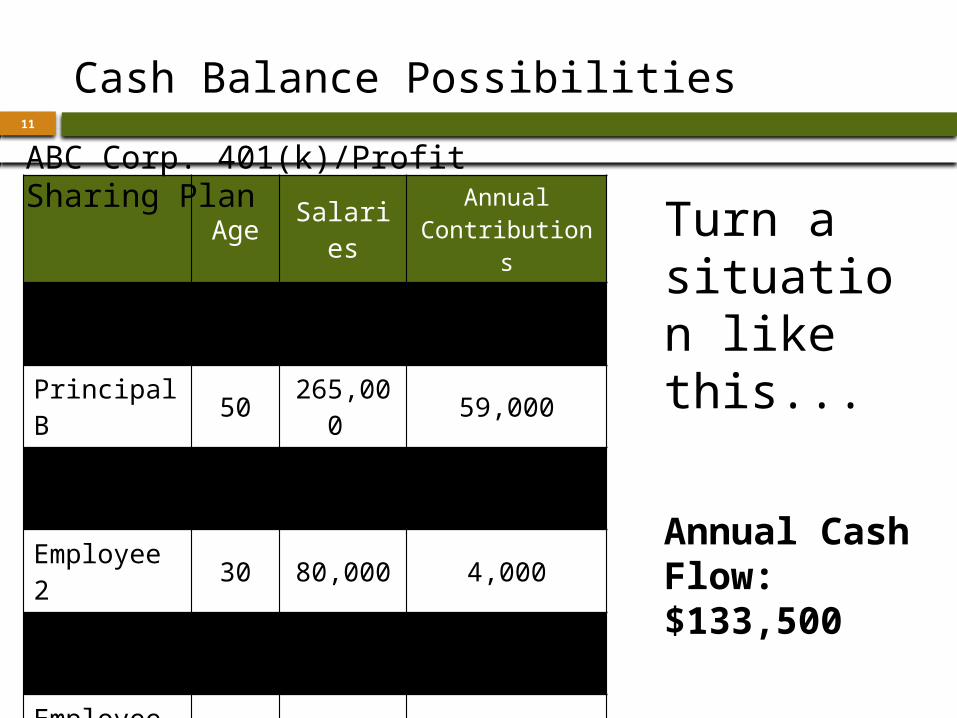

Cash Balance Possibilities

Age Salaries AnnualContributions

Principal A 56265,00

0 59,000

Principal B 50265,00

0 59,000

Employee 1 40

100,000 5,000

Employee 2 30 80,000 4,000

Employee 3 28 70,000 3,500

Employee 4 25 60,000 3,000

Total840,00

0 133,500

Turn a situation like this...

Annual Cash Flow:$133,500

ABC Corp. 401(k)/Profit Sharing Plan

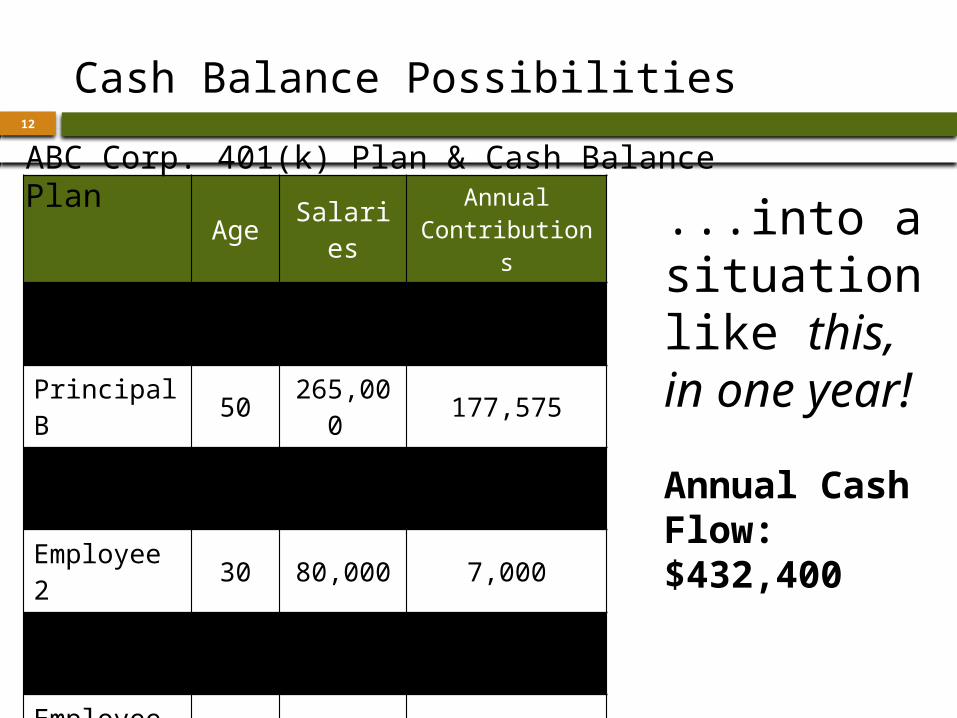

12

Cash Balance Possibilities

Age Salaries AnnualContributions

Principal A 56265,00

0 227,575

Principal B 50265,00

0 177,575

Employee 1 40

100,000 8,500

Employee 2 30 80,000 7,000

Employee 3 28 70,000 6,250

Employee 4 25 60,000 5,500

Total840,00

0 432,400

...into a situation like this, in one year!

Annual Cash Flow:$432,400

ABC Corp. 401(k) Plan & Cash Balance Plan

13 Cash Balance Case Study

14

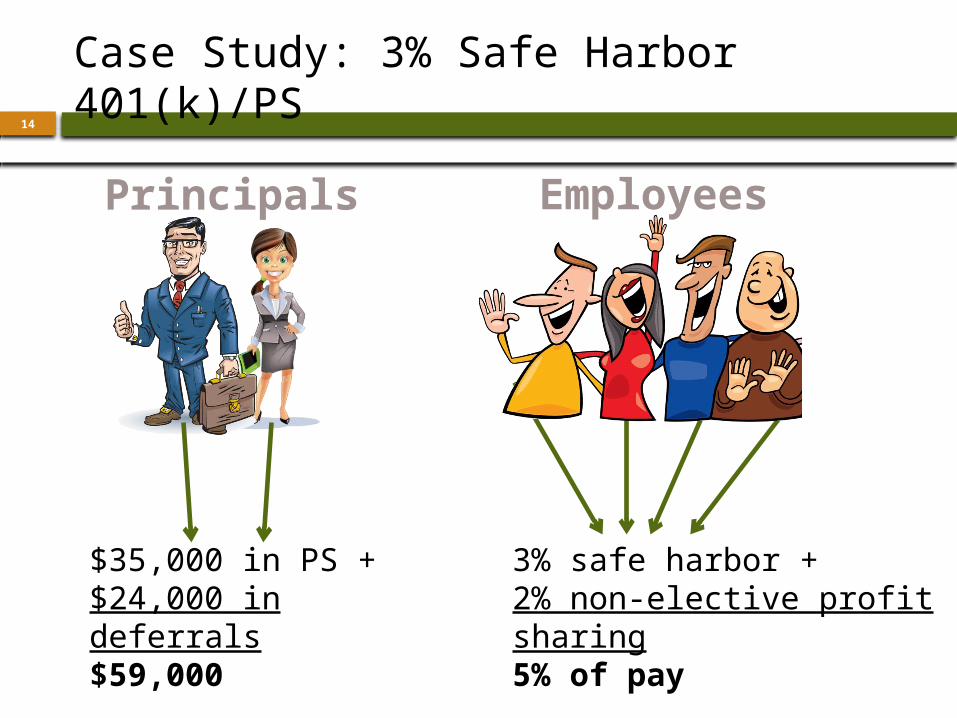

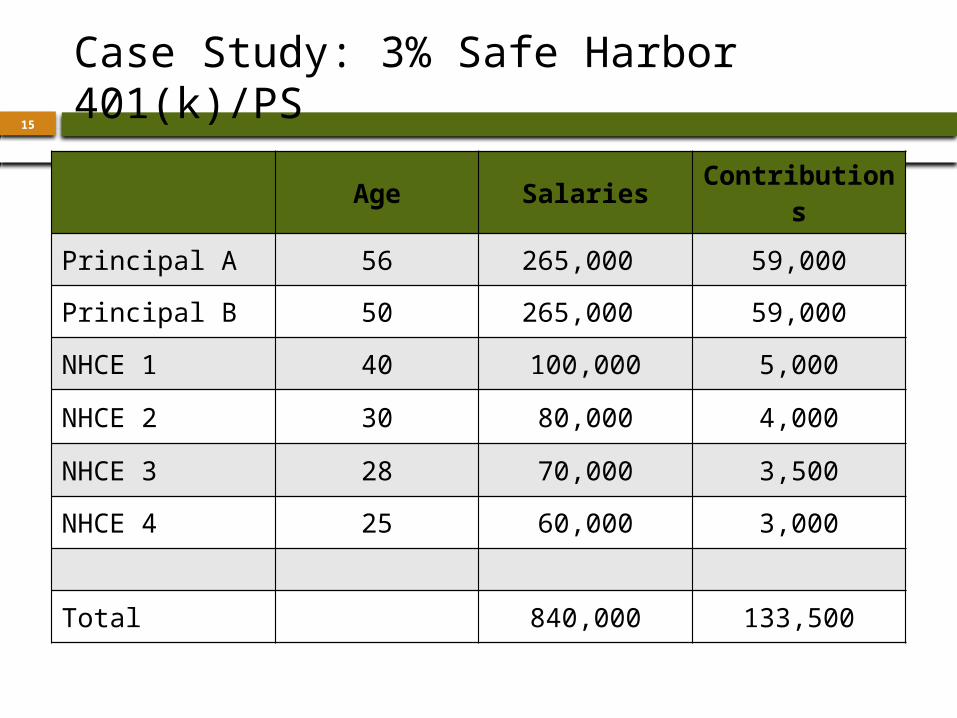

Case Study: 3% Safe Harbor 401(k)/PS

Principals

$35,000 in PS +$24,000 in deferrals$59,000

Employees

3% safe harbor +2% non-elective profit sharing5% of pay

15

Age SalariesContribution

s

Principal A 56 265,000 59,000

Principal B 50 265,000 59,000

NHCE 1 40 100,000 5,000

NHCE 2 30 80,000 4,000

NHCE 3 28 70,000 3,500

NHCE 4 25 60,000 3,000

Total 840,000 133,500

Case Study: 3% Safe Harbor 401(k)/PS

16

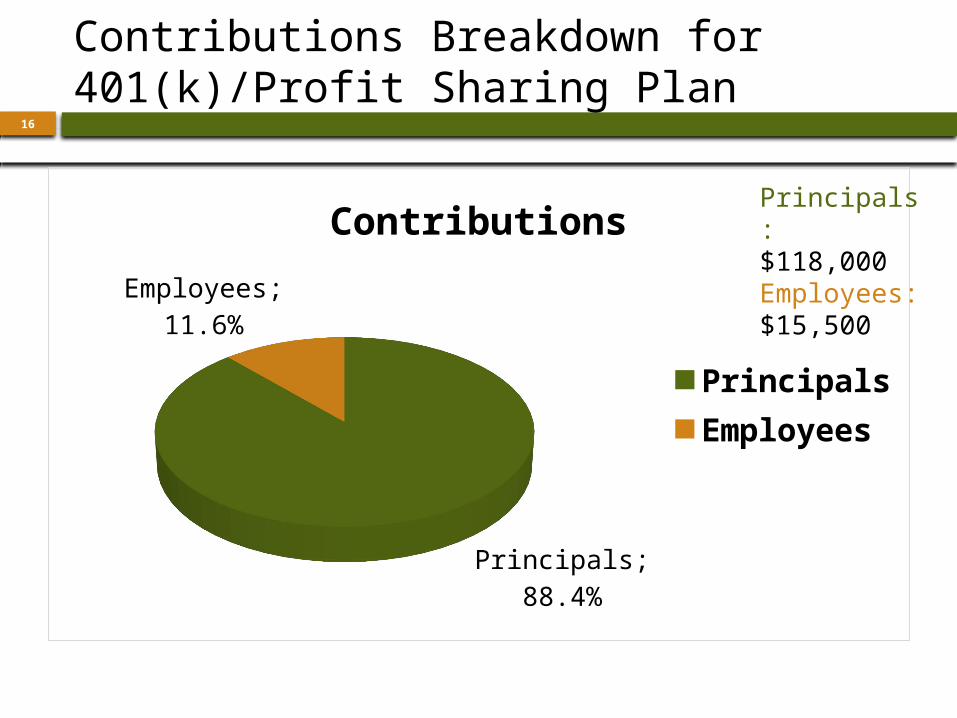

Contributions Breakdown for 401(k)/Profit Sharing Plan

Principals; 88.4%

Employees; 11.6%

Contributions

PrincipalsEmployees

Principals:$118,000Employees:$15,500

17

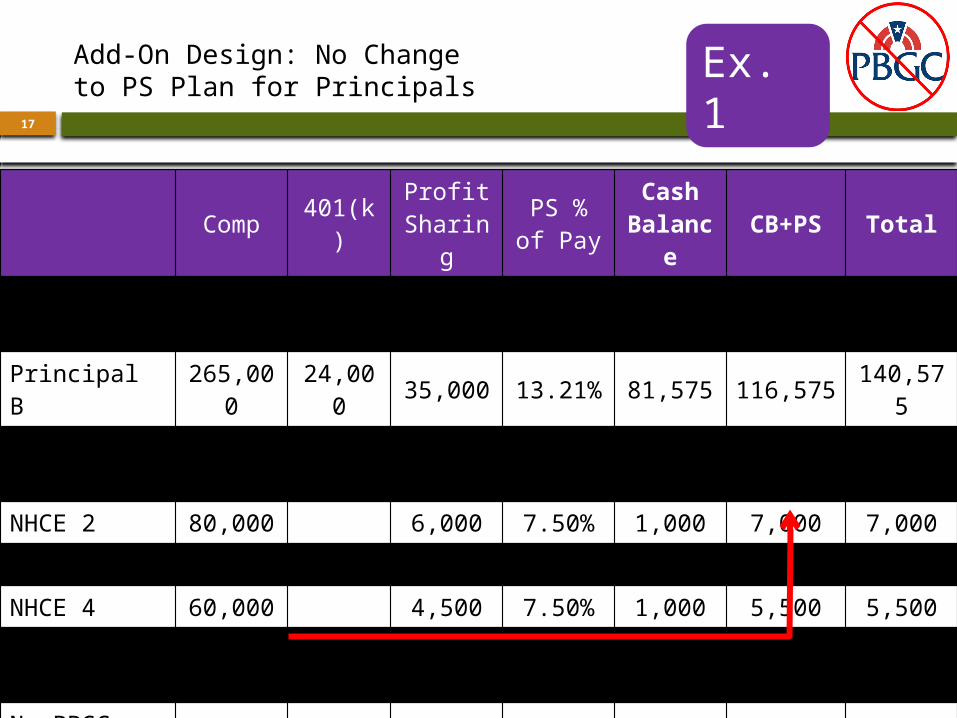

Add-On Design: No Change to PS Plan for Principals

Comp 401(k) Profit Sharing

PS % of Pay

Cash Balanc

eCB+PS Total

Principal A 265,000 24,000 35,000 13.21% 81,575 116,575 140,57

5

Principal B 265,000 24,000 35,000 13.21% 81,575 116,575 140,57

5

NHCE 1 100,000 7,500 7.50% 1,000 8,500 8,500

NHCE 2 80,000 6,000 7.50% 1,000 7,000 7,000

NHCE 3 70,000 5,250 7.50% 1,000 6,250 6,250

NHCE 4 60,000 4,500 7.50% 1,000 5,500 5,500

Totals 840,000 48,000 93,250 167,15

0 260,400 308,400

No PBGC Coverage: CB+PS ≤ 31%

x 31%

CB+PS Limit 260,400

Ex. 1

18

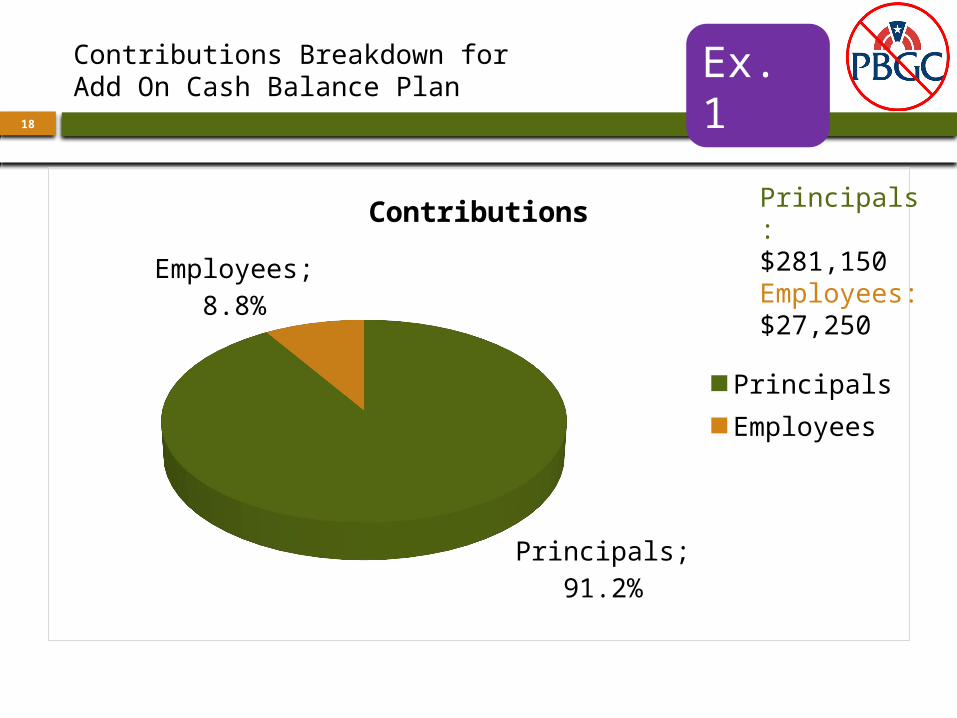

Principals; 91.2%

Employees; 8.8%

Contributions

PrincipalsEmployees

Principals:$281,150Employees:$27,250

Contributions Breakdown for Add On Cash Balance Plan

Ex. 1

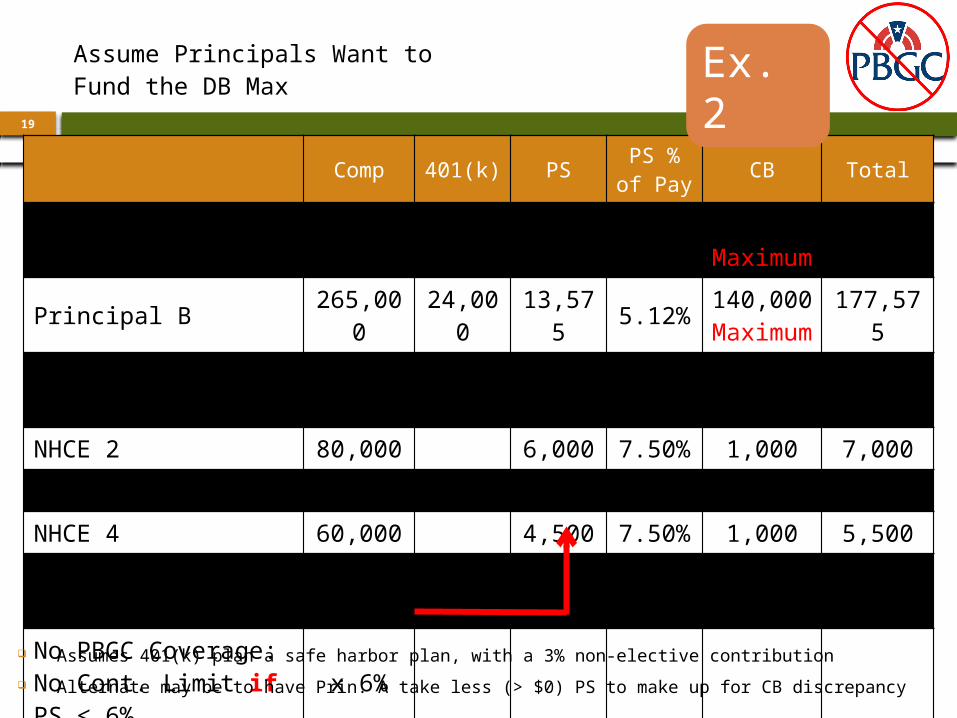

19

Comp 401(k) PS PS % of Pay CB Total

Principal A 265,000

24,000

13,575 5.12% 190,000

Maximum227,57

5

Principal B 265,000

24,000

13,575 5.12% 140,000

Maximum177,57

5

NHCE 1 100,000 7,500 7.50% 1,000 8,500

NHCE 2 80,000 6,000 7.50% 1,000 7,000

NHCE 3 70,000 5,250 7.50% 1,000 6,250

NHCE 4 60,000 4,500 7.50% 1,000 5,500

Totals 840,000

48,000

50,400 334,000 432,40

0

No PBGC Coverage: No Cont. Limit if PS ≤ 6%

x 6%

PS Limit 50,400 Assumes 401(k) plan a safe harbor plan, with a 3% non-elective contribution Alternate may be to have Prin. A take less (> $0) PS to make up for CB discrepancy

Assume Principals Want to Fund the DB Max

Ex. 2

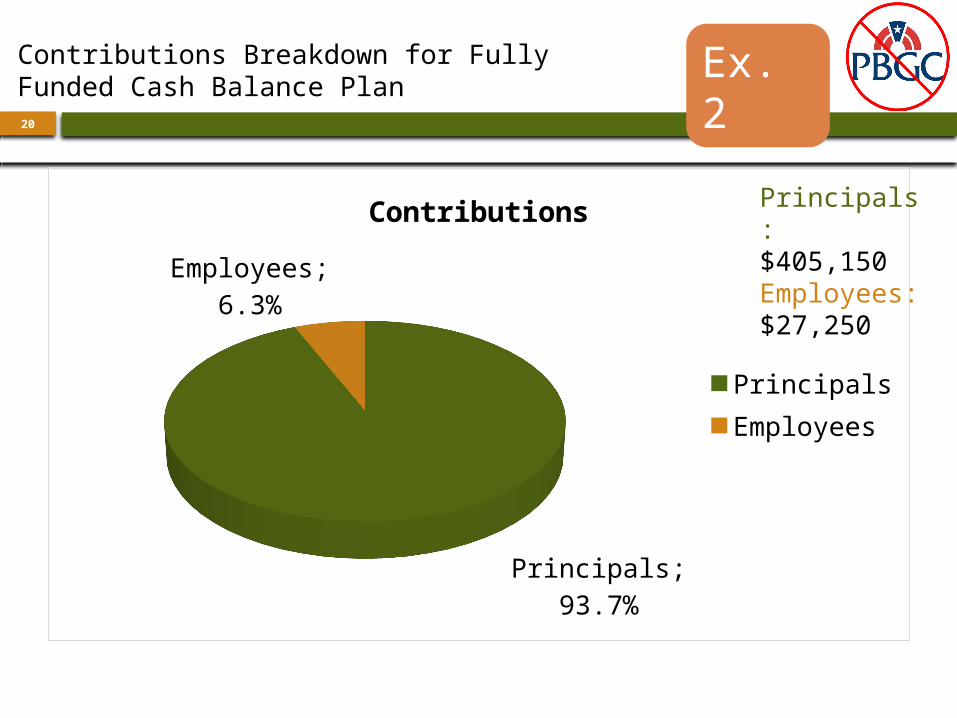

20

Principals; 93.7%

Employees; 6.3%

Contributions

PrincipalsEmployees

Principals:$405,150Employees:$27,250

Contributions Breakdown for Fully Funded Cash Balance Plan

Ex. 2

21 Cash Balance Plan Contributions

22

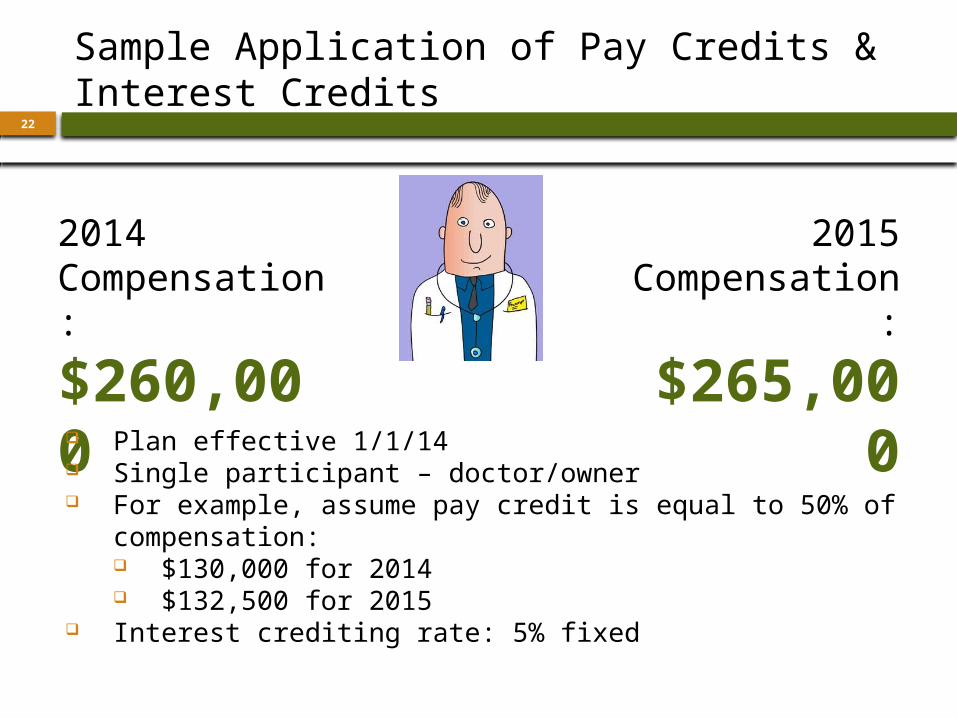

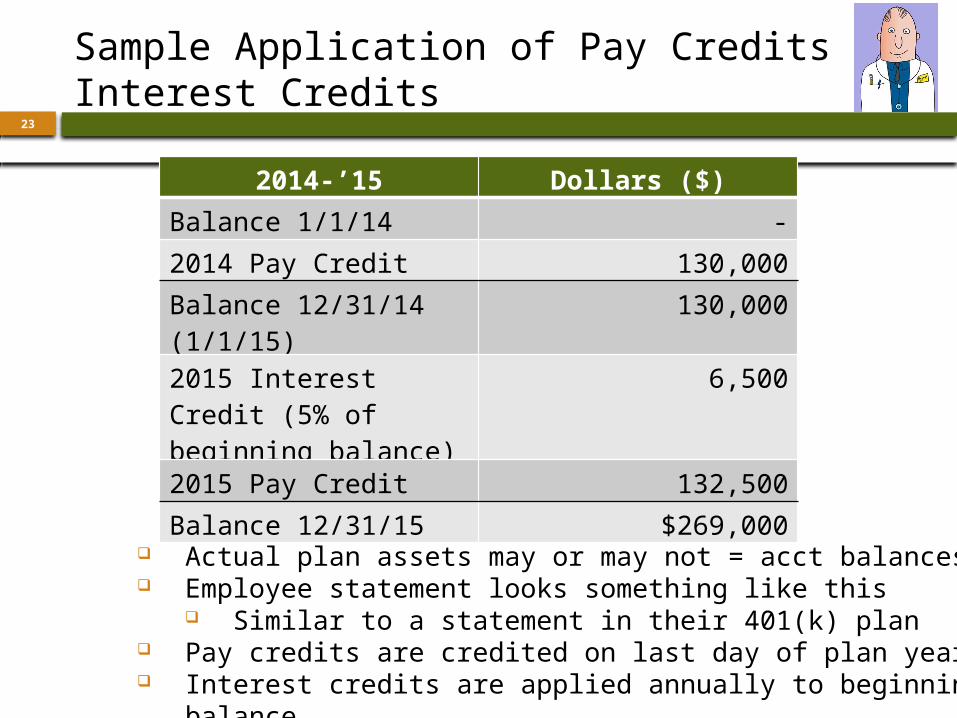

Sample Application of Pay Credits & Interest Credits

2014 Compensation:

$260,000

2015 Compensatio

n:

$265,000 Plan effective 1/1/14

Single participant – doctor/owner For example, assume pay credit is equal to 50% of

compensation: $130,000 for 2014 $132,500 for 2015

Interest crediting rate: 5% fixed

23

Sample Application of Pay Credits & Interest Credits

Actual plan assets may or may not = acct balances Employee statement looks something like this

Similar to a statement in their 401(k) plan Pay credits are credited on last day of plan year Interest credits are applied annually to beginning balance

2014-’15 Dollars ($)

Balance 1/1/14 -

2014 Pay Credit 130,000

Balance 12/31/14 (1/1/15)

130,000

2015 Interest Credit (5% of beginning balance)

6,500

2015 Pay Credit 132,500

Balance 12/31/15 $269,000

24

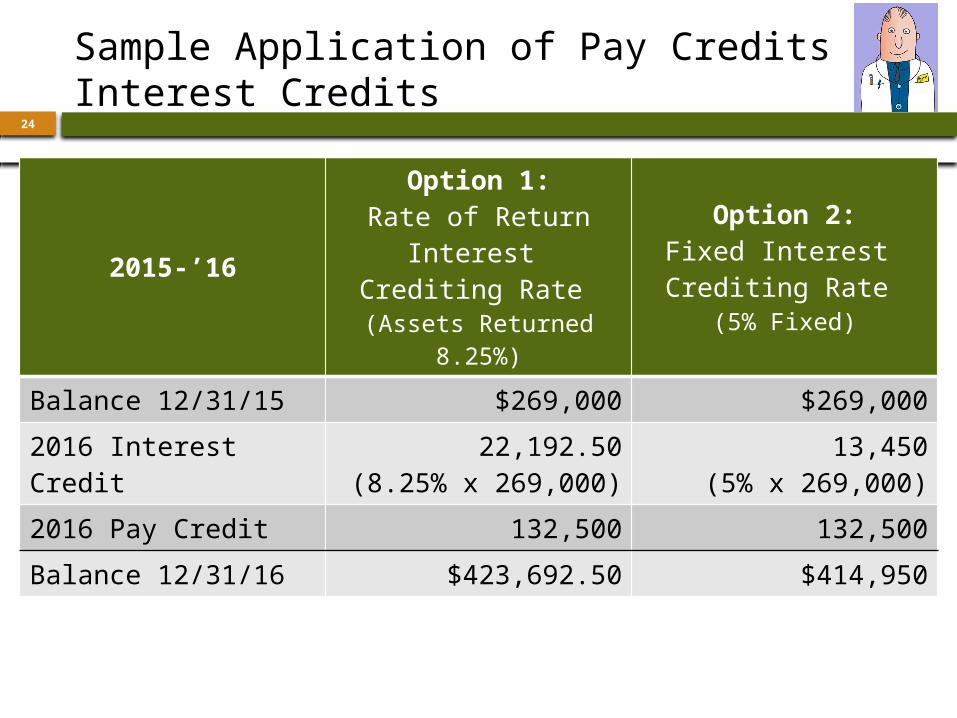

Sample Application of Pay Credits & Interest Credits

2015-’16

Option 1:Rate of Return Interest

Crediting Rate (Assets Returned 8.25%)

Option 2:Fixed Interest Crediting Rate

(5% Fixed)

Balance 12/31/15 $269,000 $269,000

2016 Interest Credit 22,192.50(8.25% x 269,000)

13,450(5% x 269,000)

2016 Pay Credit 132,500 132,500

Balance 12/31/16 $423,692.50 $414,950

25

Interest Credits

Age Discrimination started with interest credits IBM District court: cash balance plans

discriminate Younger participants have more interest credits at NRA

Appeals Courts & Congress: no age-discrimination

But what if interest credits really high, like 15%? At some point, higher interest credits become

discriminatory against older participants

26

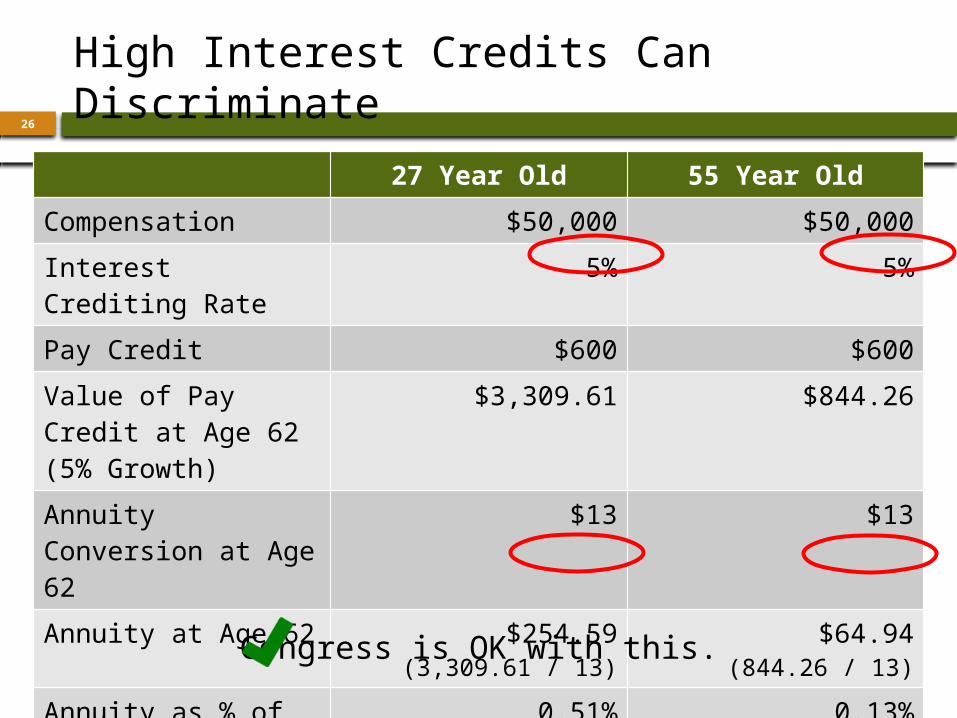

High Interest Credits Can Discriminate

27 Year Old 55 Year Old

Compensation $50,000 $50,000

Interest Crediting Rate 5% 5%

Pay Credit $600 $600

Value of Pay Credit at Age 62 (5% Growth)

$3,309.61 $844.26

Annuity Conversion at Age 62

$13 $13

Annuity at Age 62 $254.59(3,309.61 / 13)

$64.94(844.26 / 13)

Annuity as % of Compensation

0.51%(254.59 / 50,000)

0.13%(64.94 / 50,000)

Congress is OK with this.

27

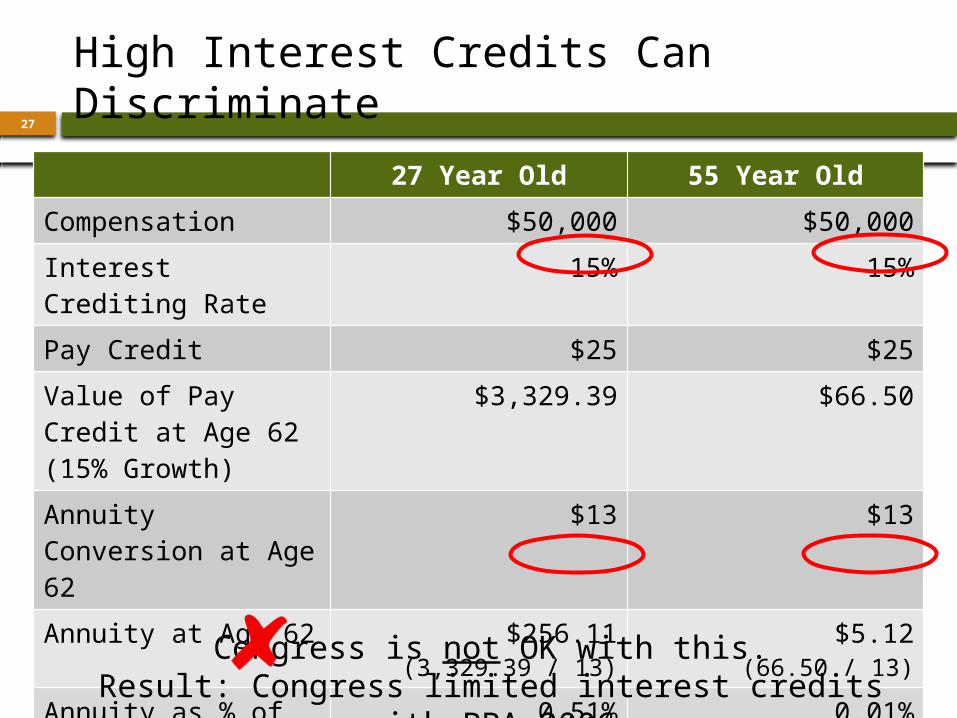

High Interest Credits Can Discriminate

27 Year Old 55 Year Old

Compensation $50,000 $50,000

Interest Crediting Rate 15% 15%

Pay Credit $25 $25

Value of Pay Credit at Age 62 (15% Growth)

$3,329.39 $66.50

Annuity Conversion at Age 62

$13 $13

Annuity at Age 62 $256.11(3,329.39 / 13)

$5.12(66.50 / 13)

Annuity as % of Compensation

0.51%(256.11 / 50,000)

0.01%(5.12 / 50,000)

Congress is not OK with this.Result: Congress limited interest credits with PPA

2006

28 Interest Crediting Rates

29

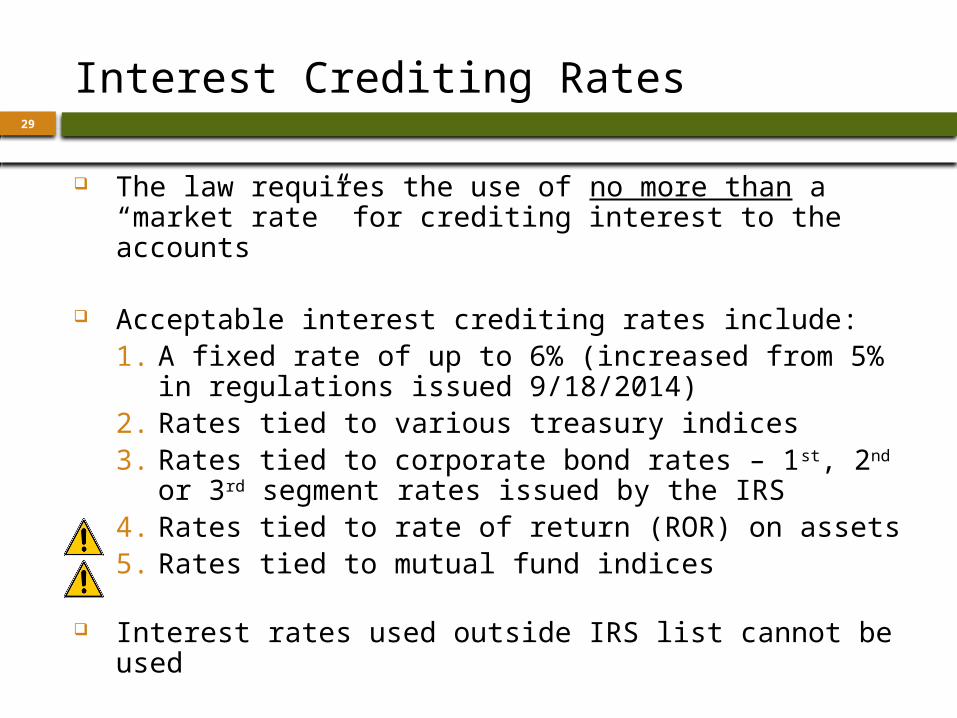

Interest Crediting Rates

The law requires the use of no more than a “market rate” for crediting interest to the accounts

Acceptable interest crediting rates include:1. A fixed rate of up to 6% (increased from 5% in

regulations issued 9/18/2014)2. Rates tied to various treasury indices3. Rates tied to corporate bond rates – 1st, 2nd or

3rd segment rates issued by the IRS4. Rates tied to rate of return (ROR) on assets5. Rates tied to mutual fund indices

Interest rates used outside IRS list cannot be used

30

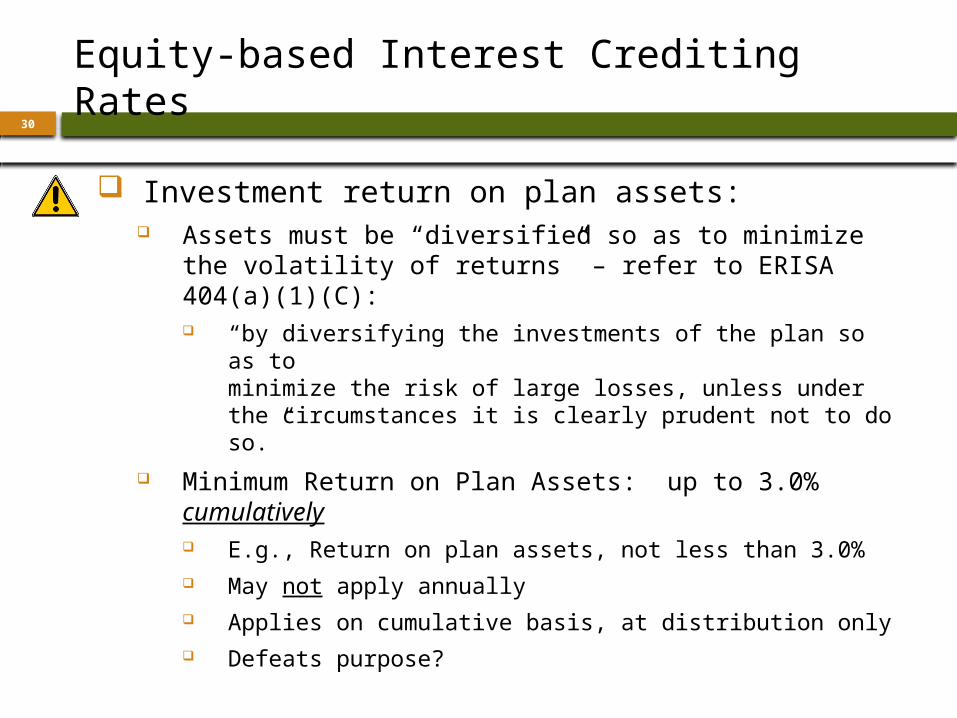

Equity-based Interest Crediting Rates

Investment return on plan assets: Assets must be “diversified so as to minimize

the volatility of returns” – refer to ERISA 404(a)(1)(C): “by diversifying the investments of the plan so as to

minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so.”

Minimum Return on Plan Assets: up to 3.0% cumulatively E.g., Return on plan assets, not less than 3.0% May not apply annually Applies on cumulative basis, at distribution only Defeats purpose?

31

Equity-based Interest Crediting Rates

Investment return on a mutual fund: Must be broad-based Not significantly more volatile than US markets E.g., no industry sector Minimum return on mutual funds:

Same as for Return on Plan Assets Again, likely defeats purpose

32

Interest Crediting Rates

Can Investment Direction be provided by employee? Suggested by IRS in 2010 regulations

Preamble to 2014 regulations: “It is possible that the Treasury Department

and the IRS will conclude that such plan designs are not permitted.”

This follows 4 pages of criticism of investment direction.

I take this as “No.” But could be wrong…

33

Crediting ROR or Mutual Fund

Why use rate of return or mutual fund? Goal is generally to invest assets to mirror

interest crediting rate Using ROR makes this goal easier to achieve Much of the investment risk is shifted to

employees Losses do not create a funding shortfall

Goal is to deposit pay credits and have interest credits equal actual earnings

34

Crediting ROR or Mutual Fund

Why not to use rate of return or mutual fund? Benefit Limits Discrimination testing Coverage testing Preservation of Capital Rule: requires

ultimate payout to be not less than cumulative pay credits So early losses could cause problem

35

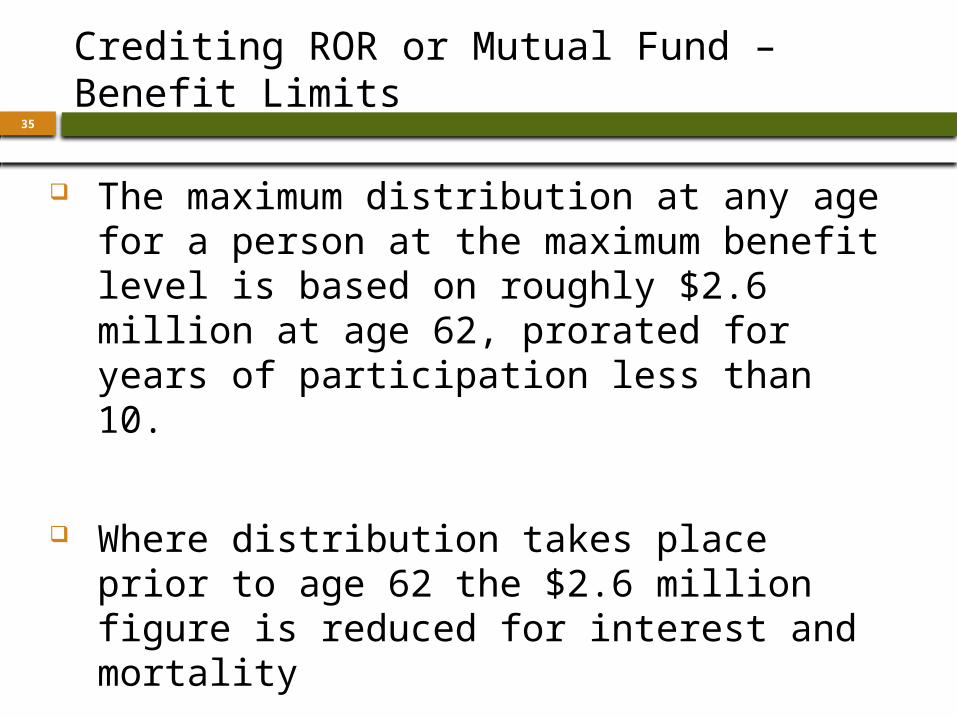

Crediting ROR or Mutual Fund – Benefit Limits

The maximum distribution at any age for a person at the maximum benefit level is based on roughly $2.6 million at age 62, prorated for years of participation less than 10.

Where distribution takes place prior to age 62 the $2.6 million figure is reduced for interest and mortality

36

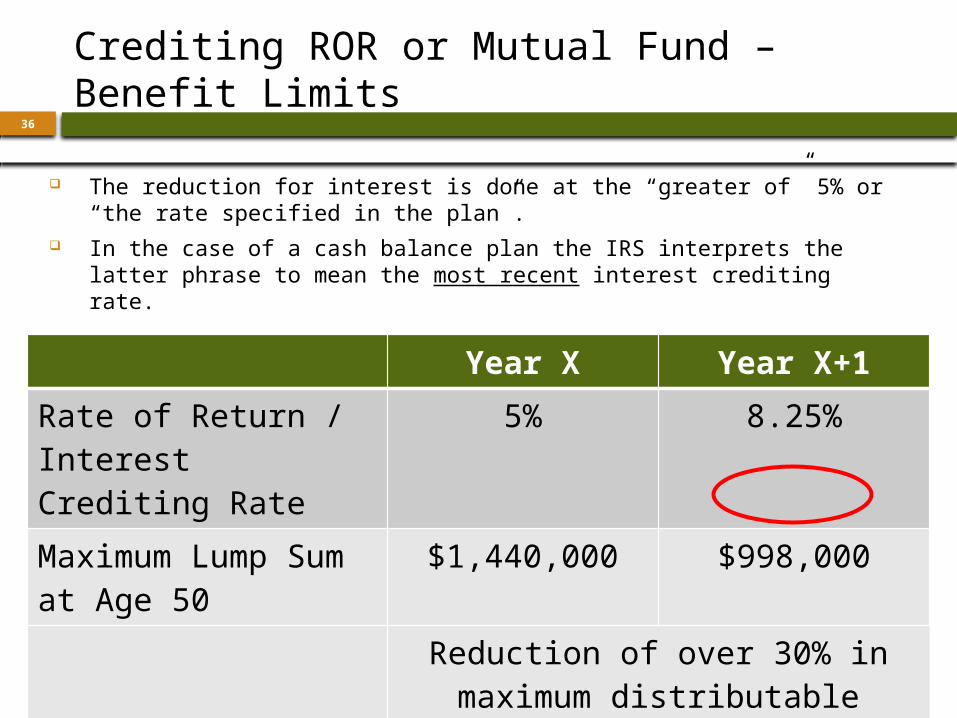

Crediting ROR or Mutual Fund – Benefit Limits

The reduction for interest is done at the “greater of” 5% or “the rate specified in the plan”.

In the case of a cash balance plan the IRS interprets the latter phrase to mean the most recent interest crediting rate.

Year X Year X+1

Rate of Return / Interest Crediting Rate

5% 8.25%

Maximum Lump Sum at Age 50

$1,440,000 $998,000

Reduction of over 30% in maximum distributable amount!

37

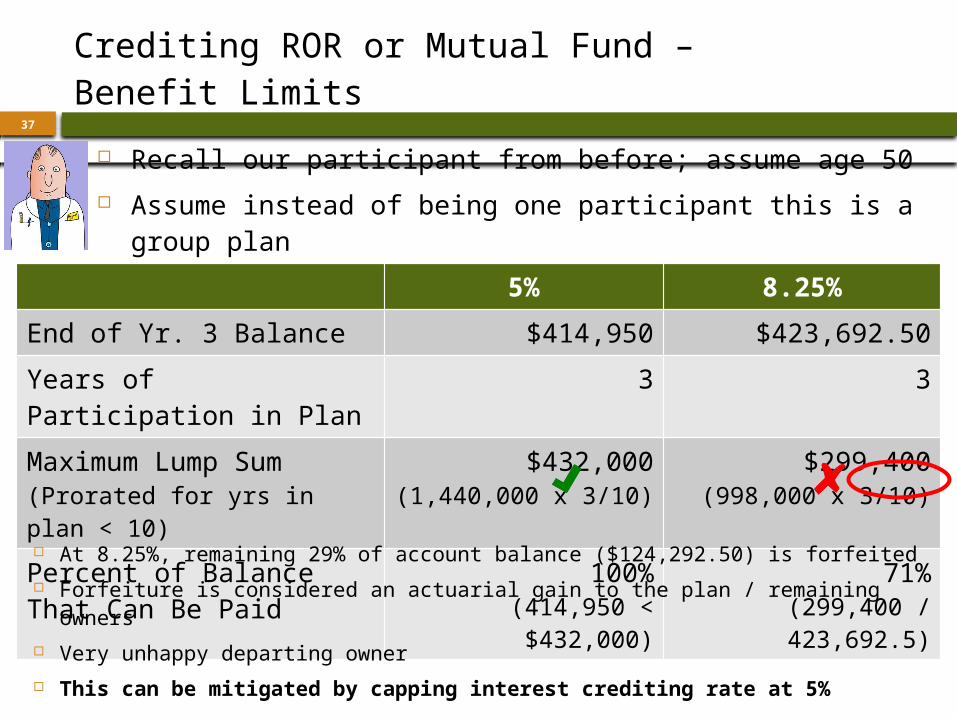

Crediting ROR or Mutual Fund – Benefit Limits

Recall our participant from before; assume age 50 Assume instead of being one participant this is a group

plan Wants to leave practice and take distribution5% 8.25%

End of Yr. 3 Balance $414,950 $423,692.50

Years of Participation in Plan 3 3

Maximum Lump Sum (Prorated for yrs in plan < 10)

$432,000(1,440,000 x 3/10)

$299,400(998,000 x 3/10)

Percent of Balance That Can Be Paid

100%(414,950 < $432,000)

71%(299,400 / 423,692.5)

At 8.25%, remaining 29% of account balance ($124,292.50) is forfeited Forfeiture is considered an actuarial gain to the plan / remaining owners Very unhappy departing owner This can be mitigated by capping interest crediting rate at 5%

38

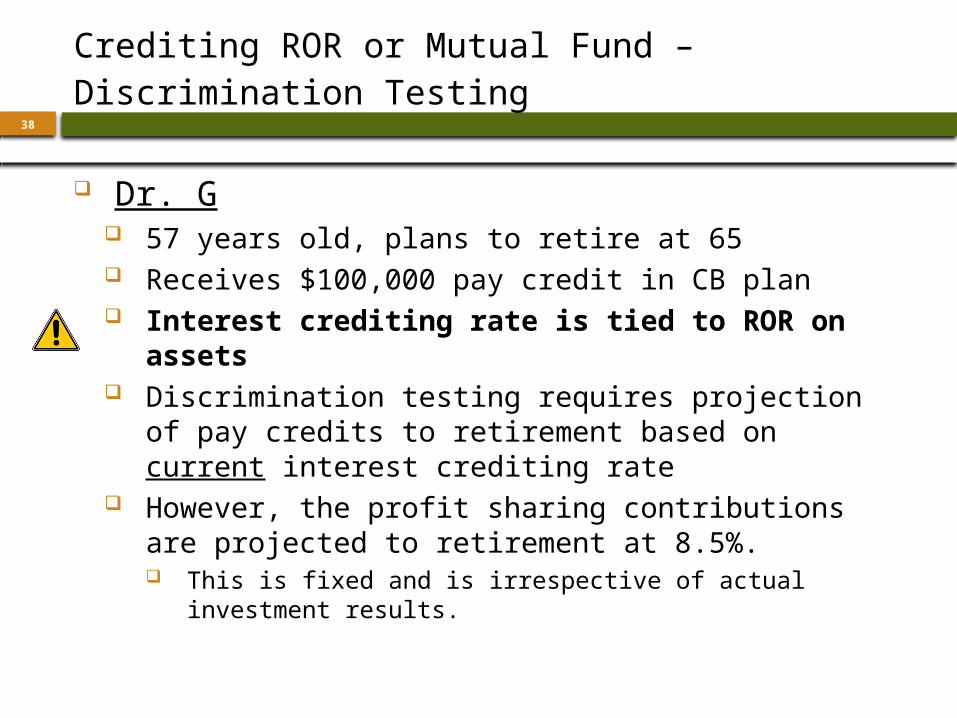

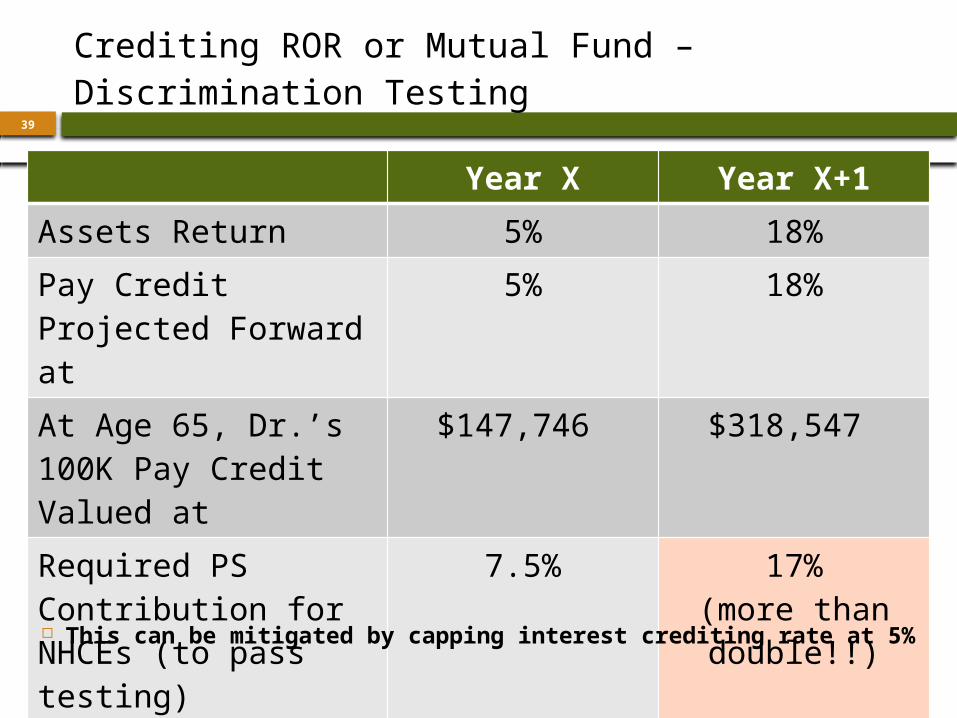

Crediting ROR or Mutual Fund – Discrimination Testing

Dr. G 57 years old, plans to retire at 65 Receives $100,000 pay credit in CB plan Interest crediting rate is tied to ROR on

assets Discrimination testing requires projection of

pay credits to retirement based on current interest crediting rate

However, the profit sharing contributions are projected to retirement at 8.5%. This is fixed and is irrespective of actual

investment results.

39

Crediting ROR or Mutual Fund – Discrimination Testing

Year X Year X+1

Assets Return 5% 18%

Pay Credit Projected Forward at

5% 18%

At Age 65, Dr.’s 100K Pay Credit Valued at

$147,746 $318,547

Required PS Contribution for NHCEs (to pass testing)

7.5% 17%(more than double!!)

This can be mitigated by capping interest crediting rate at 5%

40

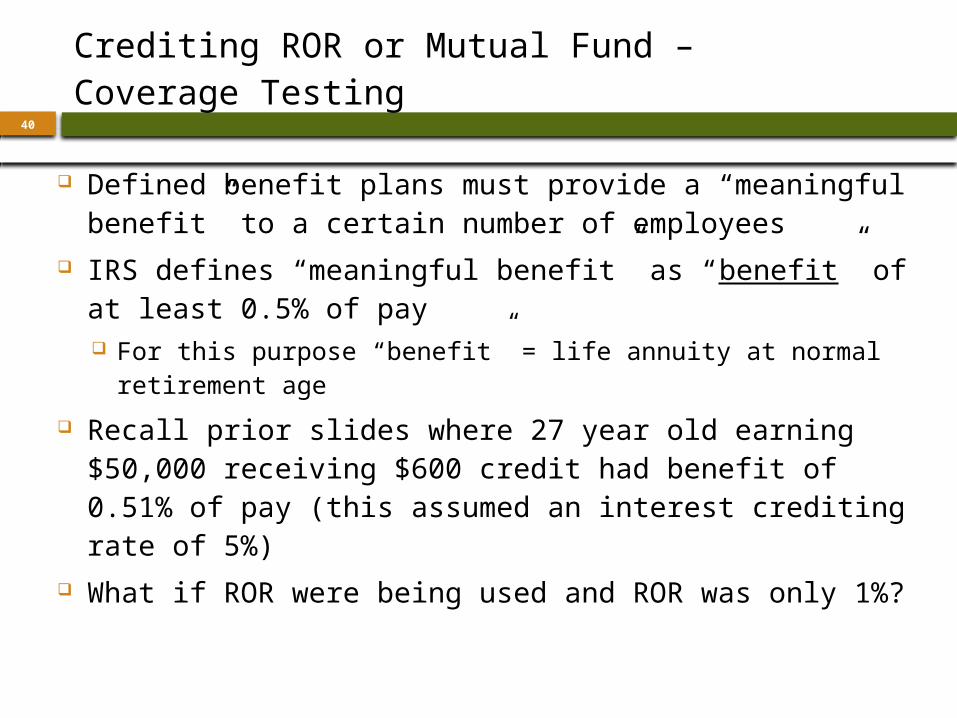

Crediting ROR or Mutual Fund – Coverage Testing

Defined benefit plans must provide a “meaningful benefit” to a certain number of employees

IRS defines “meaningful benefit” as “benefit” of at least 0.5% of pay For this purpose “benefit” = life annuity at normal

retirement age Recall prior slides where 27 year old earning $50,000

receiving $600 credit had benefit of 0.51% of pay (this assumed an interest crediting rate of 5%)

What if ROR were being used and ROR was only 1%?

41

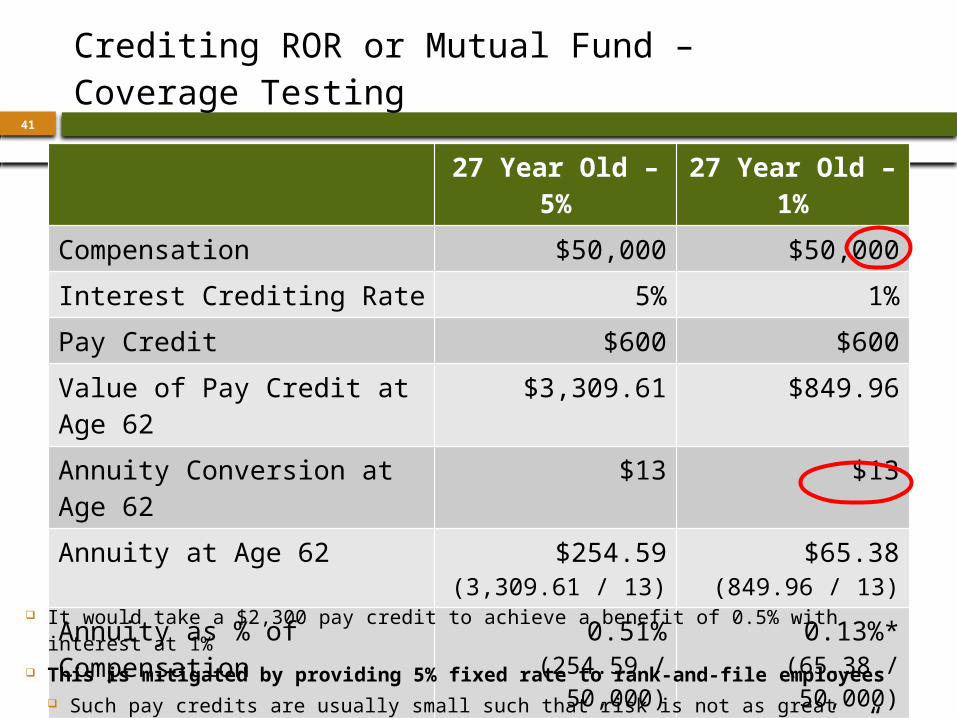

Crediting ROR or Mutual Fund – Coverage Testing

27 Year Old – 5% 27 Year Old – 1%

Compensation $50,000 $50,000

Interest Crediting Rate 5% 1%

Pay Credit $600 $600

Value of Pay Credit at Age 62 $3,309.61 $849.96

Annuity Conversion at Age 62 $13 $13

Annuity at Age 62 $254.59(3,309.61 / 13)

$65.38(849.96 / 13)

Annuity as % of Compensation 0.51%(254.59 / 50,000)

0.13%*(65.38 / 50,000)

* At 1%, the annuity is not a “meaningful benefit” (0.13% < 0.5%)

It would take a $2,300 pay credit to achieve a benefit of 0.5% with interest at 1% This is mitigated by providing 5% fixed rate to rank-and-file employees

Such pay credits are usually small such that risk is not as great

42

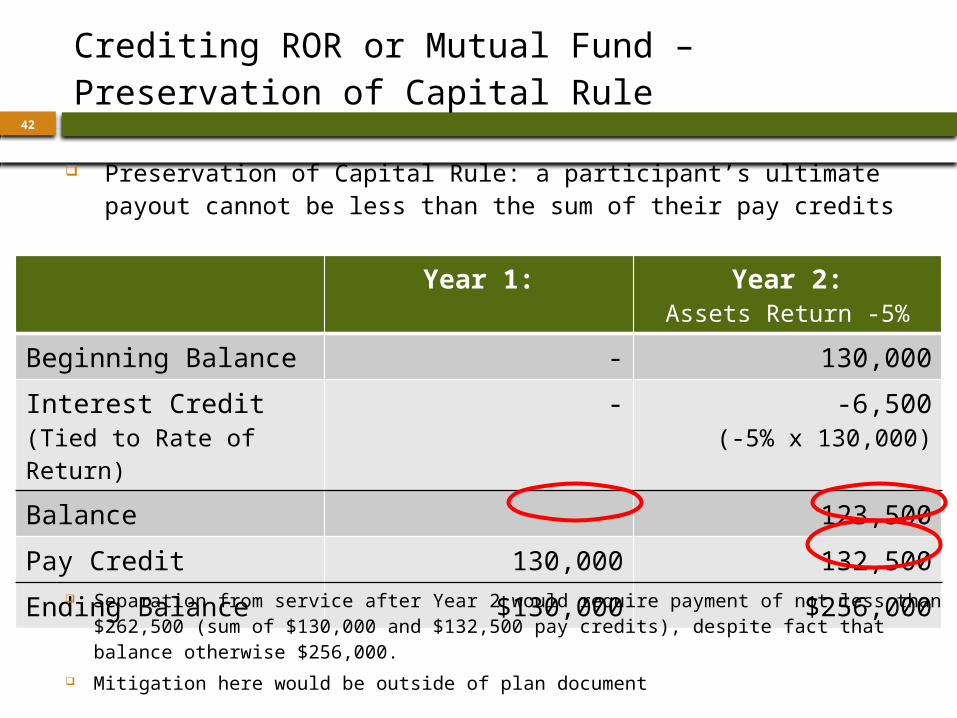

Crediting ROR or Mutual Fund – Preservation of Capital Rule

Year 1: Year 2:Assets Return -5%

Beginning Balance - 130,000

Interest Credit (Tied to Rate of Return)

- -6,500(-5% x 130,000)

Balance - 123,500

Pay Credit 130,000 132,500

Ending Balance $130,000 $256,000

Preservation of Capital Rule: a participant’s ultimate payout cannot be less than the sum of their pay credits

Separation from service after Year 2 would require payment of not less than $262,500 (sum of $130,000 and $132,500 pay credits), despite fact that balance otherwise $256,000.

Mitigation here would be outside of plan document

43

Summary of Interest Crediting Rates

The law requires the use of no more than a “market rate” for crediting interest to cash balance accounts

The interest crediting rate can be fixed or variable Care must be taken when tying to ROR on plan assets or

mutual fund indices Consider capping when crediting such rates

Mitigates issues with respect to reduced maximum benefits Can minimize fluctuation from year to year in test results

Consider fixed interest crediting rate for lower benefiting employees to alleviate “meaningful benefit” concerns

Interest credits must be applied no less often than annually Annual certainly the norm, at least in small plan market

44 Investing Cash Balance Plan Assets

45

Follow the Rate

Actuary and plan sponsor, with advisor input, select an appropriate Interest Crediting Rate when the plan is established

How do you invest to meet the stated goal? Allocation and portfolio to meet rate over time Avoid volatility

The goal is to meet the interest crediting rate over a period of time.

46

Cash Balance Investments

Cash Balance Investments Are: Pooled Trustee-Directed Guaranteed

Pay credit and interest credit are required for all eligible participants annually

47

Investment Policy Statement

ERISA does not explicitly require a written governance process or IPS, however most feel it is best practice

If you provide an IPS, follow it.

IPS includes Investments allowed and disallowed Risk and liquidity profile Investment monitoring and replacement process Roles and responsibilities of responsible parties Selecting and monitoring investment

professionals

48

Fees and Disclosures

Direct participant expenses cannot be charged to the employee

e.g. Termination fees or distribution fees

No ERISA or PARA buckets in a DB plan

Fee disclosures not required for plan participants

49

Investment Options & Models

Use investment(s) or a model that meets the return objective

Single Cash Balance Funds Single manager fund Fund of funds

Selection and monitoring meets the IPS

Choice of pooled brokerage account or eligible recordkeeper account

50

Tools for Reviews

Fi360 Individual funds Models

Morningstar Reports

Zephyr Reports

51 Next Steps

Retirement Plan Design▲Administration▲Consulting▲Actuarial Services

www.pinnacle-plan.com

53

Beth A. Cooper, CRPS®Strategic Development [email protected](520) 906-4821