Embed Size (px)

Citation preview

Congressional Budget Office

Presentation at Macroeconomic Advisers’ 25th Annual Washington Policy Seminar

Keith Hall Director

CBO’s Updated Projections for the Federal Budget and the Economy

September 9, 2015

CO NGRES S IO NA L BUDGE T O F F IC E 1

Outlook for the Budget

CO NGRES S IO NA L BUDGE T O F F IC E 2

Total Deficits or Surpluses

CO NGRES S IO NA L BUDGE T O F F IC E 3

Federal Debt Held by the Public

CO NGRES S IO NA L BUDGE T O F F IC E 4

Total Revenues

CO NGRES S IO NA L BUDGE T O F F IC E 5

Revenues, by Major Source

CO NGRES S IO NA L BUDGE T O F F IC E 6

Revenues and Tax Expenditures in 2015

CO NGRES S IO NA L BUDGE T O F F IC E 7

Total Outlays

CO NGRES S IO NA L BUDGE T O F F IC E 8

Projected Outlays in Major Budget Categories

CO NGRES S IO NA L BUDGE T O F F IC E 9

Population, by Age Group

CO NGRES S IO NA L BUDGE T O F F IC E 10

Spending for the Major Health Programs in 2025 and the Share of That Spending on People at Least 65 Years Old

CO NGRES S IO NA L BUDGE T O F F IC E 11

Projected Net Interest

CO NGRES S IO NA L BUDGE T O F F IC E 12

Defense, Nondefense, and Other Mandatory Spending

CO NGRES S IO NA L BUDGE T O F F IC E 13

Total Revenues and Outlays

CO NGRES S IO NA L BUDGE T O F F IC E 14

Spending and Revenues Projected in CBO’s Baseline, Compared With Actual Values in 1965 and 1990

Note: * = between zero and 0.05 percent.

CO NGRES S IO NA L BUDGE T O F F IC E 15

Outlook for Economic Growth

CO NGRES S IO NA L BUDGE T O F F IC E 16

Growth of Real GDP

CO NGRES S IO NA L BUDGE T O F F IC E 17

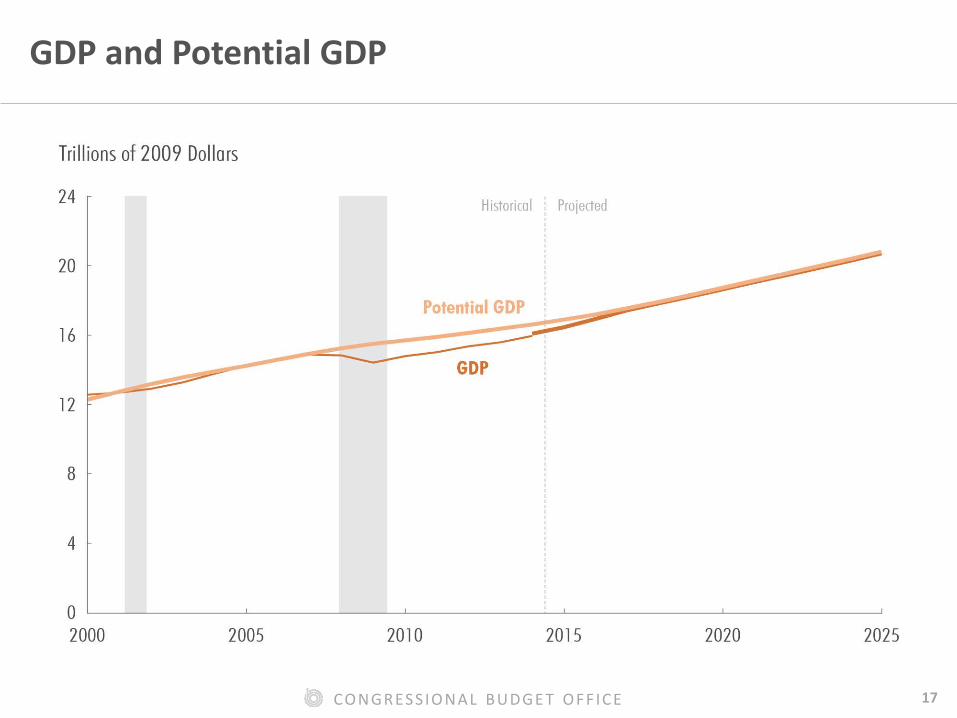

GDP and Potential GDP

CO NGRES S IO NA L BUDGE T O F F IC E 18

Contributions to the Growth of Real GDP

CO NGRES S IO NA L BUDGE T O F F IC E 19

Real Total Compensation of Employees

CO NGRES S IO NA L BUDGE T O F F IC E 20

Business Investment

CO NGRES S IO NA L BUDGE T O F F IC E 21

Household Formation

CO NGRES S IO NA L BUDGE T O F F IC E 22

Outlook for the Labor Market

CO NGRES S IO NA L BUDGE T O F F IC E 23

Rates of Short- and Long-Term Unemployment

CO NGRES S IO NA L BUDGE T O F F IC E 24

Underuse of Labor

CO NGRES S IO NA L BUDGE T O F F IC E 25

The Labor Force, Employment, and Unemployment

CO NGRES S IO NA L BUDGE T O F F IC E 26

Employment Shortfall

The employment shortfall is the number of people who would be employed if the unemployment rate equaled its rate in December 2007 (the light blue bars) and if the labor force participation rate equaled its potential rate (the dark blue bars).

CO NGRES S IO NA L BUDGE T O F F IC E 27

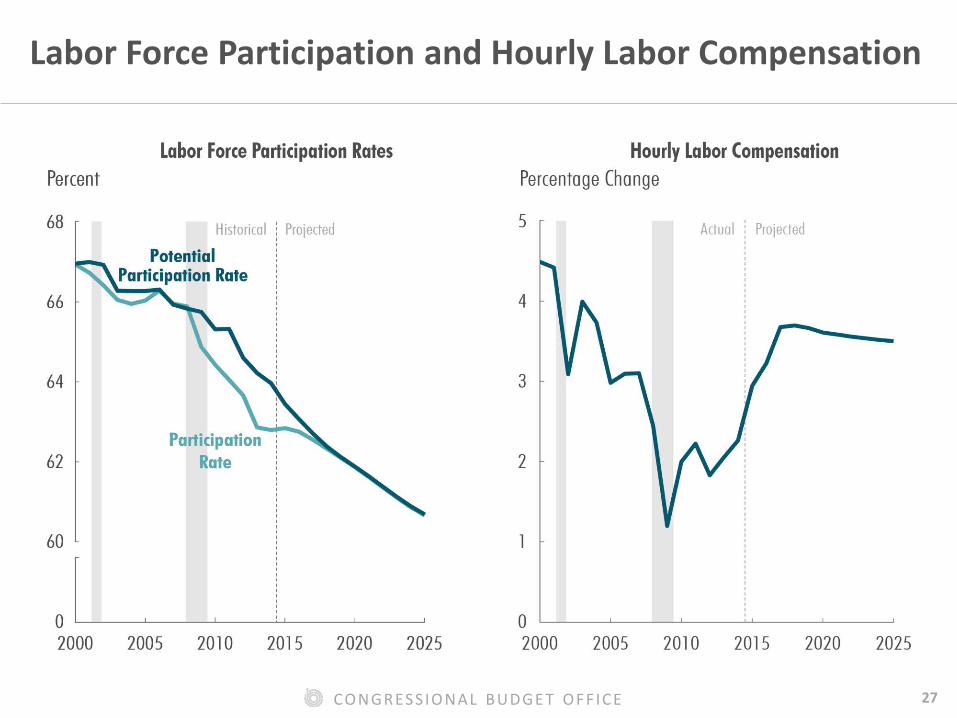

Labor Force Participation and Hourly Labor Compensation

CO NGRES S IO NA L BUDGE T O F F IC E 28

Outlook for Inflation and Interest Rates

CO NGRES S IO NA L BUDGE T O F F IC E 29

Inflation

CO NGRES S IO NA L BUDGE T O F F IC E 30

Forecasts of Interest Rates by CBO, the Federal Reserve, and Federal Funds Futures

CO NGRES S IO NA L BUDGE T O F F IC E 31

Interest Rates

CO N GR ES S IO N A L B UDGE T O F F IC E 32

Nominal and Real Interest Rates on 10-Year Treasury Notes

*Calculated using the consumer price index for all urban consumers.