Embed Size (px)

Citation preview

UGANDA BUDGET 2015/16

“MAINTAINING INFRASTRUCTURE INVESTMENT AND

PROMOTING EXCELLENCE IN PUBLIC SERVICE

DELIVERY”

This Newsletter is prepared for guidance

only and is not a substitute for professional advice.

Whilst every care has been exercised in ensuring

the accuracy of the information contained

herein, we will not accept any responsibility

for errors or omissions or for any action taken

without appropriate professional advice.

This newsletter is for exclusive use by

clients of PKF Uganda and its associates

and no part of it may be reproduced without our

prior written consent.

2015/16 UGANDA BUDGET AT A GLANCE

I. INTRODUCTION

The theme for the financial year 2015/16 Budget is “Maintaining Infrastructure Investment and Promoting Excellence in Public Service Delivery”. The underlying objective of this theme is to ensure continuous removal of the binding constraints that impede socio-economic transformation of the country into a middle income one. Consequently, the strategic sub-themes of the Budget, which is anchored on the Second National Development Plan (NDPII), include the following:

i. Maintenance of National Security and Defense; ii. Facilitating private sector enterprise for increased investment, employment and economic

growth; Effective delivery and maintenance of infrastructure; iii. Commercializing production and productivity in primary growth sectors, particularly the

agriculture and industrial sectors; iv. Enhancing capacity for increased domestic revenue mobilization; v. Increasing social service delivery; and vi. Enhanced efficiency in government management.

II. ECONOMIC PERFORMANCE FOR FY 2014/15

Uganda’s economy continued to expand through financial year 2014/15, with growth expected to reach 5.3% by end of June 2015. Although this growth is lower than the 6.1% projected in the 2014/15 Budget, it reflects an almost full recovery from the slowdown that happened in financial year 2012/13, where growth was 3.3%. Sectors that have experienced growth during 2014/15 include Agriculture (estimated at 6.6%), Manufacturing (estimated at 4.1%), Construction (estimated at 6.6%) and Services (estimated at 10.2%) sectors. This performance

has been driven by infrastructure development, improved services, product innovation and other value added services facilitated by IT.

Inflation Inflation remained low this year and dropped to 4.9% by May 2015, compared to 5.4% in May 2014. The slowdown in price increases is largely attributed to:

i. Continuing decline in food and food crop inflation resulting from improved weather conditions that contributed to bumper harvests and;

ii. Falling global oil prices which resulted in a slight decline in domestic pump prices (an average 12% decrease for both petrol and diesel).

Interest Rates

Interest rates for borrowers remain high largely due to two factors:

i. Limited supply of long term capital in the economy due to absence of a savings mechanism to mobilize long term capital, and

ii. Risk profile of borrowers which remains high, as demonstrated by high default rates and non-performing loans in the past.

These constraints are to be addressed by Government as follows:

i. Implementing the National Identification Project whose integration with financial systems will aid the verification of the creditworthiness of borrowers

ii. Undertaking reforms in the financial sector to create efficient mechanisms to mobilize long term capital.

iii. Increasing the capitalization of the Uganda Development Bank from the current UShs. 128 billion up to Shs 500 billion over the medium term.

Exchange Rates Depreciation of the Uganda Shilling against the US Dollar started in December 2014 and has continued through to June 2015. This depreciation is largely driven by the following factors:

i. Global strengthening of the US Dollar.

ii. Increased dollar demand mainly from manufacturing, telecom, trading and energy sectors amidst lower inflows, which are constrained largely due to political instability faced by regional trading partners and an economic slowdown in Europe.

To stem exchange rate volatility, the Bank of Uganda has intervened by selling dollars to the market in order to cool market pressures.

III. ECONOMIC OUTLOOK FOR FY 2015/16

During financial year 2015/16, real GDP growth is projected at 5.8%. This is largely attributed to:

i. A recovery in private sector consumption

ii. Acceleration in public and private investment.

Over the medium term, real GDP growth is expected to reach an average of 6.5% per annum over the next five years, largely driven by an increase in new public investment projects, particularly in infrastructure, and a sustained rebound in private sector activities. Another objective over the medium term is to keep annual core inflation close to the Central Bank’s 5% target and headline inflation within single digits. The strategy in the 2015/16 financial year and the medium term will focus on accelerating infrastructure development to address constraints to private sector growth and increase efficiency in service delivery.

IV. BUDGET STRATEGY FOR 2015/16

Planned interventions for the 2015/16 financial year are summarized by the thematic areas outlined above.

1. Maintenance of National Security and Defence

The 2015/16 budget will continue to facilitate professionalizing the army and other security

organs. Specific emphasis will be placed on the acquisition of modern weapons, strengthening

intelligence capability, training and welfare. An allocation of UShs 1,632.89 billion has been

approved for the Security Sector.

2. Commercializing Production and Value Addition

Agriculture

UShs. 479.96 billion has been allocated to the agriculture sector for 2015/16. Strategic

interventions to be implemented during the year include:

i. Provision of agricultural inputs to farmers;

ii. Promotion of value addition for strategic commodities;

iii. Fund research to increase productivity and disease resistance varieties;

iv. Control of pests and diseases, with special emphasis on Banana and Coffee

Bacterial Wilt and Foot and Mouth Disease;

v. Construct valley tanks and dams for livestock and crop irrigation; and

vi. Provide affordable long term financing under the Agricultural Credit Facility (ACF) for

agriculture, agro-processing and agro-based value addition.

Industrial Development

Key interventions include:

i. Continue to operationalize industrial and business parks at Namanve, Luzira, Mukono

and Mbale to provide serviced areas for development of manufacturing and other

business enterprises.

ii. Provision for warehousing and logistics including cold-storage and market auctioning for

wholesale of agricultural produce.

iii. Development of Economic Processing Zones (EPZ’s) in line with the Free Zones Act

2014.

Tourism Development

An allocation of UShs. 81.3 billion to the Tourism sector has been approved for the 2015/16 fiscal year. Activities planned for year include:

i. Skills development to meet world class requirements for high standard of performance in

the hospitality industry;

ii. Completion of hotels and restaurants rating;

iii. Development of strategic tourism infrastructure in partnership with the Private Sector;

iv. Enactment and enforcement of sector regulation to ensure maintenance of sector standards at internationally acceptable levels.

Business Climate Planned activities include:

i. Further rationalization of business licenses and procedures.

ii. Enhancing efficiency of the judiciary to reduce commercial case backlog.

3. Strategic Infrastructure Development and Maintenance

The budget for the 2015/16 financial year will continue to facilitate ongoing and new projects as follows: Transport Infrastructure

An allocation of UShs. 3,328.79 billion to the transport sector has been approved for the 2015/16 financial year. Focus will remain on improving the condition of the road network through tarmacking and maintenance of roads. Railway Transport

Priority will be on fast-tracking the ongoing process of developing the Standard Gauge Railway network throughout the country. Water Transport

Priority will be put on improvement of the inland water system through procurement of new ferry services, as well as improving the safety and quality of the water transport system. Air Transport

The budget will facilitate interventions for improving the quality of operations and maintenance of Entebbe International Airport and other air transport facilities across the country, as well as fast tracking the development of an airport in Kabale (Hoima) to ease the development of the oil refinery. The cost of the rehabilitating Entebbe International Airport over the next five year period amounts to US$ 325 million and has already been secured. Energy Infrastructure

Priority will be on fast-tracking construction of the Karuma Hydropower Project (600MW); Isimba hydro power project (183MW), other mini-hydro power projects such as Muzizi HPP, construction of at least five Small Hydropower plants (ranging from 5MW to 16MW), as well as construction of transmission lines under the Rural Electrification Programme. Oil, Gas and Mineral Development

Emphasis will be on continued exploration of oil and other valuable minerals and development of the Crude Oil Pipeline to the Indian Ocean and petroleum products pipelines. Information and Communication Technology (ICT) Infrastructure

In the 2015/16 financial year, interventions will include the following:- i. Completing the third phase of the National Backbone Infrastructure (NBI);

ii. Strengthening the legal and institutional framework for ICT use and IT information security;

iii. Establishing a fully integrated one stop centre for investment, linking the National Identity Card System, the Integrated Financial Management System, Government Payroll System, and Computerized Education Management System;

vi. Operationalize the second phase of the National Backbone Infrastructure; and

vii. Commence the construction of the National ICT Park and Innovation Centre at Namanve.

4. Human Capital Development The strategy for improving the quality of public services will seek to address challenges in human resource, performance enhancement, Monitoring and Evaluation, inspection and timely delivery of quality services with emphasis on education, health and water sectors. Education and Skills Development

In the 2015/16 financial year, an allocation of UShs 2,029 Billion has been approved. Key priorities to be financed in the FY 2015/16 include the following;

i. A UShs 39.78 billion increase in the Capitation and School Facilities funding to ensure better effectiveness of the UPE, USE/UPOLET programmes;

ii. Construction of primary schools throughout the country;

iii. Training Head Teachers and orienting School Management Committees (SMCs) in Leadership and Management Skills.

iv. Enhancing vocational and skills development by implementing the Skilling Uganda Project with additional funding of Shs 5.9 billion;

v. Increasing access to tertiary education with an additional allocation of UShs 6 billion for loans to new degree and diploma students;

vi. Supporting the Teachers SACCO with an additional UShs 5 billion in order to increase access to affordable financial and credit facilities;

vii. Increasing salaries for Lecturers in all Public Universities with additional funding of UShs 50 billion.

Health Service Delivery

An allocation of UShs. 1,270.8 billion has been approved for the 2015/16 financial year. Key interventions include construction, expansion and further rehabilitation, equipping and staffing of the national, referral, general and lower level health facilities. Water and Sanitation

An allocation of UShs. 547.3 billion has been approved for the 2015/16 financial year. Key interventions will be on:

i. Increasing access to safe water in rural and urban areas;

ii. Increasing sanitation and hygiene in rural and urban areas; and

iii. Increasing functionality of water supply systems.

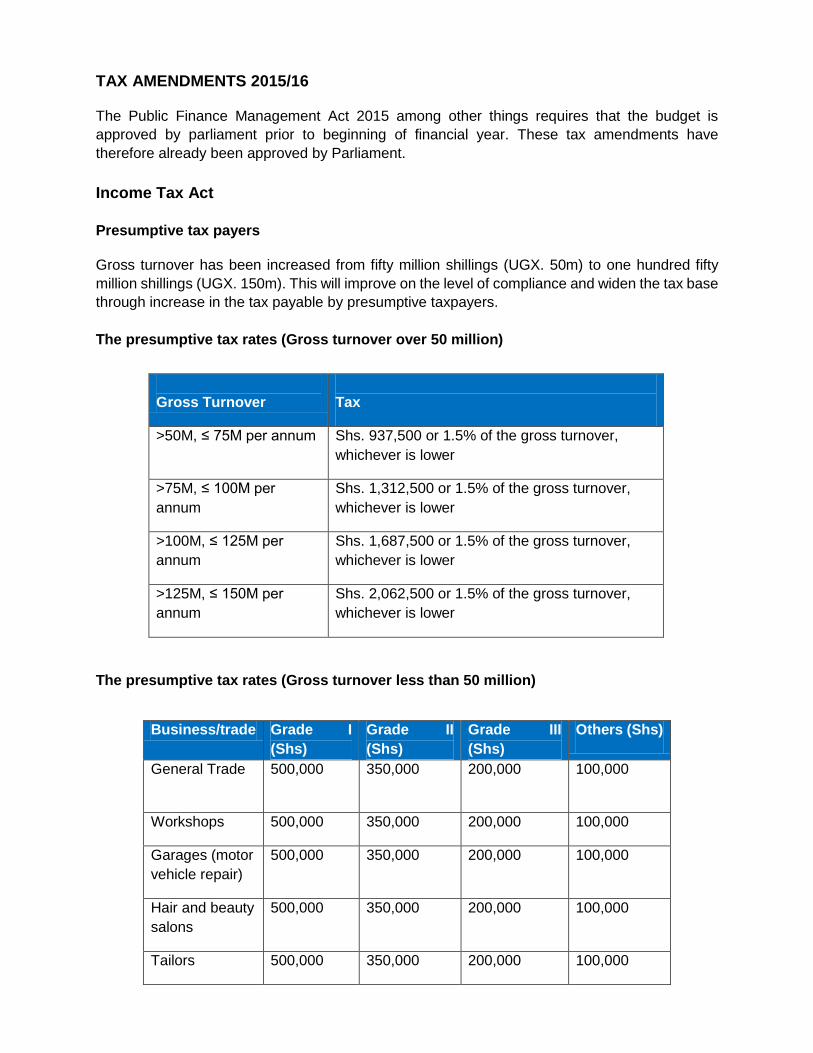

TAX AMENDMENTS 2015/16

The Public Finance Management Act 2015 among other things requires that the budget is

approved by parliament prior to beginning of financial year. These tax amendments have

therefore already been approved by Parliament.

Income Tax Act

Presumptive tax payers

Gross turnover has been increased from fifty million shillings (UGX. 50m) to one hundred fifty

million shillings (UGX. 150m). This will improve on the level of compliance and widen the tax base

through increase in the tax payable by presumptive taxpayers.

The presumptive tax rates (Gross turnover over 50 million)

The presumptive tax rates (Gross turnover less than 50 million)

Gross Turnover

Tax

>50M, ≤ 75M per annum

Shs. 937,500 or 1.5% of the gross turnover,

whichever is lower

>75M, ≤ 100M per

annum

Shs. 1,312,500 or 1.5% of the gross turnover,

whichever is lower

>100M, ≤ 125M per

annum

Shs. 1,687,500 or 1.5% of the gross turnover,

whichever is lower

>125M, ≤ 150M per

annum

Shs. 2,062,500 or 1.5% of the gross turnover,

whichever is lower

Business/trade Grade I

(Shs)

Grade II

(Shs)

Grade III

(Shs)

Others (Shs)

General Trade

500,000 350,000 200,000 100,000

Workshops 500,000 350,000 200,000 100,000

Garages (motor

vehicle repair)

500,000 350,000 200,000 100,000

Hair and beauty

salons

500,000 350,000 200,000 100,000

Tailors 500,000 350,000 200,000 100,000

Supplies from Non registered persons (Amendment of Section 22 (2) (m))

No deduction will be allowed for any expenditure above one million shillings on goods and

services from a supplier without a Taxpayer Identification Number (TIN). This implies that

taxpayers will ensure that they receive supplies from registered suppliers and therefore

unregistered suppliers will be forced to acquire TINs and hence widening the tax base.

Repeal of section 36 (mineral exploration expenditures)

A deduction allowed for any expenditure of a capital nature in searching for, discovering and

testing, or winning access deposits of minerals has been repealed. However, a comprehensive

regime for petroleum and mining sectors has been provided for in the ITA.

Business Reorganization under section 77

Reorganization is defined as-

a) a transaction which a company transfers its assets to another company that is controlled

by the transferor or its shareholders following which the stock of the transferee is

distributed; or

b) a transaction which persons whether for payment or not are allotted shares in or

debentures of a company in respect of and in proportion to, or as nearly as may be in

proportion to, their holdings of shares in the company and any case which there is more

than one class of shares and the rights attached to shares of any class are altered;

c) a merger or amalgamation where all or substantially all the assets and liabilities of one or

more transferor companies are transferred to a single transferee company, whereby the

transferor companies cease to exist by operation of law;

d) a transaction which two or more companies transfer their assets and liabilities to a single

newly established company;

Maternity

homes

500,000 350,000 200,000 100,000

Drug shops 500,000 350,000 200,000 100,000

e) corporate division; by which all or substantially all the assets of one company are

transferred in exchange for shares to at least two or more newly established or pre-existing

companies, except where the assets are already in the hands of a subsidiary;

For the avoidance of doubt, a sale of a share from one person to another does not constitute a

reorganization.

A branch under section 78

A branch also includes-

a place where a person furnishes services, including consultancy services, through

employees or other personnel engaged by the person for such purpose, but only if

activities of that nature continue for the same or a connected project for a period or periods

aggregating more than ninety days in any twelve month period;

Immovable property

Immovable property is defined as a mining right, petroleum right, mining information, or petroleum

information. This is meant to clarify on the scope of transactions that attract capital gains tax.

Source of Income

Income will be derived from sources in Uganda to the extent to which it is;

a) derived by -

i. a resident person in carrying on a business except to the extent that it is attributable

to a business carried on by the person through a branch outside Uganda;

ii. a non-resident person in carrying on a business through a branch in Uganda;”

b) derived by a resident person in carrying on business as owner or chatterer of a vehicle,

ship, or aircraft, wherever such vehicle, ship, or aircraft may be operated;

c) employment income or a fee for the provision of services—

i. derived from employment or services exercised or rendered in Uganda;

ii. paid by a resident person, other than as an expenditure of a business carried on by

a person outside Uganda through a branch; or

iii. paid by non-resident person as an expenditure of a business carried on by a person

through a branch in Uganda;”

d) derived by a resident individual from any employment exercised or services rendered as

a driver of a vehicle, or an officer or member of a crew of any vehicle, ship,, or aircraft,

wherever the vehicle, ship, or aircraft may be operated;

e) derived from rental of immovable property located in Uganda;

f) derived from the disposal of—

i. an interest in immovable property located in Uganda; or

ii. an interest in a company or other entity if the interest derives its value, directly or

indirectly, principally from immovable property located in Uganda;”

Thin capitalization rules

Foreign debt to foreign equity ratio for foreign-controlled resident has been increased from 1:1 to

1.5:1. As such, any interest in excess of the 1.5:1 ratio will not be allowable for tax purposes.

This implies that foreign controlled residents will be allowed a bigger portion of interest from the

foreign related party loans.

Withholding Tax

Introduction of 6% withholding tax on payments for goods and services on the following which

were exempt under section 119 (5) of the ITA-

a) a supply or importation of petroleum or petroleum products, including furnace oil,

cosmetics, and fabrics or yarn manufactured out of petroleum products;

b) a supply or importation of plant and machinery;

c) a supply or importation of human or animal drugs;

d) a supply or importation of scholastic materials;

e) the supply or importation of raw materials;

This will negatively affect investment and increase the cost of doing business since it is a direct

effect on the cash flows.

Reinsurance premiums

Withholding tax has been reduced from 15% to 5% on payments of re insurance premiums to

nonresidents. This will likely reduce the cost of re-insurance.

Advance tax

Introduction of advance tax on taxpayers providing a passenger transport service or a freight

transport service where the goods vehicle has a load capacity of more than 2 tones, as per the

rates below–

Taxpayer Identification Number

Every local authority, Government institution, or regulatory body shall require a taxpayer

identification number from any person applying for a license or any form of authorization

necessary for purposes of conducting any business in Uganda. This means that a person will not

acquire a license without a tax identification number.

Listed institutions

The Global Fund to fight AIDS, Malaria and Tuberculosis has been added to the listed institutions

under the first schedule of the ITA. Therefore it will be exempt from income tax.

Value Added Tax Act

Registration

Annual registration threshold has been increased from fifty million shillings (UGX. 50m) to one

hundred fifty million shillings (UGX. 150m). This is a response to the increasing inflation in Uganda

therefore, taxpayers whose turnover is one hundred fifty million and above will be required to

register for VAT.

The following persons may also apply to the Commissioner General to be registered;

(a) a licensee undertaking mining operations;

Vehicle/ Persons Tax

Van, pickup and lorries 25 currency pints per ton

Saloons, station wagons,

mini buses, buses, and

coaches

2,000 shillings per

passenger per month

Drivers Shs. 100,000 per annum

Conductors Shs. 50,000 per annum

(b) a contractor undertaking petroleum operations;

(c) a person undertaking the construction of a petroleum refinery or petroleum pipeline; and

(d) a person engaged in commercial farming.

This will enhance transparency and administration in the VAT system.

Exemption

The exemption under fifth Schedule of the East African Customs Management Act on the supply

of Compact fluorescent bulbs with a power connecting cap at the end has been removed.

Cash Basis Accounting

The threshold for applying the cash basis accounting has been increased from two hundred

million (UGX. 200m) to five hundred million (UGX. 500m). This will increase on the range of small

taxpayers who can use cash basis of accounting.

Credit for Input tax

Licensees` will be allowed a credit for input tax on imported of services. If for any tax period, a

licensee`s input tax credit exceeds his liability for the tax period, by less/ more than five million

may claim a refund. This means that licensees will be able to claim input tax from goods and

services relating to mining operations.

Public International Organisations

The following have been added to the listed under Public International Organizations –

a) Global Fund to fight AIDS, Malaria and Tuberculosis

b) Uganda Red Cross Society

Cereals

Cereals grown and milled in Uganda have now been zero rated under Third Schedule. This

promotes the activities of taxpayers who grow and mill cereals in Uganda other than importing.

Environmental Levy

Item Old rate New rate

Motor vehicles (excluding

goods vehicles) which are

between 5-10 years old

20% of CIF value 35% of CIF value

Motor vehicles (excluding

goods vehicles) which are

10 years or more

20% of CIF value

50% of CIF value

Excise Tariff Act

No Item Current Excise Duty

rate

Proposed Excise Duty

rate

a. Soft cap UShs 35,000 per 1000

sticks

UShs 45,000 per 1000

sticks

b. Hinge lid Ushs. 69,000 per 1000

sticks

UShs. 75,000 per 1000

sticks

c. Beer whose local raw material content,

excluding water, is at least 75% by

weight of its constituent

20% 30%

d. Undenatured spirits UShs. 4000 per litre or

140% whichever is

higher

UShs 1,000 per litre or

100% whichever is higher

e. Other wines (except wine made from

locally produced raw materials)

70% 80%

f. Motor Spirit (gasoline) UShs. 950/= per litre UShs. 1000/= per litre

g. Gas oil (automotive, light, amber for high

speed engine)

UShs. 630/= per litre UShs. 680/= per litre

h. Incoming international call services from

the Republic of Kenya, the Republic of

Rwanda, and the Republic of South

Sudan.

USD 0.09 per minute NIL

i. Motor vehicle lubricants NIL 5%

j. Chewing gum, sweets and chocolates NIL 10%

k. Furniture NIL 10%