Embed Size (px)

Citation preview

Page 1

Smart Grid, Smart City

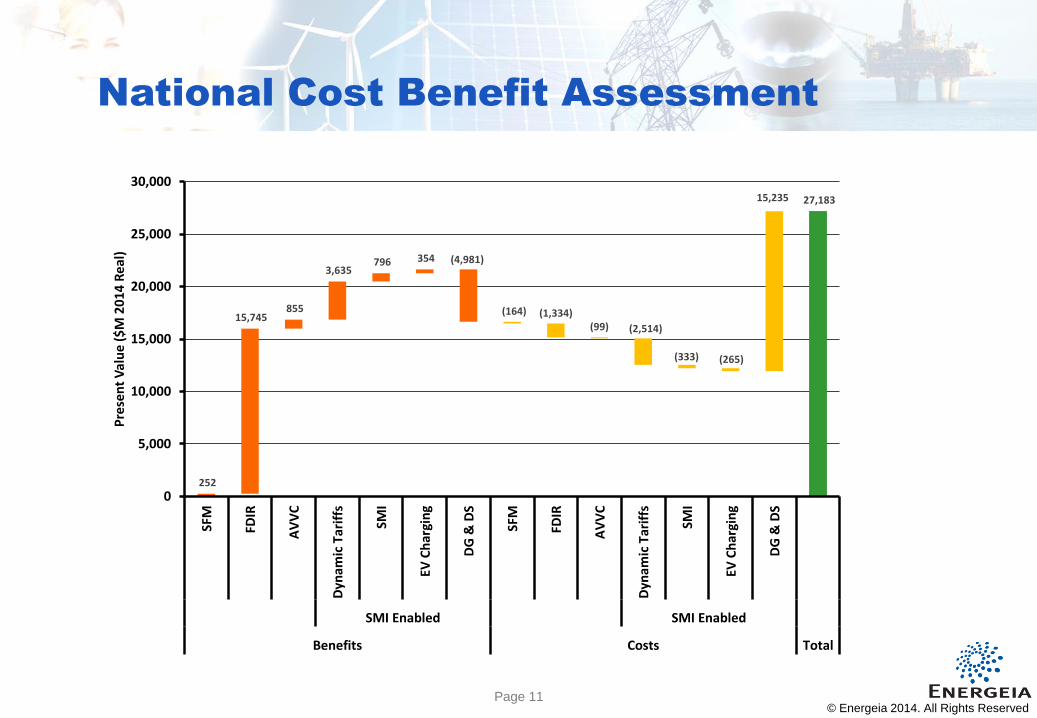

National Cost Benefit Assessment

27 November, 2014 – Smart Energy Forum

Newcastle Institute for Energy and Resources

Bob Bosler, Senior Consultant, Energeia

Ranelle Cliff, Senior Project Manager, Arup

© Energeia 2014. All Rights Reserved

Page 2

• Approach to Smart Grid, Smart City National Cost Benefit Assessment

• Outlook and technology optimisation results

• Strategic Context

• SGSC Report Conclusions and Recommendations

• Transitioning to a Smart Grid Future

• Developments since SGSC and implications

Overview

© Energeia 2014. All Rights Reserved

Page 3

Energeia

© Energeia 2014. All Rights Reserved

• Founded in 2009 in Sydney, now largest specialist consultancy in Australia

• 15 full-time experts based in Sydney, with network of distinguished experts

• We seek out transformative projects which, by their nature:

• Are technically high risk

• Have high strategic value

Confidential

Page 4

Smart Grid, Smart City

Page 5

National Cost Benefit Assessment

© Energeia 2014. All Rights Reserved

What is our independent, informed assessment of

the Business Case for the deployment of an

integrated Smart Grid in a national context?

Page 6

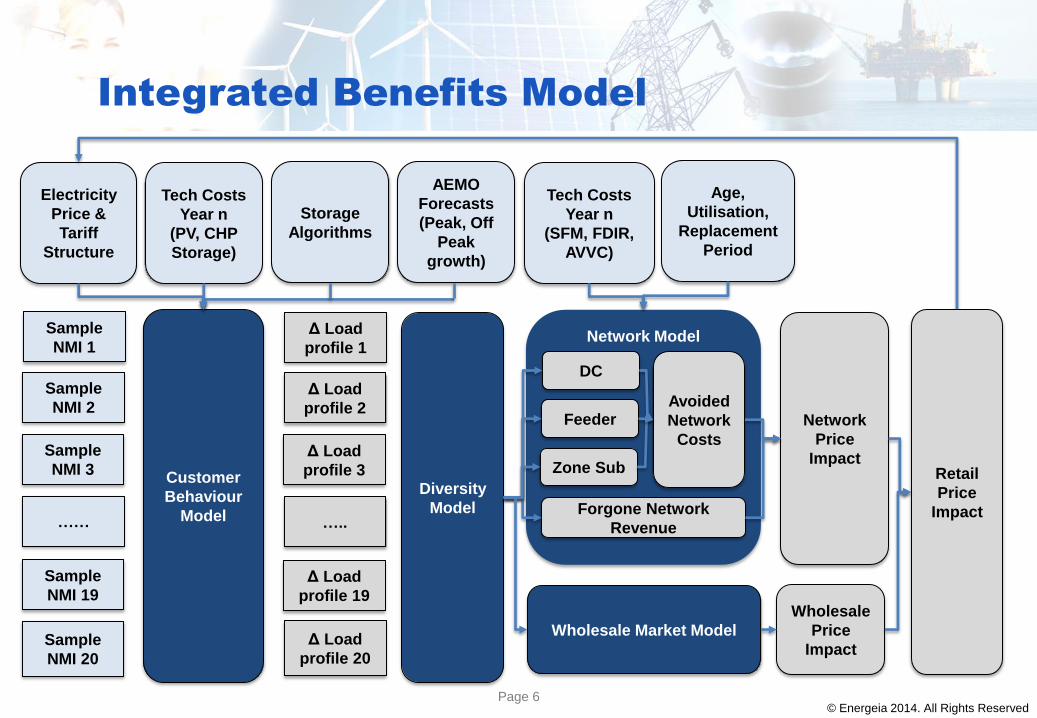

Integrated Benefits Model

© Energeia 2014. All Rights Reserved

Network Model

Customer

Behaviour

Model

Tech Costs

Year n

(PV, CHP

Storage)

DC

Network

Price

Impact

Electricity

Price &

Tariff

Structure

Sample

NMI 19

Sample

NMI 20

……

Sample

NMI 3

Sample

NMI 2

Sample

NMI 1

Δ Load

profile 19

Δ Load

profile 20

…..

Δ Load

profile 3

Δ Load

profile 2

Δ Load

profile 1

Diversity

Model Forgone Network

Revenue

Avoided

Network

Costs

Storage

Algorithms

Age,

Utilisation,

Replacement

Period

AEMO

Forecasts

(Peak, Off

Peak

growth)

Feeder

Zone Sub

Wholesale

Price

Impact

Retail

Price

Impact

Wholesale Market Model

Tech Costs

Year n

(SFM, FDIR,

AVVC)

Page 7

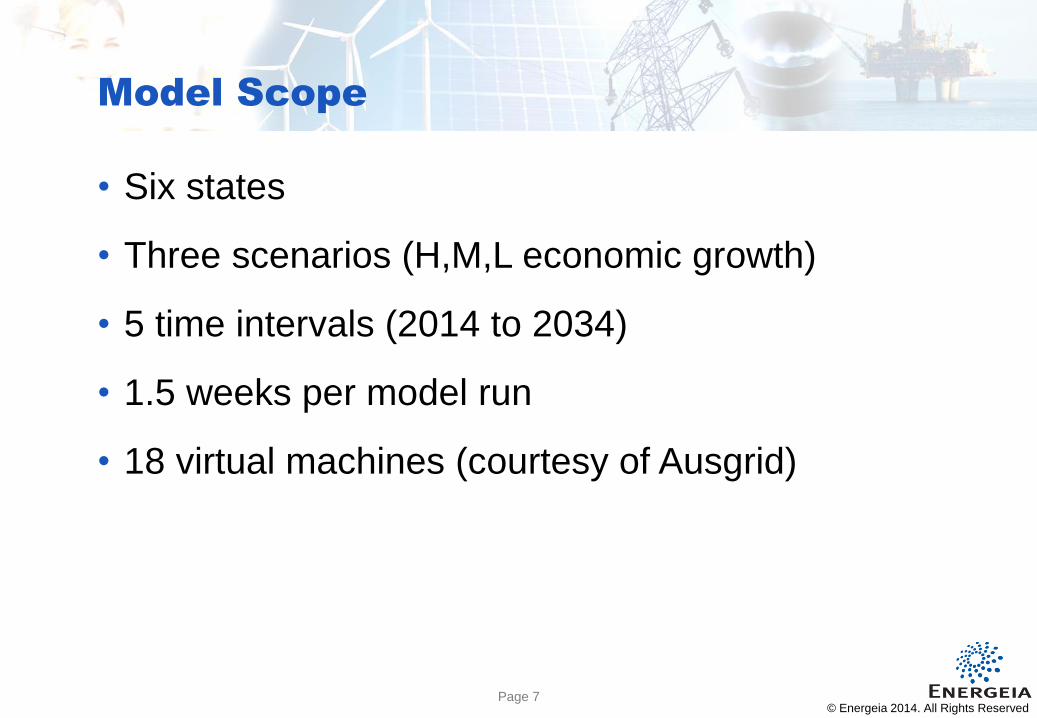

Model Scope

© Energeia 2014. All Rights Reserved

• Six states

• Three scenarios (H,M,L economic growth)

• 5 time intervals (2014 to 2034)

• 1.5 weeks per model run

• 18 virtual machines (courtesy of Ausgrid)

Page 8

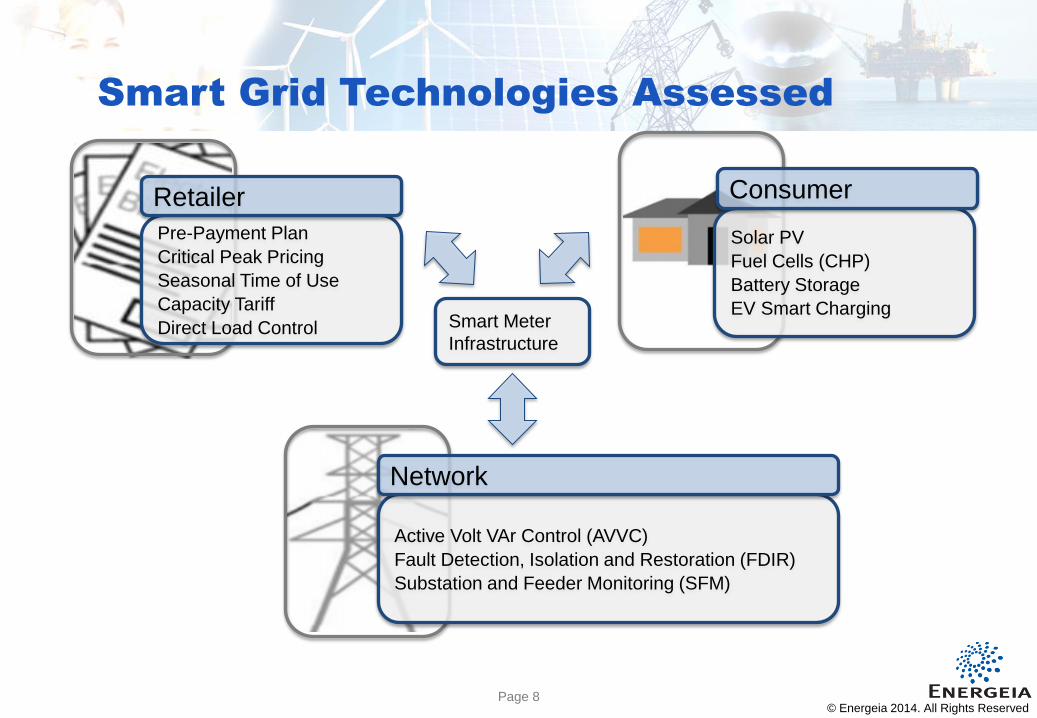

Smart Grid Technologies Assessed

© Energeia 2014. All Rights Reserved

Pre-Payment Plan

Critical Peak Pricing

Seasonal Time of Use

Capacity Tariff

Direct Load Control

Retailer

Solar PV

Fuel Cells (CHP)

Battery Storage

EV Smart Charging

Consumer

Active Volt VAr Control (AVVC)

Fault Detection, Isolation and Restoration (FDIR)

Substation and Feeder Monitoring (SFM)

Network

Smart Meter

Infrastructure

Page 9

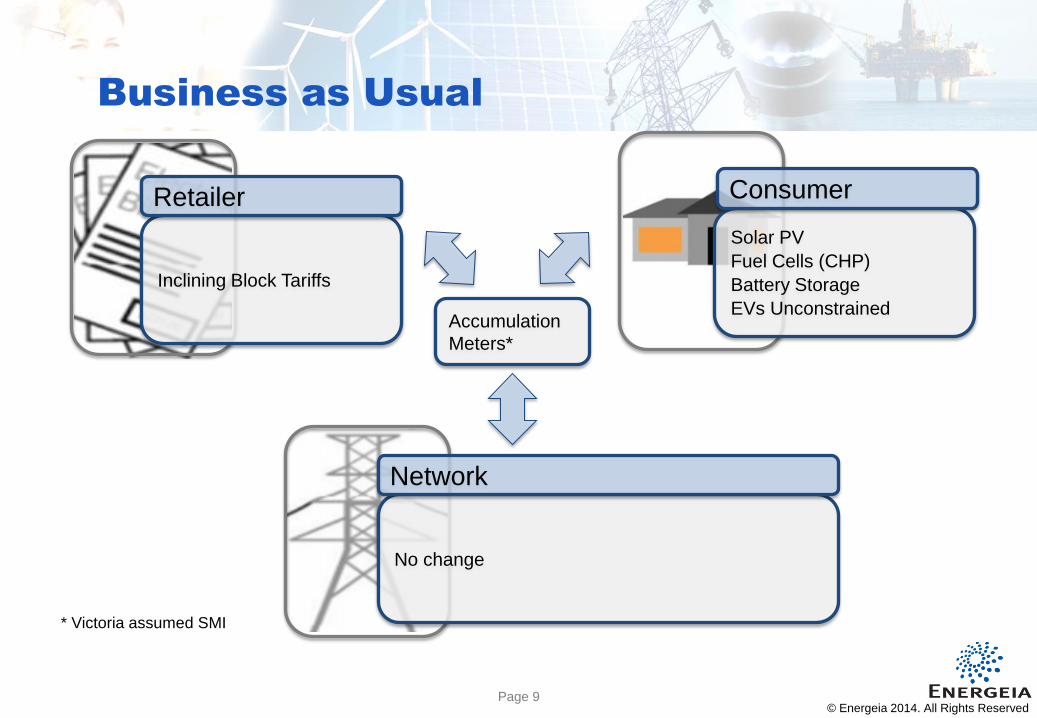

Business as Usual

© Energeia 2014. All Rights Reserved

Inclining Block Tariffs

Retailer

Solar PV

Fuel Cells (CHP)

Battery Storage

EVs Unconstrained

Consumer

No change

Network

Accumulation

Meters*

* Victoria assumed SMI

Page 10

Medium Scenario

Outlook

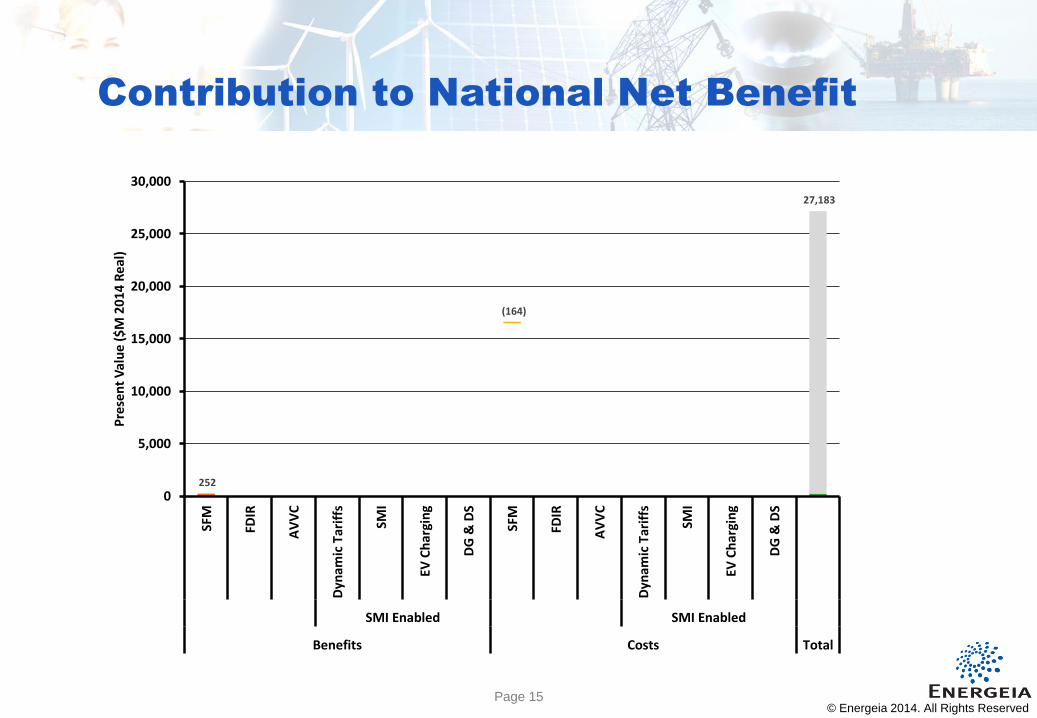

Page 11 11

252

15,745 855

3,635 796 354 (4,981)

(164) (1,334)(99) (2,514)

(333) (265)

15,235 27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

National Cost Benefit Assessment

© Energeia 2014. All Rights Reserved

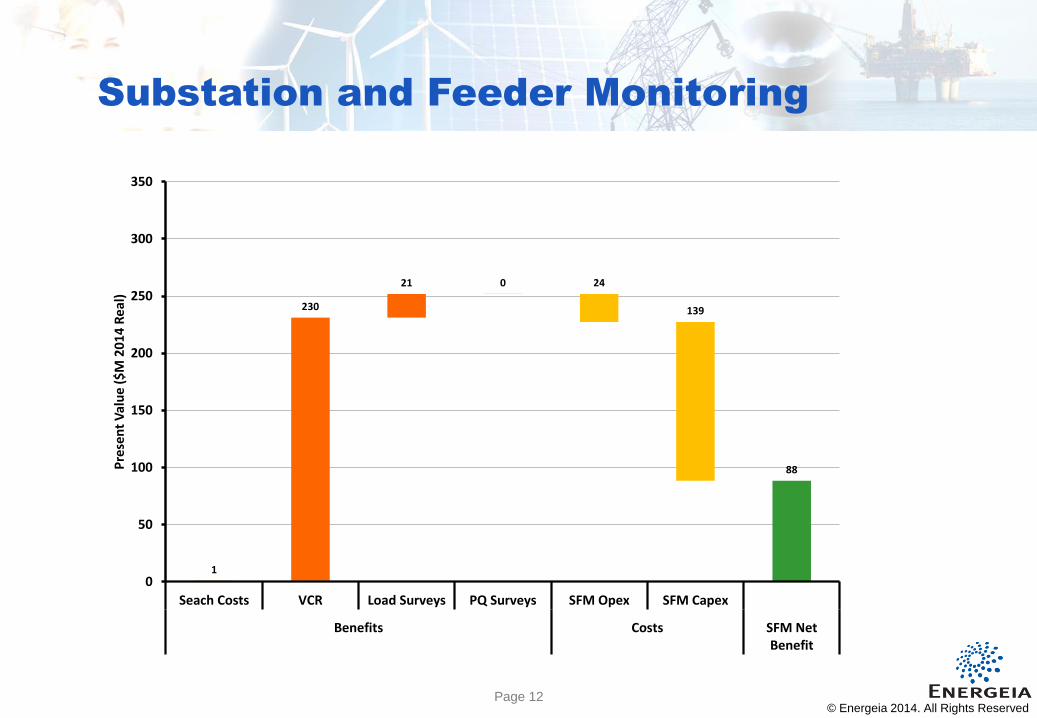

Page 12 12

1

230

21 0 24

139

88

0

50

100

150

200

250

300

350

Seach Costs VCR Load Surveys PQ Surveys SFM Opex SFM Capex

Benefits Costs SFM NetBenefit

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Substation and Feeder Monitoring

© Energeia 2014. All Rights Reserved

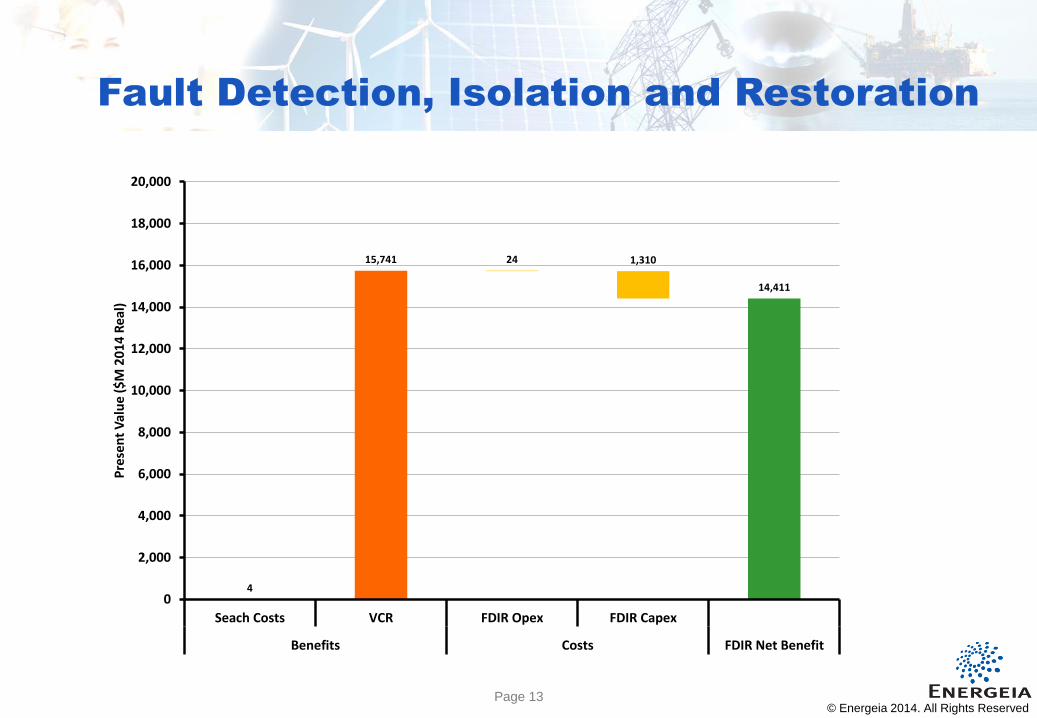

Page 13 13

4

15,741 24 1,310

14,411

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Seach Costs VCR FDIR Opex FDIR Capex

Benefits Costs FDIR Net Benefit

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Fault Detection, Isolation and Restoration

© Energeia 2014. All Rights Reserved

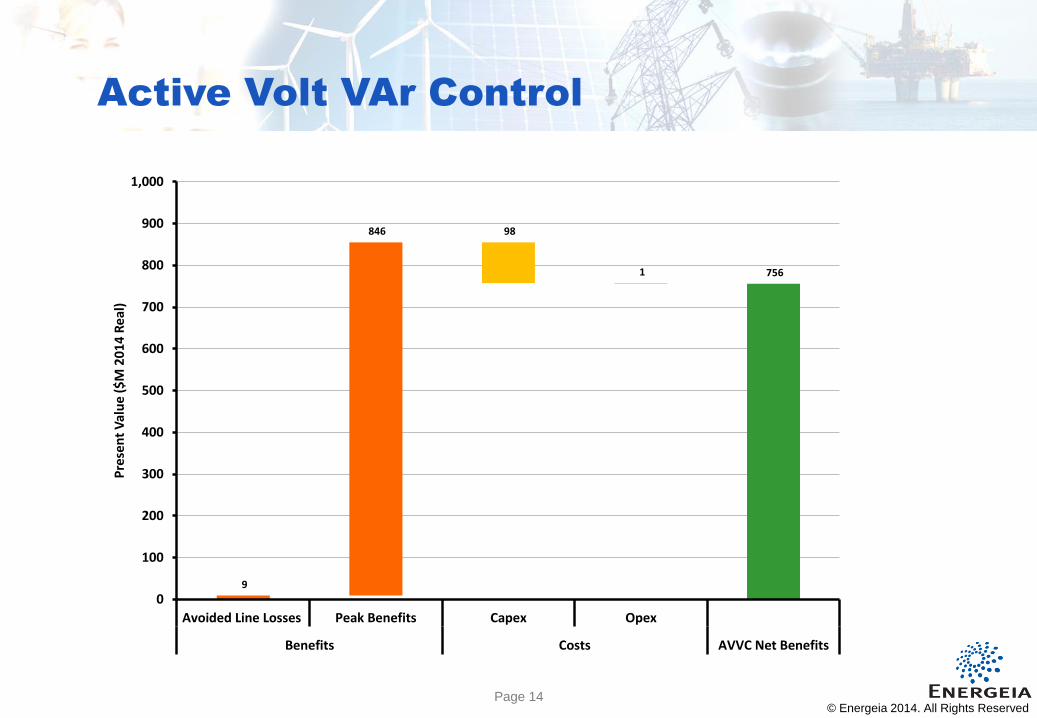

Page 14 14

9

846 98

1 756

0

100

200

300

400

500

600

700

800

900

1,000

Avoided Line Losses Peak Benefits Capex Opex

Benefits Costs AVVC Net Benefits

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Active Volt VAr Control

© Energeia 2014. All Rights Reserved

Page 15 15

252

(164)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

Page 16 16

252

15,745 (164) (1,334)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

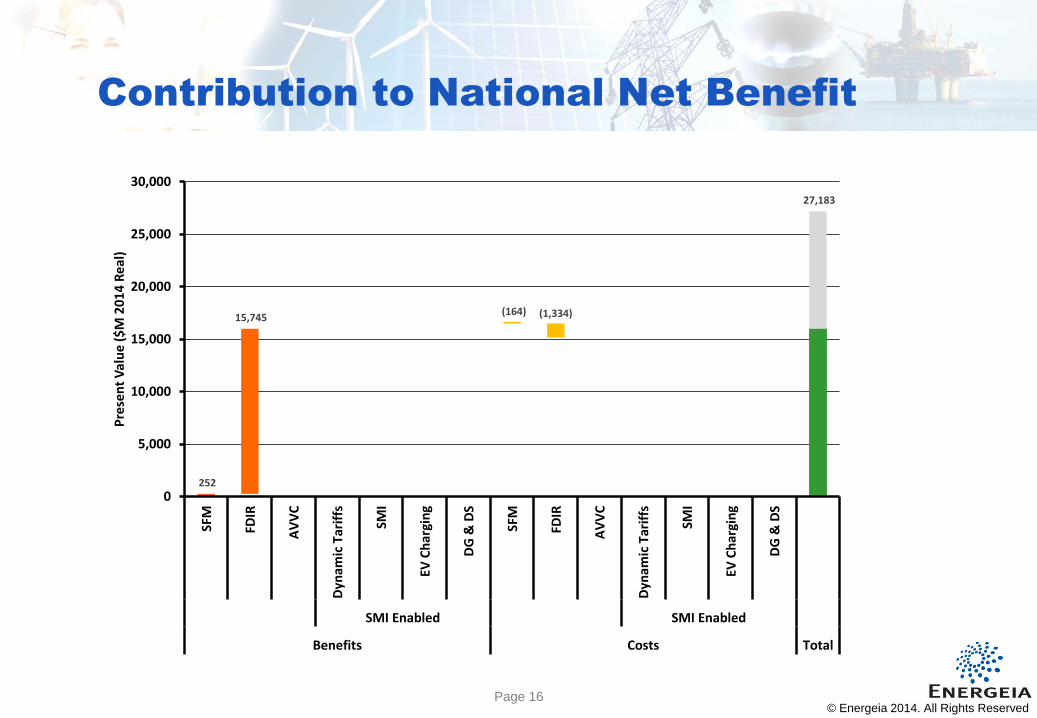

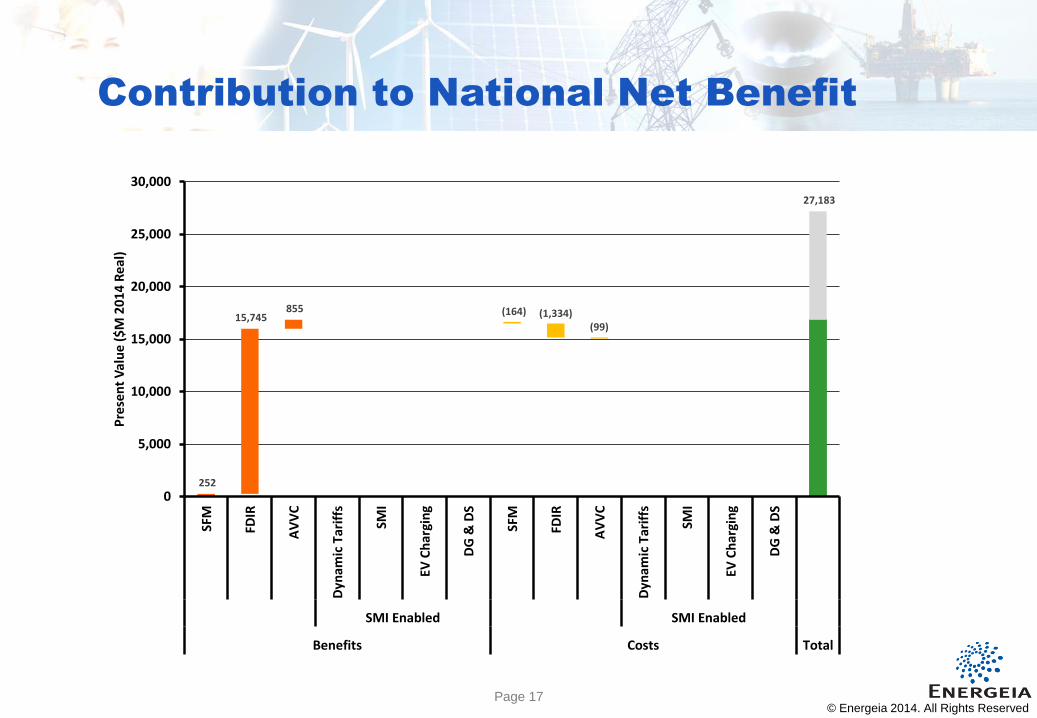

Page 17 17

252

15,745 855 (164) (1,334)

(99)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

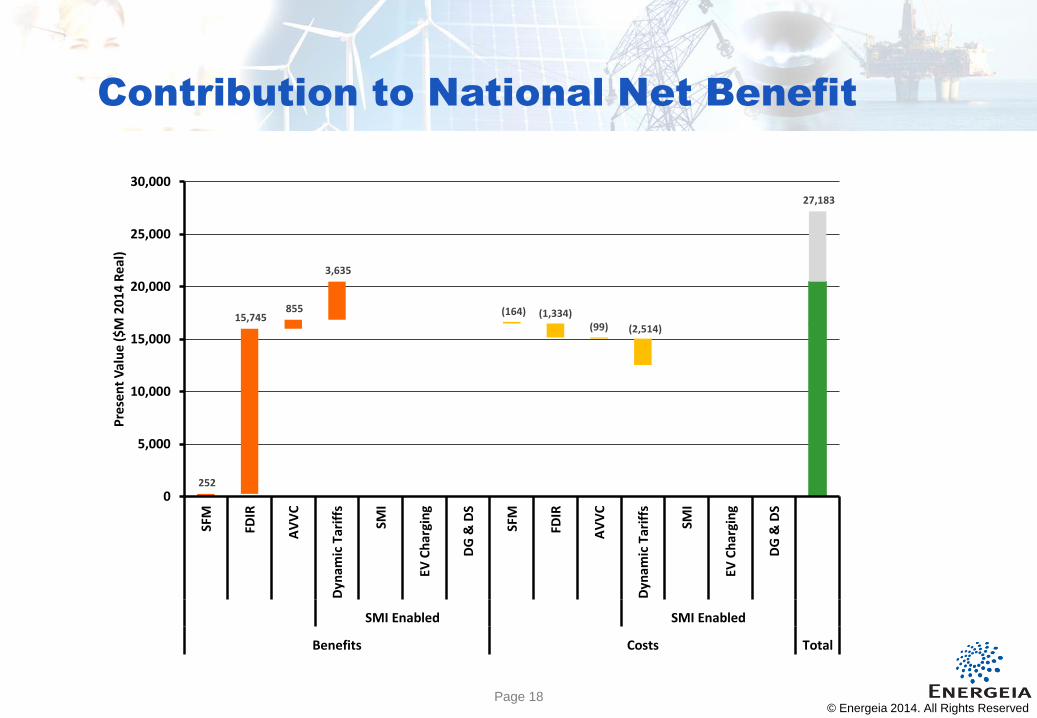

Page 18 18

252

15,745 855

3,635

(164) (1,334)(99) (2,514)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

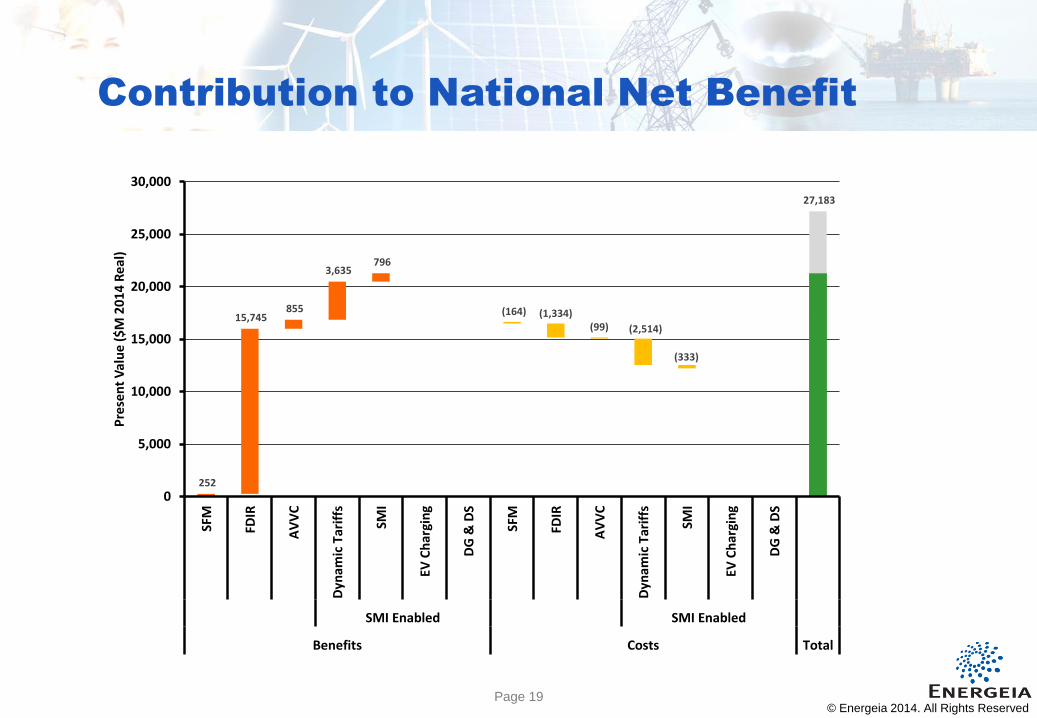

Page 19 19

252

15,745 855

3,635 796

(164) (1,334)(99) (2,514)

(333)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

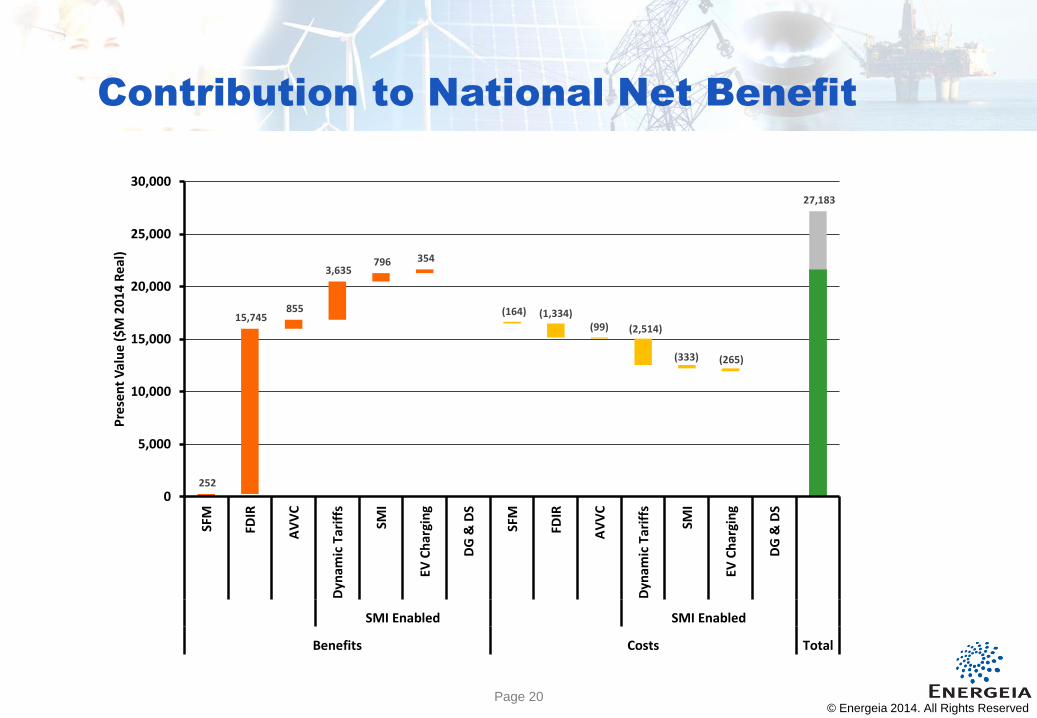

Page 20 20

252

15,745 855

3,635 796 354

(164) (1,334)(99) (2,514)

(333) (265)

27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

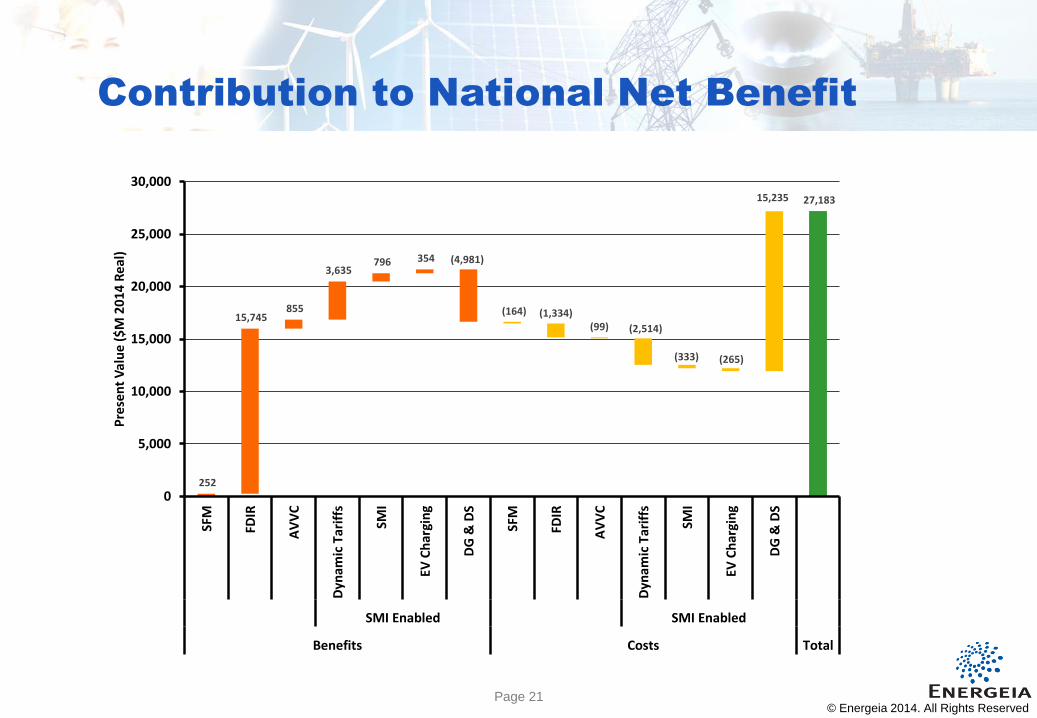

Page 21 21

252

15,745 855

3,635 796 354 (4,981)

(164) (1,334)(99) (2,514)

(333) (265)

15,235 27,183

0

5,000

10,000

15,000

20,000

25,000

30,000

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SFM

FDIR

AV

VC

Dyn

amic

Tar

iffs

SMI

EV C

har

gin

g

DG

& D

S

SMI Enabled SMI Enabled

Benefits Costs Total

Pre

sen

t V

alu

e (

$M

20

14

Re

al)

Contribution to National Net Benefit

© Energeia 2014. All Rights Reserved

Page 22 22

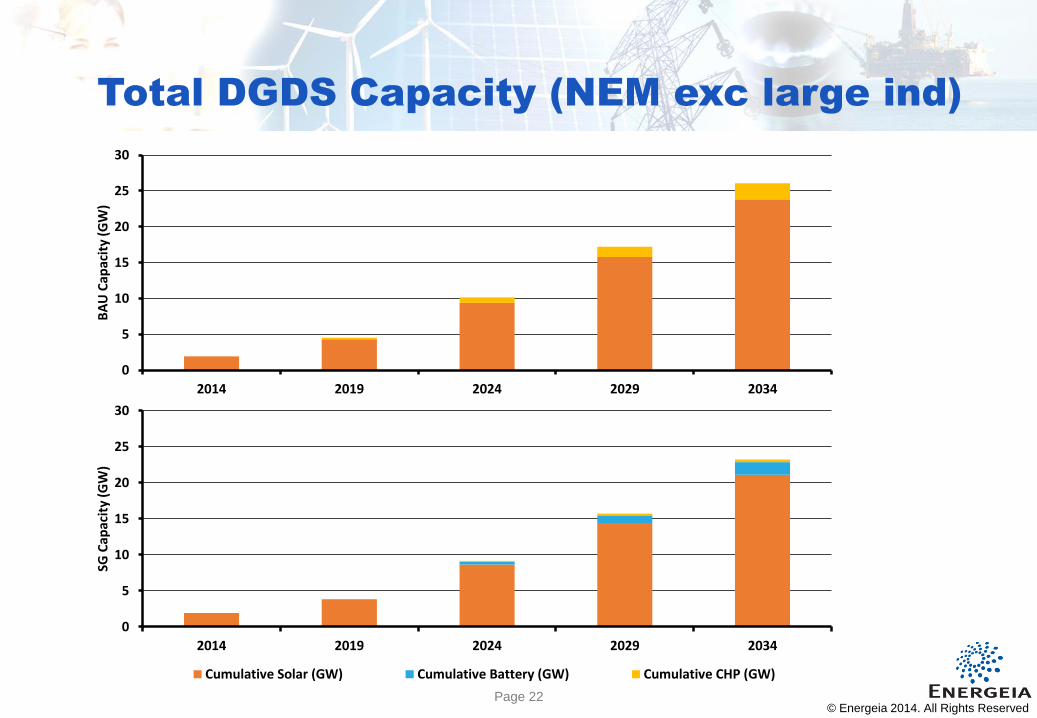

Total DGDS Capacity (NEM exc large ind)

© Energeia 2014. All Rights Reserved

0

5

10

15

20

25

30

2014 2019 2024 2029 2034

BA

U C

apac

ity

(GW

)

Cumulative Solar (GW) Cumulative Battery (GW) Cumulative CHP (GW)

0

5

10

15

20

25

30

2014 2019 2024 2029 2034

SG C

apac

ity

(GW

)

Cumulative Solar (GW) Cumulative Battery (GW) Cumulative CHP (GW)

Page 23 23

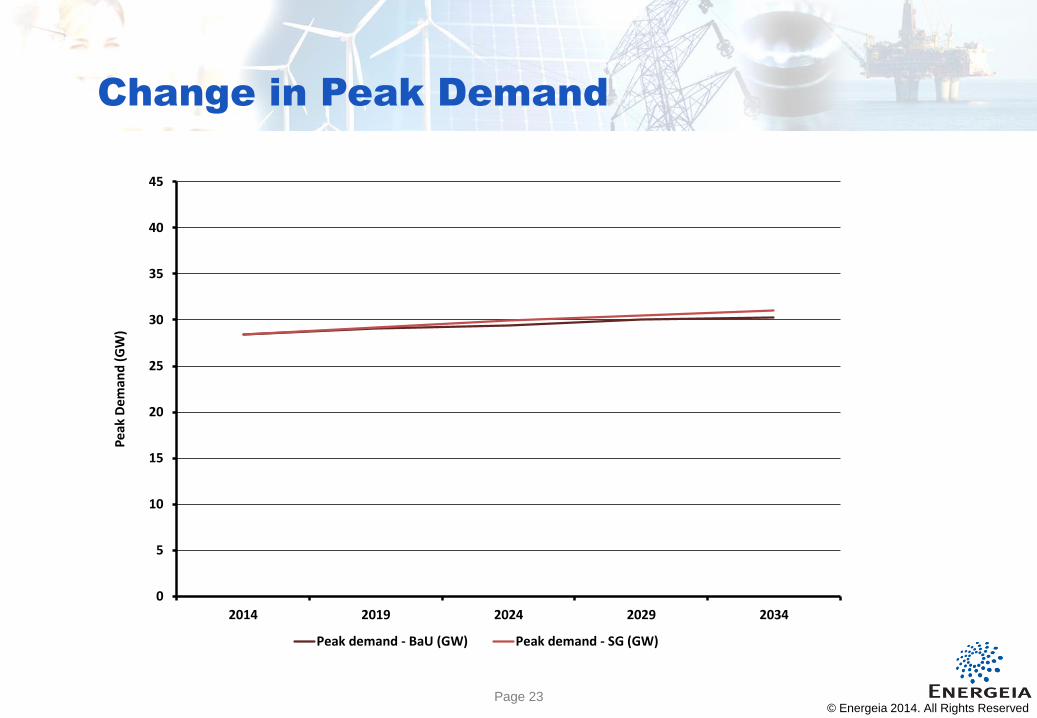

Change in Peak Demand

© Energeia 2014. All Rights Reserved

0

5

10

15

20

25

30

35

40

45

2014 2019 2024 2029 2034

Pe

ak D

em

and

(G

W)

Peak demand - BaU (GW) Peak demand - SG (GW)

Page 24 24

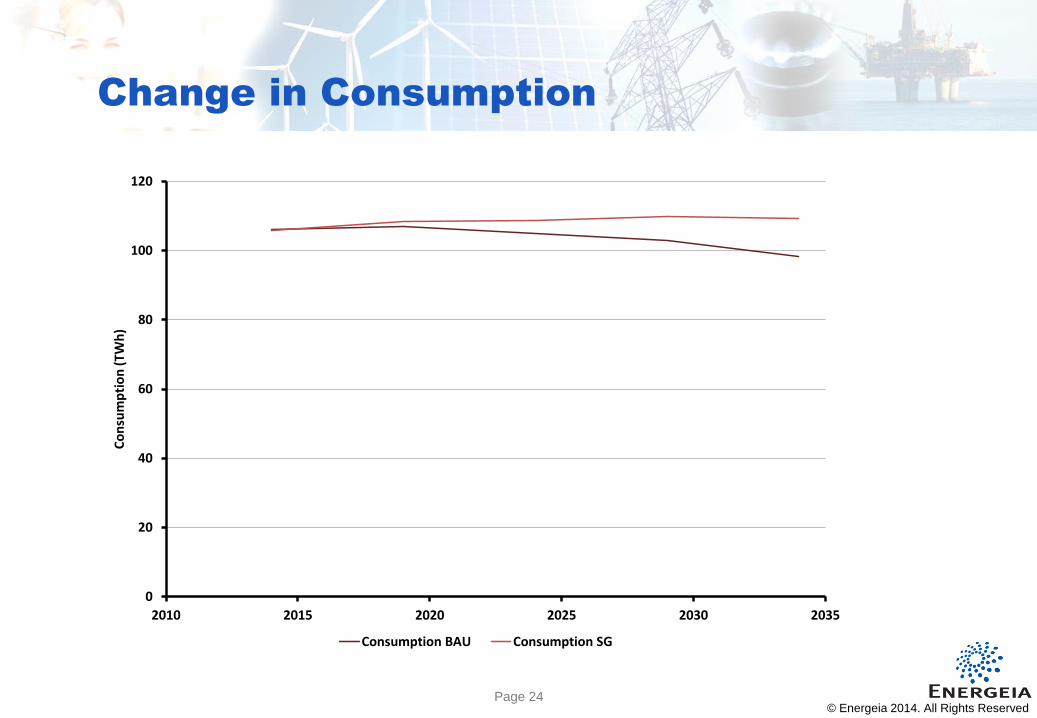

Change in Consumption

© Energeia 2014. All Rights Reserved

0

20

40

60

80

100

120

2010 2015 2020 2025 2030 2035

Co

nsu

mp

tio

n (

TWh

)

Consumption BAU Consumption SG

Page 25 25

0

5

10

15

20

25

30

351

2:0

0:0

0 A

M

1:3

0:0

0 A

M

3:0

0:0

0 A

M

4:3

0:0

0 A

M

6:0

0:0

0 A

M

7:3

0:0

0 A

M

9:0

0:0

0 A

M

10

:30

:00

AM

12

:00

:00

PM

1:3

0:0

0 P

M

3:0

0:0

0 P

M

4:3

0:0

0 P

M

6:0

0:0

0 P

M

7:3

0:0

0 P

M

9:0

0:0

0 P

M

10

:30

:00

PM

12

:00

:00

AM

De

man

d (

GW

)

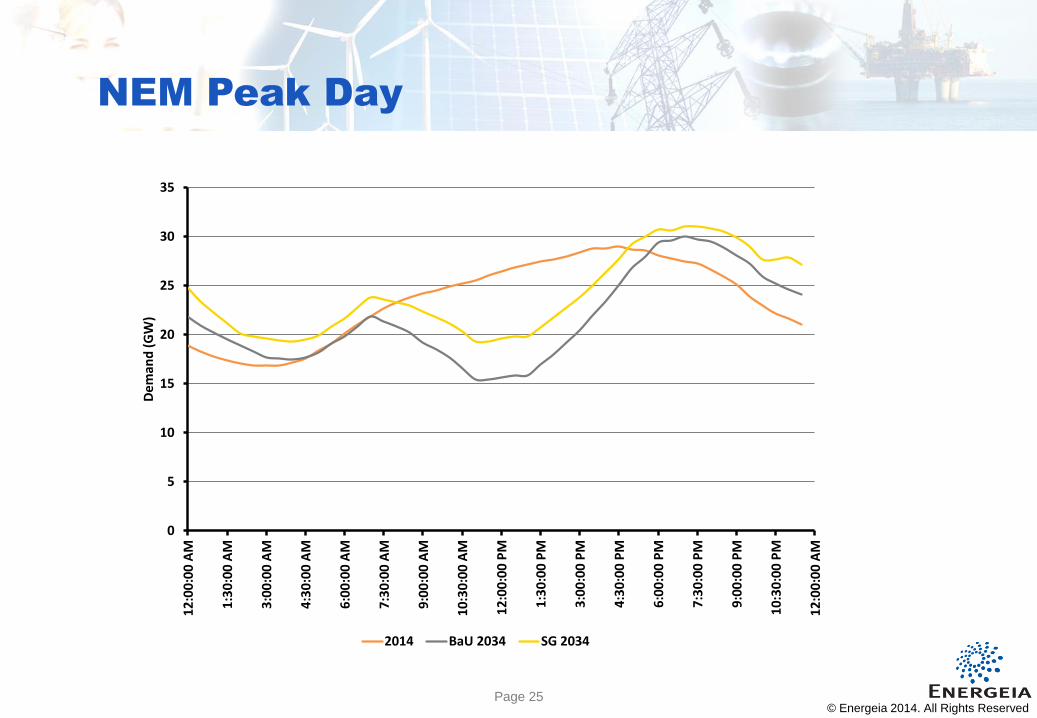

2014 BaU 2034 SG 2034

NEM Peak Day

© Energeia 2014. All Rights Reserved

Page 26 Page 26

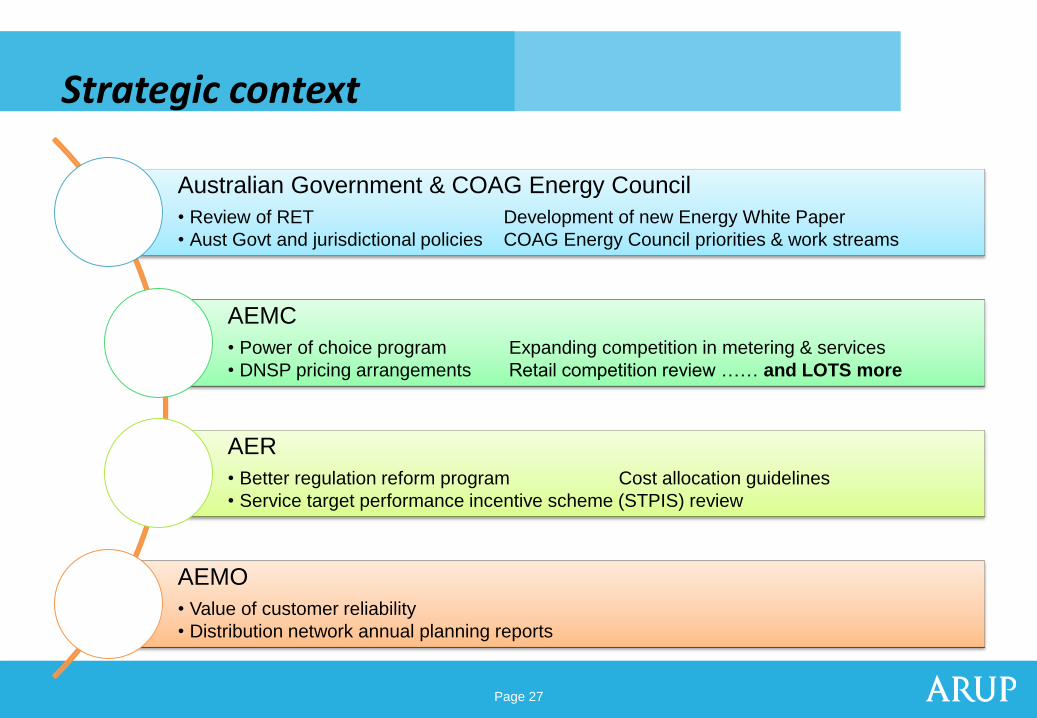

Strategic context

Page 27 Page 27

Strategic context

Australian Government & COAG Energy Council

• Review of RET Development of new Energy White Paper

• Aust Govt and jurisdictional policies COAG Energy Council priorities & work streams

AEMC

• Power of choice program Expanding competition in metering & services

• DNSP pricing arrangements Retail competition review …… and LOTS more

AER

• Better regulation reform program Cost allocation guidelines

• Service target performance incentive scheme (STPIS) review

AEMO

• Value of customer reliability

• Distribution network annual planning reports

Page 28 Page 28

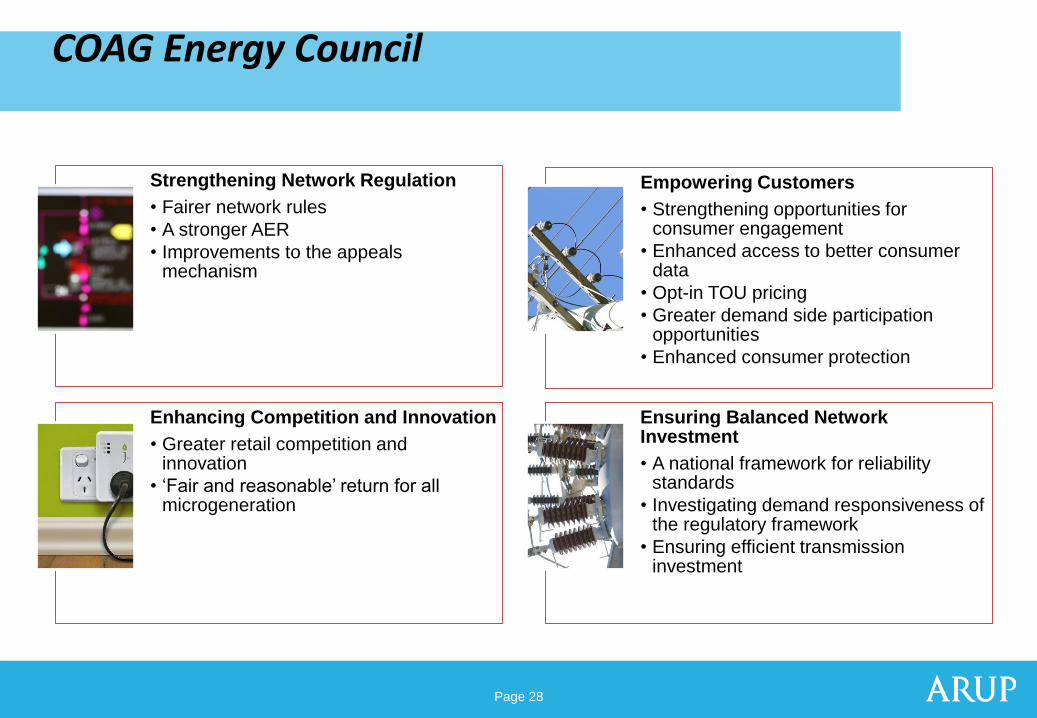

COAG Energy Council

Strengthening Network Regulation

• Fairer network rules

• A stronger AER

• Improvements to the appeals mechanism

Empowering Customers

• Strengthening opportunities for consumer engagement

• Enhanced access to better consumer data

• Opt-in TOU pricing

• Greater demand side participation opportunities

• Enhanced consumer protection

Enhancing Competition and Innovation

• Greater retail competition and innovation

• ‘Fair and reasonable’ return for all microgeneration

Ensuring Balanced Network Investment

• A national framework for reliability standards

• Investigating demand responsiveness of the regulatory framework

• Ensuring efficient transmission investment

Page 29 Page 29

Stakeholder priorities

Network impacts

Market impacts

Consumer impacts

Greenhouse gas impacts

Price

impacts

Page 30 Page 30

Conclusions and

recommendations

Page 31 Page 31

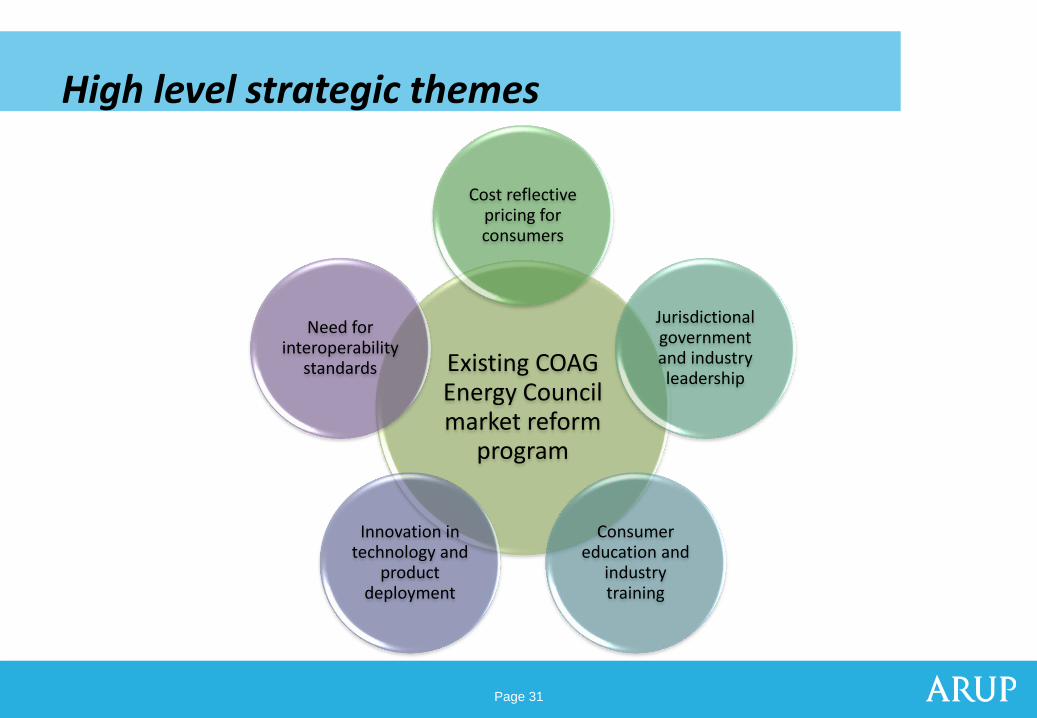

High level strategic themes

Existing COAG Energy Council market reform

program

Cost reflective pricing for consumers

Jurisdictional government and industry leadership

Consumer education and

industry training

Innovation in technology and

product deployment

Need for interoperability

standards

Page 32 Page 32

Fault Detection, Isolation & Restoration FDIR

• has the potential to deliver significant economic

benefits

• heavily dependent on the value of customer

reliability (currently being reviewed by AEMO)

Page 33 Page 33

Smart Meter Infrastructure (SMI)

• Two value propositions modeled:

• Full deployment, termed stand-alone

• Customer-led, with the smart grid

case assuming uptake with

installation of DG or DS

• Enabling infrastructure

Page 34 Page 34

SMI – (stand-alone or full deployment)

• Not yet economic (with the exception of some

long-rural network topologies in some states)

• Avoided billing, metering and customer service

costs for urban and short rural network not

sufficient to offset capital costs for SMI

Page 35 Page 35

SMI + Dynamic Tariffs + Cust Feedback

• Clear positive economic case for immediate

deployment of dynamic tariffs in Australia

(requiring SMI)

• If dynamic tariffs are voluntary, not all

customers will adopt the offer

Page 36 Page 36

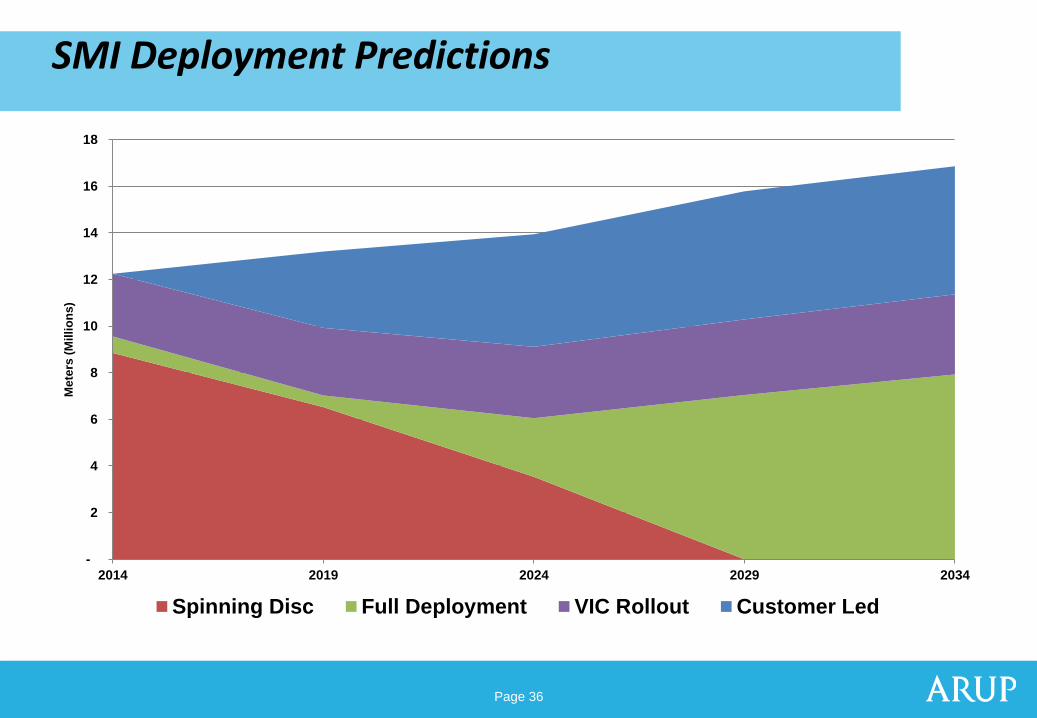

SMI Deployment Predictions

-

2

4

6

8

10

12

14

16

18

2014 2019 2024 2029 2034

Me

ters

(M

illi

on

s)

Spinning Disc Full Deployment VIC Rollout Customer Led

Page 37 Page 37

SMI + Dynamic Tariffs + Cust Feedback (2)

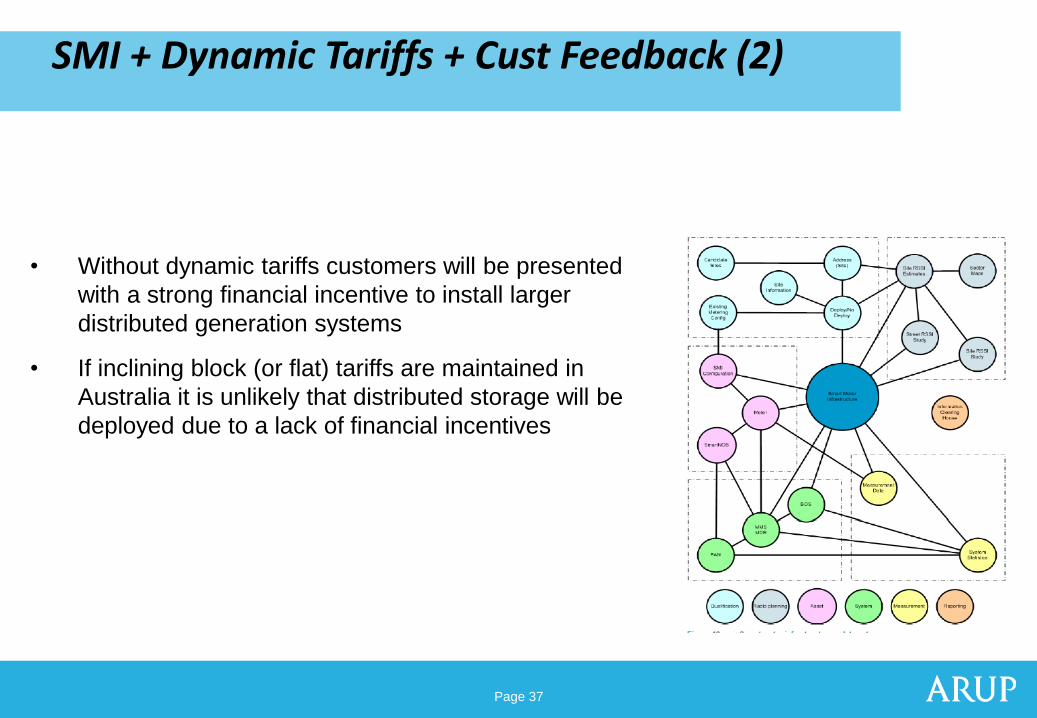

• Without dynamic tariffs customers will be presented

with a strong financial incentive to install larger

distributed generation systems

• If inclining block (or flat) tariffs are maintained in

Australia it is unlikely that distributed storage will be

deployed due to a lack of financial incentives

Page 38 Page 38

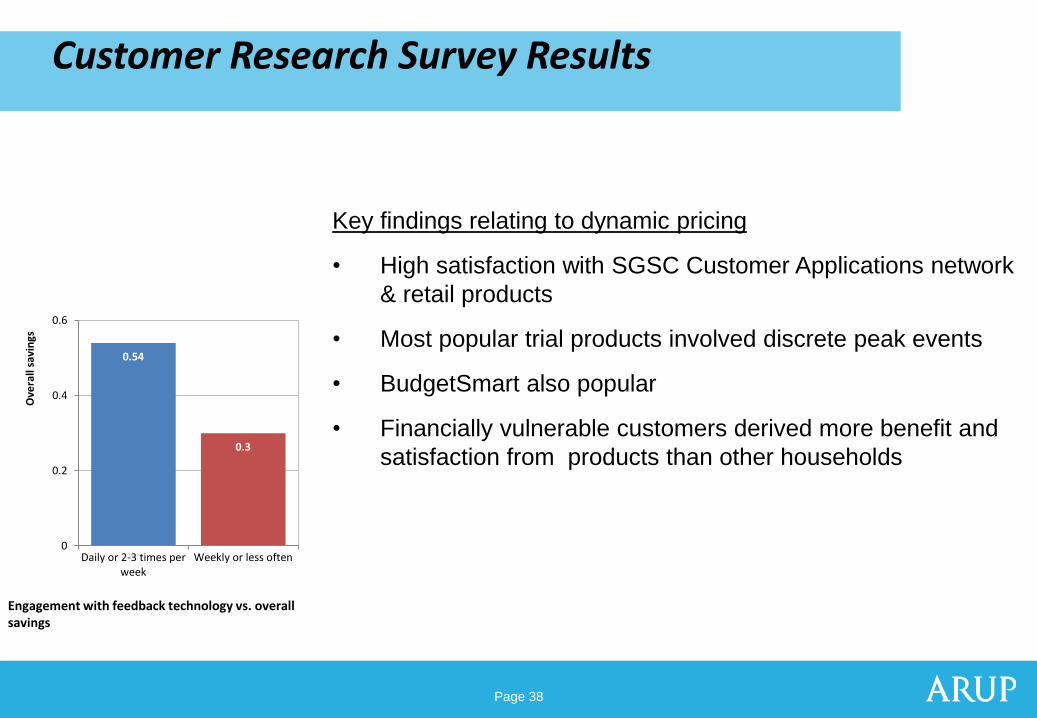

Customer Research Survey Results

Key findings relating to dynamic pricing

• High satisfaction with SGSC Customer Applications network

& retail products

• Most popular trial products involved discrete peak events

• BudgetSmart also popular

• Financially vulnerable customers derived more benefit and

satisfaction from products than other households

Engagement with feedback technology vs. overall savings

0.54

0.3

0

0.2

0.4

0.6

Daily or 2-3 times perweek

Weekly or less often

Ove

rall

savi

ngs

Page 39 Page 39

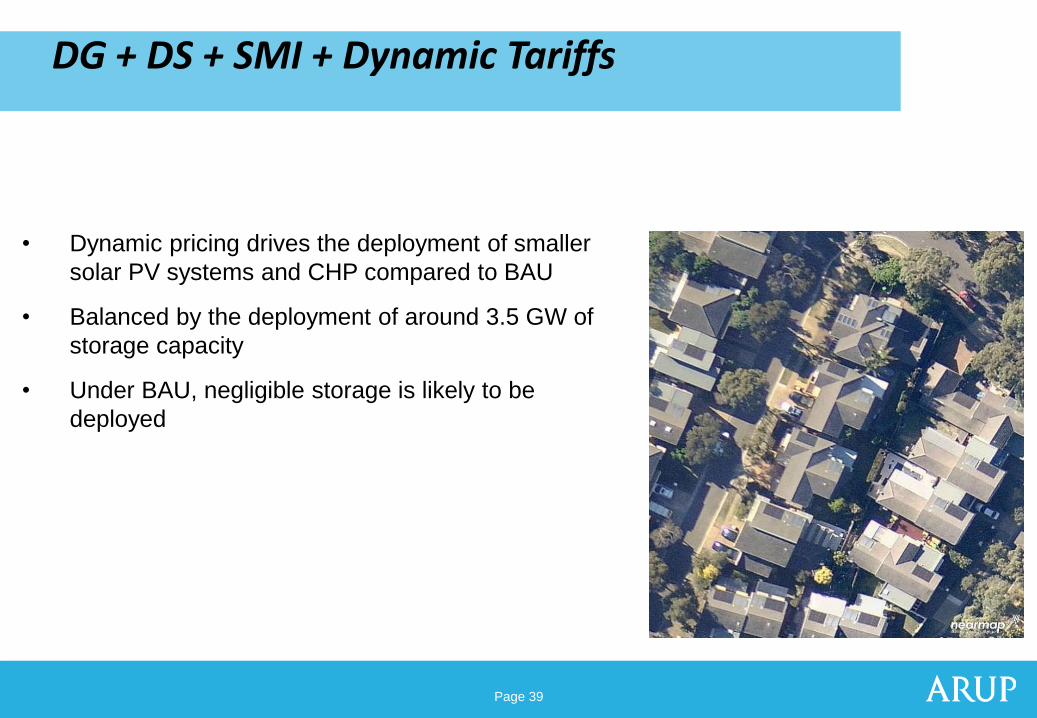

DG + DS + SMI + Dynamic Tariffs

• Dynamic pricing drives the deployment of smaller

solar PV systems and CHP compared to BAU

• Balanced by the deployment of around 3.5 GW of

storage capacity

• Under BAU, negligible storage is likely to be

deployed

Page 40 Page 40

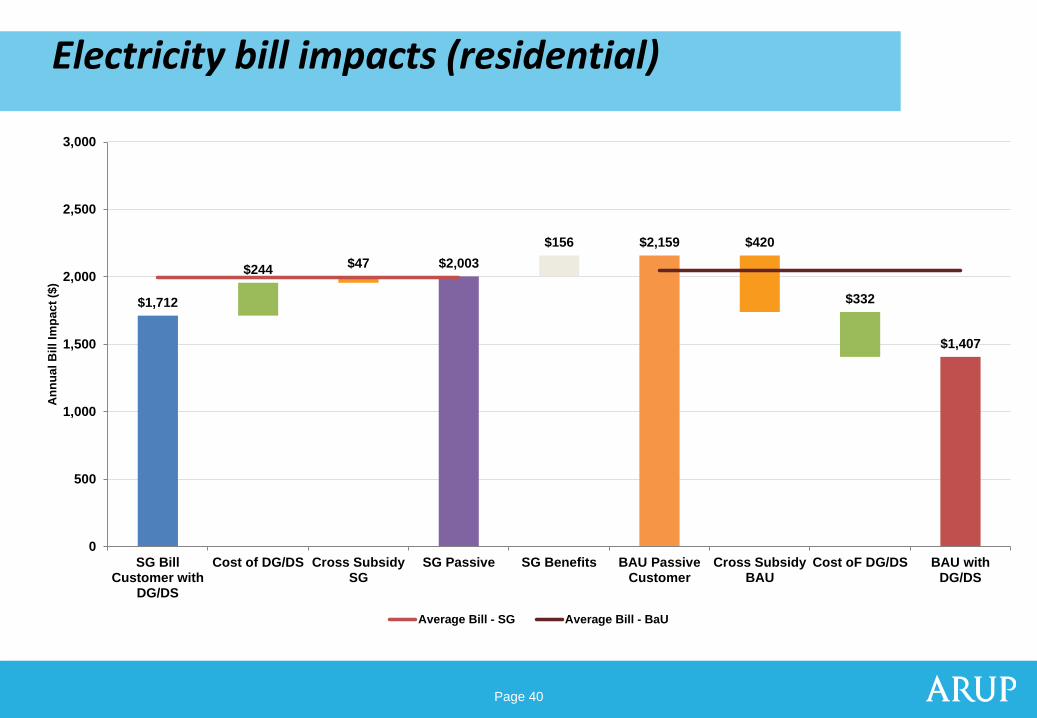

Electricity bill impacts (residential)

$1,712

$244 $47 $2,003

$156 $2,159 $420

$332

$1,407

0

500

1,000

1,500

2,000

2,500

3,000

SG BillCustomer with

DG/DS

Cost of DG/DS Cross SubsidySG

SG Passive SG Benefits BAU PassiveCustomer

Cross SubsidyBAU

Cost oF DG/DS BAU withDG/DS

An

nu

al

Bil

l Im

pa

ct

($)

Average Bill - SG Average Bill - BaU

Page 41 Page 41

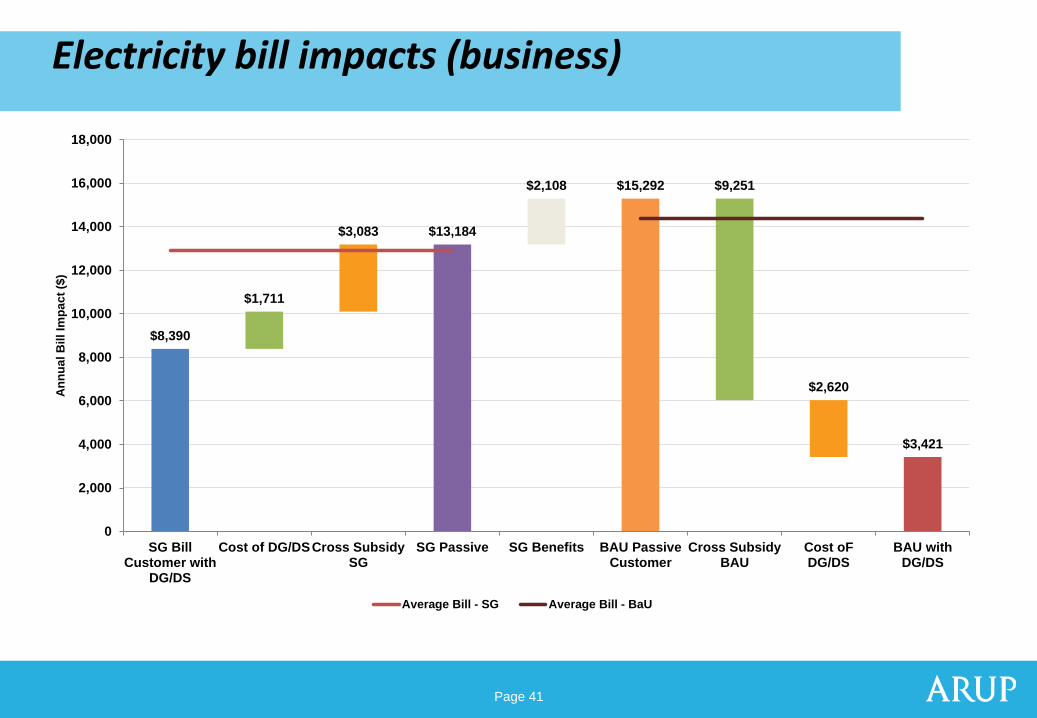

Electricity bill impacts (business)

$8,390

$1,711

$3,083 $13,184

$2,108 $15,292 $9,251

$2,620

$3,421

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

SG BillCustomer with

DG/DS

Cost of DG/DSCross SubsidySG

SG Passive SG Benefits BAU PassiveCustomer

Cross SubsidyBAU

Cost oFDG/DS

BAU withDG/DS

An

nu

al

Bil

l Im

pa

ct

($)

Average Bill - SG Average Bill - BaU

Page 42 Page 42

Transitioning to a smart grid future

Page 43 Page 43

Transitioning industry and consumers

• Balancing:

• Risks and opportunities from new smart grid

investment

• Financial, reliability and environmental benefits

and issues

• People

• Industry and electricity consumers -

understanding, education and change

Page 44 Page 44

Maximising the benefits and opportunities

• Need for interoperability standards

• Managing greater volumes of distributed generation

and introducing distributed storage

• Examining the business case for:

• Cost reflective consumer prices

• In-grid smart grid technologies

• Consumer feedback technologies

• Key costs and risks of inaction

Page 45

Post SGSC Developments

Page 46

Post SGSC Developments (1/2)

© Energeia 2014. All Rights Reserved

• AEMC Metering Contestability Rule Change (Ongoing, Draft

Determination due March 2015)

o Likely to be retailer lead

o Minimum functional spec likely to require smart metering

o New and replacements likely to include smart meter functionality

o Where there is a business case, retailers can roll out smart meters

• AEMC Distribution Network Pricing Draft Rule Determination (Aug 2014)

o Requires tariffs to be based on LRMC

o Networks already moving to capacity based tariffs (SA Power

Networks, Energex)

Page 47

Post SGSC Developments (2/2)

© Energeia 2014. All Rights Reserved

• AEMC Distribution Reliability Measures (September 2014)

o AER to develop reliability guidelines

o MAIFI increasing from 1 minute to 3 minutes

• AEMO Value Customer Reliability (October 2014)

o Residential values have not changed substantially since 2007/08

o Commercial values notably higher

Page 48

Thank You

Arup Energeia

Level 10

201 Kent Street

Sydney NSW 2000

Level 23 Gold Fields House

1 Alfred Street

Sydney NSW 2000

P +612 9320 9647

W www.arup.com

P +612 8097 0070

W www.energeia.com.au

![Smart Grid Laboratories Inventory 2016 - Europa · for the identification of Smart Grid Projects of Common Interest (PCI) [4], and the Cost Benefit Analysis of Smart Grid Projects](https://img.pdfslide.us/doc/110x75/5f87de09559f9076a1599691/smart-grid-laboratories-inventory-2016-europa-for-the-identification-of-smart.jpg)

![[Smart Grid Market Research] Smart Grid Index: November 2012 - Zpryme Smart Grid Insights](https://img.pdfslide.us/doc/110x75/541402018d7f728a698b47a5/smart-grid-market-research-smart-grid-index-november-2012-zpryme-smart-grid-insights.jpg)

![[Smart Grid Market Research] India: Smart Grid Legacy, Zpryme Smart Grid Insights, September 2011](https://img.pdfslide.us/doc/110x75/541402518d7f7294698b47d4/smart-grid-market-research-india-smart-grid-legacy-zpryme-smart-grid-insights-september-2011.jpg)

![[Smart Grid Market Research] Brazil: The Smart Grid Network, Zpryme Smart Grid Insights, October 2011](https://img.pdfslide.us/doc/110x75/577d20871a28ab4e1e931ff6/smart-grid-market-research-brazil-the-smart-grid-network-zpryme-smart-grid.jpg)