Embed Size (px)

Citation preview

Fiscal Sustainability The views expressed in this presentation are those of Messrs Vaudt, Bean, and Carruthers. Official positions of the GASB and IPSASB on accounting matters are determined only after extensive due process and deliberation.

1

OECD Accruals Symposium

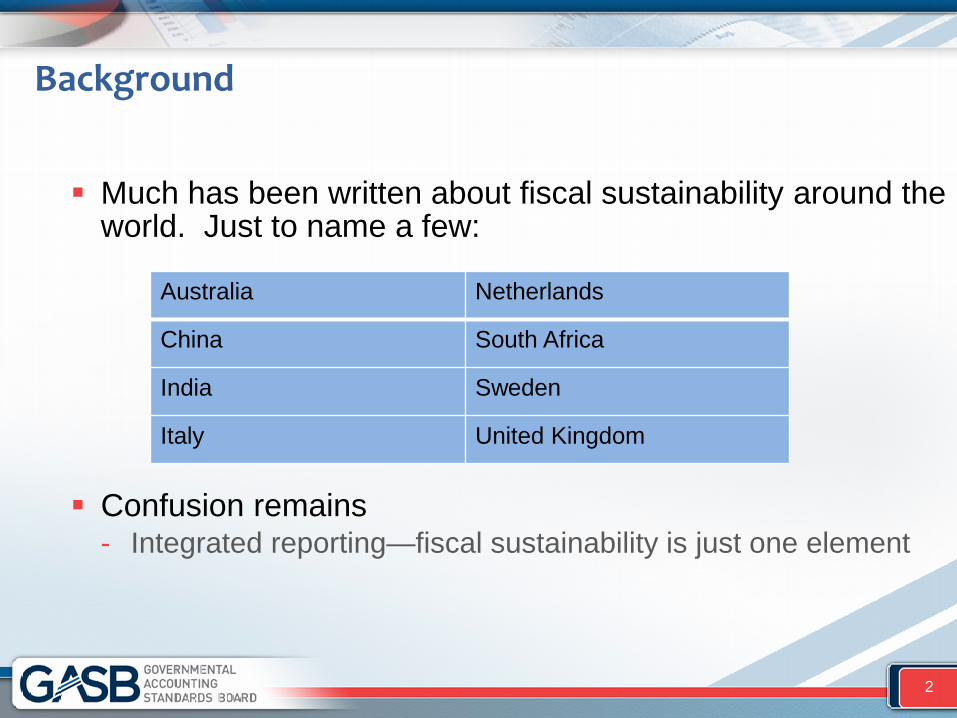

Background

Much has been written about fiscal sustainability around the world. Just to name a few:

Confusion remains - Integrated reporting—fiscal sustainability is just one element

2

Australia Netherlands

China South Africa

India Sweden

Italy United Kingdom

Goals of this Session

Discuss fiscal sustainability—what is it and how it should be reported - IPSASB RPG - GASB efforts, including assessment of state government

monitoring - UK Government experience - Open discussion

3

IPSASB RPG

Ian Carruthers IPSASB Member Executive Director, Policy and Technical, CIPFA

Public Sector Conceptual Framework

• Primary service delivery objective

• Importance of accountability

• General Purpose Financial Reports (GPFRs) – broader than General Purpose Financial Statements

• IPSASB developing Recommended Practice Guidelines (RPGs) for GPFRs

• Good practice - not required to assert IPSAS compliance

5

Reporting on the Long-Term Sustainability of an Entity’s Finances Objective •Provide indication of projected sustainability of entity’s finances over specified time horizon in accordance with stated assumptions.

Status and Scope •Recommended Practice Guideline (RPG1)

•Doesn’t directly address environmental sustainability

•Includes entity’s future financial flows across all areas

6

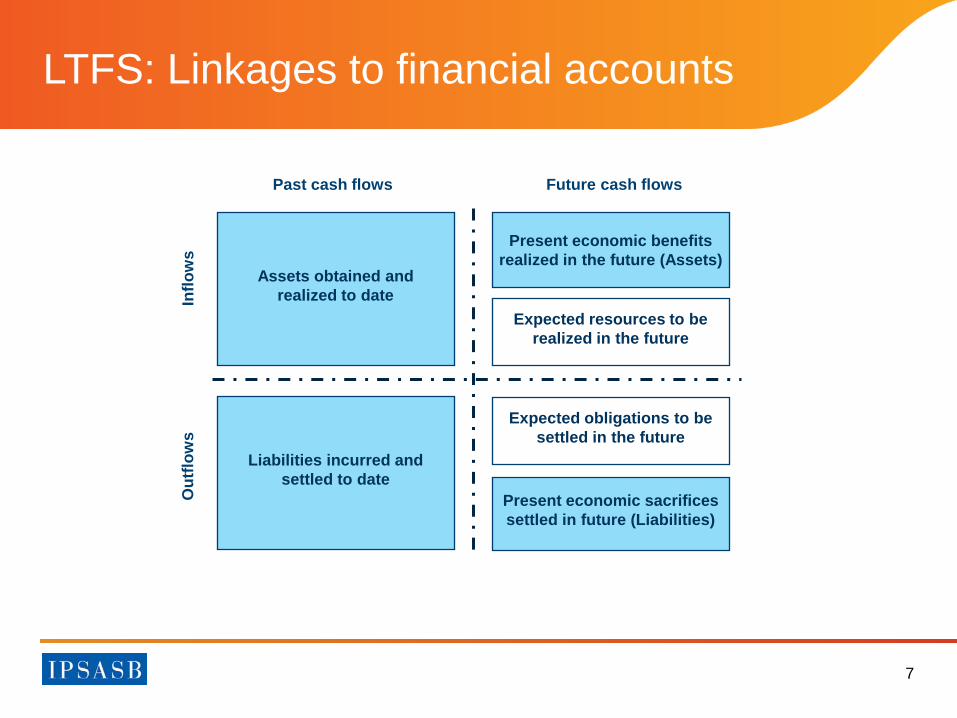

LTFS: Linkages to financial accounts

Future cash flows Past cash flows

Liabilities incurred and settled to date

Assets obtained and realized to date In

flow

s O

utflo

ws

Present economic sacrifices settled in future (Liabilities)

Present economic benefits realized in the future (Assets)

Expected resources to be realized in the future

Expected obligations to be settled in the future

7

Reporting LTFS information

• Long-Term Fiscal Sustainability (LTFS) definition: Ability of an entity to meet service delivery and financial

commitments both now and in the future • Form and content of reporting dependent on entity • May be part of GPFRs or separate report • Draw on wide range of information sources • Current policy, demographic and economic assumptions • Projection time horizons reflect entity characteristics

– Longevity of key programmes – Dependence on other entities for funding

8

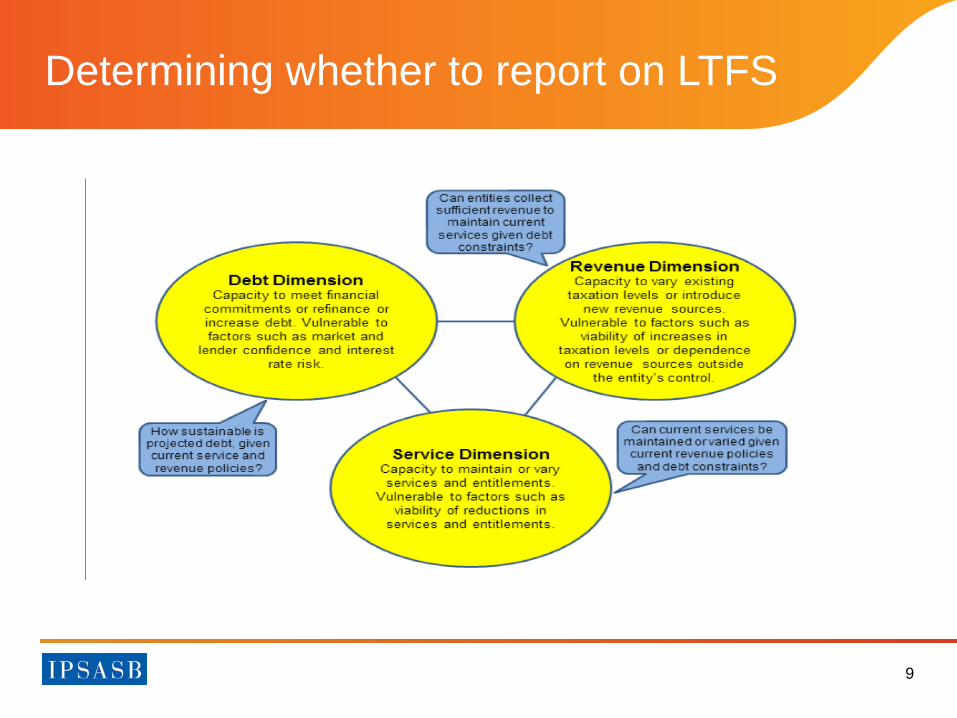

Determining whether to report on LTFS

9

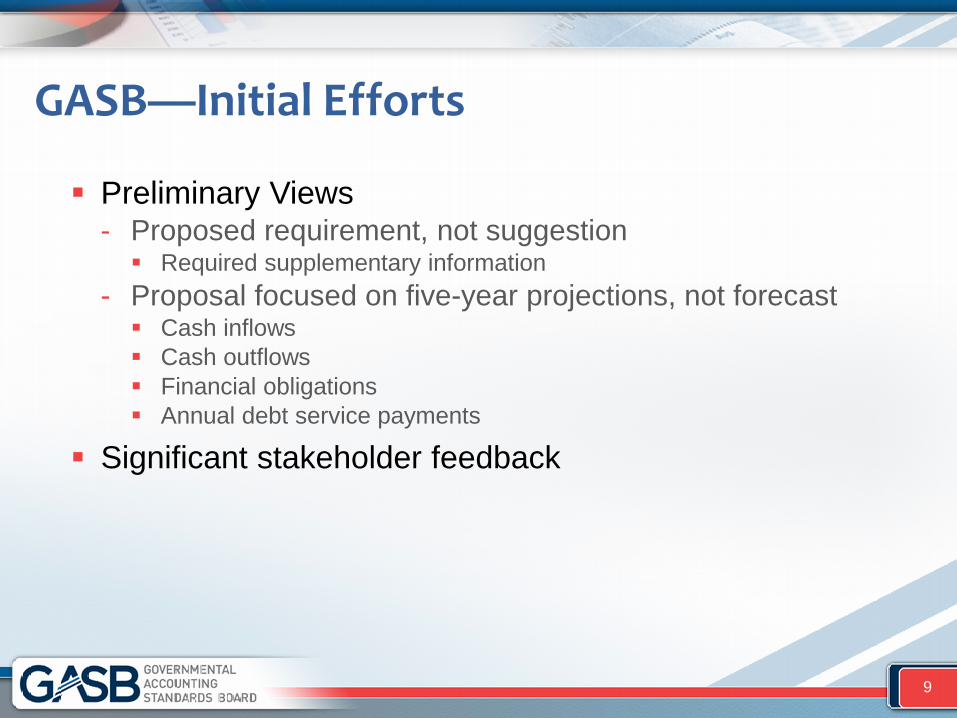

GASB—Initial Efforts

Preliminary Views - Proposed requirement, not suggestion Required supplementary information

- Proposal focused on five-year projections, not forecast Cash inflows Cash outflows Financial obligations Annual debt service payments

Significant stakeholder feedback

9

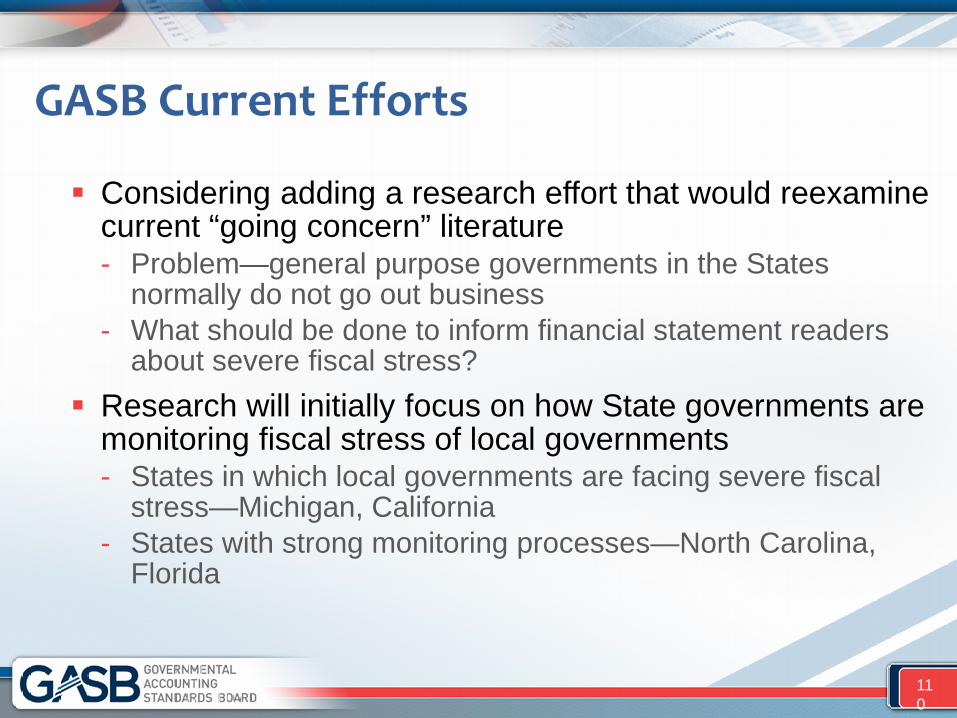

GASB Current Efforts

Considering adding a research effort that would reexamine current “going concern” literature - Problem—general purpose governments in the States

normally do not go out business - What should be done to inform financial statement readers

about severe fiscal stress? Research will initially focus on how State governments are

monitoring fiscal stress of local governments - States in which local governments are facing severe fiscal

stress—Michigan, California - States with strong monitoring processes—North Carolina,

Florida

110

Just the Beginning

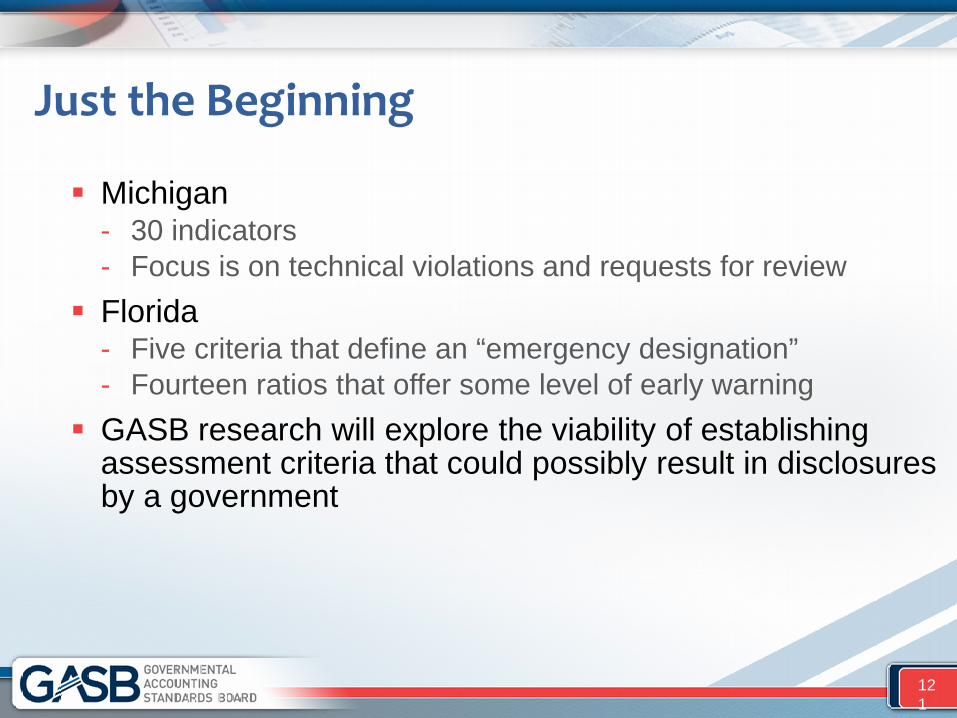

Michigan - 30 indicators - Focus is on technical violations and requests for review

Florida - Five criteria that define an “emergency designation” - Fourteen ratios that offer some level of early warning

GASB research will explore the viability of establishing assessment criteria that could possibly result in disclosures by a government

121

UK Government Experience Long-term projections in fiscal policy

Ian Carruthers Executive Director, Policy and Technical, CIPFA IPSASB Member

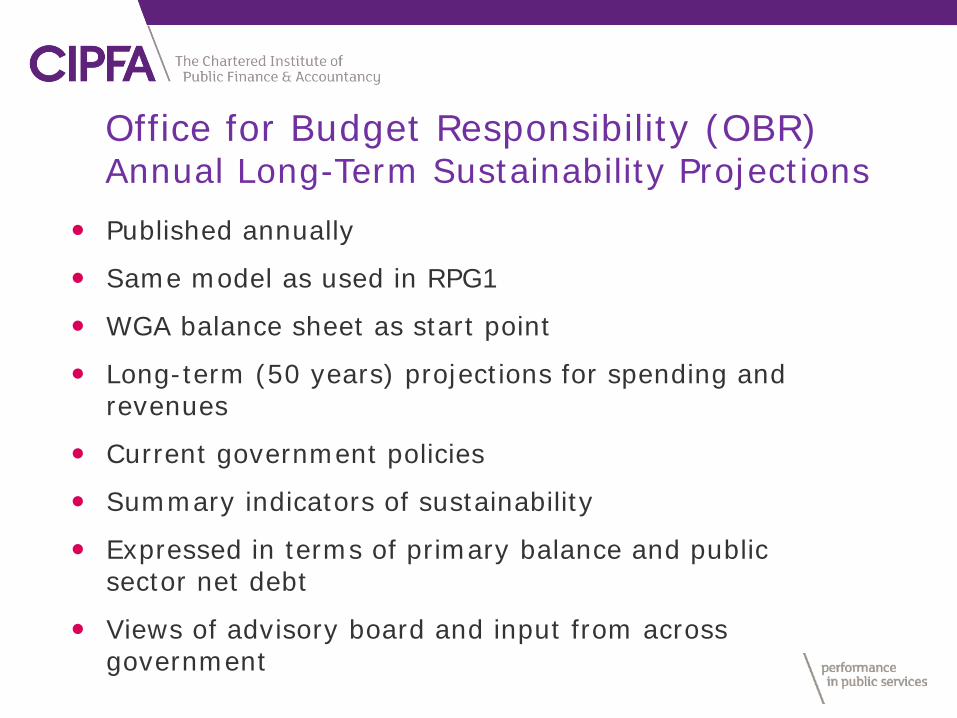

Office for Budget Responsibility (OBR) Annual Long-Term Sustainability Projections

Published annually

Same model as used in RPG1

WGA balance sheet as start point

Long-term (50 years) projections for spending and revenues

Current government policies

Summary indicators of sustainability

Expressed in terms of primary balance and public sector net debt

Views of advisory board and input from across government

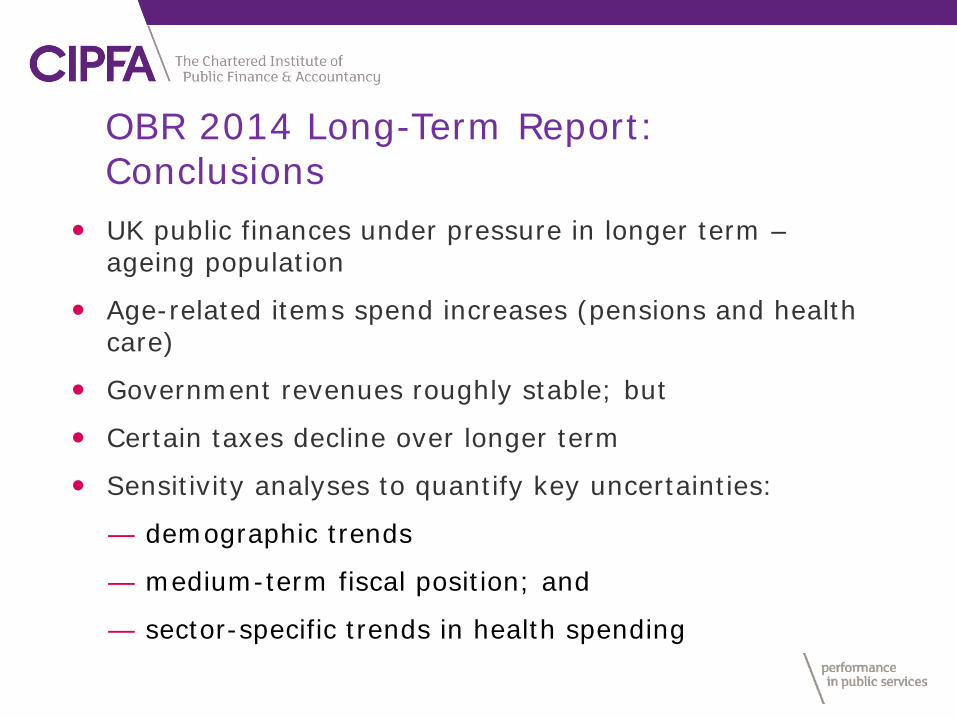

UK public finances under pressure in longer term –ageing population

Age-related items spend increases (pensions and health care)

Government revenues roughly stable; but

Certain taxes decline over longer term

Sensitivity analyses to quantify key uncertainties:

— demographic trends

— medium-term fiscal position; and

— sector-specific trends in health spending

OBR 2014 Long-Term Report: Conclusions

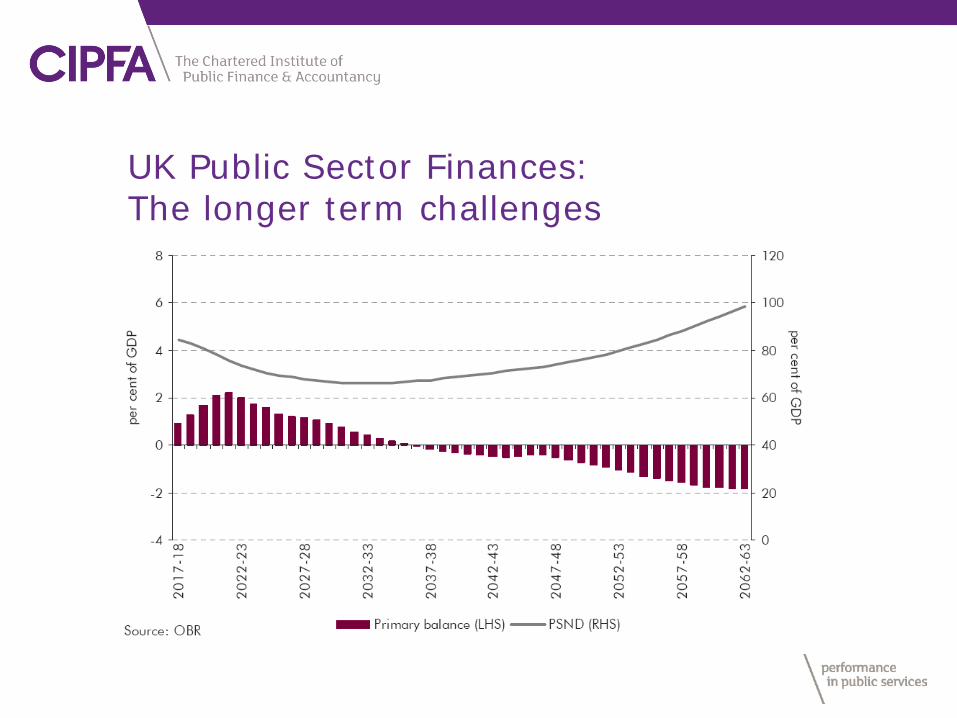

UK Public Sector Finances: The longer term challenges

What Is Being Done Around the World? How are governments currently monitoring potential local

government fiscal stress? How are government currently reporting instances of fiscal

stress?

17