Embed Size (px)

Citation preview

Comparing the use of consolidated public sector accounts

Danny Chow (Durham University, UK) Ronald Day (University of Sydney, Australia) Caroline Aggestam (Copenhagen Business School, Denmark) Raili Pollanen (Carleton University, Canada) Rachel Baskerville (Victoria University Wellington, New Zealand)

Comparing the use of consolidated public sector

accounts

Outline

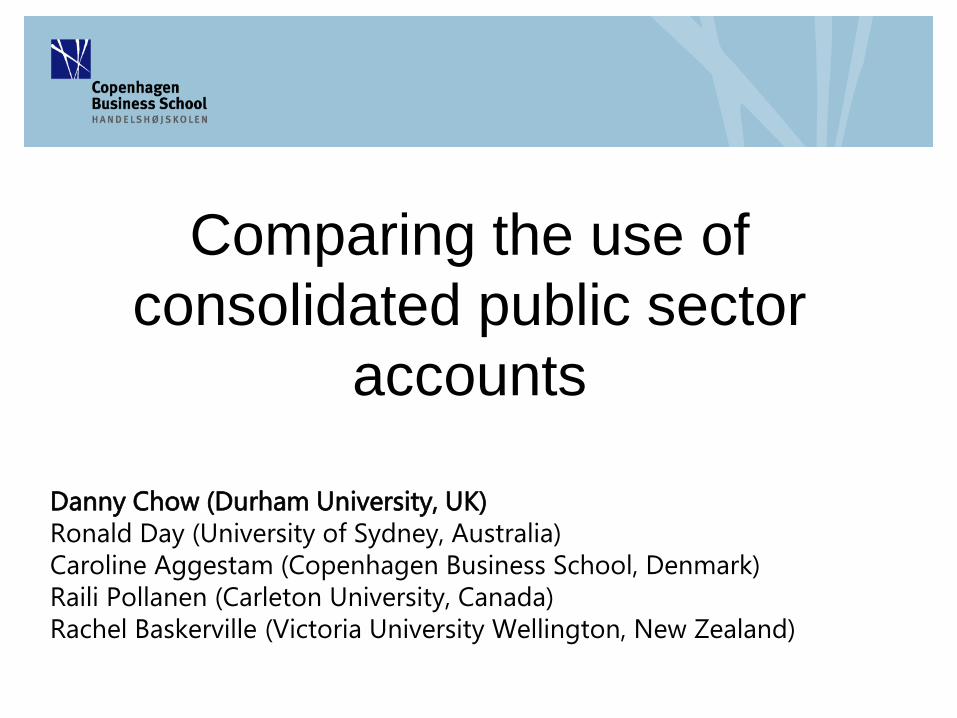

• Understand how and who uses consolidated public accounts across the selected case-countries

Focus

• Comparing the use of consolidated public sector accounts in five countries: UK, Australia, New Zealand, Canada and Sweden

Scope

• Qualitative methods and document reviews • 2014/2015

How & When

This presentation presents the high-level indicative findings of the study

Focus

• The focus of the study: Understand how, why, when and by whom consolidated public sector accounts are used.

• The use of accounting information can be related to internal and external users.

• In the public sector, external users are primarily emphasizing the control function of accounting, while internal users, in addition to that, could benefit from using accounting information as an input in various decision making processes.

How? Research methods

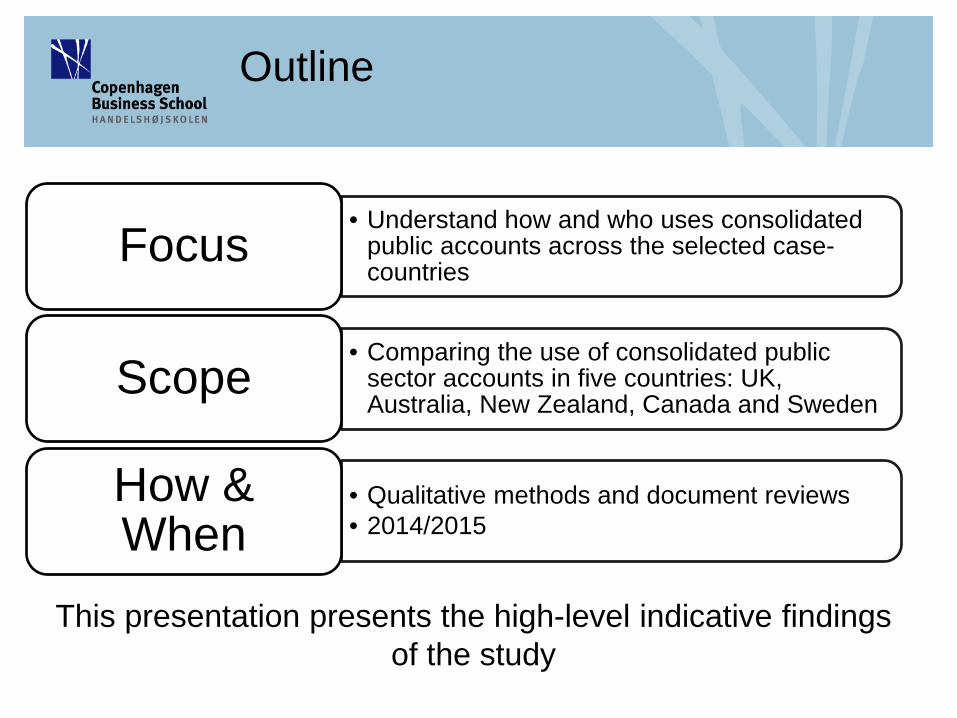

• Previous research on the use of accrual accounting information in the central government in Sweden showed that our understanding of the use of accounting information is closely related to the research method that is chosen (cf. Paulsson, 2006).

• Example: In survey studies in Sweden it had been indicated by the respondents that accrual accounting information was not used to a large extent.

• However, research has shown that the interview study, provided more subtle dimensions of the concept of use and it became evident that accounting information actually was used, although not in the most conventional meaning.

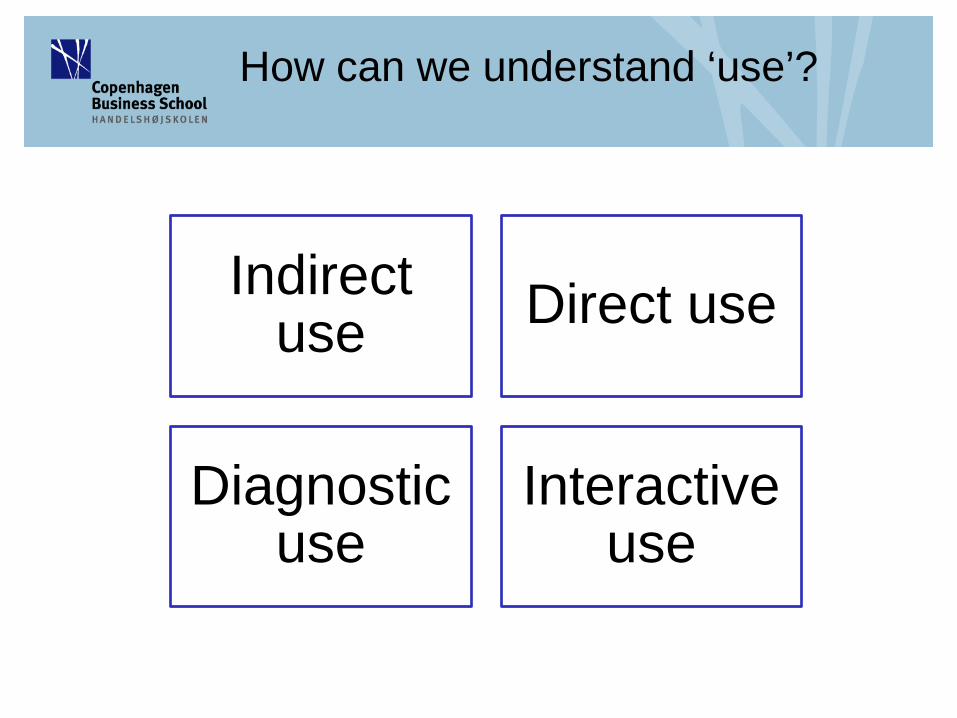

How can we understand ‘use’?

Indirect use Direct use

Diagnostic use

Interactive use

The starting point

• Reviewing how consolidations are done across the case countries

• Finding: Consolidation practices differs in each of the included countries

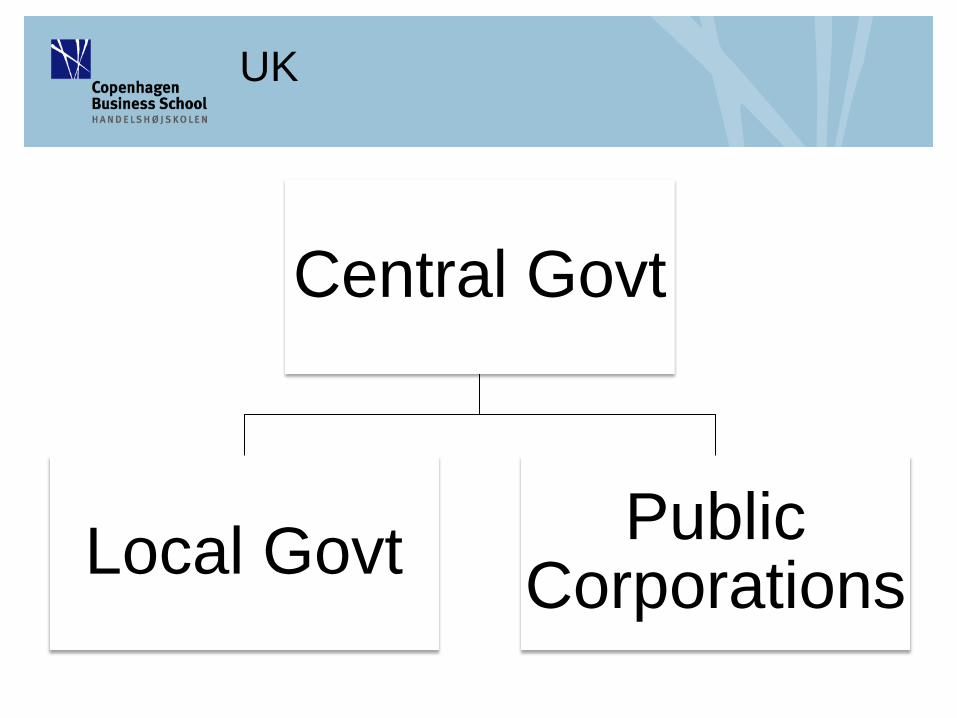

UK

Central Govt

Local Govt Public Corporations

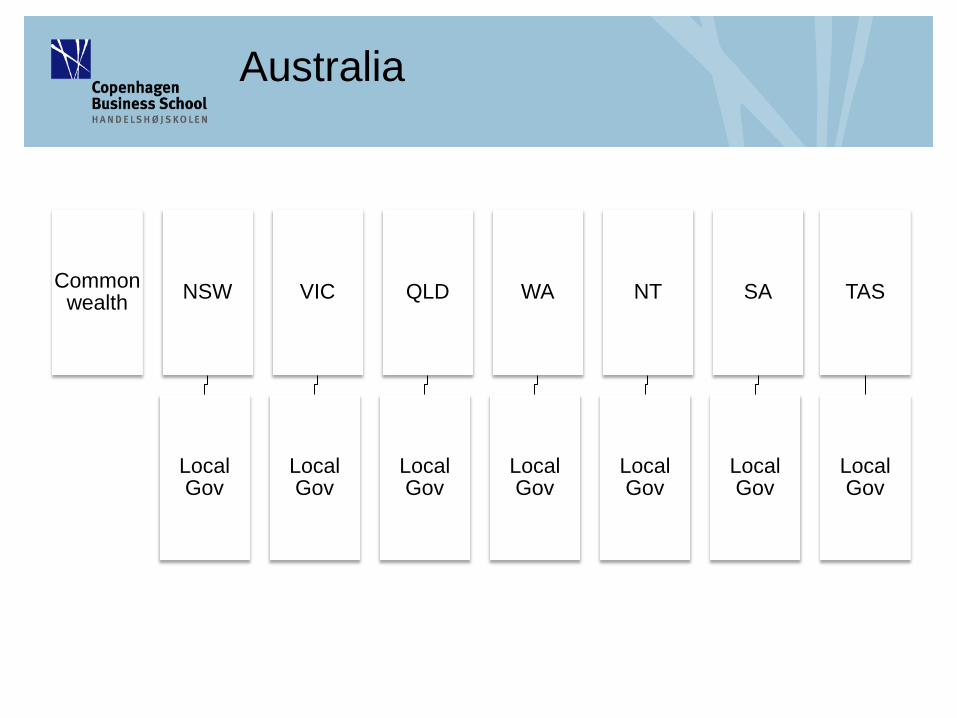

Australia

Commonwealth NSW

Local Gov

VIC

Local Gov

QLD

Local Gov

WA

Local Gov

NT

Local Gov

SA

Local Gov

TAS

Local Gov

New Zealand

Central Govt

Local Govt

Canada

Federal

States & Territories

Local

Sweden

Central Govt

Local Govt

High level conclusions

• International variation • Dependent on ‘organisation’ of government

• Local Solutions / Adaptations

Indicative findings per case country

UK

• Still primarily prepared as a statutory requirement and consequently only limited use by a small coterie of interested individuals who use WGA as a platform for broader discussions over the government's management and accountability for public finances.

• Scepticism about how useful WGA is, in part due to audit

qualifications on some entity accounts and lack of timely publication.

UK

• Some evidence that WGA is being used at the periphery for thinking about policy implications on taking on more debt. Recognised that WGA presents a sound picture of debt.

• Also it has been noted that Office for Budget Responsibility making use of WGA to forecast ahead

• It was highlighted that the accounts are written from the perspective of an accountant, so this precludes many non-specialist

UK

• WGA as a catalyst to persuade government departments to do better accounting to improve internal decision making and external accountability

• Credit rating agencies use WGA to a limited extent

• Treasury highlighted the value of WGA over national accounts especially around assets and liabilities; noted that WGA also helps to improve the evaluation of fiscal risk

Australia

• Key Treasury/Finance staff and politicians indicated only a vague understanding of the rationale and reporting frameworks

• Politicians have no training on reading and understanding WGA reports (Little to no training or background given, except on the job training)

• However…

Australia

Participants agreed that WGA reports have some benefits for ‘users’

• WGA reports include a balance sheet which provides more

recognition of future problems not just current problems this year.

• In Australia, it enables a set of financial statements to be prepared that broadly incorporate both the statistical and accounting requirements

• However…

Australia

General agreement among participants that there is a relatively low use of WGA reports partly because they are not user friendly or accessible • CFS (WGA) is more specific purpose than general purpose

reports.

• There is not much interest in them from the point of view of the public, with very little to no attention in the press about the CFS (WGA) reports

• There is little to no discussion on the balance sheet side of the financial report

Australia

• Focus of parliamentarians and other interest groups is on the budget numbers rather than the WGA accounting numbers;

• Credit ratings are a key driver for Governments, but credit rating agencies use WGA info in a small category and proportion of their assessment

Canada

• It was identified that the implementation of accrual accounting is seen as the single (or the only) most important accounting/financial reporting initiative in many decades.

• Another recent significant development was a requirement to establish

departmental audit committees, which brought additional independent oversight over departmental financial reporting and management.

• Consolidated government-wide financial statements are seen by most participants only as an external accountability tool for complying with legal and professional requirements.

Canada

• Departmental plans and priorities reports and departmental performance reports are major accountability tools to Parliament. Consolidated government-wide financial statements do not reportedly play a major role for such purposes.

• Different information needs of different stakeholders were expressed by most participants. Nonetheless, all participants agreed that financial accounting and reporting in Canadian governments has improved greatly in the past decade at all levels.

Canada

• Specific users of consolidated government-wide financial statements were difficult to identify and verify. For example, several individuals, even those referred to by others as experts or potential major users, did not seemingly consider themselves as experts.

Sweden

• User perspective integrated from the very beginning of the adoption of accrual accounting in the public sector

• Co-operation with academia during the adoption of accrual accounting at the local level (accrual accounting was first adopted at the local level and later at central government level)

• Consolidation was not seen as a separate ‘wished for’ target – it was more a side product that came out of the adoption of accrual accounting

• For most users the consolidation in two tiers (central /local) make more sense than WGA

Sweden

• Users see the timeliness of the consolidated accounts as a key factor. In Sweden central government consolidated accounts are released within 4 months of year-end. This was seen beneficial in terms of enabling use of the accounts.

• Finance-committee as a standard practice considers the consolidated financial statements at its June meeting every year

Sweden

• Finance committee plays an imperative role in the ‘use’ of the consolidated accounts. Outside the finance committee few considered themselves able to read an understand the consolidated accounts of central government

• Even though there was a consensus among users that the accounts were used, some respondents elaborated that they still were used only at the minimal level in comparison with for example budget

Direct • Finance committee / Parliamentarians • Treasury • External (e.g., Credit Rating Agencies)

Indirect • Catalyst for Change

Summarising Thoughts

• The notion of Use is subjective and highly dependent on how/why/by whom that is considering ‘use’. Conceptualise the concept of ‘use’ may assist the process

• From, for example, the preparers and auditors, it was observed across the countries that WGA is useful as it helps to catalyse other laggard organisations within government / public sector to do better accounting and also to professionalise the accounting service within government / public sector to do better accounting and also to professionalise the accounting service.

Summarising Thoughts

• Other users would, for example, consider of the use of

WGA as a platform for broader discussions over the government's management and accountability for public finances, but saw factors as the user-friendliness and timeliness as obstacles for use

Summarising Thoughts

Summarising Thoughts

• Governments need to consider how consolidated accounts (if prepared) can be used to strenghten fiscal transparency and accountability

• Consider training and education on the use of consolidated accounts

• Join up planning, annual budgeting and year end reporting information rather than treating as separate exercises

Summarising Thoughts

The consolidated reports across the countries can be improved

For example:

• producing a summary form (eg. In UK tried to do a 4 page report)

• demystify them by simplifying them and making them understandable to the public (and politicians) rather than just a few people

• Having some forward looking information if you are looking at risk is important and a bit of economic impact of any big expenditure items to happen in the immediate future, if not longer term

• Different levels of information that modern technology now allows