Embed Size (px)

Citation preview

Restaurant Valuation

Part Art / Part Science

December 2, 2014

Everyone has an opinion of value:

• The bookkeeper

• The owner

• The owner’s spouse

• The owner’s ex-spouse

• The owner’s parents

• The auditor

• The tax preparer

2

Standard of Value

Purpose or need for the valuation

• Merger or acquisition

• Family gifting

• Estate tax

• Divorce

• Shareholder oppression / dissent

• Damages

• Bankruptcy

• Shareholder agreements

• Income Tax

• Financial statement reporting

3

Standard of Value

• Fair Market Value

• Investment Value

• Fair Value

4

Standard of Value

• Going Concern Value

• Liquidation Value:

Orderly

Forced

5

Premise of Value

VALUATION THEORY

6

FINANCIAL STATEMENT

ANALYSIS

7

• True Economic Income

• Recasting / Normalizing P&L

• Normalizing Balance Sheet

• Comparative common size normalized and industry

comparison

8

Cash Flows

Source: Statement on Standards for Valuation Services #1, AICPA, June 2007

• Market Level Compensation

• Perquisites

• Market Rent (Above/Below)

• Non-recurring revenue and expense items

• POS Cash Register Info

9

Normalization Adjustments

VALUATION APPROACHES

10

• Cost Approach

• Income Approach

• Market Approach

11

Common Valuation Approaches

• Most pertinent where a company’s value is tied directly

to the value of its underlying assets.

• Generally not appropriate for restaurants because

intangible assets are not considered

12

Cost Approach

• Expectation

• Requires the determination of a company’s

representative earning power which is then discounted

back to a present value.

13

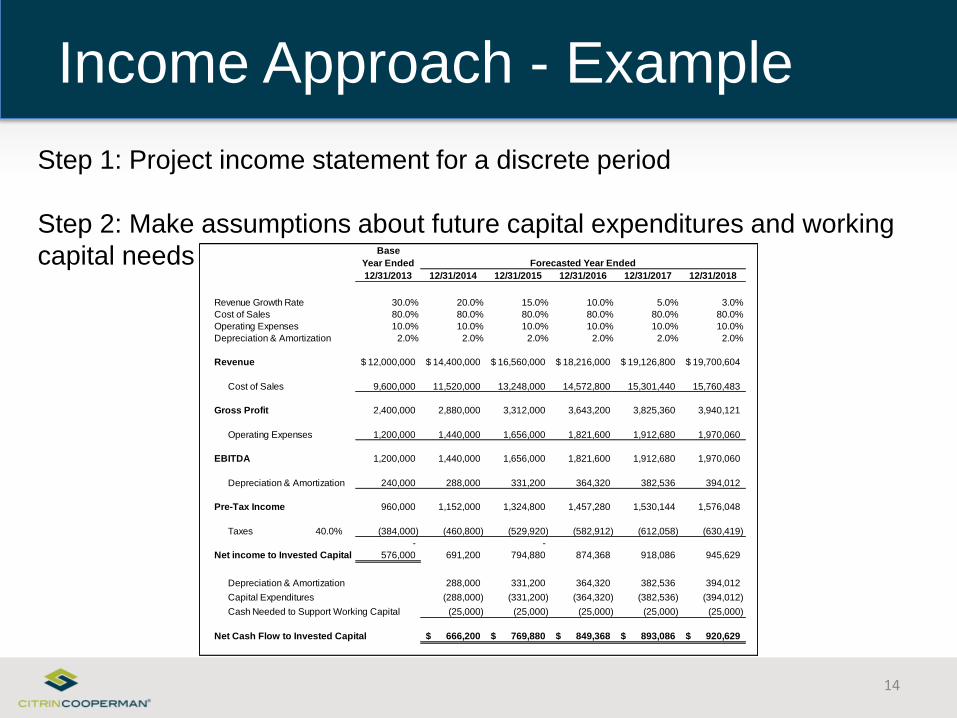

Income Approach

Step 1: Project income statement for a discrete period

Step 2: Make assumptions about future capital expenditures and working

capital needs

14

Income Approach - Example

Base

Year Ended

12/31/2013 12/31/2014 12/31/2015 12/31/2016 12/31/2017 12/31/2018

Revenue Growth Rate 30.0% 20.0% 15.0% 10.0% 5.0% 3.0%

Cost of Sales 80.0% 80.0% 80.0% 80.0% 80.0% 80.0%

Operating Expenses 10.0% 10.0% 10.0% 10.0% 10.0% 10.0%

Depreciation & Amortization 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

Revenue 12,000,000$ 14,400,000$ 16,560,000$ 18,216,000$ 19,126,800$ 19,700,604$

Cost of Sales 9,600,000 11,520,000 13,248,000 14,572,800 15,301,440 15,760,483

Gross Profit 2,400,000 2,880,000 3,312,000 3,643,200 3,825,360 3,940,121

Operating Expenses 1,200,000 1,440,000 1,656,000 1,821,600 1,912,680 1,970,060

EBITDA 1,200,000 1,440,000 1,656,000 1,821,600 1,912,680 1,970,060

Depreciation & Amortization 240,000 288,000 331,200 364,320 382,536 394,012

Pre-Tax Income 960,000 1,152,000 1,324,800 1,457,280 1,530,144 1,576,048

Taxes 40.0% (384,000) (460,800) (529,920) (582,912) (612,058) (630,419)

- -

Net income to Invested Capital 576,000 691,200 794,880 874,368 918,086 945,629

Depreciation & Amortization 288,000 331,200 364,320 382,536 394,012

Capital Expenditures (288,000) (331,200) (364,320) (382,536) (394,012)

Cash Needed to Support Working Capital (25,000) (25,000) (25,000) (25,000) (25,000)

Net Cash Flow to Invested Capital 666,200$ 769,880$ 849,368$ 893,086$ 920,629$

Forecasted Year Ended

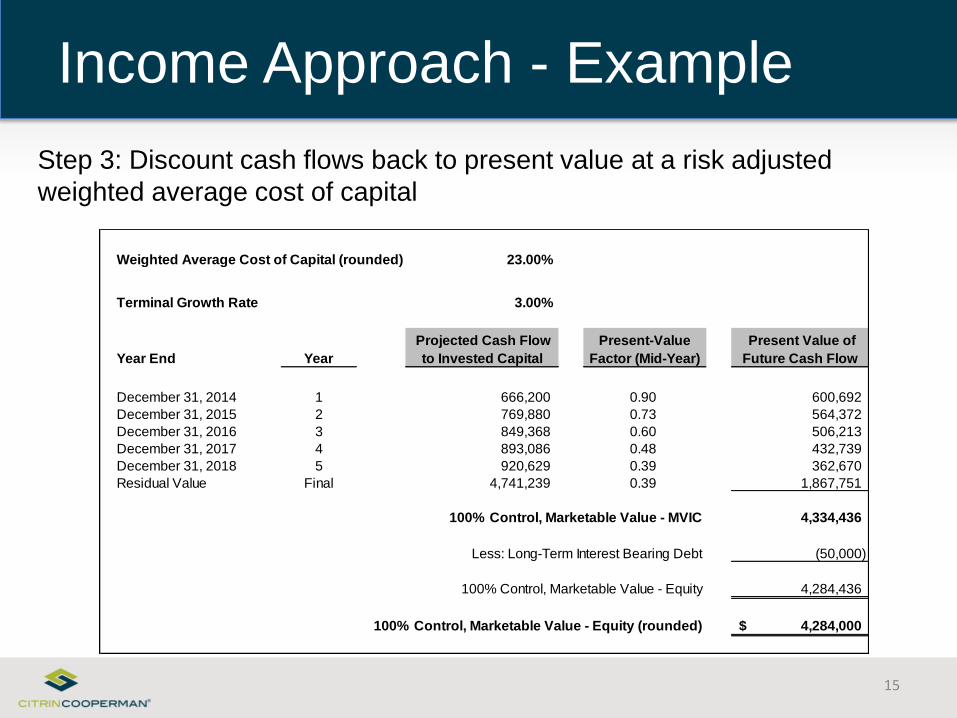

Step 3: Discount cash flows back to present value at a risk adjusted

weighted average cost of capital

15

Income Approach - Example

Weighted Average Cost of Capital (rounded) 23.00%

Terminal Growth Rate 3.00%

Year End Year

December 31, 2014 1 666,200 0.90 600,692

December 31, 2015 2 769,880 0.73 564,372

December 31, 2016 3 849,368 0.60 506,213

December 31, 2017 4 893,086 0.48 432,739

December 31, 2018 5 920,629 0.39 362,670

Residual Value Final 4,741,239 0.39 1,867,751

100% Control, Marketable Value - MVIC 4,334,436

Less: Long-Term Interest Bearing Debt (50,000)

100% Control, Marketable Value - Equity 4,284,436

100% Control, Marketable Value - Equity (rounded) 4,284,000$

Projected Cash Flow

to Invested Capital

Present-Value

Factor (Mid-Year)

Present Value of

Future Cash Flow

• Ranking

• Compares publicly traded businesses or comparable

private and public company transactions in similar

industries and financial positions and applies implied

multiples to the subject company

16

Market Approach

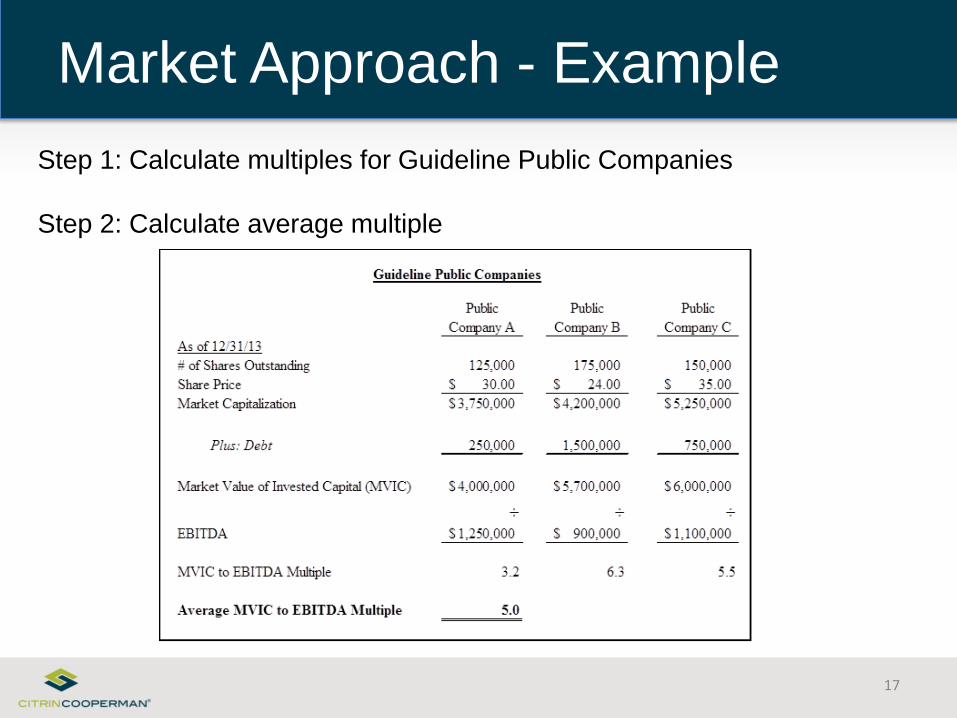

Step 1: Calculate multiples for Guideline Public Companies

Step 2: Calculate average multiple

17

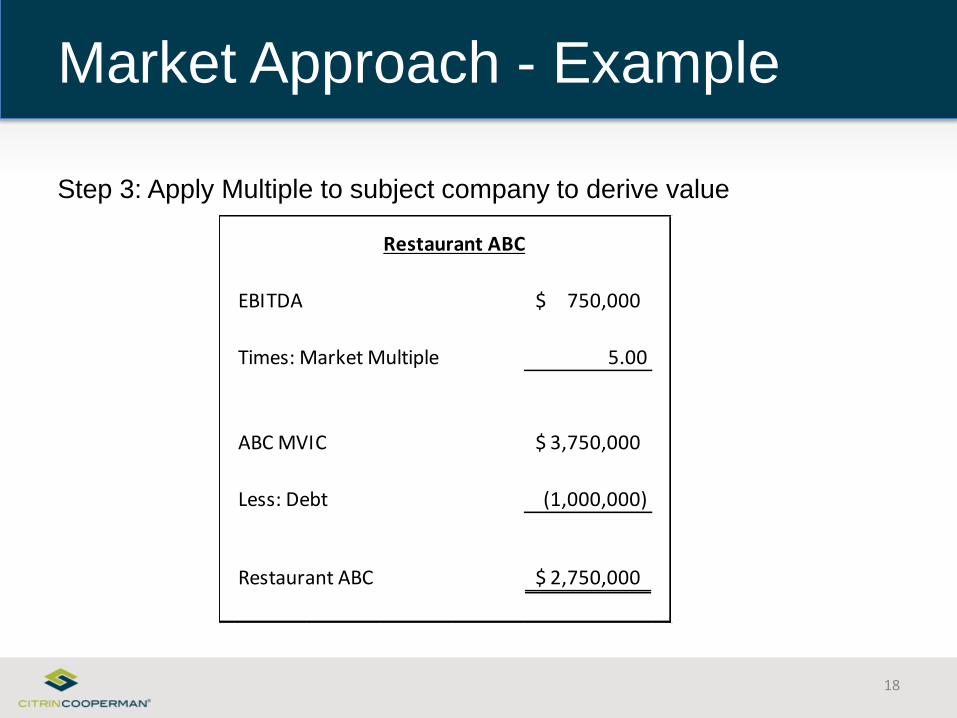

Market Approach - Example

Step 3: Apply Multiple to subject company to derive value

18

Market Approach - Example

Restaurant ABC

EBITDA 750,000$

Times: Market Multiple 5.00

ABC MVIC 3,750,000$

Less: Debt (1,000,000)

Restaurant ABC 2,750,000$

• Technically not a valuation method.

• Prevalent in the restaurant industry.

• Vary among different types of restaurants.

• Typically used as a reasonableness check.

19

Rules of Thumb

Source: BVR’s Guide to Restaurant Valuation, by Edward Moran, Business Valuation Resources, LLC, 2010

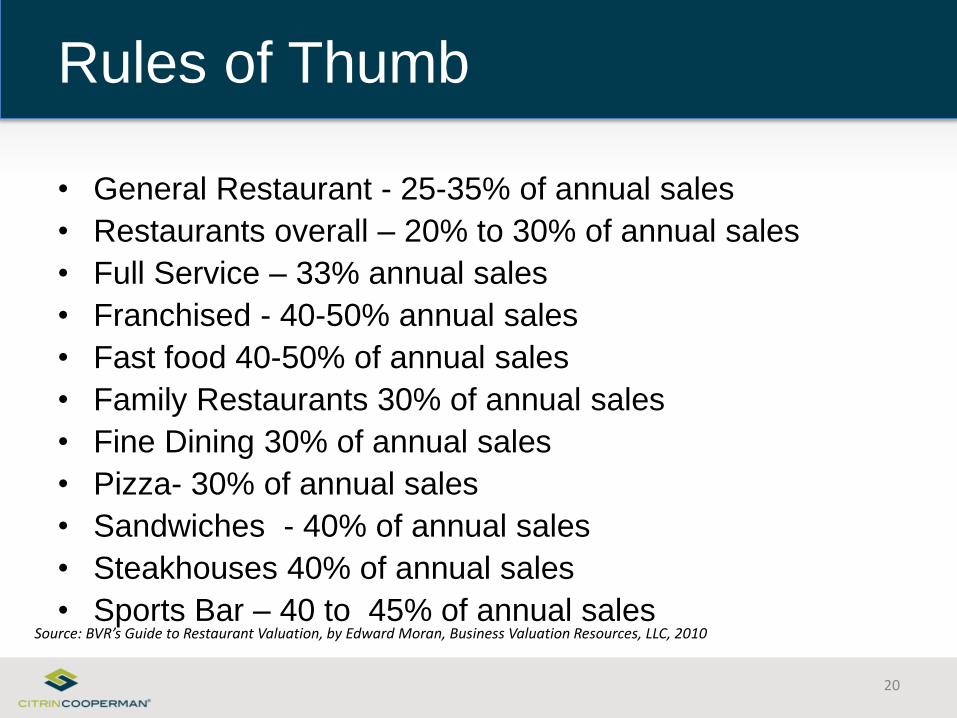

• General Restaurant - 25-35% of annual sales

• Restaurants overall – 20% to 30% of annual sales

• Full Service – 33% annual sales

• Franchised - 40-50% annual sales

• Fast food 40-50% of annual sales

• Family Restaurants 30% of annual sales

• Fine Dining 30% of annual sales

• Pizza- 30% of annual sales

• Sandwiches - 40% of annual sales

• Steakhouses 40% of annual sales

• Sports Bar – 40 to 45% of annual sales

20

Rules of Thumb

Source: BVR’s Guide to Restaurant Valuation, by Edward Moran, Business Valuation Resources, LLC, 2010

VALUE DRIVERS

21

• Location

• Concept

• Menu

• Quality of Cooking and Wait Staff

• Cost Control

• Operational profitability

• Consistency

22

Value Drivers – Restaurants

Source: Value Maps – Valuation Tools The Unlock Business Wealth – Warren D. Miller

• Controlling Costs

• Growing revenue

• Careful budgeting

• Adequate levels of cash & working capital

• Conservative levels of debt at market level interest rates

• Ongoing repair, maintenance, and replacement of worn

out machinery, equipment, and fixtures

• Below market leases

23

Value Drivers – Restaurants

Source: BVR’s Guide to Restaurant Valuation, by Edward Moran, Business Valuation Resources, LLC, 2010

Value Drivers

Cash Flows

Growth

Risk

24

• Cash Flows

– Monitor and the control

– Benchmarking

– Representative economic income

25

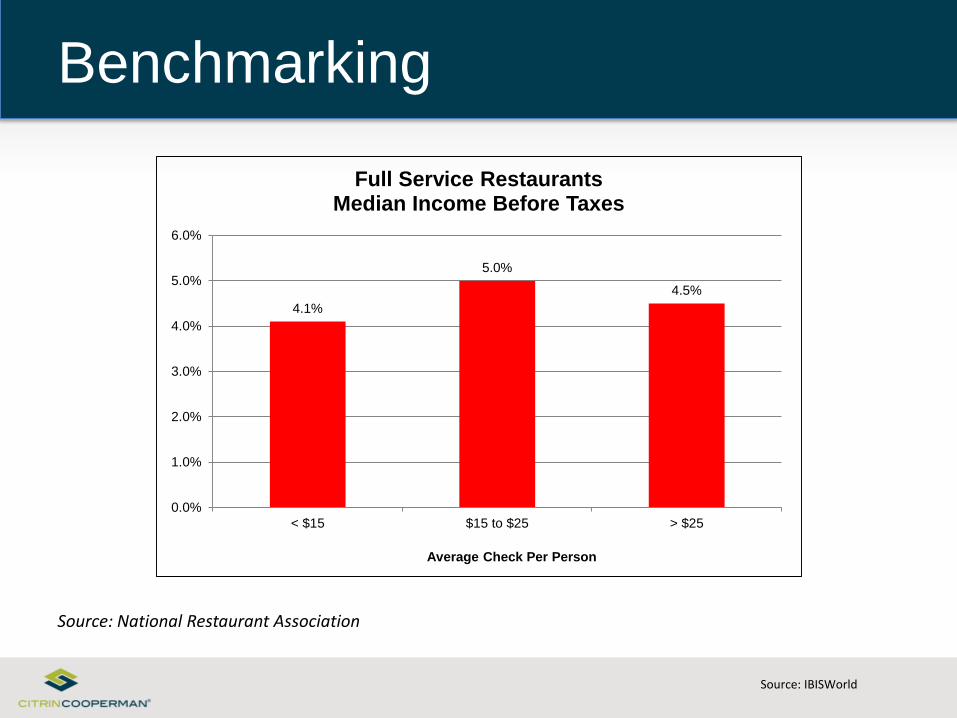

Value Drivers

Benchmarking

Source: IBISWorld

Source: National Restaurant Association

4.1%

5.0%

4.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

< $15 $15 to $25 > $25

Average Check Per Person

Full Service RestaurantsMedian Income Before Taxes

Source: American Staffing Association and IBISWorld

• Growth

– Expansion

– Benchmarking

27

Value Drivers

Growth

• Income – the #1 driver of restaurant spending.

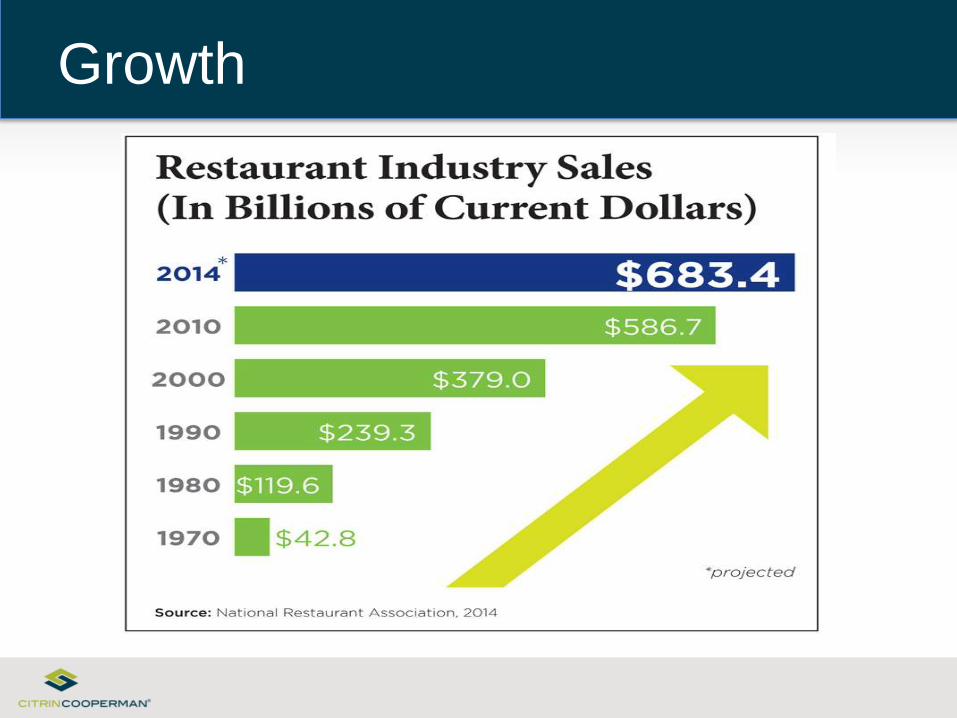

• Age – the presence of young children in a household

reduces restaurant spending.

• Geography – variations in cost of living, general

economy and lifestyles.

Growth

Source: IBISWorld

Source: National Restaurant Association

30

Trends

Trends

• Interact via Social media (e.g. Facebook, Twitter, etc.)

• View menus or make reservations online

• In-store ordering kiosks

• Smartphone apps

32

Trends

Source: National Restaurant Association

OWNERSHIP

CHARACTERISTICS OF

INTEREST BEING SOLD

33

• Determine the type of ownership interest

• Understand the classes of equity ownership

• Consider valuation adjustments - Discounts

34

Ownership Characteristics

Source: Statement on Standards for Valuation Services #1, AICPA, June 2007

• One size fits all

• Mis-matching multiples

• Misjudging the risk

• Ignoring Management

• Ignoring Real Estate / Lease

35

Common Errors

BEST PRACTICES

36

• Report income

• Fully use your POS system

• Measure of success

• Financial statements

• Health inspection reports

• Brag book

• Lease negotiations

37

Best Practices

38

QUESTIONS?

About the Presenters

GARY M. KARLITZ, CPA, ABV, CBA, ASA

• Gary is the practice leader of Citrin Cooperman's VFSgroup valuation services, forensic services, and forensicaccounting for the firm. He is located in the firm’s NewYork City and Westchester offices.

• For more than 30 years; he has negotiated on behalf ofclients in merger and acquisition matters and in divorceproceedings, in which he has provided accounting,taxation, and valuation support. Gary has also served asa court-appointed referee and neutral valuator andtestifies frequently as an expert witness in variouscourts.

• Gary is a past member of the AICPA’s Valuation ExamCommittee (1999-2008). As part of that nationalcommittee of valuation services experts, Gary wasresponsible for the preparation of the Accredited inBusiness Valuation (ABV) specialty examination.

39

About the Presenters

MANDEEP SIHOTA, CFA, ASA

• Mandeep, is a principal in Citrin Cooperman's VFS group. She leads thevaluation team and manages the preparation and delivery of valuations ofbusinesses, private equity, professional practices and income generatingassets such as derivatives and intellectual property.

• She has prepared hundreds of complex valuations and economicdamages calculations for a variety of purposes including: mergers andacquisitions, estate and gift tax planning, corporate financial planning,shareholder actions, matrimonial actions, commercial damages and otherdisputes.

• Mandeep has experience in a diverse range of industry verticals includingstaffing, hedge funds and other alternative investments, technology,construction, hospitality and a broad variety of service, manufacturing,and wholesale distribution industries.

• Mandeep has an Bcomm from the University of Toronto and an MBAfrom the Schulich School of Business, York University in Canada. She isa Chartered Financial Analyst (CFA) designation holder, an AccreditedSenior Appraiser (ASA) with the American Society of Appraisers and amember of the CFA Institute and the New York Society of SecurityAnalysts.

• Mandeep is qualified as an expert witness before the Supreme Court ofthe State of New York and testified before the September 11th VictimCompensation Fund regarding the economic damages suffered as aresult of the wrongful death of a New York City firefighter, during theSeptember 11, 2001 terrorist attack.

40

CONNECTICUT | NEW JERSEY | NEW YORK | PENNSYLVANIA

CITRINCOOPERMAN.COM