Embed Size (px)

DESCRIPTION

Dr Dev Kambhampati | USDA- Livestock & Poultry- World Markets & Trade

Citation preview

United States Department of Agriculture

ForeignAgriculturalService

Approved by the World Agricultural Outlook Board/USDA

April 2014

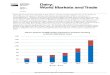

India and Turkey: Competitive Advantages Impact Global Trade

India:

Beef shipments have nearly

tripled between 2008 and

2013 and are forecast at a

record of nearly 1.9 million

tons in 2014. India has

become the world’s second

largest exporter with a 20

percent market share.

Turkey:

Broiler meat exports are

forecast at a record 480,000

tons in 2014, up from

42,000 tons in 2008.

Although Turkey has only

achieved a 4 percent share

of the global market,

shipments are primarily to

the Middle East, the

world’s strongest growth

region.

Gains are due to competitive advantages:

Geography: India and Turkey are close to key markets which facilitates shipping logistics

and lowers costs. India exports primarily to Southeast Asia and the Middle East, while

Turkey ships over half its volume overland to Iraq.

Product Differentiation: Both countries supply halal meat, a desired attribute or essential

requirement in many of their markets. India ships “carabeef” (from water buffalo), a lower-

quality price-competitive meat with binding characteristics favored in processed product

manufacturing. Sixty percent of Turkey’s exports are whole birds, preferred over parts by

Middle East consumers.

To receive the circular via email, subscribe here.

Livestock and Poultry: World Markets and Trade

April 2014

Contents

Summary: Major Traders and U.S. Trade of Beef, Pork, and Poultry

Beef Beef and Veal: 2014 Forecast Revised from November Beef Summary Tables Cattle Summary Tables

Pork Pork: 2014 Forecast Revised from November Pork Summary Tables Swine Summary Tables

Poultry Meat Broiler Meat: 2014 Forecast Revised from November Broiler Meat Summary Tables

Turkey Meat Summary Tables

Notes to Readers

April 2014

2009 2010 2011 2012 2013 (p) 2014 (f)

Percent Change 2013 to

2014

Beef and Veal /1 57,366 57,576 57,422 57,623 58,620 58,856 0.4%Pork /1 100,332 102,899 103,468 106,828 109,452 110,703 1.1%Broiler and Turkey /2 78,784 83,447 86,507 88,723 89,490 90,799 1.5%

Total 236,482 243,922 247,397 253,174 257,562 260,358 1.1%

Beef and Veal /1 56,408 56,427 55,718 56,090 56,825 57,240 0.7%Pork /1 100,246 102,756 103,118 106,266 109,075 110,435 1.2%Broiler & Turkey /2 77,669 82,116 84,918 86,708 87,651 88,667 1.2%

Total 234,323 241,299 243,754 249,064 253,551 256,342 1.1%

Beef and Veal /1 6,555 6,622 6,413 6,652 7,423 7,759 4.5%Pork /1 5,547 5,891 6,611 6,896 6,662 6,593 -1.0%Broiler and Turkey /2 7,660 8,163 8,560 8,918 9,034 9,276 2.7%

Total 19,762 20,676 21,584 22,466 23,119 23,628 2.2%

Beef and Veal /1 7,450 7,822 8,095 8,164 9,165 9,514 3.8%Pork /1 5,632 6,031 6,947 7,260 7,019 6,860 -2.3%Broiler and Turkey /2 8,965 9,449 10,167 10,797 10,917 11,434 4.7%

Total 22,047 23,302 25,209 26,221 27,101 27,808 2.6%

Beef and Veal /1 878 1,043 1,263 1,113 1,172 1,141 -2.6%Pork /1 1,857 1,915 2,354 2,441 2,264 2,200 -2.8%Broiler and Turkey /2 3,335 3,331 3,480 3,662 3,678 3,767 2.4%

Total 6,070 6,289 7,097 7,216 7,114 7,108 -0.1%

Beef and Veal /1 12% 13% 16% 14% 13% 12%Pork /1 33% 32% 34% 34% 32% 32%Broiler and Turkey /2 37% 35% 34% 34% 34% 33%

Combined 28% 27% 28% 28% 26% 26%

Notes:

Note to Readers: Totals include only those countries that make up USDA’s official PSD database are reported. This means totals do not encompass all production, consumption, and trade, but rather the sum of those countries reported in USDA’s database, which represent the most important markets in the world meat PSD situation. In an attempt to capture these major players, the list of countries reported changes periodically.

1/ 1,000 Metric Tons (Carcass Weight Equivalent)2/ 1,000 Metric Tons (Ready to Cook Equivalent)

U.S. Market Share (%) of Exports Among Major Traders

Imports

Exports

U.S. Exports

Summary:Major Traders and U.S. Trade of Beef, Pork, and Poultry

Production

Consumption

April 2014

BEEF AND VEAL: 2014 REVISED FROM NOVEMBER Highlights:

• Global production is revised slightly higher from the November forecast to a record 58.9 million tons. Increases for the United States and a number of other countries offset a downward revision for the EU and a small reduction for Australia.

• Global trade continues to flourish despite tight supplies and exports are revised over 300,000 tons higher to 9.5 million. A more favorable demand outlook for a wide range of countries such as China, Venezuela, Angola, Chile, Saudi Arabia and the EU will stimulate greater shipments by Brazil and India. For the United States and Australia, significant changes in demand and tight supplies will impact trade patterns, but not necessarily volumes.

Production:

Drought and Adverse Weather Conditions Continue To Impact Several Major Producers

Production in the United States is raised 212,000 tons to 11.2 million on larger than expected placements due to dry conditions and favorable returns to feedlot operators as well as heavier slaughter weights. However, production will still be at the lowest level in 20 years. On the contrary, Oceania remains at levels comparable to recent years despite weather challenges. Australia is forecast 25,000 tons lower to 2.2 million as drought pushed producers to slaughter in 2103, reducing the cattle available in 2014. New Zealand is also lowered slightly to 630,000 tons as lighter weights more than offset increased slaughter. Larger dairy herd numbers and a repeat of dry conditions in the biggest dairying area, Waikato, will generate a higher cow slaughter than originally forecast. Changing Dairy Policies Impact EU Production

EU production is down 180,000 tons to 7.6 million. The elevated milk price and approaching abolition of the milk quotas in 2015 will encourage farmers to retain animals to expand the dairy herd. Lower calf slaughter on the continuing economic crisis in the main veal markets (Italy, France and Spain) also contributes to the reduction.

54

56

58

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

Tons

CW

E

World Beef Production Continues Growth

April 2014

Efficiency Gains Expected For India and Mexico

India is raised 50,000 tons to a record 4.0 million due to increased weights on efficiency gains in the dairy sector such as the utilization of more nutritious feed. Mexico is 25,000 tons higher to over 1.8 million on higher carcass yields due to improved feed availability. Global Demand Bolsters Brazil and Belarus Slaughter

Increased slaughter drives Brazil 20,000 tons higher to over 9.9 million. Strong global demand and depreciation of the Real facilitates competitive export pricing and improves packer margins. Belarus is raised 20,000 tons to 295,000 as Russia’s closure to several suppliers increases demand for imports from within the Customs Union. Outlook Improved For Argentina

Argentina’s production is raised 60,000 tons to 2.9 million driven by higher slaughter. Trade: China’s Demand Forecast to Grow Significantly

Rising consumer demand and competitive prices are forecast to boost China’s imports up 75,000 tons to a record 550,000. Slower poultry demand following the recent H7N9 poultry outbreak is also a factor in stronger demand. Domestic beef production is unable to meet this growing demand which generates significant opportunities for countries eligible to supply China. As the United States, Brazil and India unable to ship to China, the market is shared by Australia, Uruguay, New Zealand, Canada and Argentina. Australia is the dominant supplier with over half the market while Uruguay comprises about one-quarter. Both are expected to capture most of the forecasted gains. Growth in Minor Markets Benefit Export Leaders Brazil and India

Despite being blocked from shipments to China, the export forecasts for the world’s largest and second largest exporters, Brazil and India, are revised upward 90,000 and 125,000 tons, respectively. While India’s forecast reaches a new record of nearly 1.9 million tons. Brazil’s forecast of over 2.0 million tons will not surpass its 2007 record (2.2 million). Imports are forecast higher for Venezuela, Angola, Chile, Saudi Arabia and Iran due to increased demand. Brazil and India are able to make additional and substantial inroads in these various markets due to their competitive pricing. Exchange Rates Impact Canada and EU Trade

Canada’s imports are cut 25,000 tons to 290,000 due to the weaker Canadian dollar combined with tight supplies in the United States, which accounts for about three-quarters of the market. However, exports will be supported by the weaker currency and are up 30,000 tons to 355,000. Nonetheless, exports remain at about half the level of the early to mid-2000s as lower production limits exportable supplies.

April 2014

EU imports from Brazil have accelerated recently due in part to the depreciation of the Real against the Euro. In addition, lower expected slaughter and beef production generates an upward revision to the EU import forecast of 30,000 tons to 380,000. The depreciation of South American currencies is expected to maintain the slightly higher import level from Brazil and Uruguay. Reduced supplies and an elevated exchange rate also spur a downward revision of EU exports by 30,000 tons to 240,000. Tight Supplies Shift Some Trading Relationships

For the United States, tight supplies with strong demand for processing beef will also prompt additional imports which are raised 28,000 tons to nearly 1.1 million. Increased volumes will be supported primarily from increased shipments by Mexico, but also Australia and Canada. Downward revisions in imports for several key Asian markets (Korea by 38,000 tons, Taiwan 25,000 tons and Japan 21,000 tons) are driven largely by tight Australian and U.S. supplies. Australia will likely reduce its shipments to these key Asian markets in order to service growing Chinese demand. In the case of Japan, U.S. beef is expected to make minor gains and raise its market share as it increasingly displaces Australian beef in that market. Total U.S. exports are up 98,000 tons to over 1.1 million despite tight supplies due to strong Asian and Mexican demand. Paraguay and Belarus to Make Gains in Russian Market

Although Brazil supplies about half the Russian beef market, restrictions and challenges for various other exporters (United States, Australia) will generate additional opportunities for Paraguay and Belarus whose export forecasts are up 25,000 and 20,000 tons, respectively. Government Intervention in Argentina Continues to Stymie Exports

Argentina’s exports are down 20,000 tons to 200,000 despite strong global demand. The government continues to assert strong control on shipments and meat packers’ returns are minimized due to the increasing costs and limited exports.

April 2014

Beef and Veal Selected Countries Summary

1,000 Metric Tons (Carcass Weight Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Production

9,9209,9009,6759,3079,0309,115 Brazil

7,5807,7607,4707,7088,1148,101 European Union

5,7605,7505,6375,5405,5505,600 China

4,0003,9503,8503,4503,2442,842 India

2,9002,8402,8502,6202,5302,620 Argentina

2,2402,2652,3592,1522,1292,129 Australia

1,8201,7951,8081,8211,8041,745 Mexico

1,6751,6001,6301,5871,5361,485 Pakistan

1,3801,3801,3701,3801,3601,435 Russia

1,0251,0201,0351,0641,1401,276 Canada

9,3269,3479,1799,1459,0029,182 Others

47,62647,60746,86345,77445,43945,530 Total Foreign

11,23011,01811,75711,84911,98312,046 United States

58,85658,62558,62057,62357,42257,576 Total

none

Total Dom. Consumption

7,9258,0007,8857,8457,7307,592 Brazil

7,7207,8407,6027,7608,0348,202 European Union

6,2636,1985,9595,5975,5245,589 China

2,7002,6202,6642,4582,3202,346 Argentina

2,3882,3922,3892,4062,3462,488 Russia

2,1252,2002,0852,0391,9761,925 India

1,8751,8101,8741,8361,9211,938 Mexico

1,6261,5521,5811,5381,5031,451 Pakistan

1,2851,2781,2321,2551,2371,225 Japan

9701,0151,0011,0239951,003 Canada

11,19111,04210,93610,59410,48610,630 Others

46,06845,94745,20844,35144,07244,389 Total Foreign

11,17211,01411,61711,73911,64612,038 United States

57,24056,96156,82556,09055,71856,427 Total

Note: May contain meat of other bovines.

April 2014

Beef and Veal Selected Countries Summary

1,000 Metric Tons (Carcass Weight Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Imports

1,0201,0201,0311,0329941,058 Russia

760781760737745721 Japan

575550473241152154 Hong Kong

550475412992940 China

380350376348365437 European Union

360398375370431366 Korea, South

300225325217195143 Venezuela

290315296301282243 Canada

255220245187180190 Chile

235235232215265296 Mexico

1,9791,8911,8771,8981,8421,932 Others

6,7046,4606,4025,6455,4805,580 Total Foreign

1,0551,0271,0211,0079331,042 United States

7,7597,4877,4236,6526,4136,622 Total

none

Total Exports

2,0301,9401,8491,5241,3401,558 Brazil

1,8751,7501,7651,4111,268917 India

1,5601,5451,5931,4071,4101,368 Australia

535536529517503530 New Zealand

385415338360320347 Uruguay

355325333335426523 Canada

350325326251197283 Paraguay

240270244296445336 European Union

230210220156147181 Belarus

200220186164213277 Argentina

613623610630563459 Others

8,3738,1597,9937,0516,8326,779 Total Foreign

1,1411,0431,1721,1131,2631,043 United States

9,5149,2029,1658,1648,0957,822 Total

Note: May contain meat of other bovines.

April 2014

Cattle Selected Countries Summary

(in 1,000 head)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Cattle Beg. Stks

329,700329,775327,100323,700320,800316,400 India

207,960208,628203,273197,550190,925185,159 Brazil

104,188104,302104,205104,346104,822105,430 China

88,00087,60087,10687,05187,83689,829 European Union

51,74552,19551,09549,59748,15649,057 Argentina

30,24030,15030,57630,91030,97130,845 Colombia

28,25028,36529,00028,50627,55027,906 Australia

19,51419,21019,98120,13419,97020,677 Russia

17,76017,63718,52120,09021,45622,192 Mexico

12,21512,32512,30512,24512,15512,670 Canada

56,21855,67055,95455,71756,10857,478 Others

945,790945,857939,116929,846920,749917,643 Total Foreign

87,73088,30089,30090,76992,68293,881 United States

1,033,5201,034,1571,028,4161,020,6151,013,4311,011,524 Total

none

Production (Calf Crop)

65,50065,50064,50063,50062,50061,700 India

50,94051,30050,18549,69049,44549,200 Brazil

42,20042,35041,55240,95040,90041,500 China

29,60029,90029,55029,80030,10029,000 European Union

14,30014,30014,20013,70013,10011,600 Argentina

8,4808,7509,1689,1219,6148,842 Australia

6,6756,6756,7006,8006,9007,000 Mexico

6,6506,8206,8406,9207,2396,952 Russia

5,0604,9855,0004,9454,7864,530 New Zealand

5,0005,0005,0005,1255,1505,200 Colombia

16,09016,09515,97415,90716,03415,972 Others

250,495251,675248,669246,458245,768241,496 Total Foreign

33,30033,30033,93034,27935,31335,695 United States

283,795284,975282,599280,737281,081277,191 Total

Notes: May contain other bovines.

April 2014

Cattle Selected Countries Summary

(in 1,000 head)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Imports

800625712616335612 Venezuela

110110971389538 Russia

1051051009570140 Egypt

1001259811710383 China

505059567356 Canada

352030101625 Mexico

131512141216 Japan

333331 Ukraine

111211 Belarus

000010 Argentina

0000669 Others

1,2171,0541,1121,0517151,041 Total Foreign

1,9701,9502,0282,2842,1072,284 United States

3,1873,0043,1403,3352,8223,325 Total

none

Total Exports

1,0501,0501,0451,5391,4351,261 Mexico

9559151,0488216961,065 Canada

900620851620695875 Australia

760550689512405655 Brazil

500500514678689492 European Union

1503252362996124 Colombia

40904178213207 Uruguay

354233423427 New Zealand

202321282928 China

15717962 Russia

10311551 Others

4,4354,1254,5064,6314,2684,637 Total Foreign

15518016519119491 United States

4,5904,3054,6714,8224,4624,728 Total

Notes: May contain other bovines.

April 2014

PORK: 2014 REVISED FROM NOVEMBER Highlights:

• Global pork production is raised 1.8 million tons from the November forecast to a record 110.7 million as growth in China and Russia more than offsets reductions in the United States and the EU.

• Global trade, on the other hand, is forecast lower, with exports reduced nearly 400,000 tons to 6.9 million. This is largely due to Russia’s restrictions on imports of EU pork as well as tight exportable supplies from the United States.

• Swine disease outbreaks are major forecast movers. Porcine epidemic diarrhea (PED) has affected production estimates in a number of North American, Asian, and South American countries. This in turn impacts import demand and exportable supplies. Meanwhile African swine fever (ASF) is cited as the reason for Russia’s restrictions on imports of European pork.

Production:

China’s Production Expands despite Low Prices

China, accounting for over half of global pork production, is raised 2.3 million tons to a record 57.0 million because of fewer swine disease outbreaks and better animal nutrition and genetics resulting in heavier slaughter weights. Government intervention programs are encouraging producers to stay in business despite low or even negative returns. For example, the government has a pork purchasing scheme and some provincial governments have implemented both hog subsidies and insurance trials, all attempting to prevent significant fluctuations in pork production.

China

Rest of World

30

35

40

45

50

55

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

Tons

CW

E

China's Pork Production Expands, Rest of World Flat

April 2014

Russia’s Import Restrictions Impact Domestic and EU Production

Russia is boosted 250,000 tons to a record 2.6 million, largely on greater producer returns resulting from tight supplies caused by import restrictions on EU pork. The Russian industry continues shifting to larger, more efficient operations. The government is supporting the modernization of pork production facilities, including subsidizing improved breeding stock and genetics through the “Pork Production Development in 2013-2015 Plan.” Small farms, on the other hand, are poorly positioned to compete with large-scale operations and are being encouraged to exit hog production in order to reduce ASF risks. With import restrictions in place against pork from the EU, the expanding industry is poised to benefit from higher prices. EU is cut 150,000 tons to 22.3 million as the loss of their top export market, Russia, limits gains in hog and pork prices, which remain below last year. Weights remain near last year’s level. Slaughter is eased as the outlook for recovery in piglet production is weakened largely due to pressure on producer returns. North American Production Is Lowered on PED Impact

Due to the effects of PED, production in the United States is lowered 453,000 tons to 10.3 million. Heavier weights will not be enough to offset tighter hog supplies. Beginning swine inventories fell 1.8 million head to 66.0 million. Piglet production is also reduced by 8.7 million head to 113.2 million as PED losses of pre-weaned piglets result in lower litter rates. Tight hog and pork supplies are expected to lead to higher prices for both domestic and export markets. To date, the spread of PED in Canada has not been as severe as in the United States, with approximately 50 cases reported in four Canadian provinces as of mid-April. Canada’s production is lowered 30,000 tons to 1.8 million, making it unchanged compared to 2013. At the current time, PED is having a minimal impact in Mexico. Production is lowered 5,000 tons to 1.3 million as heavier weights are expected to nearly offset lower slaughter. Asian Countries Are Also Impacted by PED

Production for Taiwan is lowered 25,000 tons to 815,000 as PED losses are expected to reduce slaughter hog supplies. Japan is unchanged at 1.3 million tons as heavier weights are expected to balance reduced slaughter. Meanwhile in South Korea, production is raised 10,000 tons to 1.2 million with heavier slaughter weights more than offsetting PED losses.

April 2014

Trade:

Top Exporters Constrained; EU by Trade Restrictions, United States by Tight Supplies

EU exports are forecast to drop 200,000 tons to 2.0 million due to the loss of their top market, Russia, which accounted for 23 percent of their trade in 2013. Some shipments will likely be redirected to Asia, with China expected to become their top market. Exports to the United States are also likely to increase. Greater domestic consumption is forecast, with growth from the central Member States. Russia’s import restrictions were implemented at the end of February after 4 cases of ASF were reported in Poland and Lithuania. The EU has initiated a World Trade Organization (WTO) case on Russia’s restrictions, stating that the blanket ban on pork from the entire EU is disproportionate and in violation of WTO rules. The United States is expected to decline 190,000 tons to 2.2 million as tight supplies and record high prices are impacting U.S. competitiveness. On a positive note, the United States has regained partial access to the Russian market, which had been closed since early 2013. The export share of production is now forecast to fall for the second year to 21 percent. Lower production and tight supplies are expected to boost imports, raised 25,000 tons to 415,000. Brazil Benefits from Trade Restrictions, Canada from PED-Induced Global Supply Tightness

Brazil is forecast 55,000 tons higher to 675,000, with increased shipments to Russia replacing EU pork. With an additional plant becoming eligible to ship to Russia at the beginning of April, export prospects are supported. The depreciation of the Real is also expected to make Brazilian product more competitive in the world market. Canada is raised 20,000 tons to 1.3 million, with greater shipments expected to the United States, their top market, due to reduced U.S. production tied to PED losses.

United States

European Union

Canada

Brazil

0

0.5

1

1.5

2

2.5

3

2010 2011 2012 2013 2014

Mill

ion

Tons

CW

E

United States Leads Global Pork Exports

April 2014

Growth Is Expected for Some Smaller Exporters

China and Mexico are raised slightly on stronger Asian demand. For Mexico, exports are forecast 5,000 tons higher to 125,000 mostly on Japanese demand. China is raised 10,000 tons to 275,000 on ample, relatively low priced supplies with some demand growth expected from Hong Kong, the Philippines, and Malaysia. Imports Are Limited by Trade Restrictions and Tight Exportable Supplies

Russia’s imports are lowered 270,000 tons to 650,000, the lowest level in 10 years, due to import restrictions on product from the EU, their largest supplier. Greater shipments from Brazil and resumed access for two U.S. plants are expected to replace some, but not all EU pork. Despite greater production, consumption is lowered to 2012 levels. Mexico and Canada are lowered due to tight supplies in the United States, their major supplier. Mexico is reduced 15,000 tons to 785,000 and Canada is cut 20,000 tons to 215,000. Japan is down 20,000 tons to 1.2 million with pork facing stiff competition from other protein sources. The top suppliers are expected to remain the United States (44 percent), the EU (25 percent) and Canada (17 percent). The EU could gain some market share due to more competitive prices and increased availability of product. Also, some Japanese importers are beginning to diversify their supply base, increasing imports from lower-priced suppliers. Slightly Higher Imports Are Forecast for China

China is forecast 15,000 tons higher to 790,000, yet imports still only account for one percent of consumption. Greater shipments are expected from the EU, their top supplier.

April 2014

Pork Selected Countries Summary

1,000 Metric Tons (Carcass Weight Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Production

56,95054,70055,62053,42750,60450,712 China

22,30022,45022,39022,52622,95322,627 European Union

3,4003,4353,2803,3303,2273,195 Brazil

2,5502,3002,4002,1752,0641,981 Russia

2,2602,2602,2202,1752,1302,090 Vietnam

1,8201,8501,8201,8401,8121,779 Canada

1,3901,3901,3501,3101,2881,260 Philippines

1,3051,3051,3091,2971,2671,292 Japan

1,2851,2901,2811,2391,2021,175 Mexico

1,1701,1601,2521,0868371,110 Korea, South

830820795701704631 Ukraine

815840842878865845 Taiwan

540575550584528498 Chile

440400402331301279 Argentina

365360360352344339 Australia

2,9513,0043,0513,0223,0112,900 Others

100,37198,13998,92296,27393,13792,713 Total Foreign

10,33210,78510,53010,55510,33110,186 United States

110,703108,924109,452106,828103,468102,899 Total

none

Total Dom. Consumption

57,44055,26056,09653,80251,10850,799 China

20,31520,27020,17320,38220,82220,952 European Union

3,1993,2203,2673,2083,0352,896 Russia

2,7272,8162,6962,6702,6442,577 Brazil

2,5292,5552,5492,5572,5222,488 Japan

2,2452,2452,2052,1602,1132,072 Vietnam

1,9451,9701,9531,8501,7101,784 Mexico

1,6121,6001,6281,5461,4871,539 Korea, South

1,5641,5731,5211,4461,4321,418 Philippines

1,0251,010992953806776 Ukraine

862892879906919901 Taiwan

777850810834800810 Canada

583548536547558467 Hong Kong

513529510511482482 Australia

455434419362359326 Argentina

4,0914,1144,1734,0913,9813,815 Others

101,88299,886100,40797,82594,77894,102 Total Foreign

8,5538,7858,6688,4418,3408,654 United States

110,435108,671109,075106,266103,118102,756 Total

April 2014

Pork Selected Countries Summary

1,000 Metric Tons (Carcass Weight Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Imports

1,2301,2501,2231,2591,2541,198 Japan

790775770730758415 China

785800783706594687 Mexico

6509208681,045971916 Russia

445410399414432347 Hong Kong

425425388502640382 Korea, South

215235221241204183 Canada

200210204281119146 Ukraine

190210183194175183 Australia

175185172138145159 Philippines

1001009715111786 Belarus

1001009810597104 Singapore

909288877858 Angola

757560362211 Colombia

605051261917 Chile

648686658617622609 Others

6,1786,5236,2636,5326,2475,501 Total Foreign

415390399364364390 United States

6,5936,9136,6626,8966,6115,891 Total

none

Total Exports

2,0002,2002,2322,1652,1501,705 European Union

1,2651,2451,2461,2431,1971,159 Canada

675620585661584619 Brazil

275265244235244278 China

165190164180139130 Chile

125120111958678 Mexico

6095741048562 Belarus

373636364141 Australia

252525252519 Vietnam

7127646 Norway

264531693819 Others

4,6604,8534,7554,8194,5934,116 Total Foreign

2,2002,3902,2642,4412,3541,915 United States

6,8607,2437,0197,2606,9476,031 Total

April 2014

Swine Selected Countries Summary

(in 1,000 head)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Beginning Stocks

475,110475,898475,922468,627464,600469,960 China

145,400145,250146,982149,790152,361152,780 European Union

38,84438,64838,57738,33636,65235,122 Brazil

19,18620,05018,81617,25817,23117,236 Russia

12,74513,18012,61012,62512,61512,465 Canada

9,9129,0009,9168,1718,4498,721 Korea, South

9,8769,8529,5109,2769,0078,979 Mexico

9,6009,5709,6859,7359,76810,000 Japan

7,8907,8907,5777,3737,9607,577 Ukraine

3,3004,3444,2433,9893,8873,782 Belarus

2,1402,1002,1382,2852,2892,302 Others

734,003735,782735,976727,465724,819728,924 Total Foreign

66,02567,77566,37466,36164,92564,887 United States

800,028803,557802,350793,826789,744793,811 Total

none

Production (Pig Crop)

729,105723,500720,971707,427670,196665,261 China

257,150258,000256,700257,600264,655263,076 European Union

38,47038,79537,90037,70037,75036,970 Brazil

38,29036,20036,17534,50030,65029,472 Russia

27,30027,70027,39028,34628,50028,613 Canada

17,21017,30017,35017,25017,00017,500 Japan

16,75016,85016,85016,50016,35016,200 Mexico

15,50015,80016,95316,34013,30814,923 Korea, South

9,5809,5809,1638,5388,1098,176 Ukraine

4,8354,7704,7794,5814,6594,604 Australia

4,8005,5505,0005,2755,0755,025 Others

1,158,9901,154,0451,149,2311,134,0571,096,2521,089,820 Total Foreign

113,206121,870116,410116,791115,838113,685 United States

1,272,1961,275,9151,265,6411,250,8481,212,0901,203,505 Total

April 2014

Swine Selected Countries Summary

(in 1,000 head)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Imports

20018023122511290 Ukraine

25222319156 China

15151031129 Mexico

510086334782783 Russia

313152 Belarus

22211162 Korea, South

111125 Brazil

121233 Canada

111111 Japan

000000 Australia

001212 Others

253324359627949903 Total Foreign

4,7404,9004,9585,6565,7955,749 United States

4,9935,2245,3176,2836,7446,652 Total

none

Total Exports

4,7504,9204,9755,6765,8215,761 Canada

1,7251,7701,7011,6561,5631,748 China

5505008187411,0101,011 European Union

444261 Brazil

000000 Australia

0805210311354 Belarus

000000 Japan

000000 Korea, South

000000 Mexico

000001 Russia

000111 Others

7,0297,2747,5508,1798,5148,577 Total Foreign

292034553015 United States

7,0587,2947,5848,2348,5448,592 Total

April 2014

BROILER MEAT: 2014 REVISED FROM NOVEMBER Highlights:

• Global broiler meat production is still a record, but revised downward from the November forecast by 1.7 million tons to 85.3 million due to declines in China, Brazil, Russia and the United States.

• Global trade is virtually unchanged as exports are forecast at 10.7 million tons as reductions in Brazil and the EU are offset by increases in Turkey, Ukraine and China.

Production: Avian Influenza Pressures Chinese Production

Avian influenza (AI) in China has reduced the production forecast 1.0 million tons to 12.7 million. The disease has weakened demand and encouraged consumers to substitute red meat and fish for poultry, resulting in financial loss for the industry. However, the disruption in live bird sales and reduced consumer demand for wet-market product may bolster supermarket purchases.

Lower Profitability Cuts Production in Brazil, Russia and the United States

Brazil is down 342,000 tons to 12.7 million on lower than expected domestic and foreign demand. Domestic consumption is dampened by economic uncertainty, rising inflation and greater competition from beef and pork. Russia is 200,000 tons lower to 3.1 million as expansion is constrained by high indebtedness and market saturation. The United States is cut 180,000 tons to 17.3 million, but still a record, as producers respond to moderating prices.

11

12

13

14

2009 2010 2011 2012 2013 2014

Mill

ion

Tons

RTC

Avian Influenza Diminishes Chinese Production

March 2013 – H7N9 Outbreak

April 2014

Demand Bolsters India and EU Production

India is raised 100,000 tons to a record 3.7 million on greater domestic demand and increased feed availability. The industry is thriving with improved margins as a result of relatively low corn prices and stable poultry prices. The EU is 50,000 tons higher to 10.0 million as the economic slowdown encourages consumption of more price-competitive and convenient broiler meat. Higher production in Benelux, Germany, the United Kingdom, and Romania is expected to offset declines in France and Spain. Mexico is virtually unchanged at a record 3.1 million tons. Trade: Middle East Continues to Rise, Benefiting Turkish Exporters

The Middle East remains the world’s largest regional importer and represents the largest gain in imports at 65,000 tons. Greater demand is expected to bolster imports by Saudi Arabia, up 35,000 tons to a record 860,000. Iraq is also forecast at a record level, up 30,000 tons to 730,000. Turkey’s exports are 40,000 tons higher at a record 480,000 on greater demand from the Middle East, at the expense of Brazil, the EU, and the United States. The main priority of the industry is foreign markets as domestic demand continues to decline.

Brazil and EU Exports Expected Lower

Brazil’s exports are reduced 25,000 tons to 3.6 million on lower than expected demand in Sub-Saharan Africa and greater competition in the Middle East. Despite a depreciating Real, constraints such as antidumping tariffs in South Africa continue to limit exports. EU exports

0

2

4

6

8

10

2009 2010 2011 2012 2013 2014

Mill

ion

Tons

RTC

Growing Share of World Broiler Meat Exports Directed to Middle East

MiddleEast

Rest ofWorld

April 2014

drop 35,000 tons to 1.1 million on the cessation of export restitutions, in addition to the decline in the whole-bird exports to the Middle East. Demand Shifts in Other Markets

Exports from the United States remain virtually unchanged at a record 3.4 million tons, as shipments to top markets such as Mexico and Canada remain strong. Venezuela’s imports are up 40,000 tons to 340,000. EU imports are 30,000 tons higher to 700,000 based on higher demand for inexpensive sources of animal protein. Angola’s imports are down 25,000 tons to 350,000.

April 2014

Broiler Meat Selected Countries Summary

1,000 Metric Tons (Ready to Cook Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Production

12,70013,70013,35013,70013,20012,550 China

12,67813,02012,30812,64512,86312,312 Brazil

9,9509,9009,8009,5659,3209,202 European Union

3,7253,6253,4503,1602,9002,650 India

3,1003,3003,0102,8302,5752,310 Russia

3,0603,0453,0022,9582,9062,822 Mexico

2,0802,1002,0602,0141,7701,680 Argentina

1,8101,8201,7601,7071,6191,420 Turkey

1,6001,6251,5001,5501,3501,280 Thailand

1,5651,5651,5501,5401,5151,465 Indonesia

15,74815,82615,30714,95314,48713,981 Others

68,01669,52667,09766,62264,50561,672 Total Foreign

17,27617,45616,97616,62116,69416,563 United States

85,29286,98284,07383,24381,19978,235 Total

none

Total Dom. Consumption

12,50513,55513,17413,54313,01512,457 China

9,5809,4659,3889,1989,0108,955 European Union

9,0819,3968,8299,1399,4229,041 Brazil

3,7503,7303,6793,5693,4733,364 Mexico

3,7203,6213,4453,1562,8912,648 India

3,5903,7653,5203,3213,0132,957 Russia

2,1852,1552,2012,2132,1042,080 Japan

1,7501,7551,7531,7561,6881,524 South Africa

1,7371,7471,7381,7261,5561,475 Argentina

1,5651,5651,5501,5401,5151,465 Indonesia

20,06120,23419,57919,09918,55817,657 Others

69,52470,98868,85668,26066,24563,623 Total Foreign

13,92914,08713,68313,34513,66513,472 United States

83,45385,07582,53981,60579,91077,095 Total

Note: Chicken paws are excluded.

April 2014

Broiler Meat Selected Countries Summary

1,000 Metric Tons (Ready to Cook Equivalent)

2010 2011 2012 2013 2014

Nov

2014

Apr

none

Total Imports

865855854877895789 Japan

860825820750745652 Saudi Arabia

730700673612598522 Iraq

700670671727734687 European Union

695690682616578549 Mexico

530530540560463656 Russia

350375321301287239 Angola

340340355371326240 South Africa

340300341198234237 Venezuela

255255272300410295 Hong Kong

3,1573,2663,0713,1842,9072,891 Others

8,8228,8068,6008,4968,1777,757 Total Foreign

515155514948 United States

8,8738,8578,6558,5478,2267,805 Total

none

Total Exports

3,6003,6253,4823,5083,4433,272 Brazil

1,0701,1051,0831,0941,044934 European Union

580580504538467432 Thailand

480440362285206110 Turkey

430415420411423379 China

345355324291224214 Argentina

190170141764323 Ukraine

160155150141143147 Canada

1151151001057438 Belarus

909188939079 Chile

270289243248219173 Others

7,3307,3406,8976,7906,3765,801 Total Foreign

3,4133,4253,3403,3003,1613,067 United States

10,74310,76510,23710,0909,5378,868 Total

Note: Chicken paws are excluded.

April 2014

Turkey Meat Selected Countries Summary

1,000 Metric Tons (Ready to Cook Equivalent)

2009 2010 2011 2012 2013 2014

Nov

none

Production

1,9751,9852,0101,9501,9461,795 European Union

535520510489485466 Brazil

165165161160159167 Canada

105100100907031 Russia

101014131111 Mexico

888888 South Africa

666665 China

2,8042,7942,8092,7162,6852,483 Total Foreign

2,7032,6232,6712,5922,5272,535 United States

5,5075,4175,4805,3085,2125,018 Total

none

Total Dom. Consumption

1,9351,9351,9521,8851,9111,801 European Union

355345340348327302 Brazil

171169173164163155 Mexico

147144142150143151 Canada

11911411911610572 Russia

715954403232 China

635341323434 South Africa

2,8612,8192,8212,7352,7152,547 Total Foreign

2,3532,2932,2822,2732,3062,363 United States

5,2145,1125,1035,0085,0214,910 Total

April 2014

Turkey Meat Selected Countries Summary

1,000 Metric Tons (Ready to Cook Equivalent)

2009 2010 2011 2012 2013 2014

Nov

none

Total Imports

162160160152153144 Mexico

9090938299112 European Union

655348342627 China

554533242626 South Africa

141419263541 Russia

877788 Canada

000000 Brazil

394369360325347358 Total Foreign

910119119 United States

403379371334358367 Total

none

Total Exports

180175170141158164 Brazil

130140151147134106 European Union

262623222425 Canada

111110 Mexico

000000 China

000000 Russia

000000 South Africa

337342345311317295 Total Foreign

354338362319264242 United States

691680707630581537 Total

April 2014

Notes to Readers The Livestock and Poultry: World Markets and Trade circular is designed to give a snapshot of the current situation among the major players in world beef, pork, broiler meat, and turkey meat trade. Data Modifications Prior to 2012

Cattle/Beef: • The cattle PSDs for the following countries are revised for particular years during the 2010-

2011 period on official production data revisions: Canada and European Union. • The beef PSDs for the following countries are revised for particular years during the 1996-

2011 period on additional/revised official production data available: Bosnia and Herzegovina, Canada, Ghana, Guatemala, Iran, Oman and Saudi Arabia.

• The beef PSDs for the following countries are revised for particular years during the 2003-2011 period on additional/revised trade data available: Bosnia and Herzegovina, Canada, Honduras, United Arab Emirates and Vietnam.

Swine/Pork: • The pork PSDs for the following countries are revised for particular years during the 2008-

2011 period due to additional/revised official trade or production data: Canada, China, Cote d’Ivoire, EU, and Russia.

• The swine PSDs for the following countries are revised for particular years during the 2009-2011 period due to additional/revised production data: Canada and China.

Broiler Meat:

• The broiler meat PSDs for the following countries are revised for particular years during the 1996-2011 period on additional production data available: Ghana, Malaysia, and Singapore.

• The broiler meat PSDs for the following countries are revised for particular years during the 1999-2011 period on additional trade data available: Qatar, Saudi Arabia, South Africa, and Ukraine.

Assumptions

• Diseases: Forecast reflects disease (avian influenza, African swine fever, foot and mouth disease, bovine spongiform encephalopathy, etc.) policies and restrictions in place as of April 17, 2014 and assumes their continuation.

Conversion Rates Beef &Veal Pork

Conversion Rate 1.40 1.30 HS Codes Fresh/Chilled: 0201

Frozen: 0202 Processed: 021020 & 160250

Fresh/Chilled: 020311, 020312, 020319 Frozen: 020321, 020322, 020329 Processed: 021011, 021012, 021019, 160241, 160242, 160249

Broiler Meat Turkey Meat Conversion Rate 1 1 HS Codes Fresh/Chilled: 0207.11, 0207.13

Frozen: 0207.12, 0207.14 Processed: 1602.32

Fresh/Chilled: 0207.24, 0207.26, 0207.32, 0207.34, 0207.35

Frozen: 0207.25, 0207.27, 0207.33, 0207.36 Processed: 1602.31

Note: There are several exceptions by country/product. In general, chicken paws are excluded and carabeef (buffalo meat) is included.

April 2014

Technical Notes

CWE/PWE: All quantities (beef and pork) noted are in Carcass Weight Equivalent (CWE) unless otherwise noted as Product Weight Equivalent (PWE). CWE is the weight of an animal after slaughter and removal of most internal organs, head, and skin. PWE is the actual weight of the meat product exported. FAS Reports from Overseas Offices

The Livestock and Poultry: World Markets and Trade circular is based on post reports submitted since January 2014 and on available secondary information. The individual country reports can be obtained on FAS Online at: http://gain.fas.usda.gov/Pages/Default.aspx. PSD Online

The entire USDA PSD database is available online at http://www.fas.usda.gov/psdonline. Additional Resources

Please refer to the USDA-FAS Dairy, Livestock and Poultry website at: http://www.fas.usda.gov/commodities/livestock-and-meats for additional data and analysis. Situation and outlook information on U.S. livestock and poultry can be obtained from the USDA-Economic Research Service at: http://www.ers.usda.gov/publications/ldpm-livestock,-dairy,-and-poultry-outlook/. Future Releases and Contact Information

Please visit http://www.fas.usda.gov/data/livestock-and-poultry-world-markets-and-trade to view archived and future releases. The next release of this circular will be in October 2014. To receive the circular via email, go to http://www.fas.usda.gov/data/livestock-and-poultry-world-markets-and-trade and click on "Email subscriptions to FAS reports are available through Cornell University's Mann Library" towards the bottom of the page to register. Questions may be directed to the following staff:

Lesley Ahmed (202) 720-2781 [email protected] Swine and Pork Claire Mezoughem (202) 720-7715 [email protected] Cattle and Beef

Lazaro Sandoval (202) 720-7285 [email protected] Poultry Meat

April 2014