Embed Size (px)

Citation preview

Steven French | @NMITWEETS Natural Marketing Institute

Market Insights from Top Researchers: The Latest Intelligence on Customer Attitudes and Behavior

#SB15London

Raphael Bemporad | @rbemporad BBMG

Dorothy Mackenzie | @DragonRogueUKDragon Rogue

Lucy Shea | @swishinglucy Futerra

Kristoph Kahlert Serviceplan Corporate Reputation

Dan Gavshon Brady | @DanBG88 Wolff Colins

1 © 2014, Natural Marke1ng Ins1tute

Global Sustainability Trends: Opportuni5es & Challenges

SB London 2015 Steve French, NMI Managing Partner

16 November 2015

2 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

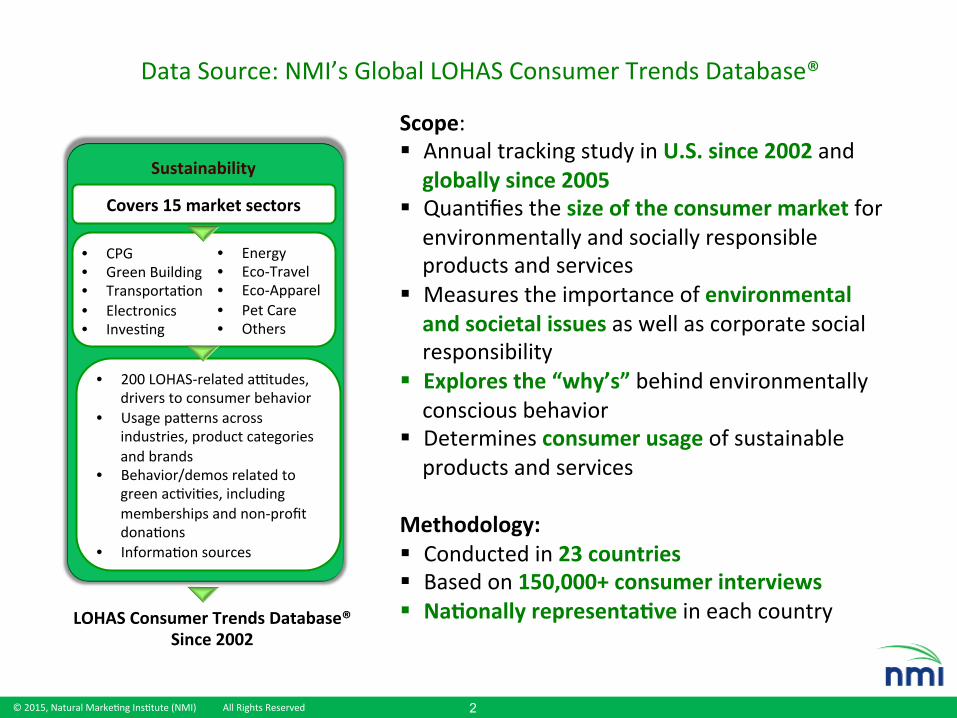

Sustainability

• 200 LOHAS-‐related aDtudes, drivers to consumer behavior

• Usage paKerns across industries, product categories and brands

• Behavior/demos related to green ac1vi1es, including memberships and non-‐profit dona1ons

• Informa1on sources

Covers 15 market sectors

• CPG • Green Building • Transporta1on • Electronics • Inves1ng

• Energy • Eco-‐Travel • Eco-‐Apparel • Pet Care • Others

LOHAS Consumer Trends Database® Since 2002

Data Source: NMI’s Global LOHAS Consumer Trends Database®

Scope: § Annual tracking study in U.S. since 2002 and globally since 2005

§ Quan1fies the size of the consumer market for environmentally and socially responsible products and services

§ Measures the importance of environmental and societal issues as well as corporate social responsibility

§ Explores the “why’s” behind environmentally conscious behavior

§ Determines consumer usage of sustainable products and services

Methodology: § Conducted in 23 countries § Based on 150,000+ consumer interviews § NaSonally representaSve in each country

3 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

• This research classified 9 countries studied into Developed and Emerging in order to beKer understand the ‘developmental stage’ of the country, thereby laying the groundwork for why differences in aDtudes and behaviors may exist.

Emerging countries -‐ Brazil, China, India, Russia, South Africa Developed countries -‐ Germany, Japan, UK, US

Developed vs. Emerging Perspec1ve

Developed countries

US UK

Germany Japan

Emerging countries

Russia China India Brazil

S. Africa

4 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Most consumers feel that the environmental ‘buzz’ is not a temporary fad, but is here to stay

Developed countries Emerging countries

2013 % total growth (2010-‐2013)

Russia 72% 112%

Brazil 71% -‐4%

China 69% -‐5%

South Africa 62% N/A

UK 57% 19%

Germany 57% 21%

U.S. 52% 4%

India 52% 2%

Japan 33% -‐18%

Top 3 countries who believe

environmental ‘movement’ is here to stay

Russia appears to be ‘buying-‐in’ on a much higher level than in the past, while Japan is s1ll on the fence.

5 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Brazil

China

Germany

India

Japan

Russia SA UK

0%

20%

40%

60%

80%

0% 20% 40% 60% 80% 100%

Socially re

spon

sible bu

sine

ss

ProtecSng the environment

Most Emerging countries (except Russia) care strongly about environmental protec1on and socially responsible business, while the Developed markets less so

% consumers who care about…

Size of bubble is determined by popula1on of each country; emerging country popula1on is adjusted for urban popula1on based on sta1s1cs from the Human Development Report Office (HDRO), 2012

US

Developed countries Emerging countries

6 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Many consumers also feel they are ‘very’ informed about how to live an eco-‐friendly and green lifestyle

Not at all informed

Very well informed

UK (28%)

China (52%)

India (60%)

Russia (44%)

Brazil (58%)

S. Africa (35%)

Germany (31%)

Japan (10%)

% countries indica1ng they feel ‘VERY’ informed about how to live an eco-‐friendly and green lifestyle

U.S. (32%)

Japan, UK and Germany lag behind, perhaps highligh1ng countries where educa1onal opportuni1es exist.

Developed countries Emerging countries

7 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Choosing sustainable or e-‐friendly products over conven1onal ones has shown some substan1al increases since 2010

48%

53% 50%

42% 43% 44%

42% 44%

42%

36% 34% 34%

New, Preliminary 2015 Data

2014 2013 2012 2011 2010

I will choose those products and services that are environmentally-‐friendly

I will choose products from sustainable sources over other conven1onal products

% U.S. General Popula1on indica1ng… “When given the choice to buy or use a product or service…”

8 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

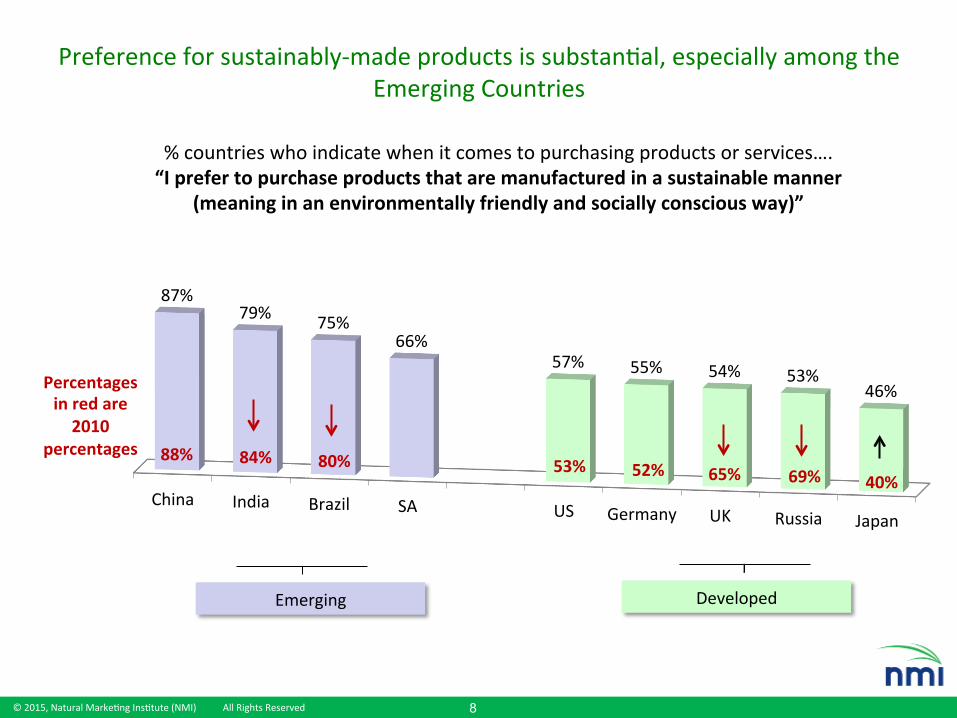

% countries who indicate when it comes to purchasing products or services…. “I prefer to purchase products that are manufactured in a sustainable manner

(meaning in an environmentally friendly and socially conscious way)”

Preference for sustainably-‐made products is substan1al, especially among the Emerging Countries

China India Brazil SA US Germany UK Russia Japan

87% 79% 75%

66% 57% 55% 54% 53%

46%

Emerging Developed

88% 84% 80% 52% 65% 69% 40%

Percentages in red are 2010

percentages 53%

9 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Brazil, China and India are extremely opportunis1c as they exhibit increasingly strong e-‐friendly behaviors

34%

40% 36%

10% 7%

26%

12%

13%

46% 51%

41%

22% 17%

7%

27%

11%

13%

Brazil China India SA Germany Japan Russia UK US

2010 2013

% countries who completely agree: “I buy as many green, eco-‐friendly products as I can”

10 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Sustainability has broad impact across brand appeal; be sure to tell your whole brand story when communica1ng with consumers

% U.S. General Popula1on indica1ng… “Knowing that a company is mindful of its impact on the environment and

society makes me…”

CAG ’09-‐’14: 4.3% 2.6% 2.4% 2.0%

more likely to try their products or services

more likely to buy their products repeatedly

more likely to talk with my friends and family about the company

less concerned with the price of their products

58% 53% 45% 30%

11 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

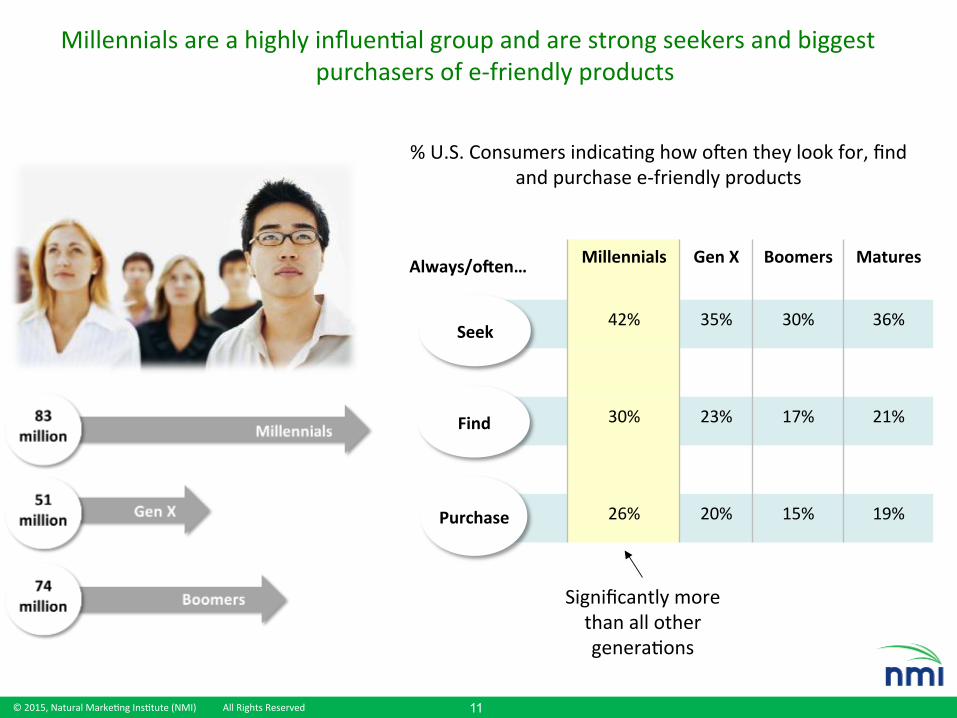

Millennials are a highly influen1al group and are strong seekers and biggest purchasers of e-‐friendly products

Millennials Gen X Boomers Matures

42% 35% 30% 36%

30% 23% 17% 21%

26% 20% 15% 19%

Seek

Find

Purchase

Always/ojen…

% U.S. Consumers indica1ng how open they look for, find and purchase e-‐friendly products

Significantly more than all other genera1ons

12 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

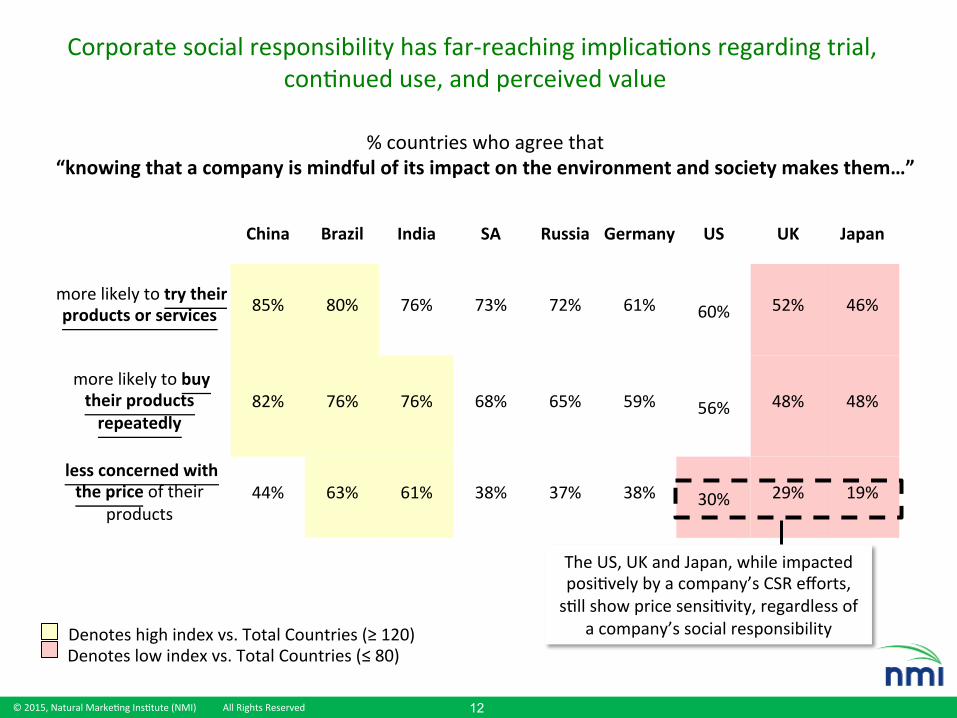

China Brazil India SA Russia Germany US UK Japan

more likely to try their products or services 85% 80% 76% 73% 72% 61% 60% 52% 46%

more likely to buy their products repeatedly

82% 76% 76% 68% 65% 59% 56% 48% 48%

less concerned with the price of their

products 44% 63% 61% 38% 37% 38% 30% 29% 19%

% countries who agree that “knowing that a company is mindful of its impact on the environment and society makes them…”

Corporate social responsibility has far-‐reaching implica1ons regarding trial, con1nued use, and perceived value

Denotes high index vs. Total Countries (≥ 120) Denotes low index vs. Total Countries (≤ 80)

The US, UK and Japan, while impacted posi1vely by a company’s CSR efforts, s1ll show price sensi1vity, regardless of

a company’s social responsibility

13 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

20%

30%

40%

50%

60%

70%

80%

90%

100%

China SA India Brazil Germany Russia US UK Japan

Quality

Price

Convenience

Anything

% countries who indicate “I do not want to sacrifice… when buying environmentally-‐friendly products”

Environmentally-‐made products cannot concede on quality or price, as consumers are not willing to sacrifice these aKributes

Emerging Developed

14 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

% U.S. General Popula1on who agree with the following statements…

Willingness to pay a premium for environmentally-‐friendly products is back on par with pre-‐recessionary levels, however, most consumers s1ll primarily price-‐driven

28% 30%

17% 15% 16% 16% 13%

27% 29% 27%

54% 61%

69% 68% 69% 68% 70% 63% 63% 64%

2006 2007 2008 2009 2010 2011 2012 2013 2014 New, Preliminary 2015 Data

I am willing to pay 20% more for products which are made in an environmentally friendly and sustainable way

I care about the environment, but my purchase is determined mainly by price

15 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

As consumer aDtudes and behaviors surrounding sustainability con1nue to grow, companies involved in the green and sustainable marketplace should also

see a growth in return on investment

Feel more responsible for protecSng

environment

Sustainability is here to

stay

Sustainable ini1a1ves boost ROI

Impact of CSR on trial and

purchase is growing

Consumers’ “green” aDtudes are growing……

16 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

The U.S. sustainability consumer market will grow to $1.5 trillion by 2020

2005 (US$ MM) 2012 (US$ MM) 2020 (US$ MM)

AlternaSve Energy $607 $700 $820

AlternaSve TransportaSon $6,121 $185,045 $572,440

Green Building $35,401 $55,722 $116,684

Natural Lifestyles $5,394 $6,394 $8,913

Organic Comon/Natural Fiber & TexSle $4,018 $7,545 $8,756

Personal Health $25,140 $36,980 $47,148

Ecotourism $24,200 $144,200 $416,929

Electronics/ Appliances $39,902 $119,491 $161,648

Consumer Packaged Goods $57,271 $104,664 $191,087

Grand Total $198,054 $660,740 $1,524,425

17 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Closing Thoughts

ü Consumers, especially those in developed countries, need guidance on how to lead an eco-‐friendly lifestyle

ü Sustainability is not just a fad, but a global ship that is here to stay

ü Sustainability has broad impact across brand appeal and CSR, especially in emerging countries

ü Many consumers want products manufactured in a sustainable manner -‐ product labeling is vital

ü Sustainable ac1on can no longer be considered a nice to have – globally, consumers expect it

ü No compromise exists – consumers not willing to sacrifice quality, price or convenience for sustainability

18 © 2015, Natural Marke1ng Ins1tute (NMI) All Rights Reserved

Natural MarkeSng InsStute (NMI) 272 Ruth Road Harleysville, PA USA 19438 Steve French Managing Partner [email protected] +1 215 513 7300 x214 www.NMIsoluSons.com All materials herein are © 2013-‐2015 by NMI (Natural Marke1ng Ins1tute). All rights reserved. Reproduc1on, publica1on (internal and/or external), transmission, or other use of any of the within materials, including but not limited to graphics, data, and/or text, for any commercial or non-‐commercial purposes, is strictly prohibited without the prior express wriKen permission of NMI.

![PRINCIPALS’ ATTITUDES AND INSIGHTS CONCERNING THE ...cnweb.cn.edu/tedu/NCATE-State/Examples-ProfMajor/EDUC600Sample[3].pdfPrincipal’s Attitudes 3 Definitions Within the context](https://img.pdfslide.us/doc/110x75/5f5072c8548981174f5e18d2/principalsa-attitudes-and-insights-concerning-the-cnwebcneduteduncate-stateexamples-profmajoreduc600sample3pdf.jpg)