Embed Size (px)

Citation preview

Financing climate

change initiatives

CPPR International Conference on:

Climate Change Paradigms

21 November 2015

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 1

Climate Finance

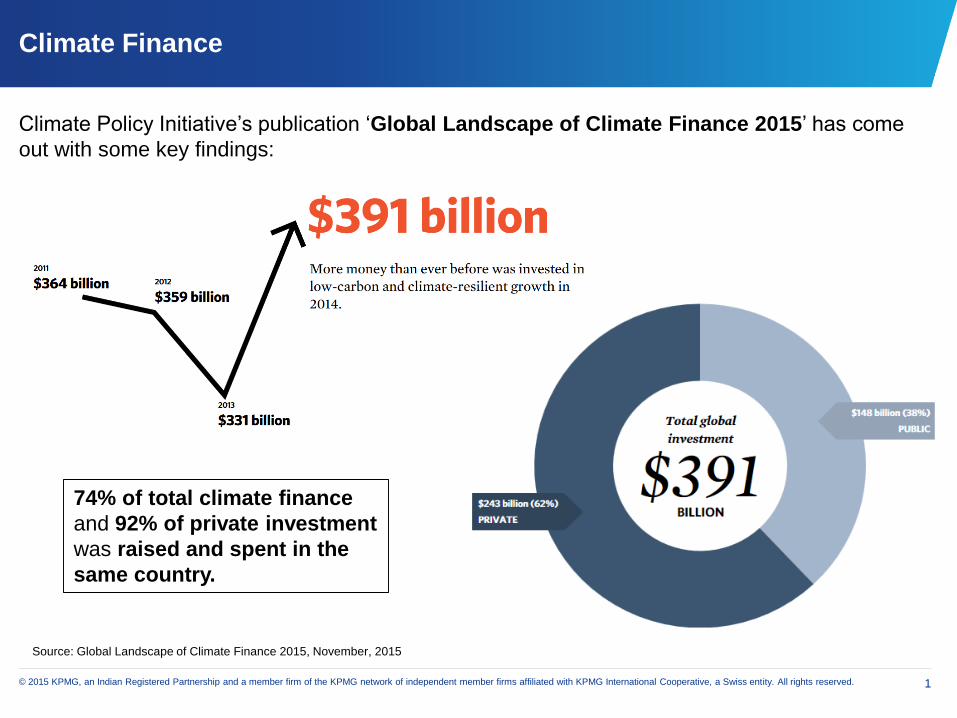

Climate Policy Initiative’s publication ‘Global Landscape of Climate Finance 2015’ has come

out with some key findings:

Source: Global Landscape of Climate Finance 2015, November, 2015

74% of total climate finance

and 92% of private investment

was raised and spent in the

same country.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 2

Climate Finance

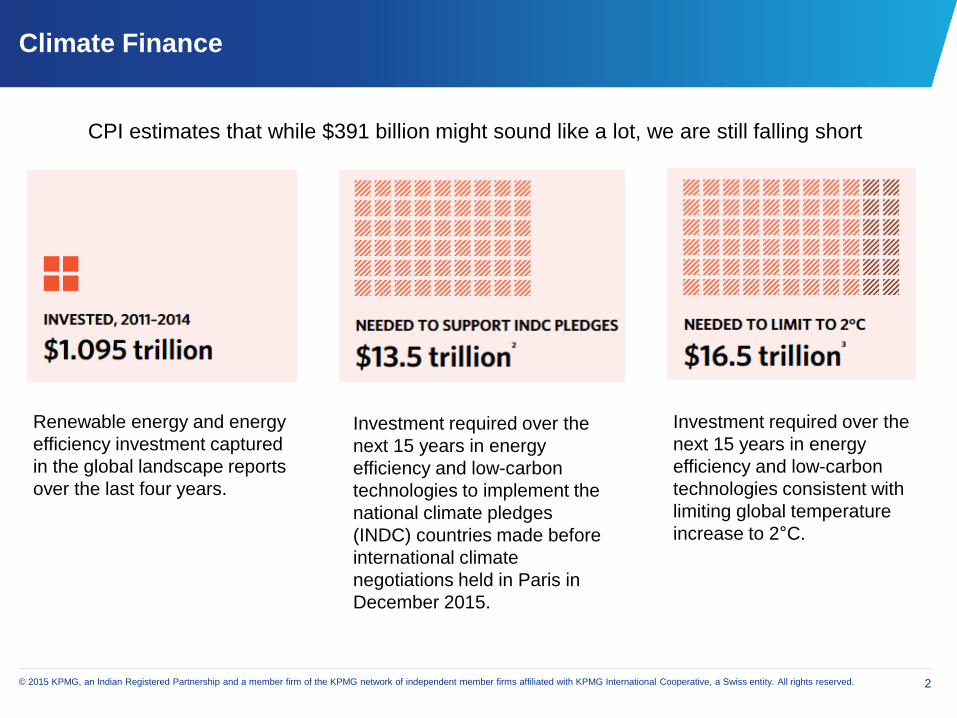

CPI estimates that while $391 billion might sound like a lot, we are still falling short

Renewable energy and energy

efficiency investment captured

in the global landscape reports

over the last four years.

Investment required over the

next 15 years in energy

efficiency and low-carbon

technologies to implement the

national climate pledges

(INDC) countries made before

international climate

negotiations held in Paris in

December 2015.

Investment required over the

next 15 years in energy

efficiency and low-carbon

technologies consistent with

limiting global temperature

increase to 2°C.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 3

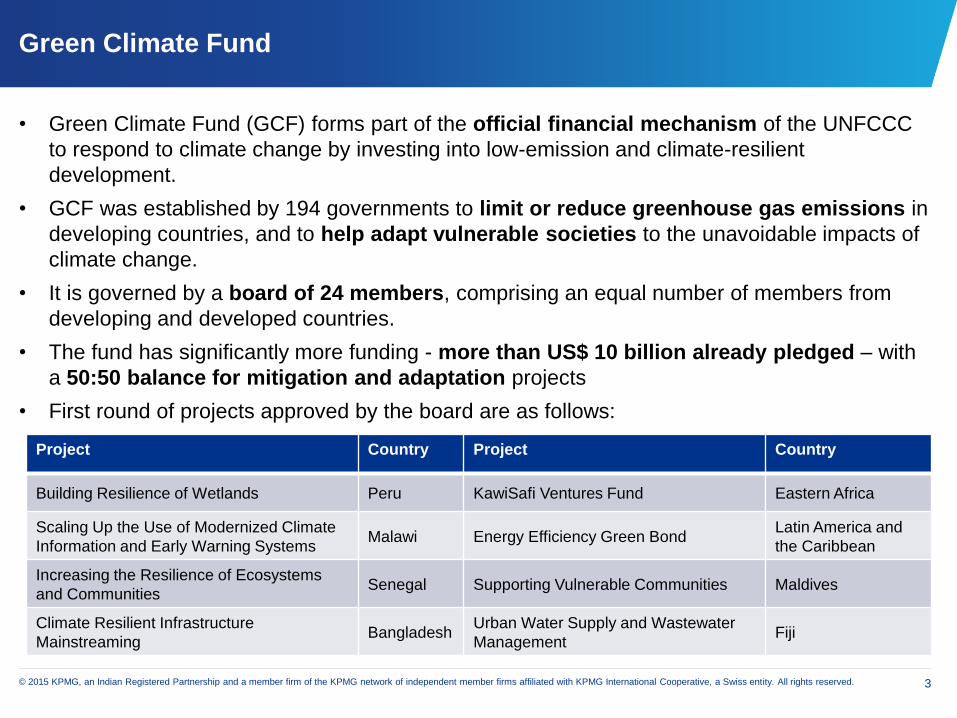

Green Climate Fund

• Green Climate Fund (GCF) forms part of the official financial mechanism of the UNFCCC

to respond to climate change by investing into low-emission and climate-resilient

development.

• GCF was established by 194 governments to limit or reduce greenhouse gas emissions in

developing countries, and to help adapt vulnerable societies to the unavoidable impacts of

climate change.

• It is governed by a board of 24 members, comprising an equal number of members from

developing and developed countries.

• The fund has significantly more funding - more than US$ 10 billion already pledged – with

a 50:50 balance for mitigation and adaptation projects

• First round of projects approved by the board are as follows:

Project Country Project Country

Building Resilience of Wetlands Peru KawiSafi Ventures Fund Eastern Africa

Scaling Up the Use of Modernized Climate

Information and Early Warning SystemsMalawi Energy Efficiency Green Bond

Latin America and

the Caribbean

Increasing the Resilience of Ecosystems

and CommunitiesSenegal Supporting Vulnerable Communities Maldives

Climate Resilient Infrastructure

MainstreamingBangladesh

Urban Water Supply and Wastewater

ManagementFiji

Nationally

Appropriate

Mitigation Actions

(NAMAs)

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 5

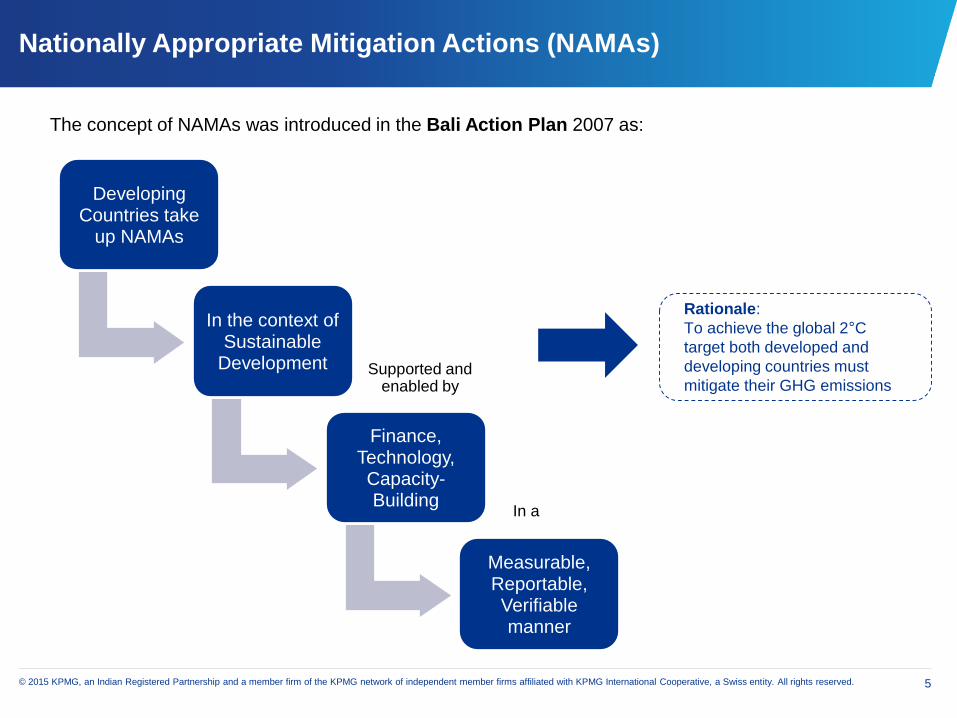

Nationally Appropriate Mitigation Actions (NAMAs)

Rationale:

To achieve the global 2°C

target both developed and

developing countries must

mitigate their GHG emissions

Developing Countries take

up NAMAs

In the context of Sustainable

Development

Finance, Technology, Capacity-Building

Measurable, Reportable, Verifiable manner

The concept of NAMAs was introduced in the Bali Action Plan 2007 as:

Supported and enabled by

In a

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 6

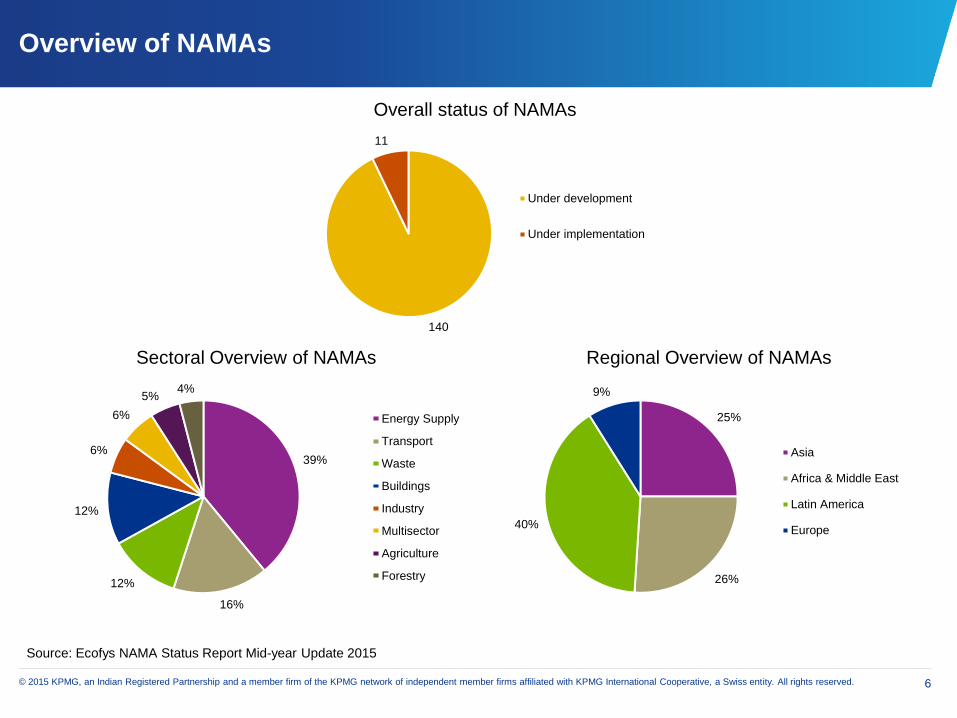

Overview of NAMAs

39%

16%

12%

12%

6%

6%

5%4%

Sectoral Overview of NAMAs

Energy Supply

Transport

Waste

Buildings

Industry

Multisector

Agriculture

Forestry

25%

26%

40%

9%

Regional Overview of NAMAs

Asia

Africa & Middle East

Latin America

Europe

140

11

Overall status of NAMAs

Under development

Under implementation

Source: Ecofys NAMA Status Report Mid-year Update 2015

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 7

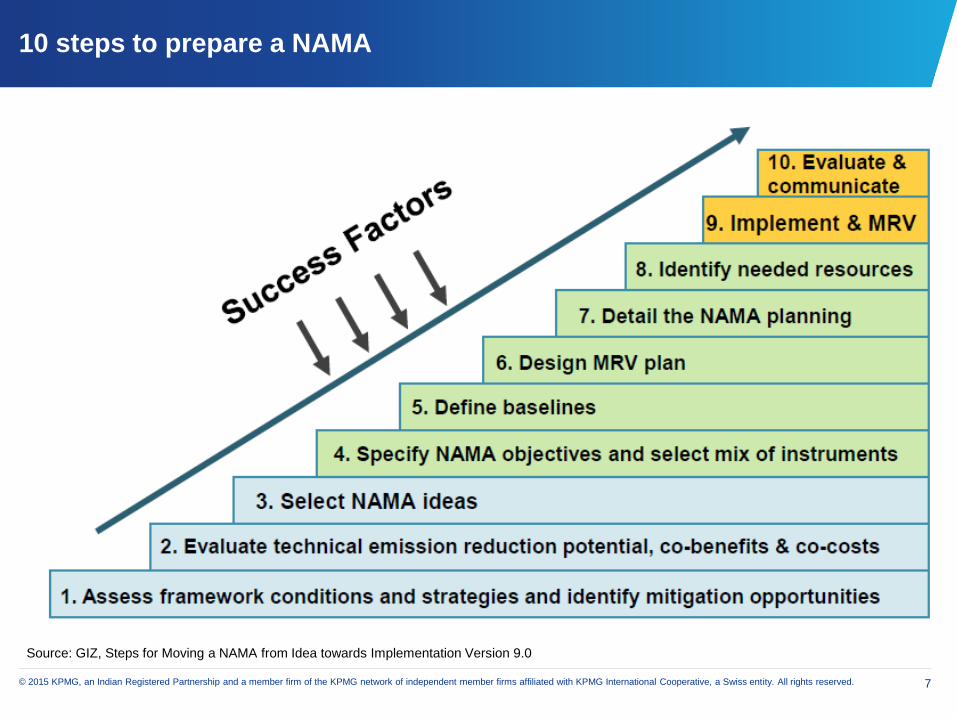

10 steps to prepare a NAMA

Source: GIZ, Steps for Moving a NAMA from Idea towards Implementation Version 9.0

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 8

NAMAs in India

• In July 2014, the Indian Ministry of Environment decided to develop NAMAs in the waste and forestry

sectors.

• On behalf of the German Federal Ministry for the Environment (BMUB), GIZ is advising the Indian Ministry

of Environment on carrying out NAMAs in India and on technical and institutional issues.

• Feasibility studies have been conducted in the two sectors to further identify sub-sectors in which NAMA

activities can achieve the most sustainable impacts.

• The NAMA plans that will subsequently be formulated on the specific activities would build on existing

Indian Government programmes or policies. At the same time, they would promote implementation of

the NAMAs and provide incentives for emission reductions.

• The next step will involve developing methods to measure and verify the NAMA activities, and support

reporting processes.

• The Ministry of Environment is receiving advice on designing the institutional and personnel structure

for the future NAMA coordination office. Together with the partners, the project is developing guidelines

and frameworks for implementing NAMAs in India.

Source: GIZ, Development and management of nationally appropriate mitigation actions (NAMAs), https://www.giz.de/en/worldwide/29663.html

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 9

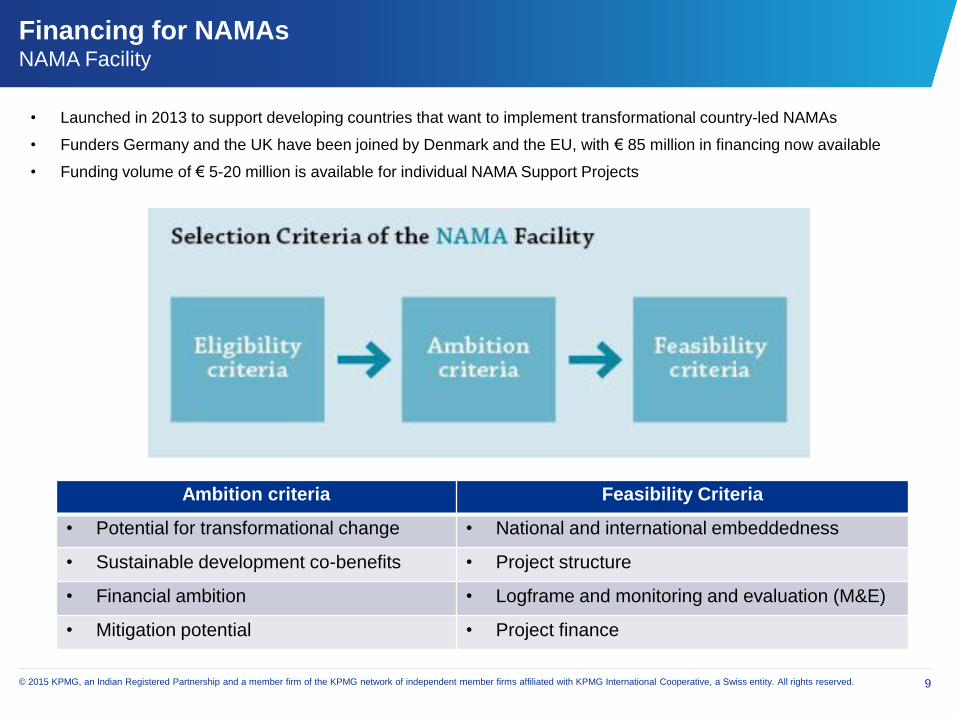

Financing for NAMAsNAMA Facility

• Launched in 2013 to support developing countries that want to implement transformational country-led NAMAs

• Funders Germany and the UK have been joined by Denmark and the EU, with € 85 million in financing now available

• Funding volume of € 5-20 million is available for individual NAMA Support Projects

Ambition criteria Feasibility Criteria

• Potential for transformational change • National and international embeddedness

• Sustainable development co-benefits • Project structure

• Financial ambition • Logframe and monitoring and evaluation (M&E)

• Mitigation potential • Project finance

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 10

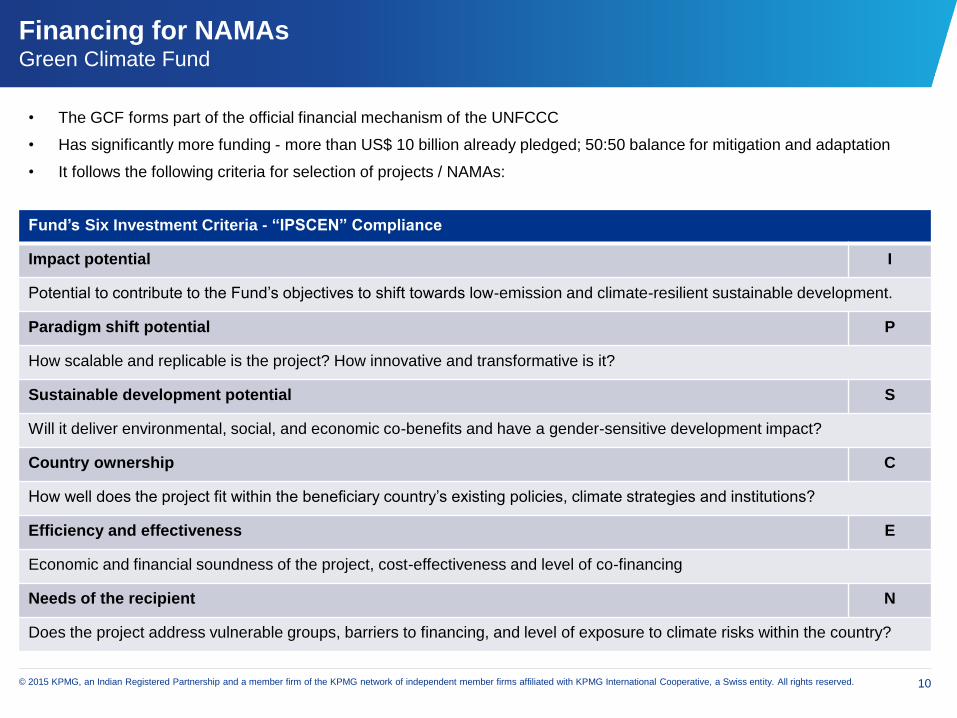

Financing for NAMAsGreen Climate Fund

• The GCF forms part of the official financial mechanism of the UNFCCC

• Has significantly more funding - more than US$ 10 billion already pledged; 50:50 balance for mitigation and adaptation

• It follows the following criteria for selection of projects / NAMAs:

Fund’s Six Investment Criteria - “IPSCEN” Compliance

Impact potential I

Potential to contribute to the Fund’s objectives to shift towards low-emission and climate-resilient sustainable development.

Paradigm shift potential P

How scalable and replicable is the project? How innovative and transformative is it?

Sustainable development potential S

Will it deliver environmental, social, and economic co-benefits and have a gender-sensitive development impact?

Country ownership C

How well does the project fit within the beneficiary country’s existing policies, climate strategies and institutions?

Efficiency and effectiveness E

Economic and financial soundness of the project, cost-effectiveness and level of co-financing

Needs of the recipient N

Does the project address vulnerable groups, barriers to financing, and level of exposure to climate risks within the country?

Green Bonds

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 12

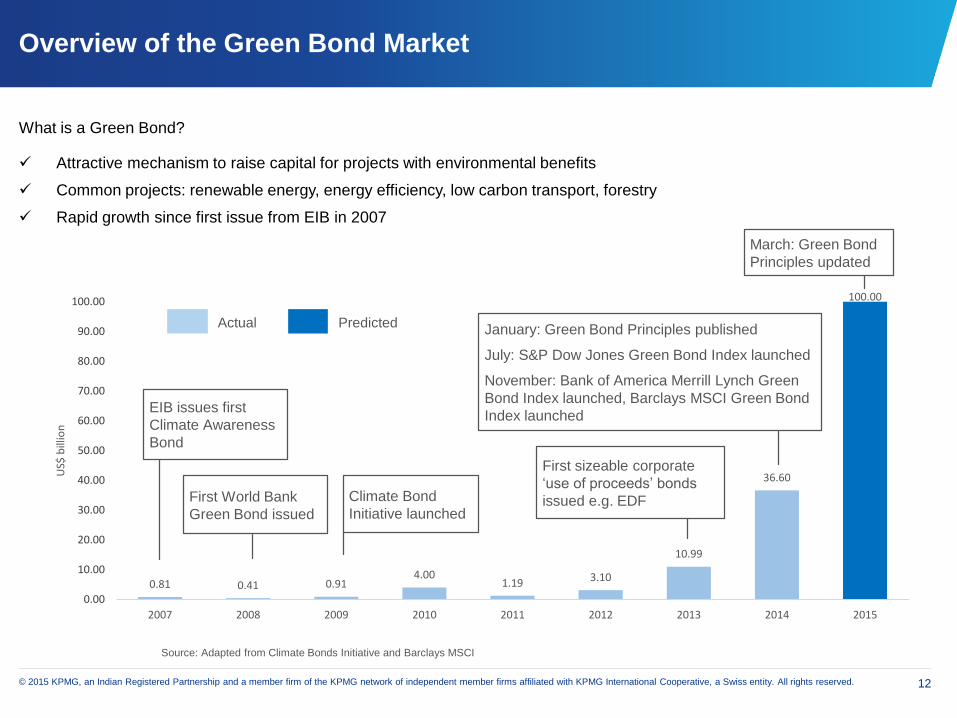

Overview of the Green Bond Market

What is a Green Bond?

Attractive mechanism to raise capital for projects with environmental benefits

Common projects: renewable energy, energy efficiency, low carbon transport, forestry

Rapid growth since first issue from EIB in 2007

0.81 0.41 0.914.00

1.19 3.10

10.99

36.60

100.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

2007 2008 2009 2010 2011 2012 2013 2014 2015

US$

bill

ion

Source: Adapted from Climate Bonds Initiative and Barclays MSCI

EIB issues first

Climate Awareness

Bond

First World Bank

Green Bond issued

Climate Bond

Initiative launched

First sizeable corporate

‘use of proceeds’ bonds

issued e.g. EDF

January: Green Bond Principles published

July: S&P Dow Jones Green Bond Index launched

November: Bank of America Merrill Lynch Green

Bond Index launched, Barclays MSCI Green Bond

Index launched

March: Green Bond

Principles updated

Actual Predicted

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 13

Overview of the Green Bond Market

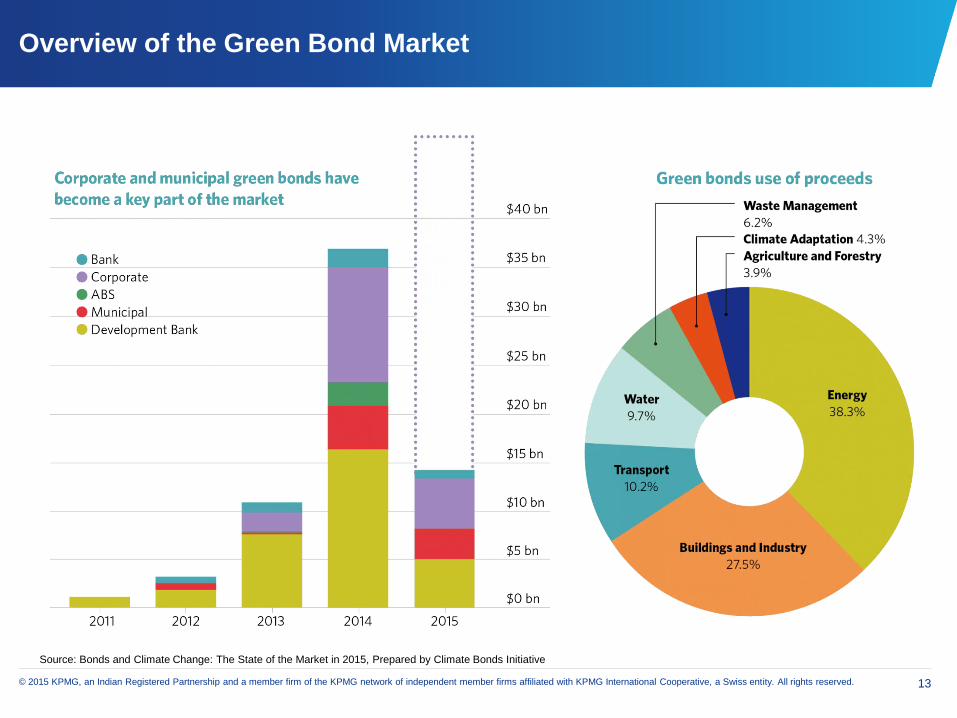

Source: Bonds and Climate Change: The State of the Market in 2015, Prepared by Climate Bonds Initiative

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 14

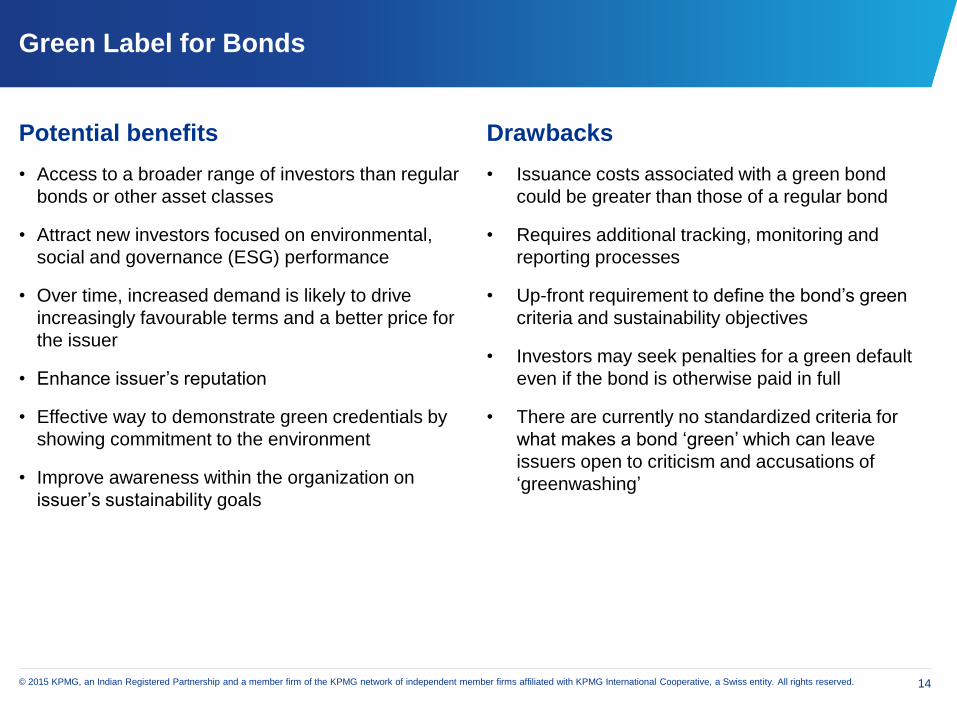

Green Label for Bonds

Potential benefits

• Access to a broader range of investors than regular

bonds or other asset classes

• Attract new investors focused on environmental,

social and governance (ESG) performance

• Over time, increased demand is likely to drive

increasingly favourable terms and a better price for

the issuer

• Enhance issuer’s reputation

• Effective way to demonstrate green credentials by

showing commitment to the environment

• Improve awareness within the organization on

issuer’s sustainability goals

Drawbacks

• Issuance costs associated with a green bond

could be greater than those of a regular bond

• Requires additional tracking, monitoring and

reporting processes

• Up-front requirement to define the bond’s green

criteria and sustainability objectives

• Investors may seek penalties for a green default

even if the bond is otherwise paid in full

• There are currently no standardized criteria for

what makes a bond ‘green’ which can leave

issuers open to criticism and accusations of

‘greenwashing’

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 15

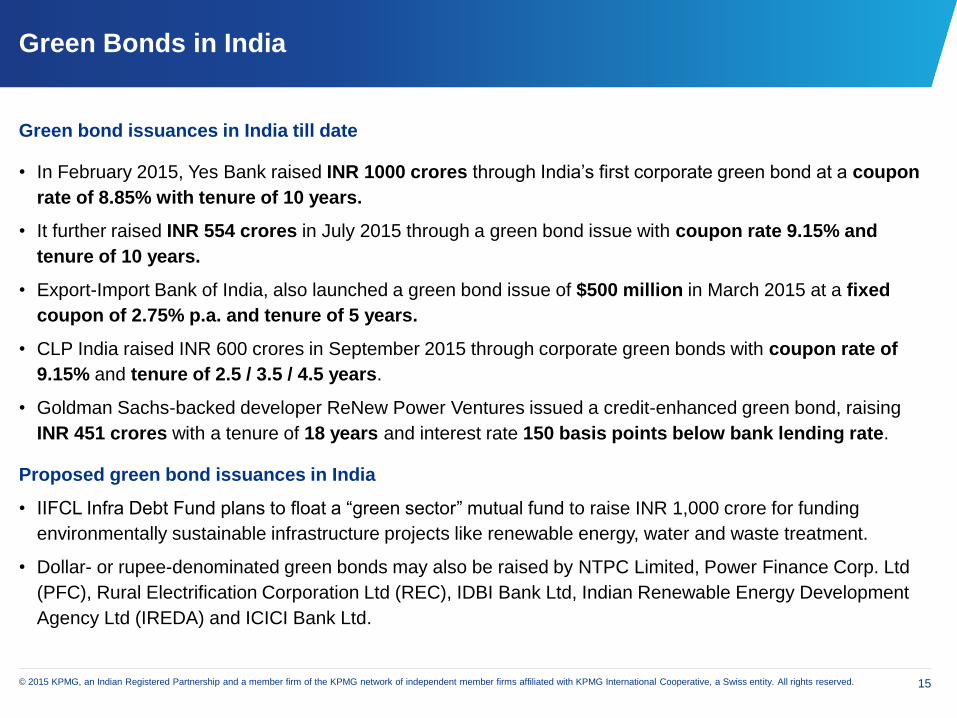

Green Bonds in India

Green bond issuances in India till date

• In February 2015, Yes Bank raised INR 1000 crores through India’s first corporate green bond at a coupon

rate of 8.85% with tenure of 10 years.

• It further raised INR 554 crores in July 2015 through a green bond issue with coupon rate 9.15% and

tenure of 10 years.

• Export-Import Bank of India, also launched a green bond issue of $500 million in March 2015 at a fixed

coupon of 2.75% p.a. and tenure of 5 years.

• CLP India raised INR 600 crores in September 2015 through corporate green bonds with coupon rate of

9.15% and tenure of 2.5 / 3.5 / 4.5 years.

• Goldman Sachs-backed developer ReNew Power Ventures issued a credit-enhanced green bond, raising

INR 451 crores with a tenure of 18 years and interest rate 150 basis points below bank lending rate.

Proposed green bond issuances in India

• IIFCL Infra Debt Fund plans to float a “green sector” mutual fund to raise INR 1,000 crore for funding

environmentally sustainable infrastructure projects like renewable energy, water and waste treatment.

• Dollar- or rupee-denominated green bonds may also be raised by NTPC Limited, Power Finance Corp. Ltd

(PFC), Rural Electrification Corporation Ltd (REC), IDBI Bank Ltd, Indian Renewable Energy Development

Agency Ltd (IREDA) and ICICI Bank Ltd.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 16

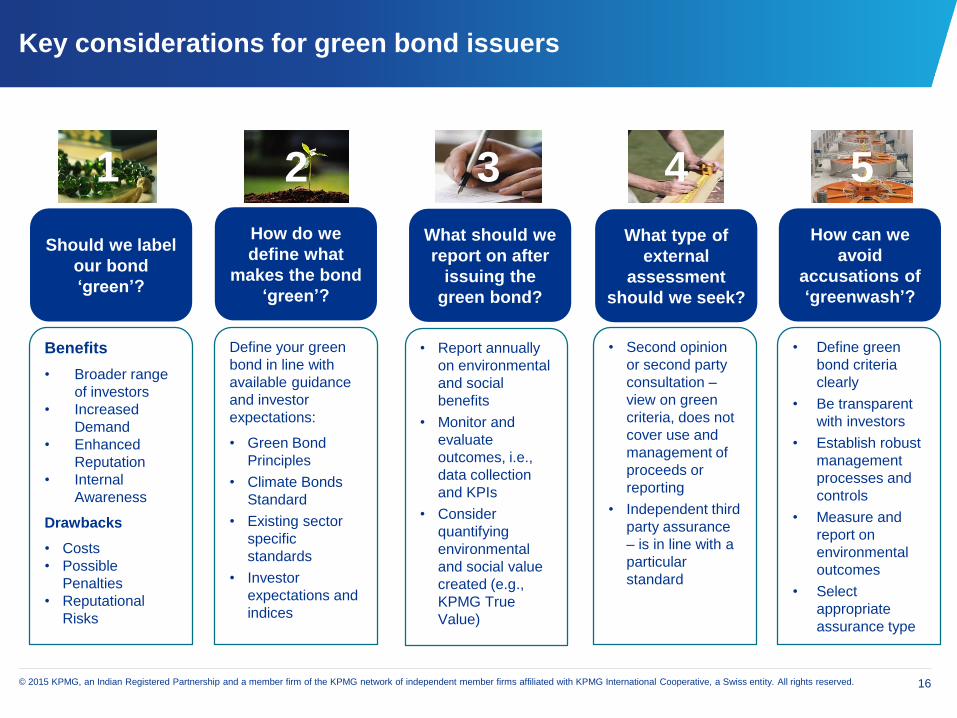

Key considerations for green bond issuers

1 2 3 4 5

Benefits

• Broader range

of investors

• Increased

Demand

• Enhanced

Reputation

• Internal

Awareness

Drawbacks

• Costs

• Possible

Penalties

• Reputational

Risks

Define your green

bond in line with

available guidance

and investor

expectations:

• Green Bond

Principles

• Climate Bonds

Standard

• Existing sector

specific

standards

• Investor

expectations and

indices

• Report annually

on environmental

and social

benefits

• Monitor and

evaluate

outcomes, i.e.,

data collection

and KPIs

• Consider

quantifying

environmental

and social value

created (e.g.,

KPMG True

Value)

• Second opinion

or second party

consultation –

view on green

criteria, does not

cover use and

management of

proceeds or

reporting

• Independent third

party assurance

– is in line with a

particular

standard

• Define green

bond criteria

clearly

• Be transparent

with investors

• Establish robust

management

processes and

controls

• Measure and

report on

environmental

outcomes

• Select

appropriate

assurance type

Should we label

our bond

‘green’?

How do we

define what

makes the bond

‘green’?

What should we

report on after

issuing the

green bond?

What type of

external

assessment

should we seek?

How can we

avoid

accusations of

‘greenwash’?

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 17

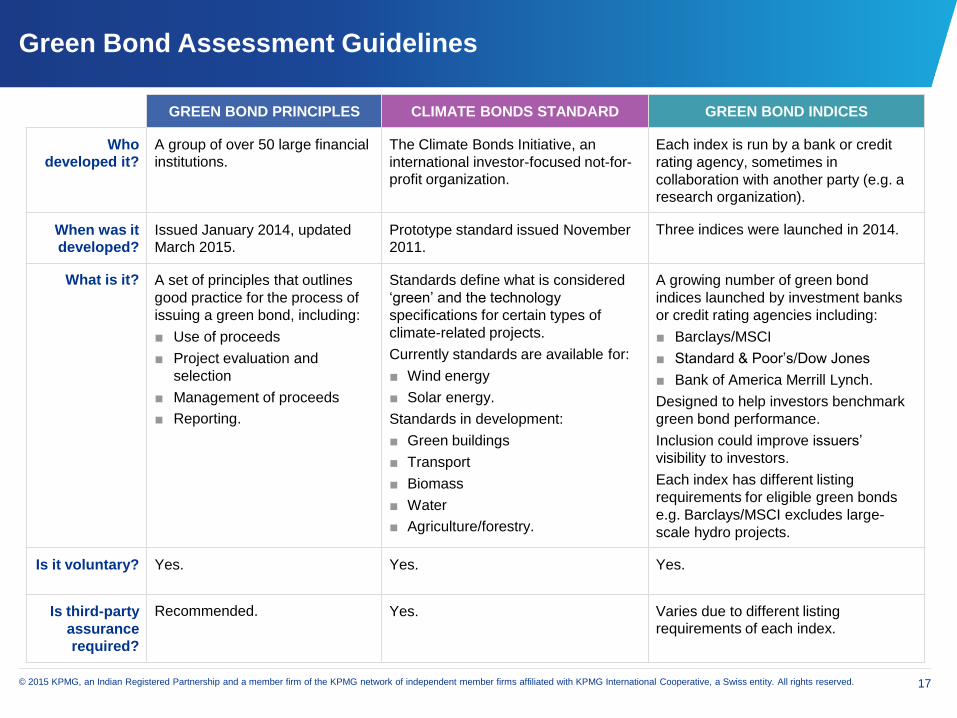

Green Bond Assessment Guidelines

GREEN BOND PRINCIPLES CLIMATE BONDS STANDARD GREEN BOND INDICES

Who

developed it?

A group of over 50 large financial

institutions.

The Climate Bonds Initiative, an

international investor-focused not-for-

profit organization.

Each index is run by a bank or credit

rating agency, sometimes in

collaboration with another party (e.g. a

research organization).

When was it

developed?

Issued January 2014, updated

March 2015.

Prototype standard issued November

2011.

Three indices were launched in 2014.

What is it? A set of principles that outlines

good practice for the process of

issuing a green bond, including:

■ Use of proceeds

■ Project evaluation and

selection

■ Management of proceeds

■ Reporting.

Standards define what is considered

‘green’ and the technology

specifications for certain types of

climate-related projects.

Currently standards are available for:

■ Wind energy

■ Solar energy.

Standards in development:

■ Green buildings

■ Transport

■ Biomass

■ Water

■ Agriculture/forestry.

A growing number of green bond

indices launched by investment banks

or credit rating agencies including:

■ Barclays/MSCI

■ Standard & Poor’s/Dow Jones

■ Bank of America Merrill Lynch.

Designed to help investors benchmark

green bond performance.

Inclusion could improve issuers’

visibility to investors.

Each index has different listing

requirements for eligible green bonds

e.g. Barclays/MSCI excludes large-

scale hydro projects.

Is it voluntary? Yes. Yes. Yes.

Is third-party

assurance

required?

Recommended. Yes. Varies due to different listing

requirements of each index.

Thank you

Presentation by Santhosh Jayaram

© 2015 KPMG, an Indian Registered Partnership and

a member firm of the KPMG network of independent

member firms affiliated with KPMG International

Cooperative, a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through

complexity” are registered trademarks or trademarks

of KPMG International.