Embed Size (px)

Citation preview

IPTV in CEE: the Way Forward or Still a Market Niche?

Edyta Kosowska, Research Analyst

Information & Communication TechnologiesInformation & Communication Technologies

14 December, 2010

Functional Expertise

• Market research & consulting expertise. Particular expertise in:

- Secondary and primary research

- Strategic analysis

- Contacts with media

Industry Expertise

� Experience base covering broad range of sectors, leveraging long-standing working relationships with leading

industry participants’ Senior Executives

- Mobile Communications

- Fixed & Mobile Broadband

- Value-added Services

- Machine-to-Machine

Today’s Presenter

2

- Machine-to-Machine

What I bring to the Team

• Telecom market knowledge (technologies, trends, etc.)

• Understanding of Central and Eastern Europe markets realities

• Analytical skills

Career Highlights

• Extensive expertise in telecom market analysis.

• Working directly with many major companies, including:

- Amdocs, USA

- Hitachi, Japan

- HP, USA

- TP SA (France Telecom), Poland

Education

• Master of Economics from University of Economics, Cracow, Poland

Edyta KosowskaResearch Analyst ICT

Frost & SullivanCentral and Eastern EuropeWarsaw

Focus Points

Introduction

Current Status of the IPTV Market in Central and Eastern Europe

IPTV Market Drivers and Challenges

3

Growth Opportunities in the IPTV Market

Conclusions

Introduction

4

IPTV Spans the Telecoms and Pay-TV Ecosystems

Pay-TV Market Segmentation

Cable TV

Analogue

Telecom Market Segmentation

Telephony

Fixed-line

5

Satellite TV

IPTV

Television over public Internet was excluded from the analysis.

Digital

Source Frost & Sullivan

Mobile

Broadband

Fixed

Mobile

Incumbents Operators in CEE Drives IPTV Market Growth

•Bulgaria

•The Czech Republic

•Hungary

6

In the near future, cable TV operators as well as ISPs are likely to play more important roles in the market.

•Poland

•Romania

Source Frost & Sullivan

Current Status of the IPTV Market in Central and Eastern Europe

7

IPTV Markets in Bulgaria and Romania are the Least Developed in the CEE Region

IPTV

� The lowest IPTV penetration in the region.

� IPTV has just become interesting for the main

telecom market participants.

� FTTH/B investment drives service development.

� New market entrants are likely to come from the

small ISPs space.

BULGARIA

HUNGARY ROMANIA

� The IPTV market is dominated by the incumbent

operator Telefonica. However, due to limited

attractiveness and technical issues, the

company's subscribers base decreased in 2010.

� IPTV has started to be deployed by smaller

telecom operators, also those who provide

broadband in FTTH/B technology.

THE CZECH REPUBLIC

8

� Penetration of pay-TV in Romania is the

highest among CEE countries what

negatively impact IPTV market growth.

� IPTV is still an emerging technology.

Until 2010, IPTV had primarily been

developed by one company, iNES.

� The future growth of the technology is

likely to be dependent on the incumbent

operator strategy, which launched IPTV

at the end of 2009.

� Magyar Telecom remains the market

leader. The company is testing

EuroDOCSIS 3.0 technology for IPTV

services provision.

� Usage of cable network for IPTV

provision as well as FTTH/B technology

development are likely to stimulate

IPTV market growth.

HUNGARY ROMANIA

� TP SA has the largest share of the IPTV market

in Poland; however, the operator has started to

focus more on satellite TV services.

� An important market participant is alternative

operator Telefonia Dialog. The service is also

developed also by ISPs: SGT and Inotel.

� In the long term cable TV operators are also

expected to play a role on the market, especially

those who invest in FTTH/B.

POLAND

Source Frost & Sullivan

6

8

10

12

IPTV Market Growth will be Especially Difficult in Countries with High Pay-TV Penetration

Ho

useh

old

Pen

etr

ati

on

(%

)

Bulgaria39

The Czech Republic

235

Poland215

Romania25

Su

bscri

bers

(T

ho

usan

d)

IPTV Market: Household Penetration (CEE), 2007-2017 IPTV Market: Number of Subscribers (CEE), 2010

9

0

2

4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Year

Bulgaria The Czech Republic

Hungary Poland

Romania

Ho

useh

old

Pen

etr

ati

on

(%

)

Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

The IPTV market in the Czech Republic was the largest in the CEE region in terms of both number of subscribers and revenues.

Hungary132

Su

bscri

bers

(T

ho

usan

d)

Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

IPTV Uptake is Directly Proportional to Broadband and Inversely Proportional to Pay-TV Market Penetration

IPTV versus Pay-TVIPTV versus Broadband

Czech Republic

Hungary4%

5%

6%

7%

IPT

V P

en

etr

ati

on

(%

)

Czech Republic

Hungary

5%

6%

7%

Pen

etr

ati

on

(%

)

IPTV Market: IPTV Household Penetration versus Broadband Household Penetration (CEE), 2010*

IPTV Market: IPTV Household Penetration versus pay-TV Household Penetration (CEE), 2010*

10

* The size of the bubble represents the total number of subscribers Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

Bulgaria

Hungary

Poland

Romania0%

1%

2%

3%

4%

40% 45% 50% 55% 60% 65% 70% 75%

Ho

useh

old

s IP

TV

Households Broadband Penetration (%)

Bulgaria

Hungary

Poland

Romania0%

1%

2%

3%

4%

40% 50% 60% 70% 80% 90% 100% 110%H

ou

seh

old

s IP

TV

Pen

etr

ati

on

(%

)

Households pay-TV Penetration (%)

* The size of the bubble represents the total number of subscribers Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

60

80

100

120

150

200

250

300

Revenue Growth will be Driven by Both ARPU and Subscribers Base Increases

Gro

wth

Rate

(%

)

Rev

en

ues (

€M

illio

n)

IPTV Market: Revenue Forecast (CEE), 2007-2017

CEE0.651.6%

ROW39.0598.4%

Su

bscri

bers

(M

illio

n)

IPTV Market: Number of Subscribers (CEE and ROW), 2010

11

0

20

40

60

0

50

100

150

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Year

Revenues Growth Rate

Gro

wth

Rate

(%

)

Rev

en

ues (

Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

Revenues from IPTV services are likely to

remain a small part of total telecoms revenues in the short to mid term.

Note : All figures are rounded; the base year is 2010. Source Frost & Sullivan

IPTV Market Drivers and Challenges

12

The IPTV Market will be Largely Driven by the Development of Bundled Services

IPTV Market Drivers in CEE Countries

Demand for Value-added

Services

Additional important stimuli are likely to be investments in deploying and upgrading broadband infrastructure.

13

Bundled Services

Development

Demand for High Quality

Digital TV Infrastructure Deployment

Source Frost & Sullivan

For New IPTV Market Entrants it is Difficult to Penetrate Saturated Pay-TV Markets

IPTV Market Restraints in CEE Countries

Relatively Low Broadband Penetration

High Pay-TV Penetration

Piracy Acceptance

Price Sensitive Society

14

Source Frost & Sullivan

Acceptance

Important restraints also include social factors.

Differentiating IPTV Offers in Terms of Quality, Content and VAS will Deliver Significant Competitive Advantages

New VAS Implementation

Getting Access to Interesting

Content

Challenges

A wide content offer at reasonable prices are the basic requirements that need to be achieved to compete

IPTV Market Challenges in CEE Countries

15

Competition with Other

Pay-TV Technologies

Technology Issues

Implementation of Adequate

Pricing Policy

Challenges achieved to compete with other pay-TV players.

Source Frost & Sullivan

Growth Opportunities in the IPTV Market

16

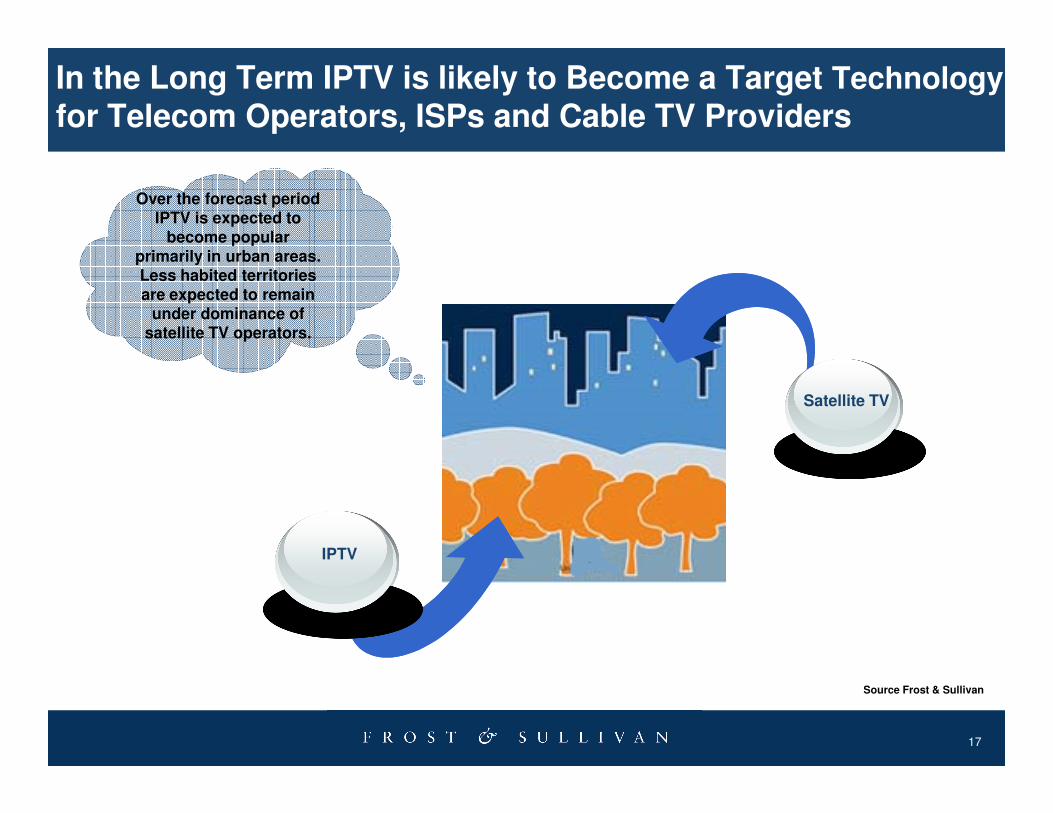

In the Long Term IPTV is likely to Become a Target Technology

for Telecom Operators, ISPs and Cable TV Providers

Satellite TV

Over the forecast period IPTV is expected to

become popular primarily in urban areas. Less habited territories are expected to remain

under dominance of satellite TV operators.

17

IPTV

Satellite TV

Source Frost & Sullivan

Changes in Media Consumption will Drive IPTV Market Growth

TV on Demand

TV as PC

Channels a-la-carte

3D TVConsumer demand is expected to drive development of more customised offers.

18

New Pricing Models

IPTV on Mobile Network

2010 2011 20122009 2013 2014 2015 2016 201720082007

HD TV

carte

TV Everywhere

Source Frost & Sullivan

New Business and Technological Opportunities are likely to Make IPTV Business More Profitable

Readiness for High Content Expenditures

Clear Communication of Value Added

Key Success

Appropriate Pricing Strategy

New pricing models are likely to attract more price sensitive

users.

19

In the near future, IPTV operators should take

advantage of lower prices of infrastructure and end-user devices.

Success Factors

Appropriate Marketing Messages

Strategic Partnerships

Infrastructure Upgrade

Source Frost & Sullivan

Summary

20

In the Short Term, IPTV in CEE Is Unlikely to Expand Beyond Market Niche

Access to premium content is expected to be the main competitive advantage.

Lack of sufficient infrastructure limits growth potential in the

IPTV market.

TV services must be embedded in all CEE telecoms offers to compete with pay-TV providers on the triple play market.

However, in the short to mid term IPTV is unlikely to be the only technology deployed. Many incumbents are expected to

focus on satellite TV development, especially in the rural areas.

21

Conclusions

Price sensitive societies expect low prices of the IPTV services.

Changing TV consumption is likely to be one of the most important market stimulus.

IPTV roll-outs are likely to be the most economically justified in the urban areas.

Source Frost & Sullivan

Partnerships with pay-TV market participants may

facilitate market entrance.

Next Steps

� Request a proposal for our Growth Partnership Services or Growth Consulting Services to support you and your team in accelerating the growth of your company. ([email protected]) + 44 (0) 207 343 8383.

� Join us at our annual Growth, Innovation, and Leadership 2011: A Frost & Sullivan Global Congress on Corporate Growth, London

(www.gil-global.com)

22

(www.gil-global.com)

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities(www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

23

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/pages/Frost-Sullivan/249995031751?ref=ts

http://www.linkedin.com/companies/4506

24

http://twitter.com/frost_sullivan

http://www.slideshare.net/FrostandSullivan

For Additional Information

Joanna Lewandowska

Corporate Communications

ICT Europe

(0048) 22 390 41 46

Gustavo Cury

Sales manager

ICT Europe

(0044) 20 7343 8310

25

Adrian Drozd

Research Manager

Telecoms Europe

(0044) 1865 398 699