Embed Size (px)

Citation preview

Auditing

By Radhika

Syllabus

Unit -1

1. Introduction to Auditing

2. Origin & Development of Auditing

3. Meaning, Definition & Characteristics of Auditing

4. Scope & Principles of Auditing

5. Functions & Limitations of Auditing

6. Objects of Auditing

7. Book keeping, Accountancy, Auditing &

investigation

Introduction

Economic decisions in every society must be based upon

the information available at the time the decision is made.

Unreliable information can cause inefficient use of resources

to the detriment of the society and to the decision makers

themselves.

As society become more complex, there is an increase

likelihood that unreliable information will be provided to

decision makers.

Cont.

There are several reasons for this: remoteness of

information, voluminous data and the existence of complex

exchange transactions.

As a means of overcoming the problem of unreliable

information, the decision-maker must develop a method of

assuring him that the information is sufficiently reliable for

these decisions. In doing this he must weigh the cost of

obtaining more reliable information against the expected

benefits.

Cont.

A common way to obtain such reliable information is to

have some type of verification (audit) performed by

independent persons. The audited information is then used in

the decision making process on the assumption that it is

reasonably complete, accurate and unbiased.

Origin And Development

The term audit is derived from the Latin term ‘audire,’ which

means to hear. In early days an auditor used to listen to the

accounts read over by an accountant in order to check them.

Auditing is as old as accounting. It was in use in all ancient

countries such as Greece, Egypt, Rome, U.K. and India. The

Vedas contain reference to accounts and auditing. Arthasashthra

by Kautilya detailed rules for accounting and auditing of public

finances.

Cont.

Auditing evolved and grew rapidly after the industrial

revolution in the 18th century with the growth of the joint stock

companies the ownership and management became separate. The

shareholders who were the owners needed a report from an

independent expert on the accounts of the company managed by

the board of directors who were the employees.

The original objective of auditing was to detect and

prevent errors and frauds.

Development

In India the companies Act 1913 made audit of company

accounts compulsory. With the increase in the size of the

companies and the volume of transactions the objective of audit

shifted and audit was expected to ascertain whether the accounts

were true and fair rather than detection of errors and frauds.

Hence the emphasis was not on arithmetical accuracy but on

a fair representation of the financial efforts the companies Act

1913 also prescribed for the first time the qualification of auditors.

Cont.

The later developments in auditing pertain to the use of

computers in accounting and auditing.

In conclusion it can be said that auditing has come a long

way from hearing of accounts to taking the help of computers to

examine computerized accounts.

Exercise

Meaning

The general meaning of an audit is a planned and documented

activity performed by qualified personnel to determine by

investigation, examination, or evaluation of objective evidence,

the adequacy and compliance with established procedures, or

applicable documents, and the effectiveness of implementation.

Definition

Simple Definition:-

“Audit is an examination of accounts & records which is

carried out by vouching the evidences, supporting various

transactions; by such an examination it is ascertained that the

Balance Sheet gives a true & fair view of the state of affairs of

business & the Profit & Loss Account gives a true & fair view

of the profit or loss of business.

Cont.

Spicer and Pegler:-

"Auditing is such an examination of books of accounts and

vouchers of business, as will enable the auditors to satisfy

himself that the balance sheet is properly drawn up, so as to give

a true and fair view of the state of affairs of the business and that

the profit and loss account gives true and fair view of the

profit/loss for the financial period, according to the best of

information and explanation given to him and as shown by the

books; and if not, in what respect he is not satisfied."

Cont.

Prof. L.R.Dicksee:-

“Auditing is an examination of accounting records undertaken

with a view to establish whether they correctly and completely

reflect the transactions to which they relate.”

Characteristics of Auditing

1. Systematic & Scientific Procedure

2. Essential Documents are integral part

3. It is done with the help of vouchers, documents, information

and explanations received from the authorities.

4. Undertaken by an Independent person or Body

5. Analytical approach

Cont.

6. Art & Science Both

7. Verification of the results

8. The Auditor has to satisfy himself with the authenticity

9. Compliance

10. The auditor has to inspect, compare, check, review,

scrutinize the vouchers supporting the transactions and

examine correspondence, Memorandum of Association and

Articles of association etc., in order to establish correctness

of the books of accounts.

Scope of AuditingThe scope of audit is increasing with the increase in the

complexities of the business. It is said that long range objectives of

an audit should be to serve as a guide to the management future

decisions.

Today most of the economic activities are largely conducted

through public finance. The auditor has to see whether these larger

funds are properly used. The scope of audit encompasses

verification of accounts with a intention of giving opinion on its

reliability. Hence it covers cost audit, management audit, social

audit etc. It should be remembered that an auditor just expressed

his opinion on the authenticity of the account. He has no power to

take action against anybody, in this regard its said that “an auditor

is a watch dog but not a blood hound”.

Cont.

1. Legal Requirements

2. Entity Aspects

3. Reliable Information

4. Proper Communication

5. Evaluation

6. Test

7. Comparison

8. Judgments

9. Work

10. Evidence

11. Misstatement

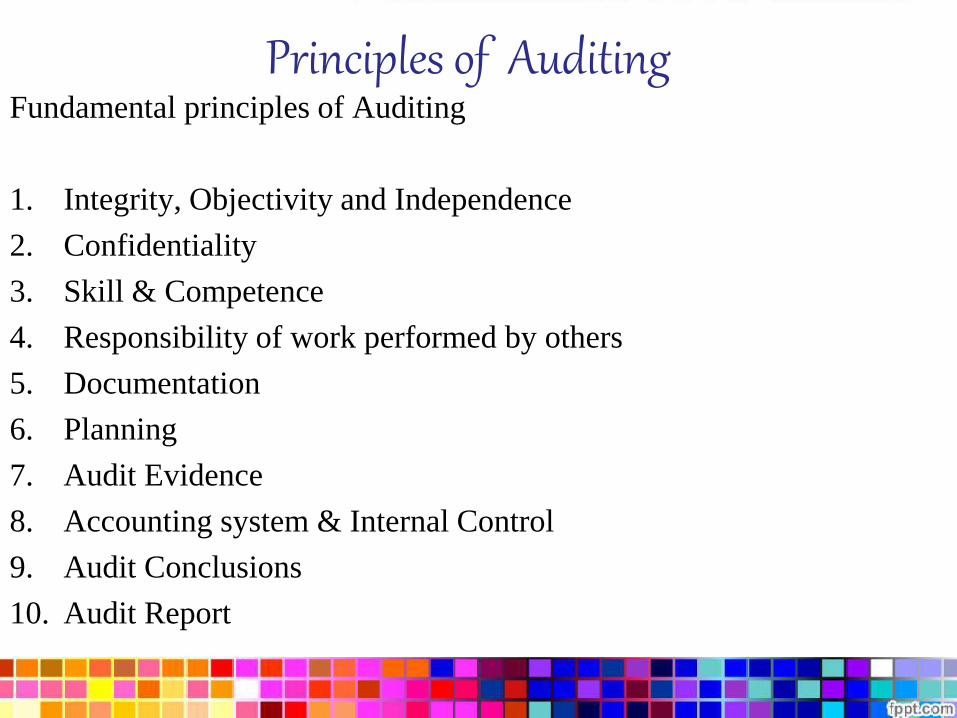

Principles of AuditingFundamental principles of Auditing

1. Integrity, Objectivity and Independence

2. Confidentiality

3. Skill & Competence

4. Responsibility of work performed by others

5. Documentation

6. Planning

7. Audit Evidence

8. Accounting system & Internal Control

9. Audit Conclusions

10. Audit Report

Functions of Auditing

1. Accounting control

Audit is an instrument of accounting control. The truth and

fairness of the accounting information is controlled and checked

by auditing activities.

2. Safeguard

Audit acts as a safeguard on behalf of the proprietor/s

(whether an individual or a group of persons) against cost

control, carelessness or fraud on the part of the proprietors’

agents or servants in the realisation and utilisation of his/their

money and other assets.

Cont.

3. Assurance

Audit assures on the proprietors’ behalf that the accounts

maintained truly represent facts and expenditure has been incurred

with due regularity and propriety.

4. Assessment

Audit assesses the adequacy of the accounting system in

order to ascertain its effectiveness in maintaining accounting

records of an organization.

5. Review

Audit carries out a review of the financial statements to know

whether the accounting records are in agreement with those

statements.

Cont.

6. Reporting tool

Audit is a tool for reporting on the financial statements as

required by the terms of the auditors’ appointment and in

compliance with the relevant statutory obligations.

7. Practical subject

Auditing is a practical subject. It is something that people do.

How it is done today is a result of long history of marginal

changes and responses to new commercial and legal developments

over the centuries with the most rapid progress in the last few

years.

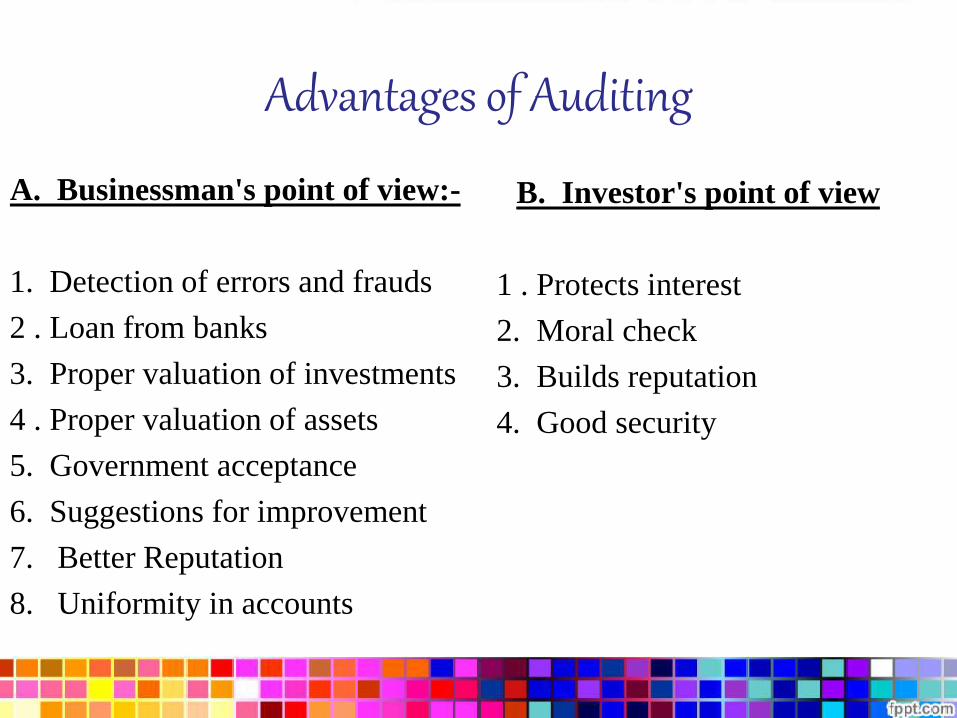

Advantages of Auditing

A. Businessman's point of view:-

1. Detection of errors and frauds

2 . Loan from banks

3. Proper valuation of investments

4 . Proper valuation of assets

5. Government acceptance

6. Suggestions for improvement

7. Better Reputation

8. Uniformity in accounts

B. Investor's point of view

1 . Protects interest

2. Moral check

3. Builds reputation

4. Good security

Cont.

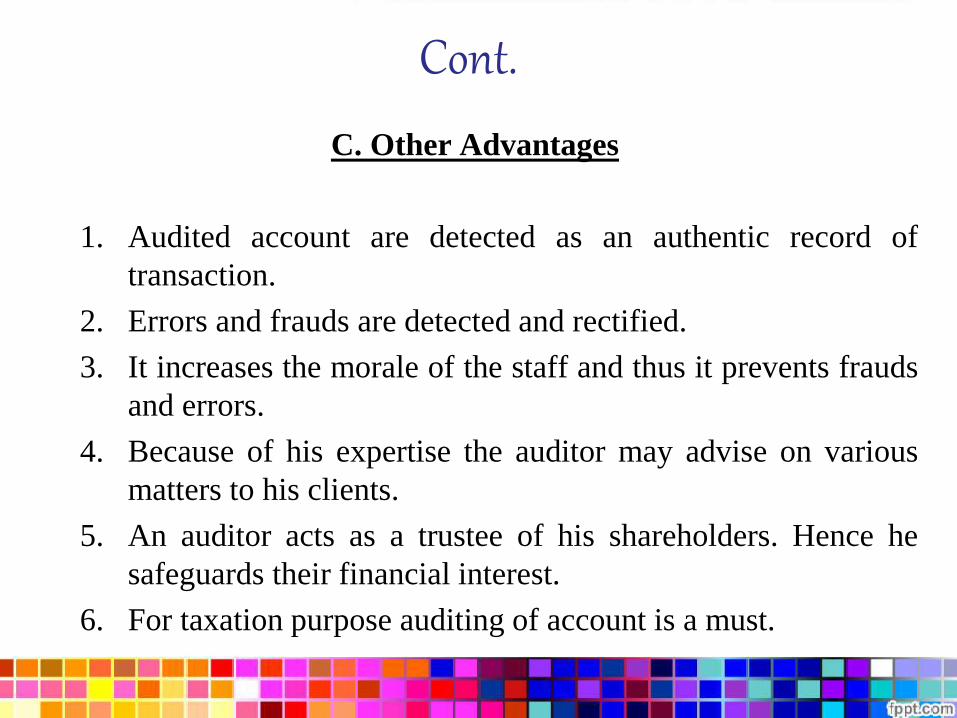

C. Other Advantages

1. Audited account are detected as an authentic record of

transaction.

2. Errors and frauds are detected and rectified.

3. It increases the morale of the staff and thus it prevents frauds

and errors.

4. Because of his expertise the auditor may advise on various

matters to his clients.

5. An auditor acts as a trustee of his shareholders. Hence he

safeguards their financial interest.

6. For taxation purpose auditing of account is a must.

Cont.

7. In case of any claim is to be made from the insurance

company only audited account should be submitted.

8. Even in case of partnership firm auditing of accounts helps in

the settlement of claim at the time of retirement/death of a

partner.

9. Auditor account helps in managerial decisions.

10. They are useful to secure loan at the of amalgamation,

absorption, reconstruction etc.

11. Auditing safeguards the interest of owners, creditors,

investors, and workers.

12. It is useful to take certain financial decisions like issuing of

shares, payment of dividend etc.

Limitations of Auditing

Truly speaking, an audit should have no limitations of its

own. It is designed to protect the interest of all parties who are

interested in the affairs of the business. If there be any

shortcoming arising there from, it may be due to its narrow

scope of application in its related field of operation and

unextended definition of the concept.

Auditing suffers from the following shortcomings:

1. Want of complete picture

The audit may not give complete picture. If the accounts are

prepared with the intention to defraud others, auditor may not be

able to detect them.

Limitations of Auditing

Truly speaking, an audit should have no limitations of its

own. It is designed to protect the interest of all parties who are

interested in the affairs of the business. If there be any

shortcoming arising there from, it may be due to its narrow

scope of application in its related field of operation and

unextended definition of the concept.

Auditing suffers from the following shortcomings:

1. Want of complete picture

The audit may not give complete picture. If the accounts are

prepared with the intention to defraud others, auditor may not be

able to detect them.

Cont.

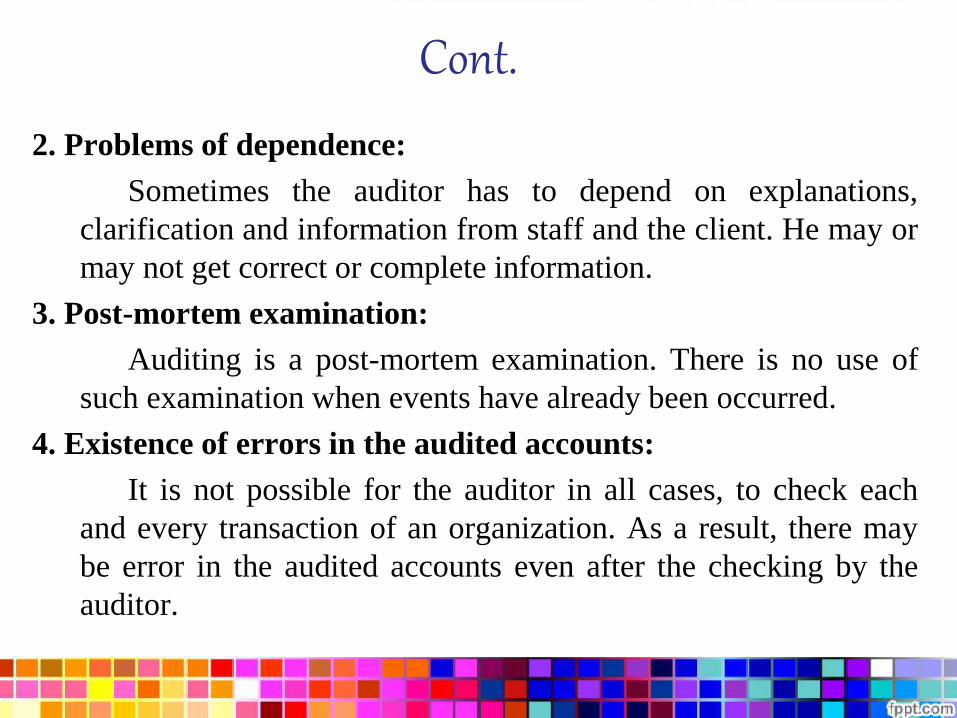

2. Problems of dependence:

Sometimes the auditor has to depend on explanations,

clarification and information from staff and the client. He may or

may not get correct or complete information.

3. Post-mortem examination:

Auditing is a post-mortem examination. There is no use of

such examination when events have already been occurred.

4. Existence of errors in the audited accounts:

It is not possible for the auditor in all cases, to check each

and every transaction of an organization. As a result, there may

be error in the audited accounts even after the checking by the

auditor.

Cont.

5. Lack of expertise:

Auditor has to seek opinion of experts on certain matters on

which he may not have experts knowledge. The auditor has to

depend upon such reports which may not always be correct.

6. Diversified situations:

Auditing is considered to be a mechanical work. Auditors

may not be in a position to frame audit programme, which can be

followed in all situations.

7. Quality of the auditor:

Success of audit depends on the sincerity with which the

auditor has performed his duties. The same audit work can be

done by two different auditors with difference in sincerity.

Cont.

8. Existence of defective policies

The auditor can only report on the truth and fairness of the

financial statements. But other defects, i.e. defects relating to

management and control may not be possible to be covered by

the auditor.

Objects of Auditing

Primary Objective

Varification of a/c

B/s shows true & fair

state

P & L a/c shows true & fair state

Secondary Objective

Detection & Prevention of Errors

Detection & Prevention of Frauds

Other Objectives

Moral Check

Complaince of Co.'s Act

to create trust in govt.

Detection & Prevention of Errors

• trasanction is to be left out to register, partial entry of one transactionError of Omission

• Rs. 1500 recorded as Rs. 5100Error of Commission

• ommission to post,posting wrong side & amount to an a/c, double posting,totalling mistake, balance b/d & c/f

Clerical Error

• fundamental principle of Accountancy & AuditingError of Principle

• two errors togather which will be resulted in trial balance sheet will agree

Compensating Error

Detection & Prevention of Frauds

Misappropriation

Of Cash

Of Goods

By Employees

Manipulation of A/c

Showing more Profits

Showing less profit

By Top Management