Embed Size (px)

DESCRIPTION

Citation preview

RUNNING HEAD: FINANCING AN INTERNET CAFÉ IN INDIA 1

Financing an Internet Café in India

Benjamin S. Cheeks

International School of Management, Paris

Author Note

This paper was submitted to fulfill the requirements of Indian Financial

Markets, IFNM 7019. I would like to thank all of the faculty and staff at Amity

University, Noida, for their support and dedication to make the first ISM / Amity

Seminar a success.

Correspondence concerning this article should be addressed to Benjamin S.

Cheeks. Email: [email protected]

FINANCING AN INTERNET CAFÉ IN INDIA 2

Abstract

India has developed a sophisticated financial system in order to facilitate the

mobilization of savings within the economy. This system is characterized by a strong

legal and regulatory environment and a sophisticated network of financial markets,

financial intermediaries, and financial instruments working together to meet the

funding needs of businesses of all sizes. This paper presents a high-level overview of

this system and then reviews the network through the eyes of a retail start-up to

determine the most suitable sources and instruments for funding.

Keywords: Indian financial system, business financing

FINANCING AN INTERNET CAFÉ IN INDIA 3

Financing a Internet Café in India

This paper will look at the various funding options for a new business

enterprise in India. For illustrative purposes, a draft business proposal for an internet

café, Social Café, will be used.

The paper is divided into three sections. The first provides an overview of the

Indian financial system; including the types of financial regulators, the financial

markets, the common financial instruments available, and the main intermediaries of

these instruments. The second section will review the funding needs of Social Café.

The final section will review and recommend the most suitable instruments and

sources for funding.

The Indian Financial System

A financial system consists of an interconnecting network of markets,

institutions, and instruments through which the savings in the economy are mobilized

and effectively allocated among the ultimate borrowers and investors. Ensuring this

timely and adequate supply of capital is critical to promote industrial growth and

economic well-being of the country. Levine (2004) suggests that a well-developed

financial system can encourage economic growth through improved information on

firms and managers, intensity with which creditors monitor and exert corporate

governance, better management of risk, pooling of savings, and ease of exchange.

In recognition of this fact, India has created a well-developed financial system.

The International Monetary Fund (2013) stated that “India has made remarkable

progress toward developing a stable financial system. Since liberalization in the early

1990s, the system’s growth and increasing commercial orientation have been

FINANCING AN INTERNET CAFÉ IN INDIA 4

accompanied by steady improvements in the legal, regulatory, and supervisory

framework”.

India’s financial system consists of financial regulators, financial markets,

financial instruments, and financial intermediaries.

Financial Regulators

There are two primary regulatory bodies in the Indian financial system. These

are the Reserve Bank of India (RBI) and the Securities and Exchange Board of India

(SEBI). The RBI is the supreme monetary authority of the country. It is responsible

for formulating and implementing monetary policy, maintaining price stability and

ensuring adequate flow of capital. The RBI issues currency, serves as the banker to

the government, sets bank rates, reverse repurchase (repo) rates, the statutory liquidity

ratio, and the cash reserve ratio. The SEBI was established under the Securities and

Exchange Board of India Act, 1992. It is governed by the Capital Markets Division of

the Department of Economic Affairs, Ministry of Finance. SEBI has the authority to

regulate capital markets, check trading of securities, investigate malpractice in

securities markets, regulate stockbrokers and sub-brokers, promote investor interests,

and make rules and regulations for the securities market.

Generally speaking, government securities and bonds, instruments issued by

banks and financial institutions are regulated by the RBI while issues of non-

government securities (i.e. issues of corporations) are regulated by SEBI.

Financial Markets

The Indian financial markets are broadly categorized into the capital market,

the money market, and the foreign exchange (forex) market.

FINANCING AN INTERNET CAFÉ IN INDIA 5

The capital market is primarily involved in long-term funding. It has two

segments, the primary or new issue market and secondary or stock market. The

primary or new market deals with securities offered to investors for the first time.

The issuer sells the securities in this market to raise funds. The secondary or stock

market supports the buying and selling of previously issued securities. The secondary

market enables holders of security to adjust their holdings in response to charges in

their evaluation of the stock or to meet cash flow needs.

The money market is involved in short-term funding. It is the organized

exchange where participants can lend and borrow money for a period of one year or

less. Key submarkets within the money market are markets for commercial paper,

call money, and treasury bills.

The forex market assists with the exchange of foreign currency. As the forex

market is not a traditional market for business financing, it is beyond the scope of this

paper.

Financial Instruments

Kahn (2006) describes three broad categories of financial instruments: direct,

indirect, and derivatives. Direct instruments are those issued by non-financial

economic units such as corporations. Key types of direct instruments are equity

shares (both common and preferred), debentures such as bonds, and innovative debt

instruments such as convertible bonds and warrants. Indirect instruments are those

issued by financial economic units. Key types of indirect instruments include mutual

fund units, insurance policies, and bank deposits. The final category of financial

instruments is derivatives. Derivatives are products whose value is derived by that of

another asset. The key types of derivatives are forwards, futures, and options.

FINANCING AN INTERNET CAFÉ IN INDIA 6

Financial Intermediaries

The primary roles of financial intermediaries are to bring together buyers and

sellers of securities, and where necessary to repackage these securities to make them

more attractive. An example of the latter would be repackaging securities into smaller

units for individual investors. The key financial intermediaries in India are banks,

financial institutions, mutual funds and insurance funds, and non-banking financial

companies (NBFCs).

Banks. The primary providers of credit in India are the banks. The banking

sector in India is comprised of commercial banks and cooperative banks. The

commercial banks include 19 Nationalized Banks, the State Bank of India (SBI) and

its six associate banks, the Regional Rural Banks (RRBs), Foreign Banks, and other

Indian private sector banks. The cooperative banks are comprised of the State

Cooperative Banks and the Urban Cooperative Banks.

Financial institutions. Financial institutions were originated to drive public

economic development. At the time of their formation, the capital markets were

relatively underdeveloped. This sector has undergone changes in recent years when

two major financial institutions, ICICI and IDBI, converted into banks. Financial

institutions are broadly categorized into All-India financial institutions, State-Level

financial institutions, and Specialized Financial Institutions. Key All-India

institutions are Industrial Finance Corporation of India Ltd (IFCI Ltd), Small

Industries Development Bank of India (SIDBI), and Industrial Investment Bank of

India Ltd (IIBI). Generally speaking, All-India institutions invest in long and medium

term projects, while State-Level institutions invest in medium and small scale

projects. The list of specialized financial institutions in India includes: Export-Import

FINANCING AN INTERNET CAFÉ IN INDIA 7

Bank Of India, Export Credit Guarantee Corporation of India Ltd, Board for Industrial

& Financial Reconstruction, and National Housing Bank.

Mutual funds and insurance organizations. Mutual funds and insurance

organizations invest in a wide-cross section of securities and sell units to investors.

This allows investors to diversify their holdings without having to buy individual

securities. The primary difference between the two is that investments with insurance

organizations also serve as life insurance policies. Also, insurance organizations are

regulated by the Insurance Regulatory and Development Authority (IRDA).

NBFC. The Reserve Bank of India (2013) states that a NBFC is a company

whose “principal business is lending, investments in various types of shares / stocks /

bonds / debentures / securities, leasing, hire-purchase, insurance business, chit

business, and its principal business is receiving deposits under any scheme or

arrangement in one lump sum or in installments.” There are three key categories of

heterogeneous NBFCs. These are Asset Finance Companies (AFC), Investment

Companies (IC), Loan Companies (LC). A separate category of NBFCs call the

residuary non-banking companies (RNBCs). These include Infrastructure Finance

Companies (IFC), Stock Exchanges, and Venture Capital-Private Equity Funds.

Funding Needs of the Internet Café

The following business plan has been created for Social Café (Bplans.com,

2013). Social Café is the answer to ever increasing internet demand and the growing

coffee-drinking culture in India. It will provide a unique social environment for

young people in New Delhi to socialize with their friends, be entertained, and access

the internet at affordable prices.

FINANCING AN INTERNET CAFÉ IN INDIA 8

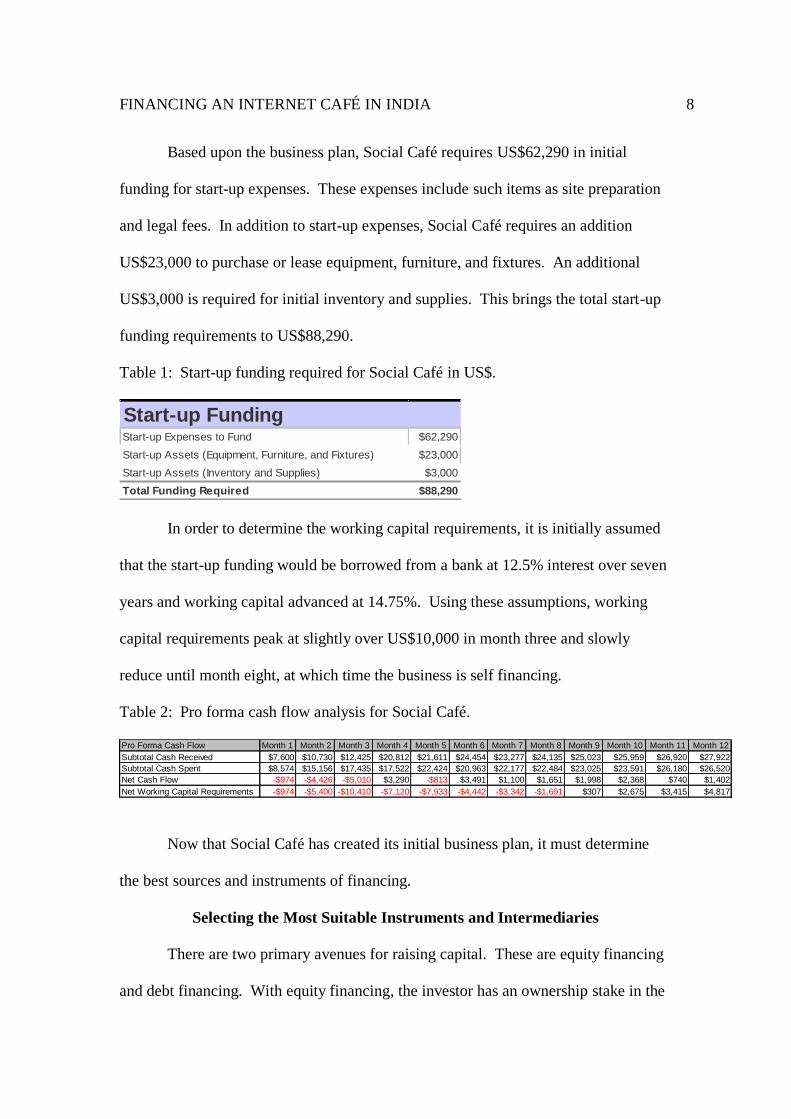

Based upon the business plan, Social Café requires US$62,290 in initial

funding for start-up expenses. These expenses include such items as site preparation

and legal fees. In addition to start-up expenses, Social Café requires an addition

US$23,000 to purchase or lease equipment, furniture, and fixtures. An additional

US$3,000 is required for initial inventory and supplies. This brings the total start-up

funding requirements to US$88,290.

Table 1: Start-up funding required for Social Café in US$.

Start-up Expenses to Fund $62,290

Start-up Assets (Equipment, Furniture, and Fixtures) $23,000

Start-up Assets (Inventory and Supplies) $3,000

Total Funding Required $88,290

Start-up Funding

In order to determine the working capital requirements, it is initially assumed

that the start-up funding would be borrowed from a bank at 12.5% interest over seven

years and working capital advanced at 14.75%. Using these assumptions, working

capital requirements peak at slightly over US$10,000 in month three and slowly

reduce until month eight, at which time the business is self financing.

Table 2: Pro forma cash flow analysis for Social Café.

Pro Forma Cash Flow Month 1 Month 2 Month 3 Month 4 Month 5 Month 6 Month 7 Month 8 Month 9 Month 10 Month 11 Month 12

Subtotal Cash Received $7,600 $10,730 $12,425 $20,812 $21,611 $24,454 $23,277 $24,135 $25,023 $25,959 $26,920 $27,922

Subtotal Cash Spent $8,574 $15,156 $17,435 $17,522 $22,424 $20,963 $22,177 $22,484 $23,025 $23,591 $26,180 $26,520

Net Cash Flow -$974 -$4,426 -$5,010 $3,290 -$813 $3,491 $1,100 $1,651 $1,998 $2,368 $740 $1,402

Net Working Capital Requirements -$974 -$5,400 -$10,410 -$7,120 -$7,933 -$4,442 -$3,342 -$1,691 $307 $2,675 $3,415 $4,817

Now that Social Café has created its initial business plan, it must determine

the best sources and instruments of financing.

Selecting the Most Suitable Instruments and Intermediaries

There are two primary avenues for raising capital. These are equity financing

and debt financing. With equity financing, the investor has an ownership stake in the

FINANCING AN INTERNET CAFÉ IN INDIA 9

business and therefore a claim on the future earnings of the firm. With debt financing,

the investor does not gain an ownership stake in the business, but will be repaid the

principal and interest at the agreed upon intervals. There are advantages and

disadvantages of each. With equity financing, the money does not have to be repaid,

so the risk falls more heavily on the investor. However, the more shareholders a

company has, the more claims on the earnings as well as involvement in key decisions

of the organization. With debt financing, companies must comply with repayment

schedules. This increases the amount of profit required to break-even. For this

example, we will assume that the owner of Social Café is open to equity financing to

some degree, but wants to retain a majority ownership stake in the business.

Equity Financing

Within the Indian financial system, there are three main intermediaries for

equity financing. The most basic is the personal savings-friends and family, the

second is venture capital-private equity funds (VC/PE), and the final is stock

exchanges.

Personal savings-friends and family. Personal savings, friends, and family

are key sources of funding for most start-up businesses. Many of the most successful

businesses in India today are family owned and managed. Some advantages of

funding from this source is the hopeful sharing of profits with friends and family as

well as having investors that are truly interested in your success. It is generally

timelier and involves less bureaucracy than dealing with professional investors. The

key disadvantages are family squabbles and meddling from family members. These

can be overcome by clarifying roles and responsibilities in the beginning. Another

key consideration is that funding from personal savings will be a prerequisite from

FINANCING AN INTERNET CAFÉ IN INDIA 10

future investors. Many require the owner provide at least 10% of the initial funding.

VC/PE. For a business of this size, the second key source of equity financing

is venture capital-private equity funds (VC/PE). Primarily due to the presence of

high-information technology skills, India has a robust VC/PE industry. According to

Venture Intelligence (2011), India had the fourth largest VC/PE penetration as a

percentage of GDP behind only Israel, the United States, and the United Kingdom.

Venture Intelligence (2012) divides the VC/PE community in India into five

categories based upon the level of investment and the timing of the investment. These

are Incubators, Angel Networks, Seed Level Funds, Early Stage Funds, Growth Stage

Funds, and SME Focused. Based upon the funding requirements of Social Café, the

Angel Networks would be the category of VC/PE to focus. Angel Investors tend to be

high net-worth individuals or groups of the same that invest in early stages of

businesses for an equity stake. In additional to the generic advantages and

disadvantages are equity investments by VC/PE funds, there are advantages and

disadvantages specific to this type of funding. The key advantage when accepting

capital from VC/PE funds is that they tend to invest in industries where they have

experience. This creates great opportunities for mentoring and network building. A

key disadvantage is the VC/PE fund often look to take a large equity position and

push for active involvement in decision making. Before reaching out to the VC/PE

community, the entrepreneur must first consider the likelihood of this type of

investment. Venture Intelligence (2011) reports that only 3% of VC/PE investments

in 2011 were in the food and beverage industries. VC/PE firms tend towards

industries with high-growth potential and low capital requirements. For 2011, the

bulk of the venture funds flowed towards IT, ecommerce, Mobile VAS, education,

FINANCING AN INTERNET CAFÉ IN INDIA 11

and health care. Therefore, while VC/PE investments offer a great potential, it is an

unlikely source of funding for an internet café. Therefore, it is advisable for the

entrepreneur to focus on more accessible sources of funding.

Stock exchanges. The final source of equity funds are the stock exchanges.

India currently has 25 stock exchanges with the key exchanges being the Bombay

Stock Exchange (now just BSE) and the National Stock Exchange (NSE). According

to the World Confederation of Exchanges (2013), as of January 2013, the BSE listed

more than 5,195 companies (number one in the world) with a total market

capitalization of US$1.32 trillion. The same report showed the NSE had 1,664

listings with US$1.29 trillion of market capitalization. Many of India’s major

companies are listed on both exchanges.

Trading on both exchanges are done by computer. There are no market

makers or specialists floor traders. Currently orders must be placed on each exchange

by a broker, but many of these brokers provide trading facilities to their customers.

The two main indices are the Sensex and the S&P CNX Nifty. The Sensex includes

30 firms listed on BSE. The Nifty includes 50 shares listed on the NSE.

These two exchanges are not appropriate for Social Café for two primary

reasons. First, they cater to companies much larger than Social Café and equity

funding through these types of exchanges tend to occur once a business has

established themselves as private companies and are looking for funds to expand.

Most of the stock exchanges in India require at least a three-year track record before

listing. The stock exchange that offers the most promise for a company such as Social

Café would be the OTC Exchange of India (OTCEI). According to their website, the

OTCEI (2013) “was set up to aid enterprising promoters in raising finance for new

FINANCING AN INTERNET CAFÉ IN INDIA 12

projects in a cost effective manner and to provide investors with a transparent &

efficient mode of trading”. However, despite this encouraging mission, it is not

recommended that Social Café attempt an offering on the OTCEI. For a company

without a track record, investors on the OTCEI would have similar hesitations as

would the VC/PE community in investing. Also, the costs associated with listing

could easily exceed the initial funding requirements. Once again, the entrepreneur’s

time would be better spent looking for alternative sources of funding.

To conclude the section of equity financing, there are many advantages that

equity financing can provide to a business. However, with the exception of friends

and family, early stage equity investment is difficult to come by unless your business

is a high-growth business with small capital investment. This is not just true in India,

but around the world. Nonetheless, the Indian financial system offers extensive

intermediary and instruments for those companies that fit the right profile.

Debt Financing

Other than equity financing, the other alternative is debt financing. The

primary instruments of debt financing in India are loans. However, the Indian

financial system ensures a full range of debt financing vehicles. In addition to loans,

some of the more common debt financing instruments are bonds, commercial paper

(CP), and leases.

Commercial paper. Commercial paper can be eliminated immediately as a

source of funding for Social Café. The Reserve Bank of India (2011) defines

commercial paper as an unsecured money-market instrument issued in the form of a

promissory note. In India, commercial paper can be issued by corporates and All-

India Financial Institutions. They are a great alternative to working capital loans to

FINANCING AN INTERNET CAFÉ IN INDIA 13

secure short-term cash flow needs. CP can be issued with maturities between seven

days and one year and can be denominated in Rs. 5 lakh or multiples there of. Social

Café could not issue CP for several reasons, but most notably it does not meet the

minimum credit rating of A-2 and does not have an audited net worth of Rs. 4 crore.

Corporate bonds. In India, the term corporate bond and debenture are used

interchangeably. As per Security and Exchange Board of India (2009) a corporate

bond is a “debt instruments issued by a corporation, the holder of which receives

interest from the corporation periodically for a fixed period of time and gets back the

principal along with the interest due at the end of the maturity period.” In India,

public and private companies can issue corporate bonds. However, a company

incorporated outside India cannot issue corporate bonds in India.

Corporate-bond funding in India makes up a very small percentage of

corporate funding needs in India. An article in the Financial Times Chilkoti (2013),

reports that in 2010-11, corporate bonds made up 4% of funding needs whereas in

China it made up 17%. One problem holding back the corporate bond market is the

lack of liquidity. In India corporate bonds are sold over-the-counter (OTC) rather

than through an organized market. Therefore, due to the limitations of the bond

market, this type of debt financing would not be appropriate for Social Café.

Leases. There are a variety of NBFCs that specialize in the leasing of

equipment or financing of such an activity. A lease is defined as a contract between

two parties for the hire of an asset where the lessor retains ownership of the asset

while the lessee has possession and use of the asset and pays specified rentals over a

period of time. The most common type of leases are short-term and long-term leases.

Short-term leases are usually two to three years for assets such as computers that have

FINANCING AN INTERNET CAFÉ IN INDIA 14

high depreciation. Long-term leases are for assets with lower depreciation such as

machinery, cars, and furniture. Leases offer a number of advantages over loans. For

example, many leasing companies will finance 100% of the capital required for the

equipment; including administrative fees. Social Café should consider lease financing

as a funding option; especially for its computers as well as its furniture and fixtures.

Based upon the initial business plan, this amount was estimated at US$23,000 in

furniture and fixtures.

Loans. The primary source of loans in India are banks. However, loans can be

obtained from financial institutions and an NBFC such as loan companies. Many

banks and financial institutions have created loan schemes designed to meet the

funding needs of businesses. In addition, there are many loans in India backed by

government funding and schemes. Many of these schemes were designed specifically

with the small to medium-size business in mind. The advantages of these loan

schemes are that they can provide loans to businesses without previous credit and/or

provide interest-rate subsidies. For companies such as Social Café, the Credit

Guarantee fund Trust for Micro and Small Enterprises (CGTMSE) is the trust behind

the Credit Guarantee Scheme (CSG). The objective of this scheme is to make

available bank credit without collateral or third party guarantees. There are currently

131 banks that are eligible to extend loans backed by the CSG.

Summary and Recommendation

Based upon the review of funding sources and types, Social Café should look

to personal savings-friends and family for initial equity investment. For debt

financing, Social Café should consider financing their computers with short-term

leases and its equipment, furniture, and fixtures with a leasing company. Naturally,

FINANCING AN INTERNET CAFÉ IN INDIA 15

this recommendation is dependent upon a lease versus buy comparison. For the

additional financing needs for start-up expenses and working capital, Social Café

should look at loan packages from banks and financial institutions; particularly those

loans backed by one of the government schemes, such as the CSG, designed to

support small to medium-size businesses.

Limitations of Analysis

This paper analysed the formal financial system in India. India has an

extensive informal network consisting of money lenders, funding clubs, chit funds,

and landlords. Due to the fragmentation of this market, it was considered beyond the

scope of this paper.

Also, this paper focused on more traditional sources of funding.

Intermediaries in India also support derivatives and other innovative instruments.

However these instruments are thinly traded and not appropriate for Social Café and

therefore considered out of scope.

Conclusion

Ensuring a timely and adequate supply of capital is critical to promote

industrial growth and economic well-being of the country. To this end, India has

developed a sophisticated network of financial markets, intermediaries, and

instruments, supported by a strong legal and regulatory environment. This paper has

presented a high-level overview of this system. It then reviewed this system through

the eyes of Social Café to determine the most suitable sources and instruments for

funding. The recommendation was for Social Café to tap into personal savings-

friends and family of the owner for initial equity funding. This is the most common

source of seed capital for a new enterprise and is usually a prerequisite for subsequent

FINANCING AN INTERNET CAFÉ IN INDIA 16

funding. To fund the remaining shortfall, Social Café should investigate lease

financing for its computers, equipment, furniture, and fixtures from one of India’s

NFBC leasing companies. For the funding of the remaining expenses and working

capital, Social Café should pursue a SME Loan Pack, especially one supported by

government schemes, from one of India’s many banks or financial institutions.

FINANCING AN INTERNET CAFÉ IN INDIA 17

References

Bose, Suchismita. 2005. “Securities Markets Regulation: Lessons from US and Indian

Experience”, Money and Finance, Jan-June, 83-124.

Bplans.com. (2013). Internet Cafe Sample Business Plan. Retrieved June 15, 2013,

from

http://www.bplans.com/internet_cafe_business_plan/executive_summary_fc.php

#.UcrurDvUmSo

BSE. (2013). BSE-Introduction. Retrieved June 20, 2013, from

http://www.bseindia.com/static/about/introduction.aspx?expandable=0

Business Portal of India. (n.d.). Business Portal of India : Business Financing :

Banks. Retrieved June 15, 2013, from

http://business.gov.in/business_financing/banks.php

Chilkoti, A. (2013, February 5). India: corporate bond market held back by

bureaucratic red tape. Financial Times. Retrieved from

http://blogs.ft.com/beyond-brics/2013/02/05/india-corporate-bond-market-held-

back-by-bureaucratic-red-tape/?#axzz2XMdlvE6R

Embassy of India. (n.d.). Embassy of India - Washington DC (official website) United

States of America - Financial System in India. Retrieved June 13, 2013, from

https://www.indianembassy.org/financial-system-in-india.php

International Monetary Fund. (2013). India: Financial system stability assessment

update. (13/8). Washington, D.C: International Monetary Fund.

Kahn, M. Y. (2006). Indian Financial System (5th ed.). New Delhi, India: Tata

McGraw-Hill Education.

FINANCING AN INTERNET CAFÉ IN INDIA 18

Levine, R. (2004). Finance and growth: theory and evidence. Handbook of economic

growth, 1, 865-934.

Ministry of Finance - Government of India. (n.d.). Acts and Rules Governed by the

Capital Markets Division: Ministry of Finance, Government of India. Retrieved

June 23, 2013, from

http://finmin.nic.in/the_ministry/dept_eco_affairs/capital_market_div/Acts%20a

nd%20Rules.asp

Reserve Bank of India. (2011, October 5). FAQs - Commercial Paper. Retrieved from

http://www.rbi.org.in/scripts/FAQView.aspx?Id=25

Reserve Bank of India. (2013, June 3). All you wanted to know about NBFCs.

Retrieved June 20, 2013, from

http://www.rbi.org.in/scripts/FAQView.aspx?Id=92

Reserve Bank of India (n.d.). Reserve Bank of India. Retrieved June 15, 2013, from

http://rbi.org.in/scripts/AboutusDisplay.aspx#MF

Securities and Exchange Board of India (2009). Investor guide for corporate bonds

market. Retrieved from

http://investor.sebi.gov.in/Reference%20Material/corporatebonds.pdf

Venture Intelligence (2011). Private Equity & Venture Capital in India: The

Changing Landscape. Retrieved from

http://chennai.tie.org/sites/default/files/chennai/article/image/funding-landscape-

india.pdf

Venture Intelligence (2012). Handbook on Venture Capital - An Entrepreneur's guide

to Early Stage Funding. Retrieved from http://www.ventureintelligence.in/vc-

handbook-2012.pdf

FINANCING AN INTERNET CAFÉ IN INDIA 19

World Federation of Exchanges. (2013, January). Statistics. Retrieved June 15, 2013,

from http://www.world-exchanges.org/statistics