Embed Size (px)

Citation preview

Business Unit

Economics

Why go into a business?

• In economics, we assume the profit motive. People generally go into business to make a profit.

• There are additional reasons, including social activism, but for now we are focused on the profit motive.

Types of Businesses

Proprietorship Partnership Corporation Franchise

Ownership and Control

1 owner (full control)

2 or more owners (Shared Control)

Many owners and owners can have limited control

Central company plus multiplefranchise owners

Formation and paper work required

Easy, less paperwork

Relatively Easy, some paperwork

Difficult, a lot of paperwork

Built-in reputation and structure, some paper work

Resources Limited access More access Better accessthrough shared sales

Franchises independently owned

Oversight Virtually none Some Lots of oversight,double taxation

High fees and strict rules

Liability 100% unlimited personal liability

100% unlimited liability

Limited personal liability

Can either be corporate or not

Why Create a Corporation?

• Corporations are harder to manage, have more government regulations and reporting requirements and are costly to start-up.

• So why create a corporation?

– To raise capital for expanding or improving the company

– To limit liability

In business, costs matter

• Businesses must manage themselves well in order to make a profit. One of the primary ways they do this is to manage their costs.

• Costs are what a business needs to spend in order to acquire what they need to run the business.

• The lower the costs relative to your revenue, the greater the profit you earn. You gain revenue through sales.

• Remember that businesses are started primary to make profit.

Understanding your supply curve

• You, as a business owner, need to think about when you will enter the market.

• That is, at what price will you begin to sell your goods and services?

• Why? Because if it costs you too much to produce it, and you were to sell it at too low a price, you will lose money.

• We all want to sell at a high price, but if it is too high, customers will go in search of a lower priced alternative.

Production Costs

• The amount paid by the

Producer/Supplier to make products,

bring them to the market and sell them

to buyers.

• Production costs include the acquiring of

raw materials, hiring workers and

purchasing of equipment and tools (the

factors of production).

• It also includes things like marketing,

distribution, management costs, etc.

Total Costs

• Total Costs = Fixed Costs + Variable Costs

Fixed Costs

• Costs that do not change as a result of a change in the quantity produced.

• If you produce one or a million units, you still pay the same fixed costs.

• Fixed costs can change, but not as a result of an increase or decrease in production, it changes as a result of the some outside reason.

– Your landlord increases your rent so he can pay his bills is an example of how fixed costs can be raised, but not as a result of how well your business is doing.

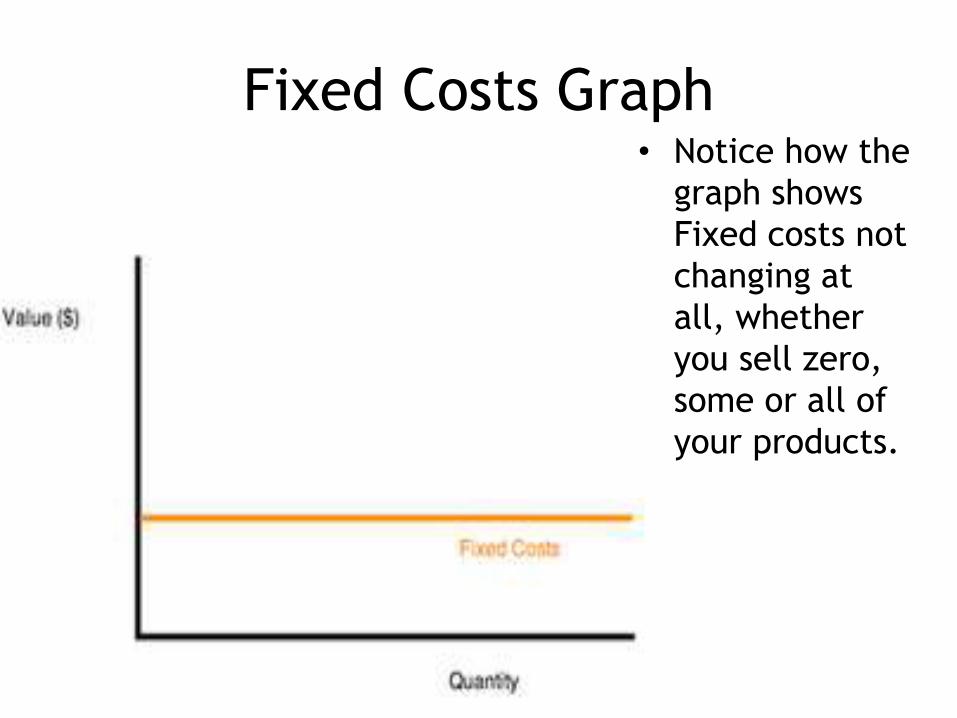

Fixed Costs Graph• Notice how the

graph shows

Fixed costs not

changing at

all, whether

you sell zero,

some or all of

your products.

“Sunk” Costs

• Another way to think about this is these costs are

usually paid up front and are “sunk”.

• You don’t actually sell these things but they do

help you sell what you are producing.

• For example: the land your business sits on is a

fixed cost. You aren’t going to sell the land to

any one, but you certainly need to place your

business there to help you sell your product.

Variable Costs

• Costs that do change as a result of a change in

production.

• As you sell more, your variable costs increase.

• As you sell less, your variable costs decrease.

• Variable costs can change for other reasons as well,

say for example the coffee crop was decimated by

a hurricane, this will cause those costs to rise,

regardless of how many cups of coffee you sell.

Variable Costs Graph • Notice

how the

costs rise

as the

number of

products

you sell,

and

therefore

need to

replace,

increases

as well.

Variable Costs = Sales costs

• Variable costs are directly related to what

you sell.

• Variable costs are proportional to the amount

of business you do. The more sales, the more

costs and vice versa.

• Variable costs can also be thought of as total

marginal costs. (Add up all of the increments

together)

So,

• Total Costs = Fixed Costs + Variable Costs

• TC=FC+VC

• Understanding total costs are important since

you need to know how much money you need to

spend to keep your business going.

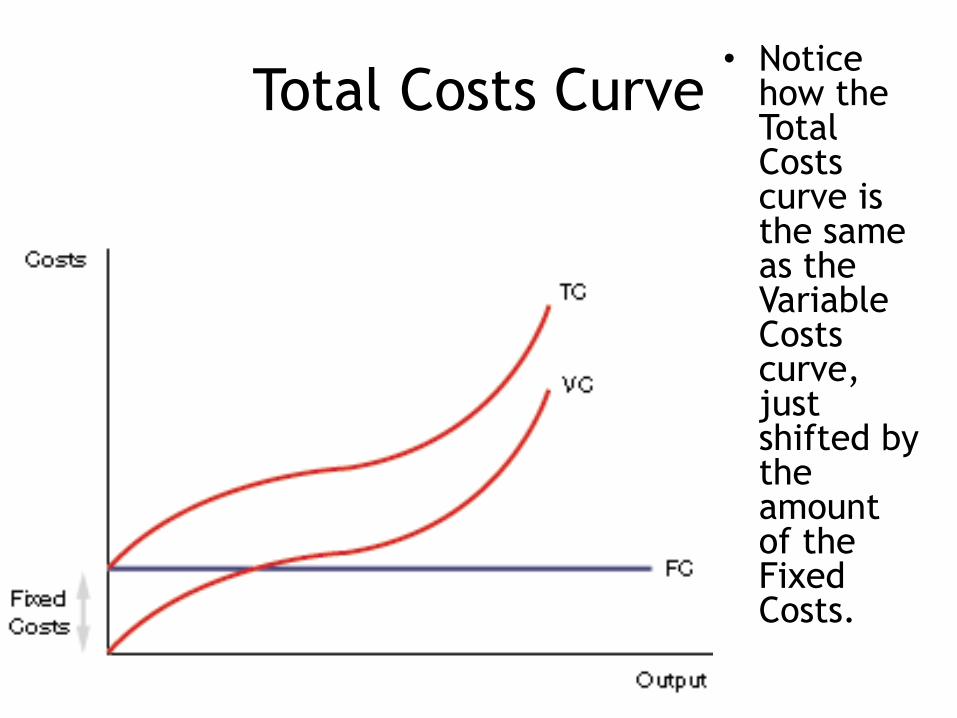

Total Costs Curve• Notice

how the Total Costs curve is the same as the Variable Costs curve, just shifted by the amount of the Fixed Costs.

In Summary:

• Fixed Costs are Overhead or Sunk

Costs

• Variable Costs are Sales Costs or

the cost of replaceables

High Variable Cost Businesses

• High Variable Cost businesses mean that you typically have a lot of products being sold and you need to replace those often.

• Examples include department stores, restaurants, and businesses that fill niche markets.

• The problem with these businesses is that you have to be good at knowing what your customers want and being able to manage inventory and costs well.

• The advantage is that these businesses are easier to start and are less risky.

High Fixed-Cost Businesses

• A high fixed-cost business is one that is difficult to get started given the high start-up costs, but can be great in the long run as you have little to worry about with regards to variable costs.

• Examples include parking lots, utility companies, recycling centers and some online companies.

• However, high fixed cost businesses are very risky because if the business isn’t successful, you stand to lose more money.

• A company called WebVan, which delivered groceries from online ordering, spent too much money on infrastructure and never generated enough sales to pay off those fixed costs.

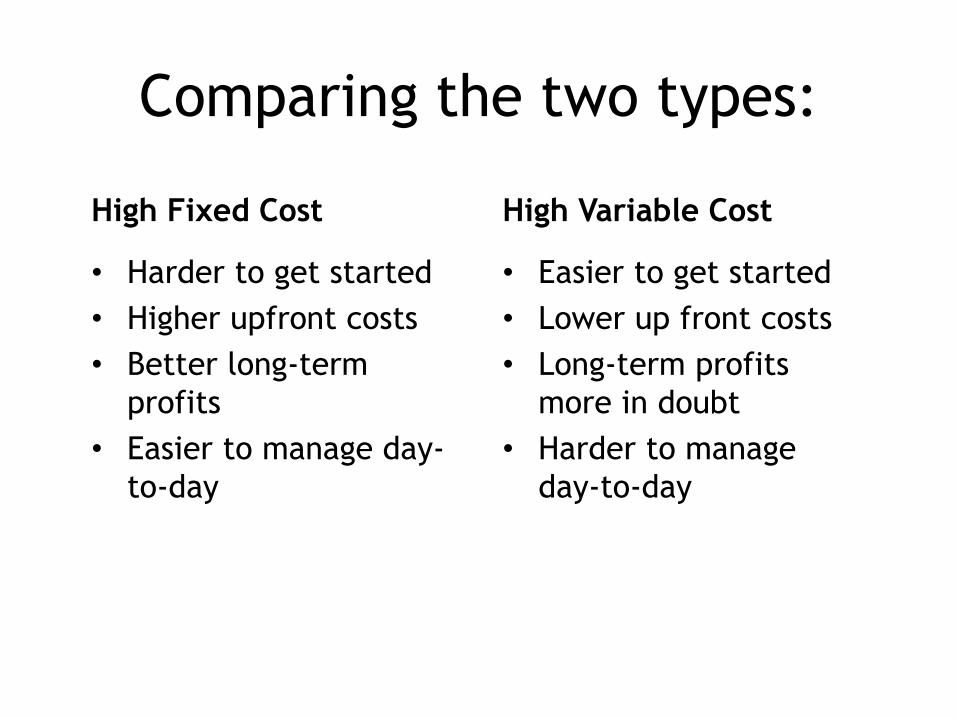

Comparing the two types:

High Fixed Cost

• Harder to get started

• Higher upfront costs

• Better long-term

profits

• Easier to manage day-

to-day

High Variable Cost

• Easier to get started

• Lower up front costs

• Long-term profits

more in doubt

• Harder to manage

day-to-day

Not all businesses are high fixed or variable

costs, some are more balanced between fixed

and variable costs.

Revenue

• Revenue is the money earned from the sale of

your products.

• Revenue is equal to Price times Quantity sold.

• R = P x Q

• This is why revenue is 0 when the price is too

low (at 0$) and too high (where no one wants

buy).

Revenue Curve• Remember

that at a certain point, your prices become to high and therefore fewer people will buy, leading to less revenue.

Selling equal revenue

• So, typically the more you sell (Q) the more money you make.

• The money you make is called revenue.

• The more revenue you have, the more likely you are to be successful in business.

Revenue does not always equal profit

• High revenue can still lead to economic losses if your production costs are too high.

• So the key isn’t just high revenues . . .

• It is also low costs!

• Low costs plus high revenues lead to economic profits.

Economics of Scale

• Economics of Scale means that you are more efficient because of large size. – Mass production = more efficient because the

way/method of production is faster and cheaper per item.

– Scaled companies are able to utilize Quantity to lower costs and increase their profits

– However, often Quality is sacrificed in the process

• The large size creates a form of protection known as “Barrier to Entry” which is that the costs to scale up to a large company is often so prohibitive that it limits the number of businesses able to do so. – Risky, and high up-front costs involved in scaling

Diseconomies of Scale

• The Opposite of Economies of Scale: where firms see increasing costs per unit as a result of increasing size.

• Typically things like mismanagement, maintenance issues, etc, create increasing costs.

Diminishing returns

• Too many cooks in the kitchen spoil the soup . . .

• It is the decrease in the marginal output as the amount of a single factor of production is increased, while others remain the same.