Embed Size (px)

Citation preview

MILP Formulationsfor Stochastic Dominance

JamesLuedtkeNew Formulations for Optimization Under Stochastic Dominance ConstraintsSIAM Journal on Optimization, 2008

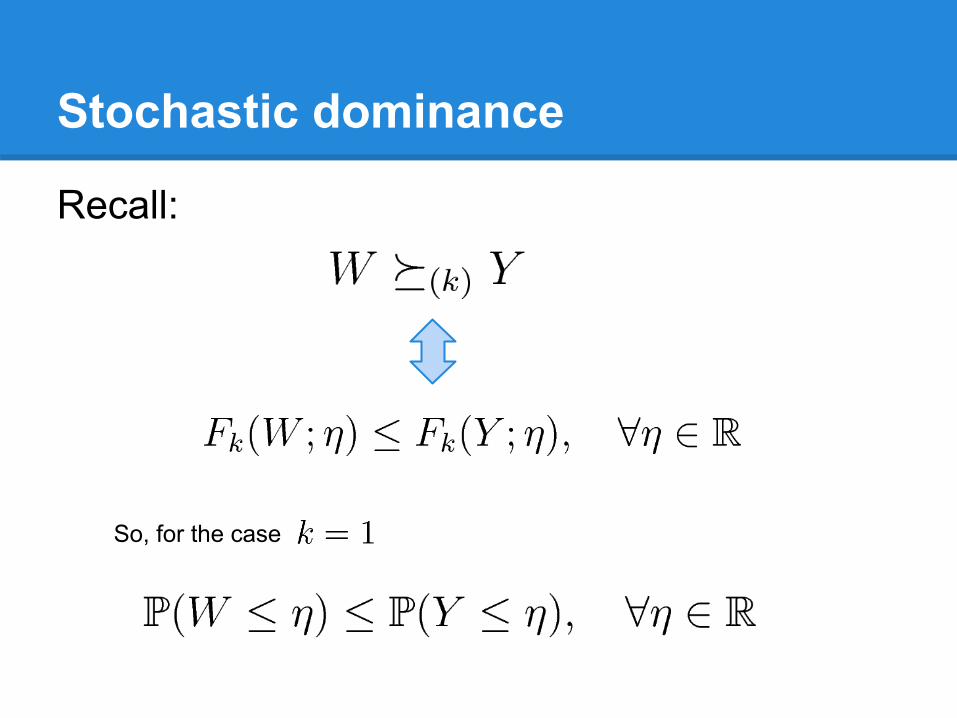

Stochastic dominance

Recall:

So, for the case

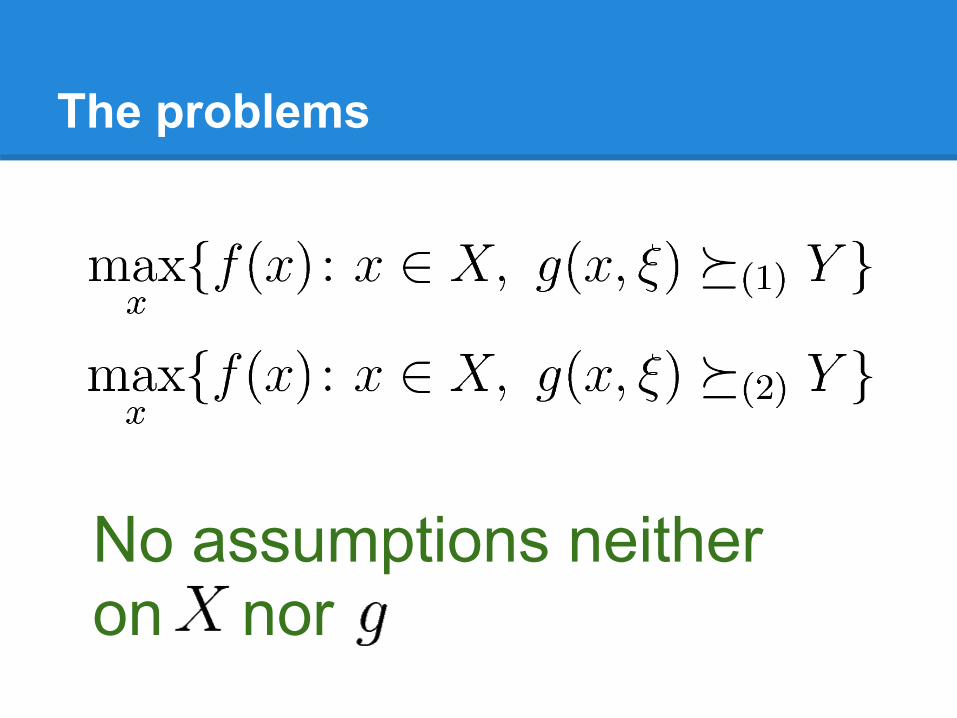

The problems

No assumptions neitheron X nor g

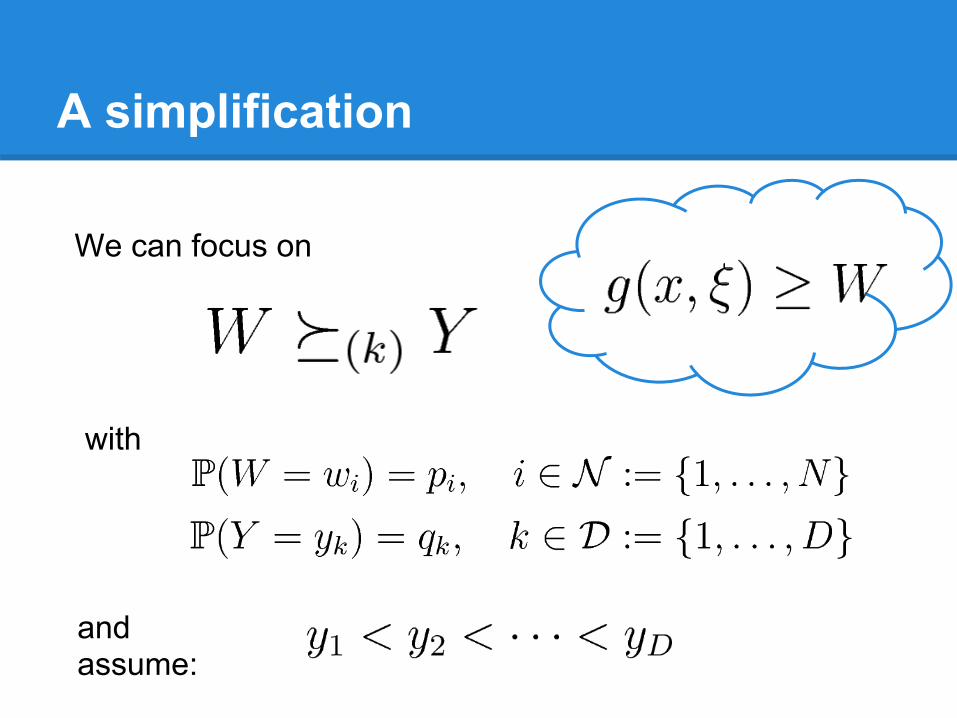

A simplification

We can focus on

with

and assume:

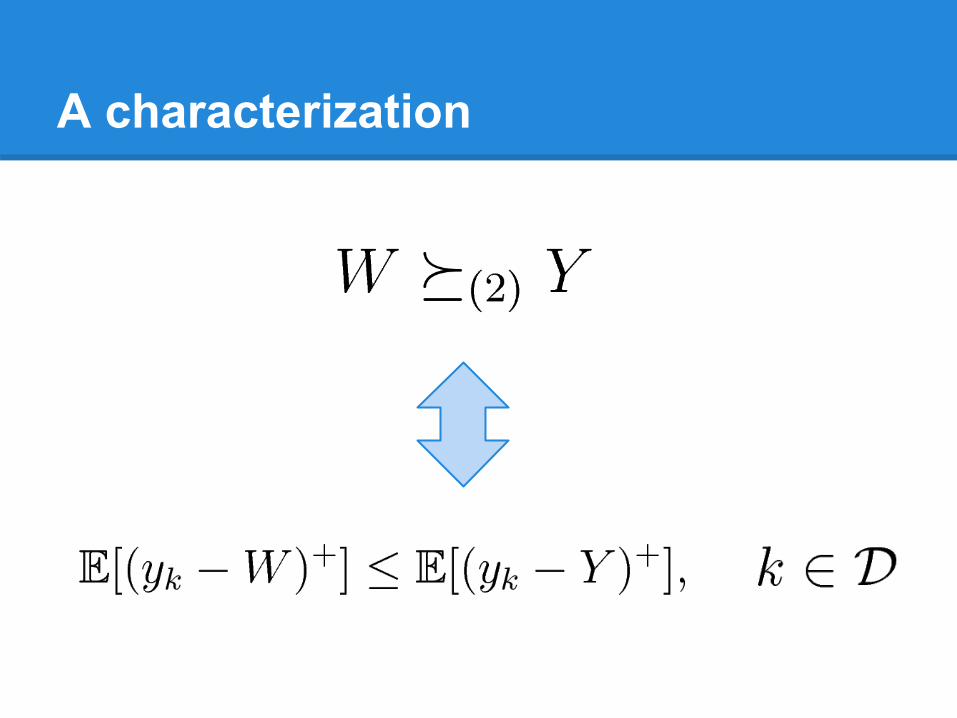

Second-order stochastic dominance

Image: http://www.flickr.com/photos/admiriam/

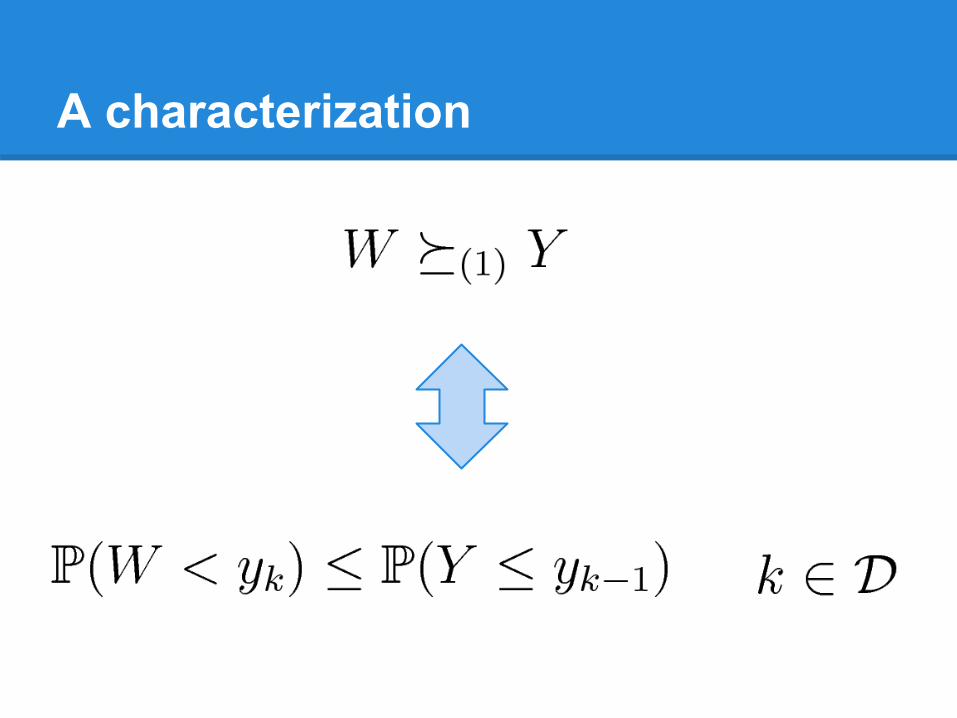

A characterization

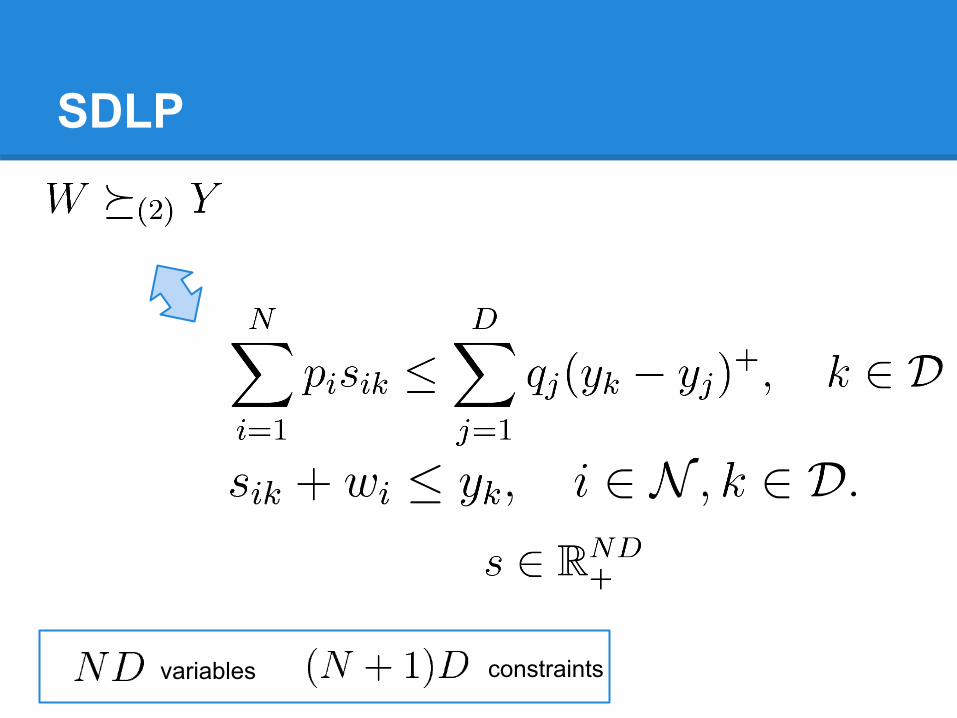

SDLP

constraintsvariables

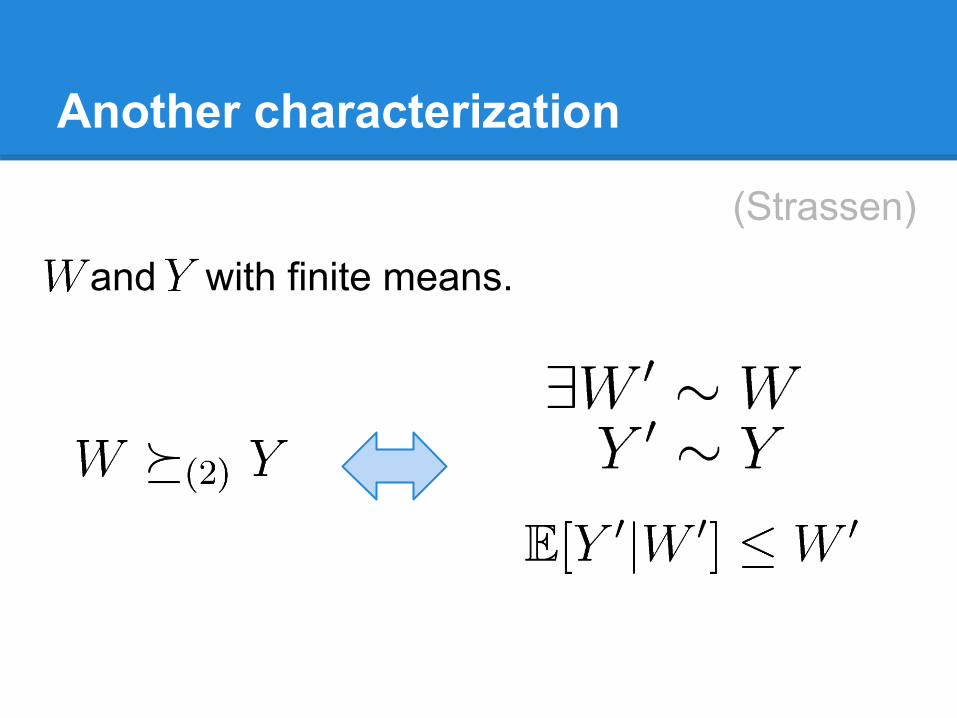

Another characterization

and Y with finite means.

(Strassen)

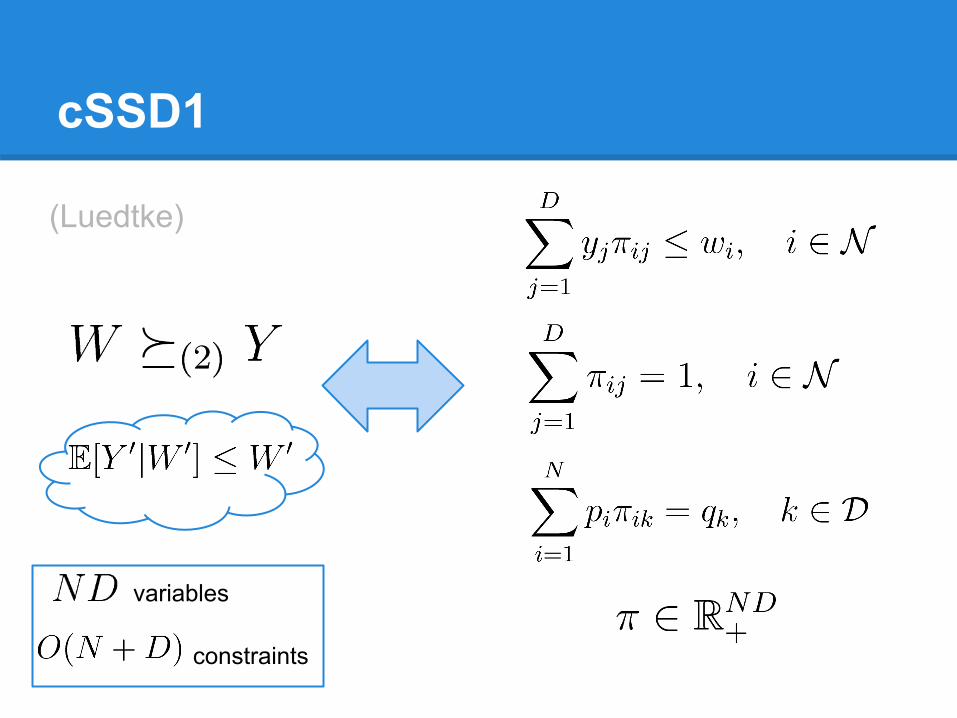

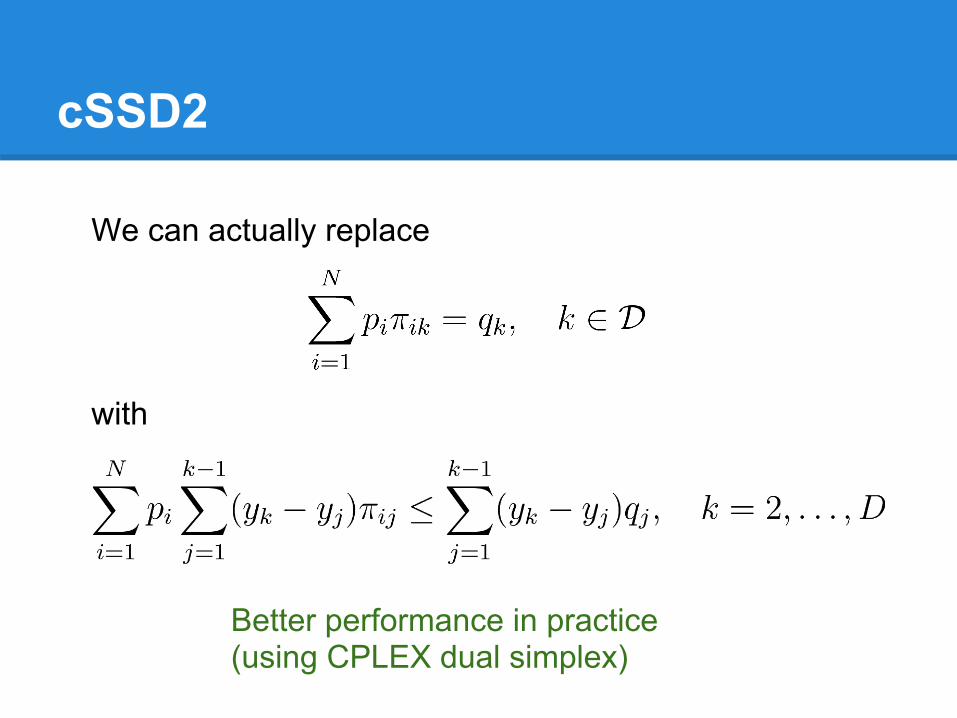

cSSD1

variables

constraints

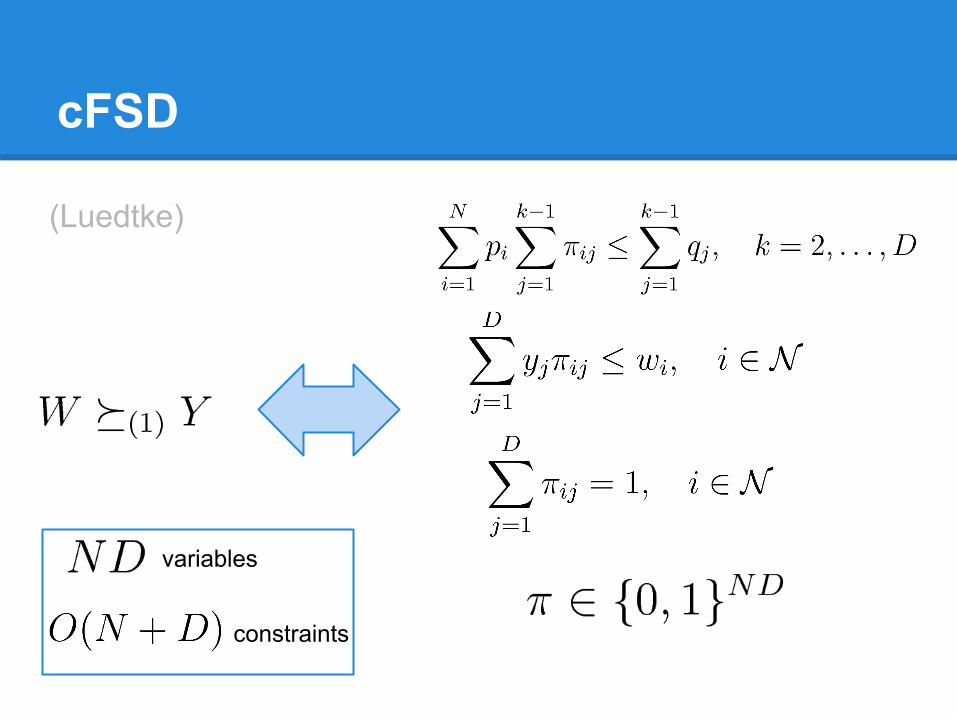

(Luedtke)

cSSD2

We can actually replace with

Better performance in practice(using CPLEX dual simplex)

First-order stochastic dominance

Image: http://www.flickr.com/photos/kome8/

A characterization

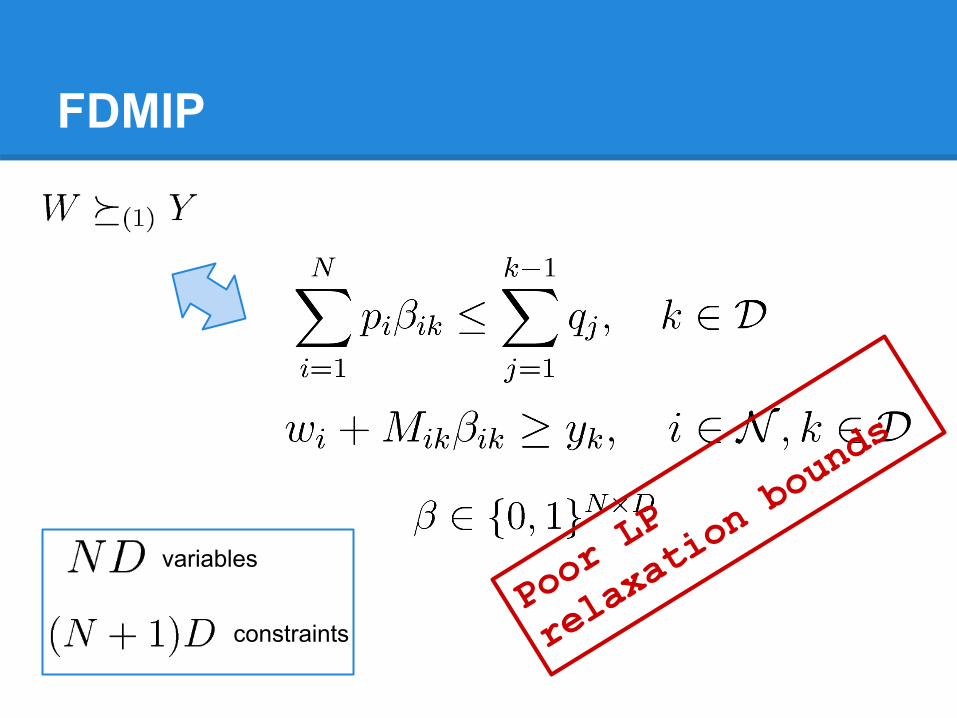

FDMIP

variables

constraintsPoor LP

relaxation bounds

cFSD

variables

constraints

(Luedtke)

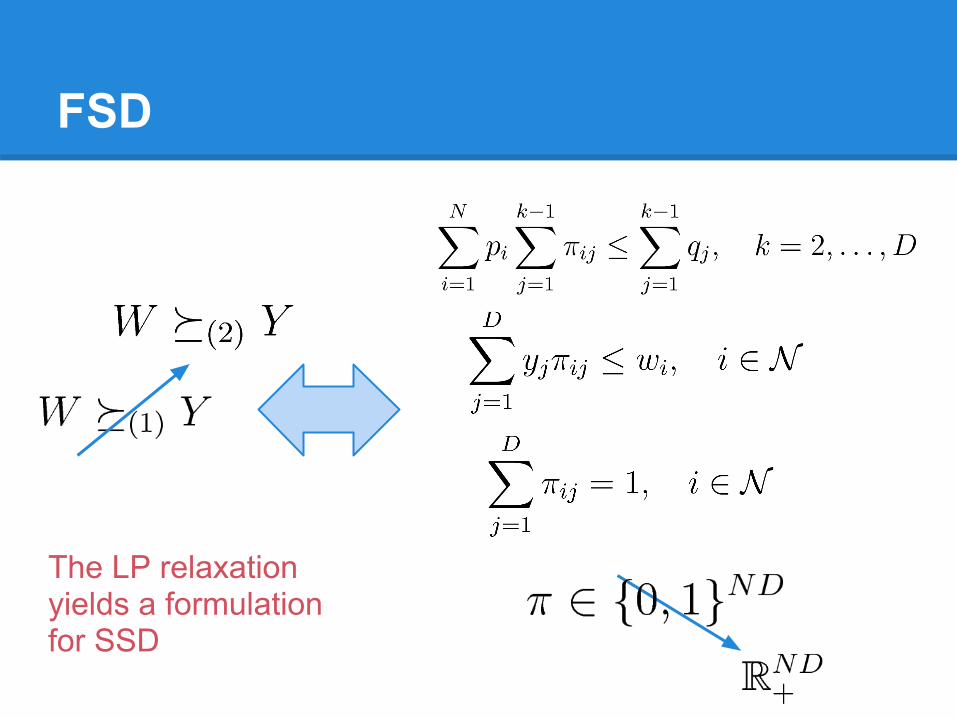

FSD

The LP relaxationyields a formulationfor SSD

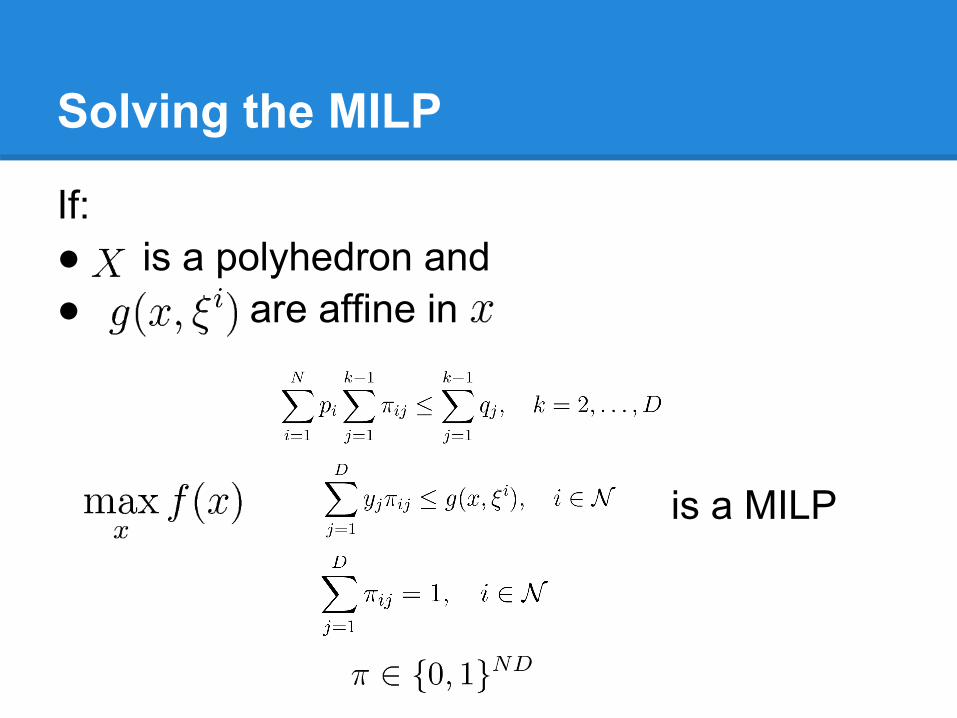

Solving the MILP

If: ● X is a polyhedron and ● g(x, \xi^iare affine in x

is a MILP

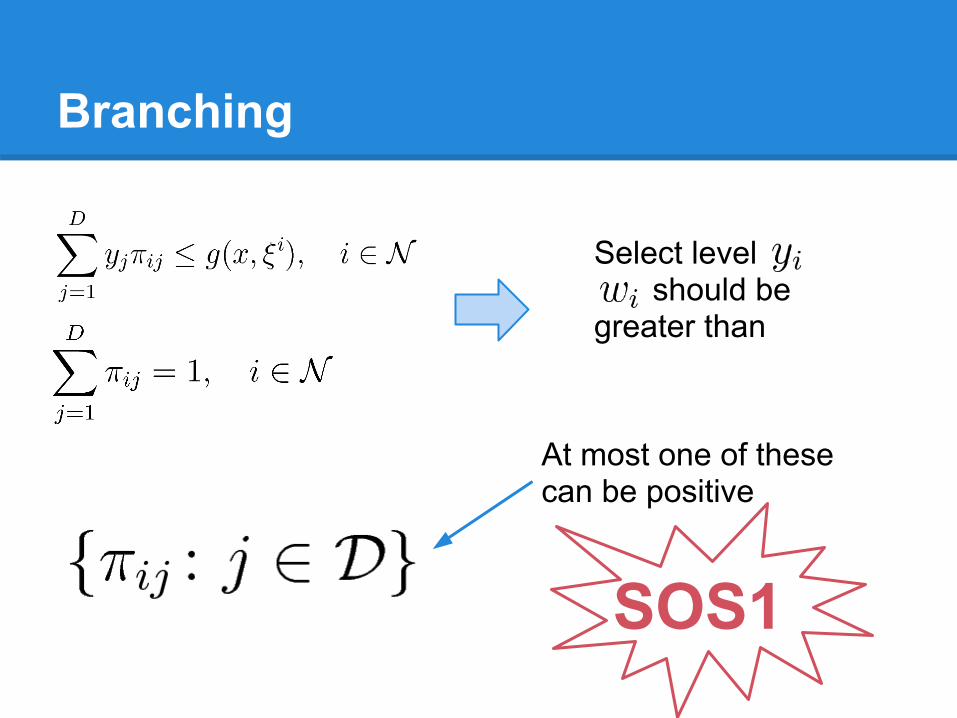

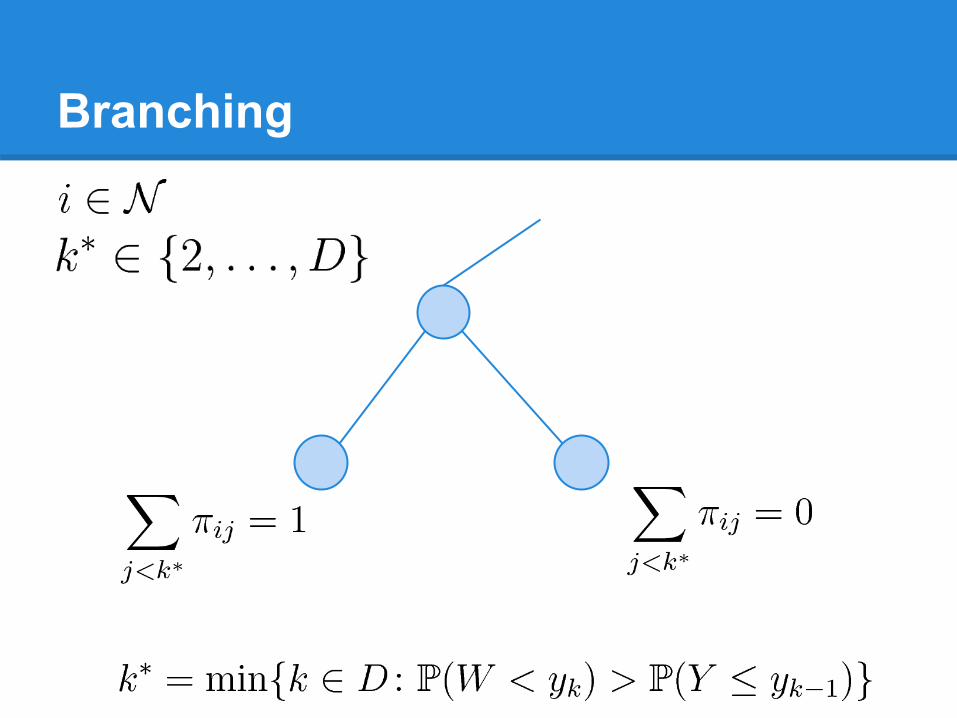

Branching

Select levelyi should begreater than

At most one of thesecan be positive

SOS1

Branching

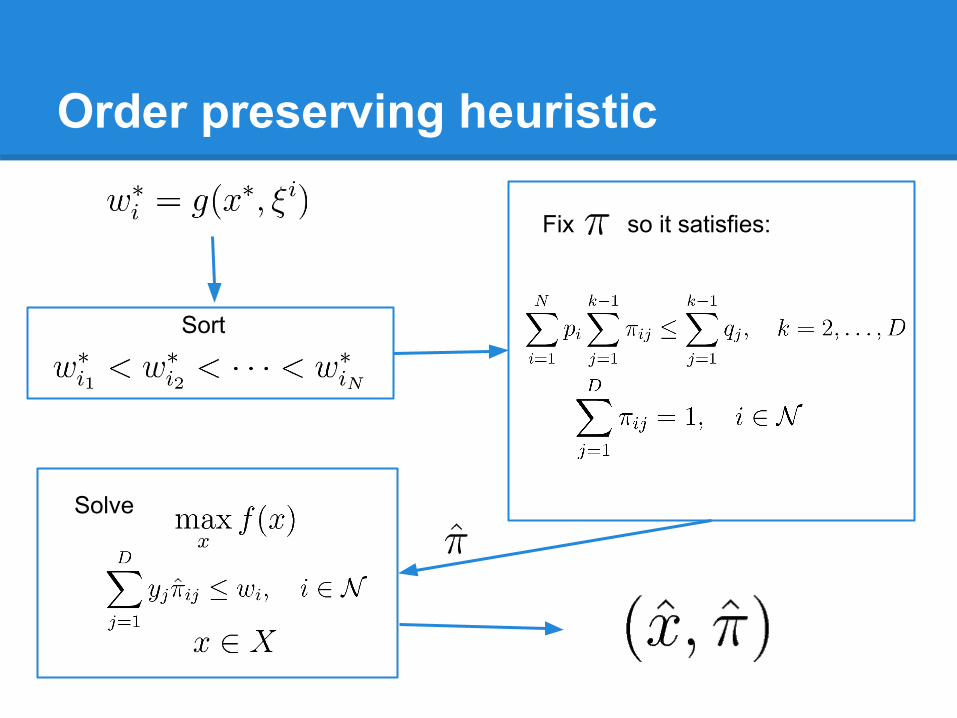

Order preserving heuristic

Sort

Fix so it satisfies:

Solve

Computational results

Image: http://www.flickr.com/photos/piper/

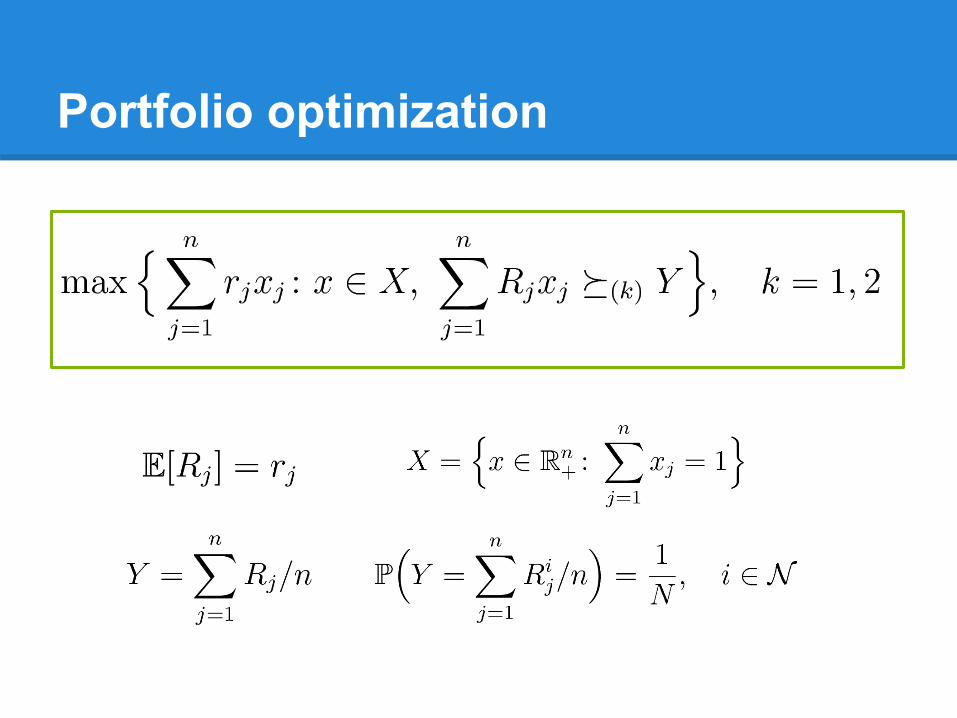

Portfolio optimization

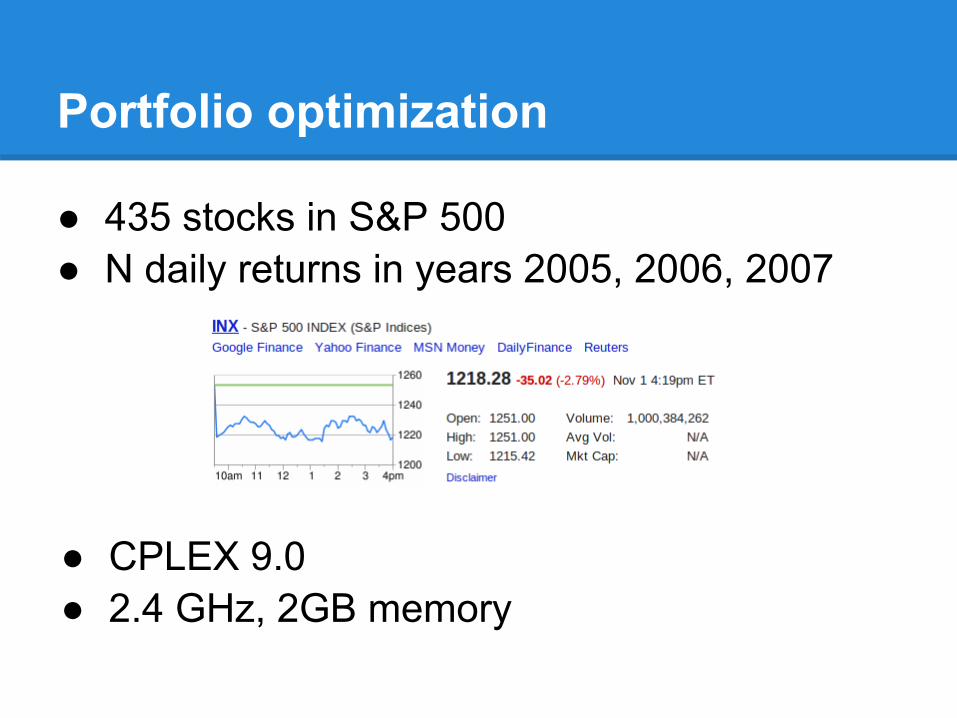

Portfolio optimization

● 435 stocks in S&P 500● N daily returns in years 2005, 2006, 2007

● CPLEX 9.0● 2.4 GHz, 2GB memory

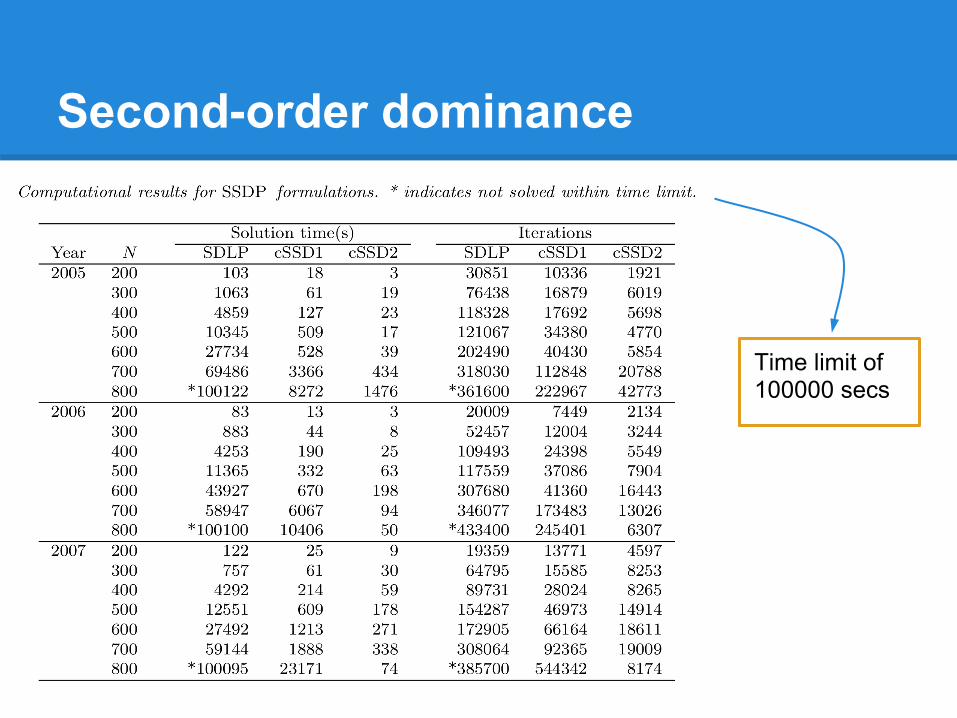

Second-order dominance

Time limit of100000 secs

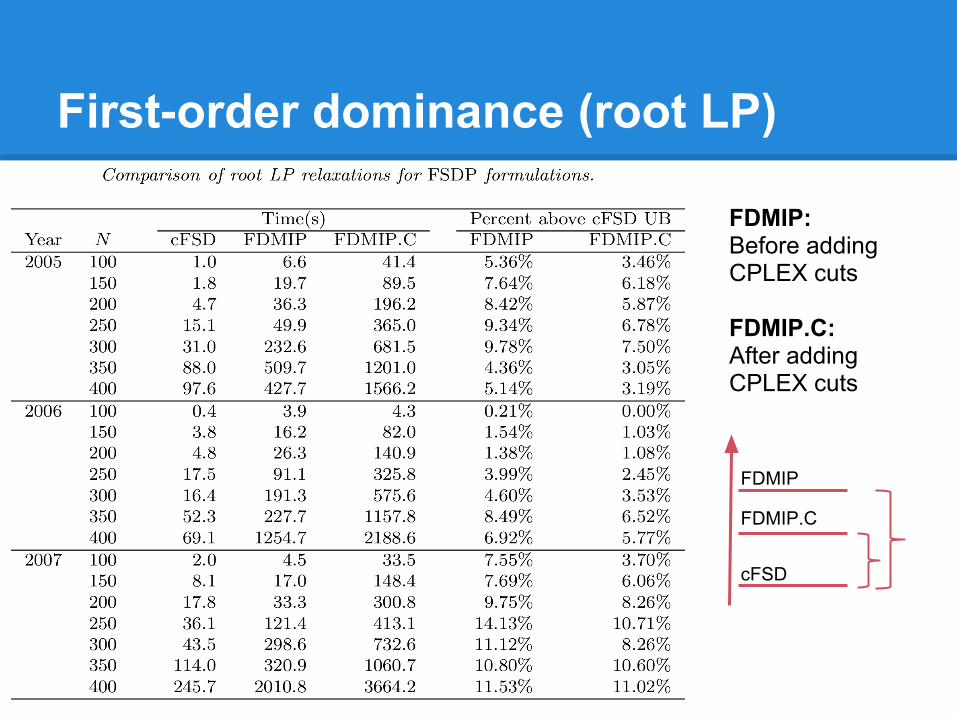

First-order dominance (root LP)

FDMIP: Before addingCPLEX cuts FDMIP.C: After addingCPLEX cuts

FDMIP

FDMIP.C

cFSD

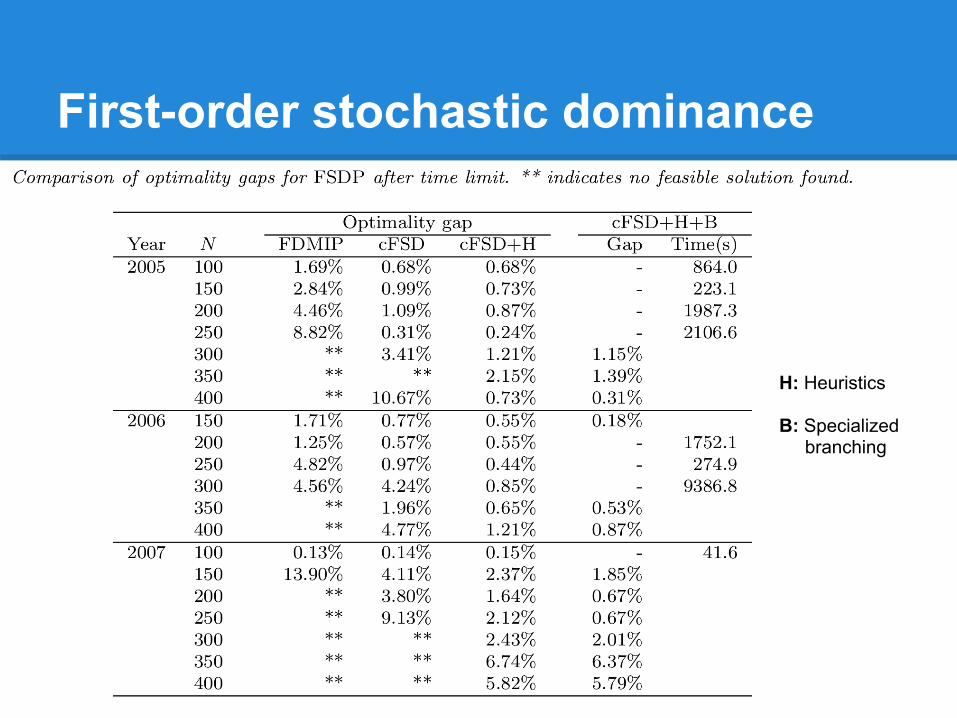

First-order stochastic dominance

H: Heuristics B: Specialized branching