Embed Size (px)

Citation preview

1

PROJECT REPORT

ON

RATIO ANALYSIS

OF

SUBMITTED TO: SUBMITTED BY:

PG Department Of Commerce SUKHCHAIN AGGARWAL

B.com (Accounting & Finance) 2ND

9007

2

DECLARATION

I hereby declare that the project entitled “RATIO ANALYSIS” is bonafide record of work

done by Sukhchain Aggarwal a student of B.com (Accounting & Finance) and is submitted to PG

Department of Commerce in partial fulfillment of the requirement for the degree.

This work has never been submitted to any Educational Institution as per good of my

knowledge.

Sukhchain Aggarwal

B.com (Accounting & Finance)

9007

3

ACKNOWLEDGEMENT

With great pleasure we are presenting this report on the basis of our visit to the “AXIS Bank”.

We are highly grateful to „Prof. Bikramjit Singh Sandhu‟ & „Prof Rohini Gupta‟ for giving

us the time, encouragement and guidance and granting permission for the project. His critical and

detailed comments and full support helped and benefited us in carrying out the project.

Thanking you,

Sukhchain Aggarwal

Raj Kumar

4

CONTENTS

Sr. No. TOPIC Page No.

1 Introduction 5

2 History 6

3 Change in Name 7

4 Research Methodology 9

5 Products & Services 10

6 Shareholding Patterns 17

7 Board of Directors 19

8 Mission & Objectives 20

9 Financial Statement Analysis 21

10 Profit & Loss Account 22

11 Balance Sheet 24

12 Ratio Analysis 26

13 Financial Ratios 32

14 Conclusions 35

15 References 36

5

Introduction

Axis Bank India, the first bank to begin operations as new private banks in 1994 after the

Government of India allowed new private banks to be established. Axis Bank was jointly promoted

by the Administrator of the specified undertaking of the Unit Trust of India (UTI-I), Life Insurance

Corporation of India (LIC) and General Insurance Corporation Ltd. Also with associates viz.

National Insurance Company Ltd., The New India Assurance Company, The Oriental Insurance

Corporation and United Insurance Company Ltd.

Axis Bank in India today is capitalized with Rs. 282.65 Crores with 57.05% public holding other

than promoters. It has more than 574 branch offices and Extension Counters in the country with

over 2428 Axis Bank ATM proving to be one of the largest ATM networks in the country. It

commits to adopt the best industry practices internationally to achieve excellence. It has strengths in

retail as well as corporate banking.

By the end of June 2007, Axis Bank in India had over 60 lakhs debit cards. This is the first bank in

India to offer the AT PAR Cheque facility, without any charges, to all its Savings Bank customers

in all the places across the country where it has presence.

With the AT PAR cheque facility, customers can make cheque payments to any beneficiary at any

of its existence place. The ceiling per instrument is Rs. 50,000/-

The latest offerings of the bank is the Australian Dollar and Canadian Dollar variants of the

international Travel Currency Card along with the US Dollar, Euro and Pound Sterling variants.

The Travel Currency Card is a signature based pre-paid travel card which enables travellers global

access to their money in local currency of the visiting country in a safe and convenient way. Along

with this the bank has also launched the credit cards in silver and gold variants which can be

accessed in 60 cities across the country.

The bank has also raised its reach to 341 cities, towns and villages. The bank has the outstanding

deposit base of more than Rs. 61,000 crores with over 65 lakh accounts.

6

HISTORY

Established in 1994, the Axis Bank Ltd was the first private sector bank in the liberalization

era with its registered office at Ahmadabad and corporate office in Mumbai. The main promoters of

this bank were Unit Trust of India, LIC of India, GIC of India (General Insurance Corporation).

Within the span of 10 years, this bank has had a momentous growth .Today it has 350 branches and

extension counters across the country .Each branch is fully computerized with a centralized

database at Mumbai and disaster management backup at Bangalore. The branches are designed in

such a manner as to offer the full range corporate and retail banking, international banking, treasury

management, merchant and investment banking. All in all the clients are assured of efficient and

hassle free banking.

Axis Bank was formed as UTI when it was incorporated in 1994 when Government of India

allowed private players in the banking sector. The bank was sponsored together by the administrator of

the specified undertaking of the Unit Trust of India, Life Insurance Corporation of India (LIC) and

General Insurance Corporation ltd. and its subsidiaries namely National insurance company ltd., the

New India Assurance Company, the Oriental Insurance Corporation and United Insurance Company

Ltd. However, the name of UTI was changed because of the disagreement on terms and conditions of

the bank authority over certain stipulations including royalty charged over the name from UTI AMC.

The bank also wanted to have a new name from its pan-Indian as well as international business

perspective. So from July 30, 2007 onwards the UTI bank was named as Axis Bank.

7

Change in Name

UTI Bank decided to change its name to Axis Bank.

REASONS : The change in the bank's name follows a year-long tiff between UTI Mutual Fund and the

bank over the use of the brand name. UTI brand was given in 1994 by its promoters and UTI Bank

could use the brand only till January 2008 as per Govt directives. Many unrelated shareholder entities

like UTI Technological Services, UTI Investor Services and UTI Securities were carrying the UTI

brand. The board feels that the need for the change of name has arisen from the brand confusion that

the UTI brand generates

NEW LOGO: The bank has retained the burgundy color, but has changed the logo. The logo uses the

alphabet 'A' from the word Axis. The logo depicts a strong growth path for the bank supported by a

strong base, indicating that the bank is moving on from a position of strength. Earlier, the bank's logo

used the letters U, T and I.

The bank is likely to spend around Rs50 crore in the re-branding exercise.

UTI Bank: Now Axis Bank

The name of the country's third largest private sector lender UTI Bank has been officially

changed to the Axis Bank Ltd with effect from 31st July, 2007. Some reasons for change in name of

'UTI Bank to Axis Bank' - are:

1) The UTI brand is owned by UTI Asset Management Company.

2) UTI Bank to shed its brand name after the split of the erstwhile UTI. Though UTI was a government

institution, its subsidiary UTI Bank has been categorized as a private sector bank, according to RBI

guidelines.

8

3) UTI Bank was started as a part of the entire UTI (Unit Trust of India) Group. But, when there were

losses incurred by UTI ( due to failure of US 64 scheme probably ) because of other reasons, it was

decided by RBI that UTI Bank should be separated as private sector bank, as several unrelated

entities were using the UTI brand.

4) The change of name to Axis Bank has been cleared from shareholders and regulators.

5) The government still has a 26% stake in UTI Bank. This stake is up for sale.

Regarding the re-branding strategy, Executive director (corporate strategy) of the bank R Ashok

Kumar said the bank had hired advertising firm O&M to help in creating awareness of the new brand

across the country. The bank would change logo and color of logo, he had said, adding, the bank is

likely to spend around Rs 50 crore (Rs 500 million) in the re-branding exercise

9

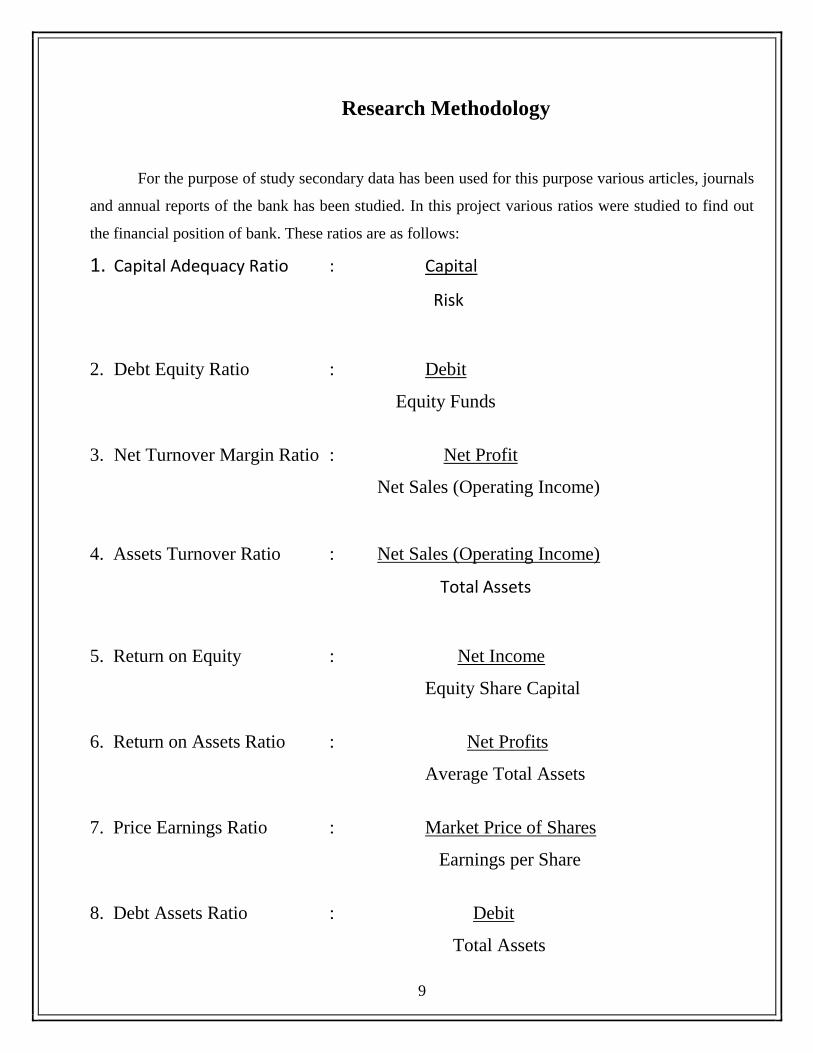

Research Methodology

For the purpose of study secondary data has been used for this purpose various articles, journals

and annual reports of the bank has been studied. In this project various ratios were studied to find out

the financial position of bank. These ratios are as follows:

1. Capital Adequacy Ratio : Capital

Risk

2. Debt Equity Ratio : Debit

Equity Funds

3. Net Turnover Margin Ratio : Net Profit

Net Sales (Operating Income)

4. Assets Turnover Ratio : Net Sales (Operating Income)

Total Assets

5. Return on Equity : Net Income

Equity Share Capital

6. Return on Assets Ratio : Net Profits

Average Total Assets

7. Price Earnings Ratio : Market Price of Shares

Earnings per Share

8. Debt Assets Ratio : Debit

Total Assets

10

PRODUCTS AND SERVICES

Facilities

1) Axis Bank is fully computerized. Which gives less possibility of errors and accuracy is increased.

Computerization also saves time which in turn improves customer service also.

2) Axis bank have also introduced Internet banking and Telebanking

Wherein you can do all your normal banking transactions sitting at home. Like in telebanking you can

inquire balances on phone. Give cheque book request on phone, etc. In internet banking you can view

your balances and statement on net. Transfer funds from one account to another through net. Do on line

shopping. Pay your Axislity bills, LIC premium through net. Do railway reservations on net. Your bank

gets debited for the same. These facilities are password protected. So that security is maintained and no

one can misuse the same.

3) One of the major breaks through in Axis banking is ATM facility. ATM gives you access to your

banking needs like withdrawal and deposits, balance inquiry, 24 hrs, 365 days of the year. Irrespective

of wherever you are you can transact from any of the ATMs. Axis bank have tie up with service

providers like Visa and MasterCard wherein customer holding ATM card of Axis bank can withdraw

from any other bank ATM also.

4) Now Online Banking or anywhere banking has also started in India. Wherein all the branches of a

particular bank are networked across the Country having one centralized database. This gives

advantage to the Customer of one branch to transit in any of the branches of that bank. For e.g.

Customer having an account in Mumbai branch of Axis Bank can also operate his account from Delhi

or Chennai branch of Axis Bank.

5) Mobile banking facilities with SMS alerts.

6) NRI services

11

7) Depositary services (Demat account).

8) Financial advisory services like sales of various Mutual funds, RBI bonds, Infrastructure bonds.

9) Retail loans like personal, housing, vehicle, consumer loans, etc.

Hassle-free Current Account for a lifetime:

After completing the necessary paperwork activity the client with a current account can look

forward to the following facilities:-

ATM Network:

Proprietary concerns are given free ATM cards to enable them to access their account at

anytime at the various ATM centre‟s across the country. In addition cash can be withdrawn from any of

the ATMs against the MasterCard {domestic /international}

Overdraft facility:

The current account holder can avail of overdraft facility against fixed deposits, Axis Schemes

and Demat shares.

Foreign Remittances.

The account holder can make remittances abroad with ease.

Instantaneous Transfers

Funds can be transferred with great speed across the various Axis branches spread across the

country.

7 Day banking

At select branches, the account holder can do his banking on all 7 days of the week .Thus the

customer is assured of non-stopnking and smooth running of business transactions.

12

Tele banking

Tele banking is another innovative service for the convenience of the client. This allows him

instant access to his account. It involves a wide range of services over the phone. The account holder

can get account information, give instructions for stop payment, make a request for cheque book

inquire about interest rates and foreign exchange rates.

Connect Net Banking

This is another revol Axis nary feature that brings the bank right up to the desktop of the holder.

He can look up the status of the account, query and undertake a wide range of financial transactions.

All this with a simple click of the mouse!

A world of convenience at no extra charges!

No wonder then that the holder finds himself laughing all the way up to the Bank!

Retail Loans

Personal Loans from Axis Bank

Want to go on your dream holiday or want to buy the latest lifestyle gizmo. Want to gift your wife a

lovely diamond ring or have a wedding in the family. Maybe your house needs renovation or your

daughter / son has obtained admission to a medical college. These are moments in life when you may

need a helping hand. That's when you can rely on Axis Bank Personal Loan. We offer personal loans to

meet all your personal requirements.

13

Cash Management Services

Our Offering

In today's competitive marketplace, effectively managing cash flow can make the difference

between success and failure. The cash flow solAxisons of the Axis give you maximum control over

this vital asset. Whether you do business locally or throughout India, they can provide you with

innovative, integrated cash management solAxisons tailored to your specific needs. Cash

Management enables the efficient Axislization of your receivables through coordinated

management of payments, collections and balances in your accounts. The objectives are to reduce

costs, enhance control and optimize returns by leveraging Banking expertise for mutual gains.

Managing Receivables: Collections

Managing Payables: Payments

Managing Taxes: CDBT / CBEC Collections

Managing Information: MIS, IT Support & Services

Managing Resources: Liquidity Management

Axis Bank's Cash Management Services is based on an extremely robust technology capable to

cater to collections or payment's requirements of: Corporate, Banks and Axislity Service providers.

Collection SolAxisons:

Managing Receivables: Collections

Axis Bank facilitates faster collections by enabling quick realization of local and upcountry

cheques and pooling the funds in a central account. We provide the following collection products:

Local Cheque Collections (LCC):

LCC enables you to realize funds (on an assured day) through local cheques payable within the

purview of local clearing. The bank provides these services at

14

Axis Bank Network: 171 Locations with Courier Pickup facility

Co-Ordinator Network: Locations with Courier Pickup facility can be added as per your

business requirements

Upcountry Cheque Collection (UCC) :

As collecting bankers, they provide you service relating to:

Public/Rights Issues

Private Placements

Buyback offers

In this current scenario of cut-throat competition, Axis Bank has designed its products to

minimize the issues faced by you in the area of fund management and reconciliation. Our aim is to

reduce the cost, time and efforts faced by corporate in collection and payment issues. The bank

provides you complete solAxisons to all your CMS needs to enable you to devote more time and

effort towards improving your business.

Bulk Collections - Axislity Bills / PDCs Management

Axis Bank, also offers a solAxison to meet Bulk Collection Requirements i.e. Post Dated

Cheques, Bulk Collections through Cheque clearing or ECS debit services, etc. The Bank processes

collections in a convenient and efficient way to avoid any reconciliation issues.

Payment SolAxisons

Payable at Par cheque:

Local cheques can be deposited at all Axis Bank locations, absolutely free of cost. This

makes us a universal customer of Axis Bank and eliminates the need for opening and tracking

separate accounts. Bulk Payments with Remote Printing & Dispatch Facility.

This enables you to avail bulk Demand drafts at all Axis Bank locations. You can also avail

online paid / unpaid status DDs purchased from any of its branches.

15

Statutory Payments

You can make statutory payments like taxes, Axislity bills, etc. within a committed time

frame at any of our branches on a regular basis which is executed through our dedicated HUB

/Dividends / Interest / Principal / Refund Order Payments

Dividends / Interest / Refund Order Payments / Redemption

AXIS Bank has launched its Centralized Bulk Payment Module that offers the following value:

Centralized maintenance of Master data for every client

Real-time clearing activity.

Online Validation with Master Data

Daily Paid - Unpaid data.

Comprehensive MIS.

Prevention of Fraudulent Payments.

Electronic Clearing Services

Credit ECS: The bank undertakes electronic clearances of credit for dividend, interest,

salary, pension, I-T Refund orders and other payments.

Debit ECS: They ensure faster clearance of telephone and electricity billings, loan

installments, PF subscriptions, etc.

You can enjoy the benefits of reduced administration costs, avoid loss of instruments and

enhanced customer service they ensure efficient fund management, reduced delays and easy

assessment of your funds position.

16

Managing Taxes - CBDT / CBEC Collections

AXIS Bank is authorized by Reserve Bank of India to conduct Government Business i.e.

collection of Income Tax, Corporation Tax, etc through 199 designated branches across the country.

They are also authorized to collect Excise and Service Tax through various designated branches in

Delhi, Mumbai and Bangalore.

Issue Management

Managing Resources: Liquidity Management

The Bank lets you achieve maximum returns on excess liquidity and optimize overdraft

charges on your account. It comprises of the Auto Sweep, which allows movement of debit and

credit balances of your various Current Accounts. They also have Financial Advisory Services to

make your money work for you.

Your Benefits

Cash flow management: Provides better management and forecasting of cash flow through the

host of services.

Optimized returns: Through the coordinated management of payments, receivables and cash

balances, you are able to reduce interest charges and optimize returns on your deposits and

investments.

Increased efficiency and productivity: Offers easy and convenient means to perform online

banking (such as cheque services and funds transfer), bulk payments and collections, etc. - leaving

your staff with more time for other tasks.

Better control: Empowered by our CMS, you now enjoy greater control over your transactions,

funds placement and the management of your various bank accounts.

Enhanced security: Advanced security features are built into our systems to ensure end-to-end

security and confidentiality, as well as control over payment processing.

17

Shareholding Patterns

Distrib Axison of Shareholding as on 30th June, 2005

As per clause 35 of Listing Agreement

Sr.

No.

Category No. of Equity

Shares

% To Total

A Promoter's Holding

1 Promoters 77245070 27.77

Indian Promoters (including Co-

Promoters)

(i) Administrator of the specified

undertaking of the Unit Trust of India

77245070 27.77

Co-promoters

(i) Life Insurance Corporation of India 29222936 10.51

(ii) General Insurance Corporation of

India & GIC Susidiaries

15397679 5.54

Foreign Promoters 0 0.00

Sub Total 44620615 16.05

Total 121865685 43.82

B Non- Promoter's Holding

2 InstitAxisonal Investors

a Mututal Funds 7953100 2.86

b Banks, Financial InstitAxisons,

Insurance Companies (Central/State

Govt. InstitAxisons/ Non-Govt.

InstitAxisons)

2012792 0.72

18

c FIIs 57320702 20.61

Sub Total 67286594 24.19

3 Others

a Private Corporate Bodies 4151658 1.49

b Indian Public 16666136 6.00

c NRIs/OCBs 289473 0.10

d Any Other(please specify)-FDI 67864319 24.40

I. HSBC Asia Pacific (UK) Limited –

33950000

II. The Bank of New York - 33914319

(Depositary for the equity shares

representing the underlying shares to

the Global Depositary Receipts

(GDRs) issued to the investors

overseas)

Sub Total 88971586 31.99

Total ( 2 + 3 ) 156258180 56.18

Grand Total (A + B) 278123865 100.00

19

Board of Directors

The Bank has 9 members on the Board. Dr. P. J. Nayak is the Chairman and Managing

Director of the Bank.

The members of the Board are:

Dr. P. J. Nayak Chairman & Managing Director

Shri Surendra Singh Director

Shri N.C. Singhal Director

Shri A.T. Pannir Selvam Director

Shri J.R. Varma Director

Dr. R. H. Patil Director

Smt. Rama Bijapurkar Director

Shri R B L Vaish Director

Shri S. Chatterjee ExecAxisve Director

Office Timings:

Except for the IT department which works for 24 hours in shifts all the remaining

departments and branches work from Monday-Saturday in 9.00am-5.00pm single shifts.

Division of work, authority and responsibility:

The corporate head office in Mumbai is the central controlling authority. The different

departments in any branch are accountable to their respective heads, who are in turn under the head

office. There is a systematic co-ordination between the various activities of each branch and also a

trouble-shooting mechanism to attend to unforeseen problems. Besides there is the Public Relations

Department to address the problems of the general public.

20

MISSION, POLICIES & OBJECTIVES

Mission and policies:

Customer services and product innovation to meet the diverse needs of the individual and

corporate clientele.

Continuous up gradation of technology while maintaining human values.

Progressive globalization and achieving international standards.

Efficiency and effectiveness based on ethical practices.

Objectives:

The main objective of Axis Bank is to understand the financial needs of each client.

Investing money is always a complicated decision .This is where the Axis bank offers “Financial

Advisory Services”. They tailor their sol Axis on according to the needs of each individual. They

diversify and spread the risk of the investment portfolio to ensure that the client spends the rest of

his life comfortably free of worries.

The main objective is to explain to the client what his money can do for him. They help in

profiling the investment horizon, risk tolerance and investment objectives. Thus investing in Axis

means investing in total peace of mind.

21

Financial Statement Analysis

A financial statement analysis consists of the application of analytical tools and techniques to

the data in financial statements in order to derive from them measurements and relationships that are

significant and useful for decision making.

Uses of Financial Statement Analysis:

Financial Statement Analysis can be used as a preliminary screening tool in the selection of

stocks in the secondary market. It can be used as a forecasting tool of future financial conditions and

results. It may be used as process of evaluation and diagnosis of managerial, operating or other problem

areas.

Sources of Financial Information:

The financial data needed in the financial analysis come from many sources. The primary

source is the data provided by the company itself in its annual report and required disclosures. The

annual report comprises of the income statement, the balance sheet, and the statement of cash flows.

Tools of Financial Analysis:

In the analysis of financial statements, the analyst has a variety of tools available to choose the

best that suits his specific purpose. In this report we will confine ourselves to Ratio Analysis based on

information provided from financial statements such as Balance Sheet and Profit & Loss Account.

22

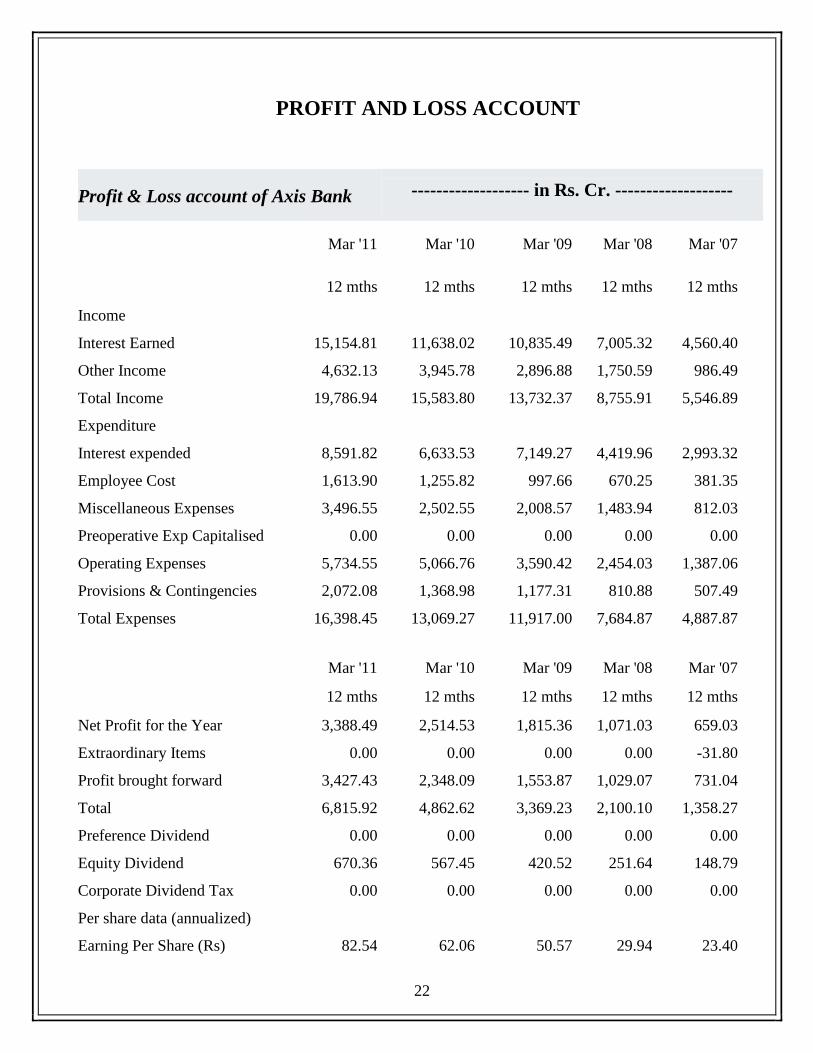

PROFIT AND LOSS ACCOUNT

Profit & Loss account of Axis Bank ------------------- in Rs. Cr. -------------------

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

12 mths 12 mths 12 mths 12 mths 12 mths

Income

Interest Earned 15,154.81 11,638.02 10,835.49 7,005.32 4,560.40

Other Income 4,632.13 3,945.78 2,896.88 1,750.59 986.49

Total Income 19,786.94 15,583.80 13,732.37 8,755.91 5,546.89

Expenditure

Interest expended 8,591.82 6,633.53 7,149.27 4,419.96 2,993.32

Employee Cost 1,613.90 1,255.82 997.66 670.25 381.35

Miscellaneous Expenses 3,496.55 2,502.55 2,008.57 1,483.94 812.03

Preoperative Exp Capitalised 0.00 0.00 0.00 0.00 0.00

Operating Expenses 5,734.55 5,066.76 3,590.42 2,454.03 1,387.06

Provisions & Contingencies 2,072.08 1,368.98 1,177.31 810.88 507.49

Total Expenses 16,398.45 13,069.27 11,917.00 7,684.87 4,887.87

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

12 mths 12 mths 12 mths 12 mths 12 mths

Net Profit for the Year 3,388.49 2,514.53 1,815.36 1,071.03 659.03

Extraordinary Items 0.00 0.00 0.00 0.00 -31.80

Profit brought forward 3,427.43 2,348.09 1,553.87 1,029.07 731.04

Total 6,815.92 4,862.62 3,369.23 2,100.10 1,358.27

Preference Dividend 0.00 0.00 0.00 0.00 0.00

Equity Dividend 670.36 567.45 420.52 251.64 148.79

Corporate Dividend Tax 0.00 0.00 0.00 0.00 0.00

Per share data (annualized)

Earning Per Share (Rs) 82.54 62.06 50.57 29.94 23.40

23

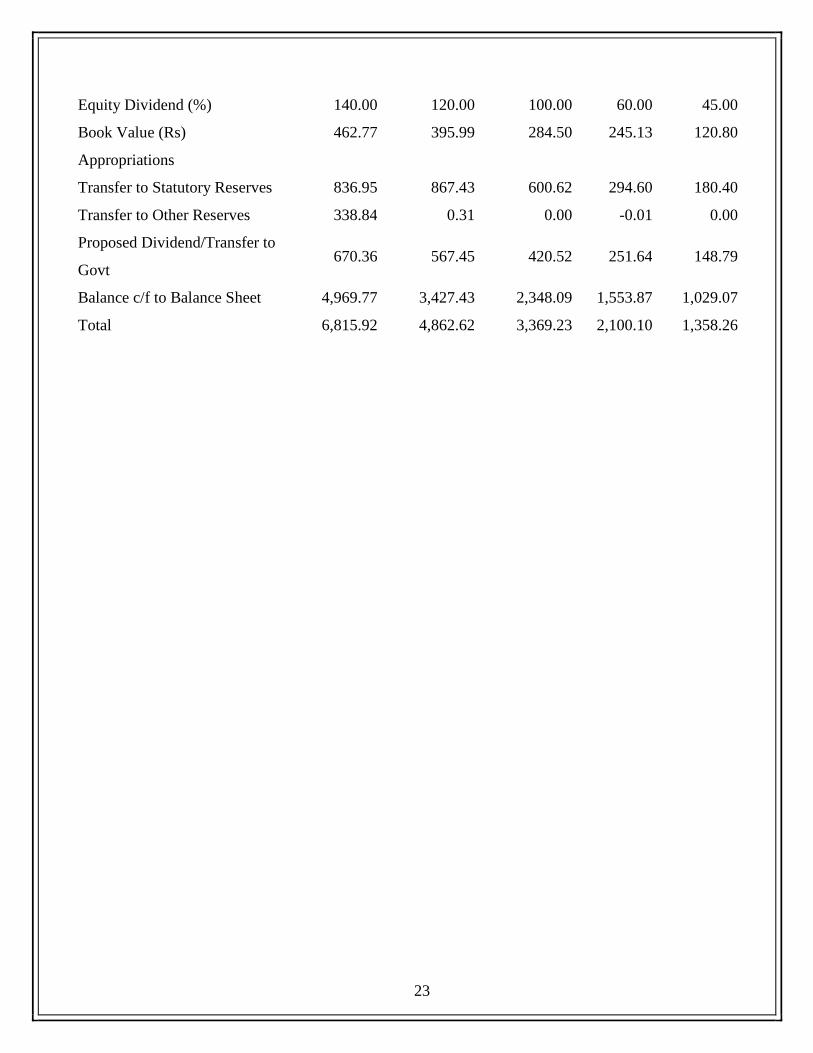

Equity Dividend (%) 140.00 120.00 100.00 60.00 45.00

Book Value (Rs) 462.77 395.99 284.50 245.13 120.80

Appropriations

Transfer to Statutory Reserves 836.95 867.43 600.62 294.60 180.40

Transfer to Other Reserves 338.84 0.31 0.00 -0.01 0.00

Proposed Dividend/Transfer to

Govt 670.36 567.45 420.52 251.64 148.79

Balance c/f to Balance Sheet 4,969.77 3,427.43 2,348.09 1,553.87 1,029.07

Total 6,815.92 4,862.62 3,369.23 2,100.10 1,358.26

24

BALANE SHEET

Balance Sheet of Axis Bank ------------------- in Rs. Cr. -------------------

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

12 mths 12 mths 12 mths 12 mths 12 mths

Capital and Liabilities:

Total Share Capital 410.55 405.17 359.01 357.71 281.63

Equity Share Capital 410.55 405.17 359.01 357.71 281.63

Share Application Money 0.00 0.17 1.21 2.19 0.00

Preference Share Capital 0.00 0.00 0.00 0.00 0.00

Reserves 18,588.28 15,639.27 9,854.58 8,410.79 3,120.58

Revaluation Reserves 0.00 0.00 0.00 0.00 0.00

Net Worth 18,998.83 16,044.61 10,214.80 8,770.69 3,402.21

Deposits 189,237.80 141,300.22 117,374.11 87,626.22 58,785.60

Borrowings 26,267.88 17,169.55 10,185.48 5,624.04 5,195.60

Total Debt 215,505.68 158,469.77 127,559.59 93,250.26 63,981.20

Other Liabilities & Provisions 8,208.86 6,133.46 9,947.67 7,556.90 5,873.80

Total Liabilities 242,713.37 180,647.84 147,722.06 109,577.85 73,257.21

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

12 mths 12 mths 12 mths 12 mths 12 mths

Assets

Cash & Balances with RBI 13,886.16 9,473.88 9,419.21 7,305.66 4,661.03

Balance with Banks, Money at

Call 7,522.49 5,732.56 5,597.69 5,198.58 2,257.27

Advances 142,407.83 104,343.12 81,556.77 59,661.14 36,876.48

Investments 71,991.62 55,974.82 46,330.35 33,705.10 26,897.16

Gross Block 3,426.49 2,107.98 1,741.86 1,384.70 1,098.93

Accumulated Depreciation 1,176.03 942.79 726.45 590.33 450.55

25

Net Block 2,250.46 1,165.19 1,015.41 794.37 648.38

Capital Work In Progress 22.69 57.24 57.48 128.48 24.82

Other Assets 4,632.12 3,901.06 3,745.15 2,784.51 1,892.07

Total Assets 242,713.37 180,647.87 147,722.06 109,577.84 73,257.21

Contingent Liabilities 429,069.63 296,125.58 104,428.39 78,028.44 55,993.04

Bills for collection 57,400.80 35,756.32 29,906.04 16,569.95 11,751.83

Book Value (Rs) 462.77 395.99 284.50 245.13 120.80

26

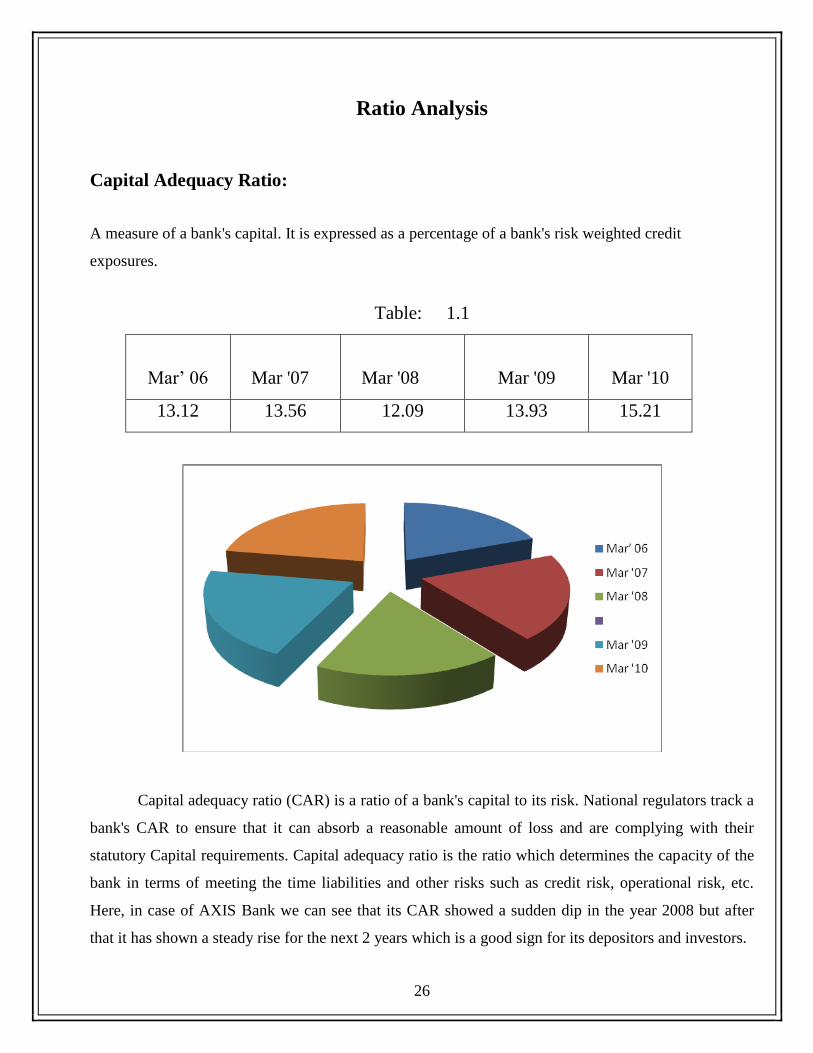

Ratio Analysis

Capital Adequacy Ratio:

A measure of a bank's capital. It is expressed as a percentage of a bank's risk weighted credit

exposures.

Table: 1.1

Mar‟ 06

Mar '07

Mar '08

Mar '09

Mar '10

13.12 13.56 12.09 13.93 15.21

Capital adequacy ratio (CAR) is a ratio of a bank's capital to its risk. National regulators track a

bank's CAR to ensure that it can absorb a reasonable amount of loss and are complying with their

statutory Capital requirements. Capital adequacy ratio is the ratio which determines the capacity of the

bank in terms of meeting the time liabilities and other risks such as credit risk, operational risk, etc.

Here, in case of AXIS Bank we can see that its CAR showed a sudden dip in the year 2008 but after

that it has shown a steady rise for the next 2 years which is a good sign for its depositors and investors.

27

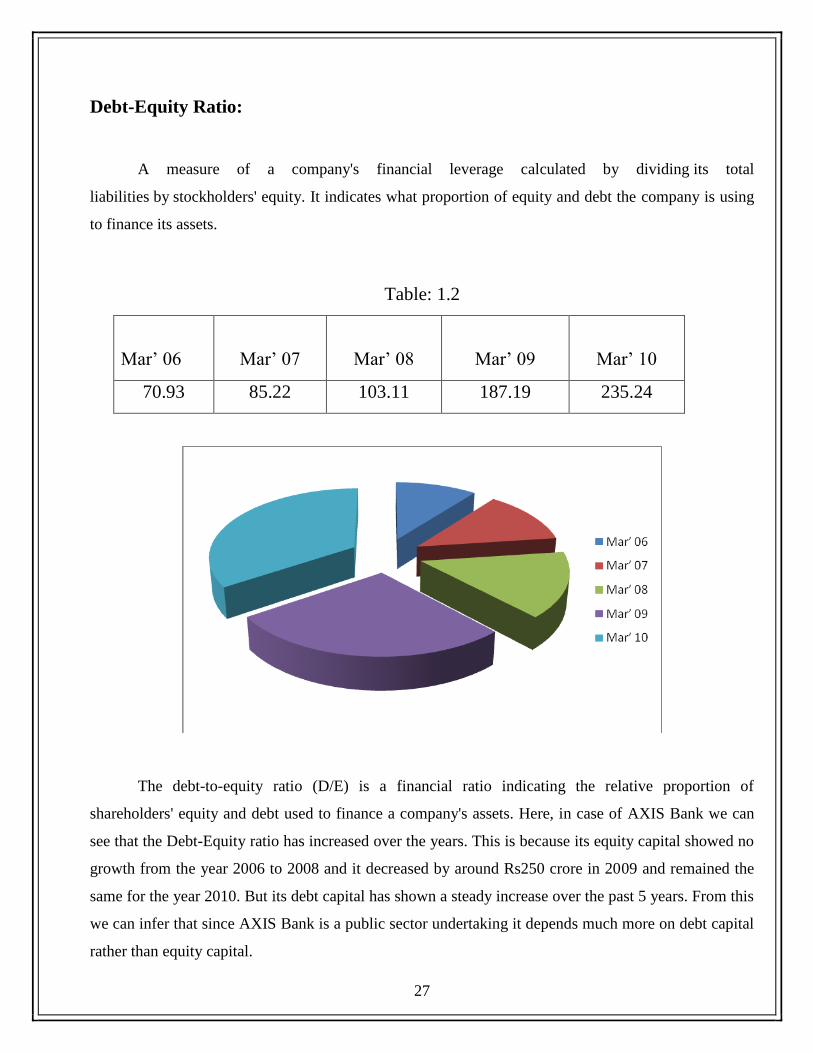

Debt-Equity Ratio:

A measure of a company's financial leverage calculated by dividing its total

liabilities by stockholders' equity. It indicates what proportion of equity and debt the company is using

to finance its assets.

Table: 1.2

Mar‟ 06

Mar‟ 07

Mar‟ 08

Mar‟ 09

Mar‟ 10

70.93 85.22 103.11 187.19 235.24

The debt-to-equity ratio (D/E) is a financial ratio indicating the relative proportion of

shareholders' equity and debt used to finance a company's assets. Here, in case of AXIS Bank we can

see that the Debt-Equity ratio has increased over the years. This is because its equity capital showed no

growth from the year 2006 to 2008 and it decreased by around Rs250 crore in 2009 and remained the

same for the year 2010. But its debt capital has shown a steady increase over the past 5 years. From this

we can infer that since AXIS Bank is a public sector undertaking it depends much more on debt capital

rather than equity capital.

28

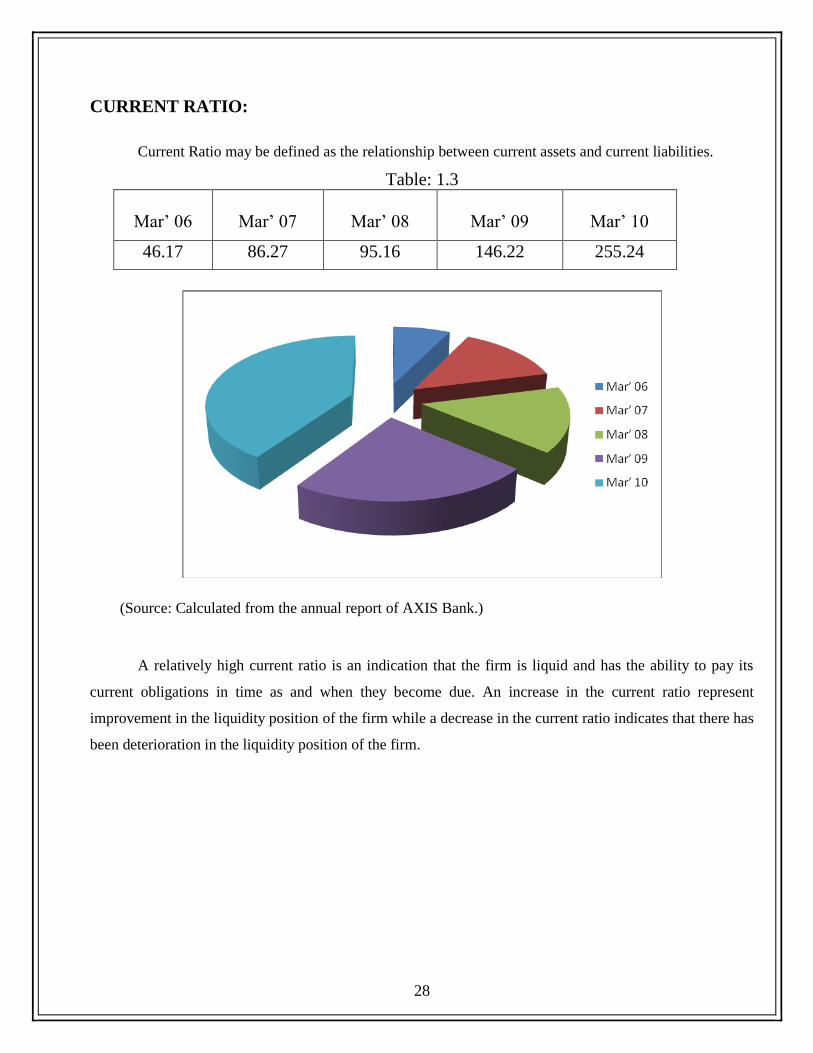

CURRENT RATIO:

Current Ratio may be defined as the relationship between current assets and current liabilities.

Table: 1.3

Mar‟ 06

Mar‟ 07

Mar‟ 08

Mar‟ 09

Mar‟ 10

46.17 86.27 95.16 146.22 255.24

(Source: Calculated from the annual report of AXIS Bank.)

A relatively high current ratio is an indication that the firm is liquid and has the ability to pay its

current obligations in time as and when they become due. An increase in the current ratio represent

improvement in the liquidity position of the firm while a decrease in the current ratio indicates that there has

been deterioration in the liquidity position of the firm.

29

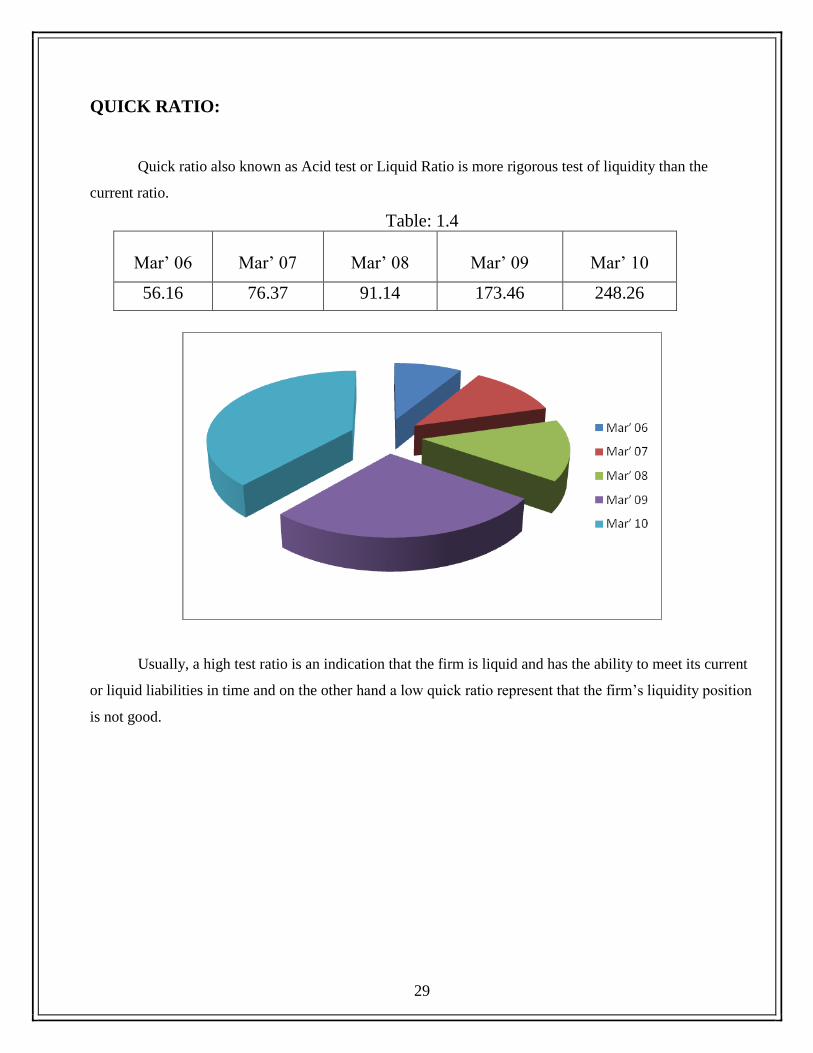

QUICK RATIO:

Quick ratio also known as Acid test or Liquid Ratio is more rigorous test of liquidity than the

current ratio.

Table: 1.4

Mar‟ 06

Mar‟ 07

Mar‟ 08

Mar‟ 09

Mar‟ 10

56.16 76.37 91.14 173.46 248.26

Usually, a high test ratio is an indication that the firm is liquid and has the ability to meet its current

or liquid liabilities in time and on the other hand a low quick ratio represent that the firm‟s liquidity position

is not good.

30

Advances to Assets:

A high ratio of Advances to Assets would mean that the chances of Non Performing Assets

formation are also high, which is not a good scenario for a bank.

Table: 2.1

Mar‟ 06

Mar‟ 07

Mar‟ 08

Mar‟ 09

Mar‟ 10

1.60 1.63 1.61 1.62 1.60

“Advances to Asset” is also a good indicator of a firm‟s Capital Adequacy. A high ratio of

Advances to Assets would mean that the chances of Non Performing Assets formation are also high,

which is not a good scenario for a bank. This would mean the credibility of its assets would go down.

In case of AXIS Bank we can see that it is able to maintain a pretty steady ratio of its Advances to

Assets which means the credibility of its assets is good.

31

Government Securities to Total Investments:

The ratio of Government Securities to Total investments shows how safe are the company‟s

investments.

Table: 2.2

Mar‟ 06

Mar‟ 07

Mar‟ 08

Mar‟ 09

Mar‟ 10

1.81 1.83 1.83 1.86 1.86

The ratio of Government Securities to Total investments shows how safe are the company‟s

investments. Here, in case of AXIS Bank we can see that its ratio of investments in Government

Securities to Total Investments is very high and it has remained quite steady over the years with

minimal fluctuations. The high ratio tells that AXIS Banks investment policy is conservative and their

investments are safe.

32

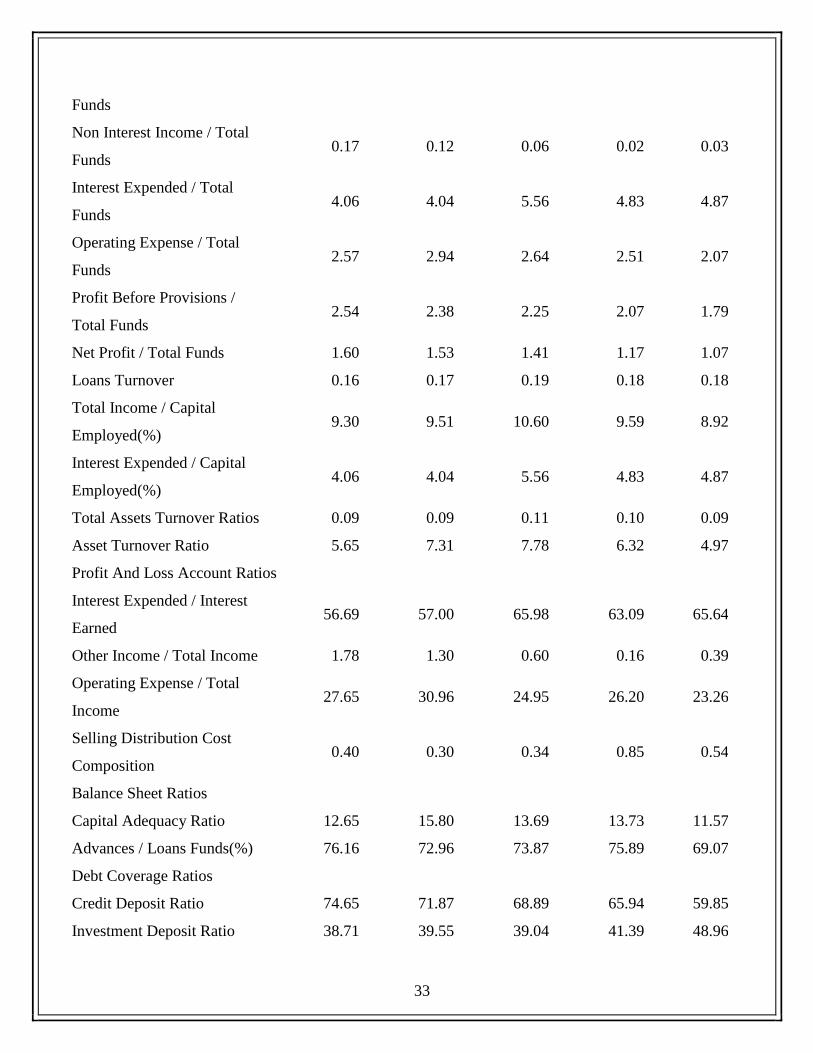

FINANCIAL RATIOS

Financial Ratios ------------------- in Rs. Cr. -------------------

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

Investment Valuation Ratios

Face Value 10.00 10.00 10.00 10.00 10.00

Dividend Per Share 14.00 12.00 10.00 6.00 4.50

Operating Profit Per Share

(Rs) 129.26 97.29 83.56 56.88 42.36

Net Operating Profit Per Share

(Rs) 471.17 380.27 377.46 244.63 193.93

Free Reserves Per Share (Rs) 373.06 325.87 230.47 208.03 86.60

Bonus in Equity Capital -- -- -- -- --

Profitability Ratios

Interest Spread 3.73 3.95 4.24 3.77 3.27

Adjusted Cash Margin(%) 18.71 17.63 14.76 14.19 14.11

Net Profit Margin 17.20 16.10 13.31 12.22 12.01

Return on Long Term

Fund(%) 72.29 66.34 97.35 71.17 119.74

Return on Net Worth(%) 17.83 15.67 17.77 12.21 19.37

Adjusted Return on Net

Worth(%) 17.87 15.69 17.85 12.38 19.45

Return on Assets Excluding

Revaluations 462.77 395.99 284.50 245.13 120.80

Return on Assets Including

Revaluations 462.77 395.99 284.50 245.13 120.80

Management Efficiency Ratios

Interest Income / Total Funds 9.14 9.38 10.53 9.57 8.88

Net Interest Income / Total 5.08 5.34 4.98 4.74 4.01

33

Funds

Non Interest Income / Total

Funds 0.17 0.12 0.06 0.02 0.03

Interest Expended / Total

Funds 4.06 4.04 5.56 4.83 4.87

Operating Expense / Total

Funds 2.57 2.94 2.64 2.51 2.07

Profit Before Provisions /

Total Funds 2.54 2.38 2.25 2.07 1.79

Net Profit / Total Funds 1.60 1.53 1.41 1.17 1.07

Loans Turnover 0.16 0.17 0.19 0.18 0.18

Total Income / Capital

Employed(%) 9.30 9.51 10.60 9.59 8.92

Interest Expended / Capital

Employed(%) 4.06 4.04 5.56 4.83 4.87

Total Assets Turnover Ratios 0.09 0.09 0.11 0.10 0.09

Asset Turnover Ratio 5.65 7.31 7.78 6.32 4.97

Profit And Loss Account Ratios

Interest Expended / Interest

Earned 56.69 57.00 65.98 63.09 65.64

Other Income / Total Income 1.78 1.30 0.60 0.16 0.39

Operating Expense / Total

Income 27.65 30.96 24.95 26.20 23.26

Selling Distribution Cost

Composition 0.40 0.30 0.34 0.85 0.54

Balance Sheet Ratios

Capital Adequacy Ratio 12.65 15.80 13.69 13.73 11.57

Advances / Loans Funds(%) 76.16 72.96 73.87 75.89 69.07

Debt Coverage Ratios

Credit Deposit Ratio 74.65 71.87 68.89 65.94 59.85

Investment Deposit Ratio 38.71 39.55 39.04 41.39 48.96

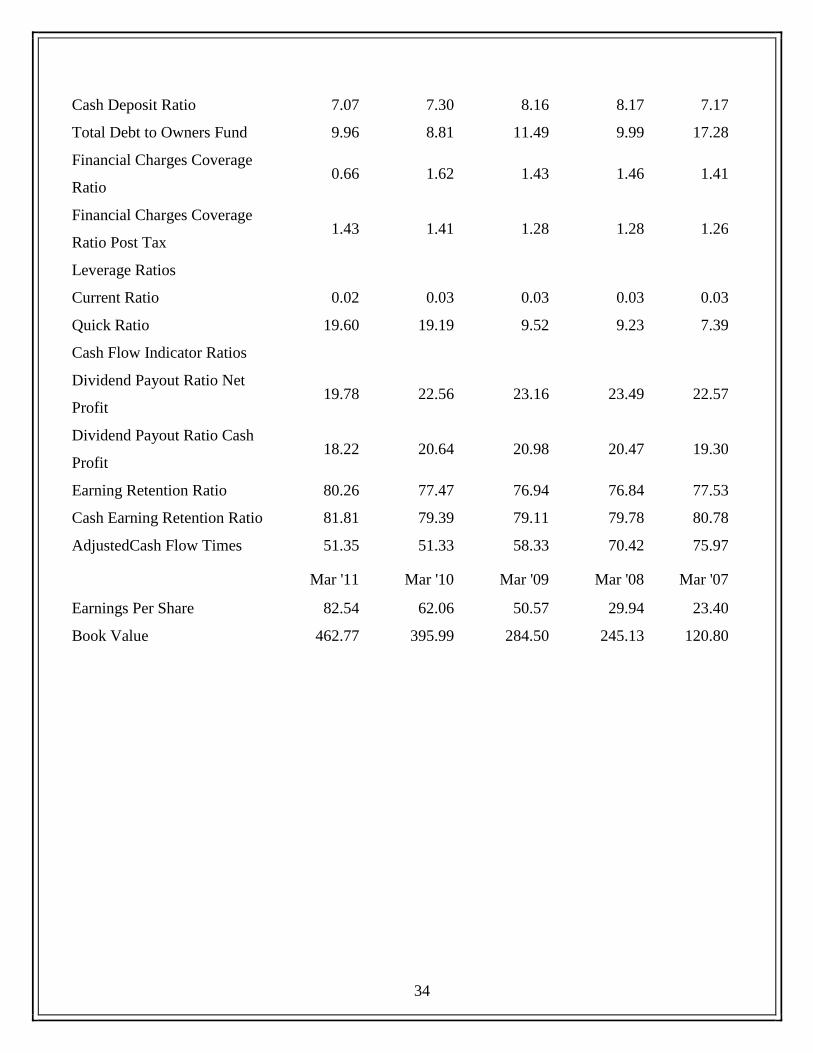

34

Cash Deposit Ratio 7.07 7.30 8.16 8.17 7.17

Total Debt to Owners Fund 9.96 8.81 11.49 9.99 17.28

Financial Charges Coverage

Ratio 0.66 1.62 1.43 1.46 1.41

Financial Charges Coverage

Ratio Post Tax 1.43 1.41 1.28 1.28 1.26

Leverage Ratios

Current Ratio 0.02 0.03 0.03 0.03 0.03

Quick Ratio 19.60 19.19 9.52 9.23 7.39

Cash Flow Indicator Ratios

Dividend Payout Ratio Net

Profit 19.78 22.56 23.16 23.49 22.57

Dividend Payout Ratio Cash

Profit 18.22 20.64 20.98 20.47 19.30

Earning Retention Ratio 80.26 77.47 76.94 76.84 77.53

Cash Earning Retention Ratio 81.81 79.39 79.11 79.78 80.78

AdjustedCash Flow Times 51.35 51.33 58.33 70.42 75.97

Mar '11 Mar '10 Mar '09 Mar '08 Mar '07

Earnings Per Share 82.54 62.06 50.57 29.94 23.40

Book Value 462.77 395.99 284.50 245.13 120.80

35

CONCLUSION

The purpose our project report at a organization was to help us attain knowledge about the

working pattern in a organization.

Applying theoretical knowledge into practice helps in gaining additional knowledge. We learnt the

skill of planning, organizing and completing the assignment within the stipulated time.

Ratio analysis of financial statement shows that bank‟s current ratio is better than the quick ratio

and fixed/worth ratio. It means bank has invested more in current assets than the fixed assets and liquid

assets. The cash flow statement shows that net increase in cash generated from operating and financing

activities is much more than the previous year but cash generated from investing activities is negative

in both years. Therefore analysis of cash flow statement shows that cash inflow is more than the cash

outflow in AXIS Bank. Thus, the ratio analysis and trend analysis and analysis of cash flow statement

show that AXIS Bank‟s financial position is good. Bank‟s profitability is increasing but not at high rate.

Bank‟s liquidity position is fair but not good because bank invests more in current assets than the liquid

assets. As we all know that AXIS Bank is on the first position among the entire private sector bank of

India in all areas but it should pay attention on its profitability and liquidity. Bank‟s position is stable.

36

References

Reports: Annual Reports of AXIS Bank.

Websites:

http://www.sharetermpapers.com/

http://money.rediff.com/companies/axis-bank-ltd/14030047

http://www.axisbank.com/

http://en.wikipedia.org/wiki/Axis_Bank

http://www.rupeetimes.com/compare/credit_cards/axis_bank.html

http://www.axisbank.hk/

http://ekikrat.in/Axis-Bank-Internet-Banking

http://www.microfinancefocus.com/axis-bank-bandhan-launch-program-poorest-families

http://www.winentrance.com/nift_entrance_exam/nift-axis-bank-branches.html

http://blog.arpitnext.com/indiatech/34/axis-bank-ewallet-virtual-credit-card

http://www.homeloanshub.com/axis-bank/