Embed Size (px)

Citation preview

CHAPTER 7

Fourth Knowledge Area:

Project Cost Management

1

PLAN

COST

MGMT

2

ESTIMATE

COST

3

DETERMINE

BUDGET

4

CONTROL

COSTS

Project Cost Management includes the processes involved in Planning,

Estimating, Budgeting, Financing, Funding, Managing, and Controlling

costs so that projects can be completed within budget

1. Plan Cost Management (Planning Process Group)

The process that establishes the policies, procedures, and documentation for planning, managing, expending, and

controlling project costs.

2. Estimate Cost (Planning Process Group)

The process of developing an approximation of the monetary resources needed to complete project activities

3. Determine Budget (Planning Process Group)

The process of aggregating the estimated costs of individual activities or work packages to establish an authorized cost

baseline

4. Control Costs (Monitoring & Controlling Process Group)

The process of monitoring the status of the project to update the project costs & managing changes to the cost baseline.

Project Cost Management must consider stakeholder’s requirements for

managing costs – each stakeholder will measure costs differently.

Project Cost Management is primarily concerned with the cost of the

resources needed to complete project activities & the subsequent costs in

using and supporting the deliverables.

The cost management planning effort occurs early in the project & sets the

framework for each of the cost management processes so that

performance will be efficient.

INPUTS TOOLS & TECHNIQUES OUTPUTS

Plan Cost Management: Inputs, Tools & Techniques, & Outputs

1. Project Management

Plan

2. Project Charter

3. Enterprise Environmental

Factors (EEFs)

4. Organizational Process

Assets (OPAs)

1. Expert Judgment

2. Analytical Techniques

3. Meeting

1. Schedule Management

Plan

• Plan Cost Management is the process of establishing the policies, procedures, and

documentations for planning, managing, expending & controlling project cost.

• It’s key benefit is it provides guidance & directions on how the project costs will be

managed throughout the project

OUTPUT

1

PROJECT

MANAGEMEN

T

PLAN

4

ORGANIZATION

AL

PROCESS

ASSETS

(OPA)

TOOLS &

TECHNIQUE

S

COSTMANAGEMENT

PLAN

3

ENTERPRISE

ENVIRONME

NT

FACTORS

(EEF)

2

PROJECT

CHARTER

OUTPUT

1. EXPERT JUDGMENT

2. ANALYTICAL TECHNIQUES

3. MEETINGS

Other Information

1. Org. Culture & Structure that influences

cost

2. Market Conditions

3. Currency exchange for international

projects

4. Published & Commercially Available Info

5. Project Management Information System

• Financial controls procedures

• Historical information & lessons learned

• Financial databases; and

• Existing formal & informal cost estimating &

budgeting policies

Describes how the project costs will be planned, structured & controlled.

Cost management plan can establish:

• Units of Measure

• Level of Precision

• Level of Accuracy

• Organizational Procedures Links

• Control Thresholds

• Rules of Performance Measurement

• Reporting Formats

• Process Descriptions

• Additional details such as description of strategic funding choices, procedure to

account for fluctuation in currency exchange & cost reporting

INPUTS TOOLS & TECHNIQUES OUTPUTS

Plan Cost Management: Inputs, Tools & Techniques, & Outputs

1. Cost Management Plan

2. Human Resource

Management Plan

3. Scope Baseline

4. Project Schedule

5. Risk Register

6. Enterprise Environmental

Factors

7. Organizational Process

Assets (OPAs)

1. Expert Judgment

2. Analogous Estimating

3. Parametric Estimating

4. Bottom-up Estimating

5. Three-points Estimating

6. Reserve Analysis

7. Cost of Quality

8. Project Management

Software

9. Vendor Bid Analysis

10. Group Decision Making

Techniques

1. Activity Cost Estimates

2. Basic of Estimates

3. Project Documents

Updates

• Estimate Cost is the process of developing an approximation of the monetary

resources needed to complete project activities.

• It’s key benefit is it determines the amount of cost required to complete project work.

3

SCOPE

BASELINE

5

RISK

REGISTER

4

PROJECT

SCHEDUL

E

OUTPUT

1

COST

MANAGEMEN

T

PLAN

7

ORGANIZATION

AL

PROCESS

ASSETS

(OPA)

TOOLS &

TECHNIQUE

S

BASIS OFESTIMATES

6

ENTERPRISE

ENVIRONME

NT

FACTORS

(EEF)

2

H.R.

MGMT

PLAN

OUTPUT

1. EXPERT JUDGMENT

2. ANALOGOUS ESTIMATING

3. PARAMETRIC ESTIMATING

4. THREE-POINT ESTIMATING

5. BOTTOM-UP ESTIMATING

6. RESERVE ANALYSIS

7. COST OF QUALITY

8. PROJECT MANAGEMENT

SOFTWARE

9. VENDOR BID ANALYSIS

10. GROUP DECISION MAKING

TECHNIQUES

1. Market Conditions

2. Published Commercially Info

• Cost Estimating Policies

• Cost Estimating Templates

• Historical Information, and

• Lessons Learned

PROJECT DOCUMENTS

UPDATES

ACTIVITYCOST ESTIMATES

WBS Dictionary

1. Expert Judgment

2. Analogous Estimating – compare with similar past projects when limited amount of detailed info

available

3. Parametric Estimating – uses statistical relationship relevant historical data & other variable

(like square footage) to calculate a cost estimate for project work. It provides higher level of accuracy

depending on past data

4. Bottom Up Estimating – cost of individual work packages are estimated to the greatest level for

detail. Its accuracy is influenced by the size & complexity of the individual activity or work package.

5. Three-Point Estimating

• Most Likely (cM) based on realistic effort assessment

• Optimistic (cO) based on best case scenario

• Pessimistic (cP) based on worst case scenario

Depending on the assumed distribution of value within the range, there are 2

formulas:

• Triangular Distribution. cE = (cO + cM + cP) /3

• Beta Distribution (from PERT analysis) cE = (cO + 4cM + cP) / 6

6. Reserve AnalysisContingency Reserves are the budget within cost baseline that is allocated for identified risks. It is often

viewed as part of the budget to address the “known-unknowns” that can affect a project. It may be a

percentage of the estimated cost, a fixed number, or may be developed by using quantitative analysis

methods.

7. Cost of Quality (COQ) – it cost less to prevent quality issue than to fix it

8. Project Management Software – Computerized spreadsheets, simulation, and statistical

tools are used to assist with cost estimating.

9. Vendor Bid Analysis – Cost estimates can be based on the responsive bids from qualified

vendors

10.Group Decision-Making TechniquesTeam based approaches, such as brainstorming, the Delphi or Nominal Group Techniques are useful for

engaging team members to improve estimate accuracy & commitment to the estimates.

BASIS OFESTIMATES

PROJECT DOCUMENTS

UPDATES

ACTIVITYCOST ESTIMATES

Quantitative assessment of the probable costs required to complete project work. It can be presented in summary form or in detail. Cost are estimated for ALL resources that are applied to the activity cost estimate

The amount and type of additional details supporting the cost estimates vary by application area.Supporting detail may include:

• Documentation of the basis of the estimate (how it was developed),

• Documentation of all assumptions made,

• Documentation of any known constraints,

• Indication of the range of possible estimates (like +/- 10%) to indicate that the item is expected to cost between a range of values, and

• Indication of the confidence level of the final estimate.

Project Documents that may be updated include, but not limited to, the risk register.

INPUTS TOOLS & TECHNIQUES OUTPUTS

Determine Budget: Inputs, Tools & Techniques, & Outputs

1. Cost Management Plan

2. Scope Baseline

3. Activity Cost Estimates

4. Basis of Estimates

5. Project Schedule

6. Resource Calendars

7. Risk Register

8. Agreements

9. Organizational Process

Assets (OPAs)

1. Cost Aggregation

2. Reserve Analysis

3. Expert Judgment

4. Historical Relationship

5. Funding Limit

Reconciliation

1. Cost Baseline

2. Project Funding

3. Project Documents

Updates

• Determine Budget is the process of aggregating the estimated costs of individual

activities or work packages to establish an authorized cost baseline

• It’s key benefit is it determines the cost baseline against which project performance

can be monitored & controlled.

6

RESOURC

E

CALENDA

RS

2

SCOPE

BASELINE

7

RISK

REGISTER

3

ACTIVITY

COST

ESTIMATE

S

OUTPUT

1

COST

MANAGEMEN

T

PLAN

9

ORGANIZATION

AL

PROCESS

ASSETS

(OPA)

TOOLS &

TECHNIQUE

S

PROJECTFUNDING

REQUIREMENTS

5

PROJECT

SCHEDULE

4

BASIS

OF

ESTIMATE

S

OUTPUT

1. COST AGGREGRATION

2. RESERVE ANALYSIS

3. EXPERT JUDGMENT

4. HISTORICAL RELATIONSHIPS

5. FUNDING LIMIT RECONCILIATION

• Existing formal & informal cost budgeting-

related policies, procedures and guidelines;

• Cost budgeting tools; and

• Reporting methods

PROJECT DOCUMENTS

UPDATES

COSTBASELINE

WBS Dictionary

8

AGREEMEN

TS

Info on which resources are

assigned

and when they are assigned

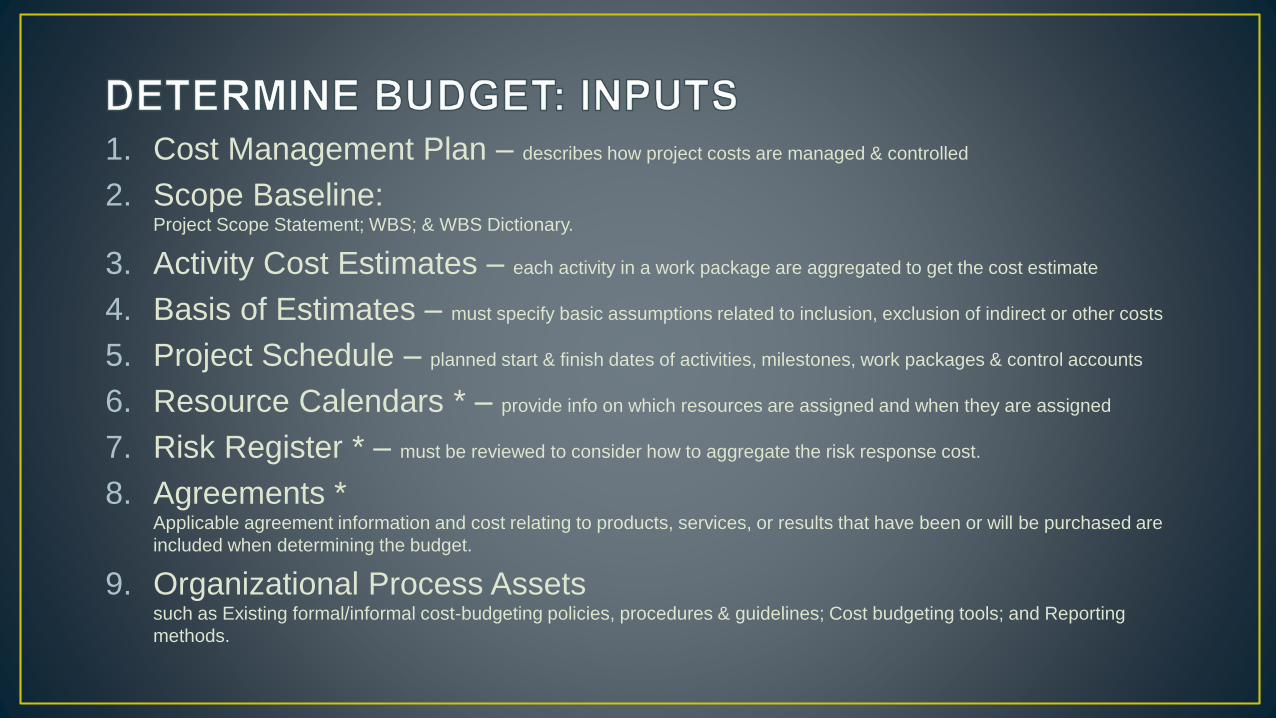

1. Cost Management Plan – describes how project costs are managed & controlled

2. Scope Baseline:Project Scope Statement; WBS; & WBS Dictionary.

3. Activity Cost Estimates – each activity in a work package are aggregated to get the cost estimate

4. Basis of Estimates – must specify basic assumptions related to inclusion, exclusion of indirect or other costs

5. Project Schedule – planned start & finish dates of activities, milestones, work packages & control accounts

6. Resource Calendars * – provide info on which resources are assigned and when they are assigned

7. Risk Register * – must be reviewed to consider how to aggregate the risk response cost.

8. Agreements *Applicable agreement information and cost relating to products, services, or results that have been or will be purchased are

included when determining the budget.

9. Organizational Process Assets such as Existing formal/informal cost-budgeting policies, procedures & guidelines; Cost budgeting tools; and Reporting

methods.

1. Cost Aggregation *costs are aggregated by work packages rolling up to the entire project

2. Reserve Analysiscan establish both contingency reserves & management reserves for the project

3. Expert Judgment such as from Other departments, consultants, stakeholders (including the customers), professional & technical associations;

and industry groups.

4. Historical Relationships *that result in parametric or analogous estimates to develop mathematical model to predict total project cost. The accuracy

depends on if the:

• Historical information used to develop the model is accurate.

• Parameters used are readily quantifiable; and

• Models are scalable

5. Funding Limit ReconciliationExpenditures must be reconciled with any funding limit. A variance may necessitate a rescheduling to level out the rate of

expenditures by placing date constraints on the schedule.

PROJECT DOCUMENTS

UPDATES

PROJECTFUNDING

REQUIREMENTS

COSTBASELINE

Approved version of the time-phased project budget (excluding any management reserves) that can only be changed via formal change control procedures. It is used as a basis for comparison to actual results.

Project Documents that may be updated include, but not limited to:Risk Register, Activity Cost Estimate, and Project Schedule

Derived from the cost baseline that include projected expenditures plus anticipated liabilities. Funding are incremental, not continuous and may not be distributed evenly

Pro

ject

Bu

dg

et

Cost

Baselin

e Contr

ol

Accounts

Work

Pa

cka

ge

Cost E

stim

ate

s

Activity

Cost

Estim

ate

s

Manage

ment

Reserve

sContingen

cy

ReservesActivity

Contingency

Reserves

Tota

l Am

ount

Project Budget Component

INPUTS TOOLS & TECHNIQUES OUTPUTS

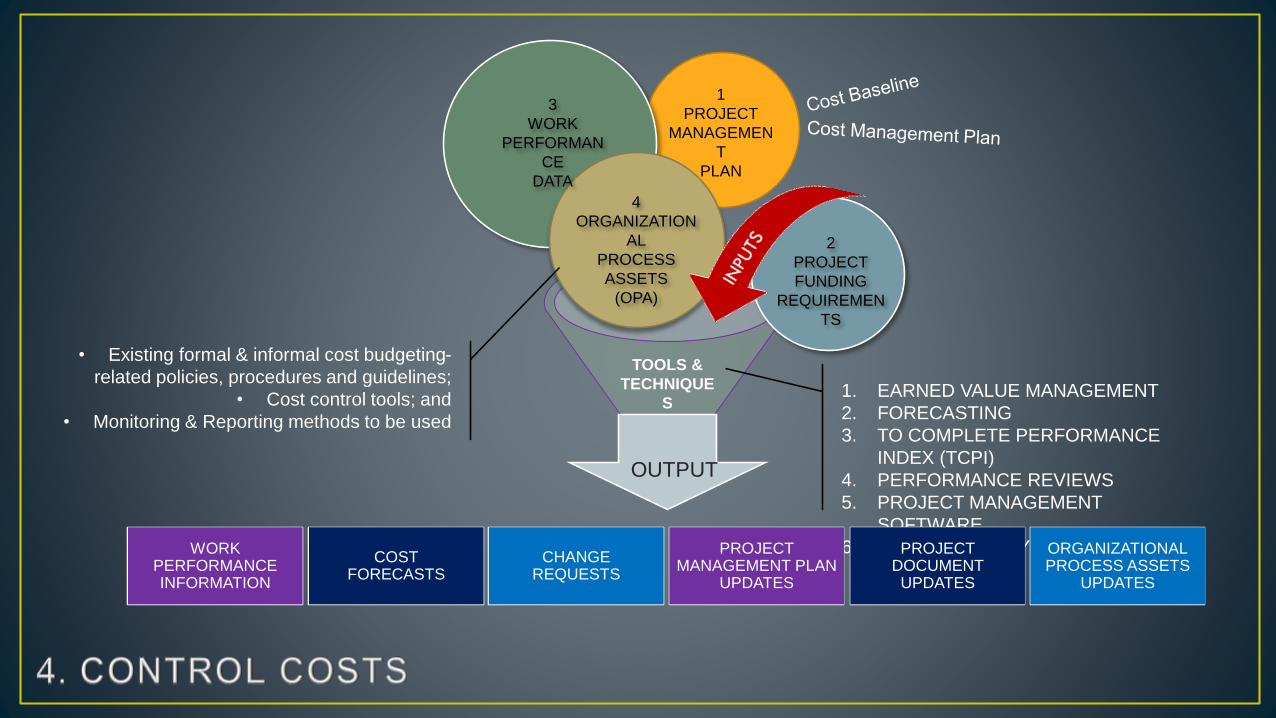

Control Costs: Inputs, Tools & Techniques, & Outputs

1. Project Management Plan

2. Project Funding

Requirements

3. Work Performance Data

4. Organization Process Assets

(OPAs)

1. Earned Value

Management

2. Forecasting

3. To Complete Performance

Index (TCPI)

4. Performance Reviews

5. Project Management

Software

6. Reserve Analysis

1. Work Performance Info

2. Cost Forecasts

3. Change Requests

4. Project Management

Plan Updates

5. Projects Documents

Updates

6. Organizational Process

Assets Updates

• Control Costs is the process of monitoring the status of the project to update the project

costs and managing changes to the cost baseline.

• It’s key benefit is it provides means to recognize variance from the plan in order to take

corrective action & minimize risk.

Much of the effort of cost control involves analyzing the relationship between the consumption of

project funds to the physical work being accomplish for such expenditures that includes:

• Influencing the factors that created changes to the authorized cost baseline;

• Ensuring that all change requests are acted on a timely manner;

• Managing the actual changes when they occur;

• Ensuring that cost expenditures do not exceed the authorized funding by period, by WBS

component, by activity, and in total for the project;

• Monitoring cost performance to isolate and understand variances from the approved cost

baseline;

• Monitoring work performance against funds expended;

• Preventing unapproved changes from being included in the reported cost of resource usage;

• Informing appropriate stakeholders of all approved changes and associated costs; and

• Bringing expected cost overruns within acceptable limits.

OUTPUT

1

PROJECT

MANAGEMEN

T

PLAN

4

ORGANIZATION

AL

PROCESS

ASSETS

(OPA)

TOOLS &

TECHNIQUE

S

COSTFORECASTS

3

WORK

PERFORMAN

CE

DATA

2

PROJECT

FUNDING

REQUIREMEN

TS

OUTPUT

1. EARNED VALUE MANAGEMENT

2. FORECASTING

3. TO COMPLETE PERFORMANCE

INDEX (TCPI)

4. PERFORMANCE REVIEWS

5. PROJECT MANAGEMENT

SOFTWARE

6. RESERVE ANALYIS

• Existing formal & informal cost budgeting-

related policies, procedures and guidelines;

• Cost control tools; and

• Monitoring & Reporting methods to be used

CHANGEREQUESTS

WORKPERFORMANCEINFORMATION

PROJECTDOCUMENTUPDATES

ORGANIZATIONALPROCESS ASSETS

UPDATES

PROJECTMANAGEMENT PLAN

UPDATES

1. Earned Value Management (EVM)A methodology that combines scope, schedule, and resource measurements to asses project performance & progress to

form performance baseline. It is a technique that requires the formation of an integrated baseline to measure performance

of the project.

EVM develops and monitor three key dimensions for each work package & control account:

• Planned Value (PV). Authorized budget assigned to scheduled work for an activity or WBS component (not

including management reserve). It is allocated by phase over the life of the project, but at a given moment, PV

defines the physical work that should have been accomplished. The total of the PV is sometimes referred to as the

Performance Measurement Baseline (PMB). Total PV for the project is also known at Budget At Completion (BAC)

• Earned Value (EV). A measure of work performed expressed in terms on the budget authorized for that work. EV

measured needs to be related to the PMB and it cannot be greater than the authorized PV budget for a component.

It’s often used to calculate the percent complete of a project.

• Actual Cost (AC). The realized cost incurred for work performed on an activity during a specific time period. It is

the total cost incurred in accomplishing the work that the EV measured. The AC needs to correspond in definition to

what was budgeted in the PV and measured in the EV. AC has no upper limit; whatever spent to achieve EV will be

measured.

Variances from the approved baseline will also be monitored:

• Schedule Variance (SV). – SV = EV – PV

A measure of schedule performance expressed as the difference between the Earned Value (EV) and the Planned

Value (PV)

EVM (Earned Value Methodology) is a useful metric that can indicate when a project is falling behind or is ahead of

its baseline schedule. The EVM schedule variance will ultimately equal zero when the project is completed because

ALL the Planned Value will have been Earned. It is best used in conjunction with Critical Path Methodology (CPM)

• Cost Variance (CV). – CV = EV – AC

The amount of budget deficit or surplus at a given point in time, expressed as the difference between Earned Value

(EV) and the Actual Cost (AC)

The cost variance at the end of the project will be the difference between the Budget At Completion (BAC) and the

Actual amount spent. The CV is very critical because it indicates the relationship of physical performance to the cost

spent. A Negative CV is often difficult for the project to recover.

• Schedule Performance Index (SPI) – SPI = EV/PV

A measure of efficiency expressed as the ratio on Earned Value to Planned Value. An SPI value of LESS than 1.0

means that it is behind schedule and GREATER than 1.0 means that it’s ahead of the schedule

• Cost Performance Index (CPI) – CPI = EV/AC

A measure of cost efficiency of budgeted resources, expressed as ratio between Earned Value to Actual Cost. A CPI

value of LESS than 1.0 means that it is Over Budget and GREATER than 1.0 means that it’s Under Budget

2. ForecastingAs the project progresses, the PM may develop a forecast for the Estimate At Completion (EAC) that may differ from the

Budget At Completion (BAC) based on performance. If the BAC is deemed no longer viable, the forecasted EAC will be

used.

EACs are typically based on actual cost incurred, plus an Estimate to Complete (ETC) the remaining work.

The most common EAC forecasting approach is a manual bottom-up summation by the PM & the project team.

EAC = AC + Bottom-Up ETC

Three common methods of calculating EAC are:

• EAC forecast for ETC work performed at the budgeted rate: Accepts the actual project performance to date as

represented by the actual costs & predicts that ALL future ETC work will be accomplished at the budgeted rate.

When actual performance is unfavorable, the assumption that future performance will improve should be accepted

only when supported by risk analysis.

EAC = AC + (BAC – EV)

• EAC forecast for ETC work performed at the present CPI: Assumes what the project has experienced to date can be

expected to continue in the future.

EAC = BAC / CPI

2. Forecasting

3. To Complete Performance Index (TCPI)

4. Performance Reviews

5. Project Management Software

6. Reserve Analysis

PROJECT DOCUMENTS

UPDATES

PROJECTFUNDING

REQUIREMENTS

COSTBASELINE

Approved version of the time-phased project budget (excluding any management reserves) that can only be changed via formal change control procedures. It is used as a basis for comparison to actual results.

Project Documents that may be updated include, but not limited to:Risk Register, Activity Cost Estimate, and Project Schedule

Derived from the cost baseline that include projected expenditures plus anticipated liabilities. Funding are incremental, not continuous and may not be distributed evenly

Pro

ject

Bu

dg

et

Cost

Baselin

e Contr

ol

Accounts

Work

Pa

cka

ge

Cost E

stim

ate

s

Activity

Cost

Estim

ate

s

Manage

ment

Reserve

sContingen

cy

ReservesActivity

Contingency

Reserves

Tota

l Am

ount

Project Budget Component