Embed Size (px)

Citation preview

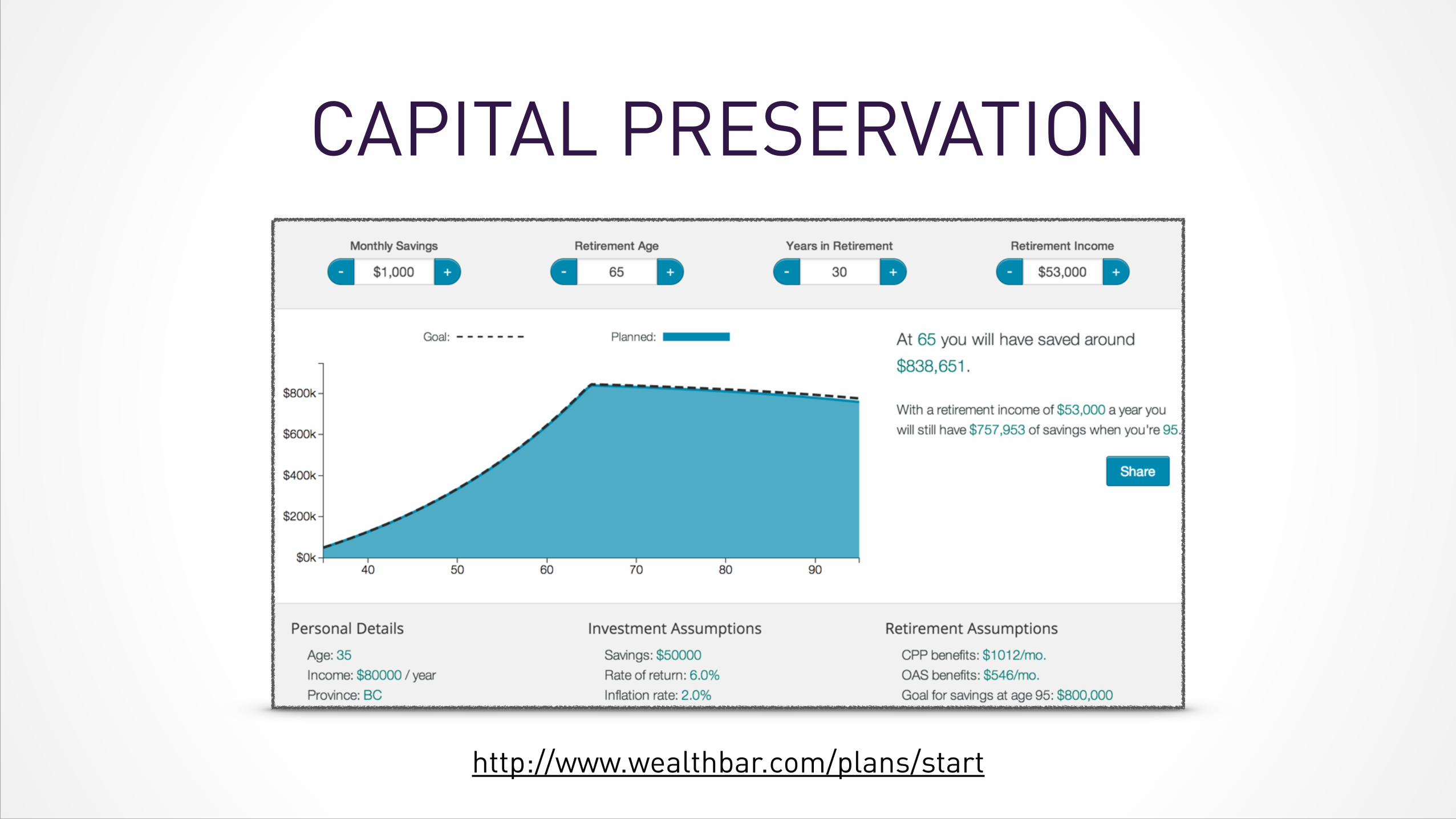

PERSONAL FINANCE 101brought to you by

Accumulation Income

Retirement Estate

RENTING VS OWNINGWho will win?

http://www.qwantz.com/index.php?comic=1636

MYTH #1“Real Estate is a superior long-term investment”

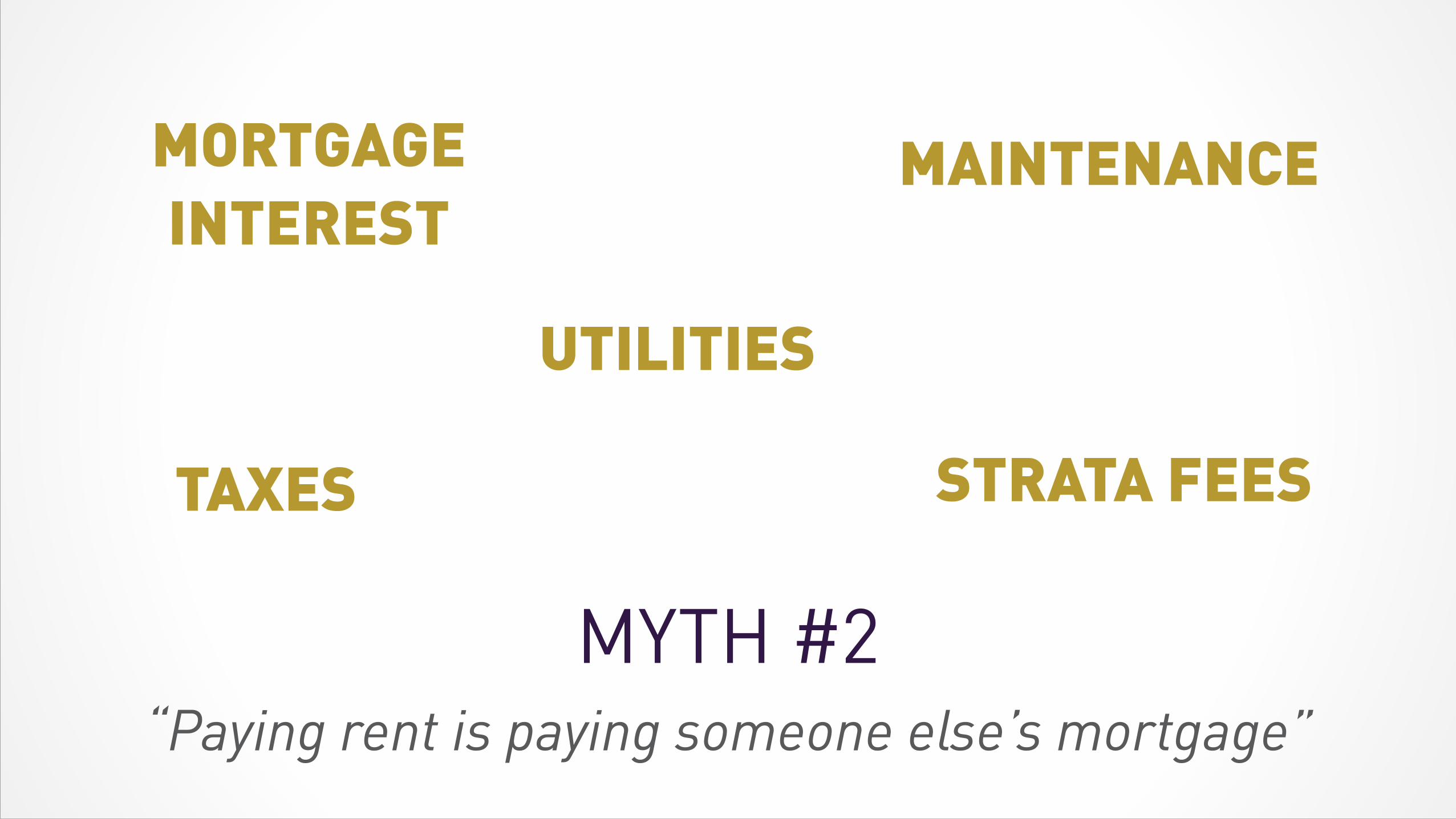

MYTH #2“Paying rent is paying someone else’s mortgage”

MAINTENANCE

UTILITIES

MORTGAGE INTEREST

STRATA FEESTAXES

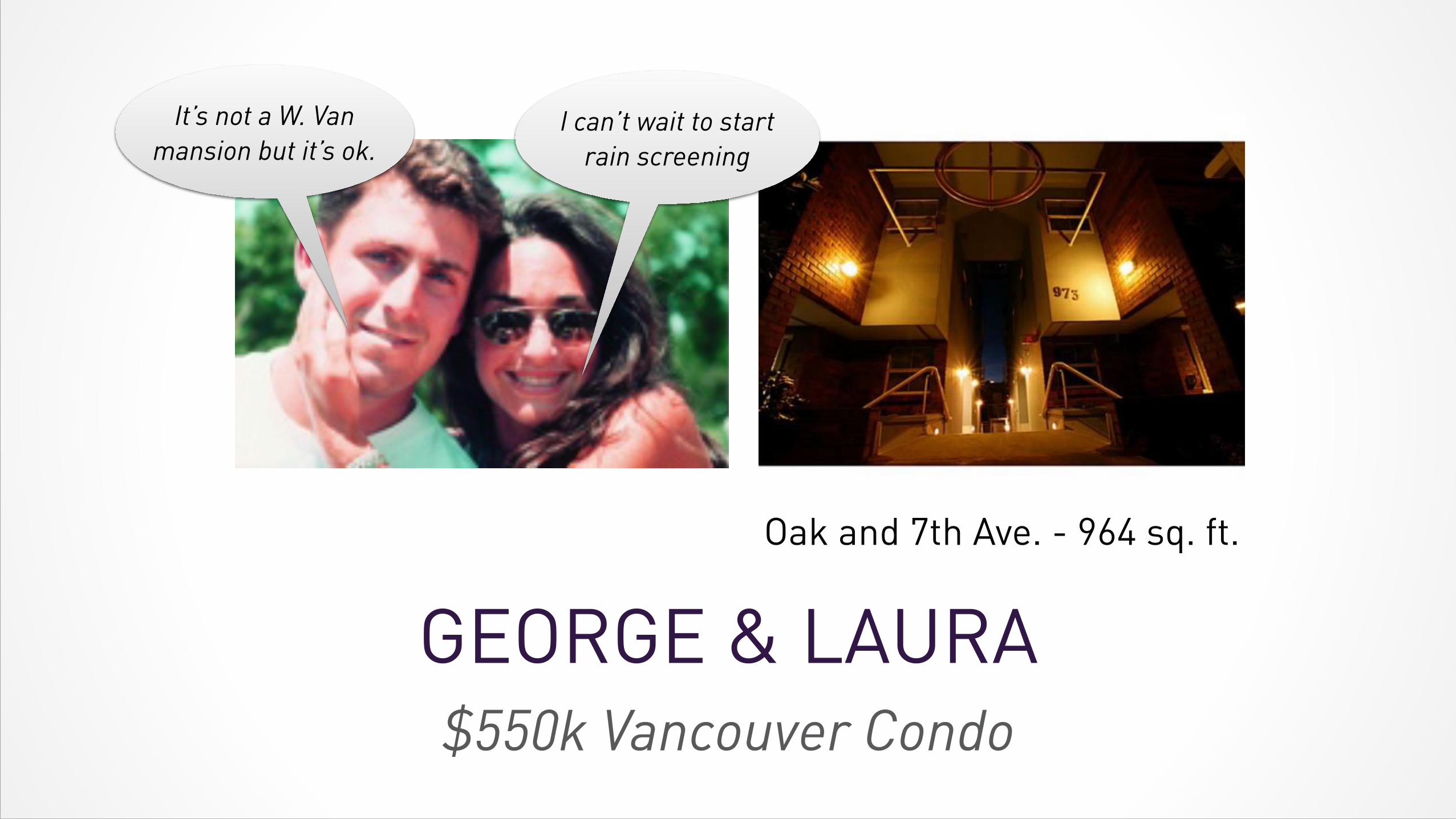

GEORGE & LAURA$550k Vancouver Condo

It’s not a W. Van mansion but it’s ok.

Oak and 7th Ave. - 964 sq. ft.

I can’t wait to start rain screening

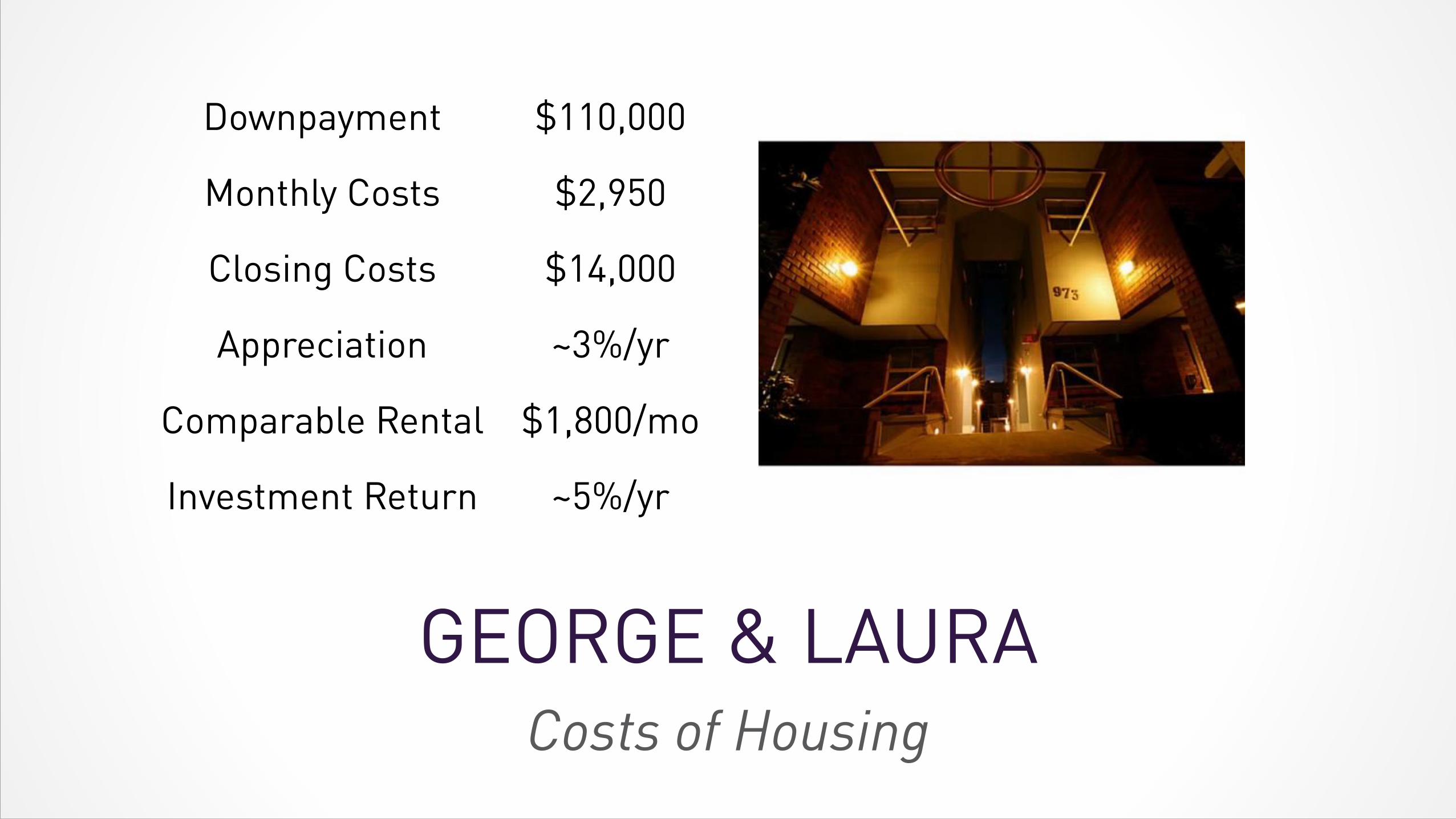

GEORGE & LAURACosts of Housing

Downpayment $110,000

Monthly Costs $2,950

Closing Costs $14,000

Appreciation ~3%/yr

Comparable Rental $1,800/mo

Investment Return ~5%/yr

GEORGE & LAURA10 Years Later

Owning Renting

Home $740k

Mortgage ($302k)

Closing Costs ($29k)

Investments $383k

Total $409k $383k

Difference $26k

INSURANCEWhat is it good for!?

http://www.qwantz.com/index.php?comic=1349

WHEN YOU NEED INSURANCE

Marriage

Children

New Home

WHY YOU NEED INSURANCE

Covering Debts Replacing Income

HOW MUCH IS ENOUGH?

George Laura

Income $35,000 $90,000

Mortgage $440,000

Children None

Coverage $500k (T-10) @ $31/mo

$1,150k (T-10) @ $59/mo

ADVANCED NEEDS

• Tax owing at death

• Charitable giving

• Estate equalization

• Legacy

COST OF INSURANCE

Smoker Status

Gender

$$$ Size of Benefit

Health

COST OF INSURANCE

$0#

$5,000#

$10,000#

$15,000#

$20,000#

$25,000#

$30,000#

$35,000#

$40,000#

34# 39# 44# 49# 54# 59# 64# 69# 74# 79# 84#

Age$34$Male$–$Mortality$Curve$

TERM

$0#

$5,000#

$10,000#

$15,000#

$20,000#

$25,000#

$30,000#

$35,000#

34# 44# 54# 64# 74#

VS. PERM

DISABILITY

• Some statistics on LTD

• 8 times more likely than dying

• 12 times more likely than a serious auto accident

• 22 time more likely than a house fire

• Average duration of LTD

• 2.6 years @ age 25

• 4.9 years @ age 55

The ability to work is your greatest asset• 42% chance of needing long term disability (90+ days) by age 65

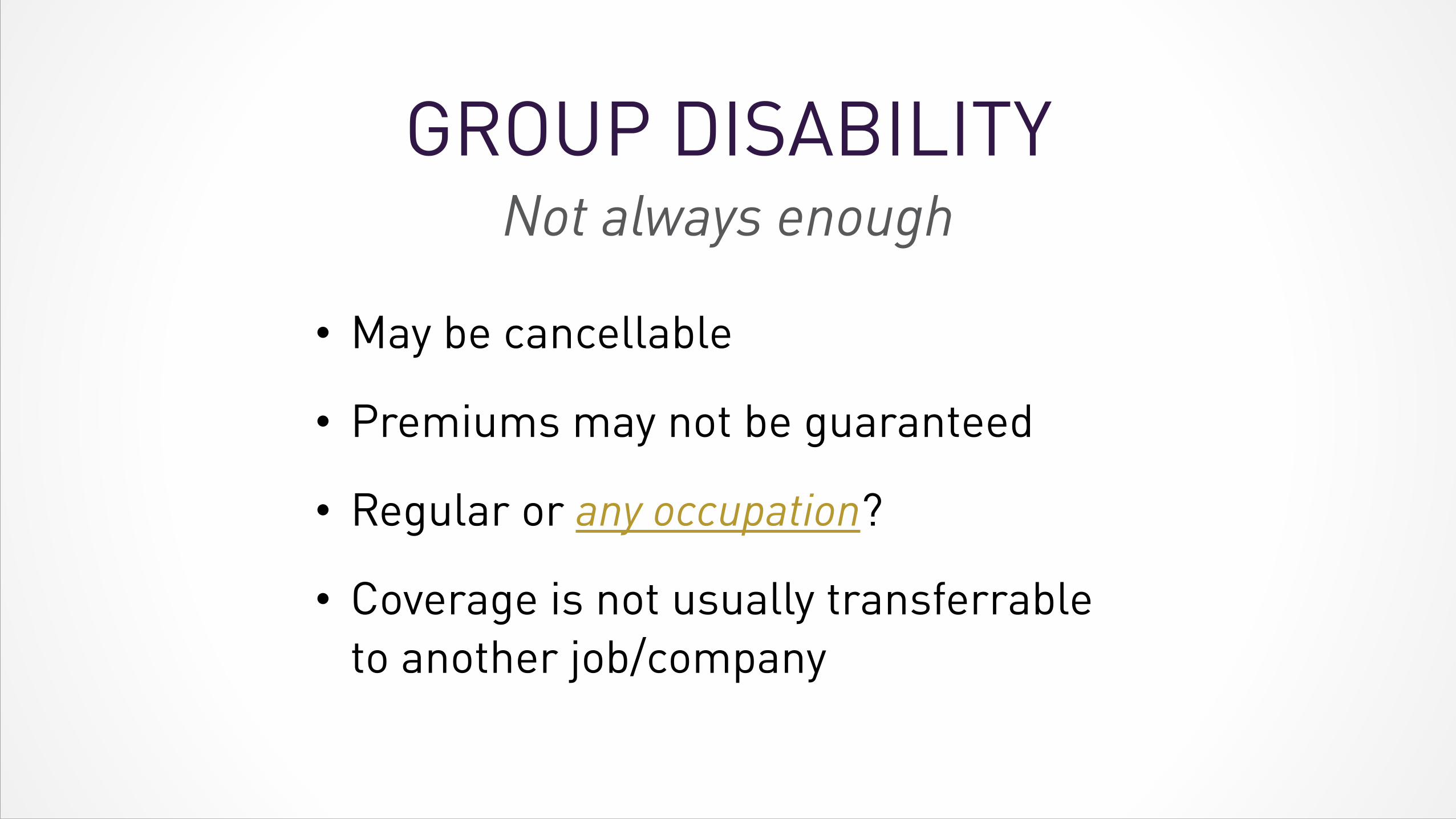

GROUP DISABILITYNot always enough

• May be cancellable

• Premiums may not be guaranteed

• Regular or any occupation?

• Coverage is not usually transferrable to another job/company

THE PRICE OF ADVICEWho is your advisor and what do they do?

http://www.qwantz.com/index.php?comic=1076

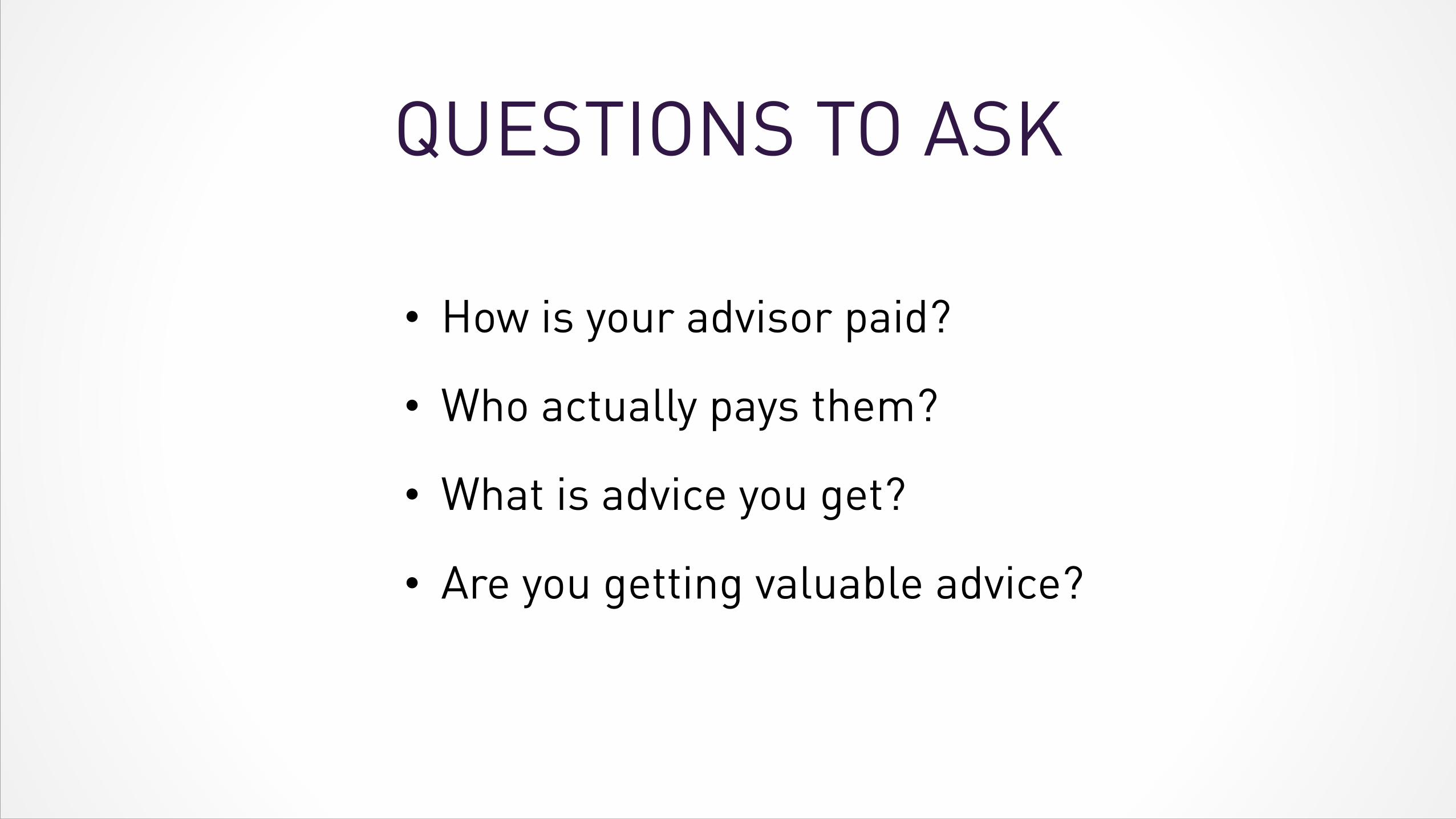

QUESTIONS TO ASK

• How is your advisor paid?

• Who actually pays them?

• What is advice you get?

• Are you getting valuable advice?

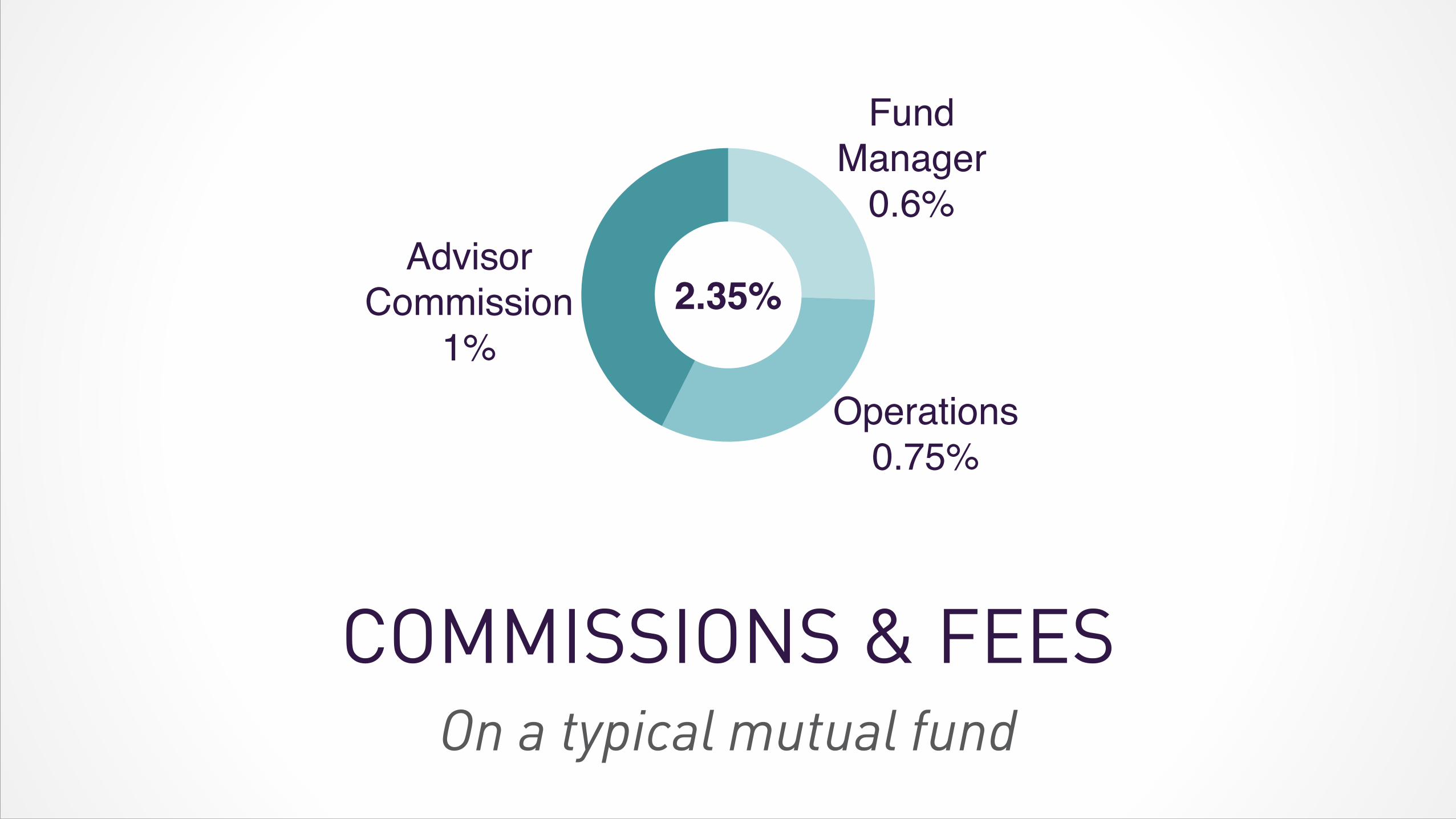

COMMISSIONS & FEESOn a typical mutual fund

Stocks 60%

Bonds 35%

Cash 5% 5% Cash

60%!Stocks

35%!Bonds

COMMISSIONS & FEESOn a typical mutual fund

Advisor!Commission!

1%

Fund!Manager!

0.6%

Operations!0.75%

2.35%

WHO WORKS FOR WHOM?Seeks advice

Recommends investment

Provides investment

and pays advisor

WHO WORKS FOR WHOM?

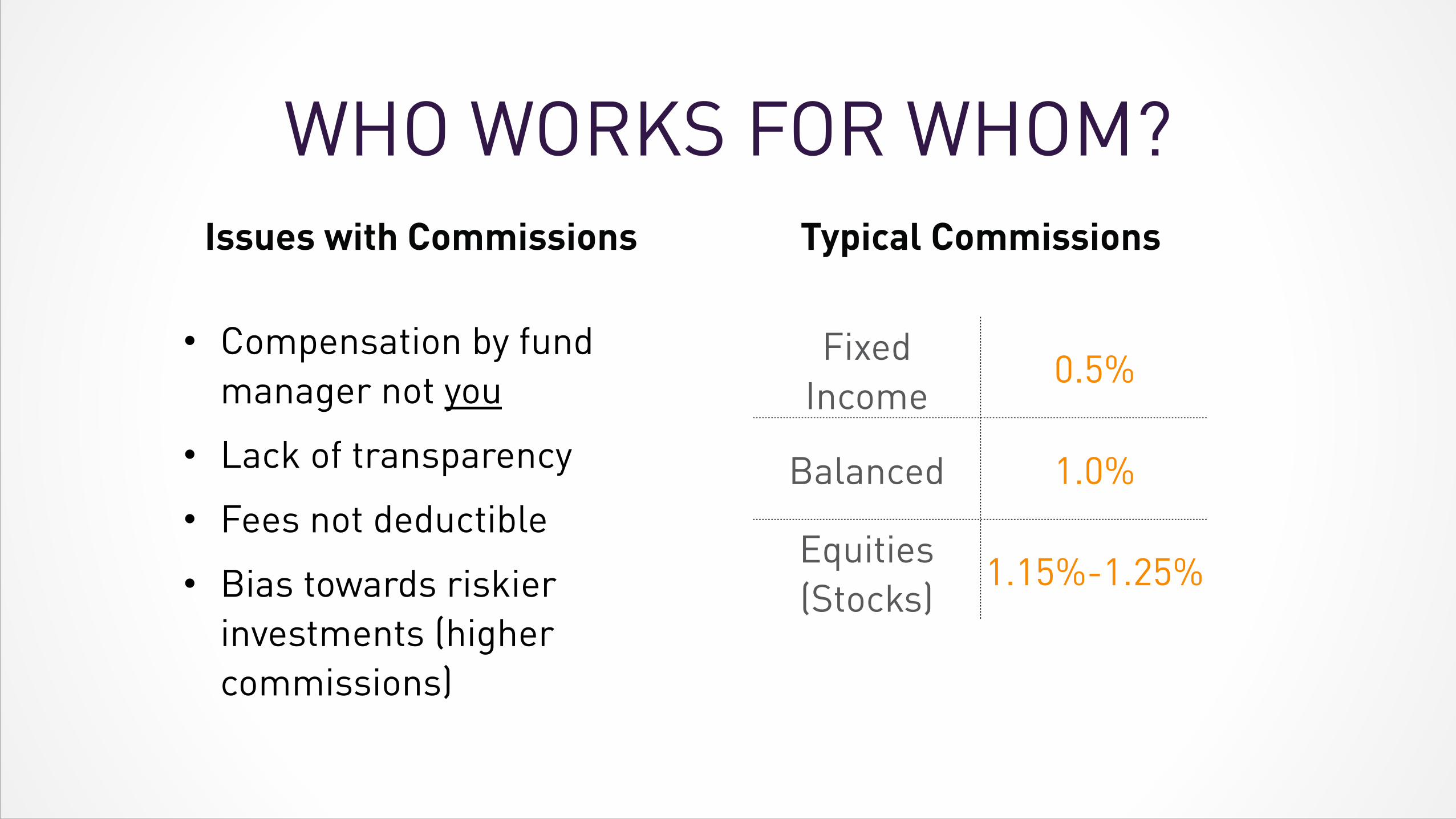

Fixed Income (Bonds)

0.5%

Balanced 1.0%

Equities (Stocks)

1.15%-1.25%

• Compensation by fund manager not you

• Lack of transparency • Fees not deductible • Bias towards riskier

investments (higher commissions)

Issues with Commissions Typical Commissions

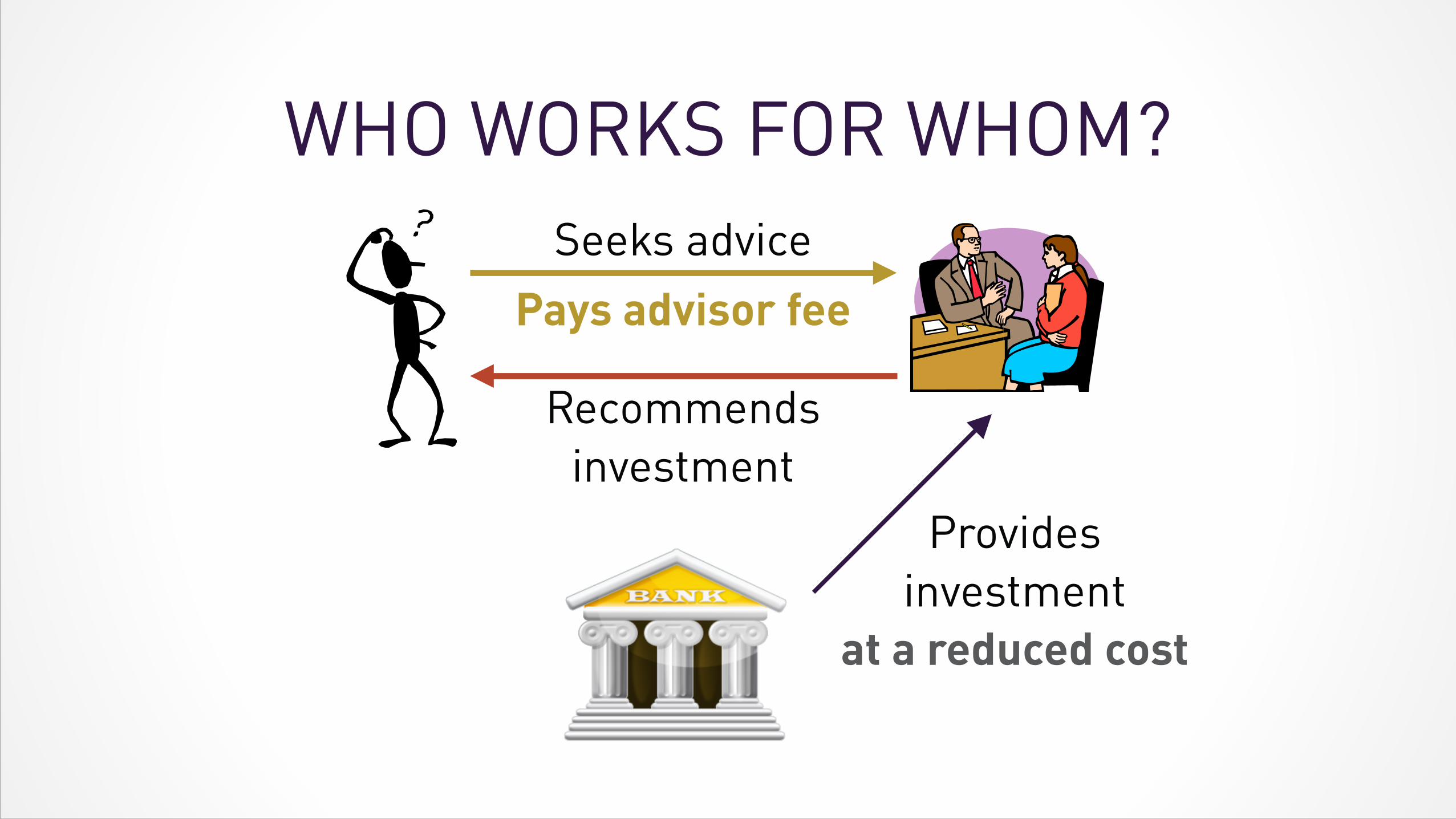

WHO WORKS FOR WHOM?Seeks advice

Recommends investment

Provides investment

at a reduced cost

Pays advisor fee

FEE BASED ADVISOR• Charge fees directly based on assets managed

(0.5-2.0%)

• Forgo or refund trailers and commissions (only get paid once)

• More transparency

• Less biased investment recommendations

• Bonus: Fees can be tax deductible

THE ADVISOR WORKS FOR YOU NOT THE BANK

WHO WORKS FOR WHOM?which is better?

• Both advisors earn a fee

• Fee-based is less common for smaller portfolios (for now…)

• What to look for…

• Proper accreditation (CFP, CIM, CFA)

• Transparency: Shows you your track record

• Just investment advice or holistic financial planning?

DOING YOUR RESEARCHOnline Research Tools

DOING YOUR RESEARCHVolatility and Risk

DOING YOUR RESEARCHFees and Costs

DOING YOUR RESEARCHStrategy

THANKS FOR COMINGQuestions?