Embed Size (px)

Citation preview

ACCOUNTING CYCLE

The Accounting Cycle is a series of steps, which are repeated every reporting period. The process starts with making accounting entries for each transaction and goes through closing the books. This Involves recording transactions in the daybooks, posting them to ledger, extracting a trial balance and finally drawing up financial statements. Step 1: Recording Transactions in Daybooks Each transaction is recorded first in one of the following daybook ( book of original entry) according to the nature of the transaction. 1. All goods sold on Credit ( Credit Sales) ….> Sales Daybook 2. All goods purchased on Credit (Credit Purchases) ….> Purchases Daybook 3. All goods sold on credit but now returned by costumers ..> Sales Return (Inwards) Daybook 4. All goods purchased on credit but now returned to suppliers…> Purchases Return Daybook The above four daybooks only record credit transactions related to movement in inventory. There are no accounts maintained inside the daybooks. It Just contains Date, Name, Source document number and Amount. 5. All transactions which relate to receipts and payments through cash or cheque ..> Cashbook Cash and Bank accounts are made inside the cashbook hence it also serves the purpose of ledger. 6. All other transactions …..> General Journal In this we actually write the double entry of only those transactions which cannot be recorded in the above five daybooks. To name a few -‐ Non Current Assets Purchased or Sold on Credit -‐ Writing off Bad debts -‐ Entries for Provisions of doubtful debts and depreciation -‐ Adjustments for Prepaid and Owings -‐ Correction of Errors

Step 2: Posting Transactions In Ledgers A ledger is a book which contains accounts ( the actual T Accounts guys). There are three types of Ledgers. In each type we have different type of accounts. Advantages Of Dividing The Ledger:

1. It facilitates division of labour in the maintenance of ledger.

2. It becomes easy to locate errors in ledger accounts.

3. It helps the ledger clerks to complete their respective work in time with perfection.

4. It becomes easy to refer to any particular account.

Sales Ledger: This contains accounts of credit costumers ( people to who we sell goods on credit) – Trader Receivables At the end of the year all the account balances in the sales ledger are listed in a schedule which is called list of Trade receivables. This shows the individual account balances( closing) and also the total debtors which goes into the trail balance. Purchase Ledger: This contains accounts of credit suppliers ( people from whom we buy goods on credit) – Trader Payables At the end of the year all the account balances in the purchase ledger are listed in a schedule which is called list of Trade Payables. This shows the individual account balances( closing) and also the total creditors which goes into the trail balance. General Ledger: This contains all the other accounts. Like all expenses ,incomes ,provisions (literally all other accounts) Please remember Sales and Purchases accounts are in the General Ledger cause they are not our costumers or suppliers . Once all the transactions are posted all the accounts are balanced via inserting a balance C/d in all accounts.

Step 3 : Extracting a Trial Balance All the closing balances in the General Ledger along with the figure of total trade receivables and payables are listed in a trail balance. Debit balances and Credit Balances are listed separately side by side. The Sum of all Debits should be equal to sum of all credit balances. The trail balances is used to check the completion of the double entry. The trail balance will balance because

-‐ For each debit entry there is a credit entry ( vice versa) -‐ The sum of all debit entries is equal to the sum of credit entries

Step 4: Closing Entries with Year end Adjustments ( Details in following pages) After making the trail balance we also have to adjust for certain items. Remember only Incomes and Expenses are taken into account while calculating profit. These accounts are closed by transferring them to the income statement ( the Profit and Loss Account). This process is called Closing Entries. Some common adjustments are

-‐ Expenses and Incomes are adjusted for prepaid (advance) and accruals(Owings) -‐ Non Current Assets are depreciated -‐ Provision for doubtful debt is adjusted -‐ Closing inventory is valued by physical stock take and it is adjusted in

calculating cost of goods sold and also for Balance Sheet -‐ Adjustments for goods withdrawn by owner or Stock Losses

Step 5 : Final Accounts: An income statement ( Trading Account till Gross Profit and Profit and Loss Account tiill Net Profit) and Balance Sheet is drawn which ends the Accounting Cycle. Now by looking at Income Statement owner can check his Profit and by looking at the Balance Sheet he can check his Net worth of the Business.

BUSINESS DOCUMENTS 1. Invoice: Whenever there is a credit sale, the selling business will send a document to buyer showing full details of the goods sold. This document is called as Invoice. It is known to the buyer as a “Purchases invoice”. And to the seller as a “Sales invoice”.

Note: Entries in the sales book and the purchases Book are made with the help of an invoice.

2. Debit Note: This document is prepared by the purchaser and it is sent to the

supplier to report him if any faulty goods are been sent or shortages or overcharges are been made.

3. Credit Note: When goods are returned, or there has been an over-‐charge, a supplier may issue a credit note to the buyer. This reduces the amount owed by the customer. Note: This document is used to make the entries in both the purchases returns Book and the sales returns Book.

4. Statement of Account: This document is prepared and sent to the customer by the supplier. It is issued to remind the customer about his due amount. It is basically a summary of the transaction of a customer during the month like sales made, Returns received and Cash received

DISCOUNTS 1. Trade Discount: It is an allowance or deduction given by the supplier to the retailer on the catalogue price or list price.

It is given to encourage him to buy in bulk.

It is given so that retailer could make some profit.

Note: It is not recorded in the books either by the seller or the buyer.

2. Cash Discount: It is an allowance or deduction given by the receiver of cash to the payer of cash for prompt payment. It is of two types discount allowed and discount received.

i. It is given to encourage the payer to pay on or before the due date.

ii. Note: This discount is recorded in the Cash Book. Discount allowed is recorded at the debit side and discount received on the credit side.

iii. Note: Discount columns are never balanced. It is just totalled.

ADJUSTMENTS IN DETAIL BAD DEBTS AND PROVISION FOR DOUBTFUL(BAD) DEBTS What is a bad debt? When a costumer to whom goods were sold on credit basis, is unable to pay his debt then it results into an expense for the business. Selling goods on credit basis involves this risk of bad debt. Any amount of debt which becomes irrecoverable should be written off as bad debt. Debit: Bad Debts Credit : Person Who is Bad :>/Trade receivable What is a Provision for bad debt? A business must consider that some costumers might not pay the amount owed by them; these debts are considered to be doubtful. Since the business does not know the exact amount of the doubtful debts( and also which costumer might not pay), an estimate for such amount is kept in a provision for doubtful debt account ( this account is not an expense account, it’s a reduction in asset from the balance sheet). Provision is created to reduce profit now for an expense which might happen in future. This is done to be pessimistic , in Accounting we call this being prudent or the Prudence Concept. How is the amount of provision estimated? ( Factors effecting it)

-‐ Age of Debts ( Since how long they owe us), higher the age more likely bad debts ( so high provision is kept If majority of the debts are owed for long)

-‐ Historical percentage of actual bad debts from previous years -‐ Reputation of people who us money in the market -‐ Nature of Business

What is the difference between accounting treatment of Provision for doubtful debts and the actual Bad debts? The Journal entry for provision: To create / Increase Debit : Profit and Loss Credit : Provision for doubtful Debts To Decrease Debit : Provision for doubtful debts Credit : Profit and Loss

The difference in accounting treatment is that the whole of bad debt is treated as an expense but only the change in provision is treated as either an expense (if increasing) or an income ( if decreasing). When we write off a bad debt, we remove the debtor from our books but in case of a provision we don’t adjust the debtor account as a separate account is maintained.

ACCOUNTING FOR NON CURRENT ASSETS Whenever we spend money we call it expenditure. The expenditure can be divided in two

Capital Expenditure Revenue Expenditure

Any expenditure incurred on buying new non-‐current asset. We take this to balance Sheet

Any day to day expense to run the business. We take this to income statement

Usually one off (doesn’t happen on daily basis)

Its recurring in nature ( we have to do it again and again)

Includes initial expenses incurred till we start using the asset e.g. Installation, delivery charges

Usually occurs after we start using the asset

Increases the value of earning capability of the asset e.g. Adding a Safety device

Maintains the value or earning capability of the asset. E.g. Repainting or Repair

In the same way we can have Capital receipts and Revenue Receipts . Capital Receipts would include money received from capital transactions e.g. taking a bank loan , selling a non current asset or additional capital introduced by the owners ( note this money coming in not earned by the business from profits) Revenue Receipts are incomes generated from day to day operations of a business ( taken to income statement) e.g. Sale of goods , Interest received rent received If these expenditures and receipts are treated in the wrong way then both income statement and balance sheet will be wrong.

Depreciation

This is an expense recorded to allocate a non current asset cost over its useful life. Deprecation is used in accounting to try to match the expense of an asset to the income that the asset helps the business to earn. For example if a business buys a piece of equipment for $1 million and expects to use it over a life of 10 years, it will be depreciated over 10 years . Every accounting year, the company will expense $100000 (assuming straight line , which will be matched with the money that the equipment helps to make each year. The Double Entry for Depreciation is : Debit : Profit and Loss Account ( Income Statement) Credit : Provision for Depreciation

Methods of Depreciation:

1. Straight Line : An equal amount of deprecation is charged every year. It is always calculated on cost . In case of scrap value (residual value) and life given use : Cost –Scrap/Life

2. Reducing Balance Method: In this deprecation for initial years in always higher then the later years. It is simply a percentage on net book value (written down value) . Net Book value represents cost minus total deprecation till date.

3. Revaluation Method:

This is usually used for loose tools ( or any asset which can only be valued collectively) . In this method at the end of the year the market value is estimated. A numerical example best explains this At the start of the year Loose Tools Valued at $5000 During the year Loose Tools purchased = $2000 Loose Tools Sold = $300 At the End Loose tools are worth $4500 Deprecation = 5000 + 2000 – 300-‐ 4500 = 2200 Opening Value+ Purchased –Sold – Closing Value Which Method is best to use? It depends on the nature of Non Current Asset

Straight Line method is appropriate for assets like office furniture and fittings (which are used evenly through out the year useful life, and the efficiency of them doesn’t fall by great amount in initial years) Reducing Balance Method is appropriate for assets like machinery or van. Since these assets are more efficient when new, more depreciation is charged in initial years. As the asset gets old it looses efficiency and so we charge less deprecation. Another way to look at it is that the maintenance and repairs of asset will increase in later years so to maintain the overall expense it makes sense to charge more depreciation in initial years when maintenance is low and then reduce it as maintenance increases. How to record disposal of Asset: Disposal of means getting ride of the fixed asset . it can be sold or may be stolen or just discarded. Usually there are 4 entries to record sale of asset

1. Remove the Cost of the Asset Sold Debit : Disposal Credit: Asset

2. Remove the Total Deprecation

Debit : Provision for Depreciation Credit : Disposal

3. Record the Selling Price Debit: Bank Credit : Disposal If exchanged then Debit : Asset Credit Disposal

4. Close the Disposal Account

Close with income statement

BANK RECONCILIATION STATEMENTS Cashbook is owner’s record (Debit means + balance, Credit means – balance) Bank statement is bank’s record (Credit means + balance, Debit means – balance) Some entries which are recorded in the bank statement but not in the cashbook: For these, we will have to correct the cashbook

1. Credit transfer (Bank Giro): Money deposited by customer directly in the bank account (We should add it to cashbook balance)

2. Standing order/ Direct Debit: Money paid to supplier directly by the bank. (We should subtract this from cashbook balance)

3. Bank Charges/ Interest Charged: Money deducted directly by the Bank. (We should subtract this from cashbook balance)

4. Interest Received/ Dividends Received: Money added to the bank account in form of interest or dividend (We should ad it to the cashbook balance)

5. Dishonored Cheque: A cheque received from customer but not acknowledged by the bank (We should subtract this from cashbook balance because we need to cancel the entry made when the cheque was received).

Some entries which are recorded in the cashbook but not on the bank statement. For this, we will have to correct the bank statement:

1. Unpresented Cheque: Cheques written by us to a creditor but not yet presented to

the bank for payment, so the bank has not deducted money from our account. (We should subtract this from bank statement balance)

2. Uncredited Cheque (Lodgments): Cheques received by us but not yet deposited in the bank, so the bank has not increased the bank balance. (We should add this to the bank statement balance)

FOR MCQ’s remember

Balance as per Bank statement + Uncredited Cheques – Unpresented Cheques = Balance as per corrected Cashbook.

If balance as per corrected cashbook is given in the question, simply ignores the entries which will affect the cashbook balance. If there is an overdraft (for either cashbook or bank statement), take it as a negative figure in the equation.

Reasons For Preparing bank Reconciliation Statement:

To ensure that the cash book entries are complete.

To discover bank errors.

To discover errors in cash book.

To check Fraud and embezzlement.

To discover dishonoured cheques.

CONTROL ACCOUNTS What is the difference between Sales Ledger and Salas Ledger Control Account? Sales ledger is where we make individual accounts of credit customers. It is part of double entry system and it gives details of amounts owing by each customer. A list of debtors is extracted from the sales ledger, which gives the figure of debtors for the trial balance. Sales ledger control account on the other hand is the total debtors account in the general ledger. It is not part of the double entry system. It I often referred as total debtors account. All the entries recorded here are totals taken from daybooks e.g. Sales figure is the total of the sales daybook, discount allowed is total discount allowed from the discount allowed account or the column in the cashbook. USES OF CONTROL ACCOUNT

1. Helps to prevent fraud 2. Helps to detect errors 3. Quickly provide figures of total debtors and creditor.

LIMITATIONS OF CONTROL ACCOUNT 1. Cant trace error of omission 2. Cant trace error of original entry

Note: Sometimes it can happen that there is a small opening Debit balance on a purchases ledger control account in addition to the usual credit balance. It happens when the business has overpaid a creditor, or has returned the goods after paying the due amount.

Note: Sometimes sales ledger control account too also has small opening credit balance b/d on a sales ledger control account, in addition to the usual opening debit balance. It happens when a debtor has over paid his account or has returned goods after paying his account or due amount.

ERRORS AND SUSPENSE Error not affecting the Trial Balance:

1. Error of complete omission: When nothing has been recorded in the books. To correct this, simply record the transaction.

2. Error of original entry: Where correct double entry is passed but with the wrong amount. To correct this, adjust for the difference.

3. Error of principal: Where a wrong type of account has been debited or credited instead. For example, we have debited Rent instead of Motor Van.

4. Error of commission: Where a wrong account but of same type (usually debtors or creditors) has been debited or credited instead. For example, we have credited Mr. A instead of Mr. B.

5. Error of complete reversal: Where a completely opposite entry is passed with the right amount. To correct this, pass the correct entry with double amounts.

6. Compensating error: Where one error compensates for other. Like a debit item (say purchase) and a credit item (say sales) are both undercast with same amounts. (don’t worry about this too much :P)

All the above errors do not affect the Trial Balance because in all situations the total debits are equal to total credits. Errors can be made which can lead to disagreement of the trial balance. This is when either we have only debited something and forgot to credit (Incomplete double entry) or we have debited something with a correct amount and credited the other with the wrong amount (Incorrect double entry). And it can also happen if any daybook is over or under cast. E.g. Sales daybook is undercast. In these situations Suspense account comes into the picture. Since sales daybook is undercast, this means only the total sales were wrong (understated), so we need to amend the sales accounts. Debit: Suspense Credit: Sales Errors affecting Profit or Loss

These errors affect those accounts which are included in the Trading and Profit and Loss Account eg purchases, sales, expenses etc. We must ask the following questions:

1) Does the error affect the gross profit, the net profit or both? (a) Errors which affect items that go into the trading account affect gross profitand net profit to the same extent and in

the same direction. Such items aresales, purchases, returns, stock, carriage inwards etc. (b) Errors which affect items that are entered in the profit and loss section of theaccount, i.e. operating expenses, affect only net profit. Purchases of fixed assets affect profit only indirectly through provisions for depreciation.

2) In what direction is profit affected?

(a) If sales are overstated or purchases understated, both gross profit and netprofit are too high and must be reduced by the relevant amount. The sameapplies if sales returns are understated or purchases returns overstated.

(b)If sales are understated or purchases overstated, both gross profit and net profit are too low and must be increased by the relevant amount. The sameapplies if sales returns are overstated or purchases returns understated.

(c) If miscellaneous receipts are overstated or if expenses are understated, gross profit is not affected but net profit will be high and must be reduced.

(d) If miscellaneous receipts are understated or if expenses are overstated, again gross profit is not affected but net profit is too low and must be increased.

(e) If capital expenditure is wrongly treated as revenue expenditure, eg if the purchase of a fixed asset is treated as an expense, then net profit will be too low and must be increased. The opposite applies if revenue expenditure is treated as capital expenditure.

3) Does the errors that affect items in the balance sheet affect profit as well?

The answer is only those that were adjusted after the trial balance was prepared. Errors affecting fixed assets, current assets and liabilities do not normally affect profit but if one of these items has changed as a result of an adjustment, then profit is affected. For example:

. (a) If the closing stock has been overvalued, the stock figure in the balance sheet is too high and so are the gross profit and the net profit. The opposite is true of a closing stock which is undervalued. Remember that closing stock adds on to gross profit and opening stock takes away from it.

. (b) If an accrued or prepaid expense is the wrong amount, both profit and the item in the balance sheet are wrong. If an amount owing is overstated or a prepayment is understated, profit is too low and must be increased, and vice versa.

. (c) The opposite to (b) applies in the case of accrued or prepaid receipts.

Estimating the effects of errors can be confusing and you must keep a clear mind. Think how the original figure has affected profit and then try to see in which direction the error is affecting the profit.

INCOMPLETE RECORDS: Remember Net profit can be calculated using the following formula. If a question says make a trading profit and loss account, than this doesn’t apply. Only when it says to calculate net profit or make a statement showing net profit. Opening Capital + Additional Capital + Net profit – Drawings = Closing Capital (I really hope you can solve for net profit), don’t memorize the formula, it’s the financed by section. J For the final account questions (where the trading, profit and loss account and a balance sheet is required), always make the following accounts. (By always, I mean always).

1. Sales ledger control account (If business only deals in cash sales, then don’t) 2. Purchase ledger control account 3. Bank account (if it is already given in the question, then it’s okay)

Once you have filled in your accounts, and then move to the Final accounts. Don’t panic if it doesn’t balance, because marks are for working. Don’t spend your entire lifetime on this question. NEVER NEVER NEVER forget depreciation. They will usually give you net book values at start and end. Depreciation = Opening NBV + Purchase of assets – Sale of assets (at NBV) – Closing NBV Also make expense accounts or adjust for prepaid and owings directly. But show all working. In your financed by section, you will need opening capital. This will come from Opening Assets – Opening Liabilities. Don’t forget to include the opening balance of the bank account in your calculation (like other idiots).

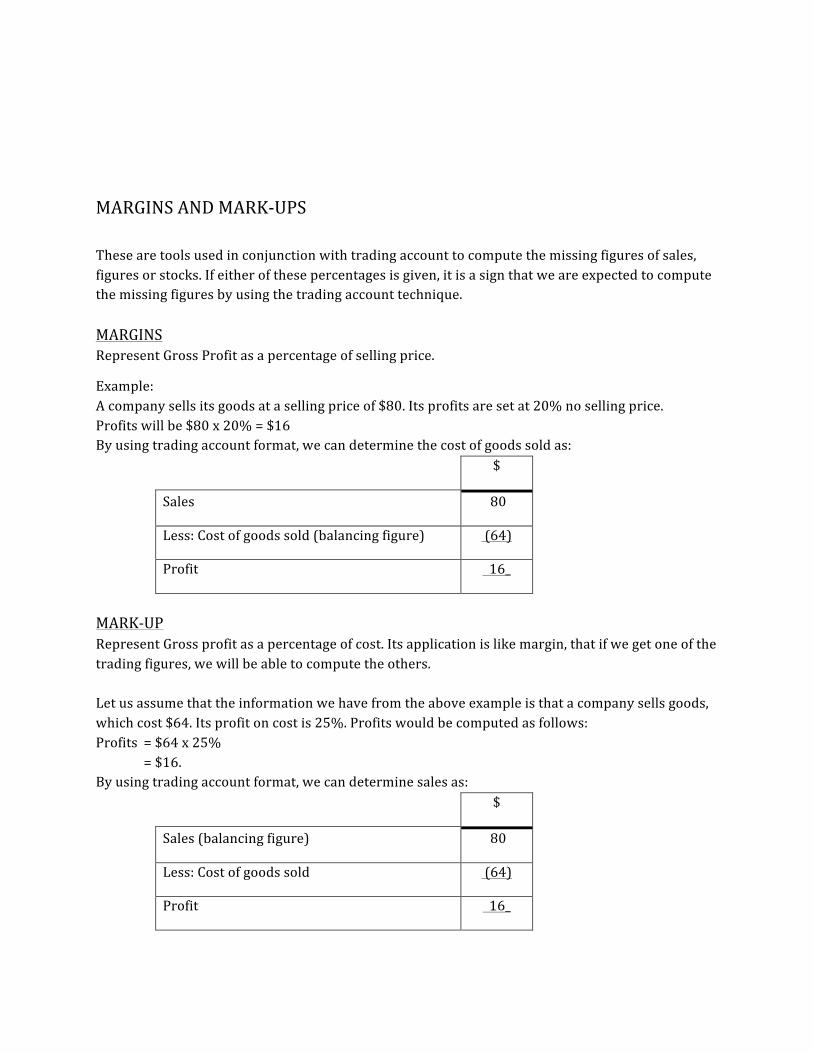

MARGINS AND MARK-‐UPS These are tools used in conjunction with trading account to compute the missing figures of sales, figures or stocks. If either of these percentages is given, it is a sign that we are expected to compute the missing figures by using the trading account technique. MARGINS Represent Gross Profit as a percentage of selling price.

Example: A company sells its goods at a selling price of $80. Its profits are set at 20% no selling price. Profits will be $80 x 20% = $16 By using trading account format, we can determine the cost of goods sold as:

$

Sales 80

Less: Cost of goods sold (balancing figure) (64)

Profit 16_

MARK-‐UP Represent Gross profit as a percentage of cost. Its application is like margin, that if we get one of the trading figures, we will be able to compute the others. Let us assume that the information we have from the above example is that a company sells goods, which cost $64. Its profit on cost is 25%. Profits would be computed as follows: Profits = $64 x 25% = $16. By using trading account format, we can determine sales as:

$

Sales (balancing figure) 80

Less: Cost of goods sold (64)

Profit 16_

Try to use Sales – Cost = Profit If Mark up if given Profit is a % of Cost and IF margin is given Profit is a % of Sales For eg. Sales = 80000 Cost = ? Margin = 25% Sales – Cost = Profit 80000-‐ x = 25 % of 80000 Cost = 60000 But if Sales = 80000 Cost = ? Markup =25% Sales – Cost = Profit 80000-‐ x = 25 % of X Cost = 64000

NON-‐PROFIT ORGANIZATION (CLUBS AND SOCITIES) The non-‐profit organization is with a view of providing services to its members. The aim is not to make profits out of trading activities, but to increase to welfare of members through social interaction and other activities. A club is owned by all the members collectively and since there is no single owner, there are no DRAWINGS. TERMINOLOGY DIFFERENCE Non-‐profit organizations Normal trading Businesses

Receipts and Payments Account Bank Account

Income and Expenditure Account Trading, Profit and Loss Account

Surplus Profit

Deficit Loss

Accumulated Funds Capital

Why is a Receipts and Payments Account unsatisfactory for the members? The receipts and Payments account does not provide information to the members relating to

1. Assets owned by the club 2. Liabilities owed by the club 3. Surplus or Deficit 4. Depreciation of fixed assets 5. Performance of the club 6. Financial position of the club.

In order to make the income and expenditure account, you will need to determine the incomes separately. Incomes may include:

-‐ Refreshment Profit/Bar profit (make a separate account to calculate net profit from this) -‐ Annual subscription (separate subscription account for this) -‐ Gain on disposal. -‐ Interest on deposit account or investment account. -‐ Profits from different events (say Dinner dance) -‐ Donations (only day to day)

Check debit side of Receipts and Payments account for anything else. What is the difference between receipts and payments account and Income and Expenditure account? Receipts and Payment account Income and Expenditure account

It shows balance of bank at start and end It shows Surplus of Deficit for the year

It records money coming in and going out It records Incomes and expenses incurred

It considers all type of money coming including capital receipts, e.g. Long term donations and all type of money going out, e.g. Purchase of fixed asset

It considers only revenue incomes and expenditure.

It is an alternative name for cashbook It is an alternative name for profit and Loss

What is a donation and what are two accounting treatments for it?

An amount received by a club which the club does not have to pay back. This includes donations, gifts, legacy and grants. If donation is for a day to day expenditure or will remain with the club only for a short period then it should be treated as an income in the income and expenditure account. If donation is for purpose of capital expenditure on long term assets, then it is shown as a special fund in the balance sheet. (Financed by section added it to accumulated funds).

PARTNERSHIP ACCOUNTS A partnership is defined by the Partnership Act 1890 as a relationship, which exists between two or more persons who carry business with a view of profit.

CHARACTERISTICS OF PARTNERSHIP • Partners are jointly and severally liable for the debts of the partnership. They have

unlimited liabilities for the debts of the partnership. • The minimum number of partners is usually two and maximum number is twenty,

with exception of banks, where the maximum number is fixed at ten and some professional practices where there is no maximum number.

• All partners usually participate in the running of their business. • There is usually a written partnership agreement.

THE PARTNERSHIP AGREEMENT The partnership agreement is a written agreement which sets up the terms of the partnership, especially the financial arrangements between the partners. The contents of the partnership agreement can vary from one partnership to another. A standard Partnership Agreement may include the following items:

1. The name of the firm, business type and duration 2. Capital contribution. 3. Profit sharing ratios. 4. Interest on Capital. 5. Partners’ salaries. 6. Drawings. 7. Interest on drawings. 8. Arrangements in case of dissolution, death or retirement of partners. 9. Arrangement for settling disputes.

In absence of a formal agreement between the partners, certain rules laid down by the Partnership Act 1890 are presumed to apply. These are:

1. Residual profits are shared equally between the partners. 2. There are no partners’ salaries. 3. No interest is charged on drawings made by the partners 4. Partners receive no interest on capital invested in the business. 5. Partners are entitled to interest of 5% per annum on any loans they advance to the business

in excess of their agreed capital.

ADVANTAGES OF PARTNERSHIP OVER SOLE TRADER

1. Additional capital from other partners, and also easier to get loans. 2. Additional expertise. 3. Additional management time. 4. Risk (losses) is shared.

DISADVANTAGES OF PARTNERSHIOP OVER A SOLE TRADER

1. Profit are shared 2. Possibility of disputes 3. Loss of control

What is a current account? Majority of partnership keep a fixed capital account, whenever they have fixed capital accounts, they will have to maintain a current account for each partner. By fixed capital account, we mean that all the appropriation and drawings will pass through a temporary capital account (current account), only additional investment by a partner will be recorded in the capital account. This gives information relating to long term and short term aspects separately. This also helps to determine the investment made by partner in the business. Some partnerships also maintain a fluctuating capital account; in this case they will not maintain a current account. All the transactions will pass through the capital account.

LIMITED COMPANIES Limited companies are business organizations, whose owners’ liabilities are limited to their capital contributed or guarantees made. CHARACTERISTICS OF LIMITED COMPANIES 1. Separate legal entity: A company is regarded as a separate person from its owners

and managers. As a result, it can sue or be sued, it can own property. This concept is often referred to as veil of incorporation.

2. Limited liability: Shareholders’ liability is limited to what they have paid for shares.

3. Perpetual succession: Unlike partnership and sole trader, a company does not cease to exist on the death or retirement of any of the owners. Owners can buy and sell their shares without affecting the running of the business.

4. Number of members: There is no limit as to the number of members

5. Capital: Company’s capital is raised through the issuance of shares

6. Profit distribution: Profits are distributed to members through dividends.

7. Retained profits: The retained profits are capitalized are reserves.

8. Legislation: Companies are highly regulated. They are required to comply with the requirements of Company’s ACT as well as Financial Reporting Standards.

ADVANTAGES OF OPERATING AS A LIMITED COMPANY:

1. The liability of the shareholders is limited. Therefore, in case of company going bankrupt, the individual assets of the owners will not be used to meet the company’s debts. Only shareholders who have only partly paid for their shares can be forced to pay the balance owing on the shares, but nothing else.

2. There is a formal separation between the ownership and management of the business. This helps in clearly identifying the responsible persons.

3. Ownership is vastly shared by many people, hence diversifying risk, and funds become available is substantial amounts.

4. Shares in the business can be transferred relatively easily. DISADVANTAGES:

1. Formation costs are normally very high. 2. Companies are highly regulated. 3. Running costs are also very high i.e. preparation and submission of annual returns, audit

fees etc. 4. Profit distribution is also subject to some restrictions. Not all surpluses from the business

transactions can be distributed back to the shareholders. 5. Company accounts must be available for inspection to the public.

There are two types of limited companies: 1. Public limited companies:

a-‐ They have the abbreviation Plc of public limited company at the end of their names b-‐ Their minimum allotted share is required to be £50 000. c-‐ They can invite the general public to subscribe for their shares d-‐ Their shares may be traded in the stock exchange i.e. they can be quoted with the stock

exchange. 2. Private limited companies:

a-‐ They have the abbreviation ‘Ltd’ for limited at the end of their names. b-‐ They are not allowed to invite general public for the subscription of their share capital.

COMPANY FINANCE As is a case with sole traders and partnerships, companies also have two main sources of finance, namely; capital and liabilities. The difference is on naming and classification of these terms. When the company is formed, it normally issues shares to be subscribed by the potential members. People who subscribe and buy company’s shares are known as shareholders, and they become the legal owners of the company depending in the proportion and type of shares they hold. They receive dividends as return on their invested capital. Dividends are, therefore, appropriations of the profits. On the other hand, the company can borrow funds from other people who are not owners. The main form of company borrowings is by issuing debenture, which is a written acknowledgement of a loan to a company, given under the company’s seal. The debenture holders are not owners of the company but they are liabilities. Debenture holders receive a fixed percentage of interest on the loan amount. Debenture interest is a business expense, which must be paid when is due. Other forms of borrowings include trade creditors and bank overdrafts. The difference between shareholders and debenture holders can be analyzed in terms of: 1. Ownership; and

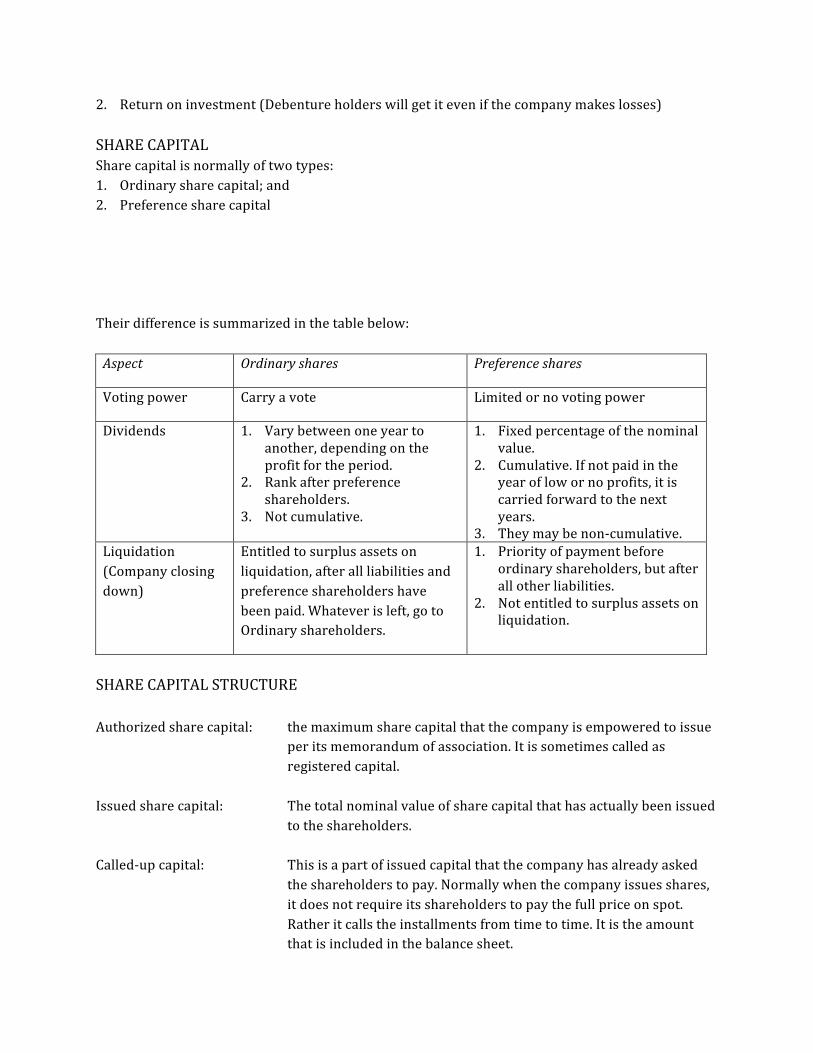

2. Return on investment (Debenture holders will get it even if the company makes losses) SHARE CAPITAL Share capital is normally of two types: 1. Ordinary share capital; and 2. Preference share capital Their difference is summarized in the table below: Aspect Ordinary shares Preference shares

Voting power Carry a vote Limited or no voting power

Dividends 1. Vary between one year to another, depending on the profit for the period.

2. Rank after preference shareholders.

3. Not cumulative.

1. Fixed percentage of the nominal value.

2. Cumulative. If not paid in the year of low or no profits, it is carried forward to the next years.

3. They may be non-‐cumulative. Liquidation (Company closing down)

Entitled to surplus assets on liquidation, after all liabilities and preference shareholders have been paid. Whatever is left, go to Ordinary shareholders.

1. Priority of payment before ordinary shareholders, but after all other liabilities.

2. Not entitled to surplus assets on liquidation.

SHARE CAPITAL STRUCTURE Authorized share capital: the maximum share capital that the company is empowered to issue

per its memorandum of association. It is sometimes called as registered capital.

Issued share capital: The total nominal value of share capital that has actually been issued

to the shareholders. Called-‐up capital: This is a part of issued capital that the company has already asked

the shareholders to pay. Normally when the company issues shares, it does not require its shareholders to pay the full price on spot. Rather it calls the installments from time to time. It is the amount that is included in the balance sheet.

Paid-‐up capital: This is the total amount of the money already collected from the

shareholders to date. Dividend is paid on this. Uncalled capital: This is the part of issued capital, which the company has not yet

requested its shareholders to pay for. Dividends: According to the new law, we only subtract the amount of dividends

paid from profit. Dividends which are announced are ignored. What is a Debenture? A debenture is a document containing details of a loan made to a company. Debentures carry the right to a fixed rate of interest . They are just treated like long term loans. What are the different Types of Preference Shares?

1. Non-‐cumulative Preference shares: In case company doesn’t pay enough profits, these shareholders will get no dividends in the year and that amount of dividend will never be given.

2. Cumulative Preference Shares: In case company doesn’t have enough profits, these shareholders will get no dividend in the year and that amount of dividend will be carried forward to next year, when the company makes enough profit, the entire amount will be payable as dividend.

3. Participating Preference Shares: These shareholders have limited voting right, i.e. they can participate in the decision making.

What is the difference between Debentures and Prefrence Shares? Debenture is Loan and Prefrence Shares are Capital (Owner) of the Business. Both get fixed rate of return( that is a similarity) but when no profits are available debenture interest still has to be paid whereas preference dividend can be saved or carried forward to next year.

GOODWILL Goodwill at time of purchasing A business: This is calculated whenever a business is purchased . The difference between purchase price and the market value of net assets (assets minus liabilities) acquired. It is the extra amount which business pays for an existing reputation of the business. It is treated as an intangible asset ( Non current) in the Balance Sheet Goodwill = Purchase Price minus Net Assets ( at market Value) Goodwill at the time of merger ( formation of partnership) When two sole traders combine to form a partnership business we also have to treat goodwill. The partnership will buy both individual sole trader businesses. Any extra amount placed on their businesses is treated as goodwill they bring into the business. There are two methods to treat this situation Goodwill is kept in the books: The individual goodwill is recorded on the credit side of partner’s capital account. The total value is then shown in the balance sheet as intangible non current assets. Goodwill is written off: The individual goodwill is recorded on the credit side of partner’s capital account. The total value is then debited to partners capital accounts in the profit sharing ratio, this is done to remove goodwill from the balance sheet. INVENTORY (WHAT IS NET REALIZABLE VALUE) This is simply the current market value of goods The amount of goods left unsold at the end of the year is known as Inventory. When calculating the value of inventory there is a special rule. If the market value of the inventory is higher then the price at which we bought it (cost) then we should record inventory at cost price. But if the market value is lower than the cost price then we should use the market value. For Example : I bought an Iphone 4 with an intention to sell at $400. This is my cost price. If the phone can be sold in the market for $500 in my balance sheet I will still record my closing inventory at $400 cause I bought it for $400 and it is still not sold. If I record it at $500 then I would be counting $100 profit which I have still not earn. Now consider the market value of the same phone was $300 ( because probably iphone 5 came out), now whenever I sell it I will have a loss of $100 , this should be reflected in my accounts and I would show the stock at $300. So a general rule is whichever is lower ( the cost price or market value) stock should be recorded at that price.

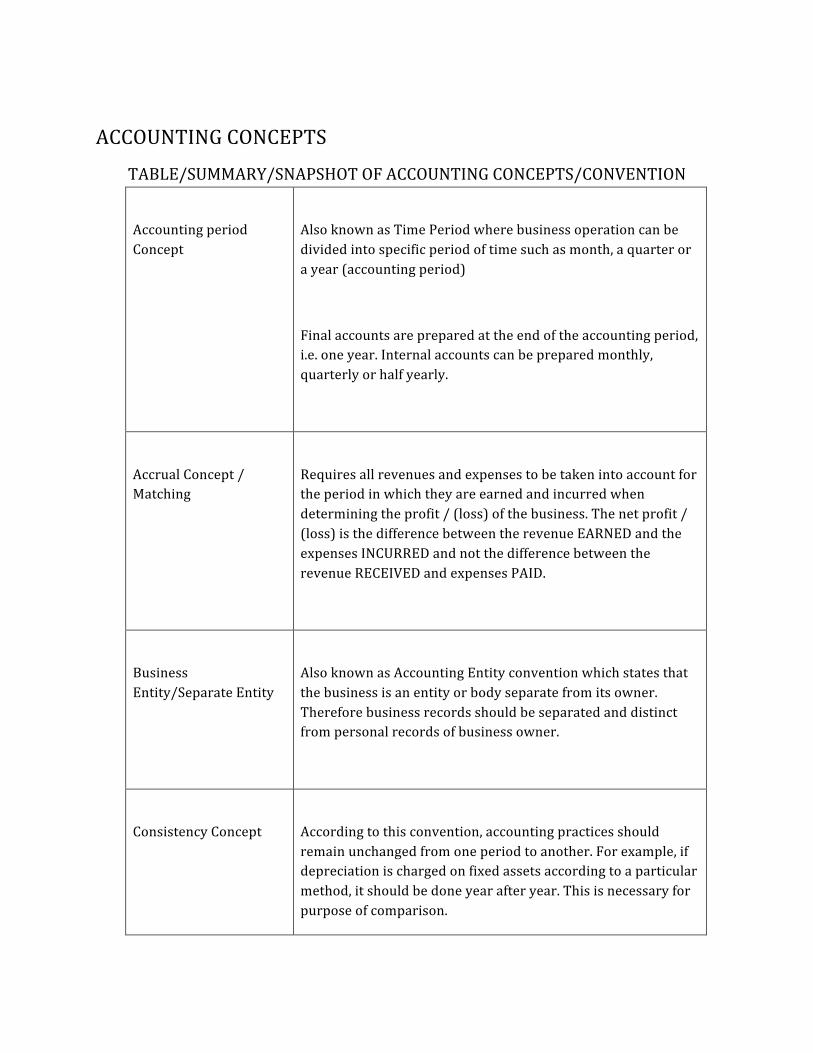

ACCOUNTING CONCEPTS

TABLE/SUMMARY/SNAPSHOT OF ACCOUNTING CONCEPTS/CONVENTION

Accounting period Concept

Also known as Time Period where business operation can be divided into specific period of time such as month, a quarter or a year (accounting period)

Final accounts are prepared at the end of the accounting period, i.e. one year. Internal accounts can be prepared monthly, quarterly or half yearly.

Accrual Concept / Matching

Requires all revenues and expenses to be taken into account for the period in which they are earned and incurred when determining the profit / (loss) of the business. The net profit / (loss) is the difference between the revenue EARNED and the expenses INCURRED and not the difference between the revenue RECEIVED and expenses PAID.

Business Entity/Separate Entity

Also known as Accounting Entity convention which states that the business is an entity or body separate from its owner. Therefore business records should be separated and distinct from personal records of business owner.

Consistency Concept

According to this convention, accounting practices should remain unchanged from one period to another. For example, if depreciation is charged on fixed assets according to a particular method, it should be done year after year. This is necessary for purpose of comparison.

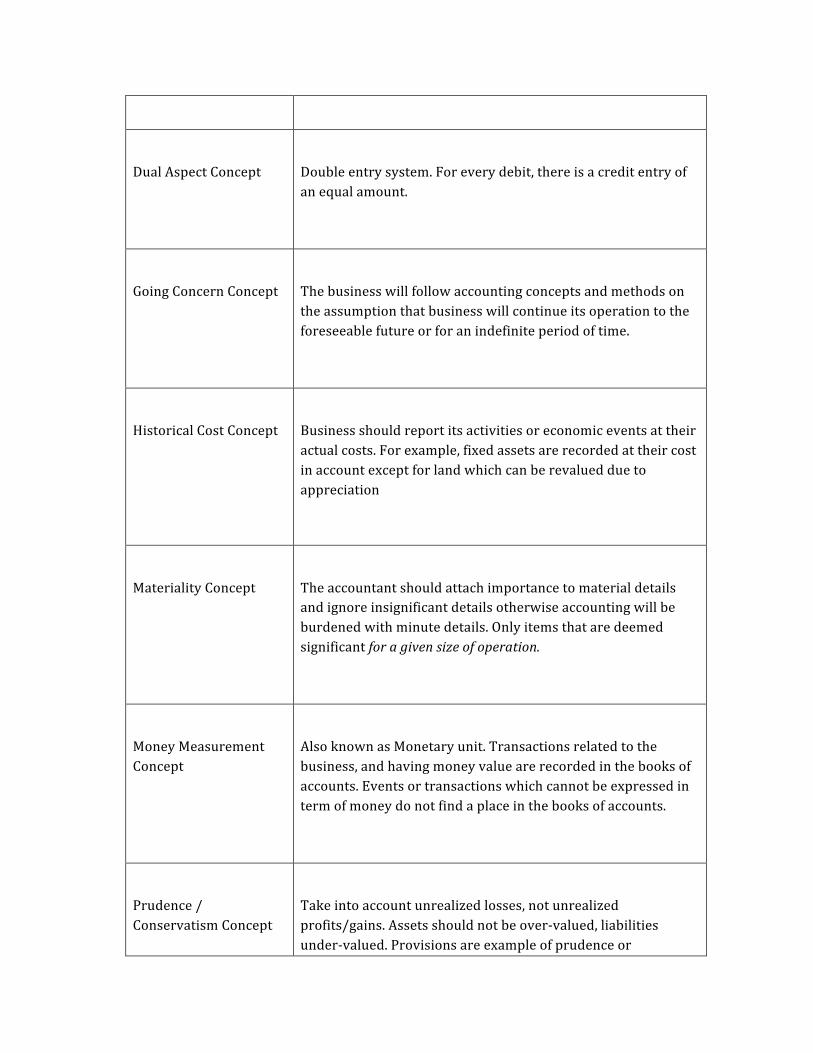

Dual Aspect Concept

Double entry system. For every debit, there is a credit entry of an equal amount.

Going Concern Concept

The business will follow accounting concepts and methods on the assumption that business will continue its operation to the foreseeable future or for an indefinite period of time.

Historical Cost Concept

Business should report its activities or economic events at their actual costs. For example, fixed assets are recorded at their cost in account except for land which can be revalued due to appreciation

Materiality Concept

The accountant should attach importance to material details and ignore insignificant details otherwise accounting will be burdened with minute details. Only items that are deemed significant for a given size of operation.

Money Measurement Concept

Also known as Monetary unit. Transactions related to the business, and having money value are recorded in the books of accounts. Events or transactions which cannot be expressed in term of money do not find a place in the books of accounts.

Prudence / Conservatism Concept

Take into account unrealized losses, not unrealized profits/gains. Assets should not be over-‐valued, liabilities under-‐valued. Provisions are example of prudence or

conservatism concept. Also under this prudence/conservatism concept, stock/inventory is value at lower of cost or market value. This concept guides accountants to choose option that minimize the possibility of overstating an asset or income.

WORKING CAPITAL

What is meant by working capital?

It is the money required to meet its every day expenses. It can be calculated by taking the difference between current assets and current liabilities. It is very important to have enough working capital to survive in the short run.

What are the effects of not having enough working capital?

(i) Problems in meeting debts as they fall due.

(ii) Inability to take advantage of cash discount.

(iii) Difficulty in obtaining further supplies.

(iv) Inability to take advantage of business opportunity as they arise.

What are ways of improving working capital.

(i)Introduction of further capital.

(ii) Obtaining long-‐term loan.

(iii) Reducing owners drawings.

(iv) Selling out useless fixed assets.

RATIOS

PROFITABILITY GROSS PROFIT MARGIN ( Gross Profit x 100 ) Net Sales While the gross profit is a dollar amount, the gross profit margin is expressed as a percentage of net sales. The Gross Profit Margin illustrates the profit a company makes after paying off its Cost of Goods sold. The Gross Profit Margin shows how efficient the management is in using its labour and raw materials in the process of production (In case of a trader, how efficient the management is in purchasing the good). There are two key ways for you to improve your gross profit margin. First, you can increase your process. Second, you can decrease the costs of the goods. Once you calculate the gross profit margin of a firm, compare it with industry standards or with the ratio of last year. For example, it does not make sense to compare the profit margin of a software company (typically 90%) with that of an airline company (5%). Reasons for this ratio to go UP (opposite for down)

1. Increase in selling price per unit 2. Decrease in purchase price per unit due to lower quality of goods or a different supplier. 3. Decrease in purchase price per unit due to bulk (trade) discounts. 4. Extensive advertising raising sales volume (units) along with selling price. 5. Understatement of opening stock. 6. Overstatement of closing stock. 7. Decrease in carriage inwards/Duties (trading expenses) 8. Change in Sales Mix (maybe we are selling some new products which give a higher margin).

NET PROFIT MARGIN ( Net Profit x 100 ) Net Sales Net profit margin tells you exactly how the management and operations of a business are performing. Net Profit Margin compares the net profit of a firm with total sales achieved. The main difference between GP Margin and NP Margin are the overhead expenses (Expenses and loss). In some businesses Gross Margin is very high but Net Margin is low due to high expenses, e.g. Software Company will have high Research expenses. Reasons for this ratio to go UP (opposite for down) All the reasons for GP margin apply here. Additionally

1. Increase in cash discounts from suppliers 2. A decrease in overhead expenses 3. Increase in other incomes like gain on disposal, Rent Received etc.

Return on Capital Employed (ROCE) This is the key profitability ratio since it calculates return on amount invested in the business. If this ratio is high, this means more profitability (In exam if ROCE is higher for any firm it is better than the other firm irrespective of GP and NP Margin). This return is important as it can be compared to other businesses and potential investment or even the Interest rate offered by the bank. If ROCE is lower than the bank interest then the owner should shoot himself. This ratio can go up if profits increase and capital employed remains the same. Also if Capital employed decreases, this ratio might go up. Net Profit x 100 Capital Employed Capital Employed = Fixed Assets + Current Assets – Current Liabilities OR

= Ordinary Share Capital + Preference Share Capital + Reserves + Long-‐term Liabilities

LIQUIDITY As we know a firm has to have different liquidity. In other words they have to be able to meet their day to day payments. It is no good having your money tied up or invested so that you haven’t enough money to meet your bills! Current assets and liabilities are an important part of this liquidity and so to measure the firms liquidity situation we can work out a ratio. The current ratio is worked out by dividing the current assets by the current liabilities. CURRENT RATIO = Current assets _ Current liabilities The figure should always be above 1 or the form does not have enough assets to meet its liabilities and is therefore technically insolvent. However, a figure close to 1 would be a little close for a firm as they would only just be able to meet their liabilities and so a figure of between 1.5 and 2 is generally considered being desirable. A figure of 2 means that they can meet their liabilities twice

over and so is safe for them. If the figure is any bigger than this then the firm may be tying too much of their money in a form that is not earning them anything. If the current ratio is bigger than 2 they should therefore perhaps consider investing some for a longer period to earn them more. However, the current assets also include the firm’s stock. If the firm has a high level of stock, it may mean one of the two things,

1. Sales are booming and they’re producing a lot to keep up with demand. 2. They can’t sell all they’re producing and it’s piling up in the warehouse!

If the second of these is true then stock may not be a very useful current asset, and even if they could sell it isn’t as liquid as cash in the bank, and so a better measure of liquidity is the ACID TEST (or QUICK) RATIO. This excludes stock from the current assets, but is otherwise the same as the current ratio. ACID TEST RATIO = Current assets – stock Current liabilities Ideally this figure should also be above 1 for the firm to be comfortable. That would mean that they can meet all their liabilities without having to pay any of their stock. This would make potential investors feel more comfortable about their liquidity. If the figure is far below 1, they may begin to get worried about their firm’s ability to meet its debts.

Rate of Stock Turnover It shows the number of times, on average, that the business will sell its stock in a given period of time. It basically gives an indication of how well the stock has been managed. A high ratio is desirable because the quicker the stock is turned over, more profit can be generated. A low ratio indicates that stocks are kept for a longer period of time (which is not good). Cost of Goods Sold = ____ Times Average Stock

Advantages of Ratios 1. Shows a trend 2. Helps to compare a single firm over a two years (time – series) 3. Helps to compare to similar firms over a particular year. 4. Helps in making decisions

Disadvantages (Limitations): 1. A ratio on its own is isolated (We need to compare it with some figures)

2. Depends upon the reliability of the information from which ratios are calculated. 3. Different industries will have different ideal ratios. 4. Different companies have different accounting policies. E.g. Method of depreciation used. 5. Ratios do not take inflation into account. 6. Ratios can ever simplify a situation so can be misleading. 7. Outside influences can affect ratios e.g. world economy, trade cycles. 8. After calculating ratios we still have to analyze them in order to derive a conclusion.

How to Comment: Usually in CIE they assign 2 marks for comment on each ratio. One mark is for indicating if the ratio is better or worse (not higher or lower). The second mark is to explain the importance or the reason of the change in ratio. For e.g. If Gross Profit Margin was 40% and now its 50%, you should say that the Gross profit Margin has improved (rather than increased) and this may be due to an increase in selling price or a decrease in cost of goods sold (depending upon the question). Also remember that the liquidity ratios should be close to industry average. Too less or too much liquidity is bad! At the end of your answer, always give a conclusion

• When comparing a single firm over two years then do mention performance of which year is better. (In terms of profitability and liquidity)

• When comparing two different firms over the same year do mention performance of which firm is better. (In terms of profitability and liquidity).

If the question says evaluate profitability then use (GP Margin, NP Margin and ROCE) If the question says evaluate liquidity, use (Current Ratio, Acid Test and Rate of Stock Turnover) If the question says evaluate the performance it means both profitability and liquidity.

DEPARTMENTAL ACCOUNTS

Departmental Accounts are the accounts that through light not only on the trading result of the business as a whole but also on the trading result of each department individually.

Reasons Or Advantages Of Making Departmental Accounts: OR

Reasons To Know The Result Of Each Department:

It lets us know the expenses and incomes of each department clearly at one place.

It helps us to compare the results i.e. G.P or N.P of one department with the other.

It helps us to formulate policies in order to develop the business on proper lines.

To decide whether to drop or start a new department.

It helps us to reward the departmental managers.

Things to be considered before closing a department:

. Consider all possible means to improve the department.

. The methods used to apportion the expenses should be studied to see if they are in fact the fairest methods.

. The effect of the closure of one department on the other department should be investigated.

. The attractive uses of the space becoming available need to be considered.

. Non-‐Monetary factors such as staff morale and the effect on supplies and customers faith is also to be considered.

MANUFACTURING ACCOUNT

. Manufacturing businesses prepare manufacturing account in addition to the usual final Accounts. Manufacturing account shows how much does it cost the business to manufacture the goods in a financial year.

. Cost Of Raw Material Consumed: It is the value of Raw material used in production. It consist of net purchases of Raw Material, carriage on raw material opening stock of raw material closing stock of Raw material.

. Prime Cost: It is the basic cost of manufacturing the goods. It consists of direct raw material direct labour and direct expenses.

. Production Cost: It is the total cost of manufacturing the goods. It consist of prime cost plus factory expenses, and it is after any adjustment for work-in- progress.

. Work-in-progress: These are the goods which are partly made, but which are not yet

completed are known as work-in-progress.

The Impact of ICT in Accounting: ICT can be used in accounting for keeping and updating the double entry system, stock records, debtor analysis and the preparation of budgets.

Benefits:

· Greater accuracy-‐automatic and error free

· Greater speed

· Improved accessibility

More information available

· Cuts in staff costs

Drawbacks:

Capital expenditure-‐cost of machines and software. Economic life can be quite short

. · Training costs-‐of training the staff to use the equipment

. Staff morale could be lowered

· Risk of data loss and security breaches can be vulnerable to crashes, viruses and hacking.

PAYROLL DOCUMENTATION PAYE SYSTEM:

The Pay As you Earn system means tax and other deductions are subtracted by the employer at source and only net pay is paid to the worker.

CLOCK CARD • Employee inserts a card into a time recording clock to record the start and finish

time for each working session • Payroll department can calculate the number of basic hours and the number of

overtime hours for each day • Payroll department can calculate the total basic hours and total overtime hours for

each week • Payroll department can calculate total gross pay

TIME SHEET The sheet contains a breakdown of working details for each day, the employee manually records the start and finish time for each session, including a reference to the time spend on each job

Payroll department can calculate the same as above.

The payroll department can cost labour hours to be charged to specific job

PAYSLIPS An employee has a legal right to receive a payslip. It is given to the employee when wages are received, or sent to employee if wages are paid by direct debit.

The payslip is used to inform the employee of pay details, including:

• Gross pay

• Details of deductions made

• Net pay

• Employee number

• Tax code number/ National insurance number

PAYROLL REGISTER

List of all employees kept by the payroll department, containing personal data and pay details which included:

Employee number Salary

Job title Tax code

Employee name National insurance number

Address Voluntary deductions

Telephone Starting date

Date of birth Leaving date

The information is for reference, and details may be kept on individual employee record card.

WAGES SHEET (also wages book, and weekly payroll) nformation from each employee’s individual payslip is listed on a sheet, showing the gross pay, tax and NIC, other deductions and net pay

Each column is totalled for the week

Is used to reconcile the gross pay and the net pay paid

ETHICS IN ACCOUNTING Ethics is a branch of philosophy and is about the way people judge rights and wrongs of their actions. It is a code of conduct that is followed by members of a community. To explain ethics, people say that ethics begins where the law ends. A person or business may act legally according to laws of the particular country, but their actions are not necessarily ethical. Profitability should not be the only consideration when formulating the policy of a business: social and moral aspects are also considered. By including such factors, a business is not only applying the laws of the country, but is also applying a moral or ethical approach. All the accounting organizations actively encourage their members to apply a minimum code of conduct. If such minimum standards are not upheld, an accountant is guilty of professional misconduct (which can result in loss of reputation, a monetary fine, and even imprisonment). To conclude From an accounting point of view, ethical issues would include the following:

-‐ Adherence to generally acceptable accounting principles and practices -‐ Honesty in recording and providing true and complete information -‐ Trustworthiness in not disclosing confidential information -‐ Competency in keeping records and preparing reports correctly -‐ Giving advice that will be in the best interest of the organisation (and that would not therefore harm the organisation) -‐ Taking measures to safeguard information and control access to computer systems INTERNATIONAL ACCOUNTING STANDARDS(IAS) International Accounting Standards provide guidelines for the preparation of financial statements. Before the International Standards were introduced each country use to have their own accounting standards

The world has become a global village. Multinationals are set up in every corner of the world. Investing companies also offer investors to invest in shares in different countries. This requires financial information to be understandable and comparable so that investors as well as any other users of financial statements to make decision. As such, many countries are moving towards adopting International Accounting Standards so that financial information become comparable across the globe. Most of the countries have now moved to IAS.

Benefits of adopting International Accounting Standards:

-‐Allows better comparison between financial statements

-‐ Reduces differences and variety of accounting practice

-‐ Makes financial information more reliable and understandable

ALL THE SMALL THINGS. Financial Accounting

-‐ Written down value or net book value means after depreciation. -‐ Only assets , drawings and expenses have debit balances, all the other things in the world

will have a credit balance. -‐ Sales invoice would mean good sold on credit. -‐ If bad debt is inside the trial balance then it means that it has already been subtracted from

the Debtors. -‐ Everything outside the Trial Balance has to come TWICE. -‐ Provision for depreciation is a Contra Asset Account. It is NOT AN EXPENSE, since its

balance is brought down. -‐ All the balance c/d go to the Balance Sheet. -‐ All the expenses and incomes are in the Profit and Loss a/c. -‐ Revenue = Sales. -‐ When it is NOT specified how you bought Machinery, you make it BANK! Automatically. -‐ If NOTHING is specified about the policy of Depreciation, then you account for it MONTHLY. -‐ Every Asset has an Opening Debit balance and Closing Credit balance. -‐ Every Liability has an Opening Credit balance and closing Debit balance. -‐ The Amount of Loan interest still owing and not paid (which was to be paid this year) comes

in the Current Liabilities. -‐ Departmental Account: If given with prepayment any expenses, then we SHOULD FIRST

ADJUST the accruals and prepayments, and then divide them into % of EACH department. -‐ Control Account is not part of the double entry. It is THE THIRD ENTRY. -‐ List price is the price WITHOUT deducting TRADE DISCOUNT. -‐ Set off always reduces the Control Account! -‐ Credit Notes received = Return Outwards -‐ Credit Notes sent = Return Inwards -‐ Whenever you receive a cheque from BANK marked ‘REFER TO DRAWER’ then it is CHEQUE

DISHONOURED -‐ FIX NET PROFIT: In the Journal, if the account goes in the N.P, then if something is being

CREDITED it will INCREASE N.P, or if it DEBITED, then it will DECREASE N.P. -‐ To find the opening balance in the Suspense LEAVE THE FIRST two lines empty. -‐ The amount of stationery used, goes in the Profit and Loss as an expense. -‐ Sundry Expense means miscellaneous expenses. -‐ Whatever goes in the Profit and Loss is REVENUE EXPENDITURE. -‐ Whatever goes in the BALANCE SHEET is CAPITAL EXPENDITURE.

-‐ CAPITAL EMPLOYED (Sole Trader) = CAPITAL OWNED – LONG-‐TERM LOAN. -‐ CAPITAL OWNED (Sole trader) = Assets – Liabilities. -‐ CAPITAL EMPLOYED (COMPANY) = OSC + PSC + RESERVES (share premium, Retain profits,

all reserves) + Long Term Liabilities. -‐ REFUND FROM Supplier is recorded on the Credit side of the Purchase Ledger Control

Account. -‐ In closing Assets, you write the Net Book Value (N.B.V) -‐ DRAWINGS ARE Neither AN Asset NOR A LIABILITY. -‐ If they ask you to make a STATEMENT TO find Profit or Loss, then just make that financed

by (Opening capital + Net Profit (x) + Capital Introduced – Drawings = Capital at end) -‐ If they say make final accounts, then make Profit and Loss and Balance Sheet. -‐ Closing Stock has a direct relation with profit. If closing stock is overstated, profit will be

overstated. -‐ Opening stock has an inverse relation with profit. If opening stock is overstated, profit will

be understated. -‐ Goods sent on sale or return basis should not be counted as sale unless accepted by the

customer. Infact they should be included in the stock. -‐ We only double the amount if it is written on the wrong side of the account. -‐ Club accounts will never have drawings. -‐ Unpresented cheques are payment by us. -‐ Uncredited cheques are receipts by us (also called LODGMENTS). -‐ If you can’t find the average debtors or stock or creditors, use closing figure instead of

instead of average. -‐ If nothing is specified, we can assume all sales and purchases are on credit basis. -‐ Provision for bad debt is a separate account. We can record the provision in debtors

account, net debtors mean after deducting provision. -‐ We only take the change in provision in the Pnl. -‐ Cashbook is both a daybook and a ledger. -‐ We only record credit sales and purchases in the Sales and Purchase Daybook, cash and

bank transactions are in the cashbook. -‐ If a daybook is overcast only that amount will be wrong. E.g. if Sales daybook is undercast,

this means only the Sales account is wrong. -‐ Long term donations are in the balance sheet of clubs and short term are incomes.. -‐ Indirect Material, Indirect Labour, Depreciation of plant and machinery will always be

Factory Overheads. -‐ Administration and selling goes in the profit and loss account. -‐ Net Assets = Assets – Liabilities, but in some cases CIE uses Net Assets as Capital Employed

which is Assets – Current Liabilities. -‐ Sale or Purchase is recorded when the goods are accepted not when the invoice is sent or

the payment is made. -‐ If only net book values are available Depreciation for the year = Opening Net Book Value +

Purchase of Asset – Sale of Asset (Nbv) – Closing Net book value.

-‐ In most question they don’t mention depreciation, that doesn’t mean there is no depreciation, use the above formula to determine. (Don’t forget the depreciation like idiots).

-‐ Accumulated funds at start or Capital at start = Opening Asset – Opening Liabilities (please don’t forget the opening balance of bank account).

-‐ Cash banked will come on the debit side of bank and credit side of cash account. -‐ Subscription owing is an asset and prepaid is a liability. -‐ Loan is as long term liability unless payable within one year. If nothing is written, assume

long term. -‐ POOP is for expenses. -‐ OPPO is for incomes. -‐ Net realizable value = current selling price – any expenses (repairs) -‐ We always ignore replacement cost in stock valuation. -‐ Perpetual methods are those where we make a table. -‐ Markup is on cost (cost is 100) -‐ Margin is on sales (Sales is 100)

HOPE THIS HELPS J