Embed Size (px)

Citation preview

Quantitative Methods & Tools for Studying Discrete Events

www.eventstudytools.com

© www.eventstudytools.com (2012) // Slide 2

Finance Theories:• Market Efficiency

Hypothesis• Theories on: regulation,

optimal capital structure,

dividends, stock splits

and repurchases

Management Theories:• Behavioral Theory• Population Ecology

Theory• Resource Based View• (…)

How To Research Discrete Events?

Phenomenon

Methods & ToolsTheoreticalPerspective

Something about a…• Specific event type• Sequence of events

• Event Study Analysis1

• Event History Analysis2

• Optimal Matching2

• …

ResearchR

esea

rch

Gap

Notes: 1 Cross-sectional method, 2 Longitudinal method

© www.eventstudytools.com (2012) // Slide 3

Phenomena

Incidents of interest that occur at specific moments in time„Discrete Events“

Individual Events

• Organizational events (competitive moves)• M&A / divestitures / joint-ventures / alliances • Earnings announcements• Stock splits• ….

• Industry events• Regulatory change• Technological shocks• Environmental catastrophes• ….

Sequences of Events

• Sequences of events• Patterns of firm behavior• Occurrences of economic shocks• …

Strategy & Economics

Finance & Strategy

© www.eventstudytools.com (2012) // Slide 4

Methods (1/3): Event Study Methodology (ESM)

Abnormal Returns (ARs):

Cumulative Abnormal Returns (CARs):

Cumulative Average Abnormal Returns (CAARs):

Dependent Variables

• Event studies numerically capture the impact of discrete events on firm values

• ESM grounds on the efficient-market hypothesis. It assumes that new information is timely reflected in stock prices.

• ESM yields a short-term performance measures (ARs, CARs, CAARs)

Prediction Models: Market Model, CAPM, Fama-French 3 Factor Model, APT

Event Window:leakage, post-event ‚digestion period‘

Grouping:Setting the grouping variable

Astra-Zeneca merger announcement on April 6, 1999

eventwindow

© www.eventstudytools.com (2012) // Slide 5

Methods (2/3): Event History Analysis (EHA)1

Firm 1

Firm 2

Firm 3

Firm 4

Firm 5

Firm 6

Duration / Spell lengthRestructuring moves

t

• EHA allows analyzing the social processes that lead towards the occurrence of events (thus its name ‚event history‘)

• Grounds on failure-likelihoods derived from ‚spell lengths‘

• Yields coefficients that express how different IVs/covariates impact the failure-likelihoods

1 Synonym names: Survival Analysis, Duration Analysis (Economics), Failure Time Analysis, Hazard Time Analysis, Transition Analysis, Reliability Analysis (Engineering)

Failure (F): The unconditional probability that an event will occurSurvival (S): The probability that ‘up until now’ the event has not yet occurred.Hazard Rate (HR): The conditional failure rate – given that the event has not yet occurred, what

are the chances that it will occur? HR

Dependent Variable

t0

Hurrikane KatrinaAugust 25, 2005

0 >> Clock Variable >>

New O

rleans

H Katrina Example: The inverted clock-variable has a negative impact on the Hazard Rate/the instantaneous probability that firms engage in restructuring moves

© www.eventstudytools.com (2012) // Slide 6

Methods (3/3): Optimal Matching Algorithm (OMA)

The distance between individual sequences (S vs. S) / sequences and typologies/Gestalt properties (S vs. T, resp. S vs. G)

Sequence 1

Sequences (Si) of Events

Sequence 2

Sequence 3

(…)

Dependent Variables (contingent on use)

Comparison of Sequences

Rhythm (G)

Benchmarks: Typical Patterns (T) or ‚Gestalt‘ Properties (G)

Market Entry (T)

• OMA is a technique for the analysis of sequence data ( process theory)

• Methodologically, OMA is a propensity score method to optimize/minimize the distance between ‘matched-pairs’ of sequences

• Technically, OMA is an OR algorithm minimizing the costs associated with individual transformation functions

• Events• Action types• Scaling attributes• Magnitude• Exploration/

Exploitation

Clustering

Through clustering of closely related sequences, one can inductively derive typologies. These can then be used as dependent or independent variables in further analysis (i.e., as dummy variables).

© www.eventstudytools.com (2012) // Slide 7

RESEARCH EXAMPLE & TOOLS

© www.eventstudytools.com (2012) // Slide 8

Example (1/6): The Phenomenon

0

20

40

60

80

100

120

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

in USD bn,indexed to 2007 Insured catastrophe losses 1998-2007

Earthquake/tsunamiMan-made disastersWeather-related Nat Cats

9/11

Katrina

Lothar/Bart

Source: Sigma Research

"When Industries Shake: How Market Shocks Affect Competitive Behavior"

2001-09-11 2005-08-25

© www.eventstudytools.com (2012) // Slide 9

Event History

Analysis

Event Study

Optimal Matching

Example (2/6): Choice of Research Method

Theory on Firm Behavior (Focus on Process/Event Sequence):

Before and after market shocks patterns of XYZ differ.

Theory on Firm Behavior (Focus on Firms’ Inclinations to do sth and its Determinants):

Following market shocks firms are more/less inclined to do XYZ.

Theory on Stock Market Perception:

Following market shocks stock markets respond differently to XYZ.

"When Industries Shake: How Market Shocks Affect Competitive Behavior"

© www.eventstudytools.com (2012) // Slide 10

"From Crisis to Opportunity: How Market shocks Impact Interfirm Rivalry"

Example (3/6): “Competitive Dynamics”

Figure adopted from Smith, Ferrier, and Ndofor (2001: 348)

1 •Competitive pressure (IV): Competitive pressure refers to the aggregate number of actions taken by a firm's rivals and expresses the pressure rivals jointly exert on a firm to take new competitive action (Zuchhini & Kretschmer, 2011; Hsieh & Chen, 2010)

•Trend toward the respective action type (IV): Given that also a firm's choice of competitive action may be driven by prior rival actions (Lieberman & Asaba, 2006/Asaba & Lieberman, 2012), we capture trends in the overall body of rival actions prior to the focal action

2 Impact of market shock (IV/MV): Impact and fading effect of a recent market shock

3 Inclination to take new competitive action (DV): Similar to Hsieh & Chen (2010) and Yu & Canella (2007), we study how firms' inclinations to take action change upon variations in a set of explanatory variables (Event history analysis; Cox model).

Firm resources

Industry structure and events Change in industry structure

Change in firm resources

Firm action(s)

Time

Rival actionRival action

1

2

3

© www.eventstudytools.com (2012) // Slide 11

Example (4/6): Theory and Hypotheses

H1: Higher degrees of competitive pressure increase a firm's inclination to take

new competitive action.

H2: A trend of rivals to pursue a distinct competitive action type increases a

firm's inclination to take new competitive action (of this type).

{ Market shocks imply uncertainty; Uncertainty breeds opportunities to outmaneuver

rivals; Mutual forbearance equilibriums will fail }

H3: Market shocks increase a firm's inclination to take new competitive action.

{ Imitation of rival actions that have lost their validity due to fundamental changes in the

environment does not make sense; Individual exposures to the shock require individual

responses }

H4: Market shocks negatively moderate the relationship between competitive

pressure and a firm's inclination to take new competitive action.

H5: Market shocks negatively moderate the relationship between the trend of

rivals to pursue a distinct competitive action type and a firm's inclination to

engage in this competitive action type.

BaselineNew

© www.eventstudytools.com (2012) // Slide 12

Example (5/6): Empirical Strategy

Website Company AWebsite

Company AWebsite

Company AWebsite Company A

Mass download 1.2

Consolidationand clean-up of news items

Sample selection

1.1

Categorizationof news items

Event studyIdentification of announcement dates

Competitive Action

• Date

• Type of competitive action

• Abnormal returns

• Press release text (for additional coding)

Competitive Behavior

• Chronology, composition, and density of

competitive action sequence

• Patterns of and deviations from typical

competitive behavior

1.3

2

3

4

Press releasearchive

1 Press release scraping Industry Context

• Structural industry characteristics

• Industry events

© www.eventstudytools.com (2012) // Slide 13

Example (6/6): Research Findings

Variables Model 1 Model 2 Model 3 Model 4 Model 5 Model 6Coef. SE Coef. SE Coef. SE Coef. SE Coef. SE Coef. SE

Firm size (0.1† (0.1) (0.1† (0.1) (0.1† (0.1) (0.1† (0.1) (0.1† (0.1) (0.1† (0.1)Business scope -0.2 (0.3) -0.2 (0.3) -0.2 (0.3) -0.2 (0.3) -0.2 (0.3) -0.2 (0.3)Diversification level (0.3 (0.3) (0.4 (0.3) (0.4 (0.3) (0.3 (0.3) (0.3 (0.3) (0.3 (0.3)Reinsurance strategy -0.1 (0.4) -0.1 (0.4) -0.1 (0.4) -0.1 (0.4) -0.1 (0.4) -0.1 (0.4)Financial leverage (1.7 (1.9) (2.0 (1.9) (2.0 (1.9) (2.0 (1.9) (2.0 (1.9) (2.0 (1.9)Investment strategy (0.5 (0.4) (0.6 (0.4) (0.6 (0.4) (0.6 (0.4) (0.6 (0.4) (0.6 (0.4)Past performance (1.5 (1.7) (1.0 (1.7) (1.0 (1.7) (0.9 (1.7) (1.0 (1.7) (1.0 (1.7)Slack 3.1*** (0.7) 3.0*** (0.7) 3.0*** (0.7) 2.9*** (0.7) 2.9*** (0.7) 2.9*** (0.7)Competitive pressure (0.03* (0.0) (0.03* (0.0) (0.03* (0.0) (0.03* (0.0) (0.03* (0.0)

Imitation (0.01* (0.0) (0.01* (0.0) (0.01* (0.0) (0.01* (0.0)

Market shock (0.7* (0.3) (0.7* (0.3) (0.7* (0.3)Market shock x Competitive pressure

-0.0 (0.0) -0.0 (0.0)

Market shock x Imitation -0.2** (0.1) -0.2** (0.1)

Observations 2'467 2'467 2'467 2'467 2'467 2'467Log-Likelihood -16831.52 -16826.30 -16825.89 -16823.33 -16819.65 -16819.61Chi-Square 26.79*** 32.58*** 36.68*** 36.65*** 66.18*** 69.66***

© www.eventstudytools.com (2012) // Slide 14

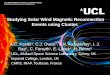

3

• Manual review• Computer-aided

text analysis

Coding of EventsData Collection

1

• „Secondary databases“ (e.g., Thomson One Banker)

• „Web harvesting“

Operational Challenges of Event-Driven Research

4

• Excel• Eventus• EST• STATA / SPSS

Statistical Analyses

Turning Qualitative Text into Quantified Metrics and Time-Series

Allocation of Events in Time

2

• Manual step• Regular

expressions

Making sense out of unstructured texts from the Internet Web 3.0 (aka the „semantic web“)

Research trends: “News Analytics” (Finance), text analysis (Strategy)

© www.eventstudytools.com (2012) // Slide 15

‘Apps’ for Studying Discrete Events

2012 William H. Newman Award Finalist (AOM)

2010 Best Paper Journal of Strategy and Management

2012 Best Conference PhD

Paper Prize (SMS)

News Retrieval Services

RegEx-Based „Date Identifier“

Computer-Aided „Text Analyzer“ with Scaling and Categorization Functions

„Abnormal Return Calculator“

Data Downlink for Yahoo!Finance

.com

© www.eventstudytools.com (2012) // Slide 16

The “News Analytics” – Framework

Website Company AWebsite

Company AWebsite

Company AWebsite Company A

Mass download 1.2

Consolidationand clean-up of news items

Sample selection1.1

Categorizationof news items

Event studyIdentification of announcement dates

Corporate News

• Date

• Type of competitive action

• Abnormal returns

• Press release text (for additional coding)

Corporate News Stream

• Chronology, composition, and density of

corporate news stream

• Patterns of and deviations from typical

information flow

1.3

2

3

4

Press releasearchive

1 Press release scraping

© www.eventstudytools.com (2012) // Slide 17

My Personal Advice on Writing a‘Quant Thesis’ Based on Events

1. Avoid the ‘paralysis-by-analysis/data-trap’: Excel on theory building

2. Take advantage of computer-aided automation (e.g., VBA / Python / EST) or offshoring of data collection (e.g., odesk.com / elance.com) whenever possible

3. Think in processes and not individual cases / observations

© www.eventstudytools.com (2012) // Slide 18

“Inspiring References” for Finding an own Thesis Topic (1/2)

Eberhard, K. (2012). Implications of pace, mechanisms, and rhythm of growth for firms' resistance to economic shocks. St. Gallen: University of St. Gallen, Institute of Management.

Fama, E. F. (1976). Foundations of finance. New York: Basic Books.Ketchen, D. J. & Palmer, T. (1999). Strategic responses to poor organizational

performance: A test of competing perspectives. Journal of Management, 25: 683-706.

Laughlin, R. C. (1991). Environmental disturbances and organizational transitions and transformations: Some alternative models. Organizational Studies: 209.

Lieberman, M. B. & Asaba, S. (2006). Why do firms imitate each other? Academy of Management Review, 31 (2): 366-385.

Lowenstein, J. & Ocasio, W. (2005). Vocabularies of organizing: How language links culture, cognition, and action in organizations. Unpublished manuscript.

MacMillan, I., McCaffrey, M. & Van Wijk, G. (1985). Competitor's responses to easily imitated new products: Exploring commercial banking product introductions. Strategic Management Journal, 6: 75-86.

Meyer, A. D., Brooks, G. R. & Goes, J. B. (1990). Environmental jolts and industry revolutions: Organizational responses to discontinuous change. Strategic Management Journal, 11 (Summer special issue): 93-110.

© www.eventstudytools.com (2012) // Slide 19

“Inspiring References” for Finding an own Thesis Topic (2/2)

Miller, D. & Friesen, P. (1980). Momentum and revolution in organizational adaptation. Academy of Management Journal, 23 (4): 591-614.

Nixon, R. D., Hitt, M., Lee, H. & Jeong, E. (2004). Market reactions to announcement of corporate downsizing actions and implementation strategies. Strategic Management Journal, 25 (11).

Schimmer, M. (2012). Competitive dynamics in the global insurance industry: strategic groups, competitive moves, and firm performance. Wiesbaden: SpringerGabler.

Staw, B. M. (1981). The escalation commitment to a course of action. Academy of Management Review, 6 (4): 577-587.

Tetlock, P. C. (2008). More than words: Quantifying language to measure firms' fundamentals. Journal of Finance, 63 (3): 1437-1467.

Tetlock, P. C. (2011). All the news that's fit to reprint: Do investors react to stale information? Review of Financial Studies, 24 (5): 1481-1512.

Wang, L. & Zajac, E. J. (2007). Alliance or acquisition? A dyadic perspective on interfirm resource combinations. Strategic Management Journal, 28: 1291-1317.

Yu, T. & Cannella, A. A. (2007). Rivalry between multinational enterprises: An event history approach. Academy of Management Journal, 50: 665-686.

Zhang, Y. & Wiersema, M. (2009). Stock market reaction to CEO certification: The signalling role of CEO background. Strategic Management Journal, 30.

© www.eventstudytools.com (2012) // Slide 20

http://www.eventstudytools.com

++ Stock Market Response Analysis ++ News Analytics ++

(Data Scraping // Date Identifier // CATA-Tool // Abnormal Return Calculator)