Embed Size (px)

Citation preview

Mastering Depreciation© American Institute of Professional Bookkeepers, 2012

Mastering Depreciation

American Institute of Professional Bookkeepers

Mastering Depreciation

Business-related AssetsThe categories of business-related assets are property, plant and equipment (PP&E)Property includes:

buildings land

Plant and plant assets (fixed assets) are: generally long-term (last longer than 1 year) acquired for business use not intended for resale to customers

Mastering DepreciationSlide 3

Depreciation of Plant AssetsDepreciation is the periodic allocation of the cost of a tangible, long-term asset over its estimated useful life.

The purpose of depreciation is to match the expense of using an asset against the revenue it produces.

Mastering DepreciationSlide 4

Booking DepreciationDepreciation expense is booked at the end of the period with an adjusting entry:

The asset’s book value is its cost less the balance in Accumulated Depreciation

Depreciation Expense

Accumulated Depreciation

xxx

xxx

The debit recognizes the expense. The credit to Accumulated Depreciation effectively reduces the balance in the related asset account.

Mastering DepreciationSlide 5

Booking DepreciationThere are two kinds of depreciation: GAAP (book) depreciation—used to prepare

the financial statements Tax depreciation—used to calculate

depreciation for tax purposes

Tax depreciation can be used for both tax and book purposes only if: the financial statements will not be audited, or tax depreciation is not materially different

from GAAP depreciation

Mastering DepreciationSlide 6

Depreciation of Plant AssetsTo compute depreciation of PP&E, you need to know: The asset’s cost The asset’s estimated residual value (also

known as salvage value, scrap value or trade-in value)

The asset’s estimated useful life in years or units

The depreciation method being used

Mastering DepreciationSlide 7

Depreciation of Plant AssetsGenerally, the cost of a property or plant asset includes all costs required to acquire, transport and prepare the asset for its intended use.

Cost includes (but is not limited to): Purchase price Transportation costs Installation or set-up costs Testing

Mastering DepreciationSlide 8

Land and Improvements to Land

Land, although not depreciable, is still a company asset. Because they are part of the land’s purchase price the following costs are also not depreciable: Brokerage commissions Survey fees Legal fees Back (delinquent) property taxes Grading/clearing Cost of demolishing or removing buildings

Mastering DepreciationSlide 9

Land and Improvements to Land

Improvements to land are depreciable because they are subject to decay: Driveways, sidewalks and parking lots Fences Sprinkler systems Lights in parking lot

Mastering DepreciationSlide 10

BuildingsThe cost of a building includes: Purchase price Brokerage commissions Sales and other taxes Expenditures for repairing or renovating

the acquired building for its intended use

Mastering DepreciationSlide 11

Determining CostMachinery or equipment costs include: Purchase price less discounts Purchase commissions Transportation Insurance in transit Sales and other taxes Installation Tests before placing the asset in service

Mastering DepreciationSlide 12

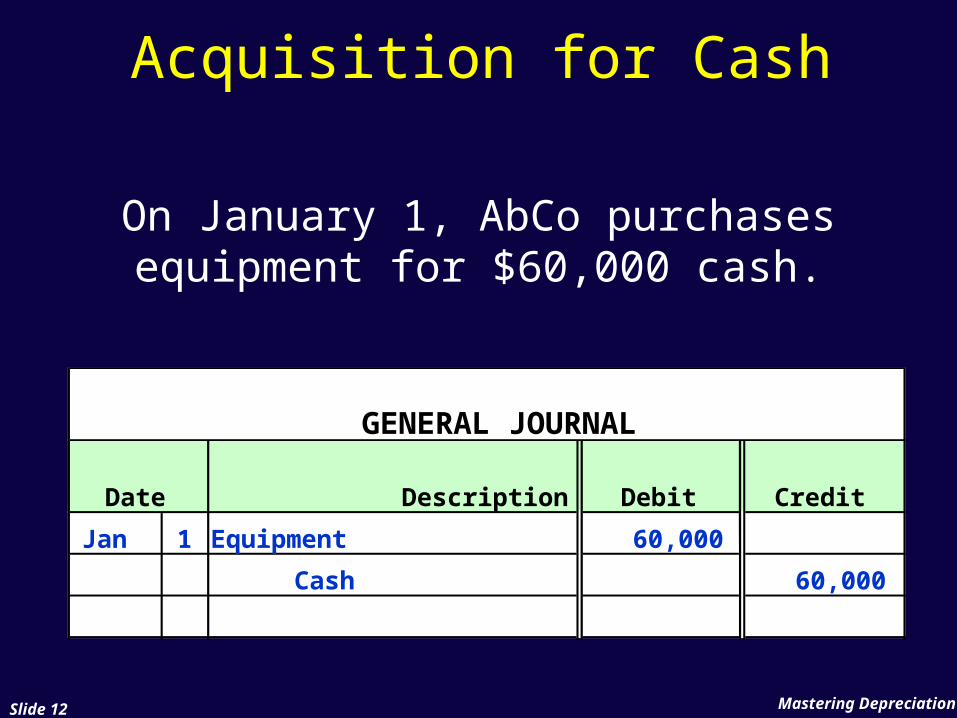

Acquisition for Cash

On January 1, AbCo purchasesequipment for $60,000 cash.

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Equipment 60,000

Cash 60,000

Mastering DepreciationSlide 13

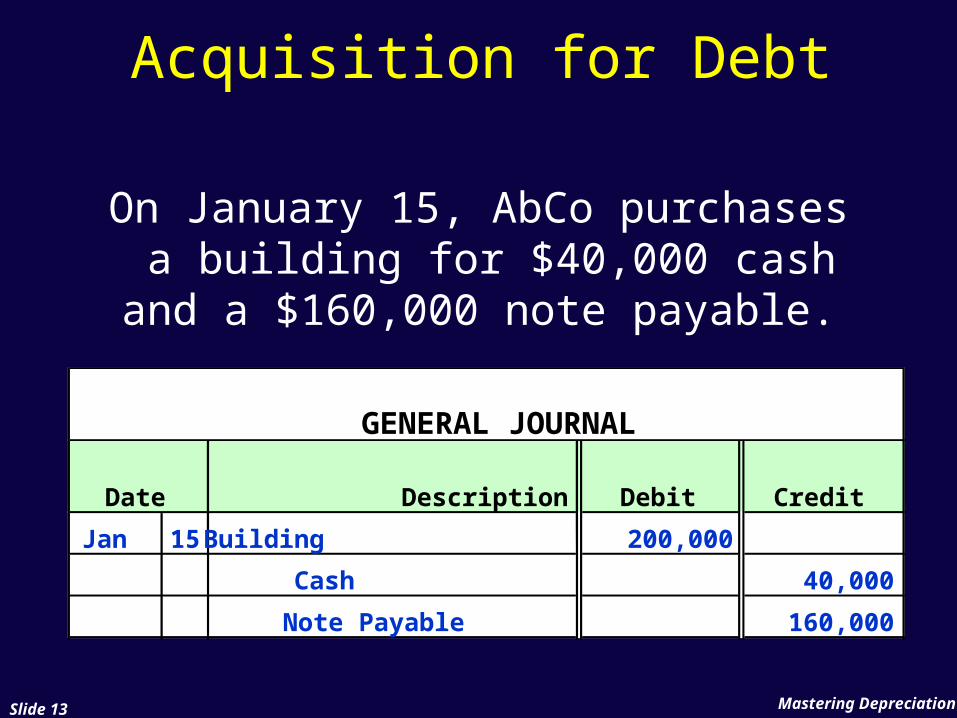

Acquisition for Debt

On January 15, AbCo purchases a building for $40,000 cash and a

$160,000 note payable.

GENERAL JOURNAL

Date Description Debit Credit

Jan 15 Building 200,000

Cash 40,000

Note Payable 160,000

Mastering DepreciationSlide 14

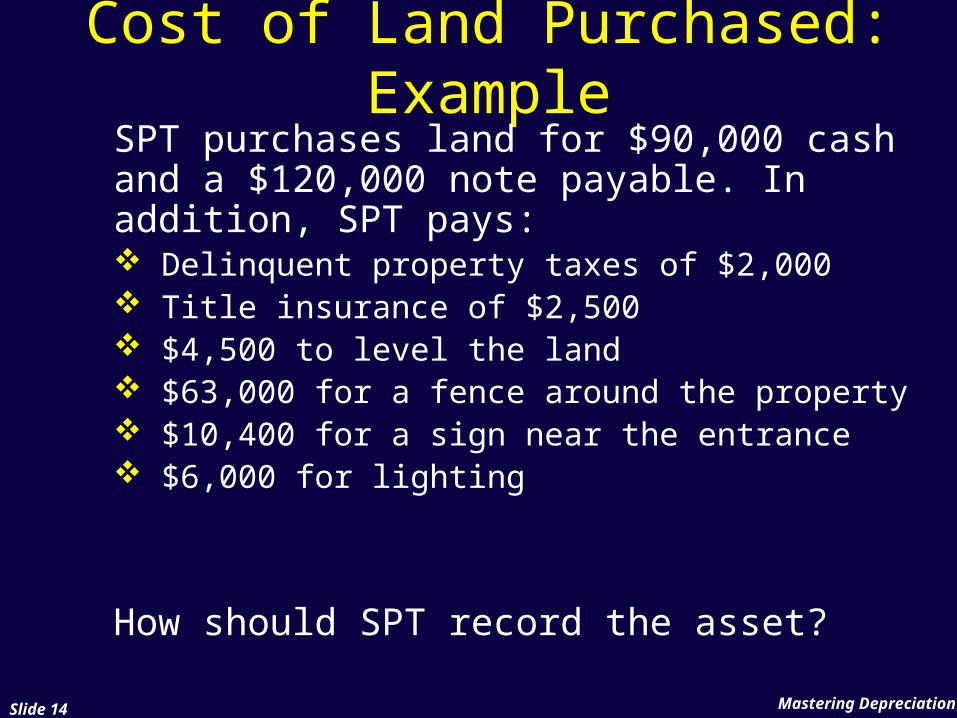

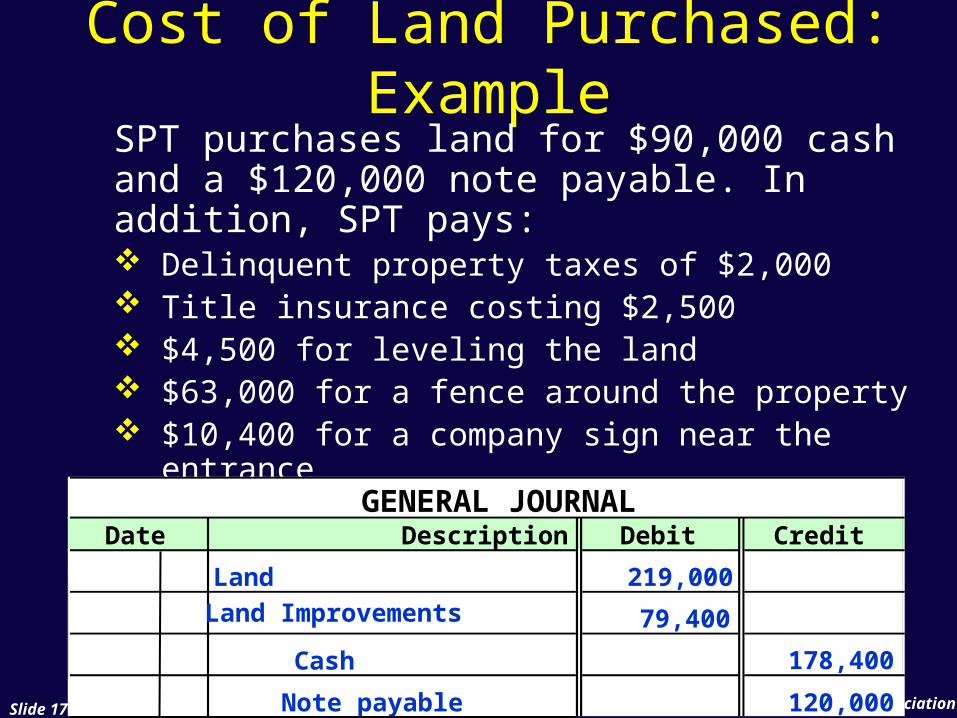

Cost of Land Purchased: Example

SPT purchases land for $90,000 cash and a $120,000 note payable. In addition, SPT pays: Delinquent property taxes of $2,000 Title insurance of $2,500 $4,500 to level the land $63,000 for a fence around the property $10,400 for a sign near the entrance $6,000 for lighting

How should SPT record the asset?

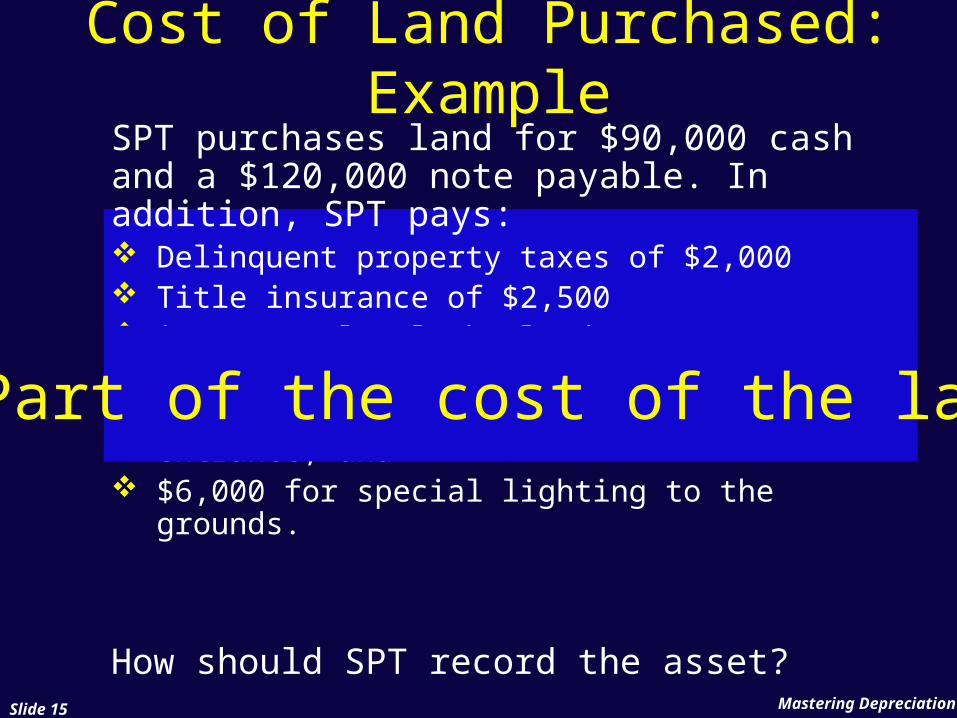

SPT purchases land for $90,000 cash and a $120,000 note payable. In addition, SPT pays: Delinquent property taxes of $2,000 Title insurance of $2,500 $4,500 to level the land $63,000 for a fence around the property; $10,400 for a company sign near the

entrance; and $6,000 for special lighting to the grounds.

How should SPT record the asset?Mastering DepreciationSlide 15

Cost of Land Purchased: Example

Part of the cost of the land

SPT purchases land for $90,000 cash and a $120,000 note payable. In addition, SPT pays: Delinquent property taxes of $2,000 Title insurance costing $2,500 $4,500 for leveling the land; $63,000 for a fence around the property $10,400 for a company sign near the

entrance $6,000 for special lighting to the grounds

How should SPT record the asset?Mastering DepreciationSlide 16

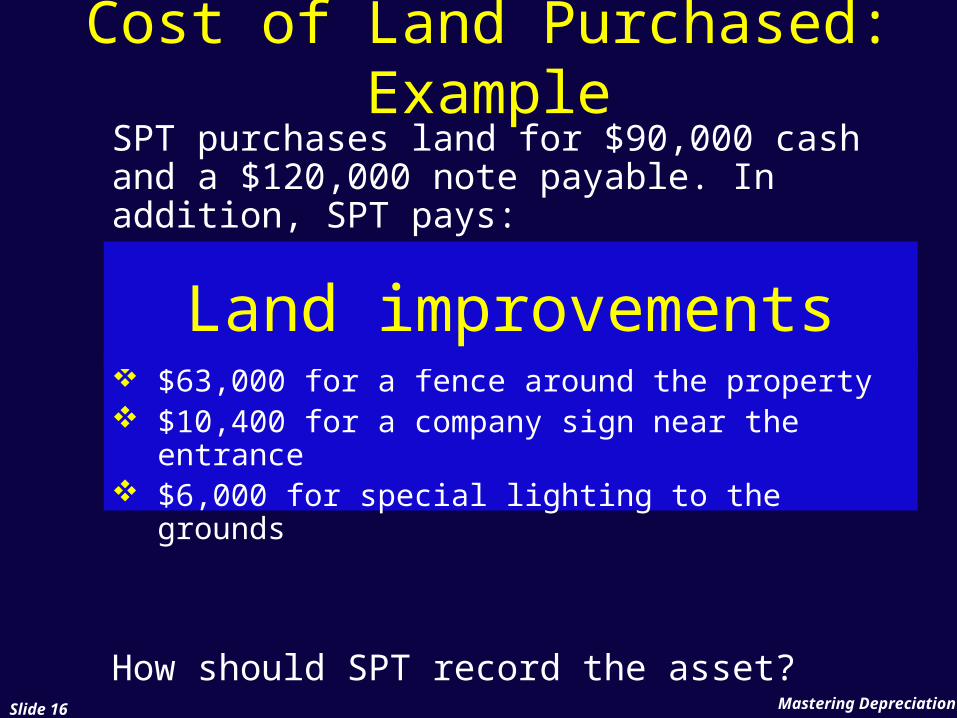

Cost of Land Purchased: Example

Land improvements

Mastering DepreciationSlide 17

Cost of Land Purchased: Example

SPT purchases land for $90,000 cash and a $120,000 note payable. In addition, SPT pays: Delinquent property taxes of $2,000 Title insurance costing $2,500 $4,500 for leveling the land $63,000 for a fence around the property $10,400 for a company sign near the

entrance $6,000 for special lighting to the grounds

GENERAL JOURNAL

Date Description Debit Credit

Land 219,000

Cash

79,400

Note payable

178,400

Land Improvements

120,000

Mastering DepreciationSlide 18

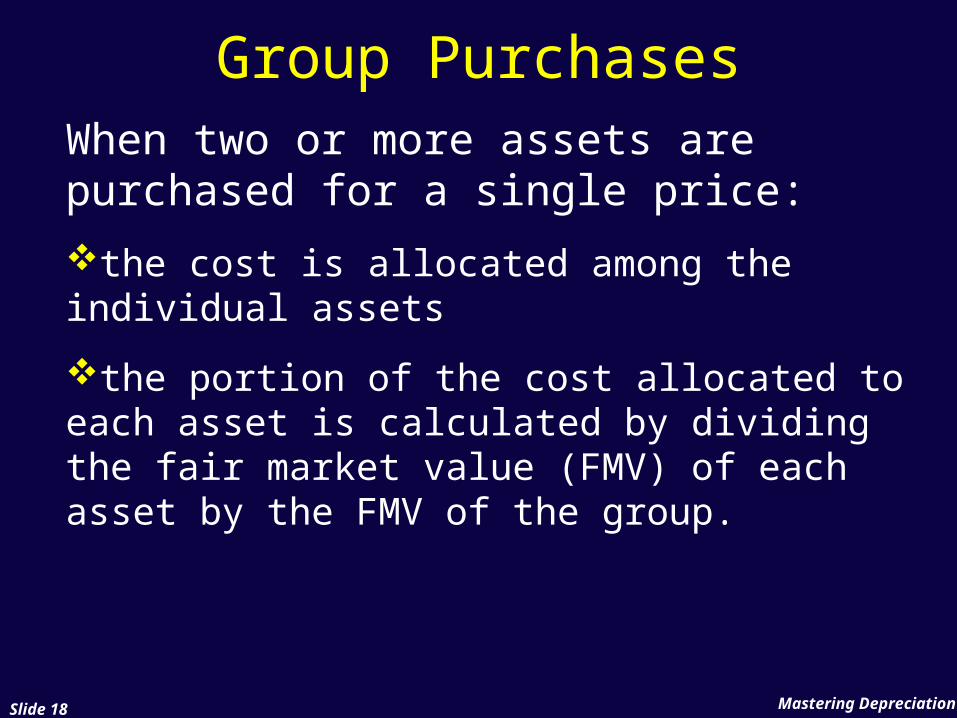

Group PurchasesWhen two or more assets are purchased for a single price:

the cost is allocated among the individual assets

the portion of the cost allocated to each asset is calculated by dividing the fair market value (FMV) of each asset by the FMV of the group.

Mastering DepreciationSlide 19

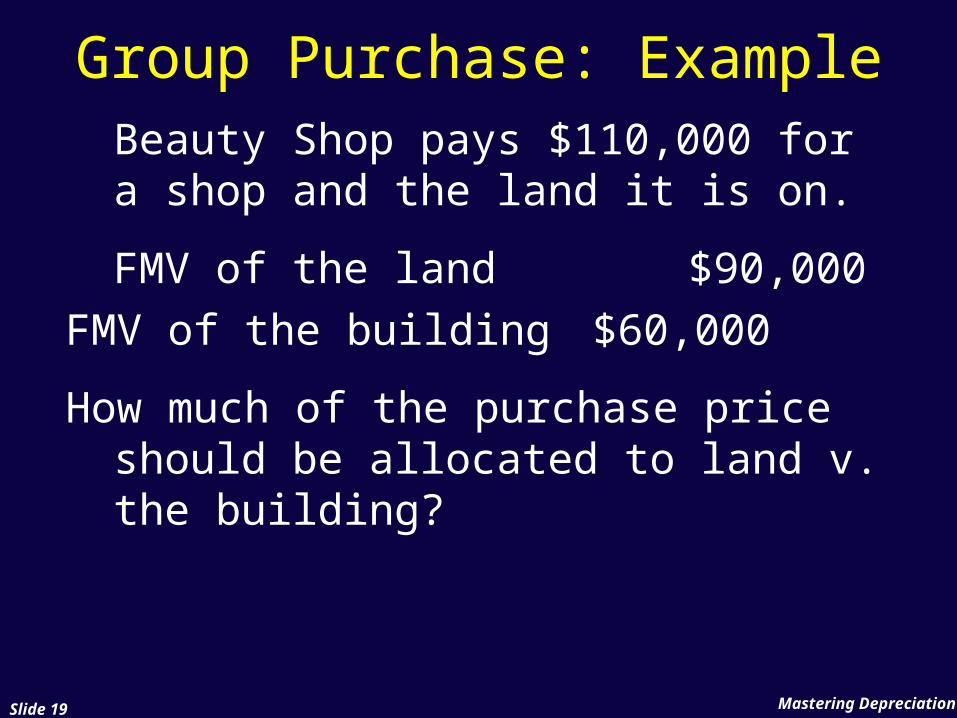

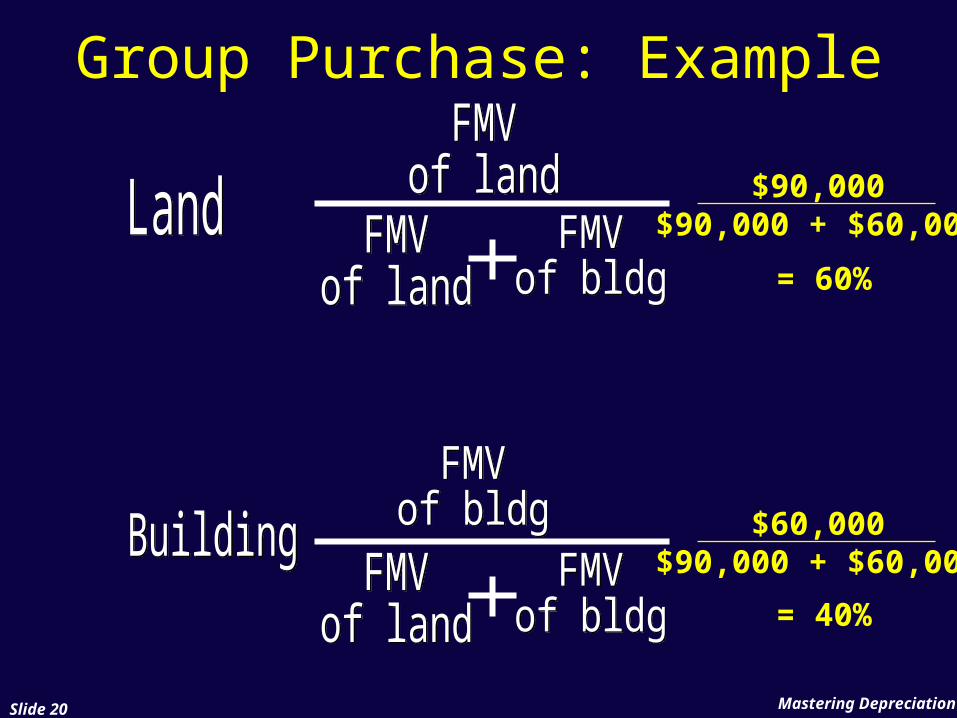

Group Purchase: ExampleBeauty Shop pays $110,000 for a shop and the land it is on.

FMV of the land $90,000 FMV of the building $60,000

How much of the purchase price should be allocated to land v. the building?

Mastering DepreciationSlide 20

Group Purchase: Example

$90,000$90,000 + $60,000

$60,000$90,000 + $60,000

= 60%

= 40%

Mastering DepreciationSlide 21

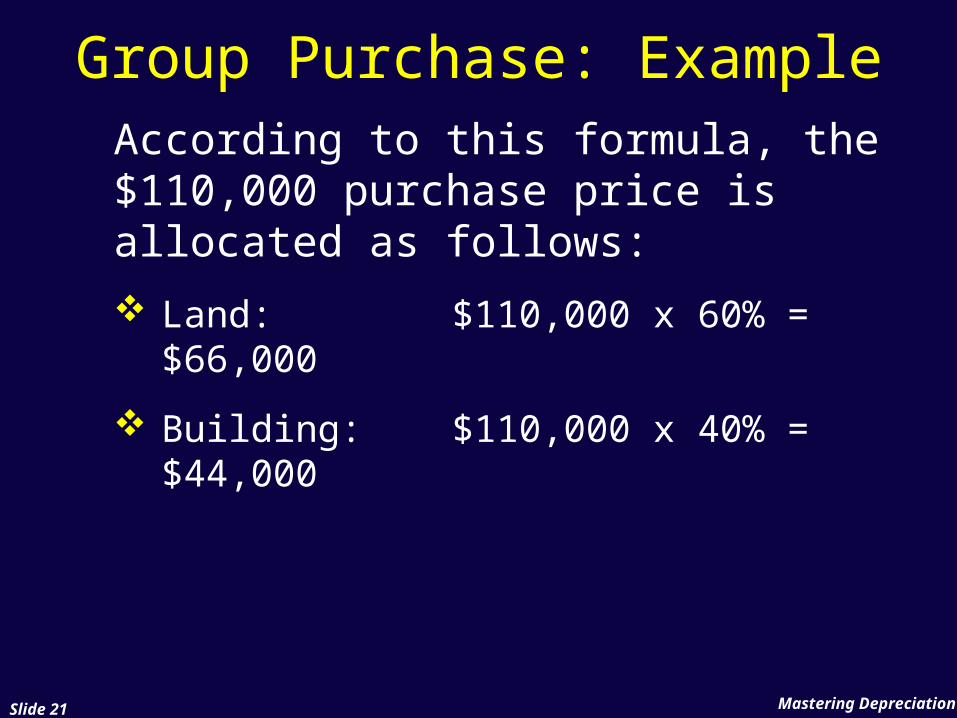

Group Purchase: ExampleAccording to this formula, the $110,000 purchase price is allocated as follows:

Land: $110,000 x 60% = $66,000

Building: $110,000 x 40% = $44,000

Mastering DepreciationSlide 22

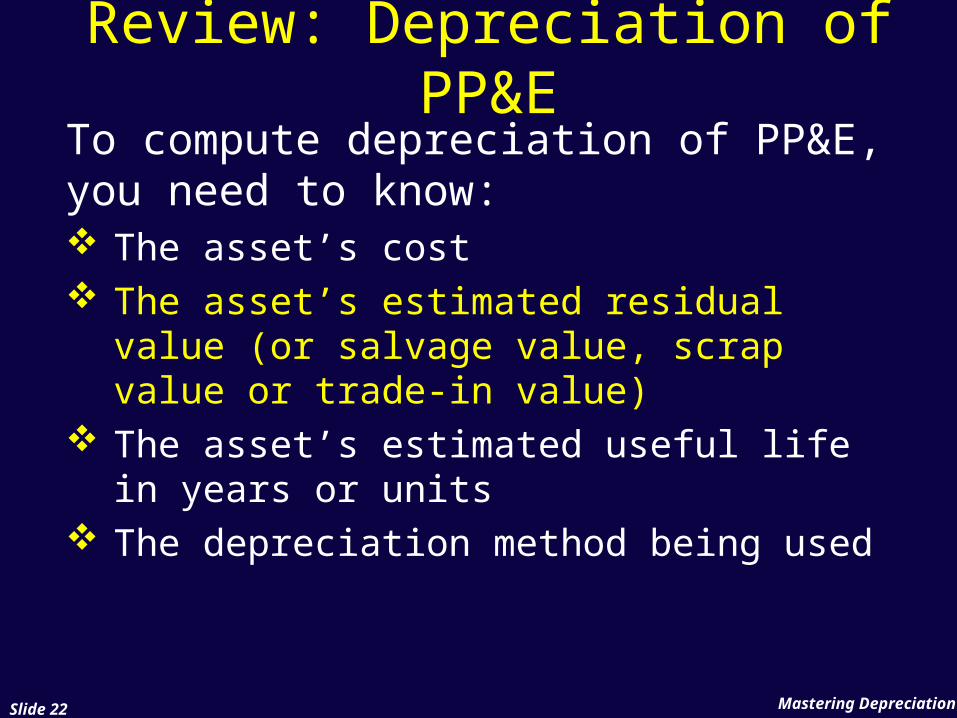

Review: Depreciation of PP&E

To compute depreciation of PP&E, you need to know: The asset’s cost The asset’s estimated residual value (or

salvage value, scrap value or trade-in value)

The asset’s estimated useful life in years or units

The depreciation method being used

Mastering DepreciationSlide 23

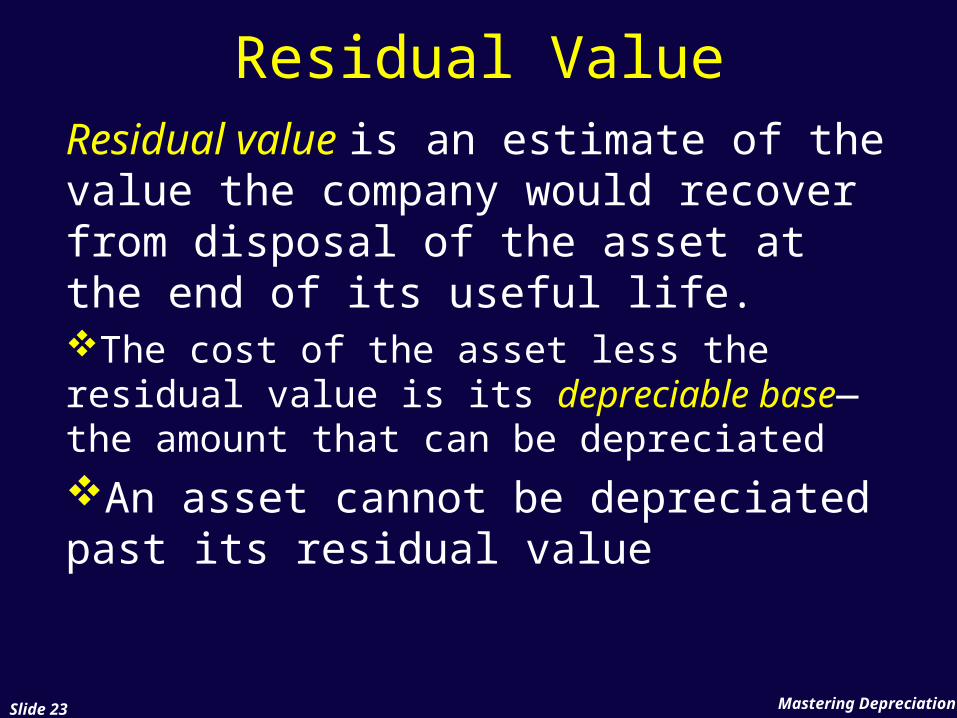

Residual ValueResidual value is an estimate of the value the company would recover from disposal of the asset at the end of its useful life.The cost of the asset less the residual value is its depreciable base—the amount that can be depreciatedAn asset cannot be depreciated past its residual value

Mastering DepreciationSlide 24

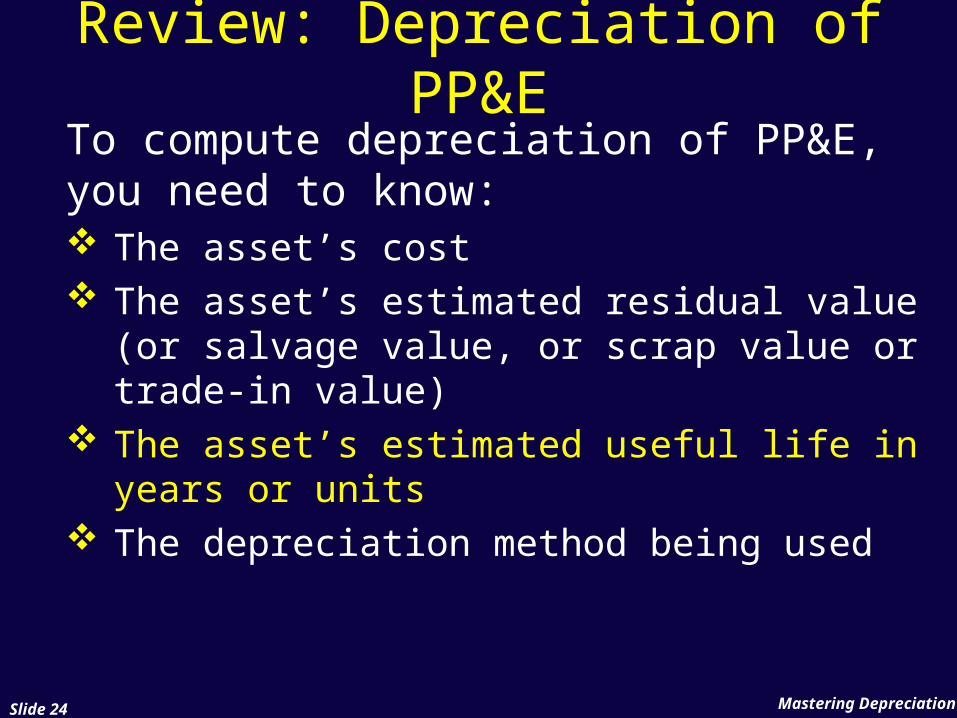

Review: Depreciation of PP&E

To compute depreciation of PP&E, you need to know: The asset’s cost The asset’s estimated residual value (or

salvage value, or scrap value or trade-in value)

The asset’s estimated useful life in years or units

The depreciation method being used

Mastering DepreciationSlide 25

Useful LifeThe useful life of a plant asset is:

The estimated years that the asset will produce or

The number of units (items, miles, etc.) that the company expects the asset to produce

Mastering DepreciationSlide 26

Review: Depreciation of PP&E

To compute depreciation of PP&E, you need to know: The asset’s cost The asset’s estimated residual value (or

salvage value, or scrap value or trade-in value)

The asset’s estimated useful life in years or units

The depreciation method being used

Mastering DepreciationSlide 27

Depreciation MethodsThere are four depreciation methods.

1. Straight-line (SL)

2. Units of production (UOP)

3. Double-declining balance (DDB)

4. Sum-of-the-years’ digits (SYD)

Each method results in the same amount of total depreciation over the life of the asset.

Mastering DepreciationSlide 28

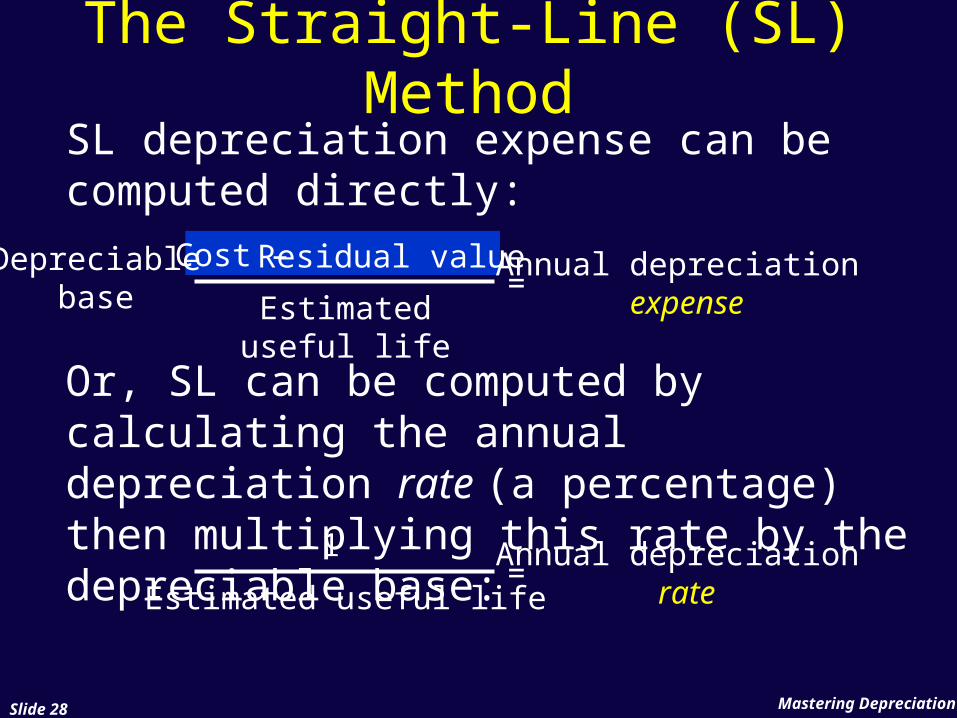

The Straight-Line (SL) Method

SL depreciation expense can be computed directly:

Or, SL can be computed by calculating the annual depreciation rate (a percentage) then multiplying this rate by the depreciable base:

Cost – Residual value

Estimated useful life

=Annual depreciation

expenseDepreciable

base

1

Estimated useful life=Annual depreciation

rate

Mastering DepreciationSlide 29

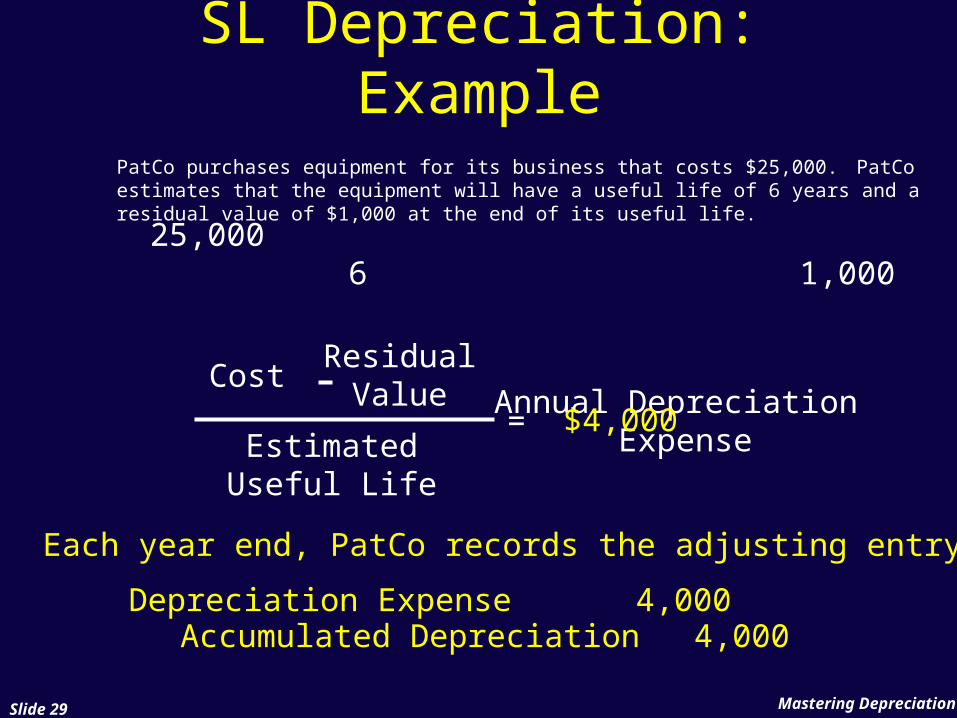

SL Depreciation: Example

PatCo purchases equipment for its business that costs $25,000. PatCo estimates that the equipment will have a useful life of 6 years and a residual value of $1,000 at the end of its useful life.

CostResidual

Value

EstimatedUseful Life

=Annual Depreciation

Expense

25,0001,0006

$4,000

Each year end, PatCo records the adjusting entry:

Depreciation ExpenseAccumulated Depreciation

4,0004,000

Mastering DepreciationSlide 30

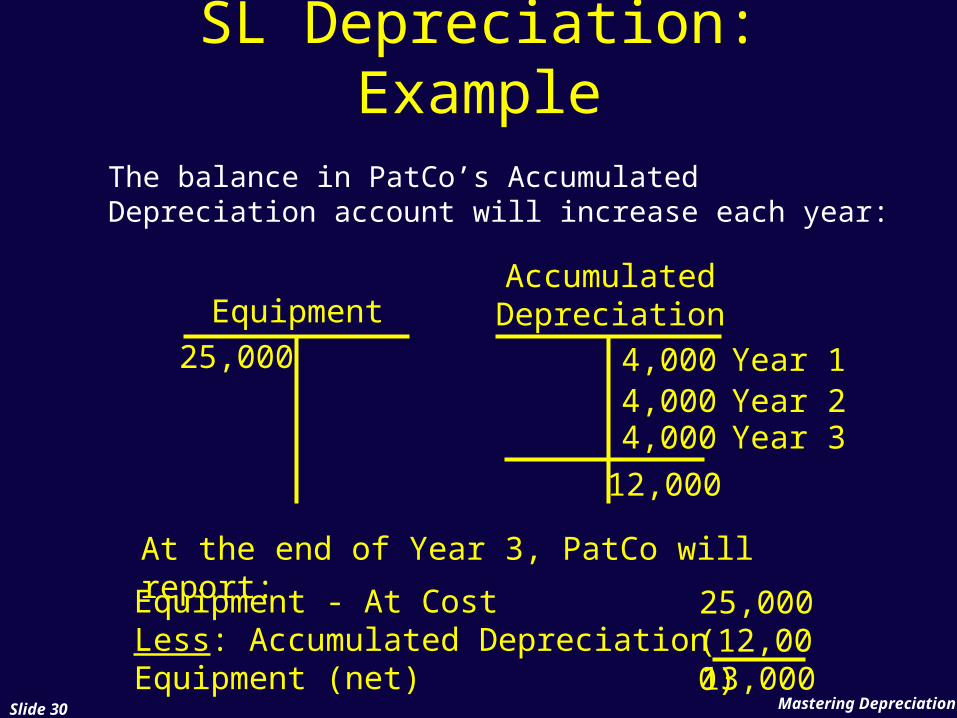

SL Depreciation: Example

The balance in PatCo’s Accumulated Depreciation account will increase each year:

At the end of Year 3, PatCo will report:

EquipmentAccumulatedDepreciation

25,000 4,000 Year 14,000 Year 24,000 Year 3

12,000

25,000(12,000)13,000

Equipment - At CostLess: Accumulated DepreciationEquipment (net)

Mastering DepreciationSlide 31

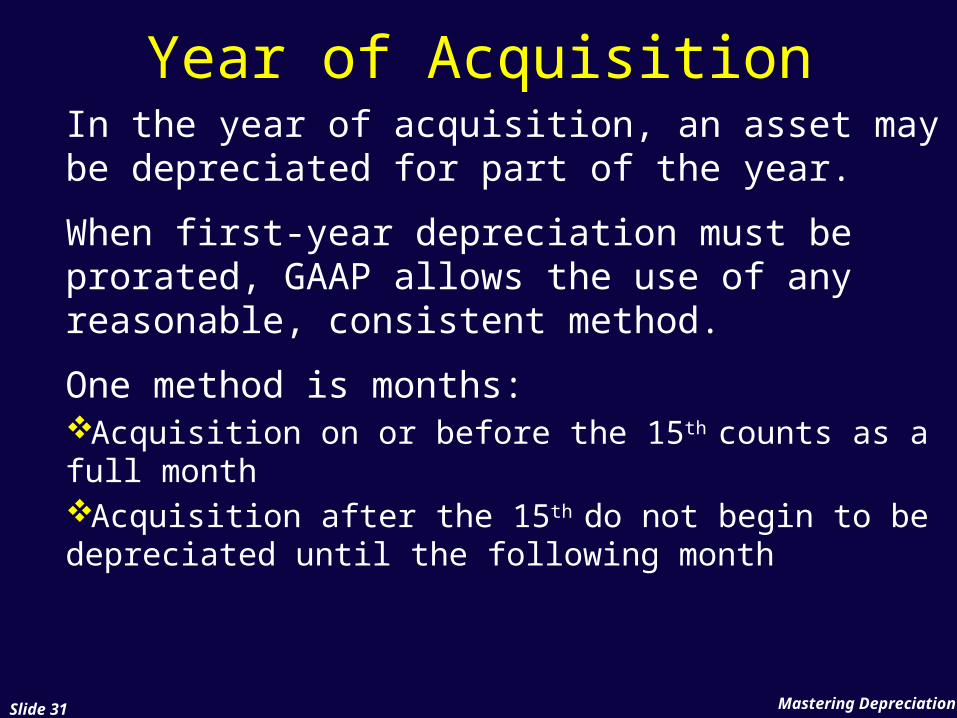

Year of AcquisitionIn the year of acquisition, an asset may be depreciated for part of the year.

When first-year depreciation must be prorated, GAAP allows the use of any reasonable, consistent method.

One method is months:Acquisition on or before the 15th counts as a full monthAcquisition after the 15th do not begin to be depreciated until the following month

Mastering DepreciationSlide 32

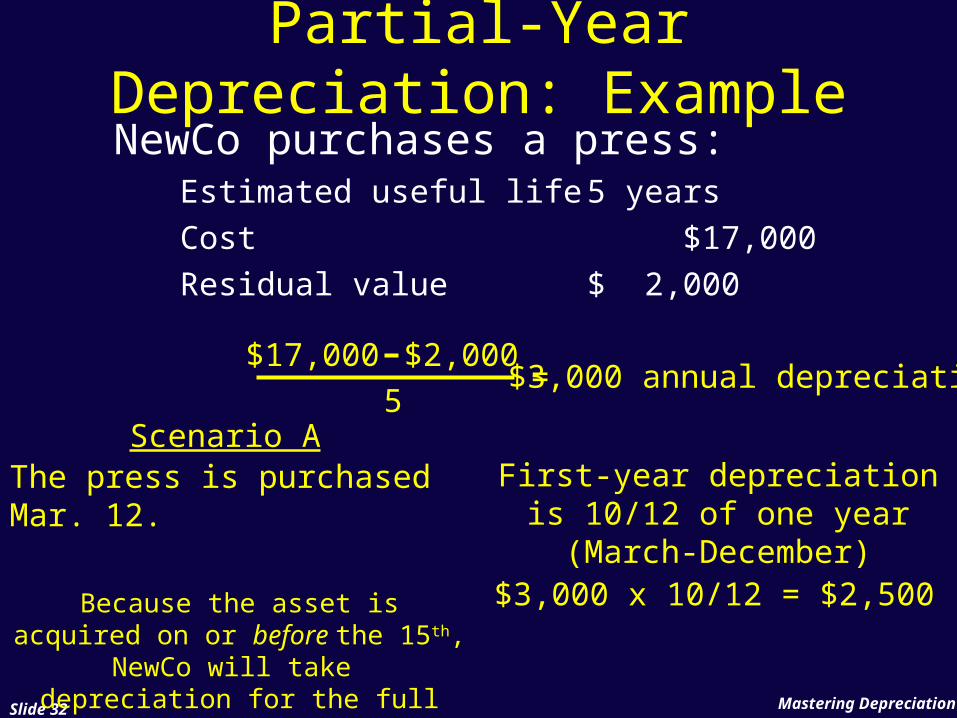

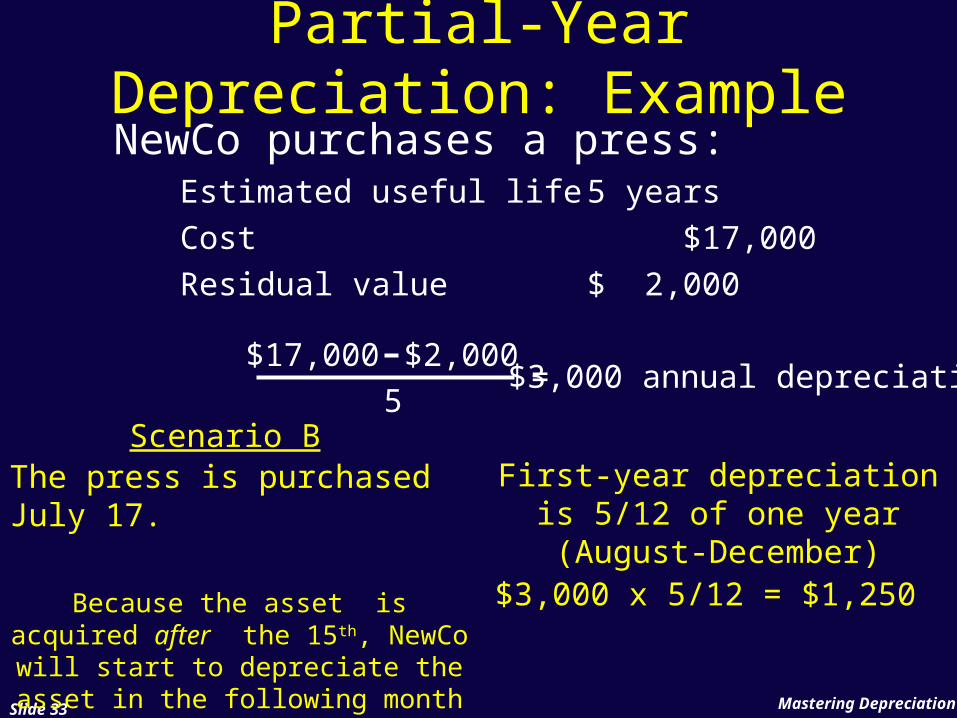

Partial-Year Depreciation: Example

NewCo purchases a press:Estimated useful life 5 yearsCost $17,000Residual value $ 2,000

Scenario AThe press is purchased Mar. 12.

Because the asset is acquired on or before the 15th, NewCo will take depreciation for the full

month

First-year depreciation is 10/12 of one year (March-

December)

$17,000 $2,0005

=$3,000 annual depreciation

$3,000 x 10/12 = $2,500

Mastering DepreciationSlide 33

NewCo purchases a press:Estimated useful life 5 yearsCost $17,000Residual value $ 2,000

Scenario BThe press is purchased July 17.

Because the asset is acquired after the 15th, NewCo will start to

depreciate the asset in the following month

First-year depreciation is 5/12 of one year (August-

December)

$17,000 $2,0005

=$3,000 annual depreciation

$3,000 x 5/12 = $1,250

Partial-Year Depreciation: Example

Mastering DepreciationSlide 34

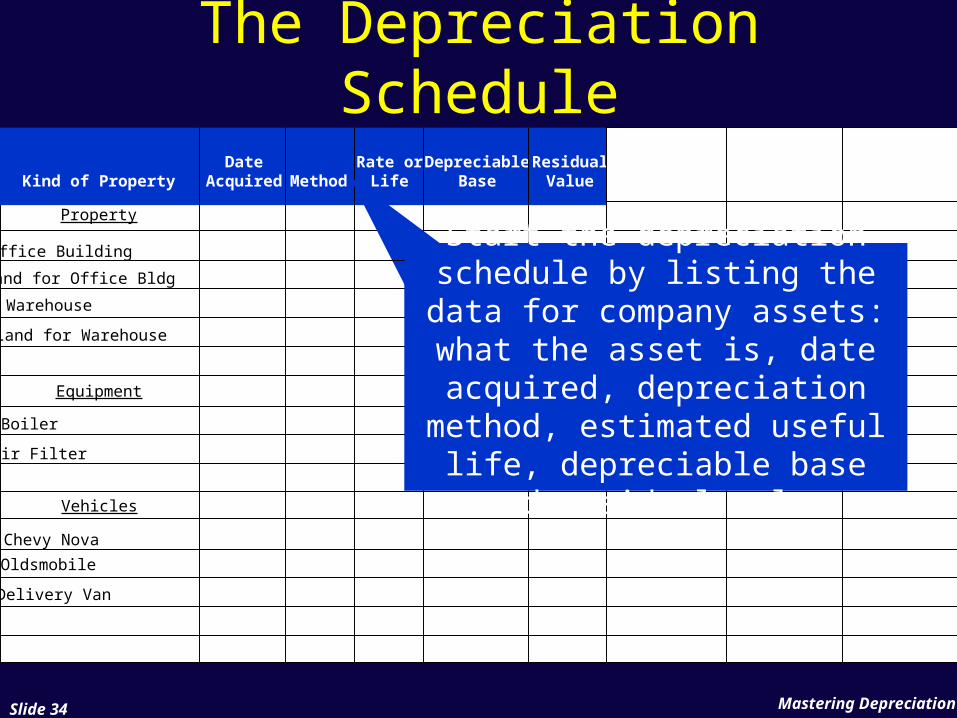

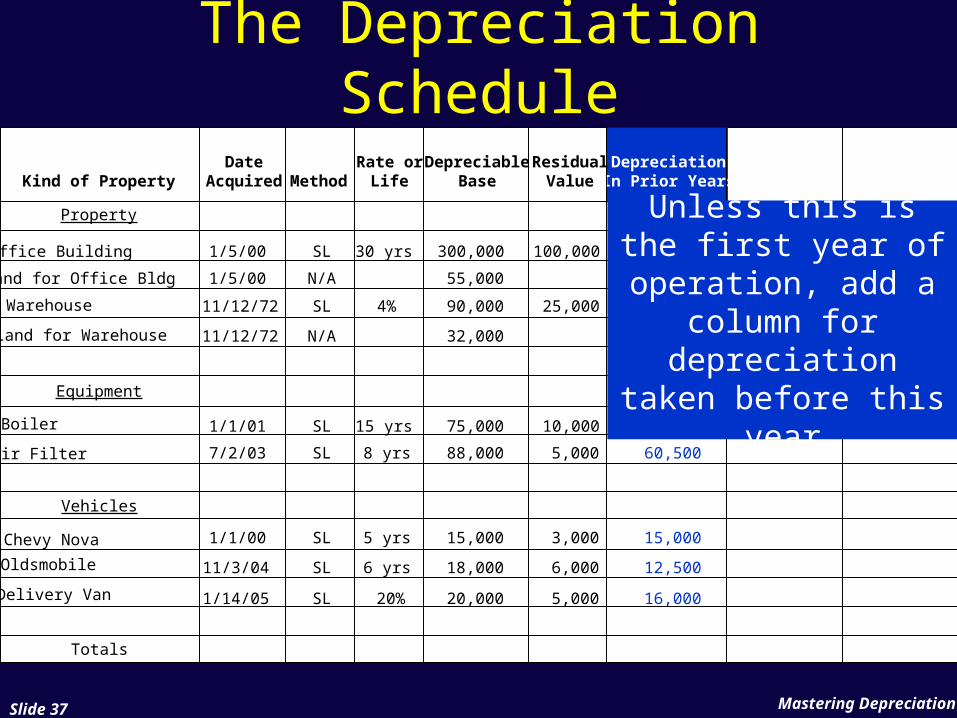

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

Start the depreciation schedule by listing the data

for company assets: what the asset is, date acquired, depreciation method, estimated useful life,

depreciable base and residual value

Property

Equipment

Vehicles

Office Building

Land for Office Bldg

Warehouse

Land for Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

Mastering DepreciationSlide 35

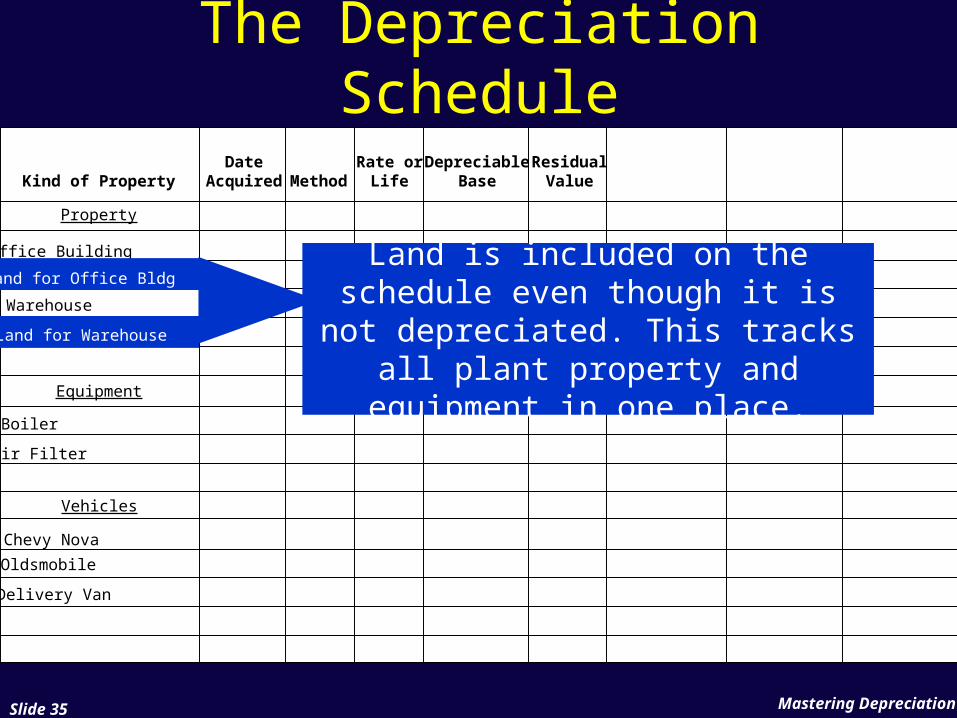

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

Land is included on the schedule even though it is not depreciated. This tracks all plant property and

equipment in one place.

Property

Equipment

Vehicles

Office Building

Land for Office Bldg

Warehouse

Land for Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

ResidualValue

Mastering DepreciationSlide 36

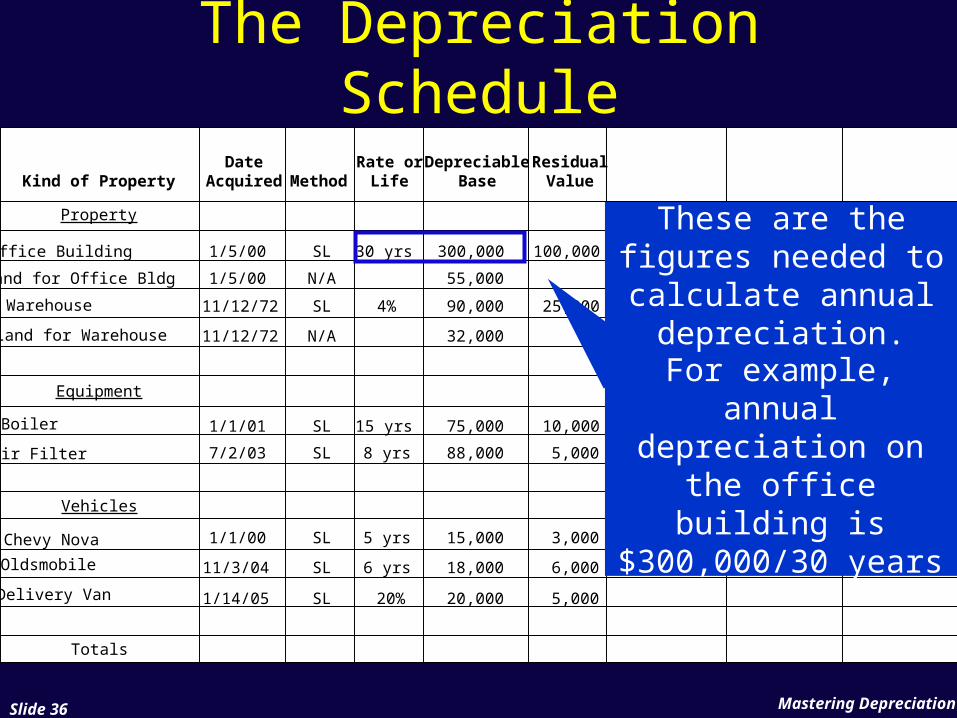

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

Property

Equipment

Vehicles

Totals

Office Building

Land for Office Bldg

Warehouse

Land for Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

4%

15 yrs

8 yrs

5 yrs

6 yrs

20%

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

5,000

These are the figures needed to calculate annual

depreciation.For example, annual depreciation on the

office building is$300,000/30 years

Mastering DepreciationSlide 37

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

Property

Equipment

Vehicles

Totals

Office Building

Land for Office Bldg

Warehouse

Land for Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

90,000

90,000

40,000

60,500

15,000

12,500

16,0005,000

Unless this is the first year of

operation, add a column for

depreciation taken before this year

4%

20%

Mastering DepreciationSlide 38

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

Property

Equipment

Vehicles

Totals

Office Building

Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

90,000

90,000

40,000

60,500

15,000

12,500

16,0005,000

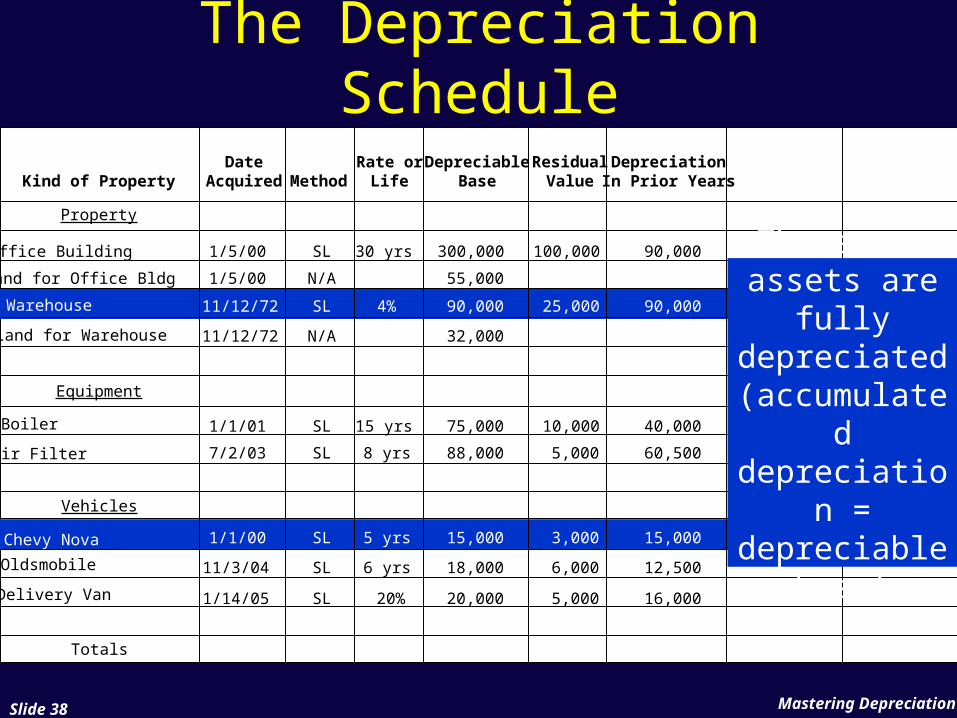

These two assets are

fully depreciated (accumulate

d depreciation

=depreciable

base)

Land for Office Bldg

Land for Warehouse

4%

20%

Mastering DepreciationSlide 39

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

Property

Equipment

Vehicles

Totals

Office Building

Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

5,000

90,000

90,000

40,000

60,500

15,000

12,500

16,000

10,000

5,000

11,000

3,000

4,000

300,00030

75,00015

88,0008

18,0006

20,000x 20%

This column is current-

year depreciation

Land for Office Bldg

Land for Warehouse

4%

20%

Mastering DepreciationSlide 40

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Property

Equipment

Vehicles

Totals

Office Building

Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

5,000

90,000

90,000

40,000

60,500

15,000

12,500

16,000

10,000

5,000

11,000

3,000

4,000

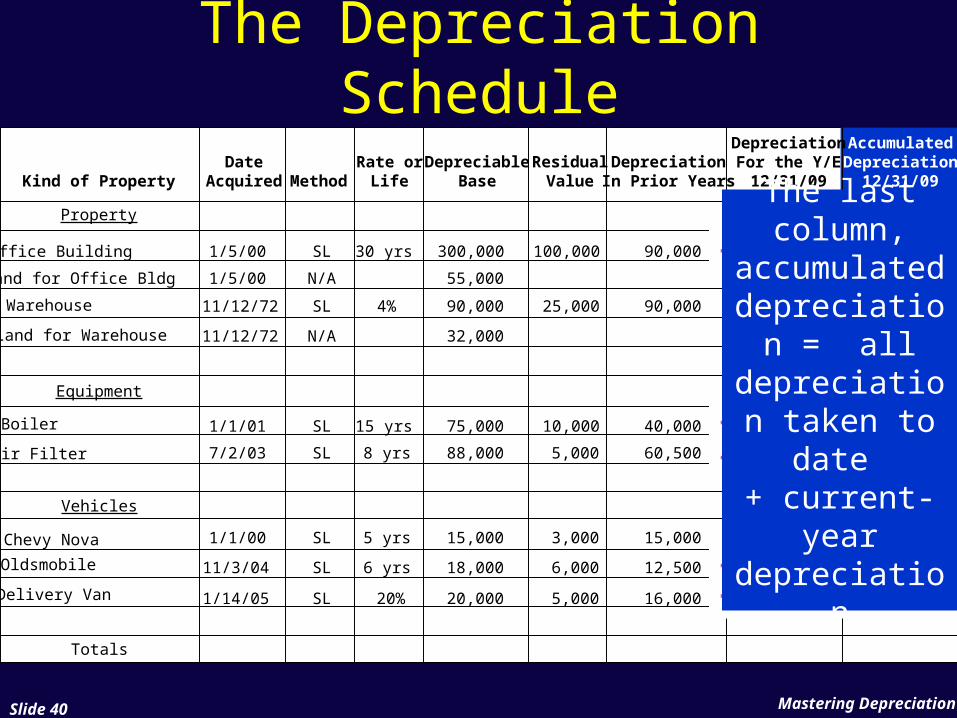

100,000

90,000

45,000

71,500

15,000

15,500

20,000

+ =

+ =+ =

+ =+ =

Land for Office Bldg

Land for Warehouse

4%

20%

The last column,

accumulated depreciation

= all depreciation taken to date

+ current-year

depreciation

Mastering DepreciationSlide 41

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Property

Equipment

Vehicles

Totals

Office Building

Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

4%

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

5,000

90,000

90,000

40,000

60,500

15,000

12,500

16,000

10,000

5,000

11,000

3,000

4,000

100,000

90,000

45,000

71,500

15,000

15,500

20,000

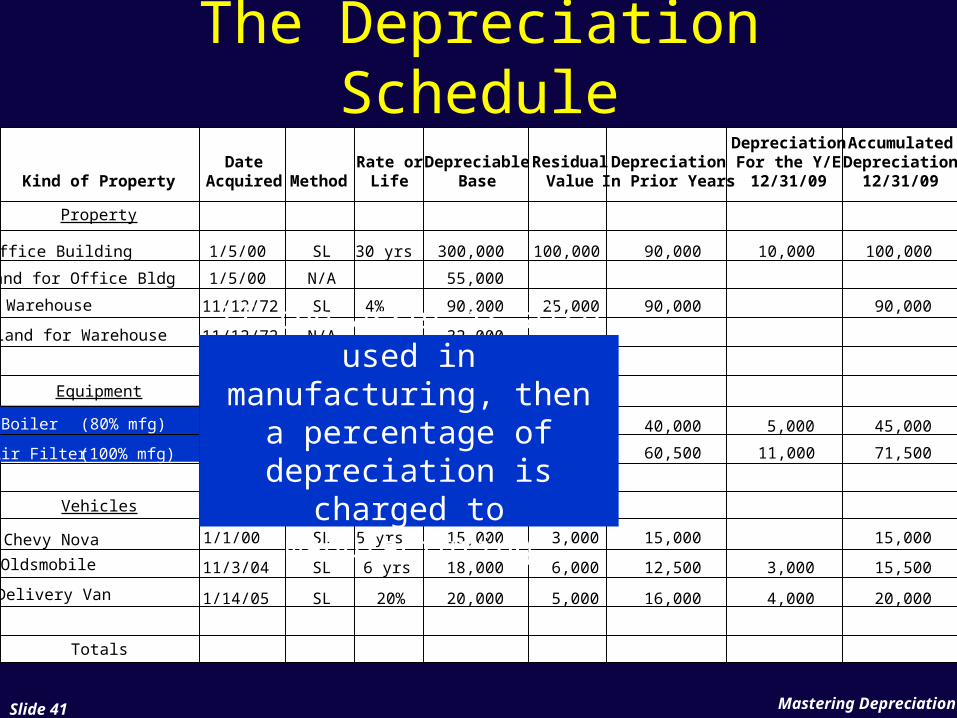

If the asset is also used in manufacturing, then a

percentage of depreciation is charged

to manufacturing

(80% mfg)

(100% mfg)

Land for Office Bldg

Land for Warehouse

20%

Mastering DepreciationSlide 42

Depreciation for Manufacturers

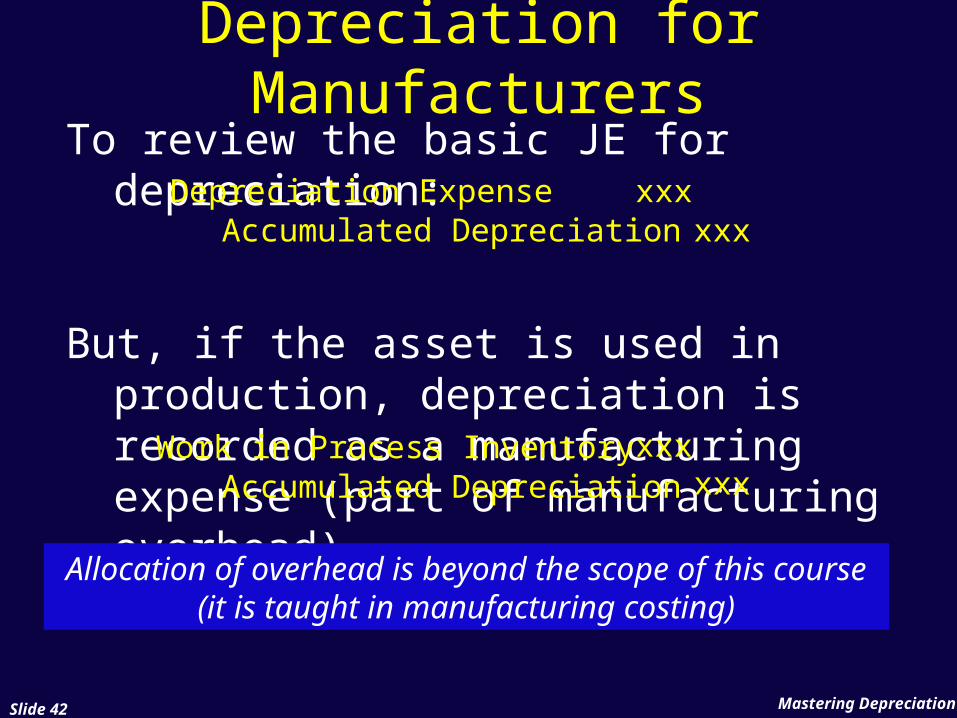

To review the basic JE for depreciation:

But, if the asset is used in production, depreciation is recorded as a manufacturing expense (part of manufacturing overhead)

Allocation of overhead is beyond the scope of this course (it is taught in manufacturing costing)

Depreciation ExpenseAccumulated Depreciation

xxxxxx

Work in Process InventoryAccumulated Depreciation

xxxxxx

Mastering DepreciationSlide 43

The Depreciation Schedule

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Property

Equipment

Vehicles

Totals

Office Building

Warehouse

Boiler

Air Filter

Chevy Nova

Oldsmobile

Delivery Van

1/5/00

1/5/00

11/12/72

11/12/72

1/1/01

7/2/03

1/1/00

11/3/04

1/14/05

SL

N/A

SL

N/A

SL

SL

SL

SL

SL

30 yrs

4%

15 yrs

8 yrs

5 yrs

6 yrs

300,000

55,000

90,000

32,000

75,000

88,000

15,000

18,000

20,000

100,000

25,000

10,000

5,000

3,000

6,000

5,000

90,000

90,000

40,000

60,500

15,000

12,500

16,000

10,000

5,000

11,000

3,000

4,000

100,000

90,000

45,000

71,500

15,000

15,500

20,000

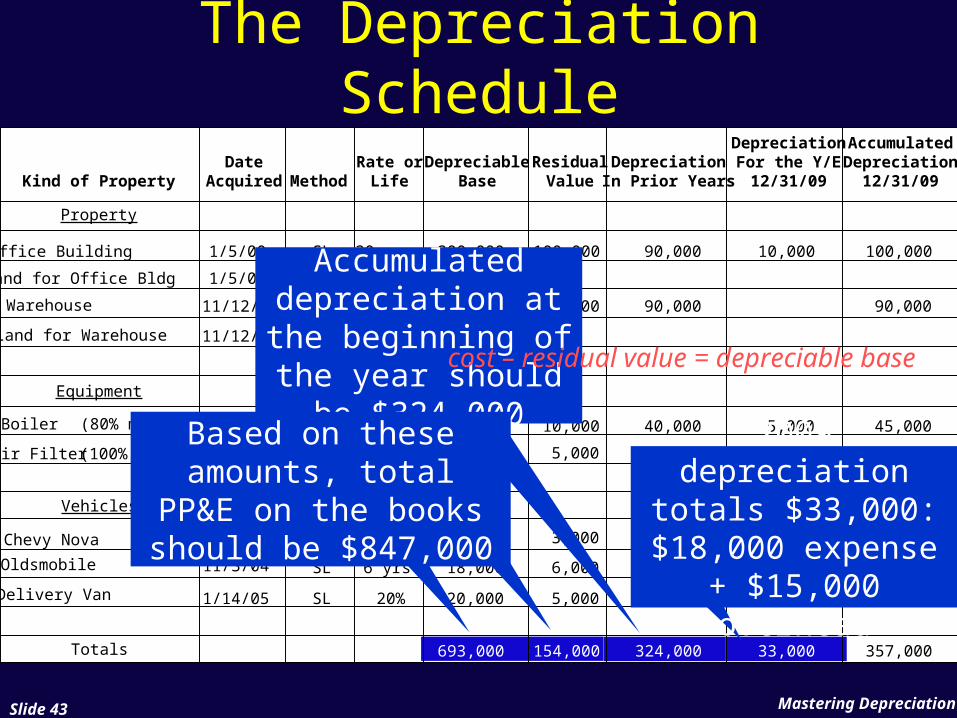

693,000 154,000 324,000 33,000 357,000

(80% mfg)

(100% mfg)

Accumulated depreciation at the

beginning of the year should be

$324,0002009 depreciation

totals $33,000: $18,000 expense

+ $15,000 overhead

Land for Office Bldg

Land for Warehouse

cost – residual value = depreciable base

20%

Based on these amounts, total PP&E on the books should

be $847,000

Mastering DepreciationSlide 44

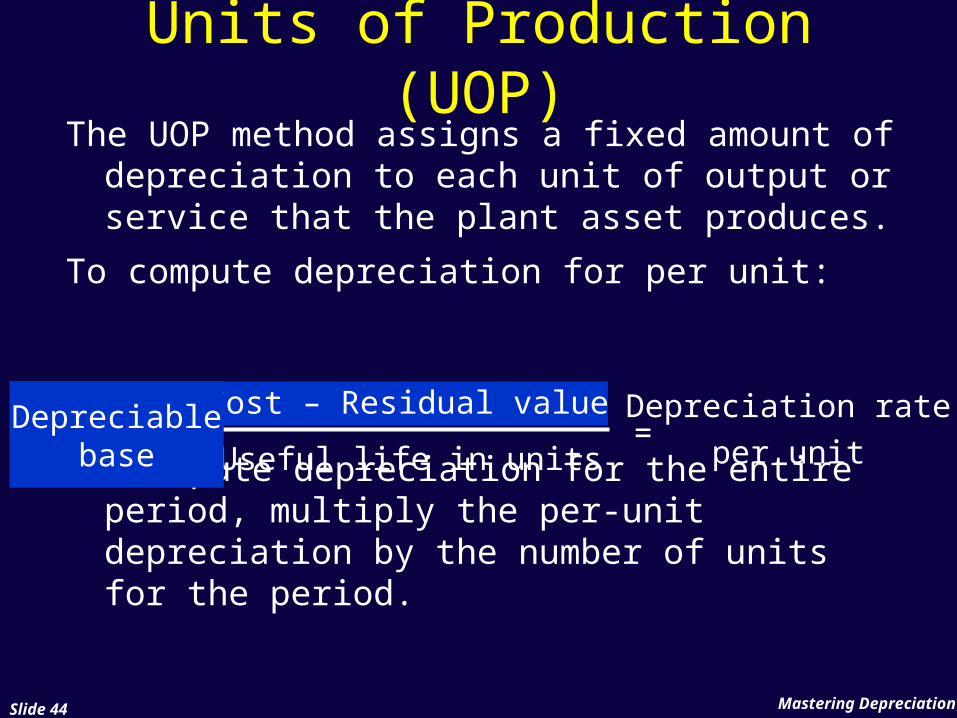

Units of Production (UOP)The UOP method assigns a fixed amount of

depreciation to each unit of output or service that the plant asset produces.

To compute depreciation for per unit:

To compute depreciation for the entire period, multiply the per-unit depreciation by the number of units for the period.

Cost – Residual value

Useful life in unitsDepreciable

base

Depreciation rateper unit

=

Depreciation rateper unit$0.20 per mile

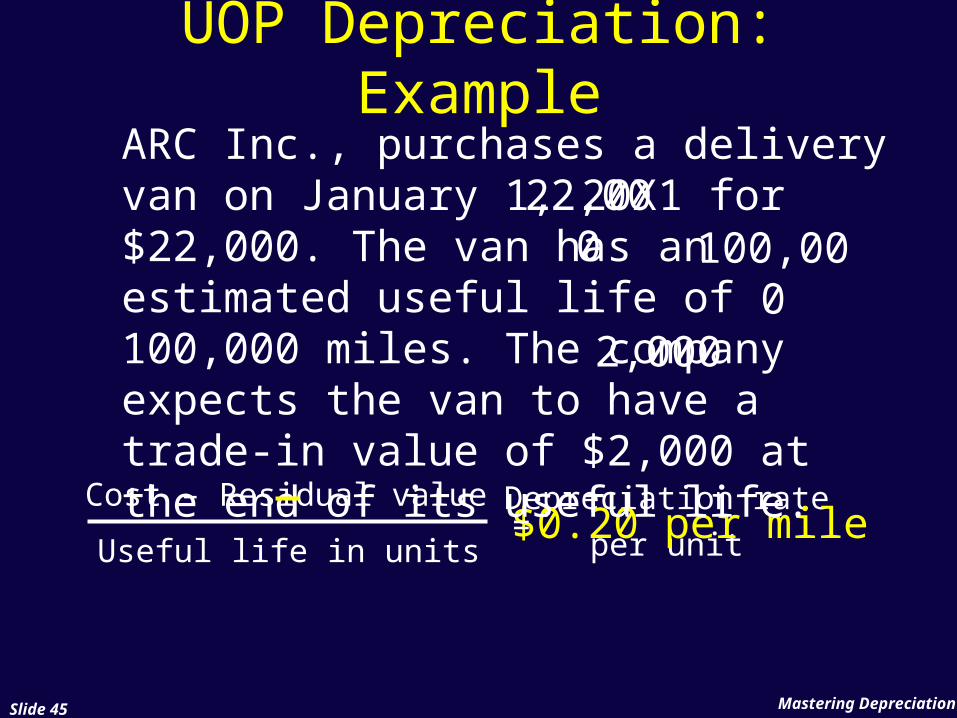

Mastering DepreciationSlide 45

UOP Depreciation: ExampleARC Inc., purchases a delivery van on January 1, 20X1 for $22,000. The van has an estimated useful life of 100,000 miles. The company expects the van to have a trade-in value of $2,000 at the end of its useful life.

22,000 100,00

02,000

Cost – Residual value

Useful life in units=

Mastering DepreciationSlide 46

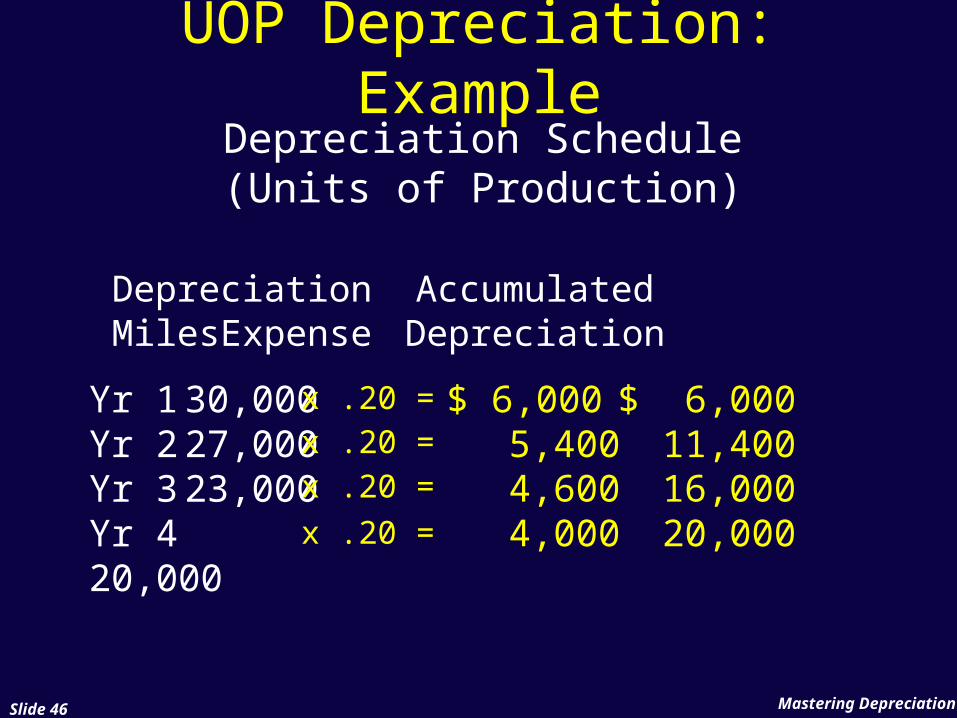

UOP Depreciation: ExampleDepreciation Schedule(Units of Production)

DepreciationAccumulatedMiles Expense Depreciation

Yr 1 30,000Yr 2 27,000Yr 3 23,000Yr 4 20,000

$ 6,000 $ 6,000 5,400 11,400 4,600 16,000 4,000 20,000

x .20 =x .20 =x .20 =x .20 =

Mastering DepreciationSlide 47

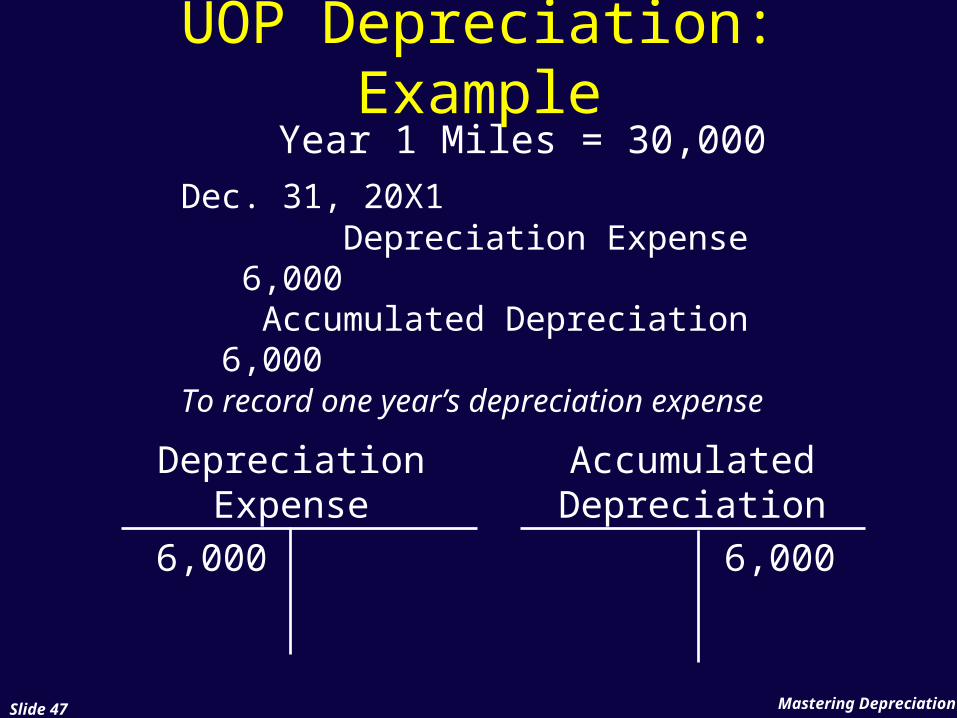

UOP Depreciation: ExampleYear 1 Miles = 30,000

Dec. 31, 20X1 Depreciation Expense 6,000 Accumulated Depreciation 6,000 To record one year’s depreciation expense

DepreciationExpense

AccumulatedDepreciation

6,000 6,000

Mastering DepreciationSlide 48

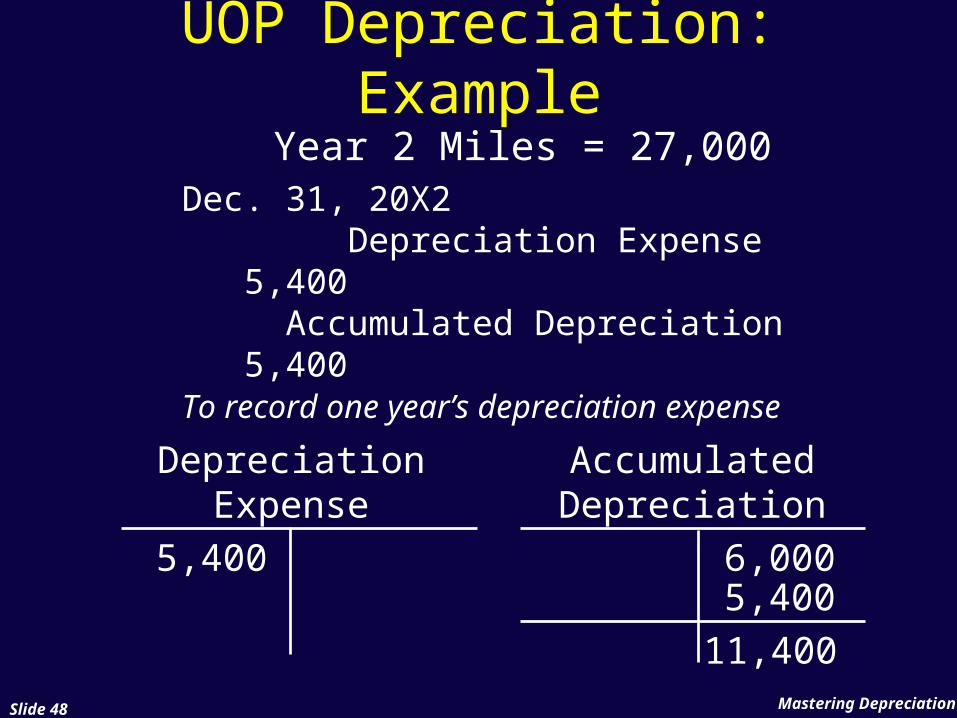

UOP Depreciation: Example

DepreciationExpense

AccumulatedDepreciation

5,400 6,0005,400

11,400

Year 2 Miles = 27,000Dec. 31, 20X2 Depreciation Expense 5,400 Accumulated Depreciation 5,400To record one year’s depreciation expense

Mastering DepreciationSlide 49

Year of AcquisitionUnder UOP, there is no need to

compute partial year depreciation because this method is based on production—not time.

Mastering DepreciationSlide 50

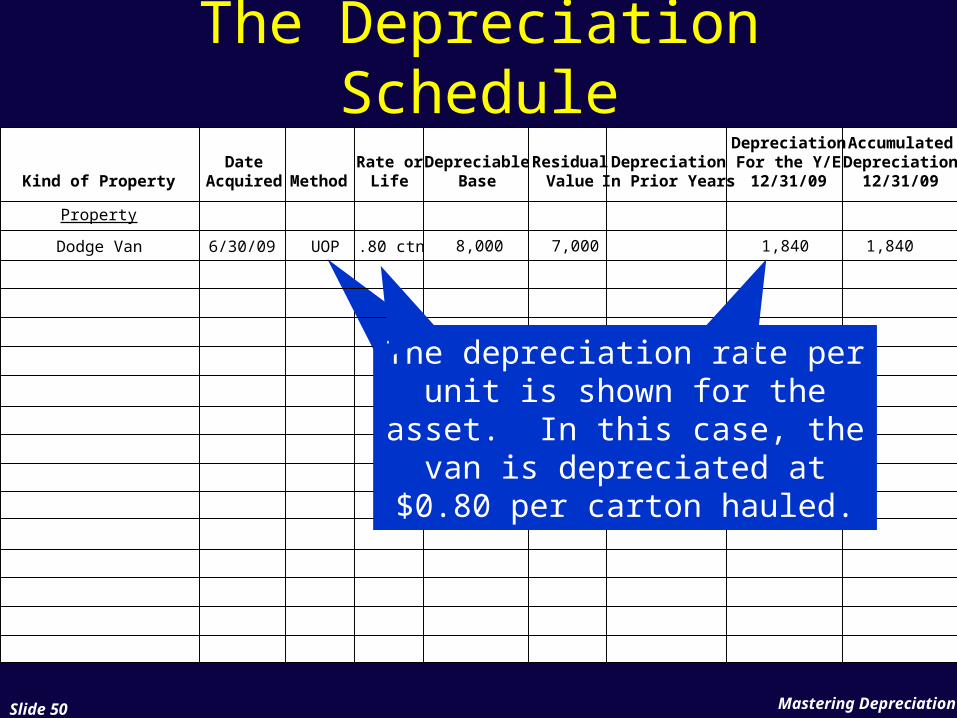

The Depreciation Schedule

If the van is used to deliver 2,300 cartons, the

depreciation expense is 2,300 x $0.80 = $1,840

An asset being depreciated using units of production is

easily shown on the depreciation schedule.

The depreciation rate per unit is shown for the asset. In this case, the van is depreciated at $0.80 per carton hauled.

Property

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Dodge Van 6/30/09 UOP .80 ctn 8,000 7,000 1,840 1,840

Mastering DepreciationSlide 51

The Declining Balance Method

Declining balance (DB) is an accelerated method that yields higher depreciation in the early years and lower depreciation in later years.

Generally, the DB method is used for an asset that will be more productive (generate more revenue) early in its life.

Mastering DepreciationSlide 52

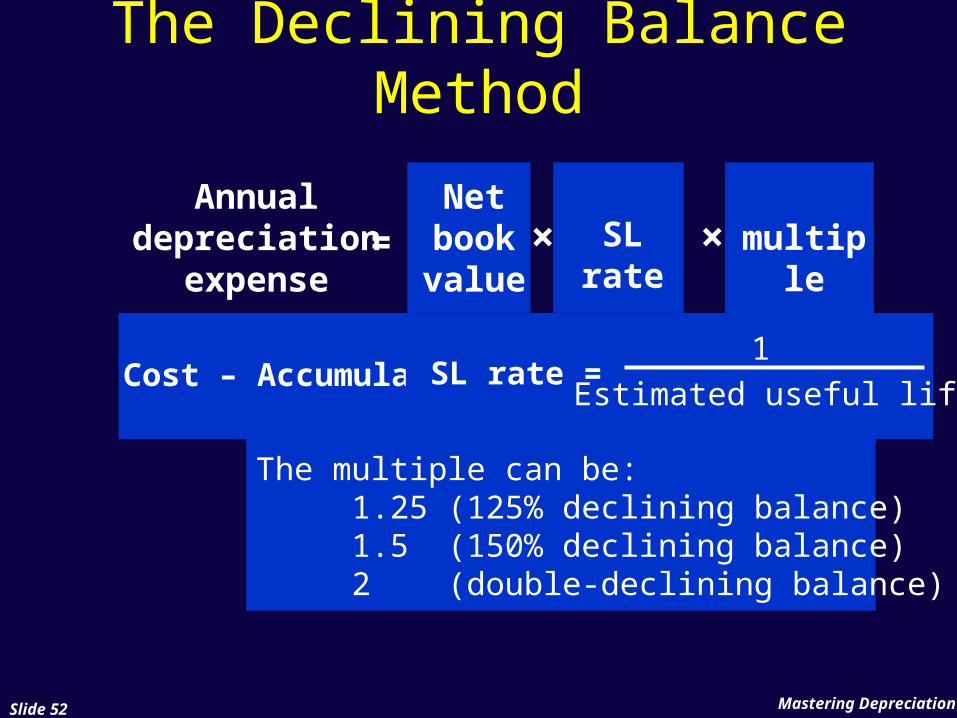

Annualdepreciation

expense

Netbookvalue

= × SL rate × multiple

Cost – Accumulated Depreciation1

Estimated useful lifeSL rate =

The multiple can be:1.25 (125% declining balance)1.5 (150% declining balance)2 (double-declining balance)

The Declining Balance Method

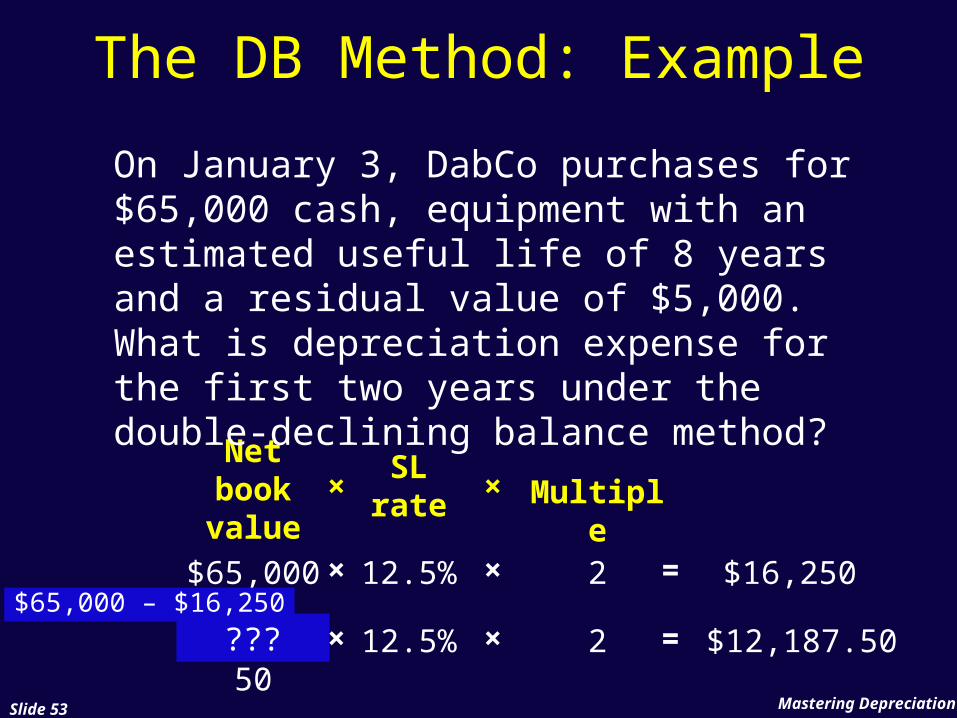

Mastering DepreciationSlide 53

$48,750

???

Netbookvalue

SL rate

The DB Method: Example

On January 3, DabCo purchases for $65,000 cash, equipment with an estimated useful life of 8 years and a residual value of $5,000. What is depreciation expense for the first two years under the double-declining balance method?

× × Multiple

$65,000 12.5% 2× × = $16,250

12.5% 2× × = $12,187.50$65,000 – $16,250

Mastering DepreciationSlide 54

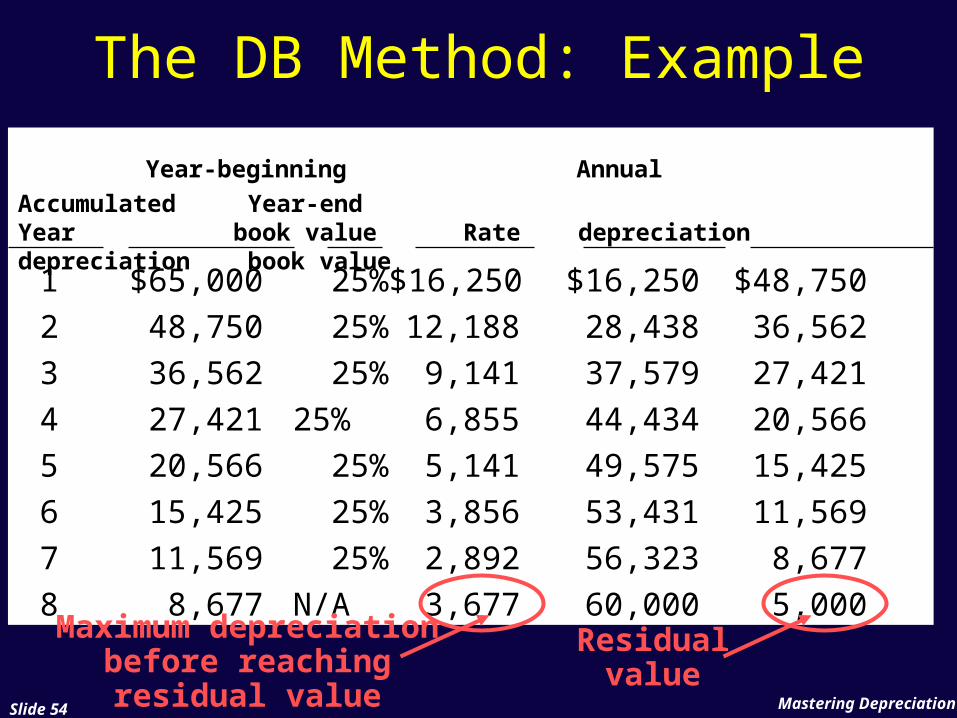

Year-beginning Annual Accumulated Year-endYear book value Rate depreciation depreciation book value

1 $65,000 25% $16,250 $16,250 $48,750

2 48,750 25% 12,188 28,438 36,562

3 36,562 25% 9,141 37,579 27,421

4 27,421 25% 6,855 44,434 20,566

5 20,566 25% 5,141 49,575 15,425

6 15,425 25% 3,856 53,431 11,569

7 11,569 25% 2,892 56,323 8,677

8 8,677 N/A 3,677 60,000 5,000Residual

value

The DB Method: Example

Maximum depreciation before reaching residual

value

Mastering DepreciationSlide 55

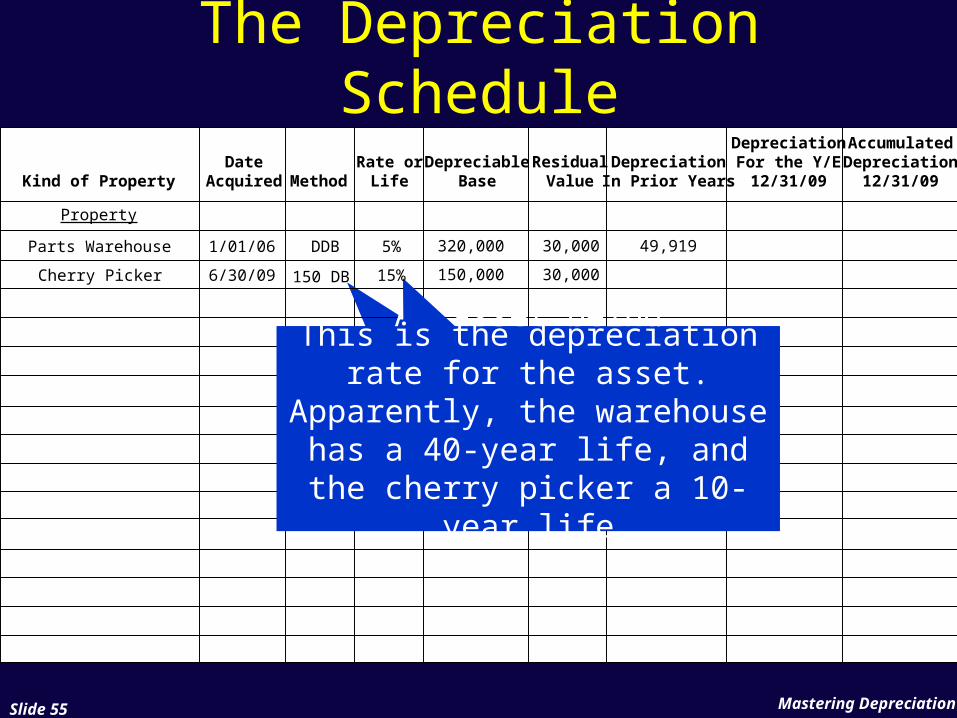

The Depreciation Schedule

An asset being depreciated using a declining balance method is shown on the

schedule as 125 DB, 150 DB, or DDB.

Property

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Parts Warehouse 1/01/06 DDB 5% 320,000 30,000

Cherry Picker 150 DB6/30/09

49,919

15% 150,000 30,000

This is the depreciation rate for the asset. Apparently, the warehouse has a 40-year life, and the cherry picker a 10-

year life

Mastering DepreciationSlide 56

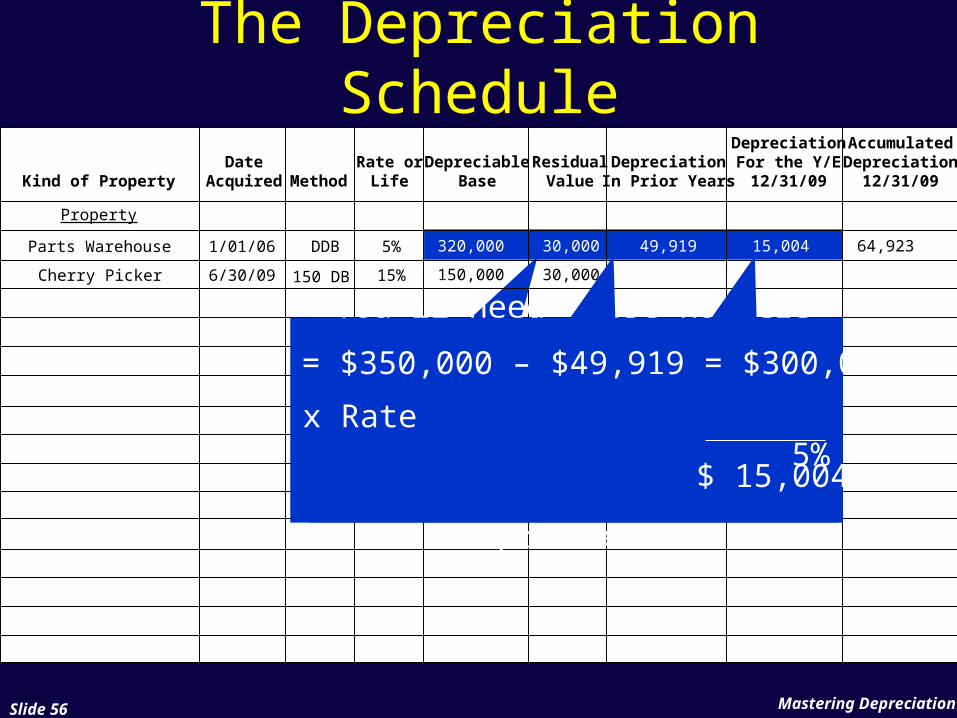

The Depreciation Schedule

You’ll need these numbers to calculate the depreciation since it is based on cost

(depreciable base plus residual value) less accumulated

depreciation

Property

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Parts Warehouse 1/01/06 DDB 5% 320,000 30,000 15,004 64,923

Cherry Picker 150 DB6/30/09

49,919

15% 150,000 30,000

BV = $350,000 – $49,919 = $300,081

x Rate 5%

$ 15,004

Mastering DepreciationSlide 57

Year of AcquisitionIn the year of acquisition: Calculate the full year’s depreciation

Prorate depreciation based on the period when it occurs (as under SL depreciation)

For Year 2 depreciation, calculate normally using the depreciable base (the book value less Year 1 depreciation).

Mastering DepreciationSlide 58

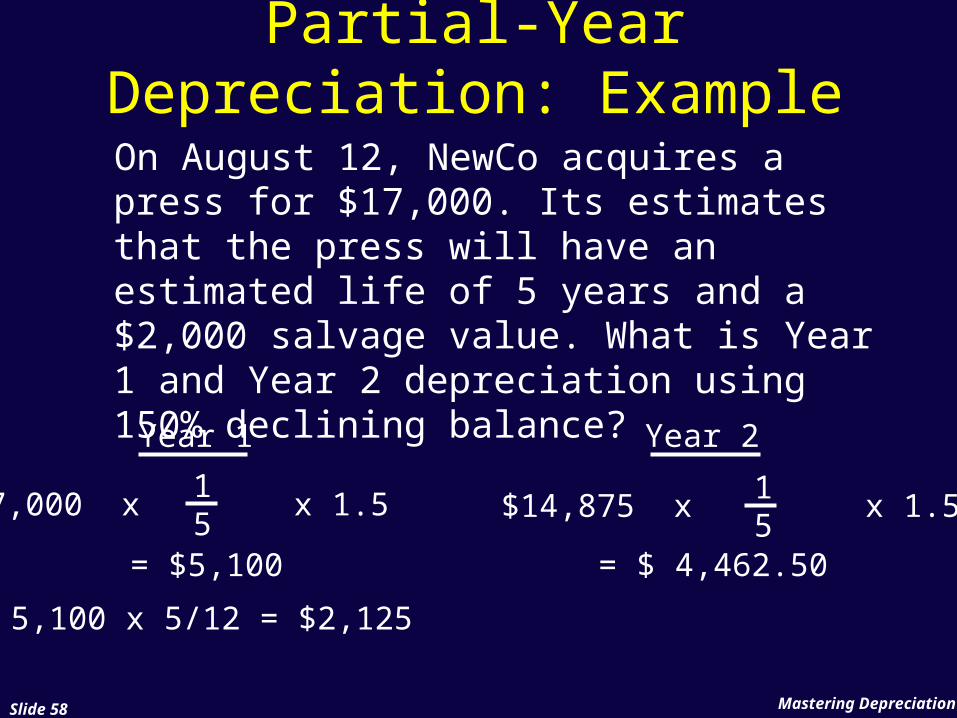

Partial-Year Depreciation: Example

On August 12, NewCo acquires a press for $17,000. Its estimates that the press will have an estimated life of 5 years and a $2,000 salvage value. What is Year 1 and Year 2 depreciation using 150% declining balance?

Year 1

15

$17,000 x x 1.5

= $5,100

$ 5,100 x 5/12 = $2,125

Year 2

$14,875 x x 1.5

= $ 4,462.50

15

Mastering DepreciationSlide 59

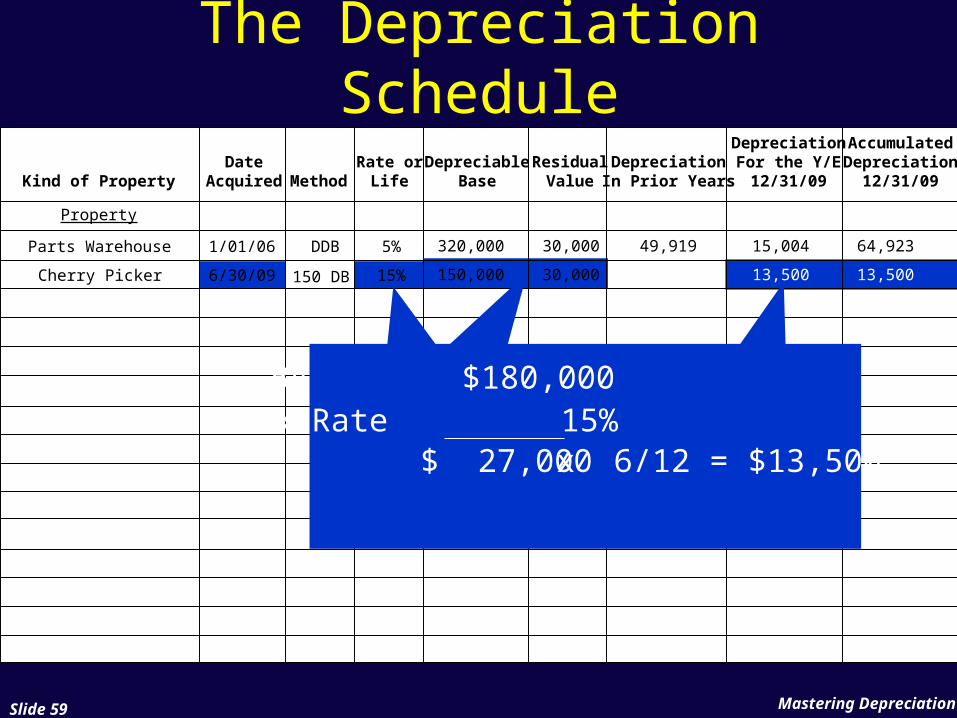

The Depreciation Schedule

Property

DateAcquiredKind of Property Method

Rate orLife

DepreciableBase

ResidualValue

DepreciationIn Prior Years

DepreciationFor the Y/E12/31/09

AccumulatedDepreciation

12/31/09

Parts Warehouse 1/01/06 DDB 5% 320,000 30,000 15,004 64,923

Cherry Picker 150 DB6/30/09

49,919

15% 150,000 30,000 13,500 13,500

BV $180,000x Rate 15%

$ 27,000 x 6/12 = $13,500

Mastering DepreciationSlide 60

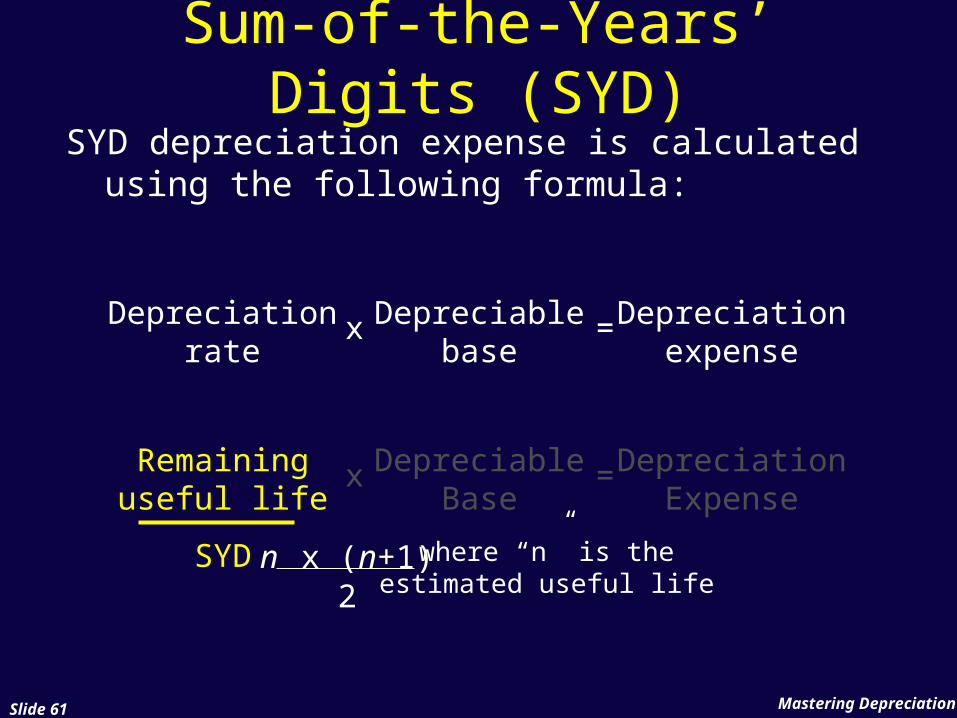

Sum-of-the-Years’ Digits (SYD)

This method, another kind of accelerated depreciation, is rarely used today.

The year-to-year decline in depreciation is typically more gradual than under the declining balance method.

Mastering DepreciationSlide 61

Sum-of-the-Years’ Digits (SYD)

SYD depreciation expense is calculated using the following formula:

Depreciationrate

Depreciablebase

Depreciationexpense

x =

Remaininguseful life

DepreciableBase

DepreciationExpense

x =

SYD n x (n+1)2

where “n” is theestimated useful life

Mastering DepreciationSlide 62

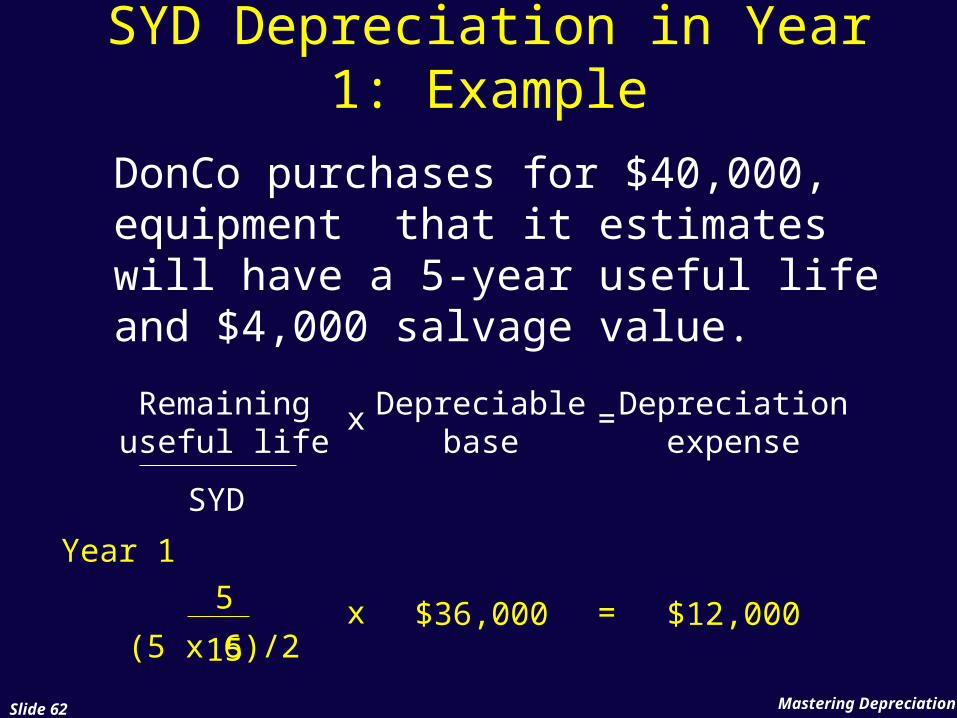

SYD Depreciation in Year 1: Example

DonCo purchases for $40,000, equipment that it estimates will have a 5-year useful life and $4,000 salvage value.

Remaininguseful life

Depreciablebase

Depreciationexpense

x =

Year 1

5 $36,000 $12,000x =15

SYD

(5 x 6)/2

Mastering DepreciationSlide 63

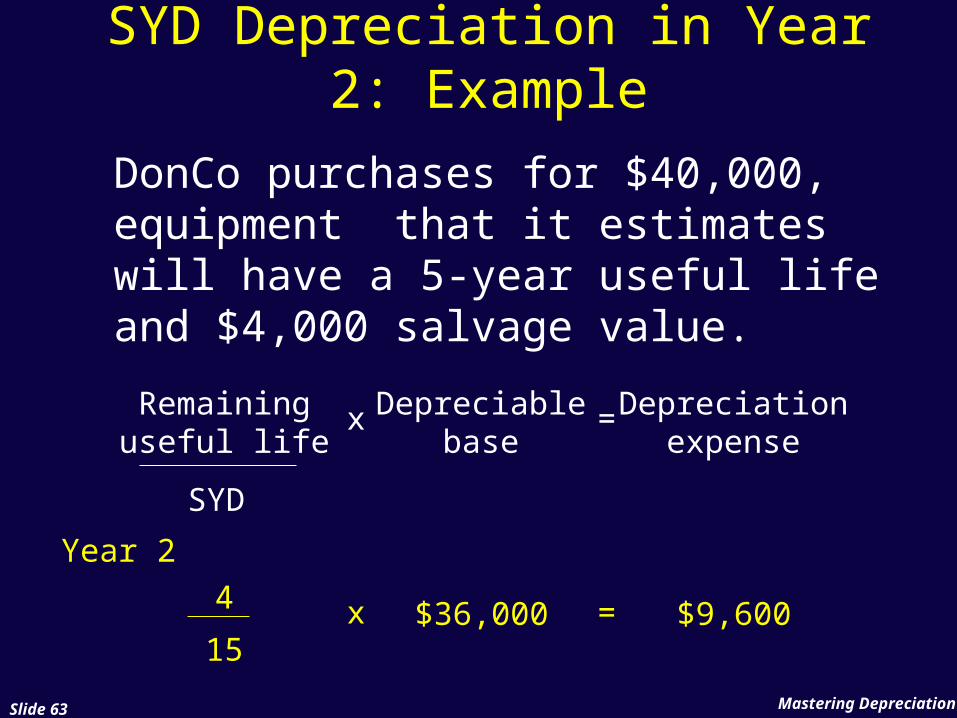

SYD Depreciation in Year 2: Example

Remaininguseful life

Depreciablebase

Depreciationexpense

x =

Year 2

4 $36,000 $9,600x =15

SYD

DonCo purchases for $40,000, equipment that it estimates will have a 5-year useful life and $4,000 salvage value.

Mastering DepreciationSlide 64

Partial-Year SYD Depreciation

Under SYD, booking a mid-year acquisition is cumbersome.

Compute full year depreciation, then prorate this amount between Years 1 and 2.

Depreciation in all future years must also be prorated.

Mastering DepreciationSlide 65

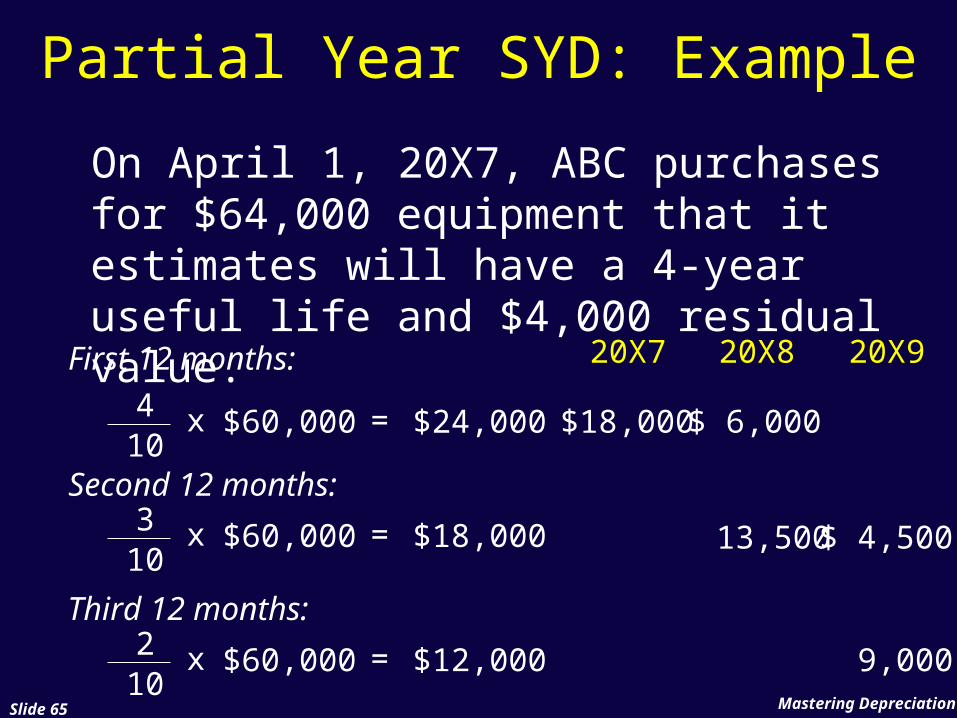

Partial Year SYD: Example

On April 1, 20X7, ABC purchases for $64,000 equipment that it estimates will have a 4-year useful life and $4,000 residual value.

First 12 months:

4 $60,000 $24,000x =10

Second 12 months:3 $60,000 $18,000x =10

Third 12 months:2 $60,000 $12,000x =10

20X7 20X8 20X9

$18,000$ 6,000

13,500$ 4,500

9,000

Mastering DepreciationSlide 66

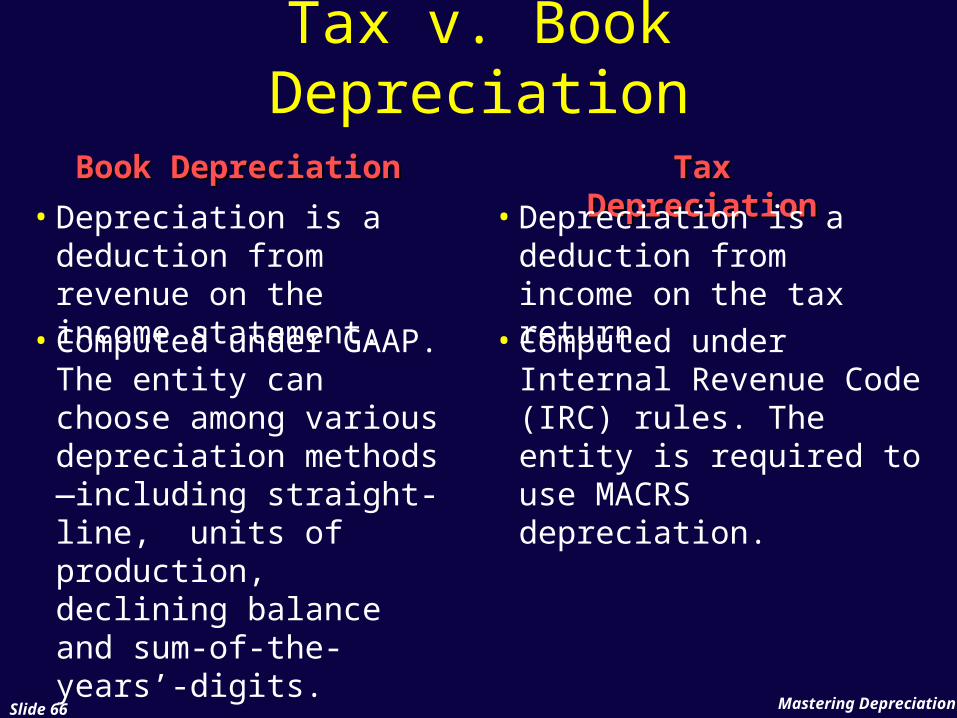

Tax v. Book Depreciation

Book Book DepreciationDepreciation

Tax Tax DepreciationDepreciation• Depreciation is a

deduction from revenue on the income statement.

• Depreciation is a deduction from income on the tax return.

• Computed under GAAP. The entity can choose among various depreciation methods—including straight-line, units of production, declining balance and sum-of-the-years’-digits.

• Computed under Internal Revenue Code (IRC) rules. The entity is required to use MACRS depreciation.

Mastering DepreciationSlide 67

Tax v. Book Depreciation

Book Book DepreciationDepreciation

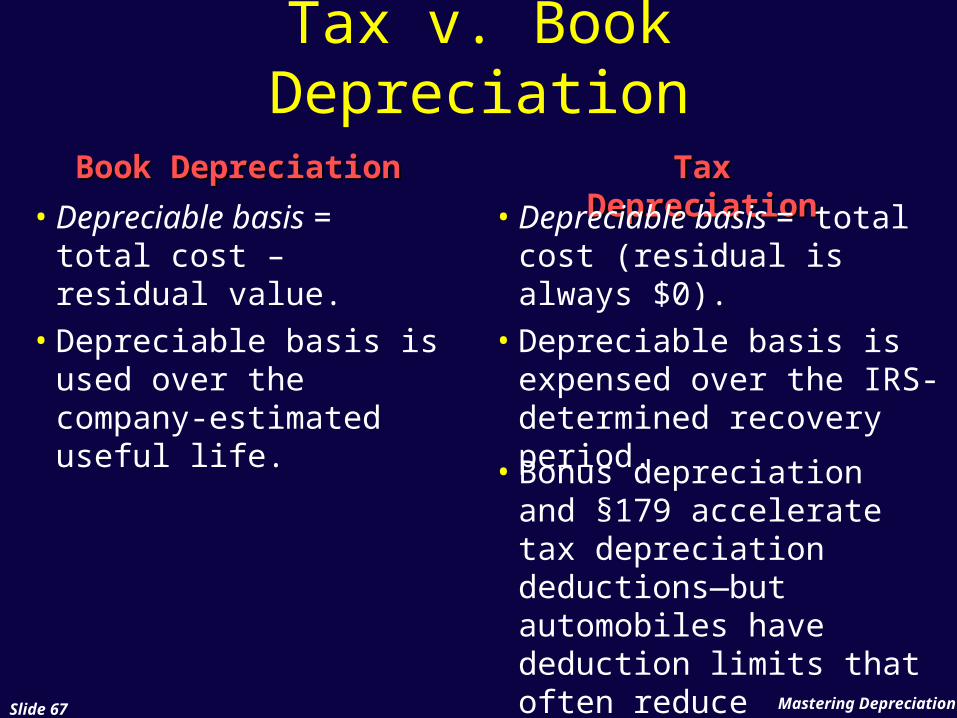

Tax Tax DepreciationDepreciation• Depreciable basis =

total cost – residual value.

• Depreciable basis = total cost (residual is always $0).

• Depreciable basis is used over the company-estimated useful life.

• Depreciable basis is expensed over the IRS-determined recovery period. • Bonus depreciation and §179 accelerate tax depreciation deductions—but automobiles have deduction limits that often reduce deductions.

Mastering DepreciationSlide 68

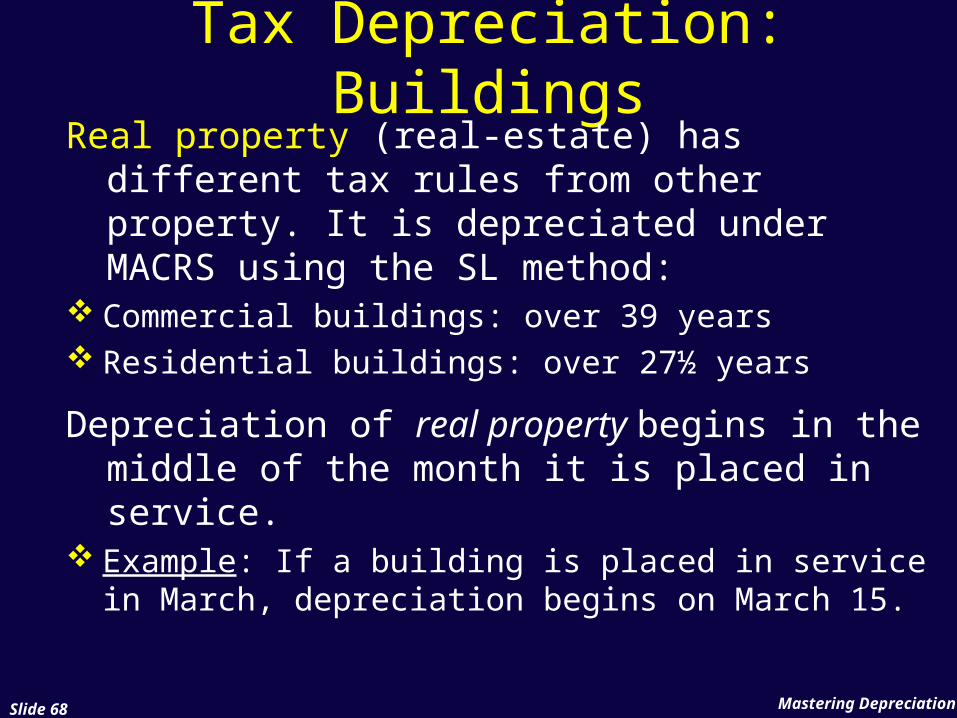

Tax Depreciation: BuildingsReal property (real-estate) has different tax

rules from other property. It is depreciated under MACRS using the SL method:

Commercial buildings: over 39 years Residential buildings: over 27½ years

Depreciation of real property begins in the middle of the month it is placed in service.

Example: If a building is placed in service in March, depreciation begins on March 15.

Use the depreciation rate in the column that corresponds to the month of the year that the property is placed in

service

Mastering DepreciationSlide 69

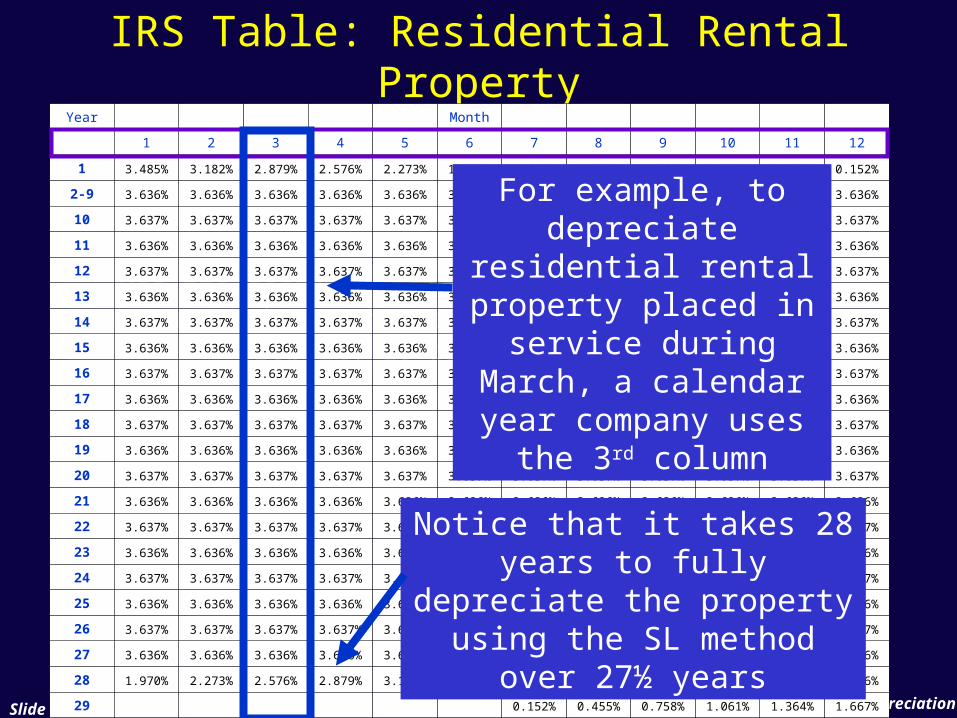

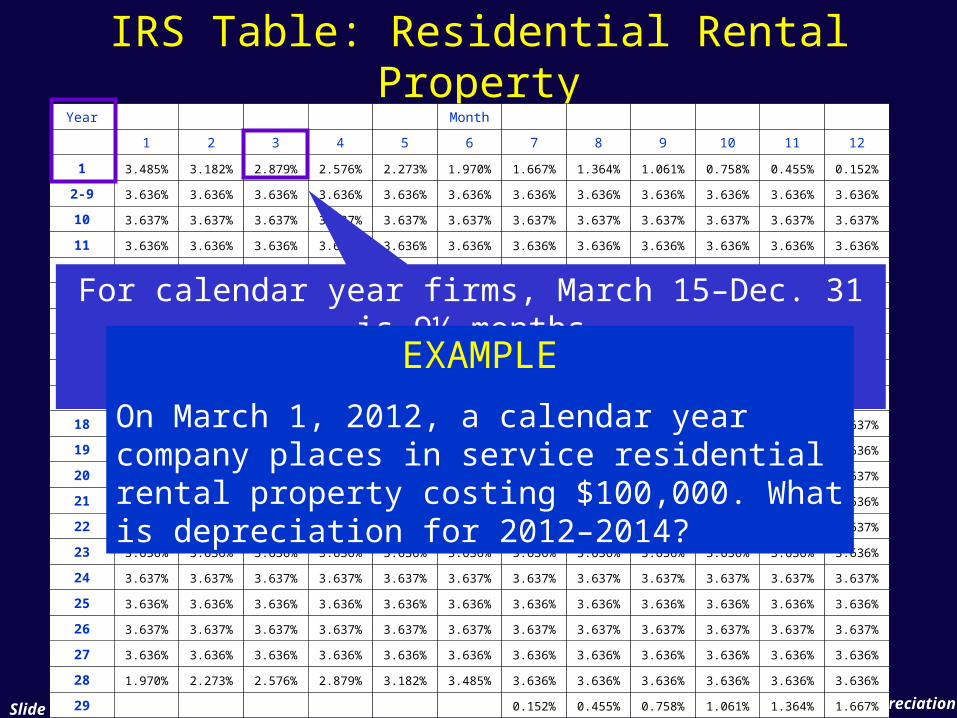

IRS Table: Residential Rental PropertyYear Month

1 2 3 4 5 6 7 8 9 10 11 12

1 3.485% 3.182% 2.879% 2.576% 2.273% 1.970% 1.667% 1.364% 1.061% 0.758% 0.455% 0.152%

2-9 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

10 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

11 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

12 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

13 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

14 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

15 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

16 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

17 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

18 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

19 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

20 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

21 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

22 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

23 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

24 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

25 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

26 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

27 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

28 1.970% 2.273% 2.576% 2.879% 3.182% 3.485% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

29 0.152% 0.455% 0.758% 1.061% 1.364% 1.667%

For example, to depreciate residential rental property placed

in service during March, a calendar

year company uses the 3rd column

Notice that it takes 28 years to fully depreciate the property using the SL method over 27½ years

Mastering DepreciationSlide 70

IRS Table: Residential Rental PropertyYear Month

1 2 3 4 5 6 7 8 9 10 11 12

1 3.485% 3.182% 2.879% 2.576% 2.273% 1.970% 1.667% 1.364% 1.061% 0.758% 0.455% 0.152%

2-9 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

10 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

11 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

12 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

13 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

14 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

15 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

16 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

17 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

18 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

19 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

20 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

21 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

22 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

23 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

24 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

25 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

26 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

27 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

28 1.970% 2.273% 2.576% 2.879% 3.182% 3.485% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

29 0.152% 0.455% 0.758% 1.061% 1.364% 1.667%

For calendar year firms, March 15–Dec. 31 is 9½ months

1/27.5 = 3.636% x 9.5/12 = 2.879%EXAMPLE

On March 1, 2012, a calendar year company places in service residential rental property costing $100,000. What is depreciation for 2012–2014?

Mastering DepreciationSlide 71

IRS Table: Residential Rental PropertyYear Month

1 2 3 4 5 6 7 8 9 10 11 12

1 3.485% 3.182% 2.879% 2.576% 2.273% 1.970% 1.667% 1.364% 1.061% 0.758% 0.455% 0.152%

2-9 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

10 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

11 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

12 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

13 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

14 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

15 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

16 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

17 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

18 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

19 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

20 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

21 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

22 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

23 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

24 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

25 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

26 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637% 3.637%

27 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

28 1.970% 2.273% 2.576% 2.879% 3.182% 3.485% 3.636% 3.636% 3.636% 3.636% 3.636% 3.636%

29 0.152% 0.455% 0.758% 1.061% 1.364% 1.667%

EXAMPLE

On March 1, 2012, a calendar year company places in service residential rental property costing $100,000. What is depreciation for 2012–2014?

2012 $100,000 x 2.879% $2,879

2013 $100,000 x 3.636% 3,636

2014 $100,000 x 3.636% 3,636

Mastering DepreciationSlide 72

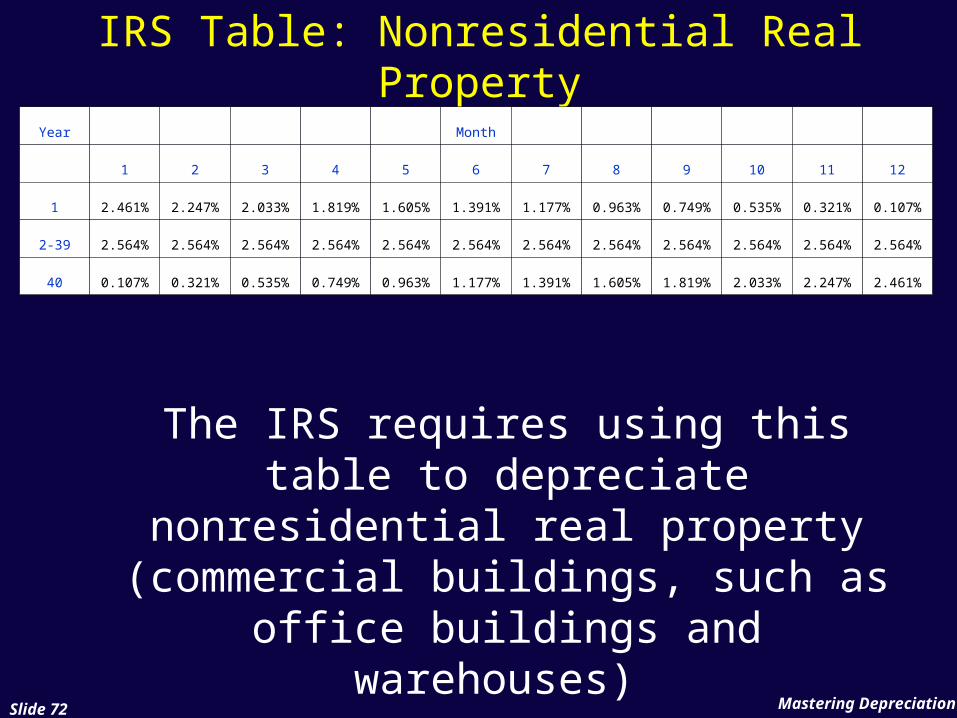

IRS Table: Nonresidential Real Property

Year Month

1 2 3 4 5 6 7 8 9 10 11 12

1 2.461% 2.247% 2.033% 1.819% 1.605% 1.391% 1.177% 0.963% 0.749% 0.535% 0.321% 0.107%

2-39 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564% 2.564%

40 0.107% 0.321% 0.535% 0.749% 0.963% 1.177% 1.391% 1.605% 1.819% 2.033% 2.247% 2.461%

The IRS requires using this table to depreciate nonresidential real

property (commercial buildings, such as office buildings and warehouses)

Mastering DepreciationSlide 73

Tax Depreciation: Plant, Equipment

Generally, IRS tables for property other than buildings—i.e., plant and equipment: specify a 5-year or 7-year recovery period use the DDB or SL method, and assume the asset was placed in service in the

middle of the year regardless of purchase dateException: Under the mid-quarter convention, when

more than 40% of the plant’s and equipment’s cost (acquisition cost – §179 deduction) is placed in service in the last quarter of the year, depreciation begins in the middle of the quarter it is placed in service.

Mastering DepreciationSlide 74

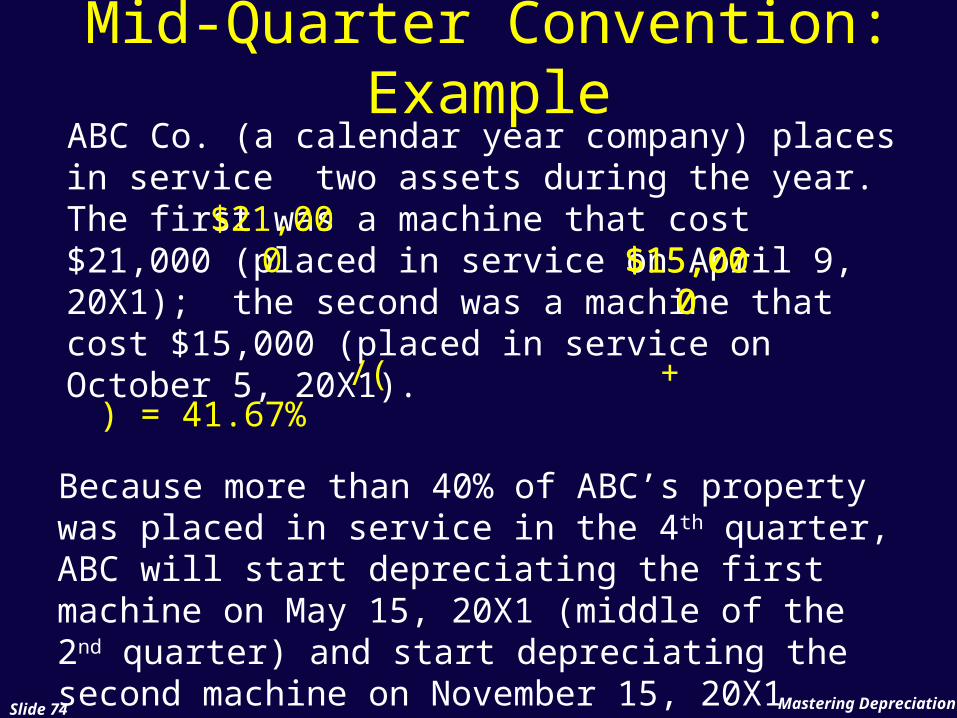

Mid-Quarter Convention: Example

ABC Co. (a calendar year company) places in service two assets during the year. The first was a machine that cost $21,000 (placed in service on April 9, 20X1); the second was a machine that cost $15,000 (placed in service on October 5, 20X1).

$15,000

$21,000 $15,00

0

/( + ) = 41.67%

Because more than 40% of ABC’s property was placed in service in the 4th quarter, ABC will start depreciating the first machine on May 15, 20X1 (middle of the 2nd quarter) and start depreciating the second machine on November 15, 20X1 (middle of the 4th quarter).

Mastering DepreciationSlide 75

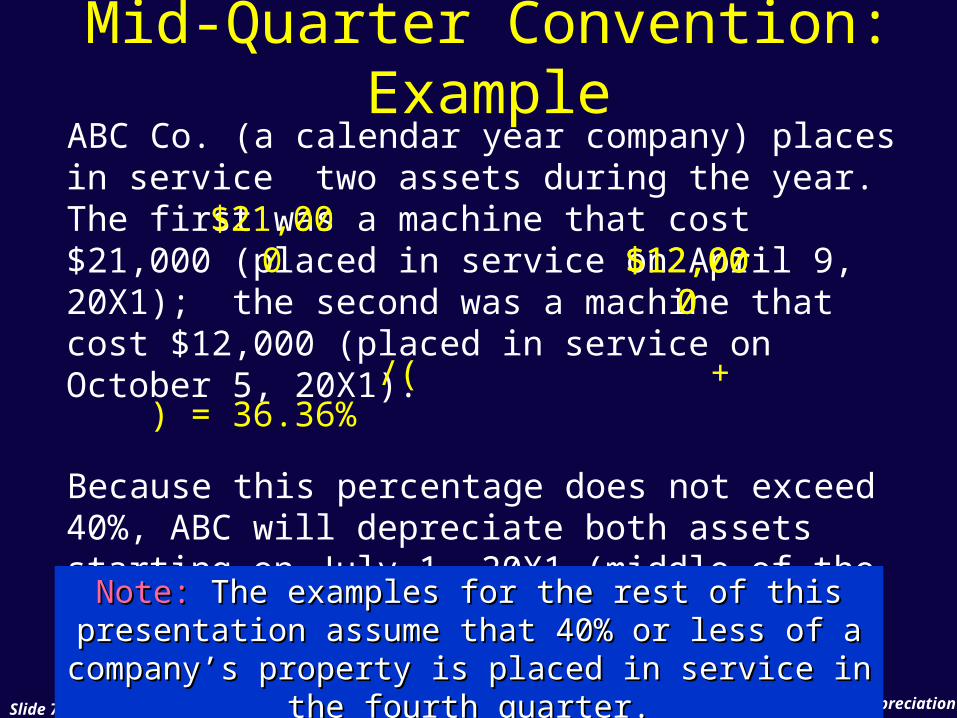

Mid-Quarter Convention: Example

ABC Co. (a calendar year company) places in service two assets during the year. The first was a machine that cost $21,000 (placed in service on April 9, 20X1); the second was a machine that cost $12,000 (placed in service on October 5, 20X1). /( + ) = 36.36%

Because this percentage does not exceed 40%, ABC will depreciate both assets starting on July 1, 20X1 (middle of the year).

$12,000

$21,000 $12,00

0

Note:Note: The examples for the rest of this The examples for the rest of this presentation assume that 40% or less of a presentation assume that 40% or less of a

company’s property is placed in service in the company’s property is placed in service in the fourth quarter.fourth quarter.

Mastering DepreciationSlide 76

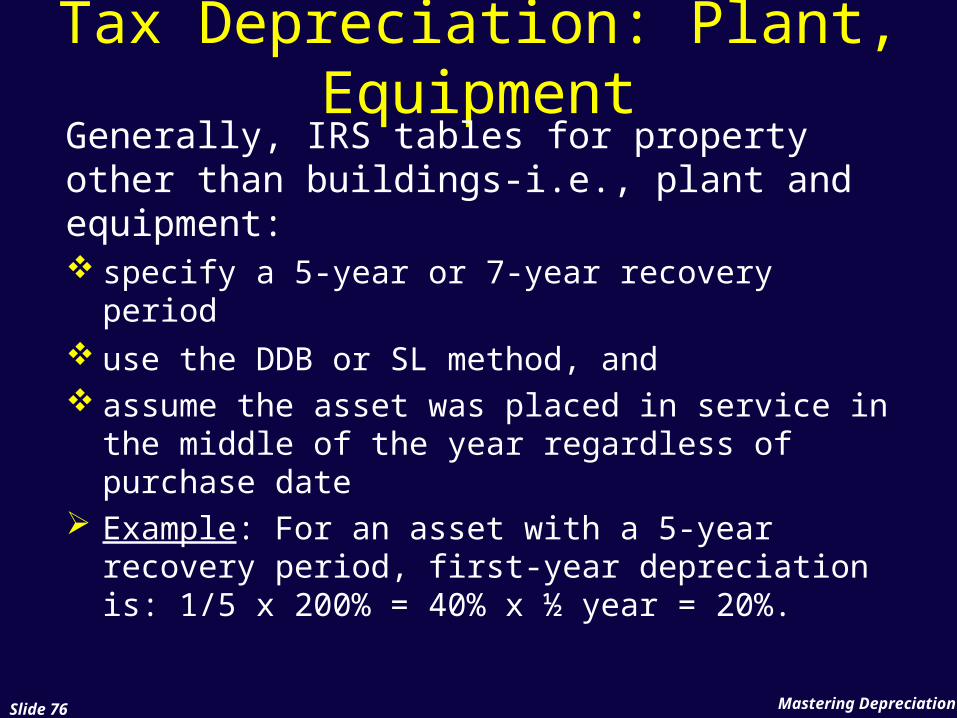

Tax Depreciation: Plant, Equipment

Generally, IRS tables for property other than buildings-i.e., plant and equipment: specify a 5-year or 7-year recovery period use the DDB or SL method, and assume the asset was placed in service in

the middle of the year regardless of purchase date

Example: For an asset with a 5-year recovery period, first-year depreciation is: 1/5 x 200% = 40% x ½ year = 20%.

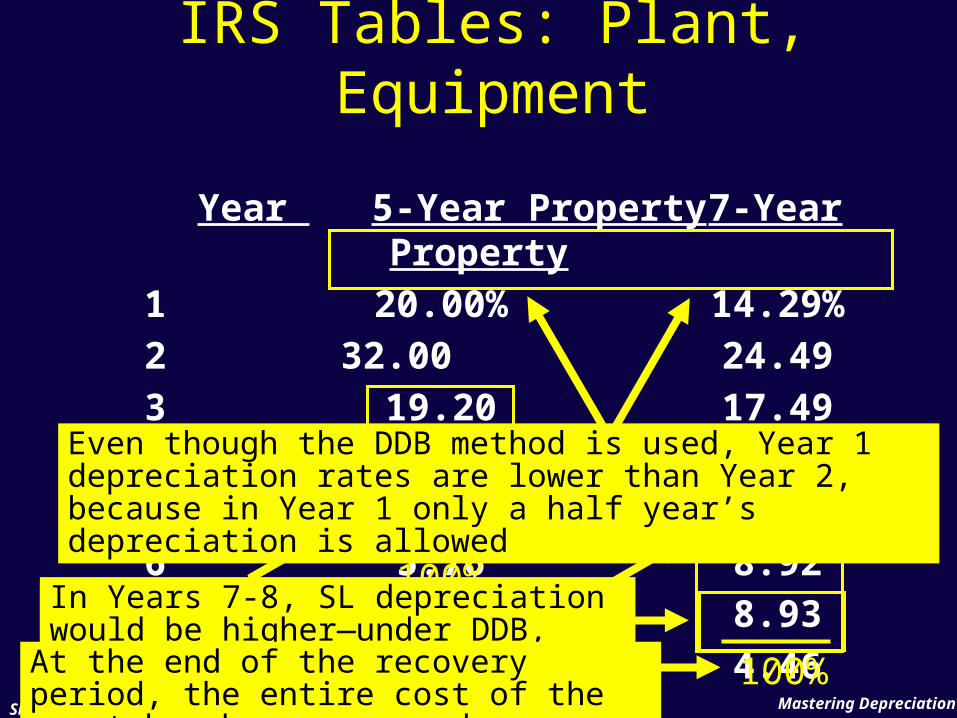

Year 5-Year Property 7-Year Property1 20.00% 14.29%2 32.00 24.493 19.20 17.494 11.52 12.495 11.52 8.936 5.76 8.927 8.938 4.46

Note that in the final year, a half year’s depreciation expense is allowed.

Mastering DepreciationSlide 77

100%

100%

IRS Tables: Plant, Equipment

Even though the DDB method is used, Year 1 depreciation rates are lower than Year 2, because in Year 1 only a half year’s depreciation is allowed

In Years 7-8, SL depreciation would be higher—under DDB, these years simply use up the remaining depreciationAt the end of the recovery period, the entire

cost of the asset has been expensed

Mastering DepreciationSlide 78

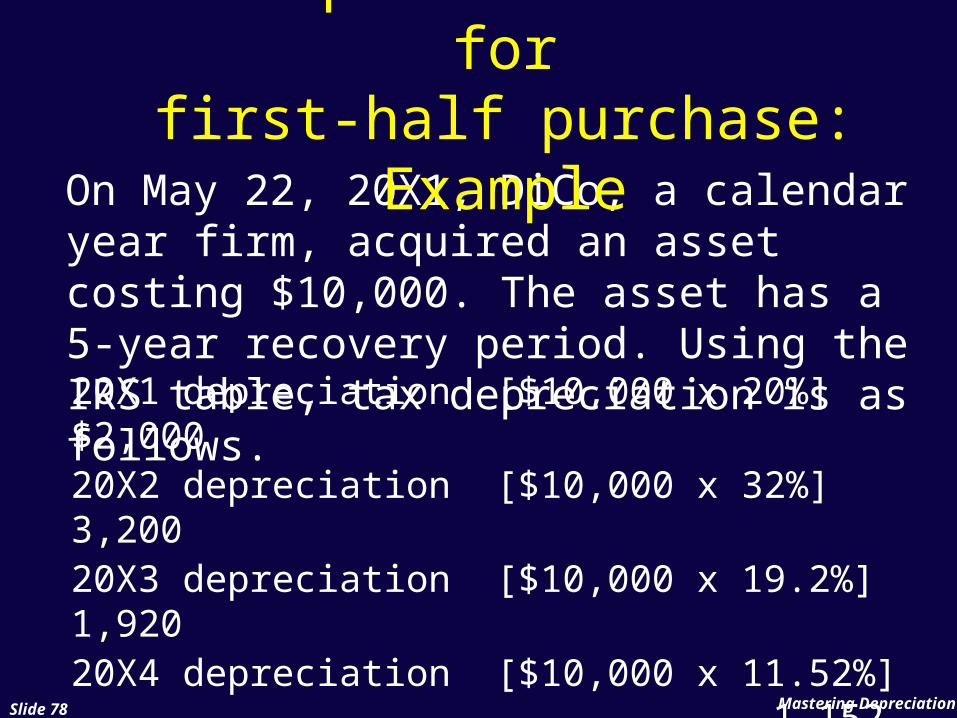

20X1 depreciation [$10,000 x 20%] $2,00020X2 depreciation [$10,000 x 32%] 3,20020X3 depreciation [$10,000 x 19.2%] 1,92020X4 depreciation [$10,000 x 11.52%] 1,15220X5 depreciation [$10,000 x 11.52%] 1,15220X6 depreciation [$10,000 x 5.76%] 576

On May 22, 20X1, DiCo, a calendar year firm, acquired an asset costing $10,000. The asset has a 5-year recovery period. Using the IRS table, tax depreciation is as follows.

Tax Depreciation Tables forfirst-half purchase: Example

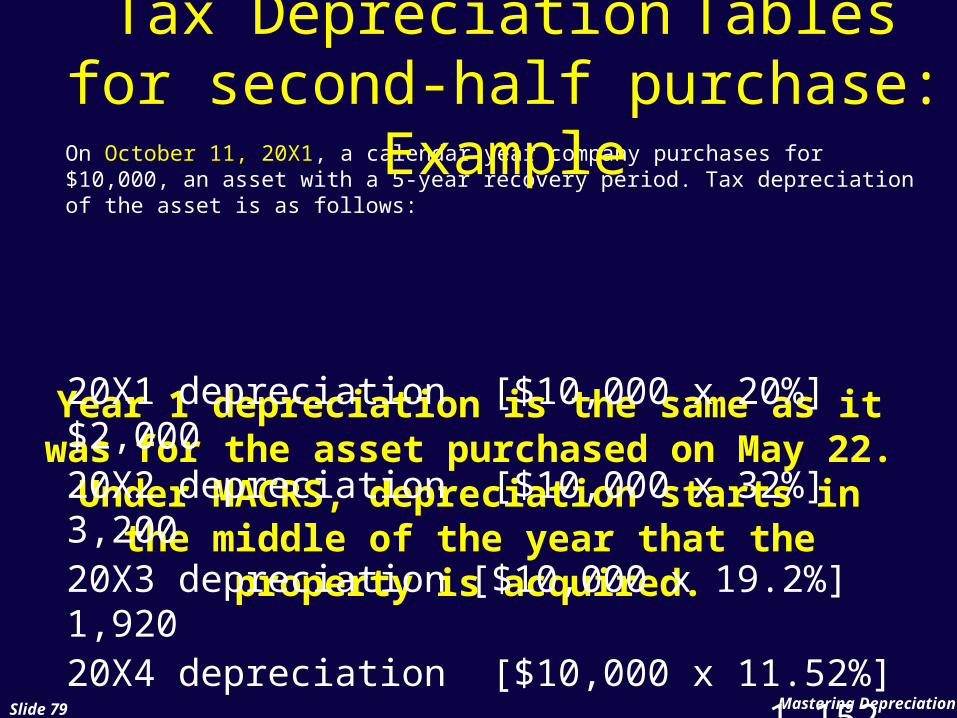

Year 1 depreciation is the same as it was for the asset purchased on May 22. Under MACRS, depreciation starts in the middle of the year that the property is

acquired.

Mastering DepreciationSlide 79

On October 11, 20X1, a calendar year company purchases for $10,000, an asset with a 5-year recovery period. Tax depreciation of the asset is as follows:

20X1 depreciation [$10,000 x 20%] $2,00020X2 depreciation [$10,000 x 32%] 3,20020X3 depreciation [$10,000 x 19.2%] 1,92020X4 depreciation [$10,000 x 11.52%] 1,15220X5 depreciation [$10,000 x 11.52%] 1,15220X6 depreciation [$10,000 x 5.76%] 576

Tax Depreciation Tables for second-half purchase:

Example

Mastering DepreciationSlide 80

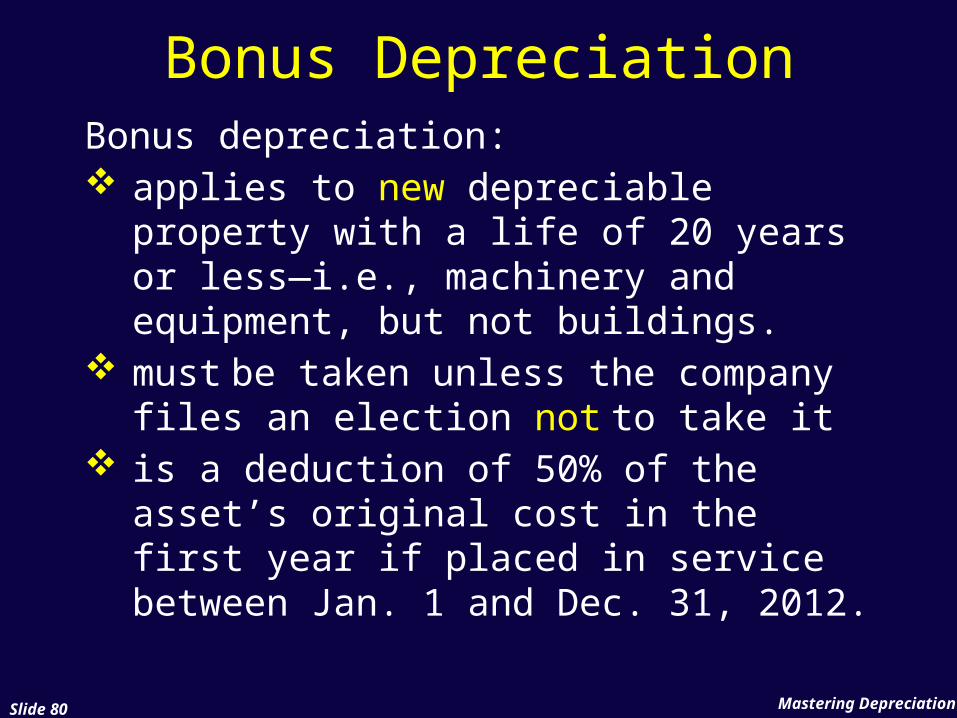

Bonus depreciation: applies to new depreciable property

with a life of 20 years or less—i.e., machinery and equipment, but not buildings.

must be taken unless the company files an election not to take it

is a deduction of 50% of the asset’s original cost in the first year if placed in service between Jan. 1 and Dec. 31, 2012.

Bonus Depreciation

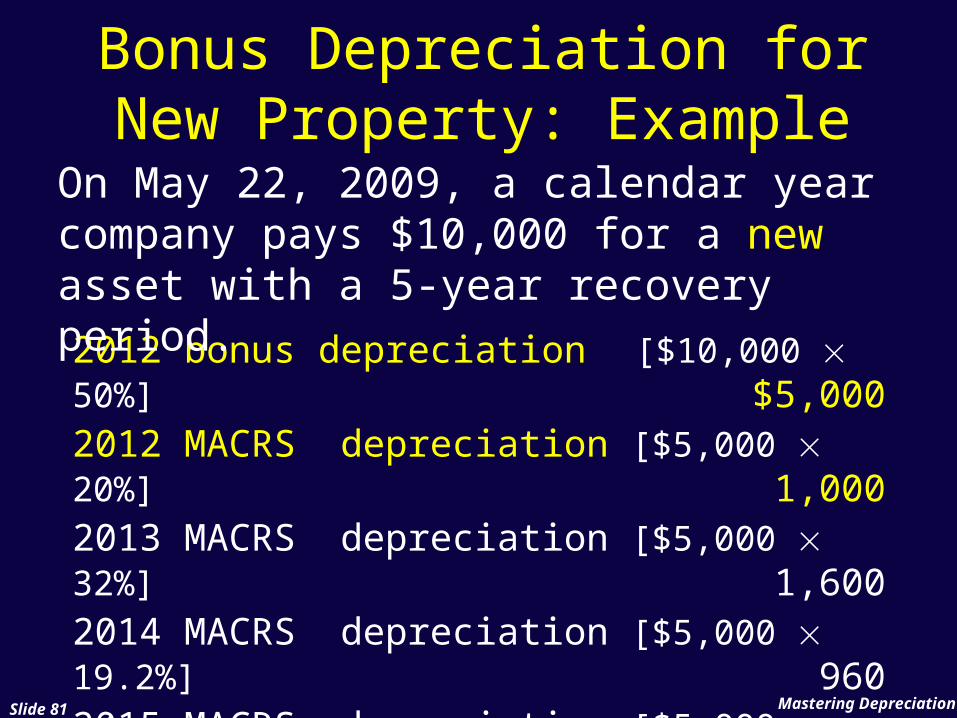

Mastering DepreciationSlide 81

2012 bonus depreciation [$10,000 50%]$5,0002012 MACRS depreciation [$5,000 20%] 1,0002013 MACRS depreciation [$5,000 32%] 1,6002014 MACRS depreciation [$5,000 19.2%] 9602015 MACRS depreciation [$5,000 11.52%] 5762016 MACRS depreciation [$5,000 11.52%] 5762017 MACRS depreciation [$5,000 5.76%] 288

On May 22, 2009, a calendar year company pays $10,000 for a new asset with a 5-year recovery period.

Bonus Depreciation for New Property: Example

Mastering DepreciationSlide 82

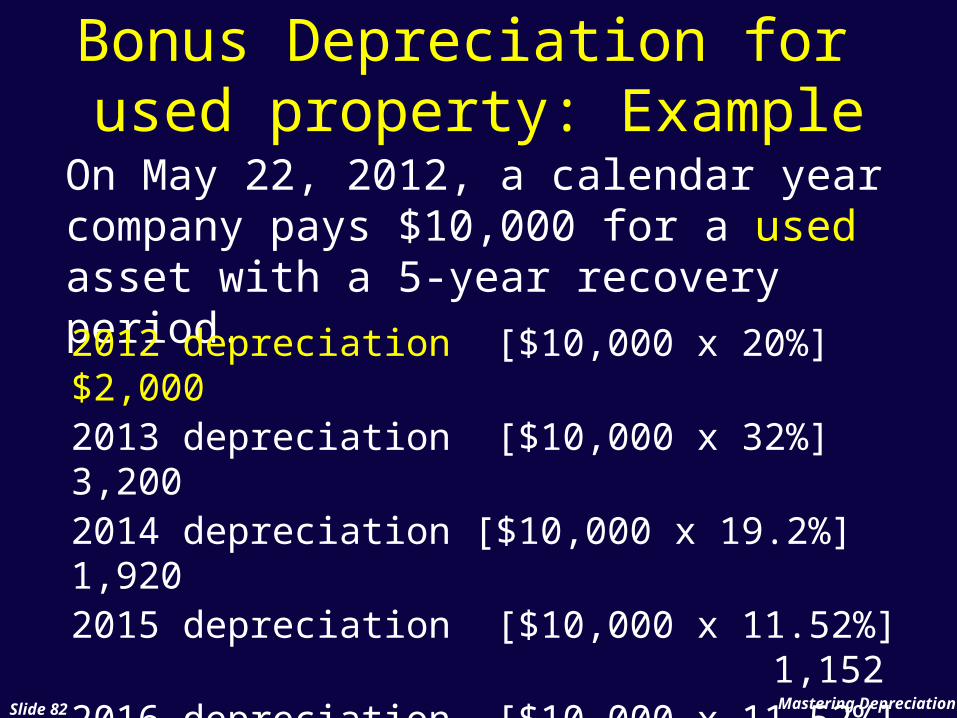

On May 22, 2012, a calendar year company pays $10,000 for a used asset with a 5-year recovery period.

2012 depreciation [$10,000 x 20%] $2,0002013 depreciation [$10,000 x 32%] 3,2002014 depreciation [$10,000 x 19.2%] 1,9202015 depreciation [$10,000 x 11.52%] 1,1522016 depreciation [$10,000 x 11.52%] 1,1522017 depreciation [$10,000 x 5.76%] 576

Bonus Depreciation for used property: Example

Mastering DepreciationSlide 83

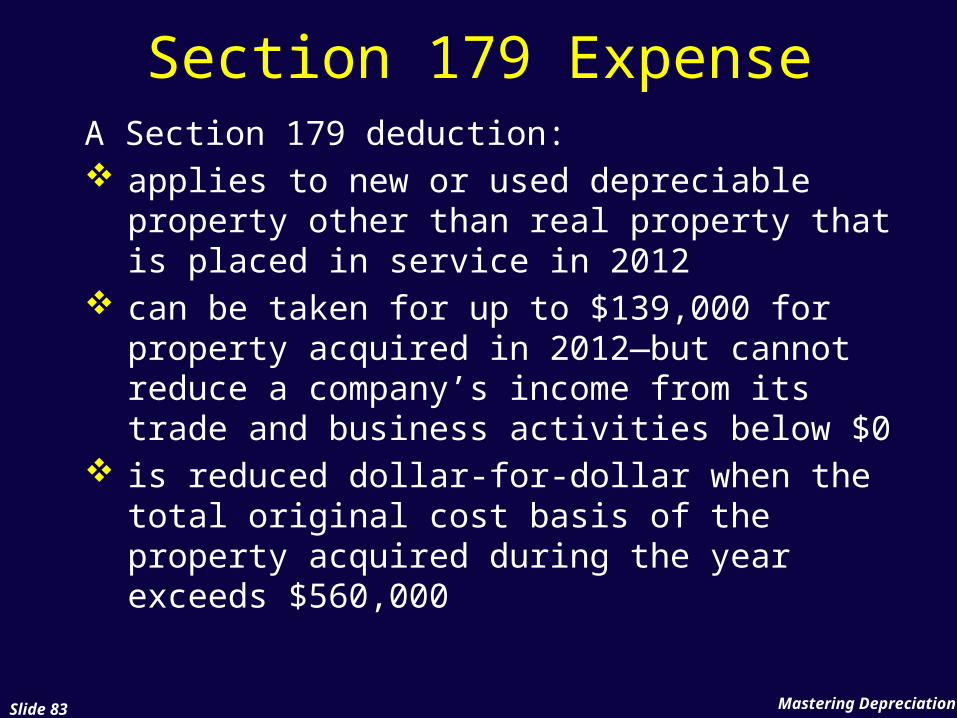

A Section 179 deduction: applies to new or used depreciable

property other than real property that is placed in service in 2012

can be taken for up to $139,000 for property acquired in 2012—but cannot reduce a company’s income from its trade and business activities below $0

is reduced dollar-for-dollar when the total original cost basis of the property acquired during the year exceeds $560,000

Section 179 Expense

Mastering DepreciationSlide 84

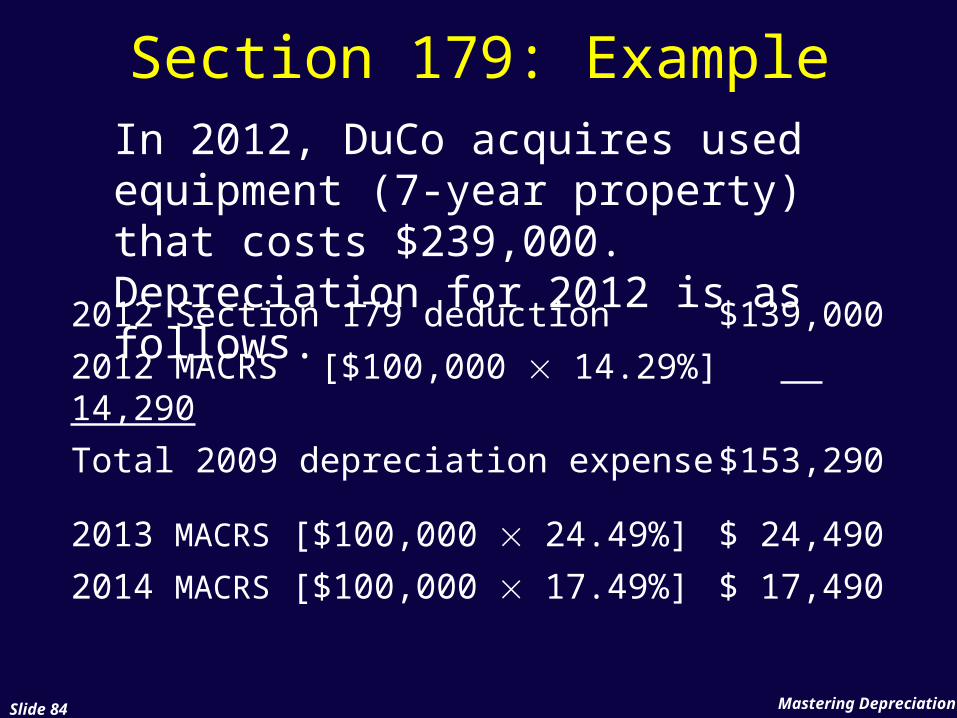

In 2012, DuCo acquires used equipment (7-year property) that costs $239,000. Depreciation for 2012 is as follows.2012 Section 179 deduction $139,000

2012 MACRS [$100,000 14.29%] 14,290

Total 2009 depreciation expense $153,290

2013 MACRS [$100,000 24.49%] $ 24,490

2014 MACRS [$100,000 17.49%] $ 17,490

Section 179: Example

Mastering DepreciationSlide 85

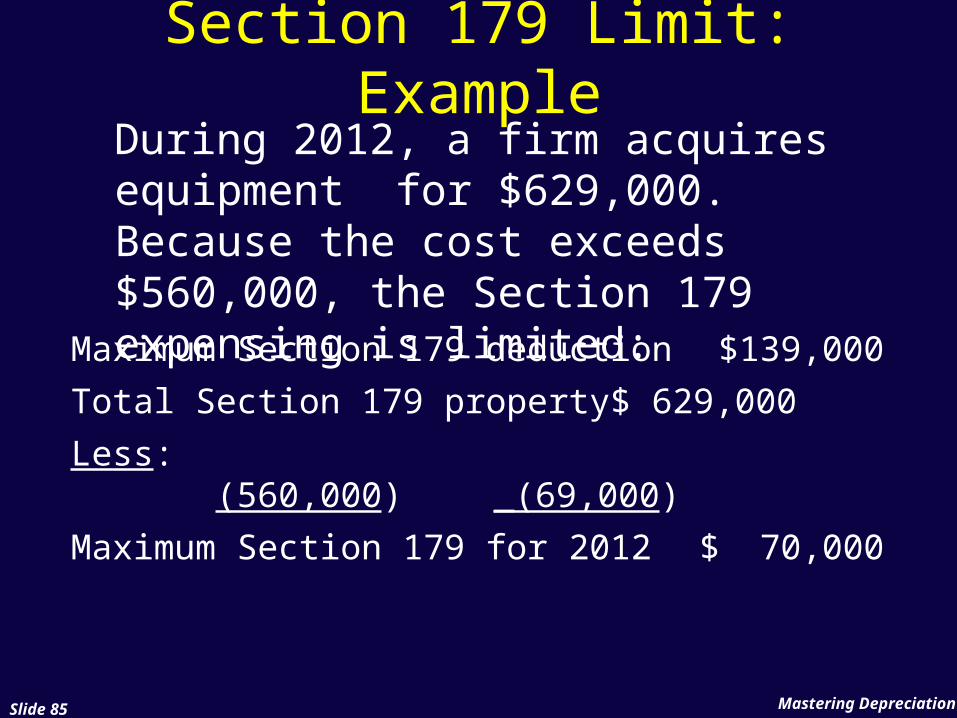

During 2012, a firm acquires equipment for $629,000. Because the cost exceeds $560,000, the Section 179 expensing is limited:

Maximum Section 179 deduction $139,000

Total Section 179 property $ 629,000

Less: (560,000) _(69,000)

Maximum Section 179 for 2012 $ 70,000

Section 179 Limit: Example

Mastering DepreciationSlide 86

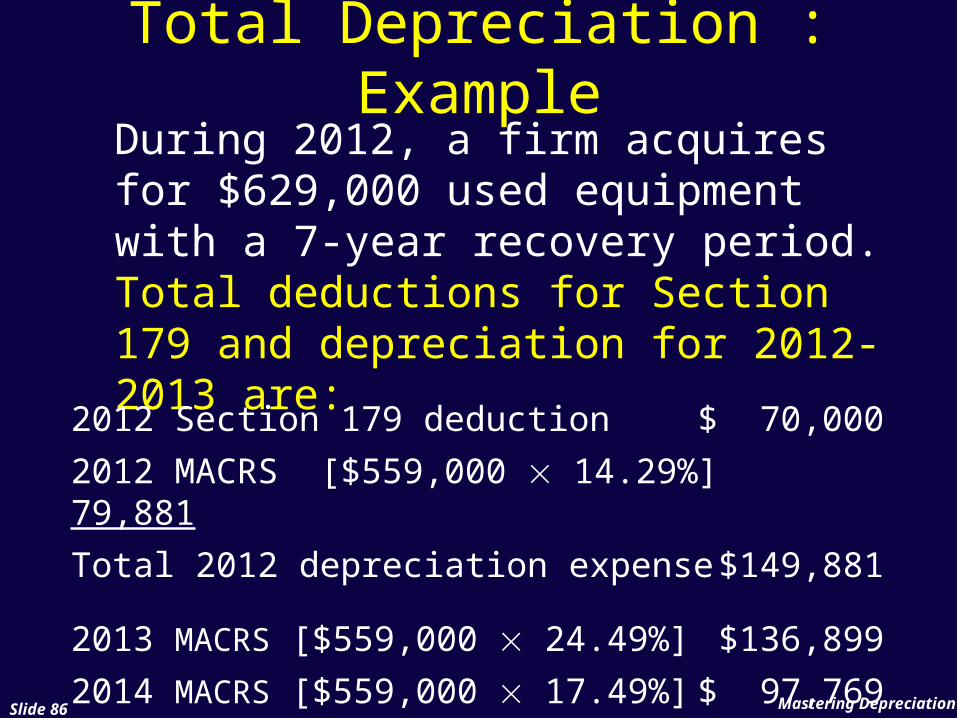

During 2012, a firm acquires for $629,000 used equipment with a 7-year recovery period. Total deductions for Section 179 and depreciation for 2012-2013 are:

Total Depreciation : Example

2012 Section 179 deduction $ 70,000

2012 MACRS [$559,000 14.29%] 79,881

Total 2012 depreciation expense $149,881

2013 MACRS [$559,000 24.49%] $136,899

2014 MACRS [$559,000 17.49%] $ 97,769

Mastering DepreciationSlide 87

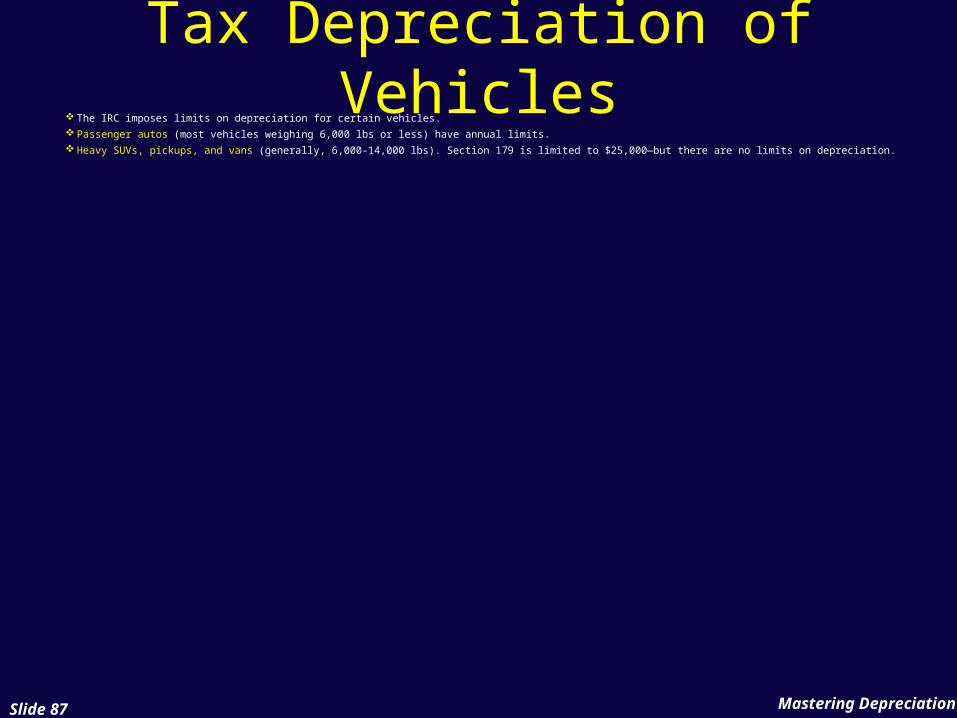

Tax Depreciation of Vehicles

The IRC imposes limits on depreciation for certain vehicles. Passenger autos (most vehicles weighing 6,000 lbs or less) have annual limits. Heavy SUVs, pickups, and vans (generally, 6,000-14,000 lbs). Section 179 is limited to $25,000—but there are no limits on depreciation.

Mastering DepreciationSlide 88

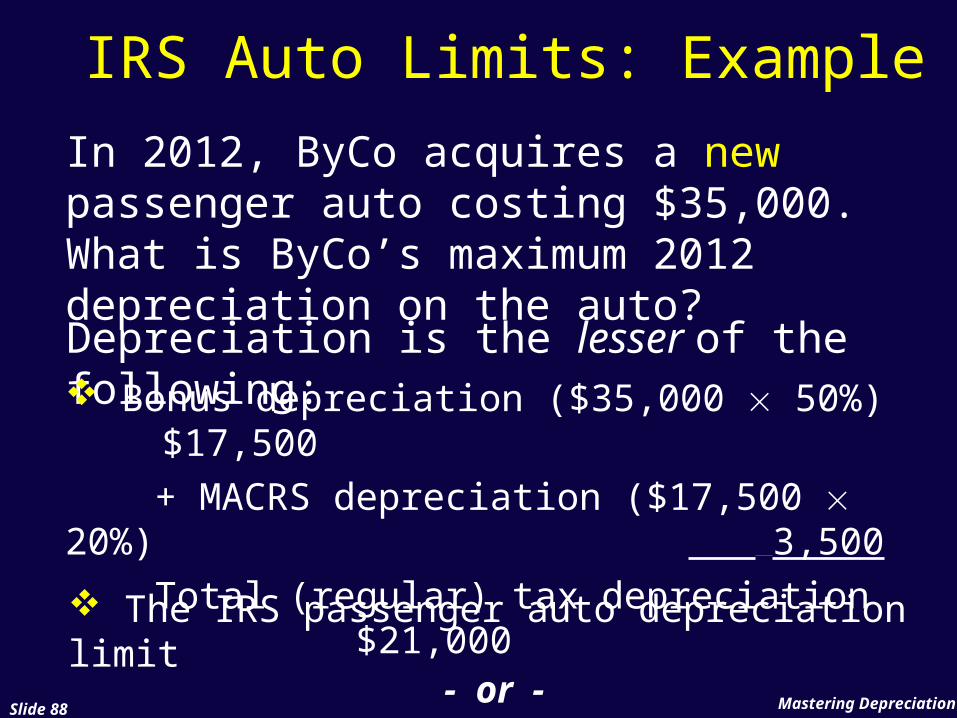

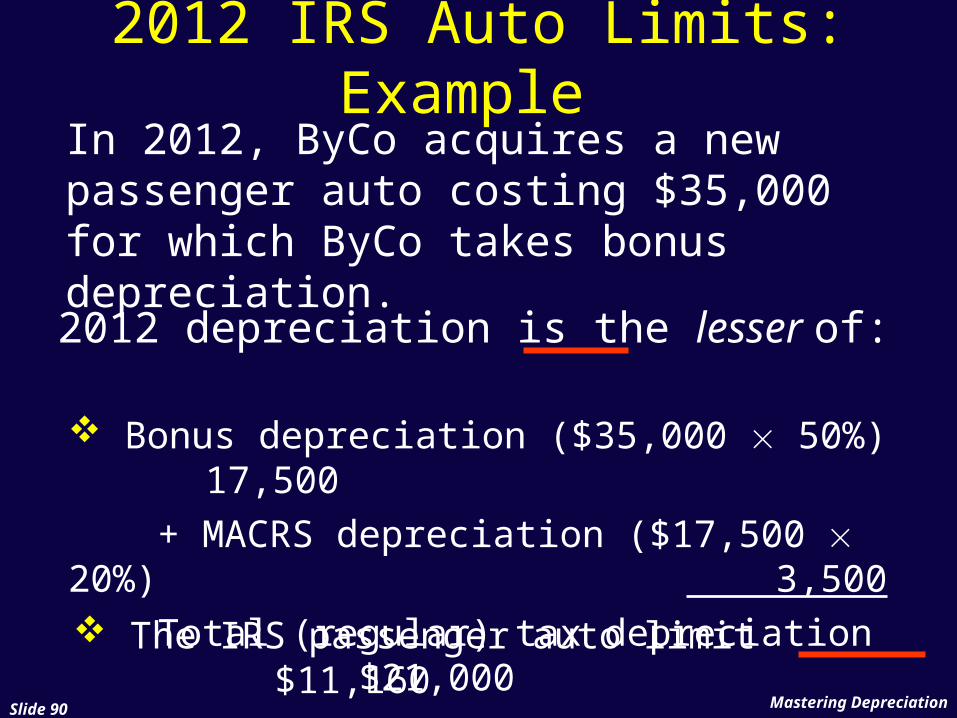

In 2012, ByCo acquires a new passenger auto costing $35,000. What is ByCo’s maximum 2012 depreciation on the auto?

IRS Auto Limits: Example

Depreciation is the lesser of the following: Bonus depreciation ($35,000 50%) $17,500

+ MACRS depreciation ($17,500 20%) 3,500

Total (regular) tax depreciation $21,000- or -

The IRS passenger auto depreciation limit

Mastering DepreciationSlide 89

IRS Auto Limits Year 1: Example

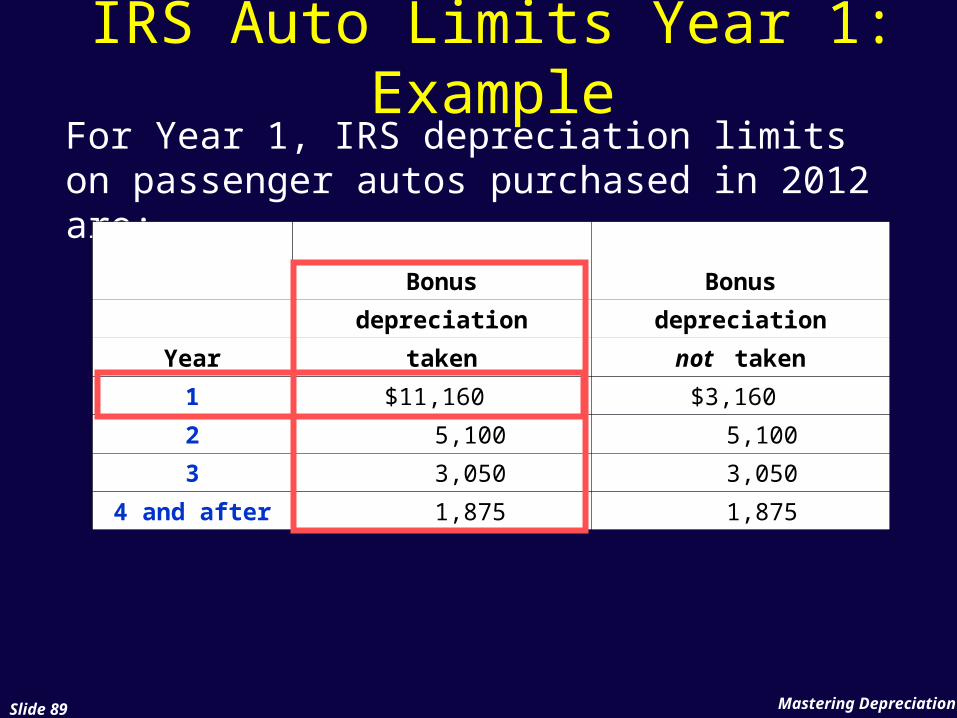

For Year 1, IRS depreciation limits on passenger autos purchased in 2012 are:

Bonus Bonus

depreciation depreciation

Year taken not taken

1 $11,160 $3,160

2 5,100 5,100

3 3,050 3,050

4 and after 1,875 1,875

Mastering DepreciationSlide 90

In 2012, ByCo acquires a new passenger auto costing $35,000 for which ByCo takes bonus depreciation.

2012 IRS Auto Limits: Example

The IRS passenger auto limit $11,160

Bonus depreciation ($35,000 50%) 17,500

+ MACRS depreciation ($17,500 20%) 3,500

Total (regular) tax depreciation $21,000- or -

2012 depreciation is the lesser of:

Mastering DepreciationSlide 91

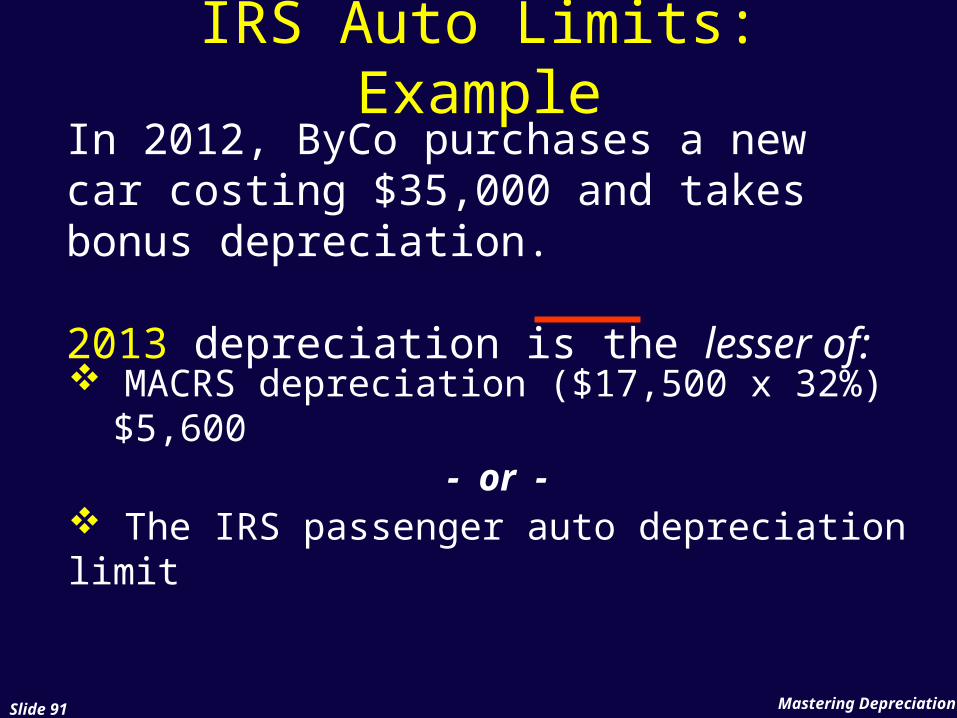

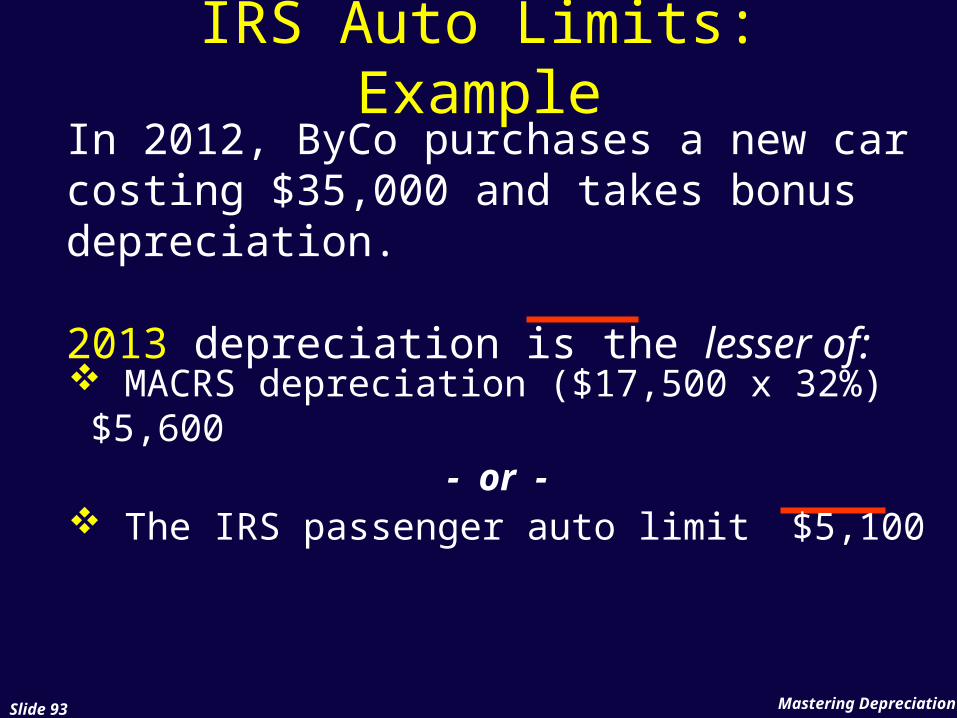

MACRS depreciation ($17,500 x 32%) $5,600- or -

The IRS passenger auto depreciation limit

IRS Auto Limits: ExampleIn 2012, ByCo purchases a new car costing $35,000 and takes bonus depreciation.

2013 depreciation is the lesser of:

Mastering DepreciationSlide 92

IRS Auto Limits Year 2: Example

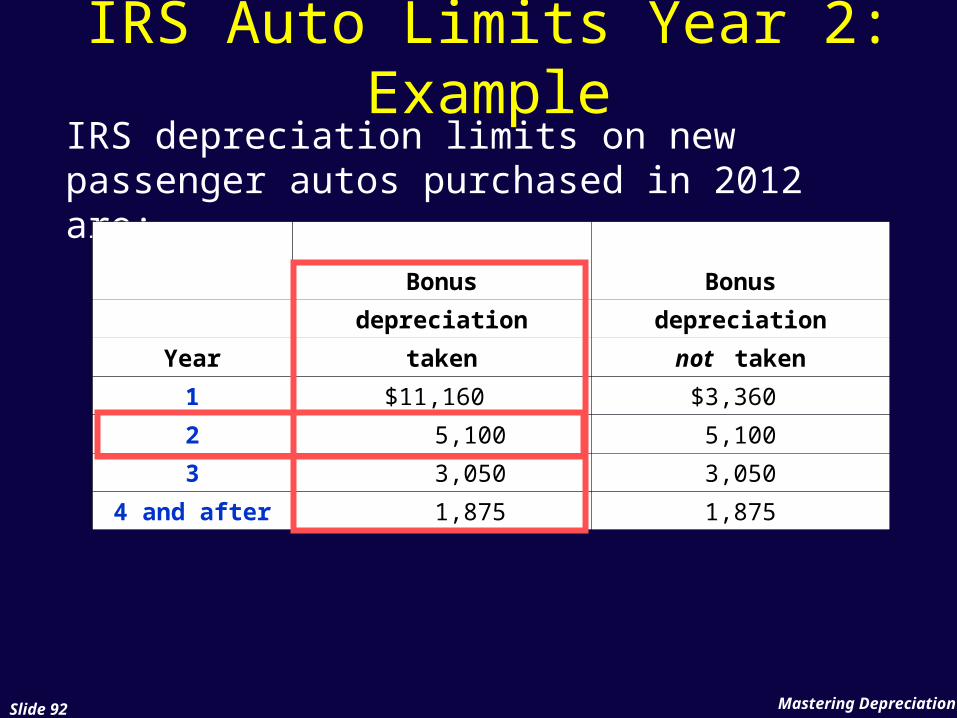

IRS depreciation limits on new passenger autos purchased in 2012 are:

Bonus Bonus

depreciation depreciation

Year taken not taken

1 $11,160 $3,360

2 5,100 5,100

3 3,050 3,050

4 and after 1,875 1,875

Mastering DepreciationSlide 93

In 2012, ByCo purchases a new car costing $35,000 and takes bonus depreciation. 2013 depreciation is the lesser of:

IRS Auto Limits: Example

MACRS depreciation ($17,500 x 32%) $5,600- or -

The IRS passenger auto limit $5,100

Mastering DepreciationSlide 94

IRS Auto Limits: Example

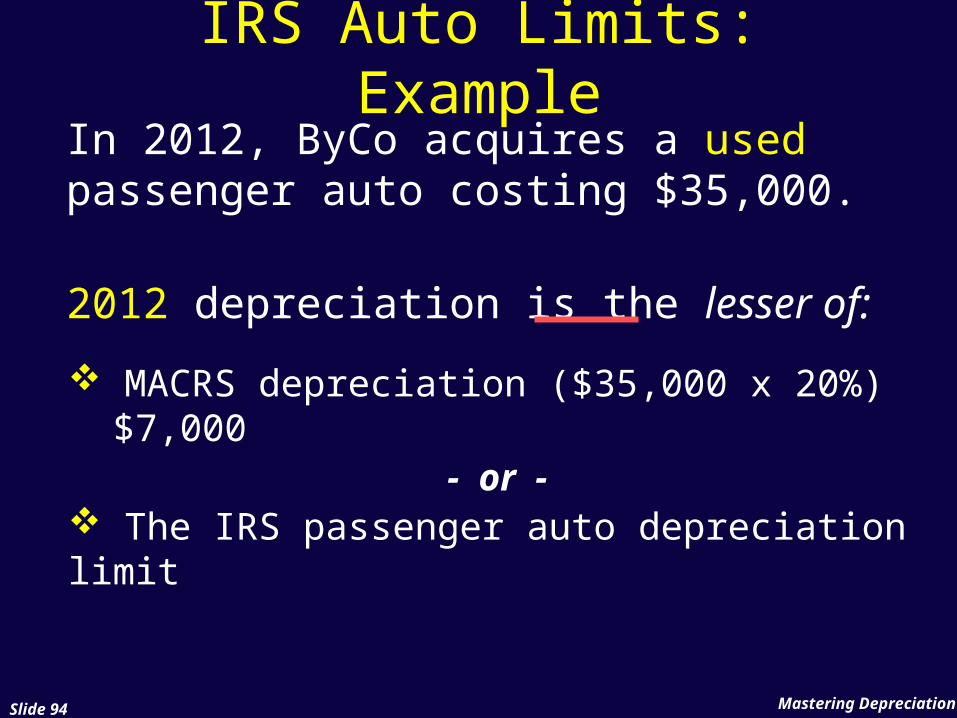

MACRS depreciation ($35,000 x 20%) $7,000- or -

The IRS passenger auto depreciation limit

2012 depreciation is the lesser of:

In 2012, ByCo acquires a used passenger auto costing $35,000.

Mastering DepreciationSlide 95

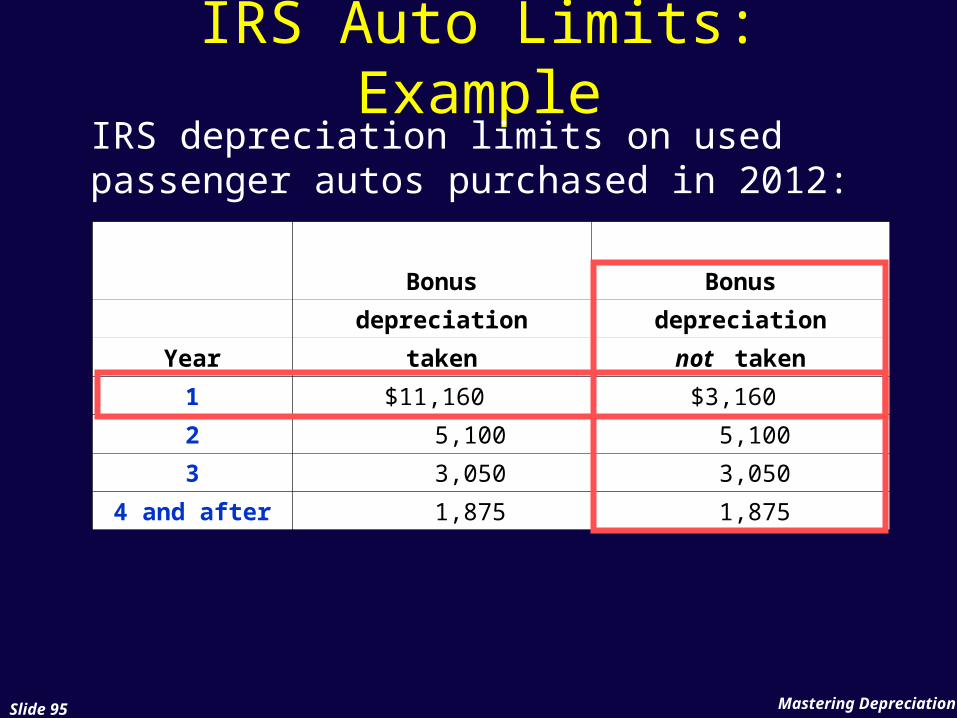

IRS Auto Limits: ExampleIRS depreciation limits on used passenger autos purchased in 2012:

Bonus Bonus

depreciation depreciation

Year taken not taken

1 $11,160 $3,160

2 5,100 5,100

3 3,050 3,050

4 and after 1,875 1,875

Mastering DepreciationSlide 96

IRS Auto Limits: Example

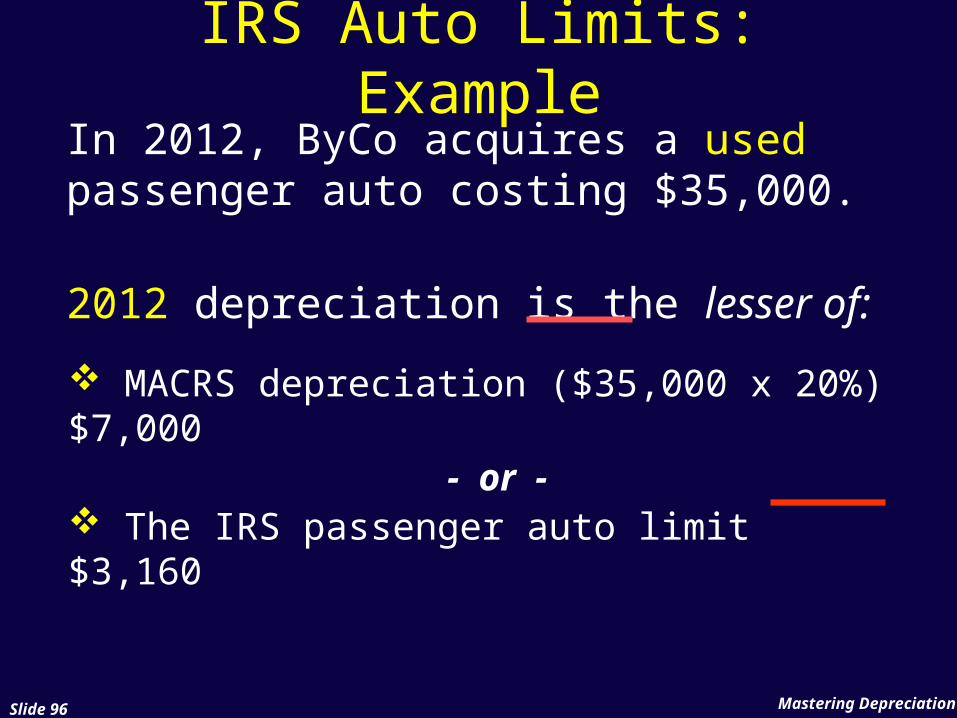

MACRS depreciation ($35,000 x 20%) $7,000- or -

The IRS passenger auto limit $3,160

2012 depreciation is the lesser of:

In 2012, ByCo acquires a used passenger auto costing $35,000.

Mastering DepreciationSlide 97

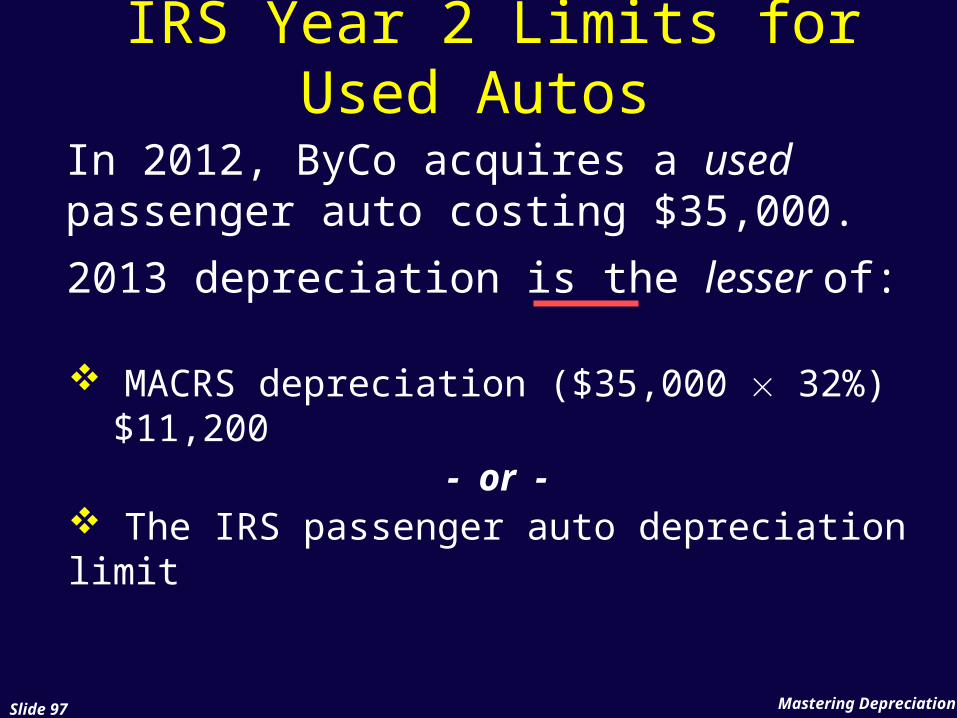

IRS Year 2 Limits for Used Autos

MACRS depreciation ($35,000 32%) $11,200

- or - The IRS passenger auto depreciation limit

2013 depreciation is the lesser of:

In 2012, ByCo acquires a used passenger auto costing $35,000.

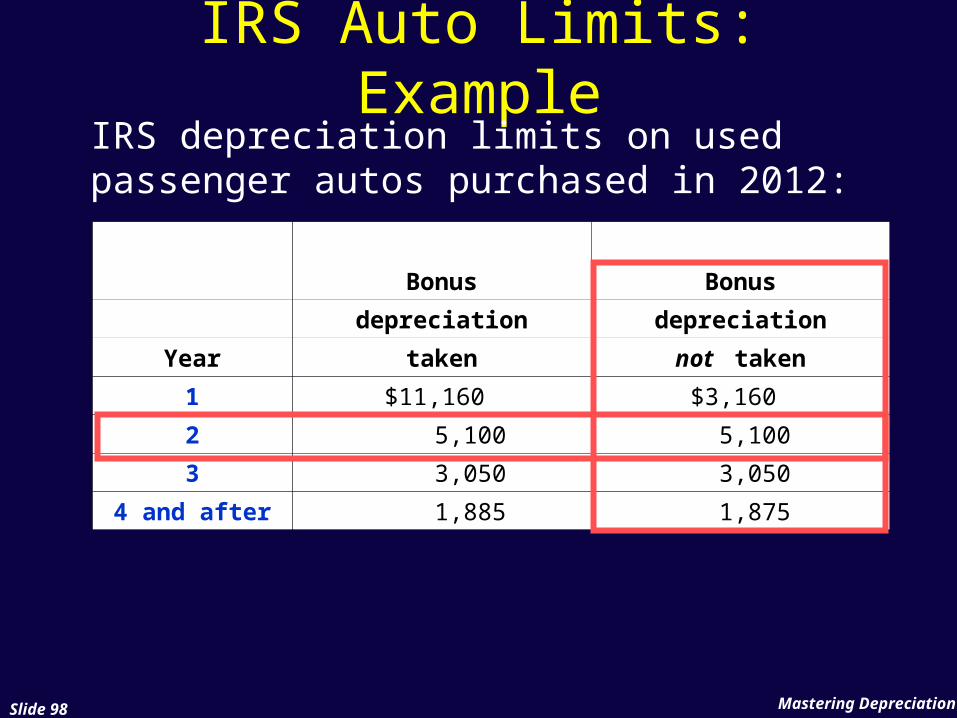

Mastering DepreciationSlide 98

IRS Auto Limits: ExampleIRS depreciation limits on used passenger autos purchased in 2012:

Bonus Bonus

depreciation depreciation

Year taken not taken

1 $11,160 $3,160

2 5,100 5,100

3 3,050 3,050

4 and after 1,885 1,875

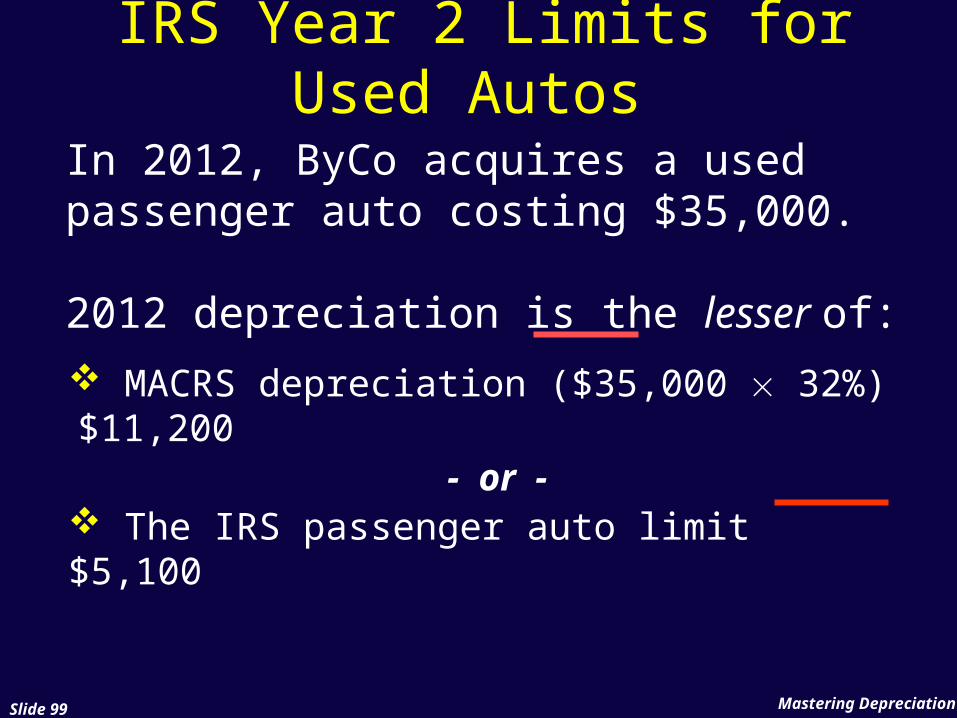

Mastering DepreciationSlide 99

MACRS depreciation ($35,000 32%) $11,200- or -

The IRS passenger auto limit $5,100

In 2012, ByCo acquires a used passenger auto costing $35,000.

2012 depreciation is the lesser of:

IRS Year 2 Limits for Used Autos

Mastering DepreciationSlide 100

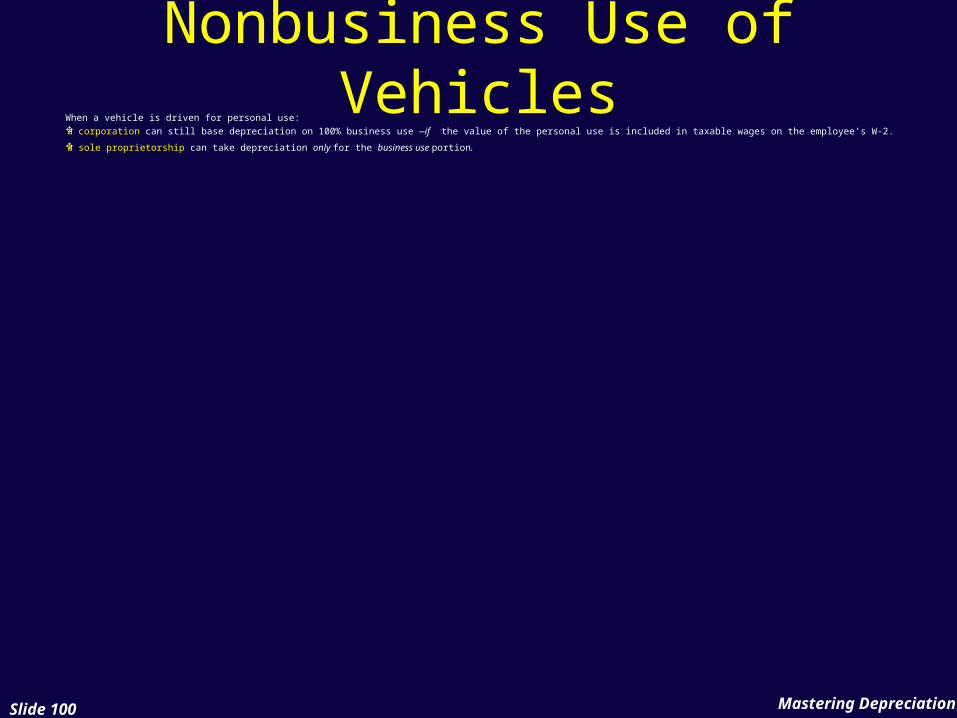

Nonbusiness Use of Vehicles

When a vehicle is driven for personal use:a corporation can still base depreciation on 100% business use —if the value of the personal use is included in taxable wages on the employee’s W-2.

a sole proprietorship can take depreciation only for the business use portion.

Mastering DepreciationSlide 101

In 2012, a corporate car is driven 80% for business and 20% for personal use.

The corporation can take 100% of the available depreciation on the car—if

the value of the 20% personal use is included in taxable wages on the employee’s W-2.

Nonbusiness Use: Example

Mastering DepreciationSlide 102

In 2012, a sole proprietor drives her car 80% for business and 20% personal use.

If the owner uses the car 80% for business, only 80% depreciation can be taken.

If the sole proprietor’s employee drives the owner’s car 80% for business and 20% for personal use, the owner has two options:

1.take 80% depreciation on the car, or

2.take 100% depreciation and include the value of the 20% personal use in wages on the employee’s W-2.

Nonbusiness Use: Example