Embed Size (px)

Citation preview

HMTHINDUSTAN MACHINE TOOLS

KALAMASSERY,KOCHI

Presented By

JIBU.AB

Reg No: 0113514029

MBA

NOORUL ISLAM UNIVERSITY

A PROJECT STUDY ON

WORKING CAPITAL MANAGEMENT

IN

HMT MACHINE TOOLS

KALAMASSERY.KOCHI.

INTRODUCTION

Working Capital Management is important part in firm financial management decision

improper management makes on the WIP- Working In Process to the develop on the

various development of working financial process on the basis of managing on

developing the financial statements. Working capital management the develop mentation

of the manufacturing their goods on the basis of short term liabilities and non-short

liabilities.

NEED OF THE STUDY

The study has been conducted for gaining particular knowledge about working capital

management & activities of HMT MACHINE TOOLS LIMITED,KALAMASSERY.

STATEMENT OF THE PROBLEM

The current problem of HMT machine tools is generally explain giving less

attention has been paid in the area of short term finance. In particular to the working

capital but the effective working capital has a crucial play in the enhancing the

profitability and growth of the firm.

OBJECTIVES OF THE STUDY

To ensure that the supply of raw material & finished goods will remain continuous so that

production process is not halted and demands of customers are duly met.

To keep investment in inventory at optimum level.

To study and analyze the various inventory policies through various methods and techniques

of inventory control.

To classify the various components based on its value and movements.

To decide which item to stock and which item to procure on demand.

To keep inventory at sufficiently high level to perform production and sales activities

smoothly.

To minimize investment in inventory at minimum level to maximize profitability.

SCOPE OF THE STUDY

Since the decision regarding working capital are of an operating nature not one time

decision the scope of the study is geared toward identifying important areas of control and

to establish model for better control of the various components of working capital.

The study would also attempt to identify the various source available for financing of

working capital.

The study gives a fair idea of improvement in efficiency of working capital management

and also to have control over the components of working capital and managing of

efficiency.

COMPANY PROFILE

Machine Tools Business group, to concentrate on metal cutting machines.

Industrial machinery business group, to deal with printing machines, Die

casting and plastic injection moldings machines, food processing machines,

and metal forming machines.

Agricultural business group, to concentrate on tractor.

Engineering components business groups, to deal with watches & Lamps.

Consumer products business groups, to deals with watches and lamps.

HMT (International).Ltd which undertakes overseas projects and

topics.

Praga Tools.Ltd which manufactures machine tools.

HMT Bearings.Ltd which manufactures precision bearings in

collaboration with M/s KOYO of Japan.

THE PRODUCT RANGE OF MACHINE TOOLS BUSINESS GROUP

Banglore

Heavy duty lathes

Single and multi-spindle automates

Radial drilling machines

Multi Spindle Drills

Cylindrical and Surface Grinders

Gear Cutting Machines

Laser Cutting Habbers

CNC Turn Mill Centres

Fine Boring Machines / SPM’s

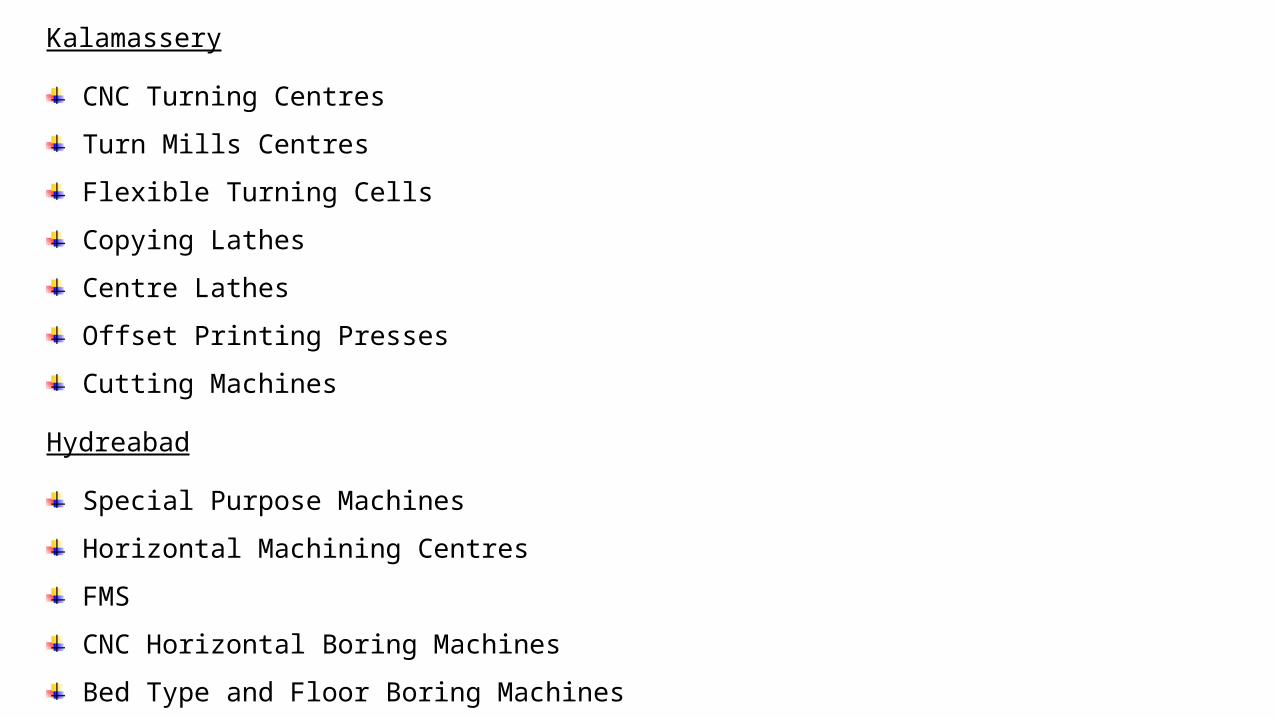

Kalamassery

CNC Turning Centres

Turn Mills Centres

Flexible Turning Cells

Copying Lathes

Centre Lathes

Offset Printing Presses

Cutting Machines

Hydreabad

Special Purpose Machines

Horizontal Machining Centres

FMS

CNC Horizontal Boring Machines

Bed Type and Floor Boring Machines

Major Machines/Inspection Facilities Available In Different MTBS Units

1) CNC ram type Plano millers

2) Horizontal machining centres

3) Vertical Machining centres

4) Horizontal jig boring machines

5) Vertical jig boring machines

6) CNC turning machines

7) Turn mill centres

8) Slide way grinders

9) Cylindrical grinders

10)Internal grinders

11)Precision gear shapers

12)Precision gear hoppers

INDUSTRY PROFILE

The Machine tool industry constitutes backbone of the industrial sector and is vital

for the growth of the Indian machine tools industry. Even though the Indian

machine tools industry is a small segment of the engineering industry it plays a very

important role in the development and technology of up graduation of the

engineering industry. The quality of mother machine tools and their automation

level. The development of the machine tools industry is therefore of paramount

importance for a competitive and self-industrial structure

HMT ORGANIZATIONAL CHART

President Of India

Ministry Of Heavy Industries

Board Of Directors

Chairman & Managing Director

Departments

Finance Department

Joint Finance Manager(JGM)

Cost Accounts

Officers

Junior Officers

Office Staffs

FINANCE DEPARTMENT CHART

Following are the major functions of finance department in HMT Machine Tools, Kalamassery.

To provide strategic financial support regarding operational and general business planning.

To meet internal and external needs and financial reporting requirements of the company at

large.

Providing financial information guidance and advising to other departments.

Vetting and appraisal of capital expenditure investment proposals to ensure their financial

viability.

Budgeting and monitoring variance.

Management of taxes.

Ensuring timely payment of employee’s salary and other welfare expenses.

Working capital management.

HMT Finance Department Has the Following Sections

1. Outward Bills Section (OBS)

2. Inward Bills Section (IBS)

3. Wages/Time Office

4. Provident Fund

5. Main Accounts & Cost Accounts

6. Cash

7. Concurrence

1) Outward Bills Section (OBS)

OBS maintains the records of sundry debtor’s accounts of sales of machines special

accessories spares and job order. OBS monitors and follow up with debtor for

realization of outstanding dues. OBS also prepares the provision entries servicing

invoices. All the works related to sales tax, excise duty and service tax comes under the

ambit of OBS.

2)Inward Bills Section (IBS)

IBS is concerned with purchase accounting and authorizing payments to creditors

contractors and also variance expenses. Like water, Electricity, Hire charges, Insurance,

Welfare expenses, Legal charges, AMC’s. This section also handles import proceedury

like LC opening, authorizing direct transfer to foreign customer (TT) monitoring

exchange rate variations arranging for forward cover from bank etc.

3.Wages / Time Office

Wages prepares payrolls of officers, workers, trainees on the basis of muster roll given by the time office given by the

time office. Payroll preparations is computerized and the salary/wages are also engage with the work of leave of

employees, conveyance reimburse settlement, calculation and disbursement of retirement benefits etc.

4. PROVIDENT FUND

Provident Fund section arranges for the recovery of Provident Fund from the employee salary. Present statutory, minimum

recovery is 12% of basic salary + Dearness allowance ( DA ) .The employees re allowed to contribute higher amount

voluntary (VPF).Out of 12% contribution made by employer an amount equal to 8.33% is transferred to employees’

pension fund. Provident Fund section also provides the loan facility to employees as per stipulated terms and conditions.

5. MAIN ACCOUNT AND COST ACCOUNTS

All cost data required by financial accounts such as SIT, WIP are prepared by cost accounts section. Main accounts related

to material accounts. Weighted average rate is following for inventory valuation .Half yearly periodical physical

verification of stock is conducted by main accounts and whenever discrepancies occurred they are analyzed and rectified.

This section prepares monthly and annual financial statements (balance sheet, P & L account, notes to accounts, cash flow

statements etc.) and co-ordinates with internal / statutory auditors and also with comptroller and auditor general of India.

6. CASH

Cash section keeps cash day book a bank day book. The payment vouchers prepared by

wages / IBS are sent to cash department for payments. Generally payments are made though

NEFT or RTGS. This section also prepares bank reconciliation statement and daily cash flow

statement and also monitor that cash credit does not exceed the permitted limit.

7. CONCURRENCE

All purchase proposals are sent to concurrence section for financial department. They make it

sure that all purchase is made according to the purchase manual. In short all purchase

(whatever it may be) can be made only with the approval of finance department.

Total Employees Strength – 25

REVIEW OF LITERATURE

• Sheridan, John W (2008) describes that besides its ability to signal changes in the business cycle

the inventory-to-sales (I/S) ratios is also looked upon as an indicator of economic health. While

the manufacturing I/S ratio are currently outstanding and the system ratio appear good, smart

buyers are continuing go view these ratios with caution. Although the low level of inventories

currently kept by manufactures significantly reduces the possibly of an economic downturn

stimulated by this sector, the retail sector is a cause for concern. A number of factors reinforce the

idea that there has been a fundamental shift in the structural relationship between manufacturing

and retail. This new inventory relationship is as yet untested. If inventories have been shifted to

the retail level and not actually lowered, then the benefits are mainly to manufacturing and will

not be realized by the system over all. It could be that the current system I/S ratios are too high.

RESEARCH METHODOLOGY

The process used to collect information and data for the purpose of making financial decisions. The

methodology may include publication research, interview, surveys and other research techniques and

could both present and historical information.

Type of research is based on descriptive and analytical research.

•Sources of data collection:

•Secondary data means the data which has already been collected by some other persons at some other

time for the other purpose.

•Important source of secondary collections are:

1. Annual reports of HMT for the past five years.

2. Internet

3. Project reports

•Period of the study- two months

DATA ANALYSIS & INTERPRETATION

•Working Capital Management is important part in firm financial management decision improper management

makes on the WIP- Working In Process to the develop on the various development of working financial process

on the basis of managing on developing the financial statements. Working capital management the develop

mentation of the manufacturing their goods on the basis of short term liabilities and non-short liabilities.

•The working capital requirements is the minimum amount of resources that a company requires to effectively

cover the usual costs and expenses necessary to operate the business. Since the capital needs of each company

will be a little different there is no ideal amount of working capital there is a universally applicable to all

business or even to companies engaged in the same industry. Even so new companies can develop an idea of

what type of requirement there will need to operate at given levels of researching the cost and expenses

associated with other corporations engaged in similar operations.

Working Capital Ratio = Current Assets

Current Liabilities

Working Capital Ratio or WCR is used to rat ionize between the capitals ratios used in every year. In every

financial year the working capital ratio where calculated by the HMT.CO.LTD. The working capital ratio is the

same as the current ratio. It is the relative proportion of an entity current assets to its current liabilities, and is

intended to show the ability of a business to pay for its current liabilities with its current assets. A working

capital ratio of less than

1.0 is an stronger indicator that there will be liquidity problems in the future while a ratio in the vicinity of 2.0

is considered to represent good short term liquidity.

To calculate the working capital ratio or WCR divided all current assets by all current liabilities.

The Formula is:

Calculation of working capital and working capital ratio of the year 2010Current Liabilities Current Assets

Current Liabilities 219973407

Provisions 199157643

Inventories 152601938

Sundry Debtors 180633762

Cash & Bank Balances 2774449

Other Current Assets 4495952

Loans & Advances 93908483

Total Liabilities = 419131050 Total Assets = 434414584

Working Capital = Current Assets – Current Liabilities

WC = 434414584-419131050

WC = 15283534

Working Capital Ratio = Current Assets Current Liabilities

WCR = 434414584 419131050

WCR = 1.03646

Calculation of Working Capital and Working Capital Ratio Of the year 2011

Current Liabilities Current Assets

Short Term Borrowings 81127245 Trade Payables 71701944 Other Current Liabilities 175501961 Short Term Provisions 109739156

Inventories 152052469 Trade Receivables 171843630 Cash & Receivables 73197 Short Term Loans & Advances 99043367 Other Current Assets 5873224

Total Liabilities = 438070306 Total Assets = 428885887

Working Capital = Current Assets – Current Liabilities

WC = 428885887-438070303

WC = -9184419

Working Capital Ratio = Current Assets Current Liabilities

WCR = 428885887 438070306 WCR = 0.97903

Calculation of Working Capital and Working Capital Ratio Of the year 2012

Current Liabilities Current Assets

Short term borrowings 68567606 Trade Payables 103898347 Other Current Liabilities 195229138 Short term provisions 84414779

Inventories 169780425 Trade Receivables 170327794 Cash & Cash equivalents 76067 Short terms loans & Advances 85224046 Other Current Assets 8289345

Total liabilities = 452109870 Total Assets = 433697677

Working Capital = Current Assets – Current Liabilities

WC = 433697677-452109870

WC = 18412193

Working Capital Ratio = Current Assets Current Liabilities WCR = 433697677 452109870 WCR = 0.95927

Calculation of Working Capital and Working Capital Ratio of the year 2013

Current Liabilities Current Assets

Short Term Borrowings 82653264 Trade Payables 70888197 Other Current Liabilities 281591160 Short Term Provisions 91140691

Inventories 143657435 Trade receivables 251713881 Cash & Cash Equivalents 1409201 Short Term Loans & Advances 91245052 Other Current Assets 7835561

Total Liabilities = 5262736312 Total Assets = 495861130

Working Capital = Current Assets-Current Liabilities

WC = 495861130-5262736312

WC = -30412182

Working Capital Ratio = Current Assets Current Liabilities WCR = 495861130 5262736312 WCR = 0.94221

Calculation of Working Capital and Working Capital Ratio of the year 2014

Current Liabilities Current Assets

Short Term Borrowings 83083395 Trade Payables 111659326 Other Current Liabilities 300623164 Short Term Provisions 78282871

Incentives 191003844 Trade Receivables 221851604 Cash & Cash Equivalents 17509886 Short Term Loans & Advances 82211666 Other Current Assets 7465983

Total Liabilities = 573648756 Total Assets = 520042983

Working Capital = Current Assets-Current Liabilities

WC = 520042983-573648756

WC = -53605773

Working Capital Ratio = Current Assets Current Liabilities WCR = 520042983 573648756 WCR = 0.90655

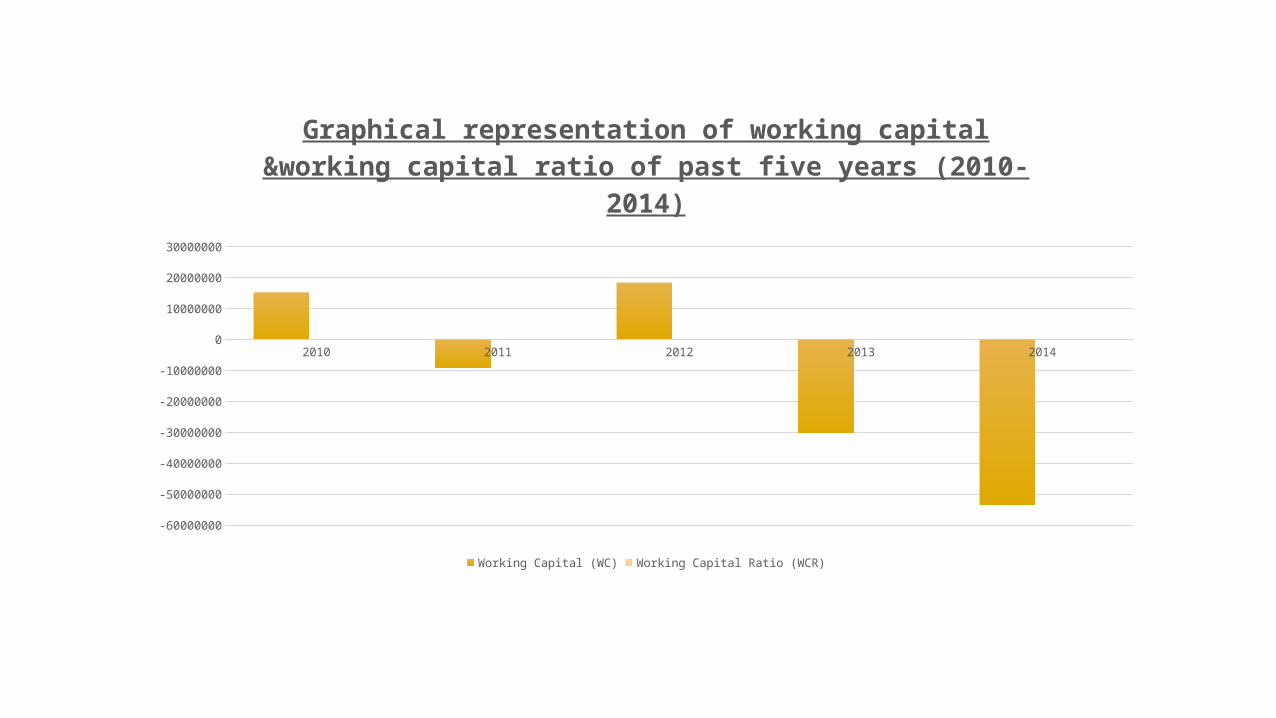

Year Working Capital (WC) Working Capital Ratio (WCR)

2010 15283534 1.03646

2011 -9184419 0.97903

2012 18412193 0.95927

2013 -30412182 0.94221

2014 -53605773 0.90655

TABLE SHOWING WORKING CAPITAL & WORKING CAPITAL RATIO OF FIVE YEARS FROM 2010-2014

2010 2011 2012 2013 2014

-60000000

-50000000

-40000000

-30000000

-20000000

-10000000

0

10000000

20000000

30000000

Graphical representation of working capital &working capital ratio of past five years (2010-2014)

Working Capital (WC) Working Capital Ratio (WCR)

FINDINGS

Working capital ratio of the company decrease every year as per the calculation of

working capital ratio of past five years.

Working Capital of the company fluctuate every year.

Working capital management of the company is efficient in managing the working

capital.

Every year increase the company’s working capital.

WC & WCR levels are fluctuate every year and make improvement for company’s

future growth.

SUGGESTIONS

More care in the handling of working capital of the company.

The lower the inventories to working capital ratio, the higher the liquidity of the

company.

HMT is a heavy consumer of electricity and in the recent past the electricity tariff

increased many folds.

More care in the controlling of liabilities with assets.

The company working capital is used efficiently and effectively.

CONCLUSION

HMT is pioneer in the market and has created reliability and credibility among the customers. It has an excellent

transporting facilities and proximity to national high way, railway line, sea port and airport as well. A better

inventory management will surely be helpful in solving the problem that the company is facing with respect to

inventory and will pave the way for reducing the huge investment or blocking of investment in inventory.

Inventory management is vitally important to almost every type of business, whether product or service oriented.

Inventory control touches almost every facets if operation. A proper balance must be struck to maintain proper

inventory with the minimum financial impact on the customer. Inventory control is the activities that maintain

stock keeping items at desired level. In manufacturing since the focus is on physical product, inventory control

focus on material control. The goal of the wealth maximization is affected by the efficiency with which inventory

is managed. Inventories constitute about 60% of current assets of companies in India. The manufacturing

companies hold inventories smooth production and sales operation to guard against the risk of unpredictable

changes in usage.

THANK YOU