Embed Size (px)

Citation preview

Fundamentals of Derivatives-

F&O

Presented by:-Hemal Muchhala 65Abhishek Pathak 75Yogesh Periwal 78Amit Shah 88

Points to remember……….

Long – Buy …………..(going long)

Short – Sell …………...(going short)

Squaring off – opposite transaction to the

previous one

Close out – opposite transaction to the previous

one (usually done by the exchange)

Buy low, sell high - gives a profit

Sell high, buy low - also gives a profit

What are Derivatives?

Derivatives are financial contracts whose value/price is dependent

on the behavior of the price of one or more basic underlying assets

(often simply known as the underlying).

Commodities

Equity shares

Equity share index

Bonds

Currencies

Eg:- CURD

Derivatives were introduced gradually in our country in thefollowing order:

NSE Index Future 12.06.2001

NSE Index Option 04.06.2001

Stock Options 02.07.2001

Stock Futures 09.11.2001

No. of securities have been increased gradually for inclusionin F&O.

Important Dates and Facts

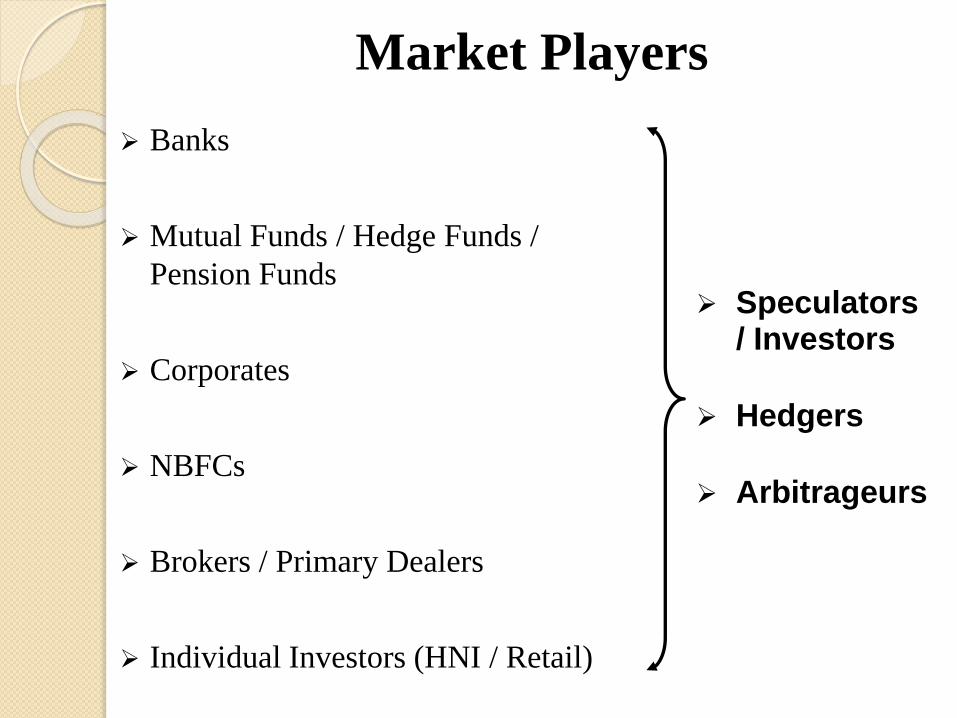

Market Players

Speculators/ Investors

Hedgers

Arbitrageurs

Banks

Mutual Funds / Hedge Funds /

Pension Funds

Corporates

NBFCs

Brokers / Primary Dealers

Individual Investors (HNI / Retail)

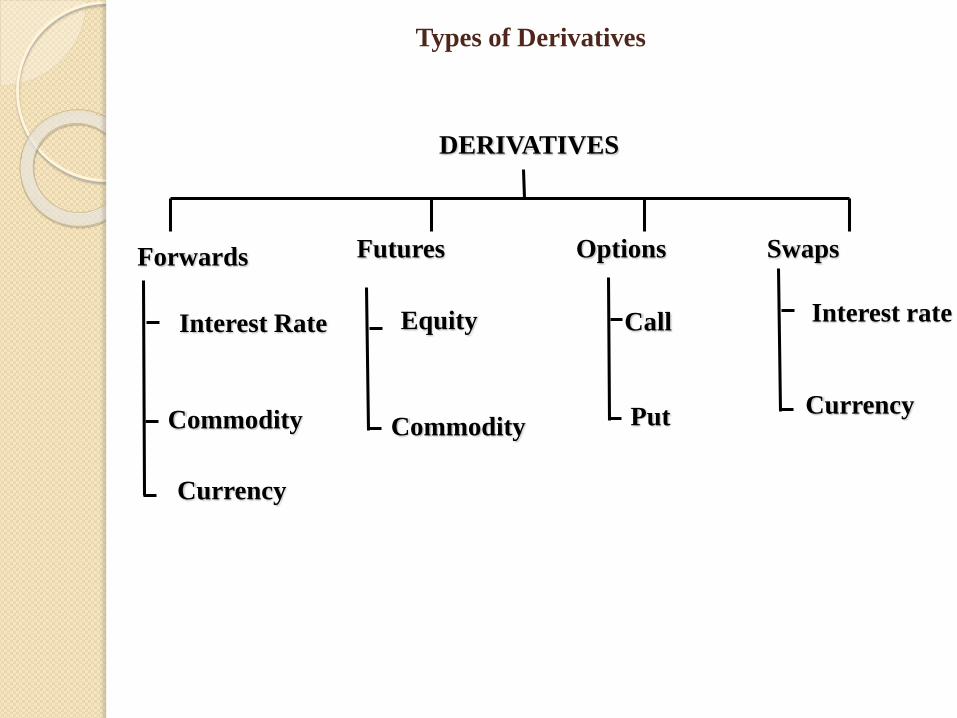

Types of Derivatives

DERIVATIVES

Forwards Futures Options Swaps

Commodity

Equity

Put

Call

Currency

Interest rate

Commodity

Interest Rate

Currency

What are forward contracts?

A forward contract is a customised

contract between the buyer and the seller

where settlement takes place on a specific

date in future at a price agreed today.

What are futures?

Futures are exchange-traded contracts to

buy or sell an asset in future at a price

agreed upon today. The asset can be share,

index, interest rate, bond, rupee-dollar

exchange rate, sugar, crude oil, soybean,

cotton, coffee etc.

Future Contracts

Three different contracts run simultaneously in Indian Market.

Current month or near month contract

Next month or mid month contract

Third month or far month contract

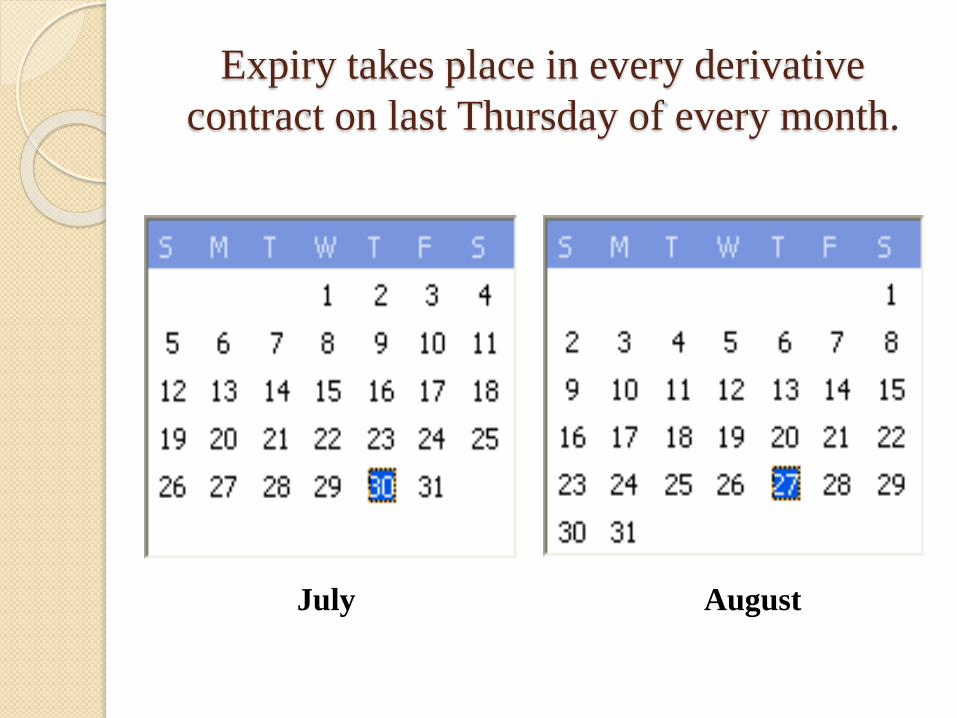

Expiry takes place in every derivative

contract on last Thursday of every month.

July August

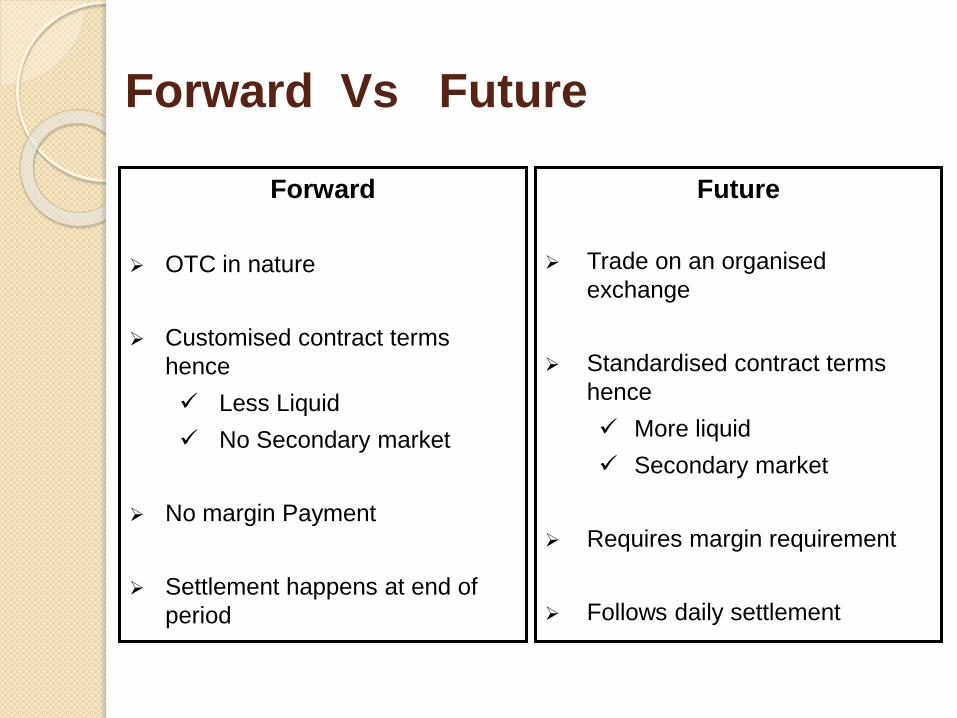

Forward Vs Future

Forward

OTC in nature

Customised contract terms

hence

Less Liquid

No Secondary market

No margin Payment

Settlement happens at end of

period

Future

Trade on an organised

exchange

Standardised contract terms

hence

More liquid

Secondary market

Requires margin requirement

Follows daily settlement

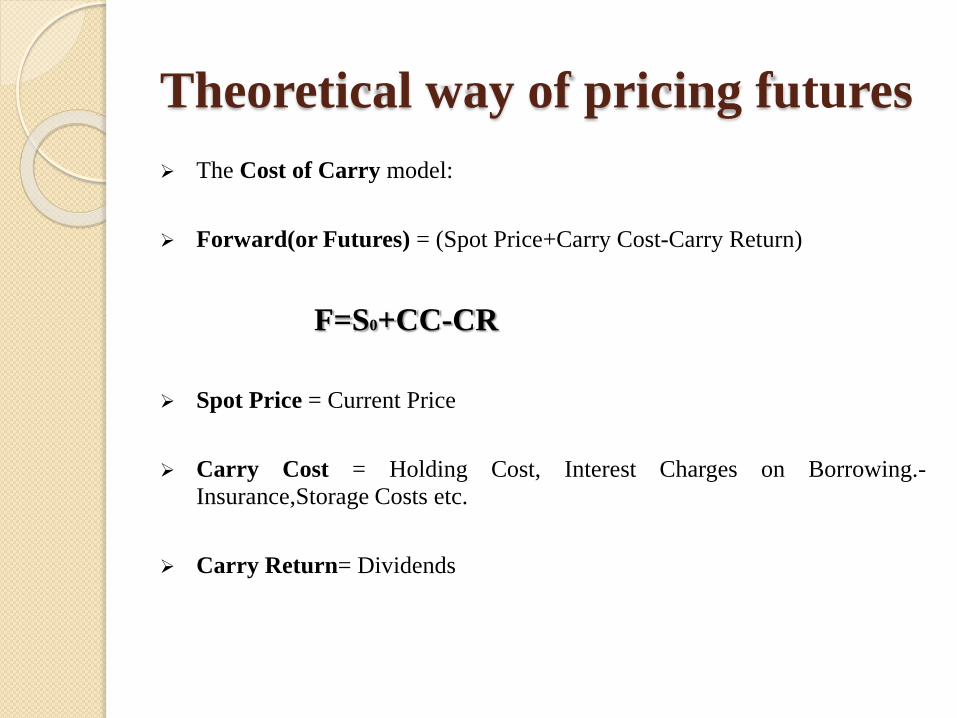

Theoretical way of pricing futures

The Cost of Carry model:

Forward(or Futures) = (Spot Price+Carry Cost-Carry Return)

F=S0+CC-CR

Spot Price = Current Price

Carry Cost = Holding Cost, Interest Charges on Borrowing.-

Insurance,Storage Costs etc.

Carry Return= Dividends

What are the advantages of trading in

futures over cash

Short Selling

Pay only Margin

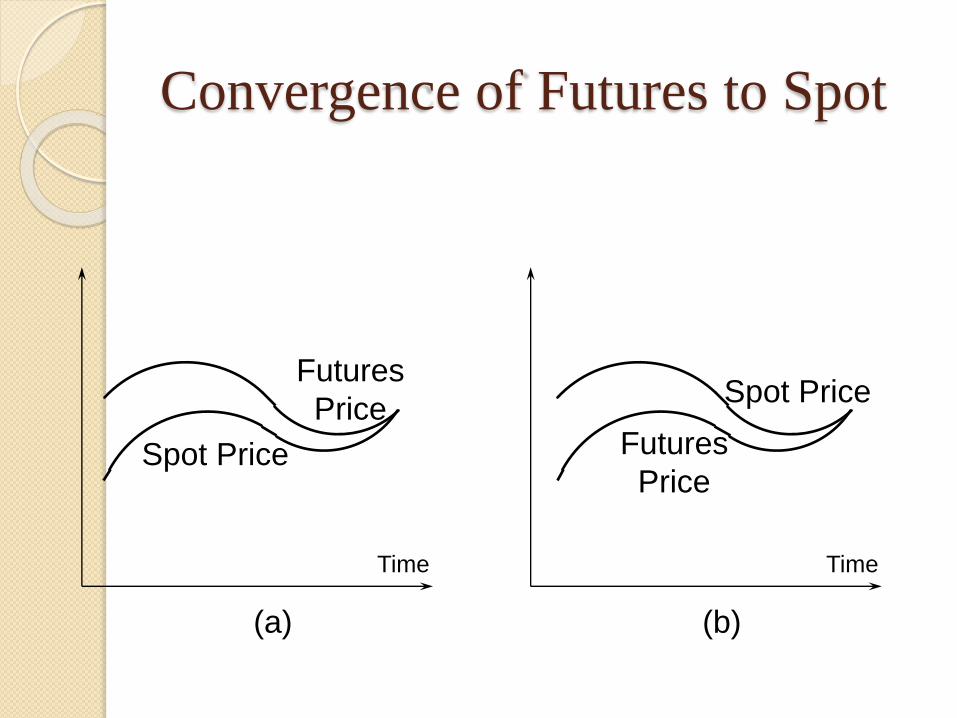

Convergence of Futures to Spot

Time Time

(a) (b)

Futures

PriceFutures

PriceSpot Price

Spot Price

Hedging in Futures

Hedging stock position using stock futures

Hedge the position using Index futures

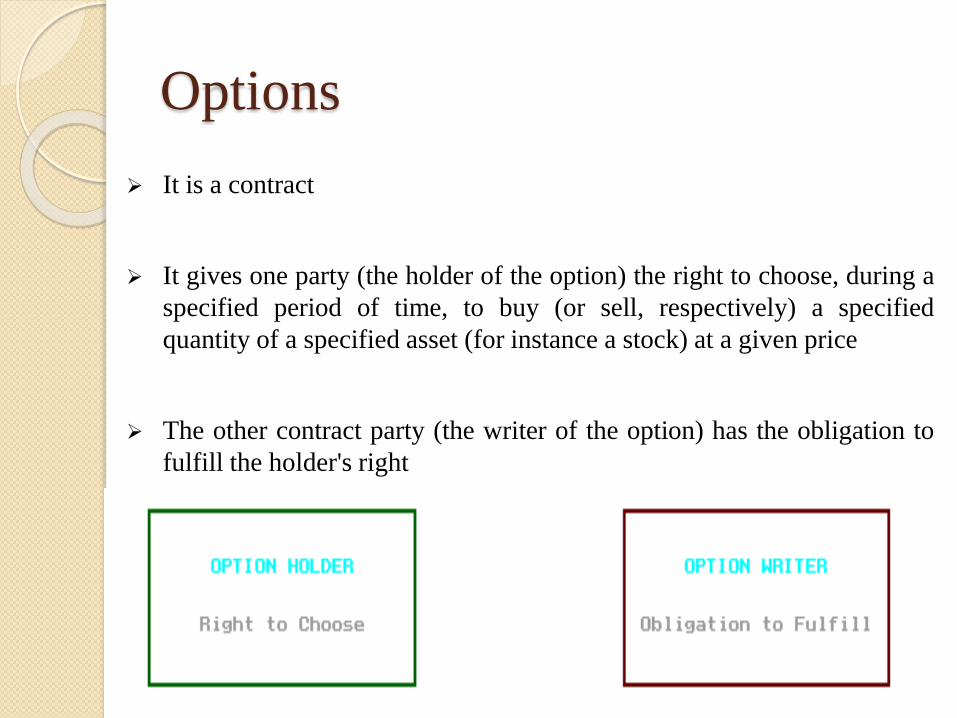

Options

It is a contract

It gives one party (the holder of the option) the right to choose, during a

specified period of time, to buy (or sell, respectively) a specified

quantity of a specified asset (for instance a stock) at a given price

The other contract party (the writer of the option) has the obligation to

fulfill the holder's right

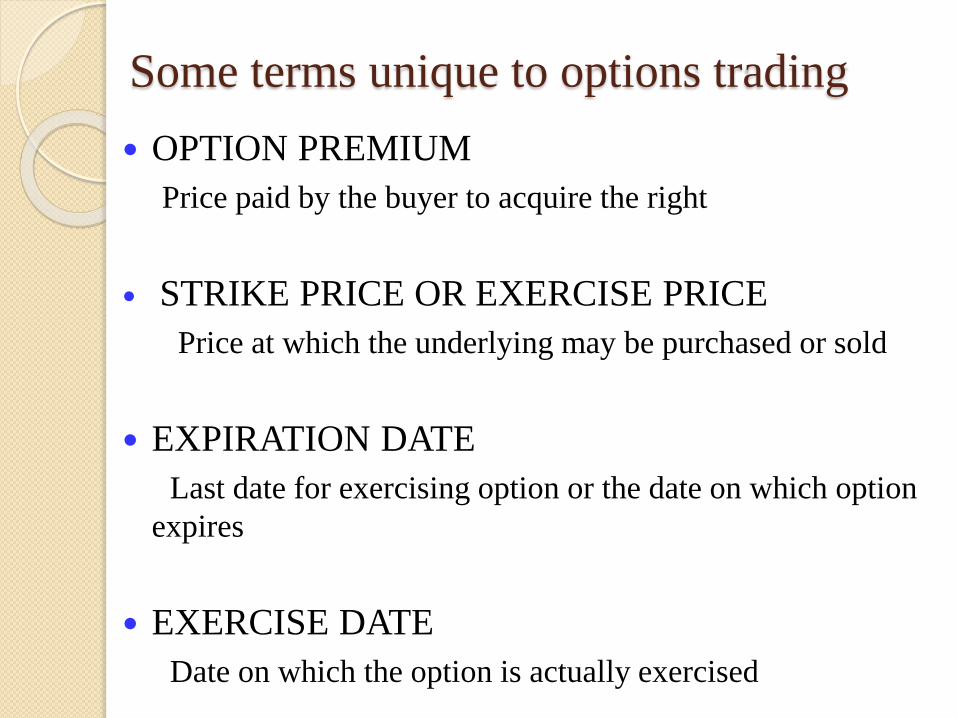

Some terms unique to options trading

OPTION PREMIUM

Price paid by the buyer to acquire the right

STRIKE PRICE OR EXERCISE PRICE

Price at which the underlying may be purchased or sold

EXPIRATION DATE

Last date for exercising option or the date on which option

expires

EXERCISE DATE

Date on which the option is actually exercised

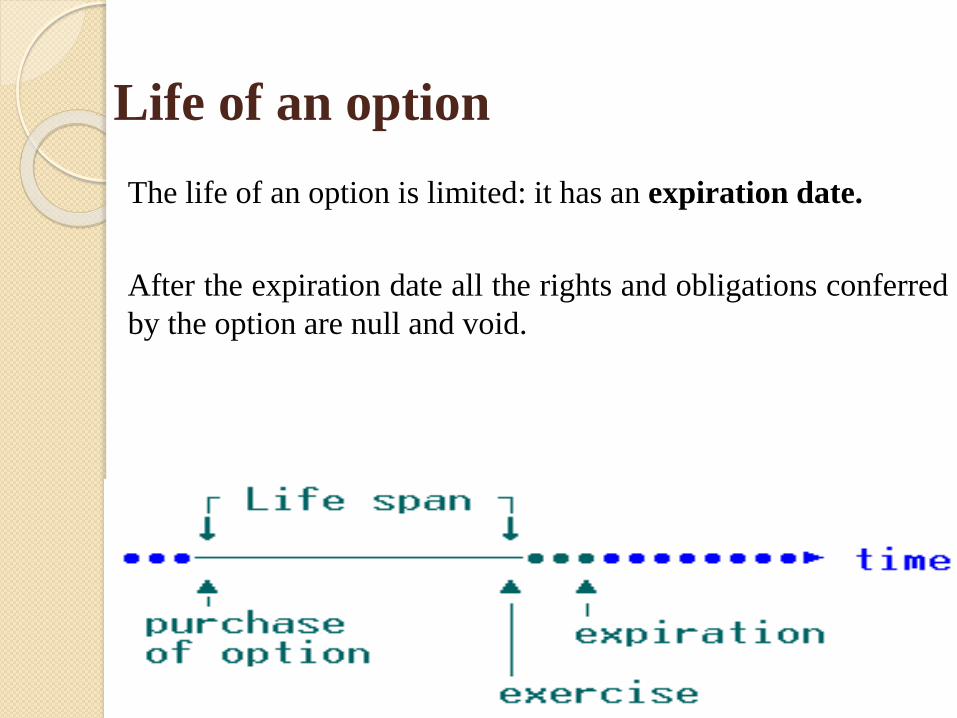

Life of an option

The life of an option is limited: it has an expiration date.

After the expiration date all the rights and obligations conferred

by the option are null and void.

Participants in the Options Market

Buyers of Calls

Sellers of Calls

Buyers of Puts

Sellers of Puts

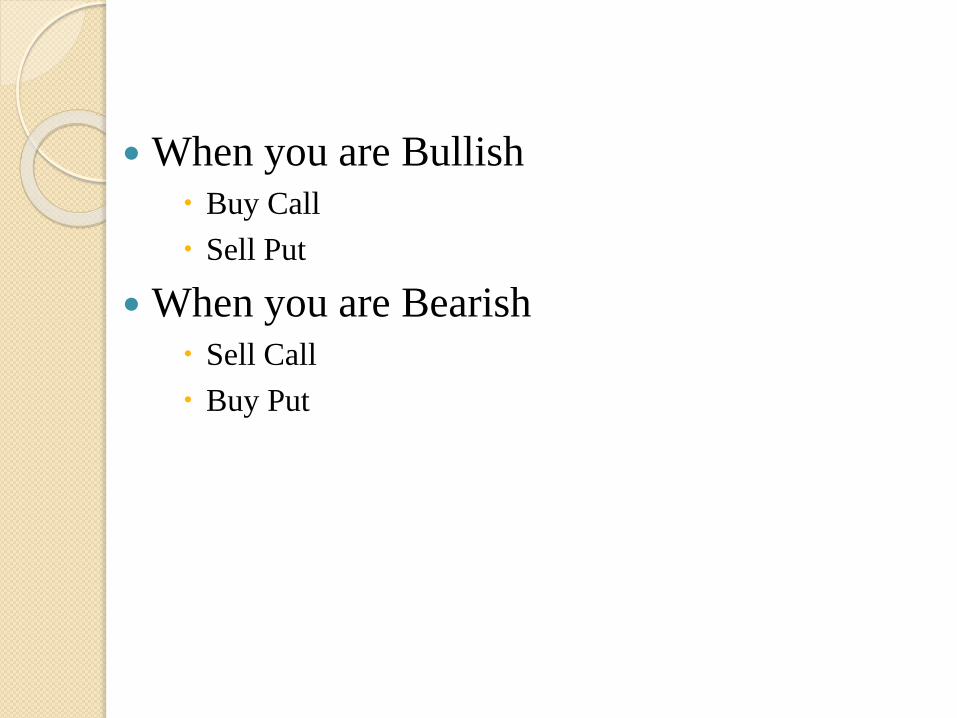

When you are Bullish Buy Call

Sell Put

When you are Bearish Sell Call

Buy Put

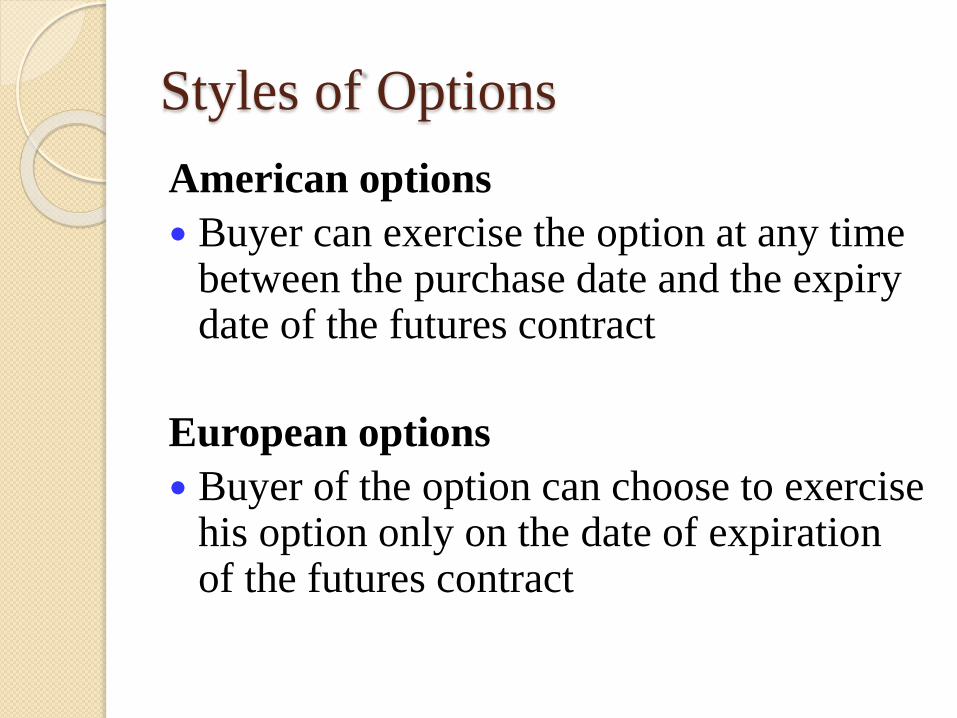

Styles of Options

American options

Buyer can exercise the option at any time between the purchase date and the expiry date of the futures contract

European options

Buyer of the option can choose to exercise his option only on the date of expiration of the futures contract

Options

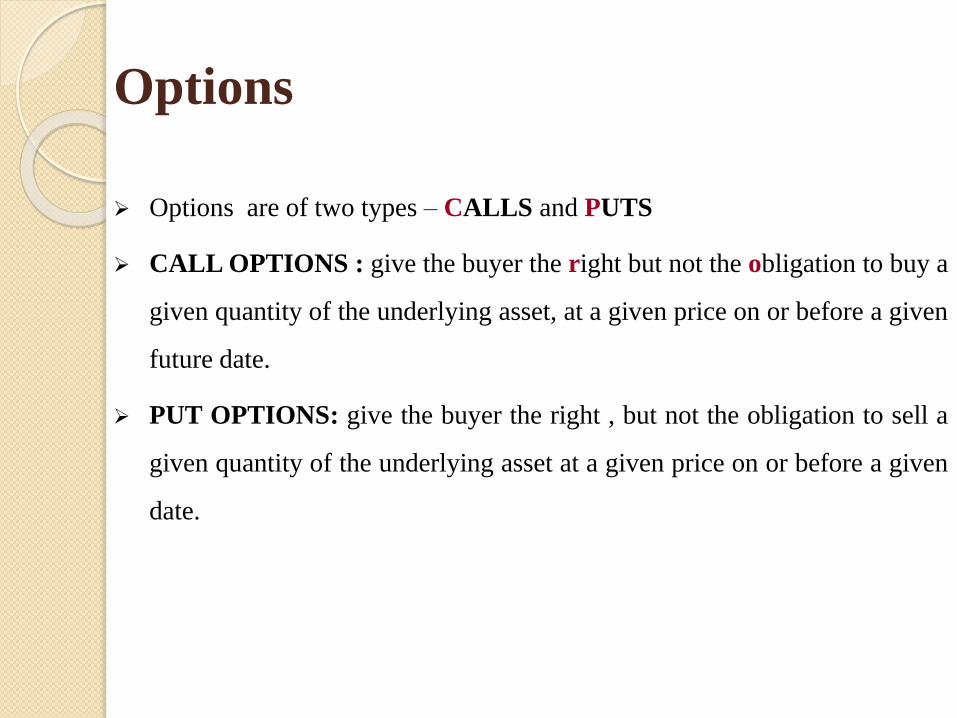

Options are of two types – CALLS and PUTS

CALL OPTIONS : give the buyer the right but not the obligation to buy a

given quantity of the underlying asset, at a given price on or before a given

future date.

PUT OPTIONS: give the buyer the right , but not the obligation to sell a

given quantity of the underlying asset at a given price on or before a given

date.

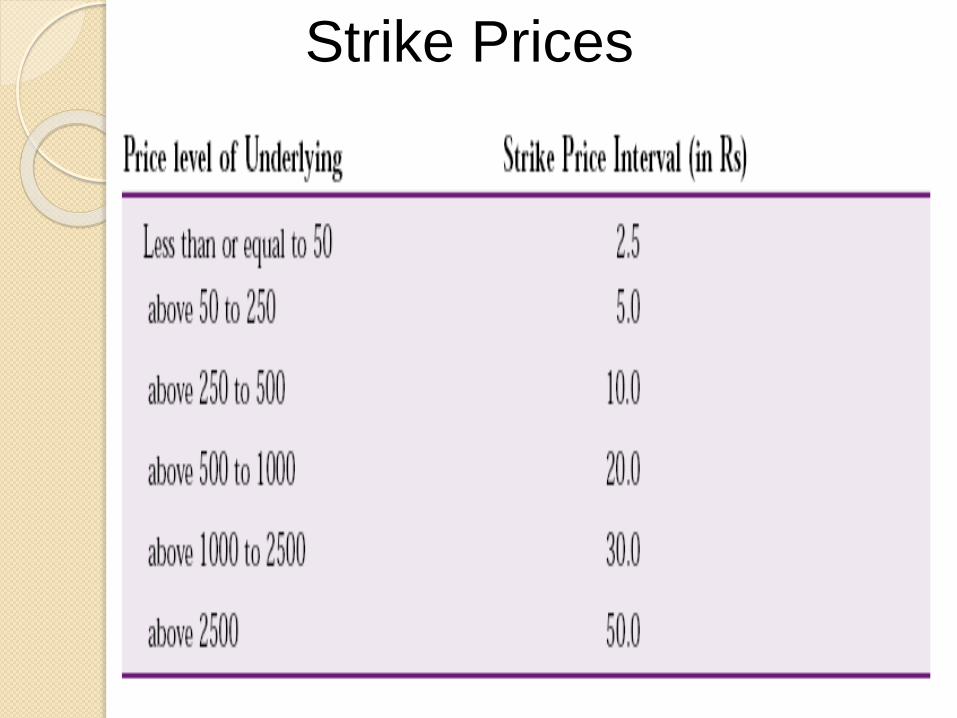

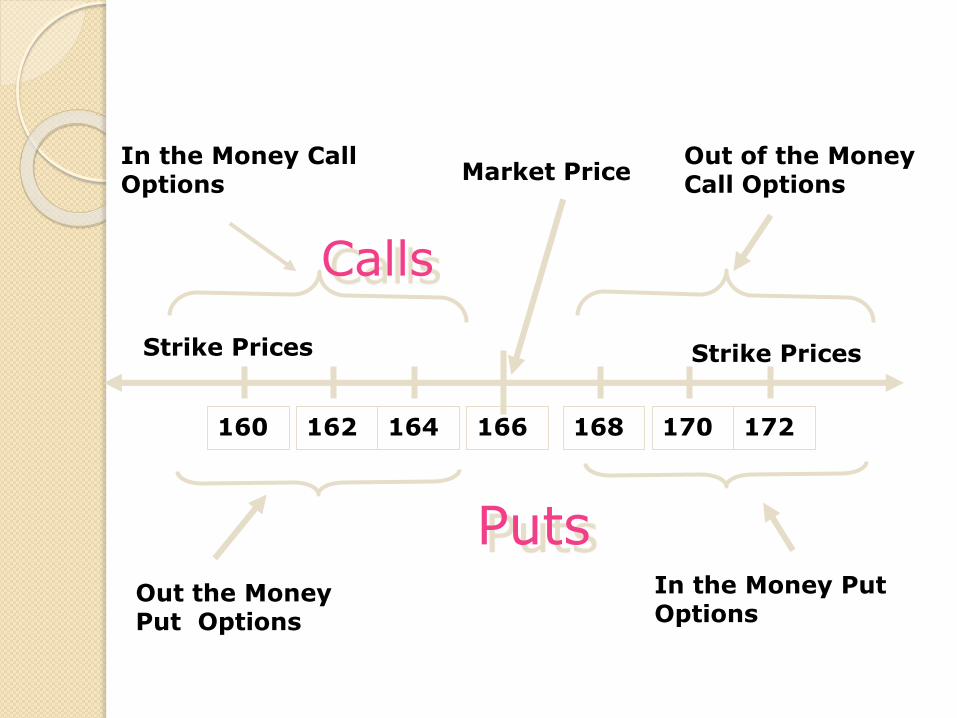

Strike Prices

Market Price

Strike Prices Strike Prices

166 168 170 172164162160

In the Money Call Options

Out of the Money Call Options

Out the Money Put Options

In the Money Put Options

Calls

Puts

Premium

Premium (or Option Price) = Intrinsic Value + Time Value

Intrinsic Value

For a CALL OPTION:

Intrinsic value = Spot Price – Strike price

For a PUT OPTION:

Intrinsic value = Strike price – Spot Price

Intrinsic value can never be negative

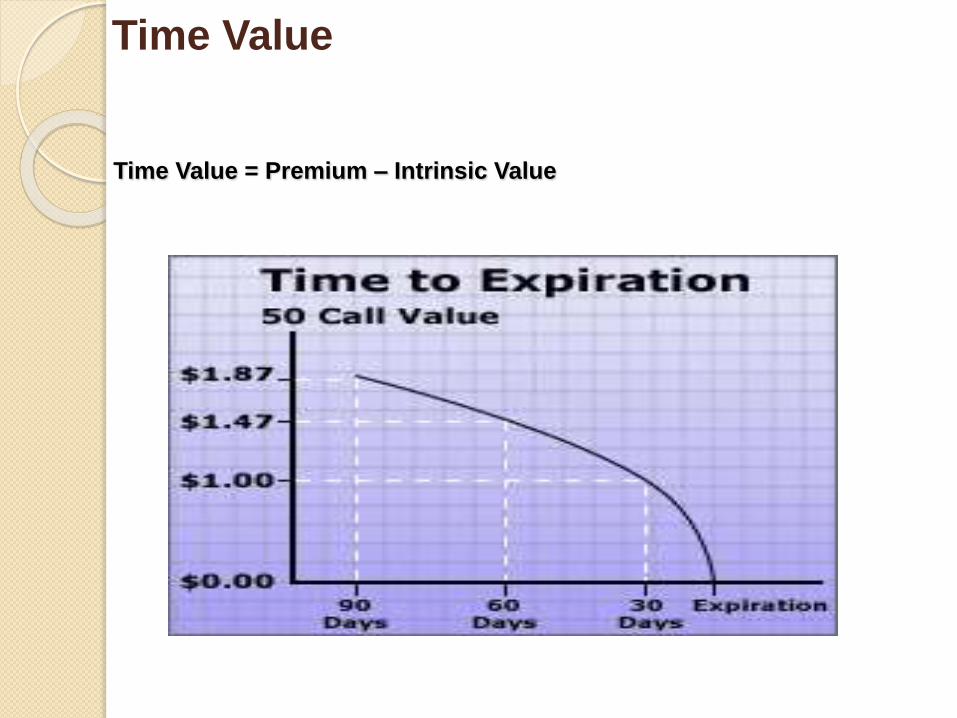

Time Value

Time Value = Premium – Intrinsic Value

Hedging Strategy

Long Put/ Short Call

Long Call/ Short Put

Problems with derivatives

1. “We know where our markets are going”

2. “We don’t understand risk management

markets”

3. “Risk management is a zero-sum game”

4. “Futures markets are speculative”

Thank You

![[Derivatives Consulting Group] Introduction to Equity Derivatives](https://img.pdfslide.us/doc/110x75/5525eed15503467c6f8b4b12/derivatives-consulting-group-introduction-to-equity-derivatives.jpg)