Embed Size (px)

Citation preview

1

CHAPTER 4SHORT TERM INVESTMENT

2

COURSE OUTLINE Characteristics of short term investment Accounting for short term investments

in debt and equity securities-Purchases, disposals and

reclassification-Application of lower of cost or

market (LCM)

3

WHY COMPANY INVEST? To receive a return on idle cash

To develop or maintain relationship with another company

To gain control of another company

4

CHARACTERISTICS OF SHORT TERM INVESTMENT 2 criteria must be met to qualify as a

short term investment: Must be capable of reasonably

prompt liquidation Must be management intent to

convert them to cash within one year (or operating cycle)

5

CLASSIFICATION OF INVESTMENTS Equities securities

Debt securities

6

EQUITIES SECURITIES Represent ownership in a company The shareholders have the right to

collect dividends and vote on corporate matters

7

DEBT SECURITIESFinancial instruments issued by a company that have the following characteristics: A maturity value, representing the

amount to be repaid to the debt holder at maturity

An interest rate, (either fixed or variable)

A maturity date, indicating when the debt obligation will be redeemed

8

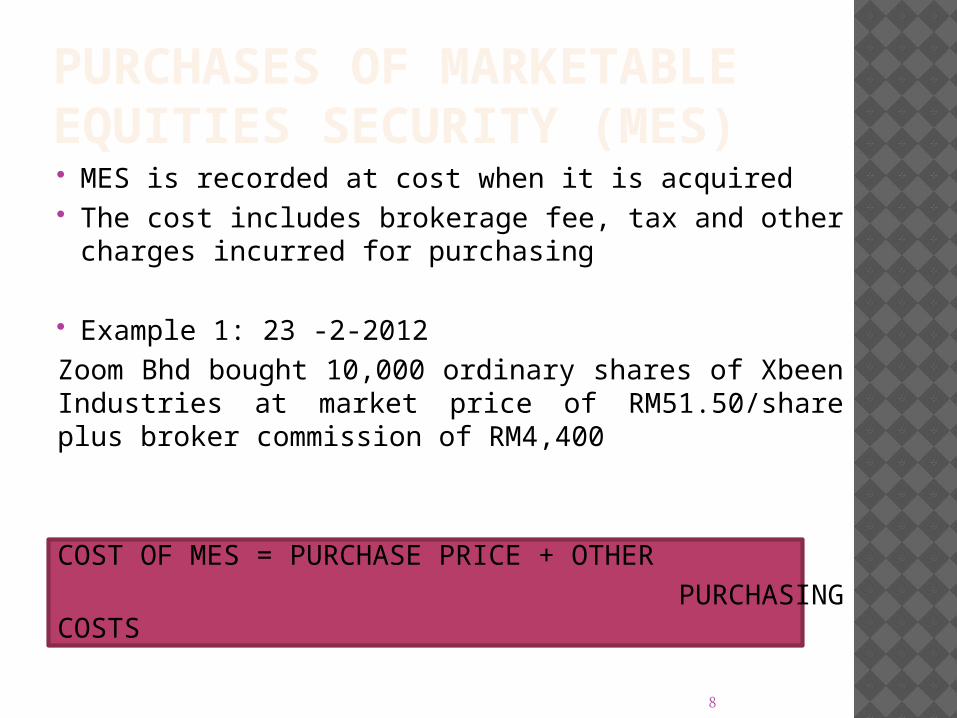

PURCHASES OF MARKETABLE EQUITIES SECURITY (MES) MES is recorded at cost when it is acquired The cost includes brokerage fee, tax and other

charges incurred for purchasing

Example 1: 23 -2-2012Zoom Bhd bought 10,000 ordinary shares of Xbeen Industries at market price of RM51.50/share plus broker commission of RM4,400

COST OF MES = PURCHASE PRICE + OTHER PURCHASING COSTS

9

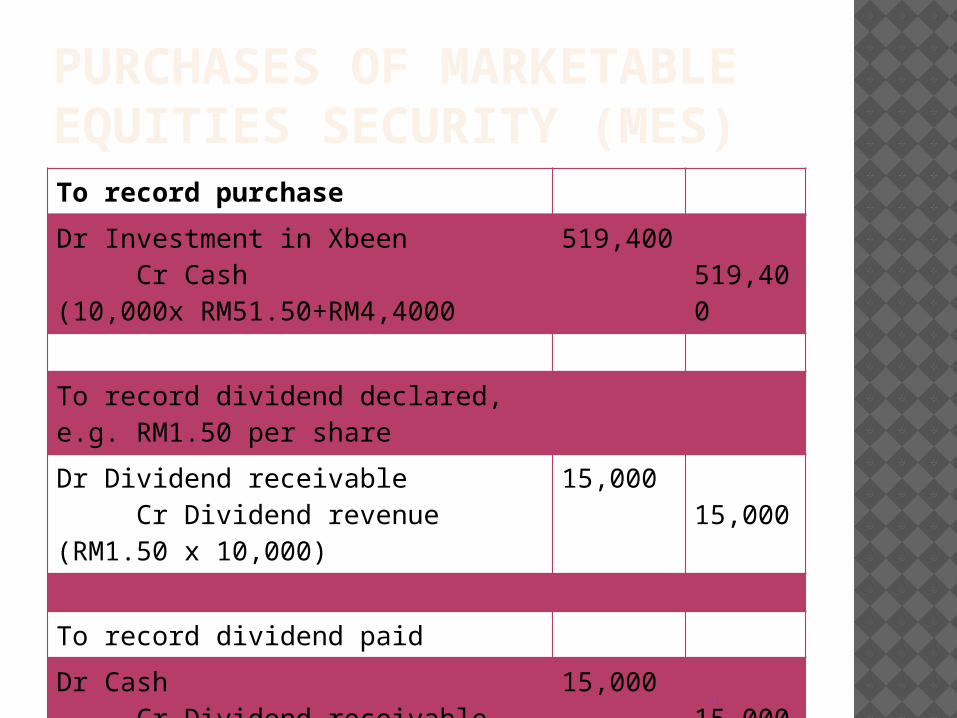

PURCHASES OF MARKETABLE EQUITIES SECURITY (MES)To record purchase

Dr Investment in Xbeen Cr Cash(10,000x RM51.50+RM4,4000

519,400519,400

To record dividend declared, e.g. RM1.50 per share

Dr Dividend receivable Cr Dividend revenue(RM1.50 x 10,000)

15,00015,000

To record dividend paid

Dr Cash Cr Dividend receivable

15,00015,000

10

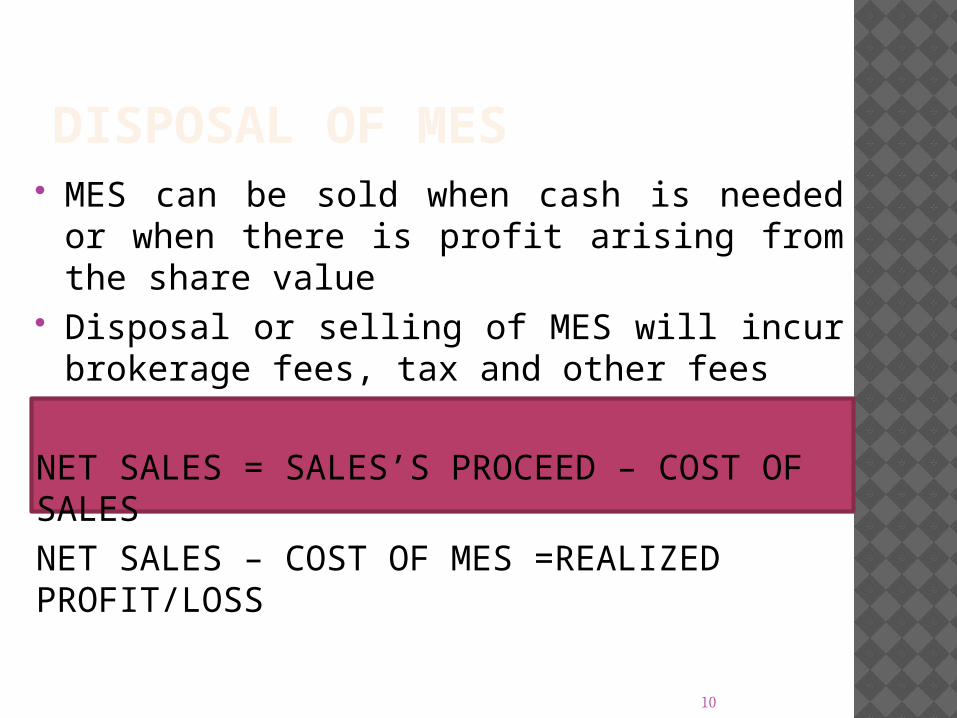

DISPOSAL OF MES MES can be sold when cash is needed or

when there is profit arising from the share value

Disposal or selling of MES will incur brokerage fees, tax and other fees

NET SALES = SALES’S PROCEED – COST OF SALESNET SALES – COST OF MES =REALIZED PROFIT/LOSS

11

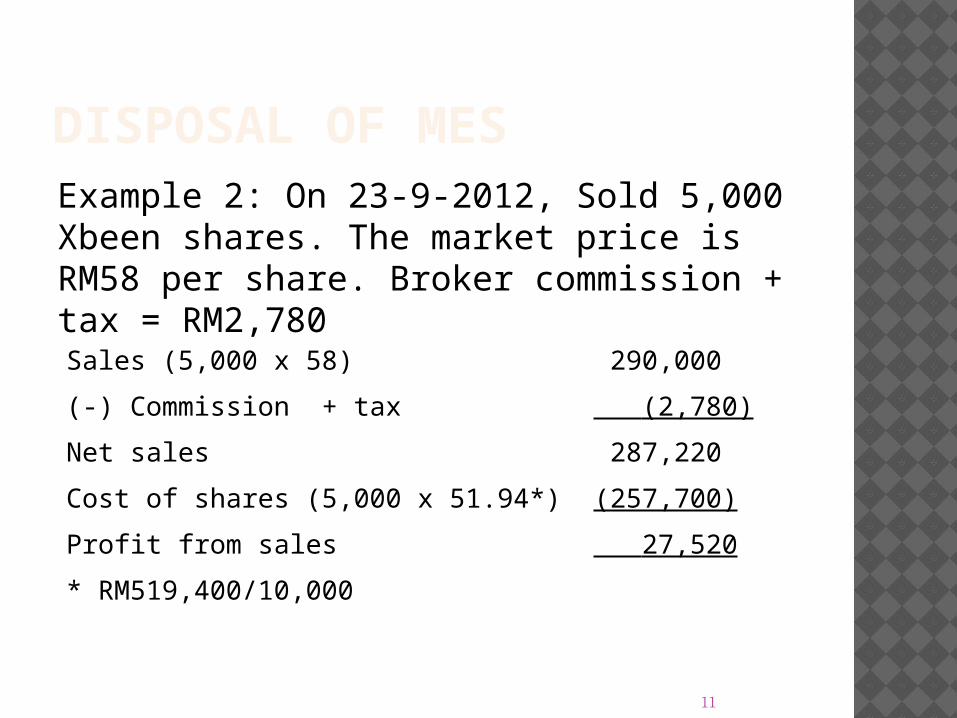

DISPOSAL OF MESExample 2: On 23-9-2012, Sold 5,000 Xbeen shares. The market price is RM58 per share. Broker commission + tax = RM2,780Sales (5,000 x 58) 290,000

(-) Commission + tax (2,780)

Net sales 287,220

Cost of shares (5,000 x 51.94*) (257,700)

Profit from sales 27,520

* RM519,400/10,000

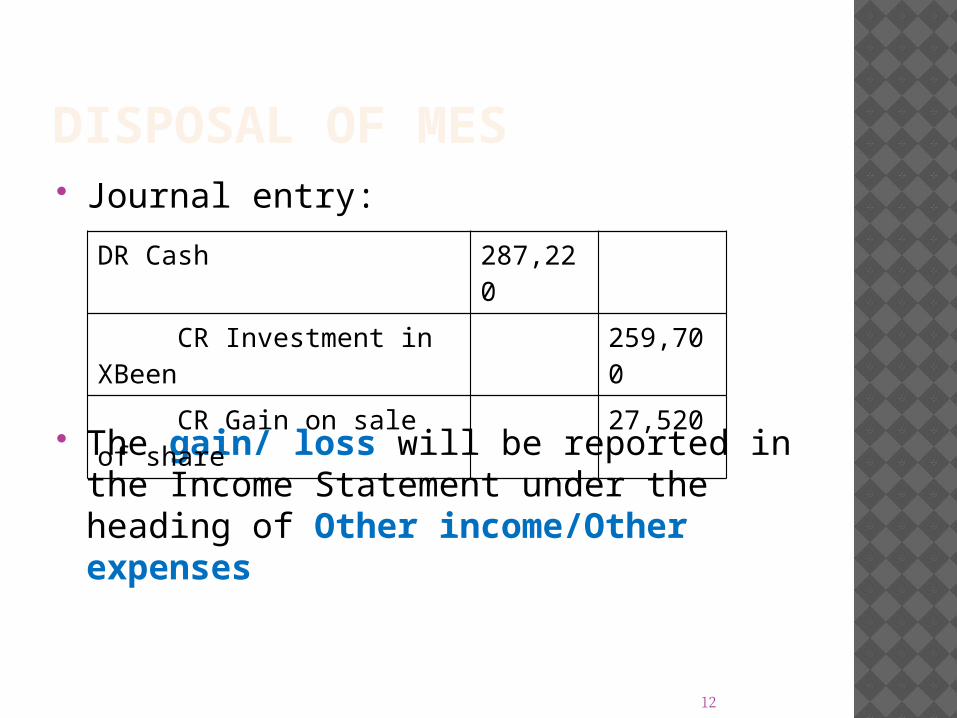

12

DISPOSAL OF MES Journal entry:

The gain/ loss will be reported in the Income Statement under the heading of Other income/Other expenses

DR Cash 287,220

CR Investment in XBeen

259,700

CR Gain on sale of share

27,520

13

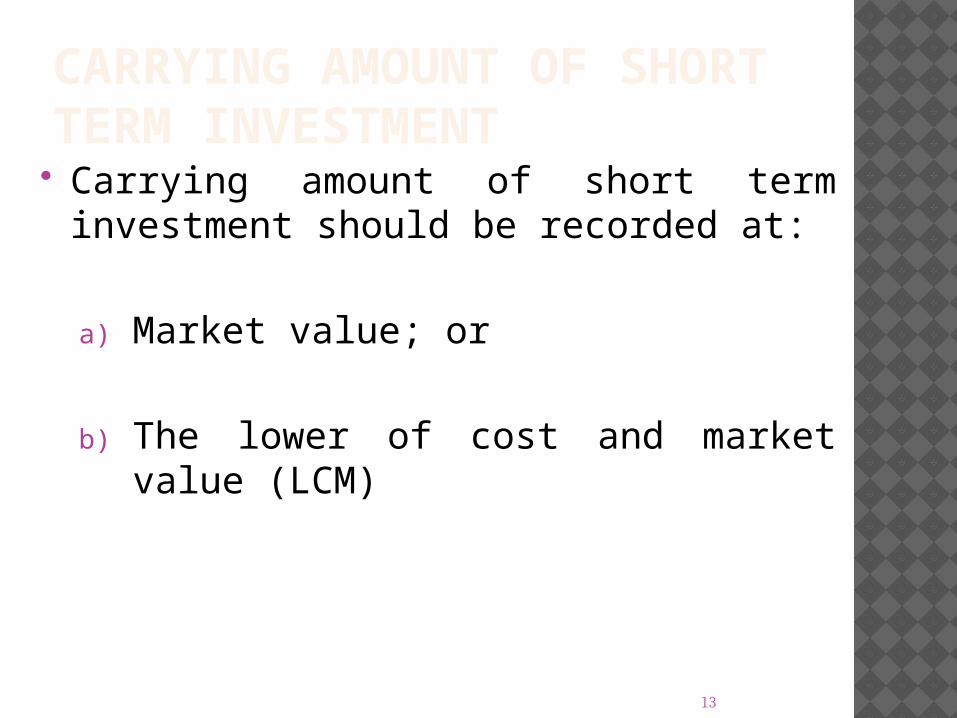

CARRYING AMOUNT OF SHORT TERM INVESTMENT

Carrying amount of short term investment should be recorded at:

a) Market value; or

b) The lower of cost and market value (LCM)

14

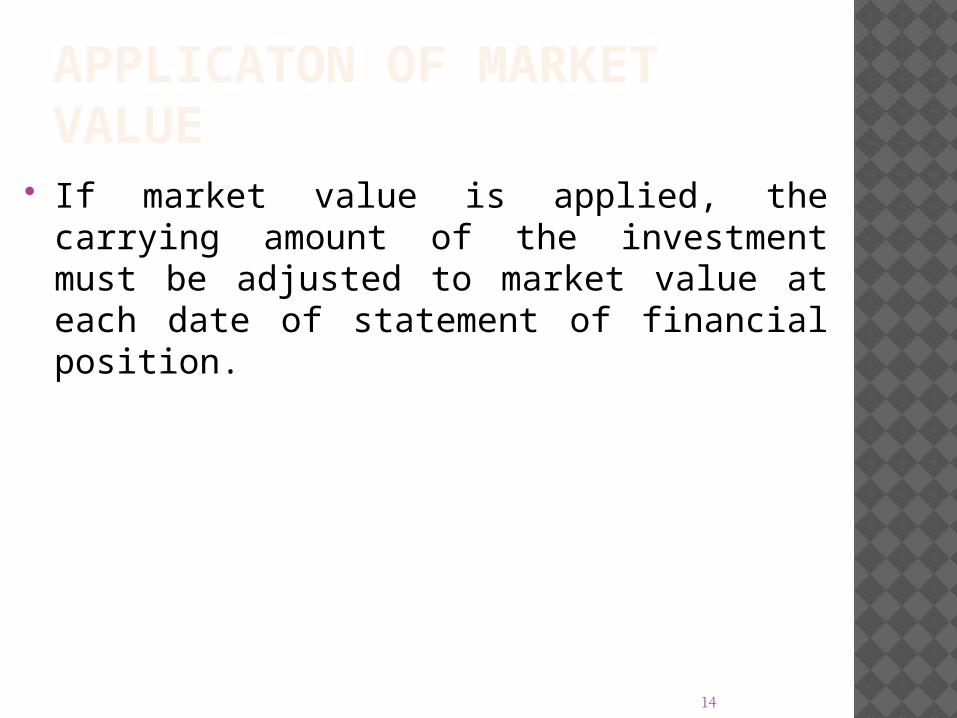

APPLICATON OF MARKET VALUE

If market value is applied, the carrying amount of the investment must be adjusted to market value at each date of statement of financial position.

15

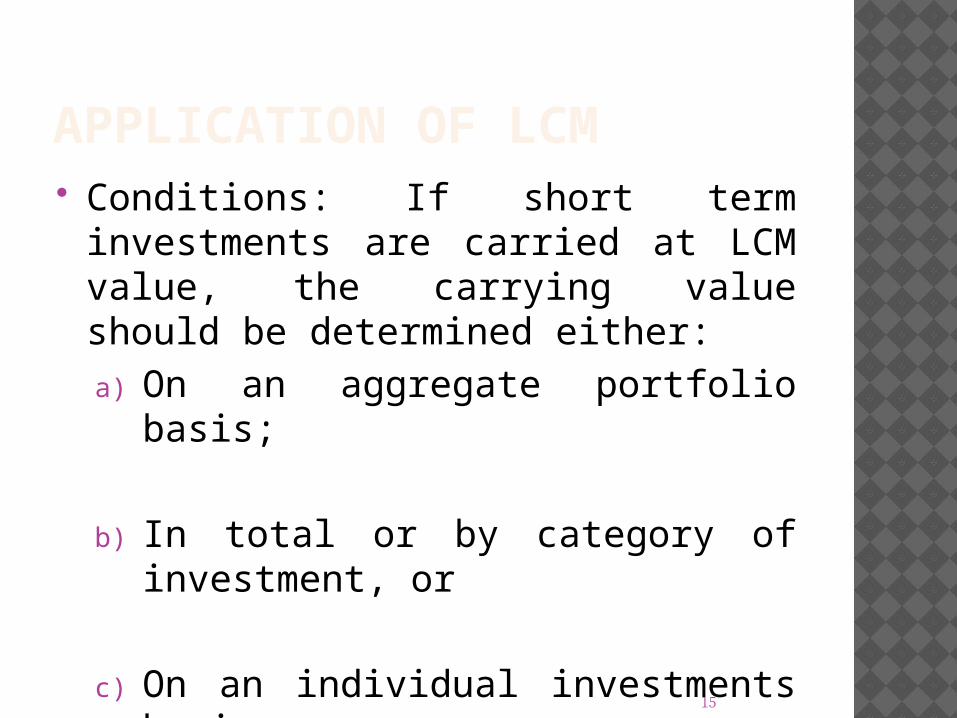

APPLICATION OF LCM Conditions: If short term investments

are carried at LCM value, the carrying value should be determined either:a) On an aggregate portfolio basis;

b) In total or by category of investment, or

c) On an individual investments basis

16

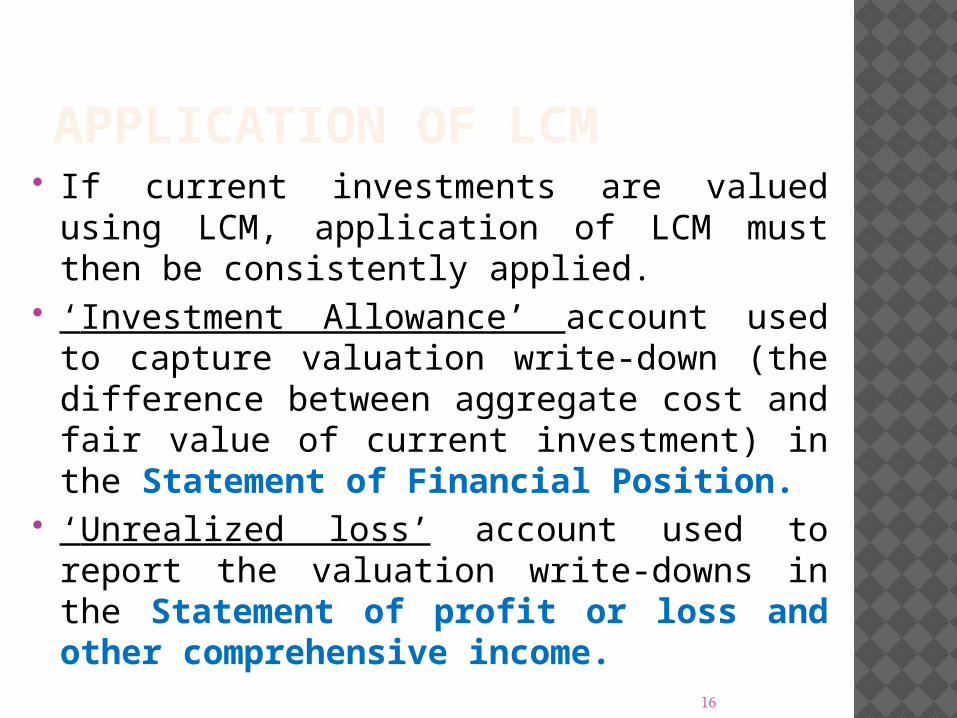

APPLICATION OF LCM If current investments are valued using

LCM, application of LCM must then be consistently applied.

‘Investment Allowance’ account used to capture valuation write-down (the difference between aggregate cost and fair value of current investment) in the Statement of Financial Position.

‘Unrealized loss’ account used to report the valuation write-downs in the Statement of profit or loss and other comprehensive income.

17

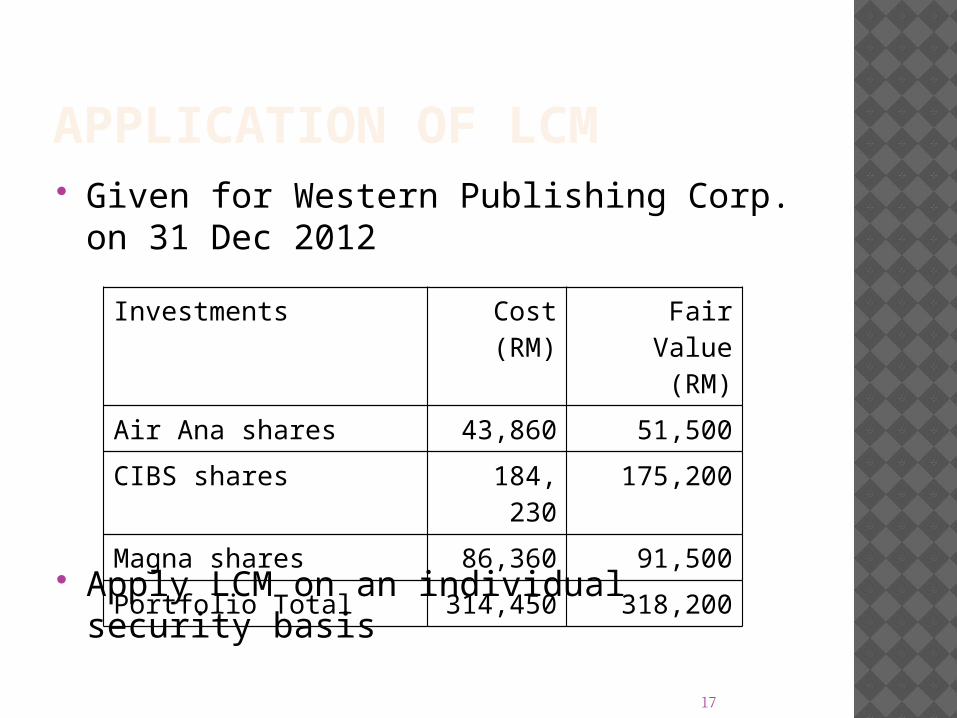

APPLICATION OF LCM Given for Western Publishing Corp. on

31 Dec 2012

Apply LCM on an individual security basis

Investments Cost (RM)

Fair Value (RM)

Air Ana shares 43,860 51,500

CIBS shares 184, 230 175,200

Magna shares 86,360 91,500

Portfolio Total 314,450 318,200

18

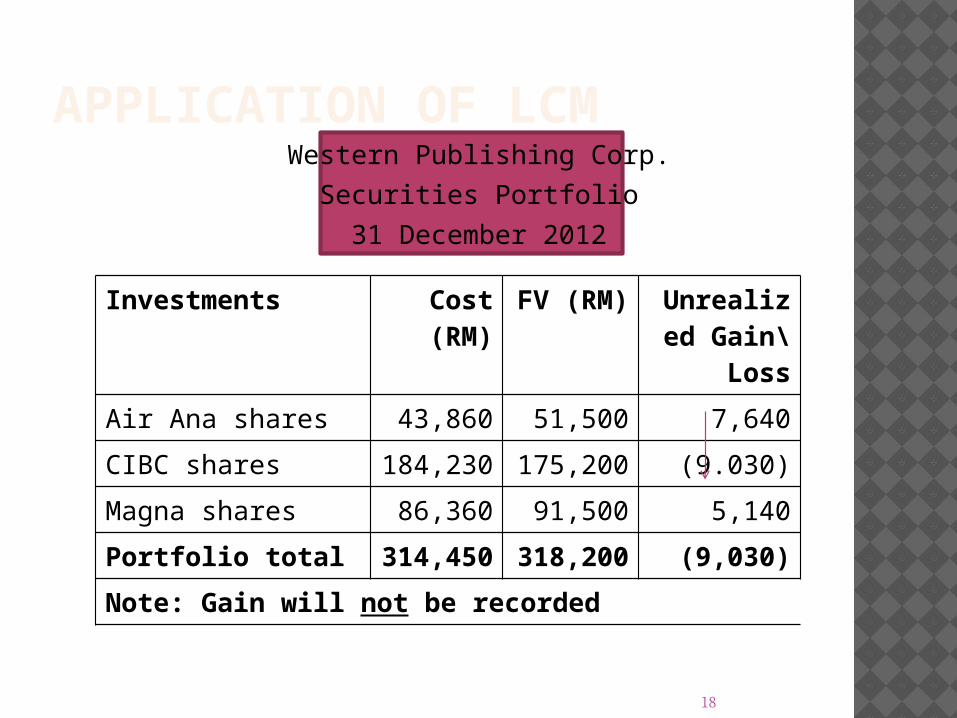

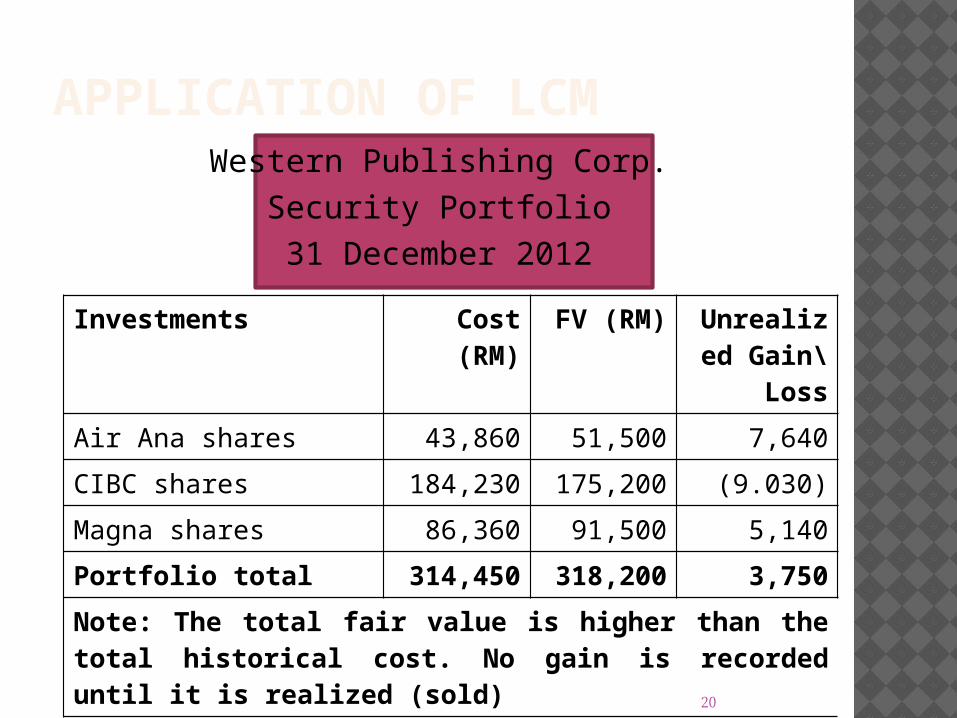

APPLICATION OF LCMWestern Publishing Corp.

Securities Portfolio

31 December 2012

Investments Cost (RM)

FV (RM)

Unrealized Gain\

Loss

Air Ana shares 43,860 51,500 7,640

CIBC shares 184,230 175,200 (9.030)

Magna shares 86,360 91,500 5,140

Portfolio total 314,450

318,200

(9,030)

Note: Gain will not be recorded

19

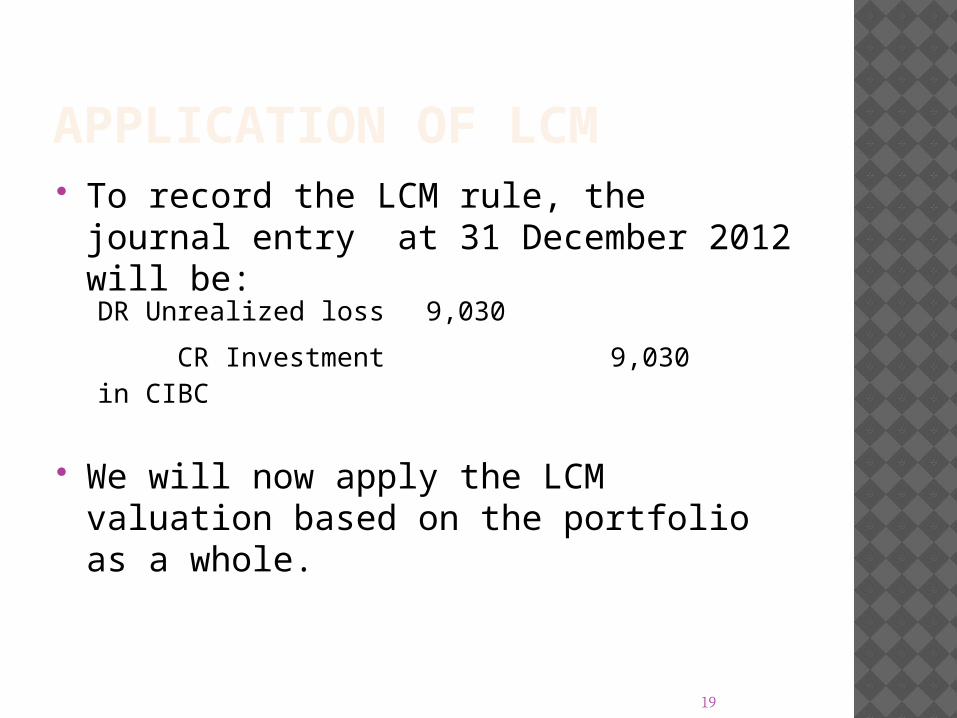

APPLICATION OF LCM To record the LCM rule, the journal entry

at 31 December 2012 will be:

We will now apply the LCM valuation based on the portfolio as a whole.

DR Unrealized loss 9,030

CR Investment in CIBC

9,030

20

APPLICATION OF LCMWestern Publishing Corp.

Security Portfolio31 December 2012

Investments Cost (RM)

FV (RM) Unrealized Gain\

Loss

Air Ana shares 43,860 51,500 7,640

CIBC shares 184,230 175,200 (9.030)

Magna shares 86,360 91,500 5,140

Portfolio total 314,450 318,200 3,750

Note: The total fair value is higher than the total historical cost. No gain is recorded until it is realized (sold)

21

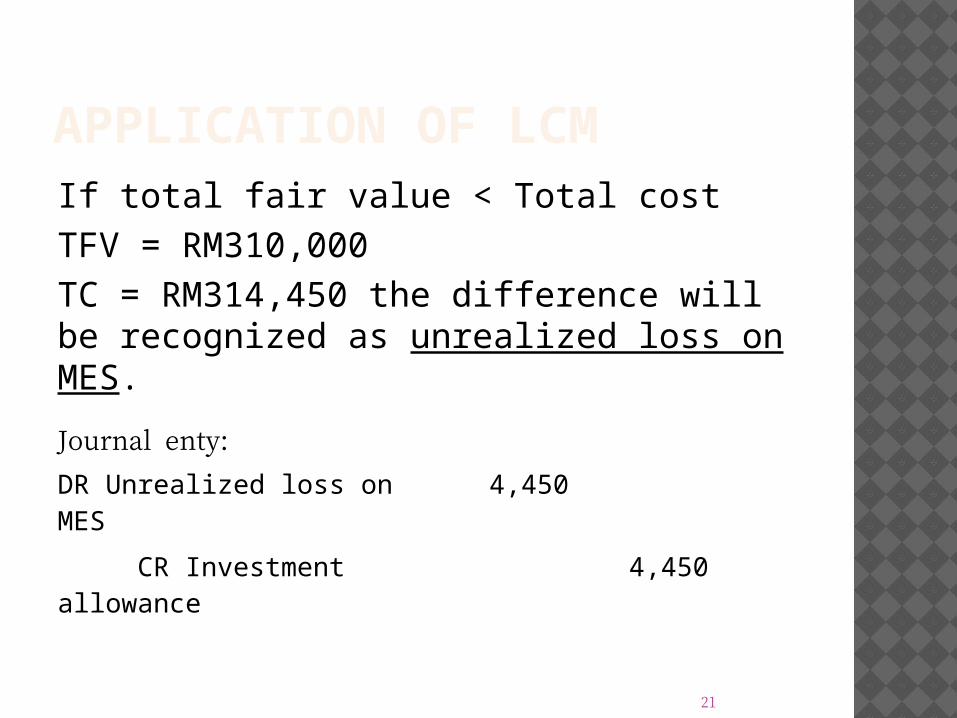

APPLICATION OF LCMIf total fair value < Total costTFV = RM310,000TC = RM314,450 the difference will be recognized as unrealized loss on MES.

Journal enty:

DR Unrealized loss on MES

4,450

CR Investment allowance

4,450

22

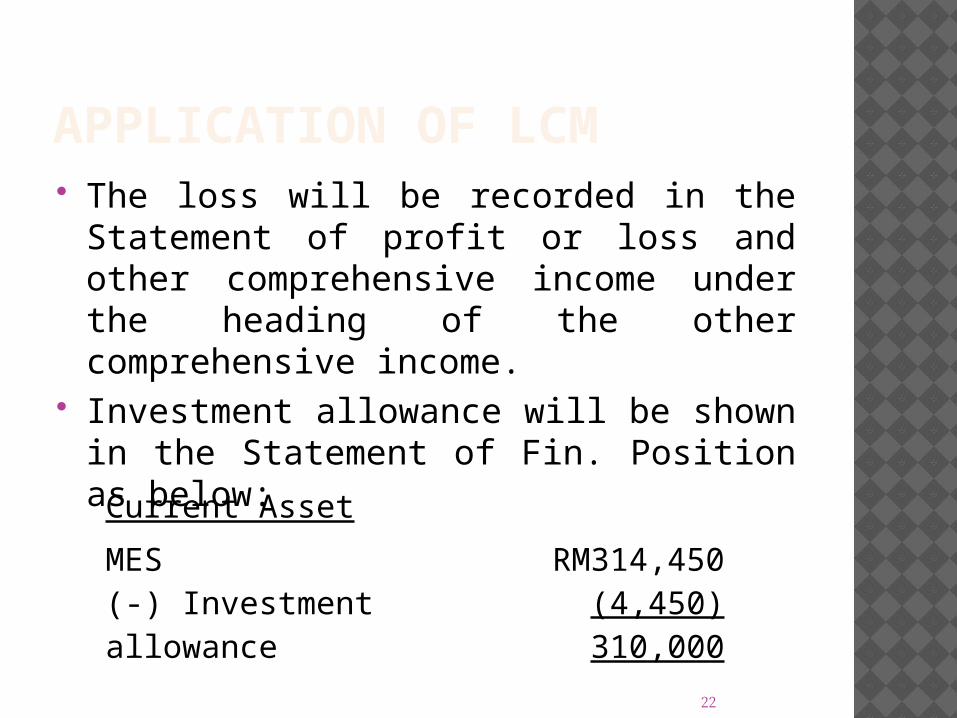

APPLICATION OF LCM The loss will be recorded in the

Statement of profit or loss and other comprehensive income under the heading of the other comprehensive income.

Investment allowance will be shown in the Statement of Fin. Position as below:Current Asset

MES(-) Investment allowance

RM314,450(4,450)

310,000

23

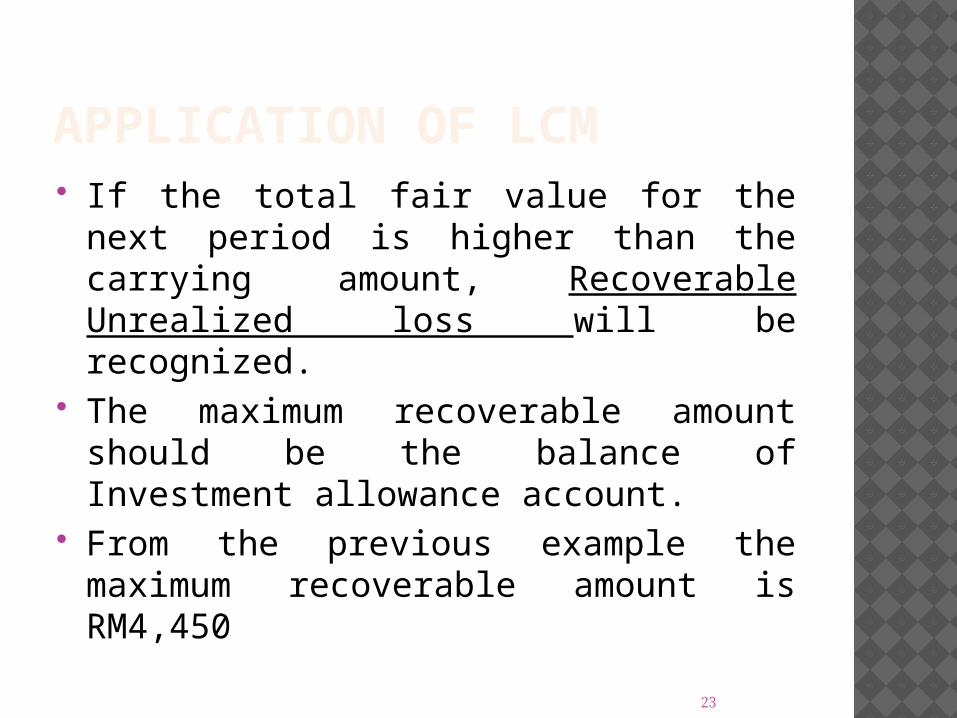

APPLICATION OF LCM If the total fair value for the next period

is higher than the carrying amount, Recoverable Unrealized loss will be recognized.

The maximum recoverable amount should be the balance of Investment allowance account.

From the previous example the maximum recoverable amount is RM4,450

24

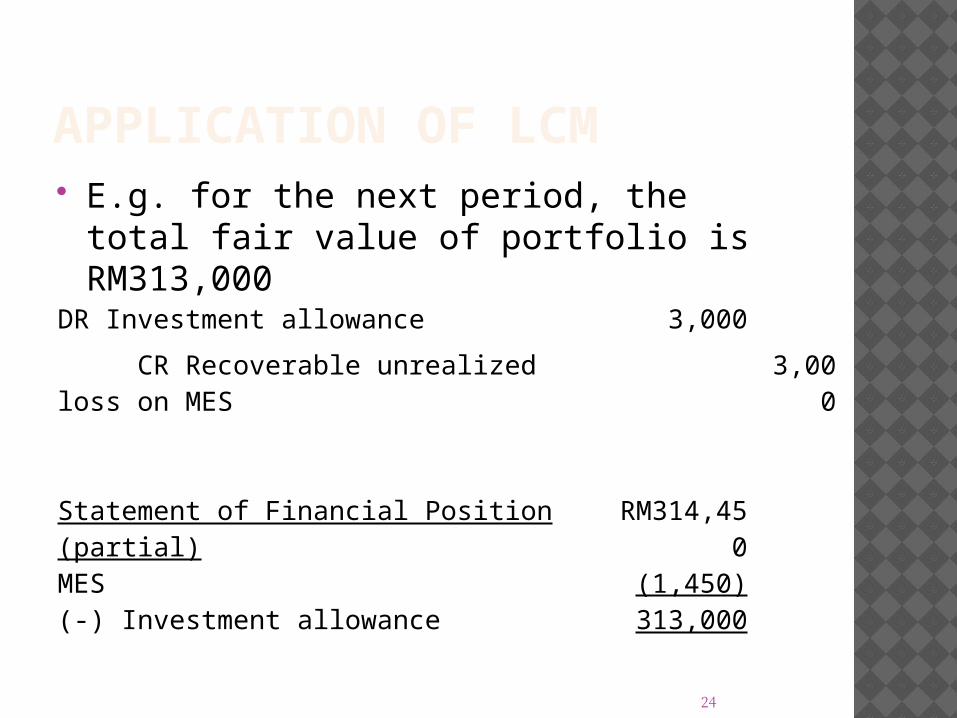

APPLICATION OF LCM E.g. for the next period, the total fair

value of portfolio is RM313,000

DR Investment allowance 3,000

CR Recoverable unrealized loss on MES

Statement of Financial Position (partial)MES(-) Investment allowance

RM314,450

(1,450)313,000

3,000

25

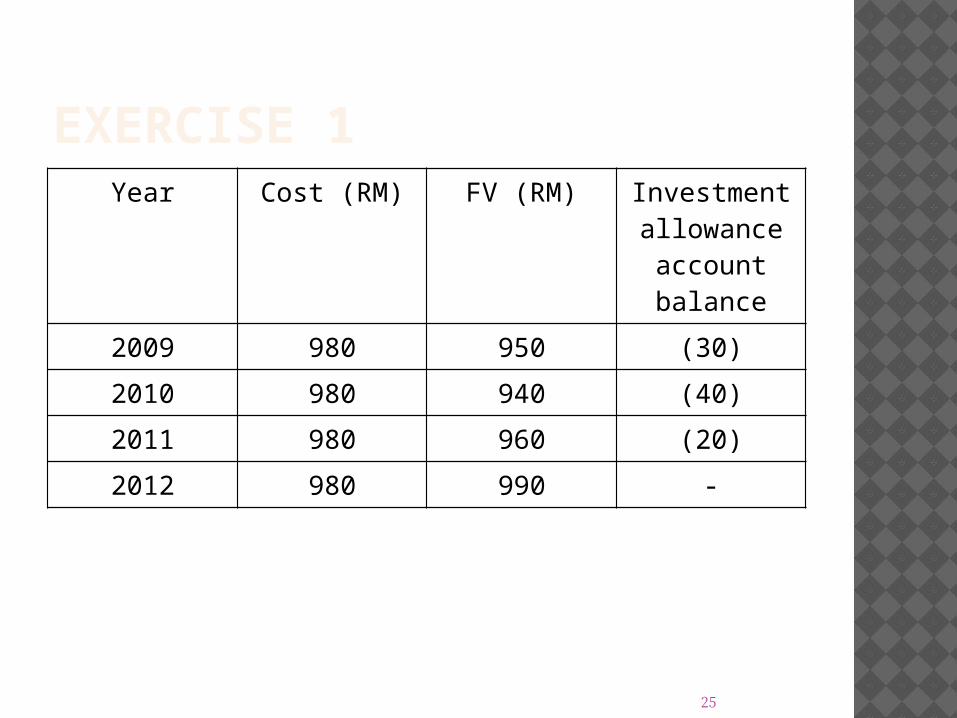

EXERCISE 1Year Cost (RM) FV (RM) Investment

allowance account balance

2009 980 950 (30)

2010 980 940 (40)

2011 980 960 (20)

2012 980 990 -

26

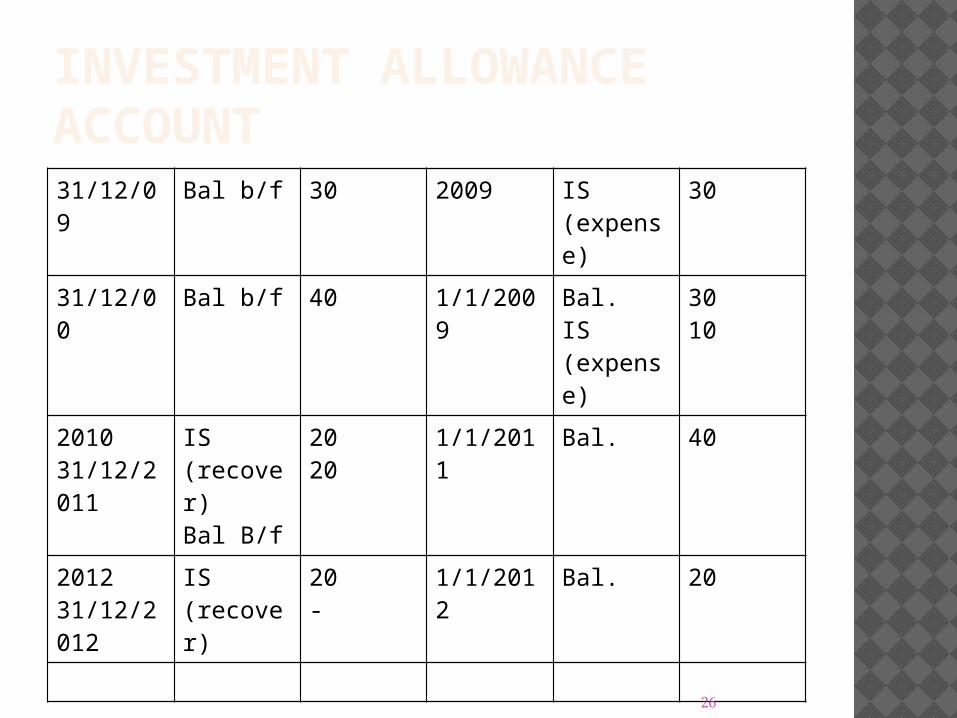

INVESTMENT ALLOWANCE ACCOUNT31/12/09 Bal b/f 30 2009 IS

(expense)

30

31/12/00 Bal b/f 40 1/1/2009 Bal.IS (expense)

3010

201031/12/2011

IS (recover)Bal B/f

2020

1/1/2011 Bal. 40

201231/12/2012

IS (recover)

20-

1/1/2012 Bal. 20

27

RECLASSIFICATION OF MARKETABLE EQUITY SECURITY If management intent changes and does not

plan to hold the investment for temporary purposes, the investment is to be reclassified as a long term investment.

The amount at which investment is transferred depends upon the accounting basis for short term investment. If the lower of cost or market was the accounting basis, LCM would be the new cost.

The difference between the cost and market value will be treated same as for sales of short term MES, i.e. either realized profit or loss will arise.

28

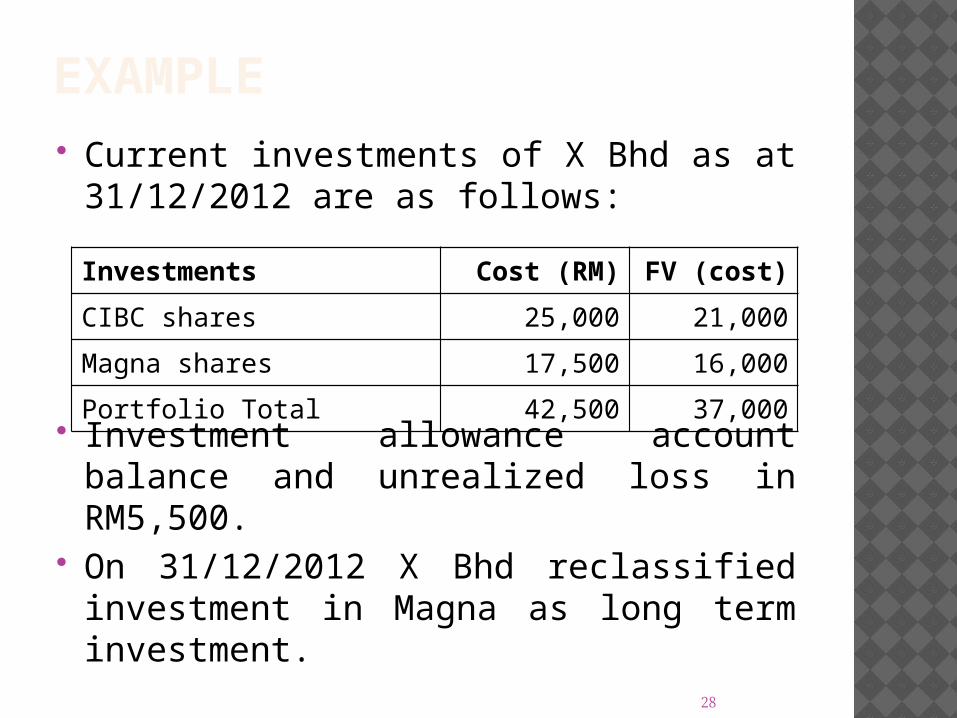

EXAMPLE Current investments of X Bhd as at

31/12/2012 are as follows:

Investment allowance account balance and unrealized loss in RM5,500.

On 31/12/2012 X Bhd reclassified investment in Magna as long term investment.

Investments Cost (RM) FV (cost)

CIBC shares 25,000 21,000

Magna shares 17,500 16,000

Portfolio Total 42,500 37,000

29

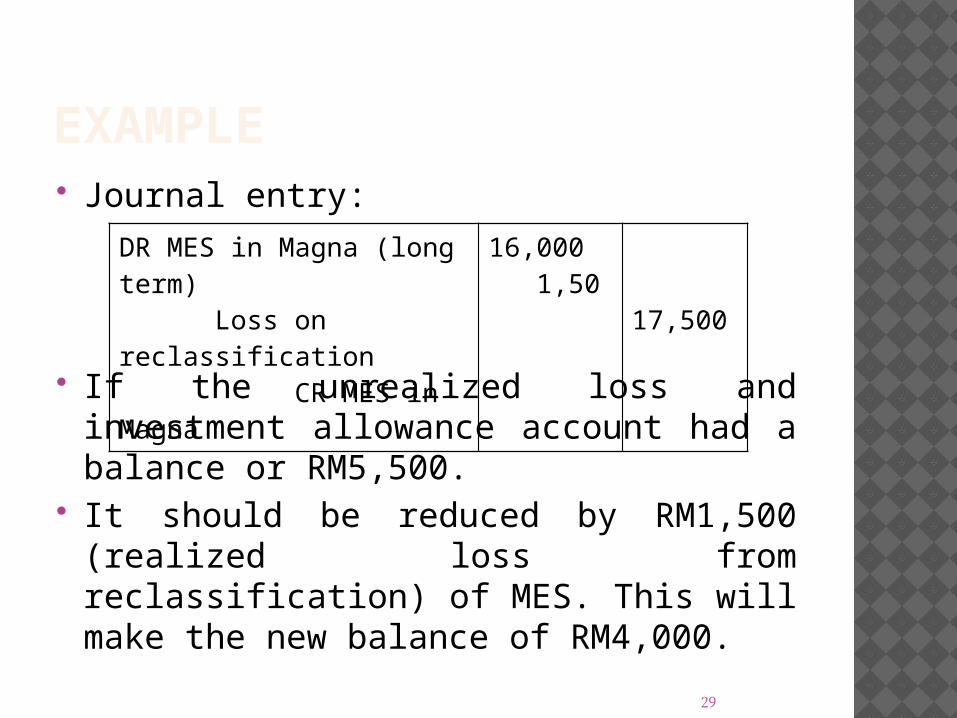

EXAMPLE Journal entry:

If the unrealized loss and investment allowance account had a balance or RM5,500.

It should be reduced by RM1,500 (realized loss from reclassification) of MES. This will make the new balance of RM4,000.

DR MES in Magna (long term) Loss on reclassification CR MES in Magna

16,000 1,50

17,500

30

MARKETABLE DEBT SECURITY (MDS) Previously MDS was recorded at cost.

However, MDS now can be recorded using LCM method.

The journal entries are same as for MES. Purchases of MDS is recorded at cost. But

when purchased between interest payment dates, the accrued interest is recorded at the date of purchase (the company has to pay the MDS cost plus accrued interest).

However, the extra charge (interest portion) will not be included as part of MDS cost but will be recorded as accrued interest.

31

MARKETABLE DEBT SECURITY (MDS) On 1/4/2011 AAA Bhd bought bonds at the

rate of 86, 100 units of BBB Bhd’s bond with face value of RM1,000, interest rate is 10%. Interest is payable on 1 July and 1 January. Broker’s cost and commission is RM1,720.

32

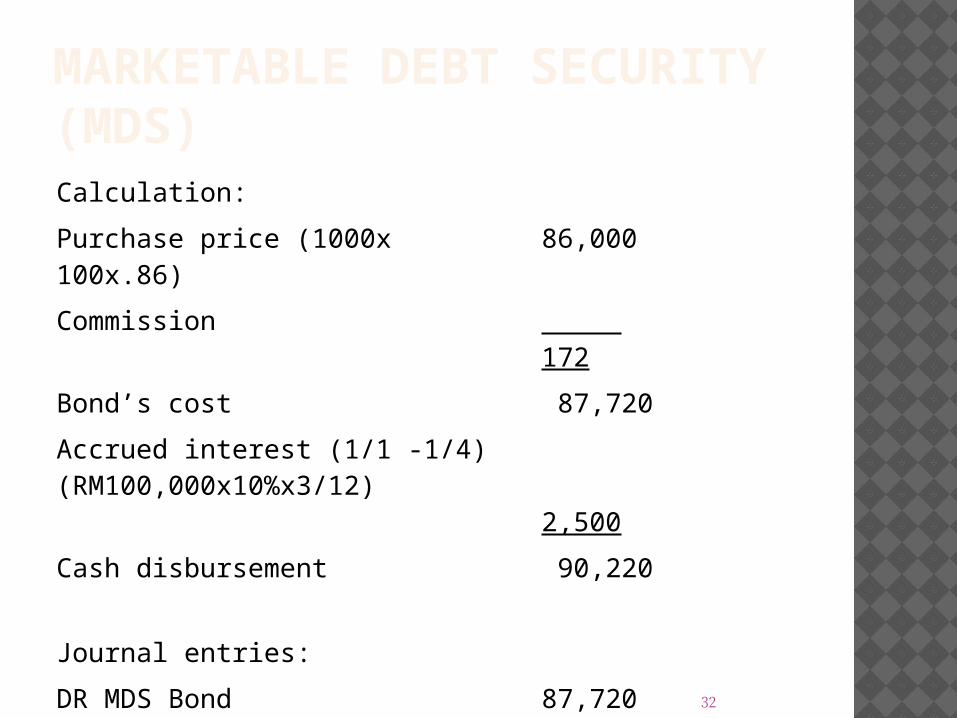

MARKETABLE DEBT SECURITY (MDS)Calculation:

Purchase price (1000x 100x.86) 86,000

Commission 172

Bond’s cost 87,720

Accrued interest (1/1 -1/4)(RM100,000x10%x3/12) 2,500

Cash disbursement 90,220

Journal entries:

DR MDS Bond Accrued interest CR Cash

87,720 2,500

90,220

33

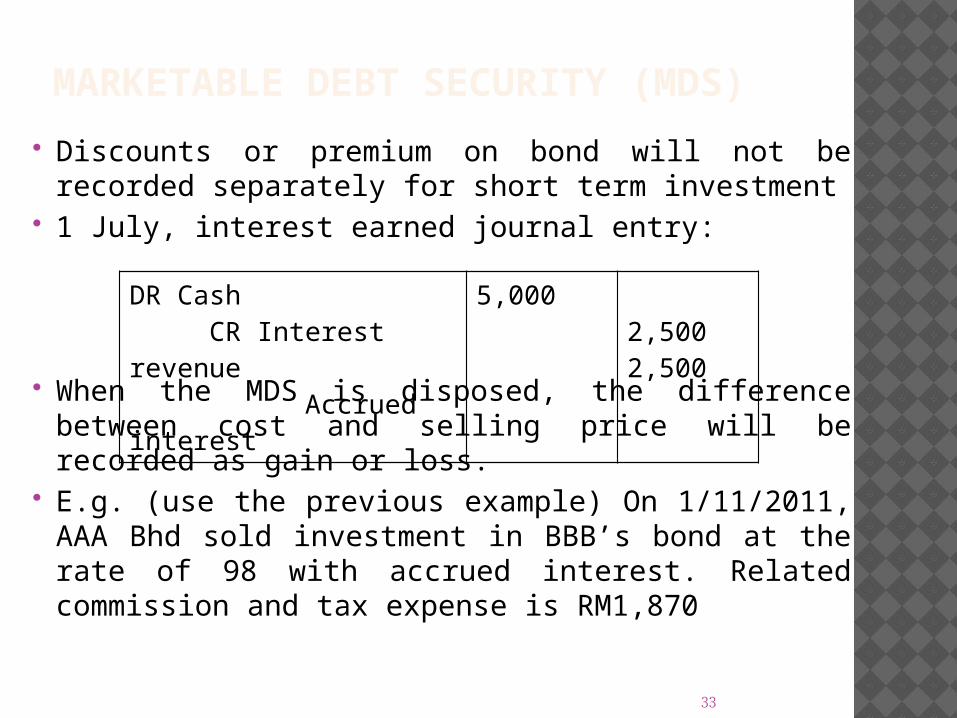

MARKETABLE DEBT SECURITY (MDS)

Discounts or premium on bond will not be recorded separately for short term investment

1 July, interest earned journal entry:

When the MDS is disposed, the difference between cost and selling price will be recorded as gain or loss.

E.g. (use the previous example) On 1/11/2011, AAA Bhd sold investment in BBB’s bond at the rate of 98 with accrued interest. Related commission and tax expense is RM1,870

DR Cash CR Interest revenue Accrued interest

5,0002,5002,500

34

MARKETABLE DEBT SECURITY (MDS)

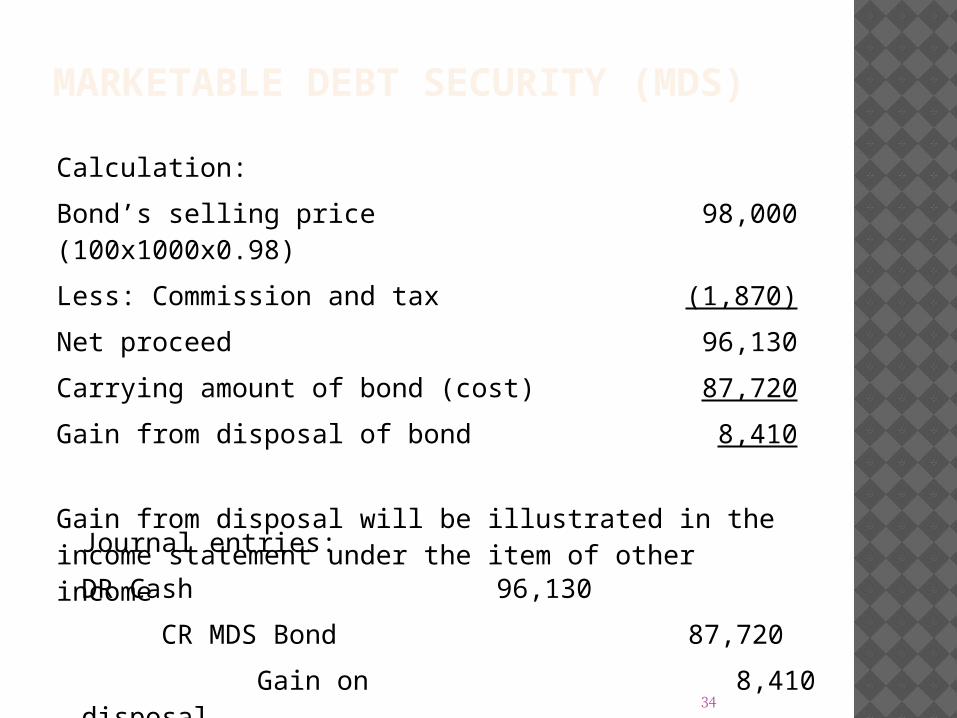

Calculation:

Bond’s selling price (100x1000x0.98) 98,000

Less: Commission and tax (1,870)

Net proceed 96,130

Carrying amount of bond (cost) 87,720

Gain from disposal of bond 8,410

Gain from disposal will be illustrated in the income statement under the item of other income

Journal entries:

DR Cash 96,130

CR MDS Bond 87,720

Gain on disposal 8,410

35

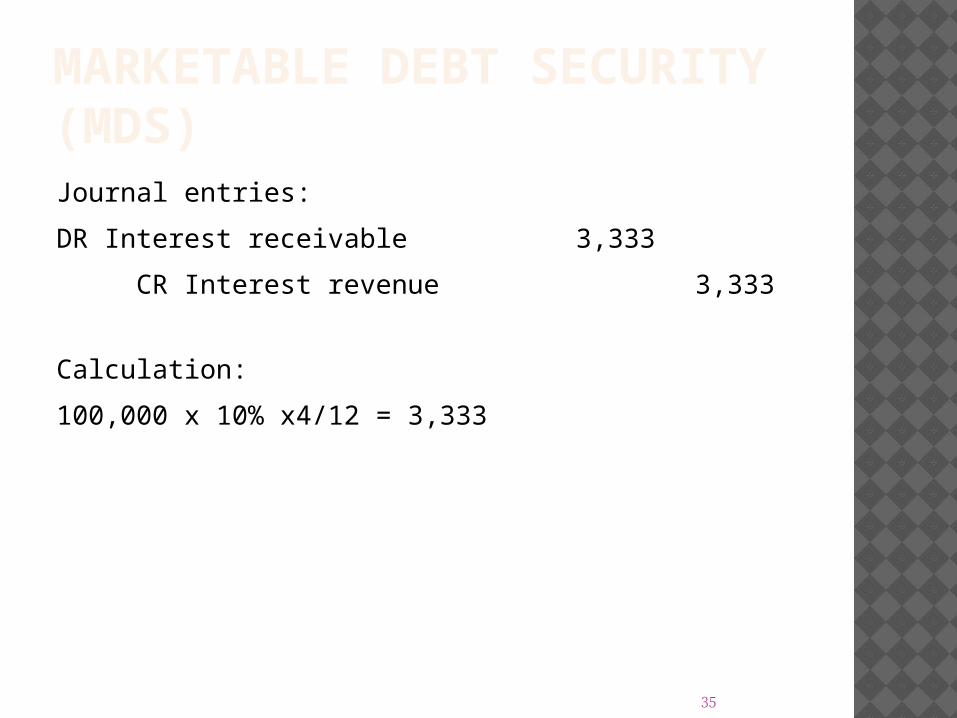

MARKETABLE DEBT SECURITY (MDS)Journal entries:

DR Interest receivable 3,333

CR Interest revenue 3,333

Calculation:

100,000 x 10% x4/12 = 3,333

36

DISCLOSURE Temporary investment is classified as

current asset in the Statement of Financial Position. Disclosure required are:1) Accounting policies

I. The determination of carrying amount of investment

II.The treatment of changes in market value of current investments carried at market value

III.The treatment of a revaluation surplus on the sale of a revalued investments

37

DISCLOSURE2) The significant amounts included in income

for:I. Interest, royalties, dividends and rentals

on long term and current investmentsII. Profit and losses on disposal of current

investments and changes in value of such investments

3) The market value of marketable investments if they are not carried at market value

4) The fair value of investment properties if they are accounted for as long term investments and not carried at fair value

38

DISCLOSURE5)Significant restrictions on the

realizability of investments or the remittance of income and proceeds of disposal

39

THANK YOU